Embed Size (px)

Citation preview

Spend ReductionA Project Guide

Date: July 17th, 2007

John Gregg, Senior Manager,

Monitor China

Key Messages

The Spend Reduction project guide is one of eight detailed project guides supporting the FSI ECR methodology. The objective of this document is to describe and provide guidance around the approach and practices applied on spend reduction engagements.

What is Spend Reduction: Spend reduction involves reducing operating expense on purchased goodsWhat is Spend Reduction: Spend reduction involves reducing operating expense on purchased goods and services through demand management, strategic sourcing, and procurement-related tax minimization. It also addresses the importance of a well-designed procurement function to achieving and sustaining spend efficiencies.

How much does it save, how fast, and how many times have we done it: Spend reduction can lead to significant cost savings typically in the range of 10-25%. It usually identifies a mix of short and longer term cost reduction opportunities On our well established spend reduction track record seelonger term cost reduction opportunities. On our well established spend reduction track record see appendix pages 51-54.

How comfortable are we with existing content: Developed content has been reviewed and approved b SME Addi i l i ll i d l d h ld b d l d liby SMEs. Additional content, potentially in a stand alone document, should be developed to outline techniques and practices specific to optimization of employee benefits (e.g., Consumer Driven Health).

1

Table of Contents

I Spend Reduction Overview 3

Page #

I. Spend Reduction Overview 3

II. Spend Reduction Approach 8

III. Spend Reduction Lessons Learned 42

IV. Developing a Procurement Organization 43

Appendix 48

2

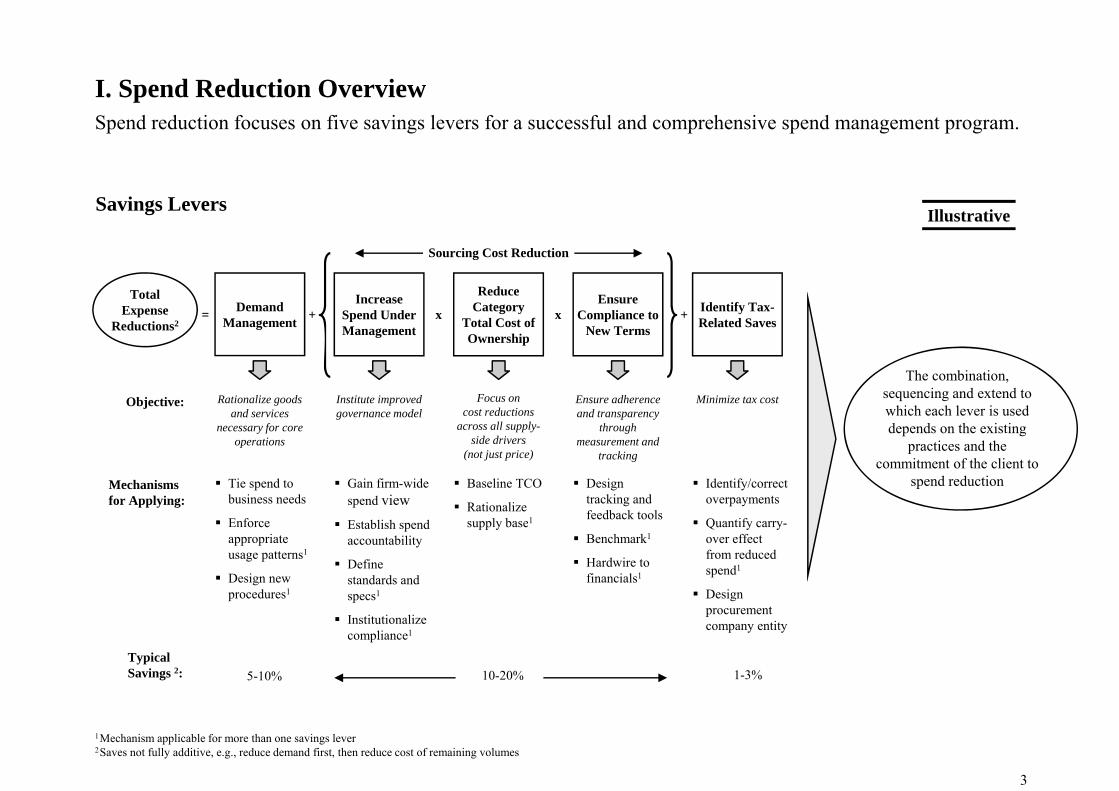

I Spend Reduction OverviewI. Spend Reduction OverviewSpend reduction focuses on five savings levers for a successful and comprehensive spend management program.

Sourcing Cost Reduction

IllustrativeSavings Levers

TotalExpense

Reductions2+ x x= +Demand

Management

IncreaseSpend UnderManagement

Reduce Category

Total Cost of Ownership

Ensure Compliance to

New Terms

Identify Tax-Related Saves

Objective: Rationalize goods and services

necessary for core ti

Institute improved governance model

Focus oncost reductions

across all supply-side drivers

Ensure adherence and transparency

through t d

Minimize tax cost

The combination, sequencing and extend to which each lever is used depends on the existing

Tie spend to business needs

Enforce

operations

Gain firm-wide spend viewEstablish spend

Baseline TCO

Rationalize supply base1

side drivers(not just price)

Design tracking and feedback tools

measurement and tracking

Identify/correct overpayments

Quantify carry-

Mechanisms for Applying:

practices and the commitment of the client to

spend reduction

o ceappropriate usage patterns1

Design new procedures1

Establish spend accountability

Define standards and specs1

i i li

supp y baseBenchmark1

Hardwire to financials1

Qua t y ca yover effect from reduced spend1

Design procurement

Institutionalize compliance1

pcompany entity

Typical Savings 2: 5-10% 10-20% 1-3%

3

1Mechanism applicable for more than one savings lever2Saves not fully additive, e.g., reduce demand first, then reduce cost of remaining volumes

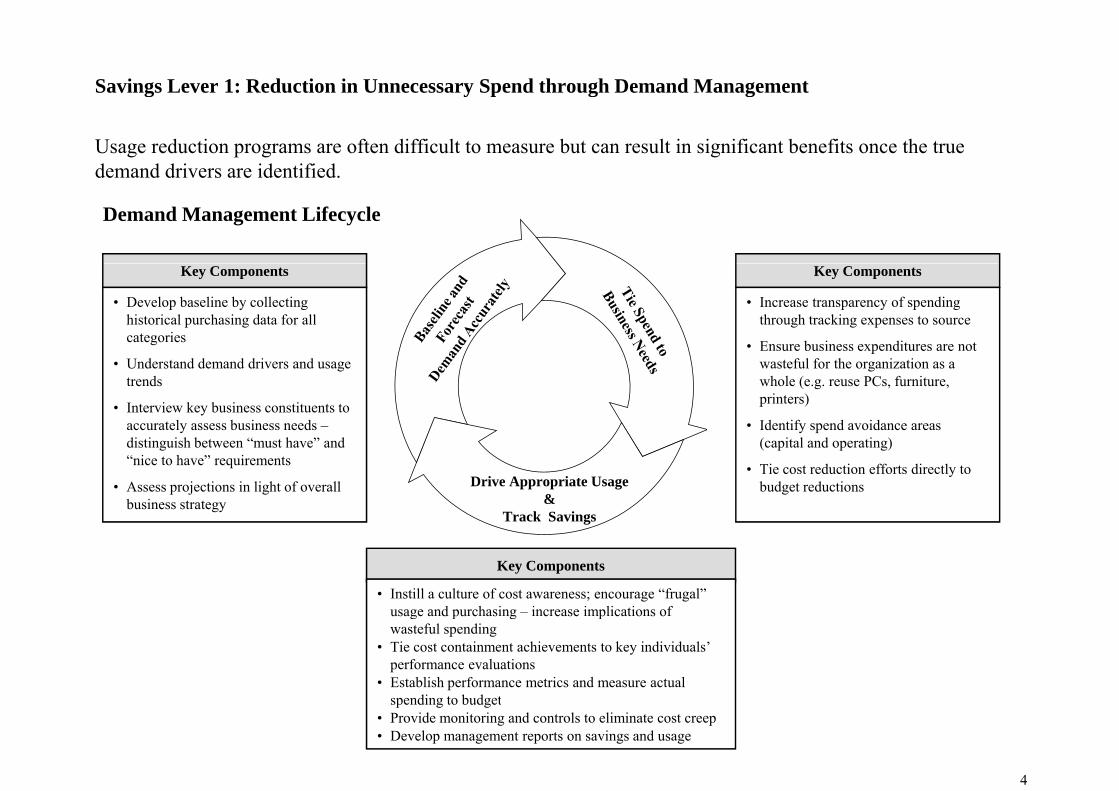

Savings Lever 1: Reduction in Unnecessary Spend through Demand Management

Usage reduction programs are often difficult to measure but can result in significant benefits once the true demand drivers are identified.

Savings Lever 1: Reduction in Unnecessary Spend through Demand Management

demand drivers are identified.

Demand Management Lifecycle

Key Components

• Develop baseline by collecting historical purchasing data for all categories

Key Components

• Increase transparency of spending through tracking expenses to source

• Ensure business expenditures are not • Understand demand drivers and usage

trends

• Interview key business constituents to accurately assess business needs –di ti i h b t “ t h ” d

pwasteful for the organization as a whole (e.g. reuse PCs, furniture, printers)

• Identify spend avoidance areas ( it l d ti )distinguish between “must have” and

“nice to have” requirements

• Assess projections in light of overall business strategy

(capital and operating)

• Tie cost reduction efforts directly to budget reductionsDrive Appropriate Usage

&Track Savings

Key Components

• Instill a culture of cost awareness; encourage “frugal” usage and purchasing – increase implications ofusage and purchasing increase implications of wasteful spending

• Tie cost containment achievements to key individuals’ performance evaluations

• Establish performance metrics and measure actual spending to budget

4

spending to budget• Provide monitoring and controls to eliminate cost creep• Develop management reports on savings and usage

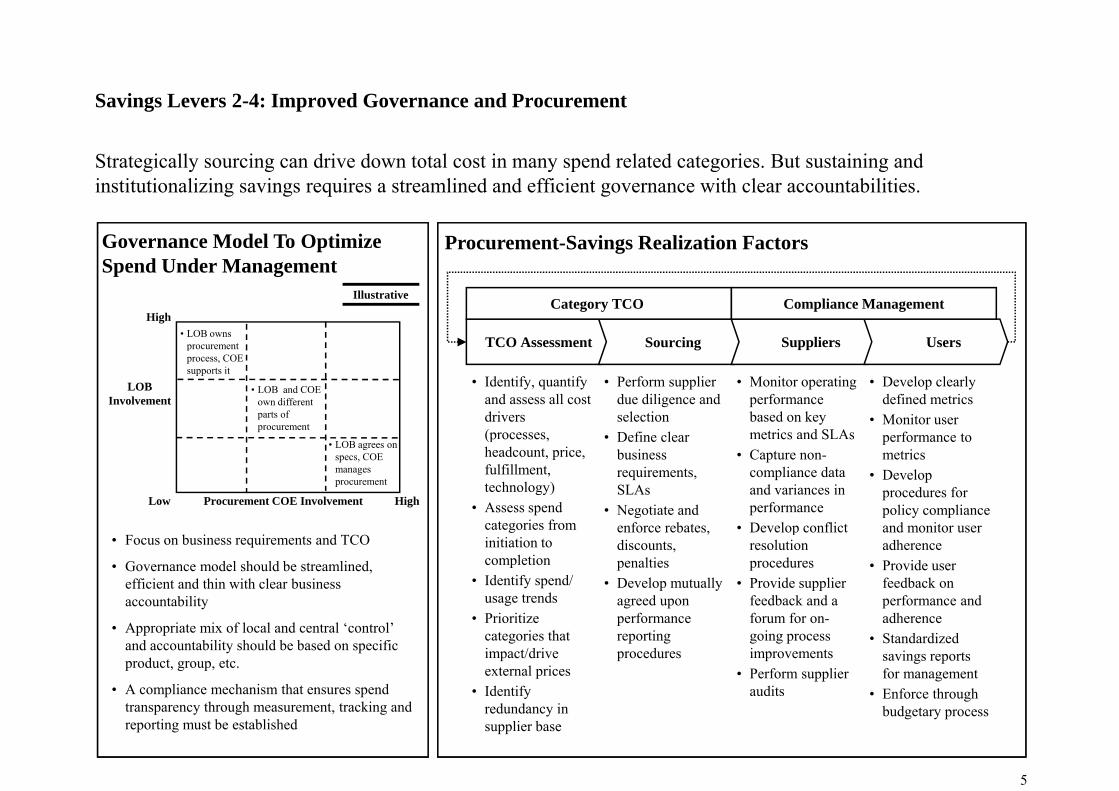

Savings Levers 2-4: Improved Governance and Procurement

Strategically sourcing can drive down total cost in many spend related categories. But sustaining and institutionalizing savings requires a streamlined and efficient governance with clear accountabilities.

Procurement-Savings Realization FactorsGovernance Model To Optimize Spend Under ManagementSpend Under Management

TCO Assessment Sourcing Suppliers Users

Category TCO Compliance ManagementHigh

• LOB owns procurement

Illustrative

• Identify, quantify and assess all cost drivers (processes,

• Perform supplier due diligence and selection

• Define clear

• Monitor operating performance based on key metrics and SLAs

• Develop clearly defined metrics

• Monitor user performance to

LOB Involvement

process, COE supports it

• LOB and COE own different parts of procurement (p ocesses,

headcount, price, fulfillment, technology)

• Assess spend categories from

Define clear business requirements, SLAs

• Negotiate and enforce rebates

e cs d S s• Capture non-

compliance data and variances in performance

• Develop conflict

performance to metrics

• Develop procedures for policy compliance and monitor user

Low Procurement COE Involvement

• LOB agrees on specs, COE manages procurement

High

• Focus on business requirements and TCO

• Governance model should be streamlined, efficient and thin with clear business accountability

categories from initiation to completion

• Identify spend/ usage trendsP i iti

enforce rebates, discounts, penalties

• Develop mutually agreed upon

f

• Develop conflict resolution procedures

• Provide supplier feedback and a f f

and monitor user adherence

• Provide user feedback on performance and dh

• Appropriate mix of local and central ‘control’ and accountability should be based on specific product, group, etc.

• A compliance mechanism that ensures spend h h ki d

• Prioritize categories that impact/drive external prices

• Identify

performance reporting procedures

forum for on-going process improvements

• Perform supplier audits

adherence• Standardized

savings reports for management

• Enforce through

5

transparency through measurement, tracking and reporting must be established

redundancy in supplier base

budgetary process

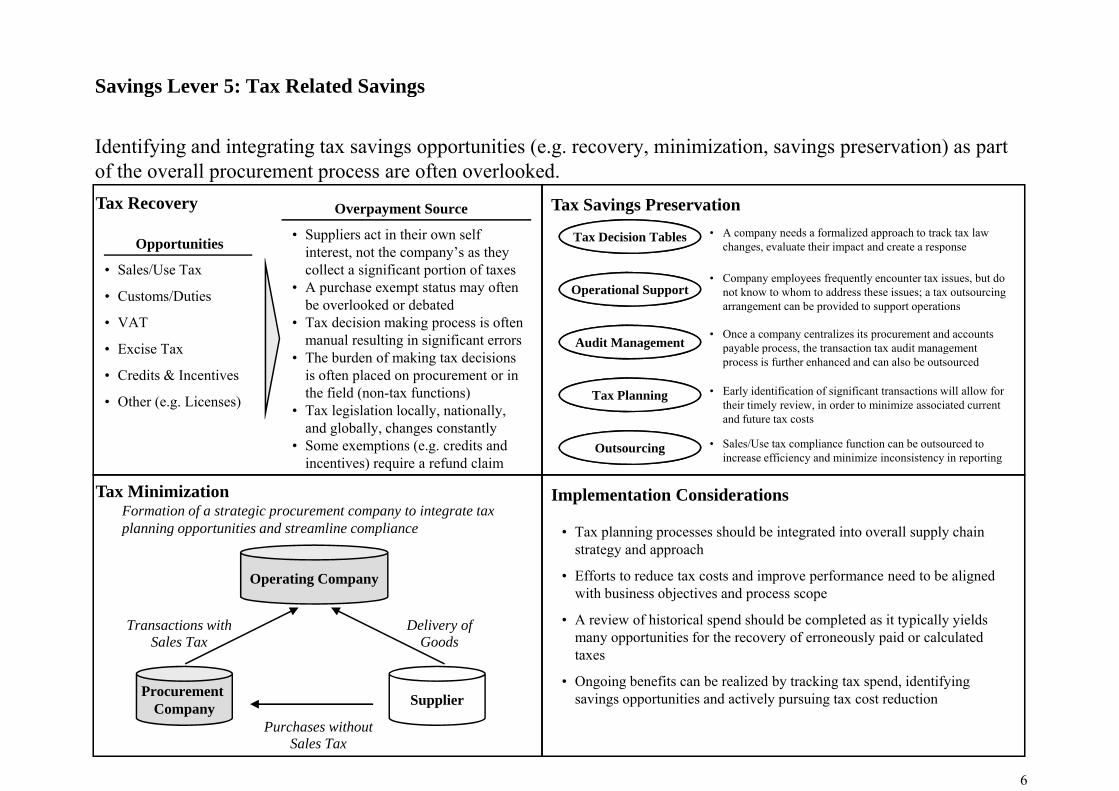

Savings Lever 5: Tax Related SavingsSavings Lever 5: Tax Related Savings

Identifying and integrating tax savings opportunities (e.g. recovery, minimization, savings preservation) as part of the overall procurement process are often overlooked.of the overall procurement process are often overlooked.Tax Recovery

Opportunities

Overpayment Source

• Suppliers act in their own self interest, not the company’s as they

Tax Savings Preservation• A company needs a formalized approach to track tax law

changes, evaluate their impact and create a responseTax Decision Tables

• Sales/Use Tax

• Customs/Duties

• VAT

• Excise Tax

collect a significant portion of taxes• A purchase exempt status may often

be overlooked or debated • Tax decision making process is often

manual resulting in significant errors

Operational Support

Audit Management

• Company employees frequently encounter tax issues, but do not know to whom to address these issues; a tax outsourcing arrangement can be provided to support operations

• Once a company centralizes its procurement and accounts payable process, the transaction tax audit managementExcise Tax

• Credits & Incentives

• Other (e.g. Licenses)

• The burden of making tax decisions is often placed on procurement or in the field (non-tax functions)

• Tax legislation locally, nationally, and globally, changes constantly

Tax Planning • Early identification of significant transactions will allow for their timely review, in order to minimize associated current and future tax costs

payable process, the transaction tax audit management process is further enhanced and can also be outsourced

l / li i b d• Some exemptions (e.g. credits and incentives) require a refund claim

Tax MinimizationFormation of a strategic procurement company to integrate tax planning opportunities and streamline compliance

Implementation Considerations

T l i h ld b i d i ll l h i

Outsourcing • Sales/Use tax compliance function can be outsourced to increase efficiency and minimize inconsistency in reporting

planning opportunities and streamline compliance

Operating Company

• Tax planning processes should be integrated into overall supply chain strategy and approach

• Efforts to reduce tax costs and improve performance need to be aligned with business objectives and process scope

A i f hi i l d h ld b l d i i ll i ld

Procurement Supplier

Transactions withSales Tax

Delivery ofGoods

• A review of historical spend should be completed as it typically yields many opportunities for the recovery of erroneously paid or calculated taxes

• Ongoing benefits can be realized by tracking tax spend, identifying savings opportunities and actively pursuing tax cost reduction

6

Company Supplier

Purchases withoutSales Tax

savings opportunities and actively pursuing tax cost reduction

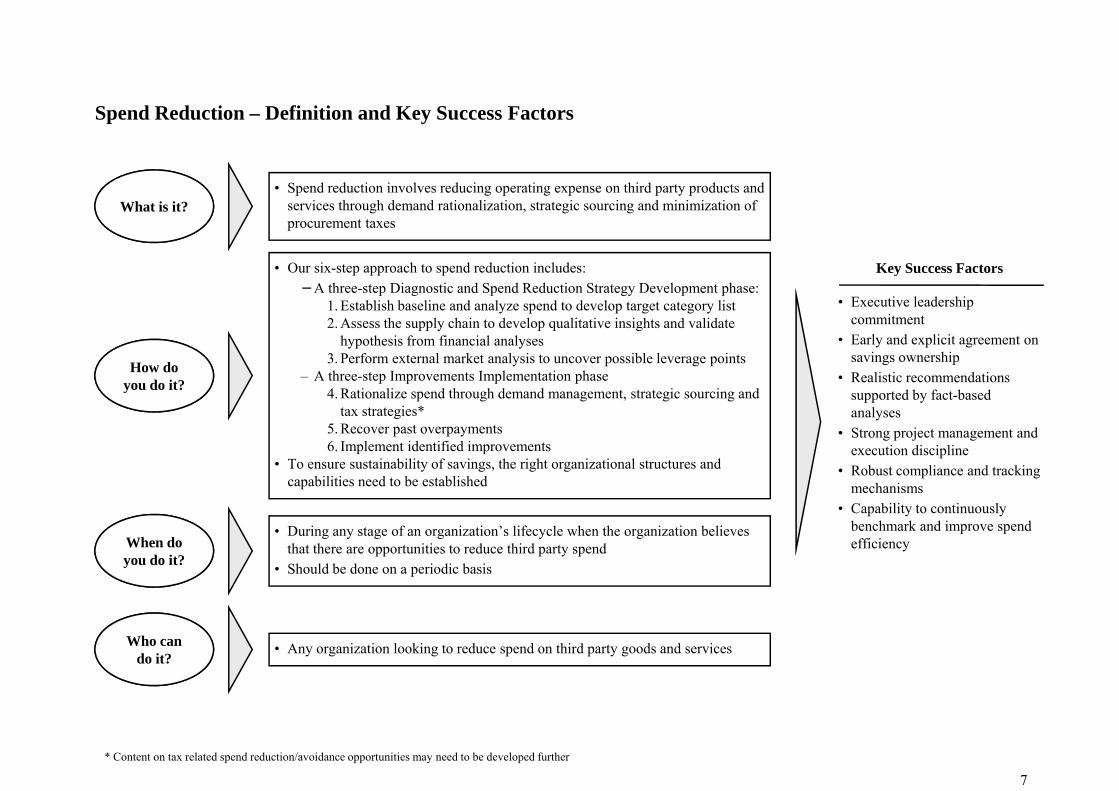

Spend Reduction – Definition and Key Success Factors

What is it?• Spend reduction involves reducing operating expense on third party products and

services through demand rationalization, strategic sourcing and minimization of procurement taxes

O i h d d i i l d K S F• Our six-step approach to spend reduction includes:−A three-step Diagnostic and Spend Reduction Strategy Development phase:

1. Establish baseline and analyze spend to develop target category list2. Assess the supply chain to develop qualitative insights and validate

hypothesis from financial analyses

• Executive leadership commitment

• Early and explicit agreement on

Key Success Factors

How do you do it?

3. Perform external market analysis to uncover possible leverage points– A three-step Improvements Implementation phase

4. Rationalize spend through demand management, strategic sourcing and tax strategies*

5. Recover past overpayments

savings ownership• Realistic recommendations

supported by fact-based analyses

• Strong project management and 6. Implement identified improvements

• To ensure sustainability of savings, the right organizational structures and capabilities need to be established

D i t f i ti ’ lif l h th i ti b li

g p j gexecution discipline

• Robust compliance and tracking mechanisms

• Capability to continuously benchmark and improve spend

When do you do it?

• During any stage of an organization’s lifecycle when the organization believes that there are opportunities to reduce third party spend

• Should be done on a periodic basis

benchmark and improve spend efficiency

Who can do it?

• Any organization looking to reduce spend on third party goods and services

7

* Content on tax related spend reduction/avoidance opportunities may need to be developed further

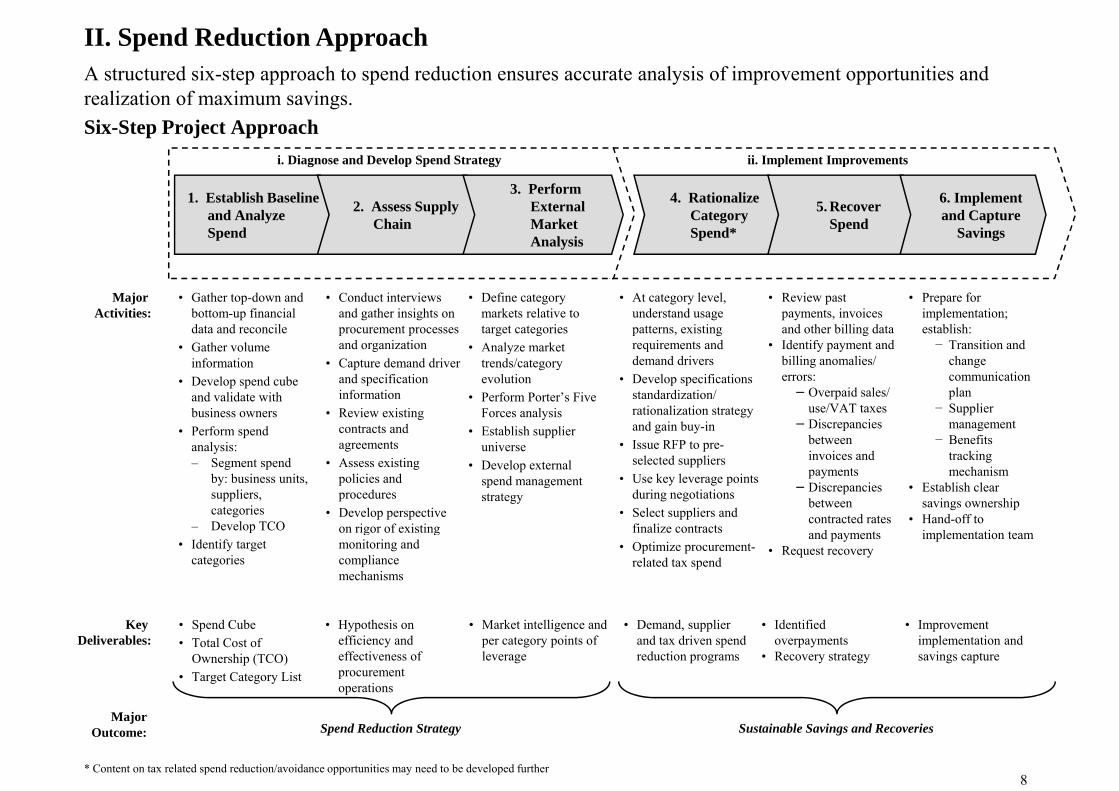

A structured six-step approach to spend reduction ensures accurate analysis of improvement opportunities and

II. Spend Reduction Approach

Six-Step Project Approachrealization of maximum savings.

i. Diagnose and Develop Spend Strategy ii. Implement Improvements

1. Establish Baseline and Analyze Spend

2. Assess Supply Chain

3. Perform External Market Analysis

4. Rationalize Category Spend*

5. Recover Spend

6. Implement and Capture

Savings

Major Activities:

• Gather top-down and bottom-up financial data and reconcile

• Gather volume

• Define category markets relative to target categories

• Analyze market

• At category level, understand usage patterns, existing requirements and

• Conduct interviews and gather insights on procurement processes and organization

• Review past payments, invoices and other billing data

• Identify payment and

• Prepare for implementation; establish:− Transition and Gat e vo u e

information• Develop spend cube

and validate with business owners

• Perform spend

a y e a ettrends/category evolution

• Perform Porter’s Five Forces analysis

• Establish supplier

qdemand drivers

• Develop specifications standardization/ rationalization strategy and gain buy-in

g• Capture demand driver

and specification information

• Review existing contracts and

y p ybilling anomalies/ errors:−Overpaid sales/

use/VAT taxes−Discrepancies

between

change communication plan

− Supplier managementBenefitsanalysis:

– Segment spend by: business units, suppliers, categories

– Develop TCO

universe• Develop external

spend management strategy

• Issue RFP to pre-selected suppliers

• Use key leverage points during negotiations

• Select suppliers and finalize contracts

agreements• Assess existing

policies and procedures

• Develop perspective on rigor of existing

between invoices and payments

−Discrepancies between contracted rates

− Benefits tracking mechanism

• Establish clear savings ownership

• Hand-off to – Develop TCO• Identify target

categories

finalize contracts• Optimize procurement-

related tax spend

on rigor of existing monitoring and compliance mechanisms

and payments• Request recovery

implementation team

Key Deliverables:

• Spend Cube• Total Cost of

Ownership (TCO)• Target Category List

• Demand, supplier and tax driven spend reduction programs

• Hypothesis on efficiency and effectiveness of procurement operations

• Market intelligence and per category points of leverage

• Identified overpayments

• Recovery strategy

• Improvement implementation and savings capture

8

Spend Reduction Strategy Sustainable Savings and RecoveriesMajor

Outcome:

* Content on tax related spend reduction/avoidance opportunities may need to be developed further

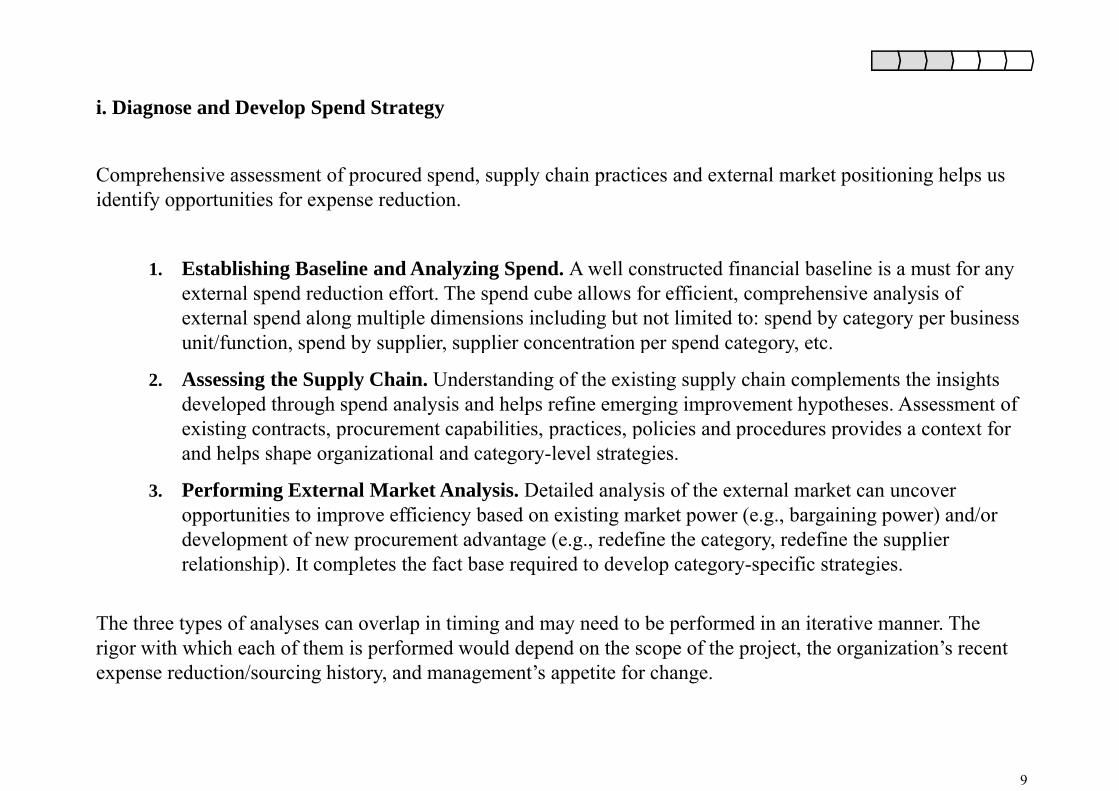

i. Diagnose and Develop Spend Strategy

Comprehensive assessment of procured spend supply chain practices and external market positioning helps usComprehensive assessment of procured spend, supply chain practices and external market positioning helps us identify opportunities for expense reduction.

1 E t bli hi B li d A l i S d A ll t t d fi i l b li i t f1. Establishing Baseline and Analyzing Spend. A well constructed financial baseline is a must for any external spend reduction effort. The spend cube allows for efficient, comprehensive analysis of external spend along multiple dimensions including but not limited to: spend by category per business unit/function, spend by supplier, supplier concentration per spend category, etc. , p y pp , pp p p g y,

2. Assessing the Supply Chain. Understanding of the existing supply chain complements the insights developed through spend analysis and helps refine emerging improvement hypotheses. Assessment of existing contracts, procurement capabilities, practices, policies and procedures provides a context for g p p p p p pand helps shape organizational and category-level strategies.

3. Performing External Market Analysis. Detailed analysis of the external market can uncover opportunities to improve efficiency based on existing market power (e.g., bargaining power) and/or development of new procurement advantage (e.g., redefine the category, redefine the supplier relationship). It completes the fact base required to develop category-specific strategies.

The three types of analyses can overlap in timing and may need to be performed in an iterative manner. The rigor with which each of them is performed would depend on the scope of the project, the organization’s recent expense reduction/sourcing history, and management’s appetite for change.

9

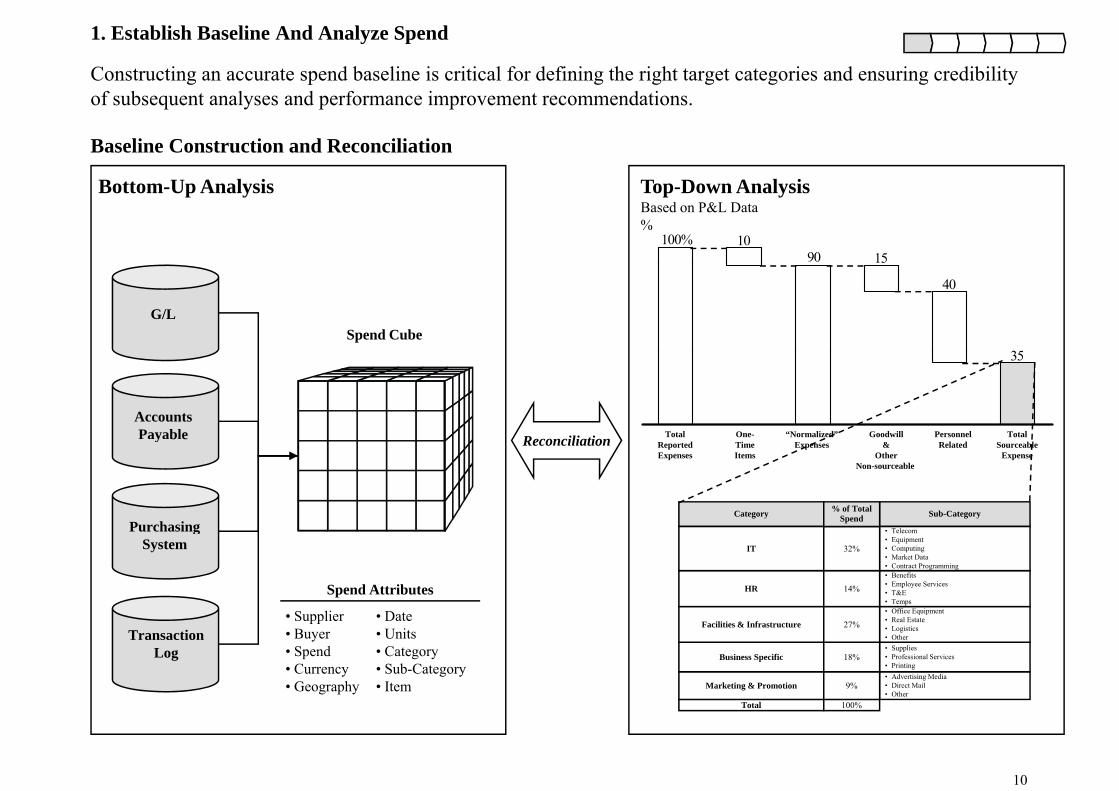

1. Establish Baseline And Analyze Spend

Constructing an accurate spend baseline is critical for defining the right target categories and ensuring credibility of subsequent analyses and performance improvement recommendations.

Baseline Construction and Reconciliation

Top-Down AnalysisBased on P&L Data%

100% 1090 15

Bottom-Up Analysis

G/LSpend Cube

35

40

Accounts Payable Reconciliation

35

Total One- “Normalized” Goodwill Personnel Totaly b e

Purchasing

Reconciliation ReportedExpenses

TimeItems

Expenses &Other

Non-sourceable

Related SourceableExpense

Sub-CategoryCategory % of Total Spend

Purchasing System

• Supplier • Date

Spend Attributes• Office Equipment

• Benefits• Employee Services• T&E• Temps

HR 14%

• Telecom• Equipment• Computing• Market Data• Contract Programming

IT 32%

Transaction Log

• Supplier • Buyer• Spend• Currency • Geography

• Date • Units• Category• Sub-Category• Item

T t l

• Advertising Media• Direct Mail• Other

Marketing & Promotion

• Supplies• Professional Services• Printing

Business Specific

• Real Estate• Logistics• Other

Facilities & Infrastructure

100%

9%

18%

27%

10

Total 100%

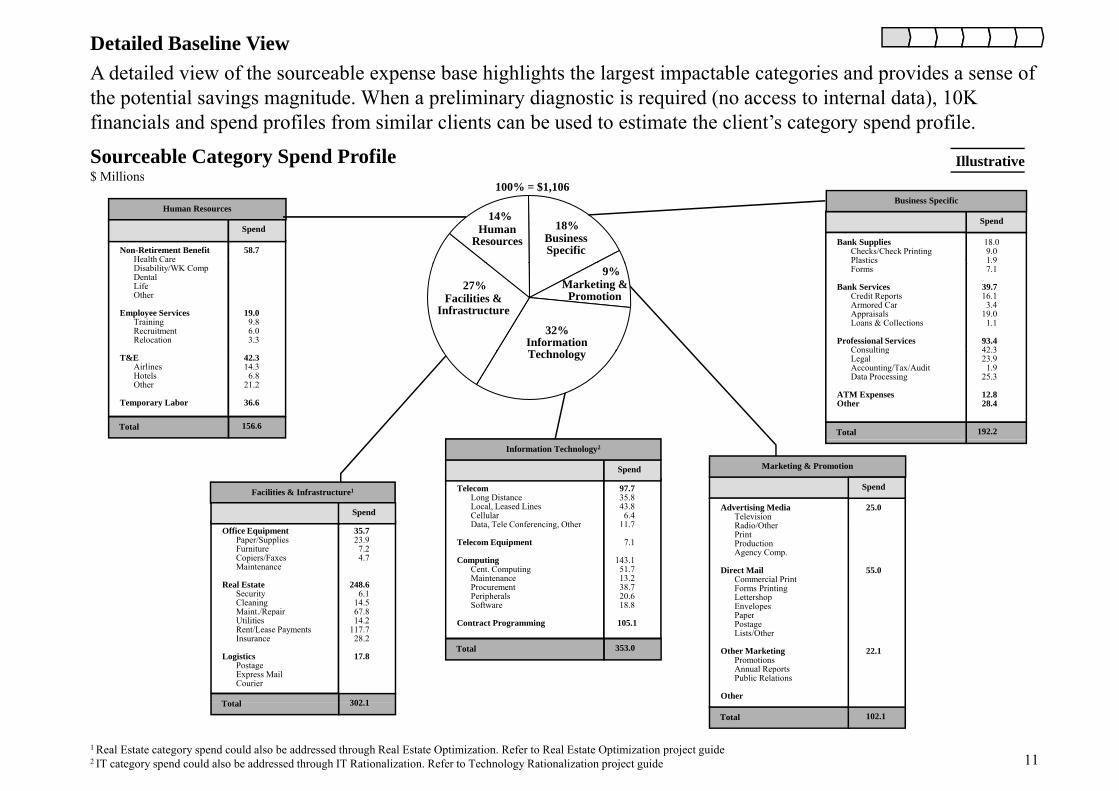

A detailed view of the sourceable expense base highlights the largest impactable categories and provides a sense of Detailed Baseline View

the potential savings magnitude. When a preliminary diagnostic is required (no access to internal data), 10K financials and spend profiles from similar clients can be used to estimate the client’s category spend profile.

Sourceable Category Spend Profile$ Millions

Illustrative

Non-Retirement BenefitHealth Care

58.7

Spend

Human Resources

Bank SuppliesChecks/Check PrintingPlastics

Human Resources Business

Specific

14%18%

100% = $1,106

18.09.0 1.9

Spend

Business Specific

$ Millions

Disability/WK CompDentalLifeOther

Employee ServicesTrainingRecruitmentRelocation

19.09.86.03.3

Forms

Bank ServicesCredit ReportsArmored CarAppraisalsLoans & Collections

Professional ServicesConsulting

Facilities & Infrastructure

Information T h l

Marketing & Promotion

27%

32%

9% 7.1

39.716.13.4

19.01.1

93.442 3

T&EAirlinesHotelsOther

Temporary Labor

42.314.3

6.821.2

36.6

ConsultingLegalAccounting/Tax/AuditData Processing

ATM ExpensesOther

Technology

Total 156.6Total

42.323.91.9

25.3

12.828.4

192.2

TelecomLong DistanceLocal, Leased LinesCellularData, Tele Conferencing, Other

97.735.843.86.4

11.7

Spend

Facilities & Infrastructure1

Spend Advertising MediaTelevisionRadio/Other

Marketing & Promotion

25.0

Spend

Information Technology2

ata, e e Co e e c g, Ot e

Telecom Equipment

ComputingCent. ComputingMaintenanceProcurementPeripheralsSoftware

.7

7.1

143.151.713.238.720.618.8

35.723.97.24.7

248.66.1

14.567.8

Office EquipmentPaper/SuppliesFurnitureCopiers/Faxes Maintenance

Real EstateSecurityCleaningMaint./Repair

Radio/OtherPrintProductionAgency Comp.

Direct MailCommercial PrintForms PrintingLettershopEnvelopesPaper

55.0

Contract Programming

Total

105.1

353.0

14.2117.728.2

17.8

pUtilitiesRent/Lease PaymentsInsurance

LogisticsPostageExpress MailCourier

302 1Total

PaperPostageLists/Other

Other MarketingPromotionsAnnual ReportsPublic Relations

Other

22.1

11

302.1TotalTotal 102.1

1 Real Estate category spend could also be addressed through Real Estate Optimization. Refer to Real Estate Optimization project guide2 IT category spend could also be addressed through IT Rationalization. Refer to Technology Rationalization project guide

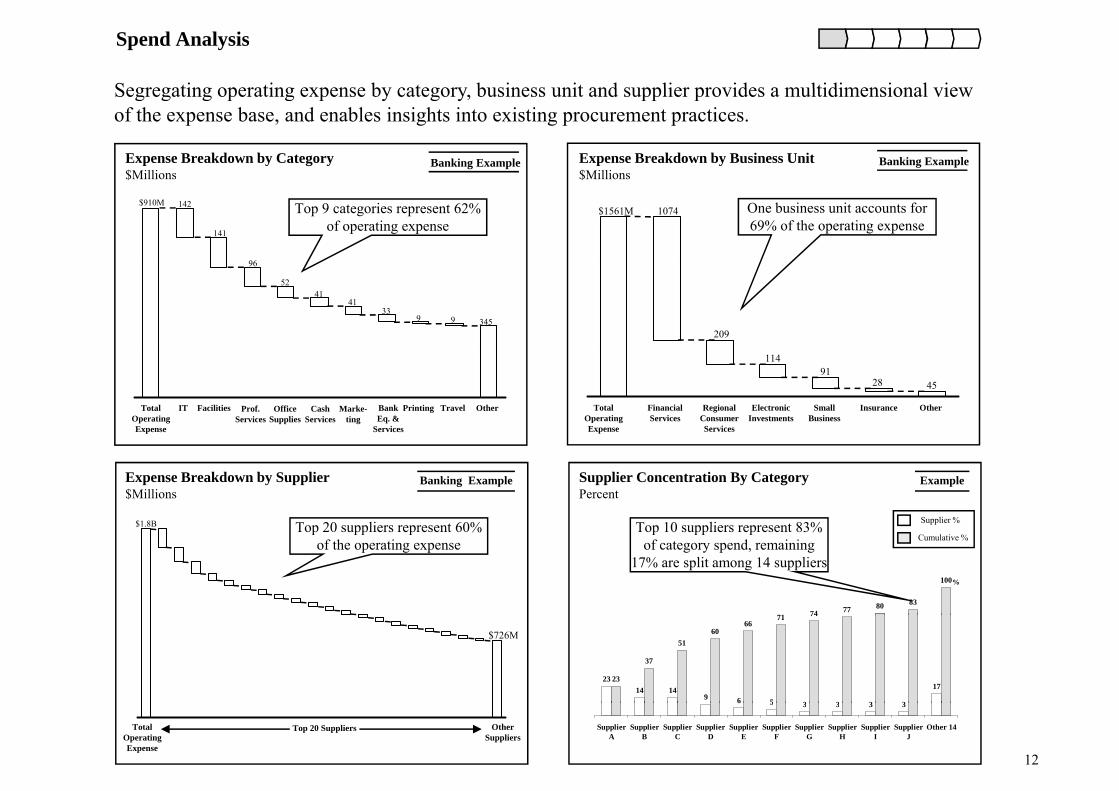

Spend Analysis

Segregating operating expense by category business unit and supplier provides a multidimensional view

Expense Breakdown by Category$Millions

Expense Breakdown by Business Unit$Millions

Segregating operating expense by category, business unit and supplier provides a multidimensional view of the expense base, and enables insights into existing procurement practices.

Banking ExampleBanking Example

$910M 142

141

96

$Millions

Top 9 categories represent 62% of operating expense

$Millions

$1561M 1074 One business unit accounts for 69% of the operating expense

96

5241

4133

9 9 345209

Total Operating Expense

IT Facilities Prof. Services

Office Supplies

Cash Services

Marke-ting

Bank Eq. &

Services

Printing Travel Other Total Operating Expense

Financial Services

Regional Consumer Services

Electronic Investments

Small Business

Insurance Other

11491

28 45

$1.8B

Expense Breakdown by Supplier$Millions

Top 20 suppliers represent 60%

Supplier Concentration By CategoryPercent

Supplier %

Banking Example Example

Top 10 suppliers represent 83%$ Top 20 suppliers represent 60% of the operating expense

71 74 77 80 83

100

Cumulative %

%

Top 10 suppliers represent 83% of category spend, remaining

17% are split among 14 suppliers

2314 14

9 6 5 3 3 3 3

1723

37

5160

6671 74

$726M

12

Total Operating Expense

Other Suppliers

Top 20 Suppliers

6 5 3 3 3 3

SupplierA

SupplierB

SupplierC

SupplierD

SupplierE

SupplierF

SupplierG

SupplierH

SupplierI

SupplierJ

Other 14

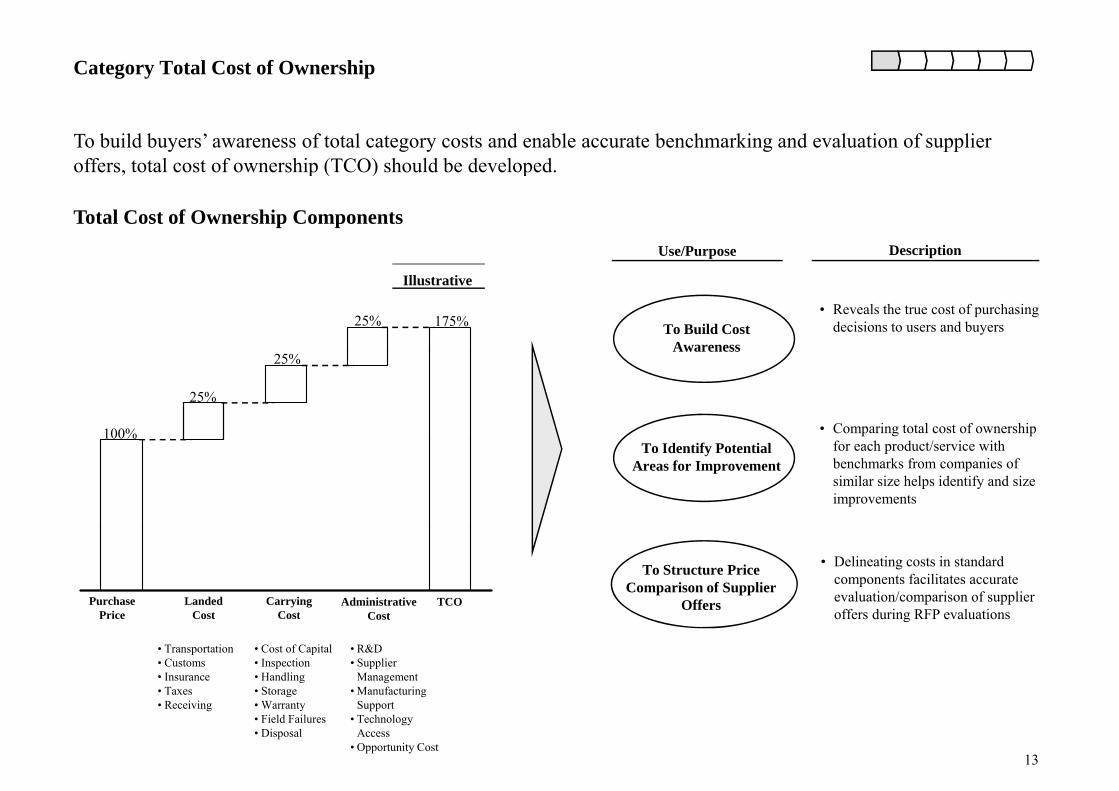

Category Total Cost of Ownership

To build buyers’ awareness of total category costs and enable accurate benchmarking and evaluation of supplier offers, total cost of ownership (TCO) should be developed.

Use/Purpose Description

p ( ) p

Total Cost of Ownership Components

25% 175%

Illustrative

To Build CostAwareness

• Reveals the true cost of purchasing decisions to users and buyers

100%

25%

25%

• Comparing total cost of ownership

Awareness

To Identify Potential Areas for Improvement

for each product/service with benchmarks from companies of similar size helps identify and size improvements

Purchase Price

Landed Cost

Carrying Cost

Administrative Cost

TCO

To Structure Price Comparison of Supplier

Offers

• Delineating costs in standard components facilitates accurate evaluation/comparison of supplier offers during RFP evaluationsPrice Cost Cost Cost

• Transportation• Customs• Insurance• Taxes

R i i

• Cost of Capital• Inspection• Handling• Storage

W t

• R&D• Supplier

Management• Manufacturing

S t

offers during RFP evaluations

13

• Receiving • Warranty• Field Failures• Disposal

Support• Technology

Access• Opportunity Cost

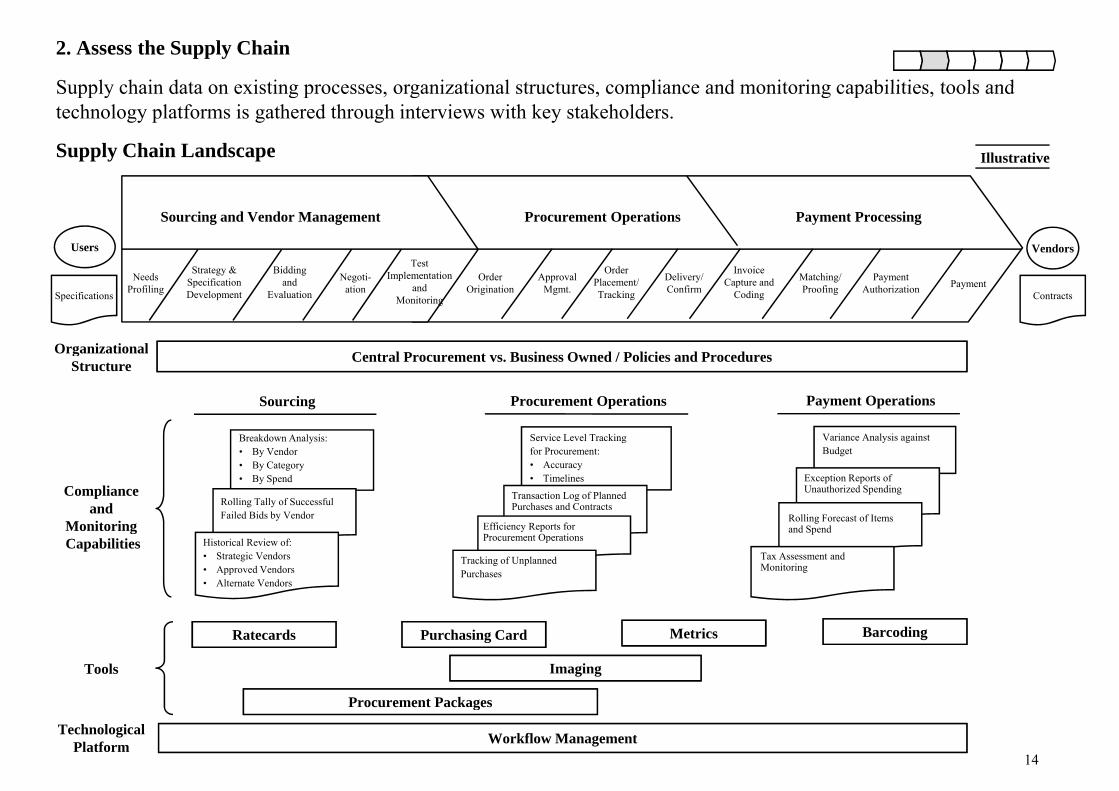

2. Assess the Supply Chain

Supply chain data on existing processes organizational structures compliance and monitoring capabilities tools and

IllustrativeSupply Chain Landscape

Supply chain data on existing processes, organizational structures, compliance and monitoring capabilities, tools and technology platforms is gathered through interviews with key stakeholders.

Users Vendors

Sourcing and Vendor Management

Test

Payment ProcessingProcurement Operations

NeedsProfiling

Strategy & Specification Development

Bidding and

Evaluation

Negoti-ation

Test Implementation

and Monitoring

Order Origination

Approval Mgmt.

Order Placement/ Tracking

Delivery/ Confirm

Invoice Capture and

Coding

Matching/ Proofing

Payment Authorization Payment

Organizational

Specifications Contracts

Breakdown Analysis:

Sourcing

Service Level Tracking

Procurement Operations

Variance Analysis against

Payment Operations

Central Procurement vs. Business Owned / Policies and ProceduresOrganizationalStructure

Breakdown Analysis:• By Vendor• By Category• By Spend

Rolling Tally of SuccessfulFailed Bids by Vendor

Compliance and

Monitoring

Service Level Tracking for Procurement:• Accuracy• Timelines

Transaction Log of Planned Purchases and Contracts

Variance Analysis against Budget

Exception Reports of Unauthorized Spending

Rolling Forecast of Items d S dEfficiency Reports for

Historical Review of:• Strategic Vendors• Approved Vendors• Alternate Vendors

MonitoringCapabilities

and Spend Efficiency Reports for Procurement Operations

Tracking of Unplanned Purchases

Tax Assessment and Monitoring

Ratecards Purchasing Card Metrics Barcoding

Imaging

Procurement Packages

Tools

14

Procurement Packages

Workflow ManagementTechnologicalPlatform

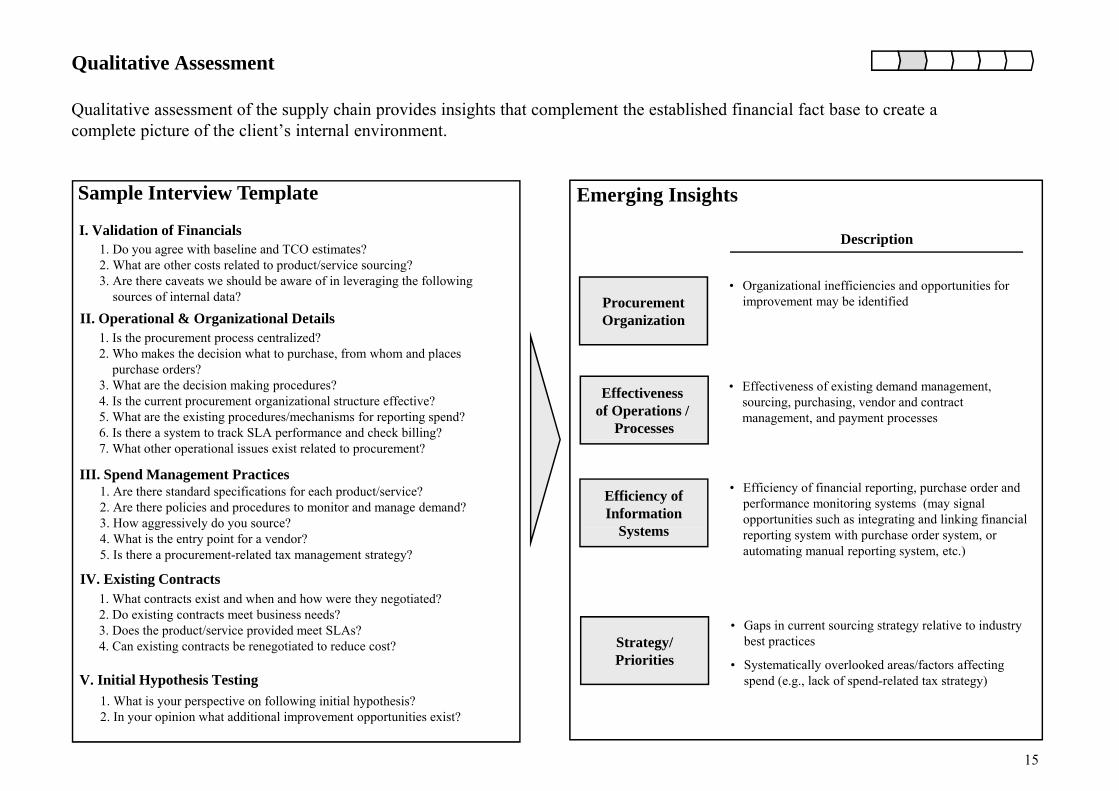

Qualitative Assessment

Qualitative assessment of the supply chain provides insights that complement the established financial fact base to create a complete picture of the client’s internal environment.

Description1. Do you agree with baseline and TCO estimates?2 What are other costs related to product/service sourcing?

Sample Interview Template Emerging InsightsI. Validation of Financials

Procurement Organization

• Organizational inefficiencies and opportunities for improvement may be identified

2. What are other costs related to product/service sourcing?3. Are there caveats we should be aware of in leveraging the following

sources of internal data?

1. Is the procurement process centralized?2 Wh k th d i i h t t h f h d l

II. Operational & Organizational Details

Effectiveness of Operations /

Processes

• Effectiveness of existing demand management, sourcing, purchasing, vendor and contract management, and payment processes

2. Who makes the decision what to purchase, from whom and places purchase orders?

3. What are the decision making procedures?4. Is the current procurement organizational structure effective?5. What are the existing procedures/mechanisms for reporting spend?6. Is there a system to track SLA performance and check billing?

Efficiency of Information

S t

• Efficiency of financial reporting, purchase order and performance monitoring systems (may signal opportunities such as integrating and linking financial

y p g7. What other operational issues exist related to procurement?

1. Are there standard specifications for each product/service?2. Are there policies and procedures to monitor and manage demand?3. How aggressively do you source?

III. Spend Management Practices

Systems reporting system with purchase order system, or automating manual reporting system, etc.)

3. How aggressively do you source?4. What is the entry point for a vendor?5. Is there a procurement-related tax management strategy?

1. What contracts exist and when and how were they negotiated?2 Do existing contracts meet business needs?

IV. Existing Contracts

Strategy/Priorities

• Gaps in current sourcing strategy relative to industry best practices

• Systematically overlooked areas/factors affecting spend (e.g., lack of spend-related tax strategy)

2. Do existing contracts meet business needs?3. Does the product/service provided meet SLAs?4. Can existing contracts be renegotiated to reduce cost?

1 What is your perspective on following initial hypothesis?V. Initial Hypothesis Testing

15

1. What is your perspective on following initial hypothesis?2. In your opinion what additional improvement opportunities exist?

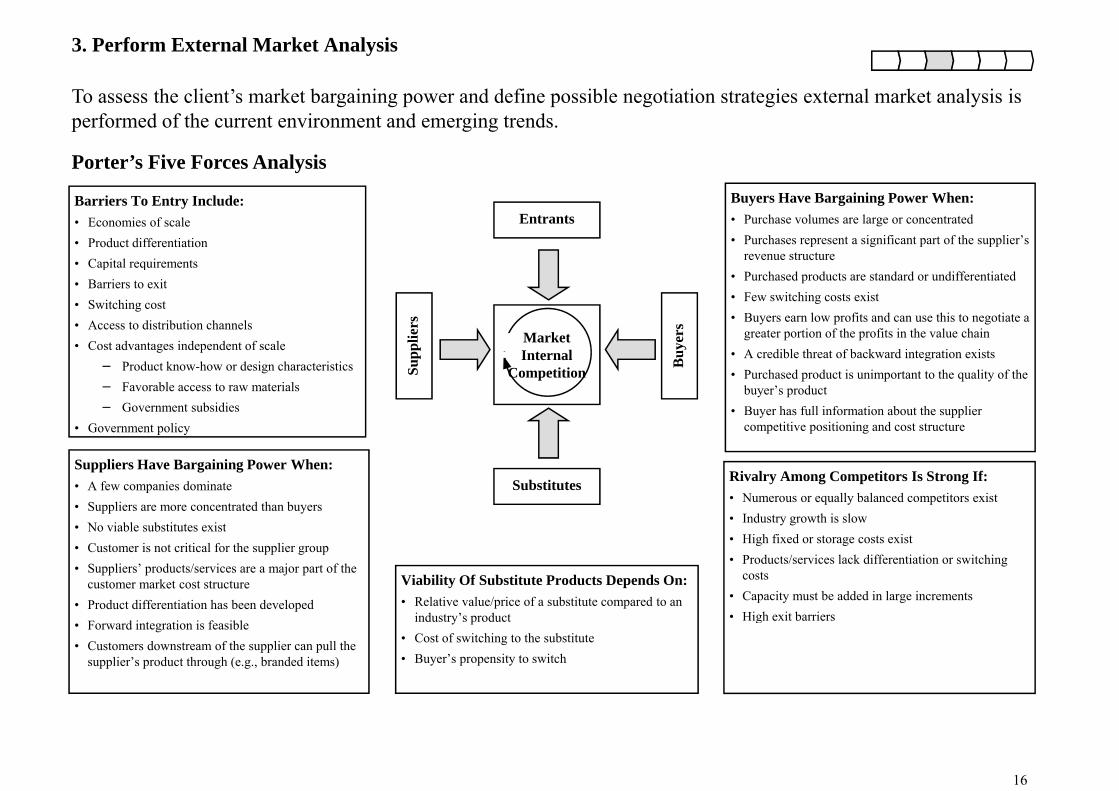

3. Perform External Market Analysis

Porter’s Five Forces Analysis

To assess the client’s market bargaining power and define possible negotiation strategies external market analysis is performed of the current environment and emerging trends.

Buyers Have Bargaining Power When:• Purchase volumes are large or concentrated• Purchases represent a significant part of the supplier’s

revenue structure

Barriers To Entry Include:• Economies of scale• Product differentiation• Capital requirements

Entrants

• Purchased products are standard or undifferentiated• Few switching costs exist• Buyers earn low profits and can use this to negotiate a

greater portion of the profits in the value chainA dibl th t f b k d i t ti i t

• Capital requirements• Barriers to exit• Switching cost• Access to distribution channels• Cost advantages independent of scale Market

I t lplie

rs

uyer

s

• A credible threat of backward integration exists• Purchased product is unimportant to the quality of the

buyer’s product• Buyer has full information about the supplier

competitive positioning and cost structure

g p− Product know-how or design characteristics− Favorable access to raw materials− Government subsidies

• Government policy

Internal CompetitionSu

p Bu

Rivalry Among Competitors Is Strong If:• Numerous or equally balanced competitors exist• Industry growth is slow

Suppliers Have Bargaining Power When:• A few companies dominate• Suppliers are more concentrated than buyers• No viable substitutes exist

Substitutes

• High fixed or storage costs exist• Products/services lack differentiation or switching

costs• Capacity must be added in large increments• High exit barriers

• No viable substitutes exist• Customer is not critical for the supplier group• Suppliers’ products/services are a major part of the

customer market cost structure• Product differentiation has been developed

Viability Of Substitute Products Depends On:• Relative value/price of a substitute compared to an

i d t ’ d t • High exit barriers• Forward integration is feasible• Customers downstream of the supplier can pull the

supplier’s product through (e.g., branded items)

industry’s product• Cost of switching to the substitute• Buyer’s propensity to switch

16

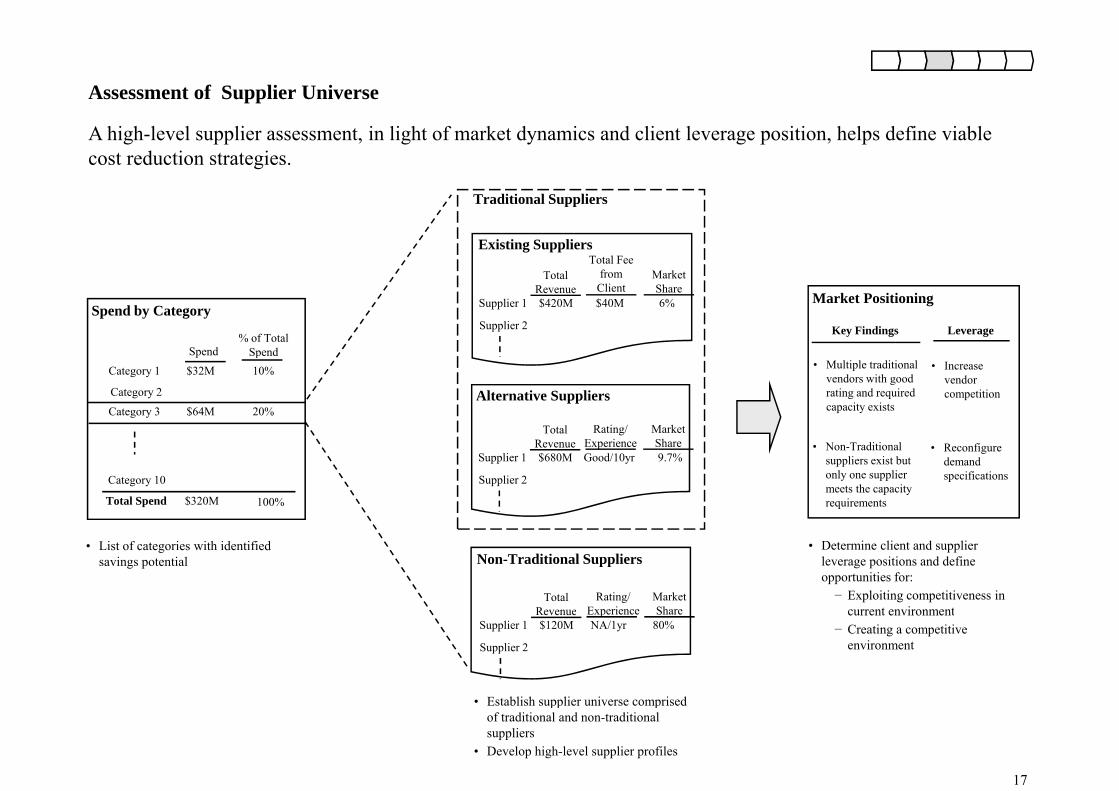

A t f S li U iAssessment of Supplier Universe

A high-level supplier assessment, in light of market dynamics and client leverage position, helps define viable cost reduction strategies.

Traditional Suppliers

Existing SuppliersTotal Fee

Spend by Category

Spend% of Total

Spend

Total Revenue

Total Fee from

ClientMarket Share

Supplier 1 $420M $40M 6%

Supplier 2

Market Positioning

Key Findings Leverage

Category 1 $32M 10%

Spend Spend

Category 2

Category 3 $64M 20%Alternative Suppliers

Total Rating/ E i

Market Sh

• Multiple traditional vendors with good rating and required capacity exists

• Increase vendor competition

Category 10

Total Spend $320M 100%

Revenue Experience ShareSupplier 1 $680M Good/10yr 9.7%

Supplier 2

• Non-Traditional suppliers exist but only one supplier meets the capacity requirements

• Reconfigure demand specifications

Non-Traditional Suppliers

Total Revenue

Rating/ Experience

Market Share

• Determine client and supplier leverage positions and define opportunities for:− Exploiting competitiveness in

current environment

• List of categories with identified savings potential

Revenue pSupplier 1 $120M NA/1yr 80%

Supplier 2

current environment− Creating a competitive

environment

• Establish supplier universe comprised

17

Establish supplier universe comprised of traditional and non-traditional suppliers

• Develop high-level supplier profiles

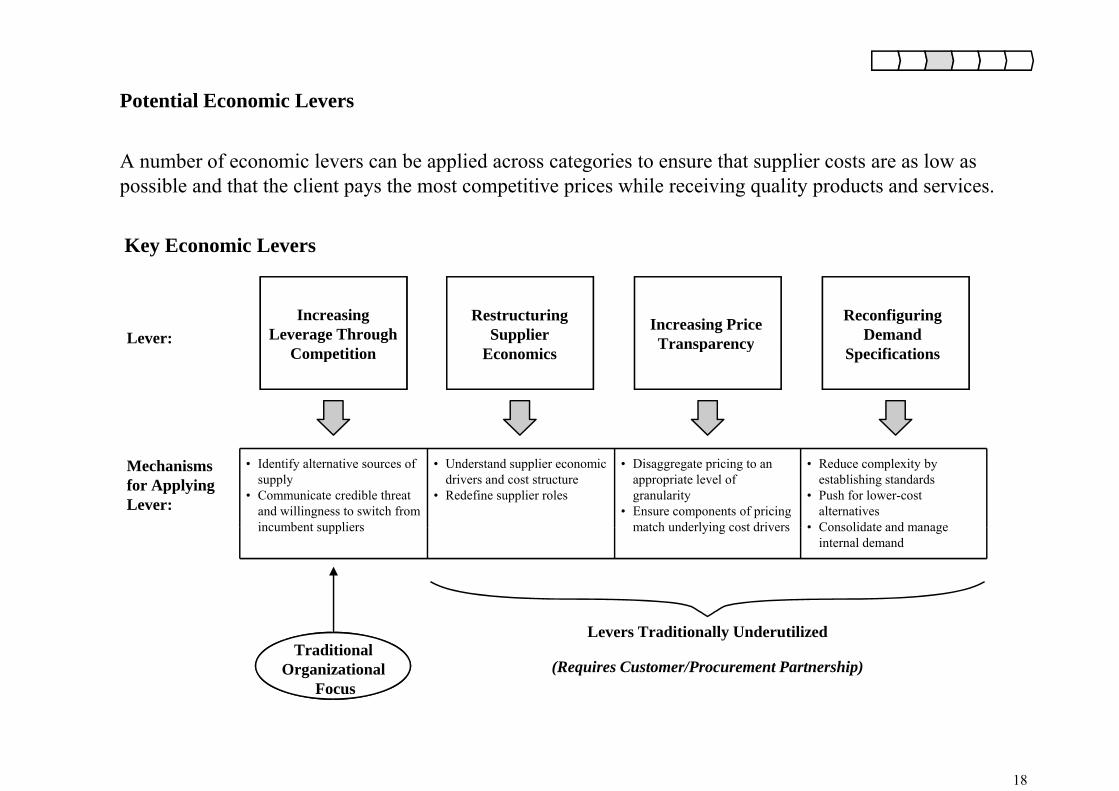

Potential Economic Levers

A number of economic levers can be applied across categories to ensure that supplier costs are as low as

Key Economic Levers

possible and that the client pays the most competitive prices while receiving quality products and services.

IncreasingLeverage Through

CompetitionLever:

Restructuring Supplier

E i

Increasing PriceTransparency

Reconfiguring Demand

S ifi tiCompetition Economics p y Specifications

Mechanisms for Applying Lever:

• Identify alternative sources of supply

• Communicate credible threat and willingness to switch from incumbent suppliers

• Understand supplier economic drivers and cost structure

• Redefine supplier roles

• Disaggregate pricing to an appropriate level of granularity

• Ensure components of pricing match underlying cost drivers

• Reduce complexity by establishing standards

• Push for lower-cost alternatives

• Consolidate and manageincumbent suppliers match underlying cost drivers • Consolidate and manage internal demand

Levers Traditionally Underutilized

(Requires Customer/Procurement Partnership)Traditional

OrganizationalFocus

18

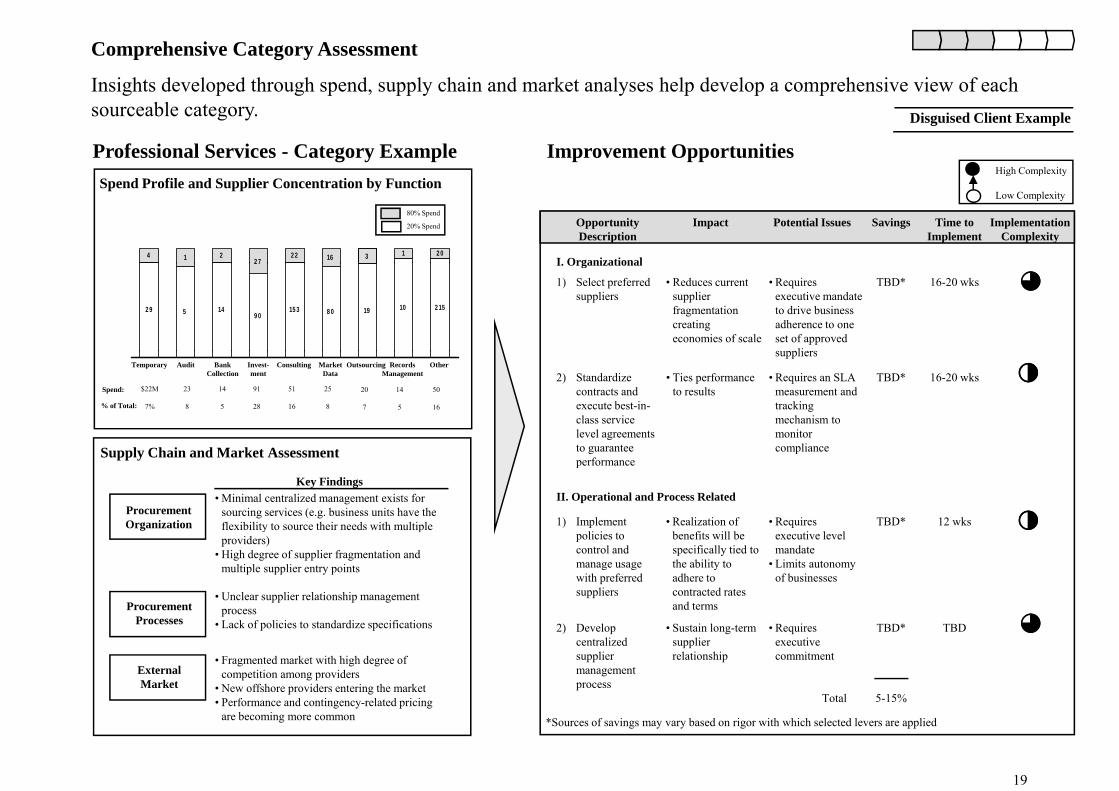

Comprehensive Category Assessment

Insights developed through spend supply chain and market analyses help develop a comprehensive view of each

Professional Services - Category Example

Disguised Client Example

Improvement OpportunitiesHigh Complexity

Insights developed through spend, supply chain and market analyses help develop a comprehensive view of each sourceable category.

Spend Profile and Supplier Concentration by Function

80% Spend

20% Spend

I Organizational

Implementation Complexity

Time to Implement

SavingsPotential IssuesImpactOpportunity Description

2 013162 7214 2 2

g p y

Low Complexity

16-20 wksTBD*• Requires executive mandate to drive business adherence to one set of approved suppliers

• Reduces current supplier fragmentation creating economies of scale

1) Select preferred suppliers

I. Organizational

2 9 5 149 0

15 3 8 0 19 10 2 15

2 7

Temporary Audit BankCollection

Invest-ment

Consulting MarketData

Outsourcing RecordsManagement

Other

Spend: $22M 23 14 91 51 25 20 14 50

% of Total: 7% 8 5 28 16 8 7 5 16

16-20 wksTBD*• Requires an SLA measurement and tracking mechanism to monitor

• Ties performance to results

2) Standardize contracts and execute best-in-class service level agreements

suppliers

Supply Chain and Market Assessment

Key Findings

Procurement Organization

• Minimal centralized management exists for sourcing services (e.g. business units have the flexibility to source their needs with multiple

II. Operational and Process Related

12 wksTBD*• Requires • Realization of 1) Implement

complianceg

to guarantee performance

Organization

Procurement

flexibility to source their needs with multiple providers)

• High degree of supplier fragmentation and multiple supplier entry points

• Unclear supplier relationship management process

qexecutive level mandate

• Limits autonomy of businesses

benefits will be specifically tied to the ability to adhere to contracted rates and terms

) ppolicies to control and manage usage with preferred suppliers

Processes

External Market

p• Lack of policies to standardize specifications

• Fragmented market with high degree of competition among providers

• New offshore providers entering the market• Performance and contingency related pricing

TBDTBD*

5-15%

• Requires executive commitment

Total

• Sustain long-term supplier relationship

2) Develop centralized supplier management process

19

• Performance and contingency-related pricing are becoming more common *Sources of savings may vary based on rigor with which selected levers are applied

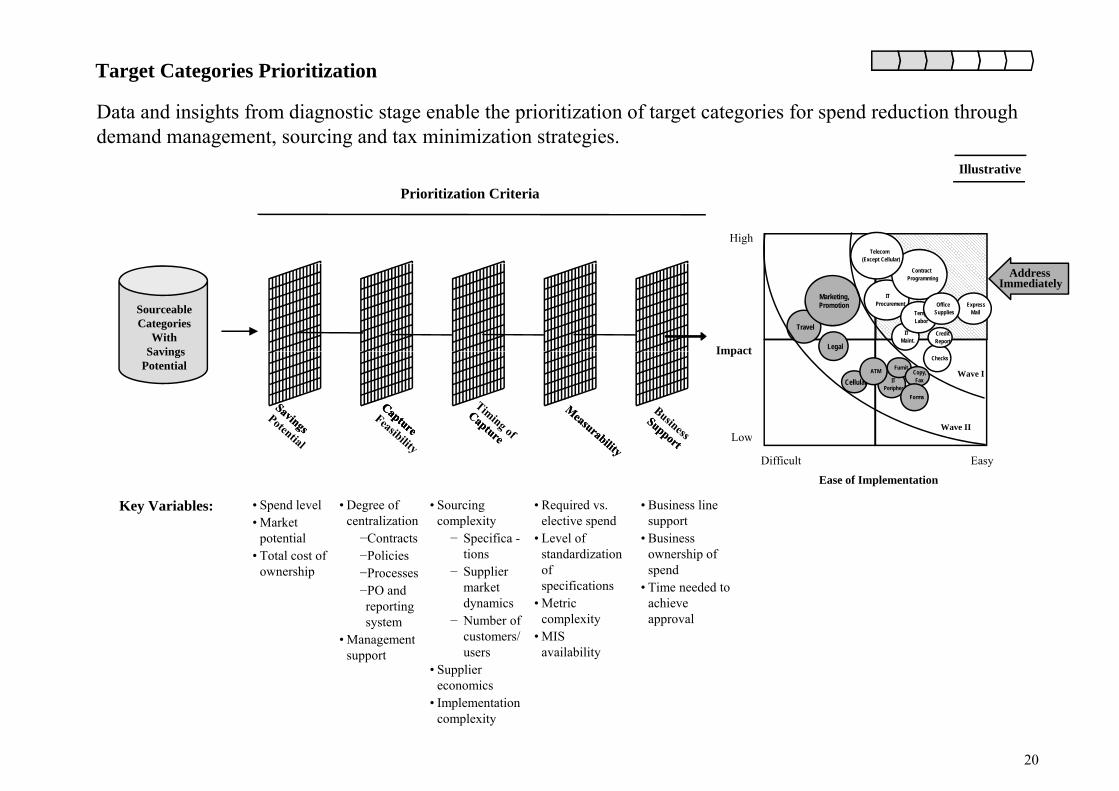

Target Categories Prioritization

Illustrative

Data and insights from diagnostic stage enable the prioritization of target categories for spend reduction through demand management, sourcing and tax minimization strategies.

Prioritization Criteria

HighTelecom

(Except Cellular)

Sourceable Categories

WithSavings Impact

ExpressMail

Travel

Marketing,Promotion

IT Procurement

Contract Programming

IT Maint.

AddressImmediately

CreditReport

Temp.Labor

Office Supplies

LegalSavings Potential

Impact

Low

CellularWave I

Wave II

ITPeripher..

ChecksFurnit.

Copy,Fax

ATM

Forms

Key Variables:

Low

Ease of Implementation

Difficult Easy

• Spend level• Market

• Degree of centralization

• Sourcing complexity

• Required vs. elective spend

• Business line support

potential• Total cost of

ownership

−Contracts−Policies−Processes−PO and reporting

p y− Specifica -

tions− Supplier

market dynamics

p• Level of

standardization of specifications

• Metric l i

pp• Business

ownership of spend

• Time needed to achieve

lsystem• Management

support

− Number of customers/ users

• Supplier economics

• Implementation

complexity• MIS

availability

approval

20

• Implementation complexity

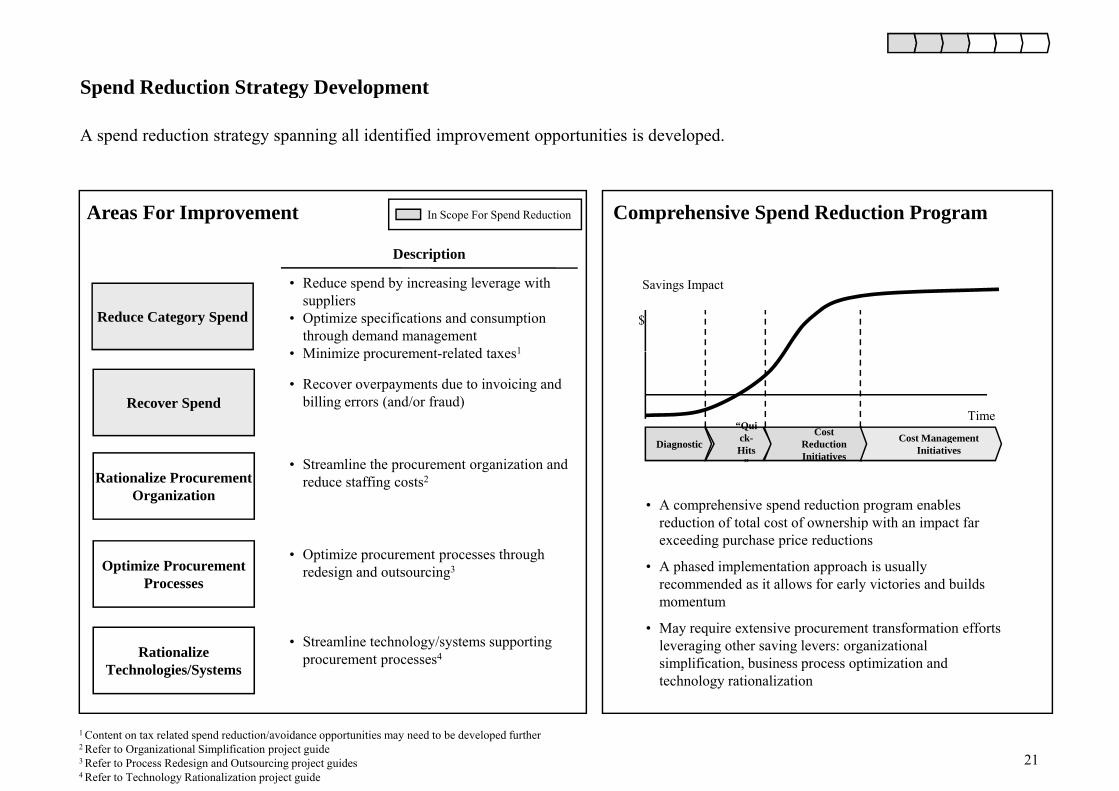

Spend Reduction Strategy Development

A spend reduction strategy spanning all identified improvement opportunities is developed.

Spend Reduction Strategy Development

Areas For Improvement

Description

Comprehensive Spend Reduction ProgramIn Scope For Spend Reduction

Reduce Category Spend $

• Reduce spend by increasing leverage with suppliers

• Optimize specifications and consumption through demand management

• Minimize procurement related taxes1

Savings Impact

Recover Spend“Quick- Cost Cost Management

Time

• Minimize procurement-related taxes1

• Recover overpayments due to invoicing and billing errors (and/or fraud)

Rationalize Procurement Organization

Diagnostic ck-Hits

”

Reduction Initiatives

Cost Management Initiatives

• Streamline the procurement organization and reduce staffing costs2

• A comprehensive spend reduction program enables reduction of total cost of ownership with an impact far

Optimize Procurement Processes

• Optimize procurement processes through redesign and outsourcing3

reduction of total cost of ownership with an impact far exceeding purchase price reductions

• A phased implementation approach is usually recommended as it allows for early victories and builds momentum

Rationalize Technologies/Systems

• Streamline technology/systems supporting procurement processes4

• May require extensive procurement transformation efforts leveraging other saving levers: organizational simplification, business process optimization and technology rationalization

21

1 Content on tax related spend reduction/avoidance opportunities may need to be developed further2 Refer to Organizational Simplification project guide3 Refer to Process Redesign and Outsourcing project guides4 Refer to Technology Rationalization project guide

ii. Implement Improvements

During the implementation phase the set of improvement opportunities identified and prioritized in theDuring the implementation phase, the set of improvement opportunities identified and prioritized in the diagnostic phase are investigated in more detail, refined and rolled out to the business(es). In the following pages we describe how to:

4 R ti li C t S d* Eff t t ti li t d i l d4. Rationalize Category Spend*. Efforts to rationalize category spend include:a. Demand Rationalization: reconfiguring of product/service specifications and optimization of

usageb Strategic Sourcing: reduction of costs by increasing leverage with vendorsb. Strategic Sourcing: reduction of costs by increasing leverage with vendorsc. Procurement Tax Optimization: minimization of procurement-related tax spend

While demand focused activities often precede supplier sourcing, both types of efforts should not be pursued in isolation of each other Tax strategies can be pursued in conjunction with demandpursued in isolation of each other. Tax strategies can be pursued in conjunction with demand management and sourcing or as part of an independent tax minimization initiative.

5. Recover Spend. In addition to reducing the operating expense base going forward, very often the opportunity exists to recover certain types of spend that have been incurred in the past due toopportunity exists to recover certain types of spend that have been incurred in the past due to errors/inefficiencies in the billing, payment and tax assessment processes.

6. Implement Improvements. When executing against a broad spectrum of spend reduction initiatives, ongoing organizational commitment and rigorous management against savings targets ensure successongoing organizational commitment and rigorous management against savings targets ensure success.

22* Content on tax related spend reduction/avoidance opportunities may need to be developed further

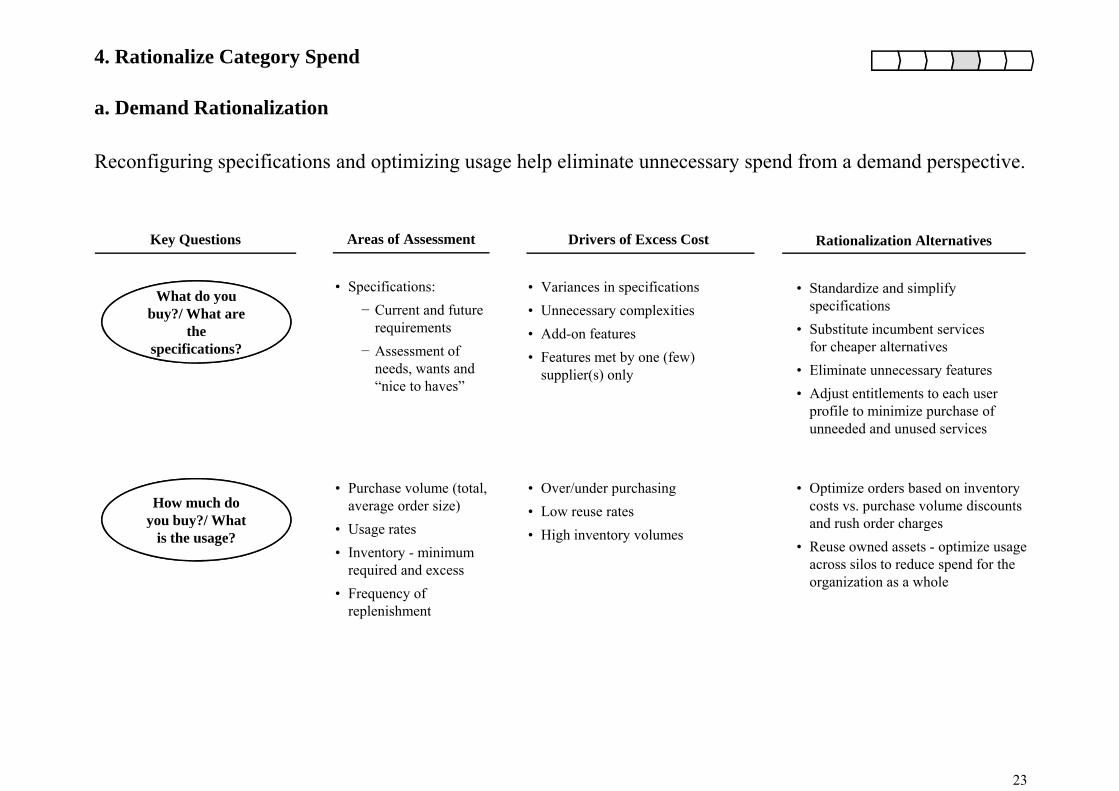

4. Rationalize Category Spend

Reconfiguring specifications and optimizing usage help eliminate unnecessary spend from a demand perspective.

a. Demand Rationalization

Key Questions Drivers of Excess Cost Rationalization AlternativesAreas of Assessment

What do you buy?/ What are

the specifications?

• Variances in specifications• Unnecessary complexities• Add-on features

• Standardize and simplify specifications

• Substitute incumbent services for cheaper alternatives

• Specifications:− Current and future

requirements− Assessment ofspecifications? • Features met by one (few)

supplier(s) only

o c eape a te at ves• Eliminate unnecessary features• Adjust entitlements to each user

profile to minimize purchase of unneeded and unused services

Assessment of needs, wants and “nice to haves”

How much do you buy?/ What

• Purchase volume (total, average order size)

• Usage rates

• Over/under purchasing• Low reuse rates

• Optimize orders based on inventory costs vs. purchase volume discounts and rush order chargesy y

is the usage? • Usage rates• Inventory - minimum

required and excess • Frequency of

replenishment

• High inventory volumesand rush order charges

• Reuse owned assets - optimize usage across silos to reduce spend for the organization as a whole

replenishment

23

Reconfiguring Specifications

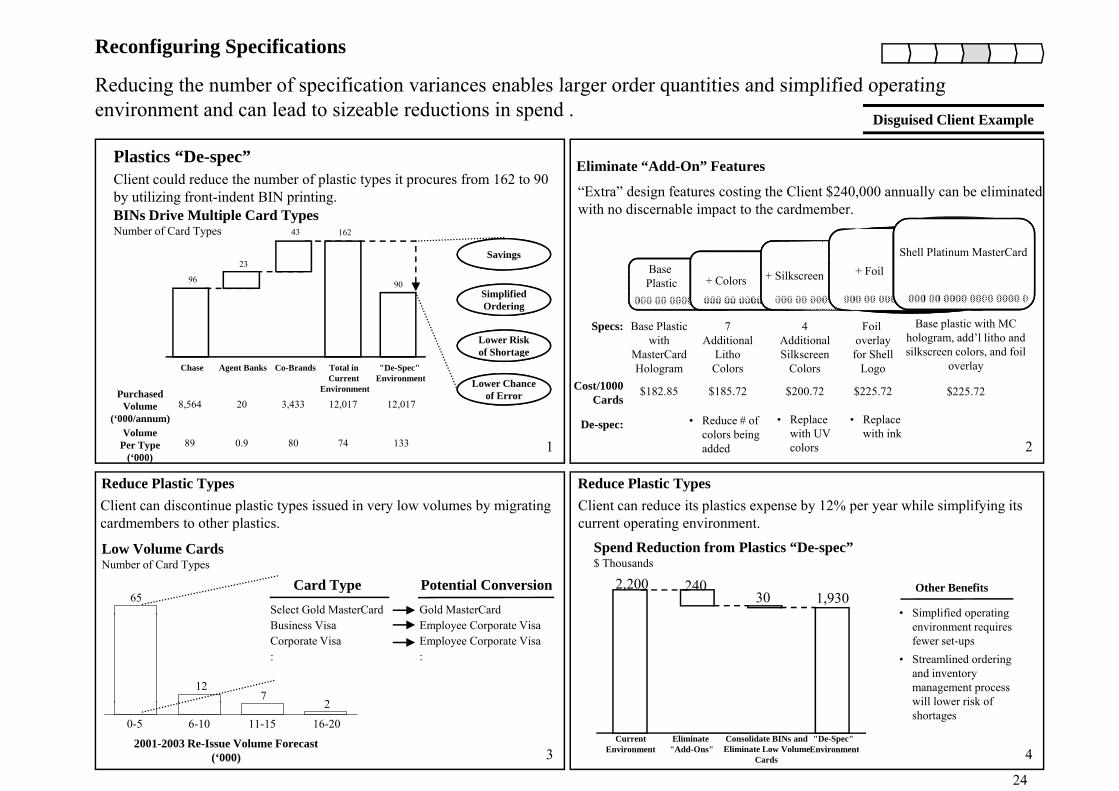

Reducing the number of specification variances enables larger order quantities and simplified operatingReducing the number of specification variances enables larger order quantities and simplified operating environment and can lead to sizeable reductions in spend .

Eliminate “Add-On” FeaturesPlastics “De-spec”Cli t ld d th b f l ti t it f 162 t 90

Disguised Client Example

“Extra” design features costing the Client $240,000 annually can be eliminated with no discernable impact to the cardmember.

Shell Platinum MasterCard

Client could reduce the number of plastic types it procures from 162 to 90 by utilizing front-indent BIN printing.BINs Drive Multiple Card TypesNumber of Card Types

23

16243

Savings

Specs:

000 00 0000 0000 0000 00 0000 0000 0000 00 0000 0000 0000 00 0000 0000 0000 00 0000 0000 0000 0

Base Plasticwith

M t C d

7Additional

Lith

4AdditionalSilk

Foil overlayf Sh ll

BasePlastic + Colors + Silkscreen + Foil

Base plastic with MC hologram, add’l litho and silkscreen colors and foil

96

23

90SimplifiedOrdering

Lower Riskof Shortage

Cost/1000Cards

$182.85

MasterCardHologram

LithoColors

SilkscreenColors

for ShellLogo

$185.72 $200.72 $225.72 $225.72

silkscreen colors, and foil overlay

• Replace with ink

• Replace with UV

• Reduce # of colors being

De-spec:

PurchasedVolume

(‘000/annum)Volume

8,564 20 3,433 12,017 12,017

Chase Agent Banks Co-Brands Total in Current

Environment

"De-Spec" Environment

of Shortage

Lower ChanceLower Chanceof Error

Client can reduce its plastics expense by 12% per year while simplifying its current operating environment.

colorsg

added

Client can discontinue plastic types issued in very low volumes by migrating cardmembers to other plastics.

Reduce Plastic Types Reduce Plastic Types

Per Type(‘000)

89 0.9 80 74 133 1 2

Spend Reduction from Plastics “De-spec”$ Thousands

current operating environment.

2,200 24030 1,930

• Simplified operating

Other Benefits

Low Volume CardsNumber of Card Types

cardmembers to other plastics.

65Select Gold MasterCard

Card Type Potential ConversionGold MasterCard Simplified operating

environment requires fewer set-ups

• Streamlined ordering and inventory management process will lower risk of

127

2

Business VisaCorporate Visa :

Employee Corporate VisaEmployee Corporate Visa:

24

Eliminate Low VolumeCurrent

Environment Eliminate

"Add-Ons"Consolidate BINs and

Cards

"De-Spec" Environment

will lower risk of shortages

2001-2003 Re-Issue Volume Forecast(‘000)

2

0-5 6-10 11-15 16-20

3 4

Optimizing Usage

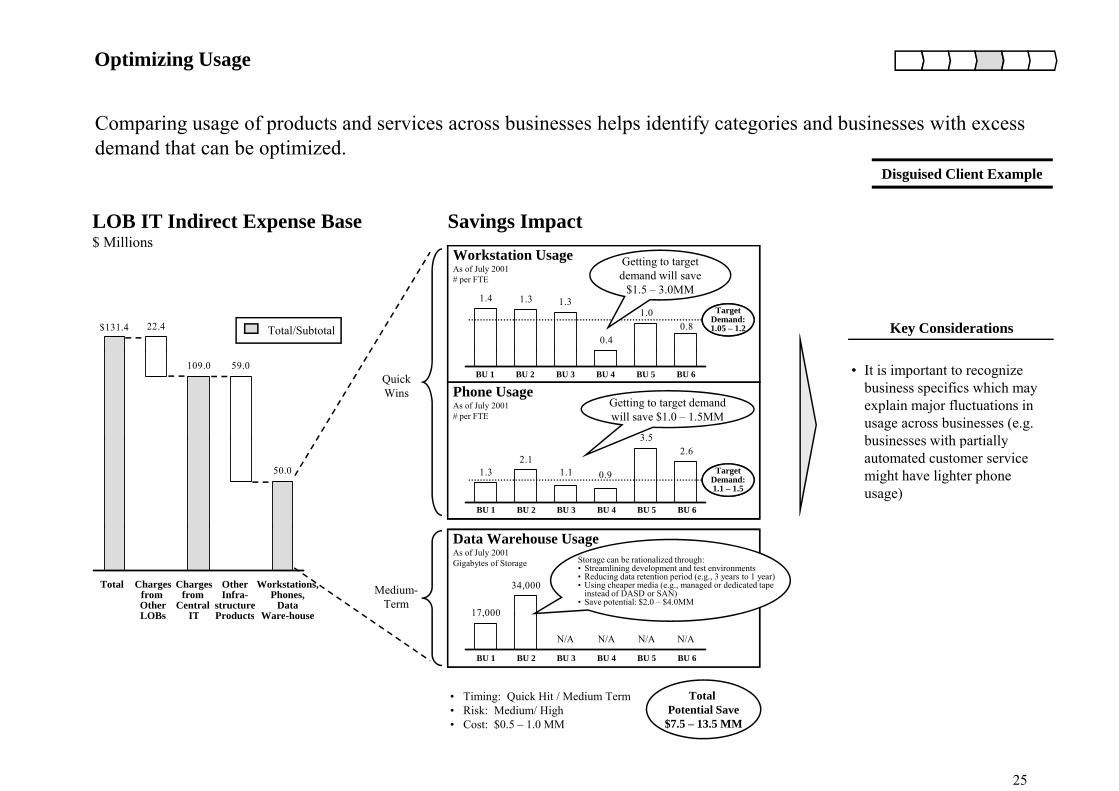

Comparing usage of products and services across businesses helps identify categories and businesses with excess demand that can be optimized.

Disguised Client ExampleDisguised Client Example

LOB IT Indirect Expense Base$ Millions

Workstation Usage Getting to target

Savings Impact

Key Considerations22.4$131.4 Total/Subtotal

As of July 2001# per FTE

0.81.0

0.4

1.31.31.4Target

1.05 1.2

TargetDemand:1.05 – 1.2

Getting to target demand will save

$1.5 – 3.0MM

• It is important to recognize business specifics which may explain major fluctuations in usage across businesses (e.g. businesses with partially

59.0109.0BU 1 BU 2 BU 3 BU 4 BU 5 BU 6

Phone UsageAs of July 2001# per FTE

3 5

Getting to target demand will save $1.0 – 1.5MM

QuickWins

businesses with partially automated customer service might have lighter phone usage)

50.0

2.63.5

0.91.12.1

1.3 Target

1.1 1.5

TargetDemand:1.1 – 1.5

BU 1 BU 2 BU 3 BU 4 BU 5 BU 6

Total Chargesfrom OtherLOBs

Chargesfrom

Central IT

OtherInfra-

structureProducts

Workstations,Phones,

DataWare house

Data Warehouse UsageAs of July 2001Gigabytes of Storage

34,000

17,000

Storage can be rationalized through:• Streamlining development and test environments• Reducing data retention period (e.g., 3 years to 1 year)• Using cheaper media (e.g., managed or dedicated tape

instead of DASD or SAN)• Save potential: $2.0 – $4.0MM

Medium-Term

LOBs IT Products Ware-house

N/AN/AN/AN/A

17,000

BU 1 BU 2 BU 3 BU 4 BU 5 BU 6

• Timing: Quick Hit / Medium Term Total

25

• Risk: Medium/ High• Cost: $0.5 – 1.0 MM

Potential Save$7.5 – 13.5 MM

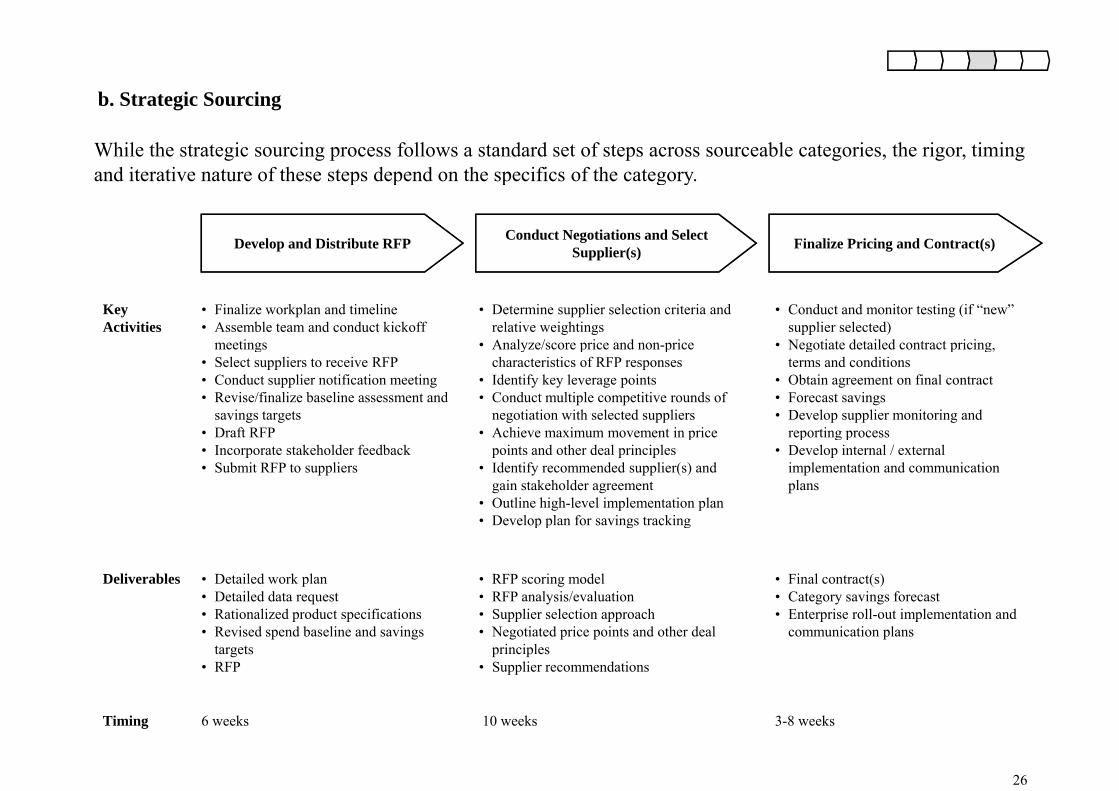

While the strategic sourcing process follows a standard set of steps across sourceable categories, the rigor, timing and iterative nature of these steps depend on the specifics of the category

b. Strategic Sourcing

and iterative nature of these steps depend on the specifics of the category.

Conduct Negotiations and Select Supplier(s) Finalize Pricing and Contract(s)Develop and Distribute RFP

• Finalize workplan and timeline• Assemble team and conduct kickoff

meetings

• Determine supplier selection criteria and relative weightings

• Analyze/score price and non-price

• Conduct and monitor testing (if “new” supplier selected)

• Negotiate detailed contract pricing,

Key Activities

g• Select suppliers to receive RFP• Conduct supplier notification meeting• Revise/finalize baseline assessment and

savings targets• Draft RFP

y p pcharacteristics of RFP responses

• Identify key leverage points • Conduct multiple competitive rounds of

negotiation with selected suppliers• Achieve maximum movement in price

g p g,terms and conditions

• Obtain agreement on final contract• Forecast savings• Develop supplier monitoring and

reporting process• Incorporate stakeholder feedback• Submit RFP to suppliers

ppoints and other deal principles

• Identify recommended supplier(s) and gain stakeholder agreement

• Outline high-level implementation plan• Develop plan for savings tracking

p g p• Develop internal / external

implementation and communication plans

Deliverables • Detailed work plan• Detailed data request• Rationalized product specifications

• RFP scoring model• RFP analysis/evaluation • Supplier selection approach

p p g g

• Final contract(s)• Category savings forecast• Enterprise roll-out implementation and• Rationalized product specifications

• Revised spend baseline and savings targets

• RFP

• Supplier selection approach• Negotiated price points and other deal

principles• Supplier recommendations

• Enterprise roll-out implementation and communication plans

26

Timing 6 weeks 10 weeks 3-8 weeks

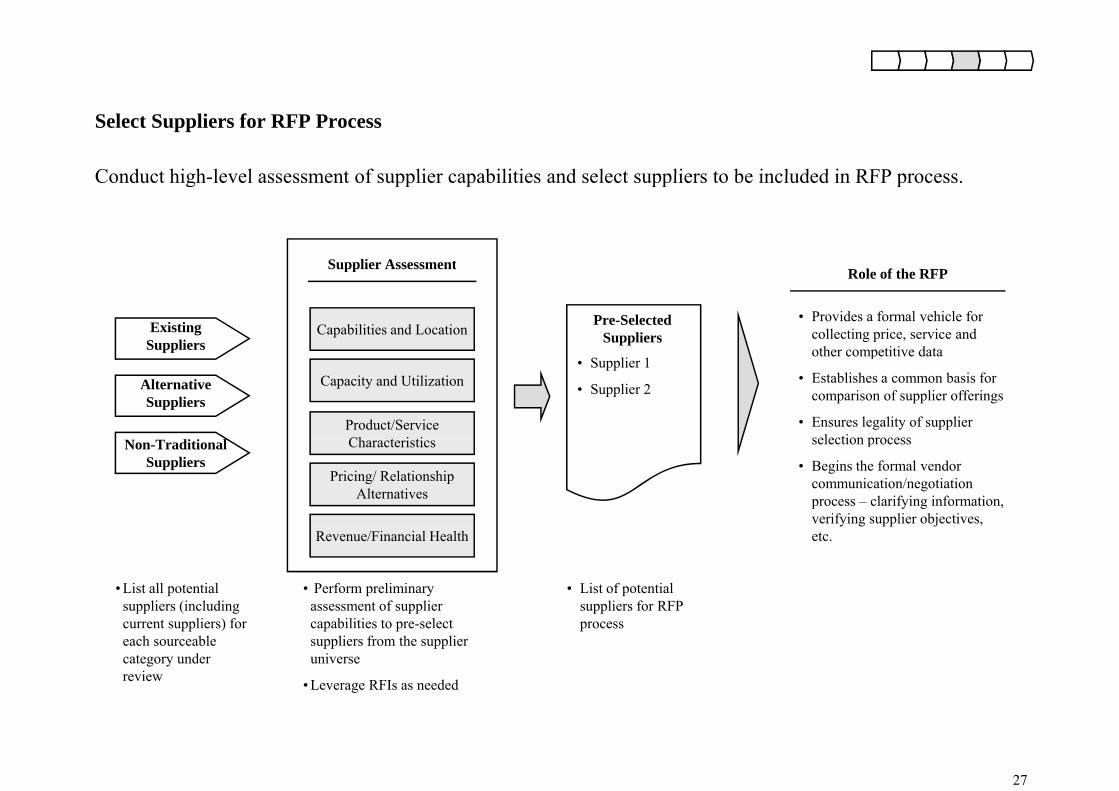

Conduct high level assessment of supplier capabilities and select suppliers to be included in RFP process

Select Suppliers for RFP Process

Conduct high-level assessment of supplier capabilities and select suppliers to be included in RFP process.

Supplier Assessment

Capabilities and Location

Supplier Assessment

Existing Suppliers

Role of the RFP

• Provides a formal vehicle for collecting price, service and other competitive data

Pre-Selected Suppliers

Capacity and Utilization

Product/Service Ch t i ti

pp

Alternative Suppliers

other competitive data

• Establishes a common basis for comparison of supplier offerings

• Ensures legality of supplier selection process

• Supplier 1

• Supplier 2

Pricing/ Relationship Alternatives

CharacteristicsNon-Traditional Suppliers

selection process

• Begins the formal vendor communication/negotiation process – clarifying information, verifying supplier objectives,

• List all potential suppliers (including

Revenue/Financial Health

• List of potential suppliers for RFP

• Perform preliminary assessment of supplier

etc.

current suppliers) for each sourceable category under review

processcapabilities to pre-select suppliers from the supplier universe

• Leverage RFIs as needed

27

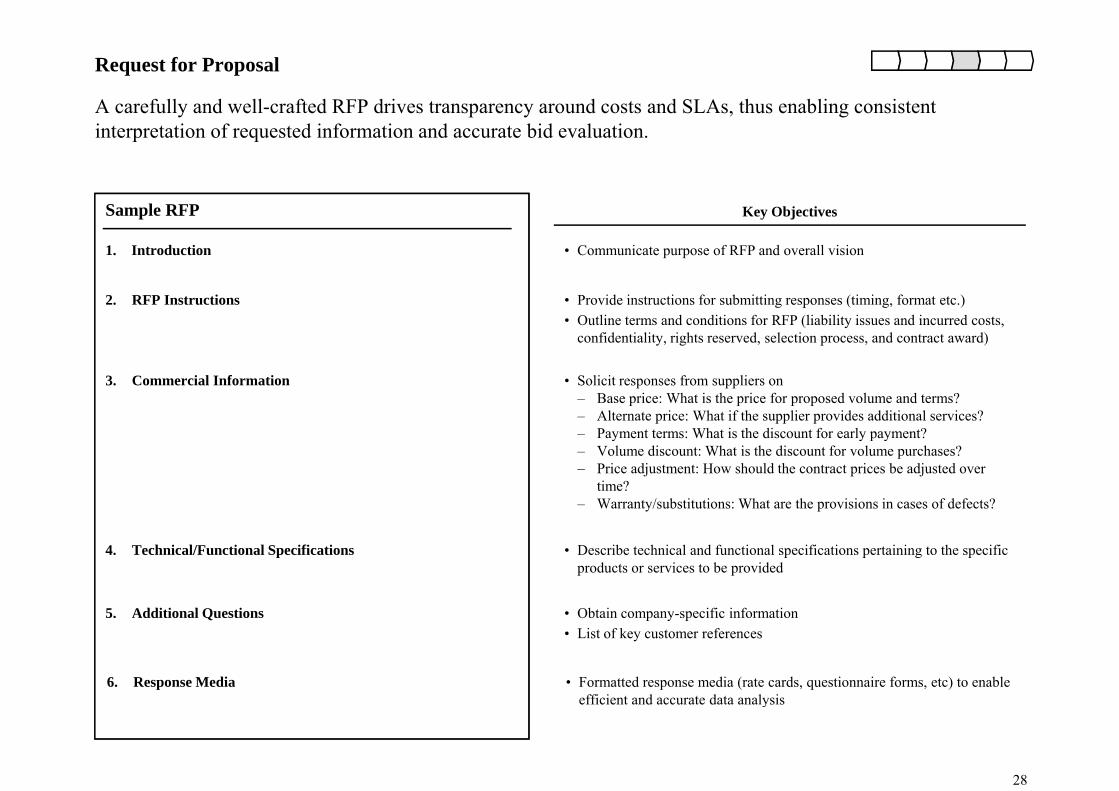

Request for Proposal

A carefully and well-crafted RFP drives transparency around costs and SLAs, thus enabling consistent interpretation of requested information and accurate bid evaluation.

Sample RFP

1. Introduction

Key Objectives

• Communicate purpose of RFP and overall vision

2. RFP Instructions • Provide instructions for submitting responses (timing, format etc.)• Outline terms and conditions for RFP (liability issues and incurred costs,

confidentiality, rights reserved, selection process, and contract award)

3. Commercial Information • Solicit responses from suppliers on– Base price: What is the price for proposed volume and terms?– Alternate price: What if the supplier provides additional services?– Payment terms: What is the discount for early payment?y y p y– Volume discount: What is the discount for volume purchases? – Price adjustment: How should the contract prices be adjusted over

time?– Warranty/substitutions: What are the provisions in cases of defects?

4. Technical/Functional Specifications

5 Additional Questions

• Describe technical and functional specifications pertaining to the specific products or services to be provided

• Obtain company-specific information5. Additional Questions Obtain company-specific information• List of key customer references

6. Response Media • Formatted response media (rate cards, questionnaire forms, etc) to enable efficient and accurate data analysis

28

efficient and accurate data analysis

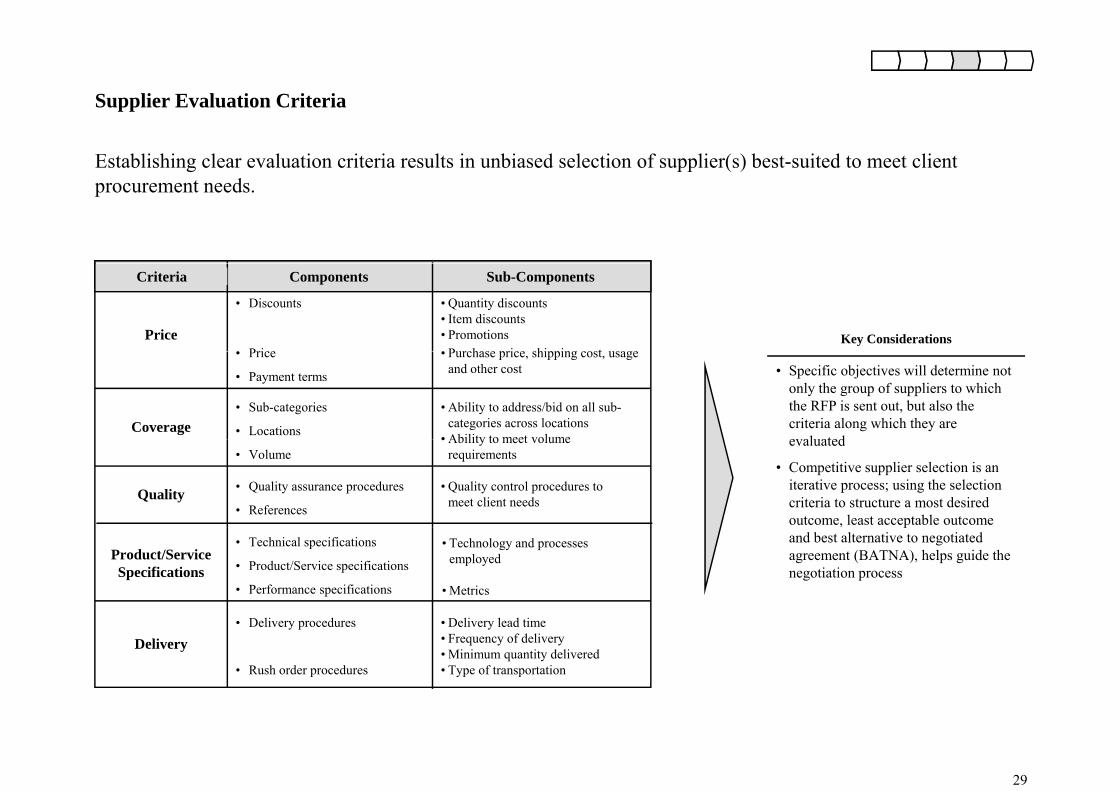

Supplier Evaluation Criteria

Establishing clear evaluation criteria results in unbiased selection of supplier(s) best-suited to meet client procurement needs.

Criteria Components Sub-Components

Price

• Discounts • Quantity discounts• Item discounts• Promotions Key Considerations• Purchase price shipping cost usage• Price

Coverage• Sub-categories

• Locations

• Ability to address/bid on all sub-categories across locations

• Ability to meet volume

• Specific objectives will determine not only the group of suppliers to which the RFP is sent out, but also the criteria along which they are evaluated

• Purchase price, shipping cost, usage and other cost

• Price

• Payment terms

• Volume• Ability to meet volume

requirementsevaluated

• Competitive supplier selection is an iterative process; using the selection criteria to structure a most desired outcome, least acceptable outcome

Quality • Quality assurance procedures

• References

• Quality control procedures to meet client needs

Product/Service Specifications

• Technical specifications

• Product/Service specifications

• Performance specifications

, pand best alternative to negotiated agreement (BATNA), helps guide the negotiation process

• Technology and processes employed

• Metrics

Delivery• Delivery procedures

• Rush order procedures

• Delivery lead time• Frequency of delivery• Minimum quantity delivered• Type of transportation

29

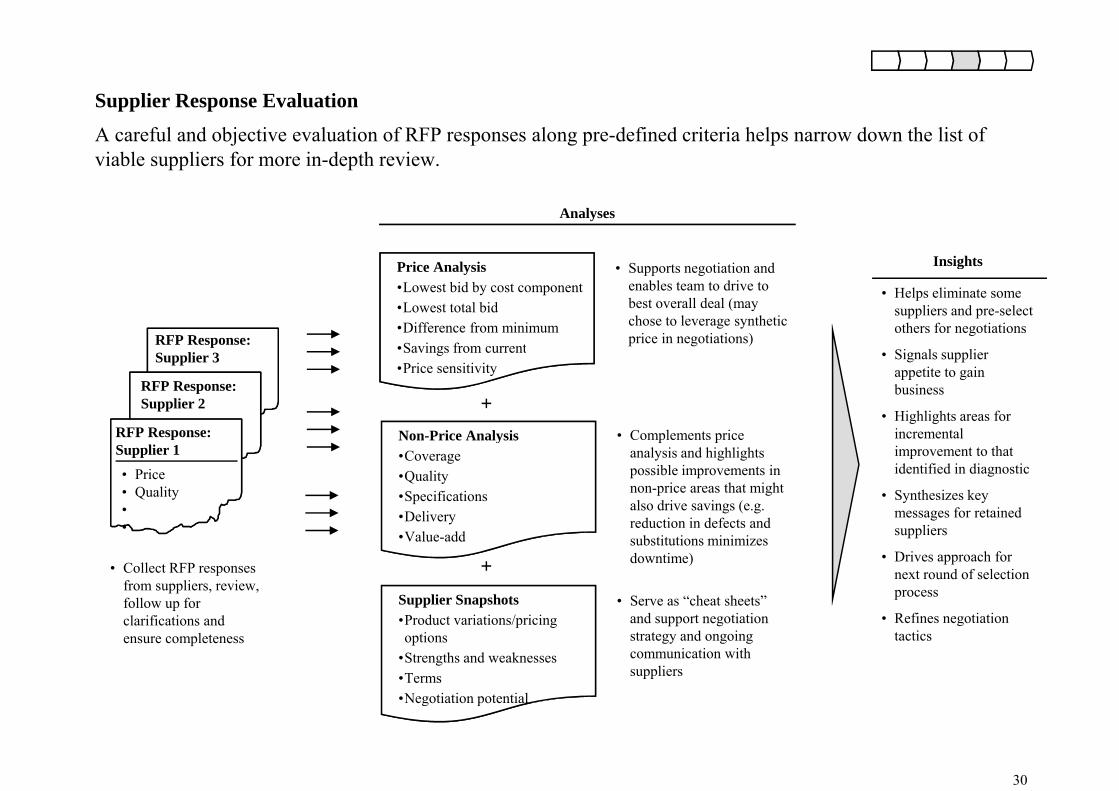

Supplier Response Evaluation

A careful and objective evaluation of RFP responses along pre-defined criteria helps narrow down the list of viable suppliers for more in-depth review.

S i i d

Analyses

P i A l i Insights• Supports negotiation and enables team to drive to best overall deal (may chose to leverage synthetic price in negotiations)RFP Response:

Price Analysis•Lowest bid by cost component•Lowest total bid•Difference from minimum•Savings from current

Insights

• Helps eliminate some suppliers and pre-select others for negotiations

Si l li

• Price• Quality ••

Supplier 3Savings from current

•Price sensitivity

• Price

RFP Response: Supplier 2

RFP Response:

• Signals supplier appetite to gain business

• Highlights areas for incremental • Complements priceNon-Price Analysis

+

• Quality ••• Price

• Quality ••

pSupplier 1 improvement to that

identified in diagnostic

• Synthesizes key messages for retained

li

Complements price analysis and highlights possible improvements in non-price areas that might also drive savings (e.g. reduction in defects and

Non Price Analysis•Coverage •Quality•Specifications•Delivery

• Collect RFP responses from suppliers, review, follow up for

• suppliers

• Drives approach for next round of selection process

R fi ti ti

reduction in defects and substitutions minimizes downtime)

•Value-add

• Serve as “cheat sheets” d t ti ti

Supplier Snapshotsd i i / i i

+

clarifications and ensure completeness

• Refines negotiation tactics

and support negotiation strategy and ongoing communication with suppliers

•Product variations/pricing options

•Strengths and weaknesses•Terms•Negotiation potential

30

Negotiation potential

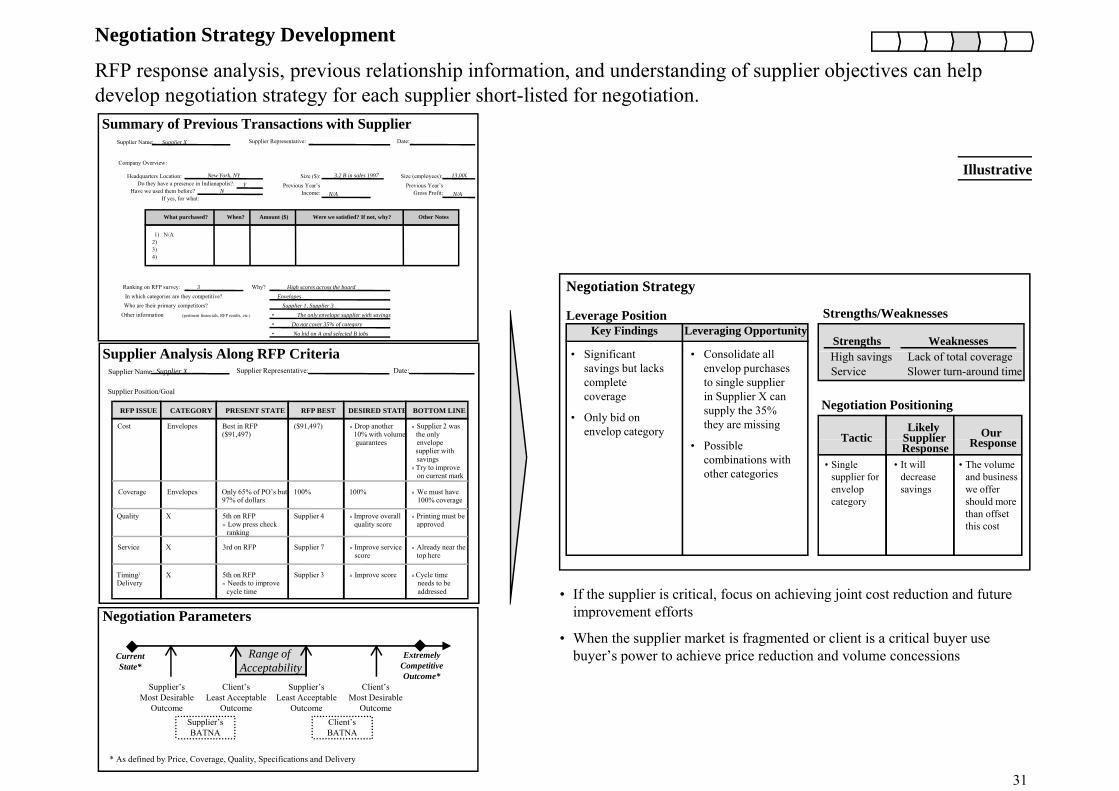

Negotiation Strategy Development

RFP response analysis, previous relationship information, and understanding of supplier objectives can help d l i i f h li h li d f i idevelop negotiation strategy for each supplier short-listed for negotiation. Summary of Previous Transactions with Supplier

Supplier Name: Supplier X Supplier Representative: Date:

Company Overview:

Headquarters Location: Size ($): Size (employees):New York NY 3 2 B in sales 1997 13 000 IllustrativeHeadquarters Location:Do they have a presence in Indianapolis?:

Have we used them before?If yes, for what:

Size ($):Previous Year’s

Income:

Size (employees):Previous Year’s

Gross Profit:

New York, NYY

N

3.2 B in sales 1997

N/AN/A

13,000

What purchased? When? Amount ($) Were we satisfied? If not, why? Other Notes

1) N/A2)3)4)

Negotiation Strategy Ranking on RFP survey:In which categories are they competitive?Who are their primary competitors?

Other information (pertinent financials, RFP results, etc.)

Why? High scores across the boardEnvelopes

Supplier 1, Supplier 3• The only envelope supplier with savings• Do not cover 35% of category• No bid on A and selected B jobs

3

S li A l i Al RFP C it i

Key Findings Leveraging OpportunityLeverage Position Strengths/Weaknesses

Strengths WeaknessesSi ifi t C lid t llSupplier Analysis Along RFP Criteria

TacticLikely

Supplier OurR

Negotiation Positioning

High savingsService

Lack of total coverageSlower turn-around timeSupplier Name: Supplier X Supplier Representative: Date:

Supplier Position/Goal

RFP ISSUE CATEGORY PRESENT STATE RFP BEST DESIRED STATE BOTTOM LINE

Cost Envelopes Best in RFP($91,497)

($91,497) n Drop another10% with volume

n Supplier 2 wasthe only

• Significant savings but lacks complete coverage

• Only bid on envelop category

• Consolidate all envelop purchases to single supplier in Supplier X can supply the 35% they are missing

Tactic SupplierResponse Responseguarantees envelope

supplier withsavings

n Try to improveon current mark

Coverage Envelopes Only 65% of PO’s but97% of dollars

100% 100% n We must have100% coverage

Quality X Supplier 4 n Printing must beapproved

n Improve overallquality score

5th on RFPn Low press check

• Possible combinations with other categories

• Single supplier for envelop category

• It will decrease savings

• The volume and business we offer should more than offset this cost

• If the supplier is critical, focus on achieving joint cost reduction and future improvement efforts

5th on RFPn Needs to improve

cycle time

ppq y

Service X 3rd on RFP Supplier 7 n Already near thetop here

n Improve servicescore

Timing/Delivery

X Supplier 3 n Cycle timeneeds to beaddressed

n Improve score

pranking

this cost

Negotiation Parameters improvement efforts

• When the supplier market is fragmented or client is a critical buyer use buyer’s power to achieve price reduction and volume concessions

Negotiation Parameters

Current State*

ExtremelyCompetitive Outcome*

Client’s Most Desirable

Supplier’sLeast Acceptable

Client’s Least Acceptable

Supplier’sMost Desirable

Range of Acceptability

31

OutcomeOutcomeOutcomeOutcomeClient’s BATNA

Supplier’sBATNA

* As defined by Price, Coverage, Quality, Specifications and Delivery

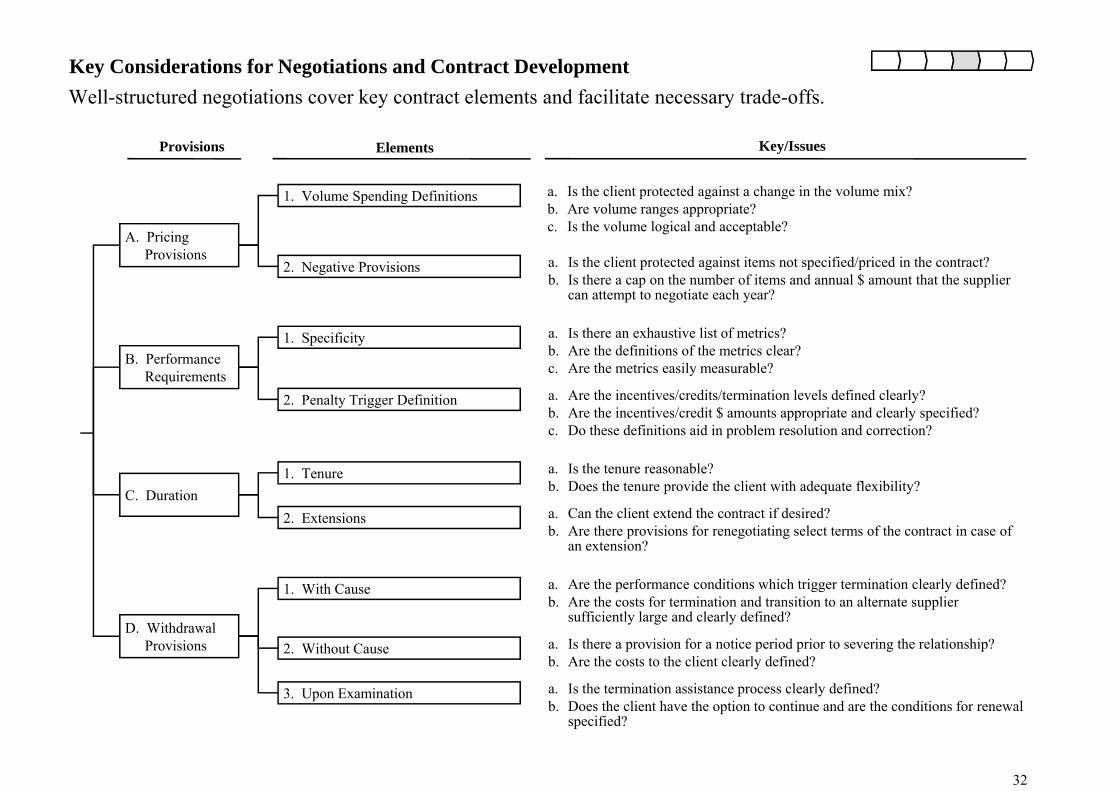

Key Considerations for Negotiations and Contract Development

Provisions Elements Key/Issues

Well-structured negotiations cover key contract elements and facilitate necessary trade-offs.

A. Pricing Provisions

a. Is the client protected against a change in the volume mix?b. Are volume ranges appropriate?c. Is the volume logical and acceptable?

1. Volume Spending Definitions

2 N ti P i i a Is the client protected against items not specified/priced in the contract?2. Negative Provisions a. Is the client protected against items not specified/priced in the contract?b. Is there a cap on the number of items and annual $ amount that the supplier

can attempt to negotiate each year?

1. Specificity a. Is there an exhaustive list of metrics?b Are the definitions of the metrics clear?B. Performance

Requirements

b. Are the definitions of the metrics clear?c. Are the metrics easily measurable?

2. Penalty Trigger Definition a. Are the incentives/credits/termination levels defined clearly?b. Are the incentives/credit $ amounts appropriate and clearly specified?c. Do these definitions aid in problem resolution and correction?

C. Duration1. Tenure a. Is the tenure reasonable?

b. Does the tenure provide the client with adequate flexibility?

2. Extensions a. Can the client extend the contract if desired?b A th i i f ti ti l t t f th t t i fb. Are there provisions for renegotiating select terms of the contract in case of

an extension?

1. With Cause a. Are the performance conditions which trigger termination clearly defined?b. Are the costs for termination and transition to an alternate supplier

sufficiently large and clearly defined?D. Withdrawal

Provisions

sufficiently large and clearly defined?

2. Without Cause a. Is there a provision for a notice period prior to severing the relationship?b. Are the costs to the client clearly defined?

3. Upon Examination a. Is the termination assistance process clearly defined?b D th li t h th ti t ti d th diti f l

32

b. Does the client have the option to continue and are the conditions for renewal specified?

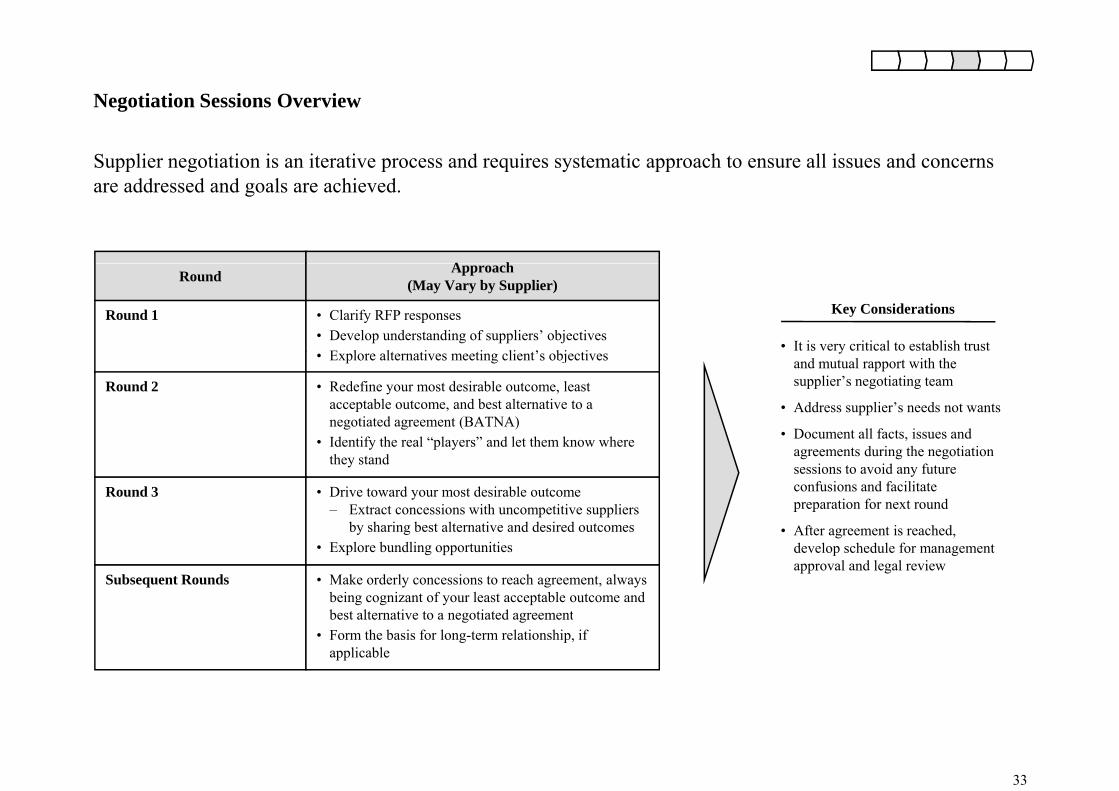

Negotiation Sessions Overview

Supplier negotiation is an iterative process and requires systematic approach to ensure all issues and concerns are addressed and goals are achieved.

A h

Key Considerations

• It is very critical to establish trust

Round 1

Round

• Clarify RFP responses• Develop understanding of suppliers’ objectives

E l l i i li ’ bj i

Approach(May Vary by Supplier)

yand mutual rapport with the supplier’s negotiating team

• Address supplier’s needs not wants

• Document all facts, issues and

• Explore alternatives meeting client’s objectives

Round 2 • Redefine your most desirable outcome, least acceptable outcome, and best alternative to a negotiated agreement (BATNA)Id tif th l “ l ” d l t th k h ,

agreements during the negotiation sessions to avoid any future confusions and facilitate preparation for next round

Aft t i h d

• Identify the real “players” and let them know where they stand

Round 3 • Drive toward your most desirable outcome – Extract concessions with uncompetitive suppliers

by sharing best alternative and desired outcomes • After agreement is reached, develop schedule for management approval and legal review

by sharing best alternative and desired outcomes• Explore bundling opportunities

Subsequent Rounds • Make orderly concessions to reach agreement, always being cognizant of your least acceptable outcome and best alternative to a negotiated agreementbest alternative to a negotiated agreement

• Form the basis for long-term relationship, if applicable

33

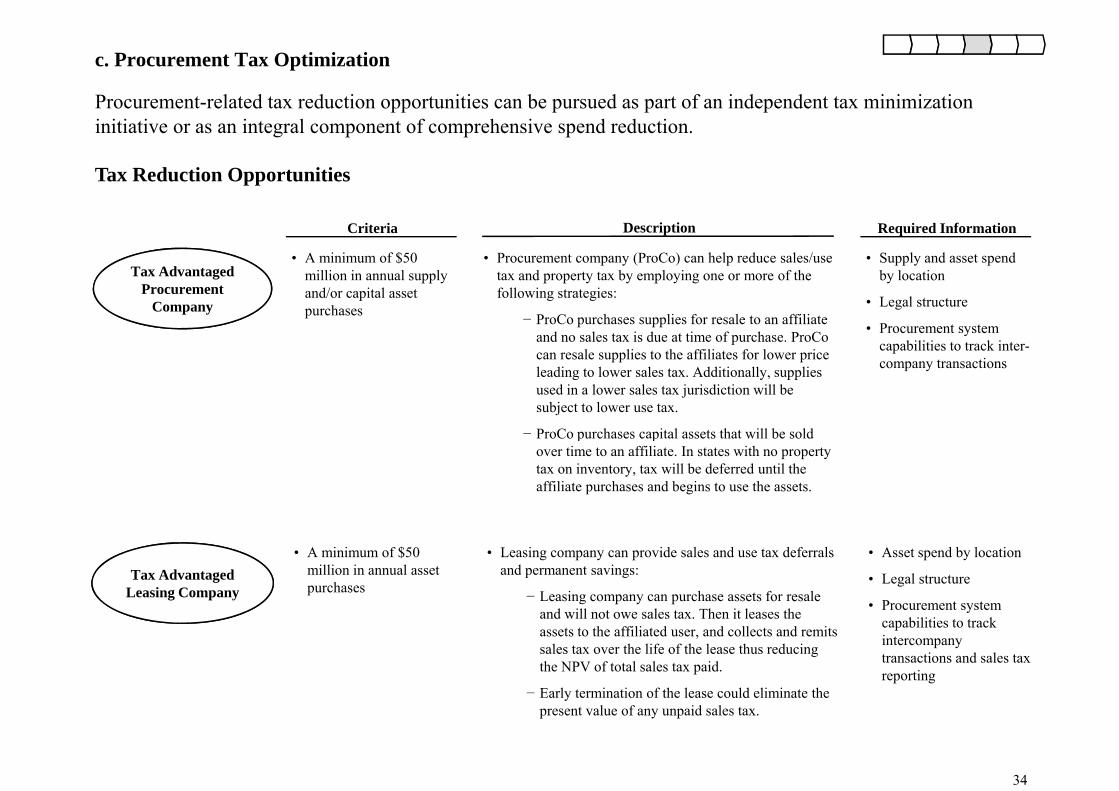

c. Procurement Tax Optimization

Procurement-related tax reduction opportunities can be pursued as part of an independent tax minimization initiative or as an integral component of comprehensive spend reduction.

Tax Reduction Opportunities

Criteria

• A minimum of $50

Description

• Procurement company (ProCo) can help reduce sales/use

Required Information

• Supply and asset spend

Tax Reduction Opportunities

Tax Advantaged Procurement

Company

$million in annual supply and/or capital asset purchases

p y ( ) ptax and property tax by employing one or more of the following strategies:

− ProCo purchases supplies for resale to an affiliate and no sales tax is due at time of purchase. ProCo

l li t th ffili t f l i

pp y pby location

• Legal structure

• Procurement system capabilities to track inter-can resale supplies to the affiliates for lower price

leading to lower sales tax. Additionally, supplies used in a lower sales tax jurisdiction will be subject to lower use tax.

− ProCo purchases capital assets that will be sold

pcompany transactions

p pover time to an affiliate. In states with no property tax on inventory, tax will be deferred until the affiliate purchases and begins to use the assets.

• A minimum of $50 million in annual asset purchases

• Leasing company can provide sales and use tax deferrals and permanent savings:

− Leasing company can purchase assets for resale and will not owe sales tax Then it leases the

• Asset spend by location

• Legal structure

• Procurement system

Tax Advantaged Leasing Company

and will not owe sales tax. Then it leases the assets to the affiliated user, and collects and remits sales tax over the life of the lease thus reducing the NPV of total sales tax paid.

− Early termination of the lease could eliminate the

capabilities to track intercompany transactions and sales tax reporting

34

present value of any unpaid sales tax.

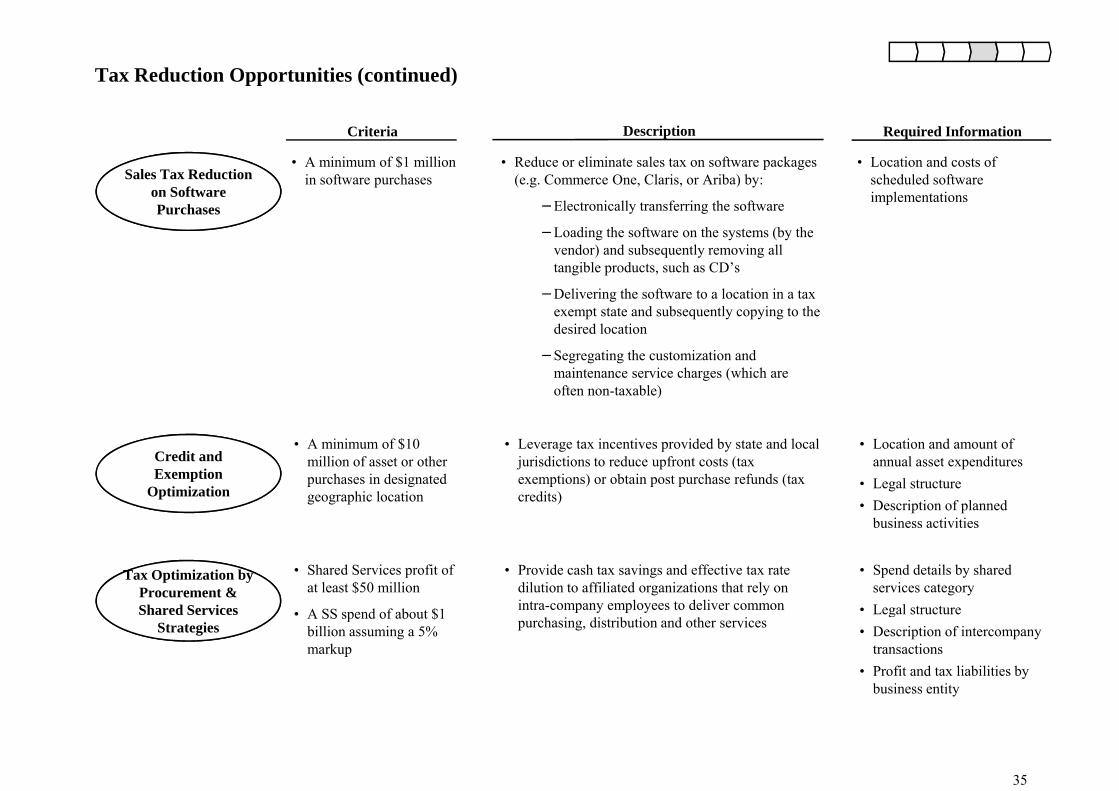

Tax Reduction Opportunities (continued)

Sales Tax Reduction

Criteria

• A minimum of $1 million i ft h

Description

• Reduce or eliminate sales tax on software packages ( C O Cl i A ib ) b

Required Information

• Location and costs of h d l d ftSales Tax Reduction

on Software Purchases

in software purchases (e.g. Commerce One, Claris, or Ariba) by:

−Electronically transferring the software

−Loading the software on the systems (by the vendor) and subsequently removing all t ibl d t h CD’

scheduled software implementations

tangible products, such as CD’s

−Delivering the software to a location in a tax exempt state and subsequently copying to the desired location

S ti th t i ti d

A i i f $10

−Segregating the customization and maintenance service charges (which are often non-taxable)

L i i id d b d l l L i d f• A minimum of $10 million of asset or other purchases in designated geographic location

• Leverage tax incentives provided by state and local jurisdictions to reduce upfront costs (tax exemptions) or obtain post purchase refunds (tax credits)

• Location and amount of annual asset expenditures

• Legal structure• Description of planned

business activities

Credit and Exemption

Optimization

business activities

• Shared Services profit of at least $50 million

• A SS spend of about $1

• Provide cash tax savings and effective tax rate dilution to affiliated organizations that rely on intra-company employees to deliver common

• Spend details by shared services category

• Legal structure

Tax Optimization by Tax Optimization by Procurement & Shared Services • A SS spend of about $1

billion assuming a 5% markup

purchasing, distribution and other servicesg

• Description of intercompany transactions

• Profit and tax liabilities by business entity

S ed Se v cesStrategies

35

5. Recover Spend

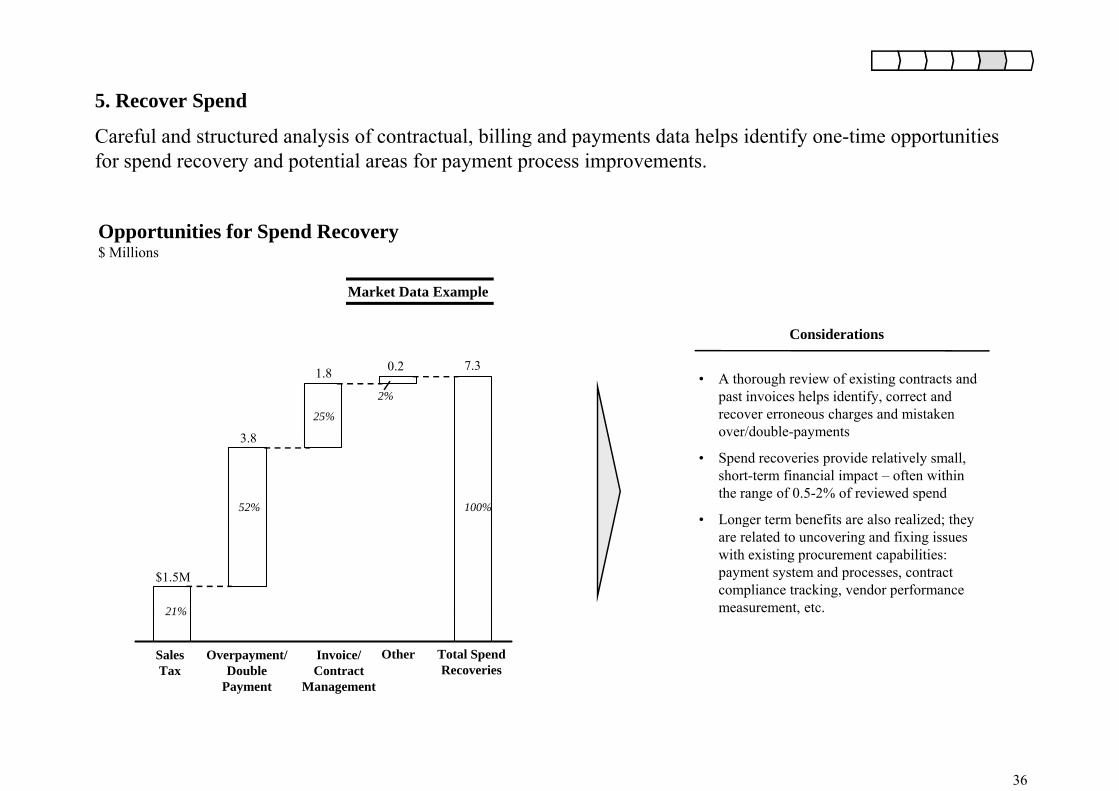

Careful and structured analysis of contractual, billing and payments data helps identify one-time opportunities for spend recovery and potential areas for payment process improvements.

Opportunities for Spend Recovery$ Millions

Considerations

Market Data Example

3 8

1.8 0.2 7.3• A thorough review of existing contracts and

past invoices helps identify, correct and recover erroneous charges and mistaken over/double-payments

25%

2%

3.8 p y

• Spend recoveries provide relatively small, short-term financial impact – often within the range of 0.5-2% of reviewed spend

• Longer term benefits are also realized; they 52% 100%

$1.5M

g yare related to uncovering and fixing issues with existing procurement capabilities: payment system and processes, contract compliance tracking, vendor performance measurement, etc.21%

Sales Tax

Overpayment/Double

Payment

Invoice/ Contract

Management

Other Total Spend Recoveries

21%

36

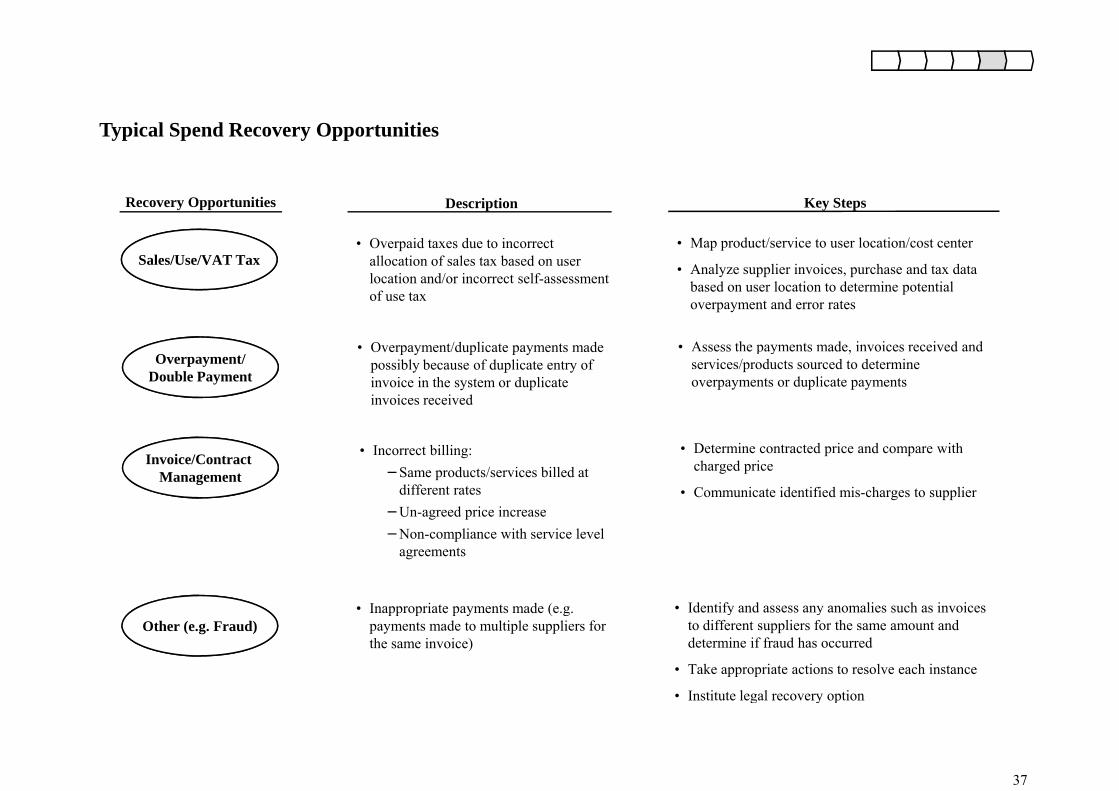

Typical Spend Recovery Opportunities

Recovery Opportunities

Sales/Use/VAT Tax

Description

• Overpaid taxes due to incorrect allocation of sales tax based on user

Key Steps

• Map product/service to user location/cost centerSales/Use/VAT Tax allocation of sales tax based on user

location and/or incorrect self-assessment of use tax

• Overpayment/duplicate payments made

• Analyze supplier invoices, purchase and tax data based on user location to determine potential overpayment and error rates

• Assess the payments made, invoices received and Overpayment/

Double Payment

Overpayment/duplicate payments made possibly because of duplicate entry of invoice in the system or duplicate invoices received

ssess t e pay e ts ade, vo ces ece ved a dservices/products sourced to determine overpayments or duplicate payments

Invoice/Contract Management

• Incorrect billing:−Same products/services billed at

different rates−Un-agreed price increase

• Determine contracted price and compare with charged price

• Communicate identified mis-charges to supplier

−Non-compliance with service level agreements

• Inappropriate payments made (e.g. • Identify and assess any anomalies such as invoices Other (e.g. Fraud)

pp p p y ( gpayments made to multiple suppliers for the same invoice)

y yto different suppliers for the same amount and determine if fraud has occurred

• Take appropriate actions to resolve each instance

• Institute legal recovery option

37

g y p

6. Implement and Capture Savings

Capturing full benefits of identified spend reduction opportunities requires detailed implementation planning, continued organizational commitment, and regular communication and follow-up.p g, g , g p

Implementation/Transition Plan. A fully dedicated implementation team with clear responsibilities and ownership should be selected to execute against a detailed plan outliningresponsibilities and ownership should be selected to execute against a detailed plan outlining (1) the transition from old to new suppliers and (2) the communication of the new sourcing strategy, policies and procedures to all affected people.

Savings Tracking Mechanism As improvements are implemented a tracking mechanismSavings Tracking Mechanism. As improvements are implemented, a tracking mechanism should be established to monitor the actual savings and timeline compared to the original estimates. Implementation progress should be communicated to the organization on a periodic basis.

Supplier Relationship Management. A core team/function with clear responsibilities should be established to manage supplier relationships, monitor performance and drive continuous efficiency improvements.

38

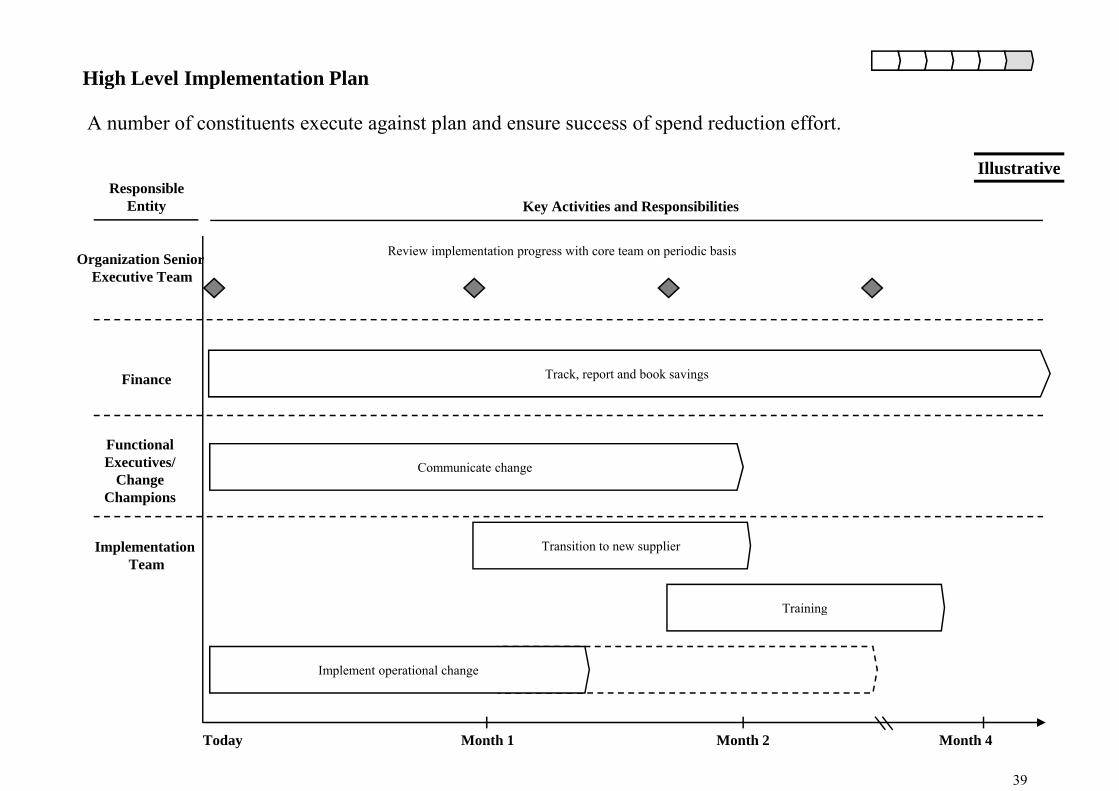

High Level Implementation Plang p

Illustrative

A number of constituents execute against plan and ensure success of spend reduction effort.

Responsible Entity Key Activities and Responsibilities

Organization Senior Review implementation progress with core team on periodic basisOrganization Senior Executive Team

Finance Track, report and book savings

Functional Executives/

Change Champions

Communicate change

Implementation Team

Transition to new supplier

Trainingg

Implement operational change

39

Today Month 1 Month 2 Month 4

Savings Tracking Mechanism

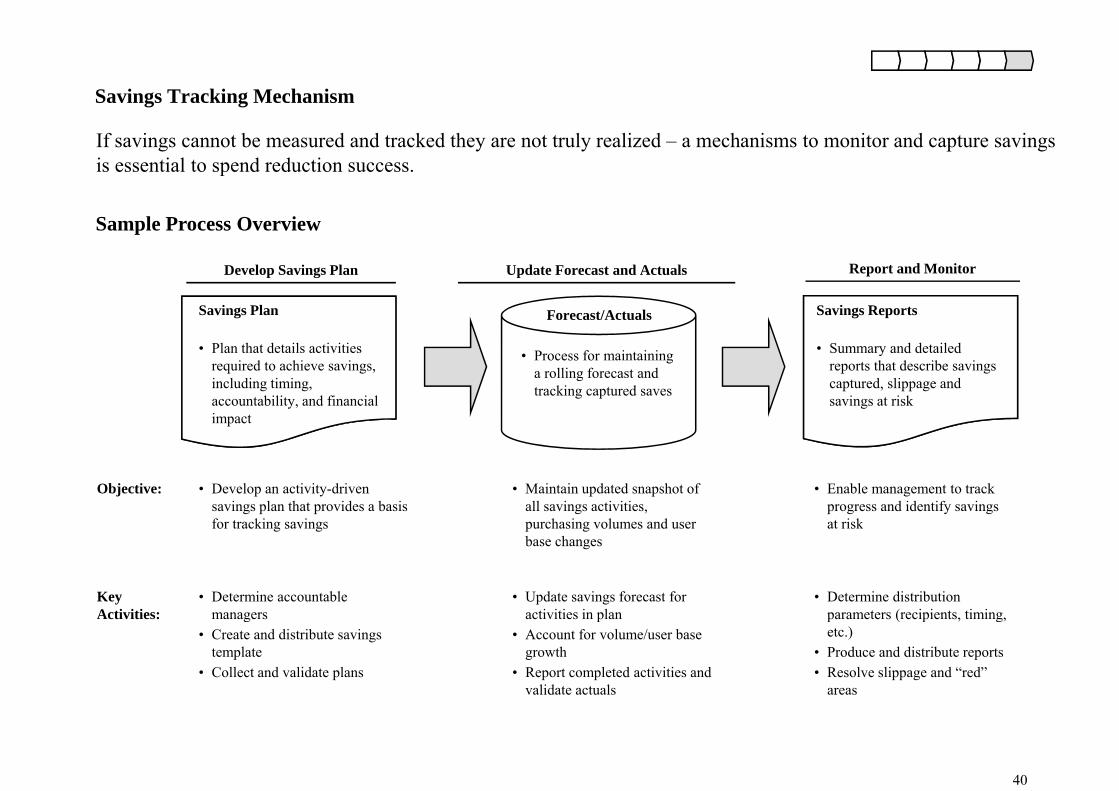

If savings cannot be measured and tracked they are not truly realized – a mechanisms to monitor and capture savings is essential to spend reduction success.

Sample Process Overview

i

p

Develop Savings Plan Update Forecast and Actuals Report and Monitor

Savings Plan

• Plan that details activities

Savings Reports

• Summary and detailed

Forecast/Actuals

P f i i iPlan that details activities required to achieve savings, including timing, accountability, and financial impact

Summary and detailed reports that describe savings captured, slippage and savings at risk

• Process for maintaining a rolling forecast and tracking captured saves

Objective: • Develop an activity-driven savings plan that provides a basis for tracking savings

• Maintain updated snapshot of all savings activities, purchasing volumes and user

• Enable management to track progress and identify savings at risk

KeyActivities:

for tracking savings purchasing volumes and user base changes

at risk

• Determine accountable managers

• Update savings forecast for activities in plan

• Determine distribution parameters (recipients timingActivities: managers

• Create and distribute savings template

• Collect and validate plans

activities in plan• Account for volume/user base

growth • Report completed activities and

validate actuals

parameters (recipients, timing, etc.)

• Produce and distribute reports • Resolve slippage and “red”

areas

40

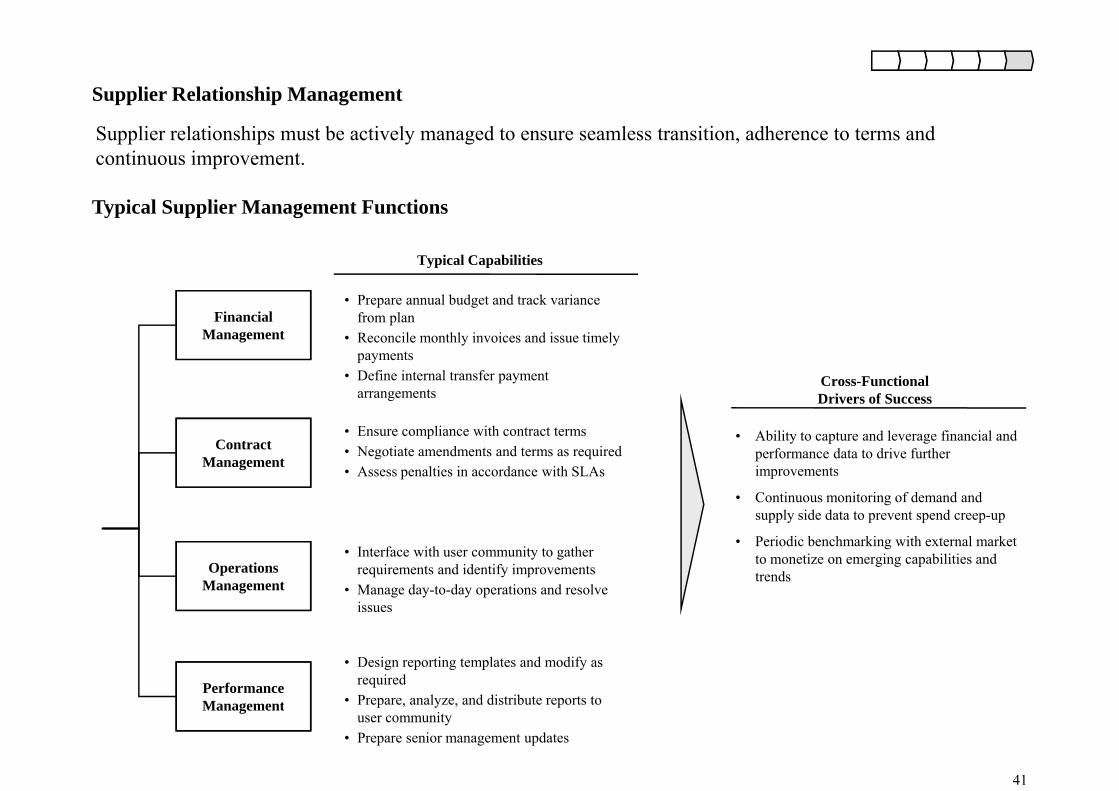

S li R l i hi M

Supplier relationships must be actively managed to ensure seamless transition, adherence to terms and continuous improvement.

Supplier Relationship Management

Typical Capabilities

Typical Supplier Management Functions

• Prepare annual budget and track variance from plan

• Reconcile monthly invoices and issue timely t

Typical Capabilities

Financial Management

payments• Define internal transfer payment

arrangements

• Ensure compliance with contract terms • Ability to capture and leverage financial and

Cross-Functional Drivers of Success

• Negotiate amendments and terms as required• Assess penalties in accordance with SLAs

Contract Management

Ability to capture and leverage financial and performance data to drive further improvements

• Continuous monitoring of demand and supply side data to prevent spend creep-up

• Interface with user community to gather requirements and identify improvements

• Manage day-to-day operations and resolve issues

Operations Management

• Periodic benchmarking with external market to monetize on emerging capabilities and trends

• Design reporting templates and modify as required

• Prepare analyze and distribute reports toPerformance M t

41

Prepare, analyze, and distribute reports to user community

• Prepare senior management updates

Management

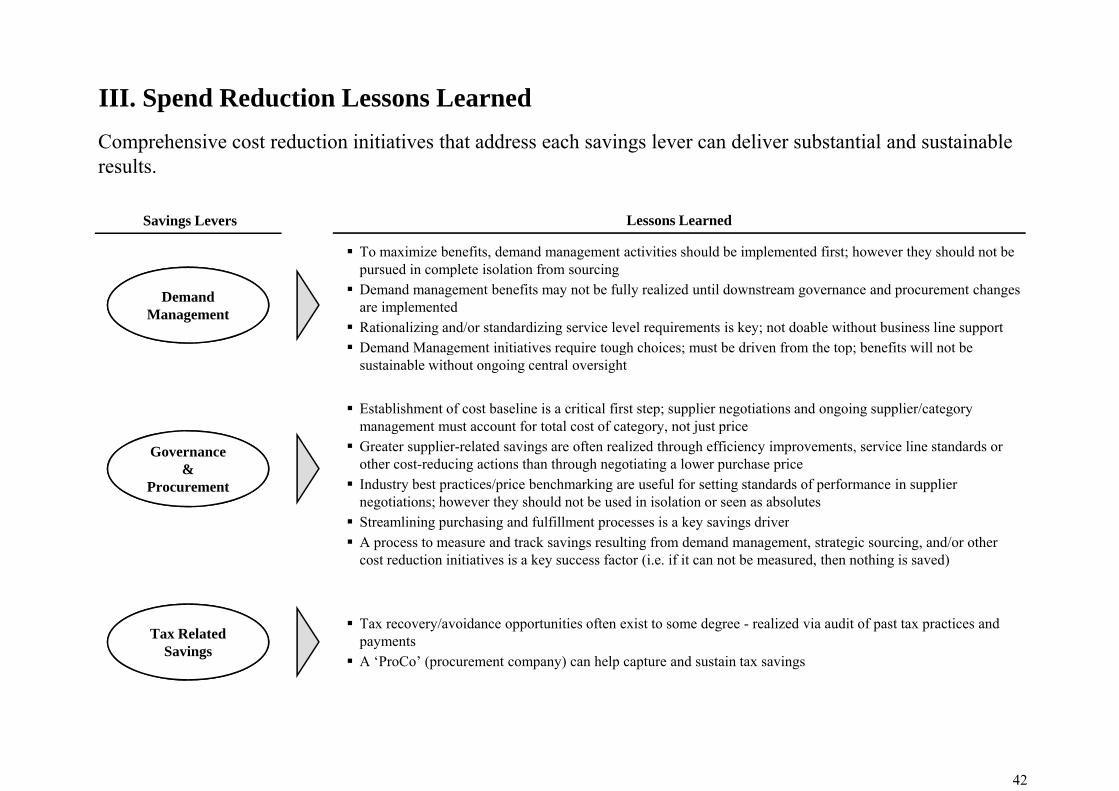

Comprehensive cost reduction initiatives that address each savings lever can deliver substantial and sustainable results.

III. Spend Reduction Lessons Learned

Lessons LearnedSavings Levers

To maximize benefits, demand management activities should be implemented first; however they should not be pursued in complete isolation from sourcingDemand management benefits may not be fully realized until downstream governance and procurement changes are implementedRationalizing and/or standardizing service level requirements is key; not doable without business line supportDemand Management initiatives require tough choices; must be driven from the top; benefits will not be

DemandManagement

Establishment of cost baseline is a critical first step; supplier negotiations and ongoing supplier/category management must account for total cost of category, not just price

Demand Management initiatives require tough choices; must be driven from the top; benefits will not be sustainable without ongoing central oversight

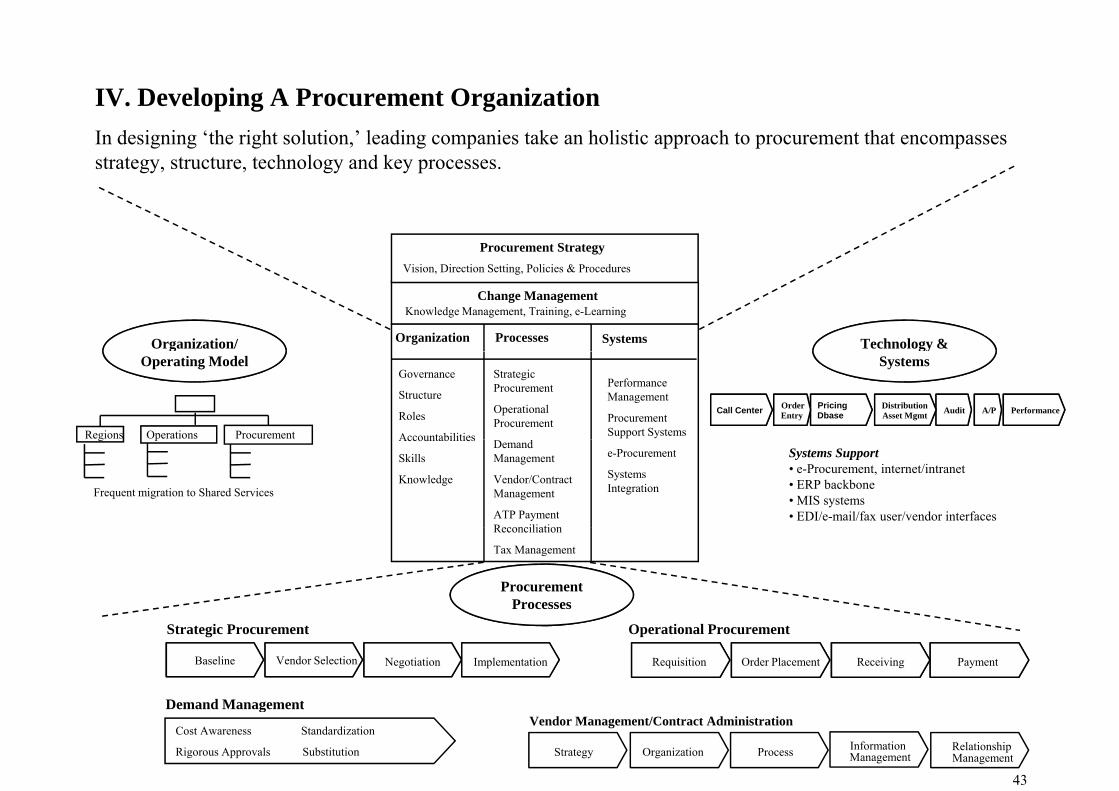

Governance&

Procurement