Embed Size (px)

Citation preview

Introduction To The Global Mining Industry

Rocky Mountain Mineral Law Foundation – Mining Law Short CourseWestminster, Colorado

Joel Schneyer – Managing Director

November 3, 2014

Adrian Kingshott203.489.3682

Ted Kinsman303.572.6013

Len LaPorta203.451.7799

Reed Macy713.876.8030

Jack Maier202.957.5155

Daniel McBroom303.951.7128

Ray McCormick724.933.6600

Gary Moon650.515.8734

Peter Nam949.706.8440

John O’Neill214.870.5040

Tess Oxenstierna203.524.0888

John Patterson908.403.2135

Jeff Ackerman617.275.4401

David Baker312.466.7677

Bob Balaban 303.792.9400

John Batdorf 415.847.8805

David Brinkley917.817.0375

Brendan Burke303.531.4603

Ricardo Campoy646.382.4000

Vince Cannaliato917.533.4152

Tyler Comann415.272.2463

Ian Cookson617.470.9338

Rick deNey203.972.9100

Mike Ewing973.713.1463

National Footprint, Global Reach: Over 25% of Revenue Cross-Border

United States

International 26 countries 50 offices 300 professionals

North America 7 offices 64 professionals

Award winning partners in the UK, France, Germany, Netherlands and India

Long history of success in Spain, Russia, Japan, Brazil, South Africa and Italy

Over 80 languages spoken

2

Horacio Facca617.312.3420

David Francione617.419.2040

Grant Garbers949.706.8444

Gregory Gerard303.572.6016

Darin Good303.549.5674

Bill Harrison917.596.5533

Sam Hill214.457.4832

CJ Hummel303.217.5743

Paul Janson303.572.6012

Rick Jeffrey917.538.2446

Roger Kahn917.597.2245

Samrat Karnik917.733.6022

RussiaDavid Wolfe12.495.721.1370

Mark Bond12.495.721.1370

SpainMaarten De Jongh34.933.426.227

Igor Gorostiaga34.944.352.311

IndiaKaran Gupta230.213.6514

Mahesh Singhi91.22.6634.6666

JapanOwen Hultman81.3.6895.5521

Masahito Tachikawa81.3.6895.5521

MexicoFausto Garcia52.55.5203.4430

Javier Arce Fernandez52.55.5208.4430

PolandMichael Harvey48.22.236.9227

Piotr Olejniczak48.22.236.9227

South AfricaPieter Veldtman27.82.566.6352

Pieter Venter27.82.566.6352

CanadaDon Lioutas416.496.3075

Eric Klein416.496.3742

South AmericaLeonardo Antunes55.21.3873.8000

Felipe Monaco55.11.4114.2047

United KingdomMark Humphries44.20.7881.2990

Mark Wilson 44.121.654.5000

Benelux Jan Willem Jonkman 31.73.623.8774

Ron Belt31.73.623.8774

France Michel Degryck33.148.246.300

Jean-Pierre Brice33.148.246.300

GermanyMichael Fabich49.611.205.4825

Ervin Schellenberg49.611.205.48.10

ItalyNuccia Cavalieri39.02.92.88.04.00

Stefano Pastore39.02.92.88.04.00

ThailandChayot Vitayanonektavee66.2664.9100

Jim Vorapon Ponvanit66.2664.9100

TurkeyOmer Unsal0212.215.52.40

Brian Pietravalle202.595.4739

Rod Rivera917.969.4270

Carlos Rodriguez858.752.4350

Joel Schneyer303.619.4211

Brad Schreiber949.706.8440

Phil Seefried303.572.6004

Kevin Slocum203.331.5955

Jerry Sturgill208.287.8903

Mike Swartz303.531.5009

Doug Usifer908.432.7792

Bill Young203.622.1044

Sun Jen Yung917.297.8716

1) Prices - Cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

3

1) Prices - Cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

4

0.000

0.500

1.000

1.500

2.000

2.500

3.000

3.500

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Al,

Cu

& N

i P

rice (

US

$/l

b)

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Ni

Pri

ce (

US

$/l

b)

copper aluminum nickel

- 4 - 6- 4 - 7+ 3

+

2

+ 5

+

2

Average Up Cycle is 3 Years – Average Down Cycle is 5 Years

5

Source: Headwaters Research

Copper Stocks and Copper Prices – Inverse Relationship

Source: International Copper Study Group – 2013 Factbook

6

Cumulative Production0% 40% 60%20% 100%80%

Supply

demand

d1

d2

d3

lower taxesmore gov’t spendinglower interest ratesloose money supply

higher taxesless gov’t spendinghigher interest ratestight money supplysubstitution

Macroeconomics – Supply & Demand

7

Source: Headwaters Research

World Copper Use Per Capita

Source: International Copper Study Group – 2013 Factbook

8

Intensity Of Use For Copper – 7 Largest Economies In 2012

Source: ICSG and IMF estimates

9

1) Prices - cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

10

Population in Millions

2014 Population Estimate = 7.2 Billion People

Source: Internet World Stats – Miniwatts Marketing Group – estimated world population 7.18 billion

11

Time to Successive Billions in World Population 1800 -2050

Source: US Census Bureau

12

Population in Millions

2050 Population Forecast = 9.1 Billion People

Source: Internet World Stats – Miniwatts Marketing Group – US Census Bureau

BRIC Countries of Brazil, Russia, India, China = 38%

13

GDP % Annual Growth Rates

Source: The World Bank

14

China Crude Steel Apparent Consumption

Source: The Globe and Mail, Mysteel

15

German Exports

Source: The Globe and Mail, Bloomberg

16

1) Prices - cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

17

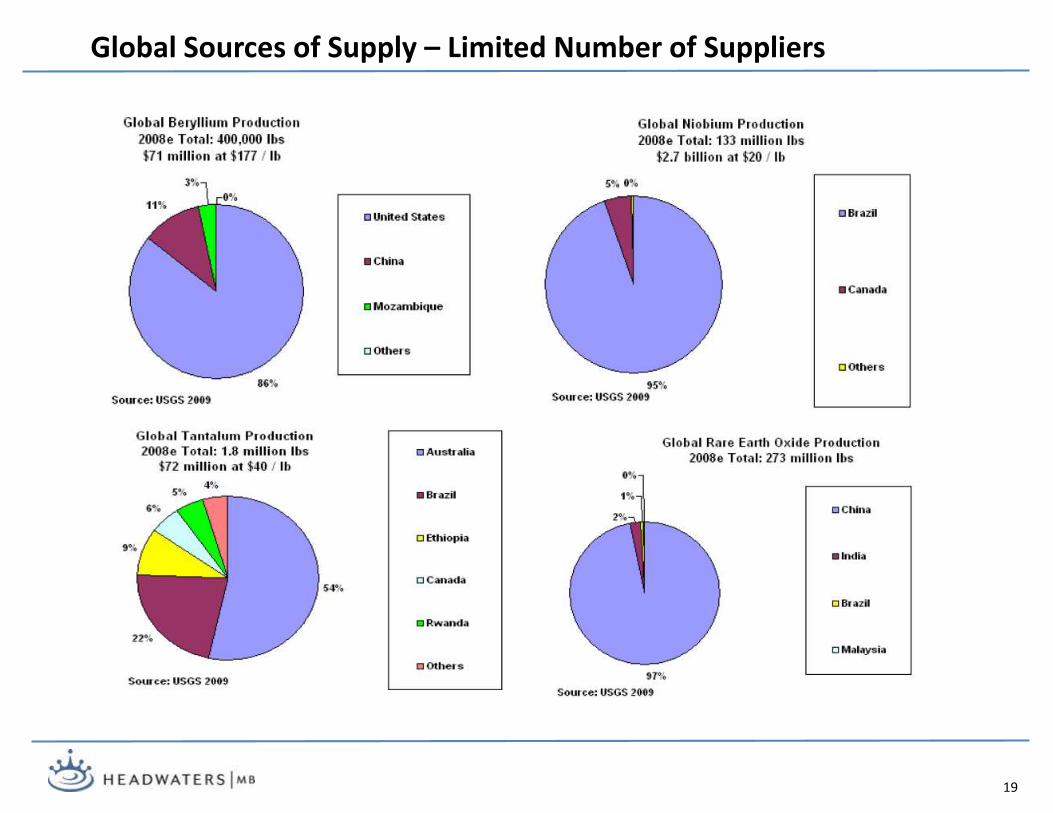

Global Sources Supply – Number of Suppliers

18

Global Sources of Supply – Limited Number of Suppliers

19

Global Sources of Chromite – Potential Supply Issues

Global Reserve Base is sufficient to meet conceivable demand for centuries

No substitute for chromium in stainless steel production

South Africa mining industry not meeting its risk adjusted returns on capital

Kazakhstan unreliable supplier

20

1) Prices - cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

21

Difficult Investment Landscape for Miners

Source: Novagold - Presentation San Francisco Gold Conference November 2013

Mexico: New 8% tax on gold profits

South America1. Peru: Construction halted at largest mine due to

gov’t review and social unrest.2. Ecuador: Political obstacles and windfall tax

discourage foreign investment in mining.3. Venezuela: Five mining companies seeking

compensation through World Bank’s arbitration court following nationalizations.

4. Bolivia: Nationalization of various natural resources assets.

5. Argentina: Miners required to repatriate revenues from foreign sales, limitations imposed on foreign exchange. Controls on imports of equipment/supplies have also been tightened

Africa6. Ghana: Increase in tariffs on mines and introduced

a windfall tax, halting project expansions.7. Guinea: New law gives government a 35% stake;

threat of nationalization.8. Mali: Recent military coup creating political

uncertainty9. Kenya: Rising mineral royalties and drilling fees for

mining.10. Congo: Plans to revise mining code, raise taxes and

increase stake in mining projects11. Zimbabwe: Gov’t plans to seize control of foreign-

owned mines.12. South Africa: Ongoing dialogue to nationalize

mining industry.

Russia, Asia & Australia13.Indonesia: Newly proposed legislation limits foreign ownership of mines to 49%.14.Philippines: New royalties and taxes being imposed on mining companies.15.Mongolia: Drafting investment law to restrict foreign ownership.16.Kyrgyzstan: Parliamentary motion calling for increased government stake in one of its largest mines

Heightened Geopolitical/Permitting Risk in North America

22

BC: Mt Polly tailings dam spill

Alaska: EPA’s “stoppage” of PebbleMine under sec 404C of clean water act

Quebec: AmendmentsTo Mining Act

BC: Canada Supreme CourtTsilhqot’in First Nation Ruling

Providing valuable information to the mining industry and policy makers since 1997 on political risk by examining 13 policy areas such as taxation, regulation, land claims, etc.

Sent to 4,100 executives at exploration, development, and mining consulting companies. Asked to respond only for jurisdictions which they know

Responses from 690 executives, representing $3.4 billion in exploration spending in 2013

A composite index of the policy areas

0 is worst policy; 100 is best

www.fraserinstitute.org

Fraser Institute 2013 Mining Survey

23

1) UNCERTAINTY REGARDING THE ADMINISTRATION, INTERPRETATION, OR ENFORCEMENT OF EXISTING REGULATIONS

2) UNCERTAINTY CONCERNING ENVIRONMENTAL REGULATIONS

3) REGULATORY DUPLICATION AND INCONSISTENCIES (includes federal/provincial, federal/state, inter-departmental overlap, etc.)

4) TAXATION REGIME (includes personal, corporate, payroll, capital, and other taxes, and complexity of tax compliance)

5) UNCERTAINTY CONCERNING NATIVE / ABORIGINAL LAND CLAIMS

6) UNCERTAINTY CONCERNING WHAT AREAS WILL BE PROTECTED AS WILDERNESS OR PARKS

7) INFRASTRUCTURE (includes access to roads, power availability, etc.)

8) SOCIOECONOMIC AGREEMENTS / COMMUNITY DEVELOPMENT CONDITIONS (includes local purchasing, processing requirements or supplying social infrastructure such as schools or hospitals, etc.)

9) POLITICAL STABILITY

10) LABOUR REGULATIONS / EMPLOYMENT AGREEMENTS

11) QUALITY OF THE GEOLOGICAL DATABASE (includes quality and scale of maps, ease of access to information, etc.)

12) SECURITY (includes physical security due to the threat of attack by terrorists, criminals, guerrilla groups, etc.)

13) AVAILABILITY OF LABOUR / SKILLS

The Fraser Institute – Policy Survey

24

Source: Fraser Institute – 2013 Mining Survey

2013 Fraser Results - Policy Perception Index

Top 10Sweden (best)FinlandAlbertaIrelandWyomingWestern AustraliaNew BrunswickNevadaNewfoundland/LabradorNorway

Bottom 10MadagascarIndonesiaIvory CoastZimbabweArgentina – MendozaAngolaArgentina – La RiojaPhilippinesVenezuelaKyrgyzstan (worst)

25

E&Y Top Business Risks in Mining Sector

26

Source: E & Y, Business Risks Facing Mining & Metals 2014 - 2015

1) Metal Prices - cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

27

2013 Mining Markets At A Glance

Source:

28

Diversity in the Issuer Base – Geographic Focus

Source:

29

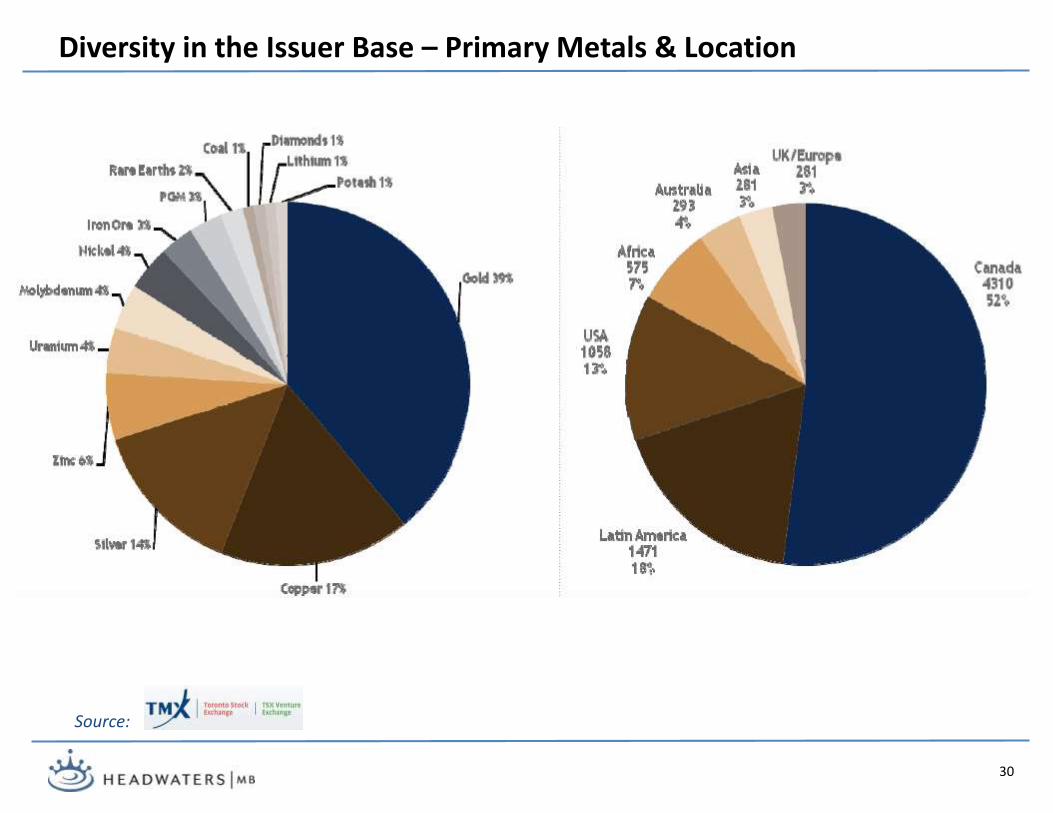

Diversity in the Issuer Base – Primary Metals & Location

Source:

30

TSX & TSXV – 3673 Issuers – 44% Mining

Source:

31

Access To Capital

Source:

32

Number of Mining Companies by the Stage of Project Development

Source:

33

Disconnect Between Gold Miner Indexes and Broader Market

34

Source: Headwaters Research

1) Metal Prices - cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

35

Source: MinEx Consulting, Mining Journal Gold Supplement, August 2014

Gold Discovery Cost

36

0

200

400

600

800

1,000

1,200

2010 2011 2012 2013

Total Cash Total Production All-In Sustaining

$739$713$624

Source: Metals Focus

$548

$1,066 $1,045

$/o

zMining Cost Inflation

37

Source: Metals Focus

$/o

z

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

0 25 50 75 100

Cumulative Gold Production (%)

Total Cash Cost H1 14 Av. H1 14 Gold Price

Total Cash Cost H1 13 Av. H1 13 Gold Price

Industry Cash Cost Curve H1 2014

38

Source: Metals Focus

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

0 25 50 75 100

Cumulative Gold Production (%)

All-In Sustaining Cost H1 14 Av. H1 14 Gold Price

All-In Sustaining Cost H1 13 Av. H1 13 Gold Price

Industry All-In Sustainable Cost H1 14

39

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14

Total Cash Cost All-In Sustaining Cost Gold Price

$301/oz

$292/oz$312/oz $338/oz $321/oz

Source: Metals Focus

$/o

z

$535/oz

Margins Under Pressure

40

SNL Pipeline Activity Index

Source: SNL Metals & Mining 2014

41

SNL Significant Gold Drill Results Announced

Source: SNL Metals & Mining 2014

42

43

The Institutional Money has lost confidence …

˗ that costs can be controlled

˗ that capital discipline will occur

˗ that restructurings can deliver on promises

˗ that returns on capital employed will improve

˗ that the industry won’t pile back into too many new projects or expensive deals when

prices rebound

˗ that resource nationalism will not overwhelm the industry

˗ that commodity prices will not collapse

˗ that “stuckholders” have an exit

… and the markets reflect this loss of confidence

Institutional Money Is Not Buying Gold Exploration Lottery Tickets

Why Buy An Illiquid Share When You Can Buy An ETF?

44

Source: Yahoo Finance

No control – generally passive

Upfront payment for metal –generally passive, much more important financing source today

Rise of PE as active investors and generally absolute control

May have board representation, early toehold in projects

The rise of state backed investments (e.g. China and Korea)

45

Company

Project

Retail

Sovereign Wealth

Inst

itu

tio

nal

Mo

ney

Private Equity

Streaming & Royalty

Strategics

Merchant Traders

Mutual Funds

Major Shift In How Institutional Money Invests In Sector

46

Development Stage Gold Companies trade at an Enterprise Value of $16 per ounce of M, I, & I (NI 43-101) with average estimated project development costs of $91 per ounce

*EV = (share price x # shares) – current assets + total liabilities**9/29/2014 share prices at close Au=$1219.50/oz, Ag=$17.58/oz

However The Development Stage Business Model Looks To Be Unsustainable

47

Once the Project enters the Development Investment Analysis Phase (PEA – Prefeasibility – Feasibility), companies see a long period of share price erosion as studies, permitting and de-risking drag on.

Life Cycle of a Gold Mining Share – Dec 2013 119th Annual Meeting

De-risking&

48

Once the Project enters the Development Investment Analysis Phase (PEA – Prefeasibility – Feasibility), companies see a long period of share price erosion as studies, permitting and de-risking drag on.

Life Cycle of a Gold Mining Share – Dec 2014 120th Annual Meeting

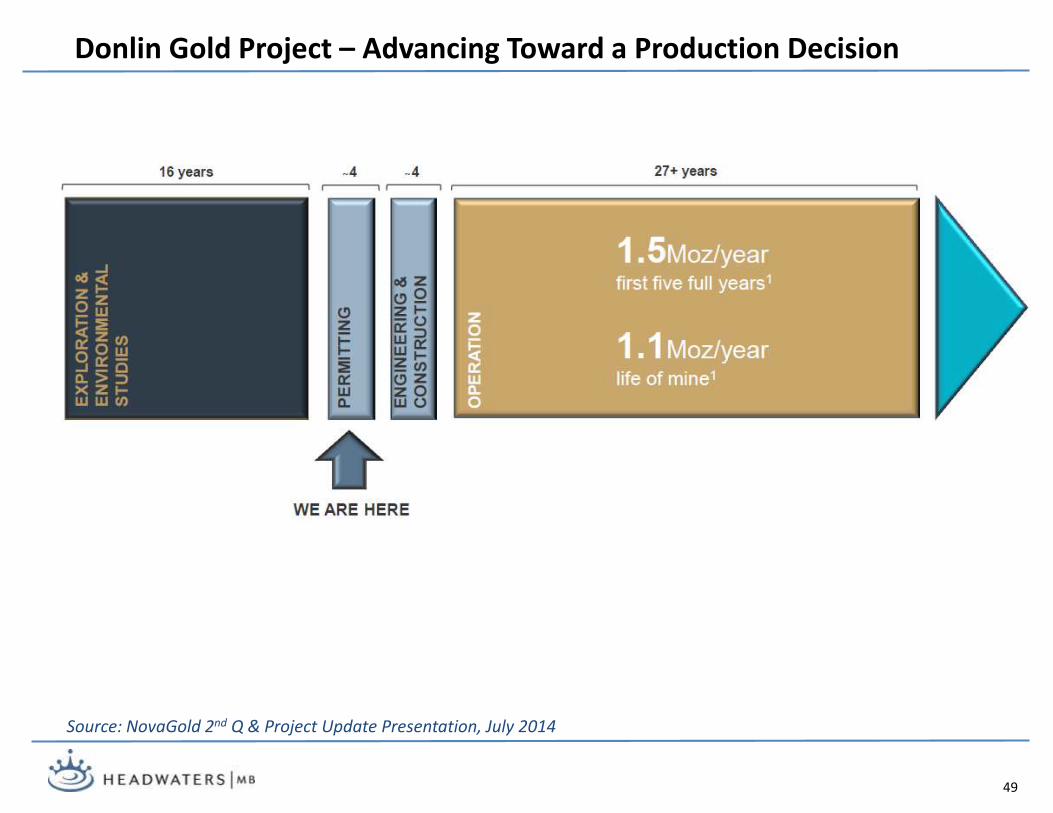

Donlin Gold Project – Advancing Toward a Production Decision

Source: NovaGold 2nd Q & Project Update Presentation, July 2014

49

50

Development Stage Gold Companies Trade on Average at $16/oz Resource

Costs to Complete Drilling, Feasibility & Permitting ~$10/oz Resource

Capital Development Costs $91/oz Resource

Owners Costs Not in Feasibility (25%) $23/oz Resource

Total $140/oz Resource

Actual Trading Market Multiples

• Small Gold Producers $71/oz Resource

• Intermediate Gold Producers $70/oz Resource

• Large Gold Producers $129/oz Resource

• Silver Producers $128/oz Resource

So What Is the Problem?

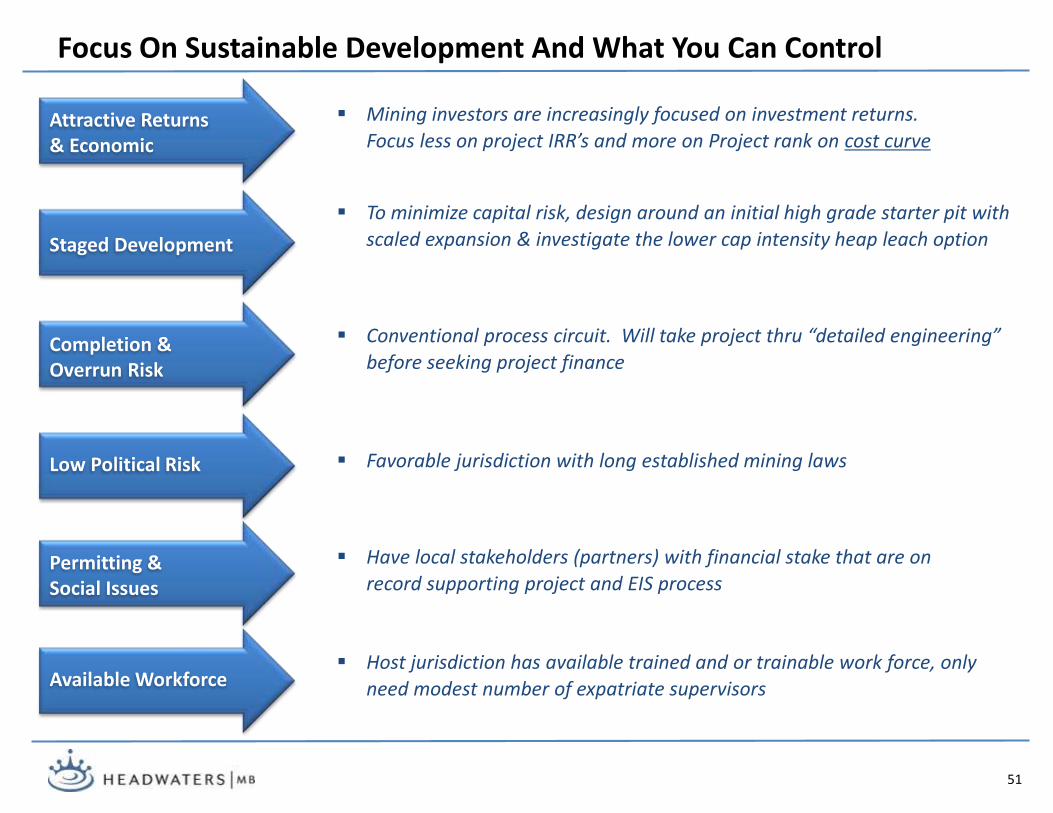

Focus On Sustainable Development And What You Can Control

Mining investors are increasingly focused on investment returns.

Focus less on project IRR’s and more on Project rank on cost curveAttractive Returns & Economic

51

Staged Development

Low Political Risk

Available Workforce

To minimize capital risk, design around an initial high grade starter pit with

scaled expansion & investigate the lower cap intensity heap leach option

Conventional process circuit. Will take project thru “detailed engineering”

before seeking project finance

Favorable jurisdiction with long established mining laws

Host jurisdiction has available trained and or trainable work force, only

need modest number of expatriate supervisors

Permitting & Social Issues

Have local stakeholders (partners) with financial stake that are on

record supporting project and EIS process

Completion & Overrun Risk

1) Metal Prices - cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

52

Industry Observations – The Unconventional Shale Plays

53

Industry Observations – Sand Market Overview

54

Major Dynamics

Demand

Supply

Competition

Pricing

Demand is increasing faster than supply Logistics capabilities are no longer a competitive advantage but still a

necessity

There is rapidly growing need for high quality frac sand - more wells per section, more stages per well, more sand per stage

Exponential decline of unconventional shale plays requires continued drilling to keep production levels up

Permitting is becoming harder (NIMBY) Economic and mineable deposits of Northern White sand hard to find

Not much of an issue in an “expanding” market The consolidation in the industry is just beginning

Long-term contract pricing of $50 to 65 per ton (20/70) FOB Mine Prices for 100 mesh have found strength

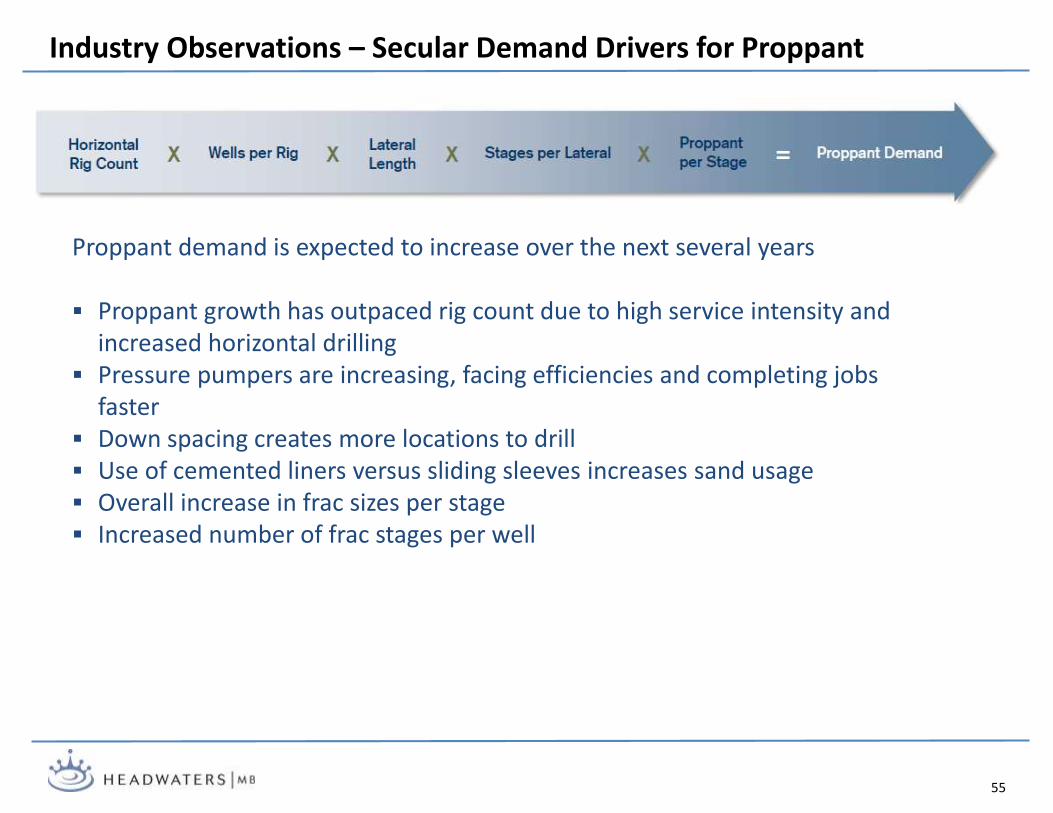

Industry Observations – Secular Demand Drivers for Proppant

55

Proppant demand is expected to increase over the next several years

Proppant growth has outpaced rig count due to high service intensity and increased horizontal drilling

Pressure pumpers are increasing, facing efficiencies and completing jobs faster

Down spacing creates more locations to drill Use of cemented liners versus sliding sleeves increases sand usage Overall increase in frac sizes per stage Increased number of frac stages per well

Proppant Market Differentiation

56

Source: Emerge Energy Services, Investor Presentation, April 2014

The quality of proppants produced from St Peter Sandstone often is a function of the process flowsheet utilized and careful attention to cleaning, not differences in the raw sand quality

Economics of the Unconventional Plays

57

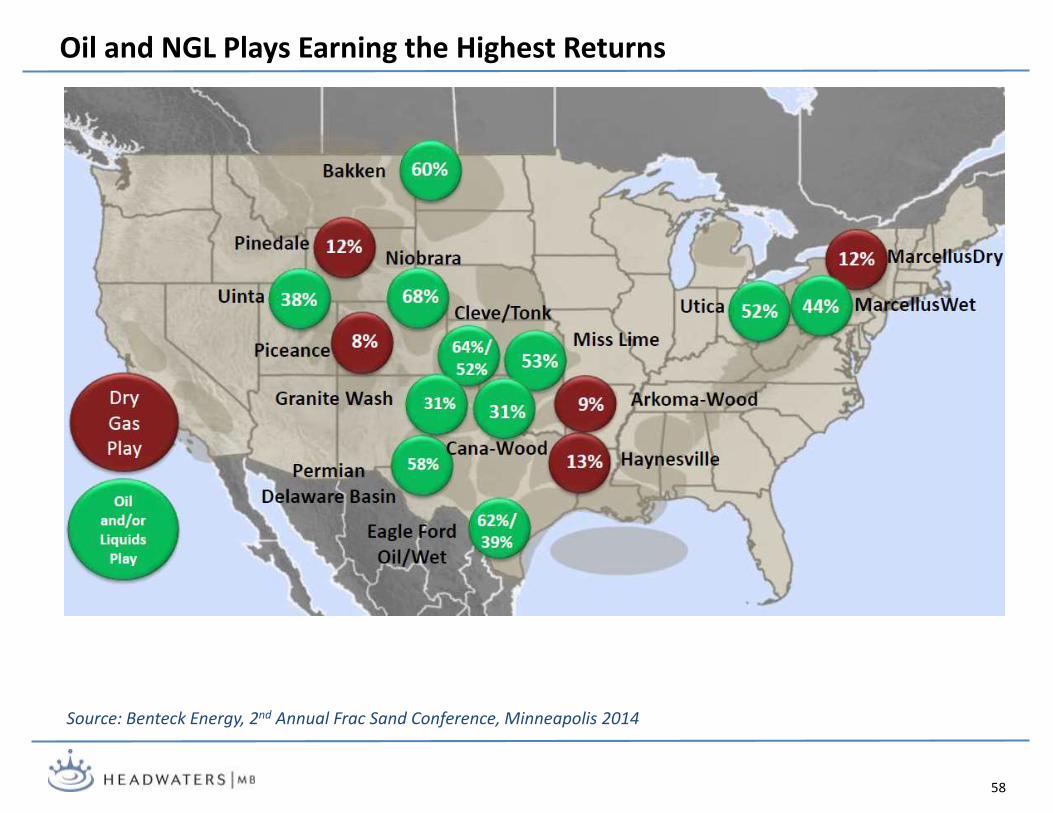

Source: Benteck Energy, 2nd Annual Frac Sand Conference, Minneapolis 2014

Oil and NGL Plays Earning the Highest Returns

58

Source: Benteck Energy, 2nd Annual Frac Sand Conference, Minneapolis 2014

Frac Sand Demand – Regional Sand Consumption (billion lbs)

59

Source: PacWest Consulting, Frac Sand Logistics Conference – San Antonio, August 2014

Industry Observations – Proppant Demand Expected to Remain Strong

60

1.8

7.0

29.6

51.2

78.5

$40

$48

$58

$68

$80

$25

$35

$45

$55

$65

$75

$85

0

20

40

60

80

100

2002 2007 2012 2017 2022

Raw Frac Sand Resin-Coated Sand, Ceramics, Other Raw Frac Sand Price (S/ton)

(Millions of Tons)

(S/Ton)Historical and Projected Industry Proppant Demand

Source: Hi-Crush Partners Company Presentation, Freedonia Group

Frac Sand Shipping Flows

61

Source: PLG Consulting, 2nd Annual Frac Sand Conference, Minneapolis 2014

Regulatory Authority and Control Nonmetallic Mining in Wisconsin

62

Source: GZA Environmental, 2nd Annual Frac Sand Conference, Minneapolis 2014

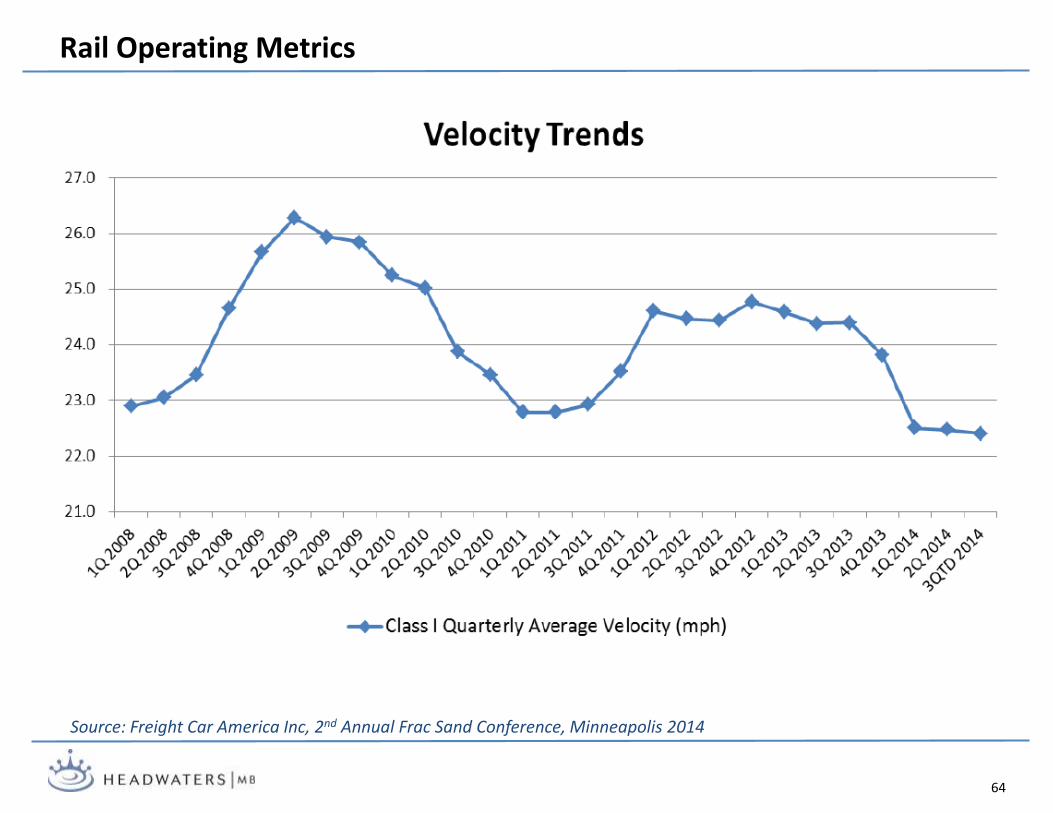

Frac Sand Handled By Railroads

63

Source: PLG Consulting, 2nd Annual Frac Sand Conference, Minneapolis 2014

Rail Operating Metrics

64

Source: Freight Car America Inc, 2nd Annual Frac Sand Conference, Minneapolis 2014

Frac Sand Delivered Cost to Wellsite

65

Source: Raymond James, Global Research Report, August 2014

The Miner = $60/t Revenue - $35/t OC = $25/t EBITDA

- Operates 15 locations across the USA, owns 297 tons of sand reserves including 138 million tons which can processed to produce API spec frac sand. In 2013, sold 8.16 million tons of sand at average price of $66.90/ton. Portfolio company of Golden Gate Capital, IPO in 2012; Golden Gate sold out its position in 2013.

- Was formed by private equity firm Insight Equity in 2012. In May 2013, Emerge Energy Services was combined with Superior Silica Sands (“SSS”), Allied Energy Company (“AEC”), and Direct Fuels (“DF”) in a series of transactions that culminated with the initial public offering of Emerge as LP. In 2013, sold 2.65 million tons of sand at average price of $63.28/ton. Still controlled by Insight Equity.

- Was formed by private equity firm Avista Capital Partners in 2010. In August 2012, initial public offering of Hi-Crush as LP. In 2013, sold 1.85 million tons of sand at average price of $82.74/ton. Still controlled by Avista Capital Partners.

Competitive Landscape

66

- Employs over 1,000 people, sold more than 6.0 million tons of sand and value-added sand products in 2011. Portfolio company of American Securities CapitalPartners. There are rumors that an IPO is forthcoming.

- One of the leading providers of high-quality proppant and related logisticsservices to the oil and gas industry in North America. All of Smart Sand’sfacilities are located near major rail transport lines, ensuring reliable, cost-effective delivery to major shale plays in the U.S. and Canada. Portfoliocompany of Clearlake Capital.

- Headquartered in Houston Texas, Cadre Services is a major supplier of API/ISO-quality Premium Hickory® Sand, with principal operations located in Voca,Texas. Portfolio company of Denham Capital Management. July 16, 2014announcement that U.S. Silica Holdings, Inc. to purchase Cadre Services Inc. for$98 million. Adjusted LTM EBITDA of $11.1 million represents purchase price of7.6x EBITDA.

- Strategically located in New Auburn, WI and Garland City, AR to meet thedemands of all major shale plays. Wisconsin plant originates on the UnionPacific railway and has access to Canadian National (CN) and BurlingtonNorthern Santa Fe (BNSF) railways. Portfolio company of Energy CapitalPartners.

Competitive Landscape

67

Median EBITDA Multiple for Trading Comps:

6.0x (Energy) – 6.8x (Materials) – 7.6x (Cadre)

Conclusion

68

July 16, 2014 announcement that U.S. Silica Holdings, Inc. to purchase Cadre Services Inc. for $98 million. Adjusted LTM EBITDA of $11.1 million represents purchase price of 7.6x EBITDA

Median Enterprise Value / EBITDA

Target's Sector

Less Than

$500M

Greater

Than $500M

Less Than

$500M

Greater

Than $500M

Less Than

$500M

Greater

Than $500M

Less Than

$500M

Greater

Than $500M

Less Than

$500M

Greater

Than $500M

Consumer Discretionary 11.3x 10.5x 12.7x 8.5x 10.8x 8.5x 9.5x 9.1x 12.8x 9.7x

Consumer Staples 12.7x 9.7x 7.2x 8.2x 9.5x 8.7x 8.7x 12.7x 9.8x 9.7x

Energy 8.4x 9.9x 10.5x 14.9x 7.2x 9.2x 5.4x 13.1x 6.0x 5.5x

Financials 12.7x 10.9x 12.7x 14.4x 11.0x 17.6x 10.3x 15.3x 12.2x 19.4x

Healthcare 10.8x 10.1x 11.9x 12.7x 12.2x 12.1x 10.2x 11.3x 8.1x 14.8x

Industrials 5.7x 9.3x 7.0x 8.8x 8.3x 11.2x 7.2x 9.7x 8.7x 10.3x

Information Technology 8.1x 13.7x 12.6x 14.9x 9.5x 15.7x 12.0x 11.2x 12.6x 18.5x

Materials 9.3x 11.9x 7.2x 10.9x 9.8x 9.7x 7.8x 8.2x 6.8x 11.4x

Telecommunication Services 5.8x 7.3x 5.9x 7.4x 11.5x 8.7x 7.6x 8.4x 11.3x 11.2x

Utilities 9.5x 11.0x 10.3x 11.3x 9.8x 10.7x 14.0x 8.7x 14.0x 9.9x

2010 2011 2012 2013 2014

Last Twelve Months Ending June 30th of:

Recent Transactions

Public Company – Frac Sand Trading Comparables

69

Source: Headwaters Research

1) Metal Prices - cyclical

2) Demand – BRIC countries are the drivers

3) Raw Material Supply

4) Political Risk in the Mining Sector – Fraser Institute

5) Raising Capital – TSX and TSXV

6) Development Stage Gold Companies Value Proposition Timeline

7) Frac Sand Industry Overview

8) Closing Thoughts

Presentation Outline

70

Exploration is extremely risky with success rates akin to Pharma R&D developing a drug that can proceeds thru medical trials, expect a large percentage of exploration companies to be forced out of business

Recognition that the replacement cost of “risked reserves” are often lower than current market capitalizations, there will be continued consolidation in the resource sector especially as a way to “bank” value

Burgeoning debt of OECD countries (and US municipalities) causes new wave of “resource taxes”

Without social license to operate, a positive permitting outcome is problematic

Any carbon capture initiatives will have a “taxing” effect on the global economy, reduce demand and GDP

Observations

71

Global Warming – Anthropogenic Carbon Production

Source: Dr. Timothy Gutowski, Department of Engineering at M.I.T., Keynote Address 40th CIRP International Manufacturing Systems Seminar at Liverpool University, 30 May to June 1 2007

These four components respectively are: 1) population, 2) affluence 3) energy intensity 4) carbon intensity

“Results in reducing emissions to slow global warming reveal that while we are improving in both of the technology terms (energy intensity & carbon intensity), these are offset by the growth terms i.e. population and affluence”

72

OECD economies will continue to grow at slow rates, drag of carbon capture initiatives, debt load, aging populations and higher taxes

BRIC countries will extend infrastructure into hinterlands to boost domestic economies, reduce dependency on exports, and reduce tension between the coastal haves and the inland have nots

China will continue to convert US paper assets into ownership of “hard assets” around the world, to have title to the means of production and security of supply with regard to raw materials inputs

For the “mining developers”, Private Equity and its “managed money approach” has replaced the public stock markets as the go to source of capital in the mining sector

The Unconventional Shale Revolution has had (and will have) an enormous global impact and is driving the US economic growth engine

Predictions

73

Real Estate Asset Bubble Collapse

US Housing Starts & Cement Consumption “Turned” 2 Years Before Dow

74

SEDAR – official site that provides access to most public securities documents and information filed by public companies and investment funds with the Canadian Securities Administrators (CSA) in the SEDAR filing system. www.sedar.com

Kitco – latest metal news, commentaries, latest company news releases, technical and fundamental analysis, top performing equities, exchange rates, metal prices and charts. www.kitco.com

The Northern Miner – global mining newspaper published out of Toronto, print and web editions, subscription service. www.northernminer.com

The Fraser Institute – registered non-profit with offices in Canada and the United States with active research ties with similar independent organizations in more than 70 countries around the world. Measures and studies the impacts of markets and government interventions on the welfare of individuals. Produces annual mining policy survey. www.fraserinstitute.org

USGS Mineral Information – mineral summaries by commodity, country, and state. Excellent source of long term data series on production, consumption, and pricing.http://minerals.usgs.gov/minerals/index.html

Institute of Corporate Directors – pre-eminent organization for directors and recognized as the leading authority of standards of good governance. Supports director education though ICD education programs. www.icd.ca

Resources

75

The Headwaters Difference

DEAL OF THE YEAR - TMT

INVESTMENT BANK OF THE YEAR

INTERNATIONAL DEAL OF THE YEAR PROFESSIONAL (B2B) SERVICES

INTERNATIONAL DEAL OF THE YEAR CONSUMER SERVICES

INTERNATIONAL INVESTMENT BANK OF THE YEAR

76

Advocacy – unapologetic and conflict free

Award-winning client advice

Deep pool of transaction experience (over $265 billion)

National footprint (7 offices)

Global reach (25 countries, 50 offices)

Focused industry coverage (specialists, not generalists)

Full product/service offering

#1 investment bank for private wealth in the US

Proprietary capital: we can invest; unique access to family office capital

Long history of success

Teamwork unrivalled in the industry

Capabilities • Culture • Results