Embed Size (px)

Citation preview

U.S. employment situation: September 2013Release date: October 22, 2013

May job growth paused: was it temporary or are we at an inflection point?U.S. employment situation: May 2016 June 3, 2016

May 2016 employment summary

• Employment growth stalls as sustaining growth becomes challenging- May’s employment growth of just 38,000 net new jobs was the lowest in years, while March and April’s growth figures were revised

downward slightly. The ability for the labor market to absorb 150,000-250,000 monthly gains is becoming increasingly difficult as slack declines and wages rise.

- Unemployment dropped to 4.7 percent, however, as the civilian labor force declined by 458,000 people, leading to a 20-basis-point decline in the labor force participation rate to 62.6 percent after a small rebound earlier in the year.

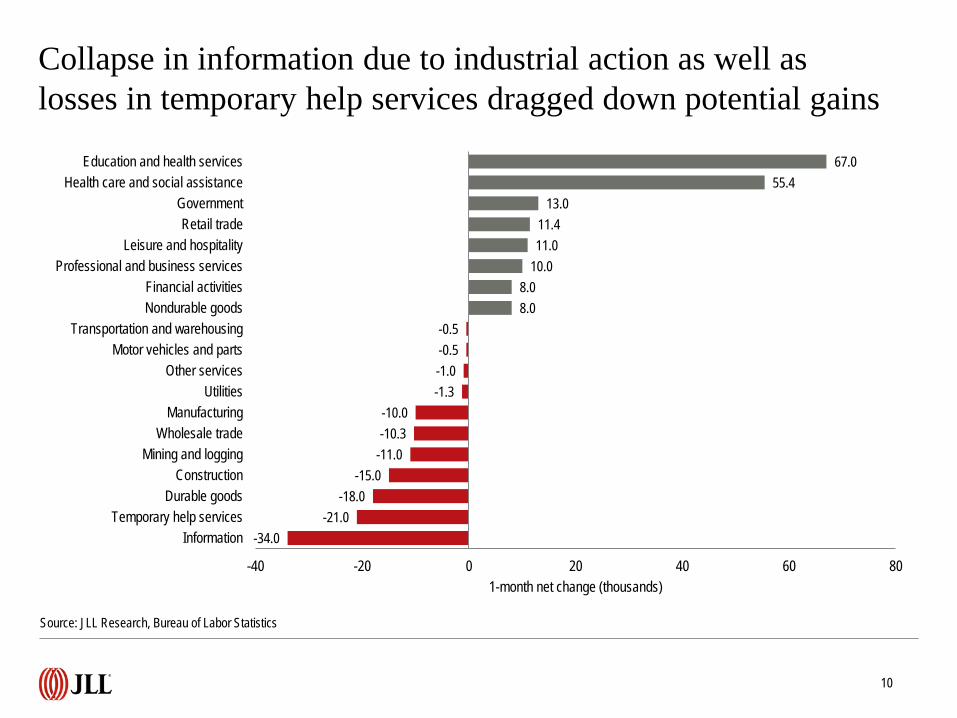

- At the industry level, performance was mixed. Goods-producing industries saw greater levels of contraction, particularly durable goods and mining, whereas education and health was largely immune to drops. Industrial action hindered information, which saw a 34,000-person decline in May.

• Labor turnover still on the up, with job openings exceeding hiring - Job openings are approaching a record 5.8 million, up 12.7 percent year-over-year. Similarly, hires and quits have risen as well, but job

openings are outpacing them significantly. - The disparity between job openings and hires/quits signals that May’s stall may have been an aberration. Employers are still looking to

increase headcount and are hiring healthily, but employees are leaving their jobs faster than are being higher.

• Indicators further delay Federal Reserve’s decision on interest rate hikes- Although unemployment fell below the 4.8-percent threshold for the Federal Reserve to consider an interest rate hike, other metrics such

as inflation have yet to rebound fast enough. - The labor market is one of the Federal Reserve’s most important indicators to guide rate hikes. The rapid slowdown in monthly gains during

2016 and downward revisions in recent months may further delay increases.

Source: JLL Research, Bureau of Labor Statistics

2

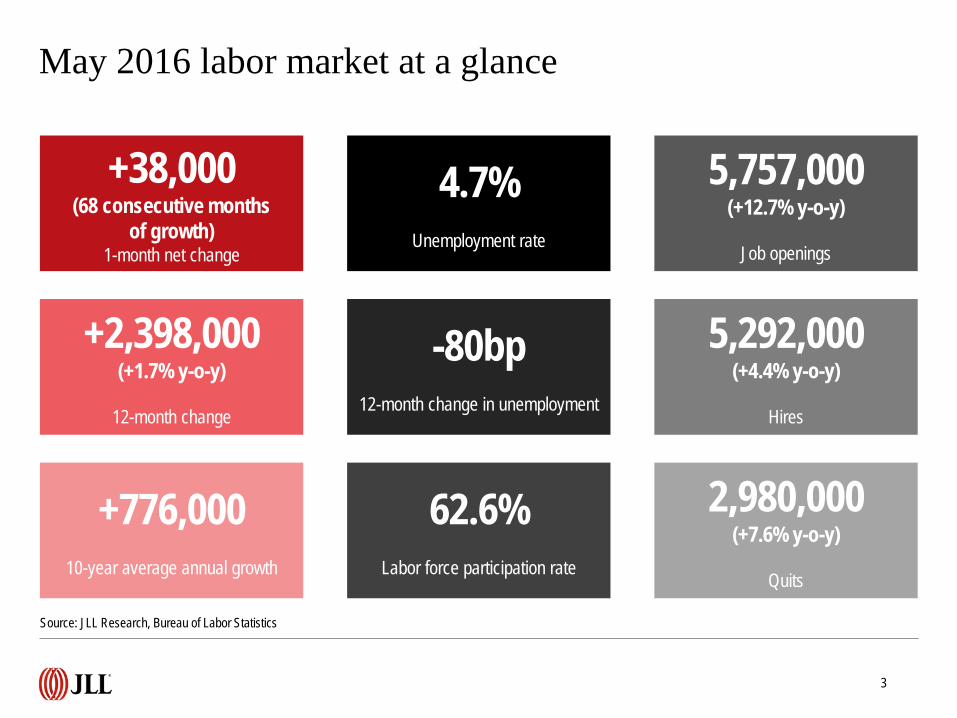

May 2016 labor market at a glance

+38,000(68 consecutive months

of growth)1-month net change

+2,398,000(+1.7% y-o-y)

12-month change

+776,00010-year average annual growth

Source: JLL Research, Bureau of Labor Statistics

4.7%Unemployment rate

-80bp12-month change in unemployment

62.6%Labor force participation rate

5,757,000(+12.7% y-o-y)

Job openings

5,292,000(+4.4% y-o-y)

Hires

2,980,000(+7.6% y-o-y)

Quits

3

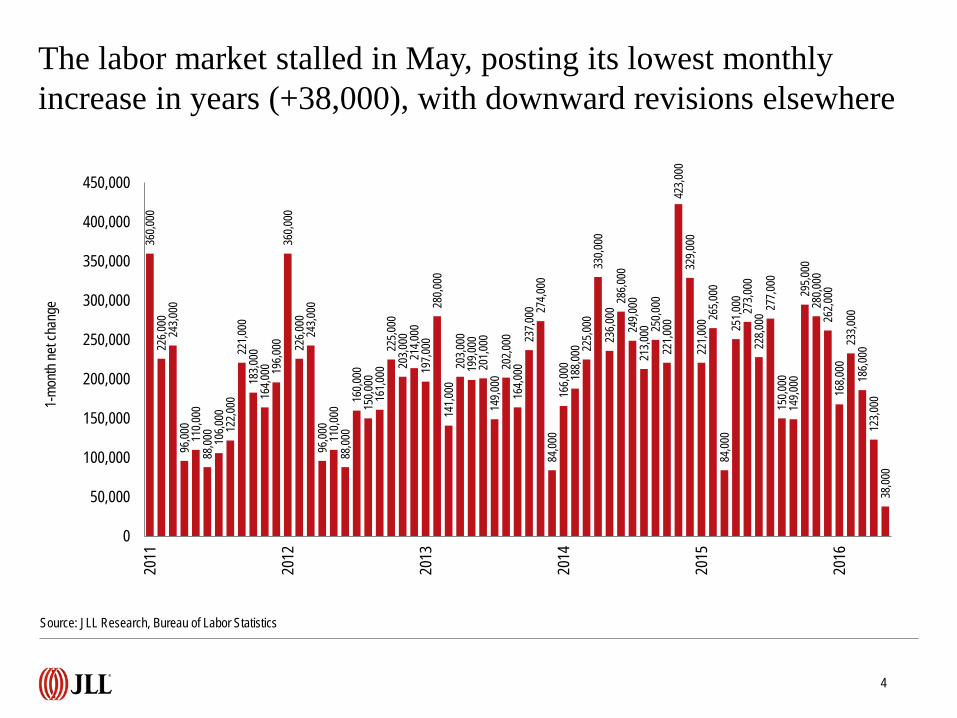

The labor market stalled in May, posting its lowest monthly increase in years (+38,000), with downward revisions elsewhere

360,0

0022

6,000

243,0

0096

,000

110,0

0088

,000

106,0

0012

2,000

221,0

0018

3,000

164,0

00 196,0

0036

0,000

226,0

0024

3,000

96,00

011

0,000

88,00

016

0,000

150,0

0016

1,000

225,0

0020

3,000

214,0

0019

7,000

280,0

0014

1,000

203,0

0019

9,000

201,0

0014

9,000

202,0

0016

4,000

237,0

00 274,0

0084

,000

166,0

00 188,0

00 225,0

0033

0,000

236,0

0028

6,000

249,0

0021

3,000 25

0,000

221,0

0042

3,000

329,0

0022

1,000

265,0

0084

,000

251,0

00 273,0

0022

8,000

277,0

0015

0,000

149,0

0029

5,000

280,0

0026

2,000

168,0

0023

3,000

186,0

0012

3,000

38,00

0

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2011

2012

2013

2014

2015

2016

1-mo

nth ne

t cha

nge

4

Source: JLL Research, Bureau of Labor Statistics

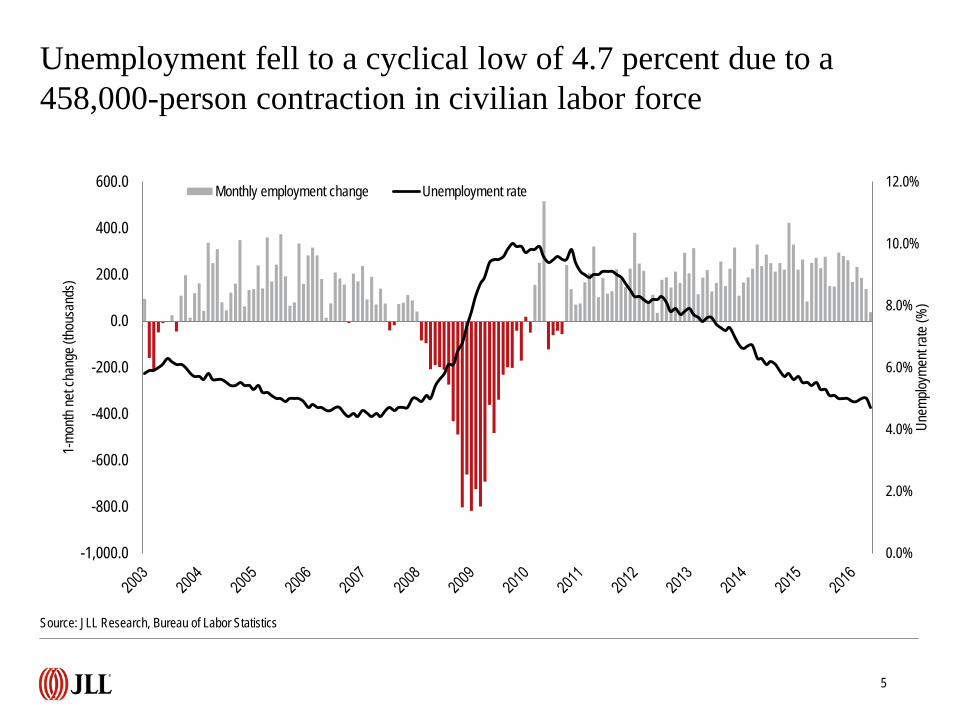

Unemployment fell to a cyclical low of 4.7 percent due to a 458,000-person contraction in civilian labor force

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

Unem

ploym

ent ra

te (%

)

1-mo

nth ne

t cha

nge (

thous

ands

)

Monthly employment change Unemployment rate

Source: JLL Research, Bureau of Labor Statistics

5

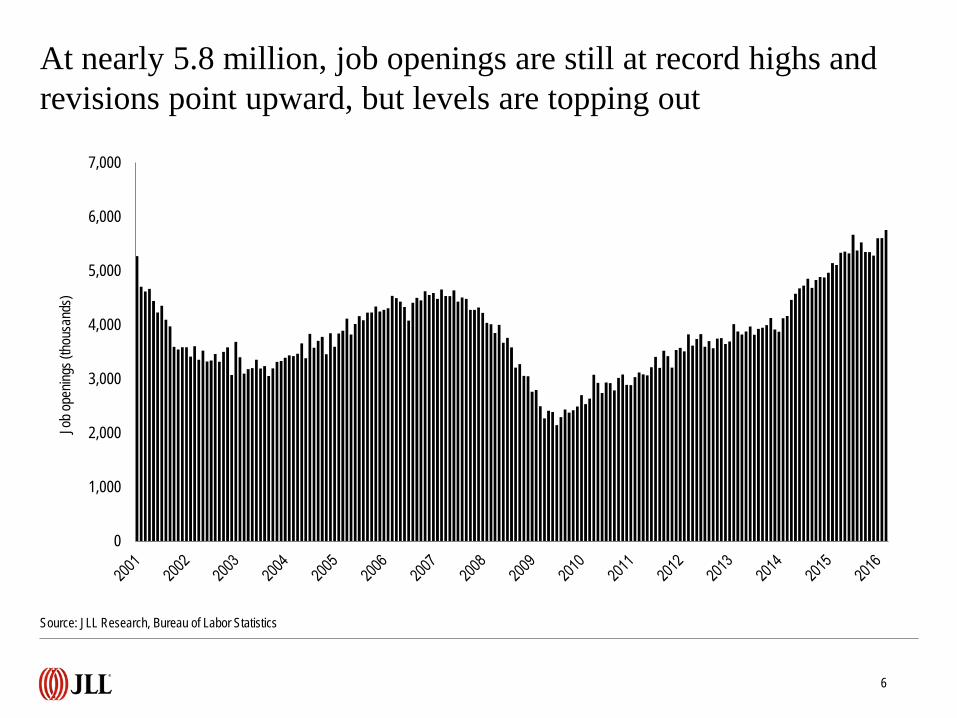

At nearly 5.8 million, job openings are still at record highs and revisions point upward, but levels are topping out

Source: JLL Research, Bureau of Labor Statistics

6

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Job o

penin

gs (t

hous

ands

)

0

20

40

60

80

100

120

140

Cons

umer

confi

denc

e Ind

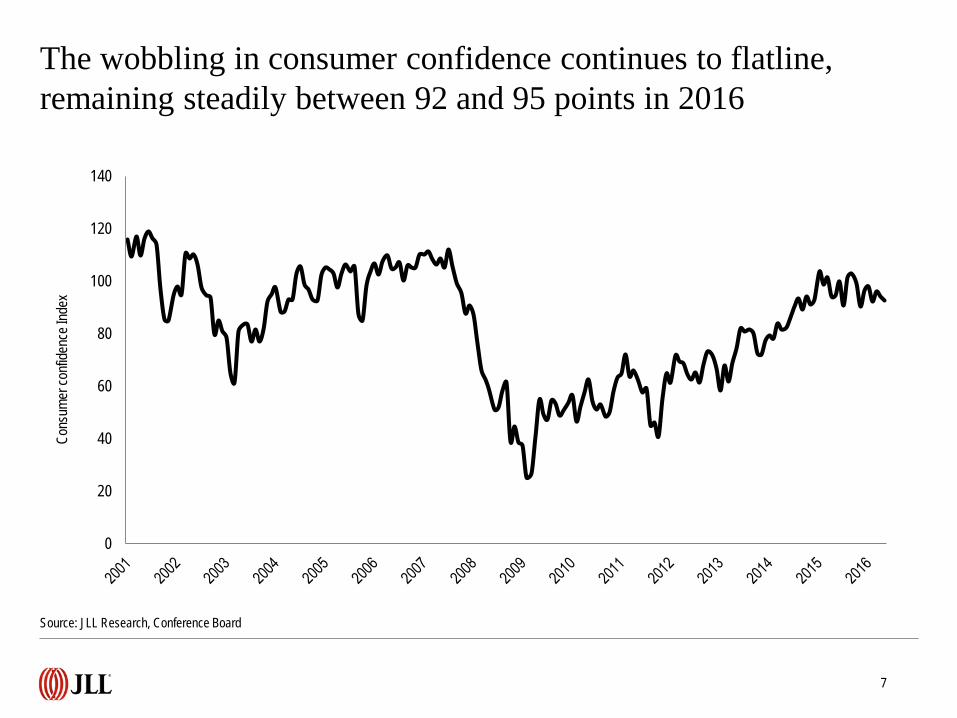

exThe wobbling in consumer confidence continues to flatline, remaining steadily between 92 and 95 points in 2016

Source: JLL Research, Conference Board

7

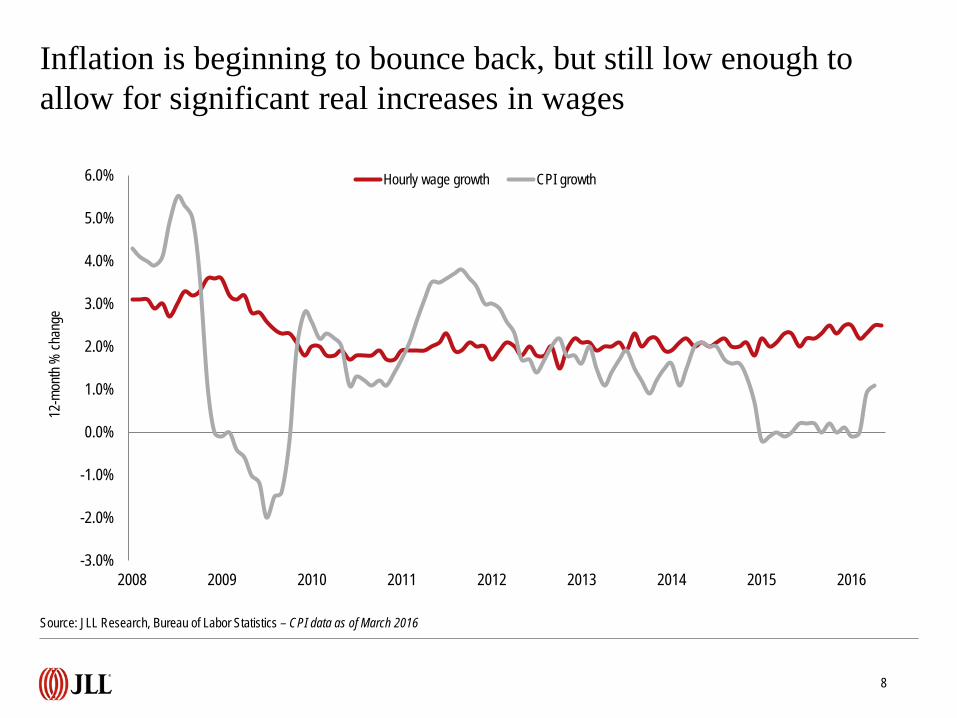

Inflation is beginning to bounce back, but still low enough to allow for significant real increases in wages

Source: JLL Research, Bureau of Labor Statistics – CPI data as of March 2016

8

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016

12-m

onth

% ch

ange

Hourly wage growth CPI growth

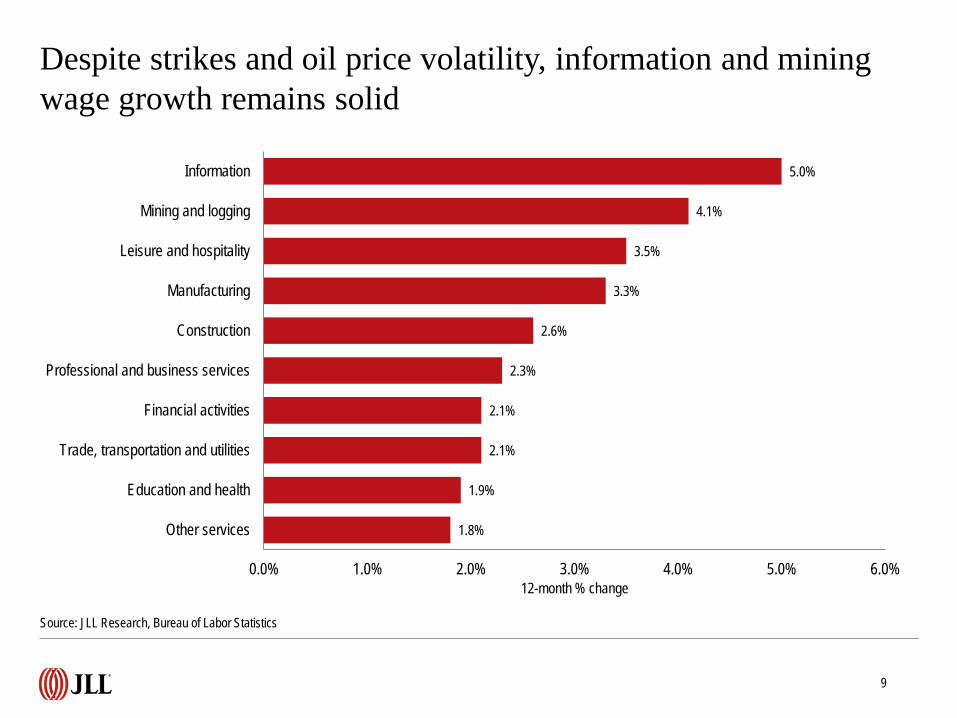

1.8%

1.9%

2.1%

2.1%

2.3%

2.6%

3.3%

3.5%

4.1%

5.0%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Other services

Education and health

Trade, transportation and utilities

Financial activities

Professional and business services

Construction

Manufacturing

Leisure and hospitality

Mining and logging

Information

12-month % change

Despite strikes and oil price volatility, information and mining wage growth remains solid

Source: JLL Research, Bureau of Labor Statistics

9

-34.0-21.0

-18.0-15.0

-11.0-10.3-10.0

-1.3-1.0-0.5-0.5

8.08.0

10.011.011.4

13.055.4

67.0

-40 -20 0 20 40 60 80

InformationTemporary help services

Durable goodsConstruction

Mining and loggingWholesale trade

ManufacturingUtilities

Other servicesMotor vehicles and parts

Transportation and warehousingNondurable goodsFinancial activities

Professional and business servicesLeisure and hospitality

Retail tradeGovernment

Health care and social assistanceEducation and health services

1-month net change (thousands)

Collapse in information due to industrial action as well as losses in temporary help services dragged down potential gains

10

Source: JLL Research, Bureau of Labor Statistics

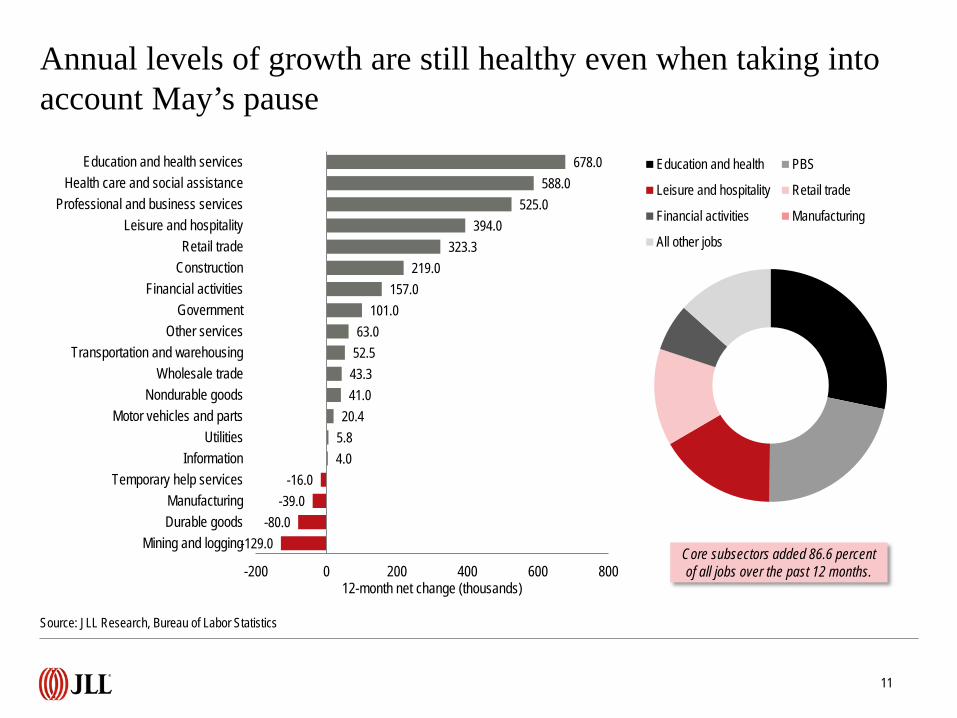

-129.0-80.0

-39.0-16.0

4.05.820.4

41.043.352.563.0

101.0157.0

219.0323.3

394.0525.0

588.0678.0

-200 0 200 400 600 800

Mining and loggingDurable goodsManufacturing

Temporary help servicesInformation

UtilitiesMotor vehicles and parts

Nondurable goodsWholesale trade

Transportation and warehousingOther services

GovernmentFinancial activities

ConstructionRetail trade

Leisure and hospitalityProfessional and business services

Health care and social assistanceEducation and health services

12-month net change (thousands)

Education and health PBS

Leisure and hospitality Retail trade

Financial activities Manufacturing

All other jobs

Annual levels of growth are still healthy even when taking into account May’s pause

Source: JLL Research, Bureau of Labor Statistics

11

Core subsectors added 86.6 percent of all jobs over the past 12 months.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Unem

ploym

ent ra

te for

bach

elor’s

degr

ee ho

lders

(%)

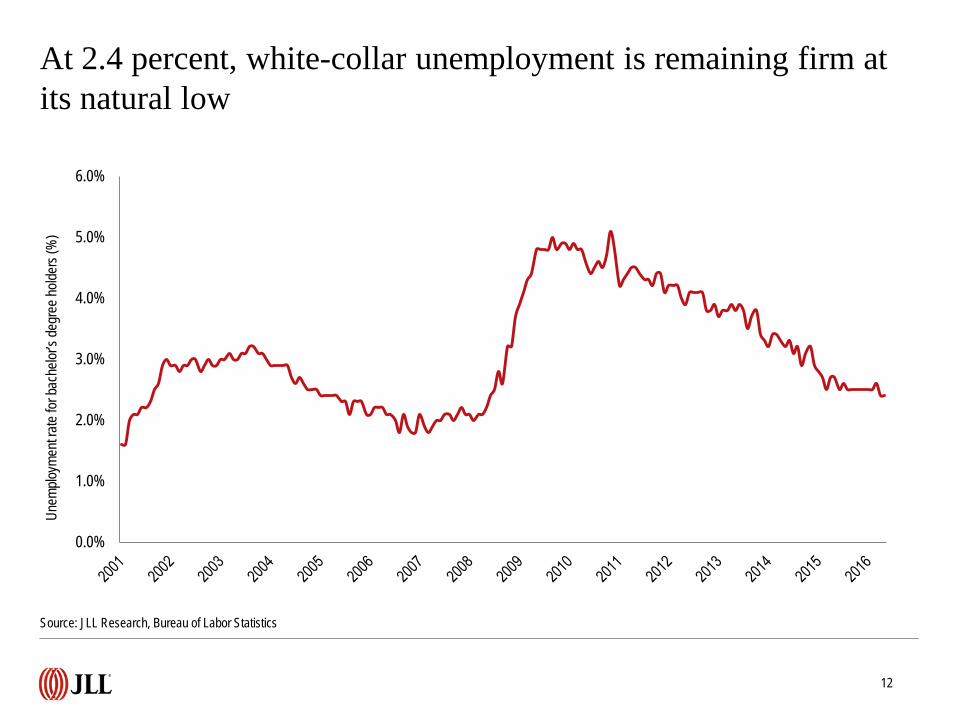

At 2.4 percent, white-collar unemployment is remaining firm at its natural low

Source: JLL Research, Bureau of Labor Statistics

12

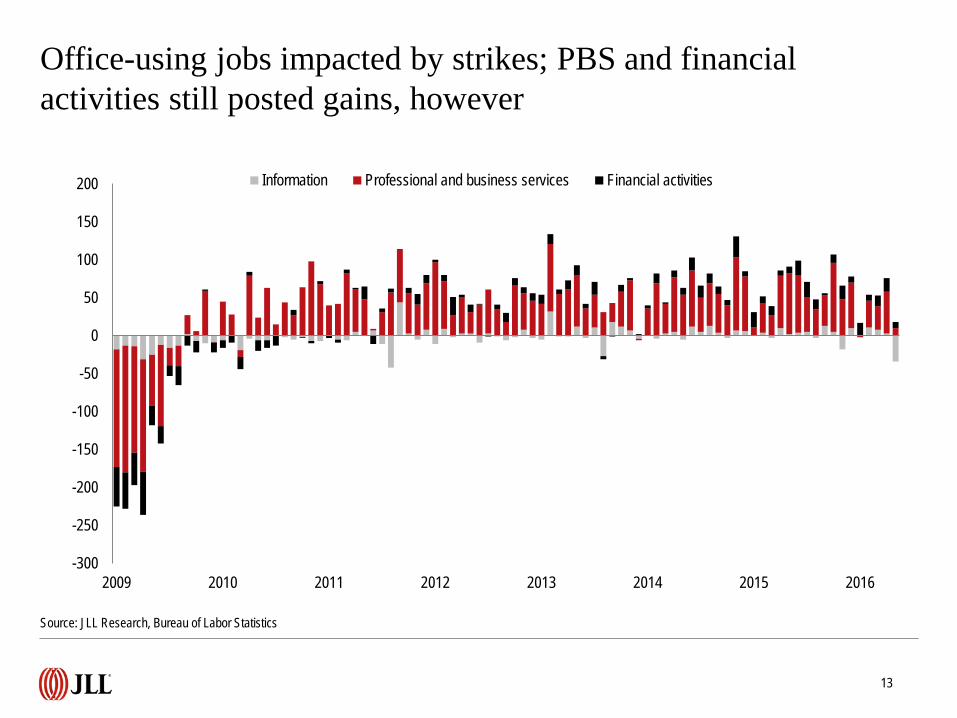

Office-using jobs impacted by strikes; PBS and financial activities still posted gains, however

-300

-250

-200

-150

-100

-50

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015 2016

Information Professional and business services Financial activities

Source: JLL Research, Bureau of Labor Statistics

13

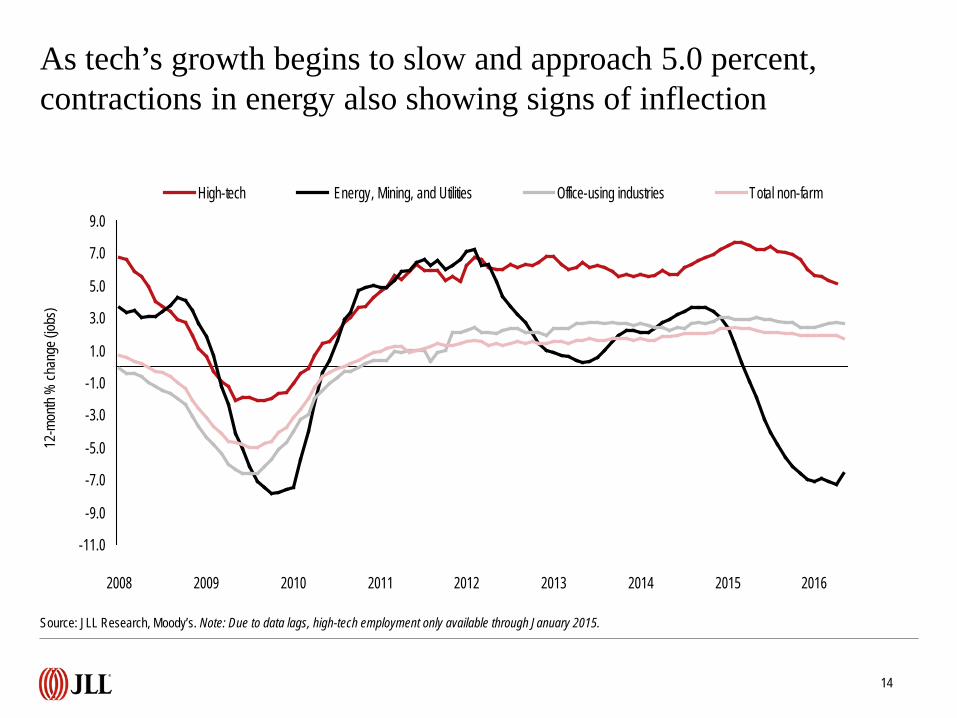

As tech’s growth begins to slow and approach 5.0 percent, contractions in energy also showing signs of inflection

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

2008 2009 2010 2011 2012 2013 2014 2015 2016

High-tech Energy, Mining, and Utilities Office-using industries Total non-farm

Source: JLL Research, Moody’s. Note: Due to data lags, high-tech employment only available through January 2015.

14

12-m

onth

% ch

ange

(jobs

)

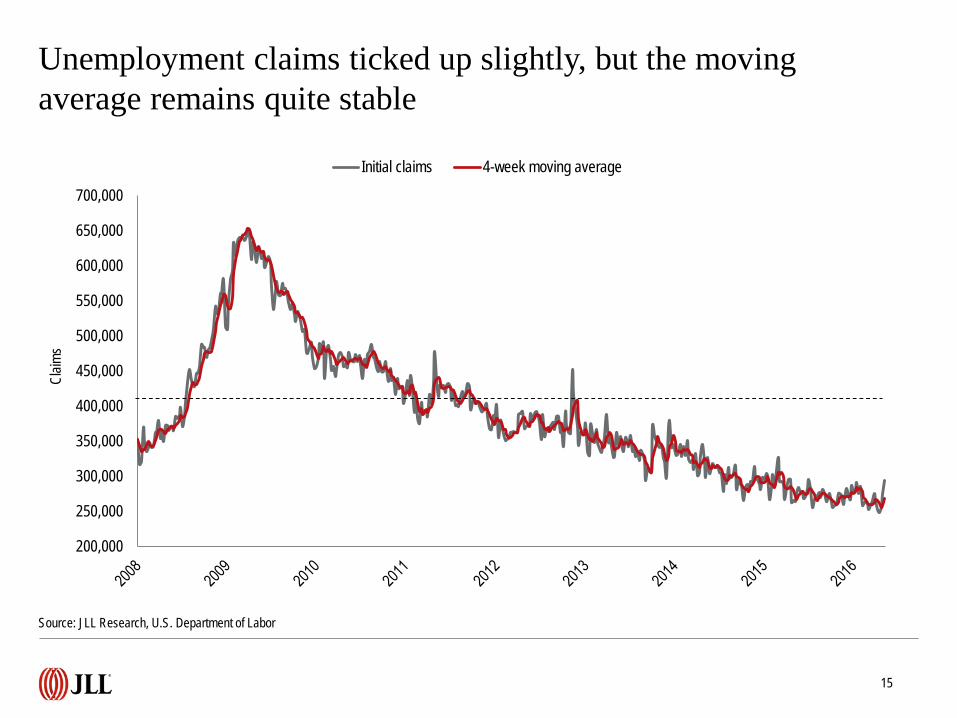

Unemployment claims ticked up slightly, but the moving average remains quite stable

Source: JLL Research, U.S. Department of Labor

15

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Claim

s

Initial claims 4-week moving average

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Hire

s and

quits

(tho

usan

ds)

Hires Quits

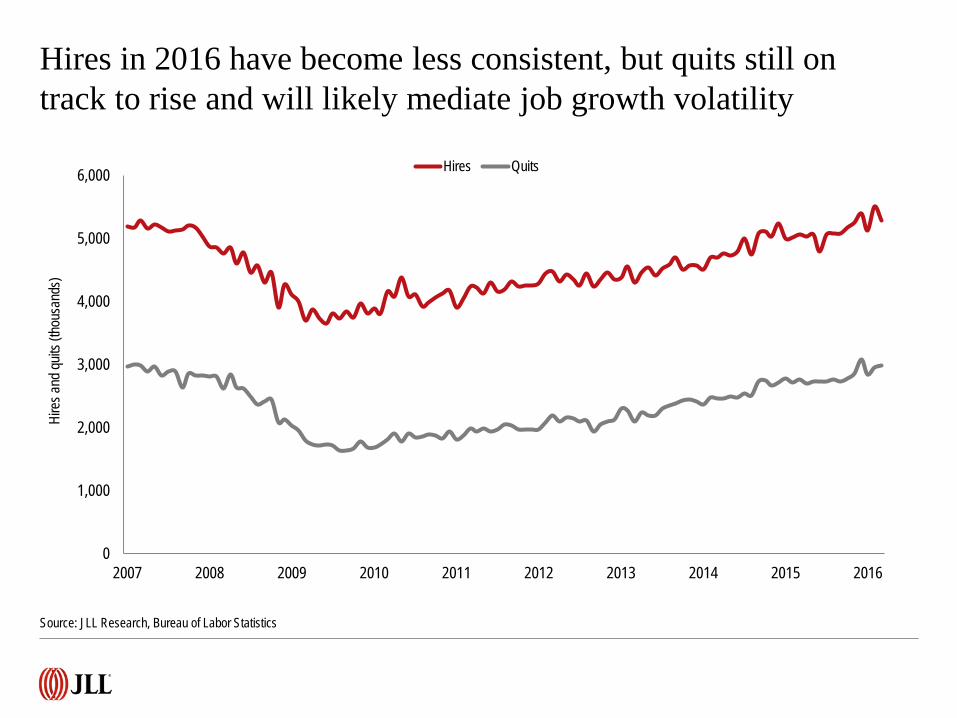

Hires in 2016 have become less consistent, but quits still on track to rise and will likely mediate job growth volatility

Source: JLL Research, Bureau of Labor Statistics

Month after month, tech and Sun Belt markets continue to surpass the national rate of job growth by more than 100bp

Source: JLL Research, Bureau of Labor Statistics

17

San Francisco

4.1%

Fort Lauderdale

4.0%

Dallas3.9%

Raleigh-Durham

3.4%Silicon Valley4.1%

Austin4.0%

0.3%

1.6%

1.7%

1.9%

2.2%

2.3%

2.5%

2.7%

3.2%

3.2%

3.9%

4.0%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5%

Houston

Chicago

Boston

New York

Philadelphia

Washington, DC

Los Angeles

South Florida

Atlanta

Seattle

Dallas

San Francisco

12-month % change

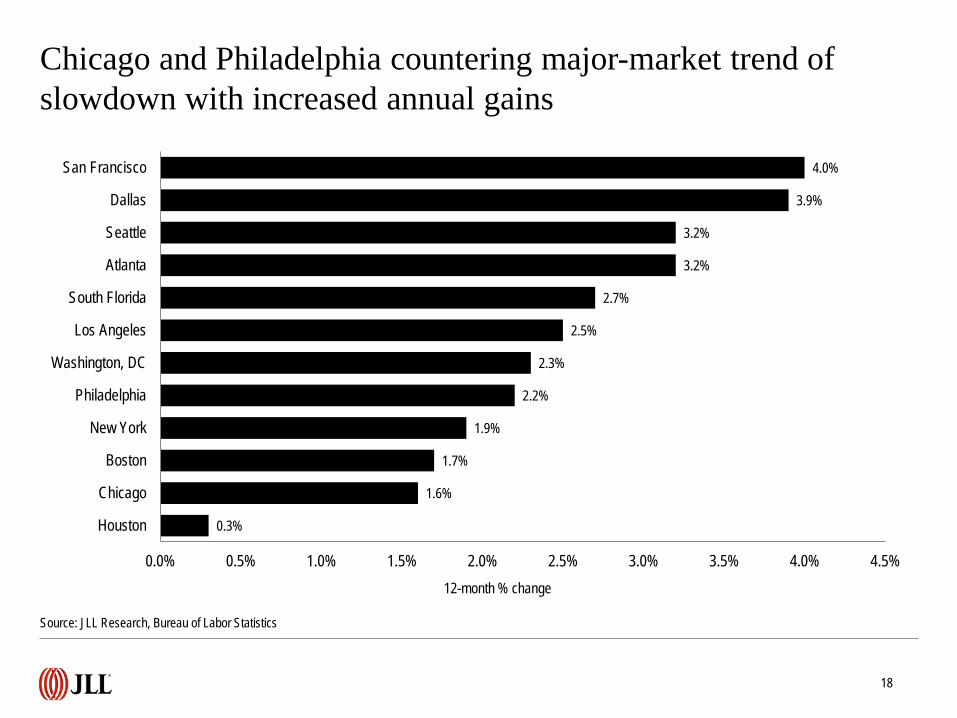

Chicago and Philadelphia countering major-market trend of slowdown with increased annual gains

Source: JLL Research, Bureau of Labor Statistics

18

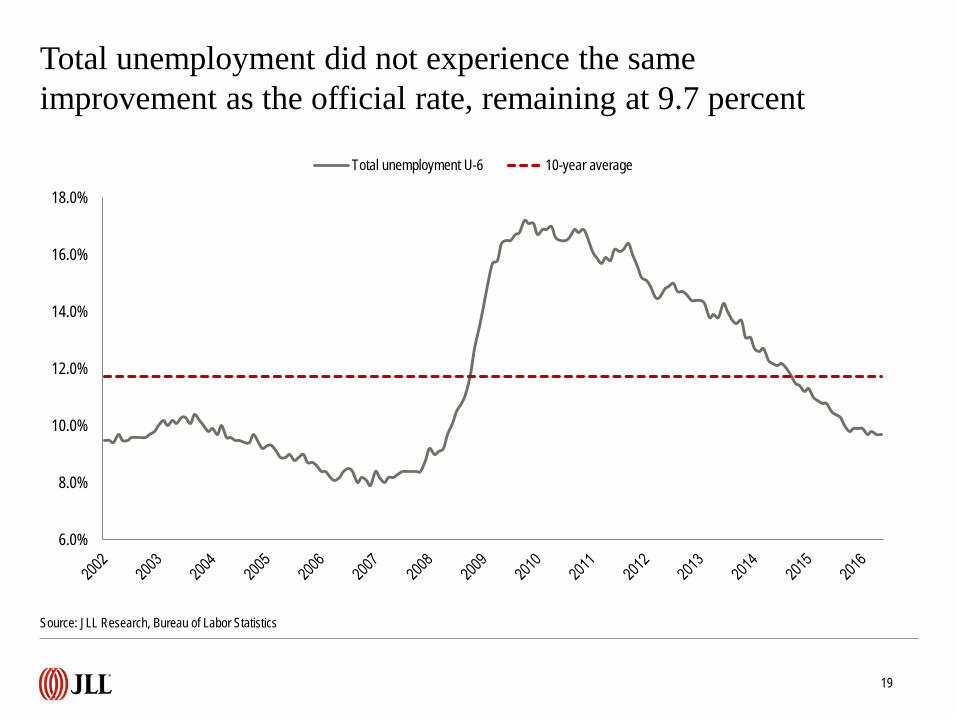

Total unemployment did not experience the same improvement as the official rate, remaining at 9.7 percent

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Total unemployment U-6 10-year average

Source: JLL Research, Bureau of Labor Statistics

19

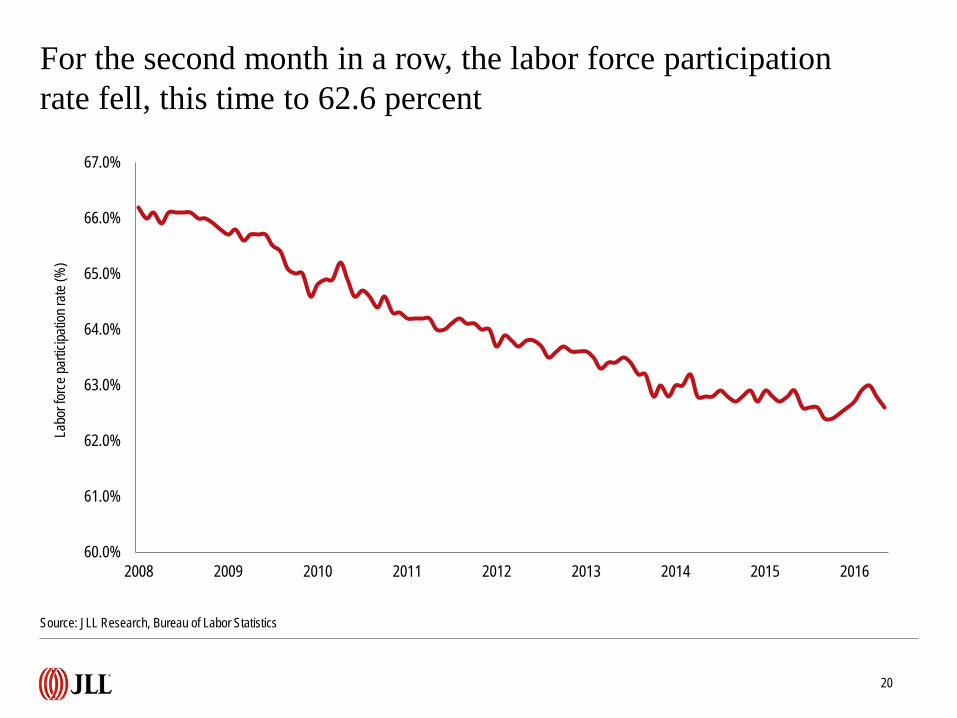

For the second month in a row, the labor force participation rate fell, this time to 62.6 percent

Source: JLL Research, Bureau of Labor Statistics

20

60.0%

61.0%

62.0%

63.0%

64.0%

65.0%

66.0%

67.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016

Labo

r for

ce pa

rticipa

tion r

ate (%

)

©2016 Jones Lang LaSalle Research IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

For more information, please contact:

Ben BreslauManaging Director - Americas [email protected]

Phil RyanSenior Research Analyst – Office and Economy [email protected]