Embed Size (px)

Citation preview

The death of UK business banking?“Entrepreneurs don’t trust their bank”

Truth? Threat? Opportunity?

The Debate

© Contexis 2017

Contexis House of St Barnabas Debates are a unique forum for Leaders

of global corporates, financial institutions and international consultancy

and advisory firms to meet with charity heads and inspiring entrepreneurs

to discuss, under a strict Chatham House rule, the critical business issues

of the day; to exchange knowledge, expertise and ideas from widely

differing perspectives.

None of this would be possible without the contribution of a wide range

of exceptional organisations and we are grateful for their time, candour

and insight. A small number of Contributors were represented in the debate

whose output you are about to read. Nothing that follows is attributable to any

one organisation.

If you would like to join a Debate we are always open to interesting and

challenging new Contributors. I’d welcome an email or tweet.

JOHN ROSLING

@jrosling

© Contexis 2017

It is said that 74% of

business owners believe

their Bank doesn’t understand

their business -

or even care about them

© Contexis 2017

We wanted to find out if this is even

remotely true..

what entrepreneurs really want from

their Bank..

and what the most innovative Banks

in the market are doing about it.

© Contexis 2017

So we brought together senior bankers from

traditional and challenger banks with

entrepreneurs, academics, journalists and

experts ..

..for an honest and sometimes fiery debate.

This is what was said..

© Contexis 2017

The entrepreneur’s perspective

I know my bank doesn’t care a

jot for me

I have three problems with my bank:

they are incredibly slow

my relationship manager can’t make

any decisions

and there is no balance in the risk - I

am taking all the risk in this

relationship

© Contexis 2017

The entrepreneur’s perspective

Most peoples views of their

Bank is “meh” - expectations

are so low

“meh” is a dangerous place to be.

I look at my Business Bank compared

to my Monzo interface and I wonder

why I need anything the Business

Bank offers.

Monzo has made me really think

© Contexis 2017

The challenger’s perspective

The failing of the UK

banking industry is the

source of our success

The Big Banks are shooting

themselves in the foot. If you are

continually telling the customer they

can’t borrow, they find money

elsewhere

© Contexis 2017

The challenger’s perspective

I can’t tell you how many

customers I’ve heard with

complaints about the Big Banks,

normally about time and lending

decisions

We were founded by entrepreneurs

not by bankers.

We are extremely speed conscious -

we don’t take 20 weeks to say no!

We invite all of our clients to sit in the

credit committee meeting

© Contexis 2017

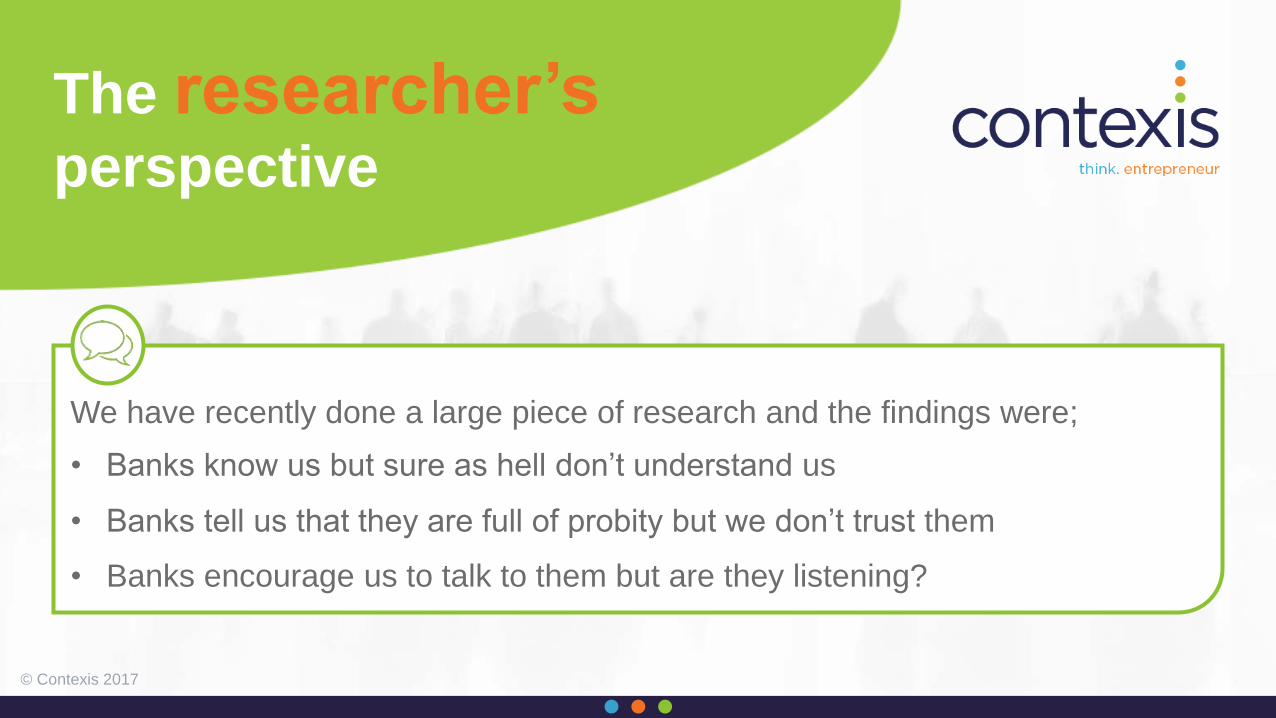

The researcher’s perspective

We have recently done a large piece of research and the findings were;

• Banks know us but sure as hell don’t understand us

• Banks tell us that they are full of probity but we don’t trust them

• Banks encourage us to talk to them but are they listening?

© Contexis 2017

The Big Bank’s perspective

The relationship

between banks and

SMEs has become

transactional

What is the unmet

demand that is being

served by all these new

banking licenses?? Most

banks are chasing the

same clients and ignoring

large parts of the market

Banks don’t have any

upside in this game;

only downside. And

margins are challenged

in a low interest world

© Contexis 2017

The Big Bank’s perspective

Fundamentally banks are there to

make money

but we have tended to

compartmentalise clients and don’t see

them as people.

We are overly product led and not

relationship or understanding led

We risk a pray and spray

approach, where some bright

spark has come up with an

idea and we tell our people our

clients need it when they don’t.

© Contexis 2017

So, what do entrepreneurs wantfrom their Bank?

I want something different. I just don’t yet know what I want from a

bank - and I don’t think the bank knows either

© Contexis 2017

Disruption; the existential threat?.

The alternatives to traditional

business banking

© Contexis 2017

Do we even need a

Bank?

I don’t think this is an

existential threat. Why

bother to change banks

when it’s a low-cost

commodity?

If banks can’t understand how

to lend in the modern world

with flexibility then they do

have an existential threat

© Contexis 2017

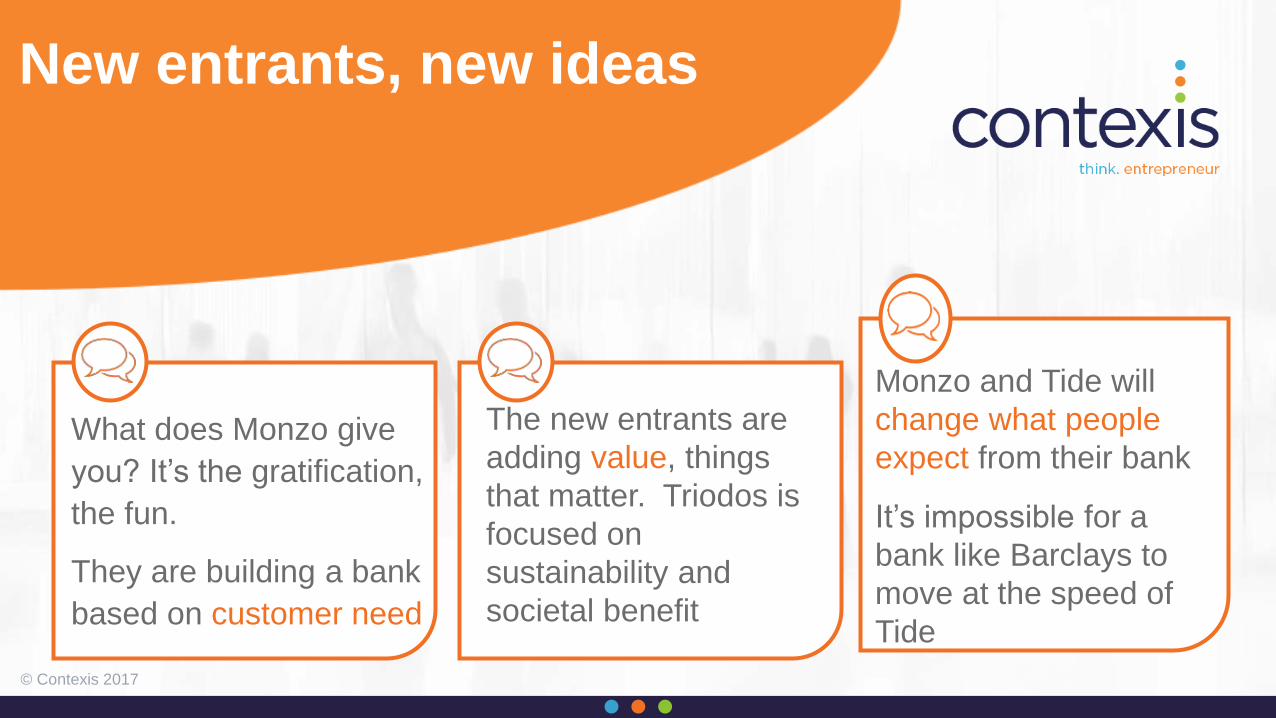

New entrants, new ideas

The new entrants are

adding value, things

that matter. Triodos is

focused on

sustainability and

societal benefit

What does Monzo give

you? It’s the gratification,

the fun.

They are building a bank

based on customer need

Monzo and Tide will

change what people

expect from their bank

It’s impossible for a

bank like Barclays to

move at the speed of

Tide

© Contexis 2017

As a customer, I do

wonder if anyone is

listening..

Banks are talking about

“customer centric” as if it was a

revolution!

That’s what business is all about!

Business used to be all about

the product now it is all about

customer.

Banks have simply not noticed

that shift

© Contexis 2017

The death of Banks

15 years ago I was turned down by 42 Banks.

Now we have seven Banks and hundreds of

millions in turnover. The banks couldn’t or

wouldn’t understand our business so we

funded ourselves through a private bond.

We have done that twice.

The real disruption is

peer to peer lending.

Apple are looking at

peer-to-peer; they don’t

need the banking

infrastructure

© Contexis 2017

The curse of legacy

thinking

Is there the desire for the Big

Banks to start up new technology

services?

We have asked every Bank and

they always have reasons for not

doing this, either legacy or

regulatory reasons

The problem as I see it is that

my Bank runs on a 1960s IBM -

and I want Monzo

© Contexis 2017

The curse of legacy

thinking

Why is it that when we wanted a

new payment system, we as an

industry couldn’t respond. PayPal

developed it. It was an

entrepreneurial not a banking

solution. To survive we need to

learn how to address that problem

PayPal is reacting immediately

because they can read their

customers and their needs

almost in real-time; have you

just had a holiday for example..

© Contexis 2017

The fastest elephantin the elephant race?

Banks are moving so

slowly. It reminds me of

the record industry. The

EMIs of this world

moved so slowly against

Apple, Spotify etc. it

feels like that

History tells us that

large, inflexible

organisations always fail

in an environment of

disruptive technology

Shifting a Big Bank is so

difficult.

Challenger Banks can

move fast because they

have no legacy

© Contexis 2017

The inconvenient truth

behind Amazon

The made a fortune but it wasn’t then who created refrigeration. They rejected the technology and believed

in the incumbency. It’s the same for Sony or Kodak.It’s takes us 20 weeks to make a loan decision, 7 days to get a debit card.

With Amazon doing everything next day, for how long is this tenable?

© Contexis 2017

Institutional

arrogance?

There is institutional arrogance in

the Banks. A sense of

entitlement. It can’t happen to

us.

It can

And it will

The Big Five are claiming to

move faster - does anyone see

any evidence of this?!

© Contexis 2017

The existential threat

The made a fortune but it wasn’t then who created refrigeration. They rejected the technology and

believed in the incumbency. It’s the same for Sony or Kodak.

The disruptor never comes from the incumbent industry. 200 years ago the

biggest US industry was cutting ice from lakes and sending it around the world.

The ice Barons of Boston made a fortune but it wasn’t them who created

refrigeration. They rejected the technology and believed in the incumbency. It’s

the same for Sony or Kodak. It’s the same for the Banks.

© Contexis 2017

It all sounds pretty bleak so far..

Is it really that bad?

The surprising answer turns out to be

.. maybe not..

© Contexis 2017

The surprising level of

affection we still have

for the Bank

At the moment the Big Banks still

have the hearts and minds of

most customers. If you continue

to abuse this, the future is a

wholesale move to someone who

will offer substantially different

benefits

The Banks right now have the

opportunity to turn around the

situation

© Contexis 2017

The rosy future for UK banking?..

in two words..

Relationship

and

Data

© Contexis 2017

1. The enduring power

of relationship

The power of the Relationship

Manager is extraordinary when

they are given the knowledge

and the opportunity. The value of

their connectivity is exceptional.

They can spot opportunities for

me and for the Bank

The insight the Banks seem uniquely

unable to grasp is that you focus your

people on what people are great at

and your technology on everything

else.

People are great at relationship.

Banks turn their people into order

takers.

© Contexis 2017

The enduring power of

relationship

All they need to do is ask

questions and learn how to listen

and only then what service they

can offer - and that might not be

anything to do with banking.

But people or listening skills are

not encouraged or taught

Why aren’t all Banks providing a

service that starts with ‘what are you

trying to achieve with your business’?

What is missing that means this

doesn’t happen?

© Contexis 2017

Relationship Management

Back to the future?

I would gladly

pay for this

There must be an

opportunity between the

service-focused private

banker and the

automated proposition

What if I asked you as an entrepreneur “would you

like a new client”. As a banker, if I understand your

business, I can provide those opportunities

As an entrepreneur I

would pay for this

service.

That is why we moved

Banks

© Contexis 2017

Taking the time to get to

know our customers

better

We take the time to get to know our customers better.

Every one of our customers has a dedicated RM.

We take time to really understand the customer and understand their investment

and payback cycles.

We are patient

© Contexis 2017

£8 billion of potential fee

income..

We looked for people

who are good listeners

and were patient, who

were willing to

understand the needs of

the business

We attribute our

spectacular growth to

the relationship

approach not the

product or price

Our research

suggests there is £8

billion of potential fee

income from SMEs in

the UK alone

© Contexis 2017

Business people, not

product sellers

Some Banks are looking to upskill their Relationship Managers. But there has to

be a choice; a low friction technical solution for those who want it, and a

relationship focused service for those who would value it.

What the Banks must do is turn their people into business people, not product

sellers

© Contexis 2017

So, what’s stoppingus?

Because the banks have

completely de-skilled their

people.

Their front-line people have no

clue about my business - or any

business

When the RM has 300 clients

how can they possibly advise or

create value?

The advice that used to be available

through RMs has been retrenched

and lost through greater

centralisation

© Contexis 2017

The choice.. one size fits

all won’t work any more

it’s a matter of choice

but surely the choice is

for the client

What do entrepreneurs

actually want; low cost

debt services or

relationship?

What we need to do is to

find out what customers

actually want from their

banks; offer a basic

frictionless, data-smart

service at low-cost, AND

offer a full service to

those who will pay for it

© Contexis 2017

2. The power of data

What the Challenger Banks and the

peer-to-peer platforms are doing well

is using data.

The Big Banks have much more of

that data but don’t know how to use it

’

The biggest opportunity for

the Big Five is big data.

And the biggest threat is big

data

© Contexis 2017

BIG data

Forward to the future

We have a view into about 25% of

all UK transactions. Apple or

Google would do something sexy

with that. We can’t seem to do

this

A.I. will start to replace some

aspects of business banking.

That’s a good thing. But the Banks

need to be careful what they

replace

© Contexis 2017

So, the future for UK banking is bright?

Well, maybe..

© Contexis 2017

The opportunity to do

both

There are so many options if we’re

just talking about debt

but not if we are talking about value.

Who has the network?

Who has relationship and can offer

partnership opportunity?

AND who has the data?

The Big Banks, uniquely,

have the opportunity to do both

relationship and technology

Their biggest opportunity is to reboot

personal relationships and work out

how to streamline the vanilla stuff

© Contexis 2017

The future is bright..

“The future for European banking is binary; it’s either fantastic or

disastrous. Banks will either learn quickly to use their assets or lose out.

They have visibility of so much data they need to learn to use it.

They have unique relationships at local level they need to learn how to stop

abusing these and create more value.

The future could be very bright. But if they don’t, alternative providers will become

dominant…

© Contexis 2017

The future is bright?

Ant Financial is five years old and already sees 90% of transactions in China.

Their approach is wholly disruptive.

They are already talking to technology companies in Europe…

© Contexis 2017

So, what have we learnt?..

© Contexis 2017

Business owners don’t trust their Banks?.

It is rather more nuanced than that:

• They don’t feel understood or listened to

• There is no real relationship in the way entrepreneurs

understand it

• They are starting to ask why they even need a Bank

© Contexis 2017

And YET .. there is still loyalty and affection for a

traditional banking model

© Contexis 2017

The Big Banks are under multiple threats.

• Challengers are much more agile, much more

customer-focused, much better at using data

• Offering value; fun, ease, social conscience

• Big Banks are:• too slow to adapt

• strangled by legacy

• arrogant

• product obsessed

• compartmentalising clients and not treating

them as people

© Contexis 2017

And YET.. the Big Banks have all the data, if

they only knew how to use it

and all the relationships if they didn’t continue

to screw them up

© Contexis 2017

The market is becoming ever more

diverse

• Multiple different forms of offering

• Masses of choice for credit

• New brands, new technology, easier and quicker

solutions

© Contexis 2017

And YET .. banking is about much more

than credit

© Contexis 2017

So, according to this group of

entrepreneurs, academics and experts,

what must the Banks do:

• Learn to ask

• Learn to listen

• Respond with genuine choice

© Contexis 2017

So, according to this group of

entrepreneurs, academics and experts,

what must the Banks do:

• Re-prioritise and rebuild relationships; the Bank’s

ultimate USP; but this requires a wholesale

reassessment of front line people from order-takers to

business partners

• Learn how to use data and innovate creatively with

the customer in mind.

© Contexis 2017

“Amazing

insights”

Entrepreneur

“A really

stimulating

discussion”

Partner professional

services

“Great discussion. Really nice group of people”

HRD, Global Multinational

“honoured to

be part of this”

Entrepreneur

Join in?Twitter: @contexis

Linkedin: Join the Purpose in Business Movement

Attend our next Roundtable: [email protected]

Get inspired: www.contexis.com/insights