Embed Size (px)

Citation preview

©2015 Experian Information Solutions, Inc. All rights reserved. Experian and the Experian marks used herein are trademarks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any form or manner without the prior written permission of Experian. Experian Public.

The positive impact of utility credit reporting

May 20, 2015

This presentation is streaming audio, which can be heard over computer speakers. There is no dial-in number for this Webinar.

2©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingSpeakers

Chris Magnotti, Analytical Consultant, ExperianChris Magnotti is an analytical consultant for CIS Analytics within Experian’s Decision Sciences group. In this role, he provides the marketing and sales organizations with customized analytic support. Scope includes analytic product support and development, full file trade line reporting, recovery and collection study, credit trends, and custom solutions. Chris is an industry expert, who is also a regular speaker at industry conferences.

Chris has 19 years of experience in disciplines including: analytics; acquisitions; account management; fraud; collections; P&L forecasting; portfolio stress testing; portfolio acquisition; due diligence; international risk assessment; merge and acquisitions; junk bond evaluation; database development. Chris’s past experiences include working for a Top-5 portfolio in each of the following industries; bankcard, subprime bankcard and private label. Chris holds a Bachelor degree in Environmental Science from the University of Delaware.

Ashley Knight, Product Management, ExperianAshley Knight is part of Experian’s Consumer Information Services and is the Product Manager for Data Integrity Services. She is responsible for the ongoing management, product development, and marketing of Data Integrity Services and works closely with internal Sales teams, Data Providers, and Consulting groups to deliver on and to enhance the product suite. Ashley joined Experian in March 2014 and has 12 years of experience in the financial services industry. She was most recently with Santander Bank as Vice President of Product Management. Prior to that Ashley was with Citizens Bank as Product Manager for the consumer checking portfolio and has also held roles in finance, marketing, and underwriting.

Ashley has a bachelor's degree in Marketing from Roger Williams University in Rhode Island and currently resides in Newport Beach, California.

3©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Credit reporting and the consumer

Background What is credit history?

What is VantageScore® 3.0?

Key terms and segment definitions

What is alternative data?

How we added the new trade data

Results Impacts to file thickness, risk

segment and score migration

Modeled bankcard interest rate

Financial impact to data reporter

Support Experian is our partner

Experian Data Integrity Services

Why furnish data?

Our investment into data quality

The positive impact of utility credit reportingAgenda

4©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Credit reporting

and the consumer The positive impact of

utility credit reporting

4

5©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingRegulatory agency’s viewpoint

One possible way to help consumers build or strengthen their credit profiles is for credit reporting agencies to incorporate additional, alternative data such as regular telecom and rental payments.

— Empowering Low Income and Economically Vulnerable Consumers, CFPB November 2013 report

“ ”

6©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingIndependent research viewpoint

A non-partisan, non-profit policy research and development institute devoted to increasing financial inclusion using information solutions

Mainstream lenders can use ‘alternative’ or ‘non-traditional’ data, including payment obligations such as rent, gas, electric, insurance and other recurring obligations, to evaluate the risk profile of a potential borrower.

— Give Credit where Credit is Due, PERC December 2006 publication

“ ”

7©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Legislative branch Bipartisan support of ‘Credit Access and

Inclusion Act’ to encourage utility companies to report positive payment history

An effective and immediate way to help underserved consumers build or restore their credit

Executive branch CFPB research efforts, interested in fairness

Treasury supportive of alternative data use

White House has shown interest in learning the impacts of adding subsidized rental housing data, interests are expanding

The positive impact of utility credit reportingPublic sector efforts to encourage full file reporting

Alternative data is key to fulfilling government sound lending regulations (Card Act, Reg. Z, Dodd-Frank), without unduly harming consumers and the economy

8©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Organizations should consider that in light of the regulated environment, reporting accurate and complete credit data has significant benefits to the consumer

Our joint obligation is to create a healthy credit eco system and support the choices consumers make as part of their financial journey

The positive impact of utility credit reportingOur obligation

9©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingCFPB quote

Most decisions to grant credit – including mortgage loans, auto loans, credit cards, and private student loans – include information contained in credit reports as part of the lending decision. These reports are also used in other spheres of decision-making, including eligibility for rental housing, setting premiums for auto and homeowners insurance in some states, or determining whether to hire an applicant for a job.

”

“

— Consumer Financial Protection Bureau, Key Dimensions and Processes in the U.S. Credit Reporting System, December 2012

Credit reports play an increasingly important role in the lives of American consumers…

— Consumer Financial Protection Bureau, Key Dimensions and Processes in the U.S. Credit Reporting System, December 2012

“ ”

10©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

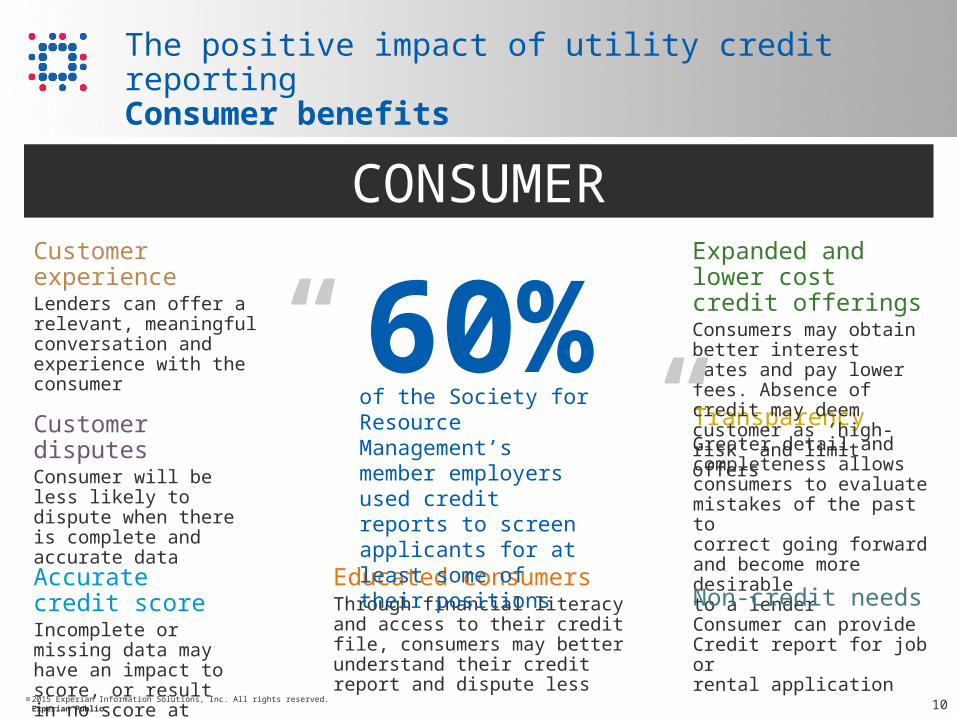

The positive impact of utility credit reportingConsumer benefits

Educated consumersThrough financial literacy and access to their credit file, consumers may better understand their credit report and dispute less

Customer disputesConsumer will be less likely to dispute when there is complete and accurate data

Accurate credit scoreIncomplete or missing data may have an impact to score, or result in no score at all

TransparencyGreater detail and completeness allows consumers to evaluate mistakes of the past to correct going forward and become more desirable to a lender

Expanded and lower cost credit offeringsConsumers may obtain better interest rates and pay lower fees. Absence of credit may deem customer as ‘high-risk’ and limit offers

Customer experienceLenders can offer a relevant, meaningful conversation and experience with the consumer

Non-credit needsConsumer can provide Credit report for job or rental application

“

”

CONSUMER

60%of the Society for Resource Management’s member employers used credit reports to screen applicants for at least some of their positions

11©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Background

The positive impact of utility credit reporting

11

12©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

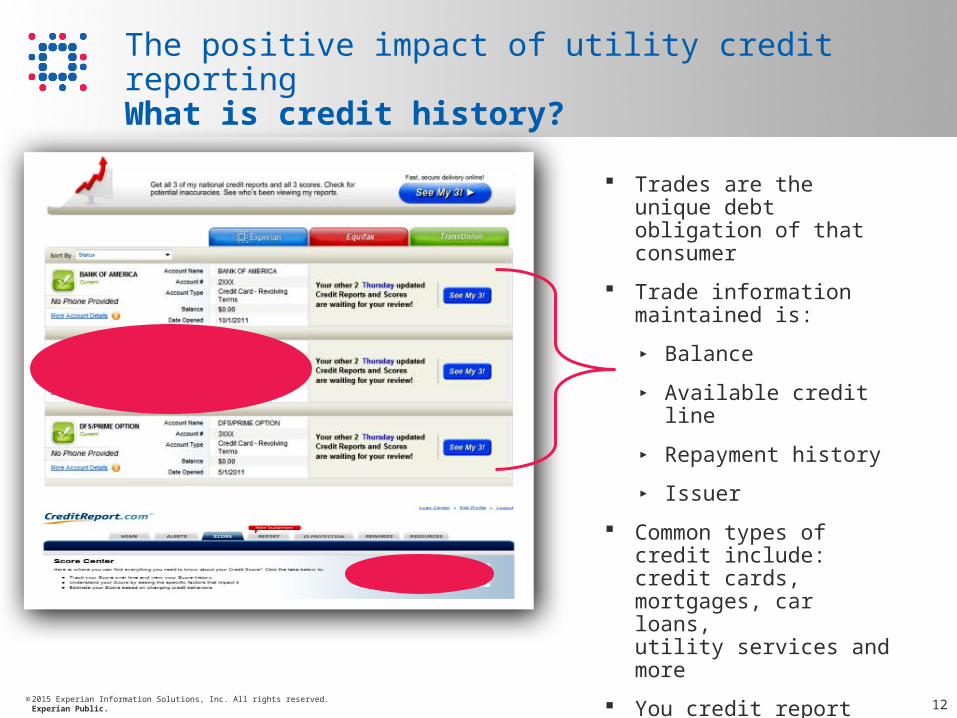

The positive impact of utility credit reportingWhat is credit history?

Trades are the unique debt obligation of that consumer

Trade information maintained is:

► Balance

► Available credit line

► Repayment history

► Issuer

Common types of credit include: credit cards, mortgages, car loans, utility services and more

You credit report serves as your financial history reference

13©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingWhat is VantageScore® 3.0?

VantageScore® is a superior credit risk model that dramatically increases the number of scoreable consumers, captures a broad and recent set of consumer behaviors, and generates more consistent credit scores across all three credit reporting agencies

VantageScore® 3.0 is a highly predictive, consistent credit risk score that lenders can use across the credit life cycle to make more informed credit risk decisions

14©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingKey terms and segment definitions

Risk segmentScore exclusions Cannot be scored using traditional scoring methods

Sub prime Weak credit history and reduced payment capability

Non (near) prime Challenged credit history, access to credit offers

Prime Most credit worthy and access to best credit offers

File thicknessNo hit Not found in Experian’s credit database

Thin Consumer with less than 5 trades on credit database

Thick Consumer 5+ trades on credit database

15©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

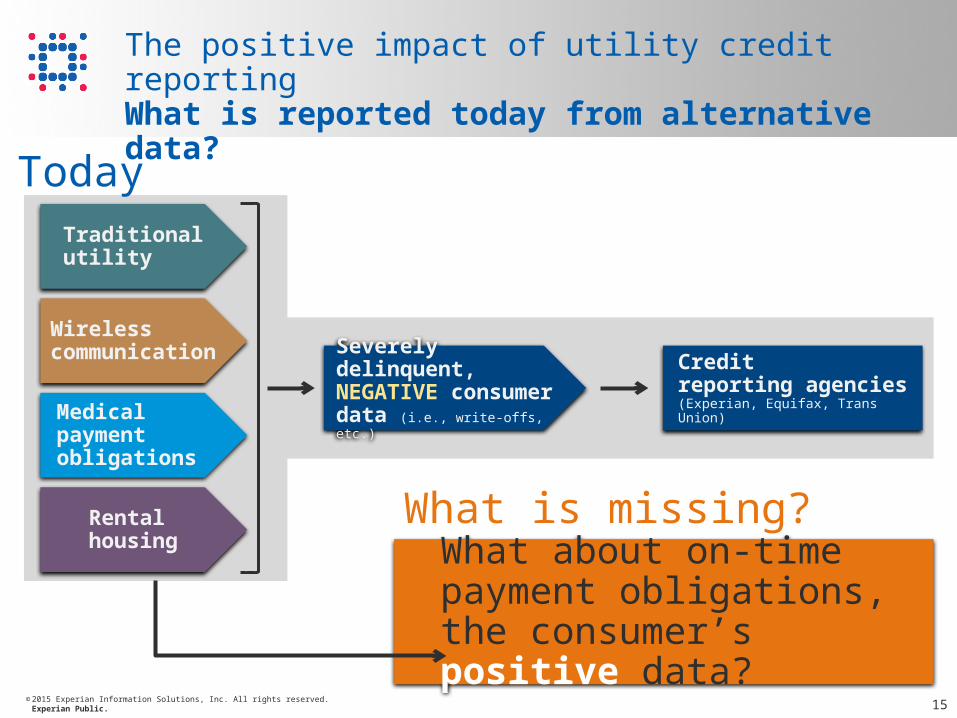

The positive impact of utility credit reportingWhat is reported today from alternative data?

Credit reporting agencies(Experian, Equifax, Trans Union)

Severely delinquent, NEGATIVE consumer data (i.e., write-offs, etc.)

Wireless communication

Medicalpaymentobligations

Rentalhousing

Traditional utility

What about on-time payment obligations, the consumer’s positive data?

What is missing?

Today

16©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Consumer trade data

Currentscenario

Final score VantageScore®

Scorelogic

The positive impact of utility credit reportingAnalysis design and how we added the new trade data

Score models leveraging the additional trade data, in their development, would become more predictive and have better insight on the consumer

Consumer trade data

Alternative tradeCurrent account status

Simulation Final score VantageScore®

Scorelogic

Each industry example will have one additional trade added to the consumer’s credit file except for Medical where up to five additional trades could have been added to their file

17©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

ResultsCurrent account statuses only

The positive impact of utility credit reporting

17

18©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

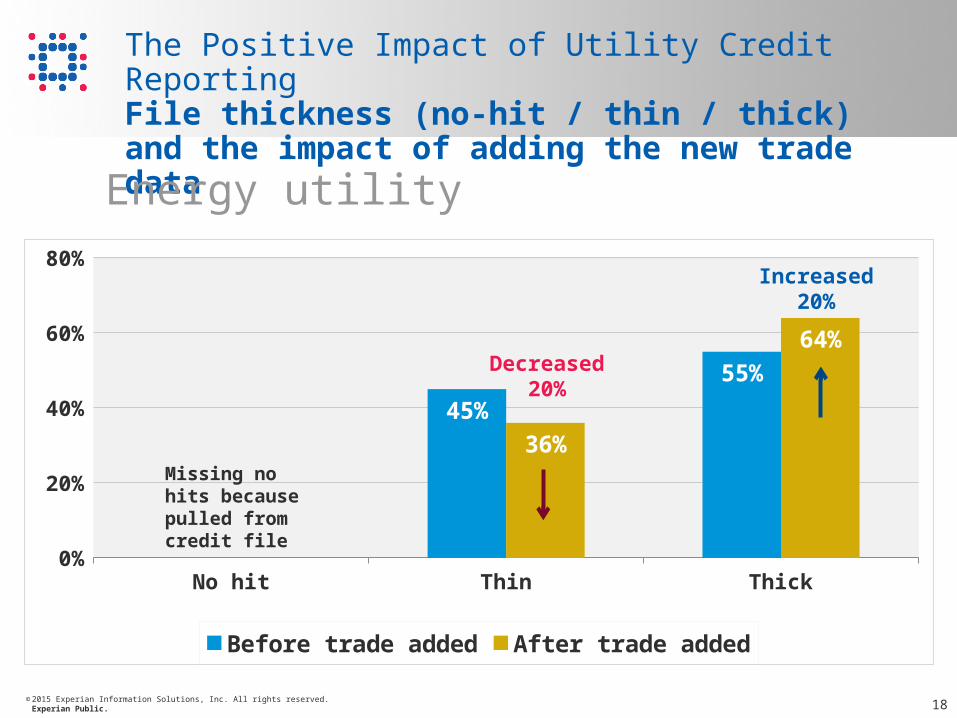

The Positive Impact of Utility Credit ReportingFile thickness (no-hit / thin / thick) and the impact of adding the new trade data

Energy utility

No hit Thin Thick0%

20%

40%

60%

80%

45%

55%

36%

64%

Before trade added After trade added

Decreased 20%

Increased 20%

Missing no hits because pulled from credit file

19©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingVantageScore® risk segment migration and the impact of adding the new trade data

Energy utility

Score exclusions Subprime Non-prime Prime0%

10%

20%

30%

40%

50%

60%

70%

3%

30%

13%

54%

2%17% 20%

62%

Before trade added After trade added

Decreased 33%

Increased 15%

Decreased 43%

Increased 54%

20©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingVantageScore® change and the impact of adding the new trade data

Energy utility

-11+ -1 to -10 0 1 to 10 11+0%

10%

20%

30%

40%

50%

1.8% 1.4%

21%

31%

46%Insignificant change*

*Experian has determined that a score change greater than 2% would constitute a significant change to bad rates

Score change = After score – Before score

21©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingVantageScore® change and the impact of adding the new trade data

Energy utility

-11+ -1 to -10 0 1 to 10 11+0%

20%

40%

60%

80%

100%

1.8% 1.4%

21%31%

46%

Total

Prime

Non-prime

Subprime

Insignificant change*

*Experian has determined that a score change greater than 2% would constitute a significant change to bad rates

Score change = After score – Before score

22©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

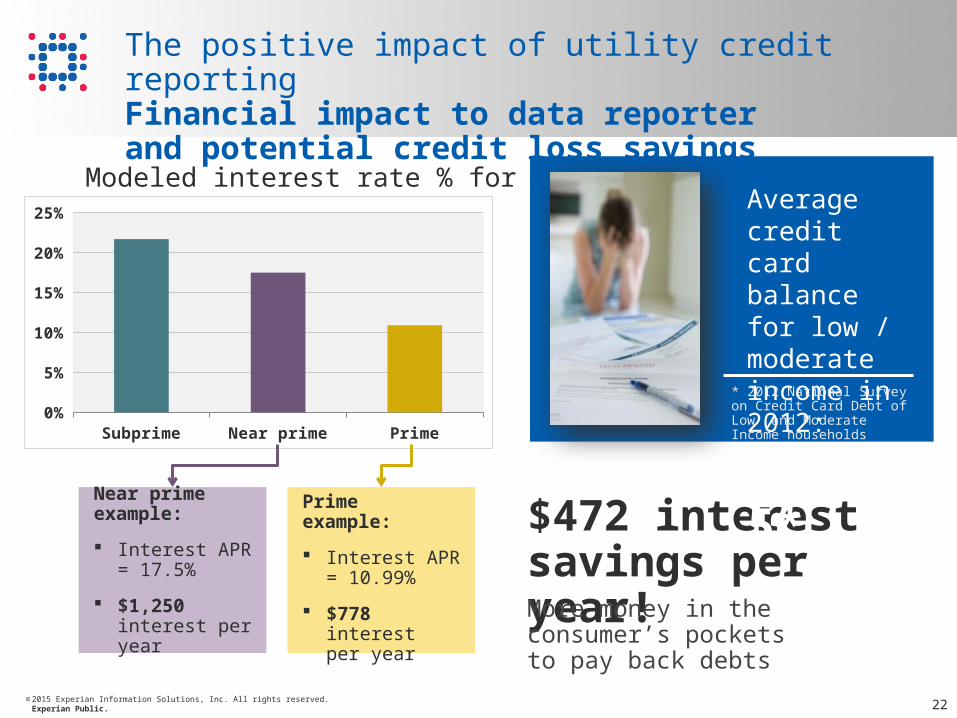

The positive impact of utility credit reportingFinancial impact to data reporter and potential credit loss savings

Subprime Near prime Prime0%

5%

10%

15%

20%

25%

Modeled interest rate % for credit card

Near prime example:

Interest APR = 17.5%

$1,250 interest per year

Primeexample:

Interest APR = 10.99%

$778 interest per year

$472 interest savings per year!More money in the consumer’s pockets to pay back debts

Average credit card balance for low / moderate income in 2012:

$7,145** 2012 National Survey on Credit Card Debt of Low and Moderate Income households

23©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingFinancial impact to data reporter 60+ DPD rates by quarter

Energy utility

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q10%

2%

4%

6%

8%

10%

12%60+ DPD

2006 2007 2008 2009 2010 2011 2012 2013 2014

Started full file reporting

40% drop in 60+ DPD

Lower delinquency rates = Lower losses

24©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Support

The positive impact of utility credit reporting

24

25©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingWhere Experian is prepared to help and support data reporting

Support

Resources

Research

IT support for file conversion Secure data transfer Data quality

Data reporting guidebook NCAC – Dispute support Pre-reporting analysis

Internal case studies PERC supporter

Experianis your partner throughout the process

26©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reportingData quality

Data Integrity Services

Metric Report DataArc Packages

Our packages offer a comprehensive solution and methodology for assessing data quality with focus on Metro 2 reporting and disputes

Obtain advanced analytics and peer benchmarking to produce information that is both insightful and actionable

Automated reporting tools help to monitor and correct rejected accounts

To help drive a positive customer experience for consumers and ensure maximum accuracy of consumer credit, we have created Experian Data Integrity Services

27©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Experian is committed to ensuring the integrity of data throughout the entire data life cycle and continues to build our repository of consumer credit information

► Experian obtains consumer credit information from over 13,000 data furnishers

► Data furnishers contribute 4.2 billion trades to our database

Furnishing credit data to Experian, benefits both clients and consumers

The positive impact of utility credit reportingWhy furnish data?

Consumer credit report

Establish payment history Increase tradeline

thickness Opportunity to improve

score Reduce ‘unscorable’

consumers

Customer experience

Potentially provide score and create consumer awareness

Establish payment history Positive customer

experience through validation of data quality

Data furnisher

Validate accuracy of on-file data and submissions

Fewer delinquencies and / or charged-off accounts

Broaden sales opportunities

Brand recognition

28©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

The positive impact of utility credit reporting Our investment into data quality

Experian is staying ahead of the curve We have invested in technology and resources to deliver quality data reporting and analysis through Experian Data Integrity Services

Our tools can help to monitor and validate the accuracy of Metro 2 submissions to create a positive customer experience while remaining compliant

29©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Download: New Experian perspective paper

“The Impact of Consumer Data Reporting” at http://www.experian.com/consumerimpact

New Experian white paper“Let There be Light” athttp://www.experian.com/utlities

Visit: Data Integrity Services Website at

http://www.experian.com/dataintegrityservices

CFPB Website at http://www.consumerfinance.gov/

The positive impact of utility credit reporting Resources

30©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.

Questions

The positive impact of utility credit reporting

30

31©2015 Experian Information Solutions, Inc. All rights reserved.Experian Public.