Embed Size (px)

Citation preview

Why not to die in a SMSF!

Disclaimer

This information has been prepared and issued by netwealth Investments Limited (netwealth), ABN 85 090 569 109, AFSL 230975. It contains factual information and general financial product advice only and has been prepared without taking into account your individual objectives, financial situation or needs. The information provided is not intended to be a substitute for professional financial product advice and you should determine its appropriateness having regard to your particular circumstances. The relevant disclosure document should be obtained from netwealth and considered before deciding whether to acquire, dispose of, or to continue to hold, an investment in any netwealth product.

While all care has been taken in the preparation of this information (using sources believed to be reliable and accurate at the time of writing), no person, including netwealth, or any other member of the netwealth group of companies, accepts responsibility for any loss suffered by any person arising from reliance on this information. Superannuation and tax law is often subject to change and you should check on the accuracy of any information prior to making any decisions that may affect your circumstances.

Nigel Smith, Technical Services

• SMSF’s – the panacea for all?

• Understanding “Super tax”

• Anti-detriment – getting that tax back!

• Dying as the ‘last man standing’ in a SMSF

• SMSF’s really do have a lifecycle

• Bringing it all together…

SMSF are great investment vehicles…

Strategic flexibility :– Better integration of business and lifestyle goals– Great for small business owners– Greater individual control

Investment flexibility– Greater choice - real property, collectables, unlisted– Limited recourse borrowing arrangements

Cost efficiency at higher asset values

Greater family involvement and privacy

BUT, they do have dangers …

× These include:– Lack of trustee administration, managerial and investment skills– Lack of initial capital – starting a SMSF too early– Potential lack of diversification – increasing single asset funds– Potential cash flow issues – over geared – Increasing regulatory oversight and penalty regime

× The greatest danger of all ….– Staying too long in a SMSF– Dying as the “last man standing” in a SMSF

Understanding super tax…

× Super is taxed in 2 ways

×15% on concessional contributions (pre-tax income)– Employer contributions– Salary sacrifice contributions– Personal deductible for self employed & substantially self employed

× Super earnings & growth in accumulation×15% on earnings×10% on realised capital gains > 12 months

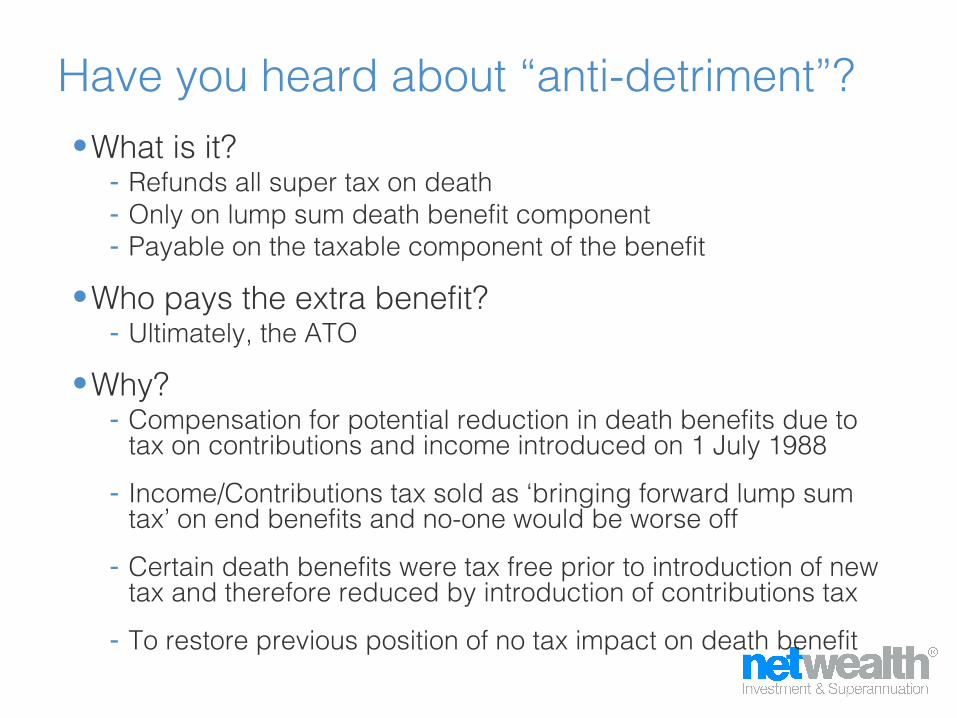

Have you heard about “anti-detriment”?•What is it? ‐ Refunds all super tax on death ‐ Only on lump sum death benefit component‐ Payable on the taxable component of the benefit

•Who pays the extra benefit? ‐ Ultimately, the ATO

•Why?‐ Compensation for potential reduction in death benefits due to

tax on contributions and income introduced on 1 July 1988

‐ Income/Contributions tax sold as ‘bringing forward lump sum tax’ on end benefits and no-one would be worse off

‐ Certain death benefits were tax free prior to introduction of new tax and therefore reduced by introduction of contributions tax

‐ To restore previous position of no tax impact on death benefit

Anti-detriment…a Super benefit to die for! •Who is entitled?‐ Spouse or former spouse‐ Child (any age) of deceased

•Trustee considerations:‐ No age restriction for death‐ Possible to paid via testamentary trust‐ May require stat declaration (“reasonable basis”)

•When is it paid?‐ Unfortunately, only on death of member

The fund MUST pay out the extra benefit and then only ‘recover’ by way of a tax deduction from the ATO

Assessment

•Trustee assesses if extra benefit payable

•Trust deed must allow for payment

Calculation

•The calculated amount is paid as ‘extra benefit’

•Amount calculated by a formula

•Additional to account balance death benefit + any insured amount

Payment

•Payment to benefit to beneficiary first

•Cannot use other members vested balance

Tax deduction

•Increased amount ‘reclaimed’ from ATO through a tax deduction to the fund

•Tax saving amount/15%

Other considerations• Only on lump sum death benefits only

• Not available if beneficiary receives a pension

• Tax treatment of ‘extra benefit’ exactly same for death benefit– Subject to usual tax rules for non-dependents– Forms part of the taxable element

• Doesn’t matter if deceased in accumulation or pension phase‐ So long as paid as a lump sum death benefit‐ Payable only on taxable component (excluding any insured

amount)

• Can be done even if reversionary pension, so long as:‐ Commute by later of:‐ 6 months of death of original pensioner‐ 3 months of probate

Calculating the benefit Most common method – ATO formula

Anti-detriment benefit (Tax saving amount) =

C x (0.15 x P) R - (0.15 x P)

C - taxable component of lump sum (excl. insurance)R - number of days in service period after 30 June 1983P - number of days in component R that occur after 30 June 1988

Calculating the benefit (Example)

John is aged 60 and has $500,000 in an account based pension, all of which is taxable component.•John’s service period commenced 1 July 1990•John dies on 1 October 2014

C = $500,000P = 8,859 days (since 30 June 1988)R = 8,859 days (since 1 July 1985)

Benefit = $500,000 x (0.15 x 8,859) 8,859 - (0.15 x 8,859)

= $88,235

To die with the benefit or without?

– Eligible service date 01/07/1990 Est Anti-Detriment increase $88,235– Date of payment 01/10/2014 Allowable tax deduction $588,235– Super death benefit (L/S) $500,000– Tax Free component $ NIL– Insurance proceeds $ NIL

Spouse Adult Child

Do nothing

D/Ben L/Sum $500,000 $500,000 Tax $Nil $85,000

Net $500,000 $415,000

With Anti-detriment benefit

D/Ben L/Sum $500,000 $500,000 Anti-detriment $88,235 $88,235 Total $588,235 $588,235 Tax $Nil $100,000 Net $588,235 $488,235

Benefit $88,235 $73,235

Which funds can pay the benefit?

•Any continuously complying superannuation fund (technically - but not practically - including SMSF)‐ Trust deed must provide for payment‐ Fund must have funds available to pay entire benefit

(reserves/insurance)

•No legislative compulsion on trustee to pay anti-detriment benefits‐ Payment is not compulsory‐ Many retail funds do, but not all‐ Industry funds?

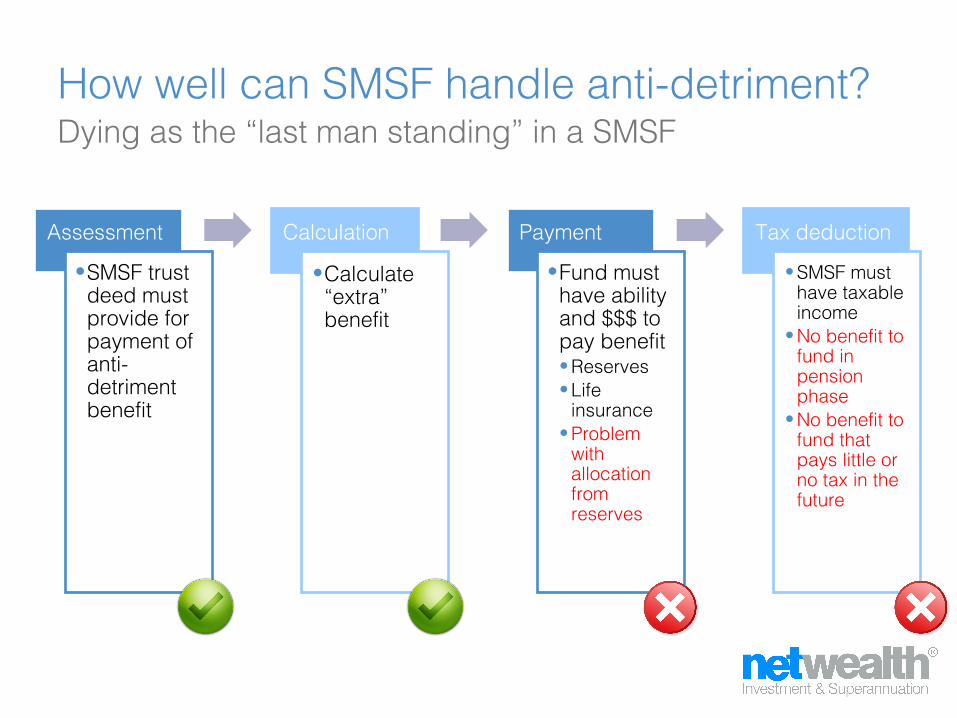

How well can SMSF handle anti-detriment?Dying as the “last man standing” in a SMSF

Assessment

•SMSF trust deed must provide for payment of anti-detriment benefit

Calculation

•Calculate “extra” benefit

Payment

•Fund must have ability and $$$ to pay benefit • Reserves• Life

insurance• Problem

with allocation from reserves

Tax deduction

• SMSF must have taxable income

• No benefit to fund in pension phase

• No benefit to fund that pays little or no tax in the future

Anti-detriment only works well in large funds

Assessment

•Needs the member to die in the large fund•Rollover

before death

Calculation

•Calculate “extra” benefit

Payment

•No problem with reserving

•Able to pay immediately

•How are we able to pay with no reserves?

Tax deduction

•Fund can recover full value of tax deduction

•Able to recover immediately, assessable income absorbs deduction

SMSFs have a use-by-date

Small contributions and small balancesStarting out in life

Growing but still a 2nd priorityOther prioritiesMortgage & young children

Salary sacrifice and gearingMerging of business & lifestyle goals

Young middle age Major earning potential or small

business owner

More investment opportunitiesMiddle age More surplus income

Final strategic planning opportunity to drive final balanceTransition to retirement

Pension phase - switch to "income" strategiesEarly years of retirement

Pension phase-increased estate planning focusLater retirement years

Maximising the cash to beneficiariesDeath

Suitable?

Wrap SMSF

Bringing it all together…

• Anti-detriment benefits are significant‐ Belongs to client and should be claimed‐ If passed to non dependents, helps offset the 15% tax + Medicare‐ Super provides potentially a 0% tax environment

• Self managed funds just simply not ideal to claim the benefit

• Not all retail funds pay anti-detriment but netwealth does

• It’s a complex area – seek help from a financial professional familiar with anti-detriment options

![SMSF webinar Sep 14.pptx [Read-Only]notchabove.com.au/wp-content/uploads/2014/09/SMSF... · •SMSF trustees have an obligation to consider whether they need to provide insurance](https://img.pdfslide.net/doc/110x75/5fca48aacae2a7533069a246/smsf-webinar-sep-14pptx-read-only-asmsf-trustees-have-an-obligation-to-consider.jpg)