Embed Size (px)

Citation preview

Please silence your cell phones! Thank you for being considerate to the people around you.

Paying for Postsecondary Education

HIGHER EDUCATION IS

CONSTANTLY CHANGING…

…Particularly Costs

Then v. Now • Please right click and duplicate slide. State School Tuition/Fees in 1993 -

$4000 State School Tuition/Fees in 2015 -

$9500 One summer of scooping ice cream could pay

for a year of college; today students would have to work about 991 hours (~25 40-hour weeks)

https://collegetuitioncosts.wordpress.com/graphs/

http://www.theatlantic.com/education/archive/2014/04/the-myth-of-working-your-way-through-college/359735/

• Please right click and duplicate slide. 2015:

4-year Public - $20k - $30k

4-year Private - $30k – over $60k

2030:

4-year Public - $40k - $60k

4-year Private - $92k - $130k

cost projector at www.finaid.org

Your education is a

good investment.

If I said, “Give me

$30,000 now, and in

40 years, I will give

you a $1M ROI -

guaranteed!,” do you

think that is a good

deal?

The higher your level of

education, the more

money you’ll earn over

your lifetime.

SO WHY IS EVERYONE

CONCERNED ABOUT

BORROWING AND

AFFORDABILITY IF STUDENTS

CAN PAY IT BACK?

Question:

Attainment • Please right click and duplicate slide. 59% of students who began

seeking a bachelor’s degree at a 4-year institution completed that

degree within 6 years

(Rate was 62% female; 56% Male)

NCES report, May 2015 (Class of 2002 and when they reached educational attainment).

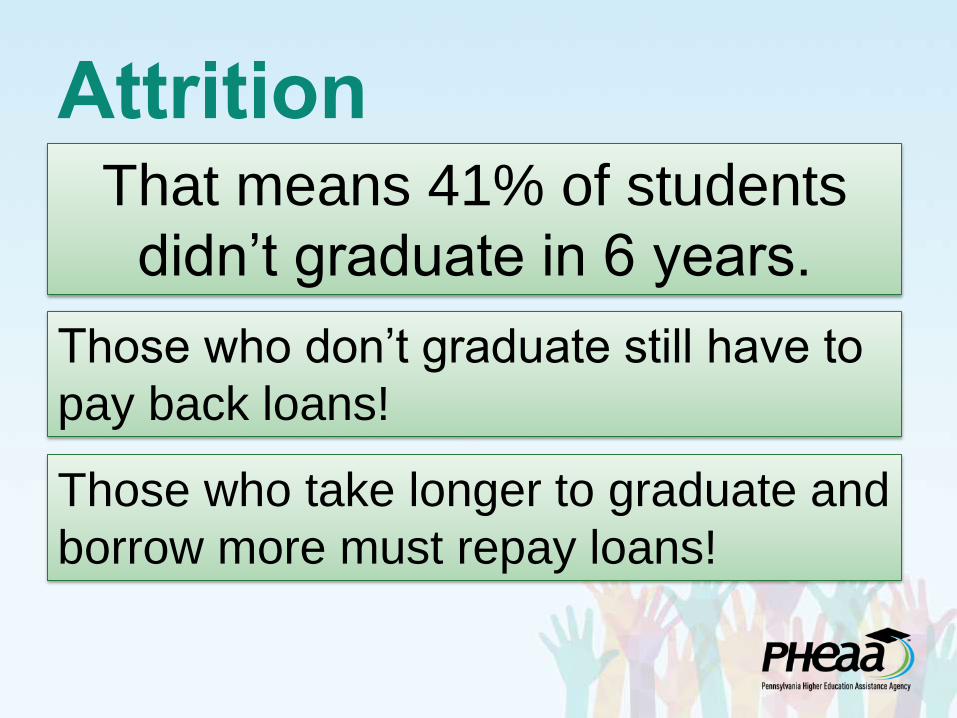

Attrition • Please right click and duplicate slide. That means 41% of students

didn’t graduate in 6 years.

Those who don’t graduate still have to

pay back loans!

Those who take longer to graduate and

borrow more must repay loans!

Source: Postsecondary Analytics, How Full-Time are “Full-Time” Students? Prepared for Complete College America, October 2013.

Most students

are NOT taking

the credits

needed to

graduate

on time

RETURN ON INVESTMENT

Affordability

Affordability/ROI for Students

• Are there going to be jobs in your field upon

graduation?

• What do those jobs pay to start?

• How much will you have to borrow for your

education?

• Do you have an open mind about your

education?

• Have you researched costs, what your

financial aid might look like, and had

discussions with your parents?

MySmartBorrowing.org

An interactive, online tool

created by PHEAA that helps

students and families:

• Estimate career salaries &

college tuition

• View the impact of savings

on overall cost

• Calculate loan repayment

• Avoid overborrowing

MySmartBorrowing.org

The Financial Aid Process

www.fafsa.gov Create your

FSA ID prior to

completing your

FAFSA. *You and your parents

need an FSA ID

Start a New

FAFSA or Log in

as a returning

user.

**File your

FAFSA every

year you will

attend

postsecondary

education.

Whose information

goes on the FAFSA? • Divorced or separated parents - the parent

that provides more than 50% of students

support (household)

• Stepparents – yes

• Adoptive parents - yes

• Grandparents – no

• Foster parents - no

• Legal guardians - no

• Anyone else the student is living with - no

Independent Students are: • 24 or older on Jan 1st of award year

(this year before 1993) • Veteran (includes active duty

personnel) • Working on graduate degree • Emancipated minor in legal

guardianship • Orphan, in foster care, or ward of

the court at anytime when student was age 13 or older

• Have legal dependents other than spouse

• Student deemed homeless by proper authority

State Grant Form

Click on Start

Your State

Application

from your

FAFSA

Confirmation

Page.

Links to

pheaa.org.

Know your deadlines! Know all of your state and school/college

deadlines and file the FAFSA by the

earliest date!

• School Priority Filing Dates – vary by school

• PA State Grant Deadlines –

◦ May 1, 2016 - First Time and Renewal Applicants that plan to enroll in a degree program or a college transferable program at a junior college or other college or university

◦ August 1, 2016 - First Time applicants that plan to enroll in a community college; a business, trade, or technical school; a hospital school of nursing; or a 2-year program that is not transferable to another institution

Expected Family Contribution

(EFC)

How is the EFC Calculated?

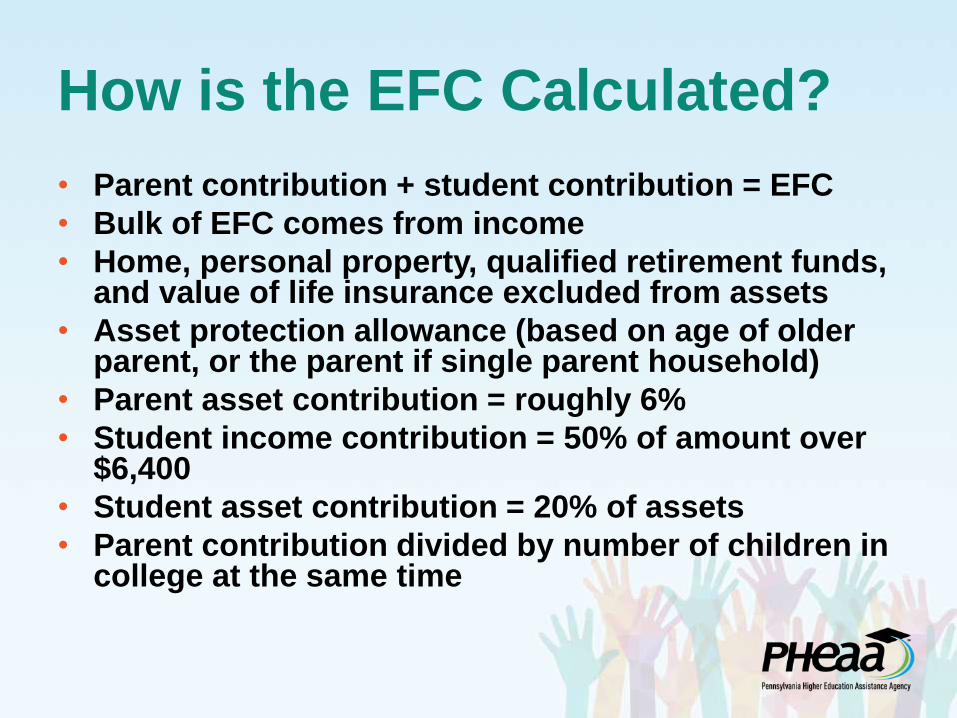

• Parent contribution + student contribution = EFC

• Bulk of EFC comes from income

• Home, personal property, qualified retirement funds, and value of life insurance excluded from assets

• Asset protection allowance (based on age of older parent, or the parent if single parent household)

• Parent asset contribution = roughly 6%

• Student income contribution = 50% of amount over $6,400

• Student asset contribution = 20% of assets

• Parent contribution divided by number of children in college at the same time

Financial Aid Award Letter –

Calculating Need Schools/colleges receive financial aid information and calculate financial need.

School cost……………………. $30,000

EFC…………………………….. - $ 3,000

Financial need………………… $27,000

FAO “packages” student based on financial need and available funding (varies from school to school).

Financial aid award letter sent to student.

Sorting it all out….

How much is

gift aid? – I

don’t have to

pay it back.

How much is

self-help aid? –

I will have to

pay it back or

earn it.

What are the

total costs and

how much will I

owe the

school?

Review and consider all of your

options! Sometimes it’s not

always your first choice!

What is Available?

Federal Programs

• Pell Grant (2015-16 max award $5775)

» *….must have high need

• Campus-based aid (amounts determined by FAO)

» FSEOG………………… up to $4000

» Federal work-study…… FAO determines

• For most programs, student must be enrolled at least half-time.

Federal Programs

• TEACH (must meet teaching commitment)

• Iraq and Afghanistan Service Grant

• Americorps (for details, go to www.americorps.gov)

PA State Grant Program

• PA State Grant*

» Full-time, in PA…...….up to $4,348

» Part time, in PA………up to $2,174

• Out of state….. Up to $600 in DE, MA, OH, VT, WV, and

DC

*Amount determined in part by the cost of the school and the student must

be attending school at least half-time to be eligible

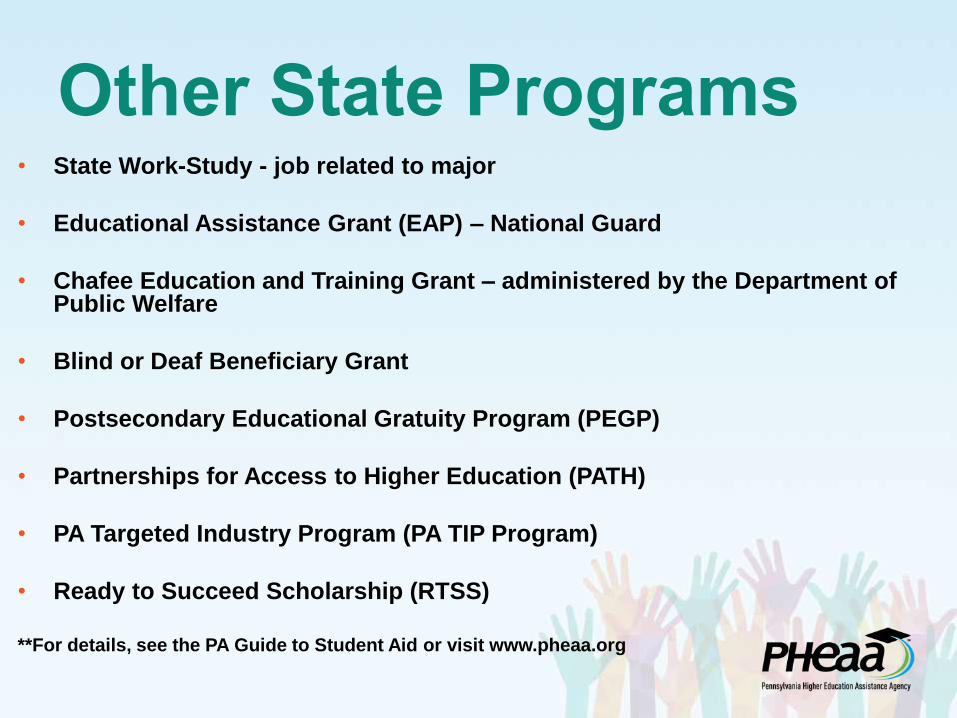

Other State Programs • State Work-Study - job related to major

• Educational Assistance Grant (EAP) – National Guard

• Chafee Education and Training Grant – administered by the Department of Public Welfare

• Blind or Deaf Beneficiary Grant

• Postsecondary Educational Gratuity Program (PEGP)

• Partnerships for Access to Higher Education (PATH)

• PA Targeted Industry Program (PA TIP Program)

• Ready to Succeed Scholarship (RTSS)

**For details, see the PA Guide to Student Aid or visit www.pheaa.org

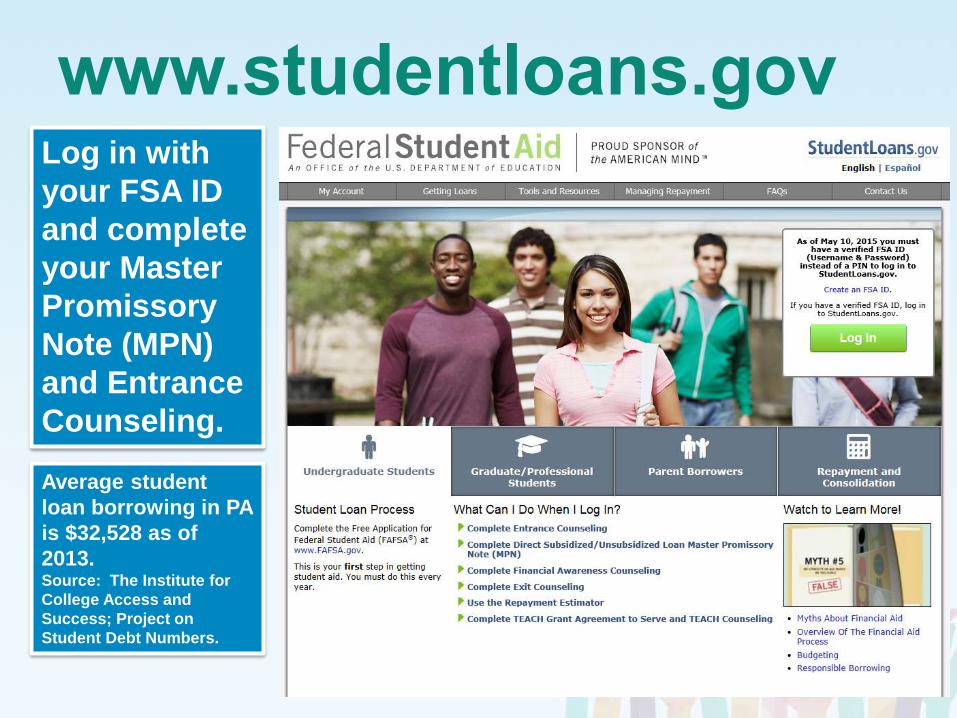

www.studentloans.gov Log in with

your FSA ID

and complete

your Master

Promissory

Note (MPN)

and Entrance

Counseling.

Average student

loan borrowing in PA

is $32,528 as of

2013. Source: The Institute for

College Access and

Success; Project on

Student Debt Numbers.

Federal Direct Loan Program

• Stafford Student Loans » Subsidized – no interest while in school

◦ Interest will be charged after an interest-free, 6-month-grace period

◦ 4.29% fixed rate for loans between 7/1/15 and 6/30/16

◦ 1.068% origination fee deducted at disbursement

» Unsubsidized – interest accrues in school and grace

◦ 4.29% fixed rate for loans between 7/1/15 and 6/30/16

◦ 1.068% origination fee deducted at disbursement

» Gross loan amount of $5500 will be $5441.26

Calculating Accrued Interest To calculate your daily interest accrual, use the following formula:

• Interest rate x current principal balance ÷ number of days in the year = daily interest

Example:

Sara Student has a $2,000 current principal balance and 4.29% interest rate this year. Using the formula:

• .0429 x $2,000 ÷ 365 = $0.24 (~$21.60 quarterly interest)

What if she borrowed $10,000?

• .0429 x $10,000 ÷ 365 = $1.18 daily (~$106 quarterly interest)

Loan Servicer (just some of the companies you might be repaying)

myfedloan.org

navient.com

mygreatlakes.org

nelnet.com

Loan Borrowing Limits

Additional Eligibility

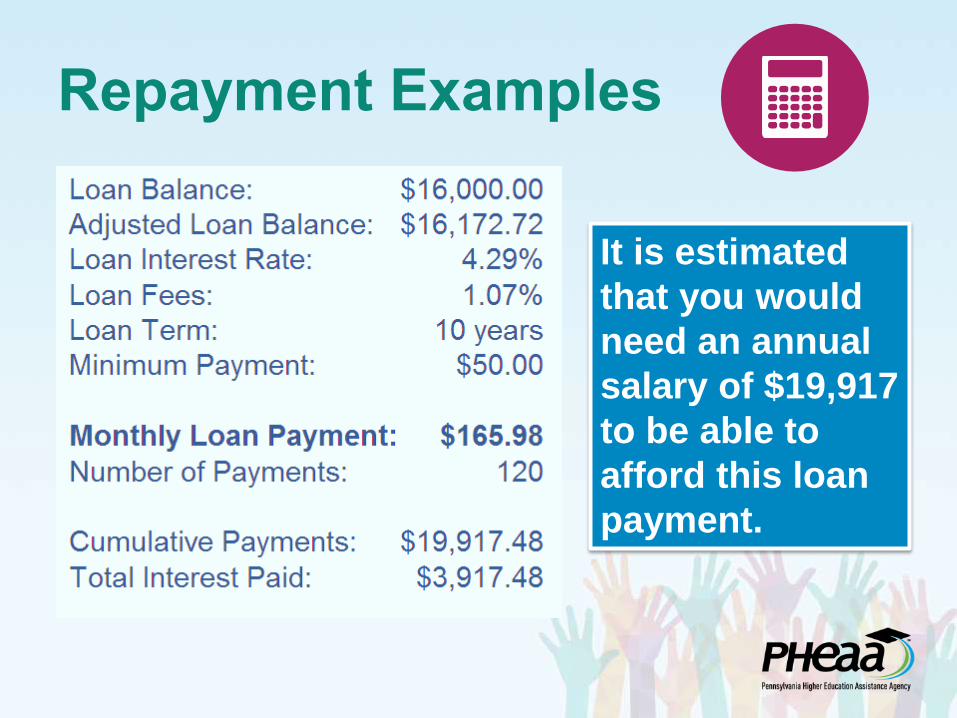

Repayment Examples

It is estimated

that you would

need an annual

salary of $37,345

to be able to

afford this loan

payment.

Repayment Examples

It is estimated

that you would

need an annual

salary of $19,917

to be able to

afford this loan

payment.

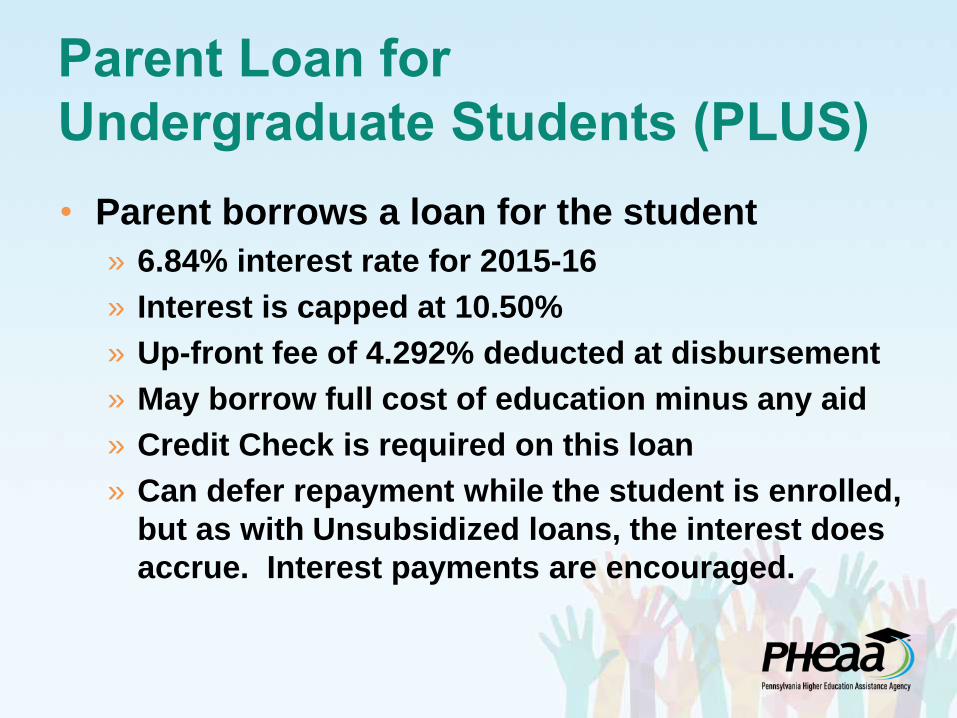

Parent Loan for

Undergraduate Students (PLUS)

• Parent borrows a loan for the student

» 6.84% interest rate for 2015-16

» Interest is capped at 10.50%

» Up-front fee of 4.292% deducted at disbursement

» May borrow full cost of education minus any aid

» Credit Check is required on this loan

» Can defer repayment while the student is enrolled,

but as with Unsubsidized loans, the interest does

accrue. Interest payments are encouraged.

Alternative/

Private Education Loans

• Nonfederal loans, made by a lender such

as a bank, credit union, state agency, or a

school.

• Student borrows in his or her own name.

• Based on credit scoring and debt-to-income ratio.

• Fees, interest rates, loan amounts, and repayment

provisions vary by lender and are generally higher than

federal student loans.

• Co-signers usually required. Some loan products

have a co-signer release option.

• Compare loans before making choice and read the fine

print!

Borrowing for Higher Education

Direct Stafford Loans

PLUS Loans

Alternative/Private Loans

What’s Next?

THE BIG PICTURE

Thinking about…

How much will I have to borrow for school?

What do I want the rest of my life to look like? What do I want to have? How do my decisions now affect my vision for my future?

Will there be jobs

available in my

chosen field?

Will I be able to afford my monthly loan payments?

Does a cheaper option make sense if my family is struggling to pay?

Determining Affordability • Approach this as though you are not buying a

school, you are buying an EDUCATION.

• Apply everywhere, but look at sticker price!!

Tuition costs in PA range from $3000 to more

than $40,000…PLUS room and board!

• Be open minded and diverse in college

searches.

• Think in terms of yesterday’s money, today’s

money, and tomorrow’s money.

• Have discussions as a family!

HOPE IS NOT A STRATEGY

Ben offers these suggestions for paying your bill:

• Can you pay anything out-of-pocket? • Does family have expendable income

each month to sign up for a payment plan?

• Has the student applied for as many scholarships as you could? (Check with guidance office, the school you’ll be attending, or do an online search).

• Can parents borrow (are they willing to borrow) or cosign a loan? (*parents can also look at a home-equity line of credit)

• Double check with the school to see if there is anything else they can offer you (additional institutional money, scholarship opportunities, institutional loans).

Scholarship search:

• Start early – and KEEP LOOKING

• Don’t forget to continue studies!

• GOOGLE your interests

• Don’t PAY for information

• Criteria varies by school

» If you’re asked to pay, it’s not free money - (SCAM)

• Don’t disqualify yourself until IT disqualifies YOU

• Don’t fear ESSAYS

• Provide what is asked

• Small scholarships ADD UP

• Activities, Athletics, Family, Hobbies, Participation,

Attributes – DO YOUR RESEARCH

• Don’t miss DEADLINES

• Write it down!

FastWeb.com

EducationPlanner.org

Chegg.com

FinAid.org

Scholarships.com

Scholarship-Page.com

DoSomething.org/Scholarships

Colleges.Niche.com

StudentScholarships.org

BigFuture.Collegeboard.org

MeritAid.com

Pittsburghfoundation.org

Google “unusual scholarships”

Don’t miss out on FREE Money!

WAYS TO SAVE Now make this AFFORDABLE!

Commute!

Plan ahead to graduate on-time!

Buy used text books, rent them or go online to find them cheaper!

RAs

ROTC

Ask about a cheaper meal plan.

Beware of the

5 or 6 year plans! • 5th year will cost 20-25% more than

your first year!

• Loss of institutional funds after 4 years.

• Loss of State Grant eligibility after 4

years.

• You will run out of federal loan

eligibility (capped at $31,000 for

undergraduate students)

What should you do now?

Complete a practice FAFSA on the

FAFSA4Caster on FAFSA.gov to see if

you might qualify for grants.

Apply for scholarships!

Visit mysmartborrowing.org to start

budget planning for each school choice.

Retake SATs or ACTs.

Apply for FSA IDs.

Special Circumstances

Recent death or disability

Reduced income

Recent separation or divorce

Contact the school and

ask for a special

consideration AND

contact State Grant

Division at PHEAA

Resources • PHEAA toll free: 1-800-692-7392

• Federal Student Aid Info Center – 1-800-433-3243

• www.pheaa.org – Account Access

• www.EducationPlanner.org

• www.MySmartBorrowing.org

• www.youcandealwithit.com

• www.fafsa.gov

• www.studentaid.ed.gov – general financial aid info » Check out their Facebook page

• www.studentloans.gov – information on federal loans

• www.nslds.ed.gov - information on your specific loans

Presenter Contact Info

Kim McCurdy Higher Education Access Partner

PHEAA

724.734.8550

QUESTIONS?