Embed Size (px)

DESCRIPTION

Citation preview

Demonstrating Transparency: An Update on Dunlap School District Finances!

Goal 5 of the District strategic plan reads “To obtain efficient, effective, and equitable use of resources.” Over the next several blog posts, an update on the financial status of the District will be provided to stakeholders. The goal is to provide effective communication regarding district finances and ensure transparency to our stakeholders. Blog topics will include:

Part 1 - School Finance 101

Part 2 - The Budget Process

Part 3 - Revenues

Part 4 - Equalized Assessed Valuation and Tax Rate

Part 5 - Expenses

Part 6 - The 2011-12 Budget

Part 7- Money Spent on Education & Return on Investment

Part 8 - Question/Answer

While Dunlap Schools can’t predict or control every aspect of local, state or national financial conditions, we believe we can keep our stakeholders informed while being proactive on property tax matters, enrollment projections, state funding, and other factors that affect our school district finances. We look forward to sharing information regarding Dunlap School District finances! The next post is titled “School Finance 101”.

Part 1- School Finance 101

School funding and budgets are unique and different from other businesses and home budgets. By law there are nine funds which each school must establish and maintain. For each of the nine funds, there is a revenue AND an expenditure budget.

The nine funds are:

Fund 10 – Education Fund: This is effectively the district’s general fund. Every transaction not accommodated by another specific fund (below) is processed through this fund.

Fund 20 – Building Fund: This fund is required if a tax is levied for the purpose of operations and maintenance of buildings and grounds.

Fund 30 – Debt Service Fund: This fund is required if taxes are levied to retire bond principal or to pay bond interest.

Fund 40 – Transportation Fund: This fund is required if a district pays for transporting pupils for any purpose. All costs of transportation, other than those authorized by statute to be paid from another fund, are paid from this fund.

Fund 50 – IMRF/SS Fund: This fund is required if a tax is levied to pay for contributions to municipal retirement systems (IMRF), Social Security, or Medicare, (for non-teacher employees not covered by the Teachers Retirement System.)

Fund 60 – Site and Construction Fund: This fund is required to account for proceeds resulting from each bond issue and/or receipts from other long term financing agreements used to finance a capital project.

Fund 70 – Working Cash: This fund is required if a tax is levied or bonds are issued for working cash purposes.

Fund 80 – Tort Fund: This fund is required if taxes are levied or bonds are sold for tort immunity or tort judgment purposes.

Fund 90 – Health Life Safety Fund: This fund is required if a tax is levied or bonds are issued for purposes of fire prevention, safety, energy conservation, or school security.

Each fund has a specific purpose and only identified and allowable revenues and expenses may be accounted for within each fund. For example, anything dealing with buses MUST be paid for from Fund 40 – Transportation Fund, which includes salaries, benefits, fuel, bus maintenance and the purchase of new busses.

Similarly, all items associated with the operations of the school MUST be paid for from Fund 10 – Education Fund. This includes administrator, teacher, teacher aides, clerical, custodial, cafeteria, and playground supervisor salaries and benefits as well as classroom supplies, equipment, and technology. As with most districts, salary and benefits account for approximately 82% of the total Education Fund expense budget in Dunlap School District.

By law each district must be audited, annually, by a certified school auditor annually. Historically, Dunlap School District has received excellent audits indicating “no significant findings.”

Additionally, the Illinois State Board of Education (ISBE) assesses the financial health of each school district in the state to gain a better understanding of where each school ranks in comparison to other schools across the State. (View Dunlap’s financial profile online).

There are five indicators which contribute to the final overall score:

1. Fund Balance to Revenue Ratio 2. Expenditure to Revenue Ratio 3. Days Cash on Hand 4. Percent of Short-Term Borrowing Maximum Remaining 5. Percent of Long-term Debt Margin Remaining

Dunlap Community Unit School District #323 has scored a 3.90 / 4.00, or Financial Recognition (view page 21). This designation represents the highest category of financial strength.

In the next blog post, we’ll discuss the budget process.

Part 2 – The Budget Process

The budget cycle for schools is not as straight forward as one would hope. It is a year-long, complex process and begins before the current year is less than half over. For example, here is how the FY 12 (July 1, 2011 – June 30, 2012) budget is developed:

1. Beginning in October/November, 2010 work on the tax levy begins. The tax levy amount is a component of the formula which is used to determine the amount of funds the district will receive from property taxes for the 2011-2012 school year. For this year the Board determined the levy amount (currently $4.17). For more information on property taxes and the tax levy, read this article titled “Property taxes 101: Taking the mystery out of the process.”

2. Simultaneously, the Director of Finance talks with the Peoria County Clerk to determine the EAV (Equalized Assessed Value) of property within the district. View the document titled “Illinois Property Tax System” to learn more about how property taxes are calculated.

3. In November, 2010 the Board held a “Truth in Taxation Hearing”. Any time the district “asks” for more than 5% of the previous year’s levy, a public hearing must be held. Read more about “Truth in Taxation.”

4. Before the last Tuesday in December, 2010 the “Certificate of Levy” must be delivered to the Peoria County Courthouse and the Regional Office of Education. This is a requirement through State Statute. Learn more about the “Certificate of Levy.”

5. Concurrently, the administration and Board begin working on the actual budget – entering new salaries, benefit costs, make making necessary changes to supply and equipment lines, etc. Learn more by reading a document titled “Mechanics of a School District Budget” published by the Illinois State Board of Education.

6. This process is on-going throughout the spring. As more information becomes available – actual amounts received from property taxes, information from the State regarding payments, etc – the Tentative Budget is updated. Learn more about the tentative budget process “Mechanics of a School District Budget” page 5.

7. In May, 2011 the Board approves the Tentative Budget for FY 12. Board approval allows the administration to begin working and preparing for the next school year – allocating funds as necessary.

8. By September 30, 2011 the Board must approve the FINAL FY 12 Budget. Learn more about the FINAL budget process “Mechanics of a School District Budget” page 38.

9. By October 30, 2011 the budget must be filed with the Illinois State Board of Education utilizing their budget format. The FY 12 budget must then be available on the District web site. Learn more about posting the budget on the District website “Mechanics of a School District Budget” page 6. View the Dunlap 2010-11 budget on our web site.

10. Beginning in October/November, 2011 the process starts over for the next fiscal year.

The next blog post will discuss District revenue.

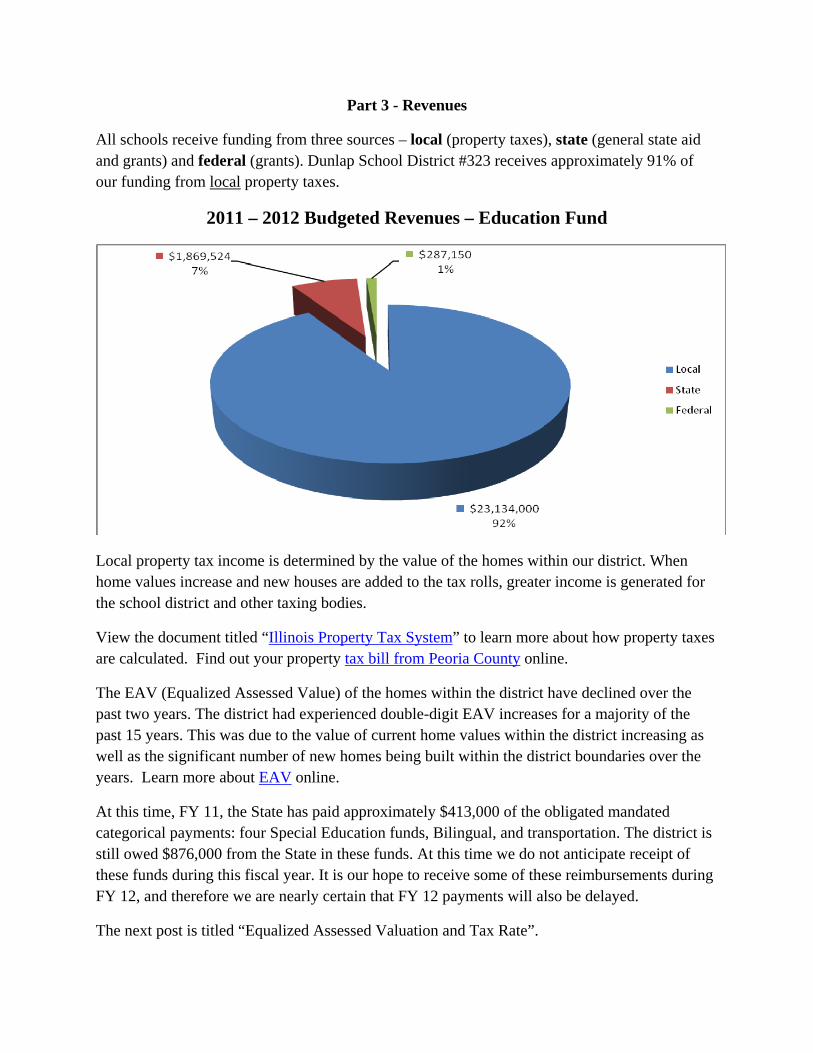

Part 3 - Revenues

All schools receive funding from three sources – local (property taxes), state (general state aid and grants) and federal (grants). Dunlap School District #323 receives approximately 91% of our funding from local property taxes.

2011 – 2012 Budgeted Revenues – Education Fund

Local property tax income is determined by the value of the homes within our district. When home values increase and new houses are added to the tax rolls, greater income is generated for the school district and other taxing bodies.

View the document titled “Illinois Property Tax System” to learn more about how property taxes are calculated. Find out your property tax bill from Peoria County online.

The EAV (Equalized Assessed Value) of the homes within the district have declined over the past two years. The district had experienced double-digit EAV increases for a majority of the past 15 years. This was due to the value of current home values within the district increasing as well as the significant number of new homes being built within the district boundaries over the years. Learn more about EAV online.

At this time, FY 11, the State has paid approximately $413,000 of the obligated mandated categorical payments: four Special Education funds, Bilingual, and transportation. The district is still owed $876,000 from the State in these funds. At this time we do not anticipate receipt of these funds during this fiscal year. It is our hope to receive some of these reimbursements during FY 12, and therefore we are nearly certain that FY 12 payments will also be delayed.

The next post is titled “Equalized Assessed Valuation and Tax Rate”.

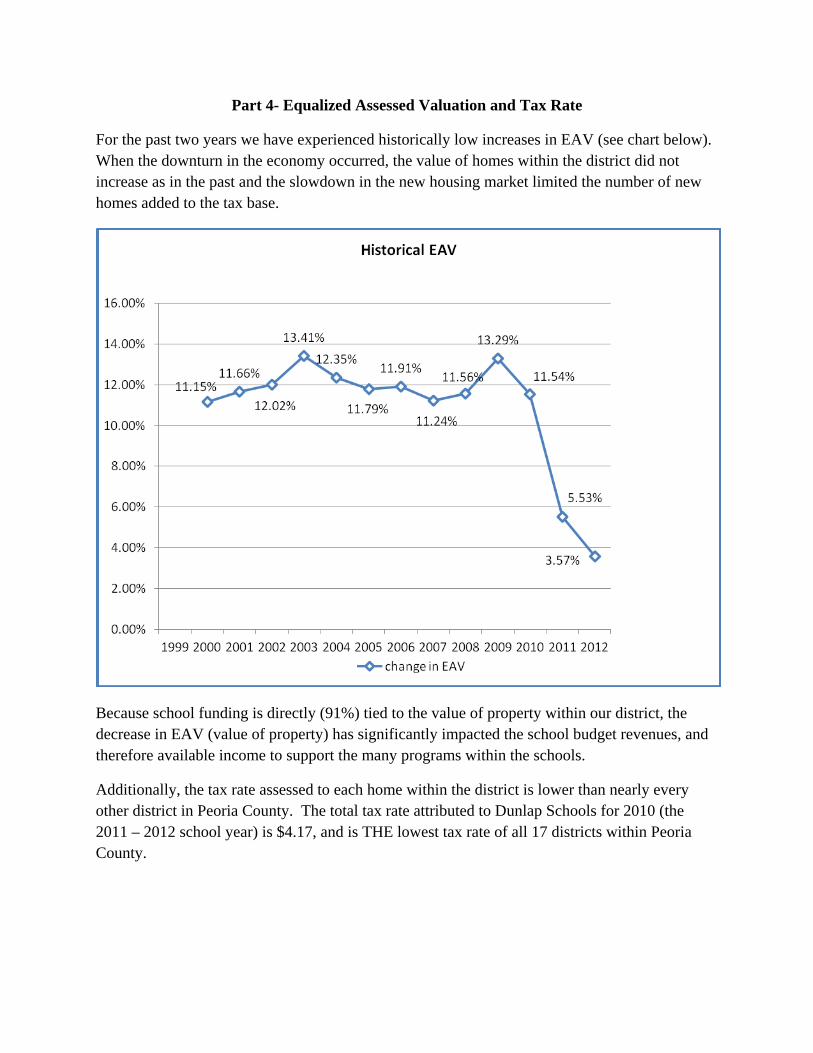

Part 4- Equalized Assessed Valuation and Tax Rate

For the past two years we have experienced historically low increases in EAV (see chart below). When the downturn in the economy occurred, the value of homes within the district did not increase as in the past and the slowdown in the new housing market limited the number of new homes added to the tax base.

Because school funding is directly (91%) tied to the value of property within our district, the decrease in EAV (value of property) has significantly impacted the school budget revenues, and therefore available income to support the many programs within the schools.

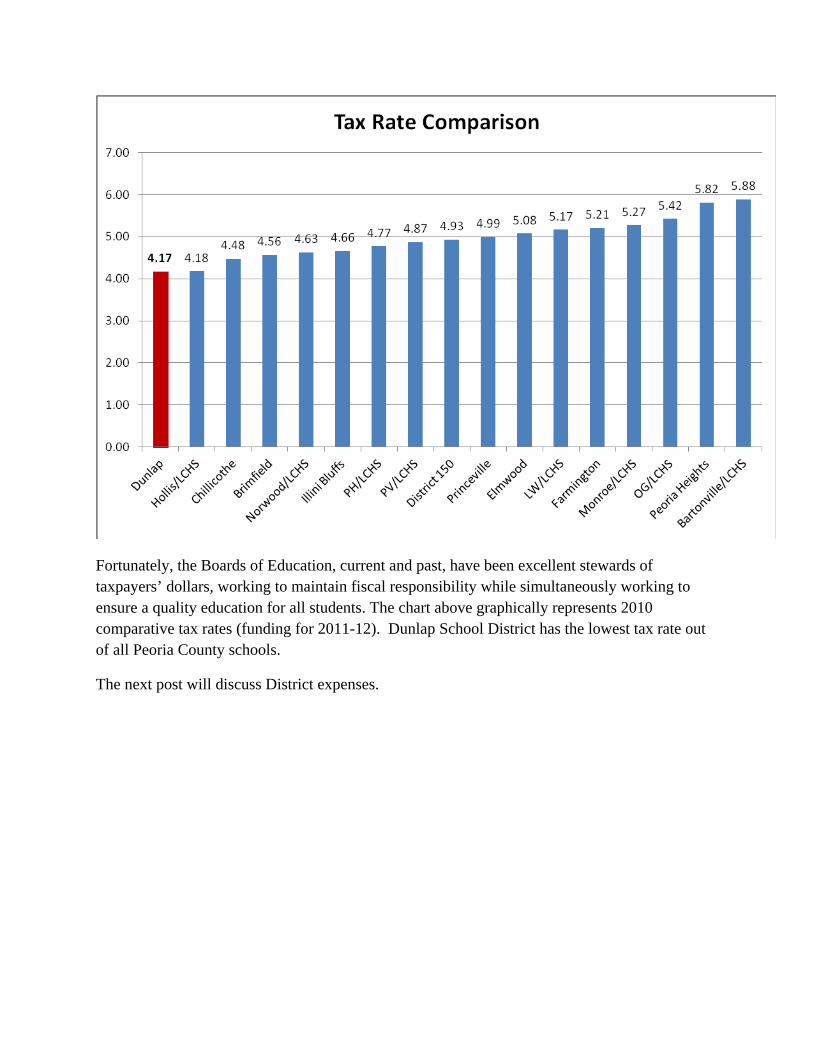

Additionally, the tax rate assessed to each home within the district is lower than nearly every other district in Peoria County. The total tax rate attributed to Dunlap Schools for 2010 (the 2011 – 2012 school year) is $4.17, and is THE lowest tax rate of all 17 districts within Peoria County.

Fortunately, the Boards of Education, current and past, have been excellent stewards of taxpayers’ dollars, working to maintain fiscal responsibility while simultaneously working to ensure a quality education for all students. The chart above graphically represents 2010 comparative tax rates (funding for 2011-12). Dunlap School District has the lowest tax rate out of all Peoria County schools.

The next post will discuss District expenses.

Part 5 - Expenses

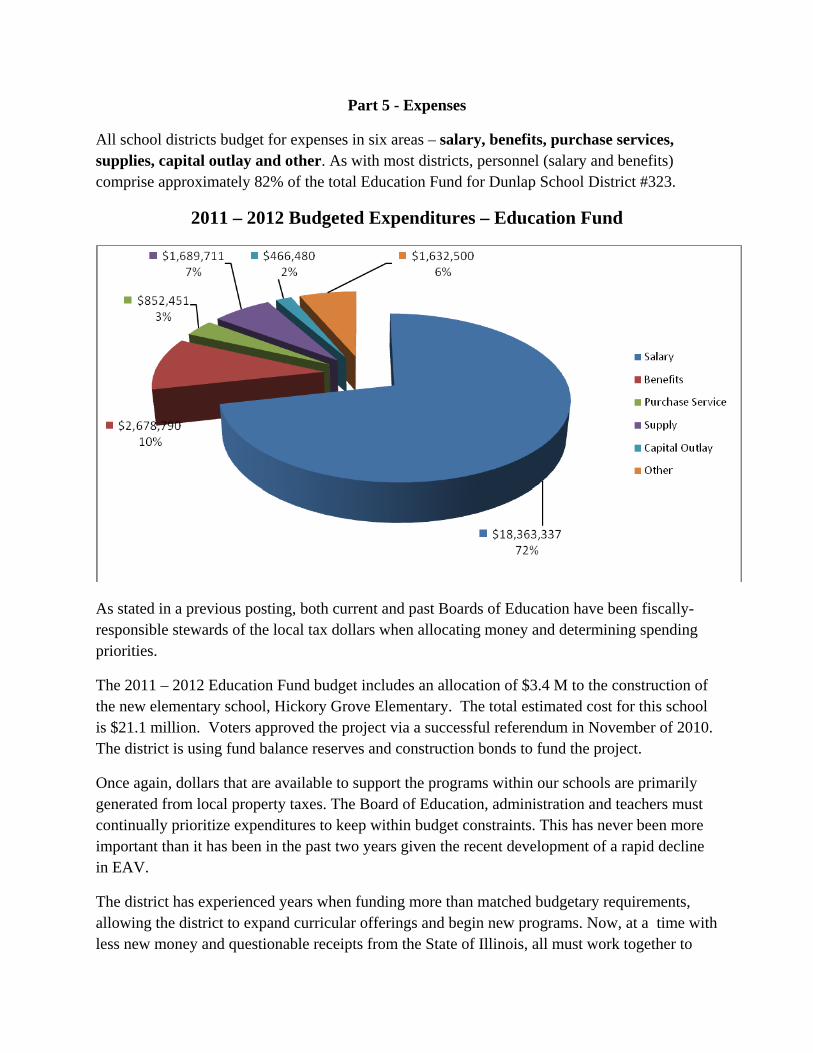

All school districts budget for expenses in six areas – salary, benefits, purchase services, supplies, capital outlay and other. As with most districts, personnel (salary and benefits) comprise approximately 82% of the total Education Fund for Dunlap School District #323.

2011 – 2012 Budgeted Expenditures – Education Fund

As stated in a previous posting, both current and past Boards of Education have been fiscally-responsible stewards of the local tax dollars when allocating money and determining spending priorities.

The 2011 – 2012 Education Fund budget includes an allocation of $3.4 M to the construction of the new elementary school, Hickory Grove Elementary. The total estimated cost for this school is $21.1 million. Voters approved the project via a successful referendum in November of 2010. The district is using fund balance reserves and construction bonds to fund the project.

Once again, dollars that are available to support the programs within our schools are primarily generated from local property taxes. The Board of Education, administration and teachers must continually prioritize expenditures to keep within budget constraints. This has never been more important than it has been in the past two years given the recent development of a rapid decline in EAV.

The district has experienced years when funding more than matched budgetary requirements, allowing the district to expand curricular offerings and begin new programs. Now, at a time with less new money and questionable receipts from the State of Illinois, all must work together to

prioritize which programs should continue and which may need to be scaled back or eliminated, allowing the district to continue to maintain sufficient fund balances.

The next post will provide information about the 2011-12 budget.

Part 6 – The 2011-12 Budget

On May 11, 2011 the Board of Education approved the FY 12 Tentative Budget. That budget, which will not be finalized until September, accounts for the construction of the new Hickory Grove Elementary School as well as athletic field/facility upgrades at DHS/DMS/DVMS.

At this time it is anticipated that the Education Fund will contribute approximately $3.4 million towards the construction of Hickory Grove. As a reminder, we are building a new elementary for $21.5 M. Funding for this building will come from three sources: an approved referendum in the amount of $11.5 M, proceeds from a previous bond issue totaling $6.7 M and $3.4 M transferred from the Education Fund reserves.

This transfer notwithstanding, the Education budget is a “deficit” budget. The budgeted amount of revenue minus the budgeted expenses totals approximately negative $3.8 M. Of that deficit, $3.4M is for construction of the new elementary school and approximately $400,000 is for operational expenses in the Education Fund Budget.

As stated in a previous post, the district receives approximately 91% of its revenue from LOCAL sources – property taxes. The State of Illinois funds about 8% - general state aide, grants, etc, and the Federal Government funds only 1%. Simultaneously, the district is currently experiencing historically low increases in EAV (Equalized Assessed Valuation) while the State of Illinois is also delinquent in making payments. Because the EAV is not increasing at the same pace (or more) as expenses, the Education Fund is budgeted to have higher expenses than revenues.

To help bridge this gap the administration and Board have approved some reductions within the budget. For example, supply budget lines for nearly every department were cut by 10%, including science, music and athletics to name a few.

This year the Education Fund Expense Budget, without the $3.4 M for construction of the new elementary school, is $25,464,024. At the recommendation of the district auditor the Board of Education has made it a goal to have six months reserve in savings at any one time. This allows the district to more effectively weather the financial high/lows – dropping property values, late payments from the State, etc. Because previous Boards of Education have been excellent stewards of district dollars, we are able to “weather this financial storm” by utilizing current reserve funds while simultaneously maintaining the six months of reserves, as recommended by our auditor.

As with home budgets in which individuals save and plan for the future, the District is no different. The District Treasurer works with four different financial institutions to ensure all district (reserve) funds are invested at levels to maximize the return on investment, while maintaining the safety of the principal.

As we prepare to open a new school, which will require additional staff, it is the intention of the administration to keep a watchful eye on all “new” expenses and to evaluate all requests to ensure that all programs and purchases align with the mission of the Dunlap Community Unit School District – “To empower all students to excel in a global society.” In short, the District is willing to accept a small deficit budget for a short time, but will not operate a deficit budget as a common practice.

The next post will provide information about money spent on education and return on investment.

Part 7- Money Spent on Education & Return on Investment

In a recent blog posting titled “Dunlap Schools’ Nationally Recognized as a Great Return on Investment”, we shared that our District ranks toward the top of the list when comparing expenditures to academic achievement. In a study by the Center for American Progress, Dunlap School District was ranked among the highest in the State of Illinois when it comes to educational productivity.

Productivity is described as the amount of learning a district produces for every dollar spent, after controlling for factors such as cost of living and students in poverty. An interactive map is available to learn more about the rankings and methodology- http://www.americanprogress.org/issues/2011/01/educational_productivity/ .

Dunlap’s “Operating Expense Per Pupil” is the gross operating cost of the district (except summer school, adult education, bond principal retired, and capital expenditures) divided by the nine-month average daily attendance (ADA) for the regular school term. The following data (chart below) is based on the 2008-09 Annual Finance Report (AFR) and shows “cost per pupil” comparative data.

In short, the Dunlap Schools District spends comparatively less per student while obtaining comparatively better academic achievement results. Thus, the Dunlap Schools District provides a good return on investment!

The next post will provide questions and answers to clarify the financial state of the District.

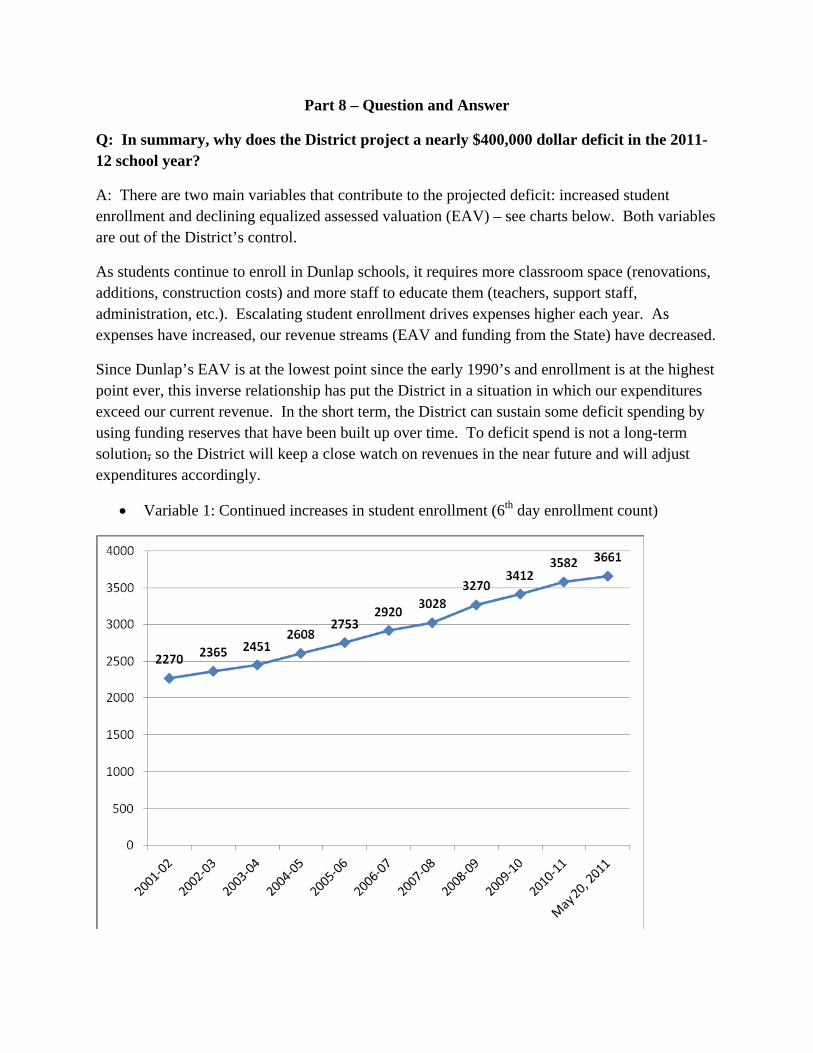

Part 8 – Question and Answer

Q: In summary, why does the District project a nearly $400,000 dollar deficit in the 2011-12 school year?

A: There are two main variables that contribute to the projected deficit: increased student enrollment and declining equalized assessed valuation (EAV) – see charts below. Both variables are out of the District’s control.

As students continue to enroll in Dunlap schools, it requires more classroom space (renovations, additions, construction costs) and more staff to educate them (teachers, support staff, administration, etc.). Escalating student enrollment drives expenses higher each year. As expenses have increased, our revenue streams (EAV and funding from the State) have decreased.

Since Dunlap’s EAV is at the lowest point since the early 1990’s and enrollment is at the highest point ever, this inverse relationship has put the District in a situation in which our expenditures exceed our current revenue. In the short term, the District can sustain some deficit spending by using funding reserves that have been built up over time. To deficit spend is not a long-term solution, so the District will keep a close watch on revenues in the near future and will adjust expenditures accordingly.

Variable 1: Continued increases in student enrollment (6th day enrollment count)

Variable 2: Continued decreases in revenue (declining Equalized Assessed Valuation and declining revenue from the State of Illinois).

Q: If the district is projecting a deficit budget for FY 12, why has the administration and Board of Education approved a new elementary school and athletic/facility upgrades.

A: The student enrollment within our schools continues to increase. Class size in most classrooms is at, or above, what we would consider optimal. Additionally, our art and music instructors at the elementary level are on a “cart” rather than having their own classroom. This limits the amount of instructional time in these areas as well as the types of instruction. Without a new elementary school the district would be forced to consider adding “trailers” to each building in an effort to add classroom space.

Regarding the athletic updates at DHS/DMS/DVMS, many of our athletic areas are in need of immediate attention. For example, the current soccer field is not regulation size, therefore we are unable to host an IHSA regional or sectional match. We were required to move the tennis courts to make room for additions at the High School. These are just a few examples of the projects to be completed this summer and the rationale behind the decision to move forward with all renovations.

Q: What happens if EAV remains at the current level or decreases even further?

A: If the EAV remains at, or below, its current level, it is anticipated that the district will continue to see a “deficit” budget in the Education Fund. There is no way to keep the budget in balance while simultaneously maintaining many of the programs which have become key to the success within each of our buildings.

Q: How does our tax rate compare to other school districts in the area? How does this relate to the “value of an education in Dunlap?”

A: In a previous post it was highlighted that the tax rate assessed to each home within the District is the lowest tax rate of all 17 districts within Peoria County. In fact, with the exception of Hollis District in the Limestone area, the next closest tax rate is IVC and it is $0.30 higher per $100 of assessed valuation.

At the lowest extreme, Dunlap is at $4.17 compared to the highest, is Bartonville/LCHS, at $5.88. Recall from an earlier post that Dunlap spends $6,353 per pupil, the lowest in the area. With this in mind, all members of the Dunlap community should be confident that their tax dollars are being utilized in the most efficient manner possible while simultaneously guaranteeing a quality education for all children.

![[Secs 16.1 Dunlap] Conservation Laws - II [Secs 2.2, 2.3, 16.4, 16.5 Dunlap]](https://img.pdfslide.net/doc/110x75/5697c0101a28abf838ccacf3/secs-161-dunlap-conservation-laws-ii-secs-22-23-164-165-dunlap.jpg)

![[Secs 16.1 Dunlap]](https://img.pdfslide.net/doc/110x75/56812bd4550346895d9036ea/secs-161-dunlap.jpg)