Embed Size (px)

Citation preview

Module 5:

Interest Rate Risk Management

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means–electronic, mechanical, photocopying, recording or otherwise–without prior

permission of the Egyptian Banking Institute.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-2

Table of Contents

Module 5: Interest Rate Risk Management

Introduction ................................................................................................................................ 3 Learning objectives ................................................................................................................ 3

The Meaning of Interest Rate Risk ............................................................................................ 4 Sources of Interest Rate Risk ..................................................................................................... 5 Effects of Interest Rate Risk ...................................................................................................... 6

Forecasting Interest Rate Moves: An elementary approach ...................................................... 7 Monetary Policy: the tradeoff between inflation and growth targeting ................................. 7 CBE’s Monetary Policy Committee (MPC) .......................................................................... 7 In Practice .............................................................................................................................. 7

First – Interest Rate Risk Measurement Techniques ................................................................. 8 Repricing Gap Analysis ......................................................................................................... 8 Duration ............................................................................................................................... 11 Simulation approaches ......................................................................................................... 12

Second – Management of interest rate risk .............................................................................. 13 Third: Banking (Fixed Income) Investment Portfolio ............................................................ 14

Nature ................................................................................................................................... 14 Components and accounting treatment ................................................................................ 14

The role in ALM .................................................................................................................. 14 Exercises .................................................................................................................................. 16

Simulation Approaches ........................................................................................................ 16 Duration ............................................................................................................................... 16

Summary .................................................................................................................................. 17

Not

For

Rel

ease

Participant Guide

DD08-V3 5-3

Asset and Liability Management – Introduction

Module 5: Interest Rate Risk Management

Introduction Building on Basel Committee recommendations and CBE directives, this session introduces

the second risk associated with ALM function, which is the interest rate risk. It starts with

defining and explaining the meaning of interest rate risk to present a general vision of this

source of risk and the importance of forecasting the course of interest rates, and then the

sources and effects of interest rate risk will be identified because following these sources later

will help to manage and control the interest rate risk.

How to use gap analysis as a basic method to measure the bank exposure toward interest rate

risk will be the next point to cover. Duration and how to use duration to measure the interest

rate risk will be explained.

This session will also include a comparison between static and dynamic gap analysis

mechanisms. Finally, the banking investment portfolio will be introduced.

Importance

The assets and liabilities management requires taking the utmost care with the interest rate

applied for both funding and lending products. So this session is concerned with the interest

rate risk management as an integral part of ALM function.

Overview

Based the on the previous introduction, this session will present and discuss the following

points:

The meaning, sources, and effects of interest rate risk

A general framework for interest rate risk management

Using the Gap and Duration analysis to evaluate bank exposure to interest rate risk

The difference between static vs. dynamic simulation approaches

How bankers forecast and plan for interest rate movements

Learning objectives

Upon the completion of this module, you will be able to:

Explain the meaning, sources, and effects of interest rate risk

Describe how to forecast and plan for interest rate movements from a simplified approach,

recognizing the tradeoff between targeting inflation on the one hand and growth and

employment on the other.

Recognize the Monetary Policy Committee (MPC) incentives for policy rate hike/drop

Explain the Gap and Duration analysis as measurement techniques of interest rate risk

Describe a general framework for interest rate risk management

Identify the difference between static vs. dynamic simulation approaches

Not

For

Rel

ease

Participant Guide

DD08-V3 5-4

Describe the banking investment portfolio; its nature, components and accounting treatment, and the role it plays in ALM.The Meaning of Interest Rate Risk

Suppose that a 10-year CD priced at a fixed rate1 of 10.5% is used to fund a 3-year floating

rate2 commercial loan priced at Corridor offer rate + 2.5%. Further, assume that the Corridor

rate equals 10% at the beginning of the deal and 8% one year later.

In this case, the bank starts with a 2% spread (10%+2.5% less 10.5%) at the beginning of the

deal that falls to 0% (8%+2.5% less 10.5%) one year later. The deposit will remain fixed at

10.5%, despite the drop in the loan applied rate.

This deal has turned from a profitable one to a break-even position because of the interest rate

risk resulting from the mismatch between the repricing dates of the asset and liability.

According to Basel Committee on Banking Supervision (BCBS); Interest rate risk is the

exposure of a bank's financial condition to adverse movements in interest rates. Accepting

this risk is a normal part of banking and can be an important source of profitability and

shareholder value. However, excessive interest rate risk can pose a significant threat to a

bank's earnings and capital base. Changes in interest rates affect a bank's earnings by

changing its net interest income and the level of other interest sensitive income and operating

expenses. Changes in interest rates also affect the underlying value of the bank's assets,

liabilities, and off-balance-sheet (OBS) instruments because the present value of future cash

flows (and in some cases, the cash flows themselves) change when interest rates change.

Accordingly, an effective risk management process that maintains interest rate risk within

prudent levels is essential to the safety and soundness of banks.3

Interest rate risk could be divided into:

Refinancing risk is the uncertainty of the cost of a new source of funds that are being

used to finance a long-term fixed-rate asset. This risk occurs when the bank is holding

fixed rate assets with maturities greater than the maturities of its fixed rate liabilities.

For example, if a bank has a ten-year fixed-rate loan funded by a 2-year time deposit,

the bank faces a risk of borrowing new deposits, or refinancing, at a higher rate in two

years. Thus, interest rate increases would reduce net interest income. The bank would

benefit if the rates fall as the cost of renewing the deposits would decrease, while the

earning rate on the assets would not change. In this case, net interest income would

increase.

Reinvestment risk is the uncertainty of the earning rate on the redeployment of assets

that have matured. This risk occurs when the bank holds fixed rate assets with

maturities that are less than the maturities of its fixed rate liabilities. For example, if a

bank has a two-year loan funded by a ten-year fixed-rate time deposit, the bank faces

the risk that it might be forced to lend or reinvest the money at lower rates after two

years, perhaps even below the deposit rates. Also, if the bank receives periodic cash

1 Fixed rate means that the pre-specified interest rate is fixed (doesn’t change) for the life of the deal.

2 Floating rate consists of a Benchmark + (or –) spread; which leads to changing the applied rate as the

benchmark changes with an agreed upon repricing frequency. The most widely used benchmarks are Corridor

rates in EGP, and LIBOR rates in foreign currencies. 3 “Principles for the management and supervision of interest rate risk”; July 2004

Not

For

Rel

ease

Participant Guide

DD08-V3 5-5

flows, such as coupon payments from a bond or monthly payments on a loan, these

periodic cash flows will also be reinvested at the new lower (or higher) interest rates.

Sources of Interest Rate Risk

Although the direct method to reduce the interest rate risk is matching the repricing dates of

assets and liabilities, but this method prevent ALM to benefits from taking view on yield

curve as well as being impractical at times. Foreign currency assets and liabilities structure is

an example of this impracticality; while depositors prefer fixed rate deposits, FCY borrowers

usually prefers floating rate loans. Still, the resulting mismatch could be hedged by using

Interest Rate Swaps (IRSs). In this specific case, the IRS is structured as that the bank pays

floating (from loans installments) and receive fixed (to be paid to depositors).

There are four sources of interest rate risk, as follows:

1. Repricing risk:

For instance, a bank that funded a long-term fixed-rate loan with a short-term deposit

could face a decline in both the future income arising from the position and its

underlying value if interest rates increase. These declines arise because the cash flows on

the loan are fixed over its lifetime, while the interest paid on the funding is variable, and

increases after the short-term deposit matures.

2. Yield curve risk:

Yield curve risk arises when unanticipated non-parallel shifts of the yield curve have

adverse effects on a bank's income or underlying economic value.

3. Basis risk:

Arises from imperfect correlation in the adjustment of the rates earned and paid on

different instruments with otherwise similar repricing characteristics. For example, a

strategy of funding a one-year loan that reprices monthly based on the one-month US

Treasury bill rate, with a one-year deposit that reprices monthly based on one-month

LIBOR, exposes the institution to the risk that the spread between the two index rates

may change unexpectedly.

4. Optionality risk:

Accounts for the risks from exercising explicit or implicit options in the bank’s assets or

liabilities, due to the effect on the timing and size of cash flows. Explicit options are very

rare in the Egyptian banking industry. Prepayment option of personal loans and early

redemption option of CDs are examples of implicit options.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-6

Effects of Interest Rate Risk There are two separate, but complementary, perspectives for assessing a bank's interest rate

risk exposure.

1. Earnings perspective:

In the earnings perspective, the focus of analysis is the impact of changes in interest rates

on accrual or reported earnings. This is the traditional approach to interest rate risk

assessment taken by many banks. Variation in earnings is an important focal point for

interest rate risk analysis because reduced earnings or outright losses can threaten the

financial stability of an institution by undermining its capital adequacy and by reducing

market confidence.

2. Economic value perspective:

Variation in market interest rates can also affect the economic value of a bank's assets,

and liabilities. Thus, the sensitivity of a bank's economic value to fluctuations in interest

rates is a particularly important consideration of shareholders, management, and

supervisors alike. The economic value of an instrument represents an assessment of the

present value of its expected net cash flows, discounted to reflect market rates. By

extension, the economic value of a bank can be viewed as the present value of the bank's

expected net cash flows, defined as the expected cash flows on assets minus the expected

cash flows on liabilities. In this sense, the economic value perspective reflects one view

of the sensitivity of the net worth of the bank to fluctuations in interest rates.

Since the economic value perspective considers the potential impact of interest rate changes

on the present value of all future cash flows, it provides a more comprehensive view of the

potential long-term effects of changes in interest rates than is offered by the earnings

perspective.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-7

Forecasting Interest Rate Moves: An elementary approach Following our understanding of the nature, source, and effects of interest rate risk, one of the

most important responsibilities of ALM is to expect the future trend of interest rates to

measure its impact on the level of interest rate risk and on the bank profitability.

Monetary Policy: the tradeoff between inflation and growth targeting

The course of interest rate changes is chiefly affected by the monetary policy decisions.

Monetary policy refers to actions taken by central banks to affect price levels (inflation),

aggregate output (GDP), and unemployment through controlling the money supply.

Many tools are available for monetary policy; including policy rate, banks’ required reserve

ratio, open market operations, and credit easing. Of those tools; policy rate is the focus of our

discussion here. Changing the policy rate affects the general level of interest rate in a given

economy. This will affect inflation and GDP in the same direction; meaning that, there is a

trade-off between inflation targeting and growth targeting.

To illustrate this central point, consider the case of increasing the policy rate, banks follow

this increase by rising both deposits and loans rates. Accordingly, saving will increase, which

will decrease money supply leading to lower inflation level. At the same time the cost of

borrowing needed for corporate expansion and funding of new projects will increase putting a

downward pressure on the economic growth, hence, employment. Decreasing the policy rate

has the opposite effect.

CBE’s Monetary Policy Committee (MPC)

The policy rate in Egypt is the Corridor rate set by CBE through the Monetary Policy

Committee. The Central Bank of Egypt (CBE) is responsible for the formulation and

implementation of monetary policy, with price stability being the primary and overriding

objective.4 The CBE is committed to achieving, over the medium term, low rates of inflation

which it believes are essential for maintaining confidence and for sustaining high rates of

investment and economic growth. The Government’s commitment to fiscal discipline is

important to achieve this objective.

In assessing the level of inflation, MPC calculates Core Consumer Price Index (CPI) by

excluding some volatile and regulated items from the headline CPI compiled by the Central

Agency for Public Mobilization and Statistics (CAPMAS). MPC judges whether the Core

CPI is within its comfort zone; if not, it decides on the appropriate action to bring it back into

an acceptable level.

In Practice

Now that we broadly understand the main factors behind fluctuations in the general level of

interest rates, ALM team needs to do the following in order to forecast the future course of

interest rates:

Follow up on major macro-economic indicators (e.g. inflation, GDP, unemployment,

money supply levels, and CBE foreign currency reserves) and analyze their collective

impact on expansionary/restrictive monetary policy stance (Corridor rates

drops/hikes).

Follow up on global economic trends pertaining to American Federal Reserve (FED)

and European Central Bank (ECB) actions.

It’s important to highlight that the economic data gathered for analysis should avoid rumors

be based on official, rigorous, and reliable sources (e.g. Bloomberg, Reuters, CBE

website,…); as the value of the analysis depends ultimately on the accuracy of the input data.

4 Law No. 88 of 2003 of the "Central Bank, Banking Sector and Monetary System"

Not

For

Rel

ease

Participant Guide

DD08-V3 5-8

First – Interest Rate Risk Measurement Techniques

Repricing Gap Analysis

The repricing gap measures the amount of mismatch between interest sensitive

assets and liabilities for each repricing tenor.

Like liquidity gaps, for any tenor, the gap could assume a positive value if , negative if , or zero if

Unlike liquidity gaps, both positive and negative repricing gaps exposes the bank to interest

rate risk depending on the future course of interest rate movement. Tabulated below are the

possible effects on the bank Net Interest Income (NII) for all possible combinations of gap

positions and interest rate changes:

Interest rate change

Gap Increase Decrease No change

Positive + – No effect

Negative – + No effect

Zero No effect No effect No effect

The time buckets (tenors) used in Egyptian bank’s interest rate risk disclosure are5:

Up to 1 month

1-3 months

3-12 months

1-5 years

> 5 years

The magnitude of effect on 12-month NII for each tenor depends on the size of the gap

and interest rate change, and the time remaining till end of the 12-month period; measured as

per the following formula:

could be the expected change in interest rates or a simulated standard shock, with 100bps

and 200bps as the most common. The total effect on 12-month NII equals the sum of effects

for tenors up to 12-month period. Using a standard shock to measure interest rate risk from

earnings perspective (effect on NII) is referred to as NII Simulation.

5 CBE “Rules of Preparation and Presentation of Financial Statements and the basis of Recognition and

Measurement”; December 2008

Not

For

Rel

ease

Participant Guide

DD08-V3 5-9

In practice

Let’s take the same four transactions from liquidity gap exercise. Recall that the deals

executed at the end of December 2015. We need to convert them into two repricing gaps; one

as of end of December 2015 and the other as of end of January 2016.

Amounts in EGP ’000

Uses Sources

Account Amount Description Account Amount Description

T-Bills 300 3-Mth at 9% Current

Account

800 Non-interest bearing, 70% of

balance is core; the remaining is

equally distributed in short term

tenors.

Commercial

Loans

700 3-year floating loan priced at

corridor + 2.5% and repriced

every month

CDs 200 3-year fixed rate at 9%

EGP Repricing Gap as of December 31, 2015

Up to

1Mth

1-3 Mth 3-6 Mth 6-12 Mth Over 12

Mth

Non-Interest Bearing Total

Assets: 1,000

T-Bills 300 300

Commercial Loans 700 700

Liabilities 1,000

Current Accounts 800 800

CDs 200 200

Current Gap 700 300 0 0 (200) 800

Cumulative Gap 700 1,000 1,000 1,000 800

What about the EGP Repricing Gap as of January 31, 2016?

The same shifting effect discussed with liquidity gaps applies for repricing gaps as well.

Limits are set for both current and cumulative gaps.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-10

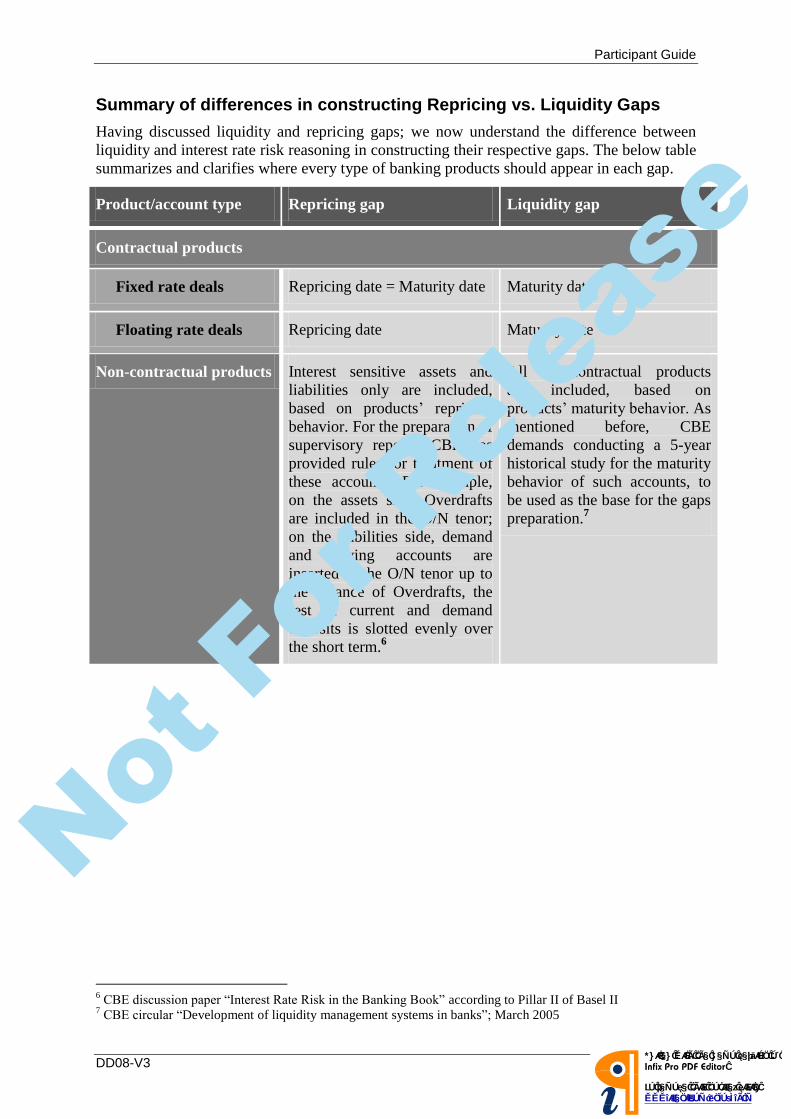

Summary of differences in constructing Repricing vs. Liquidity Gaps

Having discussed liquidity and repricing gaps; we now understand the difference between

liquidity and interest rate risk reasoning in constructing their respective gaps. The below table

summarizes and clarifies where every type of banking products should appear in each gap.

Product/account type Repricing gap Liquidity gap

Contractual products

Fixed rate deals Repricing date = Maturity date Maturity date

Floating rate deals Repricing date Maturity date

Non-contractual products Interest sensitive assets and

liabilities only are included,

based on products’ repricing

behavior. For the preparation of

supervisory reports, CBE has

provided rules for treatment of

these accounts. For example,

on the assets side, Overdrafts

are included in the O/N tenor;

on the liabilities side, demand

and saving accounts are

inserted in the O/N tenor up to

the balance of Overdrafts, the

rest of current and demand

deposits is slotted evenly over

the short term.6

All non-contractual products

are included, based on

products’ maturity behavior. As

mentioned before, CBE

demands conducting a 5-year

historical study for the maturity

behavior of such accounts, to

be used as the base for the gaps

preparation.7

6 CBE discussion paper “Interest Rate Risk in the Banking Book” according to Pillar II of Basel II

7 CBE circular “Development of liquidity management systems in banks”; March 2005

Not

For

Rel

ease

Participant Guide

DD08-V3 5-11

Duration

This kind of analysis considers the effect of change interest rate on the net worth of the bank

through the change of market value of assets and liabilities.

The duration measures the percentage change of the market value of assets and liabilities as

the result of 1% change in interest rate.

Generally, the longer the maturity or next repricing date of the instrument and the smaller the

payments that occur before maturity (e.g. coupon payments), the higher the duration (in

absolute value). Higher duration implies that a given change in the level of interest rates will

have a larger impact on economic value.

The simple methodology to calculate the change in the Economic Value of Equity (EVE)

given a parallel shift in interest rates (e.g. 200 bps) according to Basel Committee

recommendations; adopted by CBE, follows the below steps, which treats the whole bank as

if it was a bond with the repricing gaps in different tenors as its cash inflows/outflows:

Duration-based weights can be used in combination with a maturity/repricing

schedule to provide a rough approximation of the change in a bank's economic value

that would occur given a particular change in the level of market interest rates.

Specifically, an “average” duration is assumed for the positions that fall into each

time band.

The average durations are then multiplied by an assumed change in interest rates to

construct a weight for each time band.

The weighted gaps are aggregated across time bands to produce an estimate of the

change in economic value of the bank (EVE) that would result from the assumed

changes in interest rates.

Finally, the calculated EVE is then divided by the bank’s Capital Base to give an

overall assessment of the bank’s exposure to interest rate risk from an economic value

perspective.

For calculated using a 100bps change in interest rates;

Three notes are especially important in this regard:

The higher is the DOE, the higher is the bank’s economic value sensitivity to changes

in interest rates, and accordingly, the higher is the interest rate risk.

DOE is inversely related to capital, which means that, as capital increase, DOE and

hence interest rate risk decreases. Recall that as the capital increase, the leverage

decreases. So, we can conclude that as the level of leverage decreases the interest rate

risk decrease and vice versa.

DOE is the most comprehensive measure of interest rate risk, thus, is used by Basel

Committee and CBE in setting limits over interest rate risk.

Duration Gap Analysis: Another measure of interest rate risk based on duration is the duration gap.

or Duration of Assets – (Liabilities/Assets) * Duration of Liabilities

When the duration of assets is larger than the duration of liabilities, the duration gap

is positive. In this situation, if interest rates rise, assets will lose more value than

liabilities, thus reducing the value of the firm's equity. If interest rates fall, assets will

gain more value than liabilities, thus increasing the value of the firm's equity.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-12

Simulation approaches

In one sense, these approaches can be viewed as refinements of simple repricing analysis.

However, simulation approaches usually involve a more detailed breakdown of products such

that specific assumptions about product behavior can be incorporated into the analysis. These

approaches also allow for more varied changes in the interest rate environment, such as

changes in the shape and slope of the yield curve, than does repricing analysis.

Static simulation

In static simulations, the cash flows arising solely from the bank's current positions are

assessed. For assessing the exposure of earnings, simulations estimating the cash flows and

resulting earnings streams over a specific period are conducted based on one or more

assumed interest rate scenarios.

Dynamic simulation

In a dynamic simulation approach, the simulation builds in more detailed assumptions about

the future course of interest rates and the expected changes in a bank's business activity over

that time. For instance, the simulation could involve assumptions about the behavior of the

bank's customers (e.g. withdrawals from demand and savings deposits), and/or about the

future stream of business (new loans or other transactions) that the bank will encounter.

As with other approaches, the usefulness of simulation-based interest rate risk measurement

techniques depends on the validity of the underlying assumptions and the accuracy of the

basic methodology.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-13

Second – Management of interest rate risk In broad terms, the principles of sound interest rate management address the following issues:

The role of the Board and senior management in overseeing interest rate risk

management;

The need for clearly defined risk management policies and procedures that capture all

sources of interest rate risk and ensure adequate segregation of duties;

The importance of establishing and enforcing appropriate limits, of conducting stress

testing and of having adequate information systems for measuring, monitoring,

controlling and regularly reporting interest rate risk exposures; and

The need for robust internal controls that are independently reviewed on a regular

basis.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-14

Third: Banking (Fixed Income) Investment Portfolio One of the most important functions of ALM is the management of the banking investment

portfolio. Regardless of the differences in banks’ organization structures that define the

department responsible for managing this portfolio; it deserves a great deal of attention due to

its vital role in a sound ALM function.

Nature

Banks strive to increase their market shares to grow their balance sheets and increase

profitability, especially, in a broadly under-banked country like Egypt. The bank may not

have a utilization channel in loans for all deposits raised. The consequent excess liquidity in

this case is deployed in the banking investment portfolio, to be able to pay interest on the

unutilized deposits and enhance profitability.

Components and accounting treatment

The banking investment portfolio consists mainly of highly liquid fixed income products with

different maturity ranges; from short to medium and long term. Generally, the sovereigns (T-

Bills and T-Bonds) represent the major portion. Recall from our discussion of banking

financial statements that different investment classifications exist, based on the management

intention from acquiring the investment. Tabulated below is a summary of these

classifications and their main features:

Investment classification Value on the Balance sheet Revaluation (Mark to

Market) treatment

Trading Market value Unrealized gain or loss

posted to income

statement

Available for Sale Market value Unrealized gain or loss

posted directly to equity

Held to Maturity Book Cost

(Face value –/+ unamortized

discount/premium)

Not marked to market

The role in ALM

For a sound ALM function; the banking investment portfolio plays a pivotal role in both of its

risk management and profitability objectives as follows:

Risk Management:

o Liquidity risk:

The portfolio is composed of highly liquid assets with an active secondary

market (especially, T-Bills) which provides for a dependable source of funds

in case of liquidity shortage or even crisis.

o Interest rate risk:

With various ranges of maturities available in T-Bills (3, 6, 9, and 12months)

and T-Bonds (mainly 3, 5, 7, and 10years); the portfolio is an effective tool

that could be used to alter banks’ DOE and reduce exposure to interest rate

risk.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-15

Profitability:

As a secondary objective, the banking investment portfolio could provide for a

lucrative return, thus, enhance the bank’s NIM record.

This was particularly evident during the recent years post January 2011. Due to the

economic/political unrest and market turmoil witnessed post revolution, the lending

activity largely slowed down. Most of the banks kept their strategy to acquire more

market share in play. The resulting excess liquidity had no utilization alternative

rather than investing in governmental securities as part of the banking investment

book.

With the elevated country risk levels and withdrawal of foreign investors who usually

calm yields down; the increase in sovereigns’ balances was coupled with historical

hikes in yields.

Despite the fact that this had improved some banks’ profitability and NIMs

considerably, but this is not expected to last forever. As signs of market stability have

appeared, yields are calming down and on the downward trend, leaving banks with no

choice but to return to the strategic core business of lending to corporate and retail

customers even if this might put some pressure on the banks’ spreads in the near

future.

Not

For

Rel

ease

Participant Guide

DD08-V3 5-16

Exercises

Simulation Approaches

Instructions:

1. Identify the difference between Static and dynamic simulation approaches?

Duration

Instructions:

2. Corporate bonds usually pay interest semiannually. If a company decided to change from

semiannual to annual interest payments, how would this affect the bond’s interest rate risk?

Not

For

Rel

ease

Participant Guide

DD08-V3 5-17

Summary In this module, you learned how to:

Explain the meaning, sources, and effects of interest rate risk

Describe how to forecast and plan for interest rate movements from a simplified approach,

recognizing the tradeoff between targeting inflation on the one hand and growth and

employment on the other.

Recognize the Monetary Policy Committee (MPC) incentives for policy rate hike/drop

Explain the Gap and Duration analysis as measurement techniques of interest rate risk

Describe a general framework for interest rate risk management

Identify the difference between static vs. dynamic simulation approaches

Describe the banking investment portfolio; its nature, components and accounting

treatment, and the role it plays in ALM.

Not

For

Rel

ease