Embed Size (px)

Citation preview

WEALTH

TAX

&

SERVICE

TAX

By:

NARESH TOTLANI

SERVICE TAX

SERVICETAX-INDIRECT TAX (Sec-66B)

Tax on services providedOr

Agreed to be provided by service provider to service receiver.

There is no separate ACT for Service Tax , it is governed by the

Finance Act,1994

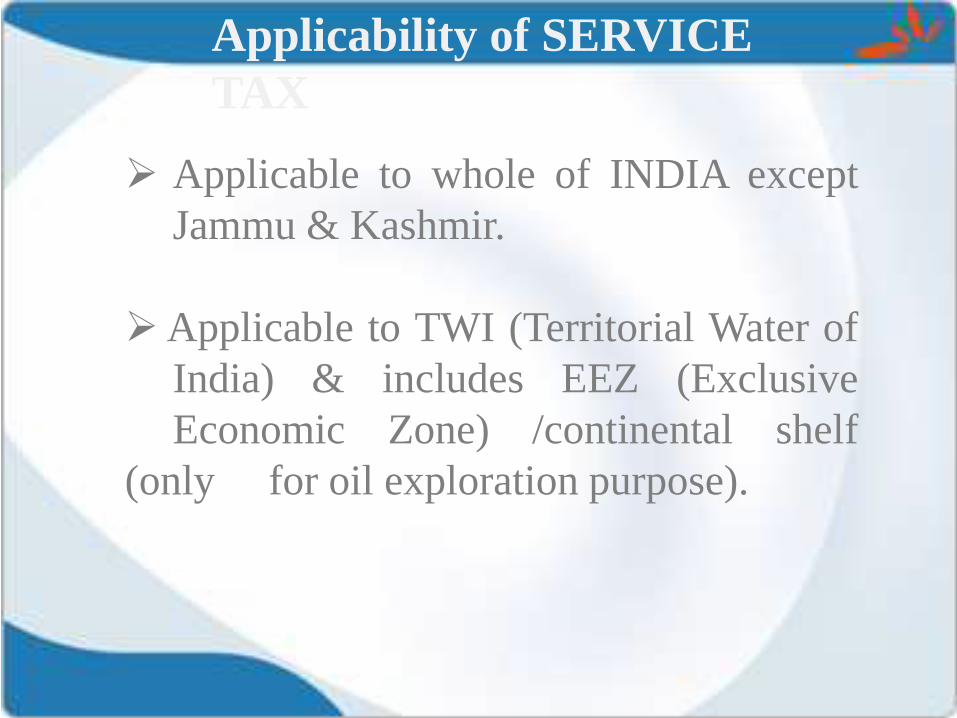

Applicability of SERVICE

TAX

Applicable to whole of INDIA except

Jammu & Kashmir.

Applicable to TWI (Territorial Water of

India) & includes EEZ (Exclusive

Economic Zone) /continental shelf

(only for oil exploration purpose).

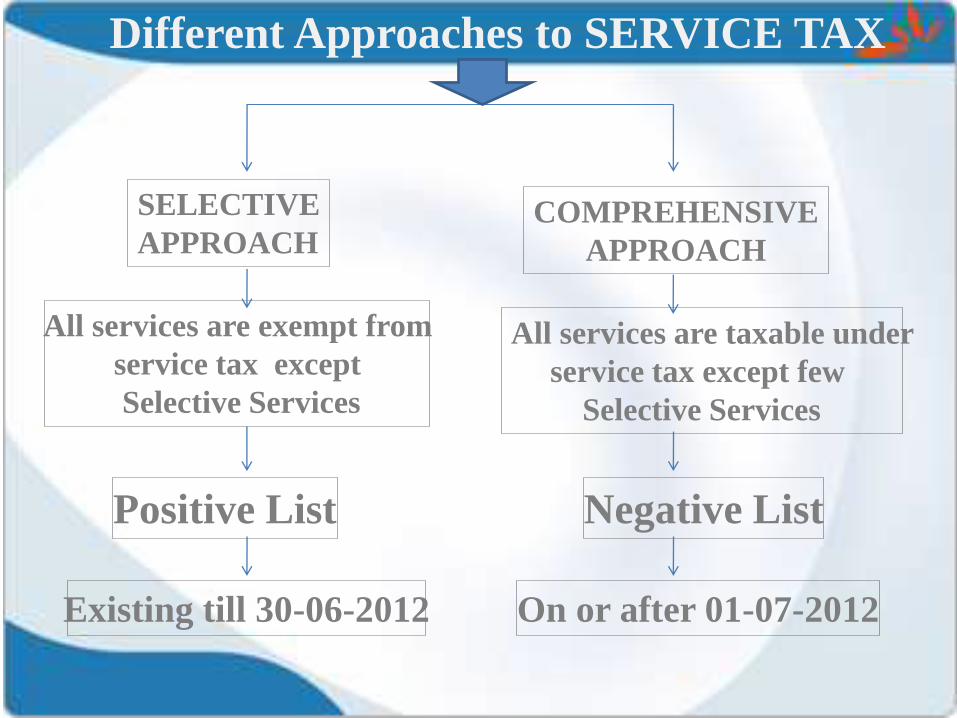

Different Approaches to SERVICE TAX

SELECTIVE

APPROACHCOMPREHENSIVE

APPROACH

All services are exempt from

service tax except

Selective Services

All services are taxable under

service tax except few

Selective Services

Positive List Negative List

Existing till 30-06-2012 On or after 01-07-2012

Road Map of SERVICE TAX

Whether Service provided or agreed to be

provided are under the definition of SERVICE

TAX ?

YES NO

No question of

Service Tax !

Whether such Services are

Negative Listed ?

YES NO

No Service Tax

will be levied !

Whether Services provided

in Taxable Territory ?

YE

S

NO

Continued…..

YES NO

Service Tax shall

be levied

No question of

Service Tax !

Whether Services are covered under MEGA

EXEMPTION NOTIFICATION

YES NO

No Liability to

pay Service Tax

Service Tax will be

collected

NEGATIVE List (SEC-66D)

i. Services provided by Government or Local Authority.

ii. Services provided by RBI.

iii. Services provided by EMBASSY.

iv. Trading of Goods (Buying & Selling).

v. Any process amounting to Manufacture/Production of

GOODS.

vi. Betting, Gambling & Lottery.

vii. Admisssion to Entertainment Events to amusement

facilities.

viii.Services provided by way of Access to Road or

Bridge on payment of TOLL Charges.

ix. Services related to Agriculture & Agriculture Produce.

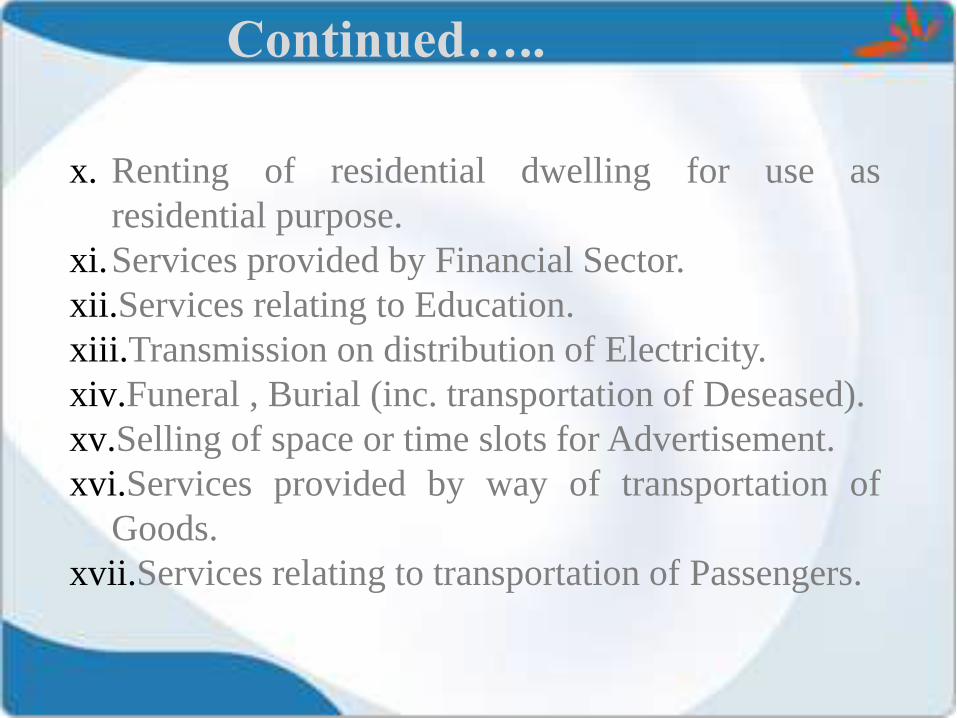

Continued…..

x. Renting of residential dwelling for use as

residential purpose.

xi.Services provided by Financial Sector.

xii.Services relating to Education.

xiii.Transmission on distribution of Electricity.

xiv.Funeral , Burial (inc. transportation of Deseased).

xv.Selling of space or time slots for Advertisement.

xvi.Services provided by way of transportation of

Goods.

xvii.Services relating to transportation of Passengers.

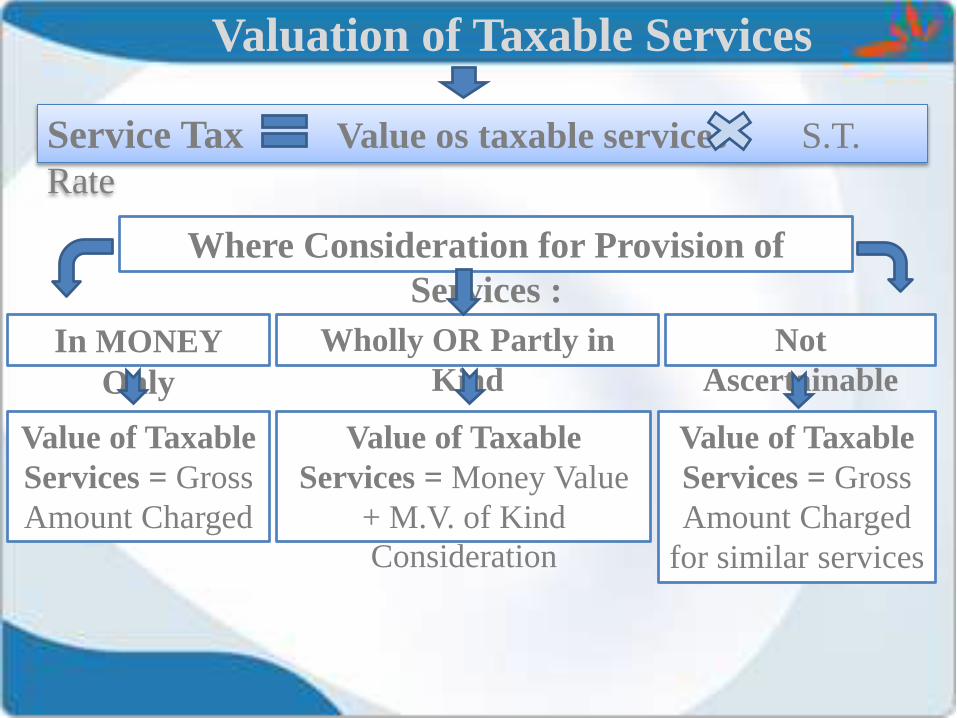

Valuation of Taxable Services

Service Tax Value os taxable services S.T.

Rate

Where Consideration for Provision of

Services :

In MONEY

Only

Wholly OR Partly in

Kind

Not

Ascertainable

Value of Taxable

Services = Gross

Amount Charged

Value of Taxable

Services = Money Value

+ M.V. of Kind

Consideration

Value of Taxable

Services = Gross

Amount Charged

for similar services

Payment of SERVICE

TAXPOINT OF TAXATION RULE -3

Whether Invoice is Raised within 30 days from the

date of Completion of Services ?

YES NO

POT will be Earlier of :-

Date of Issue of Invoice.

(OR)

Date of Payment Received.

POT will be Earlier of :-

Date of Completion of Service.

(OR)

Date of Payment Received.

Due Date for SERVICE TAX Rule-

6(1)

ASSESSEEManner of

PaymentDue Date

Individual

/Partnersh

ip

QUARTERL

Y

5th (in case of any other mode)/6th

(in case of electronic payment)

after the month immediately

following quarterly in which

service is deemed to be provided.

Others

(Co./HUF)MONTHLY

5th (in case of any other mode)/6th

(in case of electronic payment) of

the next month immediately

falling in the month in which

service is deemed to have been

provided.

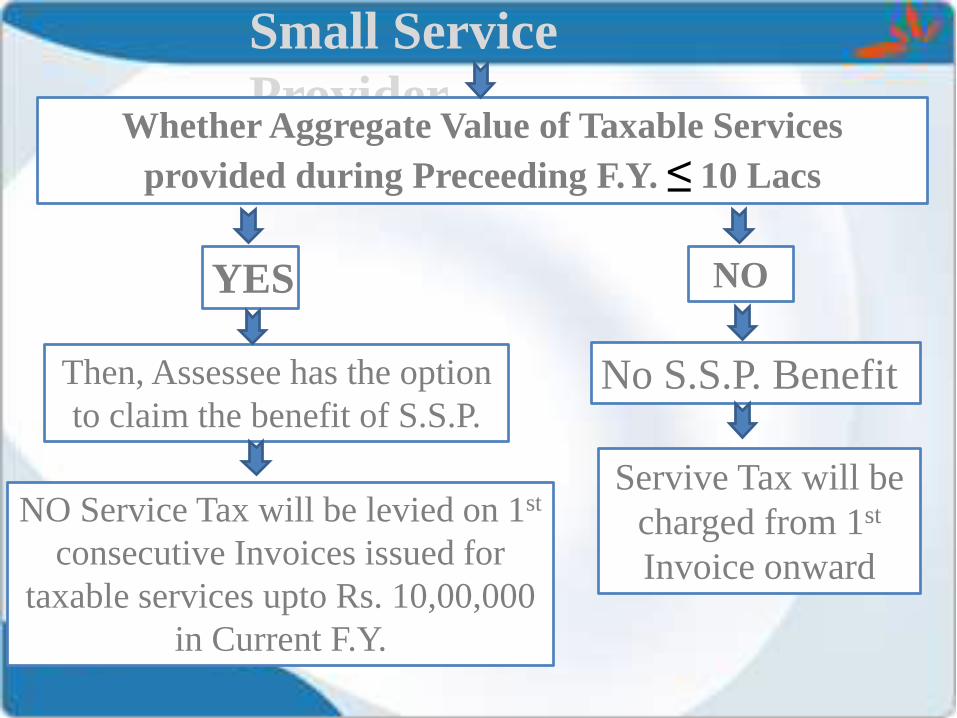

Small Service

ProviderWhether Aggregate Value of Taxable Services

provided during Preceeding F.Y. ≤ 10 Lacs

YES NO

Then, Assessee has the option

to claim the benefit of S.S.P.No S.S.P. Benefit

Servive Tax will be

charged from 1st

Invoice onward

NO Service Tax will be levied on 1st

consecutive Invoices issued for

taxable services upto Rs. 10,00,000

in Current F.Y.

REGISTRATION

PERSON liable to pay

Service Tax

PERSON Not liable to

pay Service Tax

Non-S.S.P. Service

Receiver

S.S.P. Input Service

DistributorWithin 30 Days

from the date of

commencement

of business,

(OR)

Date on which

service become

taxable

Earlier of :-

Within 30 Days

from the receipt

of service,

(OR)

Payment of

Service

Within 30

Days from

the date on

which value

of Taxable

Service

Exceeds

Rs.9,00,000

Within 30

Days from the

date of

Commenceme

nt of Business

APPLICATION

ASSESSE

E

Superintendent

of

Central Excise

Form ST-1

Document

s

Within 7Days from the Receipt of Application, the SCE must

confirm whether or not Registration have been GRANTED.

Registration certificate shall be issued in FORM ST-

2

If not replied within 7 Days then, Registration is

DEEMED to be Allowed

![MOIL LIMITED · Annual Report 2011-12 [Formerly Manganese Ore (India) Limited] There are no dues outstanding of Income Tax, Sales Tax, Wealth Tax, Service Tax, Customs Duty, Excise](https://img.pdfslide.net/doc/110x75/605aa800f3242c5e502db597/moil-limited-annual-report-2011-12-formerly-manganese-ore-india-limited-there.jpg)