Embed Size (px)

Citation preview

PAST, PRESENT, AND FUTURE ANALYSIS OF THE ARCHITECTURAL &

ENGINEERING DESIGN INDUSTRY

Prepared By: William J. McConnell, J.D., P.E.

Chief Executive Officer The Vertex Companies, Inc.

July 2016

P a g e | 2

VERTEX

Table of Contents I. Executive Summary 3

II. Design Marketplace 4

III. Overall Industry Growth 4

IV. International Growth 5

V. Market Consolidation 7

VI. Employee Owned AEC Firms 8

VII. Lifecycles of the Largest AEC Firms in the US over the past 50 Years 8

A. 24 Surviving Firms 11

B. 35 Firms that were Acquired 12

C. 41 Firms that Failed 12

VIII. Design Sector Growth 12

IX. Impact to Design Firms due to the Market Shift in the Hazardous Waste Industry during the 1990s 14

X. Technological Advances that AEC Firms Must Embrace to be Competitive in the Near Future 20

A. AEC Firms will Realize Additional Benefits of BIM 21

B. Use of Unmanned Aerial Vehicles (UAVs) to Capture Existing Conditions 21

C. Use of Laser Scanning to Capture Existing Conditions 22

D. Virtual and Augmented Reality 22

E. BIM Processes Will Revolutionize Building Delivery Via Prefabrication 23

F. Improved Energy Performance Modeling 23

G. Cloud Based Data Storage Will Improve Collaboration 24

H. 3D-Printed Architectural Models 24

I. Use of Composites in Construction 25

XI. Conclusions 25

P a g e | 3

VERTEX

I. Executive Summary

This report provides a macro view of the architectural and engineering design industry in the

U.S. in order to understand strategies employed by both successful and unsuccessful firms over the past

50 years. It also evaluates technological trends that design firms must embrace in order to maintain a

competitive edge moving forward into the future.

The majority of the top 20 design firms are publicly traded and look to M&A activity to maintain

robust growth programs. Larger firms over the past 50 years that have ignored strategic M&A activity

have steadily fallen down or off ENR’s top design firm list. Lack of M&A often leads to an

overconcentration of work in few market sectors. Because market sectors ebb and flow over time, a lack

of diversification caused several failures of large design firms since 1965. An overconcentration in oil and

gas work in the 1970s led to many failures in the 1980s. Similarly, an overweighed focus on hazardous

waste work in the 1980s and early 1990s led to a number of large bankruptcies and fire sales in the late

1990s and early 2000s. Thus, a key lesson from this study is the importance of market diversification.

Over the past twenty years the growth of the top 500 architectural and engineering design firms

has outpaced the U.S. Gross Domestic Product by nearly two percentage points in large part because of

rapid growth in international work. The average percentage of international revenue for the top 20

design firms has doubled over the past twenty years, from 14% to 28%; thus, the large firms must not

ignore international markets to maintain competitiveness.

In addition to diversification and international expansion, design firms must embrace

technological advances in order to position for future work. For instance, BIM software is utilized on

nearly all large design projects to, among other things, coordinate the work of various trades—ignoring

this trend is almost a bar to qualification for large-scale work. Newer trends, such as the use of drones

and laser scanning to capture existing conditions, cloud based storage for improved collaboration, and

3D-Printing to prepare early architectural models, must be embraced to keep on the forefront of market

P a g e | 4

VERTEX

adoption. In addition, architects and engineers must understand the use of new product offerings, such

as composites to keep designs economically viable and awe-inspiring.

II. Design Marketplace

The architectural and engineering design marketplace is made up of approximately 100,000

firms, but the majority of the industry’s revenue is generated from the top 500 companies.1 2 Like

construction, the overall design industry is fragmented—only ten percent of all firms have more than 20

employees.3 This paper focuses on the larger design firms, which traditionally fall into one of the

following five categories:

AEC: architect, engineering, and construction company AE: architect and engineering company EC: engineering and construction company A: architectural company E: engineering company Of the top 20 ranked firms, 9 are EC, 5 are AEC, 4 are AE, 1 is A, and 1 is E; hence, the majority of

top design firms also have a construction component. In addition, the only pure engineering firm (“E”) is

Tetra Tech, and it was categorized as an EC firm until last year when it dropped its construction

program, which is a trend that I will discuss later in this report. The revenue recorded by ENR, the

publication that ranks the top 500 design firms each year, does not include construction revenue; thus,

the ranking is purely based on design services.

III. Overall Industry Growth

Domestic design revenue for the top 500 design firms outpaced both the U.S. GDP and put-in-

place construction revenue over the past twenty years, with an average annual growth rate of 5.3%.

1 https://www.census.gov/epcd/susb/2002/us/US5413.HTM 2 https://research.stlouisfed.org/fred2/series/REV5413TAXABL157QNSA 3 https://www.census.gov/epcd/susb/2002/us/US5413.HTM#table1

P a g e | 5

VERTEX

International design revenue for the top 500 design companies grew at a healthy 9.8% within the noted

time frame. Combined, domestic and international design revenue grew at an annual rate of 6.1%.

Annual Growth Category Rate (’95 – ’15)

Top 500 Domestic Design Revenue: 5.3% Top 500 International Design Revenue: 9.8% Top 500 Design Revenue (Domestic & International): 6.1% US GDP4: 4.4% Put In Place Construction (domestic) 5: 3.6%

Overall design revenue outpaced construction revenue and GDP figures for two reasons. First,

the construction and GDP figures do not include international expenditures, which, as noted above, are

outpacing domestic work. Second, during the Great Recession of 2007-2009, many owners continued to

authorize design work and, once complete, projects were shelved, which caused a great impact to

overall construction revenue. As a result, the downturn did not affect design firms as severely as

contractors.

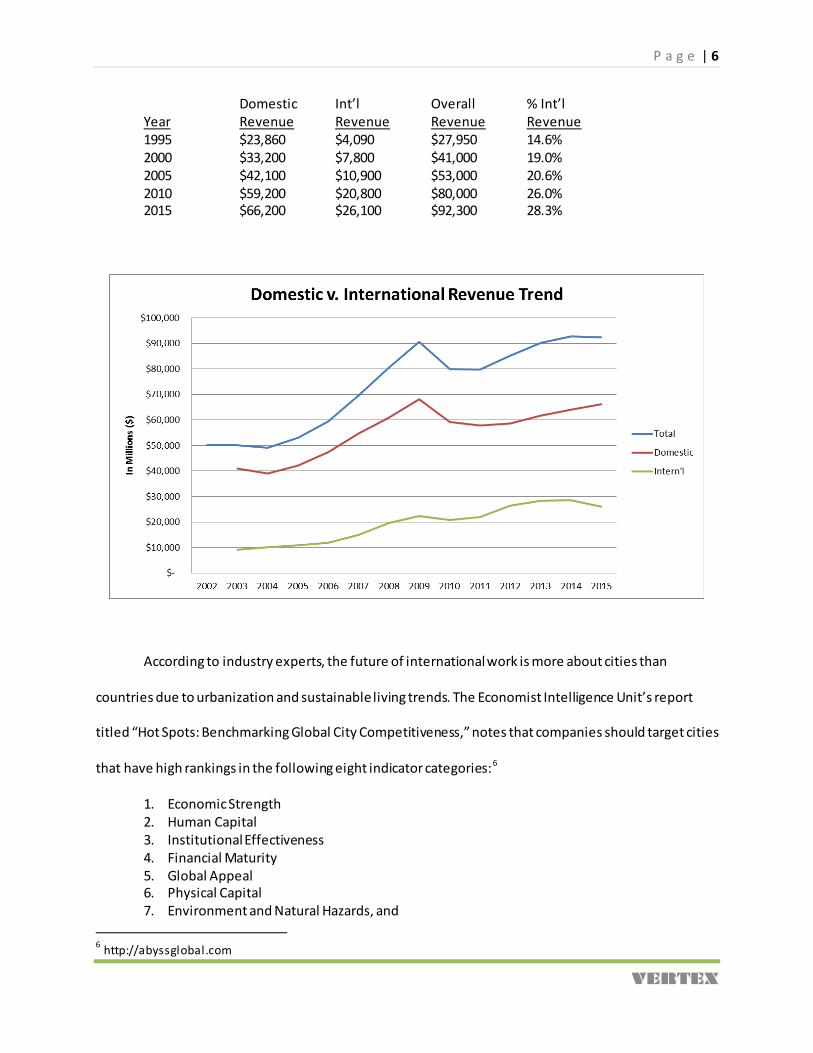

IV. International Growth

Large design firms must look to international work to maintain their position as a top player in

the marketplace. On average, the top 20 design firms generate one third of revenue from international

projects. In terms of overall figures from the top 500 designers, international work percentage has

doubled from 14.6% in 1995 to 28.3% in 2015. The figures suggest that large AEC firms can no longer

ignore the international marketplace as a source of growth.

4 http://www.bea.gov/newsreleases/national/gdp/2016/gdp4q15_3rd.htm 5 https://www.census.gov/construction/c30/c30index.html

P a g e | 6

VERTEX

Domestic Int’l Overall % Int’l Year Revenue Revenue Revenue Revenue 1995 $23,860 $4,090 $27,950 14.6% 2000 $33,200 $7,800 $41,000 19.0% 2005 $42,100 $10,900 $53,000 20.6% 2010 $59,200 $20,800 $80,000 26.0% 2015 $66,200 $26,100 $92,300 28.3%

According to industry experts, the future of international work is more about cities than

countries due to urbanization and sustainable living trends. The Economist Intelligence Unit’s report

titled “Hot Spots: Benchmarking Global City Competitiveness,” notes that companies should target cities

that have high rankings in the following eight indicator categories:6

1. Economic Strength 2. Human Capital 3. Institutional Effectiveness 4. Financial Maturity 5. Global Appeal 6. Physical Capital 7. Environment and Natural Hazards, and

6 http://abyssglobal.com

P a g e | 7

VERTEX

8. Social and Cultural Character

Reportedly, cities with the highest combined rankings, based on the noted metrics, provide sufficient

infrastructure and work/life environment for “people to conduct their lives and business effectively.”7

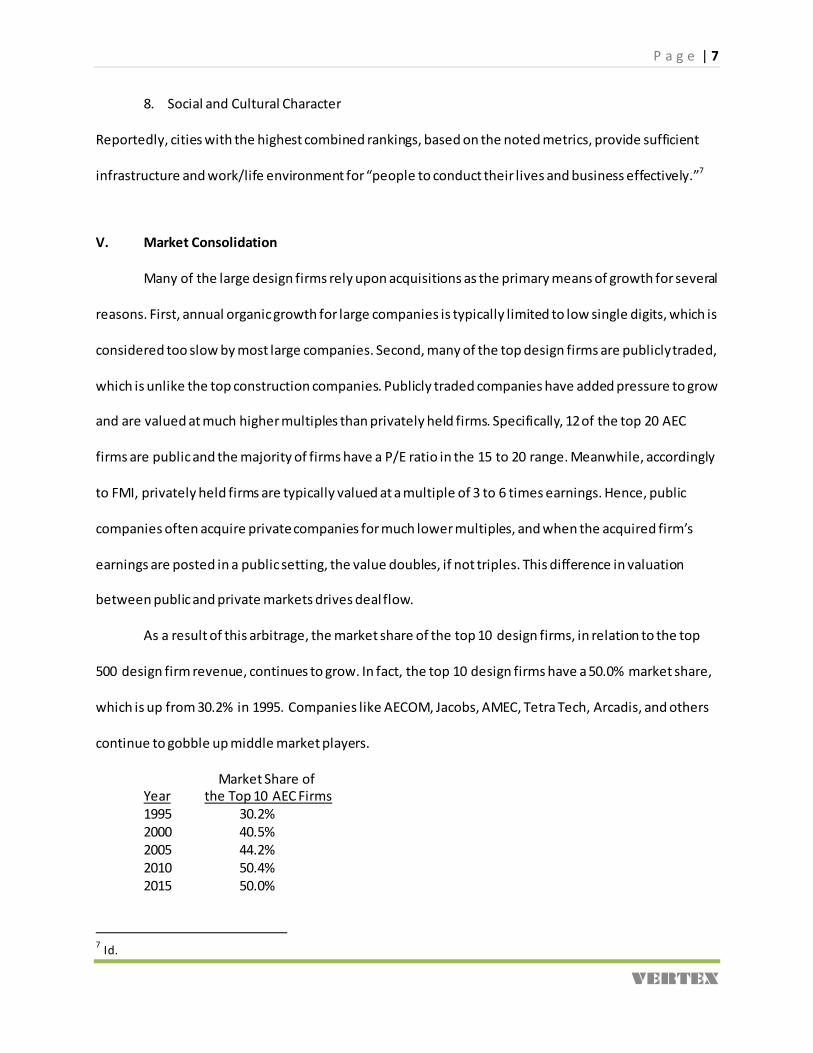

V. Market Consolidation

Many of the large design firms rely upon acquisitions as the primary means of growth for several

reasons. First, annual organic growth for large companies is typically limited to low single digits, which is

considered too slow by most large companies. Second, many of the top design firms are publicly traded,

which is unlike the top construction companies. Publicly traded companies have added pressure to grow

and are valued at much higher multiples than privately held firms. Specifically, 12 of the top 20 AEC

firms are public and the majority of firms have a P/E ratio in the 15 to 20 range. Meanwhile, accordingly

to FMI, privately held firms are typically valued at a multiple of 3 to 6 times earnings. Hence, public

companies often acquire private companies for much lower multiples, and when the acquired firm’s

earnings are posted in a public setting, the value doubles, if not triples. This difference in valuation

between public and private markets drives deal flow.

As a result of this arbitrage, the market share of the top 10 design firms, in relation to the top

500 design firm revenue, continues to grow. In fact, the top 10 design firms have a 50.0% market share,

which is up from 30.2% in 1995. Companies like AECOM, Jacobs, AMEC, Tetra Tech, Arcadis, and others

continue to gobble up middle market players.

Market Share of Year the Top 10 AEC Firms 1995 30.2% 2000 40.5% 2005 44.2% 2010 50.4% 2015 50.0%

7 Id.

P a g e | 8

VERTEX

VI. Employee Owned AEC Firms

As noted above, the 12 of the top 20 design firms are publicly traded. Of the remaining 8 firms,

7 are 100% employee owned. The only exception to this model in the top 20 list is Bechtel, which is

owned by the Bechtel family and various internally elected employees; Bechtel is the fifth largest

privately held company in the US.8 Based on my review of the ownership model of the top 100 design

firms, the most effective ownership strategies, in order to position a design firm for growth, is the public

marketplace or 100% employee ownership. The public model offers high valuation multiples which

promotes growth through acquisition, while the employee ownership model provides design teams with

additional motivation to grow the business in order to increase corporate valuation.

VII. Lifecycles of the Largest AEC Firms in the US over the past 50 Years

Of the top 100 design firms reported by ENR in 1965, 24 survived, 35 were acquired, and 41

failed. This data is similar, but surprisingly a bit bleaker, than my analysis of the top 100 contractors

listed by ENR in 1965 where 26 survived, 41 were acquired, and 33 failed.

Survived Acquired Failed Current Status of Top 100 Design Firms from 1965: 24 35 41

Current Status of Top 100 Contractors from 1965: 26 41 33

While more design firms failed when compared to contractors, the success rate of acquisitions

of design firms is considerably higher than the success rate of contractors. The vast majority of the 35

design firm acquisitions were successful, while over half of the 41 contractor acquisitions failed during

the noted time period.

Another interesting fact is that only 3 of the 8 surviving design firms that were listed in the top

25 in 1965 remain in the top 25 in 2015. The five firms that slipped out of the top 25 made minimal, if

any, acquisitions over the past 50 years. This suggests that an acquisition strategy is necessary to keep

8 http://www.forbes.com/companies/bechtel/

P a g e | 9

VERTEX

pace (or above) with the industry. Design firms that lack the personnel, capital, and/or an appetite for

risk (vis-a-vis M&A transactions) often fall down the top designer list over time. A seemingly good exit

strategy for large design firms that fall into this category is to be acquired by a large and diverse design

firm.

As noted in the “Lifecycle of Construction Contractors” study, a number of AEC firms have

started to acquire pure contractors. The converse is not true—only one pure contractor triggered a

merger with a large architectural firm (The Beck Group’s merger with Urban Architecture in 1999) based

on my research; this is likely due to lack of funding.

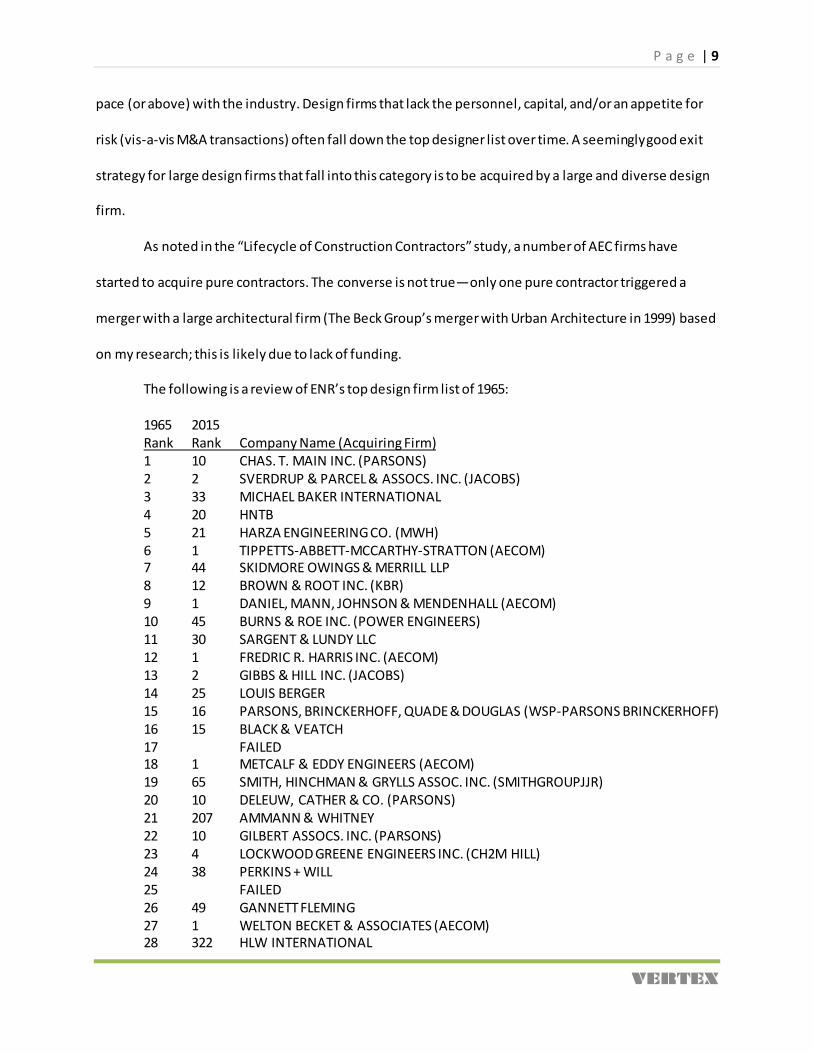

The following is a review of ENR’s top design firm list of 1965:

1965 2015 Rank Rank Company Name (Acquiring Firm) 1 10 CHAS. T. MAIN INC. (PARSONS) 2 2 SVERDRUP & PARCEL & ASSOCS. INC. (JACOBS) 3 33 MICHAEL BAKER INTERNATIONAL 4 20 HNTB 5 21 HARZA ENGINEERING CO. (MWH) 6 1 TIPPETTS-ABBETT-MCCARTHY-STRATTON (AECOM) 7 44 SKIDMORE OWINGS & MERRILL LLP 8 12 BROWN & ROOT INC. (KBR) 9 1 DANIEL, MANN, JOHNSON & MENDENHALL (AECOM) 10 45 BURNS & ROE INC. (POWER ENGINEERS) 11 30 SARGENT & LUNDY LLC 12 1 FREDRIC R. HARRIS INC. (AECOM) 13 2 GIBBS & HILL INC. (JACOBS) 14 25 LOUIS BERGER 15 16 PARSONS, BRINCKERHOFF, QUADE & DOUGLAS (WSP-PARSONS BRINCKERHOFF) 16 15 BLACK & VEATCH 17 FAILED 18 1 METCALF & EDDY ENGINEERS (AECOM) 19 65 SMITH, HINCHMAN & GRYLLS ASSOC. INC. (SMITHGROUPJJR) 20 10 DELEUW, CATHER & CO. (PARSONS) 21 207 AMMANN & WHITNEY 22 10 GILBERT ASSOCS. INC. (PARSONS) 23 4 LOCKWOOD GREENE ENGINEERS INC. (CH2M HILL) 24 38 PERKINS + WILL 25 FAILED 26 49 GANNETT FLEMING 27 1 WELTON BECKET & ASSOCIATES (AECOM) 28 322 HLW INTERNATIONAL

P a g e | 10

VERTEX

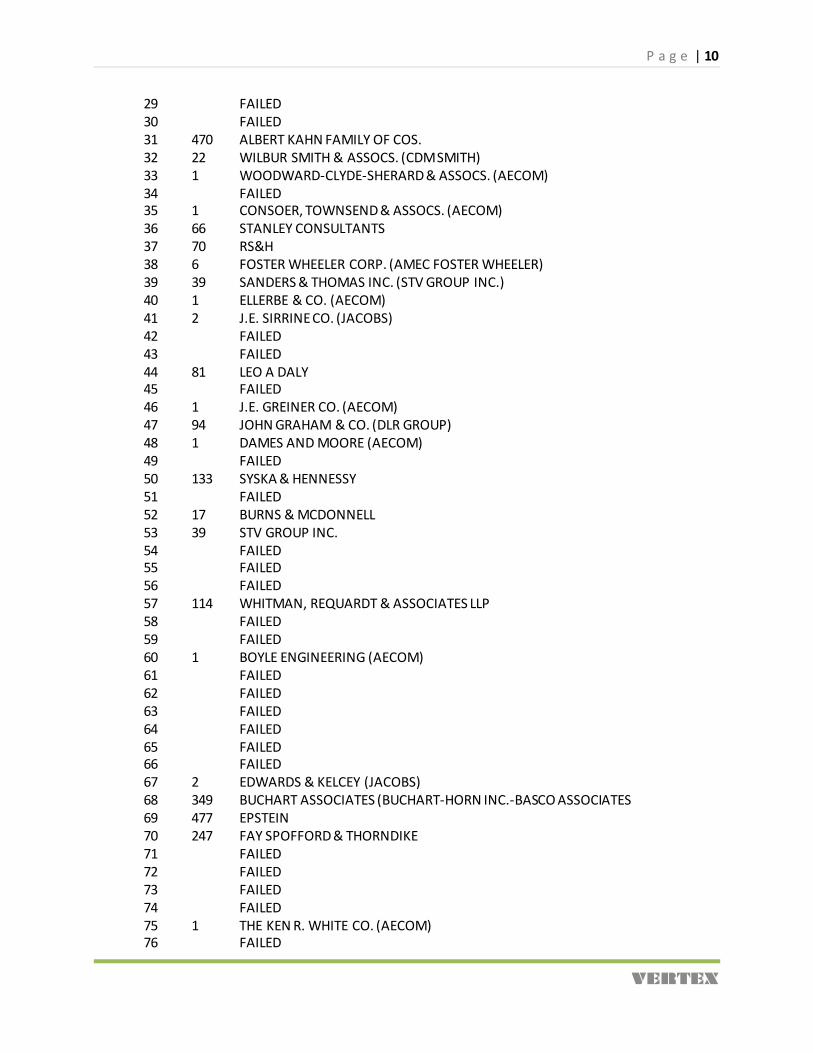

29 FAILED 30 FAILED 31 470 ALBERT KAHN FAMILY OF COS. 32 22 WILBUR SMITH & ASSOCS. (CDM SMITH) 33 1 WOODWARD-CLYDE-SHERARD & ASSOCS. (AECOM) 34 FAILED 35 1 CONSOER, TOWNSEND & ASSOCS. (AECOM) 36 66 STANLEY CONSULTANTS 37 70 RS&H 38 6 FOSTER WHEELER CORP. (AMEC FOSTER WHEELER) 39 39 SANDERS & THOMAS INC. (STV GROUP INC.) 40 1 ELLERBE & CO. (AECOM) 41 2 J.E. SIRRINE CO. (JACOBS) 42 FAILED 43 FAILED 44 81 LEO A DALY 45 FAILED 46 1 J.E. GREINER CO. (AECOM) 47 94 JOHN GRAHAM & CO. (DLR GROUP) 48 1 DAMES AND MOORE (AECOM) 49 FAILED 50 133 SYSKA & HENNESSY 51 FAILED 52 17 BURNS & MCDONNELL 53 39 STV GROUP INC. 54 FAILED 55 FAILED 56 FAILED 57 114 WHITMAN, REQUARDT & ASSOCIATES LLP 58 FAILED 59 FAILED 60 1 BOYLE ENGINEERING (AECOM) 61 FAILED 62 FAILED 63 FAILED 64 FAILED 65 FAILED 66 FAILED 67 2 EDWARDS & KELCEY (JACOBS) 68 349 BUCHART ASSOCIATES (BUCHART-HORN INC.-BASCO ASSOCIATES 69 477 EPSTEIN 70 247 FAY SPOFFORD & THORNDIKE 71 FAILED 72 FAILED 73 FAILED 74 FAILED 75 1 THE KEN R. WHITE CO. (AECOM) 76 FAILED

P a g e | 11

VERTEX

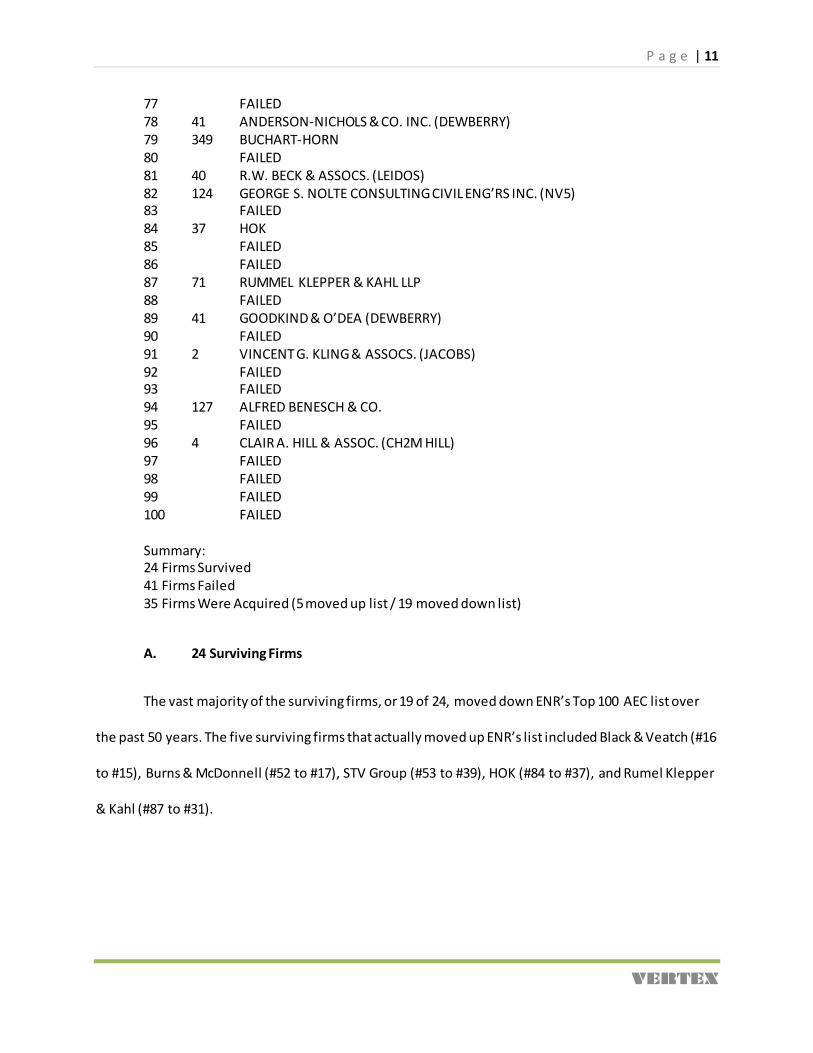

77 FAILED 78 41 ANDERSON-NICHOLS & CO. INC. (DEWBERRY) 79 349 BUCHART-HORN 80 FAILED 81 40 R.W. BECK & ASSOCS. (LEIDOS) 82 124 GEORGE S. NOLTE CONSULTING CIVIL ENG’RS INC. (NV5) 83 FAILED 84 37 HOK 85 FAILED 86 FAILED 87 71 RUMMEL KLEPPER & KAHL LLP 88 FAILED 89 41 GOODKIND & O’DEA (DEWBERRY) 90 FAILED 91 2 VINCENT G. KLING & ASSOCS. (JACOBS) 92 FAILED 93 FAILED 94 127 ALFRED BENESCH & CO. 95 FAILED 96 4 CLAIR A. HILL & ASSOC. (CH2M HILL) 97 FAILED 98 FAILED 99 FAILED 100 FAILED

Summary: 24 Firms Survived 41 Firms Failed 35 Firms Were Acquired (5 moved up list / 19 moved down list)

A. 24 Surviving Firms

The vast majority of the surviving firms, or 19 of 24, moved down ENR’s Top 100 AEC list over

the past 50 years. The five surviving firms that actually moved up ENR’s list included Black & Veatch (#16

to #15), Burns & McDonnell (#52 to #17), STV Group (#53 to #39), HOK (#84 to #37), and Rumel Klepper

& Kahl (#87 to #31).

P a g e | 12

VERTEX

B. 35 Firms that were Acquired

AECOM (publicly traded) acquired 12, or approximately one-third, of the top 100 design firms

that were acquired over the past 50 years—note the majority of AECOM’s acquisitions took place over

the past two decades. Jacobs (publicly traded) had the second most acquisitions at 4, Parsons (100%

employee owned) had the third most at 3, and CH2M (100% employee owned) and Dewberry tied for

the fourth most acquisitions at 2.

The remaining 14 companies were acquired by other large design firms. The success rate of the

acquisitions was remarkable, particularly when compared to the success rate of acquisitions in the

construction industry. As discussed further below, acquisitions made by large, diverse, and public design

firms appear to have more success than design firms with only a few service offerings. The diverse firms

tend to perform much better through lean times that hit certain industries at least once a decade.

C. 41 Firms that Failed

ENR did not list the names of the failed design firms in its analysis; thus, I was unable to evaluate

the reasons for failure. Likely the main cause of failure is lack of diversification and, as a result, failure

due to shifts in the marketplace.

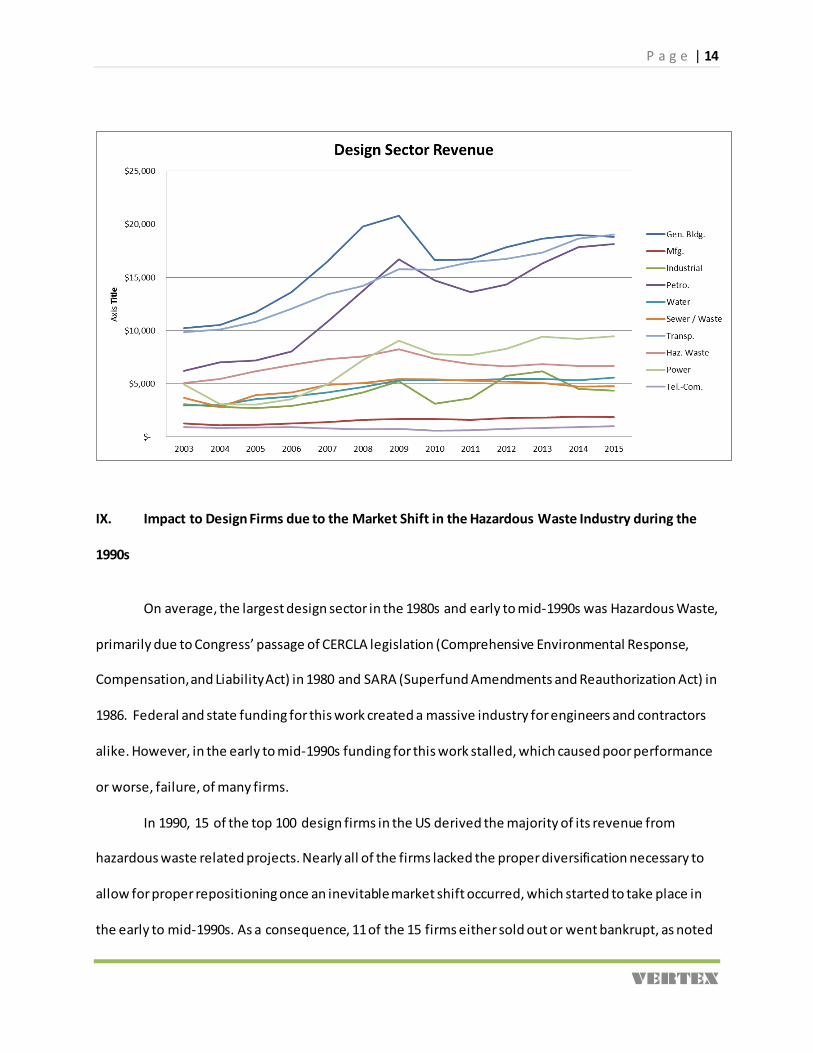

VIII. Design Sector Growth

ENR divides design revenue into nine sectors. The size and percent of contribution of each

sector is ever evolving. In 1995 the largest design sector was hazardous waste, now it ranks fifth. For the

first time in 20 years Transportation now ranks first. Understanding how each design sector ebbs and

flows is critical to survival—particularly firms that lack diversity. This issue is discussed in detail below.

P a g e | 13

VERTEX

Design Revenue Per Sector

Sector: 1995 2000 2005 2010 2015 General Building: $4,360 $8,004 $11,718 $16,594 $18,810 Manufacturing: $1,300 $1,358 $1,141 $1,674 $1,840 Industrial: $2,312 $4,099 $2,709 $3,144 $4,354 Petroleum: $3,468 $5,010 $7,183 $14,715 $18,141 Water: $1,210 $2,079 $3,542 $5,305 $5,584 Sewer/Waste: $2,320 $2,875 $3,907 $5,395 $4,794 Transportation: $4,280 $6,966 $10,800 $15,735 $19,033 Hazardous Waste: $5,470 $5,110 $6,167 $7,370 $6,662 Power: $1,900 $3,543 $3,026 $7,766 $9,453 Telecom: $0 $0 $903 $587 $1,011 Overall: $27,950 $33,200 $42,100 $59,200 $92,300

Percent Market Share per Sector

Sector: 1995 2000 2005 2010 2015 General Building: 16 25 28 28 20 (+4) Manufacturing: 5 4 3 3 2 (-3) Industrial: 8 12 6 5 5 (-3) Petroleum: 12 15 17 25 20 (+8) Water: 4 6 8 9 6 (+2) Sewer/Waste: 8 9 9 9 5 (-3) Transportation: 15 21 26 27 21 (+6) Hazardous Waste: 20 15 15 12 7 (-13) Power: 7 11 7 13 10 (+3) Telecom: 0 0 2 1 1 (+1) Overall: 100 100 100 100 100

Annual Growth Rate Between Periods

Sector: 1995 - 2000 2000 – 2005 2005 – 2010 2010 – 2015 Ave. (’95 – ’15) General Building: 12.9 7.9 7.2 2.5 7.6 Manufacturing: 0.9 -3.4 8.0 1.9 1.8 Industrial: 12.1 -7.9 3.0 6.7 3.2 Petroleum: 7.6 7.5 15.4 4.3 8.6 Water: 11.4 11.2 8.4 1.0 8.0 Sewer/Waste: 4.4 6.3 6.7 -2.3 3.7 Transportation: 10.2 9.2 7.8 3.9 7.8 Hazardous Waste: -1.4 3.8 3.6 -2.0 1.0 Power: 13.3 -3.1 20.7 4.0 8.4 Telecom: 0 0 -8.3 11.5 1.2 Overall: 3.5 4.9 7.1 9.3 6.2

P a g e | 14

VERTEX

IX. Impact to Design Firms due to the Market Shift in the Hazardous Waste Industry during the

1990s

On average, the largest design sector in the 1980s and early to mid-1990s was Hazardous Waste,

primarily due to Congress’ passage of CERCLA legislation (Comprehensive Environmental Response,

Compensation, and Liability Act) in 1980 and SARA (Superfund Amendments and Reauthorization Act) in

1986. Federal and state funding for this work created a massive industry for engineers and contractors

alike. However, in the early to mid-1990s funding for this work stalled, which caused poor performance

or worse, failure, of many firms.

In 1990, 15 of the top 100 design firms in the US derived the majority of its revenue from

hazardous waste related projects. Nearly all of the firms lacked the proper diversification necessary to

allow for proper repositioning once an inevitable market shift occurred, which started to take place in

the early to mid-1990s. As a consequence, 11 of the 15 firms either sold out or went bankrupt, as noted

P a g e | 15

VERTEX

below. Moreover, the remaining 4 firms have struggled to keep pace with average design company

performance over the past three decades. The following is a brief review of the 15 firms.

#16 Dames & Moore, Los Angeles, CA (50% Haz. Waste work in 1990)(Acquired by URS in

1999): In the early 1990s, as the hazardous waste industry started to shrink, Dames & Moore

went public in order to generate sufficient funding to go on an acquisition spree to diversify

away from the hazardous waste sector. In 1995 alone, Dames & Moore acquired Walk Haydel &

Associates Inc. (Program Management firm focused on the Power industry), O'Brien Kreitzberg,

Inc. (Construction Management firm that focused on federal building projects), and

DecisionQuest, Inc. (Behavioral Research firm). The acquisitions proved to be too little too late

as Dames & Moore sold out to URS in 1999 due to financial issues.

#20 ICF Kaiser Engineers, Oakland, CA (42% Haz. Waste work in 1990)(Acquired by IT Corp. in

1998): Similar to Dames & Moore, ICF Kaiser Engineers went public in 1991 in order to generate

funding for acquisitions to allow for diversification beyond hazardous waste work. Specifically,

ICF Kaiser attempted to enter into manufacturing, which turned out to be unsuccessful as noted

by the Washington Post, "the company proved not particularly good at managing product-

oriented businesses." Thereafter the company sold off many of its acquisitions and restructured

its debt. The company’s poor acquisition strategy, coupled with the continually shrinking

hazardous waste work, led to ICF Kaiser’s sale to IT Corp. in the late 1990s. The sale was unusual

because IT Corp. was in a similar position to ICF Kaiser—overweighed focus on hazardous waste

work. As noted below, IT Corp. filed for bankruptcy in 2002.

#24 IT Corporation, Torrance, CA (100% Haz. Waste work in 1990)(Filed for Bankruptcy in

2002): IT Corp.’s principal business involved the disposal of industrial hazardous waste. The

P a g e | 16

VERTEX

company had virtually no diversification beyond environmental work in the early 1990s.

Accordingly, IT Corp. ran into financial troubles in the 1990s due to the shrinking marketplace

and a reckless acquisition strategy. To make matters worse, the company was named in a

number of high profile environmental law suits in the early 2000s. Accordingly, IT Corp. declared

bankruptcy in 2002. Thereafter, the Shaw Group acquired substantially all of IT Corp.’s assets

and some of its liabilities out of bankruptcy.

#34 ENSR Corporation, Westford, MA (100% Haz. Waste work in 1990)(Acquired by AECOM in

2005): ENSR Corporation, like IT Corp., was solely focused on hazardous waste work in the early

1990s. As a result, ENSR struggled through the 1990s and early 2000s due to the shrinking

marketplace for hazardous waste work. Ultimately, ENSR sold out to AECOM in 2005.

#37 NUS Corporation, Gaithersburg, MD (40% Haz. Waste work in 1990)(Acquired by

Halliburton in 1992): Halliburton acquired NUS Corporation in the early 1990s as the hazardous

waste sector started to compress. Halliburton had trouble turning NUS Corp. around; therefore,

it spun NUS Corp. off to Tetra Tech Inc. in 1997. Over the past decade or so, Tetra Tech has

repositioned Tetra Tech NUS into a technology firm that is focused on the environmental

industry.9

#38 Woodward-Clyde Group, Inc., Denver, CO (33% Haz. Waste Work)(Acquired by URS in

1997): While Woodward-Clyde only generated 33% of its revenue from hazardous waste

projects, its overall focus was environmentally driven; thus, the company’s growth languished

9 http://isg.applications.tetratech.com/productGallery.aspx

P a g e | 17

VERTEX

through the early and mid-1990s.10 URS, a primarily building and transportation AEC firm,

acquired Woodward-Clyde in 1997 to diversify its service offerings.11 In 2012, URS spent $1.25

billion in its acquisition of Flint Energy Services, which created an overconcentration in revenue

and debt related to the oil and gas sector. As a result of URS’ subsequent poor performance due

to the compression of the oil and gas sector, AECOM acquired URS in late 2014.

#46 The ERM Group, Exton, PA (85% Haz Waste work in 1990)(Remains in Business): ERM

weathered the storm of the 1990s even though a large concentration of its work was focused on

hazardous waste. However, ERM has struggled with consistent growth through the 1990s. To

help boost growth, ERM aligned itself with private equity firm, Bridgeport Capital, in the early

2000s. In 2011, London-based private equity firm Charterhouse acquired a majority stake in the

business by buying out Charterhouse’s shares.12 In 2015, ERM partnered with OMERS Private

Equity to take out Charterhouse.13 Based on this volatility, ERM appears to be struggling with

this private equity formula.

#57 Groundwater Technology Inc., Norwood, MA (100% Haz. Waste work in 1990)(Acquired by

IT Corp. 1998): In 1996, Flour’s subsidiary, Flour Daniel Environmental Services, Inc. , merged

with Groundwater Technology Inc. to form Fluor Daniel GTI.14 The merger did not work out as

10 http://www.solidwaste.com/doc/urs-acquires-woodward-clyde-group-0002 11 http://www.nytimes.com/1997/08/20/business/urs-to-pay-100-mill ion-for-woodward-clyde.html 12 http://www.erm.com/en/news-events/news/erm-partners-with-omers-private-equity-to-buy-out-charterhouses-investment-in-erm/ 13 http://www.erm.com/en/news-events/news/archived-news-2011/erm-announces-that-charterhouse-is-to-acquire-a-majority-stake-in-the-business/ 14 http://investor.fluor.com/phoenix.zhtml?c=124955&p=irol-newsArticle&ID=14751

P a g e | 18

VERTEX

Flour expected; therefore, Flour sold Fluor Daniel GTI to IT Corp.15 in 1998, less than two years

after the transaction. As noted above, IT Corp. filed for bankruptcy in 2002.

#59 Harding Associates, Novato, CA (80% Haz. Waste work in 1990)(Acquired by IT Corp. in

1998): In 1998, Harding employed the IT Corp. strategy and attempted to increase its

marketshare of hazardous waste work, despite the lack of growth in this sector. In the 1998

Harding acquired ABB Environmental Services Inc. out of Portland, ME (#87 on ENR’s Top 500

Design Firms in 1990).16 Harding’s growth strategy within the hazardous waste sector did not

work as two year later it sold out to Mactec Inc. for a discounted price due to poor financial

performance.17 In 2011, AMEC acquired Mactec.18

#70 ATEC Associates Inc., Indianapolis, IN (45% Haz. Waste work in 1990)(Survived; Dropped

off of ENR’s Top 500 list): On or about 1995, ATC, an environmental firm, acquired ATEC. ATC,

like ERM, appears to be having trouble with its ownership structure over the past decade most

likely due to sluggish market growth. In 2012, Cardno Limited (Australia-based global AEC firm)

acquired ATC. In 2015, a group led by Bernhard Capital Partners (energy focused private equity

firm), acquired ATC from Cardno.19 ATC was not listed in ENR’s Top 500 Design Firm in 2015.

#79 Ecology and Environment, Inc., Lancaster, NY (90% Haz Waste work in 1990)(Survived;

Dropped down to #96 on ENR’s Top 500 list): Ecology and Environment, Inc. (“E&E”) was able to 15 http://www.nytimes.com/1998/10/29/business/company-news-it-group-acquiring-fluor-daniel-gti-for-69-mill ion.html 16 https://zweiggroup.com/newsletters/checkout.php?id=1082 17 http://www.nytimes.com/2000/03/25/business/company-news-harding-lawson-agrees-to-takeover-by-mactec.html 18 http://archive.amecfw.com/news/2011/amec-acquires-leading-us-engineering-and-environmental-services-company-mactec 19 https://www.businessreport.com/article/bernhard-acquires-lafayette-based-environmental-consulting-engineering-firm-atc-associates

P a g e | 19

VERTEX

slowly diversify its serve offerings over the past 30 years—it now offers environmental planning,

engineering, water resources, and due diligence services.20 Although E&E went public like many

of the other noted firms in the late 1980s, it did not go on a reckless spending spree that

saddled many of the other noted firms with unmanageable debt load. While E&E remains in

business today (#96 in ENR’s Top 500 Design Firm list of 2015), its financial performance has

been lackluster—E&E’s current stock price remains less than half of what it was in the 1980s.

#84 VERSAR Inc., Springfield, VA (40% Haz Waste Work)(Survived; Dropped off of ENR’s Top

500 List): As was the trend in the 1980s for environmental firms, Versar went public to fund

future expansion. Although Versar remains in business today, its financial performance has been

poor evidenced by its stock price, which is at approximately 15% of its high water mark in the

1980s.21 Versar is no longer listed on ENR’s Top 500 Design Firm list.

#87 ABB Environmental Services, Inc., Portland, ME (95% Haz. Waste work in 1990)(Acquired

by Harding in 1998 – IT Corp. acquired Harding later that year): Little information exists about

ABB Environmental Services, Inc. (not to be confused with power giant ABB Group). Because

ABB was primarily focused on hazardous waste work, they likely struggled through the 1990s,

which likely led to Harding Associates’ acquisition of the company in 1998.

#89 Geraghty & Miller Inc., Plainview, NY (95% Haz. Waste work in 1990)(Acquired by Arcadis

in 1993): Since its incorporation in the 1970s, Geraghty & Miller focused on environmental

20 http://www.ene.com/ 21 http://www.versar.com/investors/corporate.html

P a g e | 20

VERTEX

remediation work. The firm went public in 1988 in an effort to diversify. After poor results, the

company sold out to Arcadis in 1993.22

#100 EMCON Associates, San Jose, CA (40% Haz. Waste work in 1990)(Acquired by IT Corp. in

1999): Similar to several of the firms noted above, EMCON went public in the early 1990s

(Nasdaq: MCON) in an effort to diversify into other industry sectors. EMCON’s results were

mixed and in 1999 EMCON sold out to IT Corp., which subsequently went bankrupt in 2002.

Needless to say, design firms with an overconcentration of work in a shrinking marketplace have

a very difficult time with survival. Seemingly the best solution for an AEC firm in this situation is to sell to

a more diversified design firm, similar to the exit strategy of Woodward-Clyde Group, Inc. (URS) and

Geraghty & Miller Inc. (Arcadis). A sale to another non-diversified company that is stuck in the same

industry (like IT Corp. in the examples above) is clearly not the answer. The firms that survived the

compression of the hazardous waste industry did so through downsizing and slow but steady

diversification.

X. Technological Advances that AEC Firms Must Embrace to be Competitive in the Near Future

In order to maintain competitive for new work, design firms must consistently embrace

technological advancements that improve efficiencies and bolster creative designs. Firms that resist

change will have a difficult time qualifying for future work opportunities. The following is a list of

technology trends that are affecting the way the AEC industry operates.

22 http://www.enr.com/articles/7551-james-geraghty-pioneer-of-groundwater-study-is-dead-at-90

P a g e | 21

VERTEX

A. AEC Firms will Realize Additional Benefits of BIM

Over the past decade, many AEC firms used BIM software to build 3D models to create 2D

documents, much like they did with CAD software. While the production of drawings sets from BIM

software is useful, BIM information has many other advantages that AEC firms are starting to benefit

from and this trend will continue in the near future.23

BIM can be used to:24

• Visualization through 3D renderings.

• Fabrication/shop drawings preparation (for instance, sheet metal ductwork).

• Quantity takeoff for accurate cost estimating.

• 3D construction sequencing demonstrations.

• Site logistic demonstrations.

• Conflict, interference, and collision detection (primarily used for MEP coordination).

• Forensic analysis to graphically illustrate potential failures, leaks, evacuation plans, etc.

• Assist facility managers with planning for renovations, space planning, and maintenance

operations.

The economic benefits of a full use of BIM software includes a reduction of unbudgeted change (due to

less conflicts, etc.), more accurate cost estimates, and schedule improvement.

B. Use of Unmanned Aerial Vehicles (UAVs) to Capture Existing Conditions

A considerable cost in the AEC industry is capturing existing conditions of project sites. As the

cost of UAVs continues to decrease and the related capture technology continues to advance, AEC firms

will use UAVs and capture software to collect mass data at a very low cost with a high degree of

23 http://www.architectmagazine.com/technology/seven-steps-to-bim-better_o 24 http://ascelibrary.org/doi/pdf/10.1061/(ASCE)LM.1943-5630.0000127

P a g e | 22

VERTEX

accuracy. The most widely used software that bridges UAV data with design software is Autodesk’s

ReCap 360.25 One constraint to expanded usage of this technology is FAA regulations.

C. Use of Laser Scanning to Capture Existing Conditions

Historically, the capture of existing condition data is particularly expensive on restoration

projects that involve older buildings with only hand drawn plans (if that). Similar to UAV technology, 3D

laser scanning technology is more and more affordable. 3D laser scanners typically sit on a tripod and

record a site’s shape and appearance, and then convert the conditions into a cloud of data points that

can be imported into a BIM model.26 Large contractors such as Gilbane and DPR have recently used laser

scanning equipment to efficiently capture data and create BIM models on project where limited to no

data existed previously.27

D. Virtual and Augmented Reality

BIM software developers believe that AEC firms will need to adopt virtual and augmented reality

as building owners and property managers will want to “experience a building’s design before it was

ever built.”28 Virtual and augmented reality will go far beyond today’s 360-degree visualizations of a

project; once this process goes mainstream, owners will be able to see what is behind walls and in

closed spaces through head mounted display units.29

Augmented reality is a blend of virtual reality and real life. With augmented reality, users can

interact with virtual content in the real world and can distinguish between the two. Virtual reality, on

the other hand, makes it difficult for the user to distinguish between what is real and what is not.

25 http://www.prnewswire.com/news-releases/microdesk-reveals-top-trends-for-2015-that-will-shape-the-aec-industry-300003320.html 26 https://lineshapespace.com/how-laser-scanning-helps-a-building-company-save-time-and-money/ 27 Id. 28 http://www.microdesk.com/Newsroom/Recent-Coverage/Details/ArticleID/850/Microdesk-Reveals-Top-Trends-For-2015-That-Will-Shape-The-AEC-Industry 29 http://www.techtimes.com/articles/5078/20140406/augmented-reality-vs-virtual-reality-what-are-the-differences-and-similarities.htm

P a g e | 23

VERTEX

E. BIM Processes Will Revolutionize Building Delivery Via Prefabrication

Project teams are starting to use BIM to improve schedule and cost by prefabricating many

building components such as mechanical lines, plumbing infrastructure, restroom pods, framed interior

partitions, and exterior veneer panels.30 The prefabrication is typically done in a nearby factor rather

than on a hectic jobsite.31

This trend has taken off in Southeast Asia. Over the past six years, Chinese company Broad

Sustainable Building Company (“BSB”) has completed three record breaking projects due to advanced

prefabrication techniques. In 2010 BSB constructed Ark hotel, a 15 story building, in 48 hours.32 In 2011,

BSB erected T-30, a 30 story hotel, in 15 days.33 And in 2015, BSB completed J57, a 57 stories mixed use

building, in just 19 days.34 One of BRB’s projects, Sky City, is currently on hold. If this project moves

forward, BRB plans to construct the tallest building in the world (220 floors) in just 90 days. BRB is

starting to license its technology worldwide.35

F. Improved Energy Performance Modeling

Energy modeling such as daylighting and airflow models is typically a lengthy and cost

prohibitive exercise that is performed by specialty consultants; this is changing. New software by

Autodesk and Sefaira is available that allows for energy modeling during the conceptual phase of design.

This allows designers to make subtle design changes such as detailing shading devices or other options

based on simulated energy performance, which prevents costly revisions towards the tail end of a

design process.36 Autodesk’s FormIt software allows users to calculate “energy-performance feedback

30 https://soundcloud.com/autodeskaec/phil-bernstein-commentary-your-next-building-wont-be-builtit-will-be-manufactured 31 http://www.bdcnetwork.com/5-tech-trends-transforming-bimvdc 32 https://www.youtube.com/watch?v=Ps0DSihggio 33 https://www.youtube.com/watch?v=C2K53T81FEs&index=2&list=PLiwZ62tpFvnh4eNmGUVCFO4uj_hZJON3b 34 https://www.youtube.com/watch?v=veNf-bz99cI 35 http://www.constructionweekonline.com/article-19593-broad-sticks-to-90-day-worlds-tallest-target/ 36 http://www.bdcnetwork.com/5-tech-trends-transforming-bimvdc#sthash.rJpWVpZ2.dpuf

P a g e | 24

VERTEX

on early design decisions, such as building orientation, thermal performance, and massing.”37 Results

can be imported into Revit.

G. Cloud Based Data Storage Will Improve Collaboration

Historically, architects would store BIM files on his or her PC, which took up considerable hard

drive space. Now that more and more data is shifting to the cloud, the sharing of project data is

becoming is more efficient. Software companies such as Assemble Systems and Panzura have developed

cloud-based tools for advanced data management, which include data storage, consolidation, archiving,

heightened access, and security.38 39

H. 3D-Printed Architectural Models

Owners rarely approve funding for architectural models due to the expense and time required

for creation. However, with the introduction of low cost 3D printing technology, physical models are

now practical. Prices for 3D printers range from several hundred dollars to several thousand dollars for

lower to mid end models. Accordingly, the popularity of architectural models will rapidly increase over

the next several years.

The creation of architectural models has many benefits including:4041

• 3D model provide a visual perspective that cannot be achieved with blueprints, drawings, or

digital 3D models.

• Architectural models can be 3D printed in full-color for inspiring presentations and displays.

• 3D models help the communication between architects and contractors to better ensure desired

results that can help avoid expensive changes during the course of construction.

37 http://www.bdcnetwork.com/5-tech-trends-transforming-bimvdc 38 http://panzura.com/products/global-fi le-system/ 39 http://assemblesystems.com/ 40 http://www.3ders.org/3d-printing.html 41 https://www.whiteclouds.com/blog/benefits-3d-printed-architectural-models

P a g e | 25

VERTEX

• Architectural models make effective public displays that help market the project to investors

and/or tenants.

• Architectural scale models quickly communicate design concepts and allow people to easily

comprehend a project.

I. Use of Composites in Construction

Composite material is typically a mix of glass, aramid, and carbon fibers. Recent advances in

composite technology allow parts to be cured at lower pressures and temperatures, which in turn

lowers the cost of production and allows for increasing sizes of manufactured parts.42 This change has

increased the use of composites in the building industry.43 The benefit of composites include: flexibility

of form, structural capacity, durability, and life-cycle cost.

Typical applications of for composite material in construction include structural members for

bridges, hydraulic structures, and cladding material. Composite cladding can be insulated to form

sandwich panels that have efficient thermal, weather barrier, and sound properties. The main economic

benefit of composites stem from its low-weight / high-strength material properties, which can cause a

reduction in the cost of supporting structures. As the composite manufacturing process continues to

improve so will the adoption of composites into more and more construction projects.

XI. Conclusions

Diversification is a key for continued growth of large AEC firms. Failure to diversify caused many

noteworthy firms to fail over the past five decades. Moreover, AEC firms must position themselves for

international work in order to broaden their reach to maintain above average revenue progression.

Lastly, successful design firms embrace, not resist, technological advances such as the evolution from 2-

42 http://www.azom.com/article.aspx?ArticleID=1425 43 Id.

P a g e | 26

VERTEX

D to 3-D drafting and now to 4-D modeling. Changes in technology over the next decades will be drastic

and firms that ignore the efficiencies and creativity offered by such advancements will be left behind.