Embed Size (px)

Citation preview

KBC ADVANCED TECHNOLOGIESProprietary Information

SUPERIOR RESULTS. SUSTAINED.

Refiners’ Best Remaining Options for Responding to the IMO 2020 Regulations

4 August 2017

2

Before We Get Started…

• All lines have been muted on entry to avoid any noise interference

• The webinar is approximately 45 minutes

• A follow up email will be sent out with the webinar slides

• Please submit all questions through the Questions pane on the right hand side of your screen

KBC ADVANCED TECHNOLOGIESProprietary Information 4 August 2017

3

Your Presenter Today

KBC ADVANCED TECHNOLOGIESProprietary Information

Andy RobertsGlobal Practice ExecutiveProduction Optimization

4 August 2017

4

How We Got to This Point• Current max specification for ocean-going vessels is emissions equivalent to burning

3.5 wt% sulphur bunker fuel (HSFO) with no abatement. In much of Northern Europe, more stringent ECA rules apply (max 0.1 wt% sulphur equivalent)

• 2015 study by CE Delft commissioned by the International Maritime Organization (IMO) determined that it was feasible to adopt lower sulphur emissions from the initial proposed date

• IMO meeting Oct 2016 adopted max emissions at 0.5 wt% sulphur equivalent effective 1 Jan 2020 Time is already running out to meet this challenging target

• MEPC 71 July 2017: (Marine Environmental Pollution Committee of the IMO) reaffirmed the 2020 deadline “The Sub-Committee on Pollution Prevention and Response (PPR) has been instructed to explore what actions

may be taken to ensure consistent and effective implementation of the 0.50% m/m sulphur limit for fuel oil used by ships operating outside designated SOX Emission Control Areas and/or not making use of equivalent means such as exhaust gas cleaning systems; as well as actions that may facilitate the implementation of effective policies by IMO Member States”

KBC ADVANCED TECHNOLOGIESProprietary Information 4 August 2017

5

Burden of Compliance Has Fallen on the Refiners• KBC press release……

‘While the shipping industry expects the refiners to meet their supply requirements, the refining industry is still waiting to know to what extent the shipping industry will install emission ‘scrubbers’ on board’…..

- Stephen George KBC Chief Economist

• Maersk Shipping…… "In our opinion, scrubbers will not be the way forward for our fleet. Whilst the business case for investing in

scrubbers may look appealing at first, it is not a long-term solution to place such complex machinery on our vessels”

“Scrubbers require high maintenance and specialised personnel for a "relatively mitigated" health and environmental result. Moreover, scrubbers, by allowing the continuous use of cheaper fuels, may in addition ruin any kind of broader business case for enhancing energy efficiency”

“Maersk consequently prefers to take a longer term approach to secure compliance through the use of alternative fuels. Only this will ensure a swift and effective compliance for the 2020 Global Sulphur Cap.“…..

- Niels Henrik Lindegaard, Head of Maersk Oil Trading (the world’s largest container shipping company

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

6

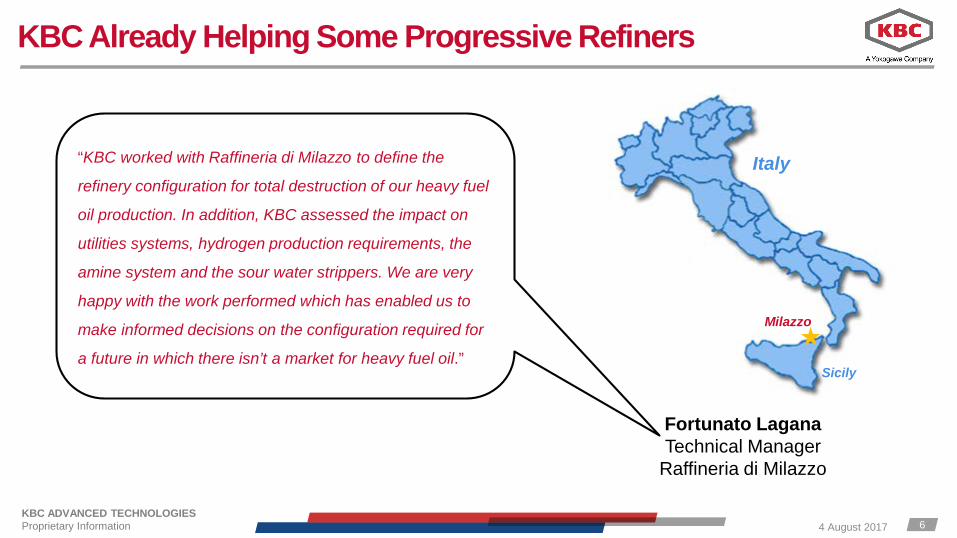

KBC Already Helping Some Progressive Refiners

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

Fortunato LaganaTechnical Manager

Raffineria di Milazzo

“KBC worked with Raffineria di Milazzo to define the

refinery configuration for total destruction of our heavy fuel

oil production. In addition, KBC assessed the impact on

utilities systems, hydrogen production requirements, the

amine system and the sour water strippers. We are very

happy with the work performed which has enabled us to

make informed decisions on the configuration required for

a future in which there isn’t a market for heavy fuel oil.”

Italy

Sicily

Milazzo

7

Do Spare a Thought for the Middlemen!

• The ‘bunkering’ industry… often forgotten in the debate of shipping vs refining response to IMO 2020 regulation

• Small and large suppliers of bunker fuels also face challenges including Managing the potential increase in choices and the impact on logistics Blending complications Fuel certification Delivery (bunker barges) systems

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

8

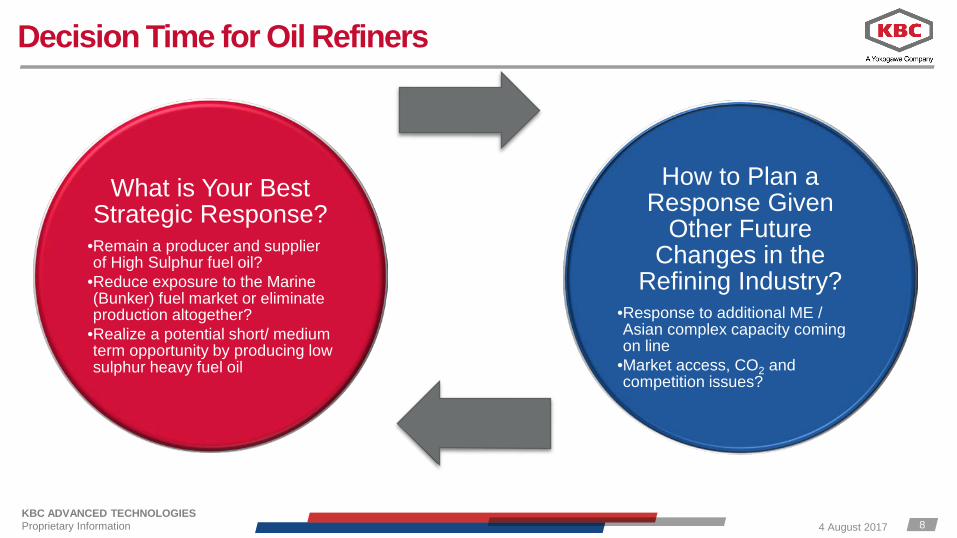

Decision Time for Oil Refiners

What is Your Best Strategic Response?

•Remain a producer and supplier of High Sulphur fuel oil?

•Reduce exposure to the Marine (Bunker) fuel market or eliminate production altogether?

•Realize a potential short/ medium term opportunity by producing low sulphur heavy fuel oil

How to Plan a Response Given

Other Future Changes in the

Refining Industry?•Response to additional ME / Asian complex capacity coming on line

•Market access, CO2 and competition issues?

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

9

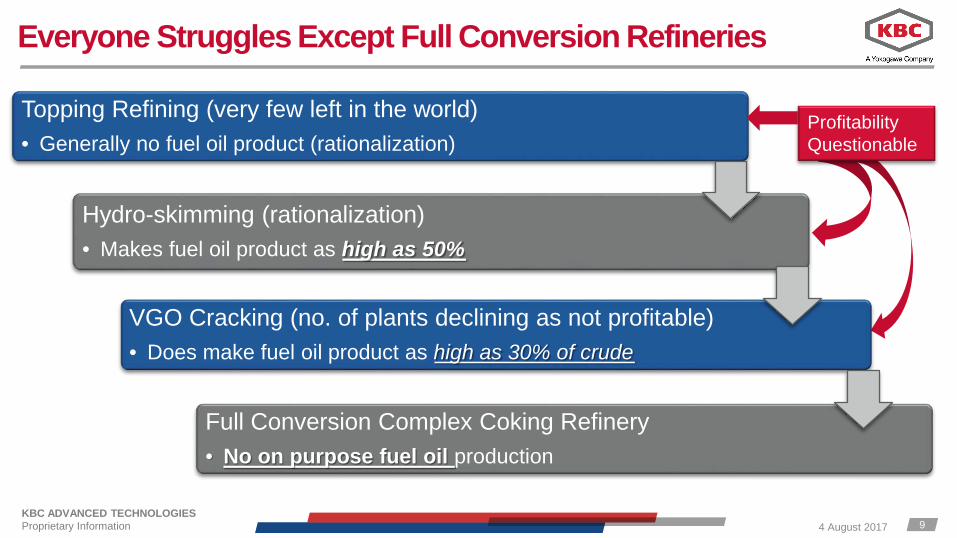

Topping Refining (very few left in the world)• Generally no fuel oil product (rationalization)

Hydro-skimming (rationalization)• Makes fuel oil product as high as 50%

VGO Cracking (no. of plants declining as not profitable)• Does make fuel oil product as high as 30% of crude

Full Conversion Complex Coking Refinery• No on purpose fuel oil production

Everyone Struggles Except Full Conversion Refineries

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

Profitability Questionable

10

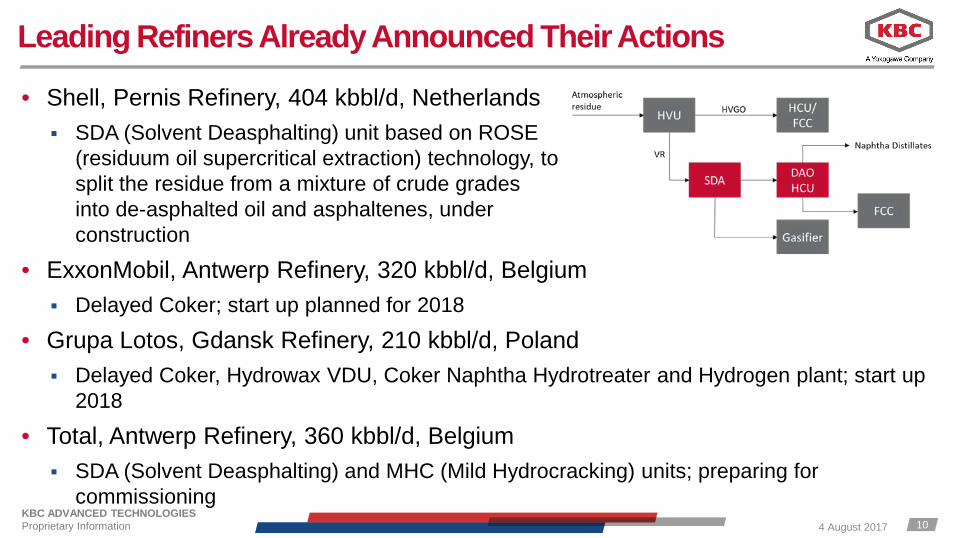

Leading Refiners Already Announced Their Actions

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

• Shell, Pernis Refinery, 404 kbbl/d, Netherlands SDA (Solvent Deasphalting) unit based on ROSE

(residuum oil supercritical extraction) technology, tosplit the residue from a mixture of crude grades into de-asphalted oil and asphaltenes, under construction

• ExxonMobil, Antwerp Refinery, 320 kbbl/d, Belgium Delayed Coker; start up planned for 2018

• Grupa Lotos, Gdansk Refinery, 210 kbbl/d, Poland Delayed Coker, Hydrowax VDU, Coker Naphtha Hydrotreater and Hydrogen plant; start up

2018

• Total, Antwerp Refinery, 360 kbbl/d, Belgium SDA (Solvent Deasphalting) and MHC (Mild Hydrocracking) units; preparing for

commissioning

11

…and More

• Preem, Sweden LC-Slurry residue conversion and Isocracking plant for Preemraff Goteborg, 100

kbd, by CB&I / Chevron Lummus Global under study New Vacuum Distillation Unit at Preemraff Lysekil, 220 kbd, under construction

• MOL/INA, Rijeka Refinery, 102 kbbl/d, Croatia Bechtel Delayed Coker under study

• Eni, Sannazzaro De Burgondi Refinery, 180 kbbl/d, Italy EST (‘Eni Slurry Technology’) heavy oil conversion unit, 23 kbbl/d

• Gazpromneft / NIS, Pancevo Refinery, 98 kbbl/d, Serbia Delayed Coker under design

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

12

KBC Insight Reveals Additional Unannounced Actions

• North West Europe – Delayed Coker installation• Central Europe – Revamping units to increase ‘residue destruction’

capability• Mediterranean – Crude oil blending strategy• Mediterranean – FCC Reconfiguration to process heavier feedstock• Mediterranean – Out of region fuel oil trading strategy• Mediterranean – Potential preferred supplier of emulsified fuel oil for

marine use

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

13

What to do With the Surplus Residues?

• Alternate outlets for higher sulphur residues?• Change crude supply strategies to reduce ‘sulphur in feeds’?• Change refinery operations, ‘repurpose units’ to focus on lower sulphur

fuel oil production?• Accept the ‘downgrade’ of lower sulphur blendstocks to dilute the higher

sulphur residues?

All the above (except the first ) require ‘molecular management’ and detailed blending analysis

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

14

Power Plants are Not Going to Soak up Surplus Residues

• The frontlines for additional emissions reductions are in the power sector, via accelerated deployment of renewables, nuclear power (where politically acceptable) and carbon capture and storage; a strong push for greater electrification and efficiency across all end-uses; and a robust and concerted clean energy research and development effort by governments and companies’

• ‘In the power sector, the cost of pollution controls, maintenance, and RFO heating often offset the lower cost of RFO in comparison with natural gas and other more expensive fuels. Consequently, power sector demand for RFO, especially in industrialized countries, is expected to decrease, although it may continue to serve as a transitional fuel in the power sectors of non-OECD countries that may be more sensitive to price and less sensitive to environmental and health implications’

Source: IEA World Energy Outlook 2016

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

15

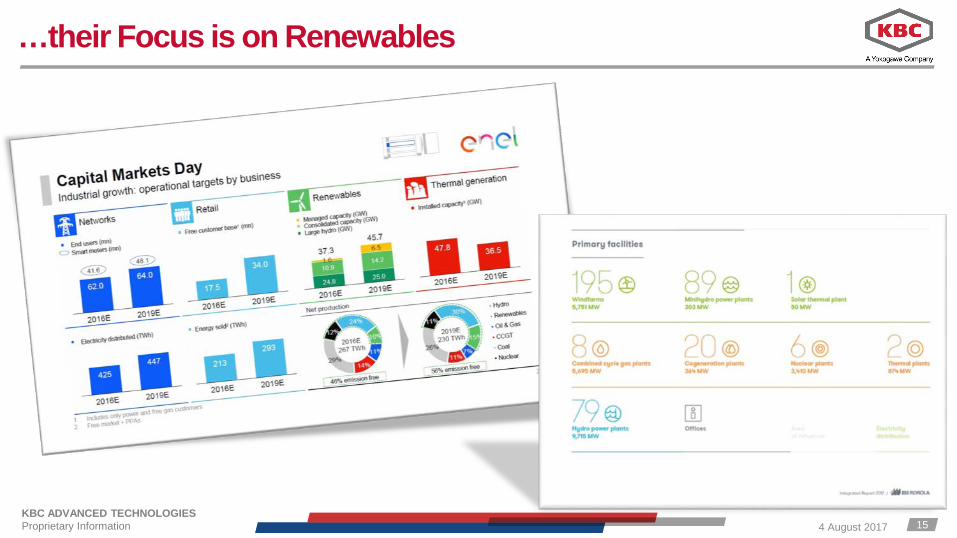

…their Focus is on Renewables

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

16

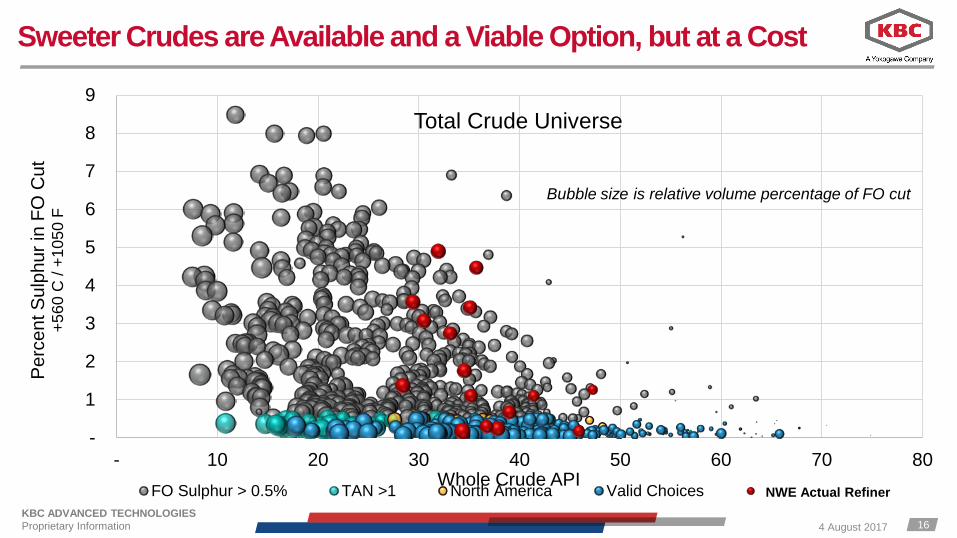

Sweeter Crudes are Available and a Viable Option, but at a Cost

-

1

2

3

4

5

6

7

8

9

- 10 20 30 40 50 60 70 80

Per

cent

Sul

phur

in F

O C

ut+5

60 C

/ +1

050

F

Whole Crude API

Total Crude Universe

FO Sulphur > 0.5% TAN >1 North America Valid Choices HELPE Actual

Bubble size is relative volume percentage of FO cut

NWE Actual RefinerKBC ADVANCED TECHNOLOGIESProprietary Information 4 August 2017

17

Repurposing Refining Units May be an Option for a Few

• Hydro-desulphurisation unit strategies

• Residue desulphurisation strategies

• FCC operational strategies

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

18

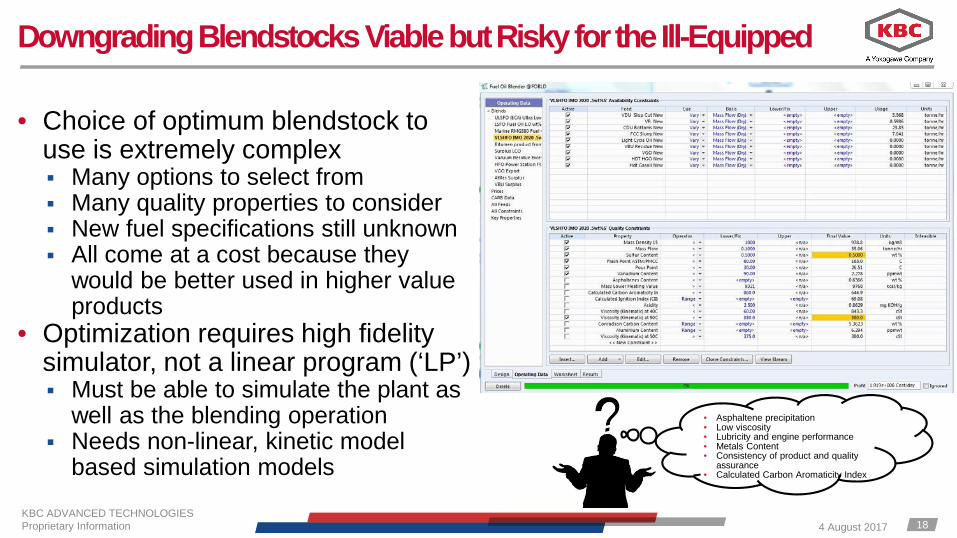

Downgrading BlendstocksViable but Risky for the Ill-Equipped

• Choice of optimum blendstock to use is extremely complex Many options to select from Many quality properties to consider New fuel specifications still unknown All come at a cost because they

would be better used in higher value products

• Optimization requires high fidelity simulator, not a linear program (‘LP’) Must be able to simulate the plant as

well as the blending operation Needs non-linear, kinetic model

based simulation models

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

• Asphaltene precipitation• Low viscosity• Lubricity and engine performance• Metals Content• Consistency of product and quality

assurance• Calculated Carbon Aromaticity Index

19

Rigorous Simulation Shows Magnitude of the Challenge

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

• KBC’s leading process simulator, Petro-SIM, has been used to illustrate some studies• The case studies to follow are based on modelling an FCC and Mid-distillate and Fuel Oil Blenders

20

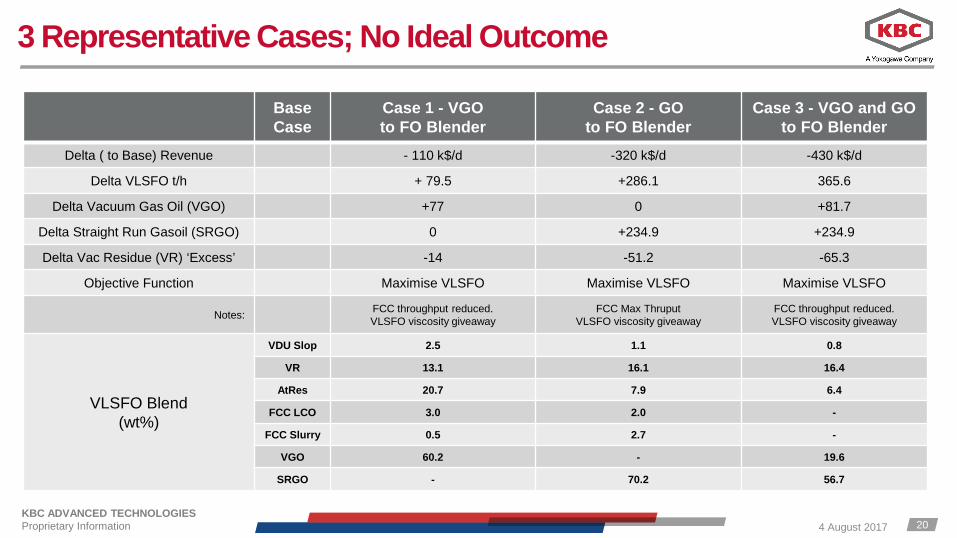

3 Representative Cases; No Ideal Outcome

Base Case

Case 1 - VGO to FO Blender

Case 2 - GO to FO Blender

Case 3 - VGO and GO to FO Blender

Delta ( to Base) Revenue - 110 k$/d -320 k$/d -430 k$/d

Delta VLSFO t/h + 79.5 +286.1 365.6

Delta Vacuum Gas Oil (VGO) +77 0 +81.7

Delta Straight Run Gasoil (SRGO) 0 +234.9 +234.9

Delta Vac Residue (VR) ‘Excess’ -14 -51.2 -65.3

Objective Function Maximise VLSFO Maximise VLSFO Maximise VLSFO

Notes: FCC throughput reduced. VLSFO viscosity giveaway

FCC Max ThruputVLSFO viscosity giveaway

FCC throughput reduced. VLSFO viscosity giveaway

VLSFO Blend(wt%)

VDU Slop 2.5 1.1 0.8

VR 13.1 16.1 16.4

AtRes 20.7 7.9 6.4

FCC LCO 3.0 2.0 -

FCC Slurry 0.5 2.7 -

VGO 60.2 - 19.6

SRGO - 70.2 56.7

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

21

Now is the Time to Act

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information

• The oil industry is resilient with the capability to adjust hardware and catalyst to meet the challenges of clean fuels to lower emissions.

• The technology solution is present, to meet low emissions in SOx and CO2compliance for bunker fuels, if appropriate investment decisions are made

Two questions1. How will your facility remain profitable at low refining complexity?2. How will you be able to produce at the new market price reality?

• There is still time to analyze your specific situation / asset mix to determine your best course of action…… but this should now be done urgently

• Only hi-fidelity, non-linear process simulation tools with well configured product blenders will give you the optimum answer

22

Identify the Best Option for Your Refinery

• Book a 1 day on-site workshop with a KBC subject matter expert Detailed assessment of the market impacts

specific to your region and refinery Assessment of your potential degree of economic

exposure Consideration of the various potential responses to

the threats and opportunities presented by the IMO 2020 regulation

Proposed action plan outlining potential operational changes and capital investments

• Email: [email protected]

4 August 2017KBC ADVANCED TECHNOLOGIESProprietary Information