Rural Finance Development Project (RRP BHU 53307)

Bhutan Development Bank

Institutional Strengthening Plan

TABLE OF CONTENTS

TABLE OF CONTENTS ..................................................................................................................... I

TABLES ........................................................................................................................................ II

FIGURES ...................................................................................................................................... IV

PREFACE AND DISCLAIMER ........................................................................................................... V

ABBREVIATIONS .......................................................................................................................... VI

EXECUTIVE SUMMARY ................................................................................................................. 1

1 BHUTAN ................................................................................................................................. 2

2 BACKGROUND, SUMMARY DATA AND FINANCIAL HIGHLIGHTS ............................................... 6

3 STRATEGIC PLANNING ............................................................................................................ 7

4 GOVERNANCE ...................................................................................................................... 10

5 ORGANIZATIONAL STRUCTURE ............................................................................................. 13

6 HUMAN RESOURCES ............................................................................................................. 15

7 INFORMATION TECHNOLOGY ............................................................................................... 19

8 INTERNAL AUDIT .................................................................................................................. 21

9 RISK MANAGEMENT ............................................................................................................. 25

10 PRODUCTS ........................................................................................................................... 26

11 COMMUNITY CENTERS ......................................................................................................... 40

12 CREDIT ................................................................................................................................ 41

13 FINANCIAL AND OPERATIONAL PERFORMANCE ..................................................................... 51

14 BDB INSTITUTIONAL STRENGTHENING/FINANCIAL STRENGTHENING PLAN - KEY ACTIONS ..... 59

ii

15 POLICY MATRIX BHUTAN RURAL FINANCE SECTOR DEVELOPMENT PROGRAM ............... ERROR!

BOOKMARK NOT DEFINED.

16 BHUTAN DEVELOPMENT BANK OPERATIONAL INSTITUTIONAL STRENGTHENING PLAN KEY

PERFORMANCE TARGETS ........................................................................................................... 67

ANNEX I – MEETING PARTICIPANTS ............................................................................................ 68

ANNEX II - FINANCIAL RATIOS DEFINITION .................................................................................. 69

ANNEX III – BDB FINANCIAL PROJECTIONS .................................................................................. 70

ANNEX IV – INDICATIVE TERMS OF REFERENCE DEPUTY CEO IN CHARGE OF CREDIT OPERATIONS 74

ANNEX V – BDB MANAGEMENT COMMENTS .............................................................................. 76

TABLES

Table 1 - Financial Sector. Evolution of Main Figures and Indicators .................................... 2

Table 2 - Bhutan Banking Sector – Financial Highlights by Bank .......................................... 3

Table 3 - Loan Classification - RMA Regulation .................................................................... 4

Table 4 - BDB Summary Data and Financial Highlights ........................................................ 6

Table 5 - 2015-2019 Business Plan Targets vs Actual ........................................................ 10

Table 6 - Personnel Number and Turnover ......................................................................... 15

Table 7 - Cases of Fraud in the Last Five Years ................................................................. 23

Table 8 - Savings Accounts Interest Rate 2019................................................................... 26

Table 9 - Bhutan Banks Savings Account Interest Rate December 2019 ............................ 26

Table 10 - BDB and Competitors Individual Term Deposit Rates as of December 2019 ...... 27

Table 11 – BDB and Competitors Corporate Term Deposit Rates. December 2019 ............ 27

Table 12 - List of Loan Products – Total Gross Loan Outstanding ...................................... 31

Table 13 – Main Products – Term and Rates ...................................................................... 32

Table 14 - Grace Period Criteria ......................................................................................... 32

Table 15 - Summary Data on Selected Loan Products as of June 30, 2019 ........................ 34

Table 16 - Group Guarantee Lending Accounts - June 2019 ............................................... 35

Table 17 - Loan Classification by Size ................................................................................ 35

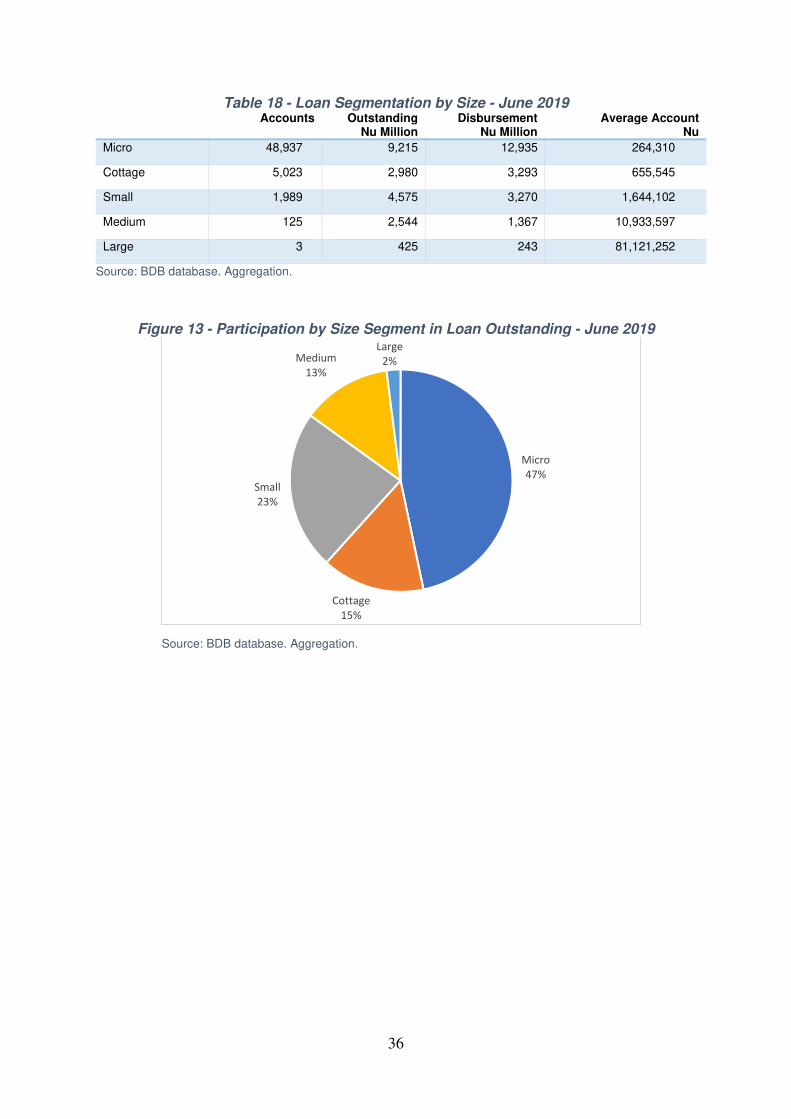

Table 18 - Loan Segmentation by Size - June 2019 ............................................................ 36

Table 19 - Loan Interest Rates Across Banks – June 2019 ................................................. 37

Table 20 - Loans by Size and Product Type ........................................................................ 38

Table 21 - Portfolio Quality Evolution – Summary ............................................................... 41

Table 22 - Branches with Largest NPLs as of June 2019 .................................................... 44

Table 23 – Indicative Write Off Exercise of Legacy Loan Losses – June 2019 .................... 46

Table 24 – Loan Approval Limits ......................................................................................... 48

Table 25 - NPL by Approval Segment Sanctioned Loans – June 2019 ............................... 48

Table 26 - BDB Ratio Benchmarking with Countries in South and East Asia ....................... 53

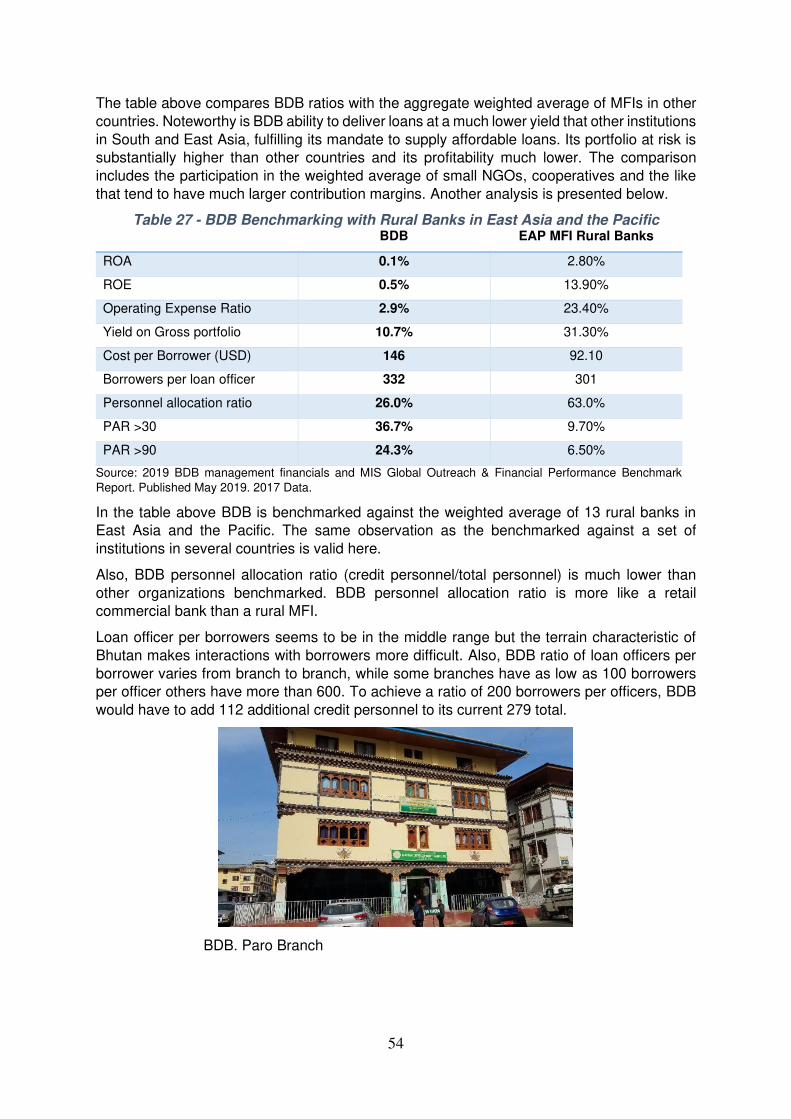

Table 27 - BDB Benchmarking with Rural Banks in East Asia and the Pacific ..................... 54

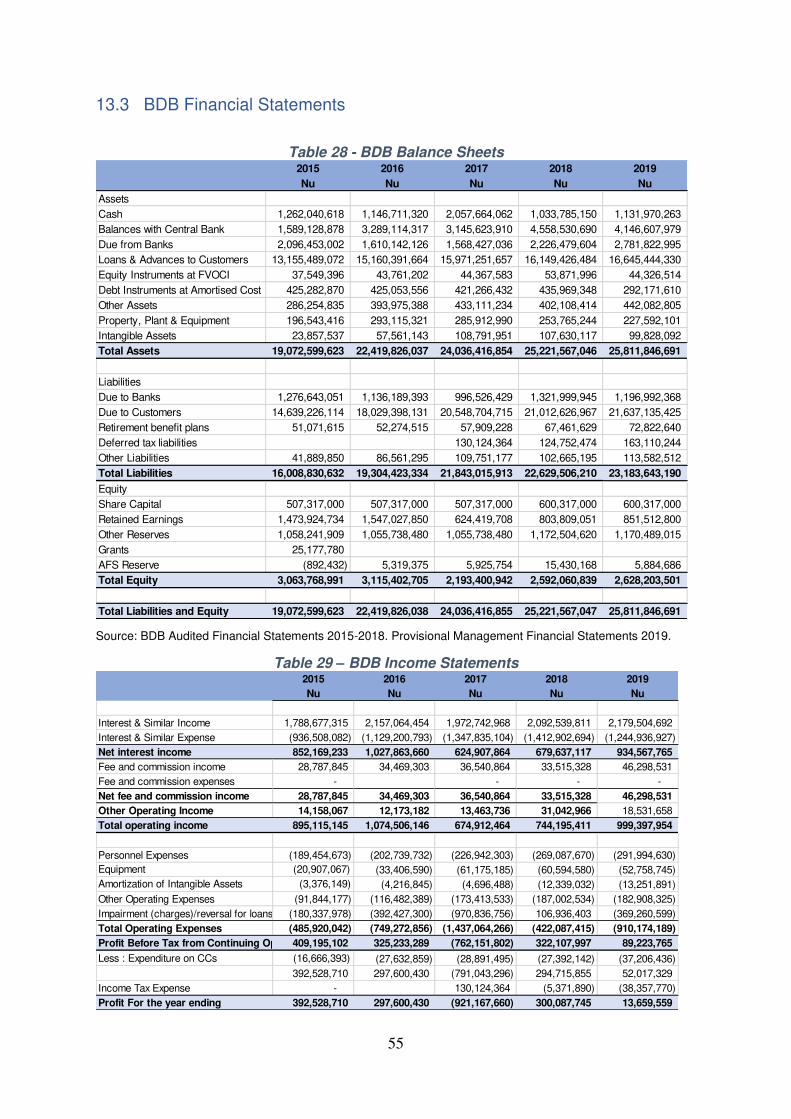

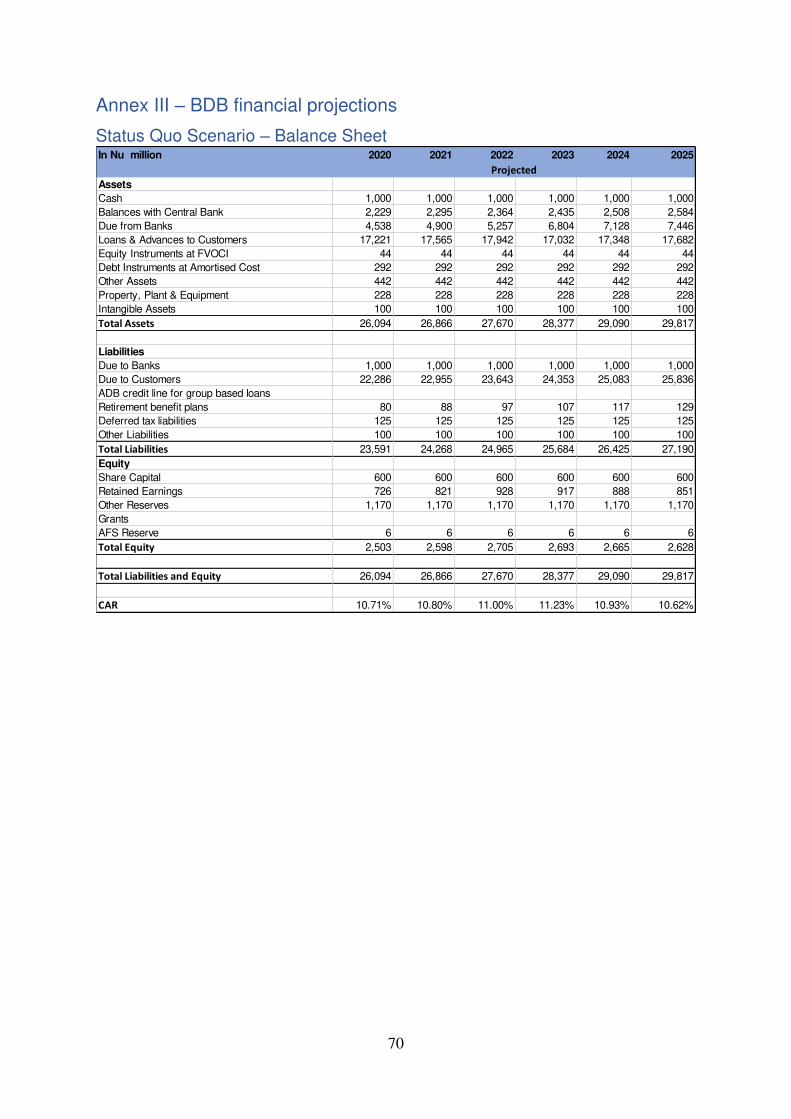

Table 28 - BDB Balance Sheets .......................................................................................... 55

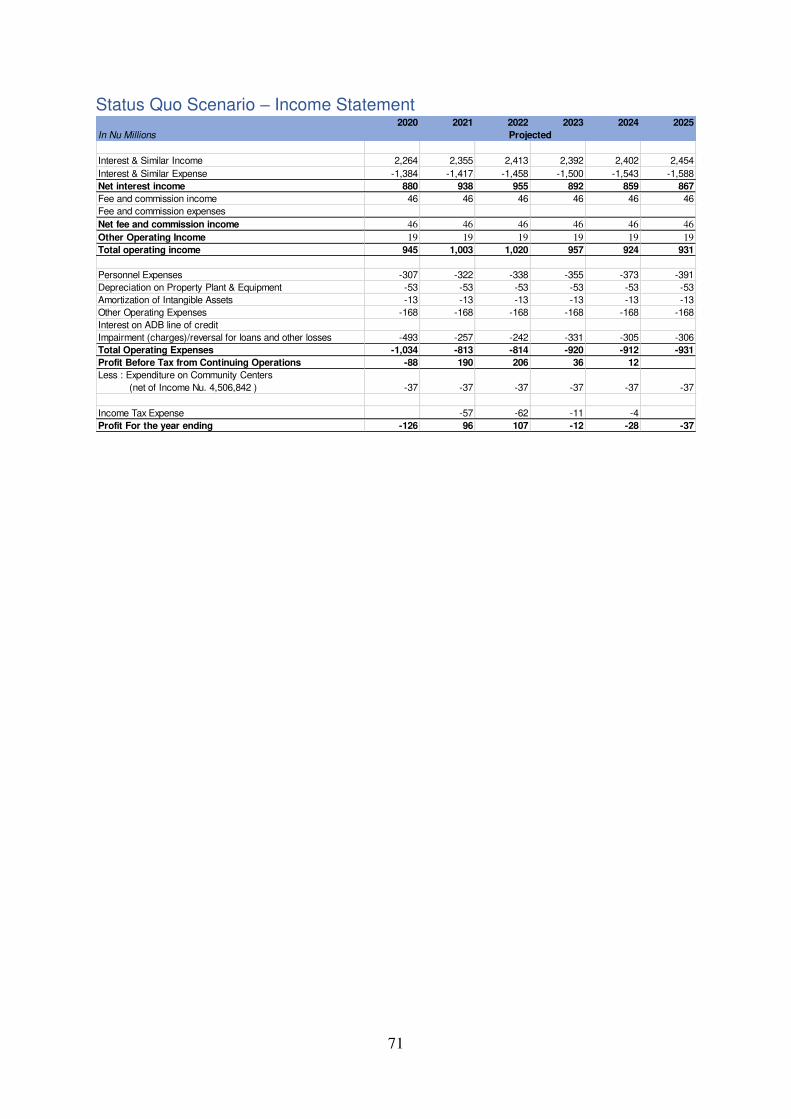

Table 29 – BDB Income Statements ................................................................................... 55

iii

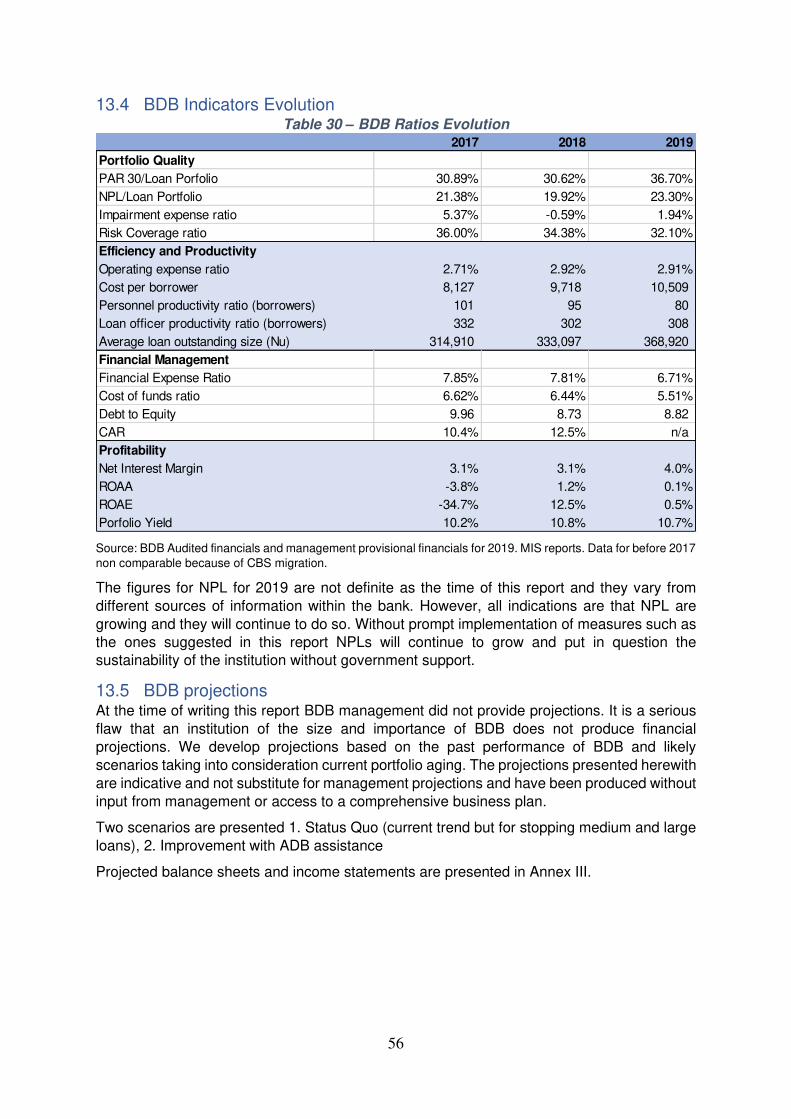

Table 30 – BDB Ratios Evolution ........................................................................................ 56

Table 31 – BDB Status Quo Scenario assumptions ............................................................ 57

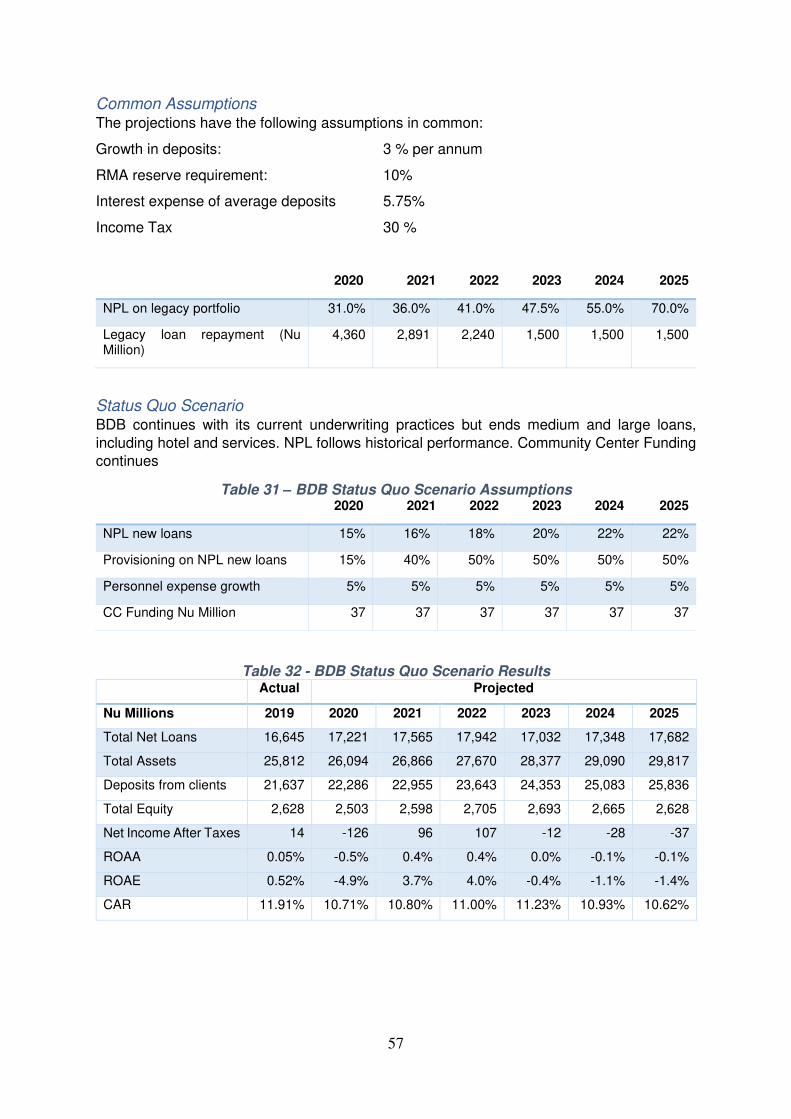

Table 32 - BDB Status Quo Scenario Results ..................................................................... 57

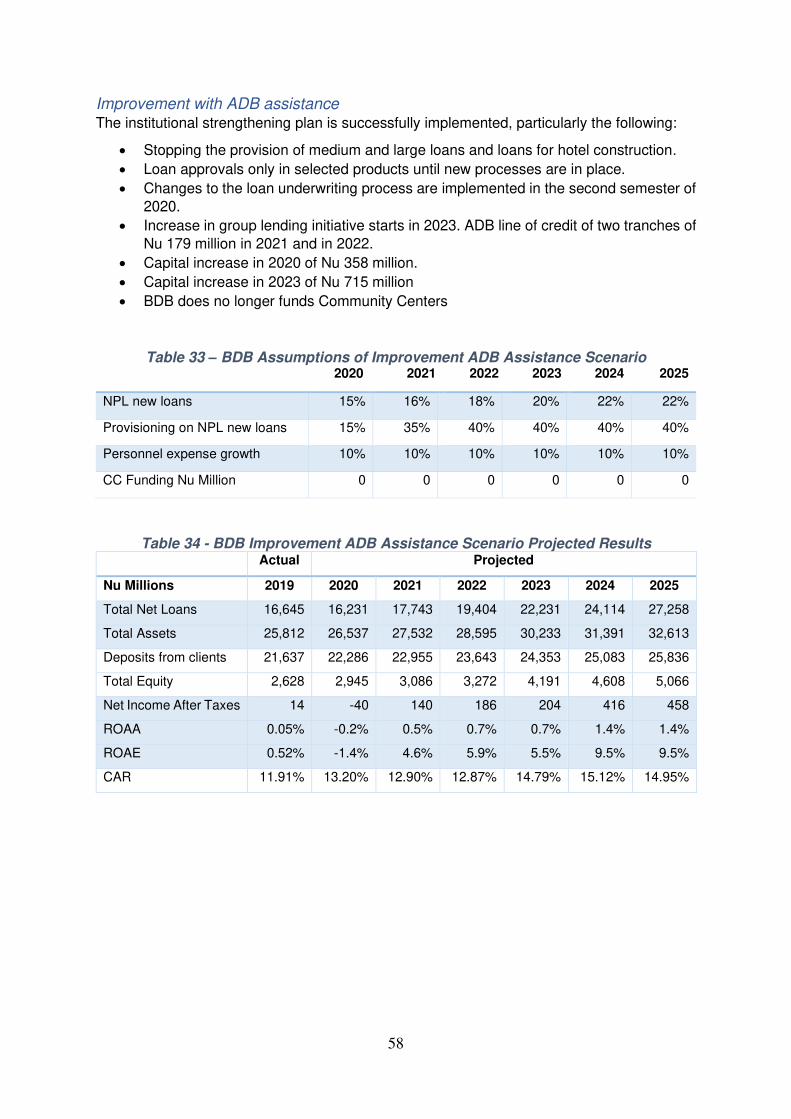

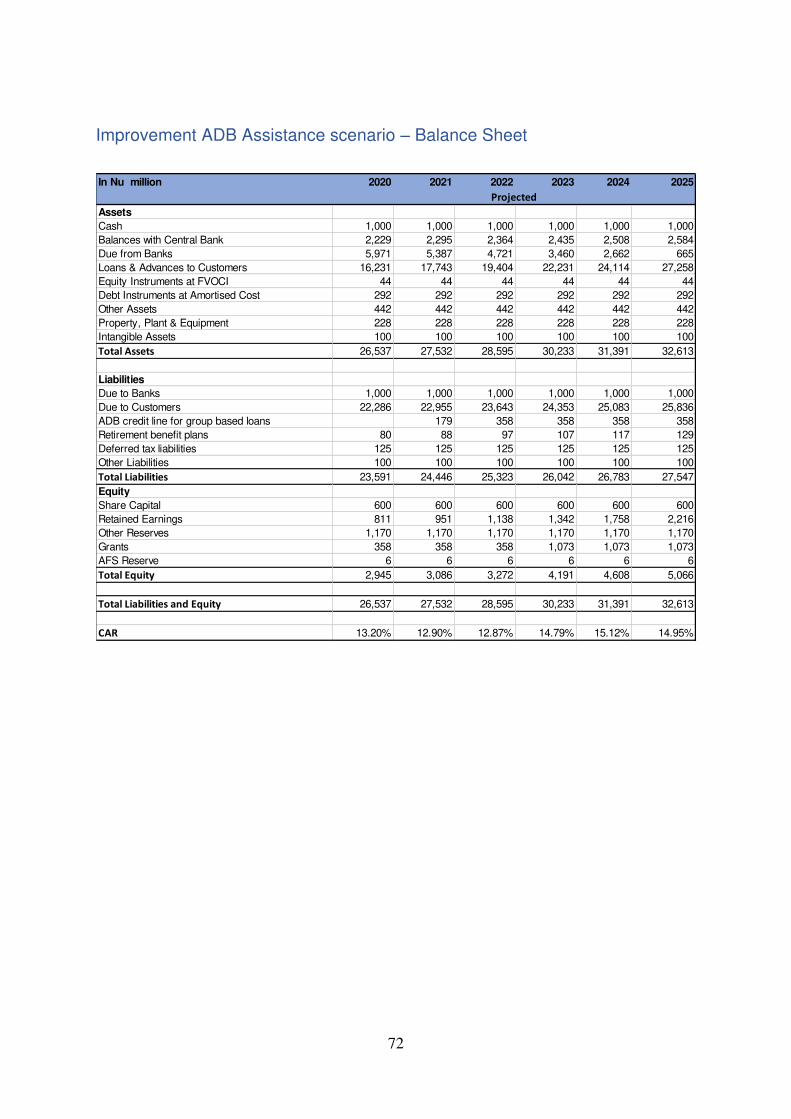

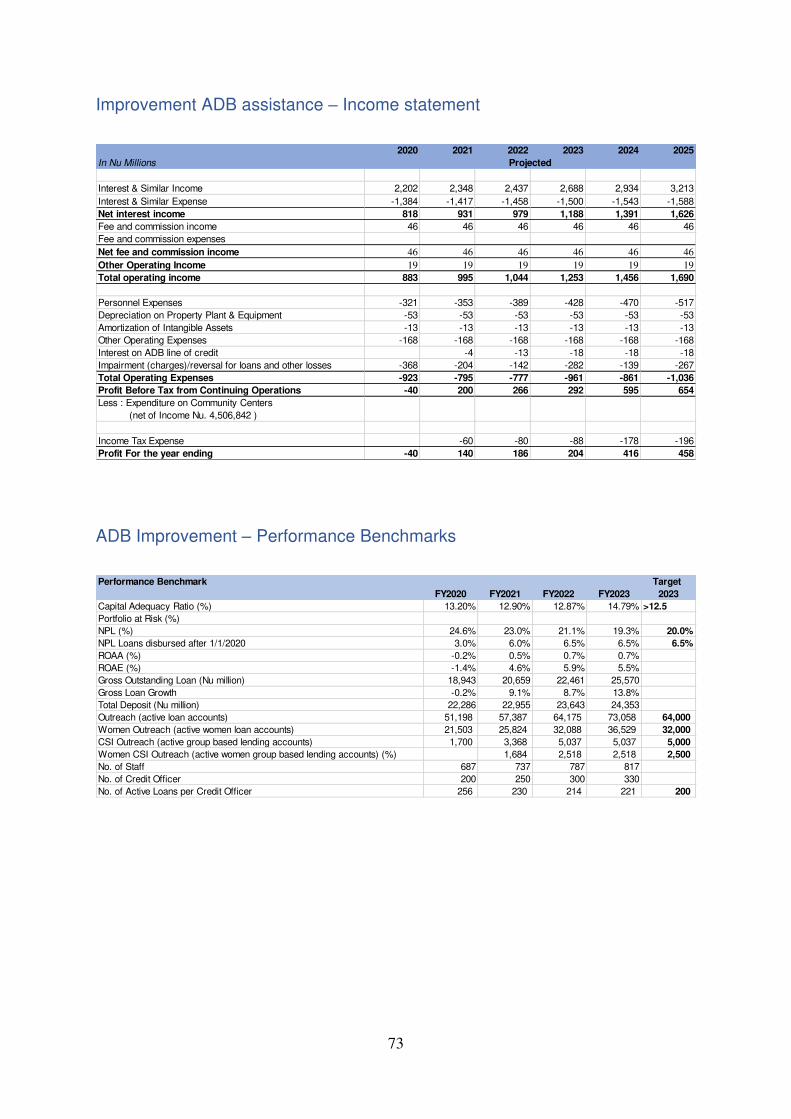

Table 33 – BDB Assumptions of Improvement ADB Assistance Scenario ........................... 58

Table 34 - BDB Improvement ADB Assistance Scenario Projected Results ........................ 58

Table 35 - Summary of Proposed Actions ........................................................................... 63

iv

Figures

Figure 1 - GNI per Capita Evolution (Current US$) ............................................................... 2

Figure 2 - Financial System. Evolution of Loans and NPL Ratio ............................................ 3

Figure 3 – Word Cloud Example ........................................................................................... 7

Figure 4 - Example of SWOT Analysis for BDB ..................................................................... 9

Figure 5 - BDB Organization Chart ...................................................................................... 13

Figure 6 - Proposed Organization ....................................................................................... 14

Figure 7 - Total Staff Evolution ............................................................................................ 15

Figure 8 – Deposits Market Share as of December 2018 .................................................... 28

Figure 9 - System Deposits and BDB Share Evolution ........................................................ 28

Figure 10 – BDB Deposit Evolution ..................................................................................... 28

Figure 11 - Share of Largest Loan Products ........................................................................ 30

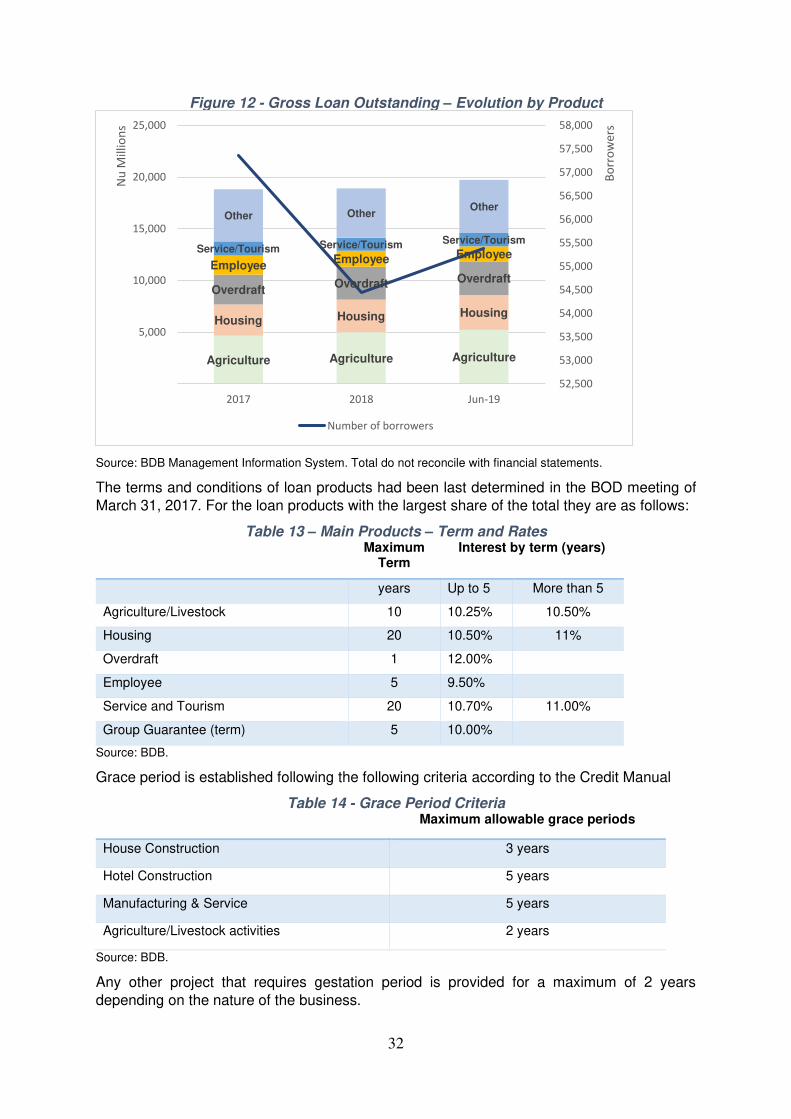

Figure 12 - Gross Loan Outstanding – Evolution by Product ............................................... 32

Figure 13 - Participation by Size Segment in Loan Outstanding - June 2019 ...................... 36

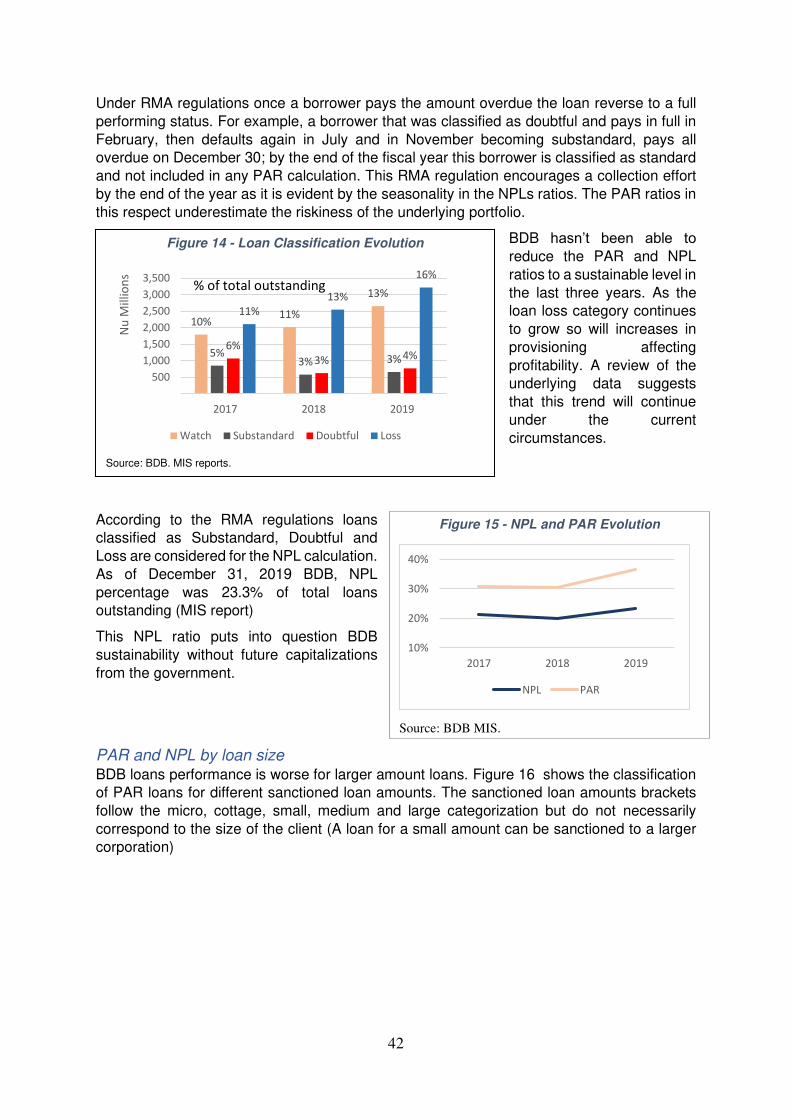

Figure 14 - Loan Classification Evolution ............................................................................ 42

Figure 15 - NPL and PAR Evolution .................................................................................... 42

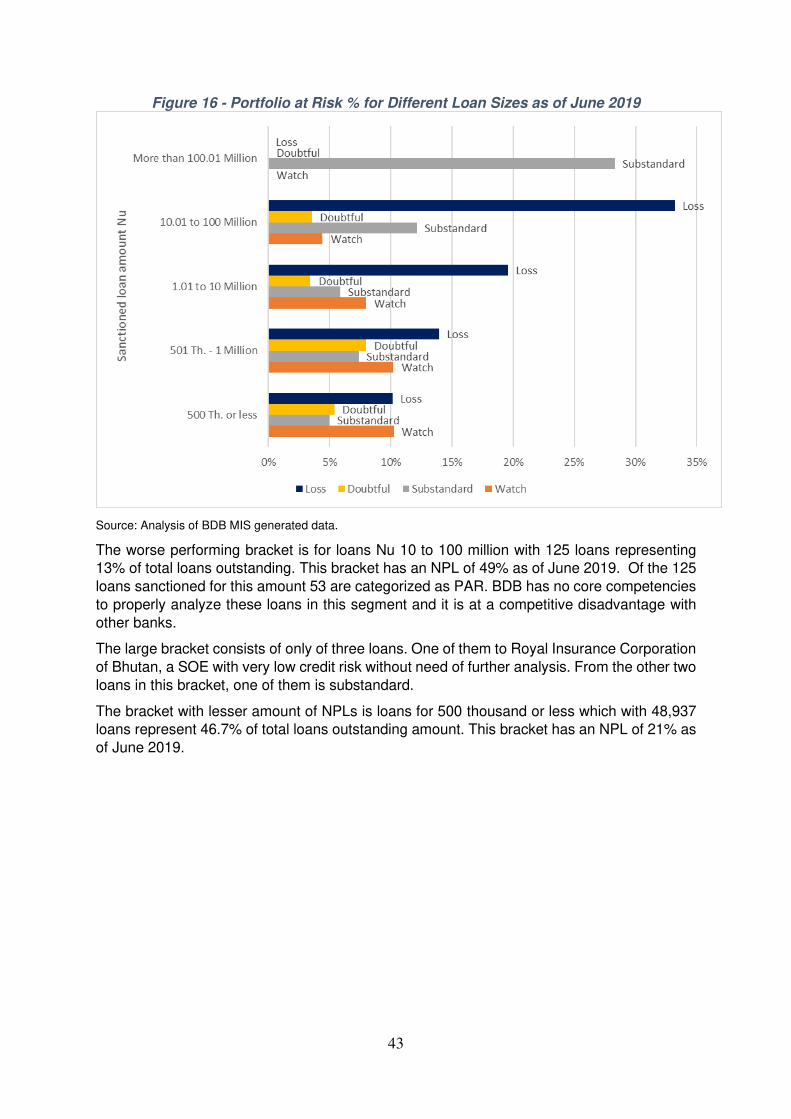

Figure 16 - Portfolio at Risk % for Different Loan Sizes as of June 2019 ............................. 43

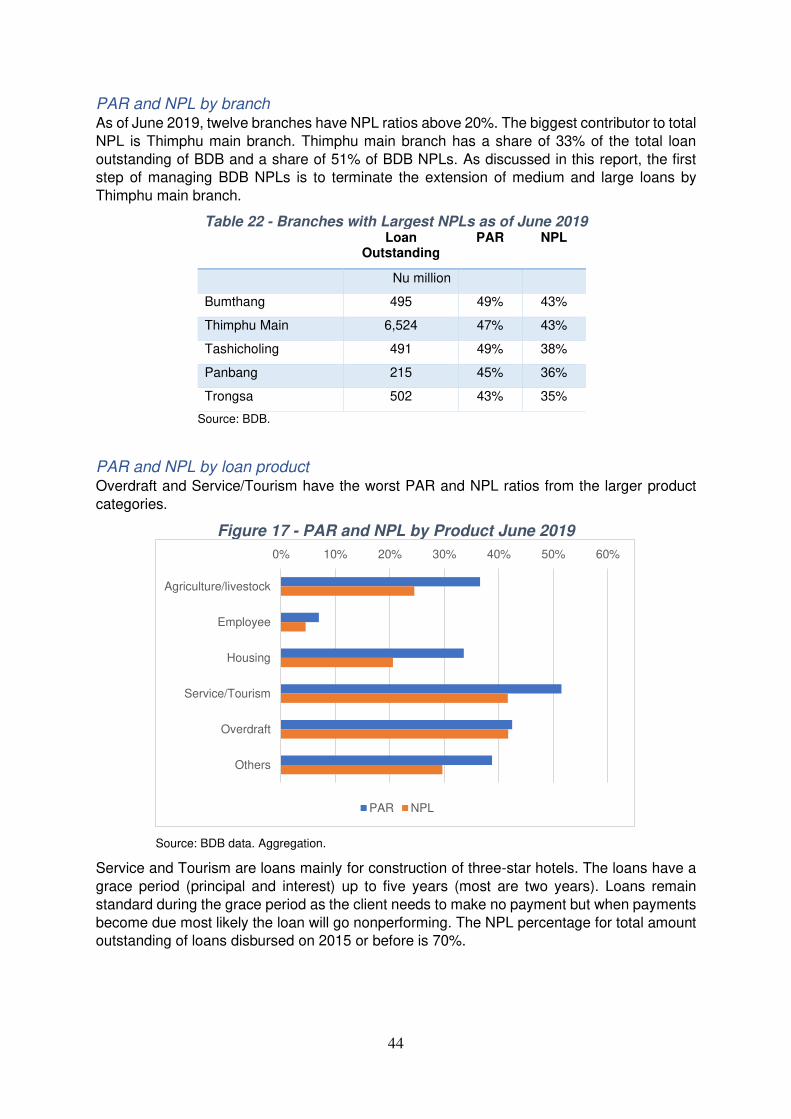

Figure 17 - PAR and NPL by Product June 2019 ................................................................ 44

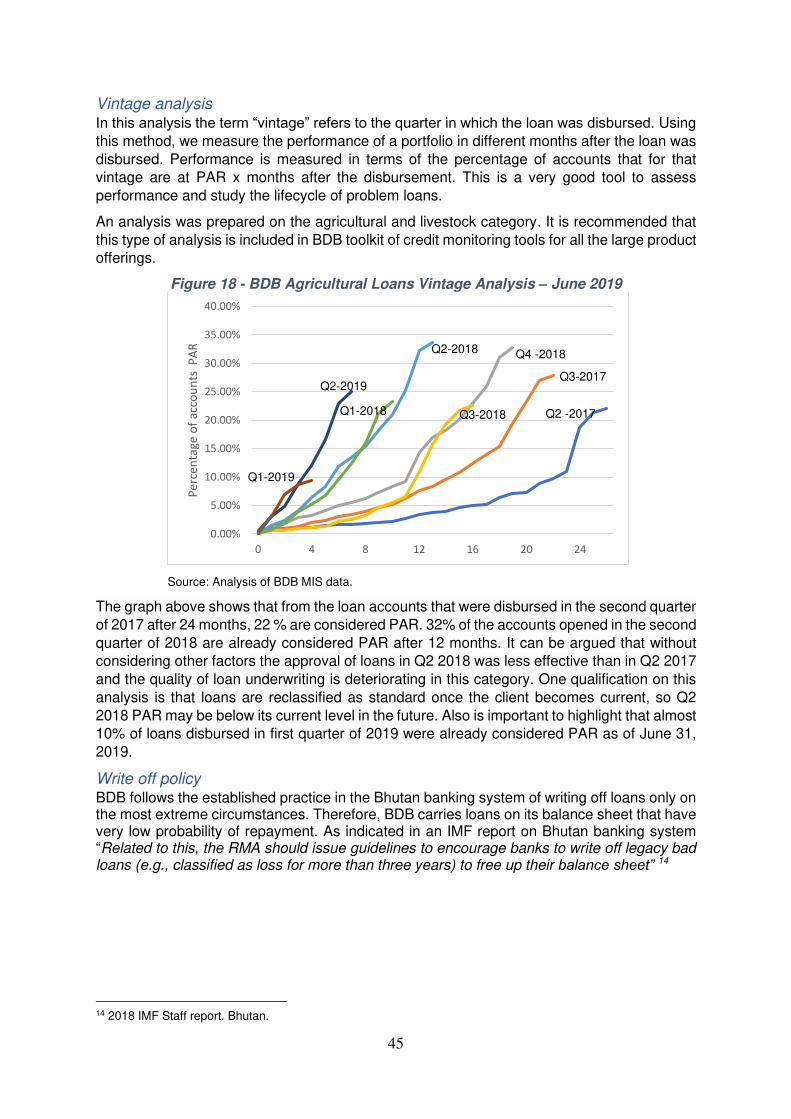

Figure 18 - BDB Agricultural Loans Vintage Analysis – June 2019 ...................................... 45

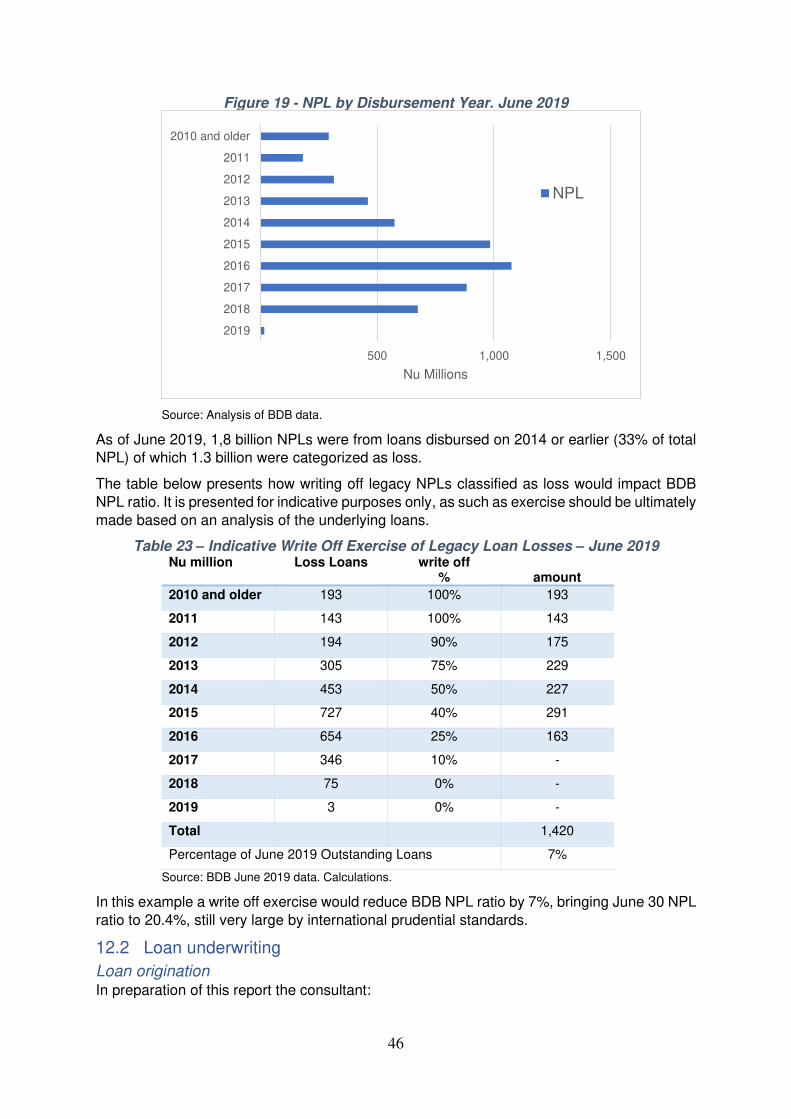

Figure 19 - NPL by Disbursement Year. June 2019 ............................................................ 46

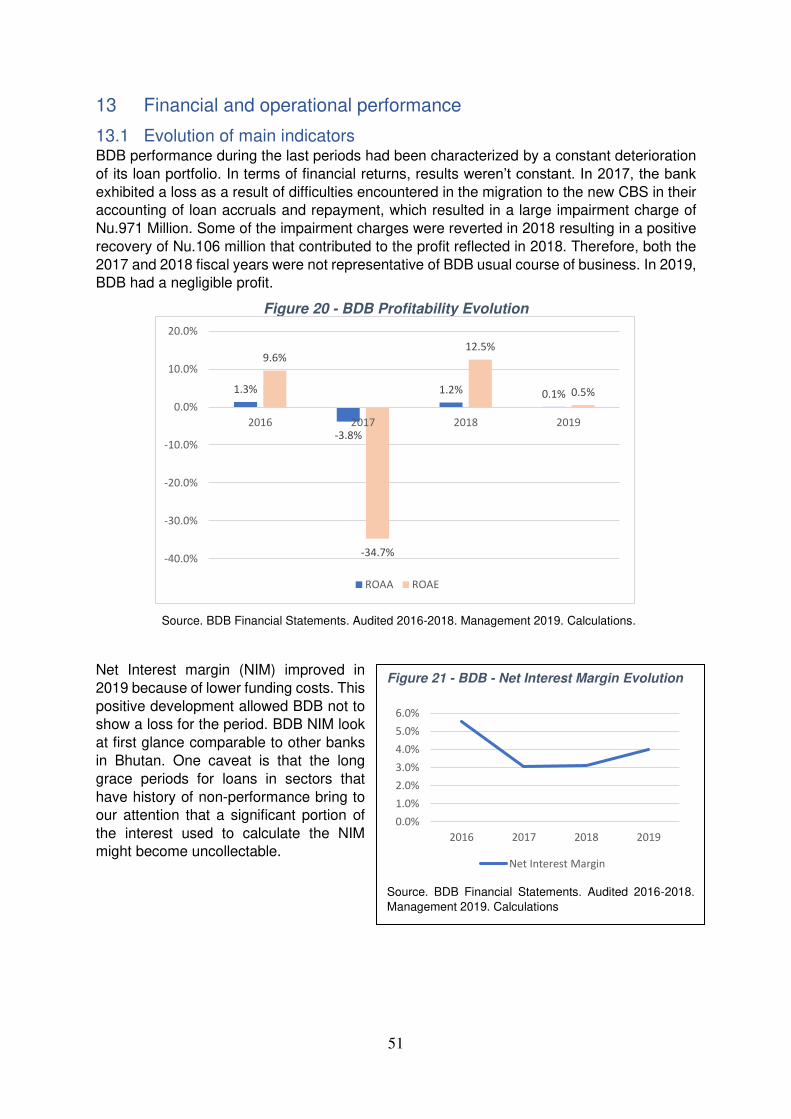

Figure 20 - BDB Profitability Evolution ................................................................................ 51

Figure 21 - BDB - Net Interest Margin Evolution .................................................................. 51

Figure 22 - BDB Gross Portfolio, Yield and Operating Expense Ratio ................................. 52

Figure 23 - BDB Portfolio Yield vs Expense Ratios ............................................................. 52

Figure 24 - BDB Employee and Loan Officer Productivity ................................................... 53

v

Preface and Disclaimer

This Draft Report has been produced by the Technical Advisor under the Technical Assistance

TA-9805 BHU: Diagnostic Study and Strategy Development for Rural Finance Sector Development - 01 Banks and Financial Institutions Specialist (53307-002)

All data on BDB set forth in this report have been represented to the Technical Advisor as materially true and correct by BDB and their representatives.

The Technical Advisor has relied on information provided by the institutions and other third parties (including public sources and summaries thereof) without independent verification. While the author believes these sources to be true and accurate, he makes no warranty thereof.

The author has received full collaboration from BDB and information requests have been handled with diligence, and therefore expresses his gratitude.

This report was prepared with data available as of December 31, 2019. It does not take into consideration the economic effects of the coronavirus disease (COVID-19) pandemic.

vi

Abbreviations

BDB Bhutan Development Bank Limited

BOD Board of Directors

CAGR Compounded Average Growth Rate

CAR Capital Adequacy Ratio

CC Community Centers

CCO Chief Credit Officer

CEO Chief Executive Office

CBS Core Banking System

CIB Customer Information Bureau

COO Chief Operating Officer

CRR Cash Reserve Ratio

CSI Cottage and Small Industries

FITI Financial Institutions Training Institute, Bhutan

FOB Farmers Outreach Banking

GNI Gross National Income

NCSIB National CSI Development Bank Limited

MCSM Micro, Cottage, Small, Medium enterprises

MFI Micro Finance Institution

MIS Management Information System

MLR Minimum Lending Rate

MOF Ministry of Finance

NIM Net Interest Margin

NPL Non-Performing Loan

OECD Organization for Economic Cooperation and Development

PAR Portfolio at Risk (over 30 days)

REDCL Rural Enterprise Development Corporation Ltd

RMA Royal Monetary Authority

ROAA Return on Average Assets

ROAE Return on Average Equity

RWA Risk Weighted Assets

SME Small Medium Enterprise

SOE State Owned Enterprise

1

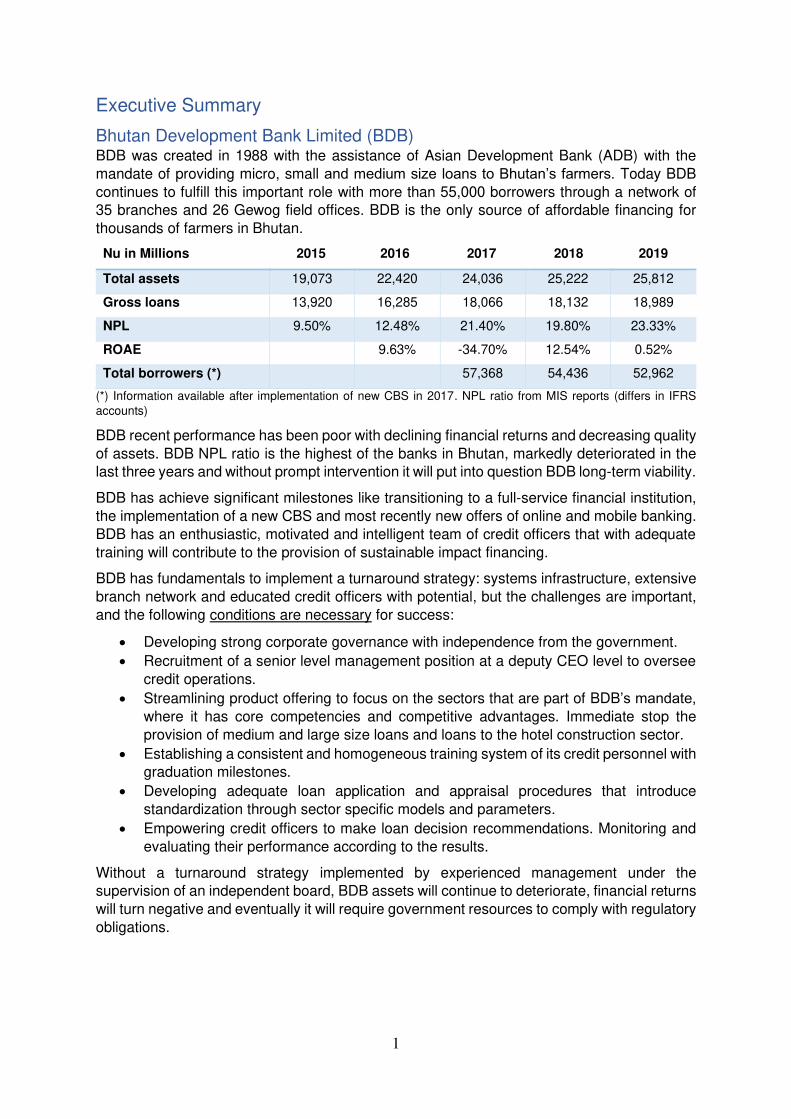

Executive Summary

Bhutan Development Bank Limited (BDB) BDB was created in 1988 with the assistance of Asian Development Bank (ADB) with the

mandate of providing micro, small and medium size loans to Bhutan’s farmers. Today BDB

continues to fulfill this important role with more than 55,000 borrowers through a network of 35 branches and 26 Gewog field offices. BDB is the only source of affordable financing for

thousands of farmers in Bhutan.

Nu in Millions 2015 2016 2017 2018 2019

Total assets 19,073 22,420 24,036 25,222 25,812

Gross loans 13,920 16,285 18,066 18,132 18,989

NPL 9.50% 12.48% 21.40% 19.80% 23.33%

ROAE

9.63% -34.70% 12.54% 0.52%

Total borrowers (*)

57,368 54,436 52,962

(*) Information available after implementation of new CBS in 2017. NPL ratio from MIS reports (differs in IFRS

accounts)

BDB recent performance has been poor with declining financial returns and decreasing quality

of assets. BDB NPL ratio is the highest of the banks in Bhutan, markedly deteriorated in the last three years and without prompt intervention it will put into question BDB long-term viability.

BDB has achieve significant milestones like transitioning to a full-service financial institution,

the implementation of a new CBS and most recently new offers of online and mobile banking.

BDB has an enthusiastic, motivated and intelligent team of credit officers that with adequate

training will contribute to the provision of sustainable impact financing.

BDB has fundamentals to implement a turnaround strategy: systems infrastructure, extensive

branch network and educated credit officers with potential, but the challenges are important,

and the following conditions are necessary for success:

• Developing strong corporate governance with independence from the government.

• Recruitment of a senior level management position at a deputy CEO level to oversee

credit operations.

• Streamlining product offering to focus on the sectors that are part of BDB’s mandate, where it has core competencies and competitive advantages. Immediate stop the

provision of medium and large size loans and loans to the hotel construction sector.

• Establishing a consistent and homogeneous training system of its credit personnel with graduation milestones.

• Developing adequate loan application and appraisal procedures that introduce

standardization through sector specific models and parameters.

• Empowering credit officers to make loan decision recommendations. Monitoring and

evaluating their performance according to the results.

Without a turnaround strategy implemented by experienced management under the supervision of an independent board, BDB assets will continue to deteriorate, financial returns

will turn negative and eventually it will require government resources to comply with regulatory

obligations.

2

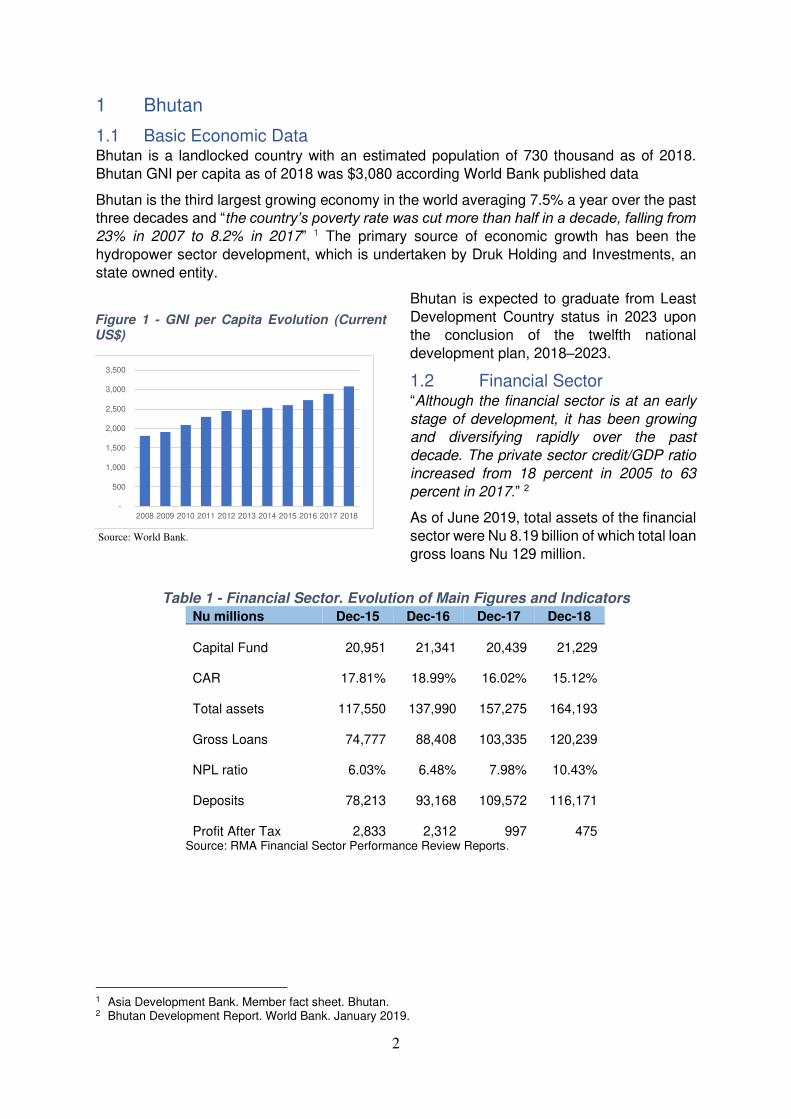

1 Bhutan

1.1 Basic Economic Data Bhutan is a landlocked country with an estimated population of 730 thousand as of 2018.

Bhutan GNI per capita as of 2018 was $3,080 according World Bank published data

Bhutan is the third largest growing economy in the world averaging 7.5% a year over the past three decades and “the country’s poverty rate was cut more than half in a decade, falling from 23% in 2007 to 8.2% in 2017” 1 The primary source of economic growth has been the

hydropower sector development, which is undertaken by Druk Holding and Investments, an

state owned entity.

Bhutan is expected to graduate from Least

Development Country status in 2023 upon

the conclusion of the twelfth national

development plan, 2018–2023.

1.2 Financial Sector “Although the financial sector is at an early

stage of development, it has been growing

and diversifying rapidly over the past

decade. The private sector credit/GDP ratio

increased from 18 percent in 2005 to 63

percent in 2017.” 2

As of June 2019, total assets of the financial

sector were Nu 8.19 billion of which total loan

gross loans Nu 129 million.

Table 1 - Financial Sector. Evolution of Main Figures and Indicators Nu millions Dec-15 Dec-16 Dec-17 Dec-18

Capital Fund

20,951

21,341

20,439 21,229

CAR 17.81% 18.99% 16.02% 15.12%

Total assets

117,550

137,990

157,275

164,193

Gross Loans

74,777

88,408

103,335

120,239

NPL ratio 6.03% 6.48% 7.98% 10.43%

Deposits

78,213

93,168

109,572

116,171

Profit After Tax

2,833

2,312 997 475 Source: RMA Financial Sector Performance Review Reports.

1 Asia Development Bank. Member fact sheet. Bhutan. 2 Bhutan Development Report. World Bank. January 2019.

Figure 1 - GNI per Capita Evolution (Current US$)

Source: World Bank.

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

3

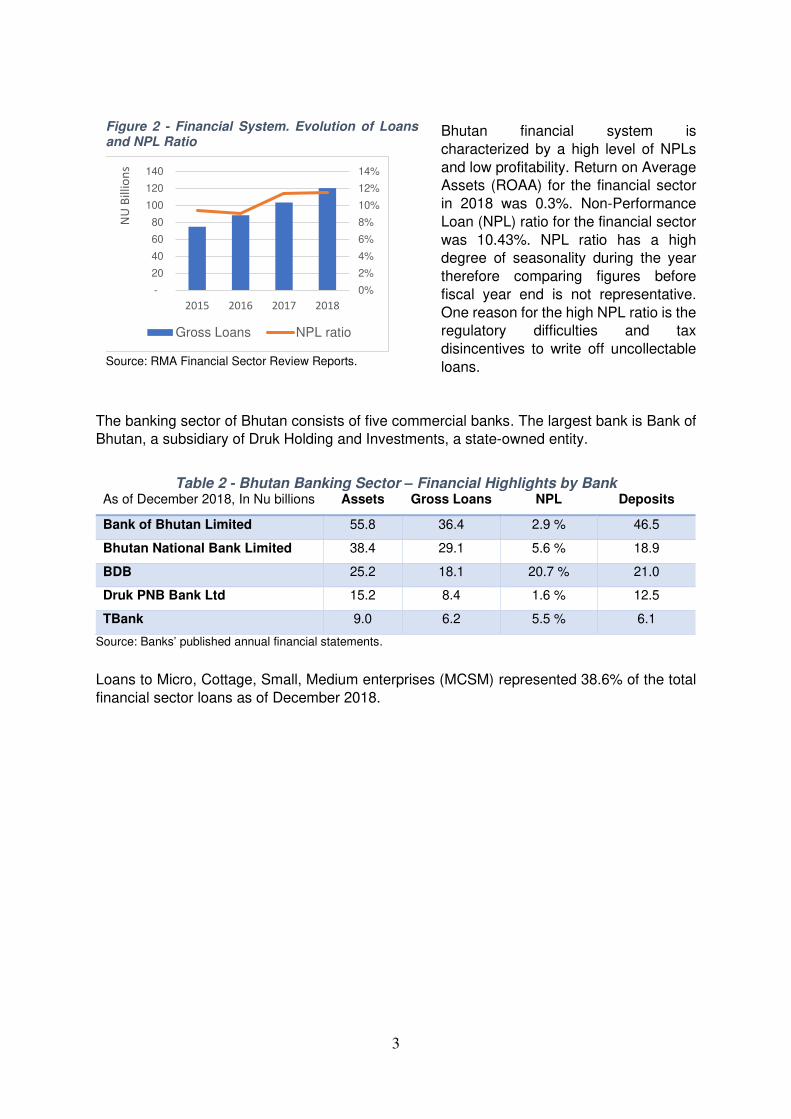

Bhutan financial system is

characterized by a high level of NPLs

and low profitability. Return on Average Assets (ROAA) for the financial sector

in 2018 was 0.3%. Non-Performance

Loan (NPL) ratio for the financial sector

was 10.43%. NPL ratio has a high degree of seasonality during the year

therefore comparing figures before

fiscal year end is not representative.

One reason for the high NPL ratio is the regulatory difficulties and tax

disincentives to write off uncollectable

loans.

The banking sector of Bhutan consists of five commercial banks. The largest bank is Bank of Bhutan, a subsidiary of Druk Holding and Investments, a state-owned entity.

Table 2 - Bhutan Banking Sector – Financial Highlights by Bank

As of December 2018, In Nu billions Assets Gross Loans NPL Deposits

Bank of Bhutan Limited 55.8 36.4 2.9 % 46.5

Bhutan National Bank Limited 38.4 29.1 5.6 % 18.9

BDB 25.2 18.1 20.7 % 21.0

Druk PNB Bank Ltd 15.2 8.4 1.6 % 12.5

TBank 9.0 6.2 5.5 % 6.1

Source: Banks’ published annual financial statements.

Loans to Micro, Cottage, Small, Medium enterprises (MCSM) represented 38.6% of the total

financial sector loans as of December 2018.

Figure 2 - Financial System. Evolution of Loans and NPL Ratio

Source: RMA Financial Sector Review Reports.

0%

2%

4%

6%

8%

10%

12%

14%

-

20

40

60

80

100

120

140

2015 2016 2017 2018

NU

Bil

lio

ns

Gross Loans NPL ratio

4

1.3 MFI Sector There are five Micro-Finance Institutions (MFI) that had been registered by the RMA.

• Rural Enterprise Development Corporation Ltd (REDCL)

• RENEW Micro-Finance Pvt. Ltd (RENEW)

• Bhutan Care Credit Ltd (BCC)

• Bhutan Association of Women Entrepreneurs (BAOWE)

• Tarayana Foundation

1.4 Regulatory Framework The financial services act of Bhutan 2011 establishes the Royal Monetary Authority (RMA) as

the regulatory entity that promotes the stability and soundness of the financial system and

determines the regulatory framework for financial services in the country.

The prudential regulations for the financial system have been issued by the RMA on 2017. The regulation establishes a minimum Capital Adequacy Ratio (CAR) for financial institutions

of 10%. In addition, institutions must maintain a Capital Conservation Buffer of 2.5%.

Every bank is required to maintain a Cash Reserve Ratio (CRR) in the form of a current

account deposit with RMA. CRR currently is at 10% of customer deposits.

The regulation establishes a classification of credit exposures as follows:

Table 3 - Loan Classification - RMA Regulation

Classification Principal or Interest Status Loan Loss Provisions

Standard Current or overdue up to 30 days

1%

Watch Overdue 31 to 90 days 1.5%

Sub-Standard Overdue 91 to 180 days 20%; 30% for sector with highest exposure

Doubtful Overdue 181 to 365 days 50%, 60% for sector with highest exposure

Loss Overdue more than 365 days 100%

Sub-Standard, Doubtful and Loss classifications are considered Non-Performing Loans (NPL). Banks cannot grant new loans to a non-performing account and institutional strengthening is

only admissible for credit exposures that have been regular and have genuine unforeseen

financial constraints.

Lending interest rates are regulated by the RMA circular on Minimum Lending Rates (MLR) The MLR is a single benchmark or minimum reference rate for lending of money for all financial

institutions. The formula considers the marginal cost of funds, the negative carry charges on

CRR and the institutions operating cost.

5

Cottage and Small Industry (CSI) Banks are regulated by the RMA rules and regulations

published to that effect on 2018 with the intention of “Develop, promote, assist and support

the establishment of, expansion or improvement of cottage and small industries by granting

credit facilities.” Under the regulation CSI banks can be either deposit taking or not deposit

taking institutions. CSI loans have been categorized as follows:

• investment size up to Nu.1 million categorized as “cottage” • and investment size above Nu. 1 million but up to Nu. 10 million categorized as “small”

industry.

CSI banks have a minimum paid up equity capital requirement of Nu 150 million for non-

deposit taking CSI banks and Nu 300 million for deposit taking CSI banks. CSI banks are

required to maintain a minimum CAR of 15% of Risk Weighted Assets (RWA)

The rate of interest on loans shall be based on Minimum Lending Rate Framework. However, a CSI bank wishing for waiver of income tax on interest income earned through preferential

lending to CSI enterprises shall be governed by the Fiscal Incentives of Government issued

by the Ministry of Finance.

BDB Headquarters Thimphu.

6

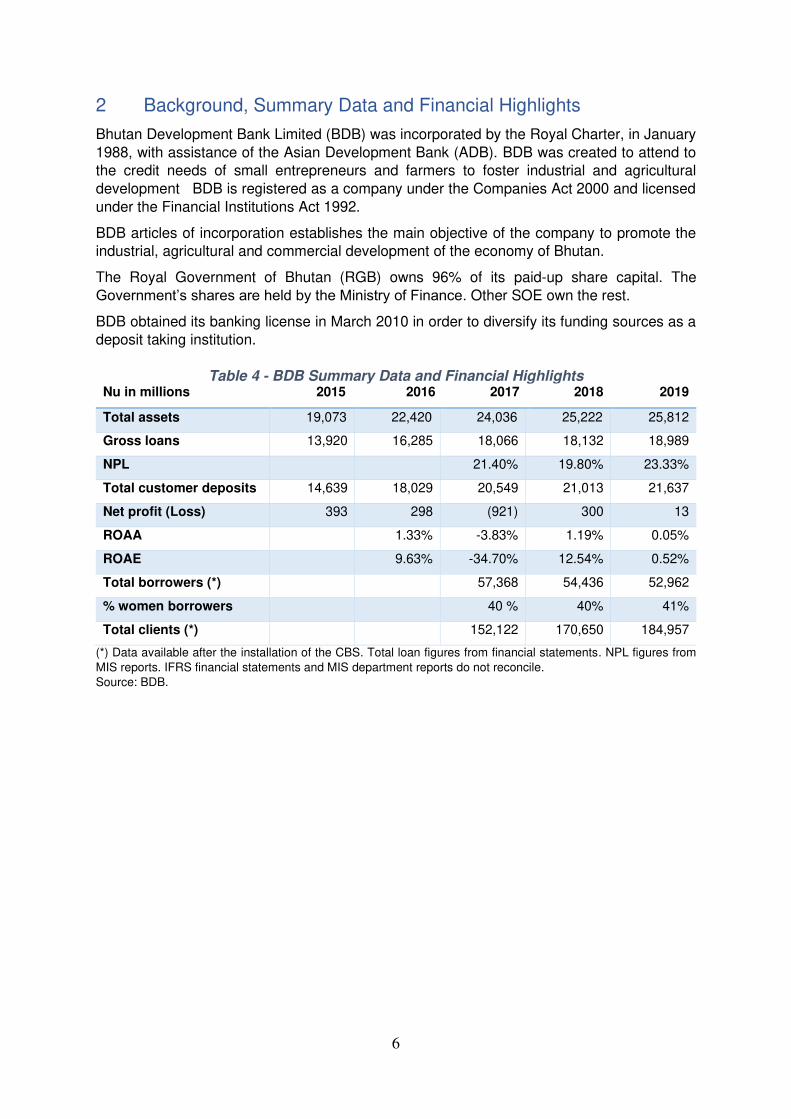

2 Background, Summary Data and Financial Highlights

Bhutan Development Bank Limited (BDB) was incorporated by the Royal Charter, in January

1988, with assistance of the Asian Development Bank (ADB). BDB was created to attend to the credit needs of small entrepreneurs and farmers to foster industrial and agricultural

development BDB is registered as a company under the Companies Act 2000 and licensed

under the Financial Institutions Act 1992.

BDB articles of incorporation establishes the main objective of the company to promote the industrial, agricultural and commercial development of the economy of Bhutan.

The Royal Government of Bhutan (RGB) owns 96% of its paid-up share capital. The

Government’s shares are held by the Ministry of Finance. Other SOE own the rest.

BDB obtained its banking license in March 2010 in order to diversify its funding sources as a deposit taking institution.

Table 4 - BDB Summary Data and Financial Highlights

Nu in millions 2015 2016 2017 2018 2019

Total assets 19,073 22,420 24,036 25,222 25,812

Gross loans 13,920 16,285 18,066 18,132 18,989

NPL

21.40% 19.80% 23.33%

Total customer deposits 14,639 18,029 20,549 21,013 21,637

Net profit (Loss) 393 298 (921) 300 13

ROAA

1.33% -3.83% 1.19% 0.05%

ROAE

9.63% -34.70% 12.54% 0.52%

Total borrowers (*)

57,368 54,436 52,962

% women borrowers 40 % 40% 41%

Total clients (*)

152,122 170,650 184,957

(*) Data available after the installation of the CBS. Total loan figures from financial statements. NPL figures from

MIS reports. IFRS financial statements and MIS department reports do not reconcile.

Source: BDB.

7

3 Strategic Planning

3.1 Vision and Mission The Business Plan 2015-2019 document establishes the following vision and mission

statements, and core values.

Vision To be the strong, dependable and customer focused Bank that contributes towards

achievement of Gross National Happiness

An effective vision statement has the following characteristics

• Concrete and specific

• Bold, challenging and exciting

• Positive and inspiring

• A goal worth “stretching” for

• Attainable

In this respect BDB vision statement is too general and doesn’t capture BDB mandate to

provide access to finance to provide micro, small and medium financial services for the

development and modernization of agricultural, commercial and industrial enterprises in the

country.

As part of BDB strategic planning effort, BDB management and

Board of Directors should engage

in a session to produce a more

effective statement. During the session participants should think

what an ideal outcome of BDB

activities in the long term would be,

what the institution wants to become and how Bhutan has

gotten better because of BDB

impact. BDB employees can

participate in the process by presenting their views on the future

of the organization. Their answers

should be taking into consideration

and can be summarized in a word cloud graph as the one presented in Figure 3 – Word Cloud Example for the consideration of

the decision makers.

Vision statement is a very important part of the strategic planning process and it needs

ownership from the institution leadership. It cannot be redacted in abstract, however the following ideas might be considered as part of a vision statement:

• Agricultural, commercial and industrial enterprises in Bhutan.

• Sustainability.

• Equitable access to finance to micro and CSI market.

Figure 3 – Word Cloud Example

8

Mission

A premier development bank with focus on rural prosperity through prompt, efficient and

effective financial services on a sustainable basis.

The purpose of a mission statement is to provide motivation, build consensus, solidify the

organization and give an image to clients and constituents. It describes what an organization

does, what services provides, what makes it unique and what is its purpose.

BDB current mission statement is adequate. A similar exercise to the one proposed to the vision statement can be used to further refine the mission statement and introduce other

important aspects of BDB purpose such as:

• Outreach to unbanked populations

• Transparency/financial literacy

• Customer service

• Branch network

There is a need for better communication with customers and an effort to improve their

financial literacy. Inclusion of this important aspect in the mission statement should help as a

reminder of the need to fulfill this need.

Core values According to BDB strategic plan “The values that employees of the Bank should embrace in the execution of the duty reflect the important role the Bank play in the development of the country. The values are known by the acronym “PEOPLE” which depicts the one of the core objectives of the Bank in providing services to the people.” • Professionalism – Give your Best

• Excellence – Aim for higher ideals

• Ownership - Own your Bank and Care for your customers

• Partnership – Work together for growth

• Loyalty – Be true to oneself and stakeholders

• Efficiency – Deliver Prompt Service It is important to convey to employees the value of integrity and honesty. As described in this

report there have been many recent instances of fraud and misappropriation of funds. While

certainly a core value statement would not be enough to address this important problem, the

institution message should be clear that integrity is a fundamental value and dishonest behavior will not be tolerated.

9

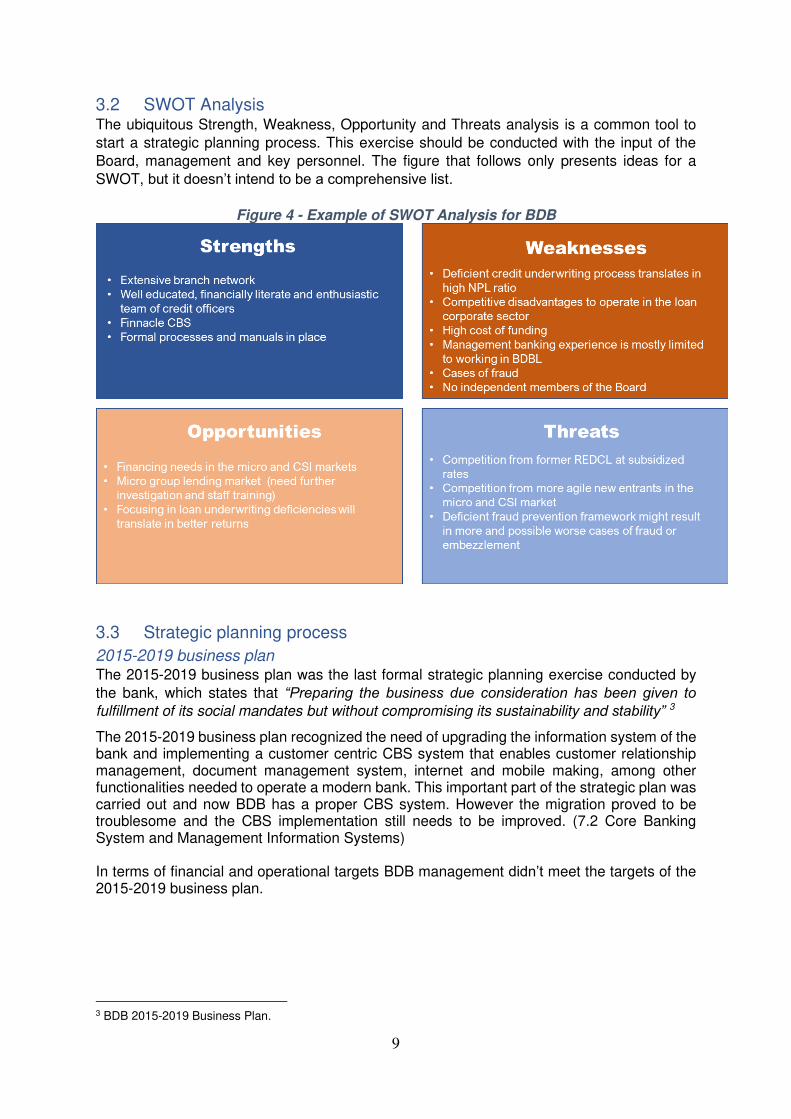

3.2 SWOT Analysis The ubiquitous Strength, Weakness, Opportunity and Threats analysis is a common tool to

start a strategic planning process. This exercise should be conducted with the input of the

Board, management and key personnel. The figure that follows only presents ideas for a

SWOT, but it doesn’t intend to be a comprehensive list.

Figure 4 - Example of SWOT Analysis for BDB

3.3 Strategic planning process

2015-2019 business plan The 2015-2019 business plan was the last formal strategic planning exercise conducted by

the bank, which states that “Preparing the business due consideration has been given to fulfillment of its social mandates but without compromising its sustainability and stability” 3

The 2015-2019 business plan recognized the need of upgrading the information system of the bank and implementing a customer centric CBS system that enables customer relationship management, document management system, internet and mobile making, among other functionalities needed to operate a modern bank. This important part of the strategic plan was carried out and now BDB has a proper CBS system. However the migration proved to be troublesome and the CBS implementation still needs to be improved. (7.2 Core Banking System and Management Information Systems) In terms of financial and operational targets BDB management didn’t meet the targets of the 2015-2019 business plan.

3 BDB 2015-2019 Business Plan.

10

Table 5 - 2015-2019 Business Plan Targets vs Actual Performance Measure 2019 Target December 2019 Actual

Total credit customers 74,000 57,319 Loan portfolio Net (Nu billion) 22.3 19.9 Agriculture and livestock loans % 30% 27% PAR 7.7% 36.6% Total deposits (Nu billion) 25.4 21.0

There are no documented efforts of attempts to follow up on performance against targets prescribed in the 2015-2019 business plan and no other formal strategic planning effort have

taking place since 2015. BDLB has no financial projections.

Recommendations

Strategic planning should be an on-going process and not a discrete event that takes place every five years. BDB performs an annual workshop each year to analyze prior year

performance and set expectations for the following year. However, strategic planning requires

a longer horizon, the yearly workshop should be also an opportunity to review the medium and

long term goals. Management should be accountable to deviations not only of yearly budget targets but also for performance on medium and long term goals

In the 2015-2019 either the targets were over ambitious and the strategic planning process

defective or management did not deliver on the expectations.

BDB management should present to the BOD for its consideration a five-year business plan inclusive of financial projections.

4 Governance

As SOE, BDB corporate governance is contained in the Corporate Governance Guidelines

(CG Guidelines 2019) for State Enterprises 2019 as sanctioned by MOF, Royal Government of Bhutan. The preface of the guidelines points out that “The CG Guidelines 2019 were

developed by MOF in close consultation with relevant agencies and was reviewed by a

Technical Committee comprising members from RMA, Companies Registrar, DHI and

representative from State Enterprises. Further, it was also reviewed by experts from the World

Bank and IFC.”

“The Government’s share in the State Enterprises and portfolio companies shall be held by the Minister of Finance who shall then be primarily responsible for monitoring and reporting

the performance of State Enterprises.” 4

The CG Guidelines 2019 enumerates the responsibilities of the MOF. Among them:

• establishing well-structured, merit-based, and transparent nomination of Board and endorsement of CEO appointment;

• establishing clear remuneration guidelines for State Enterprise that fosters the long- and medium-term interest of the enterprise;

• fixing sitting fees of the Board;

• monitoring the performance of State Enterprise;

• endorse the Articles of Incorporation of State Enterprises and any amendments thereto;

• set targets and monitor performances of State Enterprises;

• evaluate the performance of the Board as per the Performance Evaluation Framework (PEF)

4 Corporate Governance Guidelines for State Enterprises 2019.

11

4.1 Board of Directors “The governing body of a State Enterprise shall be the Board of Directors (BOD). The BOD is

the ultimate decision-making body of the Company except with respect to those matters

reserved to the shareholders. The Board shall meet at least once in every three months or no

less than four times per year and as frequently as may be deemed necessary to deal with the

business of the Company.”5

Among the BOD responsibilities:

• ensuring that the policy objectives of the Company are attained and that the Company

operates in an efficient and effective manner,

• reviewing and guiding corporate strategy, major plans of action, risk policy, annual

budgets, business plans and set performance targets,

• monitoring implementation and corporate performance; and overseeing major capital

expenditures, acquisitions and divestitures.

MOF nominates and recommend to the Government for endorsement the nomination of the

BOD members, including the Chairperson.

The CG guidelines 2019 prescribes that the BOD should have three to nine members. BDB BOD consists of seven members and that the Board shall be collectively accountable for the

governance of the Company.

Five BOD members are current or former civil servants. One is the current CEO of REDCL

and the other is BDB CEO as established in the normative (also a former civil servant)

The current chairperson is Mr. Lekzang Dorji, Director General, Department of Macro

Economic Affairs, MOF.

4.2 Chief Executive Officer The BOD is responsible to select the CEO through open competition that includes due

diligence of applicants, checks on integrity and records of past performance, short list and

interview process. BOD shall select the highest ranked candidate and recommend the selected candidate to MOF for endorsement and finalization of the remuneration package.

Ministry of Finance will review the Board’s recommendation and submit to Lhengye Zhungtshog (Prime minister and cabinet) for endorsement.

The current Chief Executive Officer since March 2016 is Mr. Phub Dorji. Mr. Dorji has a master’s in public administration (MPA) from Harvard Kennedy School, Harvard University, a

long career in civil service in the Ministry of Economic Affairs and he is in author of various

publications on economic issues and entrepreneurship.

Recommendation

• Independent BOD with the inclusion of members with business and banking experience.

The MOF guidelines dictates that “The Board shall have a balance of diverse skills, core

competencies and capabilities, knowledge and experience to aid informed, independent and

objective decision making”

The OECD Guidelines on Corporate Governance of SOEs indicates that “For SOEs engaged

in economic activities, it is recommended that board members have sufficient commercial,

financial and sectoral expertise to effectively carry out their duties. In this respect, private

sector experience can be useful” 6

5 Corporate Governance Guidelines for State Enterprises 2019. 6 OECD Guidelines on Corporate Governance of State-Owned Enterprises.2015

12

BDB BOD is composed almost exclusively by professionals with long current or former careers

as civil servants. Positions in ministries such as Agriculture, Economic Affairs or Finance are

certainly relevant experiences to bring to corporate decisions and in countries like Bhutan with limited private sector development there could be few options. However, there are other

perspectives and experiences that are also important, and it is in direct contradiction to the

normative that asks for a “balance of diverse skills”.

A risk of state-owned banks is that they will be subject to political influence that might interfere in decision making. A board formed exclusively by members whose careers might be

dependent on government decisions magnifies this problem. Management indicated that there

had been instances where the BOD overrode credit and interest setting, resulting in decisions

against the interest of BDB. This board overreaching is ineffective and reflective of poor governance.

BDB BOD should at least have four members with experience in the financial sector from

Bhutan, other countries or in International Financial Institutions. BDB needs to implement

challenging changes to secure its sustainability and fulfill its mandate. The presence in the BOD of independent, qualified and reputable professionals with a sharp understanding of

banking, microfinance and SME lending is a condition necessary for a successful turnaround

of the institution.

The inclusion of independent directors can eventually lead to an independent chair as suggested in the World Bank’s Corporate Governance Guidelines for SOEs toolkit: “Over time,

the independent representation could be gradually increased to a significant number of such

directors and eventually to a majority of directors, including a chair who is independent of the

government. Experienced foreign nationals—particularly for large and complex SOEs—may

be considered as the pool of local talent grows. While the issue is often politically sensitive,

foreign directors can increase the quality of the board, introduce new ideas and expertise, and

help insulate SOEs from political interference and corruption, as foreign board members are

less politically vulnerable.” 7

REDCL CEO (now NCSIB) is a member of the board. This is a conflict of interest even

if both institutions are state owned and should be avoided.

• Presence of management with banking, microfinance/SME lending experience outside

BDB

BDB management is motivated to fulfil the mandate given to the institution. It is

knowledgeable, have participated in numerous training programs and it is aware of the challenges facing the institution.

However, currently the top-level management of BDB is formed with professionals without a

relevant banking experience outside the institution. BDB has the framework, processes in

place and enthusiastic staff to embark in a process to turn around the institution, but such a process requires of experienced leadership without an insular perspective.

BDB BOD should recruit a senior level management position at a deputy CEO level to oversee

credit operations. This professional should ideally have more than 15 years of experience in

• banking/lending, having occupied a senior role in a financial institution outside BDB,

• microfinance/SME lending

• agriculture/livestock value chain

7 World Bank’s Corporate Governance Guidelines for SOEs A toolkit. 2014.

13

• turnaround situations

Annex IV presents indicative terms of reference for the position.

5 Organizational Structure

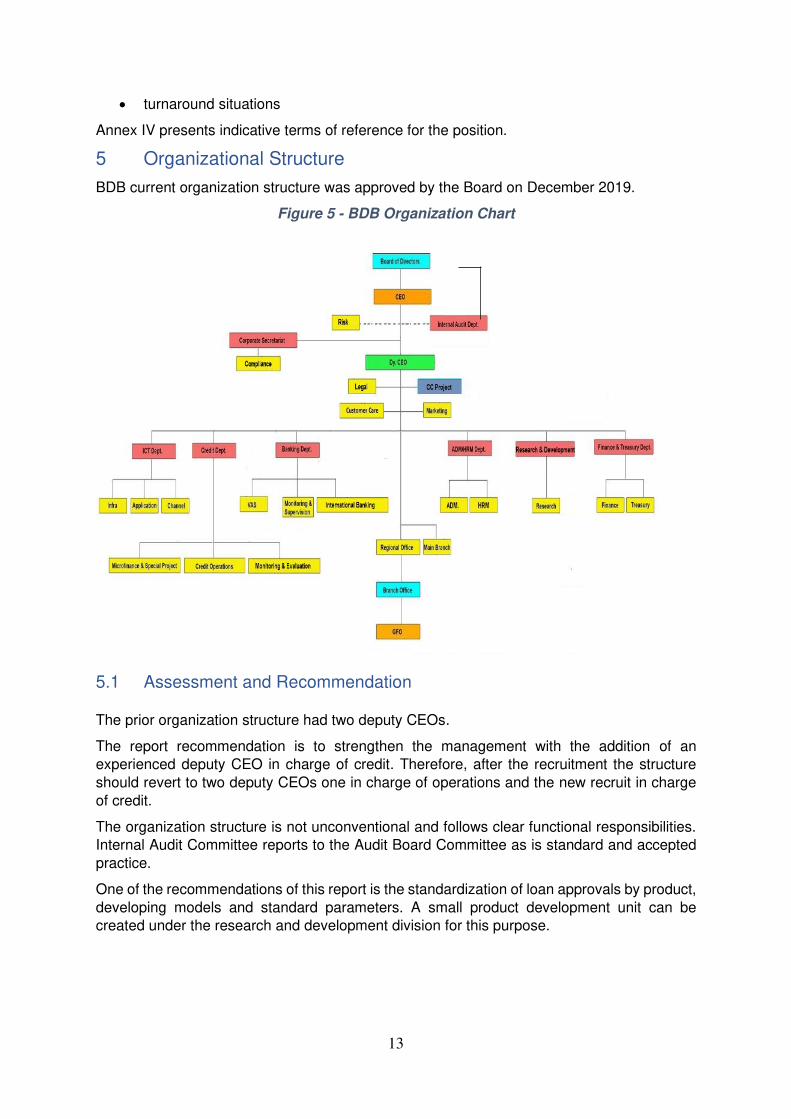

BDB current organization structure was approved by the Board on December 2019.

Figure 5 - BDB Organization Chart

5.1 Assessment and Recommendation

The prior organization structure had two deputy CEOs.

The report recommendation is to strengthen the management with the addition of an experienced deputy CEO in charge of credit. Therefore, after the recruitment the structure

should revert to two deputy CEOs one in charge of operations and the new recruit in charge

of credit.

The organization structure is not unconventional and follows clear functional responsibilities. Internal Audit Committee reports to the Audit Board Committee as is standard and accepted

practice.

One of the recommendations of this report is the standardization of loan approvals by product,

developing models and standard parameters. A small product development unit can be created under the research and development division for this purpose.

14

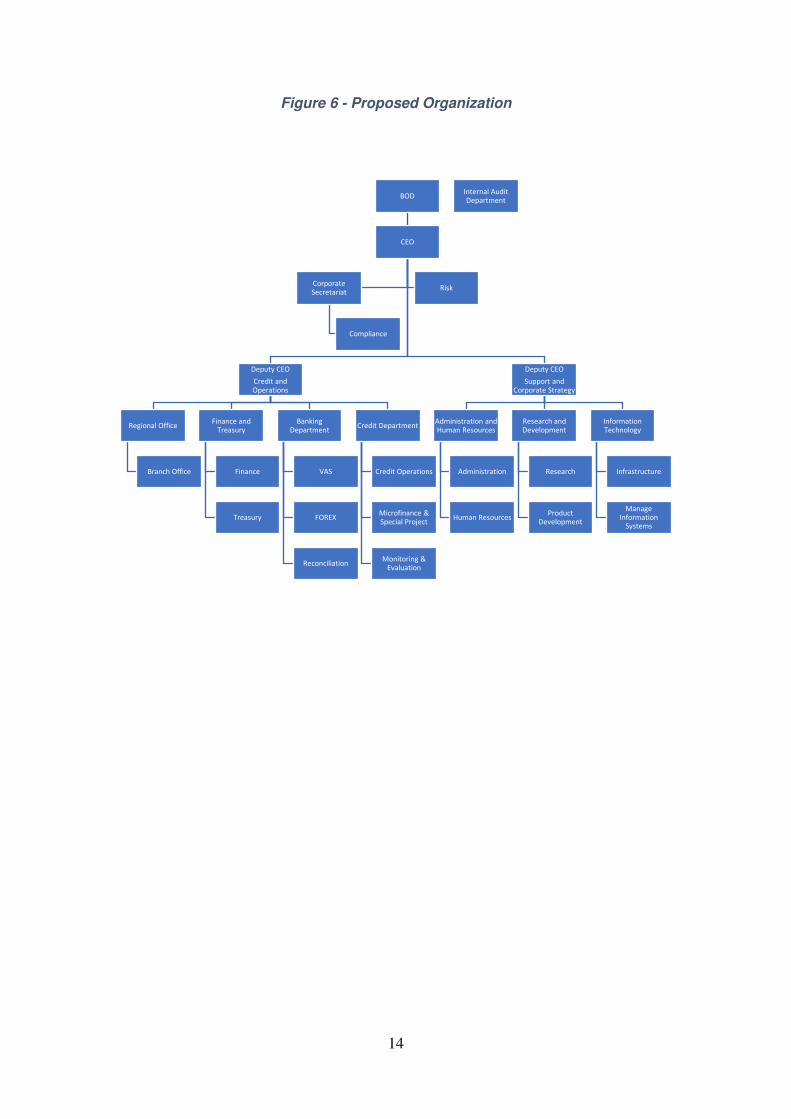

Figure 6 - Proposed Organization

BOD

CEO

Deputy CEO

Support and

Corporate Strategy

Information

Technology

Infrastructure

Manage

Information

Systems

Research and

Development

Research

Product

Development

Administration and

Human Resources

Administration

Human Resources

Deputy CEO

Credit and

Operations

Credit Department

Credit Operations

Microfinance &

Special Project

Monitoring &

Evaluation

Banking

Department

VAS

FOREX

Reconciliation

Finance and

Treasury

Finance

Treasury

Regional Office

Branch Office

RiskCorporate

Secretariat

Compliance

Internal Audit

Department

15

6 Human Resources

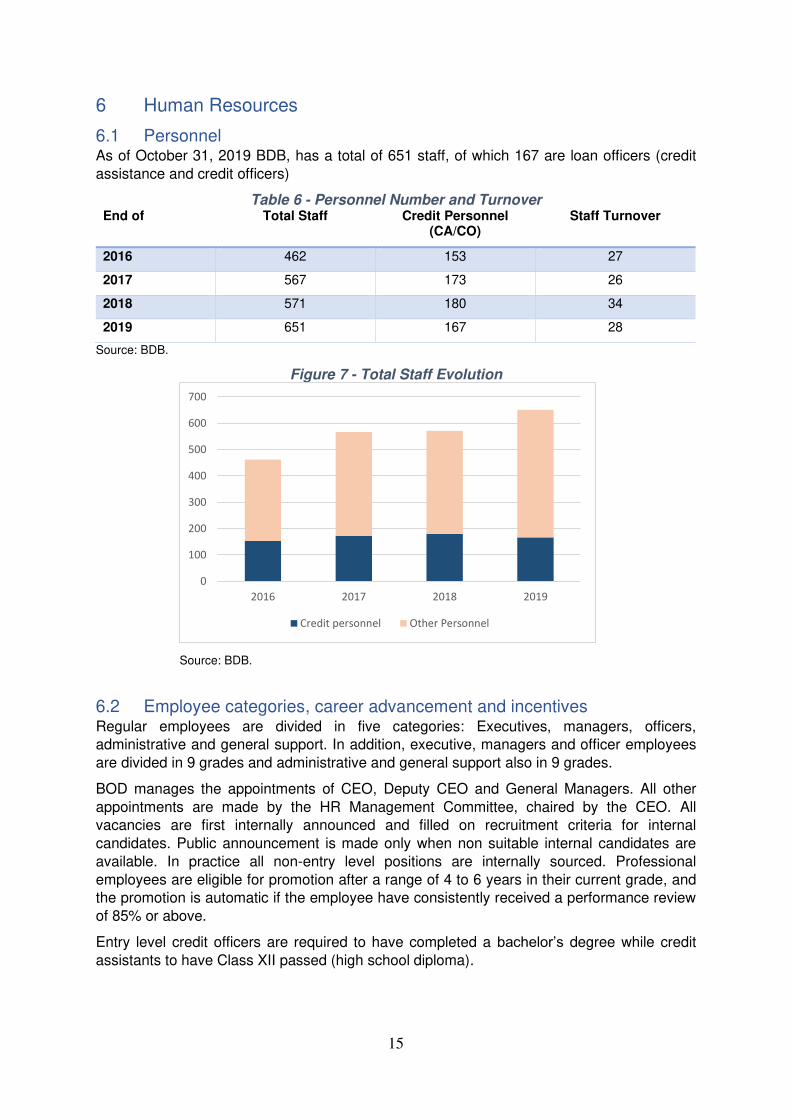

6.1 Personnel As of October 31, 2019 BDB, has a total of 651 staff, of which 167 are loan officers (credit

assistance and credit officers)

Table 6 - Personnel Number and Turnover End of Total Staff Credit Personnel

(CA/CO) Staff Turnover

2016 462 153 27

2017 567 173 26

2018 571 180 34

2019 651 167 28

Source: BDB.

Figure 7 - Total Staff Evolution

Source: BDB.

6.2 Employee categories, career advancement and incentives Regular employees are divided in five categories: Executives, managers, officers, administrative and general support. In addition, executive, managers and officer employees

are divided in 9 grades and administrative and general support also in 9 grades.

BOD manages the appointments of CEO, Deputy CEO and General Managers. All other

appointments are made by the HR Management Committee, chaired by the CEO. All vacancies are first internally announced and filled on recruitment criteria for internal

candidates. Public announcement is made only when non suitable internal candidates are

available. In practice all non-entry level positions are internally sourced. Professional

employees are eligible for promotion after a range of 4 to 6 years in their current grade, and the promotion is automatic if the employee have consistently received a performance review

of 85% or above.

Entry level credit officers are required to have completed a bachelor’s degree while credit

assistants to have Class XII passed (high school diploma).

0

100

200

300

400

500

600

700

2016 2017 2018 2019

Credit personnel Other Personnel

16

For general and regional managers, the mandatory retirement age is 60, for all other

employees is 58. Upon retirement employees are entitled to a gratuity payment of his or her

last basic salary per year of service.

The basic payment scale for employees is determined by the MOF. According to management

salary at the bank is considerably lower than similar positions in the private sector. However,

this does not seem to have an effect in turnover which is low. Employees are entitled to a 2.5%

annual increase (if they meet minimum performance grade). Employees with good performance are entitled to a bonus payment up to the equivalent of four months’ salary.

6.3 Performance evaluation system BDB implements a yearly performance evaluation system for its employees. All employees

are required to develop individual performance plans. Performance is measured in quantitative

and qualitative targets. Supervisors are required to provide feedback at frequent intervals. At

the end of the year overall performance is evaluated.

Credit assistant and officers are given annual total loan, deposit balances and PAR>90

targets. These quantitative targets account for 60% of their evaluation score. Qualitative rating

accounts for the rest of the score and is given by managers based on documentation quality,

customer relationship, accuracy and timeliness of reporting, teamwork, reliability, discipline, initiative, and integrity.

All employees scores translate to the following performance scale: outstanding, excellent,

good, satisfactory and needs improvement.

In case of consistent non-performance several strategies are utilized, including training managers on performance management, employee development, review of work

responsibilities, improvement of job environment and workload, transfer/reassignment and

disciplinary actions including termination.

The Human Resources manual delineates the overall performance evaluation system process

and follows standard managerial practices.

6.4 Capacity Development and Training

Credit training Credit officers are recruited from university upon completion of their bachelor’s degree by an

open process. Assistant officers are required to have Class XII diploma (high school) New

recruits are given a one-week training course conducted by an experienced loan officer. Both

loan and assistant officers assist to the same course. The training course consist of the exposure to basic principles of credit, case studies and BDB credit procedures. Quizzes are

part of the program to ensure proper understanding of the concepts, however there is no

examination at the end, and nobody fails the course. The trainer interviewed was

knowledgeable and had a well-structured presentation. She did not receive any formal training in credit courses.

Subsequently, new recruits receive on the job training by their supervisors.

Management indicated that during the first two years credit officers attend training abroad,

most prominently in the National Institute of Bank Management Training (NIBM) in Pune, India. The 10 days program is focused on credit assessment and financial statement analysis,

includes case analysis and a visit to a local financial institution. Also, some credit officers

attended the five days training program on credit appraisal and loan recovery training course

provided by Bangkok School of Management.

In interviews with credit officers it became apparent that some of them have not received the training abroad even after more than three years in the bank. After reviewing information

17

requested to BDB, 25 credit officers that have been in the bank since 2016 and 2017 have not

received the training abroad.

Other training In country training is provided on an ad-hoc basis to the employees based on specific needs. In 2019 training offered to the employees included: leadership training (3 attendees), training

of trainers (12 attendees), currency management (26 attendees), loans for startups and

entrepreneurs (2 attendees), and risk management of SME lending (2 attendees).

International training in other areas than credit appraisal included customer care, microfinance, IFRS and other areas in courses in Thailand, Vietnam, India and SRI Lanka,

among other locations.

6.4.1 Assessment Interviews with credit officers identified in some instances the need of a better understanding

of some elements of credit analysis. The differences among the officers in their understanding

suggests the lack of a homogeneous training system.

Credit officers are recruited directly from University and are bright young women and men among the best performing students. While some have taking formal courses in finances and

accounting others might come from other valid fields but without a finance background. BDB

does not have a training program to take advantage of the talented professionals it recruits.

A one-week course is clearly insufficient to prepare young graduates to make credit decisions. On the job training is important but ineffective in creating a minimum knowledge standard that

can be expected of a credit officer after one year in the bank. The same course is currently

attended by both credit assistant (high school education) and credit officers (university

education). The needs of both groups are clearly different, and the course curricula should also be different.

Training abroad is seeing by the employees and management in many cases more as a

motivational tool than a training exercise. All officers interviewed were appreciative of this

opportunity and expressed that the course was productive, increased their knowledge and broadened their perspective by studying case studies and visiting financial institutions in India.

This practice should continue but all officers should go through the same syllabus and

preferably same location.

The main training facility in Bhutan is the Financial Institutions Training Institute Limited (FITI). FITI was established in the year 2011 by RMA in collaboration with Financial Institutions

Association of Bhutan (FIAB), as an autonomous apex institution for training, research and

consultancy with the objective to train and build the human resource capacity of financial

sector. ADB provided technical assistance in the formation and institutionalization of FITI. BDB is a shareholder of FITI along with other financial institutions, however it does not use the

services. Exploring using FITI resources might be an option. The consultant interviewed FITI’s management and was presented with the curricula of several banking and credit courses. The

courses syllabus looked comprehensive but an assessment of FITI capabilities exceeds the terms of reference of the assignment, therefore no recommendation it is given herewith as to

the quality of the instruction and its suitability for BDB needs.

6.4.2 Recommendation BDB needs to implement a more formal, academically rigorous, and homogeneous training

process for credit assistant and credit officers. The credit and human resources departments

should create a committee to establish the new plan and follow up on its implementation.

18

Introductory/Induction course The introductory course should be at least a three weeks program in a formal classroom

setting. An examination should be mandatory for participants, and a minimum grade require

for employment as a credit assistant or officer of BDB.

The course can be taught by either i) experienced BDB credit officers (current approach) or ii)

outside instructors from training institutes like FITI or outsourced from experienced trainers

(from Bhutan or internationally). If approach i) is selected, then BDB trainers should be

prepared in training techniques and a course syllabus should be prepared with the assistance of experienced educators/trainers in the field of credit analysis.

Separate curricula should be developed for credit officers and assistants

The course should cover areas such as:

• Financial analysis and modeling. Financial statement analysis, including a clear understanding of the differences between income and cash flow.

• Preparation of cash flow and debt service coverage projections.

• SME/microfinance fundamentals.

• Calculation and interpretation of key financial ratios.

• Risk management. Identification of potential liquidity problems and collateral quality.

• Agriculture/Livestock credit fundamentals and cash drivers.

• Introduction to BDB credit models (to be developed)

• Client relationship management and due diligence. Challenges of dealing with customers without financial literacy.

• Loan file preparation

Continuing education/first two years During the first two years junior credit personnel should attend online and classroom setting

courses following up on the fundamentals of the introductory/induction course. Senior credit

officers, branch and credit management should assess the progress of the junior credit personnel and provide instruction in areas of need. Substandard performers should be

reassigned to other areas within the bank.

Two Years Junior graduation/course abroad After two years of service junior credit personnel should receive a formal evaluation by their

supervisors in addition of their annual review. Only those recommended by their supervisors and with the approval of the credit department deputy general manager should continue in the

credit department. In their third year of service all recommended credit personnel should

attend the credit training abroad, currently NIBM, India.

Credit officers are the cornerstone of a successful MFI. Only those with the right aptitude should proceed with a career in credit, for those that are not considered suitable for the career

other opportunities can be present in the bank.

Training on agriculture production and supply chains All credit personnel should go through specialized training in agriculture production and supply

chain fundamentals. Credit officers should be able to assess the cash generating capacity of different agricultural businesses, the underlying risks and success factors.

19

FITI instructional material

7 Information Technology

7.1 Hardware and Servers The following hardware is used for the CBS

• Data Center

• Sparc T7 – 4 Production Server 1

• Sparc T7 – 4 Production Server 2

• Sparc T7 – 1 UAT Server

• Oracle Server X6 – 2 OPS/ OSB

• Oracle Server X6-2L

Switch Server, Citrix

• ORACLE SERVER X6-2L

Switch Server, Citrix

• Oracle ZS3-2 Controller1

• Oracle ZS3-2 Controller2

• Oracle ZS3-2 DE2-24P-1

(JBOD-1)

• Oracle ZS3-2 DE2-24P-2

(JBOB-2)

• SL-150

• (3) Oracle Switch ES1-24

10G Ethernet Switch

• (2) Radware Alteon NLB

• Disaster recovery site:

• SPARC T7-4

• SPARC T7-1

Switch Server, Citrix

• Oracle ZS3-2 Controller1

• Oracle ZS3-2 Controller2

• Oracle ZS3-2 DE2-24P-1

(JBOD-1)

• Oracle ZS3-2 DE2-24P-1

(JBOD-2)

• San Switch

• Oracle Switch ES1-24

10G Ethernet Switch

20

7.2 Core Banking System and Management Information Systems Since the implementation of the Finacle (Infosys) CBS in 2017 all BDB branches are linked in

real time to a data center through a network. Implementation was conducted by Nelito Systems

Ltd., an Indian financial technology company. BDB currently runs Finacle version 10.2.18

Finacle CBS is customer centric. All products and services offered in Finacle are built around the customer. Every individual or business has a unique identity.

In Finacle CBS all delivery channels (ATMs, Internet, SMS, Mobile banking) are integrated.

The loan module presents a variety of useful reports and raw data in excel format to further

analysis. It is a powerful system that facilitates performance evaluation and informed decision making.

7.3 Assessment Even though the system was implemented in 2017 it still has numerous cases of erroneous and incomplete data. Obvious errors like negative principal balances, negative days aging,

loans categorized as loss but with zero days aging are present in the data. Many fields haven’t been completed, particularly sector and subsector codes.

Similar conclusion was reached by the Royal Audit Authority. On April 2019 the RAA conducted and IT audit on the core banking of BDB, with emphasis on the implementation of

Finacle. Among the findings the audit concludes that “The reports generated by Finacle CBS

were incorrect with cases such as unreconciled differences in the trail balance and wrong

information reflected in portfolio at risk reports and non-performing loan reports.” 8

Finacle CBS generates general ledger and trial balance of each branch and at bank level.

Therefore, reports generated in Finacle should have the same figures presented in the

financial statements and when there are differences, they should be reconcilable.

Unreconcilable differences reflect an integration problem in the accounting system, and it is not acceptable after the investment in the CBS. Consistent reporting figures gives

management and stakeholders confidence in the accuracy of the reporting. However, loan

reports generated by the CBS reviewed by the consultant had nontrivial differences with

figures presented in the 2018 audited reports and in management approved interim financials. For example, the amount of total loans outstanding in the management approved financial

statements ending June 2019 was Nu 18.8 billion in the MIS the figure was 19.7 billion.

Differences might be explained by difference in the treatment of interest accruals for non-

performing loans but repeated questions to management about the nature of the differences and how to reconcile them have not been answered as of the time of this report.

The audit report and the observations contained in this report show serious deficiencies in the

implementation of Finacle that have not been resolved to date.

Document management information system was integrated to Finacle in the second semester of 2018. However, the consultant had not been able to verify the existence of loan

documentation in any loan registered.

The report with management information submitted to the CEO with the monthly consolidated

statements does not contain executive information for decision making.

Aspects to include on a term of reference of a comprehensive IT audit might include: 9

• Third-party Security Controls

• Threat and Vulnerability Management

8 Royal Audit Authority. IT Audit Report on Core System in BDB. 9 KPMG. Insights to take you forward. IT internal audit planning for 2020.

21

• Identity and Access Management

• Security Strategy and Governance

• Security Incident Response and Testing Exercises

• Cyber Hygiene

• Personal Security/Insider Threat

• Remote, Mobile, and Wireless Security

• Network Security

• Security Awareness

• Product Security

• Logging and Monitoring

• Operational Technology

• Physical Security

BDB has never conducted an IT Audit.

7.4 Recommendation Finacle is a great instrument to provide up to date actionable information for decision making.

But any system is at the end as good as the quality of the data that has been entered.

In particular:

• Data in the system should be reviewed, errors rectified, and information incorporated

in blank data fields.

• There should be no unreconcilable discrepancies between the output of Finacle and

the information in the financial statements. If any difference exists, it should be easily

explained and reconciled. This should be rectified with urgency.

• All new loan documentation should be inputted in Finacle’s document management

system. An effort should be made to input existing loan documentation with certain deadlines, for example by the end of fiscal year 2020 all loans approved from 2018

should have updated documentation in the system.

• Information from Finacle system should be summarized in easily readable tables and

graphs and presented to management periodically.

• Nelito Systems Ltd quality of services should be reviewed against the specifications in

the contract.

• The results of the RAA and the assessment of this report bring into consideration the

need to conduct an independent IT audit of BDB systems by an experienced firm. This

should be done prior to the conclusion of the 2020 fiscal year.

8 Internal Audit

8.1 Board Audit Committee “The Audit Committee (BAC) has oversight responsibility on behalf of the Board and the

Shareholders to monitor and provide advices and directives on the operation of the Internal

Control system and Internal Activities, Financial reporting, External audit, Account and Legal

compliance of the Bank” 10

The BAC has two or three members with the General Manager of the Internal Audit

Department as member secretary. BAC meets quarterly or in extraordinary meeting if needed or directed by the Board. The Chairman of the Board and the CEO are not be members of the

BAC, following internationally accepted practices of internal audit.

10 BDB Board Audit Charter 2019.

22

The Board Audit charter documents BAC activities clearly and comprehensively.

8.2 Internal Audit Department The internal audit department (IAD) has eleven employees and is headed by a General

Manager that reports to the BAC. The Internal Audit Manual 2019 (IAM) regulates de

standards of practice for the Internal Audit Department. The audit services are classified into regular audit, surprise audit and investigation audit. The auditable units are all financial

services delivery units and support services that use resources of the Bank while discharging

their functions. The regular audit in the auditable units is done at least once in every three

years among the IAD, Royal Audit Authority and external auditors for mitigation of the risk of the bank. The IAM is a comprehensive manual and follows best practices.

23

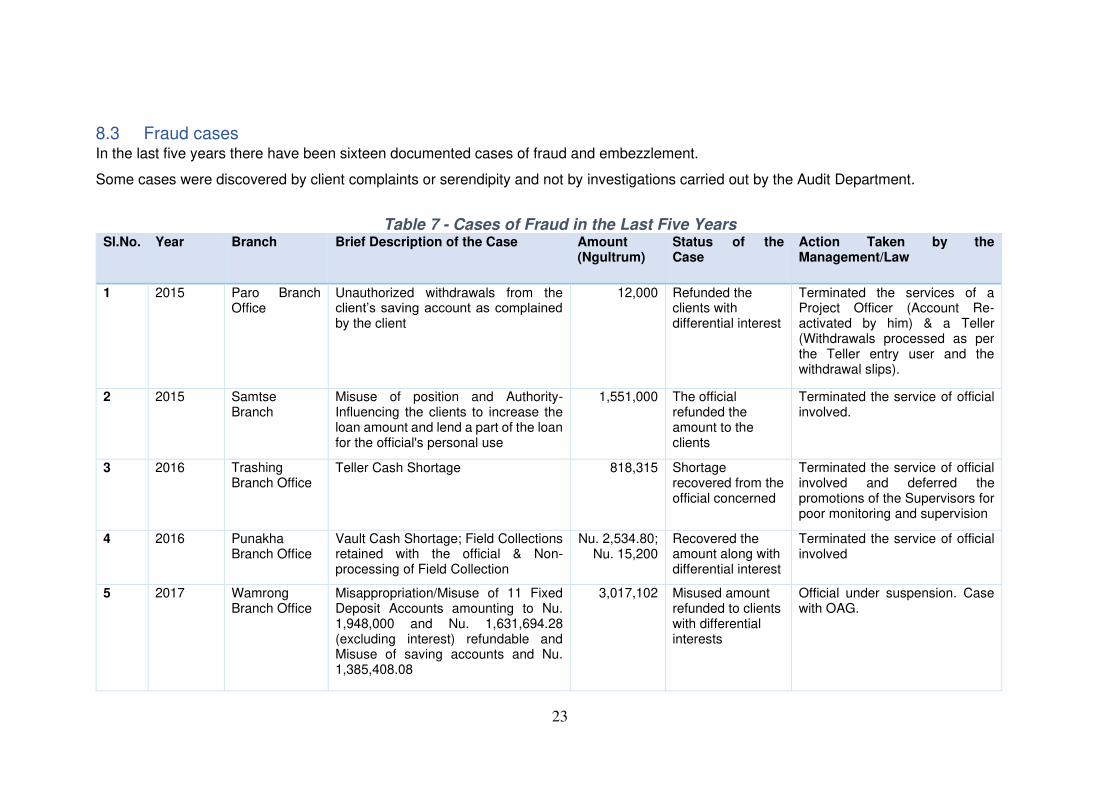

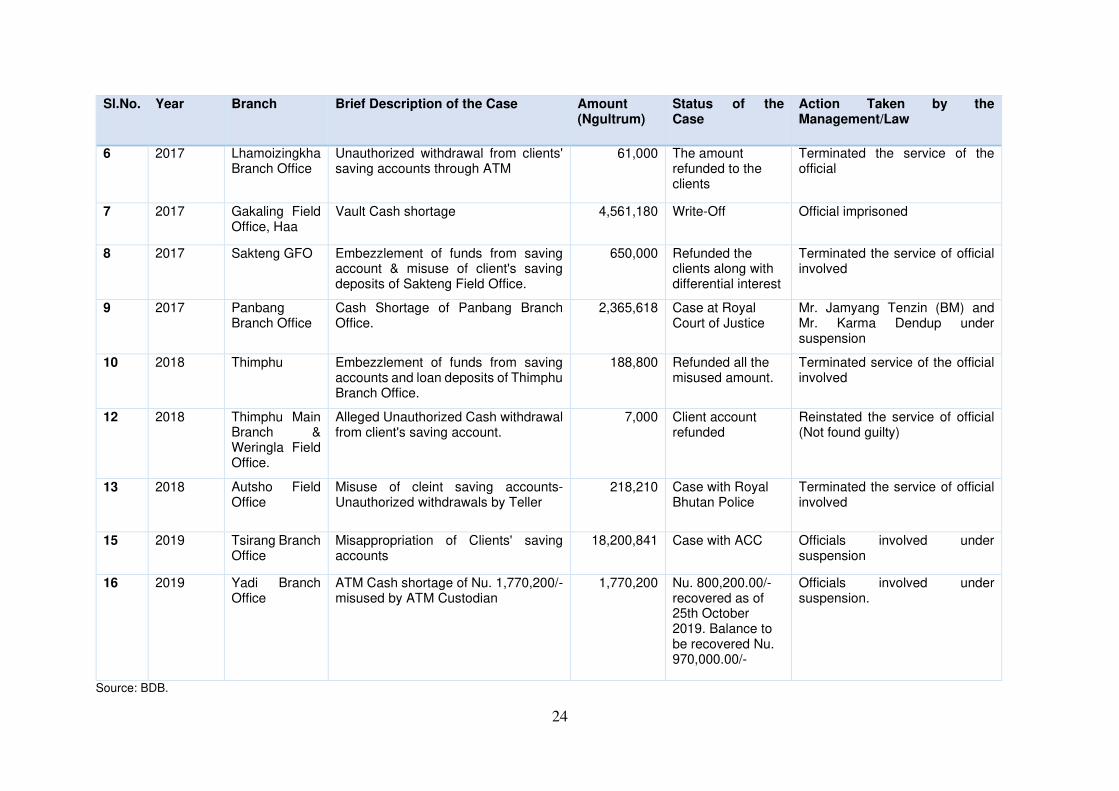

8.3 Fraud cases In the last five years there have been sixteen documented cases of fraud and embezzlement.

Some cases were discovered by client complaints or serendipity and not by investigations carried out by the Audit Department.

Table 7 - Cases of Fraud in the Last Five Years Sl.No. Year Branch Brief Description of the Case Amount

(Ngultrum) Status of the Case

Action Taken by the Management/Law

1 2015 Paro Branch Office

Unauthorized withdrawals from the client’s saving account as complained by the client

12,000 Refunded the clients with differential interest

Terminated the services of a Project Officer (Account Re-activated by him) & a Teller (Withdrawals processed as per the Teller entry user and the withdrawal slips).

2 2015 Samtse Branch

Misuse of position and Authority- Influencing the clients to increase the loan amount and lend a part of the loan for the official's personal use

1,551,000 The official refunded the amount to the clients

Terminated the service of official involved.

3 2016 Trashing Branch Office

Teller Cash Shortage 818,315 Shortage recovered from the official concerned

Terminated the service of official involved and deferred the promotions of the Supervisors for poor monitoring and supervision

4 2016 Punakha Branch Office

Vault Cash Shortage; Field Collections retained with the official & Non-processing of Field Collection

Nu. 2,534.80; Nu. 15,200

Recovered the amount along with differential interest

Terminated the service of official involved

5 2017 Wamrong Branch Office

Misappropriation/Misuse of 11 Fixed Deposit Accounts amounting to Nu. 1,948,000 and Nu. 1,631,694.28 (excluding interest) refundable and Misuse of saving accounts and Nu. 1,385,408.08

3,017,102 Misused amount refunded to clients with differential interests

Official under suspension. Case with OAG.

24

Sl.No. Year Branch Brief Description of the Case Amount (Ngultrum)

Status of the Case

Action Taken by the Management/Law

6 2017 Lhamoizingkha Branch Office

Unauthorized withdrawal from clients' saving accounts through ATM

61,000 The amount refunded to the clients

Terminated the service of the official

7 2017 Gakaling Field Office, Haa

Vault Cash shortage 4,561,180 Write-Off Official imprisoned

8 2017 Sakteng GFO Embezzlement of funds from saving account & misuse of client's saving deposits of Sakteng Field Office.

650,000 Refunded the clients along with differential interest

Terminated the service of official involved

9 2017 Panbang Branch Office

Cash Shortage of Panbang Branch Office.

2,365,618 Case at Royal Court of Justice

Mr. Jamyang Tenzin (BM) and Mr. Karma Dendup under suspension

10 2018 Thimphu Embezzlement of funds from saving accounts and loan deposits of Thimphu Branch Office.

188,800 Refunded all the misused amount.

Terminated service of the official involved

12 2018 Thimphu Main Branch & Weringla Field Office.

Alleged Unauthorized Cash withdrawal from client's saving account.

7,000 Client account refunded

Reinstated the service of official (Not found guilty)

13 2018 Autsho Field Office

Misuse of cleint saving accounts- Unauthorized withdrawals by Teller

218,210 Case with Royal Bhutan Police

Terminated the service of official involved

15 2019 Tsirang Branch Office

Misappropriation of Clients' saving accounts

18,200,841 Case with ACC Officials involved under suspension

16 2019 Yadi Branch Office

ATM Cash shortage of Nu. 1,770,200/- misused by ATM Custodian

1,770,200 Nu. 800,200.00/- recovered as of 25th October 2019. Balance to be recovered Nu. 970,000.00/-

Officials involved under suspension.

Source: BDB.

25

The largest case was uncovered in 2019:

Misappropriation of clients’ savings accounts The total refundable amount to clients for misappropriation were Nu 18.7 million.

Two tellers stole from client’s savings accounts through issuance of fake receipts, by forging the clients’ signatures and manipulating saving accounts in the system. The embezzlement

scheme went through from 2012.

The Internal Audit Department investigation cites as causes of the lapse in control:

• Poor staff integrity

• Poor supervisory control and huge leeway given to the tellers. It is not proper for the tellers who are responsible for the front office transactions to also carry out back office

transactions.

• Loan and savings balance confirmation not done. Practice is to carry out loans and

savings balance confirmation at least once a year. If practice would have been followed

the fraud would have not taken place.

• Staff transfer not done in time.

• System password sharing. Tellers used passwords allegedly shared by a project officer

and the branch assistant.

8.4 Assessment and Recommendations BDB has in place all the procedures and manuals necessary to minimize the fraud cases.

Most of the cases identified were the consequence of lapses in following procedures in place,

particularly the dual “maker and checker” process and the segregation of duties principle. The

lapses are not the product of poor procedures but a failure to apply them.

Management explains these lapses by not having enough personnel in every branch. If a

branch is not viable with the cost of having enough personnel to operate with the controls

established in the procedures of the bank, then consideration should be given to its closure or

continuing operations with adequate staffing and a cross subsidy from profitable branches. Under no circumstances exceptions to control procedures should be allowed. Internal audit

should include an assessment of the appropriateness of each branch staffing to adequately

follow procedures. Branch managers should be adequately informed of a zero-tolerance policy

and cases of no compliance taken seriously with the potential of separation of employment

from the bank.

9 Risk Management

BDB has a Risk Management Division, a Risk Management Committee, and a Risk

Management Board Committee.

The Risk Management Division is staffed with two credit officers and a division head. It produces monthly reports that are circulated to the CEO and BDB general managers.

The report is well organized and summarizes the risk status for five risk categories: Credit risk,

operational risk, reputational risk, market risk and liquidity risk. Areas in which the reporting

can be improved include branch analysis, asset liability maturity mismatch and scenario analysis. The report should include a more detail analysis of the credit management, including

the analysis and graphs presented in section 10.2 of this report.

26

10 Products

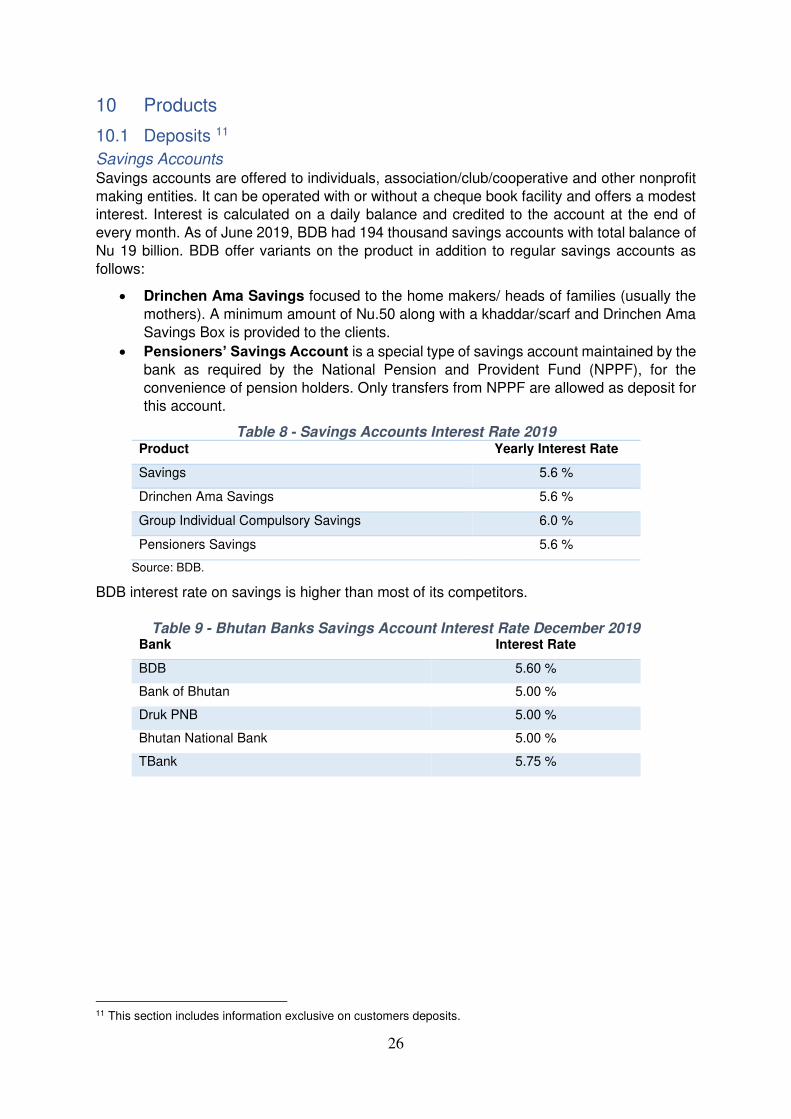

10.1 Deposits 11

Savings Accounts Savings accounts are offered to individuals, association/club/cooperative and other nonprofit

making entities. It can be operated with or without a cheque book facility and offers a modest interest. Interest is calculated on a daily balance and credited to the account at the end of

every month. As of June 2019, BDB had 194 thousand savings accounts with total balance of

Nu 19 billion. BDB offer variants on the product in addition to regular savings accounts as

follows:

• Drinchen Ama Savings focused to the home makers/ heads of families (usually the

mothers). A minimum amount of Nu.50 along with a khaddar/scarf and Drinchen Ama

Savings Box is provided to the clients.

• Pensioners’ Savings Account is a special type of savings account maintained by the

bank as required by the National Pension and Provident Fund (NPPF), for the

convenience of pension holders. Only transfers from NPPF are allowed as deposit for this account.

Table 8 - Savings Accounts Interest Rate 2019 Product Yearly Interest Rate

Savings 5.6 %

Drinchen Ama Savings 5.6 %

Group Individual Compulsory Savings 6.0 %

Pensioners Savings 5.6 %

Source: BDB.

BDB interest rate on savings is higher than most of its competitors.

Table 9 - Bhutan Banks Savings Account Interest Rate December 2019 Bank Interest Rate

BDB 5.60 %

Bank of Bhutan 5.00 %

Druk PNB 5.00 %

Bhutan National Bank 5.00 %

TBank 5.75 %

11 This section includes information exclusive on customers deposits.

27

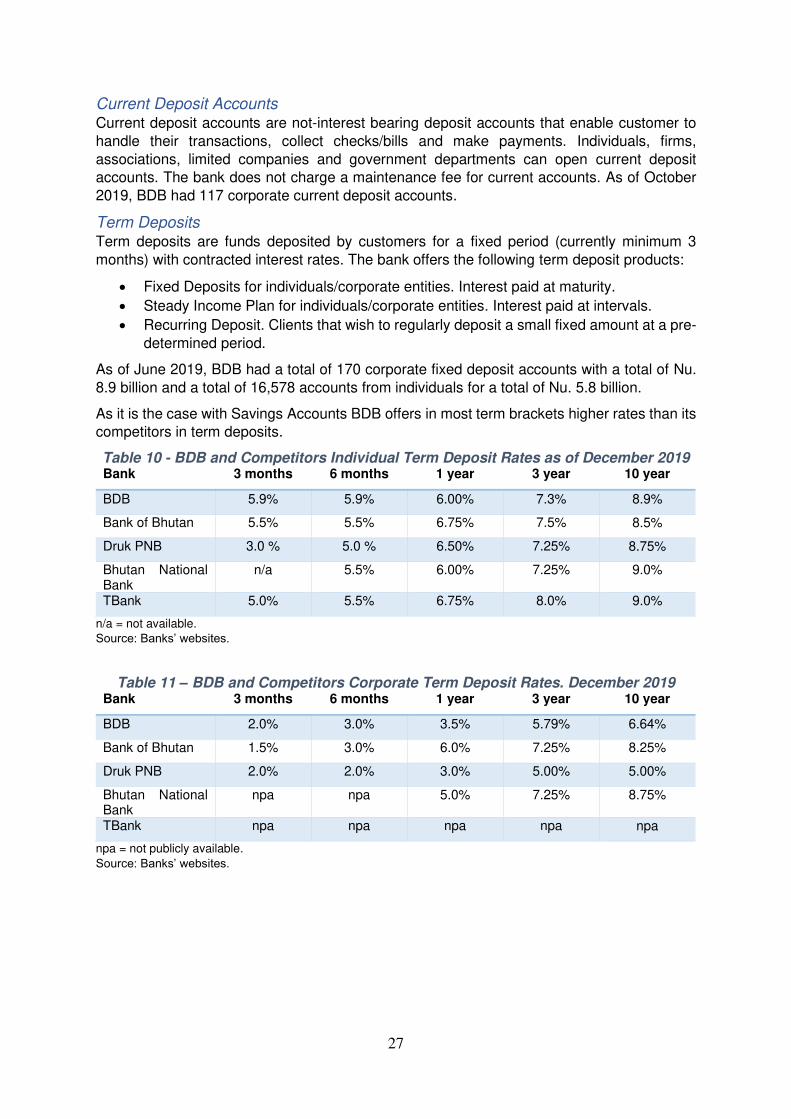

Current Deposit Accounts Current deposit accounts are not-interest bearing deposit accounts that enable customer to

handle their transactions, collect checks/bills and make payments. Individuals, firms,

associations, limited companies and government departments can open current deposit accounts. The bank does not charge a maintenance fee for current accounts. As of October

2019, BDB had 117 corporate current deposit accounts.

Term Deposits Term deposits are funds deposited by customers for a fixed period (currently minimum 3

months) with contracted interest rates. The bank offers the following term deposit products:

• Fixed Deposits for individuals/corporate entities. Interest paid at maturity.

• Steady Income Plan for individuals/corporate entities. Interest paid at intervals.

• Recurring Deposit. Clients that wish to regularly deposit a small fixed amount at a pre-

determined period.

As of June 2019, BDB had a total of 170 corporate fixed deposit accounts with a total of Nu.

8.9 billion and a total of 16,578 accounts from individuals for a total of Nu. 5.8 billion.

As it is the case with Savings Accounts BDB offers in most term brackets higher rates than its competitors in term deposits.

Table 10 - BDB and Competitors Individual Term Deposit Rates as of December 2019 Bank 3 months 6 months 1 year 3 year 10 year

BDB 5.9% 5.9% 6.00% 7.3% 8.9%

Bank of Bhutan 5.5% 5.5% 6.75% 7.5% 8.5%

Druk PNB 3.0 % 5.0 % 6.50% 7.25% 8.75%

Bhutan National Bank

n/a 5.5% 6.00% 7.25% 9.0%

TBank 5.0% 5.5% 6.75% 8.0% 9.0%

n/a = not available.

Source: Banks’ websites.

Table 11 – BDB and Competitors Corporate Term Deposit Rates. December 2019 Bank 3 months 6 months 1 year 3 year 10 year

BDB 2.0% 3.0% 3.5% 5.79% 6.64%

Bank of Bhutan 1.5% 3.0% 6.0% 7.25% 8.25%

Druk PNB 2.0% 2.0% 3.0% 5.00% 5.00%

Bhutan National Bank

npa npa 5.0% 7.25% 8.75%

TBank npa npa npa npa npa

npa = not publicly available.

Source: Banks’ websites.

28

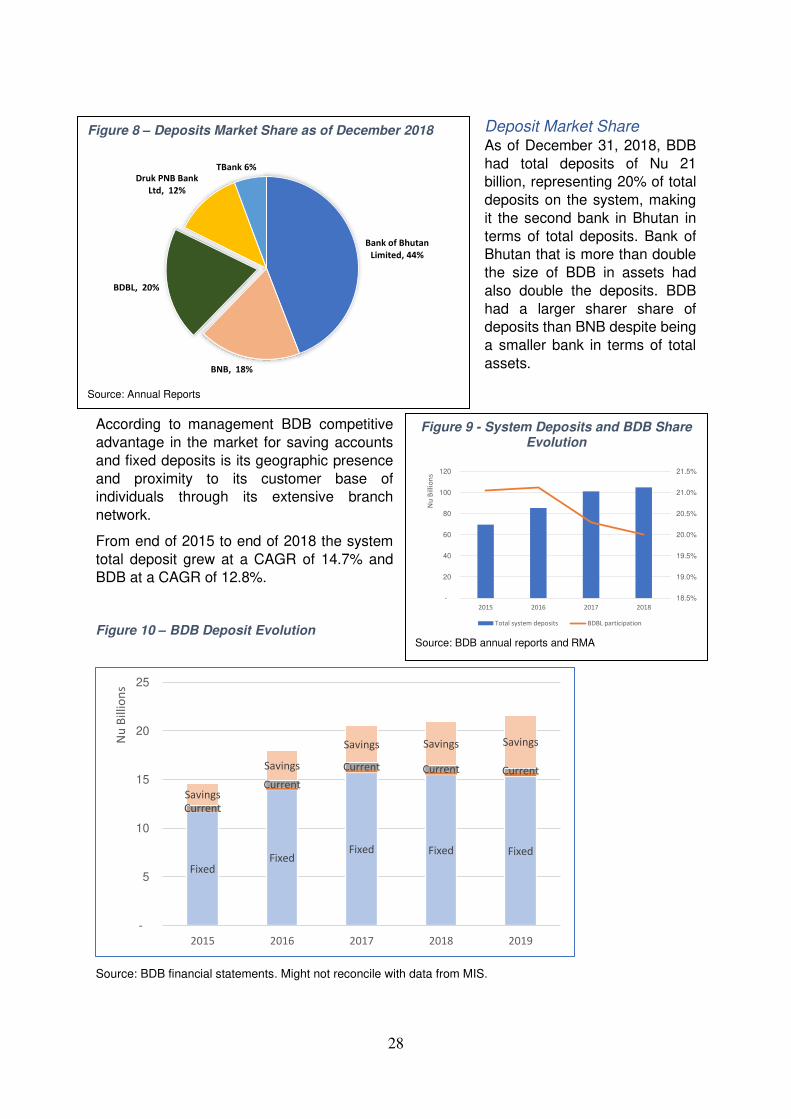

Deposit Market Share As of December 31, 2018, BDB

had total deposits of Nu 21 billion, representing 20% of total

deposits on the system, making

it the second bank in Bhutan in

terms of total deposits. Bank of Bhutan that is more than double

the size of BDB in assets had

also double the deposits. BDB

had a larger sharer share of deposits than BNB despite being

a smaller bank in terms of total

assets.

According to management BDB competitive

advantage in the market for saving accounts

and fixed deposits is its geographic presence

and proximity to its customer base of individuals through its extensive branch

network.

From end of 2015 to end of 2018 the system

total deposit grew at a CAGR of 14.7% and BDB at a CAGR of 12.8%.

Figure 10 – BDB Deposit Evolution

Source: BDB financial statements. Might not reconcile with data from MIS.

FixedFixed

Fixed Fixed Fixed

Current

Current

Current Current Current

Savings

Savings

Savings Savings Savings

-

5

10

15

20

25

2015 2016 2017 2018 2019

Nu

Bil

lio

ns

Figure 8 – Deposits Market Share as of December 2018

Source: Annual Reports

Bank of Bhutan

Limited, 44%

BNB, 18%

BDBL, 20%

Druk PNB Bank

Ltd, 12%

TBank 6%

Figure 9 - System Deposits and BDB Share Evolution

Source: BDB annual reports and RMA

18.5%

19.0%

19.5%

20.0%

20.5%

21.0%

21.5%

-

20

40

60

80

100

120

2015 2016 2017 2018

Nu

Bil

lio

ns

Total system deposits BDBL participation

29

From 2015 to 2018 interest bearing deposits represented the largest portion of BDB deposits.

BDB was able to increase the participation of lower yielding savings deposits in the mix.

Delivery channels BDB customers can have access through the network of 35 branches and 26 Geog field offices, ATMs in 39 locations and -since 2020- through internet and mobile banking (BDB

epay) BDB epay offers account statements, fund transfers, bill payment, loan repayment,

mobile eload and cardless cash withdrawal.

Deposits - Assessment and Recommendations BDB has a market share of deposits in relation with its size and further increasing it might not be possible.

BDB has a disproportionate higher share on fixed deposits (29% of the market) because of its

higher interest rates and a negligible share of current deposits (2% of the market). In

December 2018 the market mix of current accounts/total deposits was 23% while BDB was only 3%. This difference in the deposit mix to the market translates in a higher cost of funding

for BDB than that of other commercial banks.

Management indicated that one reason behind the low participation in current accounts is that

Bhutan’s government and SOEs operate through Bank of Bhutan. Also, government employees have their salaries directedly deposit to Bank of Bhutan. Management is

negotiating with the government to have access to its funds, particularly in the gewogs, where

BDB can provide better service than the competition.

BDB Punakha Branch

30

10.2 Loans 12

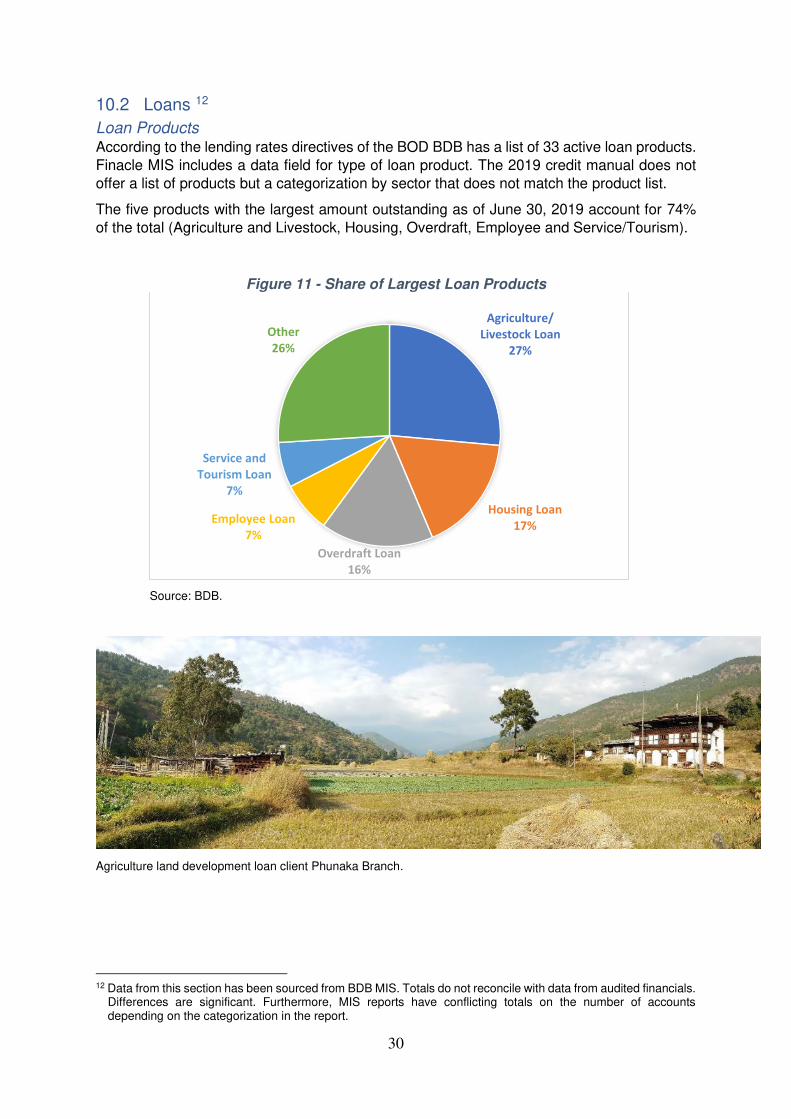

Loan Products According to the lending rates directives of the BOD BDB has a list of 33 active loan products.

Finacle MIS includes a data field for type of loan product. The 2019 credit manual does not

offer a list of products but a categorization by sector that does not match the product list.

The five products with the largest amount outstanding as of June 30, 2019 account for 74%

of the total (Agriculture and Livestock, Housing, Overdraft, Employee and Service/Tourism).

Figure 11 - Share of Largest Loan Products

Source: BDB.

Agriculture land development loan client Phunaka Branch.

12 Data from this section has been sourced from BDB MIS. Totals do not reconcile with data from audited financials.

Differences are significant. Furthermore, MIS reports have conflicting totals on the number of accounts depending on the categorization in the report.

Agriculture/

Livestock Loan

27%

Housing Loan

17%

Overdraft Loan

16%

Employee Loan

7%

Service and

Tourism Loan

7%

Other

26%

31

Table 12 - List of Loan Products – Total Gross Loan Outstanding Nu millions Jun-19 Share of total

Agriculture/Livestock Loan 5,226 26.48%

Housing loan 3,386 17.15%

Overdraft Loan 3,240 16.41%

Employee Loan 1,451 7.35%

Service and Tourism Loan 1,299 6.58%

Transport Loan 971 4.92%

General Trade Loan 765 3.87%

Personal Loan 617 3.13%

Working Capital Loan (OD) 469 2.37%

Manufacturing/Industrial Loans 440 2.23%

Overseas Education 360 1.82%

Housing loan commercial 293 1.49%

Staff Loan 292 1.48%

Seasonal Loan 242 1.22%

Group Term Loan 190 0.96%

Micro Enterprise Loan (BCCI Scheme) 128 0.65%

Education and Skill Enhancement Loan 98 0.50%

Small Scale Industrial Loan 74 0.37%

Loan Against Term Deposit 61 0.31%

Construction Loan 38 0.19%

Loan to Purchase Securities 33 0.17%

PSL (Agriculture CSI) 13 0.06%