Chapter 5: Working Capital Management 2014

1 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Financial Management

Bachelors of Business (Specialized in

HRM) – Study Notes

Chapter 5: Working Capital Management

Chapter 5: Working Capital Management 2014

2 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

INTRODUCTION

Working capital management refers to the management of current assets and current liabilities

that are required for the daily operations of the company. It involves the determination of

working capital policy and the implementation of this policy in the daily operations.

Working capital policy comprised of the working capital level and how the working capital

should be financed. For example, a firm needs to make a decision on how much cash that needs

to be kept in the accounts and the inventory level that needs to be maintained. Besides that, a

firm also needs to make decisions on whether to finance its current assets with short-term fund,

long-term funds or a combination of both.

Working capital management is more obvious in small or medium size companies. This is

because small and medium size companies have limited alternative financing compared to larger

companies. The financing resources are focused on trade credit and bank loans. Therefore, the

finance managers of small and medium size companies are more inclined to use short-term fund

resources to fulfil their financing requirements.

IMPORTANCE OF WORKING CAPITAL MANAGEMENT

The management of working capital is important for several reasons. For one thing, the current

assets of a typical manufacturing firm account for over half of its total assets. For a distribution

company, they account for even more. Excessive levels of current assets can easily result in a

firm realizing a substandard return on investment. However, firms with too few current assets

may incur shortages and difficulties in maintaining smooth operations.

For small companies, current liabilities are the principal source of external financing. These

firms do not have access to the longer-term capital markets, other than to acquire a mortgage on

a building. The fast-growing but larger company also makes use of current liability financing.

For these reasons, the financial manager and staff devote a considerable portion of their time to

working capital matters. The management of cash, marketable securities, accounts receivable,

accounts payable, accruals, and other means of short-term financing is the direct responsibility of

the financial manager; only the management of inventories is not. Moreover, these management

responsibilities require continuous, day-to-day supervision. Unlike dividend and capital structure

decisions, you cannot study the issue, reach a decision, and set the matter aside for many months

to come. Thus working capital management is important, if for no other reason than the

Chapter 5: Working Capital Management 2014

3 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

proportion of the financial manager’s time that must be devoted to it. More fundamental,

however, is the effect that working capital decisions have on the company’s risk, return, and

share price.

Working capital is required for the daily operations of the company. Efficient working capital

management is important to ensure that the firm does not have any liquidity problems that will

effect the operations of the company. At the same time, efficient working capital management

also means that the company was successful in conducting its business without too much funds

being tied up in the form of current assets.

Current assets and current liabilities are the main items in the daily operations. Most of the

management’s time is focused on the working capital management such as:

Controlling the cash inflows and outflows

Preparing credit facilities to customers; and

Always ensuring adequate stock.

Chapter 5: Working Capital Management 2014

4 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Net Working Capital

Net working capital is the difference between current assets and current liabilities.

Net working capital = Current assets - Current liabilities

To have a better understanding of the concept of net working capital, look at Example.

Based on the above summary balance sheet of Inthi Company Plc Ltd., the net working capital

for Inthi Company Plc Ltd is:

Net working capital = Current assets - Current liabilities

= MVR376,600 - MVR162,700

= MVR213, 900

This shows that Inthi Company Plc Ltd has the ability to fulfil its short-term financial claims

whenever required. In other words, the net working capital can be used as a measurement of the

company's liquidity.

Current Assets

Current assets comprise of cash and assets that can be converted into cash in a period not more

than one year. Current assets are also known as liquid assets as it is easily converted into cash in

a short period of time. Current assets comprise of:

(a) Cash

Money in hand or bank.

(b) Marketable Securities

Marketable securities are short-term investments that can be converted into cash in a short period

of time.

(c) Account Receivables

Account receivables exist when the company makes sales by credit. Normally, the credit period

given is short and customers are expected to settle their debt within the date predetermined.

When payments have been made, the account receivables will convert to cash.

(d) Inventory

Commercial goods that will be sold to customers.

Chapter 5: Working Capital Management 2014

5 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

To fully understand the approach used in working capital management, we categorised the

current assets of the company into permanent current assets and temporary current assets.

Permanent Current Assets

Permanent current assets are investment in the current assets that are expected to be permanently

held by the company for a period of more than one year. The company will keep emergency or

safety stocks as inventory to fulfil unexpected requirements.

Temporary Current Assets

Temporary assets are assets that are held by the company for only a short period of time, which

is less than a year. This situation is more obvious for seasonal businesses where at certain times;

the expected sales are more than the sales in normal situations.

For example, when the festive season is approaching, companies that sell clothes will increase its

inventory to fulfil the demand that will normally increase. This increase in inventory is only

temporary as after the festival, the inventory level will return to its normal level.

After the current assets had been categorised into permanent current assets and temporary current

assets, the next question will be related to the sources of capital financing that are used to finance

the investment in these assets. To match the financing with the investments, the sources of

financing also have to be categorised into permanent financing source and temporary financing

source.

STRATEGIES OF WORKING CAPITAL MANAGEMENT

The net working capital management is especially drawn-up to explain the level of investments

that are suitable for current assets. Working capital management involves financial decisions

making that are simultaneously and interrelated with investments in current assets together with

the financing of these assets.

One of the methods used in working capital management is the matching of the assets’ lifetime

with the financing period used. This method is known as the hedging principle. The hedging

principle is also known as the matching principle or the principle of self-liquidating debt.

The hedging principle matches the cash flow characteristics of an asset with the maturity period

of financial source that is used to finance that asset. How is this hedging principle implemented?

There are three approaches that can be used to implement this principle, which are:

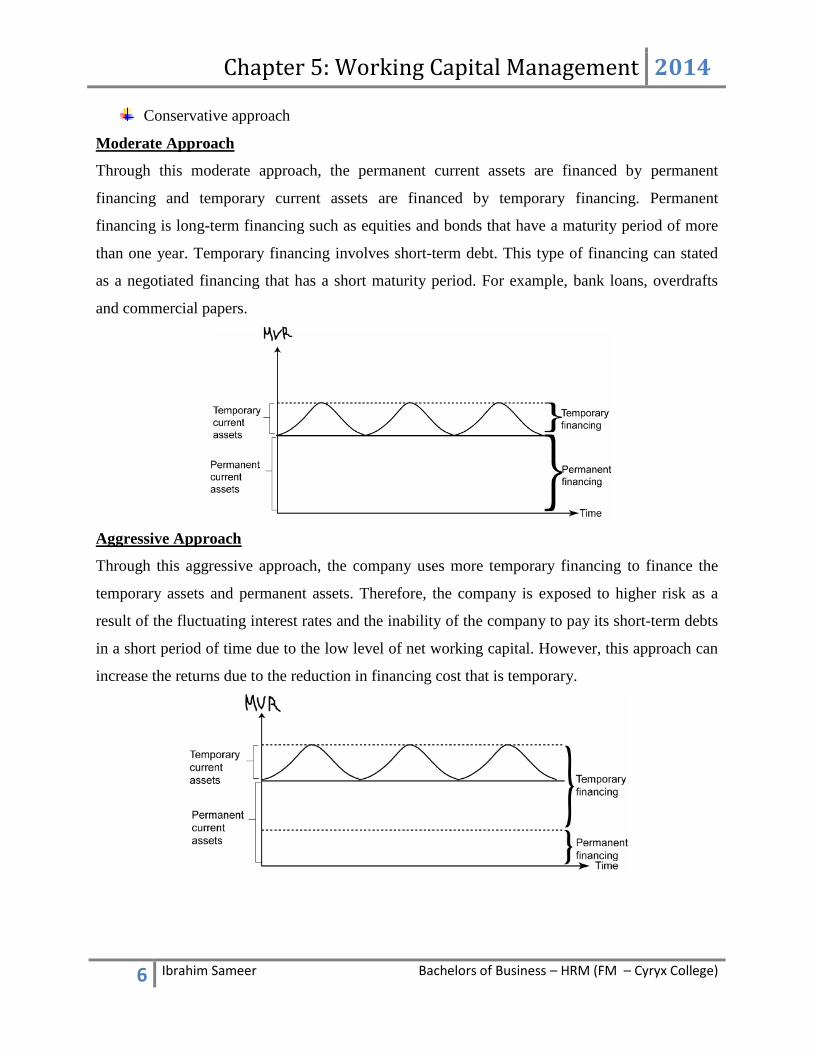

Moderate approach

Aggressive approach

Chapter 5: Working Capital Management 2014

6 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Conservative approach

Moderate Approach

Through this moderate approach, the permanent current assets are financed by permanent

financing and temporary current assets are financed by temporary financing. Permanent

financing is long-term financing such as equities and bonds that have a maturity period of more

than one year. Temporary financing involves short-term debt. This type of financing can stated

as a negotiated financing that has a short maturity period. For example, bank loans, overdrafts

and commercial papers.

Aggressive Approach

Through this aggressive approach, the company uses more temporary financing to finance the

temporary assets and permanent assets. Therefore, the company is exposed to higher risk as a

result of the fluctuating interest rates and the inability of the company to pay its short-term debts

in a short period of time due to the low level of net working capital. However, this approach can

increase the returns due to the reduction in financing cost that is temporary.

Chapter 5: Working Capital Management 2014

7 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Conservative Approach

Through this conservative approach, the permanent current assets and a part of the temporary

current assets are financed by permanent financing. A company that practices this approach has a

high level of net working capital. Therefore, it can fulfil its short-term claims at the

predetermined time. However, this approach will cause the company to be exposed to long-term

financing cost.

TYPES OF SHORT-TERM FINANCING

Current liabilities and short-term liabilities are debts or responsibilities of the company that must

be settled in the period of a year or less. In summary, short term financing is very important in

smoothing the daily operations of the company so that it would not be disrupted due to shortage

of cash.

Spontaneous Financing

Spontaneous financing exists due to the daily activities of the company. For example, when the

company’s sales increases, the inventory must also be increased and these additional purchases

are usually financed by trade credit.

Spontaneous financing can also exist as a result of the differences in timing between the actual

cash flow with the cash flow that should have occurred. For example, a company had obtained

the services of company’s employee for the period of 1 - 15 January but payments were only

made on 16 January.

The main sources for spontaneous financing are:

Chapter 5: Working Capital Management 2014

8 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

(a) Trade Credit

Trade credit is the credit facility offered by suppliers to customers. For suppliers, trade credits

will be recorded in the balance sheet at the current assets section (account receivable). While for

the customers, trade credits are located in the current liabilities section (account payable).

This financing source is obtained based on the trust by the suppliers to customers. The cost of

trade credit cannot be obtained directly, as the suppliers usually would not charge any interest on

the trade credits offered. However, when the suppliers offer discount, customers will bear a

higher effective cost if the discounts were not taken.

Example 10.2

Inthi Company Plc Ltd has made a purchase on credit from the supplier for MVR800 on the

terms of 3/10 net 30. If the company made the payment within 10 days, it will pay only MVR776

because the cash discount of MVR24 would be deducted from the invoice.

In summary, the company is assumed to have made a loan of MVR776 for the period of 20 days

with the interest payment of MVR24. Therefore, with the assumption of 365 days a year, the

annual cost borne by Inthi Company Plc Ltd as a result of foregoing the discount offered can be

estimated as follows:

Based on the calculation above, Inthi Company Plc Ltd had to bear the annual cost of 56.4% if it

did not accept the discount offer of 3/10 net 30.

(b) Accruals

Accruals exist when there is a delay in payment. For example, the employees’ salaries will only

be paid at the end of each month and also the employees’ salaries deduction (EPF and SOCSO)

by the employer will only be made on the 20th of the month. Financing sources through accruals

do not involve any costs. It is free to the company as long as it does not affect the credibility of

the company.

Negotiated Financing

The sources of negotiated financing are often obtained formally from financial institutions. It has

to undergo various procedures that have been predetermined. In this topic, we will focus on the

Chapter 5: Working Capital Management 2014

9 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

facilities provided by commercial banks, which are overdrafts and short-term loans only. Other

financing sources that will be discussed are commercial papers and factoring.

(a) Overdraft

Overdraft is a credit facility provided by banks to its customers. It is channelled through the

customer’s current accounts, where the customer is allowed to withdraw money in excess of the

balance in its current account. However, there is a limit set on the withdrawal. For example, Inthi

Company Plc Ltd received an overdraft facility for MVR50,000. This means that the company

can use the funds provided by the bank until the balance in its account reaches MVR50,000.

Overdraft facilities are very useful to a company that wishes to take the cash discount offered by

the supplier. The cost that needs to be borne by the customer who uses the overdraft service is

the interest that is applied based on the negative balance of the customer’s current account.

(b) Bank Loans

Besides overdrafts, banks will also provide services for short-term loan facilities. To understand

this negotiated financing via bank loans, see Example 10.3.

Example 10.3

Inthi Company Plc Ltd has obtained a bank loan of MVR200,000 for a period of 3 months at the

rate of 15% per year. At the end of the period, Inthi Company Plc Ltd repaid the principal

together with its interest. Before making calculations for the effective cost of the loan, the

interest amount must be ascertained in advance.

If you look at the above example, the effective cost of 15% is the same with the rate of the bank

loan. However, there are two characteristics in the cost of short-term loan that will make its value

higher than the nominal interest rate. These characteristics are the compensating balance and the

discounted interest.

Chapter 5: Working Capital Management 2014

10 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

(i) Compensating Balance

The compensating balance is the amount that must be kept in the bank account and remained as a

balance throughout the loan period. The requirement for this compensating balance makes the

actual amount received by the borrower to be less by the compensating balance amount.

However, the interest is still calculated based on the entire loan. By using Example 10.3 and

several additional information, we can see the effect of the compensating balance on the

effective cost of the loan.

The bank that provides the loan imposed the condition for compensating balance to be 10% of

the total loan. Assuming that Inthi Company Plc Ltd does not have the balance as required by the

compensating balance. Calculate the effective cost of this loan.

To obtain the effective cost of this loan, we need to obtain the value for:

Interest amount;

Compensating balance; and

Value of net loan

These information can be calculated as follows:

Based on the calculation above, the effective cost of the loan is higher compared to the value

before there was a compensating balance.

(ii) Discounted Interest

Through this characteristic, the borrower must pay interest when the loan amount is withdrawn.

This means that the payment of interest has been settled in advance before the loan can be used.

This condition makes the net amount obtained by the loan to be less than the amount borrowed.

However, the effective cost still increases as the interest is made based on the entire loan.

By using Example 10.3, the calculation of interest, net amount and the effective cost for Inthi

Company Plc Ltd are as follows:

Interest amount = MVR200,000 × 15% × 1.4 = MVR7,500

Chapter 5: Working Capital Management 2014

11 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Net loan = MVR200,000 - MVR7,500 = MVR192,500

From the explanation above, it is clear that the condition of compensating balance and

discounted interest will increase the cost of the company doing the borrowing.

(c) Commercial Papers

In Malaysia, the use of commercial papers is not widespread. Commercial papers are promissory

notes for short-term debt that are issued by companies with strong financial standing. The

issuance of this instrument is based on the confidence of investors toward the company's ability

to repay the loan at the date that has been predetermined.

Commercial papers are issued at a discounted price where the selling price is the face value after

deducting interest. The cost involved in the issuance of commercial papers comprised of all the

expenditures that are directly involved in the issuance of this security. For example, a company

that issues commercial papers will obtain the services of a merchant bank to sell it to the

investors. All these expenditure must be taken into account in estimating the effective cost of

financing through commercial papers.

Example 10.4

Inthi Company Plc Ltd will issue commercial papers that have a value of MVR20 million with a

maturity period of 6 months. The interest rate for these commercial papers is 10%. The cost

involved in issuing these commercial papers is MVR50,000.

The calculation of the effective cost is as follows:

Interest amount = MVR20 million × 10% × ½ year

= MVR1 million

Total cost = Interest + Issuing cost

= MVR1 million + MVR50,000

= MVR1.05 million

Net loan = MVR20 million - MVR1 million

= MVR19 million

Chapter 5: Working Capital Management 2014

12 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

(d) Factoring

Factoring is a transaction that involves the purchase of account receivables or the invoices from

supplier companies by the factoring companies. Financial institutions that conduct these

factoring activities are known as factor. It comprised of takeover and administration of account

receivables as well as the activity of collecting debt.

The cost of financing that is counted by factoring is the total financing and expenditure involved

such as the factoring fee (1% to 3% from the invoice value), interest on deposit and reserves (a

small percentage that is held by factor). The balance value of the invoice payable by factor will

only be settled to the company when the entire account receivables have been collected.

Example 10.5

Inthi Company Plc Ltd has factorised the account receivable totaling MVR200,000. The credit

period of the company is 60 days. The factoring fee is 3.5% of the invoice value while the

reserves are at 7.5%. The interest rate that is charged on the deposit is 12% per year. When the

deposit is received, the fees and interest must be settled. Based on previous practice of the

company, it will give cash deposit of 60% of the invoice value.

The following is the effective cost of financing through factoring:

Deposit = MVR200,000 × 60% = MVR120,000

Reserves = MVR200,000 × 7.5% = MVR15,000

Fees = MVR200,000 × 3.5% = MVR7,000

Interest = (MVR120,000 - MVR15,000 - MVR7,000) × 12% × 2/12

= MVR1,960

Net amount = MVR120,000 - MVR15,000 - MVR7,000 - 1,960

= RM96,040

Based on the calculation above, the effective cost of this financing is 55.98% and the company

obtains a deposit of MVR96,040 for the period of 2 months with the cost of MVR8,960 (fees and

Chapter 5: Working Capital Management 2014

13 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

interest). If all the account receivable can be collected successfully, the balance of RM80,000

including reserves of RM15,000 will be given by the factor to Endah Company Sdn. Bhd.

CASH CONVERSION CYCLE

The cash conversion cycle refers to the time period taken from the payment for the purchase of

raw materials to the receipt of cash from the sale of goods. Figure 10.4 shows the three main

components in the cash conversion cycle, which are:

(a) Cash/Inventory Conversion Period

- The average time period taken to convert raw materials into finished goods and selling them.

(b) Account Receivable Collection Period

- The average time period taken to obtain cash from credit sales.

(c) Deferred Payment Period

- The time period taken from the purchase of raw materials and labour until the payment of cash

for these items.

Example 10.6

Now, we will look at an example on how the calculation for cash conversion cycle is made. Jaya

Jati Company manufactures office fittings such as tables and chairs. The following are the cash

dealings of the company:

a) Purchase of raw materials on credit for the production of tables and chairs and the

company is given a period of 30 days to make payment.

b) Employees will be paid at the end of the month (that is after 30 working days).

c) The customers of the company will purchase the goods on credit. Therefore, the account

receivables will exist when sales are made.

d) The payment for raw materials and wages must be made at the date promised. As the

cash from the credit sales have not been received, the company has to finance the cash

flow with short-term loans.

Chapter 5: Working Capital Management 2014

14 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

e) The cash cycle will be complete when cash from the credit sales are received.

Subsequently, the cash will be used to pay the short-term loans that were taken to pay for

the raw materials and wages of employees.

Sales of Jaya Jati Company are RM1,500,000 while the average inventory is RM350,000.

Account receivables are RM85,750. Assume that there are 360 days in a year.

Based on the information above, the cash conversion cycle for Jaya Jati Company can be

calculated as follows:

Step 1: Calculate the cash conversion period

⁄

⁄

\

Step 2: Calculate the account receivable conversion period

⁄

⁄

\

Step 3: Calculate the deferred payment period

Based on the information above, the deferred payment period is 30 days (items a and b).

Step 4: Calculate the cash conversion cycle period

Cash conversion cycle = 84 days + 21 days - 30 days

= 75 days

Chapter 5: Working Capital Management 2014

15 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Based on the calculation above, Jaya Jati Company:

Requires 84 days to convert the raw materials into finished goods (office chairs and

tables);

21 days to obtain cash from the sales made on credit; and

Has 30 days to make payment on the purchase of raw materials and utilisation of labour.

Therefore, the time period between the withdrawal of cash (payments that were made for the

purchase of raw materials and utilisation labour) and the receiving of cash from the sales is 75

days.

BALANCE BETWEEN RISK-RETURN IN CASH MANAGEMENT

Cash management involves a balance between risk and rate of return. Cash that is insufficient

will cause the risk of liquidity or insolvency to the company such as the failure to fulfil liabilities

at the predetermined time. A cash holding that is too high will reduce the company’s returns as

cash is an asset that does not have any return.

Therefore, the management must look at the effect of risk and rate of return of the company in

determining the optimal holding level of cash and marketable securities. Decisions on the level

of risk that will be taken by the company depends on the decision that has been determined by

the companyÊs management.

Cash management has the purpose of achieving the following objectives:

Company has sufficient cash to fulfil the requirements of its transactions; and

Cash surplus must be at the minimum level as cash does not have any return.

MANAGEMENT OF ACCOUNT RECEIVABLE

Account Receivable

Account receivable exists when sales were made on credit. It is a promise from the customers to

make payment on the purchases that were made in a period that has been mutually agreed upon.

The importance of managing the account receivable can be determined by looking at the

percentage of the company's sales that were made on credit or the total account receivable for the

company.

The total account receivable for a company at a specific time is determined by the following two

factors:

(a) Credit sales level of the company

Chapter 5: Working Capital Management 2014

16 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

(b) Average collection time

Changes in any one of these factors will cause a change in the total account receivable for the

company. Therefore, the account receivable for a company at a specific time can be determined

as follows:

To further strengthen your understanding on the calculation of account receivable, refer to the

example.

Example 10.7

Rania Company is a company that manufactures plastic goods. It has an annual sales of

RM250,000 per year. All sales were made on credit and the credit terms is 2/10 net 30. Based on

previous experience, 60% of the company's customers will take the discount and pay on the 15th

day meanwhile the other 40% will make payments on the 30th day. Assuming that there are 360

days in a year, calculate the total account receivable for Rania Company.

Account receivable = Credit sales per day x Average collection time

This means that the average account receivable for Rania Company at a specific time is

RM14,583.33.

Credit Policy

The credit policy of a company is the procedure that has been set by the management in

managing the account receivable. Generally, the credit policy of a company comprised of credit

terms, credit standards and collection policies.

(a) Credit Terms

Credit terms refer to the terms that are made for the credit sales of the company. It is normally

written as x/y net z which means that the customer is entitled to get a discount or reduction in

price for x% of the purchase price if the payment is made within the period of y days. If the

customer does not want to take that discount, it has z days to make full payment.

Chapter 5: Working Capital Management 2014

17 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Assuming the credit terms of 2/10 net 30. This means that customers will get a 2% discount from

the invoice price if payment is made within 10 days of the invoice date. Customers who do not

take this discount will have to make payment within 30 days.

You can refer to the figure to get a graphical illustration of credit terms.

There are two things that form the credit term, which are:

(i) Credit Period

Credit period refers to the time period given to customers to make payments for credit purchases.

A longer credit period can increase sales and account receivable. A shorter credit period

decreases sales and account receivable.

(ii) Cash Discount

Cash discount is the reduction in price that is offered to the customers who made early payments.

The purpose of giving cash discounts to customers is to encourage early payments, attract new

customers and also to increase the sales.

Figure 10.6 shows 2 components that are involved in determining cash discounts

Example 10.8 can help you to understand the credit terms of a company more clearly.

Example 10.8

On 2 February 2001, U-Pen Company made credit sales amounting to RM85,000 based on the

terms 3/15 net 30. If the customers pay within the period of 15 days, which is until 17 February,

they will get a discount of 3%.

The discount amount can be calculated as follows:

Chapter 5: Working Capital Management 2014

18 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Discount = Percentage of discount × selling price

= 3% × RM85,000

= RM2,550

Total payments if discount is taken:

= (invoice price) × ( 1 X Discount percentage)

= RM85,000 × (1 X 0.03)

= RM82,450

Customers who do not take the discount are given 30 days to settle the payment at the invoice

price of RM85,000.

(b) Credit Standards

Customers who intend to deal in credit must fulfil the credit standards that had been determined

by the company. Credit standards can be seen as a minimum qualification test that must be

fulfilled by customers to obtain credit. The determination of credit standards will affect the risk

and rate of return.

Strict credit standard

Reduces sales, returns and financing cost for account receivables; and

Loose credit standard

Increases sales, returns and the financing cost for account receivables.

The application of the credit standards can be seen via an analysis of the Customers’ credit

applications conducted by companies via the 5C system. This system is a subjective value

measurement method that is widely used among credit managers.

This method measures the credit quality that comprised of five main sections, which are:

(i) Capacity/Capability

The capacity factor refers to the capacity or capability of the customer to make payments as

predetermined. Valuation can be made based on the consideration of business practice including

the customers’ previous records, especially those related to the pattern and trend of payments.

(ii) General Economic Conditions

The general economic conditions refer to the development in local or general economy that may

influence businesses that are being conducted by the customers. The economic conditions may

indirectly affect the ability of the customer in fulfilling their obligations.

(iii) Capital

Chapter 5: Working Capital Management 2014

19 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

The capital factor refers to the overall financial status of the customers. For the purpose of credit

evaluations, emphasis is made on the ratio related to the customers’ ownership status such as the

debt equity ratio, liquidity ratio and interest coverage ratio.

(iv) Character

Character refers to the enthusiasm shown by the customers in fulfilling their promise to make

payments as mutually agreed. Experienced credit officer can make accurate estimates on the

enthusiasm and sincerity of a customer based on information such as the customer’s previous

record with suppliers, banks and background information regarding the business owned by the

customer.

(v) Collateral

Collateral refers to any fixed assets that are pledged for the credit facilities. Finance managers

will evaluate the collateral based on the value and the marketability of the asset pledged.

(c) Collection Policies

Although most customers will make payments within the time period set, there are those who

had to delay payment unintentionally due to financial problems.

The following are the methods normally used to collect account receivable that had exceeded the

payment period set:

i. Sending reminder letters.

ii. Making telephone calls.

iii. Personal visits.

iv. Forwarding the accounts to collection agency.

v. Legal action.

vi. Including those accounts as bad debt account.

Credit Control

The next discussion involves another important aspect in the management of account receivable,

which is the evaluation on the effectiveness of the credit policy set. The optimal credit policy is

unique to a company as it is determined by the operating feature of that company itself. There are

two common methods used by companies to control account receivable, which are:

(a) Average Period Method

The average collection period refers to the average period that is required to collect cash from the

sales made on credit.

Chapter 5: Working Capital Management 2014

20 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

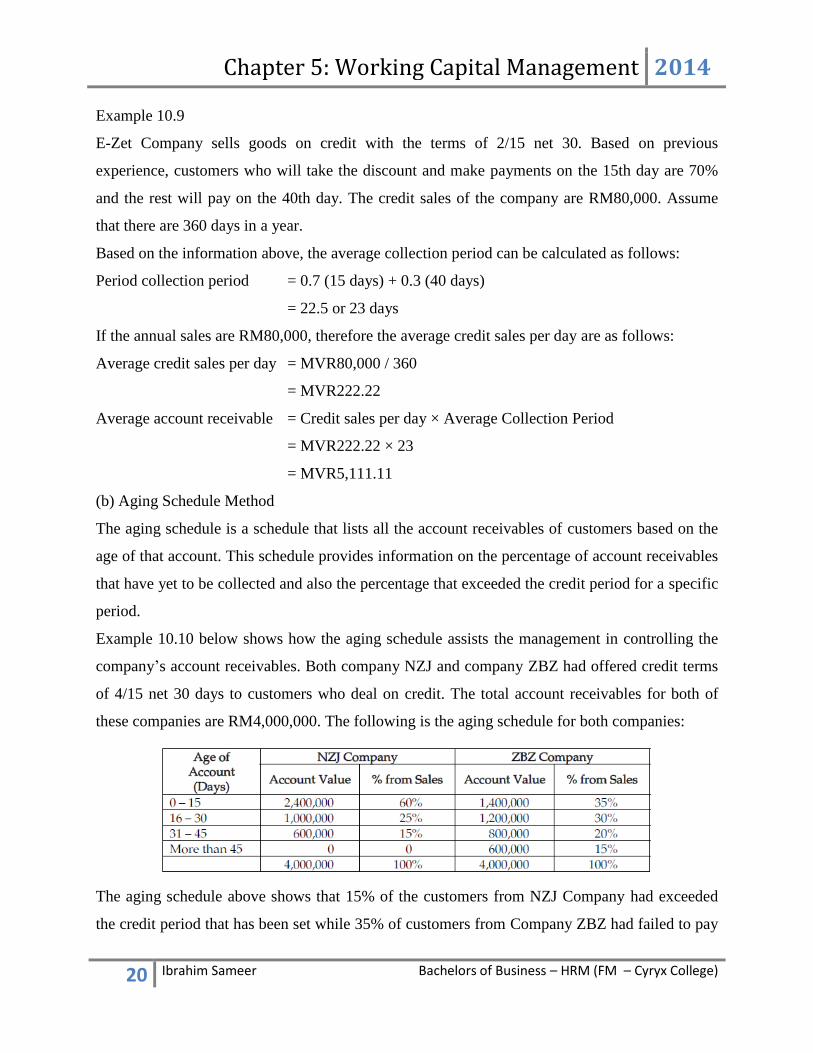

Example 10.9

E-Zet Company sells goods on credit with the terms of 2/15 net 30. Based on previous

experience, customers who will take the discount and make payments on the 15th day are 70%

and the rest will pay on the 40th day. The credit sales of the company are RM80,000. Assume

that there are 360 days in a year.

Based on the information above, the average collection period can be calculated as follows:

Period collection period = 0.7 (15 days) + 0.3 (40 days)

= 22.5 or 23 days

If the annual sales are RM80,000, therefore the average credit sales per day are as follows:

Average credit sales per day = MVR80,000 / 360

= MVR222.22

Average account receivable = Credit sales per day × Average Collection Period

= MVR222.22 × 23

= MVR5,111.11

(b) Aging Schedule Method

The aging schedule is a schedule that lists all the account receivables of customers based on the

age of that account. This schedule provides information on the percentage of account receivables

that have yet to be collected and also the percentage that exceeded the credit period for a specific

period.

Example 10.10 below shows how the aging schedule assists the management in controlling the

company’s account receivables. Both company NZJ and company ZBZ had offered credit terms

of 4/15 net 30 days to customers who deal on credit. The total account receivables for both of

these companies are RM4,000,000. The following is the aging schedule for both companies:

The aging schedule above shows that 15% of the customers from NZJ Company had exceeded

the credit period that has been set while 35% of customers from Company ZBZ had failed to pay

Chapter 5: Working Capital Management 2014

21 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

within the period set. Both these companies need to look at the credit policy that was set to

identify the problems faced in credit management of the company.

Balance between Risk-return in Management of Account Receivable

As in management of cash and marketable securities, management of account receivables is also

important as it has an effect on risk and the rate of return for the company. The balance between

risk and the rate of return is a decision that must be made by the management in managing the

account receivable of the company.

The management of account receivable starts from the decision on whether the company should

sell by credit or not. In relation to this, the company will set specific policies in managing the

account receivable which is normally known as company’s credit.

A loose credit policy normally will increase sales and this will bring a higher rate of return. But

at the same time, this policy will also increase the risk of bad debts for the company. The

increase in this risk will have a negative effect on the rate of return for the company.

On the other hand, a strict credit policy will reduce the sales of the company. However, this

policy will reduce the risk of bad debts and will indirectly have a positive effect on the rate of

return for the company. Therefore, in choosing a specific credit policy, the management of the

company must take into account the effect of the credit policy on the overall risk level and the

rate of return of the company.

………………… END………………...

Chapter 5: Working Capital Management 2014

22 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Practice Questions

Question 1

The following are the total loan by Zeeniya Company throughout the year.

Month Total (MVR)

January 12,000

February 13,000

March 9,000

April 8,000

May 9,000

June 7,000

July 6,000

August 5,000

September 6,000

October 5,000

November 7,000

December 9,000

a) Calculate the average total loans of Zeeniya Company.

b) Calculate the annual loan costs of the company at the interest rate of 15%.

Question 2

Yuin Company has obtained a loan from the bank for MVR10,000 for a period of 90 days at the

interest rate of 15% payable on the maturity date of the loan. Assume that there are 360 days in a

year.

(a) How much is the total interest (in rufiya) that must be paid by Yuin Company for this loan?

(b) Calculate the effective cost for this loan.

Question 3

Commercial papers are usually sold at a discounted rate. Mausooma Company has just sold its

commercial papers that had been issued for a period of 90 days at the face value of MVR1

million. The company receive as much as MVR978,000.

Chapter 5: Working Capital Management 2014

23 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

(a) What is the effective annual interest rate that must be paid to finance the commercial

papers?

(b) If the broker’s fee is MVR9,612 and had been paid at the beginning of the issuance of

these commercial papers, how much is the annual effective rate that must be paid by the

company?

Question 4

Didi Company intends to get an advance from the factoring account for MVR100,000 and will

mature in a period of 30 days. The factor holds 10% of the total account that will be factorised

(reserves). There is also a 2% fee on factoring and a prepayment interest rate of 15% per year.

(a) Calculate the maximum amount (in MVR) of the interest that must be paid.

(b) What is actual amount that will be obtained by the company?

(c) What is the annual cost factor (in percentage) for this transaction?

Question 5

Tholsooma Company’s ventures in a teakwood furniture business. Its supplier, Mr. Bolsooma

had been given a 20 days period to settle his payments for the inventory ordered.

Sales MVR450,000

Average inventory MVR50,000

Account receivables MVR15,000

Based on the information above, calculate the:

(a) Inventory conversion period

(b) Account receivable conversion period

(c) Deferred payments period

(d) Cash conversion cycle period

Assume that there are 360 days in a year.

Question 6

Shaheem Company offers the term of 3/10 net 30 to all the customers who purchase its goods.

Assume that 60% of its customers take the discount while the rest pays on the 30th day. The

Chapter 5: Working Capital Management 2014

24 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

annual sales of Shaheem Company is MVR500,000. Calculate the average account receivables of

Shaheem Company with the assumption that there are 360 days in a year.

Question 7

Aayaan Grocery Store ordered goods totalling MVR3,000 every 3 months. The credit term sets

by the supplier is 2/10 net 30. If it takes the discount offered by the supplier, calculate the

savings that can be obtained in a year. Assume that there are 360 days in a year.

Question 8

Mrs. Maheera buys supplies for her bakery for RM3,500 from Hashfa Supplier Company with

the credit term of 2/15 net 30 on 15 June 2001. What is the payment amount made by Mrs

Maheera if she makes payment on 27 June 2001?

Question 9

Question 10

Chapter 5: Working Capital Management 2014

25 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Question 11

Chapter 5: Working Capital Management 2014

26 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Question 12

Question 13

Chapter 5: Working Capital Management 2014

27 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Question 14

Question 15

Chapter 5: Working Capital Management 2014

28 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Question 16

Question 17

Question 18

Chapter 5: Working Capital Management 2014

29 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Question 19

Question 20

Chapter 5: Working Capital Management 2014

30 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Question 21

Question 21

Question 23

You are required to prepare a statement showing the working capital required to finance the level

of activity of 18,000 units per year from the following information:-

Particulars MVR.

Raw material Per Unit 12

Direct labor Per Unit 3

Overheads per Unit 9

Total cost Per Unit 24

Profit per Unit 6

Selling price Per Unit 30

Additional Information:

1. Raw material is in stock on an average for 2 months.

2. Materials are in process on an average for half-a- month.

Chapter 5: Working Capital Management 2014

31 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

3. Finished goods are in stock on an average for two months.

4. Credit allowed by creditors is two months in respect of raw materials supplied.

5. Credit allowed to debtors is three months.

6. Lag in payment of wages is half month. Cash on hand and at bank is expected to be MVR

7,000.

7. You are informed that all activities are evenly spread out during the year.

Question 24

Didi Ltd. had annual sales of 50,000 units at MVR100per unit. The company works for 50 weeks

in the year. Cost details of the Company are as given below:

Particulars MVR

Raw material Per Unit 30

Labour Per Unit 10

Overheads per Unit 20

Total cost Per Unit 60

Profit per Unit 40

Selling price Per Unit 100

Additional Information:

1. The Company has the practice of storing raw materials for 4weeks requirements.

2. The wages and other expenses are paid after a lag of 2 weeks.

3. Further the debtors enjoy a credit of 10 weeks and Company gets a credit of 4 weeks from

suppliers.

4. The processing time is 2 weeks and finished goods inventory is maintained for 4 weeks.

From the above information prepare a working capital estimate, allowing for a 15%

Contingency.

Chapter 5: Working Capital Management 2014

32 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Question 25

Question 26

Chapter 5: Working Capital Management 2014

33 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

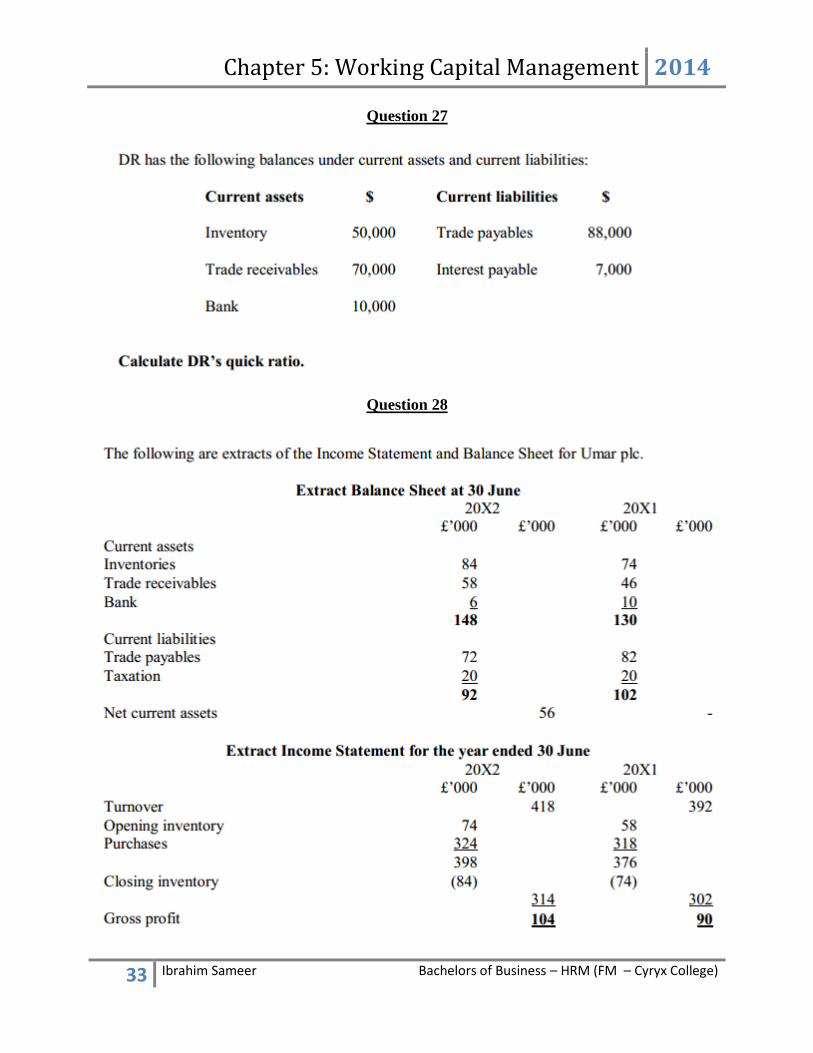

Question 27

Question 28

Chapter 5: Working Capital Management 2014

34 Ibrahim Sameer Bachelors of Business – HRM (FM – Cyryx College)

Recommended