Competitive PressureSystems Mapping andManaging MultimarketContact

FALL 2002 VOL.44 NO.1

REPRINT NUMBER 4414

By Richard A. D’Aveni

MITSloanManagement Review

Please note that gray areas reflect artwork that hasbeen intentionally removed. The substantive contentof the article appears as originally published.

FALL 2002 MIT SLOAN MANAGEMENT REVIEW 39

ecent research on multimarket contact — the partial overlap

of two firms’ geographic or product markets — has stimulated

new thinking about how and why firms put pressure on each

other.1 Not surprisingly, overlaps put pressure on competitors

and escalate the rivalry between firms in chess-like matches for

control.2 But under certain conditions, overlapping markets can

also create reciprocal threats that cause firms to reduce their rival-

rous behavior.3 By exchanging footholds (moderate market share

positions) in one another’s important markets, two firms can cre-

ate “mutual forbearance” — a lesser propensity to attack each

other with aggressive price, advertising or innovation wars for fear

of damaging counterattacks in other important markets — and a

greater inclination to seek growth in nonoverlapping markets.4

Most firms don’t do a good job of managing, through com-

petitor and market selection, the pressure they experience. All

organizations sense pressure intuitively, but it is often difficult to

see the overall pressure system — a complex, shifting pattern of

overlapping contacts among rivals that continually alters the cli-

mate of an industry by changing the incentives for players to

compete, mutually forbear or even formally cooperate.

Fortunately, these systems can be mapped and, unlike weather

pressure systems, controlled to a significant extent if they are

understood well enough.

Typically, the competitive pressure within an industry is

thought of as a continuum, running from hypercompetition to col-

lusion. An industry’s competitiveness is traditionally measured by

Richard A. D’Aveni is professor of strategic management at Dartmouth’s Tuck School of Business. Contact him at [email protected].

R

Competitive Pressure SystemsMapping and Managing Multimarket Contact

Managers typically think

that the competitive pressure

their companies experience

is solely the result of the

behavior of their rivals. But,

by mapping the system of

pressures in which they

operate, they can make

the optimal choice of

competitors, allies and

markets to gain superior

strategic influence over the

evolution of their industry

and their organization’s

role in it.

By Richard A. D’Aveni

antitrust experts using an industry’s concentration ratio or

Herfindahl index, both based on the distribution of the market

shares of firms within the industry. But recent multimarket

research indicates that competitive pressure is more complicated

than that. Overlaps between different pairs of competitors vary

widely, reducing or escalating rivalry differently. And pressure is

“asymmetrical”— that is, the pressure firm A places on firm B does

not necessarily equal the pressure that firm B puts on firm A,

because their overlapping markets may differ in importance to

each one’s portfolio.5 Each firm in a system is uniquely affected.

Some are targets, whereas others are aggressors or orchestrators of

the overall pattern of pressure. Still others are isolated from the

brunt of pressure. With all the possible combinations of overlaps

that can exist between numerous rivals, no two pressure systems

are exactly alike, even if the traditional measures of industry com-

petitiveness are identical. (See “About the Research.”)

As difficult as it is, it is vitally important for an organization

to understand its industry’s pressure system. Otherwise it can

find itself the industry’s lightning rod, attracting attacks from

all quarters. It obviously can’t avoid competitive pressure by

cooperating with every competitor in all markets: That’s illegal.

Nor can it put pressure on every competitor everywhere: That’s

suicide. Managers must understand how to use competitive

pressure to create an optimum combination of competition and

cooperation among selected rivals.

Unfortunately, managers almost always lack objective mea-

surements and useful pictures of the pressure patterns they face.

Typically, strategists see competitive pressure as being based on

five forces: buyer power, supplier power, barriers to entry,

threats posed by substitute products and intraindustry rivalry.6

Measurement of intraindustry rivalry has been proxied by fac-

tors affecting the degree of price competition in a market, such

as the number and concentration of competitors, the rate of

growth in demand, the industry’s capital intensity and fixed

costs, the lack of differentiation, switching costs, the diversity of

strategic groups within the industry and the magnitude of exit

barriers.7 However, none of these factors explicitly accounts for

the complexities presented by recent multimarket contact

research nor for the variety of pressure patterns that comprise

and influence intraindustry rivalry.

A map based on measured pressures is essential to answering

questions vital to the dynamic stability of an industry and the

profitability of firms in it. It has important implications for an

organization’s market and competitor selection, growth plans,

product portfolio and diversification strategy, resource alloca-

tion priorities, competitive intelligence system, merger and

acquisition strategy, and scenario planning process.

An overall picture of an industry’s pressure system can allow

managers to proactively and intelligently decide whether to

counter the pressure of a rival or let another competitor do it.

Organizations can apply pressure to mold the strategies of others

and even to create “win-win” situations in which both rivals

advance or protect their positions. They can tailor their selection

of markets or competitors in ways that legally redirect pressure,

create mutual forbearance or encourage indirect competition.

They can avoid entering “attractive” growth markets that will

bring on intense retaliatory pressure from unexpected quarters.

When used moderately, these tactics can prevent an industry from

becoming a pressure cooker. Or they can heat things up when

opportunities for capturing or holding industry leadership arise.

For any organization, measuring and mapping the invisible

pattern of competitive pressure among its rivals is the first step

in creating order out of the confusion that is destroying the

profitability of many highly competitive industries.8 Because of

frequent internal destabilizing actions and occasional external

shocks, pressure systems can never be frozen. The best that can

be achieved is a kind of dynamic stability. Companies must seek

superior position when possible and avoid intolerable pressure

when necessary — but it is most valuable to gain superior strate-

gic influence over the evolution of the system. This results from

superior knowledge plus the resources and intent to carry out a

coherent competitive pressure strategy.

Pressure System MappingThe more two firms’ product or geographic markets overlap,

the more pressure they exert on each other. The pressure is pro-

portional to the importance of markets to each firm and the

degree of penetration by each firm.9 This simple concept

enables organizations to quantify the degree of pressure that

one rival puts on another. (See “Pressure Measurement.”)

When measuring and mapping competitive pressure, it is

not easy to define, on an a priori basis, the boundaries of or key

players in an industry. It is best to do this empirically by begin-

ning with all competitors whose markets overlap significantly

with the focal firm (the one creating the map) and then includ-

ing firms that pressure those competitors. The primary purpose

of pressure mapping is not to illustrate the current use of com-

petitive tactics (i.e., price, advertising or innovation wars) but to

provide insight about who has the potential and the incentive to

make or avoid future use of pressure. By casting the net wide, it

is possible to find tacit allies and to identify potential acquisi-

tions or opportunities to enter new markets that could shift the

balance and direction of pressure applied to selected rivals.

Once relevant rivals are identified and competitive pressures

are quantified, they are mapped with symbols. Companies are

represented by circles, tacit or formal alliances by lines connecting

40 MIT SLOAN MANAGEMENT REVIEW FALL 2002

them, and pressure by arrows

showing its direction. Thick,

solid arrows indicate strong pres-

sure, and thin or dotted arrows

indicate milder pressure. Relative

circle size represents the relative

size of firms. The mapping is

based on hard market share and

revenue data that are often read-

ily available in marketing, com-

petitive intelligence or strategic

planning groups.

An initial pressure map is apt

to be dauntingly complex, a

formless array of sources and

targets of pressure with a

spaghetti-like tangle of lines and

arrows connecting them. It is

often useful to locate the most

focal firm or the most aggressive

or targeted rival at the center of

the map, or to place the industry

leaders at the top of the map to

minimize the number of inter-

secting arrows. Omission of low-pressure relationships and

inconsequential rivals can simplify the map to show only key

relationships that yield clear insights.

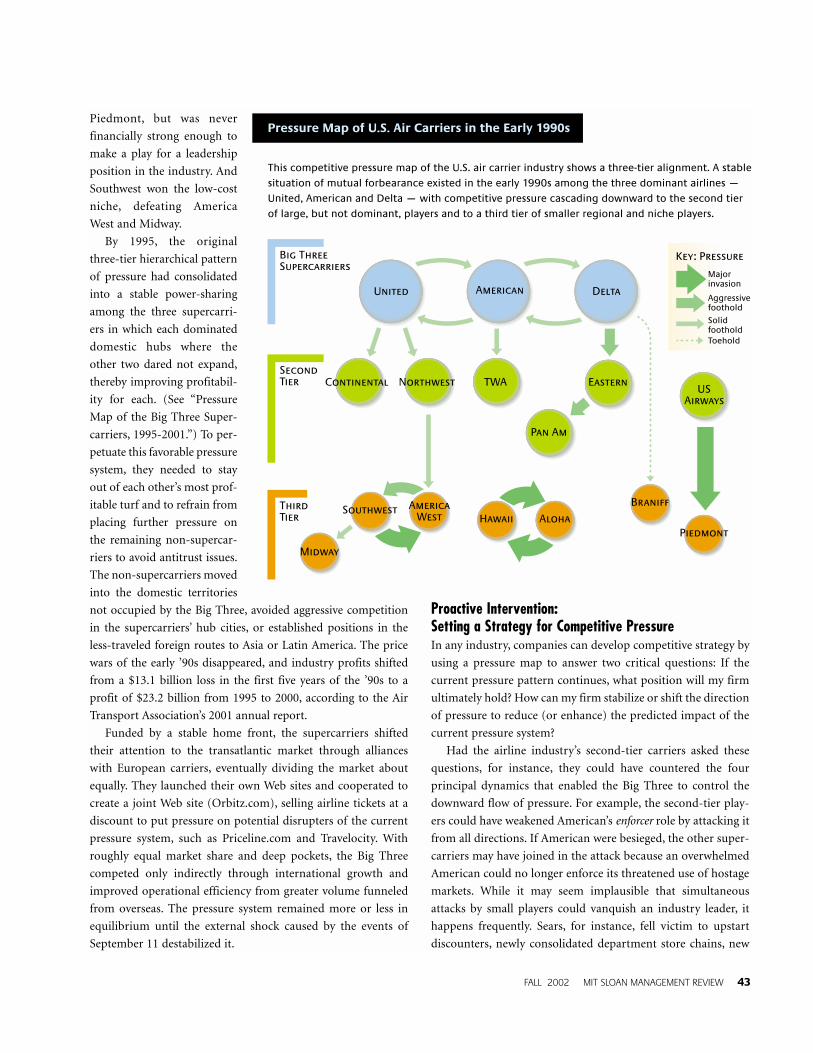

Analyzing Pressure Systems:A Look at the Early 1990s Airline IndustryConsider the airline industry as it existed in the early 1990s.

While the industry at that time appeared highly competitive to

most observers, closer investigation reveals embedded patterns

of pressure that mixed incentives to compete and cooperate.

(See “Pressure Map of U.S. Air Carriers in the Early 1990s.”)

The map reflects that the industry leaders in the early 1990s

were American, United and Delta — collectively known as the

“Big Three Supercarriers.” These three had deep pockets and

large hub-and-spoke systems with economies of scale and wider

connectivity than the other carriers. Second-tier players were

large national carriers that were not leaders for a variety of rea-

sons. Some were financially weakened by a combination of hos-

tile unions and excessive post-deregulation growth or

competition (Continental and Eastern). Others were more con-

centrated regionally despite their national reach (Northwest and

US Airways). Two low-cost niche players had arisen after dereg-

ulation: America West and Southwest. America West was built

on a hub-and-spoke system, whereas Southwest focused on

direct flights to secondary airports. Local and regional players,

like Aloha and Alaska Airlines, were engaged in a struggle for the

same geographic markets. And parts of the industry were suffer-

ing from aggressive, sporadic (some might even say almost con-

tinuous) price wars in the late 1980s and early 1990s. Fierce turf

battles were being played out as competitors entered each other’s

markets, resulting in numerous overlapping geographic markets

that had not existed at the time of deregulation in the early ’80s.

When interpreting any pressure map, it is often helpful to

start by looking at the current position and behavior of the

industry leaders. Is there one firm (or a dominant coalition of

firms) that seems to be applying a lot of pressure? Are the lead-

ers aggressively applying pressure among themselves or just

against lesser firms? Has a leader applied pressure that is so great

it constitutes a major invasion or are the leaders avoiding contact

by taking only minor positions in each other’s markets? Is the

pressure exchanged between the leaders asymmetrical or bal-

anced in intensity? Such questions naturally lead to others: Why

are they acting as they do? Are there any explicit, implicit or even

unconscious strategies unfolding? Who is central to the evolu-

tion of the system, driving the actions and position of others?

It is also useful to look for subsystems composed of smaller

numbers of firms tightly organized in pairs or triangular rela-

tionships to see how their interdependence influences their

FALL 2002 MIT SLOAN MANAGEMENT REVIEW 41

Two factors affect the strength of competitive pressure from a given incursion into a rival’sgeographical or product market: the of the market (as measured by the per-centage of the targeted firm’s total revenue represented by the market) and of theincursion (as measured by the market share achieved by the invading firm).

Pressure = (Importance of Market) X (Size of Incursion).

The total pressure on a firm is the sum of the pressures on all of its individual markets.

If the number of overlapping markets is impractically large, it is often useful to eliminatetrivial market overlaps using a decision rule, such as including only overlaps in markets thatare at least 1% of the focal firm’s total sales. The markets can be defined broadly, such aspersonal care products in Europe, or narrowly, such as soap in the south of France. Fine-grained data is better, but more expensive. Some precision may have to be sacrificedbecause of the cost or availability of data.

After computing the magnitude of pressure from each competitor using this formula,the magnitudes should be scaled such that the sum of the pressures from all of a givenfocal firm’s competitors will equal 1. Doing this provides a better predictor of each player’sbehavior, because it depicts pressures relative to each other as they appear to each focalfirm. The heaviest pressure ordinarily gets the quickest or the strongest response. Of course,it is sometimes useful to use unscaled pressure measures to determine which company inan industry is subject to the most absolute pressure and which is causing the most. Thistells you which company may be eliminated as a trivial player and which is taking thestrongest offensive posture.

Pressure Measurement

behavior. Triangles may involve formal alliances or multimarket

contacts that create mutual forbearance between all or just two

of the members. The subset of firms may act as a united bloc,

have a central player that influences the other two, or two mem-

bers that share the third as a common rival.

Consider the incomplete triangle of Delta, Eastern and

American. Although they are fighting over some of the same turf,

Delta is pressuring Eastern, but not vice versa. Delta has taken large

market share in markets important to Eastern, but Eastern has

taken only minor positions in Delta’s important markets, giving

Delta the advantage. This is a clear case of asymmetrical pressure.

Delta lacks incentive to forbear with respect to Eastern’s markets

unless Eastern were to take some moderate footholds in Delta’s

most important markets (an opportunity that Eastern missed). In

contrast, Delta and American each have moderate positions of

about equal strength in the other’s markets. These “hostage mar-

kets” are not big enough to create a struggle over identical turf, as

between Southwest and America West, but just enough to restrain

Delta and American from attacking each other aggressively.

This type of mutual opposing and equally balanced pressure

does not completely eliminate competition between two rivals,

but has the potential to redirect it in two important ways. First,

Delta is free to take on Eastern even more aggressively, without

fear of a two-fronted battle against Eastern and American in

different regions. Second, rigorous research in numerous highly

competitive industries has shown that firms pressuring each

other in this way often improve their profitability, avoid further

expansion in the overlapping rival’s markets, limit aggressive

actions to the rival’s least important markets, and focus on

growth elsewhere. Rivals may even give up share in their weak

markets in exchange for greater share in their strong markets so

they both gain economies of scale.10

Looking at the third leg of the triangle, the mutual forbear-

ance between American and Delta also influences the American-

Eastern relationship. American is deterred from forging a merger

or formal alliance with Eastern that would resuscitate Eastern

with a cash infusion. In fact, after Eastern ceased operations in

1991, Delta benefited by picking up many of Eastern’s markets,

giving it control of some “safe haven” airports. These included

hubs and mini-hubs that were largely untouched by American,

which could have invaded them were it not for the pressure-based

incentives to avoid conflict with Delta.

Examining the pressure map of the early ’90s airline industry,

one can see that several subsystems shaped how the industry

consolidated and which carriers survived. There were four prin-

cipal dynamic forces at work: Two-directional pressure between

American and Delta and between American and United created

a triumvirate of mutual forbearance that freed each company to

put pressure on the second-tier players without the threat of

intervention by another supercarrier. This allowed a division of

labor among the Big Three, with American, Delta and United

each targeting and weakening a different second-tier player. This

further allowed each to focus its resources on one or two tar-

geted carriers at most and enabled a downward pressure cascade,

which tends to cause market consolidation. American was in a

central position in the pressure system and played the role of

enforcer. Whenever Delta and United acted against each other

(because they lacked incentives for mutual forbearance),

American was caught in the crossfire, forced to defend its inter-

ests and perhaps even to use disciplinary actions. These included

the use or the threat of temporary but punishing market entries

and price-based retaliation to keep the rest of the Big Three

focused on the second tier rather than on one another.

Between 1990 and 1995, as a result of these dynamic forces,

Eastern, Pan Am and Braniff all but disappeared. TWA,

Continental and Northwest were financially weakened to the

point that they could never make a play to join the Big Three, even

if they had merged. US Airways acquired its main competitor,

About the Research

42 MIT SLOAN MANAGEMENT REVIEW FALL 2002

The conclusions of this study are derived from an ongoing,multiyear project to map competitive pressure systems inseveral industries, including U.S. airlines, European Internetservice providers (ISPs), European mobile telephony, U.S.automakers, the mutual fund industry, and the globalentertainment and media industries. Earlier data on U.S.airlines were from a published study by Ming-Jer Chen, the E. Thayer Bigelow Research Professor of BusinessAdministration at the Darden School of the University ofVirginia.* The 1995 airline data were collected from thesame public data sources used by Chen as well as marketshare data by airport from securities analyst reports.European mobile telephony and ISP data were collected,analyzed and published with the assistance and permissionof the Nolan Norton Institute of KPMG ManagementConsulting-Netherlands and Prof. Hans Strikwerda of theUniversity of Amsterdam. Research on other industries continues at Dartmouth College’s Tuck School of Businessunder the direction of the author, with the goal of gainingfurther understanding about how pressure systems differfrom industry to industry, how they evolve over time, andhow they influence and incorporate mixtures of competi-tive and cooperative behaviors among rivals.

* M. Chen, “Competitor Analysis and Interfirm Rivalry: Toward a Theoretical Integration,” Academy of Management Review 21, no. 10(1996): 100-134.

Piedmont, but was never

financially strong enough to

make a play for a leadership

position in the industry. And

Southwest won the low-cost

niche, defeating America

West and Midway.

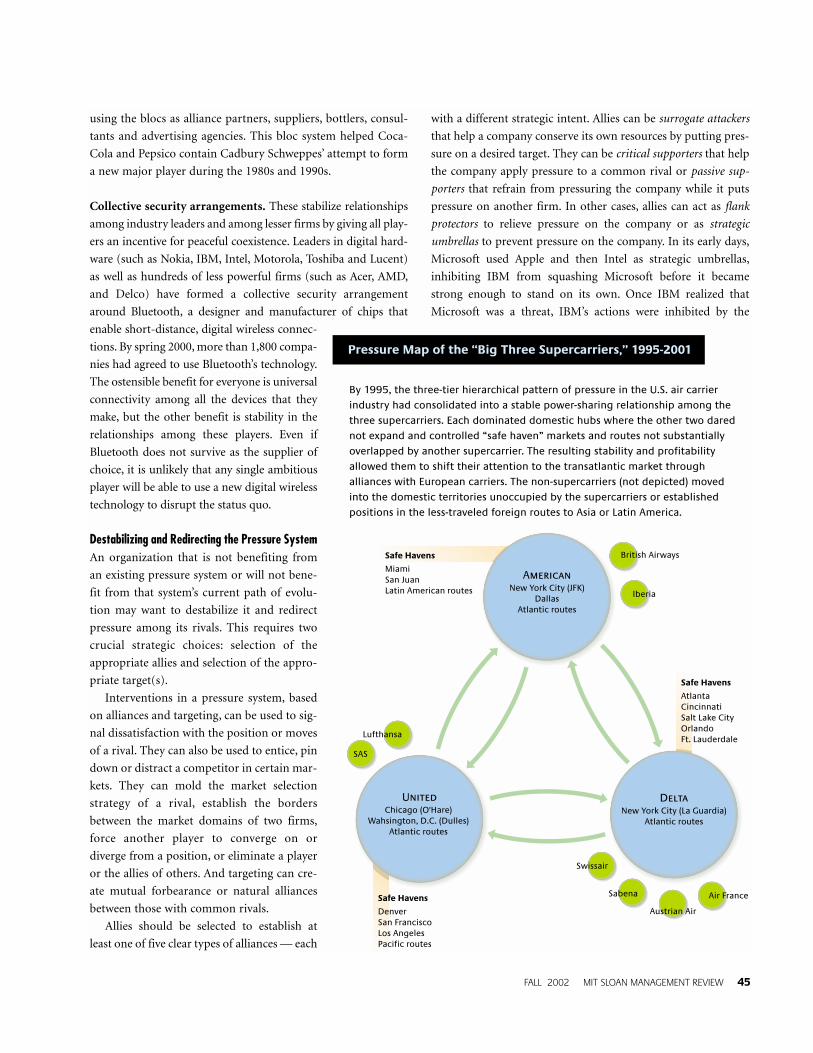

By 1995, the original

three-tier hierarchical pattern

of pressure had consolidated

into a stable power-sharing

among the three supercarri-

ers in which each dominated

domestic hubs where the

other two dared not expand,

thereby improving profitabil-

ity for each. (See “Pressure

Map of the Big Three Super-

carriers, 1995-2001.”) To per-

petuate this favorable pressure

system, they needed to stay

out of each other’s most prof-

itable turf and to refrain from

placing further pressure on

the remaining non-supercar-

riers to avoid antitrust issues.

The non-supercarriers moved

into the domestic territories

not occupied by the Big Three, avoided aggressive competition

in the supercarriers’ hub cities, or established positions in the

less-traveled foreign routes to Asia or Latin America. The price

wars of the early ’90s disappeared, and industry profits shifted

from a $13.1 billion loss in the first five years of the ’90s to a

profit of $23.2 billion from 1995 to 2000, according to the Air

Transport Association’s 2001 annual report.

Funded by a stable home front, the supercarriers shifted

their attention to the transatlantic market through alliances

with European carriers, eventually dividing the market about

equally. They launched their own Web sites and cooperated to

create a joint Web site (Orbitz.com), selling airline tickets at a

discount to put pressure on potential disrupters of the current

pressure system, such as Priceline.com and Travelocity. With

roughly equal market share and deep pockets, the Big Three

competed only indirectly through international growth and

improved operational efficiency from greater volume funneled

from overseas. The pressure system remained more or less in

equilibrium until the external shock caused by the events of

September 11 destabilized it.

Proactive Intervention: Setting a Strategy for Competitive PressureIn any industry, companies can develop competitive strategy by

using a pressure map to answer two critical questions: If the

current pressure pattern continues, what position will my firm

ultimately hold? How can my firm stabilize or shift the direction

of pressure to reduce (or enhance) the predicted impact of the

current pressure system?

Had the airline industry’s second-tier carriers asked these

questions, for instance, they could have countered the four

principal dynamics that enabled the Big Three to control the

downward flow of pressure. For example, the second-tier play-

ers could have weakened American’s enforcer role by attacking it

from all directions. If American were besieged, the other super-

carriers may have joined in the attack because an overwhelmed

American could no longer enforce its threatened use of hostage

markets. While it may seem implausible that simultaneous

attacks by small players could vanquish an industry leader, it

happens frequently. Sears, for instance, fell victim to upstart

discounters, newly consolidated department store chains, new

FALL 2002 MIT SLOAN MANAGEMENT REVIEW 43

Big ThreeSupercarriers

United American Delta

SecondTier Continental Northwest TWA Eastern

Pan Am

USAirways

ThirdTier

AmericaWest

Southwest

Midway

BraniffHawaii Aloha

Piedmont

Key: Pressure

Majorinvasion

AggressivefootholdSolidfootholdToehold

Pressure Map of U.S. Air Carriers in the Early 1990s

This competitive pressure map of the U.S. air carrier industry shows a three-tier alignment. A stablesituation of mutual forbearance existed in the early 1990s among the three dominant airlines —United, American and Delta — with competitive pressure cascading downward to the second tierof large, but not dominant, players and to a third tier of smaller regional and niche players.

specialty catalogues, growing hardware franchisers, new cate-

gory killers in consumer electronics and home appliances, and

Home Depot.

Alternatively, some of the second-tier carriers could have

consolidated and attacked the markets exchanged as hostages

among two of the Big Three. By combining as one major player,

they could also have worked to establish their own mutual for-

bearance with some of the supercarriers. While there would

have been many obstacles to such a merger, it would have

unraveled the triumvirate by forcing some of them to fight with

each other and that would have alleviated the downward cas-

cade of pressure. As a third possibility, Eastern, which was once

one of the largest airlines in the world, might have moved to

undermine the triangle formed by American and Delta by real-

locating its routes to create mutual forbearance with at least one

of those players.

Whether a company is the beneficiary or the victim of the

pressure system in its industry, it can intervene to alter that sys-

tem and gain strategic advantage through competitor and market

selection, mergers and acquisitions or formal alliances, and other

powerful strategic tools described below. Depending on the situ-

ation, the goal may be either to stabilize the current system or to

destabilize it and redirect the existing pressure patterns.

Stabilizing the Pressure System In 19th-century Europe, royal fam-

ilies cooperated in what was known as a “concert of powers” to

control disruptive nations while continuing to compete among

themselves for colonies, economic power and influence. In busi-

ness, most industries have only a few leaders and they frequently

exhibit a similar dynamic, as evidenced by the preceding airline

industry example.

Similar to the “great power nations” of world history, indus-

try leaders generally prefer stable systems and employ five time-

tested mechanisms to achieve that stability: checks and balances;

tit for tat; shared power systems; polarized blocs; and collective secu-

rity arrangements.11 Over time, the use of these mechanisms sig-

nals each leader’s tolerances and limitations to the others. These

mechanisms are used in sequence or in combination, depend-

ing upon the financial and strategic capability and will of an

industry’s leaders to carry them out.

Checks and balances. Industry leaders simultaneously use

competitive pressure to hold ambitious competitors in check

either by containing, constricting or undermining their growth

and economic power. This was the case when the major airlines

took on Peoples Express during the 1980s. Similarly, to support

its Java programming language, Sun Microsystems organized an

informal “everybody-but-Microsoft” alliance of software and

hardware makers in the ’90s to check the power of Microsoft’s

ActiveX language.

Tit for tat. Individual leaders sequentially discipline potential

rivals when they threaten the current pressure pattern, as

American Airlines did when it acted as enforcer during the early

’90s, using selective fare wars to keep the other supercarriers off

its turf. This pattern began at Texas airports during the ’80s when

American played tit for tat against Braniff and Texas Air, two

Texas-based airlines whose strong growth strategies threatened to

preempt American’s home base in the Dallas/Fort Worth hub.

Sharing power. Leaders achieve a consensus that no major com-

petitor will attempt to disrupt the pressure system, as the Big

Three Supercarriers did in the late 1990s. Each is free to pursue

growth in new areas and to poach on nondominant players that

are not cooperating with the coalition. However, if one of the

leaders gains too much power, it will be ostracized and lose its

influence. For example, Sony and Philips Electronics have evolved

a power-sharing arrangement that has both tacit and explicit

aspects. Sony has traditionally focused on the United States and

Asia, while Philips has dominance in Europe and Latin America.

The two share power over traditional Asian “fast followers” and

component suppliers. Recently, the two companies entered into

an agreement to develop a joint operating system for digital

consumer-electronic systems that will network home computers,

television, video games, personal digital assistants, home appli-

ances and audio equipment. The intent seems to be to block

Microsoft’s Windows CE from reaching prominence within the

consumer electronics world. It remains to be seen if Philips’

recent troubles with high manufacturing costs and downsizing

will make Philips a junior partner in the power-sharing arrange-

ment. It also remains to be seen if Matsushita will be invited to

adopt the Sony-Philips standard, forgoing historic rivalries to

fend off the computing hardware makers that are converging on

the digital appliance and home server markets.

Polarized blocs. These are modified shared-power systems.

When there are two or more leaders in an industry, they can enter

into shared power arrangements in separate blocs of opposing

alliances. Unlike shared power systems, a polarized bloc may

include industry nonleaders. Polarized blocs compete with each

other, but strongly encourage nonaligned players to join the

blocs. Nonleaders that align with a bloc benefit from preferred

relationships within the bloc, but can be ostracized if they refuse

to take sides or prove disloyal. Probably the most well-known

polarized blocs are affiliated with Coca-Cola and Pepsico. Their

blocs include other beverage makers that distribute or bottle

44 MIT SLOAN MANAGEMENT REVIEW FALL 2002

using the blocs as alliance partners, suppliers, bottlers, consul-

tants and advertising agencies. This bloc system helped Coca-

Cola and Pepsico contain Cadbury Schweppes’ attempt to form

a new major player during the 1980s and 1990s.

Collective security arrangements. These stabilize relationships

among industry leaders and among lesser firms by giving all play-

ers an incentive for peaceful coexistence. Leaders in digital hard-

ware (such as Nokia, IBM, Intel, Motorola, Toshiba and Lucent)

as well as hundreds of less powerful firms (such as Acer, AMD,

and Delco) have formed a collective security arrangement

around Bluetooth, a designer and manufacturer of chips that

enable short-distance, digital wireless connec-

tions. By spring 2000, more than 1,800 compa-

nies had agreed to use Bluetooth’s technology.

The ostensible benefit for everyone is universal

connectivity among all the devices that they

make, but the other benefit is stability in the

relationships among these players. Even if

Bluetooth does not survive as the supplier of

choice, it is unlikely that any single ambitious

player will be able to use a new digital wireless

technology to disrupt the status quo.

Destabilizing and Redirecting the Pressure SystemAn organization that is not benefiting from

an existing pressure system or will not bene-

fit from that system’s current path of evolu-

tion may want to destabilize it and redirect

pressure among its rivals. This requires two

crucial strategic choices: selection of the

appropriate allies and selection of the appro-

priate target(s).

Interventions in a pressure system, based

on alliances and targeting, can be used to sig-

nal dissatisfaction with the position or moves

of a rival. They can also be used to entice, pin

down or distract a competitor in certain mar-

kets. They can mold the market selection

strategy of a rival, establish the borders

between the market domains of two firms,

force another player to converge on or

diverge from a position, or eliminate a player

or the allies of others. And targeting can cre-

ate mutual forbearance or natural alliances

between those with common rivals.

Allies should be selected to establish at

least one of five clear types of alliances — each

with a different strategic intent. Allies can be surrogate attackers

that help a company conserve its own resources by putting pres-

sure on a desired target. They can be critical supporters that help

the company apply pressure to a common rival or passive sup-

porters that refrain from pressuring the company while it puts

pressure on another firm. In other cases, allies can act as flank

protectors to relieve pressure on the company or as strategic

umbrellas to prevent pressure on the company. In its early days,

Microsoft used Apple and then Intel as strategic umbrellas,

inhibiting IBM from squashing Microsoft before it became

strong enough to stand on its own. Once IBM realized that

Microsoft was a threat, IBM’s actions were inhibited by the

FALL 2002 MIT SLOAN MANAGEMENT REVIEW 45

Safe Havens

MiamiSan JuanLatin American routes

United

American

Delta

Safe Havens

DenverSan FranciscoLos AngelesPacific routes

Chicago (O'Hare)Wahsington, D.C. (Dulles)

Atlantic routes

New York City (JFK)Dallas

Atlantic routes

New York City (La Guardia)Atlantic routes

British Airways

Iberia

SAS

Lufthansa

Swissair

Sabena

Austrian Air

Air France

Safe Havens

AtlantaCincinnatiSalt Lake CityOrlandoFt. Lauderdale

Pressure Map of the “Big Three Supercarriers,” 1995-2001

By 1995, the three-tier hierarchical pattern of pressure in the U.S. air carrierindustry had consolidated into a stable power-sharing relationship among thethree supercarriers. Each dominated domestic hubs where the other two darednot expand and controlled “safe haven” markets and routes not substantiallyoverlapped by another supercarrier. The resulting stability and profitabilityallowed them to shift their attention to the transatlantic market throughalliances with European carriers. The non-supercarriers (not depicted) movedinto the domestic territories unoccupied by the supercarriers or establishedpositions in the less-traveled foreign routes to Asia or Latin America.

potential reactions of the umbrella firms with which Microsoft

had alliances. These five types of alliances can be established

informally by signaling through public announcements or by

applying pressure to create mutual forbearance, or they can be

created formally through joint ventures and long-term contracts.

Desired alliance partners often ignore suitors’ overtures if

they do not currently share interest in a common target or a

common vision for the pressure system’s future. So it is up to the

suitor to shape the potential ally’s interests. Public signals or for-

mal offers of alliance must be preceded by competitive pressure

to put teeth into the signal or offer. Methods for realigning the

willingness of others to ally (or accept common targets) include

the divide and conquer, balancer and assimilator strategies.

Divide and conquer. By separating central players from their

mutual forbearance or alliance relationships, each member of the

coalition can be induced to reassess its position. Coca-Cola did

this when it severed Pepsico’s 50-year Venezuelan distribution

partnership with the Cisneros family by convincing the family to

sign a more lucrative deal with Coke. Pepsico’s market share in its

only real foothold in South America fell from 42% to zero

overnight. American Airlines also used a divide-and-conquer

strategy when it forced the breakup of a US Airways-British

Airways alliance upon making its own controversial alliance with

British Airways for transatlantic travelers. Resistance from gov-

ernment agencies in the United States and Europe ultimately gut-

ted the power of the American-British Airways alliance, but

American kept the alliance, perhaps to block British Airways

from forming an alliance with one of the other Big Three.

Balancer. A balancer throws its weight back and forth between

rivals, enabling it (or the firm that encouraged it to get into the

balancing act) to influence the rivals’ positioning and movement.

For example, in defense contracting, Boeing and Lockheed

Martin compete for major contracts. Winning the contract

depends upon the support of radar and avionics suppliers (e.g.,

Northrop Grumman) and airframe designer/manufacturers

(e.g., British Aerospace) that regularly switch allegiances between

the two defense giants. Their influence is considerable because

contract awards are typically all or nothing. The jet engine man-

ufacturers (e.g., General Electric, Pratt & Whitney and Rolls-

Royce) have chosen not to play this game, often supplying

whoever wins the contract.

Assimilator. This strategy is based on acquiring the tacit or for-

mal alliance partners of your rivals, balancers and/or your rivals’

rivals. Assimilation can be accomplished through merger and

acquisition or through exclusive supply or distribution contracts.

For example, in 1998 and 1999, Microsoft paid $5 billion for a

chunk of AT&T, $600 million for a stake in Nextel, $200 million

for a piece of Qwest Communications, $1 billion for a portion of

Comcast, $400 million for a stake in Canada’s Rogers Cable,

$212.5 million for part of Road Runner cable modem service, as

well as making investments in several dozen other telecom and

cable companies. Sun Microsystems’ CEO Scott McNealy saw

this as an assimilation strategy to squeeze his company, since

Sun’s biggest business at the time was selling Sun’s Solaris Unix

operating systems to communications companies, its largest

customer segment.12

In choosing the right targets, several options exist. A com-

pany may want to take on its biggest threat, the weakest of the

major players, a rising or aggressive player, or a competitor that

doesn’t pressure it directly but represents an attractive market.

The choice usually depends on the targeting firm’s goal for the

pressure system’s future pattern, the feasibility of the action and

the opportunities that present themselves.

Consider AOL’s Internet service provider business in Europe.

Despite coming late to the market, by 2001 AOL had attained the

number three position in a fragmented market with three other

leaders: number one T-Online (based in Germany), number two

Tiscali (Italy) and number four Wanadoo (France). T-Online, a

Deutsche Telekom (DT) subsidiary, is by far the largest European

ISP and holds the leadership position in its home market because

its service is provided, by default, to DT subscribers. T-Online

has had some trouble replicating its success outside of Germany

but does have a presence in several other countries and grew 35%

in fiscal year 2001 to 10.7 million users. Growing-but-weak

Tiscali has made numerous small acquisitions in 15 countries,

but it holds only the number three or four position and has low

brand recognition in most of them. In its home market, it holds

only the fifth spot. Wanadoo has a strong position in its home

market, as well as a strong position in the United Kingdom

because of its acquisition of Freeserve, the country’s top ISP.

In this case, AOL had several options: Attack or acquire into

the leader’s (T-Online’s) home market; target markets not

important to T-Online; go after the home market of the most

vulnerable player (Tiscali); or target no one and grow diffusely

across Europe. While AOL is making inroads across Europe, it

appears to be targeting T-Online. AOL is exerting significant

effort in Germany, packaging its content to keep its users online

2.5 to 4 times longer (by different estimates) than T-Online users,

suing DT over its allegedly favorable telephone rates for T-Online

users in Germany and using massive ad campaigns to capture

German users. Because T-Online lacks any counter-pressure

through a foothold in AOL’s home ISP market (the United

States), AOL has not been constrained from its aggressive efforts.

46 MIT SLOAN MANAGEMENT REVIEW FALL 2002

FALL 2002 MIT SLOAN MANAGEMENT REVIEW 47

Most industry leaders prefer to fight small battles rather than

large, risky ones, so they target the most vulnerable player. However,

this is not always the best choice. It is often better for a company to

redirect pressure away from itself or to weaken several players

simultaneously than to eliminate the weakest player, because the lat-

ter scenario leaves major competitors capable of exerting a lot of

pressure. Not targeting the weakest player may leave more rivals on

the field, but each with reduced focus and power.

Consider General Motors’ position in the automobile indus-

try. Its home market is the United States, but it has a strong

foothold in Europe (its Opel division). Ford presents a strong

challenge in the U.S. and also has a strong position in Europe.

Toyota has the dominant position in Japan, with a strong and

expanding foothold in the U.S. DaimlerChrysler has a strong

position in Europe and a weak position in the U.S. GM could

target the weakest global player, DaimlerChrysler, which is in

financial difficulty, but it would still face two powerful competi-

tors (Ford and Toyota). Or it could target the strongest competi-

tor on each continent: Ford in the U.S., Toyota in Asia and

Daimler in Europe. This seems to be GM’s preferred strategy, as

evidenced by the fact that it has been buying up or taking minor-

ity stakes in the weaker players of Asia and Europe. This strategy

may be difficult to realize, since both Ford and Toyota are strong

in the U.S. and Toyota’s position in Japan is unassailable given

the existing trade and cultural barriers. But in the unlikely event

that GM succeeds, it would become the undisputed global

leader, facing three weakened competitors.

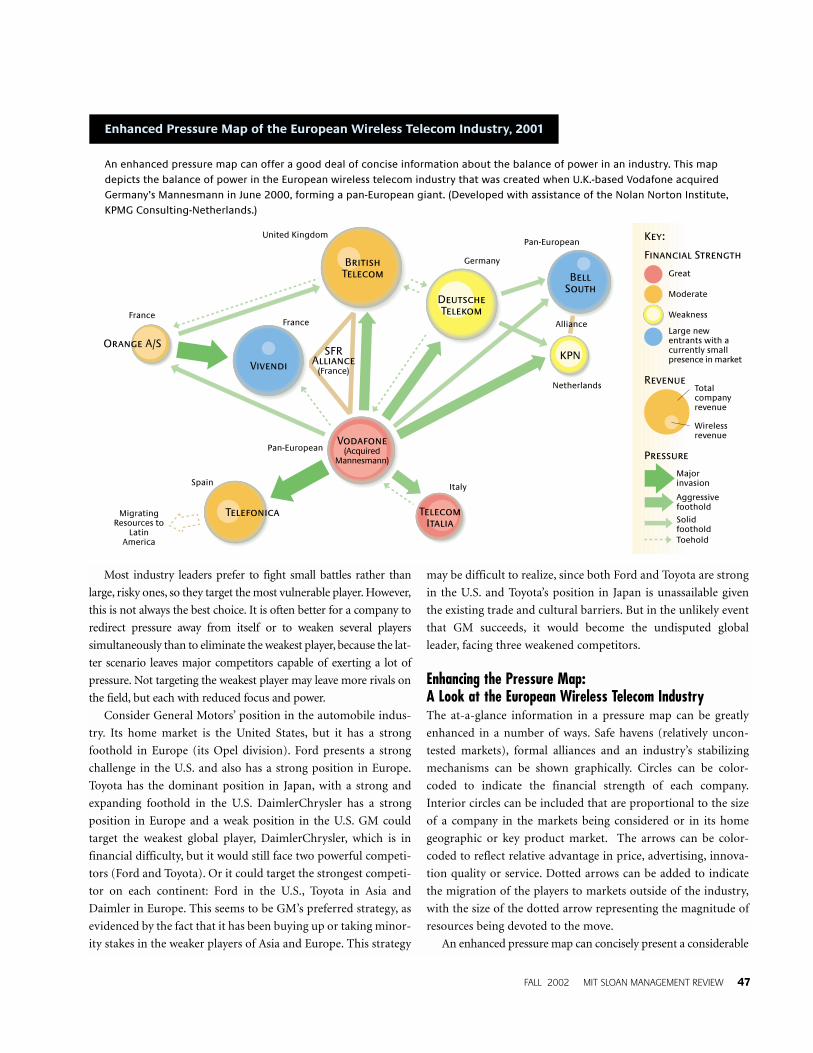

Enhancing the Pressure Map: A Look at the European Wireless Telecom IndustryThe at-a-glance information in a pressure map can be greatly

enhanced in a number of ways. Safe havens (relatively uncon-

tested markets), formal alliances and an industry’s stabilizing

mechanisms can be shown graphically. Circles can be color-

coded to indicate the financial strength of each company.

Interior circles can be included that are proportional to the size

of a company in the markets being considered or in its home

geographic or key product market. The arrows can be color-

coded to reflect relative advantage in price, advertising, innova-

tion quality or service. Dotted arrows can be added to indicate

the migration of the players to markets outside of the industry,

with the size of the dotted arrow representing the magnitude of

resources being devoted to the move.

An enhanced pressure map can concisely present a considerable

United Kingdom

BritishTelecom

Germany

DeutscheTelekom

Pan-European

BellSouth

Netherlands

KPN

France

Orange A/S

France

VivendiSFR

Alliance(France)

Vodafone(Acquired

Mannesmann)Pan-European

Spain

TelefonicaMigratingResources to

LatinAmerica

Italy

TelecomItalia

Pressure

Majorinvasion

AggressivefootholdSolidfootholdToehold

Financial Strength

Great

Moderate

Weakness

Large newentrants with acurrently smallpresence in market

Key:

Revenue

Wirelessrevenue

Totalcompanyrevenue

Alliance

Enhanced Pressure Map of the European Wireless Telecom Industry, 2001

An enhanced pressure map can offer a good deal of concise information about the balance of power in an industry. This mapdepicts the balance of power in the European wireless telecom industry that was created when U.K.-based Vodafone acquiredGermany’s Mannesmann in June 2000, forming a pan-European giant. (Developed with assistance of the Nolan Norton Institute,KPMG Consulting-Netherlands.)

48 MIT SLOAN MANAGEMENT REVIEW FALL 2002

amount of information about the balance of power in an industry.

Look, for example, at the industry landscape that was created when

U.K.-based Vodafone acquired Germany’s Mannesmann in June

2000, forming a pan-European giant with $24 billion in revenues

and 34 million customers — in an industry that had previously

been operated by nationally dominant state-owned or -regulated

firms. (See “Enhanced Pressure Map of the European Wireless

Telecom Industry, 2001.”)

In 2002, Vodafone is the undisputed industry leader with

lower subscriber acquisition costs and greater economies of scale

and connectivity than its competitors. It has strong, positive free

cash flow and holds strong positions — approximately one-third

of the home market — against each of the national wireless lead-

ers in Germany (DT), Italy (Telecom Italia) and Spain

(Telefonica). It’s partnership with Vivendi, SBC Communications

and British Telecom, called SFR, holds a third of the French mar-

ket against France Telecom’s Orange A/S.

The enhanced pressure map of the wireless industry helps

make sense of a seemingly simple situation that has triggered

complex maneuvers with sometimes-obscure rationales. On the

surface, the map indicates clearly that, in 2001, players such as

British Telecom, France Telecom’s Orange A/S and DT were on

the defensive and had to counter Vodafone if they wished to

avoid becoming second-tier players. The simple solution — an

assimilation strategy — would have been to merge their mobile

operations, attract several smaller players and form another pan-

European mobile telecom, a powerful counter-balancing rival to

Vodafone, thereby creating two polarized blocs in the European

wireless industry. But this strategy would have been politically

impossible, given the current nationalistic regulation of

European telephone companies.

Analysis of the map also suggests that the players could check

and balance Vodafone in more complex, but still effective, ways.

That seems to have been the chosen strategy, and, in 2002,

Vodafone has begun to feel the counter-pressure. In Germany,

Vodafone faces a strong defensive counterattack from DT.

Vodafone lost 400,000 subscribers in that country in the first

quarter of 2002 alone. In its home U.K. market, Vodafone is in a

tight market-share race with British Telecom’s Cellnet

(rebranded mmO2), France Telecom’s Orange A/S, and DT-

owned One2One (rebranded T-Mobile). Given its active defense

in Germany, DT is aggressively attacking and taking market

share in the United Kingdom, unfettered by fear of Vodafone

retaliating in the German market. France Telecom’s Orange A/S

is even more aggressive, attacking Vodafone in the United

Kingdom, unconstrained by fear of counterattack in its home

market where it holds 43% market share.

Vodafone appears to be trying to hold its market share posi-

tion against British Telecom and France Telecom’s Orange A/S in

the U.K. to reduce its pressure against DT in Germany and to

concede to Orange A/S in France. Meanwhile, Vodafone’s strat-

egy seems to include attacking Telecom Italia — its financially

strongest opponent but lacking the multimarket contact to

counterattack elsewhere — and Telefonica, which has demon-

strated a lack of commitment to Europe by migrating excessively

(dotted arrow) to Latin America.

The SFR alliance, originally conceived as a counterbalancing

move against France Telecom by two British firms (Vodafone

and British Telecom), is troubled by the conflicting interests of

its partners, including an intense rivalry between Vodafone and

British Telecom in their home market and Vivendi’s redeploy-

ment of resources to the entertainment industry. Vodafone was

reported to be interested in buying out Vivendi’s stake13 — perhaps

to make SFR an aggressive counterbalance against Orange A/S in

France once again — and British Telecom has indicated its will-

ingness to sell out as well.

In addition, Vodafone is reportedly considering exiting its

joint venture with Verizon in the U.S. wireless market to bring

cash home to support its European initiative. This may be nec-

essary because of the rising counterpressure from rivals, the fear

of a consolidation of several rivals if political conditions were to

permit, and the need for funds (for initiatives such as 2.5 and 3G

technology) to remain the leader.

The European wireless industry illustrates how an enhanced

pressure map can enable “what if” exercises and contingency

planning, allowing all players to anticipate with greater accuracy

the outcomes of their own or others’ potential strategies. In fact,

if Vodafone’s competitors had used pressure mapping to do

what-if analyses, it might have stimulated a more aggressive pre-

emptive assimilation or alliance strategy among them before

Vodafone acquired Mannesmann.

Putting Competitive Pressure in ContextAs the old military maxim goes, a good plan never lasts longer

than contact with the enemy. But, by using competitive pressure

maps and a systems approach to understanding the dynamic

patterns underlying multimarket contacts within an industry,

competitors can make a good plan for making contact with ene-

mies and allies alike.

Systems of mixed cooperation, competition and forbearance

exist in every industry and are not necessarily anticompetitive,

collusive oligopolies. Pressure maps are not intended to encour-

age firms to conspire in smoke-filled rooms. They merely indi-

cate and help predict the economic incentives for, and

consequences of, given actions. If taken too far, of course, mutual

forbearance can reach the point of collusion, but there is a lot of

FALL 2002 MIT SLOAN MANAGEMENT REVIEW 49

room for cooperation before it reaches that stage. In fact, if used

properly, pressure mapping can actually reduce the temptation

to collude, drive industry growth to new heights and in new

directions through increased indirect competition, and make

room for clever small players that act as balancers or members of

polarized blocs and collective security agreements. In the end,

use of pressure and mutual forbearance must be responsible and

tailored to avoid violation of antitrust and any other relevant

national laws. As with any strategy, companies should use their

ability to change the pressure situation in their industries for the

greater good of shareholders, customers and society as a whole.

Although the general logic and strategy of pressure systems will

apply to a wide variety of situations involving geographic and

product markets, there are industries in which pressure patterns

are obvious and maps may not be revealing. Still, evidence of sig-

nificant profit impact from pressure based on multimarket con-

tacts has been found for industries as diverse as banking,14

cement,15 hotels,16 knitwear manufacturing,17 mobile telephone

service18 and petroleum19 — on both the global and local levels.

Of course, competitive pressure is not the only force that

affects profitability and survival. To be effective, pressure maps

must be interpreted in the context of the macroeconomy. Major

discontinuities, such as terrorism or technological revolution,

can destroy even the most stabilized systems. And firms can

implode from labor problems, poor management and imple-

mentation errors that shift the balance of power among the play-

ers to stronger players outside the current leadership.

The changing nature of industries and the external forces that

affect them suggest that pressure systems require constant reex-

amination. And pressure mappings can show dynamic shifts in a

visual way. Indeed, if several maps done at periodic intervals are

viewed electronically in rapid sequence, like an animated film, an

industry can be seen evolving, providing a powerful and visceral

understanding of how the world is moving and how the pressure

is flowing.

REFERENCES

1. R.A. D’Aveni, “Strategic Supremacy: How Industry Leaders CreateGrowth, Wealth and Power Through Spheres of Influence” (New York:Free Press, 2001).2. R. McGrath, M. Chen and I. MacMillan, “Multimarket Maneuvering in Uncertain Spheres of Influence: Resource Diversion Strategies,”Academy of Management Review 23, no. 4 (1998): 724-740.3. I. Jans and D.I. Rosenbaum, “Multimarket Contact and Pricing:Evidence From the U.S. Cement Industry,” International Journal ofIndustrial Organization 15 (1997): 391-412; J. Porac, H. Thomas, F. Wilson and S. Kanfer, “Rivalry and the Industry Model of ScottishKnitwear Producers,” Administrative Science Quarterly 40 (1995): 203-217; J. Gimeno and C. Woo, “Hypercompetition in a Multimarket

Environment: The Role of Strategic Similarity and Multimarket Contact inCompetitive De-Escalation,” Organization Science 7 (1996): 322-341;and J. Gimeno, “Reciprocal Threats in Multimarket Rivalry,” StrategicManagement Journal 20 (1999): 101-128.4. H. Haveman and L. Nonnemaker, “Competition in Multiple GeographicMarkets: The Impact on Growth and Market Entry,” AdministrativeScience Quarterly 45 (2000): 232-267.5. M. Chen, “Competitor Analysis and Interfirm Rivalry: Toward aTheoretical Integration,” Academy of Management Review 21, no. 1(1996): 100-134.6. M.E. Porter, “Competitive Strategy: Techniques for Analyzing Industriesand Competitors” (New York: Free Press, 1980).7. Ibid., 17-20.8. J. Gimeno and C.Y. Woo, “Hypercompetition in a MultimarketEnvironment: The Role of Strategic Similarity and Multimarket Contact inCompetitive De-escalation,” Organization Science 7, no. 3 (1996): 322-341.9. M. Chen, “Competitor Analysis and Interfirm Rivalry: Toward aTheoretical Integration,” Academy of Management Review 21, no. 10(1996): 100-134.10. S. Borenstein, “The Dominant Firm Advantage in MultiproductIndustries: Evidence From the Airline Industry,” Quarterly Journal ofEconomics 20 (1991): 344-365; W.N. Evans and I. Kessides, “Living by theGolden Rule: Multimarket Contact in the U.S. Airline Industry,” QuarterlyJournal of Economics 25 (1996): 341-366; J. Baum and H. Haveman, “LoveThey Neighbor? Differential and Spatial Agglomeration in the ManhattanHotel Industry,” Administrative Science Quarterly 42 (1997): 304-338.11. H.J. Morgenthau, “Politics Among Nations” (New York: WCB/McGraw-Hill, 1985).12. D. Kirkpatrick, “Man Bites God: Scott McNealy’s Plan to Punish BillGates,” Fortune, Oct. 25, 1999, 37.13. J. Carreyrou and A. Raghavan, “Leading the News: Vodafone MayBid for Cegetel Stake — Vivendi Could Receive Offer of $4.61 Billion forShare of 44% in Telecom Firm,” Wall Street Journal, July 8, 2002, A3.14. H. Ma and D.B. Jemison, “Effects of Spheres of Influence and FirmResources and Capabilities on the Intensity of Rivalry in Multiple MarketCompetition,” unpublished working paper, Bryant College, Smithfield,Rhode Island, 1994; J.E. Martinez, “The Linked Oligopoly Concept: RecentEvidence From Banking,” Journal of Economic Issues 24 (1990): 589-595;H.A. Haveman and L. Nonnemaker, “Competition in Multiple GeographicMarkets: The Impact on Growth and Market Entry,” Administrative ScienceQuarterly 45 (2000): 232-267.15. I. Jans and D.I. Rosenbaum, “Multimarket Contact and Pricing:Evidence in the U.S. Cement Industry,” International Journal of IndustrialOrganization 15 (1997): 391-412.16. J.A.C. Baum and H.A. Haveman, “Love Thy Neighbor? Differential andSpatial Agglomeration in the Manhattan Hotel Industry,” AdministrativeScience Quarterly 42 (1997): 304-338.17. J.F. Porac, H. Thomas, F. Wilson and S. Kanfer, “Rivalry and theIndustry Model of Scottish Knitwear Producers,” Administrative ScienceQuarterly 40 (1995): 203-217.18. P.M. Parker and L.H. Roller, “Collusive Conduct in Duopolies:Multimarket Conduct and Cross Ownership in the Mobile TelephoneIndustry,” Rand Journal of Economics 28 (1997): 304-322.19. H.G. Broadman, “Intraindustry Structure, Integration Strategies, andPetroleum Firm Performance” (Ph.D. dissertation, University of Michigan,Department of Economics, 1981).

Reprint 4414Copyright Massachusetts Institute of Technology, 2002. All rights reserved.

Reprints/Back IssuesElectronic copies of SMR articles can be purchased onour website: www.mit-smr.comTo order bulk copies of SMRreprints, or to request a freecopy of our reprint index, contact: MIT Sloan Management Review Reprints E60-100 77 Massachusetts AvenueCambridge MA 02139-4307Telephone: 617-253-7170 Toll-free in US or Canada: 877-727-7170 Fax: 617-258-9739 E-mail: [email protected]

Copyright PermissionTo reproduce or transmit oneor more SMR articles by electronic or mechanicalmeans (including photocopyingor archiving in any informationstorage or retrieval system)requires written permission.To request permission to copyarticles, contact: P. Fitzpatrick, Permissions ManagerTelephone: 617-258-7485Fax: 617-258-9739E-mail: [email protected]

MITSloanManagement Review

Recommended