- 1 -

TRADE MARKS ORDINANCE (CAP. 559)

OPPOSITION TO TRADE MARK APPLICATION NO. 301410227

MARKS:

CLASSES : 35, 36

APPLICANT : CAPITAL DYNAMICS HOLDING AG

OPPONENTS : 1) CAPITAL DYNAMICS SDN. BHD.

2) CAPITAL DYNAMICS ASSET MANAGEMENT SDN. BHD.

3) CAPITAL DYNAMICS (S) PRIVATE LIMITED

4) CAPITAL DYNAMICS (AUSTRALIA) LIMITED

_____________________________________________________________________

STATEMENT OF REASONS FOR DECISION

Background

1. On 20 August 2009 (“Application Date”), Capital Dynamics Holding AG

( “Applicant”), filed an application (“subject application”) under the Trade

Marks Ordinance (Cap.559) (“Ordinance”) for registration of the following

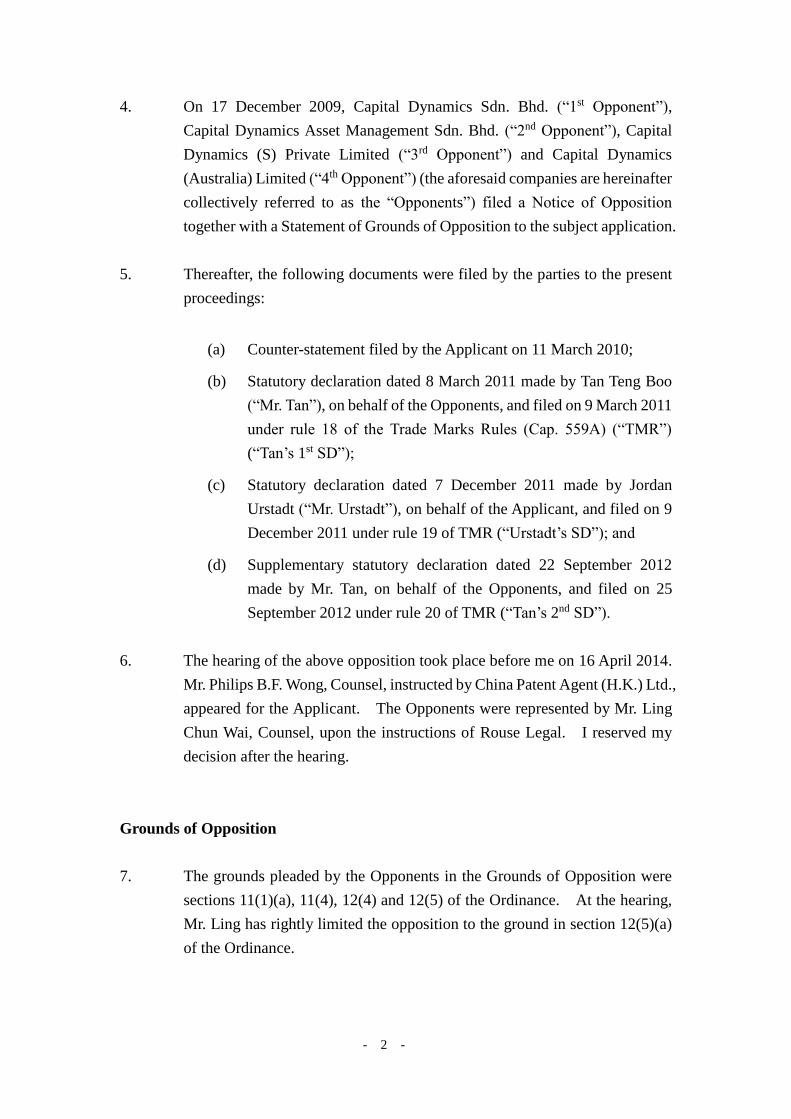

marks as a series of marks (collectively, the “subject marks”):

(Mark A) (Mark B) (Mark C)

The application number assigned by the Registrar of Trade Marks

(“Registrar”) to the subject application was 301410227.

2. Registration of the subject marks was sought in respect of services in classes

35 and 36, the details of which are set out in Schedule A of this decision

(collectively, the “subject services”).

3. Particulars of the subject application were published on 18 September 2009.

- 2 -

4. On 17 December 2009, Capital Dynamics Sdn. Bhd. (“1st Opponent”),

Capital Dynamics Asset Management Sdn. Bhd. (“2nd Opponent”), Capital

Dynamics (S) Private Limited (“3rd Opponent”) and Capital Dynamics

(Australia) Limited (“4th Opponent”) (the aforesaid companies are hereinafter

collectively referred to as the “Opponents”) filed a Notice of Opposition

together with a Statement of Grounds of Opposition to the subject application.

5. Thereafter, the following documents were filed by the parties to the present

proceedings:

(a) Counter-statement filed by the Applicant on 11 March 2010;

(b) Statutory declaration dated 8 March 2011 made by Tan Teng Boo

(“Mr. Tan”), on behalf of the Opponents, and filed on 9 March 2011

under rule 18 of the Trade Marks Rules (Cap. 559A) (“TMR”)

(“Tan’s 1st SD”);

(c) Statutory declaration dated 7 December 2011 made by Jordan

Urstadt (“Mr. Urstadt”), on behalf of the Applicant, and filed on 9

December 2011 under rule 19 of TMR (“Urstadt’s SD”); and

(d) Supplementary statutory declaration dated 22 September 2012

made by Mr. Tan, on behalf of the Opponents, and filed on 25

September 2012 under rule 20 of TMR (“Tan’s 2nd SD”).

6. The hearing of the above opposition took place before me on 16 April 2014.

Mr. Philips B.F. Wong, Counsel, instructed by China Patent Agent (H.K.) Ltd.,

appeared for the Applicant. The Opponents were represented by Mr. Ling

Chun Wai, Counsel, upon the instructions of Rouse Legal. I reserved my

decision after the hearing.

Grounds of Opposition

7. The grounds pleaded by the Opponents in the Grounds of Opposition were

sections 11(1)(a), 11(4), 12(4) and 12(5) of the Ordinance. At the hearing,

Mr. Ling has rightly limited the opposition to the ground in section 12(5)(a)

of the Ordinance.

- 3 -

The Opponents’ evidence

8. According to Tan’s 1st SD, the Opponents were part of the Capital Dynamics

group of companies (“CD Group”) founded by Mr. Tan. The 1st Opponent

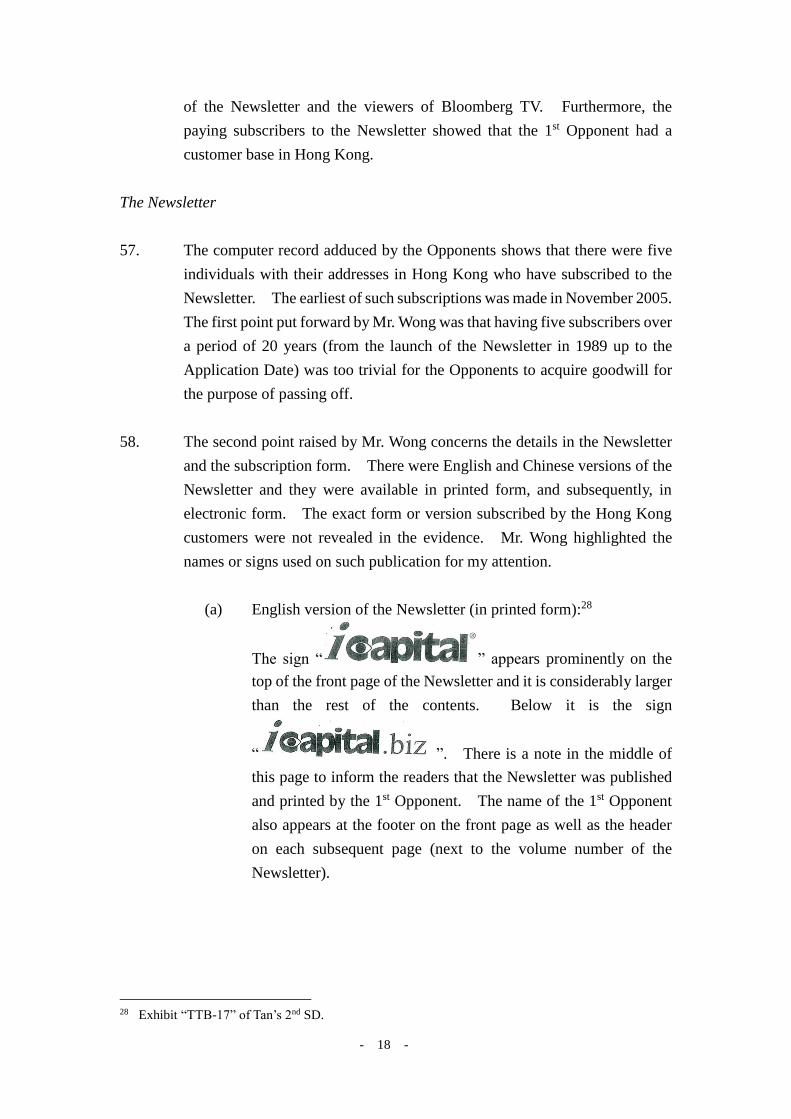

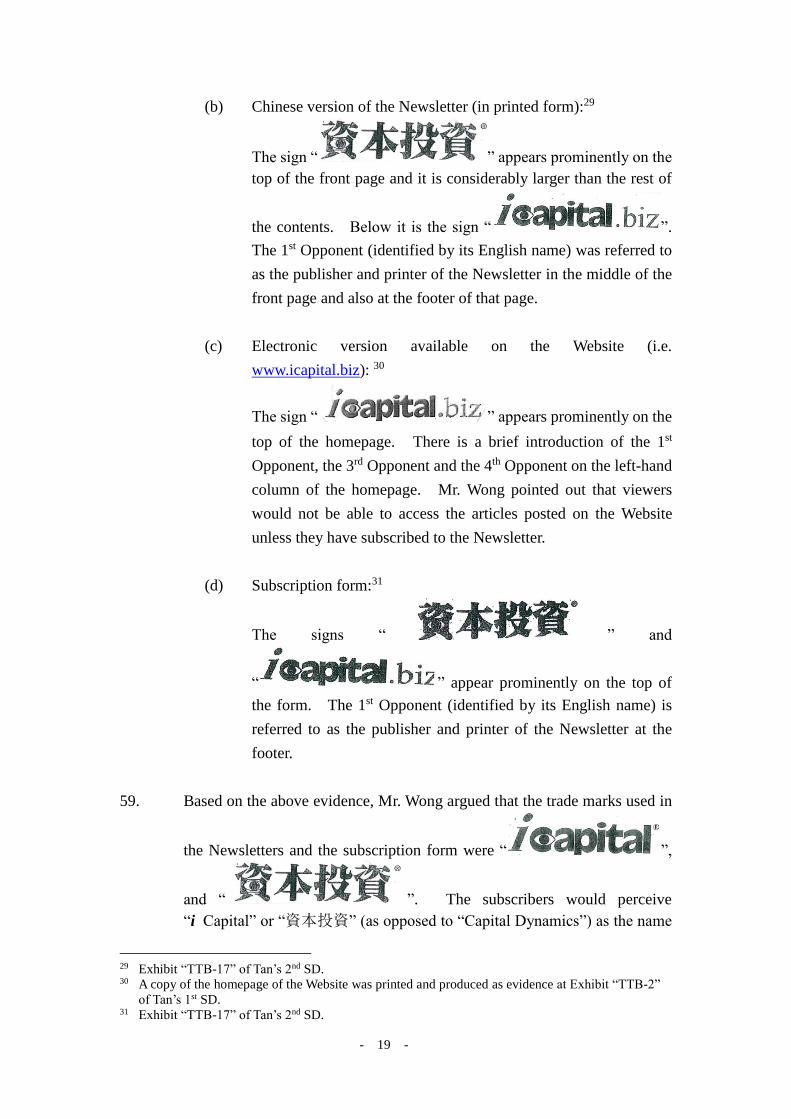

was a Malaysian company founded in 1988 as Malaysia’s first independent

investment advisor. It was the investment advisor of icapital.biz.Bhd., a

closed-end fund that has been listed on the Main Market of Bursa Malaysia

Securities Berhad (“listed fund”) since 2005. The 2nd Opponent was a

Malaysian company and the fund manager of the listed fund. The 3rd

Opponent, a company incorporated in Singapore, was the first Asian

privately-owned global fund manager. The 4th Opponent was also a fund

management company that held an Australian Financial Services Licence.

9. In 1989, the 1st Opponent launched the English and Chinese printed editions

of a weekly investment publication called “i Capital” and “資本投資”

(“Newsletter” or “Newsletters”). It was initially available in printed form.

In 2002, the Internet edition of the Newletter was launched at

www.icapital.biz (“Website”). The publication was available to investors

and readers worldwide, including Hong Kong.

10. According to computer records adduced by the Opponents, there were five

individual subscribers with addresses in Hong Kong.1 The earliest of such

subscriptions was made in November 2005.

11. According to Tan’s 2nd SD, the Internet traffic data for the Website showed

that traffic originating from Hong Kong from 2004 to 2009 ranged from

36,519 to 204,788 hits per annum.2

12. It is clear from the evidence that Mr. Tan has been active in the media. He

was the guest in a number of interviews on Bloomberg TV and in some of

those interviews, he was identified as the managing director and CEO of the

CD Group. He considered that such interviews have served to publicise the

Opponents and their businesses that were carried on under the name of

“Capital Dynamics”.

1 Exhibit “TTB-3” of Tan’s 1st SD. 2 Paragraph 20 of Tan’s 2nd SD.

- 4 -

13. Apart from the Bloomberg interviews, Mr. Tan has also given interviews with

various Malaysian broadcast channels as well as newspapers and finance

magazines.

14. The annual turnover of the Opponents in Asia from 2004 to 2009 increased

from MYR 2 million to MYR 29.9 million per annum.3 Their advertising

expenditures in Asia ranged from MYR 108,000 to MYR 464,000 per annum

during the above period.4

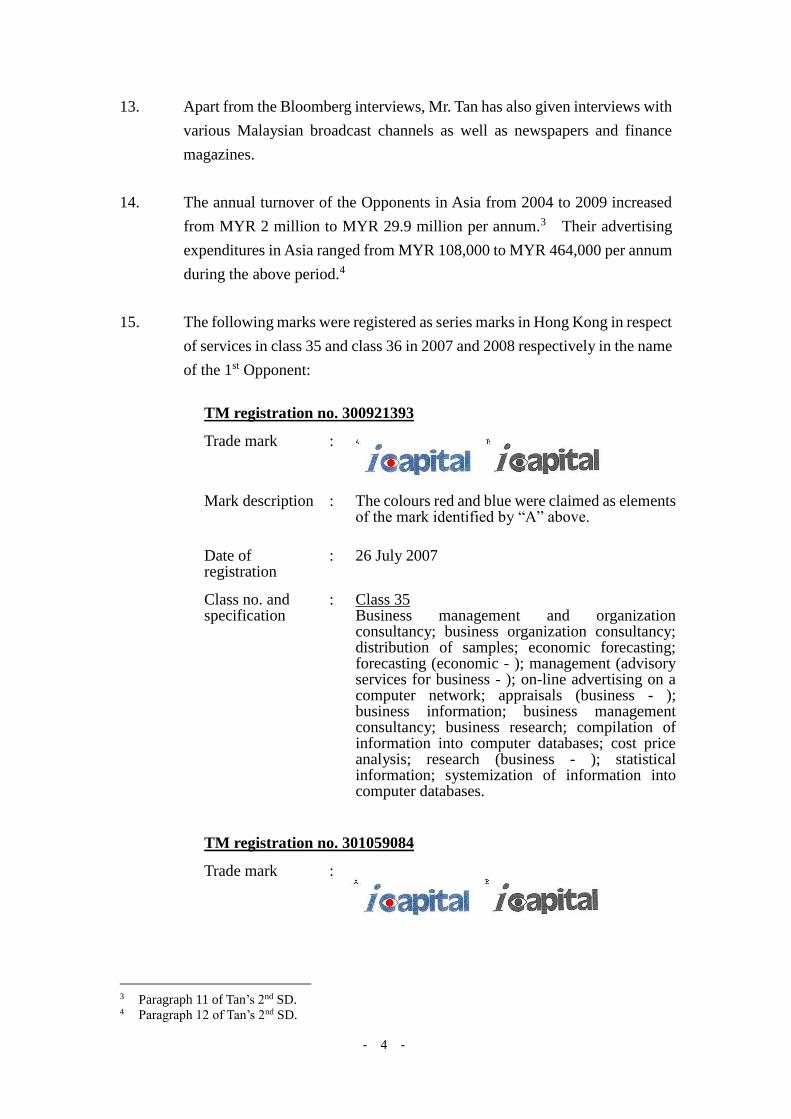

15. The following marks were registered as series marks in Hong Kong in respect

of services in class 35 and class 36 in 2007 and 2008 respectively in the name

of the 1st Opponent:

TM registration no. 300921393

Trade mark :

Mark description : The colours red and blue were claimed as elements of the mark identified by “A” above.

Date of registration

: 26 July 2007

Class no. and specification

: Class 35 Business management and organization consultancy; business organization consultancy; distribution of samples; economic forecasting; forecasting (economic - ); management (advisory services for business - ); on-line advertising on a computer network; appraisals (business - ); business information; business management consultancy; business research; compilation of information into computer databases; cost price analysis; research (business - ); statistical information; systemization of information into computer databases.

TM registration no. 301059084

Trade mark :

3 Paragraph 11 of Tan’s 2nd SD. 4 Paragraph 12 of Tan’s 2nd SD.

- 5 -

Mark description : The colours red and blue were claimed as elements of the mark identified by “A” above.

Date of registration

: 26 February 2008

Class no. and specification

: Class 36 Analysis (financial - ); administration of capital investment services; administration of fund investment; administration of investments; administrative services relating to investments; advisory services relating to investments; capital fund investment; capital investment advisory services; capital investments; computerised information services relating to investments; financial investment; financial investment fund services; financial investment research services; fund investment management; international fund investment; investment; investment analysis; investment asset management; investment business services; investment in securities (services for - ); investment information; investment of money (services for - ); investment portfolio management services; mutual funds; private client investment services; provident fund investment; provision of investment information; provision of investment services; securities investment services for personal investors; stock investment management; unit trust investment; advisory services relating to financial investment; consultancy services relating to investment; investment advice; investment management; investment of funds (services for - ); management of investment funds; research services relating to investment.

16. The 3rd Opponent has obtained trade mark registrations of “CAPITAL

DYNAMICS” and/or “Capital Dynamics” in classes 16, 35, 36 and/or 41 in

Malaysia, Singapore, Australia and Mainland China. International

registration of “CAPITAL DYNAMICS” was also obtained under the Madrid

Agreement and Protocol designating the Russian Federation and Vietnam.

The Applicant’s evidence

17. According to the Urstadt’s SD, the Applicant was a Swiss company and an

independent asset management firm that focused on private assets, including

private equity, clean energy, infrastructure and real estate. The name

“Capital Dynamics” was first adopted by Capital Dynamics AG, a wholly-

owned subsidiary of the Applicant, as its trade mark and company name in

- 6 -

December 1999. Following certain corporate restructurings in or around

2000, the Applicant became the parent company of Capital Dynamics AG

and the name “Capital Dynamics” has since been continuously used as part

of the company name and trade mark of the Applicant and its affiliated

companies (collectively, the “Applicant’s Group”).

18. The Applicant’s Group has been investing in private equity funds since 1999

and it has developed relationships with over 350 general partners in more

than 800 funds worldwide. As regards their exposure in Asia, the Applicant

currently has one Asian fund of funds and one Asian separate account for a

UK public pension fund with aggregated commitments of US$264 million.

In addition, the Applicant’s Group has exposure to 38 Asian funds through

advisory and/or non-discretionary mandates, totaling over US$1.2 billion in

assets. Of these funds, eight of them were in Hong Kong, with a total

exposure of over US$580 million.

19. Mr. Urstadt deposed that the worldwide advertising costs of the Applicant’s

Group for services promoted under the subject marks from 2004 to 2009

ranged from US$250,977 to US$444,157 per annum. The worldwide

annual turnover of the services provided under the subject marks during the

above period increased from US$3.42 million to US$39.26 million per

annum.

20. The Applicant’s Hong Kong office was opened in March 2007 and its

activities were operated by Capital Dynamics (Hong Kong) Limited. Its

revenues were generated by intercompany servicing fees relating to transfer

pricing income from the Applicant and other companies within the

Applicant’s Group.

21. With a view to protecting the marks used by the Applicant’s Group, trade

mark registrations in respect of services in classes 35 and 36 were obtained

by the Applicant in various countries. The relevant marks included Mark A

of the subject marks and “ ” and the countries included

Switzerland, Ireland, United States, Taiwan and New Zealand. The earliest

registration was obtained in Switzerland which took effect in 1999. In

addition, international registration under the Madrid Agreement and Protocol

- 7 -

was also obtained and the countries designated thereunder included a number

of European countries.

The subject marks

22. Each of the subject marks consists of the words “Capital” and “Dynamics”.

The two words are represented in the upper case or the lower case or a

combination of both.

The relevant consumers

23. The subject services include mainly business management and consultancy,

asset management, financial investment and management of funds and

financial analysis. The relevant consumers include both business

organisations and individuals who are interested in obtaining the above

management or financial services.

The relevant date

24. For the purpose of the subject opposition, the relevant date is the Application

Date (i.e. 20 August 2009).

The relevant law

25. Section 12(5)(a) of the Ordinance is worded as follows:

“(5) Subject to subsection (6), a trade mark shall not be registered if, or

to the extent that, its use in Hong Kong is liable to be prevented-

(a) by virtue of any rule of law protecting an unregistered trade

mark or other sign used in the course of trade or business

(in particular, by virtue of the law of passing off); or

(b) ……….

and a person thus entitled to prevent the use of a trade mark is referred to

- 8 -

in this Ordinance as the owner of an "earlier right" in relation to the trade

mark.”

26. The requisite elements for establishing a passing-off action have long been

formulated in the well-known case of Reckitt & Colman Products v. Borden

Inc.5 These elements have been repeatedly relied upon by the courts in

Hong Kong including the Court of Final Appeal in the decision of Re Ping

An Securities Ltd. 6 In essence, these elements are:

(a) the plaintiff has goodwill attached to the services that he supplies

in the mind of the purchasing public by association with a trade

mark under which his services are offered to the public, such that

the trade mark is recognized by the public as distinctive specifically

of the plaintiff’s services;

(b) the defendant has made a misrepresentation to the public leading or

likely to lead the public to believe that the services offered by him

are the services of the plaintiff; and

(c) the plaintiff suffers, or is likely to suffer, damage by reason of the

erroneous belief engendered by the defendant’s misrepresentation

that the source of the defendant’s services is the same as the source

of those of the plaintiff.

Case law on goodwill

27. It is clear from the evidence that none of the Opponents has business

operations in Hong Kong. It appears that their businesses were principally

based in Malaysia, Singapore and Australia. Hence, the submissions of the

parties at the hearing were focused on whether the Opponents have goodwill

in Hong Kong prior to the relevant date for the purpose of a passing off action.

28. “Goodwill” is often described as “the attractive force which brings in

custom”. 7 There have been many case authorities and discussions on

whether a business based abroad has acquired the requisite goodwill to

maintain a passing off action in a place outside its home country. Mr. Ling,

5 [1990] R.P.C. 341. 6 (2009) 12 HKCFAR 808 at 816-817. 7 IRC v. Muller’s Margarine [1901] A.C. at 223.

- 9 -

on behalf of the Opponents, submitted that there was clear divergence in the

approach adopted in England and that used in other common law jurisdictions,

including Hong Kong. Thus, he recommended that the English authorities

should be approached with caution and we should focus on the case law in

Hong Kong. He relied extensively on the cases of Wienerwald Holding AG

v. Kwan Wong Tan and Fong (a firm)(the Wienerwald case),8 Hong Kong

Caterers Ltd v. Maxim’s Ltd (the Maxim’s case),9 Ten-Ichi Company Ltd v.

Jancar Limited (the Ten-Ichi case),10 Kabushiki Kaisha Yakult Honsha v.

Yakudo Group Holdings Ltd (the Yakult case) 11 and Harbour Fit Industrial

Ltd v. Tan Kwai Garden Seafood Restaurant Ltd (the Harbour Fit case) 12 in

his submissions. He also cited the Irish case of C & A Modes v. C & A

(Waterford) Ltd. (the C&A case)13, as it was principally relied upon by the

judge in the Wienerwald case in arriving at his decision.

29. As the case authorities in Hong Kong are directly binding on me, I will

consider these authorities in the main and will refer to the case law in other

jurisdictions where appropriate.

Case authorities submitted by the Opponents

The C&A case

30. This case was cited in all the Hong Kong cases discussed below. The

plaintiff (respondent) was a long established UK company which owned and

operated more than 60 retail drapery shops throughout the UK, including a

large branch shop in Belfast to which large numbers of citizens of the Irish

Republic travelled to purchase their goods. The trading style used by the

plaintiff was the sign “C & A” and this also formed part of its company name.

The plaintiff had advertised its goods extensively in the Irish Republic

through newspapers and magazines circulating there and on television

channels that were available to the viewers in that country. It recruited staff

from the Irish Republic but it did not have any business there. The

defendant (appellant) was a recently incorporated Irish company which also

carried on a retail drapery business using a large motor van with the letters

8 [1979] FSR 381. 9 [1983] HKLR 287. 10 [1990] FSR 151. 11 [2002] 3 HKLRD 595. 12 [2002] 2 HKC 487. 13 [1978] FSR 126.

- 10 -

“C & A” painted on its sides. Those letters also formed part of the trading

name of the defendant. The defendant offered no explanation for the choice

of its name and its trading style.

31. The plaintiff succeeded in an action for passing off in the Irish Republic

against the defendant and the decision was unanimously confirmed on appeal.

Henchy J. made the following comment at the appellate court:

“Goodwill does not necessarily stop at a frontier. Whether in a

particular area a plaintiff has a goodwill which is liable to be damaged

by the unlawful competition resulting from passing off is a question of

fact and of degree.”14 [my emphasis]

32. The judges were convinced that the plaintiff has a protectable goodwill in the

Irish Republic based on the extensive evidence filed. Such evidence

included the massive advertising conducted by the plaintiff, and the

considerable number of consumers that travelled from the Irish Republic to

the Belfast C&A outlet to do their shopping.

The Wienerwald case

33. The plaintiff in this case was a Swiss company that owned and managed a

chain of more than 400 restaurants trading under the name of “Wienerwald”

in Continental Europe, United States, South Africa and Japan. It planned to

expand its business to Hong Kong and it soon discovered that company

names incorporating the word “Wienerwald” had been reserved by the

defendants, a local firm of accountants. The plaintiff has never carried on

business or engaged in any advertising in Hong Kong. The only advertising

that might come to the attention of the public in Hong Kong was through

some German or other Continental publications. In an action for passing off,

the plaintiff sought interim injunction against the defendants.

34. The Court agreed with the principles in the C&A case and in particular, the

analysis of Henchy J. in that decision. Leonard J. was prepared to accept

that “the reputation to be protected is reputation already existing in this

Colony albeit that reputation may be acquired here even when no business is

14 Per Henchy J. at page 138 of the decision.

- 11 -

carried on here.”15 However, the court was not convinced from the evidence

adduced that there was a triable issue that the plaintiff had acquired reputation

among a significant segment of the population in Hong Kong. The

application for interim injunction was thus refused.

35. The Wienerwald case confirmed that the court would be prepared to find that

a foreign plaintiff has goodwill in Hong Kong although it does not have a

business here. However, it must be able to show that the goodwill of its

business has penetrated into Hong Kong.16

The Maxim’s case

36. This is an opposition case decided under the repealed Trade Marks Ordinance

(“Cap. 43”)(“repealed Ordinance”). The case concerns an application for

registration of the mark “Maxim’s” together with its Chinese name in respect

of bakery products made by Hong Kong Caterers Ltd. The owner of the

world-renowned restaurant, the Maxim’s of Paris, opposed the application.

The Assistant Registrar of Trade Marks refused the application by the

exercise of his discretion under section 13(2) of the repealed Ordinance.

The applicant appealed to the High Court. One of the issues that Hunter J.

found necessary to consider at the outset was whether the reputation of a

business has to be based upon and supported by the conduct of a business in

Hong Kong; by actual user in Hong Kong; or by the presence of customers

in Hong Kong.

37. After examining the authorities in this area (including the C&A case, the

Wienerwald case and other authorities in UK, Australia and New Zealand),

Hunter J. summarised his view on this issue as follows:

“It therefore seems to me right in Hong Kong to treat the existence here

of a trading reputation, for both trade mark and passing off purposes, as

a question of pure fact to be determined on the evidence as a

whole.”17[my emphasis]

15 Per Leonard J. at page 392 of the decision. 16 “As I see it what cannot be protected in passing off is a goodwill existing elsewhere which has not yet

penetrated to this jurisdiction.” Per Leonard J. at page 392 of the decision. 17 Per Hunter J. on page 296 of the decision.

- 12 -

38. Mr. Ling submitted that the above statement has succinctly summarised the

concept of goodwill under Hong Kong law.

The Ten-Ichi case

39. The approach in the Maxim’s case on goodwill or reputation was followed in

the Ten-Ichi case. This is a passing off action in which an application was

made for an interlocutory injunction. The plaintiff was the owner of a chain

of more than 40 Japanese restaurants in Japan called “Ten-Ichi” written in a

certain style of characters. The name was a household name in Japan. The

defendants operated a Japanese restaurant in Hong Kong called “Ten-Ichi”

written in identical style of ideograms as that of the plaintiff’s. The

defendants admitted that they had deliberately chosen to copy the name and

the characters used by the plaintiff. In deciding whether the plaintiff had

goodwill or reputation that should be protected in Hong Kong, Sears J.

highlighted the following facts that appeared clear from the evidence:

(a) the deliberate copying of the plaintiff’s name by the defendants in

a manner that was calculated to cause confusion to the public and

to mislead them in thinking that the defendants’ restaurant was that

of the plaintiff’s;

(b) the location of the defendants’ restaurant was in Tsimshatsui, the

heart of the entertainment and tourist belt;

(c) the large number of tourists between Hong Kong and Japan;

(d) the large population of Japanese residing in Hong Kong;

(e) the trading and commercial activities between the two places; and

(f) the plaintiff’s intention to expand its business to Hong Kong.

40. The judge considered that the defendants must have realized that, as the

plaintiff was so well-known and of such high international reputation,

copying and exploiting its name would lead to financial benefit. According

to his view, this fact alone demonstrated that the plaintiff did have goodwill

in Hong Kong. He then went on to add that other factors such as the number

of Japanese people living in Hong Kong and the plaintiff’s intention to

- 13 -

expand its business to Hong Kong were also important.18 The judge was

thus satisfied that there was a serious question to be tried that the plaintiff has

established goodwill here and an interlocutory injunction was granted.

41. This case has highlighted some of the factors and circumstances that the

courts would take into account in determining whether goodwill has been

established.

The Harbour Fit case

42. The plaintiff in this case operated three very successful restaurants in

Shenzhen under the name “Tan Gwai Hin”. The restaurants were advertised

in Hong Kong and patronised by Hong Kong citizens who visited Shenzhen.

With the flow of people between Shenzhen and Hong Kong, the restaurants

looked to both cities for their business. The defendant opened a restaurant

in Kowloon. The first three characters of the name of the defendant and its

restaurant were identical to those of the plaintiff. The plaintiff sued for

passing off and applied for an interlocutory injunction against the defendant.

43. After reviewing the previous authorities on the issue of territoriality in

relation to goodwill and the evidence adduced in this case, the court found

that there was a strong case that the plaintiff has an established goodwill in

Hong Kong and that it has at least a serious case to be tried. The application

for interlocutory injunction was refused merely because there was delay on

the part of the plaintiff in taking out the application.

The Yakult case

44. This is a passing off and trade mark infringement case of which the plaintiffs

were a group of companies that owned the trade names and trade marks

relating to the “Yakult” products worldwide. In Hong Kong, the products

were sold in bottles bearing the names “Yakult” and “益力多”. In Taiwan,

they were manufactured and marketed under the name “養樂多”. The

defendant was a Hong Kong company which marketed a similar product

under the name of “Yakudo” in the Mainland. It has not yet launched its

products in Hong Kong but has applied to the Hong Kong Trade Marks

18 Analysis of Sears J. at page 155 of the decision.

- 14 -

Registry for registration of “Yakudo (養樂多)” and device. Furthermore, it

has applied to the Hong Kong Stock Exchange for listing.

45. The defendant agreed that the plaintiffs had goodwill in Hong Kong in

relation to the name “益力多”. However, it argued that since “養樂多” was

only used in Taiwan by the Taiwanese affiliated company and given that the

Taiwanese affiliate has neither business nor customers in Hong Kong, it did

not have goodwill here for passing off purpose. At the interlocutory stage,

Deputy Judge Lam granted an injunction to restrain the defendant from

seeking a listing status in Hong Kong pending the trial of the action. He

held that there were serious questions to be tried including whether the name

“Yakult” was a badge of goodwill in Hong Kong. He then went further to

express his view that it must be arguable that the law should recognise the

concept of an international goodwill and it was a pure question of fact

whether the goodwill of the plaintiffs manifested itself also in the words “養

樂多”. However, at the trial of the action, the judge did not discuss the issue

of “international goodwill”. He simply held that the plaintiffs enjoyed

substantial goodwill in Hong Kong in relation to “益力多” and the use of “養

樂多” by the defendant would cause substantial confusion in Hong Kong.

Case authorities submitted by the Applicant

46. Mr. Wong, on behalf of the Applicant, submitted that goodwill remained one

of the elements that a plaintiff must prove in a passing off claim. He referred

to Kerly’s Law of Trade Marks and Trade Names19 which said that where a

foreign plaintiff has a substantial reputation within the jurisdiction where the

claim was made, the court would normally accept minimal evidence that a

business existed within such jurisdiction, but there must be some. In the

C&A case, the plaintiff was able to show that it has a substantial body of

customers in the Irish Republic. In the Wienerwald case, the judge did not

hold that pure reputation with no customers in Hong Kong would be

sufficient for a passing off action. Instead, he clearly expressed the view

that local goodwill could be proved by showing the presence of “intermittent

customers” coupled with other factors. 20 As for the Maxim’s case, Mr.

Wong pointed out that passing off was not a specific ground of opposition

under the repealed Ordinance and the court was only concerned with section

19 15th Ed. (2011), paragraph 18-053. 20 Page 389 – 390 of the decision.

- 15 -

12(1) of the repealed Ordinance. In the Yakult case, the judge specifically

emphasised, at the interlocutory stage, that he has not come to any concluded

view on the law of international reputation. Mr. Wong then drew my

attention to the UK decisions of Anheuser-Busch Inc v. Budejovicky Budvar

NP (the Anheuser case),21 Hotel Cipriani SRL v. Cipriani (Grosvenor Street)

Ltd (the Cipriani case)22 and Starbucks (HK) Ltd v. British Sky Broadcasting

Group Plc. (the Starbucks case).23

47. Based on the above UK authorities, Mr. Wong submitted that in order for the

Opponents to succeed on the ground of passing off, they must have sufficient

goodwill in Hong Kong before the Application Date. Further, such

goodwill could either be proved by actual business carried on in Hong Kong,

or in the absence of such actual business, substantial reputation coupled with

some customers in Hong Kong.

The Anheuser case

48. The plaintiff (appellant) in this case was the brewer of beers in US sold under

the “Budweiser” trade mark. The defendant (respondent) was the brewer of

beers in the Czech Republic in a town formerly called Budweis and its beers

were also sold by the name “Budweiser”. The plaintiff exported a

significant quantity of its beers to UK but they were limited for the use of and

sale in the US military and diplomatic establishments there. Sales of its

beers in the open market were however minimal. When the defendant

actively marketed its beers and achieved substantial sales in UK, the plaintiff

claimed inter alia injunctive relief to prevent the defendant from selling beers

with the “Budweiser” trade mark.

49. The UK Court of Appeal held that the plaintiff had to establish goodwill in

UK in the above trade mark. Goodwill, as opposed to mere reputation,

could not exist except in relation to a business carried in UK. The court

further held that the plaintiff’s trading activities could not constitute a

business if it has no British customers. Customers could include consumers

who purchased the goods directly from the plaintiff or indirectly through the

market. However, the plaintiff’s sporadic and occasional sales of beers in

21 [1984] FSR 413. 22 [2010] RPC 16. 23 [2014] ECC 4.

- 16 -

the US military base and the diplomatic establishments in UK could not

constitute the carrying of a business there.24

The Cipriani case

50. This is a fairly complex case and one of issues discussed was whether the

claimant, the owner and operator of Hotel Cipriani in Venice, has goodwill in

UK. The Court of Appeal confirmed that the claimant (respondent) has

goodwill in UK on the basis that it had a substantial reputation there and a

substantial body of customers from UK. The findings were partly the result

of the claimant’s significant marketing efforts which were directed at the

relevant public in UK and the significant volume of business placed directly

from UK, either directly by individual clients or via travel agents.25

The Starbucks case

51. The claimants (appellants) in this case included PCCW Media Ltd (“PCCW”),

an internet service provider with an established goodwill in Hong Kong in

relation to the “NOW TV” service. In trying to establish that PCCW also

has a goodwill in England in relation to the supply of the TV service, the

claimants argued that some of the programmes supplied to the subscribers of

NOW TV service in Hong Kong were also viewed free via the internet by a

section of the public in England. The evidence showed that PCCW’s

website could be accessed worldwide and it was not specifically targeted at

the consumers in England.

52. The Court of Appeal confirmed the decision of the trial judge and held that

PCCW has failed to establish a goodwill in UK in respect of the “NOW TV”

services. The judge took the view that the universal presence and

accessibility of the Internet, which enabled access to be gained in UK to

programmes emanating from Hong Kong, was not a sufficiently close market

link to establish an identifiable goodwill with a customer base there. Sir

John Mummery further elaborated this point and said that “generating a

goodwill for service delivery generally involves making, or at least

attempting to make, some kind of connection with customers in the market

with a view to transacting business and repeat business with them”.26

24 See analysis in the judgement of Oliver L. J. from pages 464 – 467 of the decision. 25 Judgement of Lloyd L. J. at paragraph 118 of the decision. 26 Paragraph 104 at page 58 of the decision.

- 17 -

The position in Hong Kong

53. In today’s world of rapid improvements in the means of communication, it is

not surprising that case law relating to the territorial scope of the goodwill of

a business is still evolving. The case decisions in UK have evolved from

the requirement that the plaintiff must be carrying on a business in UK

(Bernardin v. Pavilion Properties)27 to that of having a substantial body of

customers from UK (the Cipriani case) or a sufficiently close market link

with UK (through making or attempting to make connections with customers

in UK with a view to transacting business with them) (the Starbucks case).

The Hong Kong courts have however approached the issue of goodwill as a

question of fact to be determined based on the evidence as a whole in each

case. That said, whether the plaintiff has customers in Hong Kong, the

promotion and marketing efforts of the plaintiff and the extent of its

reputation in Hong Kong are important factors that the courts would take into

account when determining the issue of goodwill.

54. Using the approach adopted by the courts in Hong Kong, I will proceed to

examine whether the Opponents have established that they have goodwill in

Hong Kong for the purpose of a passing off action.

Do the Opponents have goodwill in Hong Kong?

55. The Opponents claimed that they enjoyed a significant reputation in Hong

Kong in respect of the services which they provided by reference to the name

or trade mark “Capital Dynamics”. At the hearing, Mr. Ling focused his

submissions on the goodwill of the 1st Opponent and, to a lesser extent, the

2nd Opponent in relation to investment advisory and fund management

services.

1st Opponent

56. The 1st Opponent was an independent financial advisor and the publisher of

the Newsletter. Mr. Ling submitted that the 1st Opponent enjoyed a degree

of reputation among the public in Hong Kong for its investment advisory

services under the name “Capital Dynamics”, particularly among the readers

27 [1967] R.P.C. 581.

- 18 -

of the Newsletter and the viewers of Bloomberg TV. Furthermore, the

paying subscribers to the Newsletter showed that the 1st Opponent had a

customer base in Hong Kong.

The Newsletter

57. The computer record adduced by the Opponents shows that there were five

individuals with their addresses in Hong Kong who have subscribed to the

Newsletter. The earliest of such subscriptions was made in November 2005.

The first point put forward by Mr. Wong was that having five subscribers over

a period of 20 years (from the launch of the Newsletter in 1989 up to the

Application Date) was too trivial for the Opponents to acquire goodwill for

the purpose of passing off.

58. The second point raised by Mr. Wong concerns the details in the Newsletter

and the subscription form. There were English and Chinese versions of the

Newsletter and they were available in printed form, and subsequently, in

electronic form. The exact form or version subscribed by the Hong Kong

customers were not revealed in the evidence. Mr. Wong highlighted the

names or signs used on such publication for my attention.

(a) English version of the Newsletter (in printed form):28

The sign “ ” appears prominently on the

top of the front page of the Newsletter and it is considerably larger

than the rest of the contents. Below it is the sign

“ ”. There is a note in the middle of

this page to inform the readers that the Newsletter was published

and printed by the 1st Opponent. The name of the 1st Opponent

also appears at the footer on the front page as well as the header

on each subsequent page (next to the volume number of the

Newsletter).

28 Exhibit “TTB-17” of Tan’s 2nd SD.

- 19 -

(b) Chinese version of the Newsletter (in printed form):29

The sign “ ” appears prominently on the

top of the front page and it is considerably larger than the rest of

the contents. Below it is the sign “ ”.

The 1st Opponent (identified by its English name) was referred to

as the publisher and printer of the Newsletter in the middle of the

front page and also at the footer of that page.

(c) Electronic version available on the Website (i.e.

www.icapital.biz): 30

The sign “ ” appears prominently on the

top of the homepage. There is a brief introduction of the 1st

Opponent, the 3rd Opponent and the 4th Opponent on the left-hand

column of the homepage. Mr. Wong pointed out that viewers

would not be able to access the articles posted on the Website

unless they have subscribed to the Newsletter.

(d) Subscription form:31

The signs “ ” and

“ ” appear prominently on the top of

the form. The 1st Opponent (identified by its English name) is

referred to as the publisher and printer of the Newsletter at the

footer.

59. Based on the above evidence, Mr. Wong argued that the trade marks used in

the Newsletters and the subscription form were “ ”,

and “ ”. The subscribers would perceive

“i Capital” or “資本投資” (as opposed to “Capital Dynamics”) as the name

29 Exhibit “TTB-17” of Tan’s 2nd SD. 30 A copy of the homepage of the Website was printed and produced as evidence at Exhibit “TTB-2”

of Tan’s 1st SD. 31 Exhibit “TTB-17” of Tan’s 2nd SD.

- 20 -

of the Newsletter. Furthermore, the issuance of a financial publication to

the public is different from the provision of financial advice to the public.

The subscribers should be regarded as customers of the Newsletter instead of

the Opponent’s investment advisory services.

60. I agree that it is clear from the evidence that the Newsletter would be referred

to by its subscribers as “i Capital”, “資本投資” and perhaps to a lesser extent,

“iCapital.biz”. However, I consider that the subscribers to a financial

publication would also pay due regard to the identity of the publisher. They

would generally exercise care in choosing a publication that would give them

a more accurate picture of the market conditions and the available investment

opportunities. The identity of the publisher is one of the factors that they

would take into account in the selection process. That said, the publisher

(i.e. the 1st Opponent) is not giving investment advice to the individual

subscribers through the issue of the Newsletter. This is evident from the

following statements on the front page of the Newsletter:

“Any recommendation contained in this publication does not have any

regard to the specific investment objectives, financial situation and

particular needs of any specific addressee. It is published for the

assistance of recipients but it is not to be relied upon as authoritative or

taken in substitution for the exercise of judgements by any recipient.”32

61. Furthermore, it is worth noting that the issue of a newspaper, magazine or

other publication which is generally available to the public does not fall

within the definition of “advising on securities” which is a regulated activity

under the Securities and Futures Ordinance (Cap. 571).33

62. The Newsletter was made available to the public through subscription and it

contains the views of the CD Group on the general market conditions and its

analysis on selected securities. Given the wide range of background and

financial conditions of the subscribers, the contents were not, and could not

be, directed at the investment needs and circumstances of each subscriber.

On the other hand, a consumer who seeks professional investment advisory

services would expect his advisor to consider his financial conditions,

investment objectives and risk appetite before advising him of the financial

32 The Chinese version of the Newsletter also contains statements to the same effect. 33 Part 2 of Schedule 5 of the Securities and Futures Ordinance (Cap.571).

- 21 -

products that suit his needs. It should be clear to him that a financial

publication that is generally available to the public could not serve his

purpose. Based on the above analysis, I do not consider that the Hong Kong

subscribers of the Newsletter could be regarded as customers of the

investment advisory services provided by the 1st Opponent. Rather, they

were merely customers of the Newsletter published by the 1st Opponent.

The Bloomberg interviews

63. Mr. Tan deposed that he has given a number of interviews on Bloomberg TV

that identified him as the managing director and CEO of the CD Group.

Such interviews were broadcasted to viewers in real-time around the world

including Hong Kong, and could also be downloaded from Bloomberg’s

website. In one of the interviews aired on 28 July 2005,34 Mr. Tan was

introduced as an investment guru who was noted for his insight into global

stock markets, particularly those in Asia. As Bloomberg is a well-known

provider of business information, it is highly persuasive and enjoys a high

captive audience in a major international financial centre like Hong Kong.

64. The Opponents also provided printouts from Bloomberg’s website to show

that its programmes were broadcasted by certain television channels in Hong

Kong including 1010 Studio on Demand, BBTV – Hong Kong Broadband,

Hong Kong i-Cable, PCCW Now TV and Smartone Vodafone Fone TV.35

The programmes were also broadcasted daily on the local free TVB Pearl

channel.36

65. Mr. Ling emphasised that the above Bloomberg interviews were broadcasted

live to viewers or subscribers of Bloomberg TV. Live broadcast should be

distinguished from Internet TV services through which the NOW TV

programmes were made available to viewers in the Starbucks case. In that

case, the NOW TV programmes were made available on PCCW’s website for

access by any user of the Internet from anywhere in the world free of charge.

Furthermore, such website was not specifically targeted at the viewers in UK.

This is to be distinguished from Bloomberg TV that was broadcasted live to

its viewers or subscribers of its services.

34 CD-Rom adduced at Exhibit “TTB-4” of Tan’s 1st SD. 35 Exhibit “TTB-19” of Tan’s 2nd SD. 36 Exhibit “TTB-20” of Tan’s 2nd SD.

- 22 -

66. Based on the above evidence and analysis, Mr. Ling submitted that the 1st

Opponent enjoyed a degree of reputation among the public in Hong Kong

and in particular, the viewers of Bloomberg TV.

67. On the other hand, Mr. Wong drew my attention to the printouts from

Bloomberg’s website (paragraph 64 above). He submitted that such

printouts could only show the state of things as at the date the relevant

webpages were printed (i.e. 31 August 2012). However, what is material in

this case is whether the Bloomberg interviews were available for viewing by

the public in Hong Kong at the time when they were broadcasted. In any

event, there was no evidence on the number of viewers of Bloomberg TV in

Hong Kong at the relevant times. I agree that Mr. Wong has raised some

valid observations. However, they should not be taken too far as Bloomberg

TV has long been used and relied upon by professionals engaged in the

financial and commercial fields in Hong Kong as one of the important

providers of financial information.

68. At the same time, I note from the interview recorded on the CD-rom and those

available via the Internet links 37 that only five interviews (“relevant

interviews”) were relevant for the purpose of assessing the goodwill of the

Opponents’ services in relation to the name “Capital Dynamics”. The

relevant interviews were conducted on 28 July 2005, 5 July and 27 November

2006, 6 April 2007 and 22 July 2008 and Mr. Tan was introduced therein by

reference to his position in the CD Group. As for the other interviews, they

were either dated after the Application Date or the dates of the

interviews/broadcasts could not be ascertained from the evidence provided.

Furthermore, Mr. Tan was often introduced with reference to “i Capital

Global Fund” (as opposed to “Capital Dynamics”).

Internet hits

69. Mr. Tan deposed that the Internet traffic for the Website originating from

Hong Kong varied between approximately 36,000 to 204,000 hits per annum

from 2004 to 2009. This piece of evidence also helped to show that the 1st

Opponent has a reputation among the public in Hong Kong.

37 Paragraphs 10 and 12 of Tan’s 1st SD and paragraph 16 of Tan’s 2nd SD.

- 23 -

70. On the other hand, Mr. Wong highlighted for my attention that viewers of the

Website would not be able to access its contents and the articles posted

thereon unless they have subscribed to the Newsletter.

71. I remind myself that the evidence adduced by the Opponents shows that there

were only five Hong Kong subscribers to the Newsletter over a period of 20

years. It is likely that some of the hits mentioned in paragraph 69 above

might represent repeated access by the subscribers of the electronic version

of the Newsletter. At the same time, there could also be other circumstances

upon which Internet users (aside from the subscribers of the Newsletter)

would come across the Website. It is possible that some Internet users might

be looking up for information concerning the CD Group. However, since

the name of the Applicant’s Group also contain the words “Capital

Dynamics”, it is equally possible that users could in fact be trying to access

the website of the Applicant’s Group or locating their information. Besides,

it is worth noting that “capital” and “dynamic” are common English words

which do not possess a high degree of distinctiveness in the investment and

financial field and these words could be used by Internet users (with no prior

knowledge of the CD Group or the Applicant’s Group) in conducting their

searches.

72. All in all, I do not consider that the Internet hits to the Website would be of

much assistance in establishing the goodwill of the 1st Opponent.

Other media and press interviews

73. Besides the Bloomberg interviews, the Opponents also adduced voluminous

evidence of press cuttings and media interviews with a view to establishing

the reputation of the Opponents. It is clear from the evidence that Mr. Tan

has been actively engaged in media interviews and his comments and analysis

on the financial markets have been quoted and published by the media. In

these interviews, he was often introduced with reference to his title in the CD

Group or “i Capital”. However, it is noted that most of these interviews

were conducted by the Malaysian media38 and the press cuttings were mostly

from newspapers and magazines published in Malaysia.39 There is also no

evidence to show that these interviews or publications were broadcasted or

circulated in Hong Kong.

38 Paragraph 13 of Tan’s 1st SD. 39 Paragraph 17 and exhibit “TTB-22” of Tan’s 2nd SD.

- 24 -

Findings in relation to the 1st Opponent

74. To sum up, the evidence principally relied on by the 1st Opponent to establish

its goodwill or reputation in Hong Kong in relation to investment advisory

services, includes the following:

(a) the Newsletter that were available to the public for subscription

and in respect of which there were five subscribers based in Hong

Kong;

(b) the five relevant interviews conducted by Mr. Tan over a period of

three years;

(c) the number of hits to the Website where the electronic version of

the Newsletter was posted; and

(d) other press and media interviews with the Malaysian press

broadcasting channels of which there was no evidence of their

availability or circulation in Hong Kong.

75. Looking at the evidence as a whole and in particular, taking into account my

observations in relation to each category of evidence, I am not satisfied the

1st Opponent has established goodwill in Hong Kong in respect of investment

advisory services with reference to the name “Capital Dynamics”.

76. Lest I am wrong on the above findings and, based on the evidence, the 1st

Opponent should be regarded as having acquired some goodwill in Hong

Kong in respect of investment advisory services, I consider that such

goodwill was too trivial for the purpose of a passing off action.

77. In Hart v. Relentless Records Ltd.,40 the UK court held, inter alia, that the

law of passing off does not protect a goodwill of trivial nature. In that case,

the claimant has engaged in some activities under the name of “Relentless”

by making and distributing small quantities of “white label” (promotional)

records. These records were given away to DJs to generate an interest in the

records. A few years later, the defendant (Relentless Records Ltd) launched

a track that was an immediate commercial success. On the issue of passing

off raised by the claimant, the judge was of the view that the name “Relentless”

as denoting the claimant could have been exposed to no more than a few

40 [2003] F.S.R. 36.

- 25 -

hundred semi-amateur DJs. He doubted how many of them could have

actually remembered the name although it would not be unreasonable to

assume that a proportion did. There were odd mentions of it on the radio

and a few magazines. However, in the above situations, what would have

mattered most was the track and performer and not the record company.

The judge concluded that it was a minuscule reputation and the law of passing

off would not protect a goodwill of trivial extent.

78. In the subject opposition, the 1st Opponent has five Hong Kong subscribers

to the Newsletter from the time it launched the publication up to the

Application Date (covering a period of 20 years). The CD Group (including

the name “Capital Dynamics”) was mentioned on five occasions in the

interviews that Mr. Tan had with Bloomberg TV. On such limited evidence,

I am of the view that even if the 1st Opponent did have some goodwill in

respect of investment advisory services, such goodwill is only trivial in nature

and is not adequate for the purpose of a passing off action.

79. I will now proceed to consider whether the other Opponents have acquired

the requisite goodwill in Hong Kong.

2nd Opponent

80. The 2nd Opponent was a Malaysian company (incorporated in 1997) and the

fund manager of the listed fund. The Opponents claimed that the 2nd

Opponent enjoyed an excellent track record in relation to the listed fund. Mr.

Ling acknowledged that the 2nd Opponent did not have any identifiable

customers in Hong Kong. However, he argued that the subscribers of the

Newsletter and the viewers of Bloomberg TV in Hong Kong should be aware

that the 2nd Opponent has been providing fund management and investment

services to the listed fund.

81. Besides the above background information, the 2nd Opponent was in essence

seeking to rely on the same set of evidence as that of the 1st Opponent. This

would include, in the main, subscription to the Newsletter by the five local

subscribers and the relevant interviews.

82. The 2nd Opponent was not the publisher of the Newsletter and did not have

any contractual relationship with the Hong Kong subscribers. Hence, its

- 26 -

connection with the Hong Kong subscribers was even more remote than the

1st Opponent. My analysis above regarding the Bloomberg interviews also

applies to the position of the 2nd Opponent. On such basis, I find that the

2nd Opponent has failed to establish that it has a goodwill in Hong Kong in

respect of fund management and investment services for passing off purpose.

3rd Opponent and 4th Opponent

83. The 3rd Opponent was a Singaporean fund management company that

launched the “i Capital Global Fund”. The 4th Opponent was an Australian

fund management company which launched the “i Capital International Value

Fund” that was targeted at retail investors. No further details were provided

on the connection between the above companies and Hong Kong.

84. Based on the evidence provided, I am not satisfied that the 3rd Opponent and

the 4th Opponent have established that they have goodwill in Hong Kong in

respect of the fund management and investment services for passing off

purpose.

Findings on section 12(5)(a) of the Ordinance

85. As the first element of a passing off action could not be established, there is

no need for me to proceed further to consider the elements of

misrepresentation and damage.

86. The Opponents have failed to establish the ground of opposition under

section 12(5)(a) of the Ordinance.

Conclusion

87. Besides section 12(5)(a) of the Ordinance, the Opponents have not relied

upon or made submissions on other grounds of opposition at the hearing.

Based on my findings above, the opposition fails.

- 27 -

Costs

88. The Applicant has sought costs and there is nothing in the circumstances or

conduct of this case which would warrant a departure from the general rule

that the successful party is entitled to its costs. Accordingly, I order that the

Opponents should pay the costs of these proceedings.

89. Subject to any representations as to the amount of costs or calling for special

treatment, which either party makes within one month from the date of this

decision, costs will be calculated with reference to the usual scale in Part I of

the First Schedule to Order 62 of the Rules of the High Court (Cap. 4A) as

applied to trade mark matters, unless otherwise agreed between the parties.

(Maria K. Ng)

for Registrar of Trade Marks

19 September 2014

- 28 -

Schedule A

The subject services

Class 35

Business management and organization consultancy.

Class 36

Asset management and financial transactions of all kinds namely institutional financial

asset management, financial portfolio management, allocation, and structuring for

assets of all kinds, creation and placement of institutional investment products,

financial transaction processing, financial risk analysis, technical analysis of asset

management portfolios and risk management transactions, financial investment and

management in the fields of private investment funds, private investment fund of funds,

hedge funds, buyout funds, real estate funds, and real estate fund of funds, management

of private equity funds, private equity fund investment services, and monetary

operations.

Recommended