Embed Size (px)

Citation preview

Tripping Over A Dollar To Save A Dime : Tips To

Refining Your Budget ProcessTrevor Pinn, CPA CA

Director of Finance and POA Court Services

Town of Parry Sound

Agenda

• Importance of Financial Policies

• Budget and Financial Control Policy –The Framework

• Budget Process

• Areas to Improve

• A Council Perspective

Importance of Financial PoliciesA Foundation for Transparency and Consistency

Financial Policies –Why They Are Necessary

• Communicates Council's priorities to staff and the public

• Ensures consistency for all taxpayers

• Ensures predictability

• Everybody retires

• Provides a written knowledge of how things are done

• Makes transitioning staff easier

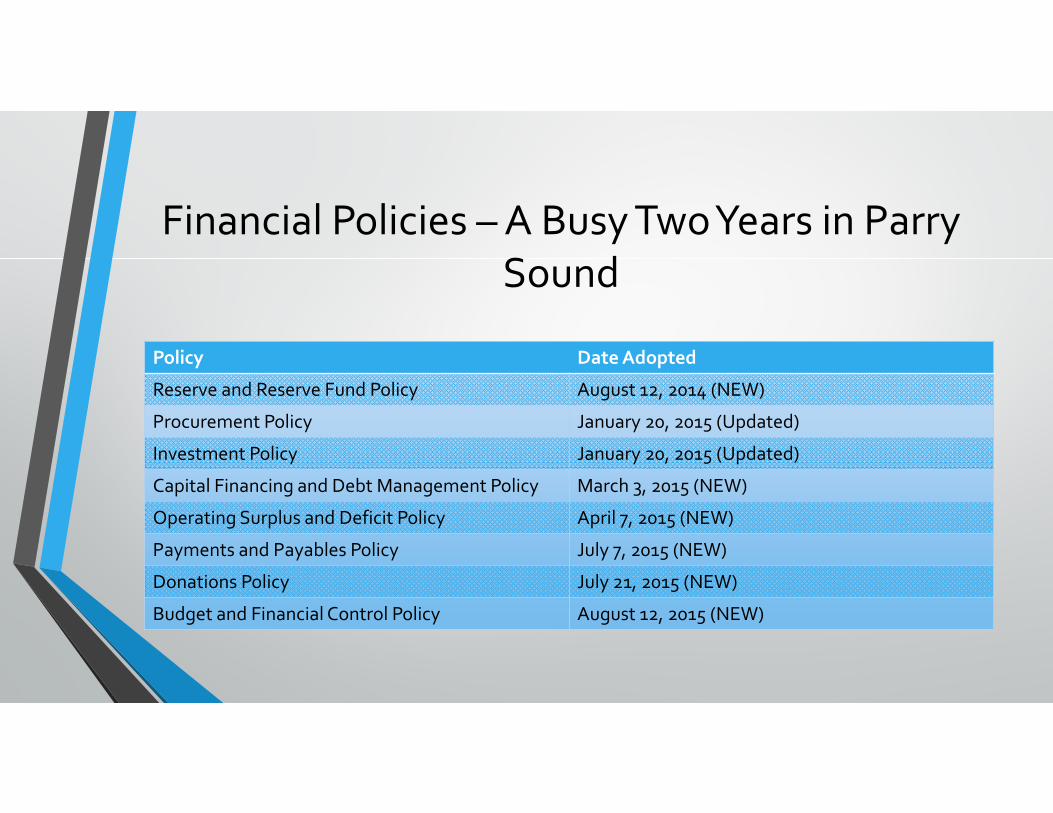

Financial Policies –A Busy Two Years in Parry Sound

Policy Date Adopted

Reserve and Reserve Fund Policy August 12, 2014 (NEW)

Procurement Policy January 20, 2015 (Updated)

Investment Policy January 20, 2015 (Updated)

Capital Financing and Debt Management Policy March 3, 2015 (NEW)

Operating Surplus and Deficit Policy April 7, 2015 (NEW)

Payments and Payables Policy July 7, 2015 (NEW)

Donations Policy July 21, 2015 (NEW)

Budget and Financial Control Policy August 12, 2015 (NEW)

Financial Policies – Streamlining the Budget Process

• Adopting policies makes the budget process faster

• Reserve and Reserve Fund Policy• Provides a mechanism to save for future needs (it is not just "rainy day")

• You do not need a reserve or fund for every different thing…Think larger bucket

• Town went from 153 reserve accounts (57 active) to 19 reserves (now 28)

• Group similar reserves together

• Operating Surplus and Deficit Policy• Know what you are already going to do with any differences from budget

• Fund to Reserves and Reserve Funds

• Do not need to wait for the year end to be done in order to finish your budget

Budget and Financial Control PolicyDeveloping the Framework for Better Budgets

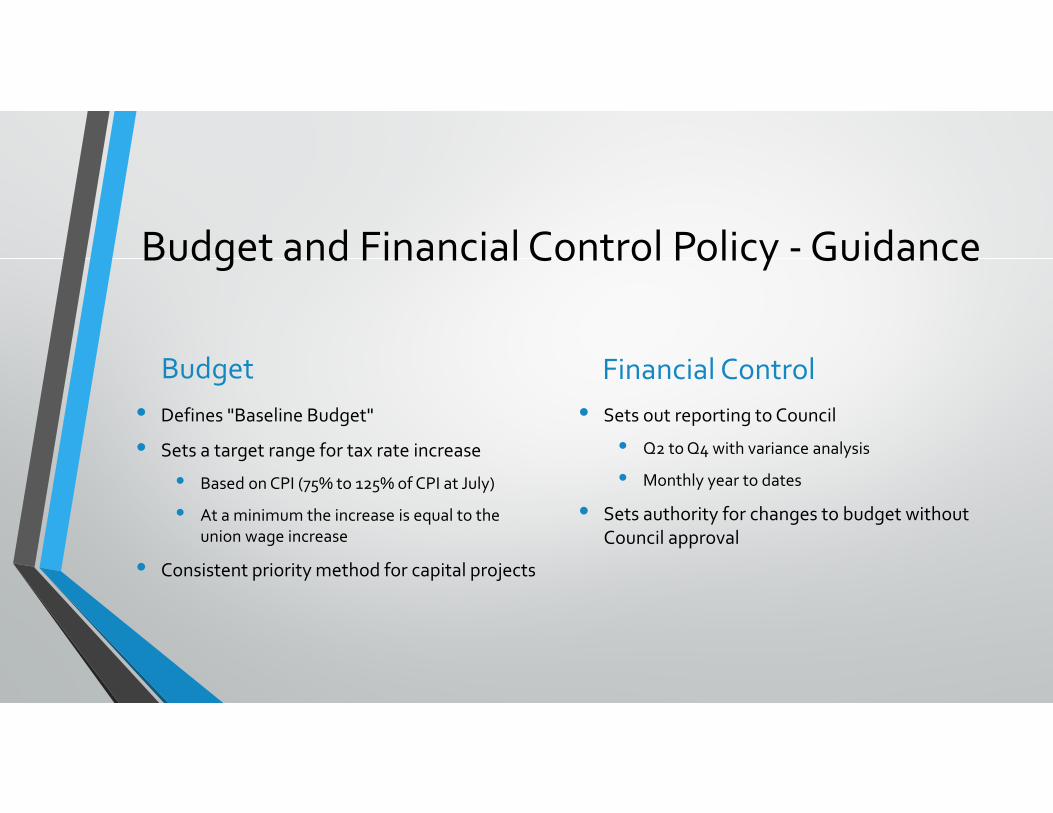

Budget and Financial Control Policy ‐Guidance

Budget• Defines "Baseline Budget"

• Sets a target range for tax rate increase

• Based on CPI (75% to 125% of CPI at July)

• At a minimum the increase is equal to the union wage increase

• Consistent priority method for capital projects

Financial Control• Sets out reporting to Council

• Q2 to Q4 with variance analysis

• Monthly year to dates

• Sets authority for changes to budget without Council approval

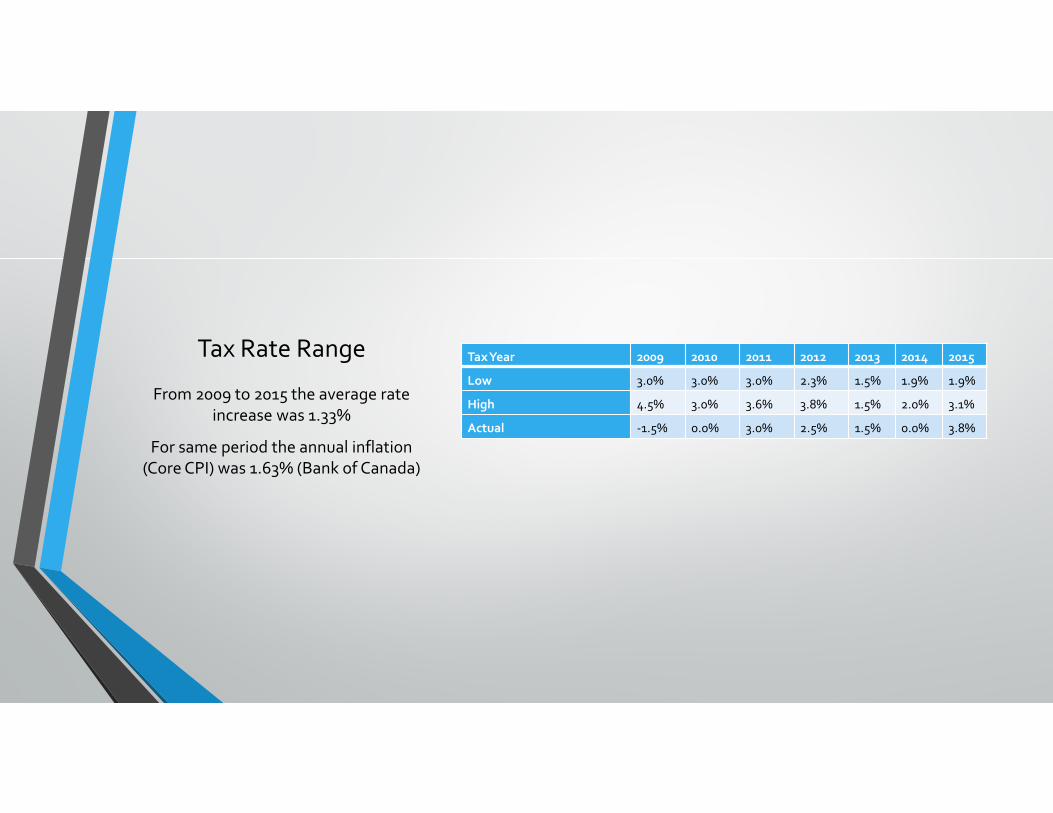

Tax Rate Range Tax Year 2009 2010 2011 2012 2013 2014 2015

Low 3.0% 3.0% 3.0% 2.3% 1.5% 1.9% 1.9%

High 4.5% 3.0% 3.6% 3.8% 1.5% 2.0% 3.1%

Actual ‐1.5% 0.0% 3.0% 2.5% 1.5% 0.0% 3.8%

From 2009 to 2015 the average rate increase was 1.33%

For same period the annual inflation (Core CPI) was 1.63% (Bank of Canada)

Budget ProcessTransparency, Understandability, Appropriate Detail

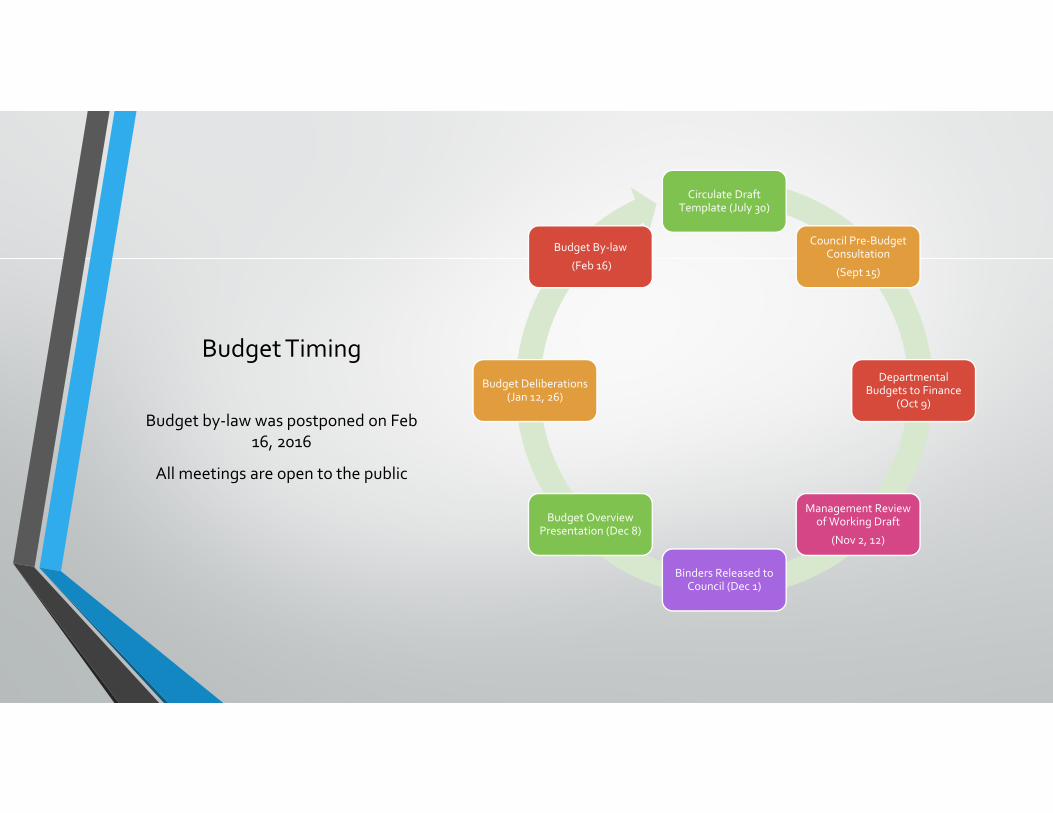

Budget Timing

Circulate Draft Template (July 30)

Council Pre‐Budget Consultation

(Sept 15)

Departmental Budgets to Finance

(Oct 9)

Management Review of Working Draft

(Nov 2, 12)

Binders Released to Council (Dec 1)

Budget Overview Presentation (Dec 8)

Budget Deliberations (Jan 12, 26)

Budget By‐law

(Feb 16)

Budget by‐law was postponed on Feb 16, 2016

All meetings are open to the public

Presentations to Council

• A general “Overview” meeting to go over the budget as a whole• Did not get into specific departments

• Highlighted the “New Initiatives” and “Considered and Cut” lists

• Highlighted capital

• Making it “Fun”• Use PowerPoint

• Use tables / charts

Budget Binder

Before 2015• Determination of Levy

• Convert PSAB to "levy"

• Listed the capital expenditures line by line

• Listed the transfers line by line

• Operating line budget

Now• Policy and Overview

• Determination of Levy

• Convert PSAB to "levy"

• Summary of capital expenditures and transfers to reserves

• Operating budget

• Capital budget

• Reserve and Reserve Fund Transfers

Budget Binder – Policy and Overview

• Executive Summary

• Determination of tax levy

• New Initiatives Summary

• Items considered by staff and removed

• Summary of Operating Budget

• Financial Overview

• Strategic Plan

• Financial Policies

• Performance Information

• Org Chart and Staffing

9,972,616

11,228,832

10,968,020

11,233,338

11,667,606

2011 2012 2013 2014 2015 Budget

Total Taxation

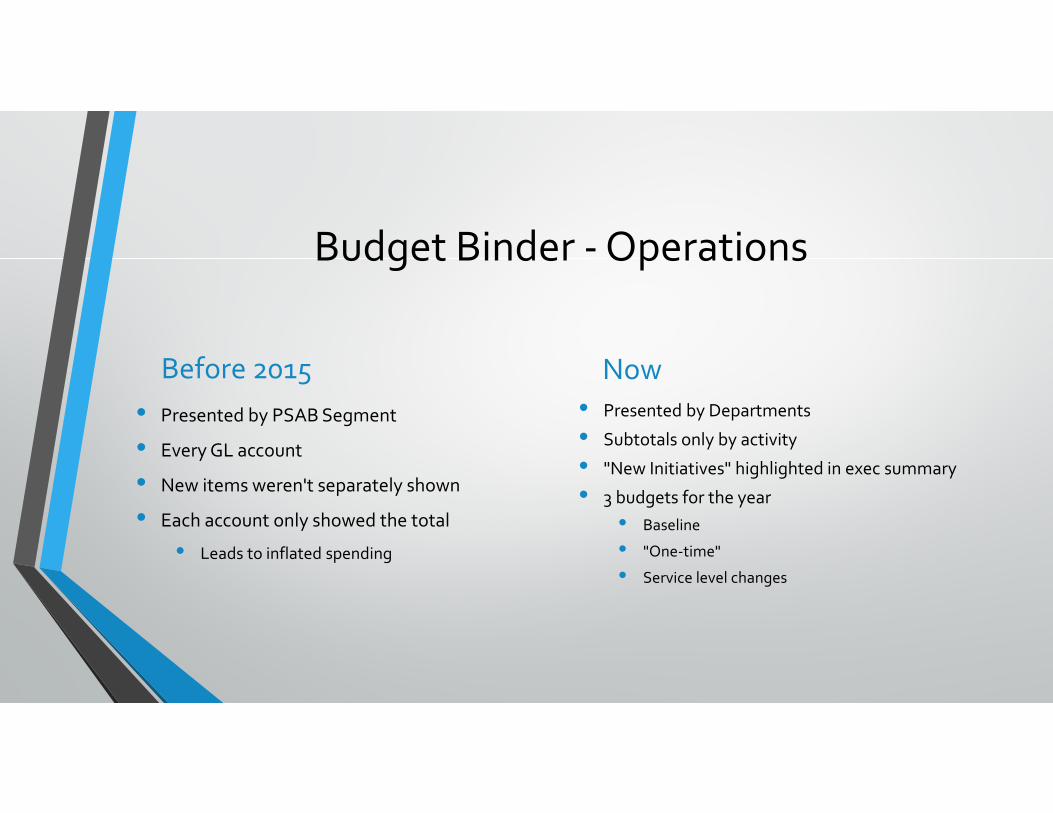

Budget Binder ‐Operations

Before 2015• Presented by PSAB Segment

• Every GL account

• New items weren't separately shown

• Each account only showed the total

• Leads to inflated spending

Now• Presented by Departments

• Subtotals only by activity

• "New Initiatives" highlighted in exec summary

• 3 budgets for the year• Baseline

• "One‐time"

• Service level changes

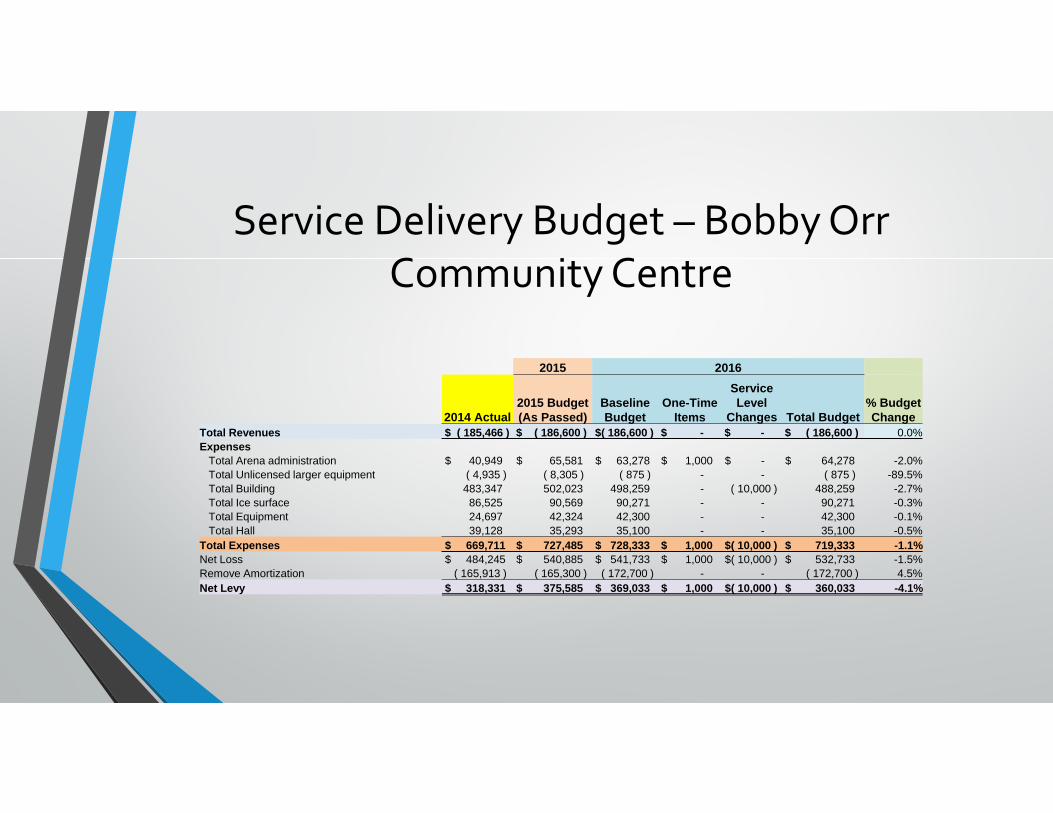

Service Delivery Budget – Bobby Orr Community Centre

2015 2016

2014 Actual 2015 Budget (As Passed)

Baseline Budget

One-Time Items

Service Level

Changes Total Budget% Budget Change

Total Revenues $ ( 185,466 ) $ ( 186,600 ) $( 186,600 ) $ - $ - $ ( 186,600 ) 0.0%Expenses

Total Arena administration $ 40,949 $ 65,581 $ 63,278 $ 1,000 $ - $ 64,278 -2.0%Total Unlicensed larger equipment ( 4,935 ) ( 8,305 ) ( 875 ) - - ( 875 ) -89.5%Total Building 483,347 502,023 498,259 - ( 10,000 ) 488,259 -2.7%Total Ice surface 86,525 90,569 90,271 - - 90,271 -0.3%Total Equipment 24,697 42,324 42,300 - - 42,300 -0.1%Total Hall 39,128 35,293 35,100 - - 35,100 -0.5%

Total Expenses $ 669,711 $ 727,485 $ 728,333 $ 1,000 $( 10,000 ) $ 719,333 -1.1%Net Loss $ 484,245 $ 540,885 $ 541,733 $ 1,000 $( 10,000 ) $ 532,733 -1.5%Remove Amortization ( 165,913 ) ( 165,300 ) ( 172,700 ) - - ( 172,700 ) 4.5%Net Levy $ 318,331 $ 375,585 $ 369,033 $ 1,000 $( 10,000 ) $ 360,033 -4.1%

Budget Binders ‐Capital

Before 2015• Only one year presented

• Showed only the total spent

• Included "old definition" capital

• Repairs

• Consulting reports

• "Not every year" expenditures

Now• 5 Years, 1 year budget plus 4 forecast

• Shows the cost plus the source of funds

• Only includes Tangible Capital Assets

• Irregular expenditures are "one‐time" costs in the operating budget

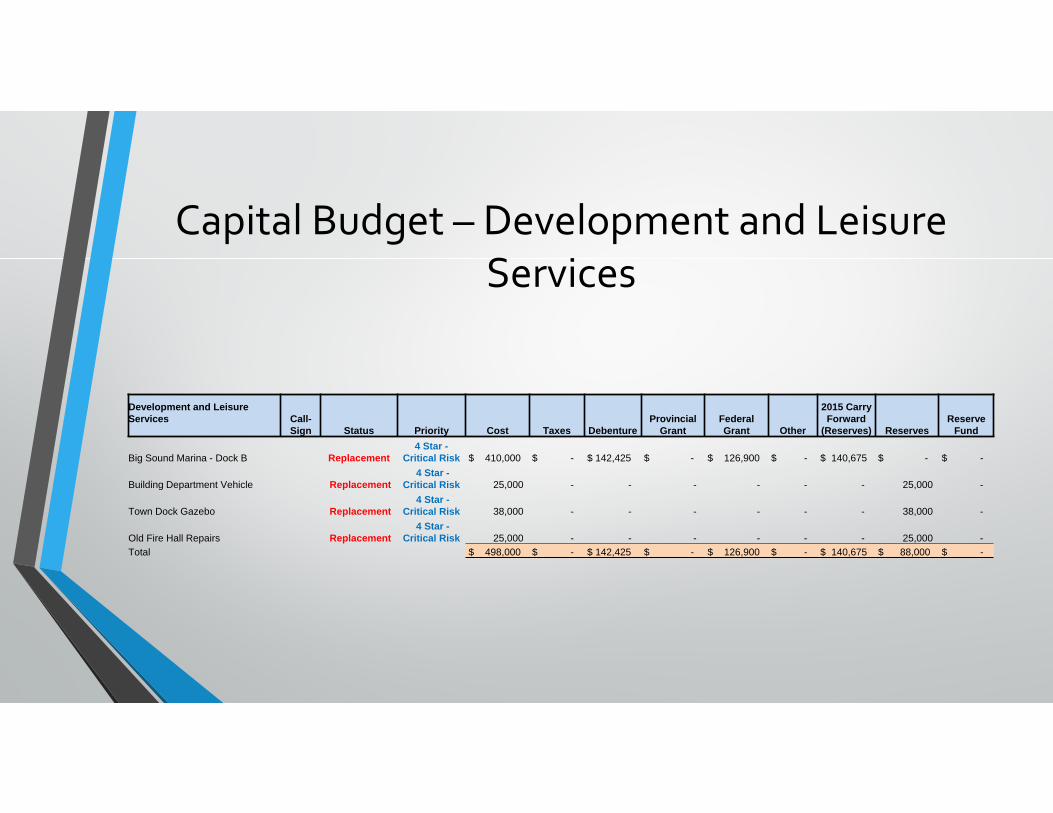

Capital Budget – Development and Leisure Services

Development and Leisure Services Call-

Sign Status Priority Cost Taxes DebentureProvincial

GrantFederal Grant Other

2015 Carry Forward

(Reserves) ReservesReserve

Fund

Big Sound Marina - Dock B Replacement4 Star -

Critical Risk $ 410,000 $ - $ 142,425 $ - $ 126,900 $ - $ 140,675 $ - $ -

Building Department Vehicle Replacement 4 Star -

Critical Risk 25,000 - - - - - - 25,000 -

Town Dock Gazebo Replacement 4 Star -

Critical Risk 38,000 - - - - - - 38,000 -

Old Fire Hall Repairs Replacement 4 Star -

Critical Risk 25,000 - - - - - - 25,000 -Total $ 498,000 $ - $ 142,425 $ - $ 126,900 $ - $ 140,675 $ 88,000 $ -

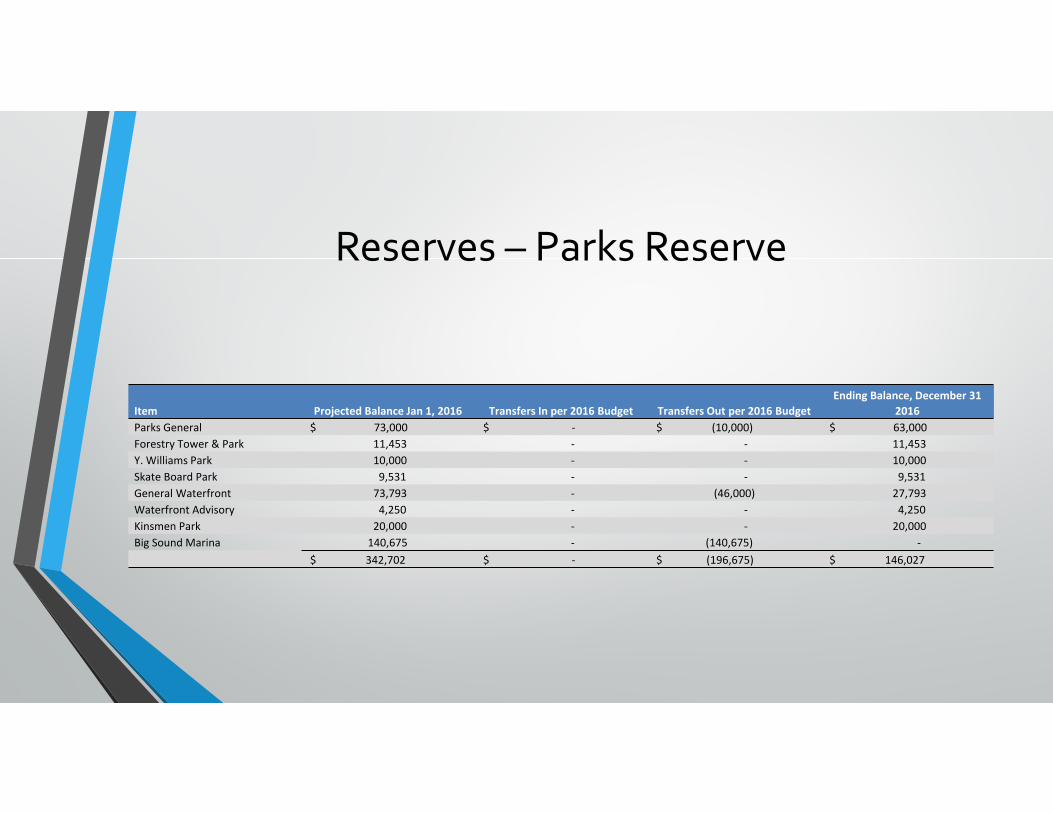

Reserves – Parks Reserve

Item Projected Balance Jan 1, 2016 Transfers In per 2016 Budget Transfers Out per 2016 BudgetEnding Balance, December 31

2016Parks General $ 73,000 $ ‐ $ (10,000) $ 63,000 Forestry Tower & Park 11,453 ‐ ‐ 11,453 Y. Williams Park 10,000 ‐ ‐ 10,000 Skate Board Park 9,531 ‐ ‐ 9,531 General Waterfront 73,793 ‐ (46,000) 27,793 Waterfront Advisory 4,250 ‐ ‐ 4,250 Kinsmen Park 20,000 ‐ ‐ 20,000 Big Sound Marina 140,675 ‐ (140,675) ‐

$ 342,702 $ ‐ $ (196,675) $ 146,027

Areas To ImproveNot A One Year Journey

Public Engagement

• Use of Town website for budget survey

• Streaming Council meetings, including budget meetings

• Open house

Budget Report

• Break amortization out of operating expenses to show "tax levy" portion

• Slightly more detail in operating• Salary and Benefits

• Materials

• Contracted Services

• Extend debt forecast for life of debt

• Project future debt needs

Budget Process

• Starting earlier

• Strategic priority meeting in May

• Capital budget and projections extended past 5 years

• Forecast operating for 2 years

Budget Policy

• Change to the tax rate range

• Is not sufficient for "new services"

• May not be sufficient to fund the capital investment requirements of the AMP

• Is the CPI reflective of the inflation for a municipality??

• Discuss requirements for public engagement

• Adopt multi‐year budgets

A Council PerspectiveMayor Jamie McGarvey

Mayor’s Perspective

• Understandability of financial information• Presentations of information in a non‐technical manner

• Focused discussion on the “Bigger” issues• Do we want to expand services offered at the arena?

• Do we want to invest in the waterfront?

• Council had the information to make informed, strategic decisions• Service A costs $xx,xxx and is 1.0% increase to the tax rate, meets 1 priority

• Service B, C, D and E cost the same and would meet, meets all 5 priorities