Embed Size (px)

DESCRIPTION

In this paper, we attempt to bring out the current state of affairs in the healthcare delivery space in the northern region of India, recent trends in the sector and challenges in executing an effective healthcare agenda, with recommendations and actions for transforming healthcare in North India.

Citation preview

© Grant Thornton India LLP. All rights reserved.

Agenda for Transforming Healthcare Delivery in the Northern Region

Bridging the Divide - for a Healthy India

© Grant Thornton India LLP. All rights reserved.

03 | Foreword

04 | The Healthcare industry

09 | Healthcare delivery

17 | Healthcare infrastructure

23 | Investment Horizon

28 | Changing trends

32 | Outlook

37 | Appendices

48 | Contact us

Contents

© Grant Thornton India LLP. All rights reserved. 3

Foreword

In a populous nation like ours, with an ever increasing need for healthcare infrastructure and

services, the private sector has remained the lynchpin of growth, accounting for more than half of

the total healthcare spending in the country.

The healthcare delivery sector is characterised by wide regional disparities with rural India being

highly underserved. Further, the Southern region has been a change catalyst and far ahead of its

Northern counterpart in terms of access, technology, infrastructure and sometimes even, in the

quality of service.

Against a backdrop of changing demographics and socio economic mix in the Indian population, it

is imperative to raise the bar on quality of healthcare service delivery and ensure equitable and

affordable access across social strata. Achieving this requires several factors to come together, not

least the optimal utilization of existing healthcare resources and the role the government needs to

play in the holistic development of a regional healthcare system.

In this paper, we attempt to bring out the current state of affairs in the healthcare delivery space in

the northern region of India, recent trends in the sector and challenges in executing an effective

healthcare agenda, with recommendations and actions for transforming healthcare in North India.

Mahadevan Narayanamoni

Partner and Practice Leader

Healthcare and Life-sciences

Advisory

Grant Thornton India LLP

Harpal Singh

Conference Chairman &

Past Chairman

CII Northern Region

© Grant Thornton India LLP. All rights reserved. 4

The Healthcare industry Market size and segmentation

© Grant Thornton India LLP. All rights reserved. 5

Glaring statistics

our country ranks 112th on the World Health Organisation’s (WHO) ranking of the

world’s health systems.

doctor-to-patient ratio for rural India, as per the Health Ministry statistics, stands

at 1:30,000, well below the WHO’s recommended 1:1,000.

Overall healthcare spending (public and private) accounts for a mere 4% of India's

GDP, far below the average of 9.5% across Organisation for Economic Co-operation

and Development (OECD) countries. Private sector accounts for more than 70% of

this spend, while the public sector spend has been only 1.4%.

in terms of the total health expenditure per capita (in US$), India spends the least

on public healthcare among the BRICS nations.

for FY14, the Union Budget has allocated larger funds for the health sector, Rs

37,330 crore from the revised estimates of Rs 24,894 crore for FY13

merely 20% of India’s 1.2 billion population is covered by health insurance

of the 1.35 million hospital beds in the country, only 48% are functional

the private sector accounts for 65% of the total number of operational beds, and

over 70% of the spending on healthcare in India.

lack of healthcare facilities in the rural areas as well as among those at the

bottom of the pyramid is one of the big challenges in delivering scalable

healthcare options

© Grant Thornton India LLP. All rights reserved. 6

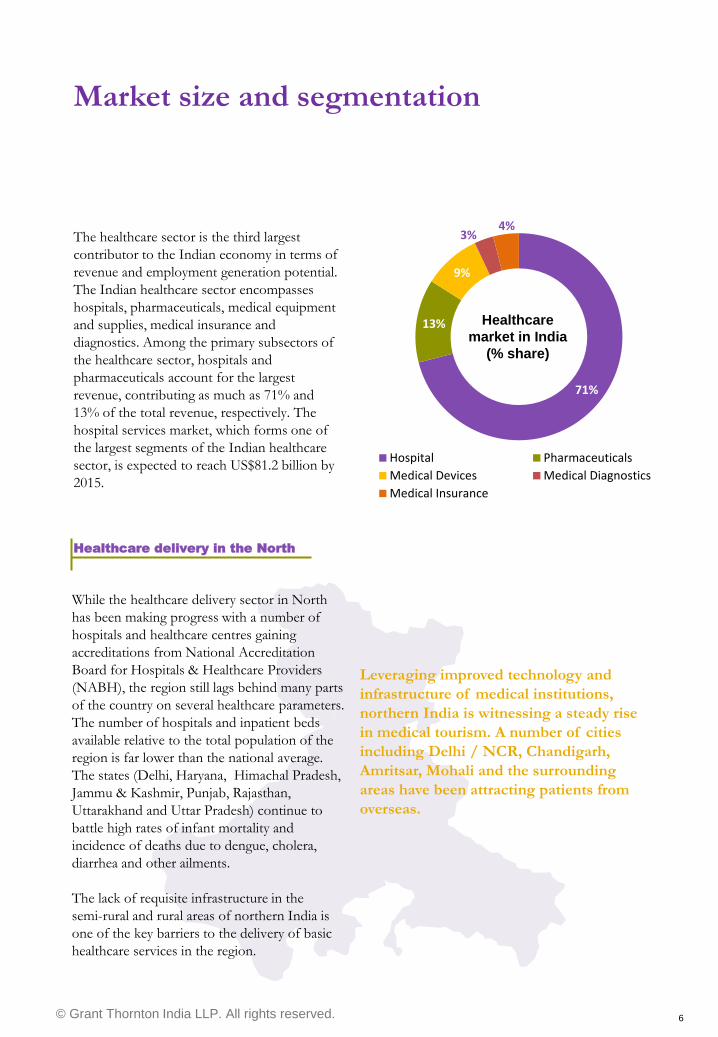

While the healthcare delivery sector in North

has been making progress with a number of

hospitals and healthcare centres gaining

accreditations from National Accreditation

Board for Hospitals & Healthcare Providers

(NABH), the region still lags behind many parts

of the country on several healthcare parameters.

The number of hospitals and inpatient beds

available relative to the total population of the

region is far lower than the national average.

The states (Delhi, Haryana, Himachal Pradesh,

Jammu & Kashmir, Punjab, Rajasthan,

Uttarakhand and Uttar Pradesh) continue to

battle high rates of infant mortality and

incidence of deaths due to dengue, cholera,

diarrhea and other ailments.

The lack of requisite infrastructure in the

semi-rural and rural areas of northern India is

one of the key barriers to the delivery of basic

healthcare services in the region.

Market size and segmentation

The healthcare sector is the third largest

contributor to the Indian economy in terms of

revenue and employment generation potential.

The Indian healthcare sector encompasses

hospitals, pharmaceuticals, medical equipment

and supplies, medical insurance and

diagnostics. Among the primary subsectors of

the healthcare sector, hospitals and

pharmaceuticals account for the largest

revenue, contributing as much as 71% and

13% of the total revenue, respectively. The

hospital services market, which forms one of

the largest segments of the Indian healthcare

sector, is expected to reach US$81.2 billion by

2015.

Leveraging improved technology and

infrastructure of medical institutions,

northern India is witnessing a steady rise

in medical tourism. A number of cities

including Delhi / NCR, Chandigarh,

Amritsar, Mohali and the surrounding

areas have been attracting patients from

overseas.

Healthcare delivery in the North

71%

13%

9%

3% 4%

Hospital Pharmaceuticals

Medical Devices Medical Diagnostics

Medical Insurance

Healthcare

market in India

(% share)

© Grant Thornton India LLP. All rights reserved. 7

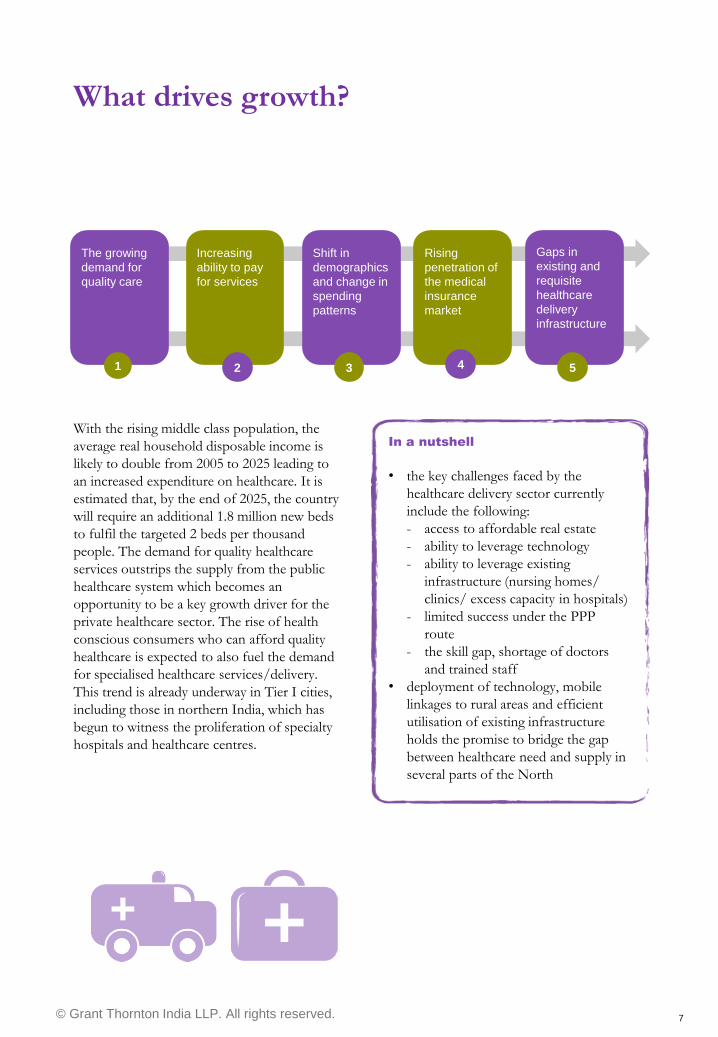

What drives growth?

With the rising middle class population, the

average real household disposable income is

likely to double from 2005 to 2025 leading to

an increased expenditure on healthcare. It is

estimated that, by the end of 2025, the country

will require an additional 1.8 million new beds

to fulfil the targeted 2 beds per thousand

people. The demand for quality healthcare

services outstrips the supply from the public

healthcare system which becomes an

opportunity to be a key growth driver for the

private healthcare sector. The rise of health

conscious consumers who can afford quality

healthcare is expected to also fuel the demand

for specialised healthcare services/delivery.

This trend is already underway in Tier I cities,

including those in northern India, which has

begun to witness the proliferation of specialty

hospitals and healthcare centres.

The growing

demand for

quality care

Shift in

demographics

and change in

spending

patterns

Increasing

ability to pay

for services

Rising

penetration of

the medical

insurance

market

Gaps in

existing and

requisite

healthcare

delivery

infrastructure

1

. 2 3 4 5

In a nutshell

• the key challenges faced by the

healthcare delivery sector currently

include the following:

- access to affordable real estate

- ability to leverage technology

- ability to leverage existing

infrastructure (nursing homes/

clinics/ excess capacity in hospitals)

- limited success under the PPP

route

- the skill gap, shortage of doctors

and trained staff

• deployment of technology, mobile

linkages to rural areas and efficient

utilisation of existing infrastructure

holds the promise to bridge the gap

between healthcare need and supply in

several parts of the North

© Grant Thornton India LLP. All rights reserved. 8

Recent policy initiatives

To increase access and utilisation of quality

health services by the rural population, the

Central Government launched the National

Rural Health Mission (NRHM) in April 2005.

NRHM has helped upgrade health

infrastructure, improve manpower availability

and skills of healthcare service providers and

improve accessibility of drugs and diagnostics

and service delivery in the rural areas. The

Centre is also planning to launch the National

Urban Health Mission (NUHM), which will

focus on slums and urban poor. NUHM will

cover all cities and towns with a population of

more than 50,000. The scheme will cover

over 779 Indian cities and towns, as well as

several Tier I cities.

As a part of NRHM, Government of India's

Ministry of Health and Family Welfare

(MoHFW) has instituted Accredited Social

Health Activists (ASHAs). The initiative

entails the provision of a trained female

community health activist in every village in

the country. The female community health

activist is a representative of the village and

works as an interface between the community

and the public health system.

To-do’s

• efficiently utilise current infrastructure, before allowing for more

• link ASHA‟s to the nearest facilities, provide infrastructure and financial support

• mobile healthcare units to form the link between the interiors and the nearest facility

• rural public infrastructure must remain at the forefront of healthcare policies

• preferential land allotment/ subsidies where there is infrastructure gap

• cutting down the risk of deaths in maternal and perinatal conditions

• increase public health spending

• streamline drug purchase stocking distribution arrangements

• low-cost day care surgery models at government hospitals

• continued focus on development of medical colleges and institutions

© Grant Thornton India LLP. All rights reserved. 9

Healthcare delivery Key players, operating models and recent trends

© Grant Thornton India LLP. All rights reserved. 10

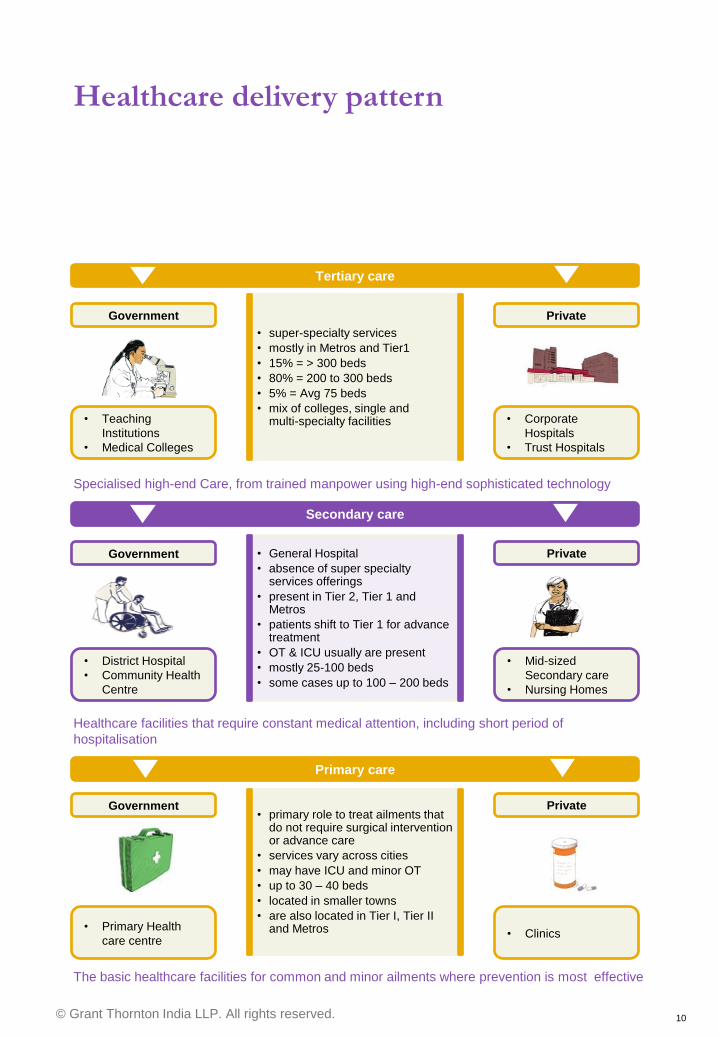

Healthcare delivery pattern

• General Hospital

• absence of super specialty services offerings

• present in Tier 2, Tier 1 and Metros

• patients shift to Tier 1 for advance treatment

• OT & ICU usually are present

• mostly 25-100 beds

• some cases up to 100 – 200 beds

Tertiary care

Government

• Teaching

Institutions

• Medical Colleges

Private

• Corporate

Hospitals

• Trust Hospitals

Specialised high-end Care, from trained manpower using high-end sophisticated technology

Secondary care

Government

• District Hospital

• Community Health

Centre

Private

• Mid-sized

Secondary care

• Nursing Homes

Healthcare facilities that require constant medical attention, including short period of

hospitalisation

The basic healthcare facilities for common and minor ailments where prevention is most effective

Primary care

Government

• Primary Health

care centre

Private

• Clinics

• super-specialty services

• mostly in Metros and Tier1

• 15% = > 300 beds

• 80% = 200 to 300 beds

• 5% = Avg 75 beds

• mix of colleges, single and multi-specialty facilities

• primary role to treat ailments that do not require surgical intervention or advance care

• services vary across cities

• may have ICU and minor OT

• up to 30 – 40 beds

• located in smaller towns

• are also located in Tier I, Tier II and Metros

© Grant Thornton India LLP. All rights reserved. 11

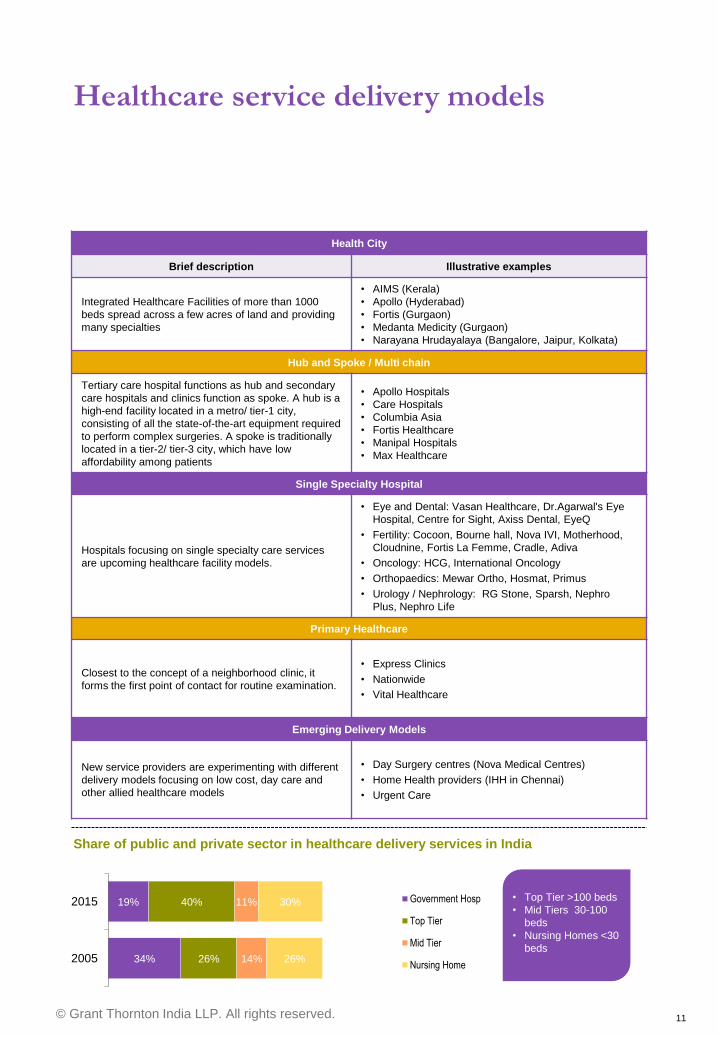

Healthcare service delivery models

Health City

Brief description Illustrative examples

Integrated Healthcare Facilities of more than 1000

beds spread across a few acres of land and providing

many specialties

• AIMS (Kerala)

• Apollo (Hyderabad)

• Fortis (Gurgaon)

• Medanta Medicity (Gurgaon)

• Narayana Hrudayalaya (Bangalore, Jaipur, Kolkata)

Hub and Spoke / Multi chain

Tertiary care hospital functions as hub and secondary

care hospitals and clinics function as spoke. A hub is a

high-end facility located in a metro/ tier-1 city,

consisting of all the state-of-the-art equipment required

to perform complex surgeries. A spoke is traditionally

located in a tier-2/ tier-3 city, which have low

affordability among patients

• Apollo Hospitals

• Care Hospitals

• Columbia Asia

• Fortis Healthcare

• Manipal Hospitals

• Max Healthcare

Single Specialty Hospital

Hospitals focusing on single specialty care services

are upcoming healthcare facility models.

• Eye and Dental: Vasan Healthcare, Dr.Agarwal's Eye

Hospital, Centre for Sight, Axiss Dental, EyeQ

• Fertility: Cocoon, Bourne hall, Nova IVI, Motherhood,

Cloudnine, Fortis La Femme, Cradle, Adiva

• Oncology: HCG, International Oncology

• Orthopaedics: Mewar Ortho, Hosmat, Primus

• Urology / Nephrology: RG Stone, Sparsh, Nephro

Plus, Nephro Life

Primary Healthcare

Closest to the concept of a neighborhood clinic, it

forms the first point of contact for routine examination.

• Express Clinics

• Nationwide

• Vital Healthcare

Emerging Delivery Models

New service providers are experimenting with different

delivery models focusing on low cost, day care and

other allied healthcare models

• Day Surgery centres (Nova Medical Centres)

• Home Health providers (IHH in Chennai)

• Urgent Care

34%

19%

26%

40%

14%

11%

26%

30%

2005

2015 Government Hosp

Top Tier

Mid Tier

Nursing Home

• Top Tier >100 beds

• Mid Tiers 30-100

beds

• Nursing Homes <30

beds

Share of public and private sector in healthcare delivery services in India

© Grant Thornton India LLP. All rights reserved. 12

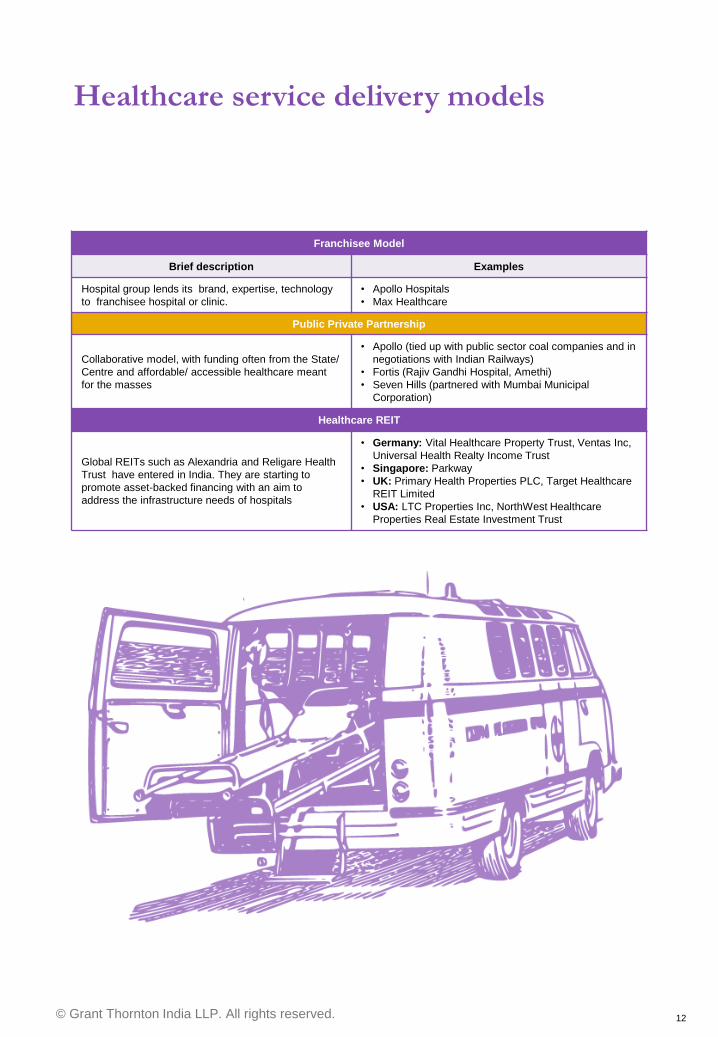

Franchisee Model

Brief description Examples

Hospital group lends its brand, expertise, technology

to franchisee hospital or clinic.

• Apollo Hospitals

• Max Healthcare

Public Private Partnership

Collaborative model, with funding often from the State/

Centre and affordable/ accessible healthcare meant

for the masses

• Apollo (tied up with public sector coal companies and in

negotiations with Indian Railways)

• Fortis (Rajiv Gandhi Hospital, Amethi)

• Seven Hills (partnered with Mumbai Municipal

Corporation)

Healthcare REIT

Global REITs such as Alexandria and Religare Health

Trust have entered in India. They are starting to

promote asset-backed financing with an aim to

address the infrastructure needs of hospitals

• Germany: Vital Healthcare Property Trust, Ventas Inc,

Universal Health Realty Income Trust

• Singapore: Parkway

• UK: Primary Health Properties PLC, Target Healthcare

REIT Limited

• USA: LTC Properties Inc, NorthWest Healthcare

Properties Real Estate Investment Trust

Healthcare service delivery models

Top Tier >100 beds

Mid Tiers 30-100

beds

Nursing Homes <30

beds

Top Tier >100 beds

Mid Tiers 30-100

beds

Nursing Homes <30

beds

© Grant Thornton India LLP. All rights reserved. 13

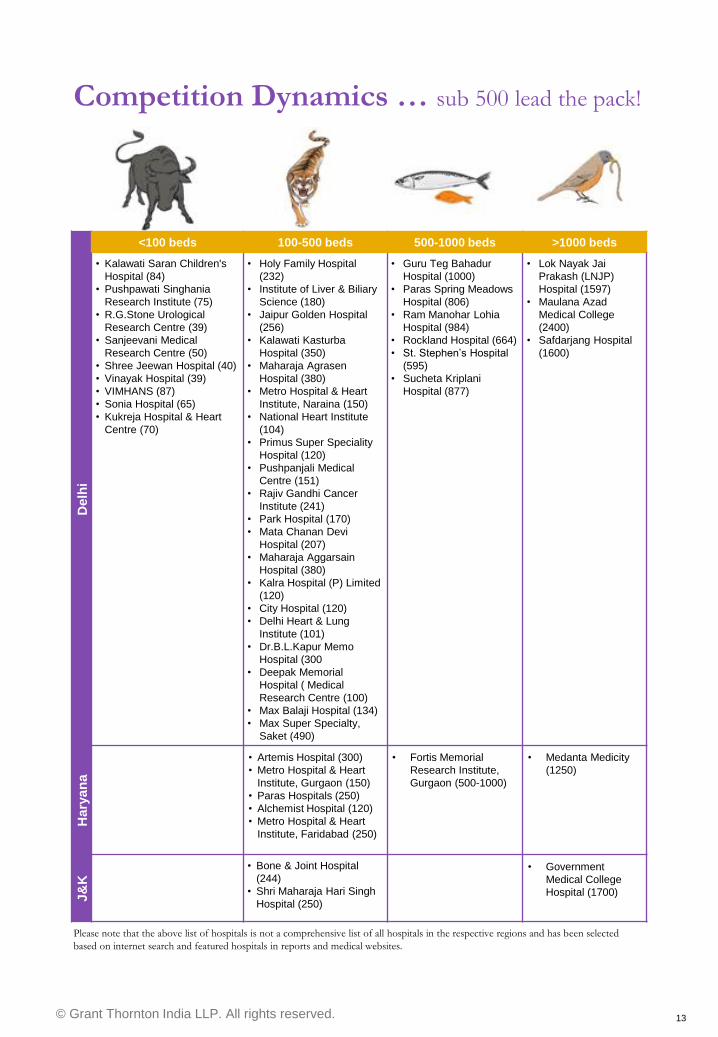

Competition Dynamics … sub 500 lead the pack!

<100 beds 100-500 beds 500-1000 beds >1000 beds

Delh

i

• Kalawati Saran Children's

Hospital (84)

• Pushpawati Singhania

Research Institute (75)

• R.G.Stone Urological

Research Centre (39)

• Sanjeevani Medical

Research Centre (50)

• Shree Jeewan Hospital (40)

• Vinayak Hospital (39)

• VIMHANS (87)

• Sonia Hospital (65)

• Kukreja Hospital & Heart

Centre (70)

• Holy Family Hospital

(232)

• Institute of Liver & Biliary

Science (180)

• Jaipur Golden Hospital

(256)

• Kalawati Kasturba

Hospital (350)

• Maharaja Agrasen

Hospital (380)

• Metro Hospital & Heart

Institute, Naraina (150)

• National Heart Institute

(104)

• Primus Super Speciality

Hospital (120)

• Pushpanjali Medical

Centre (151)

• Rajiv Gandhi Cancer

Institute (241)

• Park Hospital (170)

• Mata Chanan Devi

Hospital (207)

• Maharaja Aggarsain

Hospital (380)

• Kalra Hospital (P) Limited

(120)

• City Hospital (120)

• Delhi Heart & Lung

Institute (101)

• Dr.B.L.Kapur Memo

Hospital (300

• Deepak Memorial

Hospital ( Medical

Research Centre (100)

• Max Balaji Hospital (134)

• Max Super Specialty,

Saket (490)

• Guru Teg Bahadur

Hospital (1000)

• Paras Spring Meadows

Hospital (806)

• Ram Manohar Lohia

Hospital (984)

• Rockland Hospital (664)

• St. Stephen‟s Hospital

(595)

• Sucheta Kriplani

Hospital (877)

• Lok Nayak Jai

Prakash (LNJP)

Hospital (1597)

• Maulana Azad

Medical College

(2400)

• Safdarjang Hospital

(1600)

Hary

an

a

• Artemis Hospital (300)

• Metro Hospital & Heart

Institute, Gurgaon (150)

• Paras Hospitals (250)

• Alchemist Hospital (120)

• Metro Hospital & Heart

Institute, Faridabad (250)

• Fortis Memorial

Research Institute,

Gurgaon (500-1000)

• Medanta Medicity

(1250)

J&

K

• Bone & Joint Hospital

(244)

• Shri Maharaja Hari Singh

Hospital (250)

• Government

Medical College

Hospital (1700)

Please note that the above list of hospitals is not a comprehensive list of all hospitals in the respective regions and has been selected

based on internet search and featured hospitals in reports and medical websites.

© Grant Thornton India LLP. All rights reserved. 14

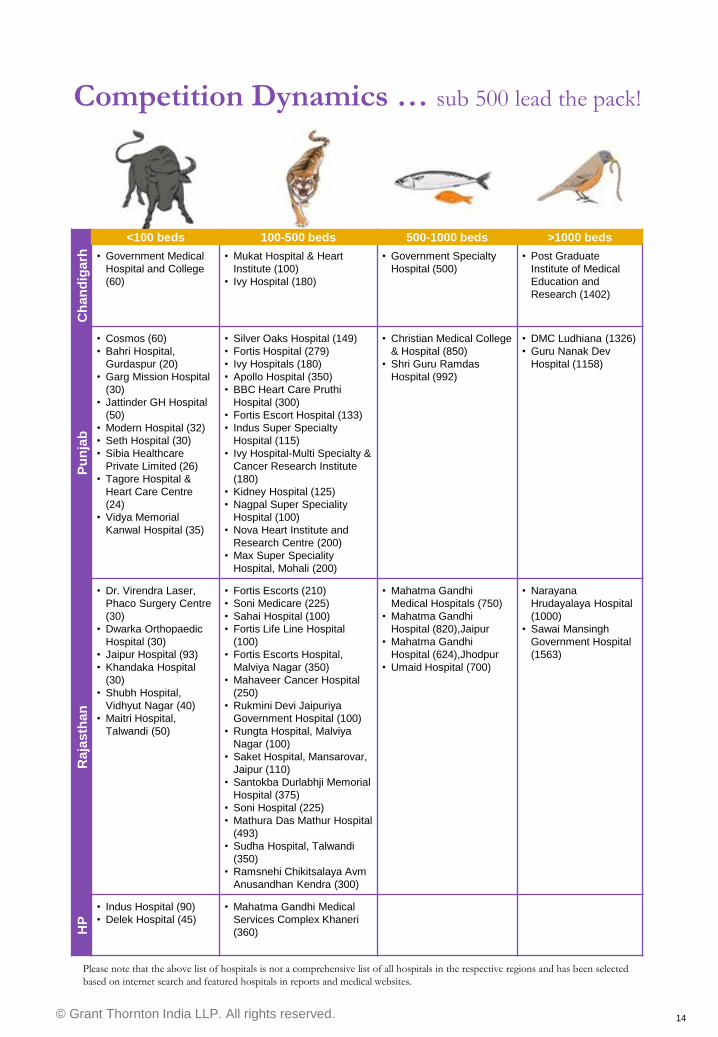

<100 beds 100-500 beds 500-1000 beds >1000 beds

Ch

an

dig

arh

• Government Medical

Hospital and College

(60)

• Mukat Hospital & Heart

Institute (100)

• Ivy Hospital (180)

• Government Specialty

Hospital (500)

• Post Graduate

Institute of Medical

Education and

Research (1402)

Pu

nja

b

• Cosmos (60)

• Bahri Hospital,

Gurdaspur (20)

• Garg Mission Hospital

(30)

• Jattinder GH Hospital

(50)

• Modern Hospital (32)

• Seth Hospital (30)

• Sibia Healthcare

Private Limited (26)

• Tagore Hospital &

Heart Care Centre

(24)

• Vidya Memorial

Kanwal Hospital (35)

• Silver Oaks Hospital (149)

• Fortis Hospital (279)

• Ivy Hospitals (180)

• Apollo Hospital (350)

• BBC Heart Care Pruthi

Hospital (300)

• Fortis Escort Hospital (133)

• Indus Super Specialty

Hospital (115)

• Ivy Hospital-Multi Specialty &

Cancer Research Institute

(180)

• Kidney Hospital (125)

• Nagpal Super Speciality

Hospital (100)

• Nova Heart Institute and

Research Centre (200)

• Max Super Speciality

Hospital, Mohali (200)

• Christian Medical College

& Hospital (850)

• Shri Guru Ramdas

Hospital (992)

• DMC Ludhiana (1326)

• Guru Nanak Dev

Hospital (1158)

Raja

sth

an

• Dr. Virendra Laser,

Phaco Surgery Centre

(30)

• Dwarka Orthopaedic

Hospital (30)

• Jaipur Hospital (93)

• Khandaka Hospital

(30)

• Shubh Hospital,

Vidhyut Nagar (40)

• Maitri Hospital,

Talwandi (50)

• Fortis Escorts (210)

• Soni Medicare (225)

• Sahai Hospital (100)

• Fortis Life Line Hospital

(100)

• Fortis Escorts Hospital,

Malviya Nagar (350)

• Mahaveer Cancer Hospital

(250)

• Rukmini Devi Jaipuriya

Government Hospital (100)

• Rungta Hospital, Malviya

Nagar (100)

• Saket Hospital, Mansarovar,

Jaipur (110)

• Santokba Durlabhji Memorial

Hospital (375)

• Soni Hospital (225)

• Mathura Das Mathur Hospital

(493)

• Sudha Hospital, Talwandi

(350)

• Ramsnehi Chikitsalaya Avm

Anusandhan Kendra (300)

• Mahatma Gandhi

Medical Hospitals (750)

• Mahatma Gandhi

Hospital (820),Jaipur

• Mahatma Gandhi

Hospital (624),Jhodpur

• Umaid Hospital (700)

• Narayana

Hrudayalaya Hospital

(1000)

• Sawai Mansingh

Government Hospital

(1563)

HP

• Indus Hospital (90)

• Delek Hospital (45)

• Mahatma Gandhi Medical

Services Complex Khaneri

(360)

Competition Dynamics … sub 500 lead the pack!

Please note that the above list of hospitals is not a comprehensive list of all hospitals in the respective regions and has been selected

based on internet search and featured hospitals in reports and medical websites.

© Grant Thornton India LLP. All rights reserved. 15

<100 beds 100-500 beds 500-1000 beds >1000 beds

Utt

ar

Pra

desh

• Sri Ram Hospital (50)

• Bhola Hospital (40)

• Heartline Cardiac Care

Hospital (50)

• Happy Family Hospital

(62)

• Jain Hospital (30)

• R K Devi Memorial

Hospital (45)

• Fortis Hospital (75)

• Asopa Hospital, Sikandra

(100)

• District Hospital (118)

• Lady Lyall Hospital, Noorie

Gate (331)

• Pushpanjali Hospital and

Research Center, Delhi

Gate (350)

• Jeevan Jyothi Multi

Speciality Hospital (400)

• Kamla Nehru Memorial

Hospital (306)

• Nazreth Hospital (300)

• Priti Hospital (108)

• Pushpanjali Crosslay

Hospital, Vaishali (400)

• Gangasheel Hospital (100)

• Shanti Gopal Hospital

(102)

• Yashoda Super Speciality

Hospital (106)

• District Hospital (172)

• Divisional Railway Hospital

(185)

• Kulwanti Hospital and

Research Center (100)

• Nirmal Hospital (150)

• Chandani Hospital (152)

• Mariampur Hospital (194)

• Regency Hospital Limited

(225)

• Ajanta Hospital (100)

• Awadh Hospital (102)

• Chhatrapati Shahuji

Maharaj Medical University

(226)

• Mayo Hospital (300)

• Neera Hospital (160)

• Kailash Hospital & Heart

Institute (325)

• Vinayak Hospital (150)

• Kailash Hospital & Heart

Institute (325)

• Vinayak Hospital (150)

• Institute of Mental Health

and Hospital, Billochpura

(838)

• Sarojini Naidu Medical

College (976)

• Moti Lal Nehru Hospital

(1000)

• District Deen Dayal

Upadhayay Hospital

(500)

• Jawaharlal Nehru

Medical College, A.M.U

(1000)

• Jeevan Jyoti Hospital

(500)

• MLB Medical College

and Hospital (700)

• Command Hospital (544)

• Ram Raghu Hospital

(1047)

• LLR Hospital (1615)

Competition Dynamics … sub 500 lead the pack!

Please note that the above list of hospitals is not a comprehensive list of all hospitals in the respective regions and has been selected

based on internet search and featured hospitals in reports and medical websites.

© Grant Thornton India LLP. All rights reserved. 16

Industry speak

“We need to re-write the blueprint for

Health India…

All three segments (public health

systems, NGOs and private sector)

should be aligned to make a full chain

from ground up…

We have a mass enabler already – in

the form of ASHA - upgrade their

skills, provide access to technology,

clearly define the functionalities, use

mobile units for connectivity to B&C

cities and a national network will be

in place”

Dr Naresh Trehan

Medanta Medicity, envisioned as a

health city, has changed the face of

surgery in India across multiple

specialties.

Dr Amit Sachdeva

Axiss Dental is currently a North

India focused chain of dental

centres providing orthodontic and

implantology solutions. The

chain has recently secured

private equity funding from India

Equity Partners.

Dr Manish Chhaparwal

Mewar Ortho provides high quality,

fast turnaround care for patients in Tier

II cities, where there is a dearth of

orthopaedic and allied care facilities.

Mewar has recently completed its first

institutional round of equity funding

from Matrix Partners.

“We aim to keep our capital and

operating costs low and operate our

centres in an environment of patient

centricity –quality surgeries, quick

discharge, technology advancement

and safe infrastructure”

© Grant Thornton India LLP. All rights reserved. 17

Healthcare infrastructure Public health, disease profiles, mortality

rates

© Grant Thornton India LLP. All rights reserved. 18

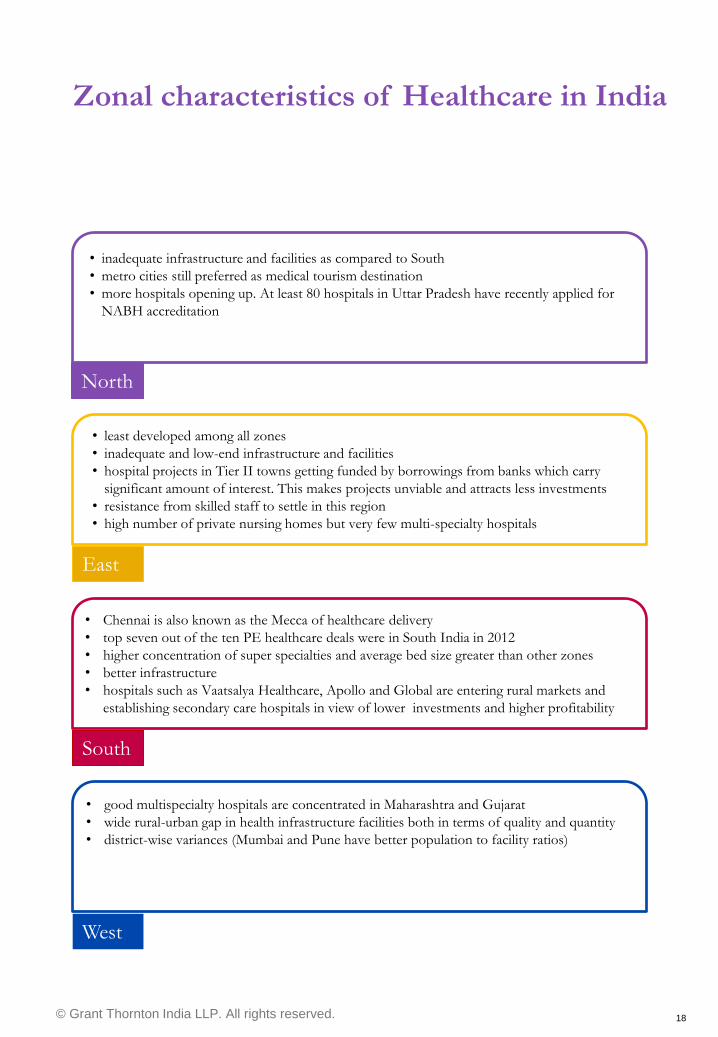

North

• inadequate infrastructure and facilities as compared to South

• metro cities still preferred as medical tourism destination

• more hospitals opening up. At least 80 hospitals in Uttar Pradesh have recently applied for

NABH accreditation

East

• least developed among all zones

• inadequate and low-end infrastructure and facilities

• hospital projects in Tier II towns getting funded by borrowings from banks which carry

significant amount of interest. This makes projects unviable and attracts less investments

• resistance from skilled staff to settle in this region

• high number of private nursing homes but very few multi-specialty hospitals

South

• Chennai is also known as the Mecca of healthcare delivery

• top seven out of the ten PE healthcare deals were in South India in 2012

• higher concentration of super specialties and average bed size greater than other zones

• better infrastructure

• hospitals such as Vaatsalya Healthcare, Apollo and Global are entering rural markets and

establishing secondary care hospitals in view of lower investments and higher profitability

West

• good multispecialty hospitals are concentrated in Maharashtra and Gujarat

• wide rural-urban gap in health infrastructure facilities both in terms of quality and quantity

• district-wise variances (Mumbai and Pune have better population to facility ratios)

Zonal characteristics of Healthcare in India

© Grant Thornton India LLP. All rights reserved. 19

Population: 12,548,926

Doctors: 11,200

Population served per doctor:

1120

IMR: Rural – 43 (M), 47 (F);

Urban – 28 (M), 37 (F)

MMR (2007-09): N/A

Population: 6,856,509

Doctors: 800

Population served per

doctor: 8571

IMR: N/A

MMR (2007-09): N/A

Population: 27,704,236

Doctors: 38,400

Population served per

doctor: 721

IMR: Rural – 36 (M), 39

(F); Urban – 27 (M), 29 (F)

MMR (2007-09): 172

Population: 25,353,081

Doctors: 4100

Population served per doctor

6184

IMR: Rural – 51 (M), 52 (F);

Urban – 35 (M), 42 (F)

MMR (2007-09): 153

Population: 68,621,012

Doctors: 28500

Population served per

doctor 2408

IMR: Rural – 58 (M), 64

(F); Urban – 29 (M), 34 (F)

MMR (2007-09): 318

Population: 16,753,235

Doctors: 46800

Population served per

doctor: 358

IMR: Rural – 32 (M), 42

(F); Urban – 29 (M), 29 (F)

MMR (2007-09): N/A

Population: 10,116,752

Doctors: 3300

Population served per doctor

3066

IMR: N/A

MMR (2007-09): N/A

Population: 199,581,477

Doctors: 57900

Population served per

doctor 3477

IMR: Rural – 61 (M), 67 (F);

Urban – 44 (M), 45 (F)

MMR (2007-09): 359

1 2 3

4 5 6

7 8

Source: Ministry of Health & Family Welfare and National Health Profile, 2011, Medical Council of India (MCI), Press Information

Bureau, Figures of Medical Practioners are related to doctors registered with State Medical Councils.

J&K

Rajasthan UP

Himachal

Pradesh

Punjab

Haryana

Uttarakhand

Delhi

1

2 3

4

5

6

7

8

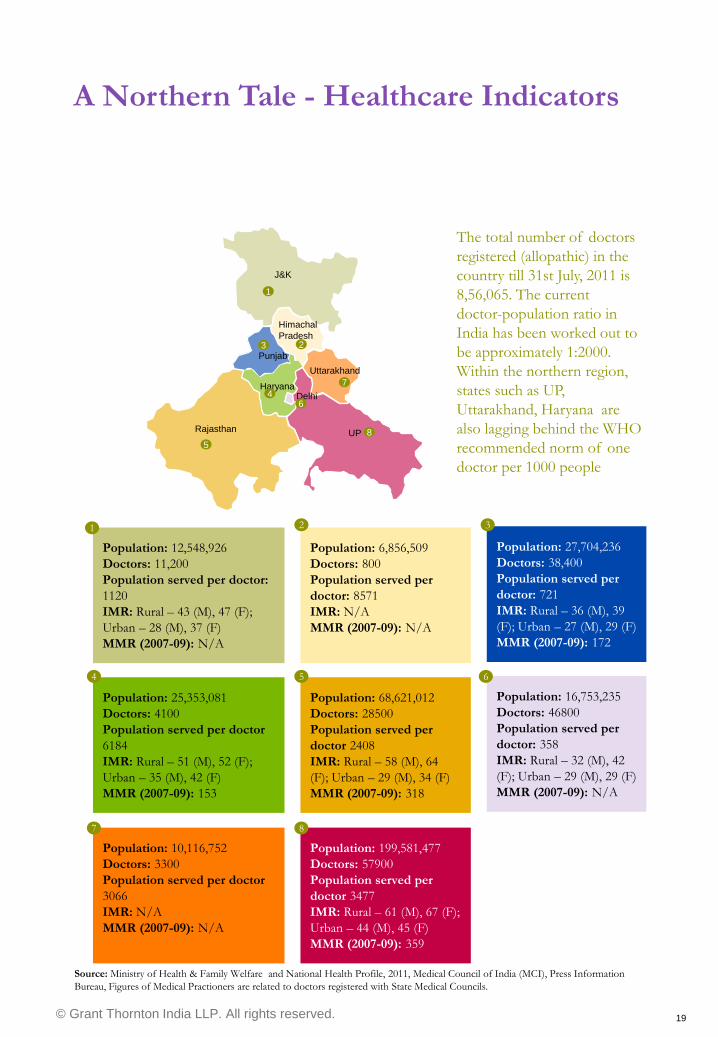

The total number of doctors

registered (allopathic) in the

country till 31st July, 2011 is

8,56,065. The current

doctor-population ratio in

India has been worked out to

be approximately 1:2000.

Within the northern region,

states such as UP,

Uttarakhand, Haryana are

also lagging behind the WHO

recommended norm of one

doctor per 1000 people

A Northern Tale - Healthcare Indicators

© Grant Thornton India LLP. All rights reserved. 20

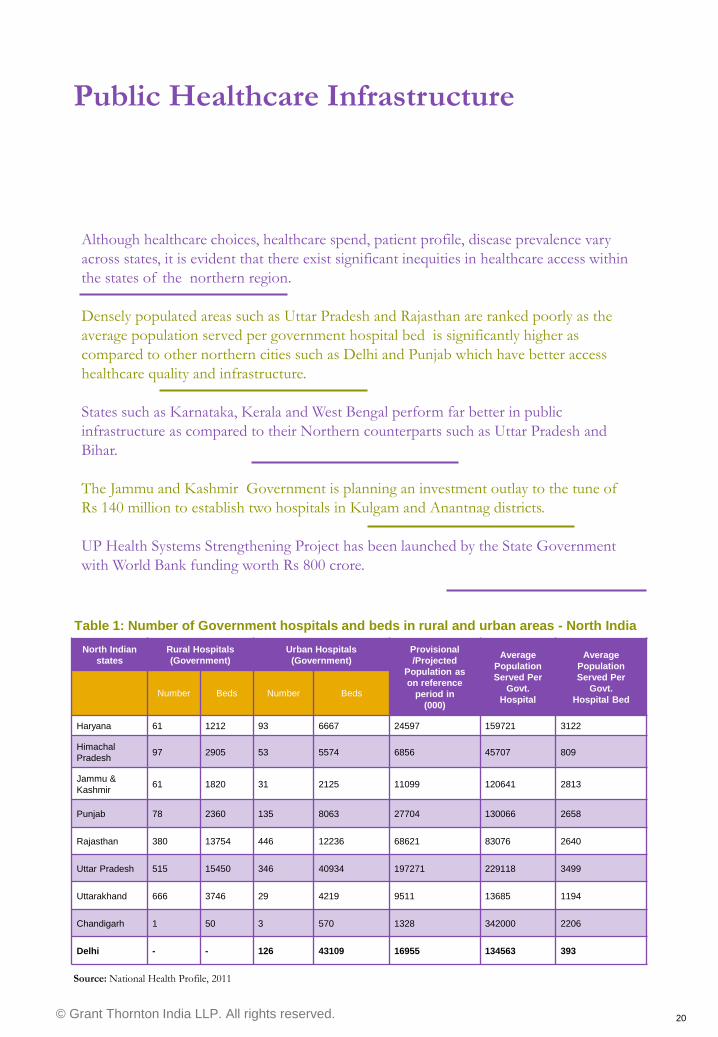

Table 1: Number of Government hospitals and beds in rural and urban areas - North India

North Indian

states

Rural Hospitals

(Government)

Urban Hospitals

(Government)

Provisional

/Projected

Population as

on reference

period in

(000)

Average

Population

Served Per

Govt.

Hospital

Average

Population

Served Per

Govt.

Hospital Bed Number Beds Number Beds

Haryana 61 1212 93 6667 24597 159721 3122

Himachal

Pradesh 97 2905 53 5574 6856 45707 809

Jammu &

Kashmir 61 1820 31 2125 11099 120641 2813

Punjab 78 2360 135 8063 27704 130066 2658

Rajasthan 380 13754 446 12236 68621 83076 2640

Uttar Pradesh 515 15450 346 40934 197271 229118 3499

Uttarakhand 666 3746 29 4219 9511 13685 1194

Chandigarh 1 50 3 570 1328 342000 2206

Delhi - - 126 43109 16955 134563 393

Source: National Health Profile, 2011

Although healthcare choices, healthcare spend, patient profile, disease prevalence vary

across states, it is evident that there exist significant inequities in healthcare access within

the states of the northern region.

Densely populated areas such as Uttar Pradesh and Rajasthan are ranked poorly as the

average population served per government hospital bed is significantly higher as

compared to other northern cities such as Delhi and Punjab which have better access

healthcare quality and infrastructure.

States such as Karnataka, Kerala and West Bengal perform far better in public

infrastructure as compared to their Northern counterparts such as Uttar Pradesh and

Bihar.

The Jammu and Kashmir Government is planning an investment outlay to the tune of

Rs 140 million to establish two hospitals in Kulgam and Anantnag districts.

UP Health Systems Strengthening Project has been launched by the State Government

with World Bank funding worth Rs 800 crore.

Public Healthcare Infrastructure

© Grant Thornton India LLP. All rights reserved. 21

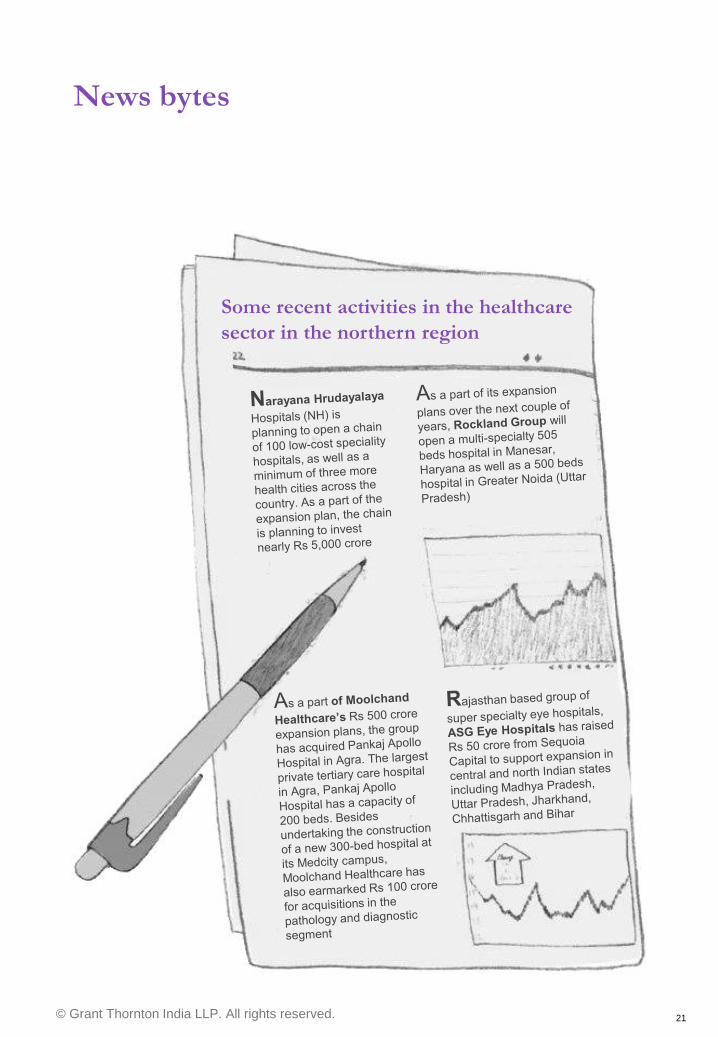

Some recent activities in the healthcare

sector in the northern region

News bytes

© Grant Thornton India LLP. All rights reserved. 22

Fortis Healthcare (India)

plans to launch four

hospitals including one in

Himachal Pradesh to be

operational by 2013, as

part of its plans to

strengthen its nationwide

presence.

Immediate expansion plans

for Mewar Ortho include

setting up a 100–bed

centre of excellence in

Udaipur while also

increasing its footprint in

Central India with centres

in Sirohi, Mandsaur,

Chittorgarh and several

more.

ASG Eye Hospitals, a

Rajasthan based group of

super specialty eye

hospitals has recently

raised Rs 50 crore from

Sequoia Capital. The fund

will support the expansion

plan of the hospital

Metropolis Healthcare has

made investments of Rs

one crore each in Tier II

and Tier III cities such as

Lucknow, Bareilly, and

Jalandhar and has recently

acquired two brownfield

ventures in Chandigarh

and Jodhpur.

Apollo Hospitals Group

launched its first Apollo

Cosmetic Clinic in North

India.

As a part of its expansion

plans over the next couple

of years, Rockland Group

will open a multi-specialty

505 beds hospital in

Manesar, Haryana as well

as a 500 beds hospital in

Greater Noida (Uttar

Pradesh)

Rajasthan based group of

super specialty eye

hospitals, ASG Eye

Hospitals has raised Rs 50

crore from Sequoia Capital

to support expansion in

central and north Indian

states including Madhya

Pradesh, Uttar Pradesh,

Jharkhand, Chhattisgarh

and Bihar

Besides undertaking the

construction of a new 300-

bed hospital at its Medcity

campus, Moolchand

Healthcare has also

earmarked Rs 100 crore

for acquisitions in the

pathology and diagnostic

segment

News bytes

Some recent activities in the healthcare sector in the northern region

© Grant Thornton India LLP. All rights reserved. 23

Investment Horizon Deal trends, options – public and private route

© Grant Thornton India LLP. All rights reserved. 24

Private Funding Options

Establishing and growing a hospital business requires intensive planning and large capital outlay,

which makes it imperative for players to pursue new avenues to meet their capital needs.

2 Capital

Markets

Depends

entirely on

market

conditions,

not easy for

mid-cap

companies

Mezz/ Debt

High fixed

cost,

restrictions

on deal

structures

due to FDI

regulations,

limited

number of

providers

Private

Equity

Growth

Capital –

Most active

in today's

market

Overseas

Listing

Depends on

market

conditions

REIT

Limited

number of

operators,

restrictions

on deal

structures

due to FDI

regulations

1 3 4 5 Angel

Investors

For very

early stage

deals, there

is usually no

other option

6

© Grant Thornton India LLP. All rights reserved. 25

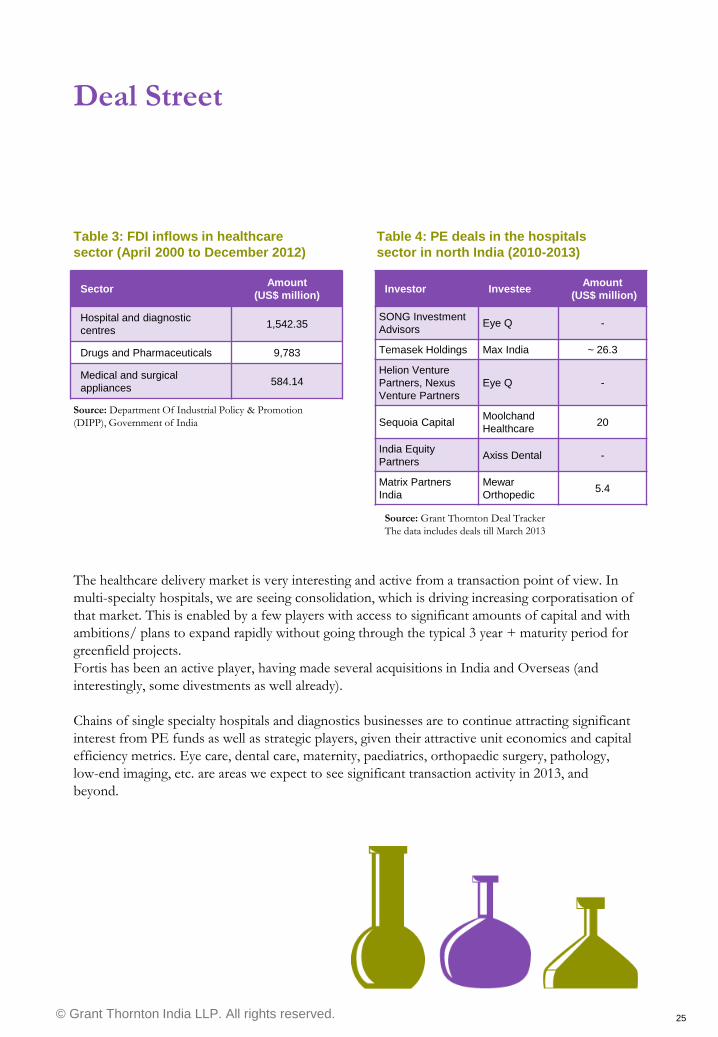

Deal Street

The healthcare delivery market is very interesting and active from a transaction point of view. In

multi-specialty hospitals, we are seeing consolidation, which is driving increasing corporatisation of

that market. This is enabled by a few players with access to significant amounts of capital and with

ambitions/ plans to expand rapidly without going through the typical 3 year + maturity period for

greenfield projects.

Fortis has been an active player, having made several acquisitions in India and Overseas (and

interestingly, some divestments as well already).

Chains of single specialty hospitals and diagnostics businesses are to continue attracting significant

interest from PE funds as well as strategic players, given their attractive unit economics and capital

efficiency metrics. Eye care, dental care, maternity, paediatrics, orthopaedic surgery, pathology,

low-end imaging, etc. are areas we expect to see significant transaction activity in 2013, and

beyond.

Investor Investee Amount

(US$ million)

SONG Investment

Advisors Eye Q -

Temasek Holdings Max India ~ 26.3

Helion Venture

Partners, Nexus

Venture Partners

Eye Q -

Sequoia Capital Moolchand

Healthcare 20

India Equity

Partners Axiss Dental -

Matrix Partners

India

Mewar

Orthopedic 5.4

Source: Grant Thornton Deal Tracker

The data includes deals till March 2013

Table 4: PE deals in the hospitals

sector in north India (2010-2013)

Sector Amount

(US$ million)

Hospital and diagnostic

centres 1,542.35

Drugs and Pharmaceuticals 9,783

Medical and surgical

appliances 584.14

Table 3: FDI inflows in healthcare

sector (April 2000 to December 2012)

Source: Department Of Industrial Policy & Promotion

(DIPP), Government of India

© Grant Thornton India LLP. All rights reserved. 26

Policy Initiatives

National Health Mission (NHM)

Creation of a new integrated NHM

with an allocation of Rs 21,239

crores

National Program for Healthcare of Elderly

Allocation of Rs 150 Crores to National

Programme for the Health Care of Elderly

(implemented in 100 selected districts of 21

States)

Rashtriya Swasthiya Bima Yojana

Health insurance covers under extended

to include rickshaw pullers, taxi drivers,

sanitation workers, rag pickers and mine

workers

Infrastructure Development

Intends to enhance its investment

outlay in the infrastructure development

to over Rs 46.74 trillion during the next

five years

Medical Education

To improve medical education, training and

research Rs 4,727 Crores has been

allocated. Additional funding of Rs 1,650

Crores provided to AIIMS-like institutions

commissioned in September 2012 for

developmental activities

Tax Initiatives

Subsection (11C) in Section 80-IB, the

Government is granting Tax Holiday to

hospitals starting their operations in rural

belts between 01 April 2008 to 31 March

2013

Union Budget 2013-2014

© Grant Thornton India LLP. All rights reserved. 27

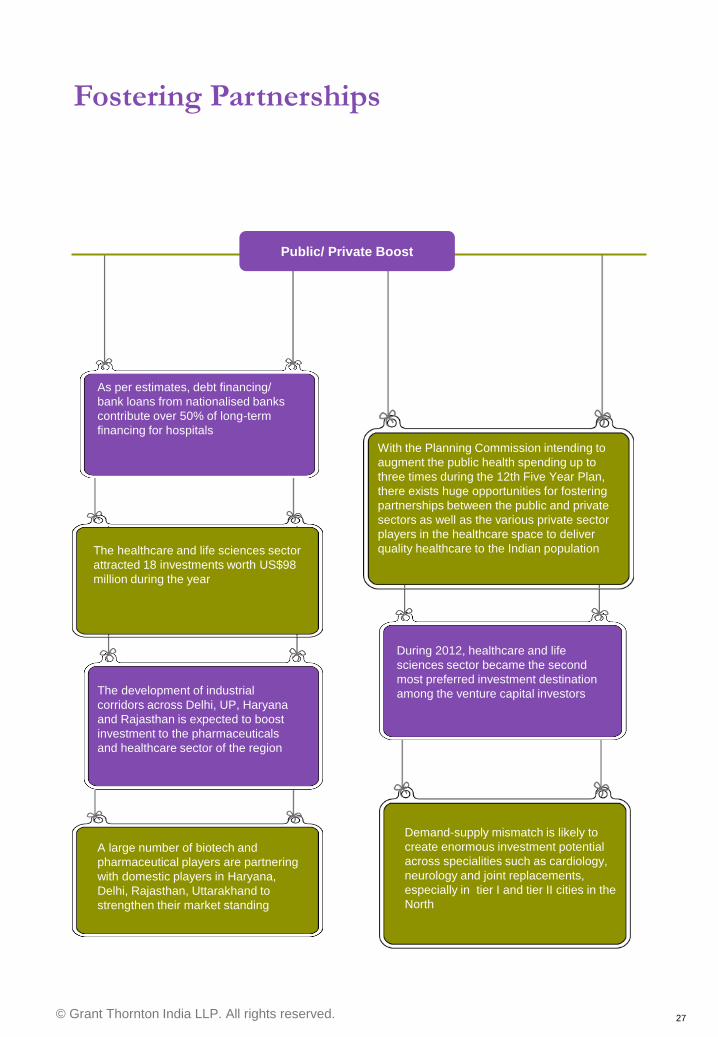

Fostering Partnerships

As per estimates, debt financing/

bank loans from nationalised banks

contribute over 50% of long-term

financing for hospitals

With the Planning Commission intending to

augment the public health spending up to

three times during the 12th Five Year Plan,

there exists huge opportunities for fostering

partnerships between the public and private

sectors as well as the various private sector

players in the healthcare space to deliver

quality healthcare to the Indian population

During 2012, healthcare and life

sciences sector became the second

most preferred investment destination

among the venture capital investors

The healthcare and life sciences sector

attracted 18 investments worth US$98

million during the year

The development of industrial

corridors across Delhi, UP, Haryana

and Rajasthan is expected to boost

investment to the pharmaceuticals

and healthcare sector of the region

A large number of biotech and

pharmaceutical players are partnering

with domestic players in Haryana,

Delhi, Rajasthan, Uttarakhand to

strengthen their market standing

Demand-supply mismatch is likely to

create enormous investment potential

across specialities such as cardiology,

neurology and joint replacements,

especially in tier I and tier II cities in the

North

Public/ Private Boost

© Grant Thornton India LLP. All rights reserved. 28

Changing trends Improving healthcare delivery

© Grant Thornton India LLP. All rights reserved. 29

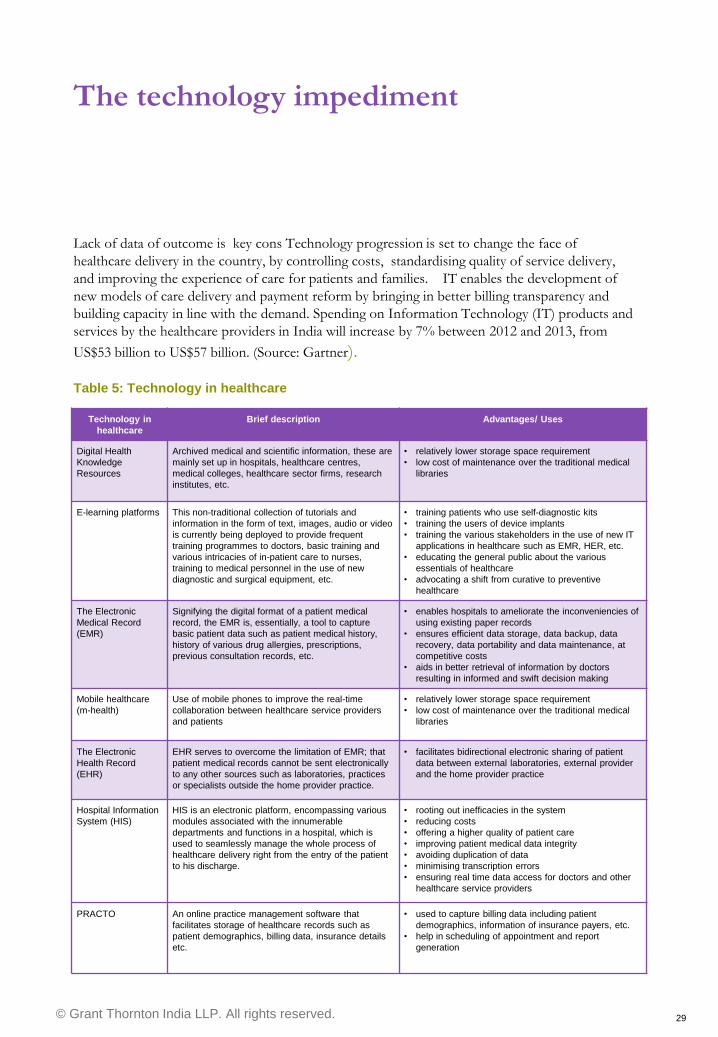

The technology impediment

Lack of data of outcome is key cons Technology progression is set to change the face of

healthcare delivery in the country, by controlling costs, standardising quality of service delivery,

and improving the experience of care for patients and families. IT enables the development of

new models of care delivery and payment reform by bringing in better billing transparency and

building capacity in line with the demand. Spending on Information Technology (IT) products and

services by the healthcare providers in India will increase by 7% between 2012 and 2013, from

US$53 billion to US$57 billion. (Source: Gartner).

Technology in

healthcare

Brief description Advantages/ Uses

Digital Health

Knowledge

Resources

Archived medical and scientific information, these are

mainly set up in hospitals, healthcare centres,

medical colleges, healthcare sector firms, research

institutes, etc.

• relatively lower storage space requirement

• low cost of maintenance over the traditional medical

libraries

E-learning platforms This non-traditional collection of tutorials and

information in the form of text, images, audio or video

is currently being deployed to provide frequent

training programmes to doctors, basic training and

various intricacies of in-patient care to nurses,

training to medical personnel in the use of new

diagnostic and surgical equipment, etc.

• training patients who use self-diagnostic kits

• training the users of device implants

• training the various stakeholders in the use of new IT

applications in healthcare such as EMR, HER, etc.

• educating the general public about the various

essentials of healthcare

• advocating a shift from curative to preventive

healthcare

The Electronic

Medical Record

(EMR)

Signifying the digital format of a patient medical

record, the EMR is, essentially, a tool to capture

basic patient data such as patient medical history,

history of various drug allergies, prescriptions,

previous consultation records, etc.

• enables hospitals to ameliorate the inconveniencies of

using existing paper records

• ensures efficient data storage, data backup, data

recovery, data portability and data maintenance, at

competitive costs

• aids in better retrieval of information by doctors

resulting in informed and swift decision making

Mobile healthcare

(m-health)

Use of mobile phones to improve the real-time

collaboration between healthcare service providers

and patients

• relatively lower storage space requirement

• low cost of maintenance over the traditional medical

libraries

The Electronic

Health Record

(EHR)

EHR serves to overcome the limitation of EMR; that

patient medical records cannot be sent electronically

to any other sources such as laboratories, practices

or specialists outside the home provider practice.

• facilitates bidirectional electronic sharing of patient

data between external laboratories, external provider

and the home provider practice

Hospital Information

System (HIS)

HIS is an electronic platform, encompassing various

modules associated with the innumerable

departments and functions in a hospital, which is

used to seamlessly manage the whole process of

healthcare delivery right from the entry of the patient

to his discharge.

• rooting out inefficacies in the system

• reducing costs

• offering a higher quality of patient care

• improving patient medical data integrity

• avoiding duplication of data

• minimising transcription errors

• ensuring real time data access for doctors and other

healthcare service providers

PRACTO An online practice management software that

facilitates storage of healthcare records such as

patient demographics, billing data, insurance details

etc.

• used to capture billing data including patient

demographics, information of insurance payers, etc.

• help in scheduling of appointment and report

generation

Table 5: Technology in healthcare

© Grant Thornton India LLP. All rights reserved. 30

Tele-docs and Tele-medicine

A novel idea implemented by

Haryana Jiva International, a

healthcare venture on the outskirts

of Delhi. It deploys a GPRS enabled

Java application to enhance the

reach of medical care to rural parts

of the region. The project, known as

the “Teledoc” project, has won

widespread acclaim globally,

including the World Summit Award

for eHealth.

Grameen Foundation has rolled

out an m-health service for AIDS

patients in India. The application

is used to send healthy living

tips, messages and reminders

regarding consultations and

medications to AIDS patients.

In a recent report for the 12th Five Year Plan, the steering committee on health has

recommended connecting all the district hospitals to tertiary care centres by telemedicine

using applications such as “Skype” which facilitate audio-visual interactions. The committee

also advocates adoption of mobile health solutions to enhance real-time collaboration

between patients and providers and between providers, improvement in the rate of

transmission of data and information between the various stakeholders and promotion for

the adoption of preventive healthcare across the various Indian states.

© Grant Thornton India LLP. All rights reserved. 31

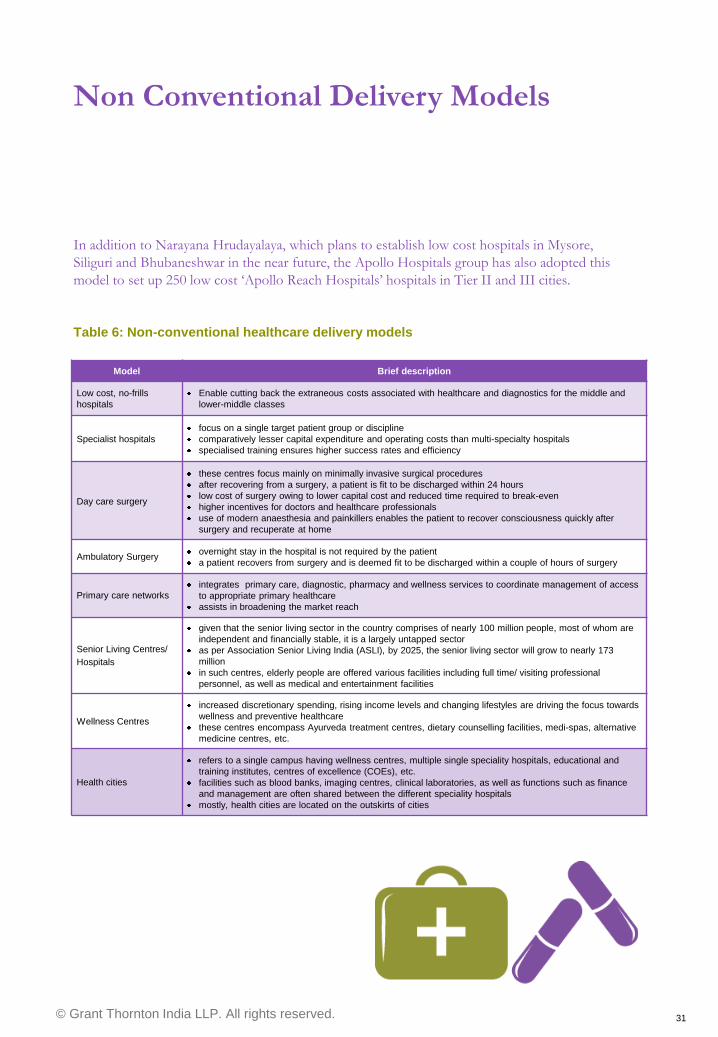

Non Conventional Delivery Models

In addition to Narayana Hrudayalaya, which plans to establish low cost hospitals in Mysore,

Siliguri and Bhubaneshwar in the near future, the Apollo Hospitals group has also adopted this

model to set up 250 low cost „Apollo Reach Hospitals‟ hospitals in Tier II and III cities.

Model Brief description

Low cost, no-frills

hospitals

Enable cutting back the extraneous costs associated with healthcare and diagnostics for the middle and

lower-middle classes

Specialist hospitals

focus on a single target patient group or discipline

comparatively lesser capital expenditure and operating costs than multi-specialty hospitals

specialised training ensures higher success rates and efficiency

Day care surgery

these centres focus mainly on minimally invasive surgical procedures

after recovering from a surgery, a patient is fit to be discharged within 24 hours

low cost of surgery owing to lower capital cost and reduced time required to break-even

higher incentives for doctors and healthcare professionals

use of modern anaesthesia and painkillers enables the patient to recover consciousness quickly after

surgery and recuperate at home

Ambulatory Surgery overnight stay in the hospital is not required by the patient

a patient recovers from surgery and is deemed fit to be discharged within a couple of hours of surgery

Primary care networks integrates primary care, diagnostic, pharmacy and wellness services to coordinate management of access

to appropriate primary healthcare

assists in broadening the market reach

Senior Living Centres/

Hospitals

given that the senior living sector in the country comprises of nearly 100 million people, most of whom are

independent and financially stable, it is a largely untapped sector

as per Association Senior Living India (ASLI), by 2025, the senior living sector will grow to nearly 173

million

in such centres, elderly people are offered various facilities including full time/ visiting professional

personnel, as well as medical and entertainment facilities

Wellness Centres

increased discretionary spending, rising income levels and changing lifestyles are driving the focus towards

wellness and preventive healthcare

these centres encompass Ayurveda treatment centres, dietary counselling facilities, medi-spas, alternative

medicine centres, etc.

Health cities

refers to a single campus having wellness centres, multiple single speciality hospitals, educational and

training institutes, centres of excellence (COEs), etc.

facilities such as blood banks, imaging centres, clinical laboratories, as well as functions such as finance

and management are often shared between the different speciality hospitals

mostly, health cities are located on the outskirts of cities

Table 6: Non-conventional healthcare delivery models

© Grant Thornton India LLP. All rights reserved. 32

Outlook Strategic recommendations

© Grant Thornton India LLP. All rights reserved. 33

Transforming Healthcare - Agenda

for action

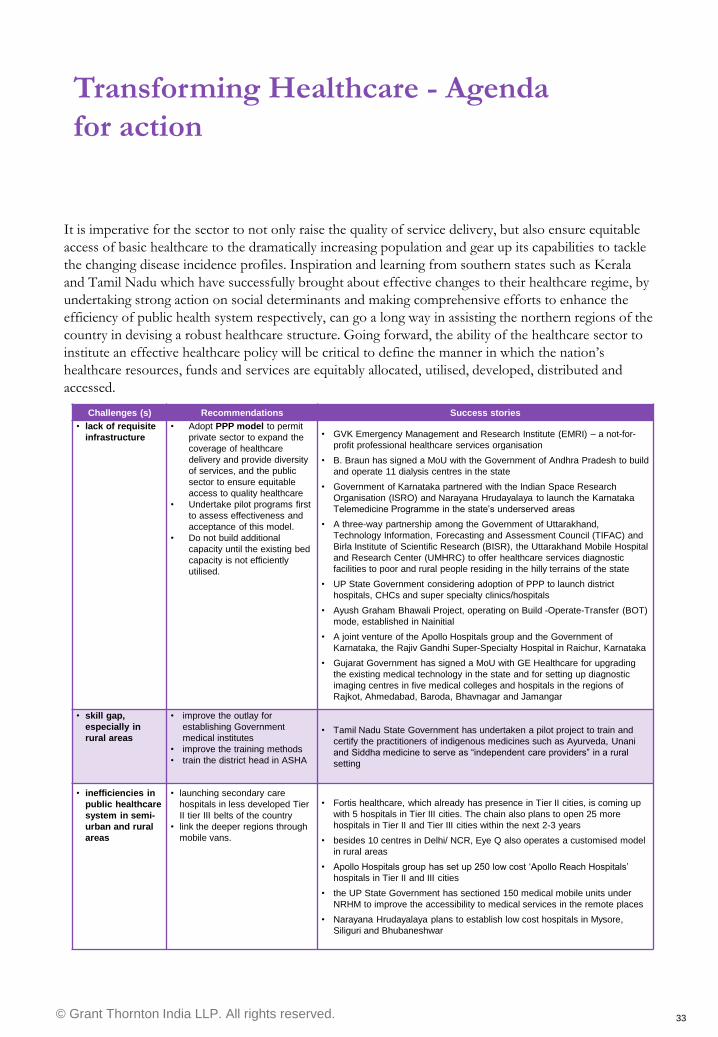

Challenges (s) Recommendations Success stories

• lack of requisite

infrastructure

• Adopt PPP model to permit

private sector to expand the

coverage of healthcare

delivery and provide diversity

of services, and the public

sector to ensure equitable

access to quality healthcare

• Undertake pilot programs first

to assess effectiveness and

acceptance of this model.

• Do not build additional

capacity until the existing bed

capacity is not efficiently

utilised.

• GVK Emergency Management and Research Institute (EMRI) – a not-for-

profit professional healthcare services organisation

• B. Braun has signed a MoU with the Government of Andhra Pradesh to build

and operate 11 dialysis centres in the state

• Government of Karnataka partnered with the Indian Space Research

Organisation (ISRO) and Narayana Hrudayalaya to launch the Karnataka

Telemedicine Programme in the state‟s underserved areas

• A three-way partnership among the Government of Uttarakhand,

Technology Information, Forecasting and Assessment Council (TIFAC) and

Birla Institute of Scientific Research (BISR), the Uttarakhand Mobile Hospital

and Research Center (UMHRC) to offer healthcare services diagnostic

facilities to poor and rural people residing in the hilly terrains of the state

• UP State Government considering adoption of PPP to launch district

hospitals, CHCs and super specialty clinics/hospitals

• Ayush Graham Bhawali Project, operating on Build -Operate-Transfer (BOT)

mode, established in Nainitial

• A joint venture of the Apollo Hospitals group and the Government of

Karnataka, the Rajiv Gandhi Super-Specialty Hospital in Raichur, Karnataka

• Gujarat Government has signed a MoU with GE Healthcare for upgrading

the existing medical technology in the state and for setting up diagnostic

imaging centres in five medical colleges and hospitals in the regions of

Rajkot, Ahmedabad, Baroda, Bhavnagar and Jamangar

• skill gap,

especially in

rural areas

• improve the outlay for

establishing Government

medical institutes

• improve the training methods

• train the district head in ASHA

• Tamil Nadu State Government has undertaken a pilot project to train and

certify the practitioners of indigenous medicines such as Ayurveda, Unani

and Siddha medicine to serve as “independent care providers” in a rural

setting

• inefficiencies in

public healthcare

system in semi-

urban and rural

areas

• launching secondary care

hospitals in less developed Tier

II tier III belts of the country

• link the deeper regions through

mobile vans.

• Fortis healthcare, which already has presence in Tier II cities, is coming up

with 5 hospitals in Tier III cities. The chain also plans to open 25 more

hospitals in Tier II and Tier III cities within the next 2-3 years

• besides 10 centres in Delhi/ NCR, Eye Q also operates a customised model

in rural areas

• Apollo Hospitals group has set up 250 low cost „Apollo Reach Hospitals‟

hospitals in Tier II and III cities

• the UP State Government has sectioned 150 medical mobile units under

NRHM to improve the accessibility to medical services in the remote places

• Narayana Hrudayalaya plans to establish low cost hospitals in Mysore,

Siliguri and Bhubaneshwar

It is imperative for the sector to not only raise the quality of service delivery, but also ensure equitable

access of basic healthcare to the dramatically increasing population and gear up its capabilities to tackle

the changing disease incidence profiles. Inspiration and learning from southern states such as Kerala

and Tamil Nadu which have successfully brought about effective changes to their healthcare regime, by

undertaking strong action on social determinants and making comprehensive efforts to enhance the

efficiency of public health system respectively, can go a long way in assisting the northern regions of the

country in devising a robust healthcare structure. Going forward, the ability of the healthcare sector to

institute an effective healthcare policy will be critical to define the manner in which the nation‟s

healthcare resources, funds and services are equitably allocated, utilised, developed, distributed and

accessed.

© Grant Thornton India LLP. All rights reserved. 34

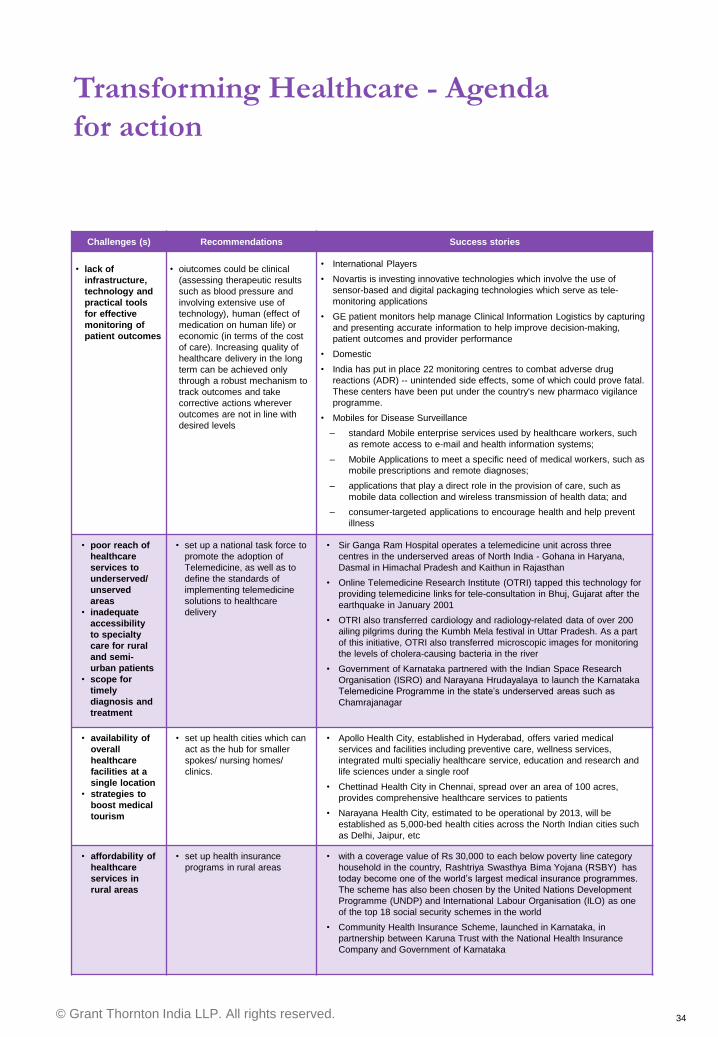

Challenges (s) Recommendations Success stories

• lack of

infrastructure,

technology and

practical tools

for effective

monitoring of

patient outcomes

• oiutcomes could be clinical

(assessing therapeutic results

such as blood pressure and

involving extensive use of

technology), human (effect of

medication on human life) or

economic (in terms of the cost

of care). Increasing quality of

healthcare delivery in the long

term can be achieved only

through a robust mechanism to

track outcomes and take

corrective actions wherever

outcomes are not in line with

desired levels

• International Players

• Novartis is investing innovative technologies which involve the use of

sensor-based and digital packaging technologies which serve as tele-

monitoring applications

• GE patient monitors help manage Clinical Information Logistics by capturing

and presenting accurate information to help improve decision-making,

patient outcomes and provider performance

• Domestic

• India has put in place 22 monitoring centres to combat adverse drug

reactions (ADR) -- unintended side effects, some of which could prove fatal.

These centers have been put under the country's new pharmaco vigilance

programme.

• Mobiles for Disease Surveillance

‒ standard Mobile enterprise services used by healthcare workers, such

as remote access to e-mail and health information systems;

‒ Mobile Applications to meet a specific need of medical workers, such as

mobile prescriptions and remote diagnoses;

‒ applications that play a direct role in the provision of care, such as

mobile data collection and wireless transmission of health data; and

‒ consumer-targeted applications to encourage health and help prevent

illness

• poor reach of

healthcare

services to

underserved/

unserved

areas

• inadequate

accessibility

to specialty

care for rural

and semi-

urban patients

• scope for

timely

diagnosis and

treatment

• set up a national task force to

promote the adoption of

Telemedicine, as well as to

define the standards of

implementing telemedicine

solutions to healthcare

delivery

• Sir Ganga Ram Hospital operates a telemedicine unit across three

centres in the underserved areas of North India - Gohana in Haryana,

Dasmal in Himachal Pradesh and Kaithun in Rajasthan

• Online Telemedicine Research Institute (OTRI) tapped this technology for

providing telemedicine links for tele-consultation in Bhuj, Gujarat after the

earthquake in January 2001

• OTRI also transferred cardiology and radiology-related data of over 200

ailing pilgrims during the Kumbh Mela festival in Uttar Pradesh. As a part

of this initiative, OTRI also transferred microscopic images for monitoring

the levels of cholera-causing bacteria in the river

• Government of Karnataka partnered with the Indian Space Research

Organisation (ISRO) and Narayana Hrudayalaya to launch the Karnataka

Telemedicine Programme in the state‟s underserved areas such as

Chamrajanagar

• availability of

overall

healthcare

facilities at a

single location

• strategies to

boost medical

tourism

• set up health cities which can

act as the hub for smaller

spokes/ nursing homes/

clinics.

• Apollo Health City, established in Hyderabad, offers varied medical

services and facilities including preventive care, wellness services,

integrated multi specialiy healthcare service, education and research and

life sciences under a single roof

• Chettinad Health City in Chennai, spread over an area of 100 acres,

provides comprehensive healthcare services to patients

• Narayana Health City, estimated to be operational by 2013, will be

established as 5,000-bed health cities across the North Indian cities such

as Delhi, Jaipur, etc

• affordability of

healthcare

services in

rural areas

• set up health insurance

programs in rural areas

• with a coverage value of Rs 30,000 to each below poverty line category

household in the country, Rashtriya Swasthya Bima Yojana (RSBY) has

today become one of the world‟s largest medical insurance programmes.

The scheme has also been chosen by the United Nations Development

Programme (UNDP) and International Labour Organisation (ILO) as one

of the top 18 social security schemes in the world

• Community Health Insurance Scheme, launched in Karnataka, in

partnership between Karuna Trust with the National Health Insurance

Company and Government of Karnataka

Transforming Healthcare - Agenda

for action

© Grant Thornton India LLP. All rights reserved. 35

Transforming Healthcare - Agenda

for action

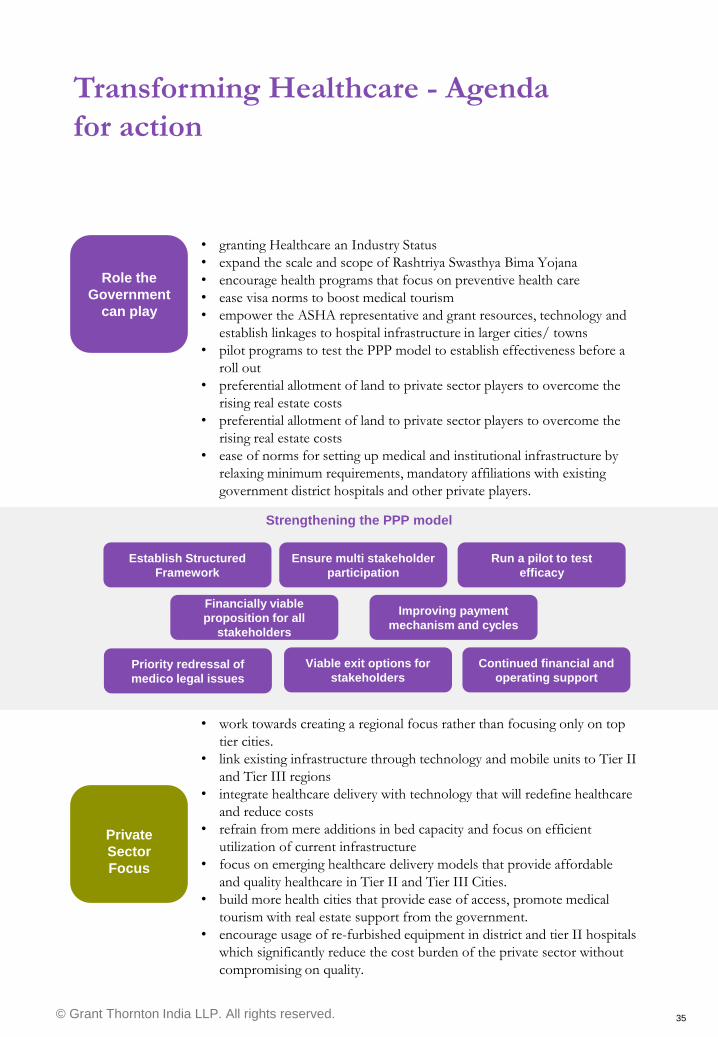

Role the

Government

can play

Private

Sector

Focus

Strengthening the PPP model

Establish Structured

Framework

Ensure multi stakeholder

participation

Run a pilot to test

efficacy

Financially viable

proposition for all

stakeholders

Improving payment

mechanism and cycles

Priority redressal of

medico legal issues

Viable exit options for

stakeholders

Continued financial and

operating support

• work towards creating a regional focus rather than focusing only on top

tier cities.

• link existing infrastructure through technology and mobile units to Tier II

and Tier III regions

• integrate healthcare delivery with technology that will redefine healthcare

and reduce costs

• refrain from mere additions in bed capacity and focus on efficient

utilization of current infrastructure

• focus on emerging healthcare delivery models that provide affordable

and quality healthcare in Tier II and Tier III Cities.

• build more health cities that provide ease of access, promote medical

tourism with real estate support from the government.

• encourage usage of re-furbished equipment in district and tier II hospitals

which significantly reduce the cost burden of the private sector without

compromising on quality.

• granting Healthcare an Industry Status

• expand the scale and scope of Rashtriya Swasthya Bima Yojana

• encourage health programs that focus on preventive health care

• ease visa norms to boost medical tourism

• empower the ASHA representative and grant resources, technology and

establish linkages to hospital infrastructure in larger cities/ towns

• pilot programs to test the PPP model to establish effectiveness before a

roll out

• preferential allotment of land to private sector players to overcome the

rising real estate costs

• preferential allotment of land to private sector players to overcome the

rising real estate costs

• ease of norms for setting up medical and institutional infrastructure by

relaxing minimum requirements, mandatory affiliations with existing

government district hospitals and other private players.

© Grant Thornton India LLP. All rights reserved. 36

A regional health strategy

A regional approach for developing sustainable health systems is the only means to address the

ballooning healthcare need of the Northern Region. Combined with innovative delivery models

and technological interface to bring regions together, Healthcare continues to remain one of the

most promising sectors for the Indian Economy for the coming decade and thereafter.

A regional focus can be maintained either through the current state wise institutional

framework or by channelizing the existing ecosystem of district/ civil hospitals, smaller

hospitals/ nursing care to larger hospitals in Tier I and Tier II cities. Spreading out

delivery models on the basis of the population profile of regions and doctor availability

will ensure equitable allocation of healthcare resources across all regions

Reach

Integration

Keeping the drivers in mind

Developing a clinical pathway

Skill enhancement

Integration of primary care and hospital based infrastructure to provide seamless,

uniform and pro-active care, keeping in mind the level of clinician support (doctor

availability and referral channels) that are available in and around such regions.

Ageing population profile, disease prevalence and general medical technology are key

drivers fueling the demand for healthcare in the Northern Region.

Depending on the need and complexity of surgical intervention, every doctor/

representative at the bottom of the clinical ecocystem shall decide on what activities can

be done at the primary centre level, what needs to be referred to relatively larger

hospitals/ nursing homes and finally acute needs which may need to be referred to

specialty hospitals with skilled professionals. A clear, well defined policy framework of

this clinical pathway is critical for the creation of a holistic and interlinked regional

healthcare system.

Overcome resistance of skilled medical professionals in moving to Tier II, Tier III cities

by creating a timetable of periodic mobility of professionals across deeper regions.

Develop adequate infrastructure and provide institutional support by regular and

continuous training of medical doctors and other skilled manpower to service the sector

Infrastructure support

Reducing the real estate burden and providing support for setting up infrastructure

across the entire spectrum of this regional ecosystem.

© Grant Thornton India LLP. All rights reserved. 37

Appendices Healthcare Indicators, Deal summary

© Grant Thornton India LLP. All rights reserved. 38

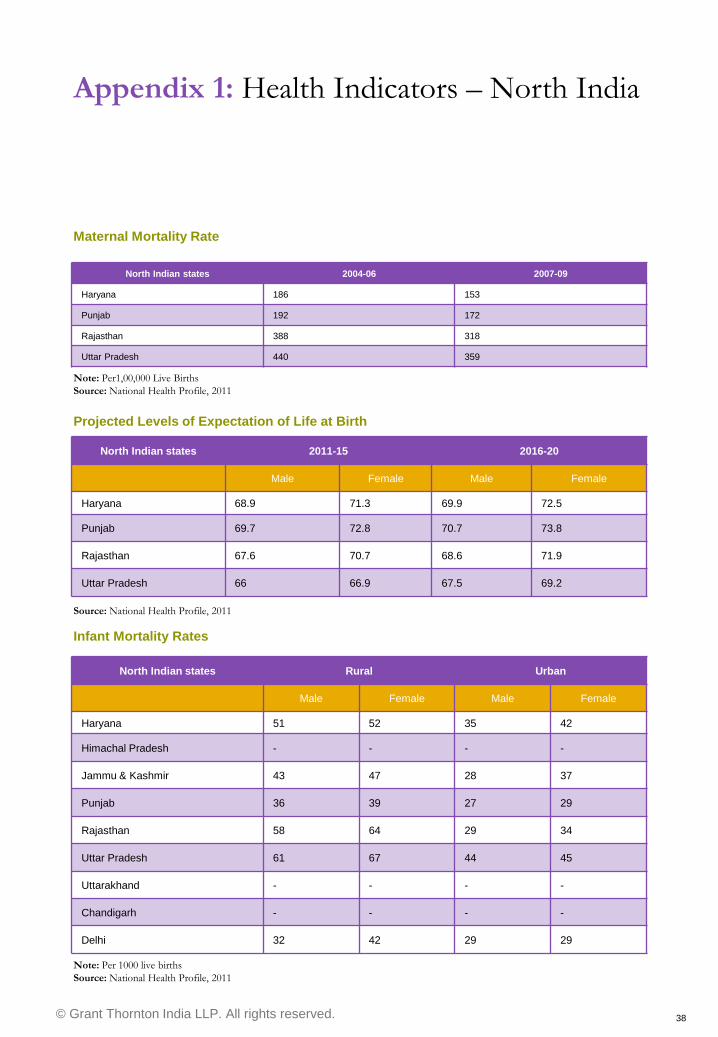

Maternal Mortality Rate

North Indian states 2004-06 2007-09

Haryana 186 153

Punjab 192 172

Rajasthan 388 318

Uttar Pradesh 440 359

Note: Per1,00,000 Live Births

Source: National Health Profile, 2011

Projected Levels of Expectation of Life at Birth

North Indian states 2011-15 2016-20

Male Female Male Female

Haryana 68.9 71.3 69.9 72.5

Punjab 69.7 72.8 70.7 73.8

Rajasthan 67.6 70.7 68.6 71.9

Uttar Pradesh 66 66.9 67.5 69.2

Source: National Health Profile, 2011

Infant Mortality Rates

North Indian states Rural Urban

Male Female Male Female

Haryana 51 52 35 42

Himachal Pradesh - - - -

Jammu & Kashmir 43 47 28 37

Punjab 36 39 27 29

Rajasthan 58 64 29 34

Uttar Pradesh 61 67 44 45

Uttarakhand - - - -

Chandigarh - - - -

Delhi 32 42 29 29

Note: Per 1000 live births

Source: National Health Profile, 2011

Appendix 1: Health Indicators – North India

© Grant Thornton India LLP. All rights reserved. 39

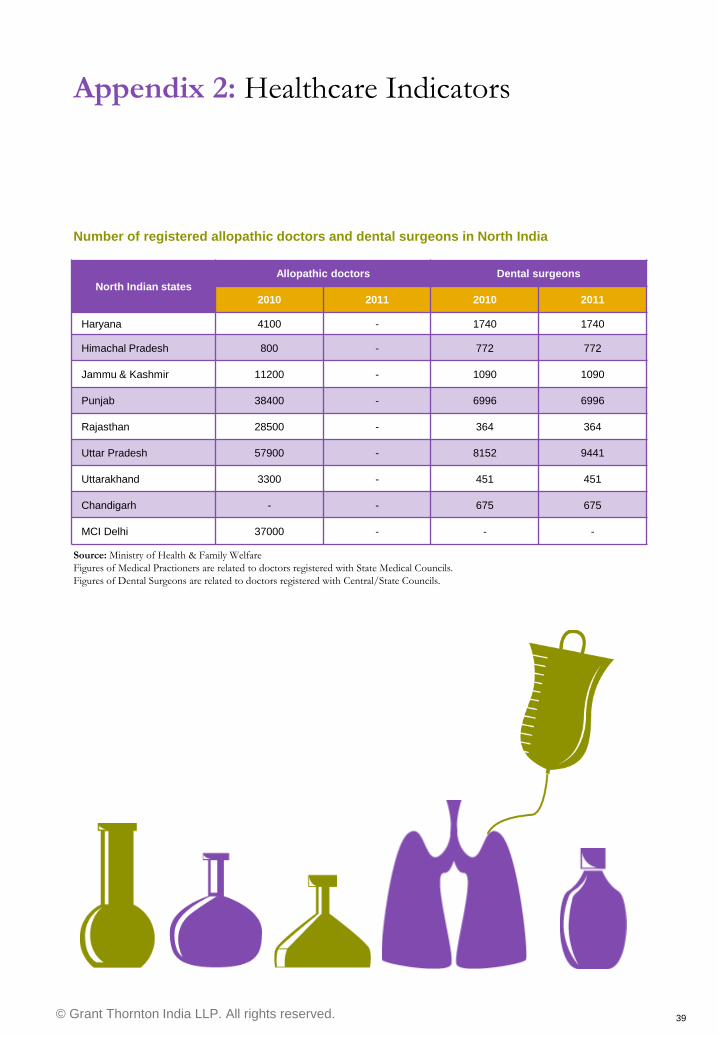

Number of registered allopathic doctors and dental surgeons in North India

Source: Ministry of Health & Family Welfare

Figures of Medical Practioners are related to doctors registered with State Medical Councils.

Figures of Dental Surgeons are related to doctors registered with Central/State Councils.

North Indian states

Allopathic doctors Dental surgeons

2010 2011 2010 2011

Haryana 4100 - 1740 1740

Himachal Pradesh 800 - 772 772

Jammu & Kashmir 11200 - 1090 1090

Punjab 38400 - 6996 6996

Rajasthan 28500 - 364 364

Uttar Pradesh 57900 - 8152 9441

Uttarakhand 3300 - 451 451

Chandigarh - - 675 675

MCI Delhi 37000 - - -

Appendix 2: Healthcare Indicators

© Grant Thornton India LLP. All rights reserved. 40

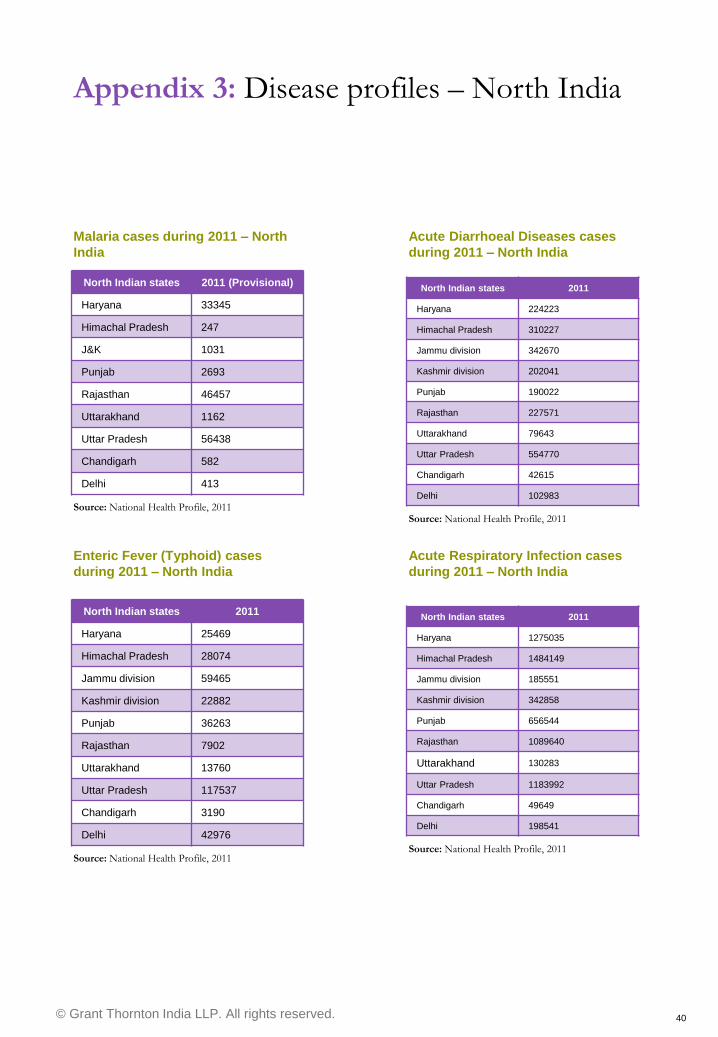

Malaria cases during 2011 – North

India

Source: National Health Profile, 2011

Appendix 3: Disease profiles – North India

North Indian states 2011 (Provisional)

Haryana 33345

Himachal Pradesh 247

J&K 1031

Punjab 2693

Rajasthan 46457

Uttarakhand 1162

Uttar Pradesh 56438

Chandigarh 582

Delhi 413

Acute Diarrhoeal Diseases cases

during 2011 – North India

North Indian states 2011

Haryana 224223

Himachal Pradesh 310227

Jammu division 342670

Kashmir division 202041

Punjab 190022

Rajasthan 227571

Uttarakhand 79643

Uttar Pradesh 554770

Chandigarh 42615

Delhi 102983

Source: National Health Profile, 2011

Enteric Fever (Typhoid) cases

during 2011 – North India

Source: National Health Profile, 2011

Acute Respiratory Infection cases

during 2011 – North India

North Indian states 2011

Haryana 1275035

Himachal Pradesh 1484149

Jammu division 185551

Kashmir division 342858

Punjab 656544

Rajasthan 1089640

Uttarakhand 130283

Uttar Pradesh 1183992

Chandigarh 49649

Delhi 198541

Source: National Health Profile, 2011

North Indian states 2011

Haryana 25469

Himachal Pradesh 28074

Jammu division 59465

Kashmir division 22882

Punjab 36263

Rajasthan 7902

Uttarakhand 13760

Uttar Pradesh 117537

Chandigarh 3190

Delhi 42976

© Grant Thornton India LLP. All rights reserved. 41

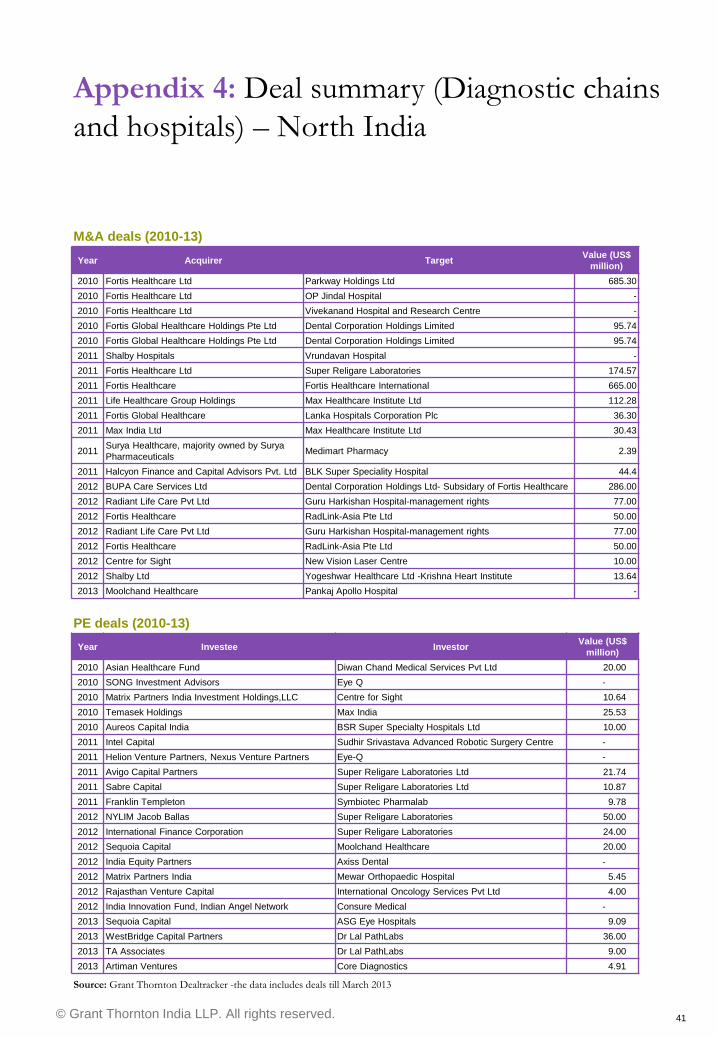

Appendix 4: Deal summary (Diagnostic chains

and hospitals) – North India

Year Acquirer Target Value (US$

million)

2010 Fortis Healthcare Ltd Parkway Holdings Ltd 685.30

2010 Fortis Healthcare Ltd OP Jindal Hospital -

2010 Fortis Healthcare Ltd Vivekanand Hospital and Research Centre -

2010 Fortis Global Healthcare Holdings Pte Ltd Dental Corporation Holdings Limited 95.74

2010 Fortis Global Healthcare Holdings Pte Ltd Dental Corporation Holdings Limited 95.74

2011 Shalby Hospitals Vrundavan Hospital -

2011 Fortis Healthcare Ltd Super Religare Laboratories 174.57

2011 Fortis Healthcare Fortis Healthcare International 665.00

2011 Life Healthcare Group Holdings Max Healthcare Institute Ltd 112.28

2011 Fortis Global Healthcare Lanka Hospitals Corporation Plc 36.30

2011 Max India Ltd Max Healthcare Institute Ltd 30.43

2011 Surya Healthcare, majority owned by Surya

Pharmaceuticals Medimart Pharmacy 2.39

2011 Halcyon Finance and Capital Advisors Pvt. Ltd BLK Super Speciality Hospital 44.4

2012 BUPA Care Services Ltd Dental Corporation Holdings Ltd- Subsidary of Fortis Healthcare 286.00

2012 Radiant Life Care Pvt Ltd Guru Harkishan Hospital-management rights 77.00

2012 Fortis Healthcare RadLink-Asia Pte Ltd 50.00

2012 Radiant Life Care Pvt Ltd Guru Harkishan Hospital-management rights 77.00

2012 Fortis Healthcare RadLink-Asia Pte Ltd 50.00

2012 Centre for Sight New Vision Laser Centre 10.00

2012 Shalby Ltd Yogeshwar Healthcare Ltd -Krishna Heart Institute 13.64

2013 Moolchand Healthcare Pankaj Apollo Hospital -

M&A deals (2010-13)

Source: Grant Thornton Dealtracker -the data includes deals till March 2013

Year Investee Investor Value (US$

million)

2010 Asian Healthcare Fund Diwan Chand Medical Services Pvt Ltd 20.00

2010 SONG Investment Advisors Eye Q -

2010 Matrix Partners India Investment Holdings,LLC Centre for Sight 10.64

2010 Temasek Holdings Max India 25.53

2010 Aureos Capital India BSR Super Specialty Hospitals Ltd 10.00

2011 Intel Capital Sudhir Srivastava Advanced Robotic Surgery Centre -

2011 Helion Venture Partners, Nexus Venture Partners Eye-Q -

2011 Avigo Capital Partners Super Religare Laboratories Ltd 21.74

2011 Sabre Capital Super Religare Laboratories Ltd 10.87

2011 Franklin Templeton Symbiotec Pharmalab 9.78

2012 NYLIM Jacob Ballas Super Religare Laboratories 50.00

2012 International Finance Corporation Super Religare Laboratories 24.00

2012 Sequoia Capital Moolchand Healthcare 20.00

2012 India Equity Partners Axiss Dental -

2012 Matrix Partners India Mewar Orthopaedic Hospital 5.45

2012 Rajasthan Venture Capital International Oncology Services Pvt Ltd 4.00

2012 India Innovation Fund, Indian Angel Network Consure Medical -

2013 Sequoia Capital ASG Eye Hospitals 9.09

2013 WestBridge Capital Partners Dr Lal PathLabs 36.00

2013 TA Associates Dr Lal PathLabs 9.00

2013 Artiman Ventures Core Diagnostics 4.91

PE deals (2010-13)

© Grant Thornton India LLP. All rights reserved. 42

• IMR: Infant Mortality Rate

• MMR: Maternal Mortality Rate

• GDP: Gross Domestic Product

• OECD: Organisation for Economic Co-

operation and Development

• BRICS: Brazil, Russia, India, China and

South Africa

• FDI: Foreign Direct Investment

• PE: Private Equity

• FVCI: Foreign Venture Capital Funds

• FIIs: Foreign Institutional Investors

• ADR: American Depositary Receipt

• GDR: Global Depository Receipt

• M&A: Mergers and Acquisitions

• NRI: Non-resident Indian

• Pvt: Private

• Ltd: Limited

• MoU: Memorandum of Understanding

• IT: Information Technology

• HIS: Hospital Information System

• EHR: Electronic Health Record

• EMR: Electronic Medical Record

• RGI: Registrar General Of India

• SRS: Sample Registration System

• RSBY: Rashtriya Swasthya Bima Yojana

• ASHAs: Accredited Social Health Activists

• OT: Operation Theatre

• ICU: Intensive Care Unit

• US: United States of America

• UK: United Kingdom

• UT: Union Territory

• MIOT: Madras Institute of Orthopaedics

and Traumatology

• GPRS: General Packet Radio Service

• AYUSH: Department of Ayurveda, Yoga &

Naturopathy, Unani, Siddha and

Homoeopathy, Government of India

• AHM: Ahmedabad

• CHD: Chandigarh

• DEL: Delhi

• GUR: Gurgaon

• GZB: Ghaziabad

• LUD: Ludhiana

• RAJ: Rajasthan

• UP: Uttar Pradesh

• J&K: Jammu and Kashmir

• WHO: World Health Organisation

• PPP: Public-Private Partnership

• ANC: Ante-Natal Care

• CAGR: Compounded Annual Growth Rate

• NRHM: National Rural Health Mission

• NABH: National Accreditation Board for

Hospitals & Healthcare Providers

• MoHFW: Ministry of Health and Family

Welfare

• NUHM: Ministry of Health and Family

Welfare

• OTRI: Online Telemedicine Research

Institute

• TIFAC: Forecasting and Assessment

Council

• BISR: Birla Institute of Scientific Research

• UMHRC: Uttarakhand Mobile Hospital

and Research Centre

• BOT: Build–Operate–Transfer

• AIIMS: All India Institute of Medical

Sciences

• AIDS: Acquired Immunodeficiency

Syndrome

• ISRO: Indian Space Research Organisation

• ILO: International Labour Organisation

• UNDP: United Nations Development

Programme

Appendix 5: Abbreviations

© Grant Thornton India LLP. All rights reserved. 43

References

• http://www.gartner.com/newsroom/id/234

4215

• http://data.worldbank.org/indicator/SH.XP

D.PCAP/countries

• Health at a Glance 2011: OECD indicators

• http://www.business-

standard.com/article/economy-

policy/doing-less-with-more-india-s-health-

care-system-113033000209_1.html

• http://www.changemakers.com/changesho

p/primary-healthcare-rural-indian-

populations

• http://www.ncbi.nlm.nih.gov/pmc/articles/

PMC3283025/

• http://www.business-

standard.com/article/management/improvi

ng-the-picture-of-india-s-healthcare-

112061800066_1.html

• http://www.photius.com/rankings/healthra

nks.html

• http://www.ibef.org/download/Healthcare

50112.pdf

• http://ehealth.eletsonline.com/2013/02/he

alth-gets-over-28-hikes-in-budget/

• http://www.photius.com/rankings/world_h

ealth_systems.html

• Indian Healthcare sector report – MegStrat

Consulting

• http://www.indianmirror.com/indian-

industries/2012/health-2012.html

• http://www.business-

standard.com/article/companies/indian-

pharma-market-to-grow-at-15-cagr-by-fy14-

112060300047_1.html

• http://data.worldbank.org/indicator/NY.G

DP.PCAP.CD

• http://articles.timesofindia.indiatimes.com/

2012-11-01/jaipur/34856928_1_imr-infant-

mortality-rate-sample-registration-survey

• National Health Profile – 2011 and 2010

• http://www.businessinsider.com/inside-

indias-no-frills-hospitals-where-heart-

surgery-costs-just-800-2013-4

• http://www.livemint.com/Politics/D0gBg

wCn3huK72S06p8K5H/The-dark-

underbelly-of-Indias-clinical-trials-

business.html

• http://www.photius.com/rankings/world_

health_systems.html

• Grant Thornton Healthcare Sector Budget

report 2013-14

• Research on India – Hospital Market in

India (March 2012)

© Grant Thornton India LLP. All rights reserved. 44

About CII

The Confederation of Indian Industry (CII) works to create and sustain an environment conducive

to the development of India, partnering industry, Government, and civil society, through advisory

and consultative processes. CII is a non-government, not-for-profit, industry led and industry

managed organization, playing a proactive role in India's development process. Founded over 118

years ago, India's premier business association has over 7100 member organizations, from the private

as well as public sectors, including SMEs and MNCs, and an indirect membership of over 90,000

companies from around 257 national and regional sectoral associations.

CII charts change by working closely with Government on policy issues, interfacing with thought

leaders, and enhancing efficiency, competitiveness and business opportunities for industry through a

range of specialised services and global linkages. It also provides a platform for consensus-building

and networking on diverse issues. Extending its agenda beyond business, CII assists industry to

identify and execute corporate citizenship programmes. Partnerships with over 120 NGOs across the

country carry forward our initiatives for integrated and inclusive development, in affirmative action,

healthcare, education, livelihood, diversity management, skill development, empowerment of women,

and water, to name a few.

The CII Theme for 2013-14 is Accelerating Economic Growth through Innovation,

Transformation, Inclusion and Governance. Towards this, CII advocacy will accord top priority

to stepping up the growth trajectory of the nation, while retaining a strong focus on accountability,

transparency and measurement in both the corporate and social eco-system, building a knowledge

economy, and broad-basing development to help deliver the fruits of progress to many.

With 63 offices including 10 Centres of Excellence in India, and 7 overseas offices in Australia,

China, France, Singapore, South Africa, UK, and USA, as well as institutional partnerships with 224

counterpart organizations in 90 countries, CII serves as a reference point for Indian industry and the

international business community.

Confederation of Indian Industry