Embed Size (px)

Citation preview

VC Survey Results January 2017

1

Mark Suster, @msusterChang Xu, @_changxu

“It’s a great time to be a startup raising money”

2

Mark Suster, March 2017

3

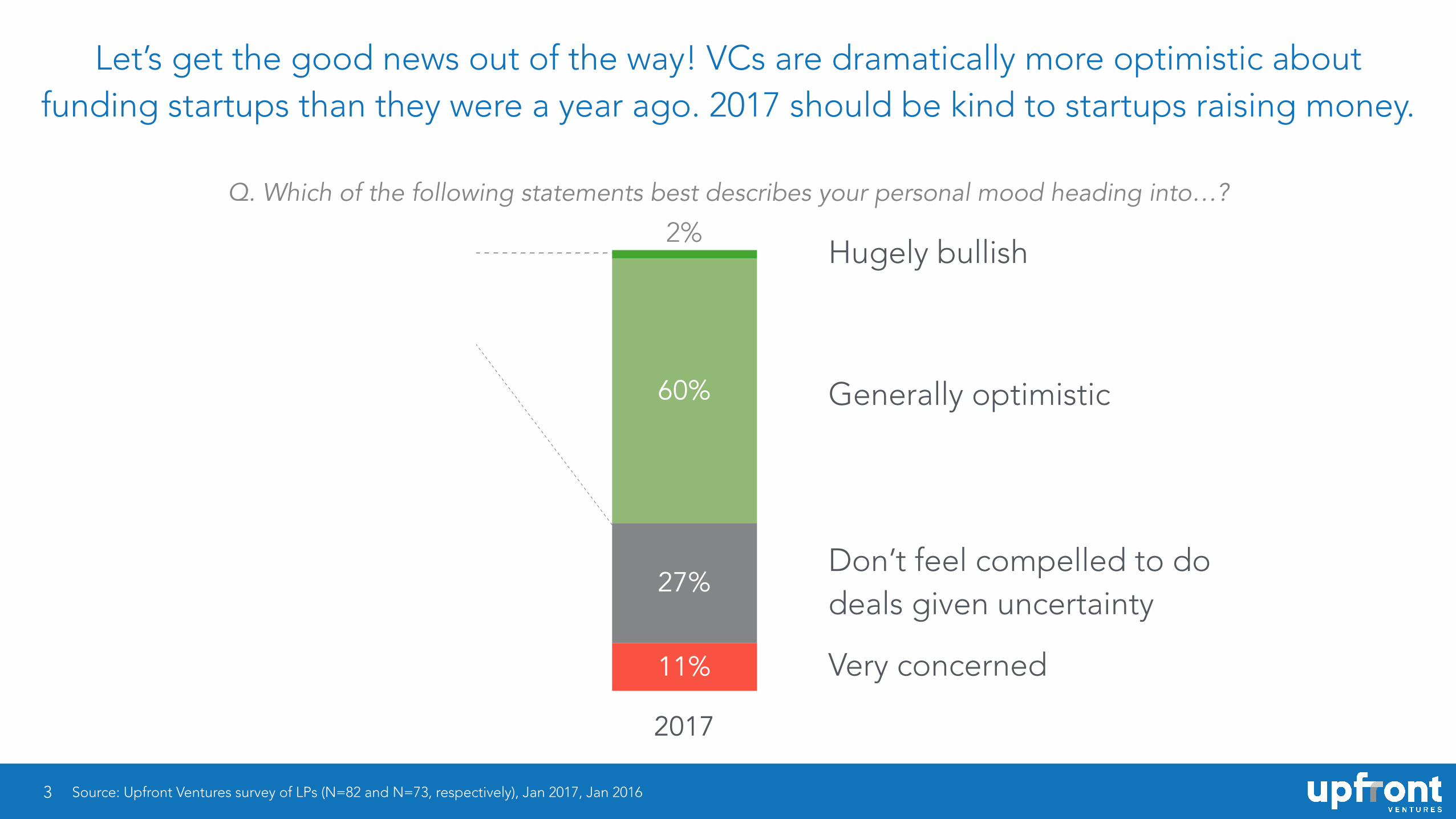

Let’s get the good news out of the way! VCs are dramatically more optimistic about funding startups than they were a year ago. 2017 should be kind to startups raising money.

Source: Upfront Ventures survey of LPs (N=82 and N=73, respectively), Jan 2017, Jan 2016

2016 2017

2%9%

60%

9%

27%

50%

11%

32%

Q. Which of the following statements best describes your personal mood heading into…?

Hugely bullish

Very concerned

Don’t feel compelled to do deals given uncertainty

Generally optimistic

2%

4

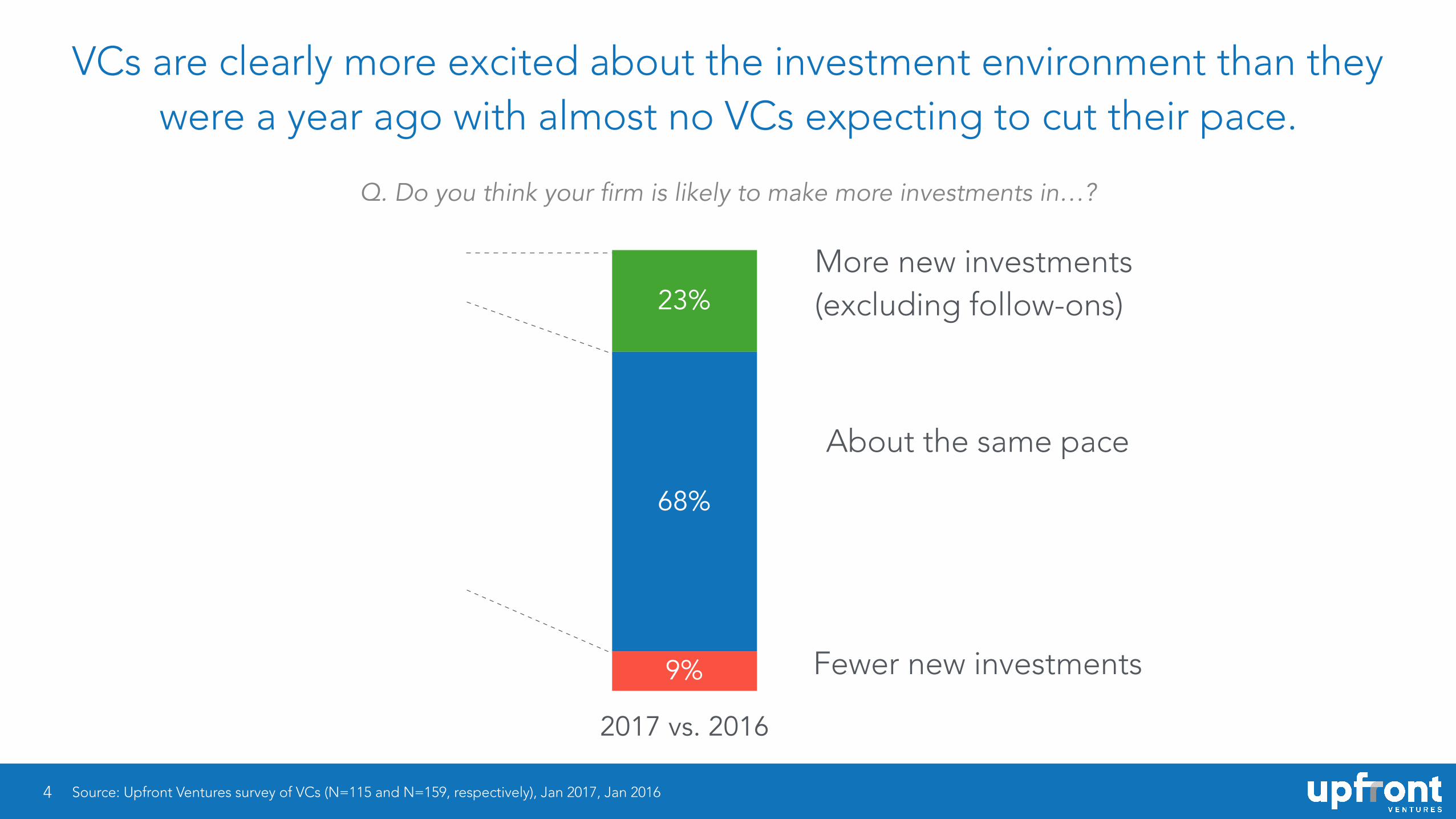

VCs are clearly more excited about the investment environment than they were a year ago with almost no VCs expecting to cut their pace.

Source: Upfront Ventures survey of VCs (N=115 and N=159, respectively), Jan 2017, Jan 2016

2016 vs. 2015 2017 vs. 2016

23%11%

68%

66%

9%23%

Fewer new investments

More new investments (excluding follow-ons)

About the same pace

Q. Do you think your firm is likely to make more investments in…?

VC experienced a “mild winter” in 2016

5

6

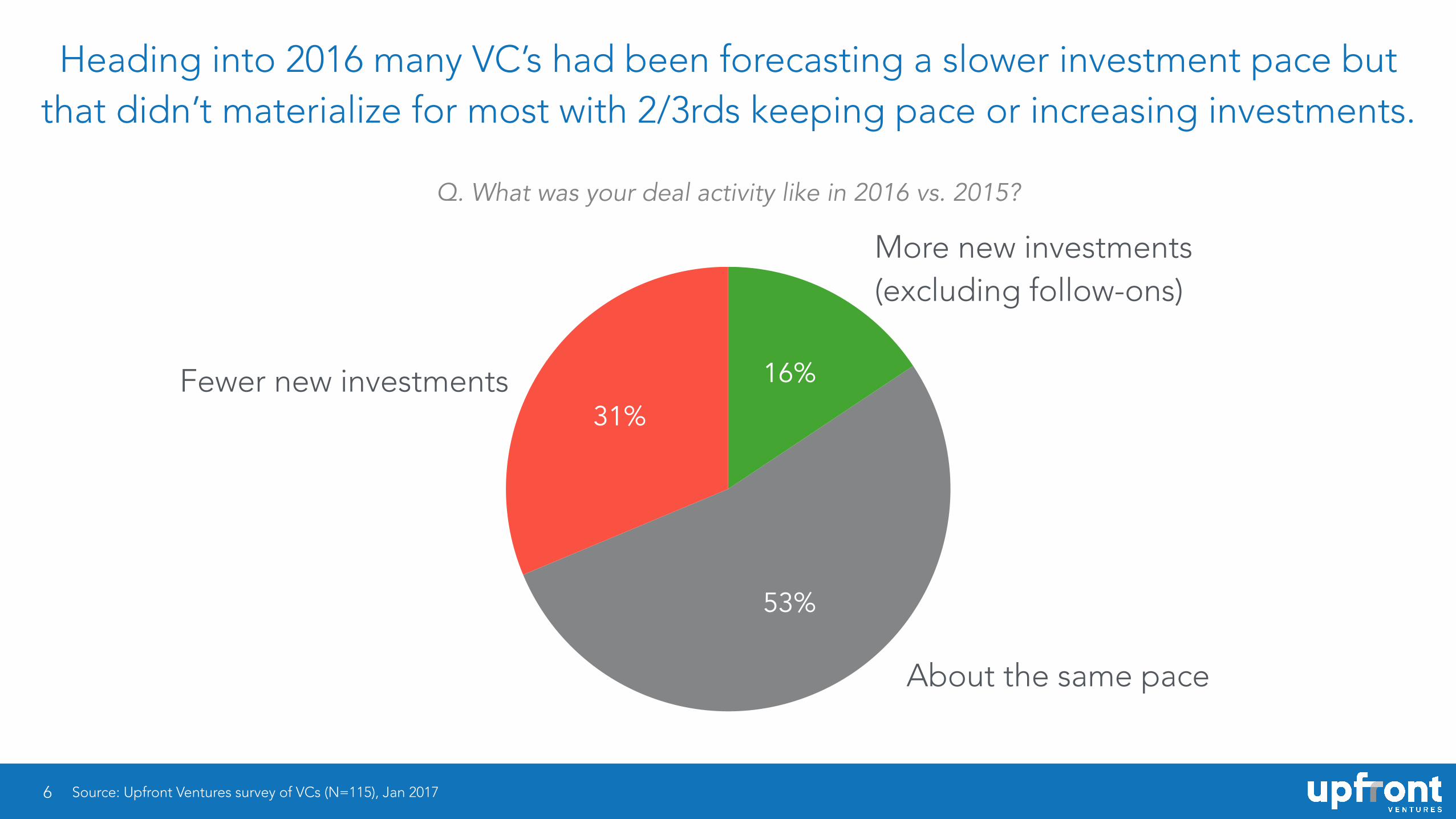

Heading into 2016 many VC’s had been forecasting a slower investment pace but that didn’t materialize for most with 2/3rds keeping pace or increasing investments.

31%

53%

16%

More new investments (excluding follow-ons)

Fewer new investments

About the same pace

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

Q. What was your deal activity like in 2016 vs. 2015?

7

And while valuations have cooled off slightly it has much less significant than the industry had expected. 30% expected big drops yet only 3% have seen it.

Prediction in 2016 Reflection in 2017

8%

16%

8%

73%

61%

3%

30%

Increased

Significantly dropped

Marginally came down

About the same

2017Q. Would you say valuations in 2016 were higher, lower or remained

about the same vs. 2015?

2016Q. Do you expect valuations in Q1 / Q2 2016 to go up, down or remain about the same as previous quarters?

Source: Upfront Ventures survey of VCs (N=115 and N=159, respectively), Jan 2017, Jan 2016

8

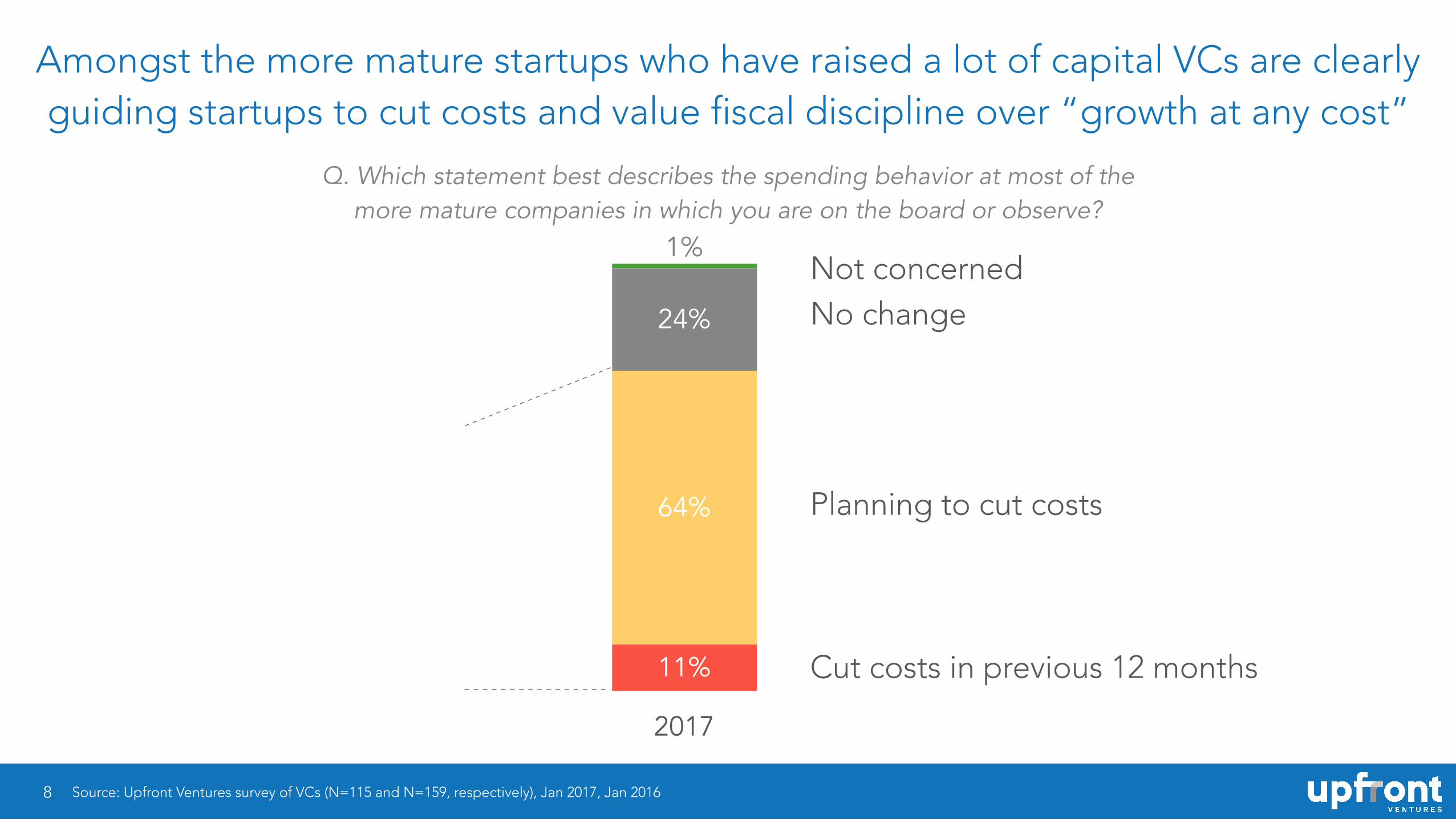

Amongst the more mature startups who have raised a lot of capital VCs are clearly guiding startups to cut costs and value fiscal discipline over “growth at any cost”

2016 2017

1%4%

24%35%

64%

62%

11%

Q. Which statement best describes the spending behavior at most of the more mature companies in which you are on the board or observe?

Planning to cut costs

Not concernedNo change

Cut costs in previous 12 months

Source: Upfront Ventures survey of VCs (N=115 and N=159, respectively), Jan 2017, Jan 2016

9

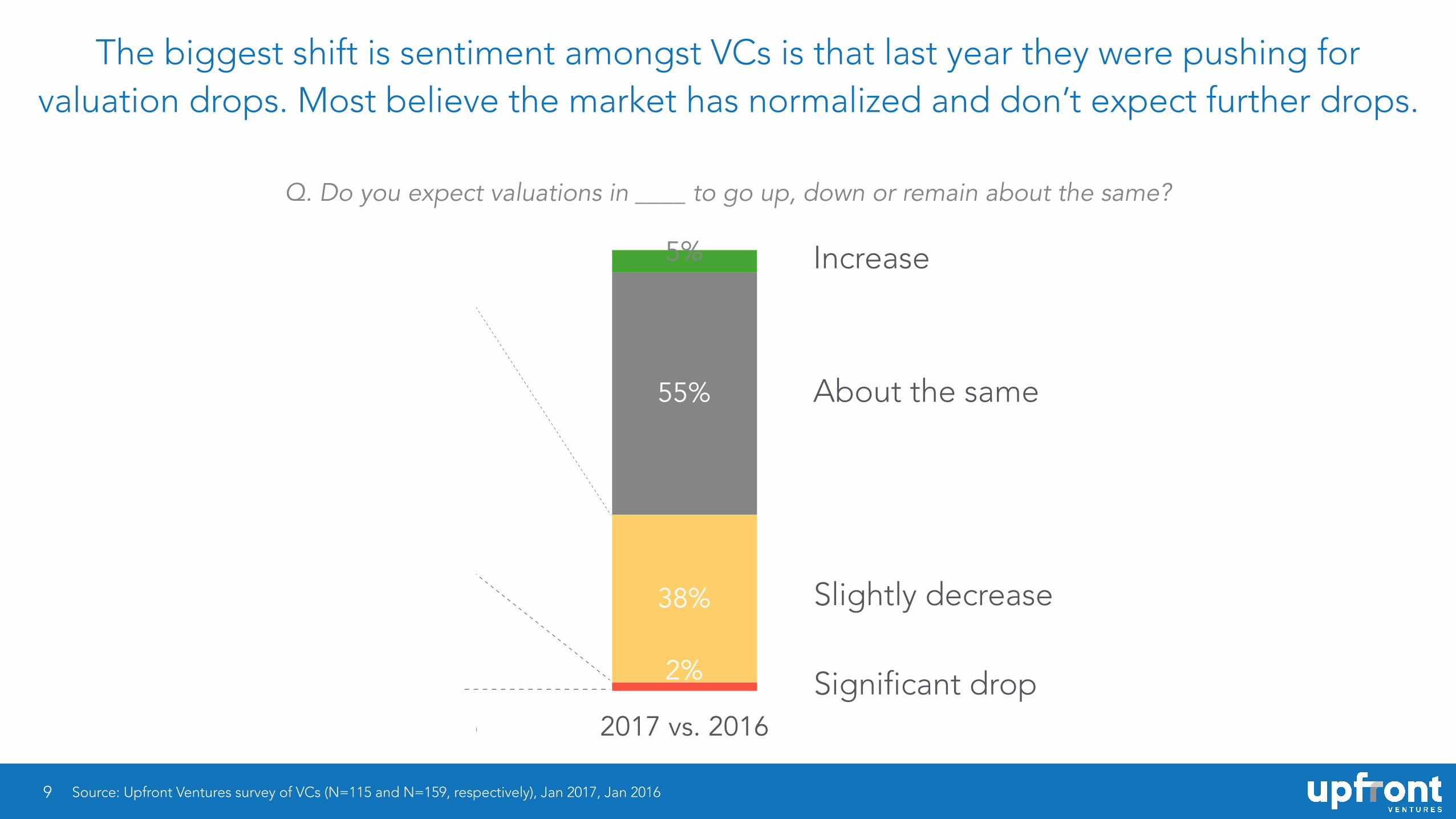

The biggest shift is sentiment amongst VCs is that last year they were pushing for valuation drops. Most believe the market has normalized and don’t expect further drops.

2016 vs. 2015 2017 vs. 2016

5%

55%

8%

38%

62%

2%

30%

Q. Do you expect valuations in ____ to go up, down or remain about the same?

Increase

Significant drop

Slightly decrease

About the same

Source: Upfront Ventures survey of VCs (N=115 and N=159, respectively), Jan 2017, Jan 2016

10

VCs aren’t expecting 2017 to be a floodgate of IPOs for unicorns with more realistic options getting out via M&A or restructuring to become healthier businesses.

7%8%

34% 36%

15%

Many more will IPONone of the above

More restructuring

M&A

No realistic options, will cut burn

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

Q. Of the unicorns minted in the past 2-3 years, what do you think 2017 will hold for them?

11

VCs attribute the “mild winter” to the low interest rates and also the huge influx of capital from big funds, new funds, corporate funds & foreign money.

Low interest rate environment

Late-stage VC funds raising larger funds

Many new VC funds

Increases in corporate VC arms

Increases in Chinese money

Increases in Sovereign Wealth Funds

Increases in LPs making direct investments

Mutual funds and hedge funds 14%

21%

25%

30%

32%

54%

54%

58%

Note: Survey asked respondents to rate each item on a scale of 1-5. Above chart indicates percent of respondents that rated 4 (relevant) or 5 (most relevant). Source: Upfront Ventures survey of VCs (N=115), Jan 2017

Q. In 2016 many investors warned “Winter is Coming” referring to a slowdown in venture markets. That slowdown happened but was very short lived. Which of the following are relevant in influencing why “Winter was Mild”?

VCs expect to be raising less money themselves in 2017

12

13

2016 was a huge year for VCs looking to raise money from LPs. Many expect 2017 will cool a bit or keep pace. Very few expect increased fund raising. (maybe it’s a good time to be raising?) :)

3%

40%

45%

13%

Same as 2016

Fewer than 2016

Don’t knowMore

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

Q. Do you expect VCs raising funds from LPs to increase in 2017?

14

Almost half of VCs think it will be harder to fundraise from LPs in 2017 - but this is strangely at odds with what LPs told us in their surveys.

47%

48%

5%

Same

Harder

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

Easier

Q. Do you expect VCs raising funds from LPs to be easier or harder in 2017?

15

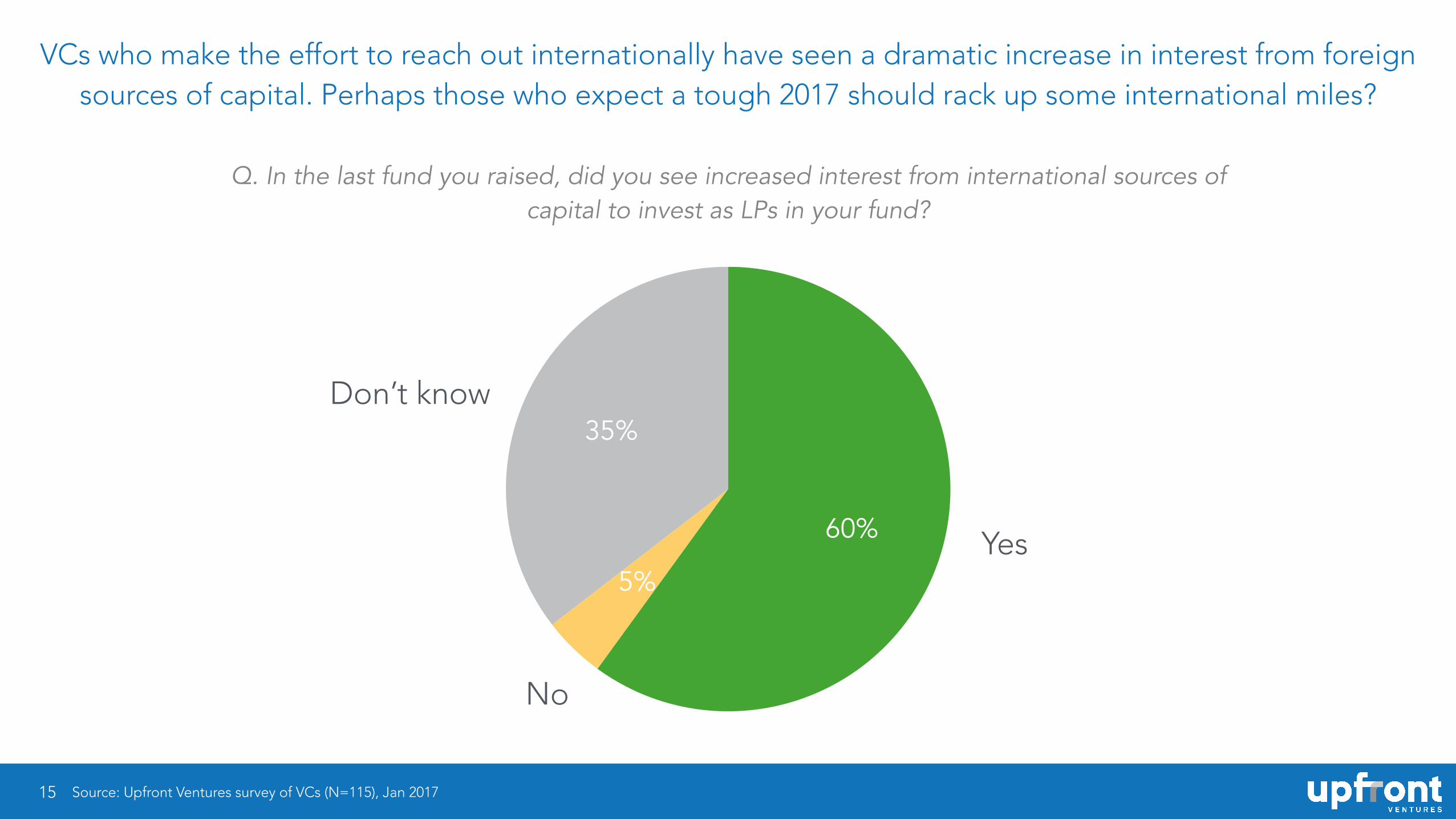

VCs who make the effort to reach out internationally have seen a dramatic increase in interest from foreign sources of capital. Perhaps those who expect a tough 2017 should rack up some international miles?

35%

5%

60% Yes

No

Don’t know

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

Q. In the last fund you raised, did you see increased interest from international sources of capital to invest as LPs in your fund?

VC views on emerging investment areas

16

17

Most VCs are most excited about AI & Machine Learning as their most important investment theme for the coming 5-10 years.

AI / ML IoT AR / VR Blockchain Bots-based

2%9%

20%9%

58%

15%16%

23%42%

27%

30%

42%23%

30%

8%

40%

26%33%18%

7% 13%7%1%1%

Deeply skepticalToo hypedSimilar to other areasSome interesting investmentsMost important for next 5-10yrs

Q. How do you feel about the following investment areas?

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

commerce

18

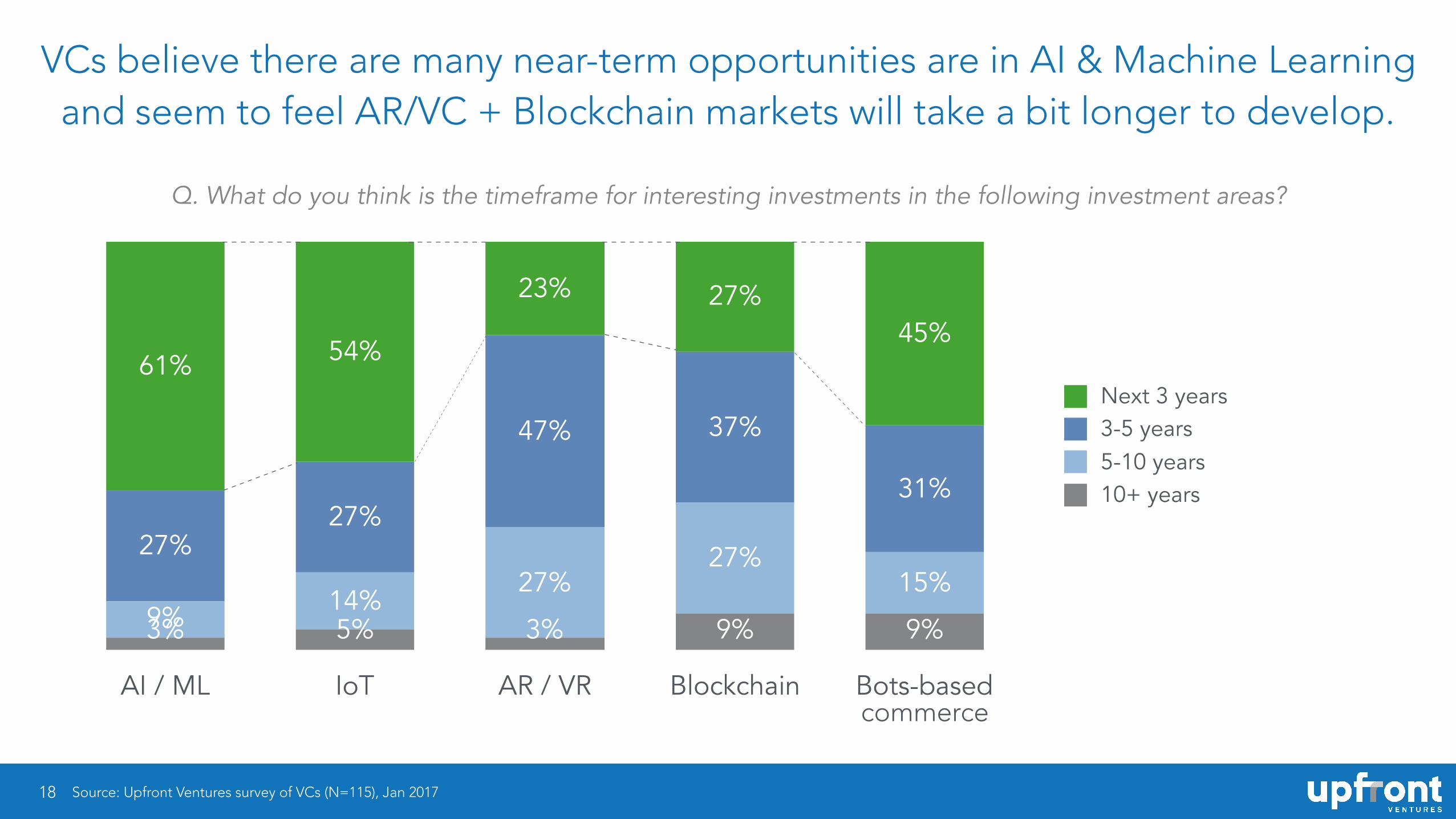

VCs believe there are many near-term opportunities are in AI & Machine Learning and seem to feel AR/VC + Blockchain markets will take a bit longer to develop.

AI / ML IoT AR / VR Blockchain Bots-based

45%27%23%

54%61%

31%

37%47%

27%27%

15%27%

27%14%9% 9%9%3%5%3%

10+ years5-10 years3-5 yearsNext 3 years

Q. What do you think is the timeframe for interesting investments in the following investment areas?

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

commerce

How did VCs feel about Trump — before

the inauguration?

19

20

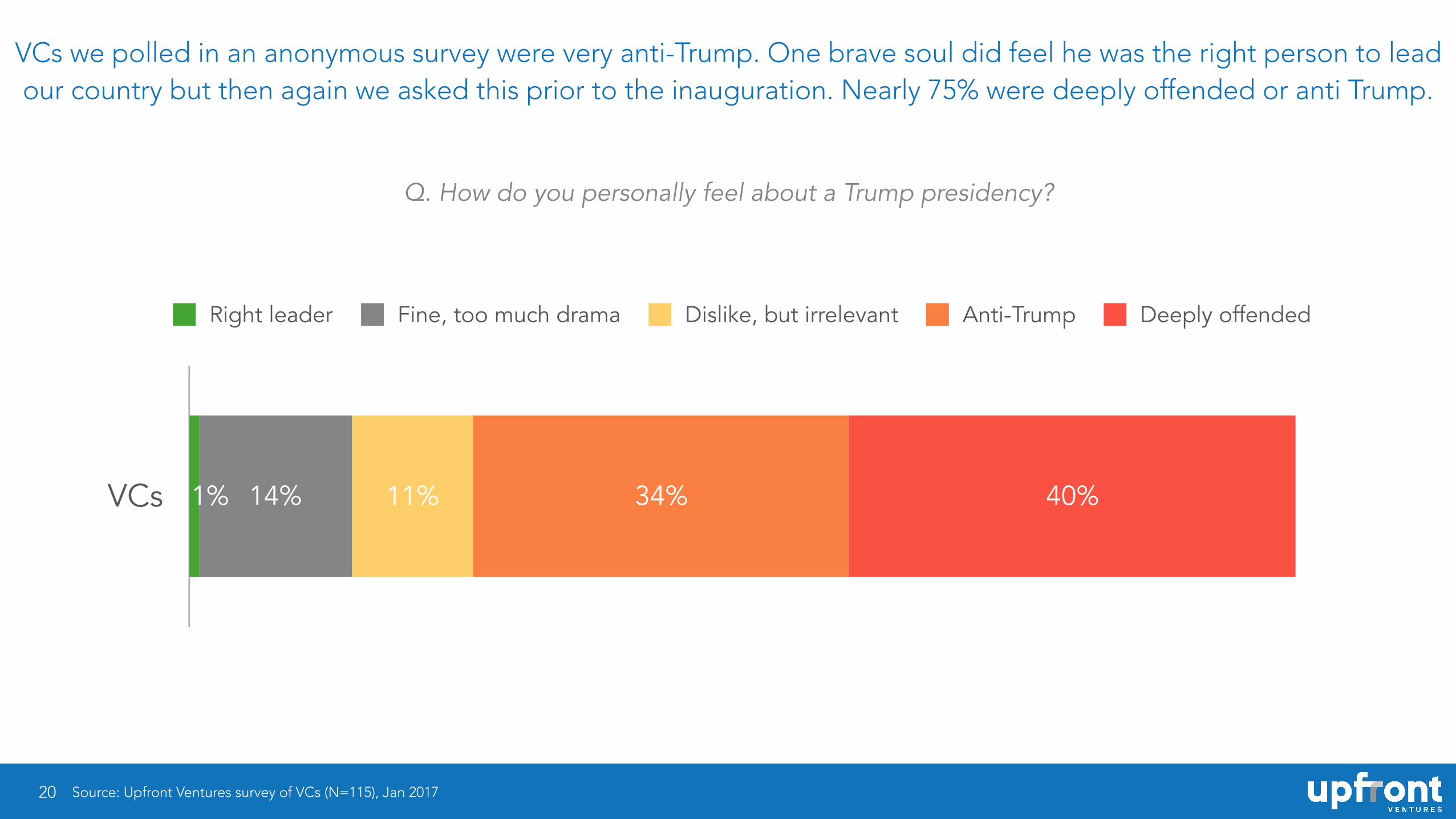

VCs we polled in an anonymous survey were very anti-Trump. One brave soul did feel he was the right person to lead our country but then again we asked this prior to the inauguration. Nearly 75% were deeply offended or anti Trump.

VCs 40%34%11%14%1%

Right leader Fine, too much drama Dislike, but irrelevant Anti-Trump Deeply offended

Q. How do you personally feel about a Trump presidency?

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

21

Two-thirds of VCs were shared some concerns about Trump’s social policies affecting the startup ecosystem with 20% deeply worried. This was before inauguration. We imagine a re-polling on this

question if done today might yield even bigger concerns.

VCs 20%27%24%28%2%

Right direction No impact Discourage from entering tech Concerned Deeply worried

Q. How will a Trump presidency impact startup companies and tech company employment & social policies including ethnic diversity, immigration, religious tolerance, gender equality and transgender rights?

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

22

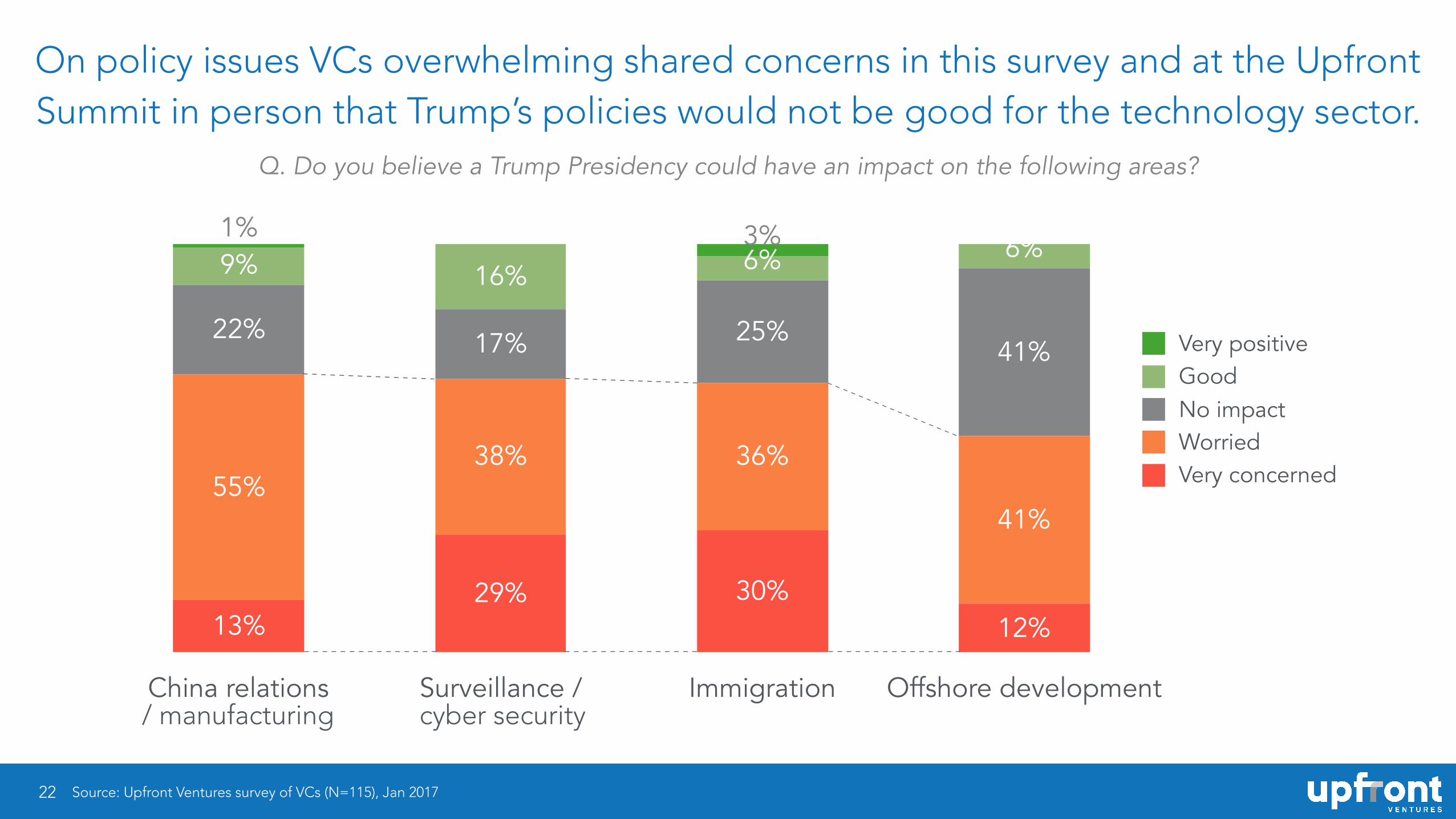

On policy issues VCs overwhelming shared concerns in this survey and at the Upfront Summit in person that Trump’s policies would not be good for the technology sector.

China relations Surveillance / Immigration Offshore development

3%1%6%6%16%9%

41%25%17%22%

41%

36%38%55%

12%30%29%

13%

Very concernedWorriedNo impactGoodVery positive

Q. Do you believe a Trump Presidency could have an impact on the following areas?

/ manufacturing cyber security

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

23

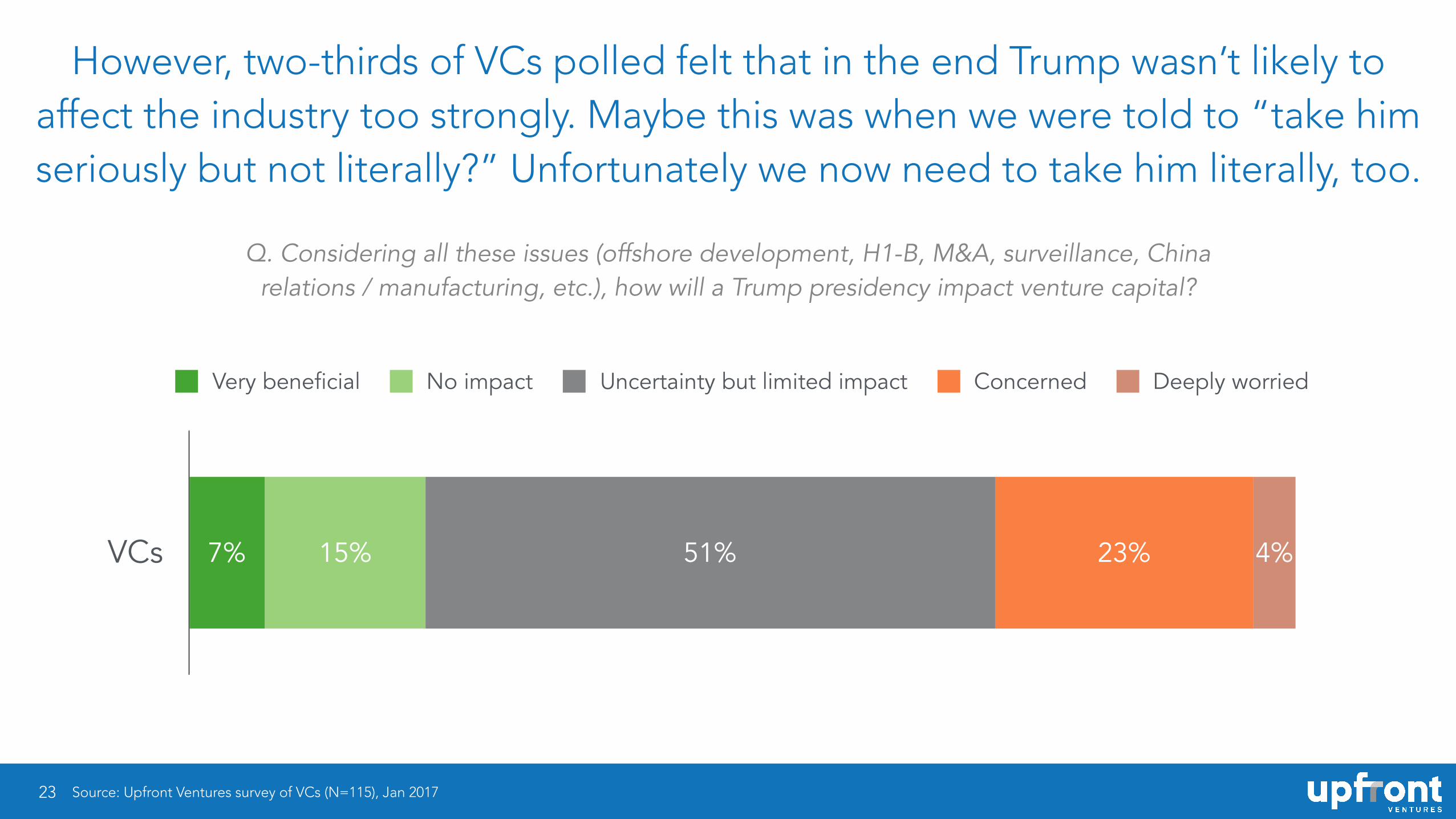

However, two-thirds of VCs polled felt that in the end Trump wasn’t likely to affect the industry too strongly. Maybe this was when we were told to “take him seriously but not literally?” Unfortunately we now need to take him literally, too.

VCs 4%23%51%15%7%

Very beneficial No impact Uncertainty but limited impact Concerned Deeply worried

Q. Considering all these issues (offshore development, H1-B, M&A, surveillance, China relations / manufacturing, etc.), how will a Trump presidency impact venture capital?

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

Appendix Annual Upfront VC Survey Participants

115 respondents in January 2017* 159 respondents in January 2016

24

* In 2017, we split out corporate VCs (CVC) into a separate survey so that we could ask a range of CVC specific questions so they weren’t included in this report.

2017 VC respondent demographics (I)

25

Fund type

0

20

40

60

Angel Seed VC (Early) VC (Mid) VC (Late) PE

199

38

54

2

Fund size ($ million)

0

13

27

40

$1-20 $20-100 $100-300 $300-999 $1000+ Evergreen

4

10

19

3233

17

New investments per partner per year (excl. follow-on’s)

0

17

33

50

1 2 3-4 5-10 10+

12

26

4034

3

Number of board or observer seats per partner

0

13

27

40

0 1-3 4-6 7-10 11-14 15+

32

353632

7

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

2017 VC respondent demographics (II)

26

Survey respondent geography

0

30

60

SF/Bay Area SoCal New York Boston Other US ROW

462

2329

51

Position

0

40

80

120

Partner / MD Analyst to Principal Sole proprietor/personal investor

18

106

How long has your firm existed (years)

0

30

60

0-3 3-10 10-20 20+

17

26

48

23

Personal investment experience (years)

0

20

40

0-3 3-6 6-10 10-15 15+

31

18

31

25

10

Source: Upfront Ventures survey of VCs (N=115), Jan 2017

2016 VC respondent demographics (I)

27

New investments per partner per year (excl. follow-on’s)

0

20

40

60

1 2 3-4 5-10 10+

8

38

5350

9

Number of board or observer seats per partner

0

25

50

75

0 1-3 4-6 7-10 11-14 15+

34

36

62

38

15

Source: Upfront Ventures survey of VCs (N=159), Jan 2016

Fund type

0

25

50

75

Angel Seed VC (Early) VC (Mid) VC (Late) PE Corp (blank)

1196

19

47

60

7

Fund size ($ million)

0

20

40

60

$1-20 $20-100 $300-999 $100-300 $1000+ Evergreen Personal

779

2833

47

19

2016 VC respondent demographics (II)

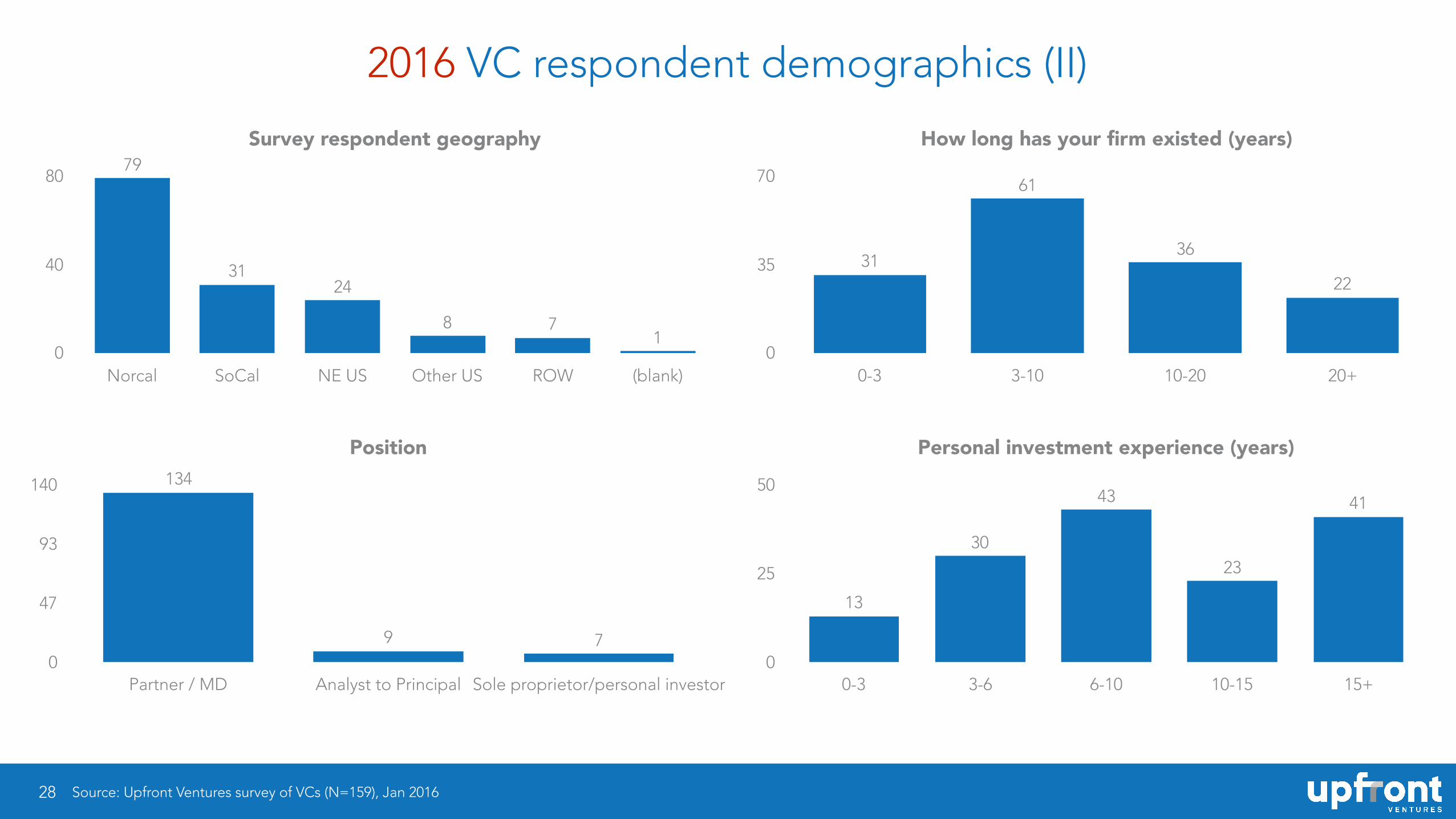

28 Source: Upfront Ventures survey of VCs (N=159), Jan 2016

Survey respondent geography

0

40

80

Norcal SoCal NE US Other US ROW (blank)

178

2431

79

Position

0

47

93

140

Partner / MD Analyst to Principal Sole proprietor/personal investor

79

134

How long has your firm existed (years)

0

35

70

0-3 3-10 10-20 20+

22

36

61

31

Personal investment experience (years)

0

25

50

0-3 3-6 6-10 10-15 15+

41

23

43

30

13