Embed Size (px)

Citation preview

Investor Presentation &

2014 Q1 Bulletin

Istanbul Stock Exchange: BRISA www.brisa.com.tr

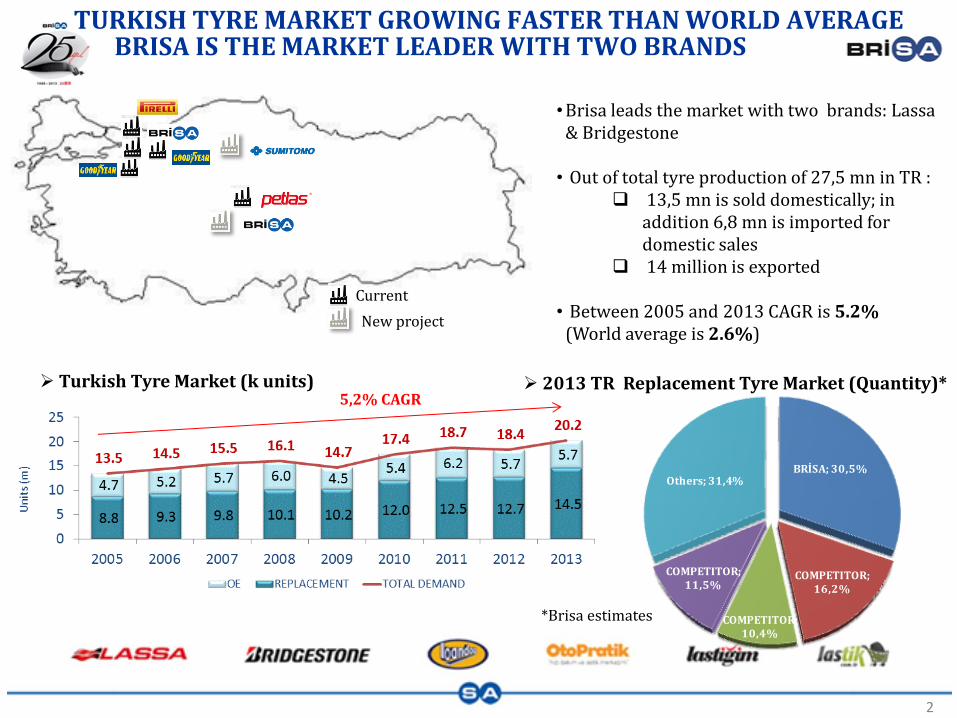

TURKISH TYRE MARKET GROWING FASTER THAN WORLD AVERAGE BRISA IS THE MARKET LEADER WITH TWO BRANDS

2

Current

2013 TR Replacement Tyre Market (Quantity)* Turkish Tyre Market (k units)

•Brisa leads the market with two brands: Lassa & Bridgestone • Out of total tyre production of 27,5 mn in TR :

13,5 mn is sold domestically; in addition 6,8 mn is imported for domestic sales

14 million is exported • Between 2005 and 2013 CAGR is 5.2%

(World average is 2.6%)

New project

*Brisa estimates

5,2% CAGR

BRİSA; 30,5%

COMPETITOR; 16,2%

COMPETITOR; 10,4%

COMPETITOR; 11,5%

Others; 31,4%

3

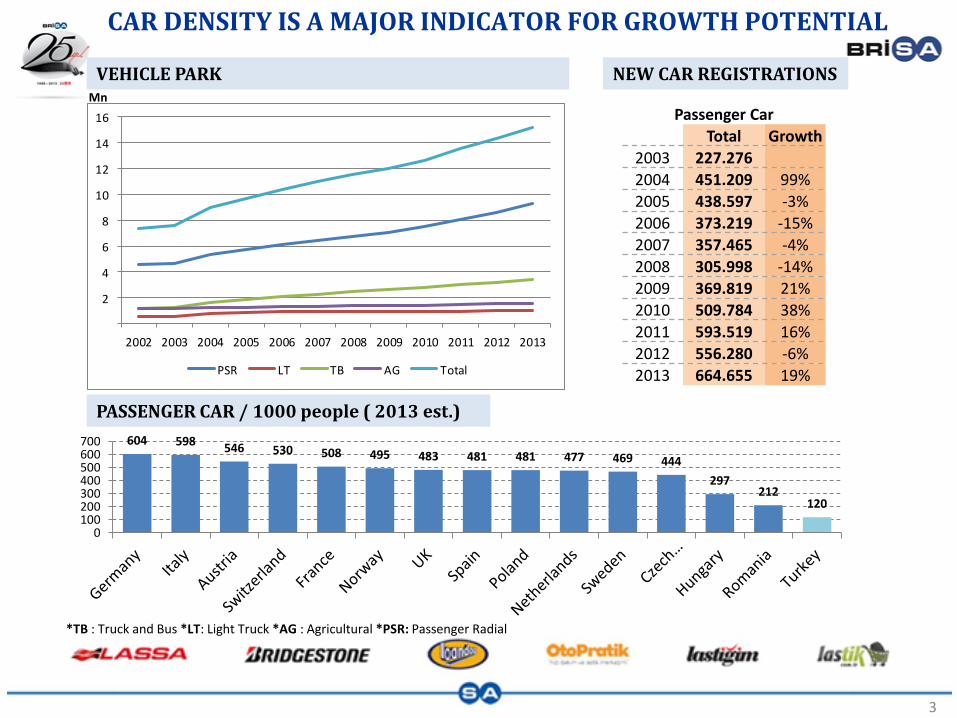

CAR DENSITY IS A MAJOR INDICATOR FOR GROWTH POTENTIAL

Mn

NEW CAR REGISTRATIONS

Passenger Car

Total Growth

2003 227.276

2004 451.209 99%

2005 438.597 -3%

2006 373.219 -15%

2007 357.465 -4%

2008 305.998 -14%

2009 369.819 21%

2010 509.784 38%

2011 593.519 16%

2012 556.280 -6%

2013 664.655 19%

VEHICLE PARK

604 598 546 530 508 495 483 481 481 477 469 444

297 212

120

0100200300400500600700

PASSENGER CAR / 1000 people ( 2013 est.)

*TB : Truck and Bus *LT: Light Truck *AG : Agricultural *PSR: Passenger Radial

2

4

6

8

10

12

14

16

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

PSR LT TB AG Total

4

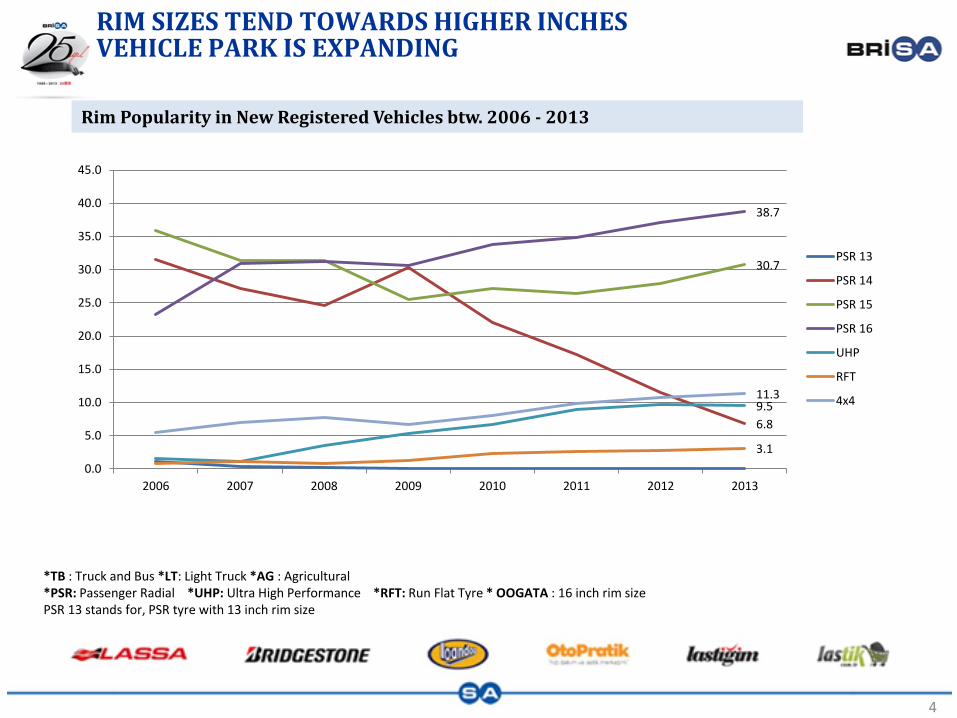

RIM SIZES TEND TOWARDS HIGHER INCHES VEHICLE PARK IS EXPANDING

*TB : Truck and Bus *LT: Light Truck *AG : Agricultural *PSR: Passenger Radial *UHP: Ultra High Performance *RFT: Run Flat Tyre * OOGATA : 16 inch rim size PSR 13 stands for, PSR tyre with 13 inch rim size

Rim Popularity in New Registered Vehicles btw. 2006 - 2013

6.8

30.7

38.7

9.5

3.1

11.3

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2006 2007 2008 2009 2010 2011 2012 2013

PSR 13

PSR 14

PSR 15

PSR 16

UHP

RFT

4x4

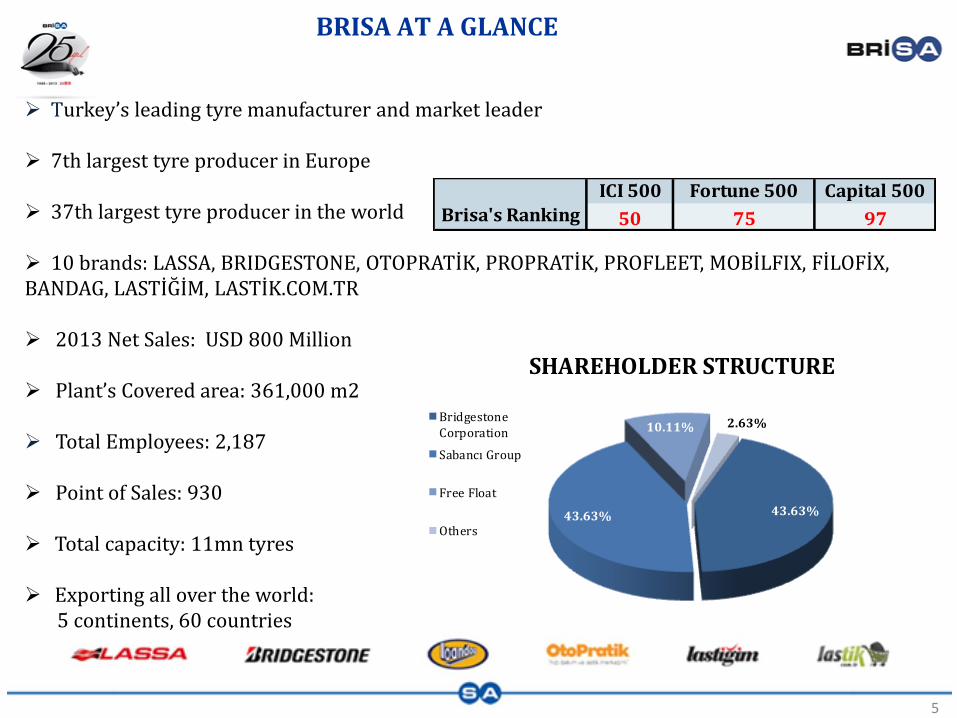

BRISA AT A GLANCE

Turkey’s leading tyre manufacturer and market leader

7th largest tyre producer in Europe

37th largest tyre producer in the world

10 brands: LASSA, BRIDGESTONE, OTOPRATİK, PROPRATİK, PROFLEET, MOBİLFIX, FİLOFİX, BANDAG, LASTİĞİM, LASTİK.COM.TR

2013 Net Sales: USD 800 Million Plant’s Covered area: 361,000 m2

Total Employees: 2,187

Point of Sales: 930

Total capacity: 11mn tyres

Exporting all over the world: 5 continents, 60 countries

5

43.63%43.63%

10.11% 2.63%

SHAREHOLDER STRUCTURE

BridgestoneCorporation

Sabancı Group

Free Float

Others

ICI 500 Fortune 500 Capital 500

Brisa's Ranking 50 75 97

PRODUCT RANGE

Passenger

Light Truck and

Commercial Vehicle

Truck and Bus

Agricultural Motorcycle Off the road Other

SALES CHANNEL

REPLACEMENT

•Dealer •Fast-fits •Fleet •OE Plaza •Key accounts •Customer Service •Mobile Service •Fleet Solutions •Retread

ORIGINAL

EQUIPMENT

•Vehicle Manufacturers •Technical properties determined together with the customer

•Technical complexity

INTERNATIONAL SALES

•60 Country •80Distributors

MAIN BRANDS

OUR BUSINESS INCLUDES B2B, B2C AND EXPORT WITH A DIVERSIFIED CUSTOMER BASE

HP

UHP

RFT

4*4

Winter

6

60% of sales ($500 mn)

15% of sales ($100 mn)

25% of sales ($200 mn)

• Forwarding to all cities • %100 Land Transport • Over 3,000 destination

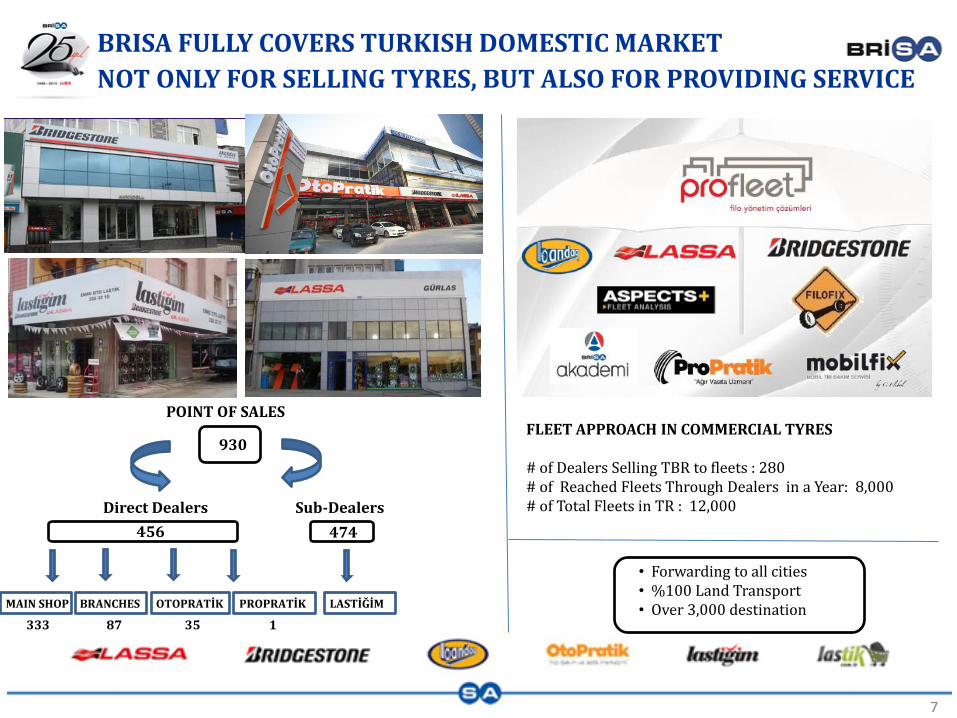

BRISA FULLY COVERS TURKISH DOMESTIC MARKET

NOT ONLY FOR SELLING TYRES, BUT ALSO FOR PROVIDING SERVICE

7

POINT OF SALES FLEET APPROACH IN COMMERCIAL TYRES # of Dealers Selling TBR to fleets : 280 # of Reached Fleets Through Dealers in a Year: 8,000 # of Total Fleets in TR : 12,000

930

Direct Dealers Sub-Dealers

474

MAIN SHOP BRANCHES OTOPRATİK PROPRATİK LASTİĞİM

333 87 35 1

456

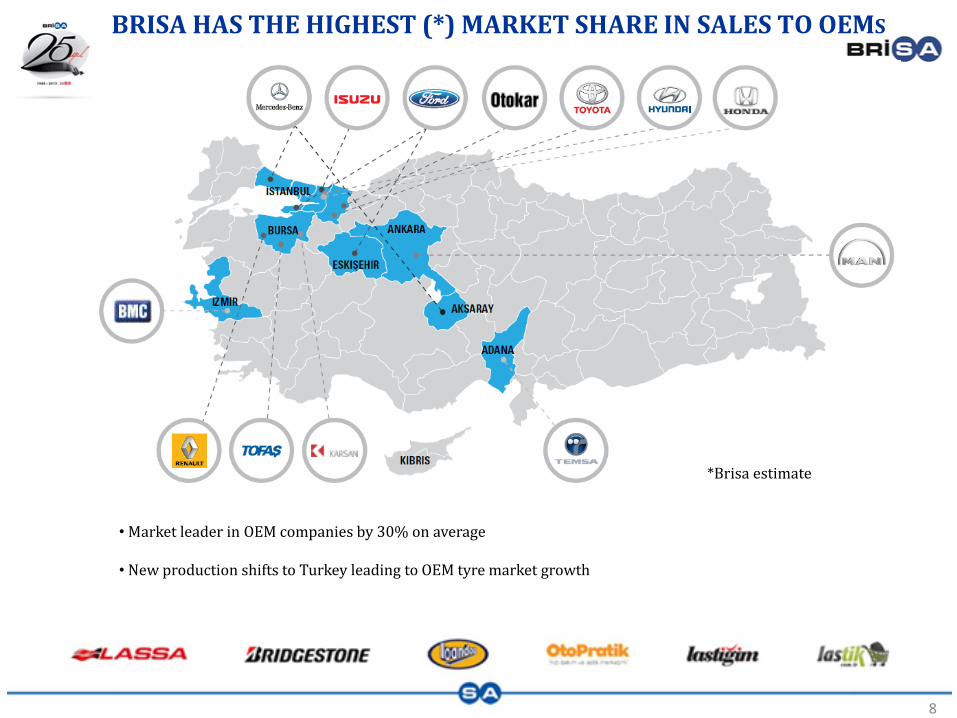

BRISA HAS THE HIGHEST (*) MARKET SHARE IN SALES TO OEMS

8

• Market leader in OEM companies by 30% on average • New production shifts to Turkey leading to OEM tyre market growth

*Brisa estimate

9

STRATEGY SETTING WITH TWO BRANDS

“Safety Tyre” Image Campaign

Image campaign based on “Durability”

Premium Positioning

Mid range Positioning

102 96120

157 144 136

0

20

40

60

80

100

120

140

160

180

2008 2009 2010 2011 2012 2013

GROWING FURTHER IN EXPORT MARKETS

10

• Over 60 Countries

• 5000 sales points with 80 distributors

• Profitable growth in international sales by mix management (product & country)

• Growth via high potential countries, new countries/customers

• Balanced customer portfolio (currency effect)

• 33% increase in sales between 2008 and 2013

• New export markets in 2011, 2012 and 2013

• Constitutes %20 of total Brisa sales (2013)

Lassa Export (mn USD)

Lassa sold countries

MARKETING ACTIVITIES IN INTERNATIONAL BUSINESS

Currently 100 shops in more than 21 countries

11

Official sponsorships

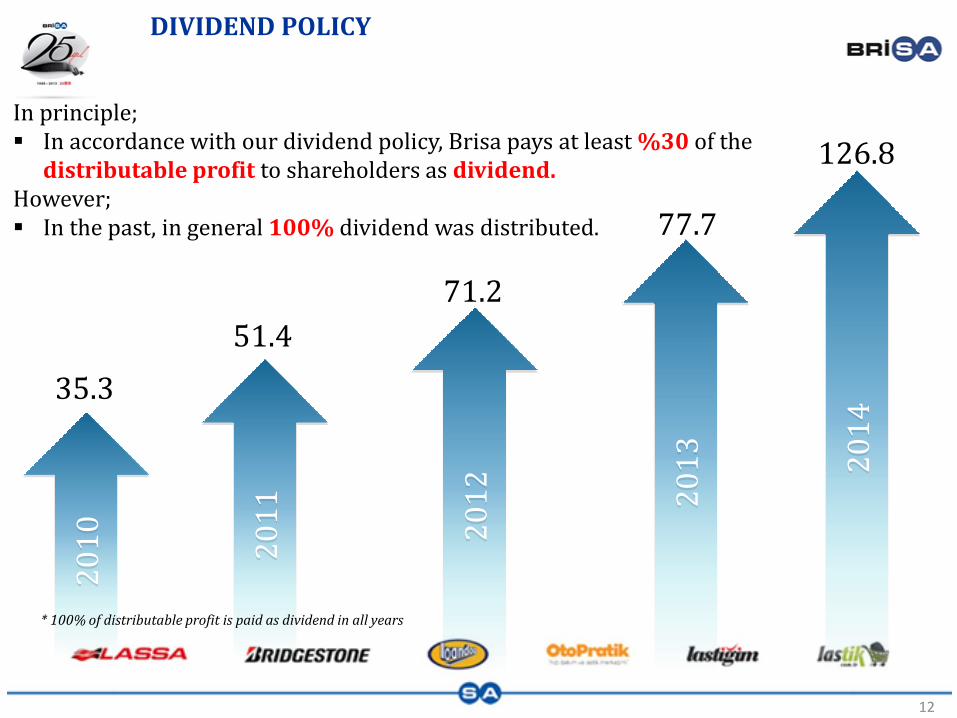

DIVIDEND POLICY

In principle; In accordance with our dividend policy, Brisa pays at least %30 of the

distributable profit to shareholders as dividend. However; In the past, in general 100% dividend was distributed.

20

10

20

11

20

12

35.3

51.4

71.2

12 2

01

3

77.7

* 100% of distributable profit is paid as dividend in all years

20

14

126.8

13

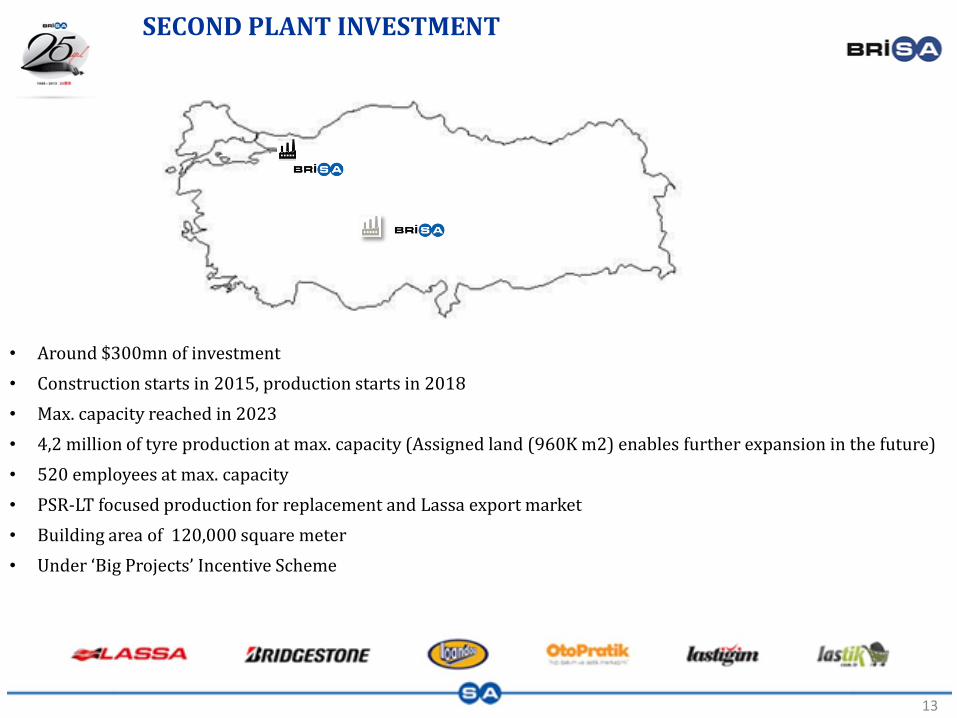

SECOND PLANT INVESTMENT

• Around $300mn of investment

• Construction starts in 2015, production starts in 2018

• Max. capacity reached in 2023

• 4,2 million of tyre production at max. capacity (Assigned land (960K m2) enables further expansion in the future)

• 520 employees at max. capacity

• PSR-LT focused production for replacement and Lassa export market

• Building area of 120,000 square meter

• Under ‘Big Projects’ Incentive Scheme

14

WHY INVEST IN BRISA...

Fast growing market: Increasing capacity of automotive manufacturers and old vehicle park

Further expansion with second plant

Access for new export markets

Strong brands, likely to benefit more strongly from growth

Focus on channel management and end-customer to secure and increase profitability

Diversified channel and customer portfolio

Continued leadership in market share, new products and services

Disclaimer Statement

The information and opinions contained in this document have been compiled or arrived at by Brisa from sources believed to be reliable and in good faith, but no representation or warranty, expressed or implied, is made as to their accuracy, completeness or correctness. All opinions and estimates contained in this document constitute the Company’s judgement as of the date of this document and are subject to change without notice. The information contained in this document is published for the assistance of recipients, but is not to be relied upon as authoritative or taken in substitution for the exercise of judgement by any recipient. The company does not accept any liability whatsoever for any direct or consequential loss arising from any use of this document or its contents.

Istanbul Stock Exchange: BRISA www.brisa.com.tr

2014 Q1 BULLETIN

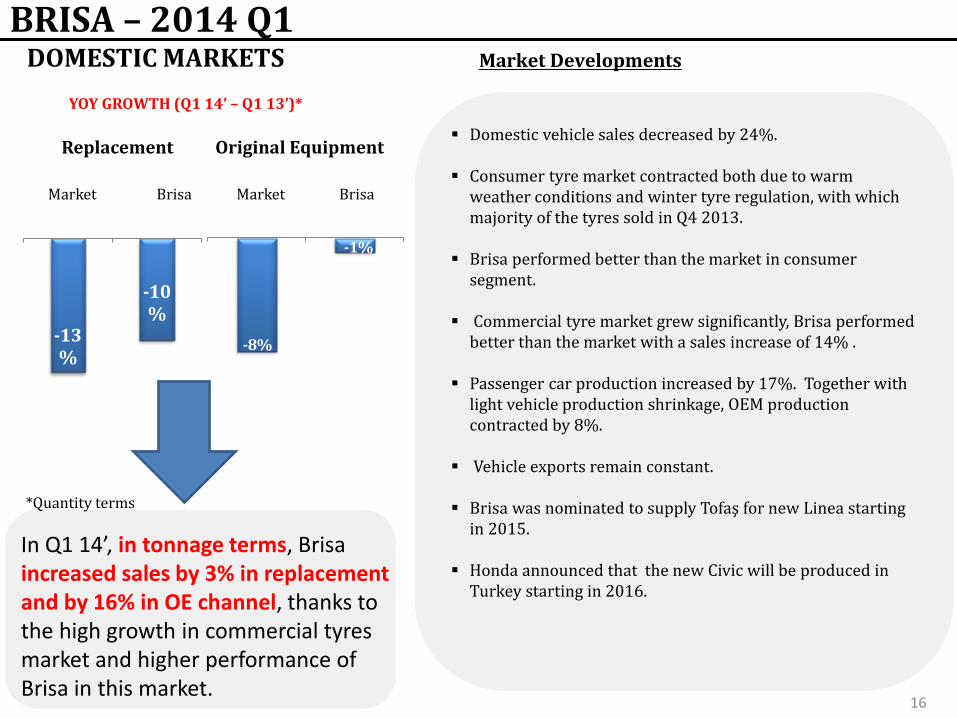

-13%

-10%

YOY GROWTH (Q1 14’ – Q1 13’)*

-8%

-1%

BRISA – 2014 Q1 DOMESTIC MARKETS Market Developments

Domestic vehicle sales decreased by 24%.

Consumer tyre market contracted both due to warm weather conditions and winter tyre regulation, with which majority of the tyres sold in Q4 2013.

Brisa performed better than the market in consumer segment.

Commercial tyre market grew significantly, Brisa performed better than the market with a sales increase of 14% .

Passenger car production increased by 17%. Together with light vehicle production shrinkage, OEM production contracted by 8%.

Vehicle exports remain constant. Brisa was nominated to supply Tofaş for new Linea starting

in 2015. Honda announced that the new Civic will be produced in

Turkey starting in 2016.

Replacement

Market

Original Equipment

Brisa Market Brisa

16

In Q1 14’, in tonnage terms, Brisa increased sales by 3% in replacement and by 16% in OE channel, thanks to the high growth in commercial tyres market and higher performance of Brisa in this market.

*Quantity terms

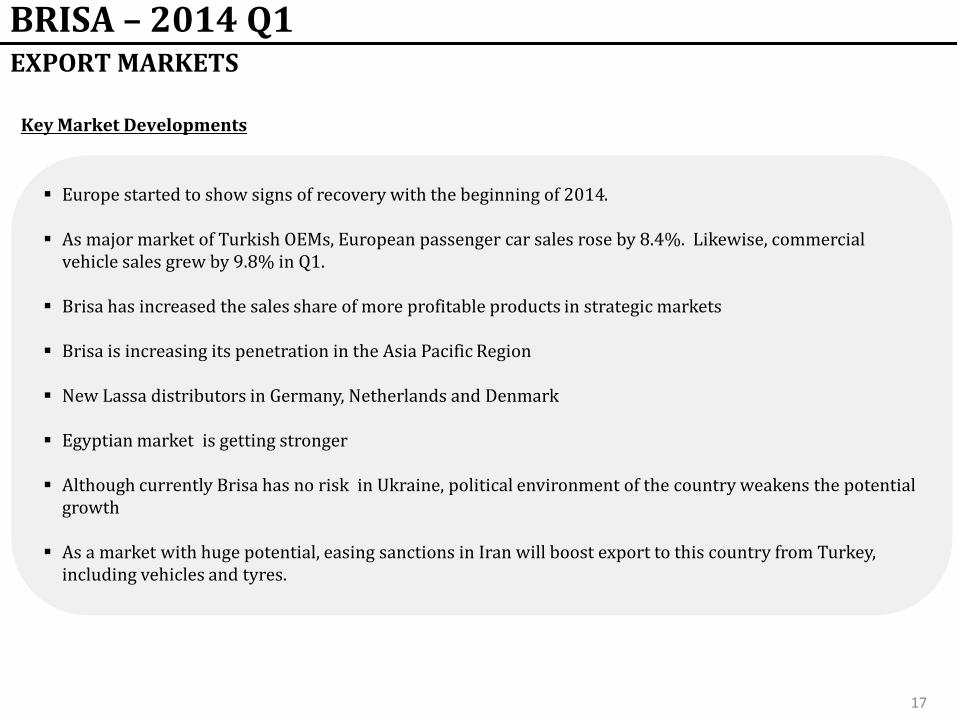

BRISA – 2014 Q1 EXPORT MARKETS

Key Market Developments

Europe started to show signs of recovery with the beginning of 2014.

As major market of Turkish OEMs, European passenger car sales rose by 8.4%. Likewise, commercial vehicle sales grew by 9.8% in Q1.

Brisa has increased the sales share of more profitable products in strategic markets

Brisa is increasing its penetration in the Asia Pacific Region

New Lassa distributors in Germany, Netherlands and Denmark

Egyptian market is getting stronger

Although currently Brisa has no risk in Ukraine, political environment of the country weakens the potential

growth

As a market with huge potential, easing sanctions in Iran will boost export to this country from Turkey, including vehicles and tyres.

17

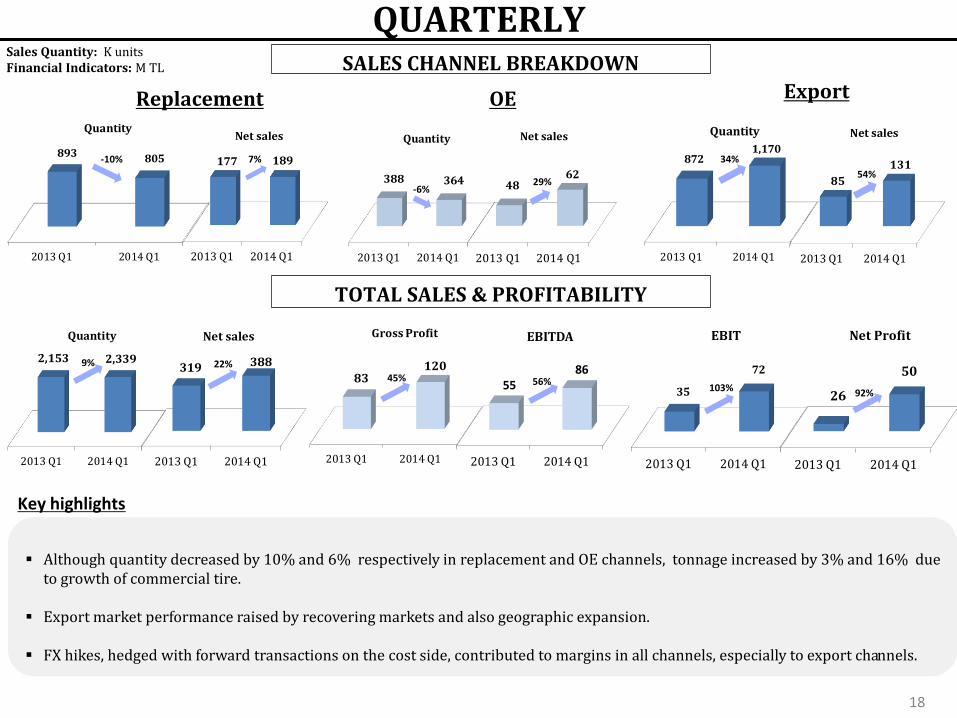

2013 Q1 2014 Q1

83120

Gross Profit

QUARTERLY

Replacement OE Export

SALES CHANNEL BREAKDOWN

TOTAL SALES & PROFITABILITY

Key highlights

Although quantity decreased by 10% and 6% respectively in replacement and OE channels, tonnage increased by 3% and 16% due

to growth of commercial tire.

Export market performance raised by recovering markets and also geographic expansion.

FX hikes, hedged with forward transactions on the cost side, contributed to margins in all channels, especially to export channels.

Sales Quantity: K units Financial Indicators: M TL

18

2013 Q1 2014 Q1

893 805

Quantity

-10%

2013 Q1 2014 Q1

177 189

Net sales

7%

2013 Q1 2014 Q1

388 364

Quantity

-6%

2013 Q1 2014 Q1

4862

Net sales

29%

2013 Q1 2014 Q1

8721,170

Quantity

34%

2013 Q1 2014 Q1

85

131

Net sales

54%

2013 Q1 2014 Q1

2,153 2,339

Quantity

9%

2013 Q1 2014 Q1

319 388

Net sales

22%

2013 Q1 2014 Q1

55 86

EBITDA

45% 56%

2013 Q1 2014 Q1

35

72

EBIT

2013 Q1 2014 Q1

26

50

Net Profit

103% 92%

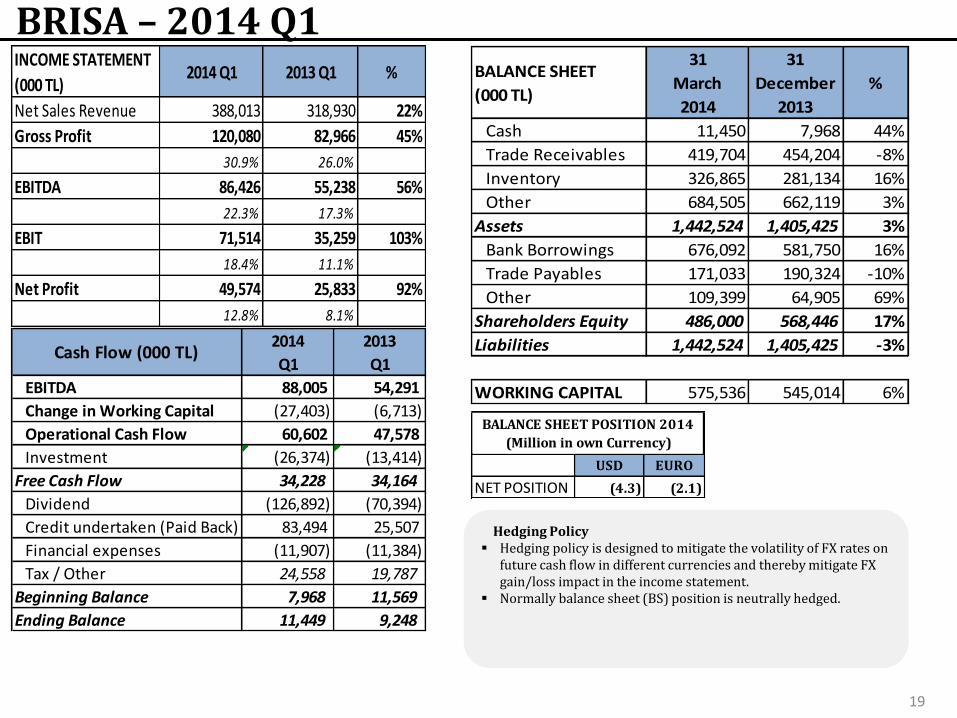

BRISA – 2014 Q1

Hedging Policy Hedging policy is designed to mitigate the volatility of FX rates on

future cash flow in different currencies and thereby mitigate FX gain/loss impact in the income statement.

Normally balance sheet (BS) position is neutrally hedged.

19

USD EURO

NET POSITION (4.3) (2.1)

BALANCE SHEET POSITION 2014

(Million in own Currency)

INCOME STATEMENT

(000 TL)2014 Q1 2013 Q1 %

Net Sales Revenue 388,013 318,930 22%

Gross Profit 120,080 82,966 45%

30.9% 26.0%

EBITDA 86,426 55,238 56%

22.3% 17.3%

EBIT 71,514 35,259 103%

18.4% 11.1%

Net Profit 49,574 25,833 92%

12.8% 8.1%

BALANCE SHEET

(000 TL)

31

March

2014

31

December

2013

%

Cash 11,450 7,968 44%

Trade Receivables 419,704 454,204 -8%

Inventory 326,865 281,134 16%

Other 684,505 662,119 3%

Assets 1,442,524 1,405,425 3%

Bank Borrowings 676,092 581,750 16%

Trade Payables 171,033 190,324 -10%

Other 109,399 64,905 69%

Shareholders Equity 486,000 568,446 17%

Liabilities 1,442,524 1,405,425 -3%

WORKING CAPITAL 575,536 545,014 6%

Cash Flow (000 TL)2014

Q1

2013

Q1

EBITDA 88,005 54,291

Change in Working Capital (27,403) (6,713)

Operational Cash Flow 60,602 47,578

Investment (26,374) (13,414)

Free Cash Flow 34,228 34,164

Dividend (126,892) (70,394)

Credit undertaken (Paid Back) 83,494 25,507

Financial expenses (11,907) (11,384)

Tax / Other 24,558 19,787

Beginning Balance 7,968 11,569

Ending Balance 11,449 9,248

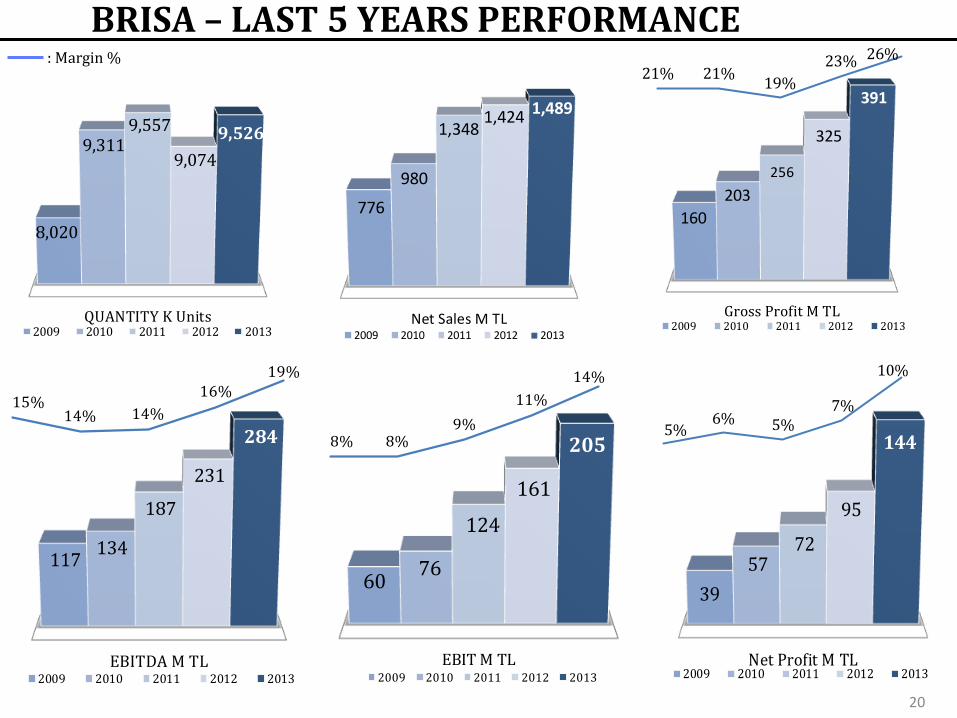

BRISA – LAST 5 YEARS PERFORMANCE

QUANTITY K Units

8,020

9,311 9,557

9,074

9,526

2009 2010 2011 2012 2013Net Sales M TL

776

980

1,348 1,424 1,489

2009 2010 2011 2012 2013

Net Profit M TL

39

57 72

95

144

2009 2010 2011 2012 2013

Gross Profit M TL

160

203

256

325

391

2009 2010 2011 2012 2013

21% 21%19%

23% 26%

EBITDA M TL

117 134

187

231

284

2009 2010 2011 2012 2013

15%14% 14%

16%19%

EBIT M TL

60 76

124

161

205

2009 2010 2011 2012 2013

8% 8%9%

11%

14%

5%6% 5%

7%

10%

: Margin %

20

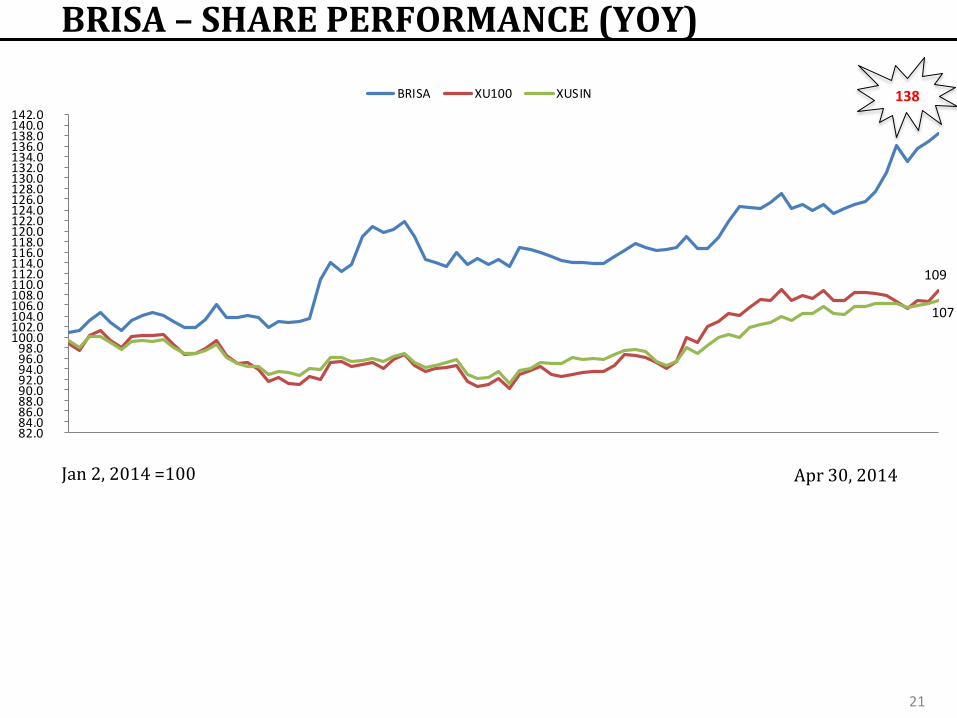

BRISA – SHARE PERFORMANCE (YOY)

Jan 2, 2014 =100 Apr 30, 2014

21

82.0 84.0 86.0 88.0 90.0 92.0 94.0 96.0 98.0

100.0 102.0 104.0 106.0 108.0 110.0 112.0 114.0 116.0 118.0 120.0 122.0 124.0 126.0 128.0 130.0 132.0 134.0 136.0 138.0 140.0 142.0

BRISA XU100 XUSIN 138

109

107

THANK YOU…

22

Contacts: Bora Çermikli Chief Financial Officer

+90 (262) 316 56 00 [email protected]

Reşat Oruç Budget and Finance Manager +90 (262) 316 57 00

[email protected] Disclaimer Statement

The information and opinions contained in this document have been compiled or arrived at by Brisa from sources believed to be reliable and in good faith, but no representation or warranty, expressed or implied, is made as to their accuracy, completeness or correctness. All opinions and estimates contained in this document constitute the Company’s judgement as of the date of this document and are subject to change without notice. The information contained in this document is published for the assistance of recipients, but is not to be relied upon as authoritative or taken in substitution for the exercise of judgement by any recipient. The company does not accept any liability whatsoever for any direct or consequential loss arising from any use of this document or its contents.

23