Embed Size (px)

Citation preview

1Moscow, 27 March 2015

Q4 AND 12M’14 US GAAP CONSOLIDATED FINANCIAL RESULTS

This document is confidential and has been prepared by NLMK (the “Company”) solely for use at the presentation of the Company and may not be reproduced, retransmitted or further distributed to any other person or published, in whole or in part, for any other purpose.

This document does not constitute or form part of any advertisement of securities, any offer or invitation to sell or issue or any solicitation of any offer to purchase or subscribe for, any shares in the Company or Global Depositary Shares (GDSs), nor shall it or any part of it nor the fact of its presentation or distribution form the basis of, or be relied on in connection with, any contract or investment decision.

No reliance may be placed for any purpose whatsoever on the information contained in this document or on assumptions made as to its completeness. No representation or warranty, express or implied, is given by the Company, its subsidiaries or any of their respective advisers, officers, employees or agents, as to the accuracy of the information or opinions or for any loss howsoever arising, directly or indirectly, from any use of this presentation or its contents.

The distribution of this document in other jurisdictions may be restricted by law and any person into whose possession this document comes should inform themselves about, and observe, any such restrictions.

This document may include forward-looking statements. These forward-looking statements include matters that are not historical facts or statements regarding the Company’s intentions, beliefs or current expectations concerning, among other things, the Company’s results of operations, financial condition, liquidity, prospects, growth, strategies, and the industry in which the Company operates. By their nature, forwarding-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. The Company cautions you that forward-looking statements are not guarantees of future performance and that the Company’s actual results of operations, financial condition and liquidity and the development of the industry in which the Company operates may differ materially from those made in or suggested by the forward-looking statements contained in this document. In addition, even if the Company’s results of operations, financial condition and liquidity and the development of the industry in which the Company operates areconsistent with the forward-looking statements contained in this document, those results or developments may not be indicative of results or developments in future periods. The Company does not undertake any obligation to review or confirm analysts’ expectations or estimates or to update any forward-looking statements to reflect events that occur or circumstances that arise after the date of this presentation.

By attending this presentation you agree to be bound by the foregoing terms.

2

DISCLAIMER

CONTENT

1. Key results

2. Financial highlights

3. Segment results

4. Annex

3

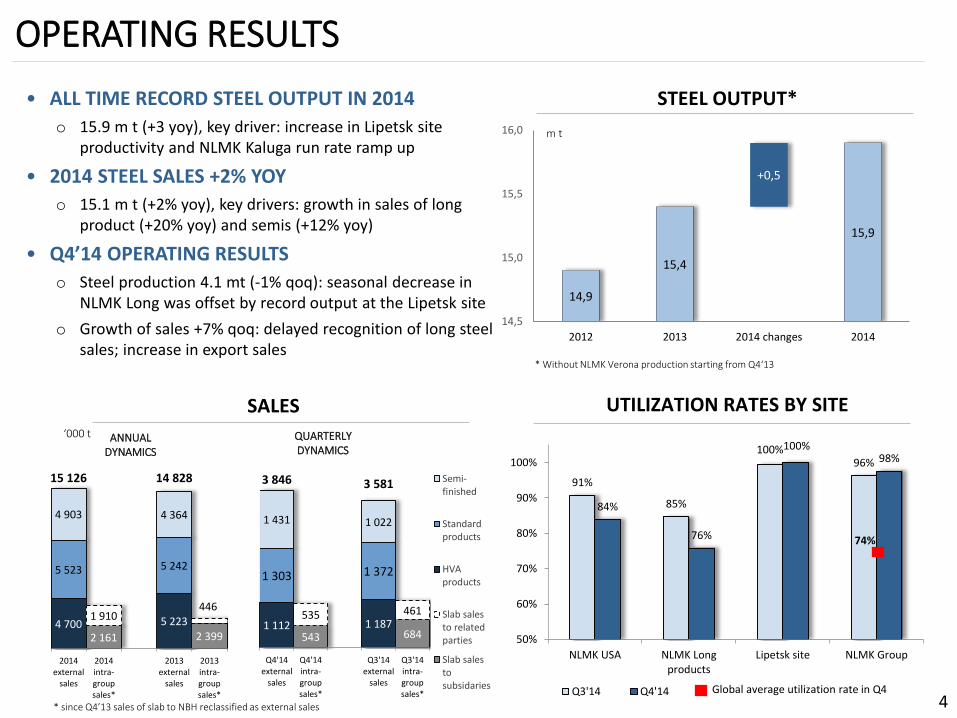

OPERATING RESULTS

• ALL TIME RECORD STEEL OUTPUT IN 2014

o 15.9 m t (+3 yoy), key driver: increase in Lipetsk site productivity and NLMK Kaluga run rate ramp up

• 2014 STEEL SALES +2% YOY

o 15.1 m t (+2% yoy), key drivers: growth in sales of long product (+20% yoy) and semis (+12% yoy)

• Q4’14 OPERATING RESULTS

o Steel production 4.1 mt (-1% qoq): seasonal decrease in NLMK Long was offset by record output at the Lipetsk site

o Growth of sales +7% qoq: delayed recognition of long steel sales; increase in export sales

4

STEEL OUTPUT*

m t

14,9

15,4

15,9

+0,5

14,5

15,0

15,5

16,0

2012 2013 2014 changes 2014

91%

85%

100%96%

84%

76%

100%98%

50%

60%

70%

80%

90%

100%

NLMK USA NLMK Longproducts

Lipetsk site NLMK Group

Q3'14 Q4'14 Global average utilization rate in Q4

74%

UTILIZATION RATES BY SITE

* Without NLMK Verona production starting from Q4‘13

SALES

543 684

535 4611 112 1 187

1 303 1 372

1 431 1 022

3 846 3 581

Q4'14external

sales

Q4'14intra-groupsales*

Q3'14external

sales

Q3'14intra-groupsales*

Semi-finished

Standardproducts

HVAproducts

Slab salesto relatedparties

Slab salestosubsidaries

‘000 t

2 161 2 3994 700 5 223

5 523 5 242

4 903 4 364

1 910446

15 126 14 828

2014external

sales

2014intra-groupsales*

2013external

sales

2013intra-groupsales*

ANNUAL DYNAMICS

QUARTERLY DYNAMICS

* since Q4’13 sales of slab to NBH reclassified as external sales

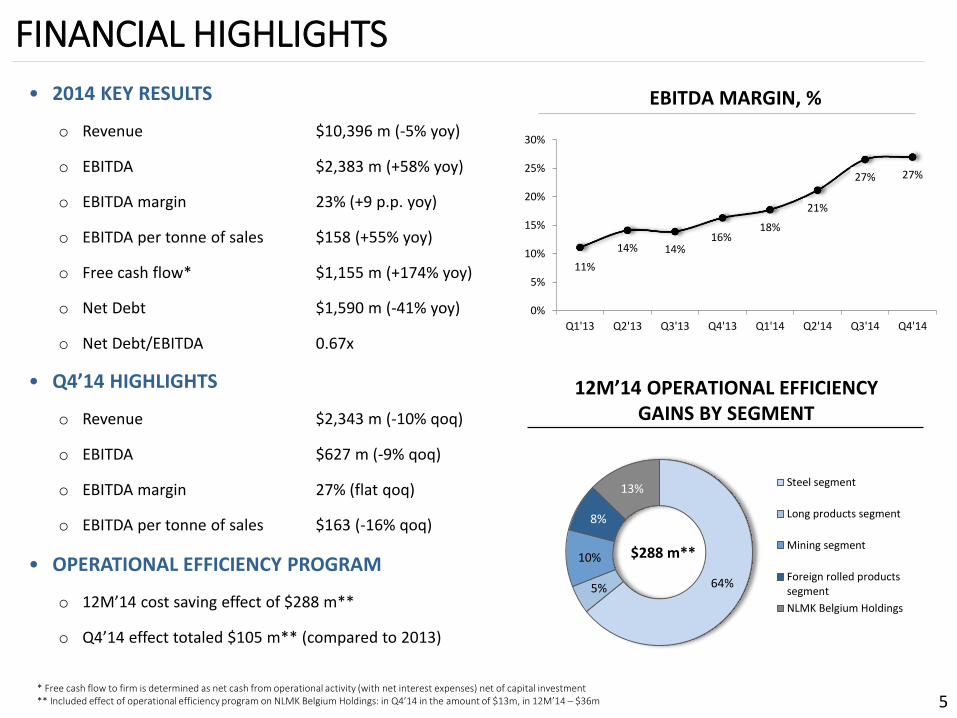

FINANCIAL HIGHLIGHTS

5

• 2014 KEY RESULTS

o Revenue $10,396 m (-5% yoy)

o EBITDA $2,383 m (+58% yoy)

o EBITDA margin 23% (+9 p.p. yoy)

o EBITDA per tonne of sales $158 (+55% yoy)

o Free cash flow* $1,155 m (+174% yoy)

o Net Debt $1,590 m (-41% yoy)

o Net Debt/EBITDA 0.67х

• Q4’14 HIGHLIGHTS

o Revenue $2,343 m (-10% qoq)

o EBITDA $627 m (-9% qoq)

o EBITDA margin 27% (flat qoq)

o EBITDA per tonne of sales $163 (-16% qoq)

• OPERATIONAL EFFICIENCY PROGRAM

o 12M’14 cost saving effect of $288 m**

o Q4’14 effect totaled $105 m** (compared to 2013)

EBITDA MARGIN, %

11%

14% 14%16%

18%

21%

27% 27%

0%

5%

10%

15%

20%

25%

30%

Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

* Free cash flow to firm is determined as net cash from operational activity (with net interest expenses) net of capital investment** Included effect of operational efficiency program on NLMK Belgium Holdings: in Q4’14 in the amount of $13m, in 12M’14 – $36m

12M’14 OPERATIONAL EFFICIENCY GAINS BY SEGMENT

64%5%

10%

8%

13%Steel segment

Long products segment

Mining segment

Foreign rolled productssegment

NLMK Belgium Holdings

$288 m**

Q1’15 OUTLOOK

• MARKET

o Russia

◦ Consumption growth (+2% yoy in January-February 2015) on the back of trader restocking and increased demand for pipe products (+13% yoy in January-February 2015)

◦ Seasonal slowdown in the construction sector

◦ Decrease in import deliveries by 30% yoy

◦ Decrease in prices denominated in dollars by 10% qoq due to ruble devaluation and the increase in ruble prices during the quarter

o Europe: stable demand for steel products

o USA: weakening business activity and steel demand

• OPERATIONAL RESULTS

o Stable operational results qoq expected

6

CONTENT

1. Key results

2. Financial highlights

3. Segment results

4. Annex

7

1 757

1 505

252

121149

230

125

2 383

EBITDA2013

Efficiencyprogram**

Volumeand

structure

Spreadand costinflation

FXeffect

NBHdeconso-lidation

EBITDA2014

395411

383361 364

348329

349

310 308295

225

21 22 21 23 23 22 23 22 19 18 1914

0

20

40

60

80

100

100

150

200

250

300

350

400

450

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Slab cash cost(Lipetsk site)

Iron ore concentrate cash cost(SGOK, rh)

2014 PROFITABILITY ANALYSIS

8

• EBITDA 2014: $2 383 M (+58% YOY)

o (+) Efficiency program

o (+) Increase of sales volume by 2% yoy

o (+) Widening of spread between prices of finished products and raw materials

o (+) Devaluation of Russian ruble FX rate

• EBITDA 2014 PER TONNE: $158/t (+55% YOY)

• REDUCTION OF SLAB AND IRON ORE CASH COST

o Positive effect of operational efficiency program

o Increase of production volumes

EBITDA PER TONNE OF SALES

112

156

127

106

85

106 102 115

121

155

193

163

400

450

500

550

600

650

700

50

100

150

200

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

EBITDA per tonne of sales Annual average HRC price(rh)*

$/t

EBITDA ANALYSIS 2014/2013

$m

$/t

* HRC price – export from Russia, FOB Black sea. Source: Metal Bulletin

CASH COST OF IRON ORE AND SLABS$/t $/t

**Doesn’t include of NBH effect in the amount of $36 m. Cumulative effect - $288 m

Q4’14 PROFITABILITY ANALYSIS

9

• Q4’14 EBITDA: $627 M (-9% QOQ)

• EBITDA MARGIN IN Q4’14: 27%

• STEEL SEGMENT: EBITDA MARGIN 30%

o (+) Operational efficiency gains

o (+) Increased demand for ordinary grades on export markets

o (+) Russian ruble devaluation

• LONG PRODUCTS SEGMENT: SEASONAL DECLINE IN DEMAND

o (-) Seasonal narrowing of long product/scrap spreads

o (-) Russian ruble devaluation

• MINING SEGMENT: NEGATIVE PRICE TREND

o (-) Decrease in iron ore prices

o (-) Russian ruble devaluation

• FOREIGN ROLLED PRODUCTS SEGMENT: WEAKENING DEMAND ON THE USA MARKET

o (-) Weakening of demand in the USA

o (+) Growth of EU steel consumption

EBITDA CHANGE BY SEGMENT (QOQ)

$ m

551

13

101 19

-57

627

300

400

500

600

700

800

Stee

l seg

men

t

Lon

g p

rod

uct

sse

gmen

t

Min

ing

segm

ent

Fore

ign

ro

lled

pro

du

cts

segm

ent

Oth

er a

nd

inte

rseg

men

tal

op

erat

ion

s

Q4

'14

$ m

SEGMENT CONTRIBUTION TO EBITDA

693

96-64

-44-17

-38

627

400

500

600

700

800

Q3

'14

Stee

l seg

men

t

Lon

g p

rod

uct

sse

gmen

t

Min

ing

segm

ent

Fore

ign

ro

lled

pro

du

cts

segm

ent

Oth

er a

nd

inte

rseg

men

tal

op

erat

ion

s

Q4

'14

EBITDA

Working capital changes

Other non-cash operations*

Income tax

Net interest **

NET OPERATING CASH FLOW

Capital expenditures ***

FREE CASH FLOW TO THE FIRM

Net repayments of borrowings/attraction of funds

FREE CASH FLOW TO EQUITY

Change in deposits and financial investment

Dividends

FX rate change

CHANGE IN CASH

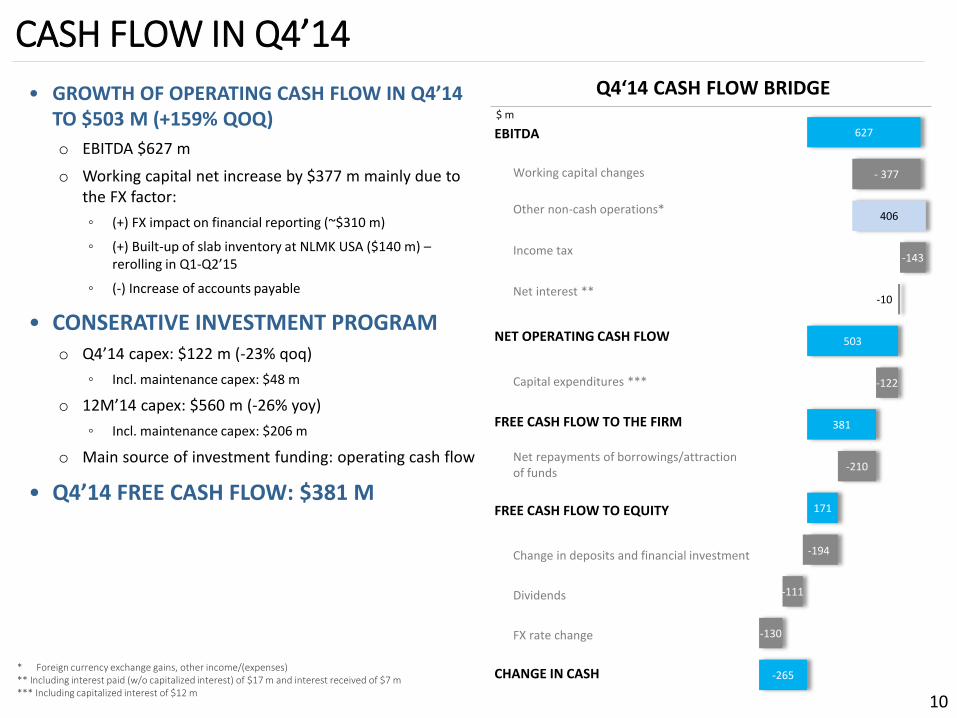

CASH FLOW IN Q4’14

10

Q4‘14 CASH FLOW BRIDGE• GROWTH OF OPERATING CASH FLOW IN Q4’14 TO $503 M (+159% QOQ)

o EBITDA $627 m

o Working capital net increase by $377 m mainly due to the FX factor:

◦ (+) FX impact on financial reporting (~$310 m)

◦ (+) Built-up of slab inventory at NLMK USA ($140 m) –rerolling in Q1-Q2’15

◦ (-) Increase of accounts payable

• CONSERATIVE INVESTMENT PROGRAM o Q4’14 capex: $122 m (-23% qoq)

◦ Incl. maintenance capex: $48 m

o 12M’14 capex: $560 m (-26% yoy)

◦ Incl. maintenance capex: $206 m

o Main source of investment funding: operating cash flow

• Q4’14 FREE CASH FLOW: $381 M

$ m

* Foreign currency exchange gains, other income/(expenses)** Including interest paid (w/o capitalized interest) of $17 m and interest received of $7 m*** Including capitalized interest of $12 m

-265

-130

-111

-194

171

-210

381

-122

503

-10

-143

406

- 377

627

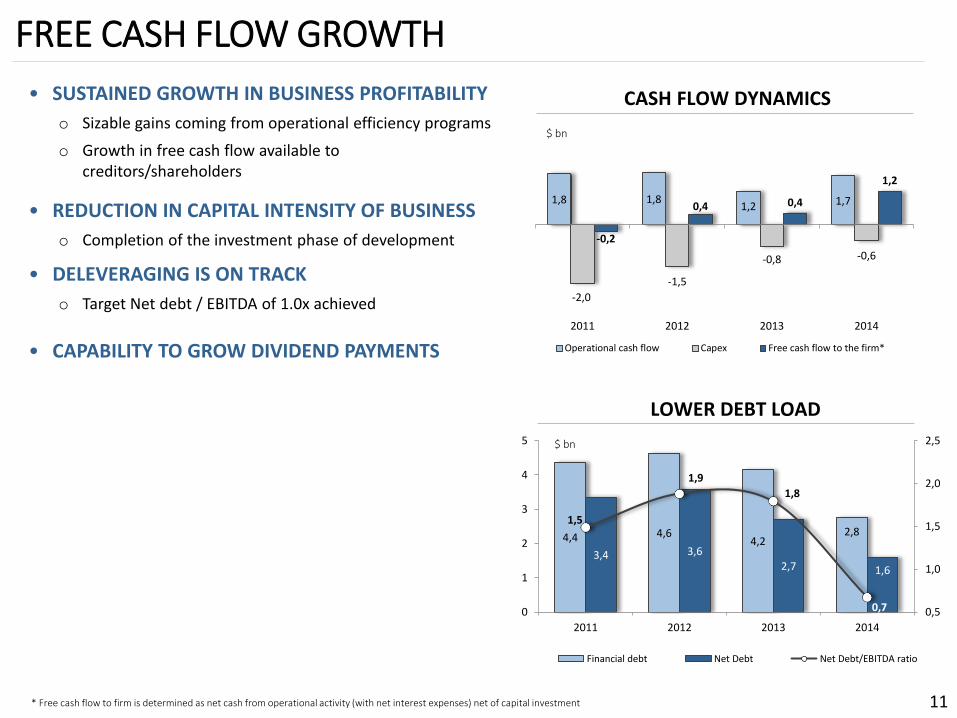

FREE CASH FLOW GROWTH

11

• SUSTAINED GROWTH IN BUSINESS PROFITABILITY

o Sizable gains coming from operational efficiency programs

o Growth in free cash flow available to creditors/shareholders

• REDUCTION IN CAPITAL INTENSITY OF BUSINESS

o Completion of the investment phase of development

• DELEVERAGING IS ON TRACK

o Target Net debt / EBITDA of 1.0x achieved

• CAPABILITY TO GROW DIVIDEND PAYMENTS

1,8 1,81,2 1,7

-2,0

-1,5

-0,8 -0,6

-0,2

0,4 0,4

1,2

2011 2012 2013 2014

Operational cash flow Capex Free cash flow to the firm*

CASH FLOW DYNAMICS

$ bn

4,4 4,64,2

2,8

3,4 3,62,7 1,6

1,5

1,9

1,8

0,7 0,5

1,0

1,5

2,0

2,5

0

1

2

3

4

5

2011 2012 2013 2014

Financial debt Net Debt Net Debt/EBITDA ratio

LOWER DEBT LOAD

$ bn

* Free cash flow to firm is determined as net cash from operational activity (with net interest expenses) net of capital investment

DEBT POSITION

12

• DROP IN DEBT AND HIGH LIQUIDITY LEVEL

o Net Debt: $1.59 bn (-12% qoq, -41% yoy)

o Total debt: $2.76 bn (-16% qoq, -34% yoy)

o Cash and equivalents*: $1.17 bn(-21% qoq, -20% yoy)

• NET DEBT / 12M EBITDA: 0.67x(-0.16 P. QOQ, -1.13 P. YOY)

MATURITY AND NET DEBT/EBITDA

* Cash and equivalents and short term investments

Weighted average maturity

1,93

2,15

1,87

1,80

1,39

1,14

0,830,67

0,0

0,5

1,0

1,5

2,0

2,5

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Net debt/EBITDA

Strategy 2017 target – 1.0

3,33,4

3,6

3,33,2

3,02,9

3,1

2,4

2,8

3,2

3,6

4,0

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

2,361,96

0,93 -0,29

+0,08

-0,31 0,80

0

1

2

3

4

30 Sep '14 Debt repaid Borrowedfunds

FX rate changeimpact

31 Dec '14

ST debt LT debt

CHANGE IN DEBT POSITION IN Q4’14$ bn

3.29

2.76

1 170767

1 868

134191 247 195

0

1 000

2 000

3 000

4 000

Liquid assets Q1'15 Q2 '15 Q3 '15 Q4 '15 2015

767

292 276

816

568

$0

$200

$400

$600

$800

$1 000

2015 2016 2017 2018 2019 andonward

Other debt

Revolving credit lines for working capital financing

Eurobonds (USD)

ECA financing and investment credits

Ruble bonds

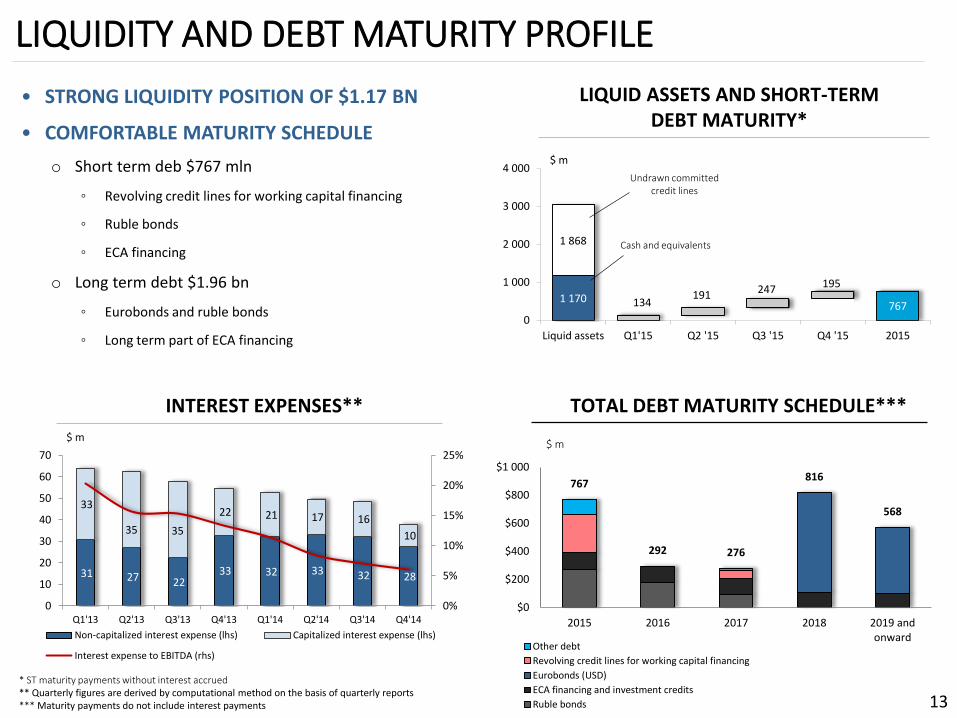

LIQUIDITY AND DEBT MATURITY PROFILE

13

• STRONG LIQUIDITY POSITION OF $1.17 BN

• COMFORTABLE MATURITY SCHEDULE

o Short term deb $767 mln

◦ Revolving credit lines for working capital financing

◦ Ruble bonds

◦ ECA financing

o Long term debt $1.96 bn

◦ Eurobonds and ruble bonds

◦ Long term part of ECA financing

TOTAL DEBT MATURITY SCHEDULE***INTEREST EXPENSES**

$ m

$ m

Undrawn committed credit lines

Cash and equivalents

LIQUID ASSETS AND SHORT-TERM DEBT MATURITY*

31 27 22 33 32 33 32 28

33

35 35

22 21 17 16

10

0%

5%

10%

15%

20%

25%

0

10

20

30

40

50

60

70

Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

Non-capitalized interest expense (lhs) Capitalized interest expense (lhs)

Interest expense to EBITDA (rhs)

* ST maturity payments without interest accrued** Quarterly figures are derived by computational method on the basis of quarterly reports*** Maturity payments do not include interest payments

$ m

STRUCTURAL IMPOVEMENT OF FINANCIAL PERFOMANCE

• Sizable effect coming from operational efficiency programs

• Leadership in low-cost production

• Profitability growing since beginning of 2013 through six quarters

• Structural reduction in capex

• Debt reduced below Strategy 2017 target level

• Capability in free cash flow growth available for distribution to shareholders

14

CONTENT

1. Key results

2. Financial highlights

3. Segment results

4. Annex

15

1,66 1,68

1,53 1,60 1,74 1,73

1,64 1,48

0,35 0,37 0,47 0,21

0,30 0,27 0,37 0,34

0,080,21 0,19 0,15

0,26 0,350,46 0,55

0,0

0,5

1,0

1,5

2,0

2,5

Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

Revenue from intercompany sales Revenue from sales to third parties

EBITDA

4%

10% 9%8%

13%18%

23%

30%

EBITDA margin

22%

21%

9%7%7%

5%

6%

10%

3%9%

Iron ore materials

Coke and coal

Scrap

Ferroalloys

Other raw materials

Electricity

Natural gas

Other energy resources

Personnel costs

Other expenses and changes in inventories

Depreciation

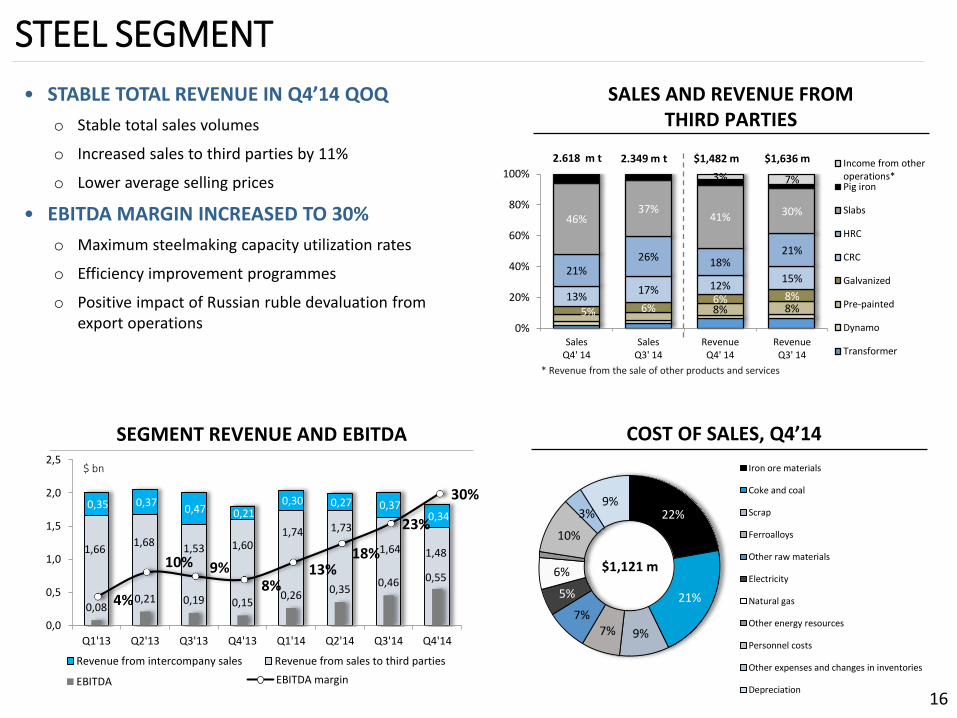

STEEL SEGMENT

• STABLE TOTAL REVENUE IN Q4’14 QOQ

o Stable total sales volumes

o Increased sales to third parties by 11%

o Lower average selling prices

• EBITDA MARGIN INCREASED TO 30%

o Maximum steelmaking capacity utilization rates

o Efficiency improvement programmes

o Positive impact of Russian ruble devaluation from export operations

COST OF SALES, Q4’14SEGMENT REVENUE AND EBITDA

SALES AND REVENUE FROM THIRD PARTIES

$ bn

16

8% 8%5% 6%6% 8%13%

17% 12%15%

21%26% 18%

21%

46%37%

41% 30%

3% 7%

0%

20%

40%

60%

80%

100%

SalesQ4' 14

SalesQ3' 14

RevenueQ4' 14

RevenueQ3' 14

Income from otheroperations*Pig iron

Slabs

HRC

CRC

Galvanized

Pre-painted

Dynamo

Transformer

2.618 m t $1,482 m

* Revenue from the sale of other products and services

2.349 m t $1,636 m

$1,121 m

288 314355 371 337

430 378302

59

113 114102

57

101115

94

20 2340

12 752

77

130

70

140

210

280

350

420

490

560

Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

Revenue from intra-group sales Revenue from third parties EBITDA

6%5%

8%

3% 2%

10%

16%

3%

EBITDA margin

56%

2%1%

5%

8%

22%

6%

Scrap

Ferroalloys

Other raw materials

Electricity

Personnel

Other expenses

Depreciation

$358 m

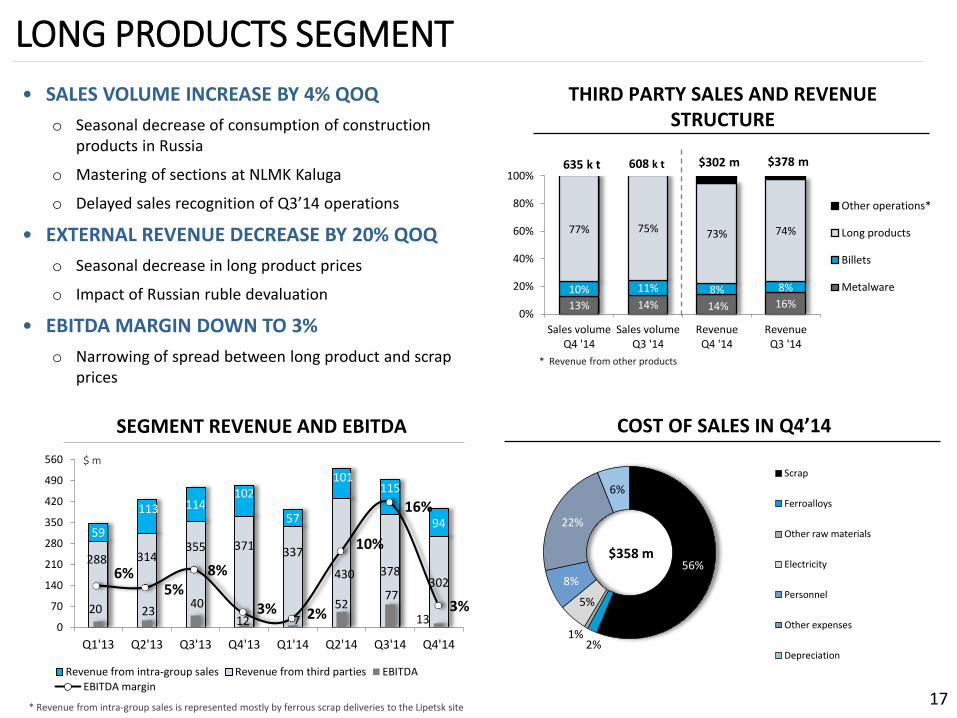

LONG PRODUCTS SEGMENT

• SALES VOLUME INCREASE BY 4% QOQ

o Seasonal decrease of consumption of construction products in Russia

o Mastering of sections at NLMK Kaluga

o Delayed sales recognition of Q3’14 operations

• EXTERNAL REVENUE DECREASE BY 20% QOQ

o Seasonal decrease in long product prices

o Impact of Russian ruble devaluation

• EBITDA MARGIN DOWN TO 3%

o Narrowing of spread between long product and scrap prices

SEGMENT REVENUE AND EBITDA

THIRD PARTY SALES AND REVENUE STRUCTURE

$ m

17

COST OF SALES IN Q4’14

* Revenue from intra-group sales is represented mostly by ferrous scrap deliveries to the Lipetsk site

13% 14% 14% 16%10% 11% 8% 8%

77% 75% 73% 74%

0%

20%

40%

60%

80%

100%

Sales volumeQ4 '14

Sales volumeQ3 '14

RevenueQ4 '14

RevenueQ3 '14

Other operations*

Long products

Billets

Metalware

608 k t $378 m

* Revenue from other products

$302 m635 k t

92 100 86 94 88 117

70 70

245 249 226

259 229 189

178

126 215 227190

228 209185

145101

0

100

200

300

400

500

Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14 Q4 '14Revenue from intersegmental salesRevenue from third partiesEBITDA

64%65% 61%

65%

66%

60%58%

51%

EBITDA margin

6%

21%

1%6%

27%

20%

19%

Raw materials

Electricity

Natural gas

Other energy resources

Personnel

Other expenses

Depreciation

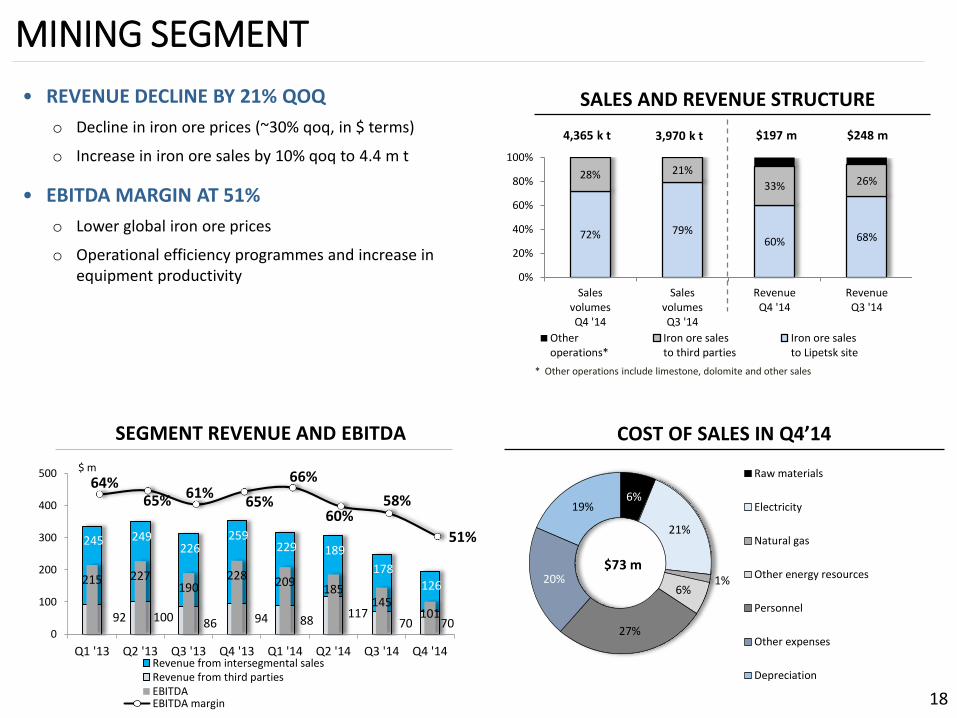

MINING SEGMENT

• REVENUE DECLINE BY 21% QOQ

o Decline in iron ore prices (~30% qoq, in $ terms)

o Increase in iron ore sales by 10% qoq to 4.4 m t

• EBITDA MARGIN AT 51%

o Lower global iron ore prices

o Operational efficiency programmes and increase in equipment productivity

SALES AND REVENUE STRUCTURE

18

COST OF SALES IN Q4’14

72% 79%60% 68%

28% 21%

33% 26%

0%

20%

40%

60%

80%

100%

SalesvolumesQ4 '14

SalesvolumesQ3 '14

RevenueQ4 '14

RevenueQ3 '14

Otheroperations*

Iron ore salesto third parties

Iron ore salesto Lipetsk site

3,970 k t $248 m$197 m4,365 k t

* Other operations include limestone, dolomite and other sales

SEGMENT REVENUE AND EBITDA

$ m

$73 m

817730 750

445 471533 523 488

-26 -62 -35 30 23 19 36 19

-3%

-9%

-5%

7%5%

4%

7%

4%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-200

0

200

400

600

800

1 000

Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14 Q4 '14

Revenue EBITDA EBITDA margin (r.h.)

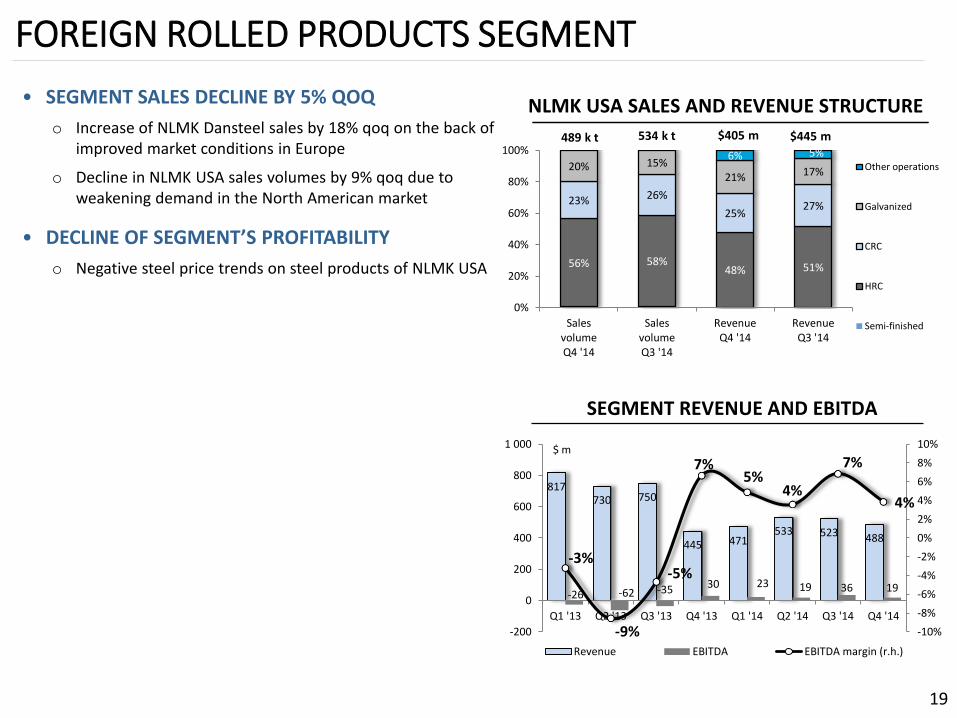

FOREIGN ROLLED PRODUCTS SEGMENT

• SEGMENT SALES DECLINE BY 5% QOQ

o Increase of NLMK Dansteel sales by 18% qoq on the back of improved market conditions in Europe

o Decline in NLMK USA sales volumes by 9% qoq due to weakening demand in the North American market

• DECLINE OF SEGMENT’S PROFITABILITY

o Negative steel price trends on steel products of NLMK USA

NLMK USA SALES AND REVENUE STRUCTURE

19

$ m

SEGMENT REVENUE AND EBITDA

56% 58%48% 51%

23% 26%

25%27%

20% 15%21% 17%

6% 5%

0%

20%

40%

60%

80%

100%

SalesvolumeQ4 '14

SalesvolumeQ3 '14

RevenueQ4 '14

RevenueQ3 '14

Other operations

Galvanized

CRC

HRC

Semi-finished

534 k t $445 m$405 m489 k t

APPENDICES

20

SALES STRUCTURE

21

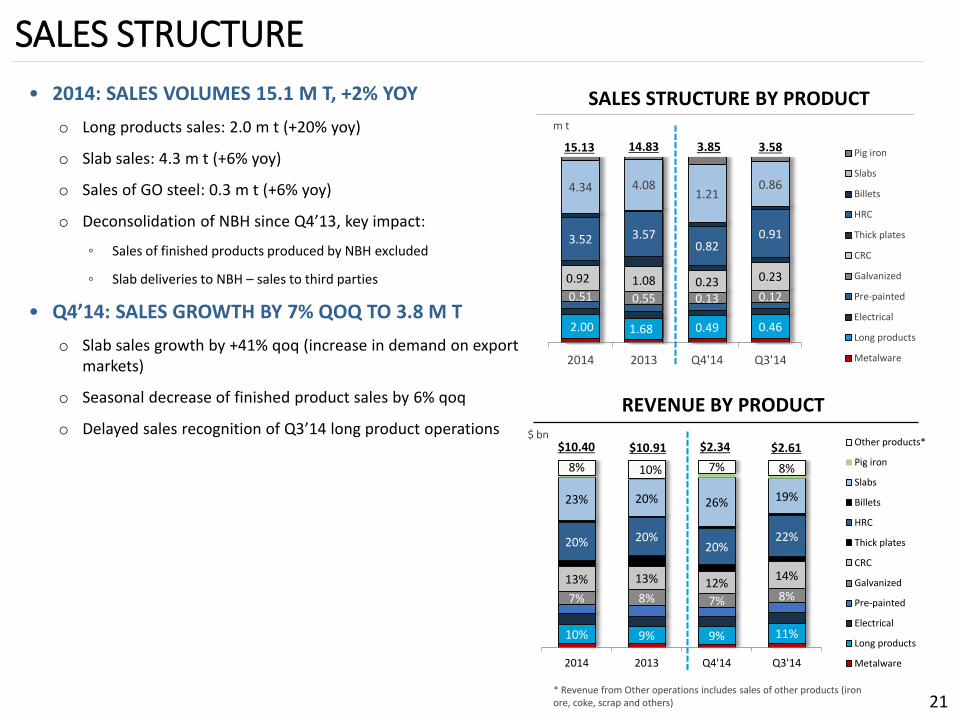

• 2014: SALES VOLUMES 15.1 M T, +2% YOY

o Long products sales: 2.0 m t (+20% yoy)

o Slab sales: 4.3 m t (+6% yoy)

o Sales of GO steel: 0.3 m t (+6% yoy)

o Deconsolidation of NBH since Q4’13, key impact:

◦ Sales of finished products produced by NBH excluded

◦ Slab deliveries to NBH – sales to third parties

• Q4’14: SALES GROWTH BY 7% QOQ TO 3.8 M T

o Slab sales growth by +41% qoq (increase in demand on export markets)

o Seasonal decrease of finished product sales by 6% qoq

o Delayed sales recognition of Q3’14 long product operations

SALES STRUCTURE BY PRODUCT

REVENUE BY PRODUCT

2.00 1.68 0.49 0.46

0.51 0.55 0.13 0.12

0.92 1.08 0.23 0.23

3.52 3.570.82

0.91

4.34 4.081.21

0.86

2014 2013 Q4'14 Q3'14

Pig iron

Slabs

Billets

HRC

Thick plates

CRC

Galvanized

Pre-painted

Electrical

Long products

Metalware

15.13 3.85

m t

3.58

10% 9% 9% 11%

7% 8% 7% 8%

13% 13% 12%14%

20% 20%20%

22%

23% 20% 26% 19%

8% 10% 7% 8%

2014 2013 Q4'14 Q3'14

Other products*

Pig iron

Slabs

Billets

HRC

Thick plates

CRC

Galvanized

Pre-painted

Electrical

Long products

Metalware

$10.91$10.40

14.83

$ bn$2.34 $2.61

* Revenue from Other operations includes sales of other products (iron ore, coke, scrap and others)

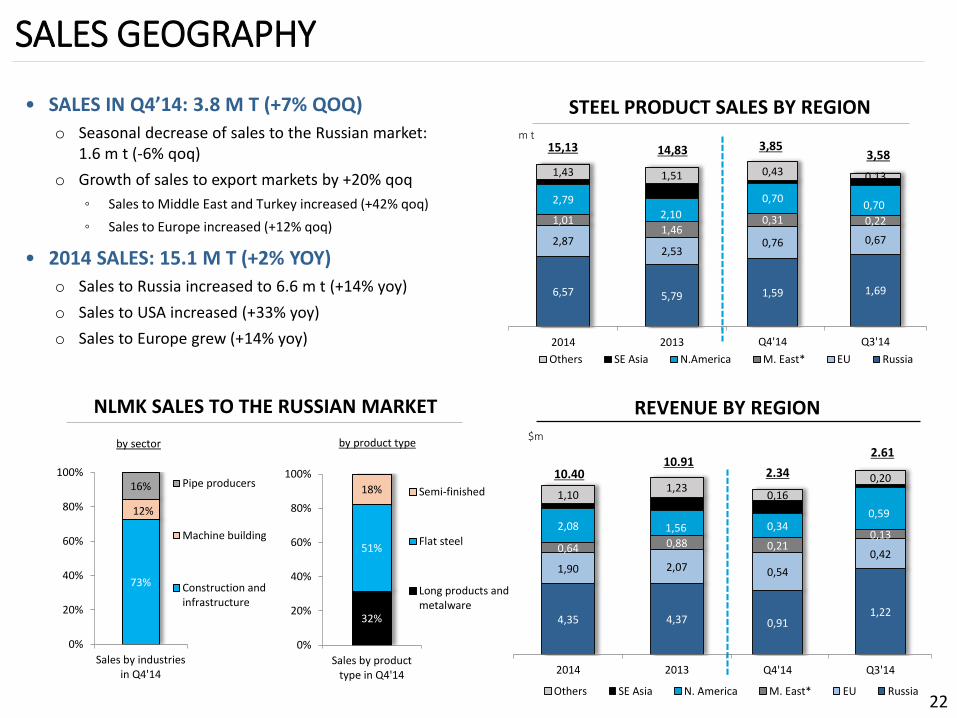

SALES GEOGRAPHY

22

• SALES IN Q4’14: 3.8 M T (+7% QOQ)

o Seasonal decrease of sales to the Russian market: 1.6 m t (-6% qoq)

o Growth of sales to export markets by +20% qoq

◦ Sales to Middle East and Turkey increased (+42% qoq)

◦ Sales to Europe increased (+12% qoq)

• 2014 SALES: 15.1 M T (+2% YOY)

o Sales to Russia increased to 6.6 m t (+14% yoy)

o Sales to USA increased (+33% yoy)

o Sales to Europe grew (+14% yoy)

NLMK SALES TO THE RUSSIAN MARKET

by sector by product type

0,911,22

0,54

0,420,21

0,130,34

0,59

0,16

0,20

Q4'14 Q3'14

Others SE Asia N. America M. East* EU Russia

4,35 4,37

1,90 2,07

0,64 0,88

2,08 1,56

1,101,23

2014 2013

1,59 1,69

0,76 0,67

0,31 0,22

0,700,70

0,43 0,13

Q4'14 Q3'14

Others SE Asia N.America M. East* EU Russia

6,57 5,79

2,872,53

1,011,46

2,792,10

1,43 1,51

2014 2013

m t

STEEL PRODUCT SALES BY REGION

REVENUE BY REGION

15,13 14,83 3,853,58

10.4010.91

2.34

2.61$m

73%

12%

16%

0%

20%

40%

60%

80%

100%

Sales by industriesin Q4'14

Pipe producers

Machine building

Construction andinfrastructure

32%

51%

18%

0%

20%

40%

60%

80%

100%

Sales by producttype in Q4'14

Semi-finished

Flat steel

Long products andmetalware

450

-26

370

-28

374

-26

346

-65

-100

0

100

200

300

400

500

Rev

enu

eQ

1'1

4

EBIT

DA

Q1

'14

Rev

enu

eQ

2'1

4

EBIT

DA

Q2

'14

Rev

enu

eQ

3'1

4

EBIT

DA

Q3

'14

Rev

enu

eQ

4'1

4

EBIT

DA

Q4

'14

FOREIGN ASSETS PERFORMANCE

23

NBH FINANCIAL RESULTS$ m

NLMK USA AND NLMK DANSTEEL ROLLED PRODUCT SALES

0,25

0,30 0,310,27

0,13 0,160,14 0,11

0,07 0,08 0,08 0,100,10 0,10

0,090,11

0,56

0,64 0,620,59

0,00

0,10

0,20

0,30

0,40

0,50

0,60

0,70

0

0,1

0,2

0,3

0,4

0,5

Q1'14 Q2'14 Q3'14 Q4'14

HRC CRC Galvanized Thick plates (NLMK Dansteel)

m t

NBH ROLLED PRODUCT SALES

0,170,15

0,16

0,20

0,02 0,02 0,01 0,01

0,09 0,080,07 0,07

0,180,16 0,17 0,17

0,450,41 0,41

0,45

0,00

0,10

0,20

0,30

0,40

0,50

0,60

0,00

0,05

0,10

0,15

0,20

0,25

Q1'14 Q2'14 Q3'14 Q4'14

HRC CRC Coated steel Thick plates

m t

SLAB SALES

0,81

0,54

0,40

0,67

0,480,43 0,46

0,53

0,11 0,12 0,11 0,09

0,370,32

0,58

0,45

1,77

1,411,54

1,75

0,00

0,50

1,00

1,50

2,00

-

0,2

0,4

0,6

0,8

1,0

1,2

1,4

Q1'14 Q2'14 Q3'14 Q4'14

To third parties NBH NLMK Dansteel NLMK USA

m t

Jan

13

Feb

13

Mar

13

Ap

r 1

3M

ay 1

3Ju

n 1

3Ju

l 13

Au

g 1

3Se

p 1

3O

ct 1

3N

ov

13

Dec

13

Jan

14

Feb

14

Mar

14

Ap

r 1

4M

ay 1

4Ju

n 1

4Ju

l 14

Au

g 1

4Se

p 1

4O

ct 1

4N

ov

14

Dec

14

Jan

15

Feb

15

Mar

15

25

35

45

55

65

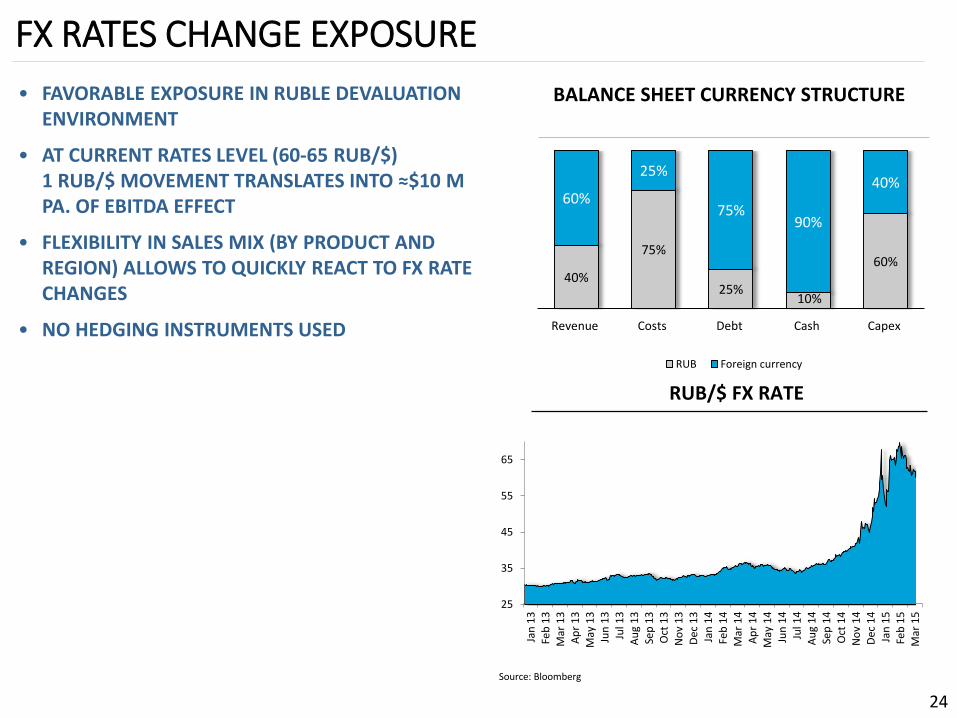

FX RATES CHANGE EXPOSURE

24

• FAVORABLE EXPOSURE IN RUBLE DEVALUATION ENVIRONMENT

• AT CURRENT RATES LEVEL (60-65 RUB/$) 1 RUB/$ MOVEMENT TRANSLATES INTO ≈$10 M PA. OF EBITDA EFFECT

• FLEXIBILITY IN SALES MIX (BY PRODUCT AND REGION) ALLOWS TO QUICKLY REACT TO FX RATE CHANGES

• NO HEDGING INSTRUMENTS USED

BALANCE SHEET CURRENCY STRUCTURE

RUB/$ FX RATE

40%

75%

25%10%

60%

60%

25%

75%90%

40%

Revenue Costs Debt Cash Capex

RUB Foreign currency

Source: Bloomberg

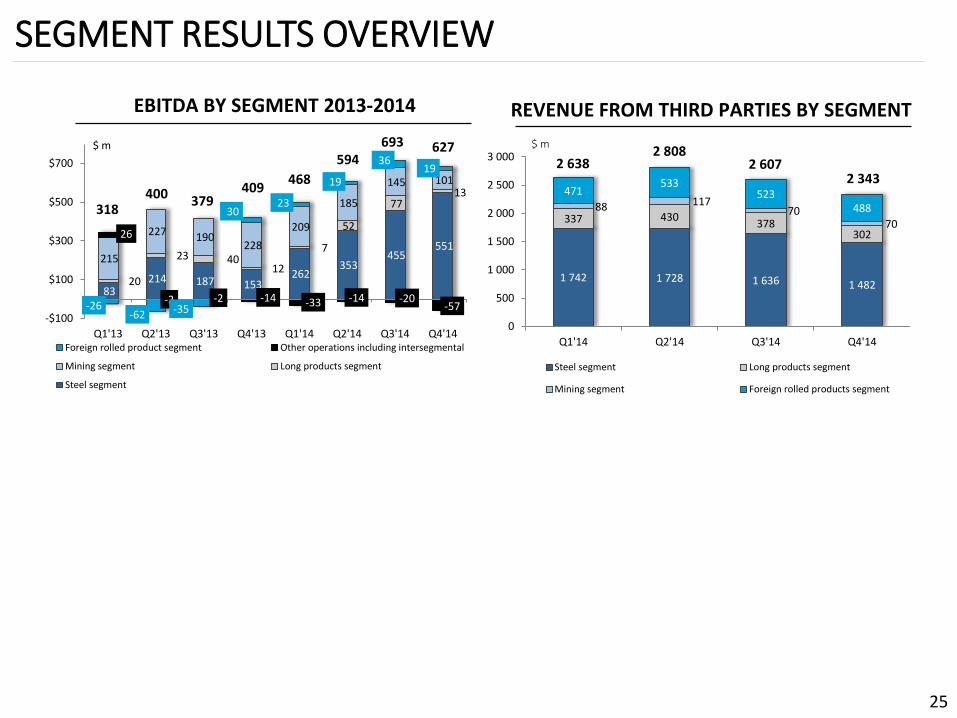

SEGMENT RESULTS OVERVIEW

REVENUE FROM THIRD PARTIES BY SEGMENT

83 214 187 153

262 353

455 551

20

23 40 12

7

52

77 13

215

227 190 228

209

185

145 101

26

-2 -2 -14 -33 -14 -20-57-26

-62 -35

30 23

19

36 19

-$100

$100

$300

$500

$700

Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14Foreign rolled product segment Other operations including intersegmental

Mining segment Long products segment

Steel segment

$ m

409379400

318

594

468

EBITDA BY SEGMENT 2013-2014

693 627

25

$ m

1 742 1 728 1 636 1 482

337 430378

302

88 11770

70

471533

523488

0

500

1 000

1 500

2 000

2 500

3 000

Q1'14 Q2'14 Q3'14 Q4'14

Steel segment Long products segment

Mining segment Foreign rolled products segment

2 6382 808

2 6072 343

EBITDA

Working capital changes

Other non-cash operations*

Income tax

Net interest **

NET OPERATING CASH FLOW

Capital expenditures ***

FREE CASH FLOW TO THE FIRM

Net repayments of borrowings/attraction of funds

FREE CASH FLOW TO EQUITY

Change in deposits and financial investment

Dividends

FX rate change

CHANGE IN CASH

CASH FLOW IN 2014

26

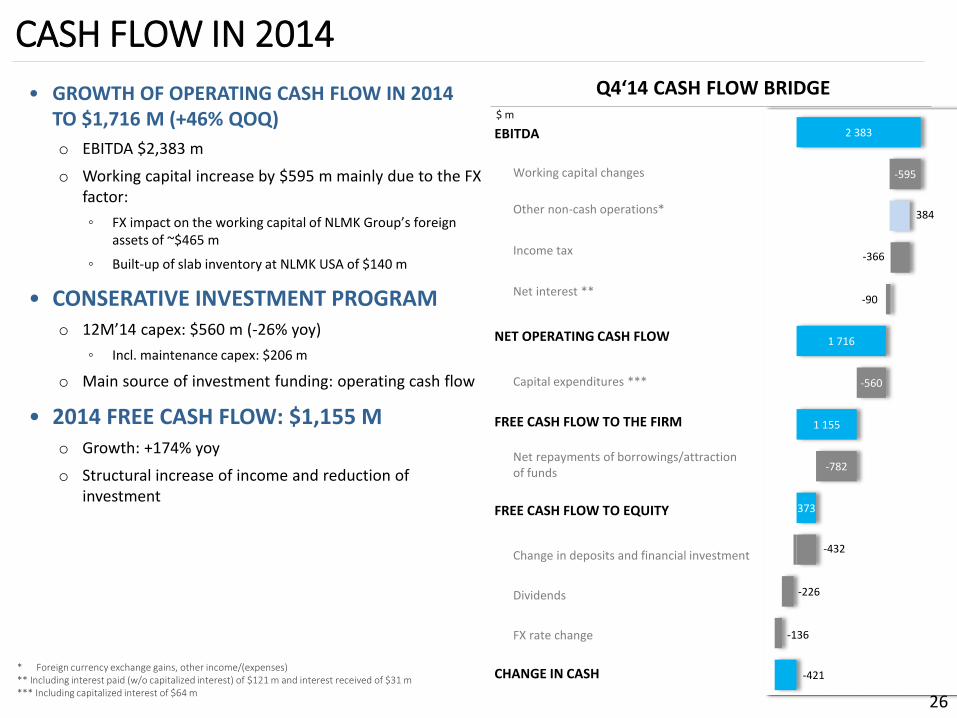

Q4‘14 CASH FLOW BRIDGE• GROWTH OF OPERATING CASH FLOW IN 2014 TO $1,716 M (+46% QOQ)

o EBITDA $2,383 m

o Working capital increase by $595 m mainly due to the FX factor:

◦ FX impact on the working capital of NLMK Group’s foreign assets of ~$465 m

◦ Built-up of slab inventory at NLMK USA of $140 m

• CONSERATIVE INVESTMENT PROGRAM o 12M’14 capex: $560 m (-26% yoy)

◦ Incl. maintenance capex: $206 m

o Main source of investment funding: operating cash flow

• 2014 FREE CASH FLOW: $1,155 M o Growth: +174% yoy

o Structural increase of income and reduction of investment

$ m

* Foreign currency exchange gains, other income/(expenses)** Including interest paid (w/o capitalized interest) of $121 m and interest received of $31 m*** Including capitalized interest of $64 m

-421

-136

-226

-432

373

-782

1 155

-560

1 716

-90

-366

384

-595

2 383

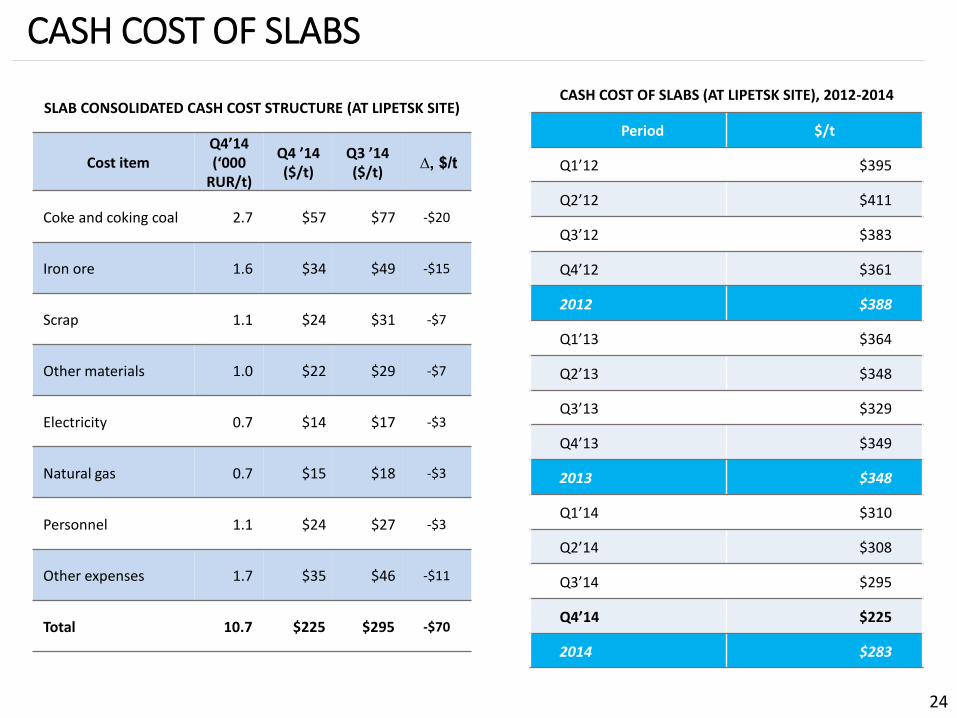

CASH COST OF SLABS

SLAB CONSOLIDATED CASH COST STRUCTURE (AT LIPETSK SITE)

Cost itemQ4’14(‘000

RUR/t)

Q4 ’14($/t)

Q3 ’14($/t)

∆, $/t

Coke and coking coal 2.7 $57 $77 -$20

Iron ore 1.6 $34 $49 -$15

Scrap 1.1 $24 $31 -$7

Other materials 1.0 $22 $29 -$7

Electricity 0.7 $14 $17 -$3

Natural gas 0.7 $15 $18 -$3

Personnel 1.1 $24 $27 -$3

Other expenses 1.7 $35 $46 -$11

Total 10.7 $225 $295 -$70

CASH COST OF SLABS (AT LIPETSK SITE), 2012-2014

Period $/t

Q1’12 $395

Q2’12 $411

Q3’12 $383

Q4’12 $361

2012 $388

Q1’13 $364

Q2’13 $348

Q3’13 $329

Q4’13 $349

2013 $348

Q1’14 $310

Q2’14 $308

Q3’14 $295

Q4’14 $225

2014 $283

24

1 as of 31.12.2014

2 as of 30.09.2014

SEGMENT INFORMATION

25

Q4 2014

(million USD)

Revenue from external customers 1 482 488 302 70 0 2 343 2 343

Intersegment revenue 344 94 126 564 (564)

Gross profit 705 17 39 124 (1) 884 (94) 790

Operating income/(loss) 449 (8) (122) 88 (2) 405 (57) 348

as % of net sales 25% (2%) (31%) 45% 15%

Income / (loss) from continuing operations

before minority interest436 (10) (162) 280 (1) 626 (35) 591

as % of net sales 24% (2%) (41%) 143% 25%

Segment assets including goodwill1 8 792 1 697 1 487 1 935 100 14 010 (3 604) 10 406

Q3 2014

(million USD)

Revenue from external customers 1 636 523 378 70 0 2 607 2 607

Intersegment revenue 373 115 178 666 (666)

Gross profit 576 39 97 159 (1) 871 (65) 807

Operating income/(loss) 312 (67) 49 127 (1) 421 (19) 402

as % of net sales 16% (13%) 10% 51% 15%

Income / (loss) from continuing operations

before minority interest378 (165) 233 172 1 619 (282) 337

as % of net sales 19% (31%) 47% 69% 13%

Segment assets including goodwill2 11 350 1 786 2 360 2 041 138 17 674 (3 661) 14 013

Totals

Intersegmental

operations and

balances

Consolidated

Steel

Foreign

rolled

products

Long

productsMining All other Totals

Intersegmental

operations and

balances

Consolidated

Steel

Foreign

rolled

products

Long

productsMining All other

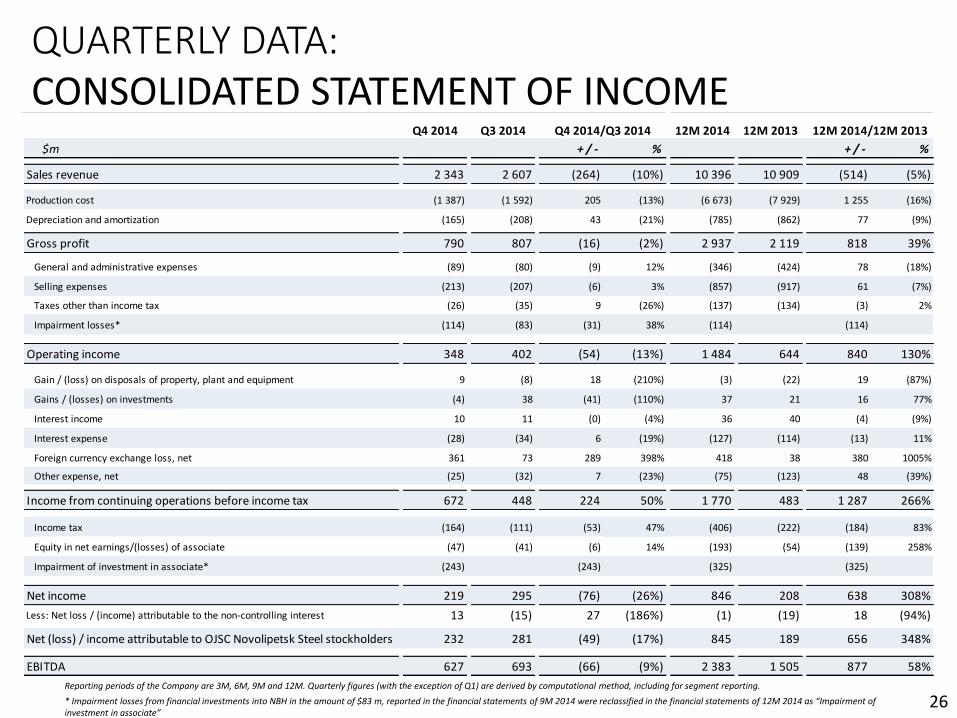

QUARTERLY DATA: CONSOLIDATED STATEMENT OF INCOME

Reporting periods of the Company are 3M, 6M, 9M and 12M. Quarterly figures (with the exception of Q1) are derived by computational method, including for segment reporting.

* Impairment losses from financial investments into NBH in the amount of $83 m, reported in the financial statements of 9M 2014 were reclassified in the financial statements of 12M 2014 as “Impairment of investment in associate”

26

Q4 2014 Q3 2014 12M 2014 12M 2013

$m + / - % + / - %

Sales revenue 2 343 2 607 (264) (10%) 10 396 10 909 (514) (5%)

Production cost (1 387) (1 592) 205 (13%) (6 673) (7 929) 1 255 (16%)

Depreciation and amortization (165) (208) 43 (21%) (785) (862) 77 (9%)

Gross profit 790 807 (16) (2%) 2 937 2 119 818 39%

General and administrative expenses (89) (80) (9) 12% (346) (424) 78 (18%)

Selling expenses (213) (207) (6) 3% (857) (917) 61 (7%)

Taxes other than income tax (26) (35) 9 (26%) (137) (134) (3) 2%

Impairment losses* (114) (83) (31) 38% (114) (114)

Operating income 348 402 (54) (13%) 1 484 644 840 130%

Gain / (loss) on disposals of property, plant and equipment 9 (8) 18 (210%) (3) (22) 19 (87%)

Gains / (losses) on investments (4) 38 (41) (110%) 37 21 16 77%

Interest income 10 11 (0) (4%) 36 40 (4) (9%)

Interest expense (28) (34) 6 (19%) (127) (114) (13) 11%

Foreign currency exchange loss, net 361 73 289 398% 418 38 380 1005%

Other expense, net (25) (32) 7 (23%) (75) (123) 48 (39%)

Income from continuing operations before income tax 672 448 224 50% 1 770 483 1 287 266%

Income tax (164) (111) (53) 47% (406) (222) (184) 83%

Equity in net earnings/(losses) of associate (47) (41) (6) 14% (193) (54) (139) 258%

Impairment of investment in associate* (243) (243) (325) (325)

Net income 219 295 (76) (26%) 846 208 638 308%

Less: Net loss / (income) attributable to the non-controlling interest 13 (15) 27 (186%) (1) (19) 18 (94%)

Net (loss) / income attributable to OJSC Novolipetsk Steel stockholders 232 281 (49) (17%) 845 189 656 348%

EBITDA 627 693 (66) (9%) 2 383 1 505 877 58%

Q4 2014/Q3 2014 12M 2014/12M 2013

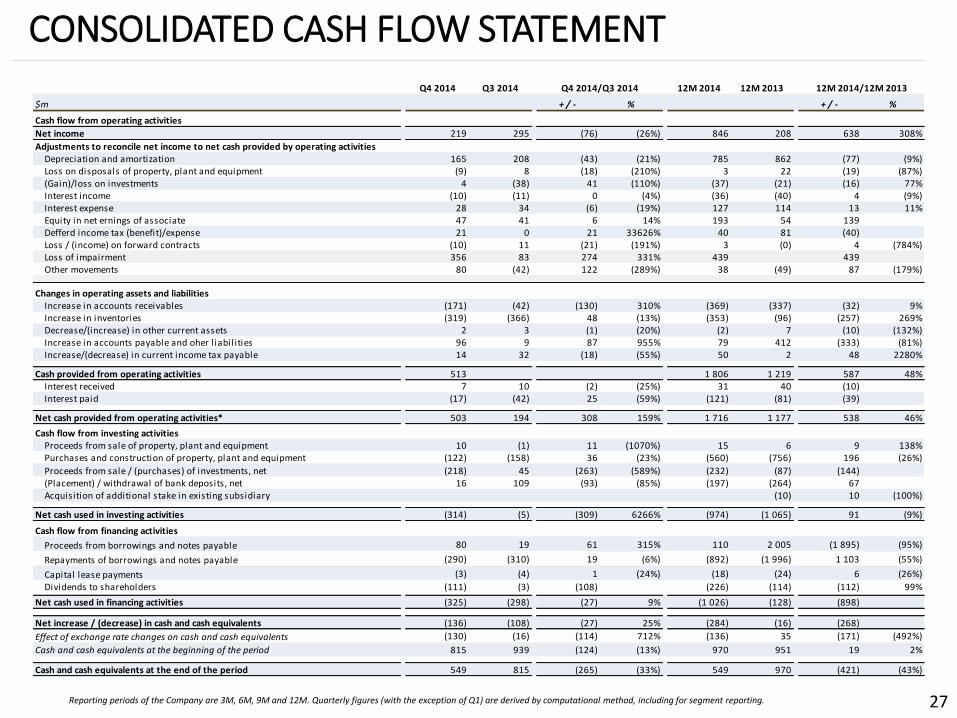

CONSOLIDATED CASH FLOW STATEMENT

Reporting periods of the Company are 3M, 6M, 9M and 12M. Quarterly figures (with the exception of Q1) are derived by computational method, including for segment reporting. 27

Q4 2014 Q3 2014 12M 2014 12M 2013

$m + / - % + / - %

Cash flow from operating activities

Net income 219 295 (76) (26%) 846 208 638 308%

Adjustments to reconcile net income to net cash provided by operating activitiesDepreciation and amortization 165 208 (43) (21%) 785 862 (77) (9%)Loss on disposals of property, plant and equipment (9) 8 (18) (210%) 3 22 (19) (87%)(Gain)/loss on investments 4 (38) 41 (110%) (37) (21) (16) 77%Interest income (10) (11) 0 (4%) (36) (40) 4 (9%)Interest expense 28 34 (6) (19%) 127 114 13 11%Equity in net ernings of associate 47 41 6 14% 193 54 139Defferd income tax (benefit)/expense 21 0 21 33626% 40 81 (40)Loss / (income) on forward contracts (10) 11 (21) (191%) 3 (0) 4 (784%)Loss of impairment 356 83 274 331% 439 439Other movements 80 (42) 122 (289%) 38 (49) 87 (179%)

Changes in operating assets and liabilitiesIncrease in accounts receivables (171) (42) (130) 310% (369) (337) (32) 9%Increase in inventories (319) (366) 48 (13%) (353) (96) (257) 269%Decrease/(increase) in other current assets 2 3 (1) (20%) (2) 7 (10) (132%)Increase in accounts payable and oher l iabilities 96 9 87 955% 79 412 (333) (81%)Increase/(decrease) in current income tax payable 14 32 (18) (55%) 50 2 48 2280%

Cash provided from operating activities 513 1 806 1 219 587 48%Interest received 7 10 (2) (25%) 31 40 (10)Interest paid (17) (42) 25 (59%) (121) (81) (39)

Net cash provided from operating activities* 503 194 308 159% 1 716 1 177 538 46%

Cash flow from investing activities Proceeds from sale of property, plant and equipment 10 (1) 11 (1070%) 15 6 9 138%Purchases and construction of property, plant and equipment (122) (158) 36 (23%) (560) (756) 196 (26%)

Proceeds from sale / (purchases) of investments, net (218) 45 (263) (589%) (232) (87) (144)(Placement) / withdrawal of bank deposits, net 16 109 (93) (85%) (197) (264) 67Acquisition of additional stake in existing subsidiary (10) 10 (100%)

Net cash used in investing activities (314) (5) (309) 6266% (974) (1 065) 91 (9%)0

Cash flow from financing activities

Proceeds from borrowings and notes payable 80 19 61 315% 110 2 005 (1 895) (95%)

Repayments of borrowings and notes payable (290) (310) 19 (6%) (892) (1 996) 1 103 (55%)

Capital lease payments (3) (4) 1 (24%) (18) (24) 6 (26%)

Dividends to shareholders (111) (3) (108) (226) (114) (112) 99%

Net cash used in financing activities (325) (298) (27) 9% (1 026) (128) (898)

Net increase / (decrease) in cash and cash equivalents (136) (108) (27) 25% (284) (16) (268)

Effect of exchange rate changes on cash and cash equivalents (130) (16) (114) 712% (136) 35 (171) (492%)

Cash and cash equivalents at the beginning of the period 815 939 (124) (13%) 970 951 19 2%

Cash and cash equivalents at the end of the period 549 815 (265) (33%) 549 970 (421) (43%)

Q4 2014/Q3 2014 12M 2014/12M 2013

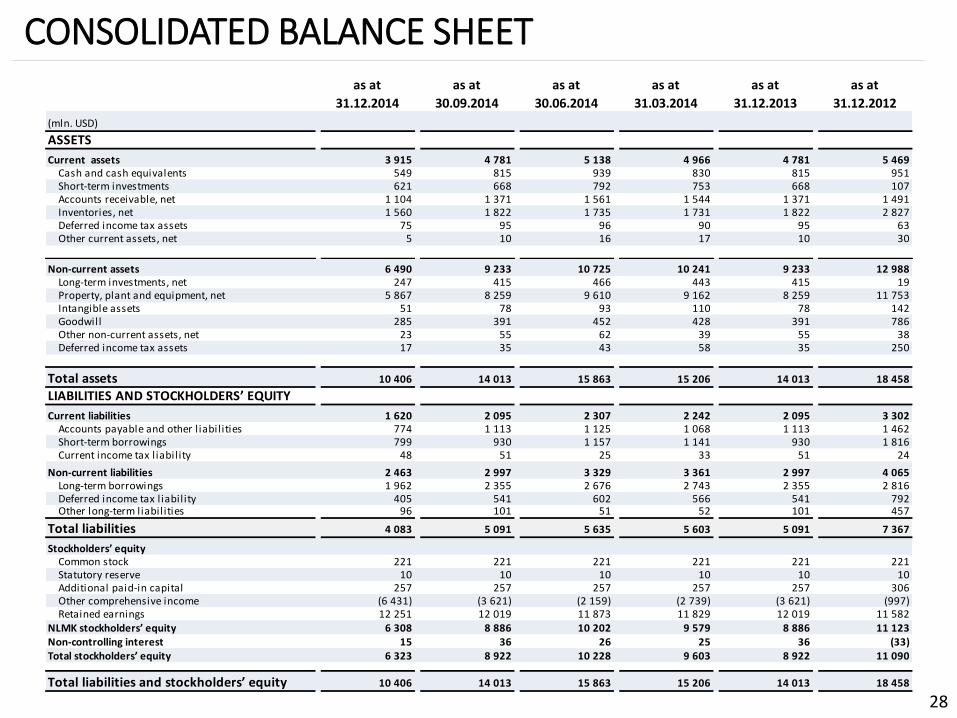

CONSOLIDATED BALANCE SHEET

28

as at

31.12.2014

as at

30.09.2014

as at

30.06.2014

as at

31.03.2014

as at

31.12.2013

as at

31.12.2012

(mln. USD)

ASSETS

Current assets 3 915 4 781 5 138 4 966 4 781 5 469Cash and cash equivalents 549 815 939 830 815 951Short-term investments 621 668 792 753 668 107Accounts receivable, net 1 104 1 371 1 561 1 544 1 371 1 491Inventories, net 1 560 1 822 1 735 1 731 1 822 2 827Deferred income tax assets 75 95 96 90 95 63Other current assets, net 5 10 16 17 10 30

Non-current assets 6 490 9 233 10 725 10 241 9 233 12 988Long-term investments, net 247 415 466 443 415 19Property, plant and equipment, net 5 867 8 259 9 610 9 162 8 259 11 753Intangible assets 51 78 93 110 78 142Goodwill 285 391 452 428 391 786Other non-current assets, net 23 55 62 39 55 38Deferred income tax assets 17 35 43 58 35 250

Total assets 10 406 14 013 15 863 15 206 14 013 18 458

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current liabilities 1 620 2 095 2 307 2 242 2 095 3 302Accounts payable and other l iabilities 774 1 113 1 125 1 068 1 113 1 462Short-term borrowings 799 930 1 157 1 141 930 1 816Current income tax liability 48 51 25 33 51 24

Non-current liabilities 2 463 2 997 3 329 3 361 2 997 4 065Long-term borrowings 1 962 2 355 2 676 2 743 2 355 2 816Deferred income tax liability 405 541 602 566 541 792Other long-term liabilities 96 101 51 52 101 457

Total liabilities 4 083 5 091 5 635 5 603 5 091 7 367

Stockholders’ equityCommon stock 221 221 221 221 221 221Statutory reserve 10 10 10 10 10 10Additional paid-in capital 257 257 257 257 257 306Other comprehensive income (6 431) (3 621) (2 159) (2 739) (3 621) (997)Retained earnings 12 251 12 019 11 873 11 829 12 019 11 582

NLMK stockholders’ equity 6 308 8 886 10 202 9 579 8 886 11 123Non-controlling interest 15 36 26 25 36 (33)Total stockholders’ equity 6 323 8 922 10 228 9 603 8 922 11 090

Total liabilities and stockholders’ equity 10 406 14 013 15 863 15 206 14 013 18 458

www.nlmk.com

NLMK

Investor Relations

Russia, 115054, Moscow

18, Bakhrushina str, bldg 1

t. +7 495 915 15 75

f. +7 495 915 79 04

29