Embed Size (px)

Citation preview

good afternoonme;

• andrew hughes

• from the UK, been in AU for 5 years

• worked media agency side for 4 years

delivering digital; search, social,

analytics, tech, data and programmatic

solutions

• @y0z2a for comments/discussion

louder;

• started in mid-2014

• independent

• working with;

– businesses of all walks

– with all vendors

• tech

• media

• datalouder.com.au

What Do Louder Think

louder.com.auImage Credit: emotivebrand.com

our thinking - programmatic• disclosed, and/or transparent is the right way from a marketers perspective

• marketers need to be prepared to pay for people, media, service and tech

• through the use of improved programmatic models, brands should see greater media

exposure for their $media spend & therefore improved returns

• programmatic is not just for acquisition – it delivers full funnel efficiency

• technology is driving transparency on every level – media cost / viewability /

attribution

more change management, less technology louder.com.au

our thinking - data• ownership and control of your data is only way forward

• Remove almost all 3rd party tags, unless you control the data

• digital platforms need to be integrated and linked around a common anonymous ID

• it is useless modeling if you’re not going to action change

• you need people who know what they are doing

• data partnerships and mutually beneficial co-operatives will blossom

collect it, improve it, action it louder.com.au

our thinking - general• brands should own their technology and data (both enable programmatic strategy) -

it can be informed and enhanced by 3rd parties, but ideally not controlled by them

• brands need to select and own the direction of their technology stack– AdServer, conversion and general tag deployment

– DSP / exchange

– DMP / audience

– web analytics

– CMS / Cx

– Ux / CRO

– CRM / EDM

• media, digital and creative agencies (and some publishers) can help to deliver

How do we see it coming together? louder.com.au

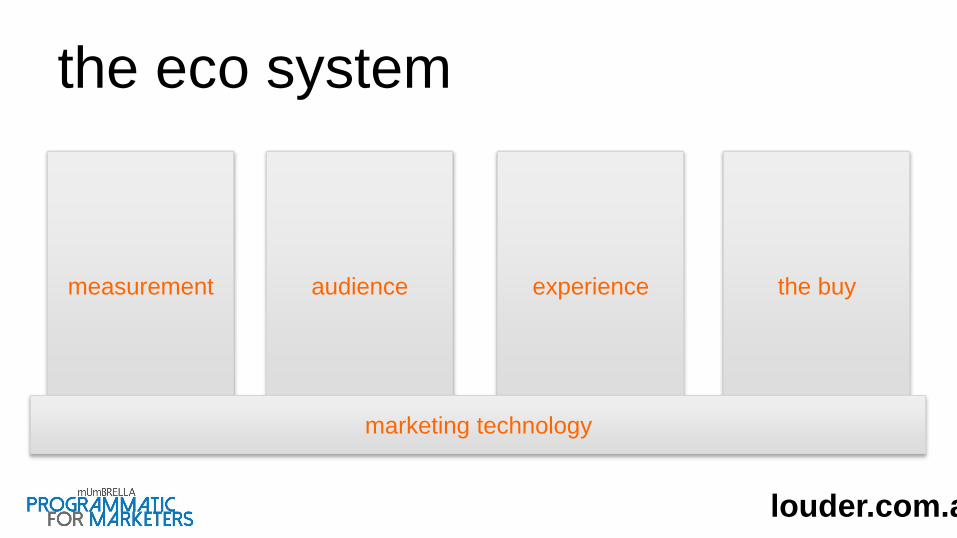

the eco system

measurement audience experience the buy

marketing technology

louder.com.au

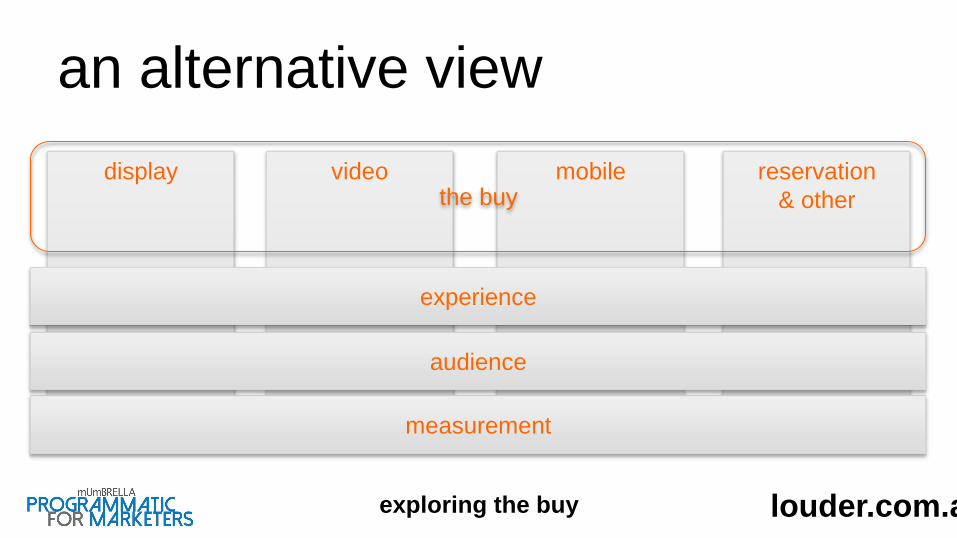

an alternative view

display video mobile reservation

& other

measurement

louder.com.au

audience

experience

the buy

exploring the buy

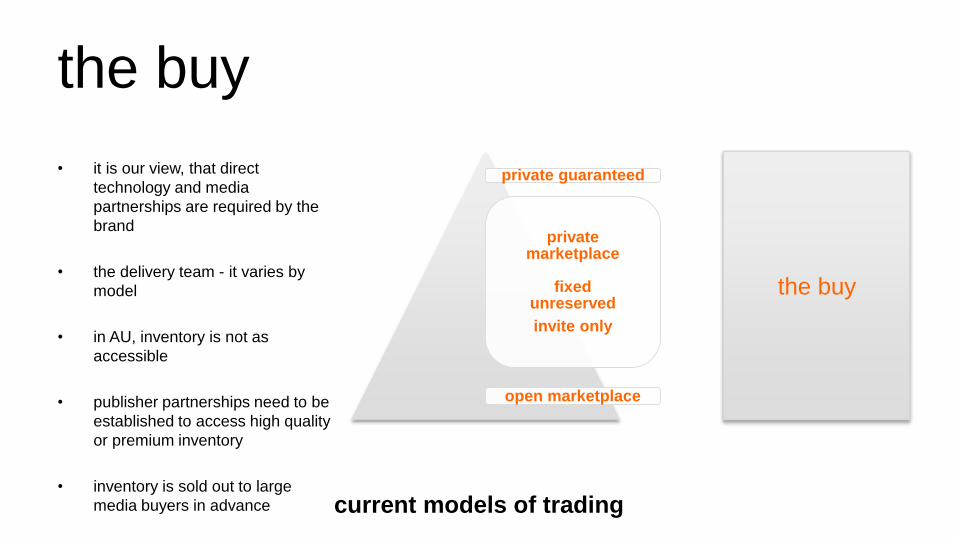

the buy

the buy

private guaranteed

private marketplace

fixedunreserved

invite only

open marketplace

• it is our view, that direct

technology and media

partnerships are required by the

brand

• the delivery team - it varies by

model

• in AU, inventory is not as

accessible

• publisher partnerships need to be

established to access high quality

or premium inventory

• inventory is sold out to large

media buyers in advance current models of trading

current programmatic modelsthere are three models;

– agency trade desk / managed service

– hybrid (or transition) agency desk

– in house desk

• all could be argued are right for your business by the different parties involved in the

fight.

• you need to understand what they are and how they work before you commit

• a “ball-park” number to start considering an in house approach is circa 1.5m / annum

in digital media (excluding search) – obviously, it takes time to set up, and digital

spend is increasing louder.com.auhow to calculate it?

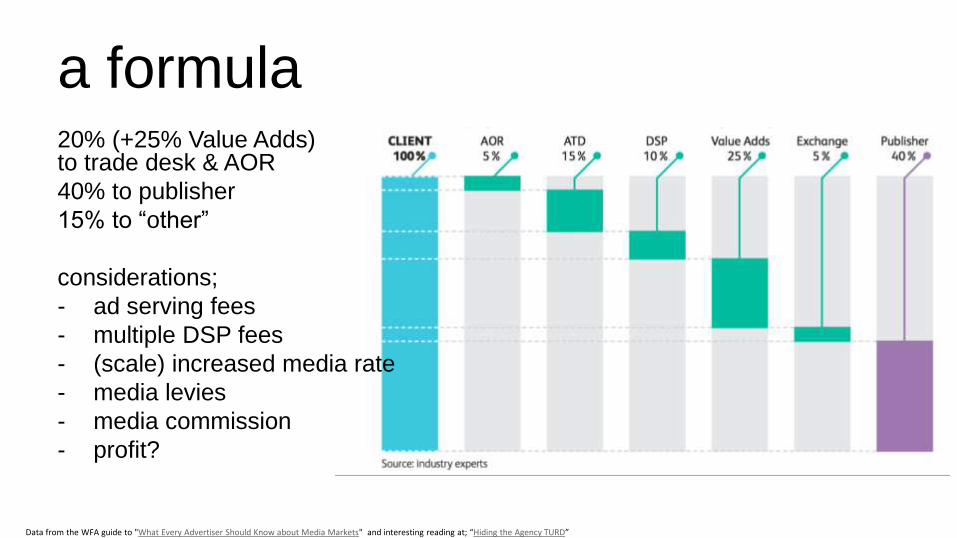

a formula20% (+25% Value Adds)to trade desk & AOR

40% to publisher

15% to “other”

considerations;

- ad serving fees

- multiple DSP fees

- (scale) increased media rate

- media levies

- media commission

- profit?

Data from the WFA guide to "What Every Advertiser Should Know about Media Markets" and interesting reading at; “Hiding the Agency TURD”

it’s not just about performance

Acquisition

– outcome based

– allocating budget to

outcome (performance)

– some dynamic creative

– limited integration

– executional/campaign

Branding

– online video (pre-roll)

– repurposed TVC’s

– poor content, targeting and

placement

– no sequence of

progression through funnel

– control

how to protect yourself when investing more

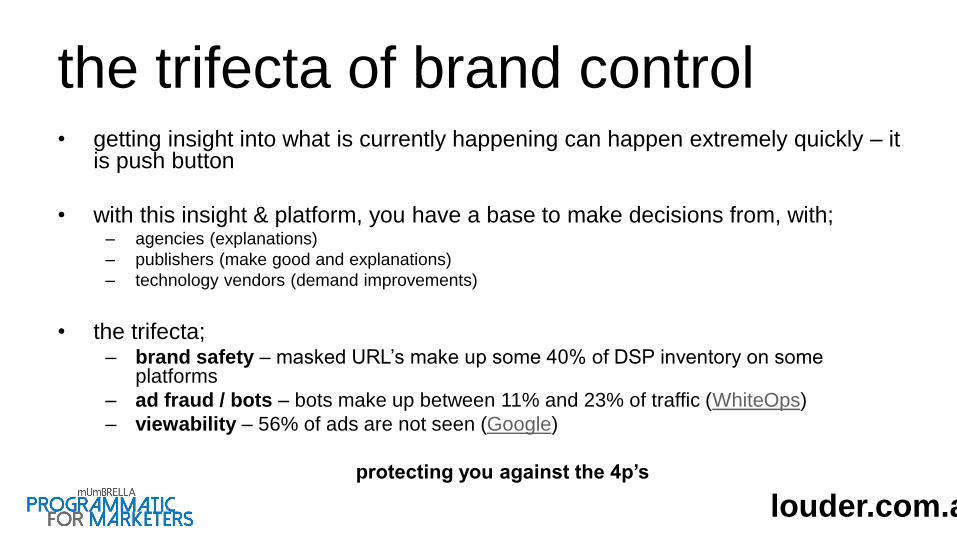

the trifecta of brand control• getting insight into what is currently happening can happen extremely quickly – it

is push button

• with this insight & platform, you have a base to make decisions from, with;– agencies (explanations)

– publishers (make good and explanations)

– technology vendors (demand improvements)

• the trifecta;– brand safety – masked URL’s make up some 40% of DSP inventory on some

platforms

– ad fraud / bots – bots make up between 11% and 23% of traffic (WhiteOps)

– viewability – 56% of ads are not seen (Google)

protecting you against the 4p’s

louder.com.au

So, “how can marketers take ownership”

louder.com.au

the marketers role• it’s not;

– too fragmented

– too complicated

– exclusively a specialist’s job

– your agencies role

• surround yourself by the best vendors and strategists

• it’s really bloody exciting, and will open you to a new world and facet of marketing

take ownership, educate yourself, as in not doing so, you are complicit in supporting the inefficiencies

being delivered by the current media trading models

you will become an invaluable resource to your CMO & CFO’s

louder.com.au

3 steps to success

louder.com.au

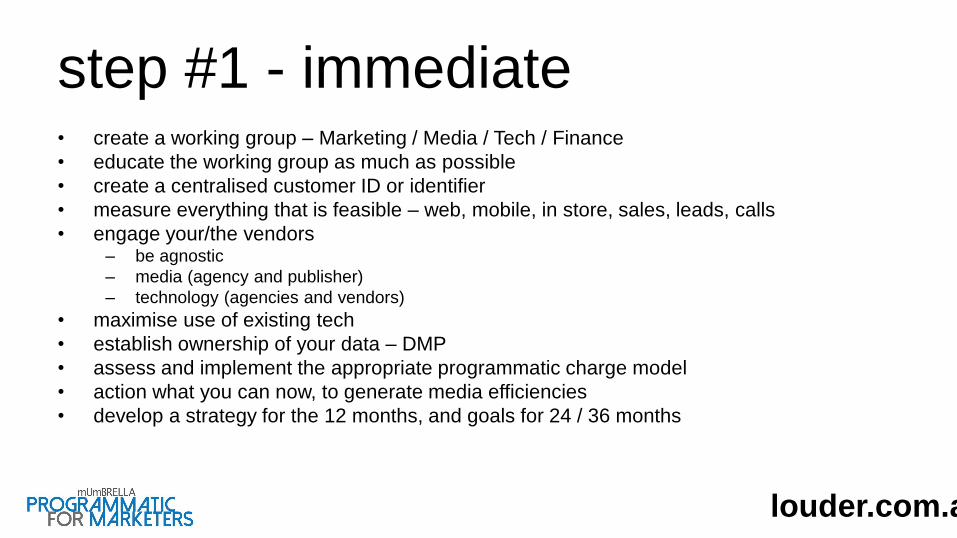

step #1 - immediate• create a working group – Marketing / Media / Tech / Finance

• educate the working group as much as possible

• create a centralised customer ID or identifier

• measure everything that is feasible – web, mobile, in store, sales, leads, calls

• engage your/the vendors– be agnostic

– media (agency and publisher)

– technology (agencies and vendors)

• maximise use of existing tech

• establish ownership of your data – DMP

• assess and implement the appropriate programmatic charge model

• action what you can now, to generate media efficiencies

• develop a strategy for the 12 months, and goals for 24 / 36 months

louder.com.au

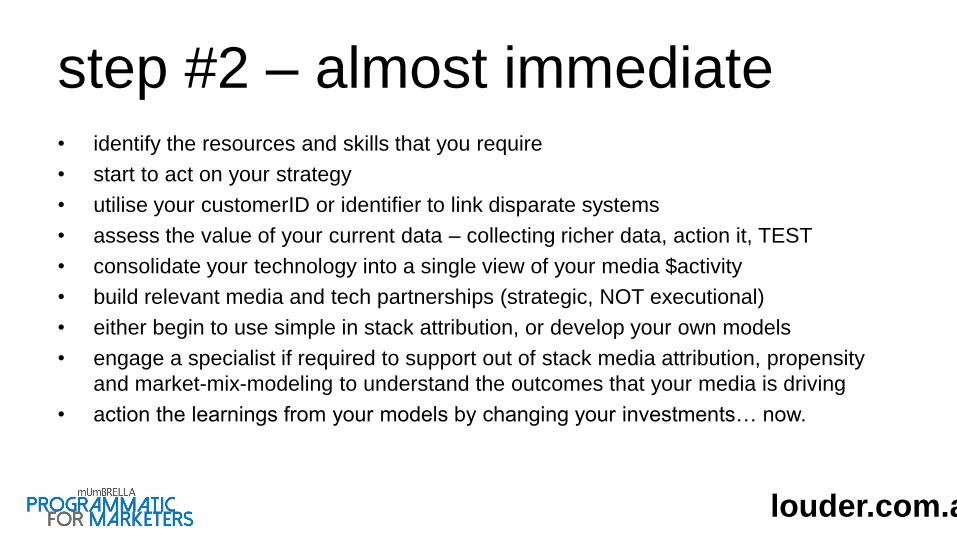

step #2 – almost immediate• identify the resources and skills that you require

• start to act on your strategy

• utilise your customerID or identifier to link disparate systems

• assess the value of your current data – collecting richer data, action it, TEST

• consolidate your technology into a single view of your media $activity

• build relevant media and tech partnerships (strategic, NOT executional)

• either begin to use simple in stack attribution, or develop your own models

• engage a specialist if required to support out of stack media attribution, propensity

and market-mix-modeling to understand the outcomes that your media is driving

• action the learnings from your models by changing your investments… now.

louder.com.au

step #3 – the longer term• roll out your own technology stack

• be agile – test new technology

• build stronger media relationships with successful partners

• test new partnerships and inventory regularly

• build relevant strategic media and tech partnerships

• begin to use attribution, propensity and market mix modelling to understand the outcomes that your media is driving

louder.com.au

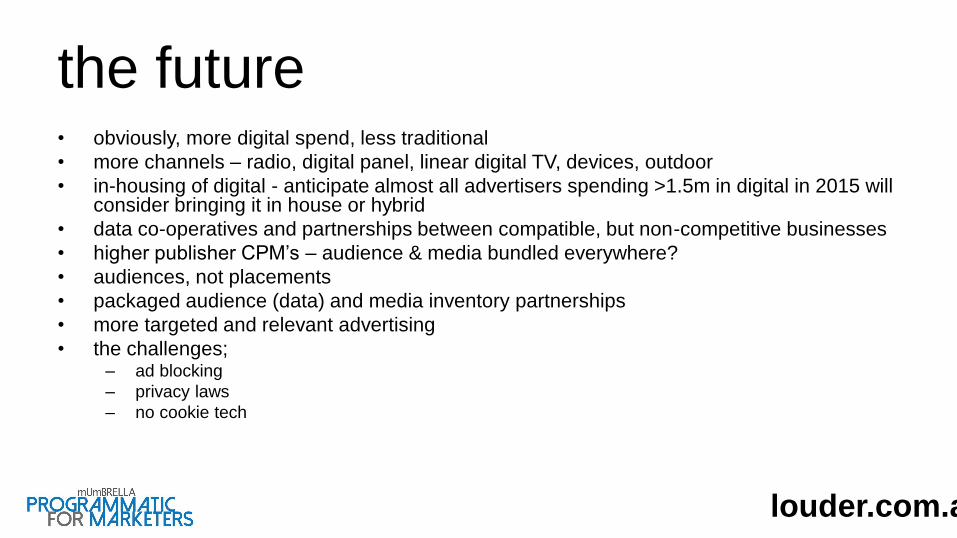

the future• obviously, more digital spend, less traditional

• more channels – radio, digital panel, linear digital TV, devices, outdoor

• in-housing of digital - anticipate almost all advertisers spending >1.5m in digital in 2015 will consider bringing it in house or hybrid

• data co-operatives and partnerships between compatible, but non-competitive businesses

• higher publisher CPM’s – audience & media bundled everywhere?

• audiences, not placements

• packaged audience (data) and media inventory partnerships

• more targeted and relevant advertising

• the challenges;– ad blocking

– privacy laws

– no cookie tech

louder.com.au

Questions?

louder.com.auandrew hughes - @y0z2a #mumbrellaPFM

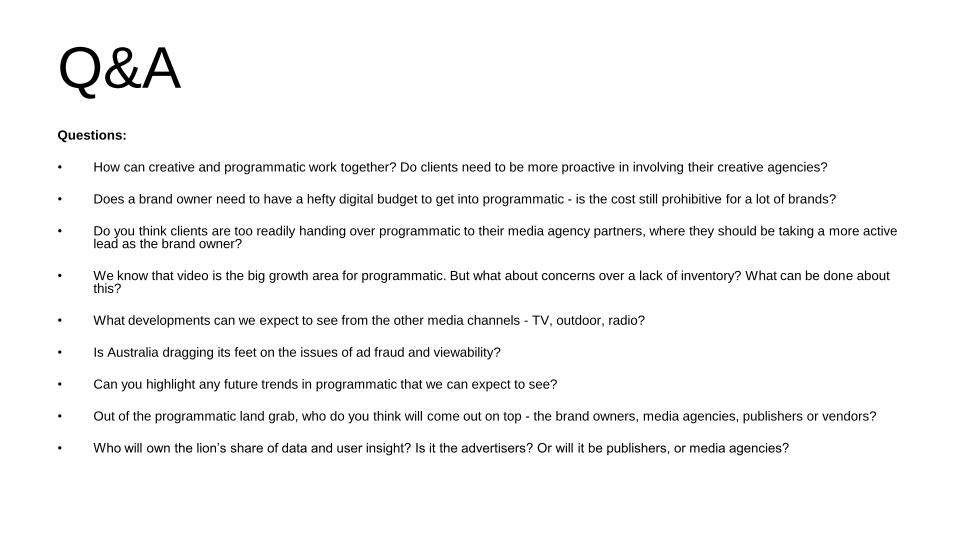

Q&AQuestions:

• How can creative and programmatic work together? Do clients need to be more proactive in involving their creative agencies?

• Does a brand owner need to have a hefty digital budget to get into programmatic - is the cost still prohibitive for a lot of brands?

• Do you think clients are too readily handing over programmatic to their media agency partners, where they should be taking a more active lead as the brand owner?

• We know that video is the big growth area for programmatic. But what about concerns over a lack of inventory? What can be done about this?

• What developments can we expect to see from the other media channels - TV, outdoor, radio?

• Is Australia dragging its feet on the issues of ad fraud and viewability?

• Can you highlight any future trends in programmatic that we can expect to see?

• Out of the programmatic land grab, who do you think will come out on top - the brand owners, media agencies, publishers or vendors?

• Who will own the lion’s share of data and user insight? Is it the advertisers? Or will it be publishers, or media agencies?

![Marketing Automation - Demystifying Big Data [Mumbrella Digital School]](https://img.pdfslide.net/doc/110x75/555af39dd8b42a4c7d8b52f1/marketing-automation-demystifying-big-data-mumbrella-digital-school.jpg)