Embed Size (px)

Citation preview

1

Deborah Weinswig

Managing Director

US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

Future of Retail: Is It Coming Apart at the Seams?

June 9, 2016

2

Agenda

ABOUT US

RETAIL LANDSCAPE OVERVIEW

TOP 20 RETAIL & TECH TRENDS FOR 2016

3

About Us

4

About Fung Group

TRADING LOGISTICS DISTRIBUTION RETAILING

Li & Fung LimitedListed on SEHK

Global Brands

GroupListed on SEHK

Fung Retailing

LimitedPrivately Held Entity

Convenience

RetailAsia Limited

Listed on SEHK

Trinity Limited

Listed on SEHK

Branded Lifestyle Holdings Limited

LiFung Kids (Holdings) Limited

Toyrs “R” Us (Asia)

Suhyang Networks

UCCAL Fashion GroupPrivately Held Entities

Fung Holdings (1937) Ltd.

A privately held entity and major shareholder of the Fung Group

5

Retail, Tech, and Fashion

• Fung Global Retail & Technology advises retailers, real estate developers, tech

companies, and others on projects situated at the intersection of retail, tech and/or fashion

• Our team offers a robust knowledge bank and deep-rooted experience across the

retail, fashion and tech industries. We are involved in many areas of the business,

which allows us to offer a unique perspective on the future and where the sector is heading.

6

Retail Landscape Overview

7

All-Channel Universe

Order From

Fulfilled By

Where Received

Home

Elsewhere

Your Store

Different Store

Mobile

Direct DC

Store DC

Your Store

Different Store

Vendor

Home

Elsewhere

Your Store

Different Store

Source: Hudson’s Bay

8

Retail Destruction

“We are seeing continued weakness in consumer spending

levels for apparel and related categories.”

-Terry J. Lundgren, Chairman and CEO of Macy’s, Q2 earnings call

“They (consumers) are not buying apparel.”

-Wesley McDonald, CFO of Kohl’s, Q2 2016 earnings call

“While apparel will always be important to JCPenney, we've

conducted a detailed review of our customers’ current and

future shopping patterns, and we'll start to strategically shift

our merchandising mix to sell more products and services that

correlate to where customers are spending the greater

percent of their dollars.”

-Marvin R. Ellison, CEO and Director of JCPenney

“There's no doubt that the luxury market is the most

challenging market we participate in right now. And you've

seen that in the results of companies across the luxury

spectrum.”

-Gerald L. Storch, CEO of Hudson’s Bay

Company Actual Estimate

Kohl’s (3.9%) 0.2%

Nordstrom (1.7%) 0.1%

Guess (4,2%) (1.6%)

Macy’s (6.1%) (3.4%)

JCPenney (0.4%) 3.2%

Pottery Barn 0.2% 2.5%

H&M 5.0% 9.0%

Target 1.2% 1.7%

Foot Locker 2.9% 4.5%

Costco 0.0% 0.9%

Dollar General 2.2% 2.4%

Source: StreetAccount

Actual Comps/Sales Results Versus Estimates

9

The Beauty Category Outperforms Apparel

“Selfie culture, if you take a photo 10 times today…the result is people are using

more makeup and more instant skin care.”

-Fabrizio Freda, CEO of Estée Lauder, commenting on 11% growth in makeup sales in 1Q16

IndustryGlobal Revenue

2015

Annual Growth

10-15

Cosmetics $276bn 3.2%

Apparel $618bn 0.6%

Source: IBISWorld

10

Experiences Trump “Things”

• Over the next 5 years US

consumer spending is

forecasted to grow by 22%;

non-essential categories,

including vacations and dining

out, will see the fastest growth,

about 27% (Mintel)

• More than 3 in 4 millennials

would choose to spend money

on a desirable experience

• Experiences are what people

use to define themselves across

social channels

11

The Instagram Effect

Never Be Photographed in the Same Dress Twice

12

Beauty and Food Retailers are Immune from

Secondary Market

No market for used lipsticks or half-eaten sandwiches

13

The Presidential Election: Cautious Consumers

• The 2016 presidential campaign is one of the most unpredictable election years

• Election cycles always prove to be consumer mood-dampeners

• The luxury sector is affected the most because most of luxury spending is mood-driven

• The US luxury market is in decline with no support from tourism and election

uncertainty

14

US: Election Years Influence Stock Market

Election

An early pullback in spending

that is followed by a strong recovery later in the year.

Pre-Election

The best stock market returns

compared to post election, midterm and election years.

14%

5%

5%

7%8%

0%

4%

8%

12%

16%

Pre-Election Midterm Post-Election Election Year Average

Source: Bloomberg

S&P 500 Average Returns

15

The Consumer Hourglass

• The top half and bottom half are doing

better, with outperformance at the bottom

• The “consumer hourglass” phenomenon generates opportunities in the value-for-

money segment

Squeeze in the Middle Segment Neiman Marcus

Saks

Nordstrom

Bloomingdale’s

Dillard’s

Macy’s

Kohl’s

Sears

JCPenney

Target

Walmart

CostcoTJ Maxx/Off-Price

Primark

Aldi / Trader Joe’s

Dollar Stores

16

Four-Quadrant Disruptors FrameworkNAME UR

PRICE

SELF-

CHECKOUT

EVANGELIZE

THRIVE

EXPERIENTIAL RETAIL: MAKE THE STORE AN AWESOME PLACE

CUSTOMER ENGAGEMENT: HOW DO YOU CONVERT THE CONSUMER

ALL CHANNEL: The CONSUMER CAN SHOP WHEREVER +

WHENEVER

REACTION COMMERCE

NEW RETAIL MODELS:HOW WILL THE CONSUMER SHOP IN THE

FUTURE

17

Top 20 Retail & Tech Trends for 2016

1. Store Traffic

2. Experiential Retail

3. Smart Malls

4. Augmented Reality

5. Virtual Reality

6. Robotics

7. Facial Recognition

8. Wearables

9. Evolving Pure Plays

10. Loyalty Programs

11. Influencers

12. Consumers Have Full Power:

Name Your Price

13. Secondary Market for Fashion

14. Subscription Economy

15. Sharing Economy

16. Rental Economy

17. Caring Economy

18. Silver Economy

19. Amazon Leads Retail Growth

20. Artificial Intelligence

18

1. With Store Traffic Down, In-Store

Experience Is Key

• US mall traffic has decreased for

42 consecutive months and continues to be challenging

• Malls have seen an average 6.5%

YoY decrease in traffic since

January 2015

– High-end malls appear less affected

– General Growth Properties:

traffic up 2% in 2015

– Simon Malls: traffic up 1.5%

in 2015

– Taubman Centers: traffic up in 2015

Source: RetailNext

-16.0%

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Monthly US In-store Traffic YoY%

19

1. With Store Traffic Down, Department Stores

Go Off-Price

• Department stores are offering below-retail prices through off-price chains. Both Kohl’s

and Macy’s are opening off-price stores this year

– Kohl’s opened a single store selling returned items in Cherry Hill, NJ in June 2015

– Macy’s discount chain “Macy’s Backstage” opened four stores in greater New

York City area in September 2015

20

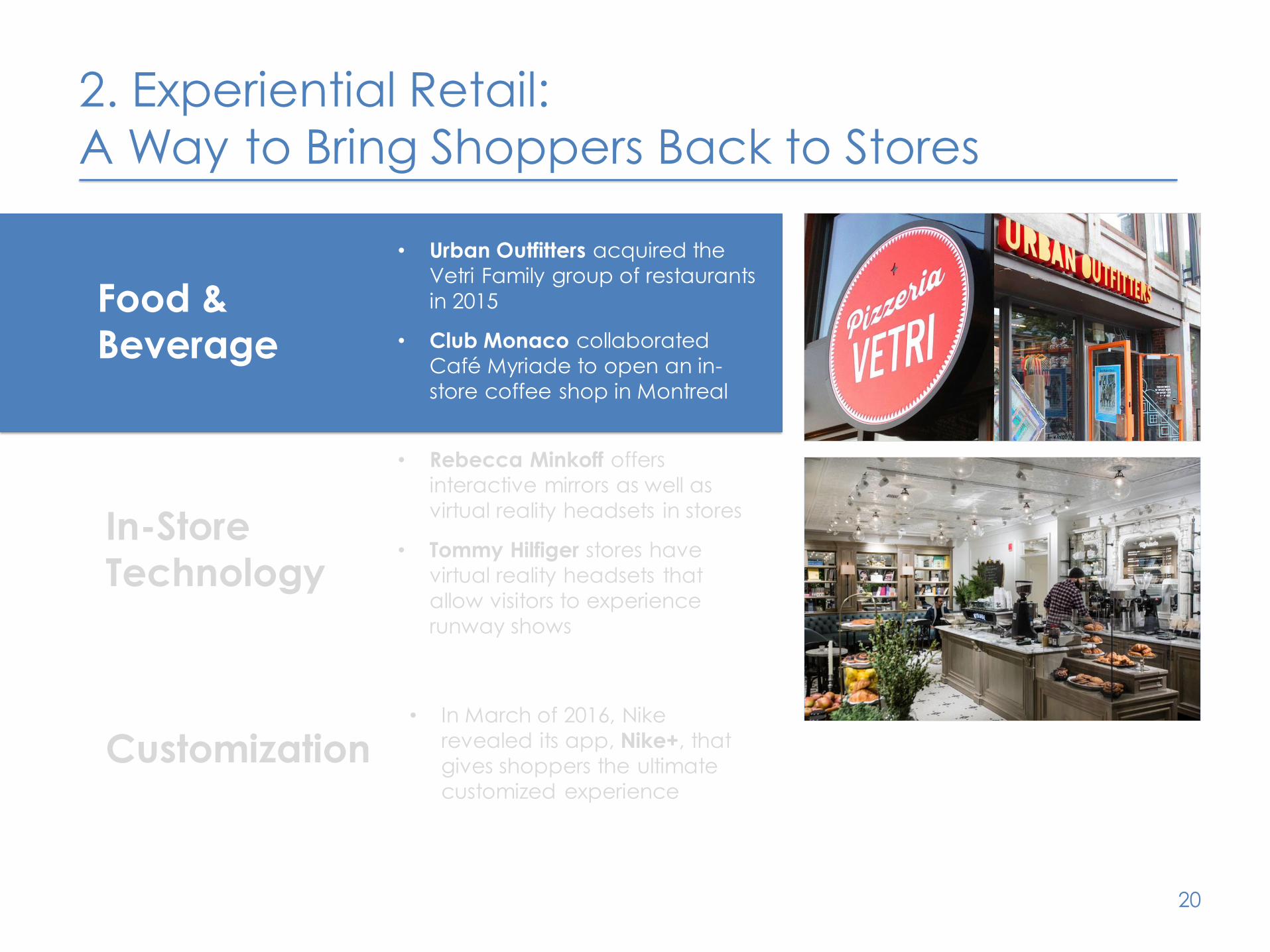

2. Experiential Retail:

A Way to Bring Shoppers Back to Stores

• Urban Outfitters acquired the

Vetri Family group of restaurants

in 2015

• Club Monaco collaborated

Café Myriade to open an in-

store coffee shop in Montreal

• Rebecca Minkoff offers

interactive mirrors as well as

virtual reality headsets in stores

• Tommy Hilfiger stores have

virtual reality headsets that

allow visitors to experience

runway shows

• In March of 2016, Nike

revealed its app, Nike+, that

gives shoppers the ultimate

customized experience

Food & Beverage

In-Store Technology

Customization

21

2. Experiential Retail:

Making the Experience Engaging

• Rebecca Minkoff offers

interactive mirrors as well as

virtual reality headsets in stores

• Tommy Hilfiger stores have

virtual reality headsets that

allow visitors to experience

runway shows

• In March of 2016, Nike

revealed its app, Nike+, that

gives shoppers the ultimate

customized experience

Food & Beverage

In-Store Technology

Customization

• Urban Outfitters acquired the

Vetri Family group of restaurants

in 2015

• Club Monaco collaborated

Café Myriade to open an in-

store coffee shop in Montreal

22

2. Experiential Retail:

Customization and Personalization

• Rebecca Minkoff offers

interactive mirrors as well as

virtual reality headsets in stores

• Tommy Hilfiger stores have

virtual reality headsets that

allow visitors to experience

runway shows

• In March of 2016, Nike

revealed its app, Nike+, that

gives shoppers the ultimate

customized experience

Food & Beverage

Customization

In-Store Technology

• Urban Outfitters acquired the

Vetri Family group of restaurants

in 2015

• Club Monaco collaborated

Café Myriade to open an in-

store coffee shop in Montreal

23

24

3. Smart Malls:

Reshaping the Physical Shopping Experience

Data-enabled

personalized and timely

promotions

Track movement,

behavior and preferences

Beacon-enabled

location-based advertising

25

4. Augmented Reality

uses augmented reality and configurable 3D models

of products to drive sales and conversion

Augmented

Commerce Click and

see the products in 3D

at home

Augmented Stores:

“Endless aisle” or virtual

showroom

Augmented Sales

A B2B sales tool for

sales associates to use

with customers

26

5. Virtual Reality

means presenting the senses with a computer-

generated virtual environment

• VR—Oculus Rift headset

• Samsung’s Gear VR headset to be priced at $99 and to hit stores next year

• Widespread adoption of VR in the retail space is expected in as little as three years

• Industry even has a new term for selling via VR: v-commerce

Source: Digital Trends/Ad Age

27

6. Robotics

• Starwood Hotels is using robotic butlers in the Aloft Silicon Valley hotel

• Suitable Technologies: entire store with telepresence robots

– Robots created for corporate boardrooms

– Allow users to interact remotely from home

(or wherever they are)

– In the Suitable Technologies

showroom, salespeople appear only as robots

– SoftBank’s new robot Pepper is capable of engaging

customers as a sales assistant in store

28

7. Facial Recognition

The global advanced Facial Recognition market expected growth: $2.77 Bil. in 2015 to

$6.19 Bil. in 2020 (CAGR 17.4%)30% of retailers are using facial recognition technology to

track customers in stores (ICSC)

Applications are

increasing: health,

wellness, beauty and

advertising

In 2015, Walmart tested

with FaceFirst

Intel released RealSense

facial recognition

technology in 2015

29

8. Wearables: All About Medical

Electronic glasses that

enable blind to see

3-D Printing:

ProstethicsSecond Generation

Hearing Aid

Created by eSight

Seen at 2016 WEAR

Conference in Boston

Created by Enabling the

future.org

Allowing consumers to

design and DIY

Created by ReSound

Smart hearing aids

controlled on iPhone, or

iPad. Users can adjust

volume, treble, bass.

30

31

8. Wearables Make Them Wantables : All About the

Hype

• Global demand for smart and interactive textiles is still small. It is expected to hit

$3.8B in 2020, or a CAGR of 14%.

• So far smart clothing products are all about the hype

• Ralph Lauren’s PoloTech shirt replaces wrist-worn fitness trackers (manufactured by OMsignal)

• Others: Visijax cycling jacket, Sensoria smart socks, Hexoskin smart fabric shirt, MYO armband

32

9. Evolving Pure Plays

(Number of Actual/Planned Physical Stores)

1 400 120 1 3 2

3 21 1 1 7

4 27 25 12 2

33

10. Loyalty Programs: Case Studies

Today’s Loyalty

Cards with bar codes, reward programs

Use of gamification (membership

levels, points, leaderboards)

Last-generation

Loyalty

Coupons, membership

cards

Tomorrow’s Loyalty

Smartphone based

Integration of tracking status, payment, gift cards, ect.

34

11. Influencers: A Marketplace

• Marketers felt the biggest issue

is scale, with 59%, intending to increase their influencer

marketing budgets. (Tidal Labs)

• A transparent marketplace

can:

– Search all influencers by relevant attributes

– Streamline process to cut

overhead

– Remove friction in

reaching out to startups via email

– Problems the sector is

facing: fragmentation,

scale, and authenticity

Main Challenges When Rolling Out Influencer

Engagement Strategy

Source: Augure/State of Influencer Engagement Survey

35

11. Influencers:

A Few Voices Reach and Impact Many

Vloggers Blogs Influencers

Joy Cho

12.8M

followers

Chris Ozner

Over 75M

daily users

Nash Grier (age 16)

1.5B plays per day

Leandra Medine

Over 2.6M

followers/month

Aimee Song

Over 2M

followers/month

Zoe Sugg

Over 1.6M

followers/month

Carli Bybel

Over 1.2M

followers/month

36

12. Consumers Have More Power:

Name your price

• Name-your-own-price model: allows customers to state the price they are willing to

pay

• Dynamic pricing and data-driven repricing: prices change in response to real-time supply and demand

• 40% of retailers plan to use cloud/Saas solutions for dynamic pricing

• Implementing dynamic pricing can improve revenues and profits by 8% and 25%,

respectively

Source: WisePricer

Best Buy and

Walmart

implement price

changes over

50,000 items

per month.

Amazon changes

prices every 10

minutes or more!

37

12. Consumers Have More Power:

Name your price

is a smart wishlist generator for customers

Follow friends’ and

families’ wishlists on

social media

Slide price bar to

indicate the price

you want to pay

Set an expiration date

for auto-buying service

when the app discovers

a sale

38

12. Consumers Have More Power:

Name your price

is an app that empowers customers through PAY WHAT

YOU WANNA PAY

Discretionary Nice-

to-Have product

categories

Slide the price bar to

indicate customer

willingness: a lower

price corresponds to

a longer waiting time

Inventory turnover

maximization for

retailers

39

13. Secondary Market for Fashion

• Online resale fashion industry is worth $25 billion by 2025

• Rise of retail brands’ resale programs

• Consumers are convinced by the great quality of the secondhand apparel bought via

online platforms

• Societal shift toward less ownership — the art of decluttering

• 87% of individuals who bought secondhand clothing online shifted their spending away from off-price retailers.

• Sentiment toward secondhand has shifted

40

13. Secondary Market for Fashion: Partnerships

A program that lets customers exchange their

well-maintained, name-brand clothing for

Macy’s gift cards to make the world greener

Easy steps for big rewards

Order a Clean out Kit

Fill it up; send it out

Get gift cards after

thredUP’s review

Strict rules to maintain excellent

quality

Less than five year old

Selected name-brands

Clean, trendy and women’s only

Expanding partnership

and impact

Diapers.com since 2014

Gymboree since 2012

41

13. Barter Instead of Buying- reKindness

is a unique “swap to shop” online fashion barter

community

Barter spare clothes

in reKindness’s

community closet

online and at local

events

Reduce personal

environmental

footprint by recycling

clothes

De-clutter mass-market

items to make life less

stressful

42

43

14. Subscription Economy:

Beauty and Fashion Are Growing

• Convenience and curated products for consumers

• Recurring revenue model for retailers

• Element of self-gifting and beauty is the biggest category

• Fashion-styling subscriptions are becoming popular

Le Tote, Birchbox, BarkBox, Pijon, Stitch Fix, Bookofthemonth

44

15. Sharing Economy:

“Uberifying” Virtually Every Industry

• Valuations of sharing-economy companies have skyrocketed

• Revenues are projected to catch up to aggressive valuations

• Sharing-economy market:

Disruptors: Uber, Airbnb, Lending Club, WeWork

45

16. Rental Economy: Fashion Rental Leading

Disruptors: Style Lend, VillageLuxe, Le Tote, Lena the Fashion Library and Borrow For Your Bump

(maternity)

Following Rent the Runway, a new generation of fashion-rental companies has emerged

46

17. Caring Economy Promotes Startups for

Social Good

Disruptors: TOMS, Reformation, Warby Parker, NOURI, SoapBox Soaps, Zady, GoodXChange

• Promotes social activism over self-indulgence

– Consumers, especially Gen Z, demand integrity from brands and retailers

• Startups with social missions apply market-based strategies to achieve a social goal

– TOMS, the shoe company, has a “one for one” business model

– Reformation designs and manufactures sustainable apparel; sources sustainable fabrics

and vintage garments

– Kohl’s Cares gives back to communities with Salina Yoon children’s books

47

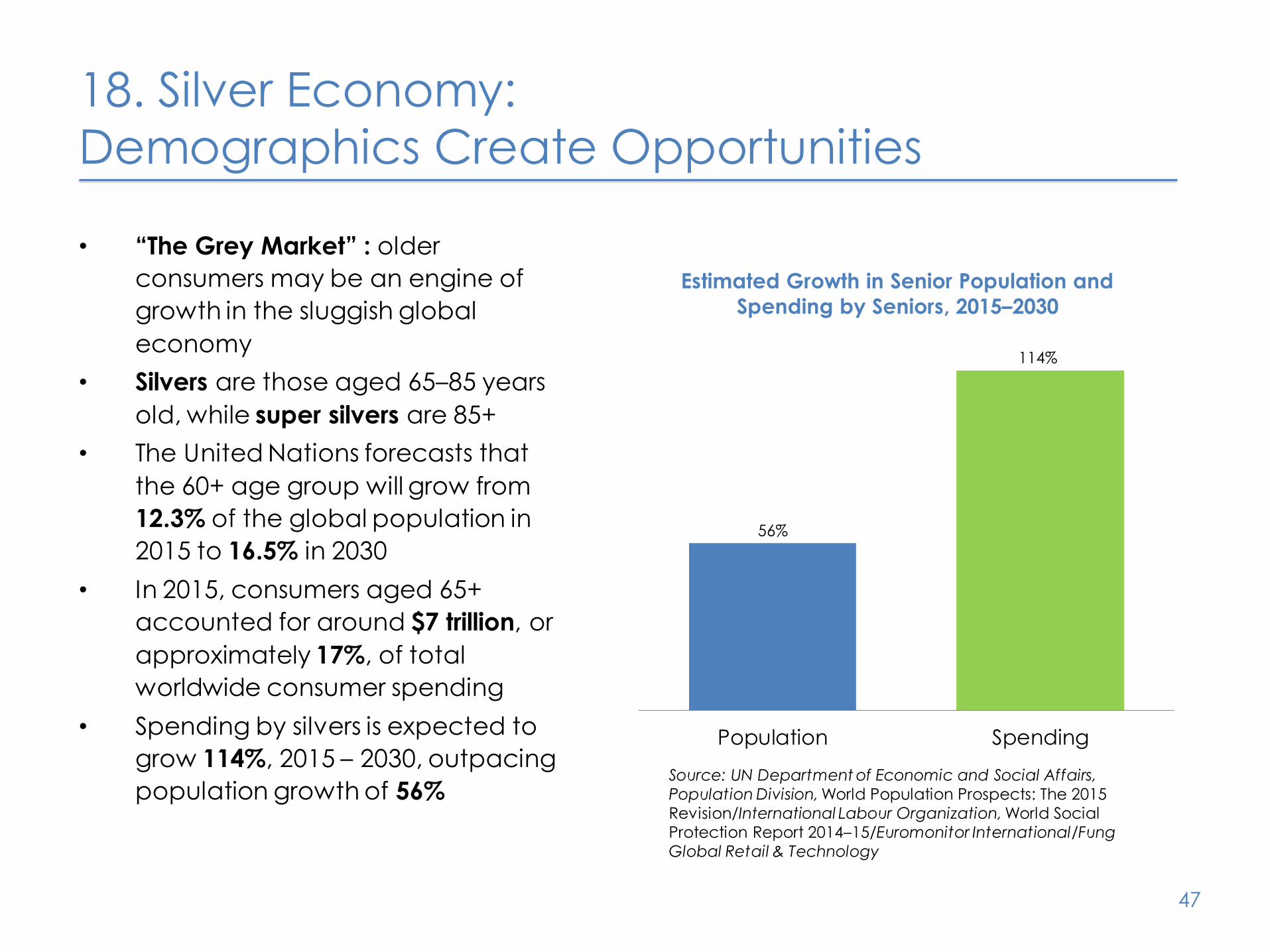

18. Silver Economy:

Demographics Create Opportunities

• “The Grey Market” : older

consumers may be an engine of

growth in the sluggish global

economy

• Silvers are those aged 65–85 years

old, while super silvers are 85+

• The United Nations forecasts that

the 60+ age group will grow from

12.3% of the global population in

2015 to 16.5% in 2030

• In 2015, consumers aged 65+

accounted for around $7 trillion, or

approximately 17%, of total

worldwide consumer spending

• Spending by silvers is expected to

grow 114%, 2015 – 2030, outpacing

population growth of 56%Source: UN Department of Economic and Social Affairs,

Population Division, World Population Prospects: The 2015

Revision/International Labour Organization, World Social

Protection Report 2014–15/Euromonitor International/Fung

Global Retail & Technology

56%

114%

Population Spending

Estimated Growth in Senior Population and

Spending by Seniors, 2015–2030

48

49

19. Amazon Leads Retail Growth

• Accounted for $0.51 of every

$1.00 of growth in US e-commerce in 2015

• Generated 24% of total retail

growth in the United States

• New Amazon services are

changing consumer preferences

Amazon Annual Sales Growth

Source: Bloomberg and US Census Bureau

50

19. Amazon Leads Retail Growth

PROS

• 110 Amazon Dash Buttons available

• Two-day shipping on all items

• Set up with existing Amazon account

• Dash Buttons are available to Prime members for $4.99 each, with a $4.99 credit after the first order

CONS

• Does not provide data to brands

• Selective regarding which brands can participate

• Controls the channel while promoting private label brand

• Items must be Prime-eligible

51

20. Artificial Intelligence: Amazon Echo & Alexa

• Paired with Alex, Echo allows for “always on” AI in your home – without needing your phone or

pushing a button.

• Echo becomes the central nervous system of the connected home

Ford is partnering with Amazon to integrate vehicles with Echo, Amazon’s smart-home device

52

Bonus: Israel-China Silk Road

• Are Israel and China creating a Silk

Road for startups?

• China is a “mobile first” country

• Chinese companies are

developing apps

• In 2014, Chinese investors invested

US$302 million in Israeli companies,

and in 2015, that number rose to

more than US$500 million, a

significant increase.

53

Bonus:

Fung Group’s Explorium Project in Shanghai

Explorium a retail “omni-platform lab” consisting of a

60,000 square foot space in Shanghai that has an

interconnected digital network of services, including a

mobile shopping application, an i-beacon tracking

solution and a data analytics platform.

Partnership with IBM

and Pico35 Participating

Brands

12,000 Employees as

Shoppers

54

Thank You!Deborah Weinswig

Managing Director

US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

June 9, 2016