Embed Size (px)

DESCRIPTION

Following a year of record growth in 2010, the solar industry is facing another period of uncertainty. In this session, GTM Research’s Solar Analyst Team will discuss the implications of their research findings on corporate strategy to help your company succeed in the increasingly dynamic solar market.

Citation preview

Greentech Media’s 2011 Solar Summit

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

From Polysilicon to Power: The Solar Market in 2011 and Beyond

Greentech Media Solar Summit

Shayle Kann, Managing Director, Solar Shyam Mehta, Senior Analyst, Solar Markets

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Agenda Global PV Demand

2010 Recap 2011 Outlook U.S. Market Focus

Global PV Supply The Industrial Age Manufacturing Costs: Current Benchmarks, Evolution, Revolution Supply-Demand Dynamics Thin Film PV: Time to Taste the Pudding Supplier Competitive Positioning Where is U.S. PV Manufacturing Heading?

Q&A

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!4

Global PV Demand: A Series of Gold Rushes

Source: GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Germany in 2011? Look at 2010

Source: Bundesnetzagentur, GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Are Other Gold Rush Markets Brewing?

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

2011 and Beyond: Global Market Outlook

Current 2011 estimate: 20.6 GW (17% growth), but significant uncertainty

2012: flat given clamp-down of incentives in key FiT markets, followed by 12-20% growth in 2013-2015

Key trend is demand diffusion

Source: GTM Research Source: GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

U.S. Market Focus

Source: GTM Research/SEIA® U.S. Solar Market Insight TM: 2010 Year-in-Review

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!9

The Growing Importance of the U.S. Market

Source: GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

U.S. States With >10 MW of PV Installations, 2007

NV

NJ

CO CA

Source: GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

U.S. States With >10 MW of PV Installations, 2010

HI

NV CO

CA

FL

AZ NM

TX

IL OH

PA

MA NY

NC

NJ

OR

Source: GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Pie Size Represents Total Capacity Installed (MWdc) 258.9

MWdc

Residential

Utility

Non-Residential 2.2 MWdc

U.S. Market in 2010 - by State & Segment

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Will the Utility Market Take Over?

13

Source: GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Foreign Entrants

European PV Developers

Pure Play U.S. PV Developers

Divisions of Other Corporate Parents

Joint Ventures

Verti

cally

Inte

grat

ed M

anuf

actu

rers

Util

ity A

ffilia

tes

Inde

pend

ent P

ower

Pro

duce

rs

Ups

tream

Ent

rant

s Traditional Entrants

Corporate Entrants JV Entrants

U.S. Utility PV Project Developer Taxonomy

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Final Thoughts: We Have a Long Way to Go

15

Source: DOE, GTM Research

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

How a PV Module is Born

Polysilicon Wafer Cell Module

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

PV Enters the Industrial Age Factories w/capacity above 1 GW 2009: 1 wafer, 1 cell, 1 module 2013: 22 wafer, 15 cell, 11 module

Vertically integrated wafer-cell-module facility is dominant model of the “gigawatt fab”

Distributed module assembly model still favored by many

Polysilicon: Absence of sustained bottleneck, capital risk, technical challenges limited instances of integration

How important is downstream integration at this scale?

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

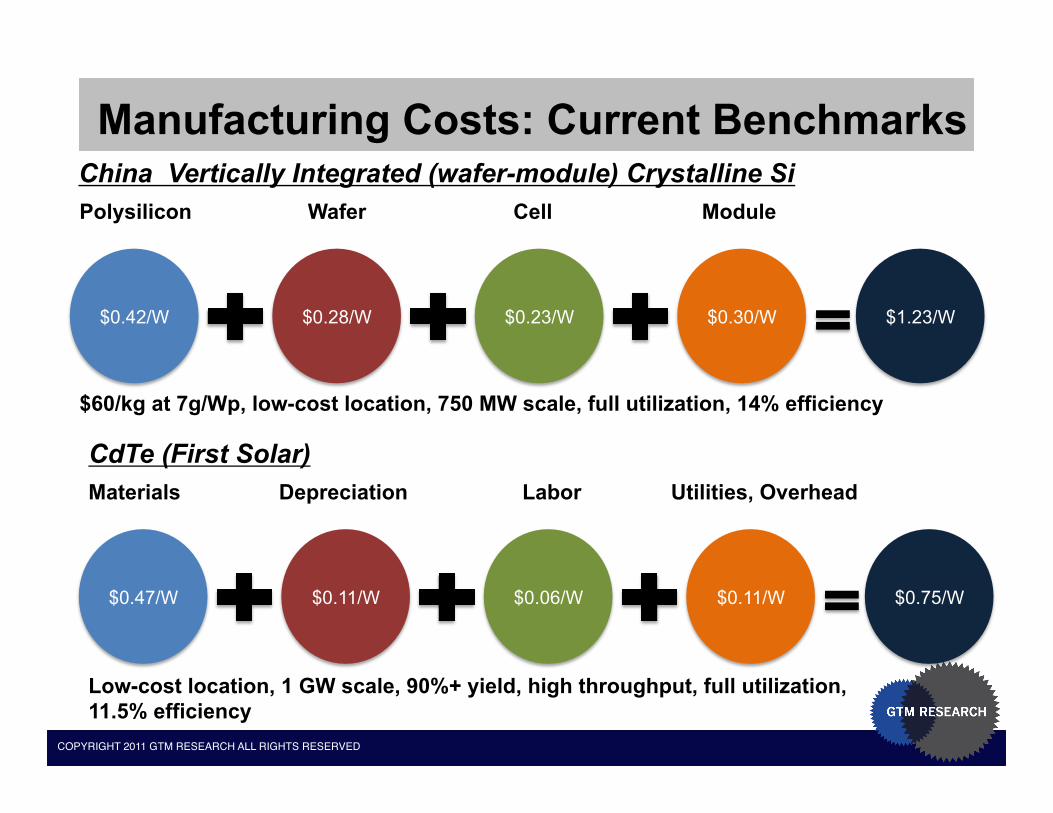

Manufacturing Costs: Current Benchmarks

$0.42/W $0.28/W $0.23/W $0.30/W $1.23/W

Polysilicon

$60/kg at 7g/Wp, low-cost location, 750 MW scale, full utilization, 14% efficiency

Wafer Cell Module

$0.47/W $0.11/W $0.06/W $0.11/W $0.75/W

Materials Depreciation Labor Utilities, Overhead

China Vertically Integrated (wafer-module) Crystalline Si

CdTe (First Solar)

Low-cost location, 1 GW scale, 90%+ yield, high throughput, full utilization, 11.5% efficiency

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Manufacturing Costs: Evolution Need to distinguish b/w

incremental improvements (current technology) vs. step-function reduction (innovation)

Incremental drivers: Cheaper poly (~$35/kg) Thinner wafers (~145 ųm) Efficiency up (~15%) Vertical integration (wafer-module) Scale-up (2 GW+)

Threats to cost reductions: Poly bottlenecks Commodity prices (Al, Ag, glass) Cost/efficiency trade-offs

When does existing technology hit a plateau?

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Manufacturing Costs: Revolution What technologies could drive step-

function cost reductions in $/kWh? Polysilicon

FBR (MEMC, REC) UMG (CaliSolar)

Wafer Diamond saws Ultra-thin wafers (< 100 ųm) Kerfless wafering (SiGen, 1366)

Cell N-type (Yingli, Suniva) Ion implantation (Suniva) Back-contact (Trina) Selective emitter (Solarfun, Schott) Other (PERL, EWT, MWT, Silicon ink)

Module High-efficiency glass (Corning) Ultra-thin/reflective encapsulant (DuPont) Glass-free front sheet (Saint-Gobain)

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Supply-Demand Dynamics Wafer/cell – need to distinguish

between low-cost and high-cost supply; module – bankable supply vs. other

Acute undersupply of low-cost cells, wafers, and bankable low-cost modules in 2010; likely to continue in H1 2011 and gate demand; pricing, availability will be tight

H2 2011 more uncertain, but likely to see price drops, higher availability of modules

2012: The return of oversupply? Price reductions required to trigger demand elasticity?

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

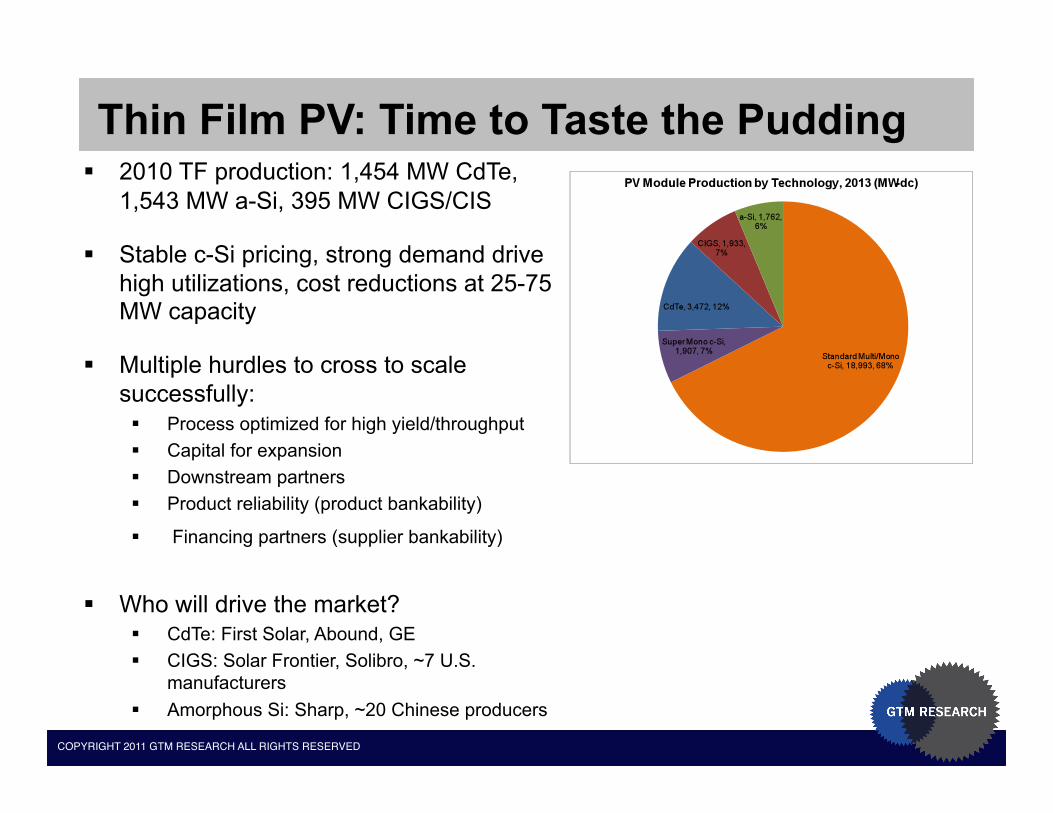

Thin Film PV: Time to Taste the Pudding 2010 TF production: 1,454 MW CdTe,

1,543 MW a-Si, 395 MW CIGS/CIS

Stable c-Si pricing, strong demand drive high utilizations, cost reductions at 25-75 MW capacity

Multiple hurdles to cross to scale successfully: Process optimized for high yield/throughput Capital for expansion Downstream partners Product reliability (product bankability)

Financing partners (supplier bankability)

Who will drive the market? CdTe: First Solar, Abound, GE CIGS: Solar Frontier, Solibro, ~7 U.S.

manufacturers Amorphous Si: Sharp, ~20 Chinese producers

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Supplier Competitive Positioning

23

Trina, Yingli

First Solar

Solar Frontier Sharp (tandem)

SunPower

Suntech

Canadian, Jinko, Hanwha

REC (Singapore)

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Where is U.S. PV Manufacturing Headed? 2013

c -‐ Si Wafer W C c -‐ Si Cell c-‐Si Module CdTe CIGS Amorphous Si

P Polysilicon M

Inverter i

COPYRIGHT 2011 GTM RESEARCH ALL RIGHTS RESERVED!

Thank You! Email:

[email protected] [email protected]

GTM Research: www.gtmresearch.com

SEIA/GTM Research U.S. Solar Market Insight: www.gtmresearch.com/solarinsight