Embed Size (px)

Citation preview

© 2013 Information Services Group, Inc. All Rights Reserved.

Proprietary and Confidential. No part of this document may be reproduced in any form or by any electronic or mechanical means,

including information storage and retrieval devices or systems, without prior written permission from Information Services Group, Inc.

HRO Today Forum, London

Julie Fernandez, Director ISG

November 2013

Practical Lessons from HR Buyers

HR SaaS

© 2013 Information Services Group, Inc. All Rights Reserved 2

HR Provider Market

AcquiringAcquiring BuildingBuilding Providing HRO ServicesProviding HRO Services

March 2012

April 2012

November 2011 Time Tracking

Canada Payroll

Big Data Analytics

HR SaaS platforms race to round out their offerings at a time when HR must

address its next generation delivery. But is HR ready and able to make the buy?

► Enterprise demand for SaaS is surging.

► Providers are acquiring, building, and wrapping services around SaaS platforms at a breakneck

pace.

► Options to buy and integrate HR technology and services have become much more complex

Aon Hewitt

IBM*

NGA*

Aon Hewitt*

* Client(s) In transition, but not yet live

© 2013 Information Services Group, Inc. All Rights Reserved 3

ISG Client Experience

► Media and marketing noise suggests a heightened level of interest from HR buyers in

aggressively pursuing and buying HR technology and/or services

� There is a significant amount of formal RFX and informal “shopping” activity by

buyers

o Direct pursuits may outnumber advisor-led projects, but are less likely to have

the same diligence, broad scope, or executive sponsorship or success

o Fast growing armies of software firms use demos and grassroots appeal to stir

demand from a user perspective

� HR SaaS suppliers cite growth in number of client logos with little apples-to-apples

comparison in client size, geography, or comparable platforms

► The extent to which this activity materializes into signed HR Cloud and/or HR

Outsourcing deals is elusive to most, if not all, HR buyers

� ISG’s analysis of engagement details for 24 HR buyers in the last 24 months

represents the largest available data set for HR clients with 10,000+ employees in

scope1

With nearly 25 recent data points from HR buyers, ISG has perhaps the largest

sample of actual data and results from HR clients actively seeking SaaS solutions

1 All but two of the client HR engagements analyzed included 10,000+ employees in-scope.

© 2013 Information Services Group, Inc. All Rights Reserved 4

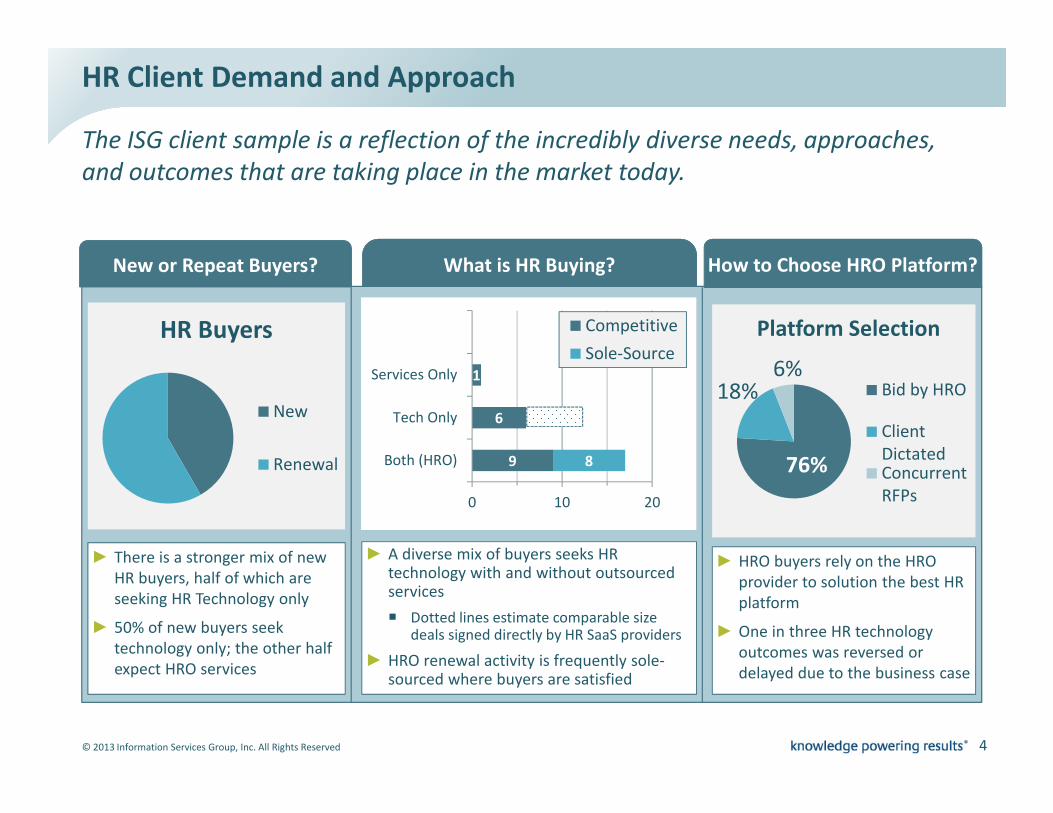

How to Choose HRO Platform?New or Repeat Buyers? What is HR Buying?

HR Client Demand and Approach

The ISG client sample is a reflection of the incredibly diverse needs, approaches,

and outcomes that are taking place in the market today.

9

6

1

8

0

0

Both (HRO)

Tech Only

Services Only

0 10 20

Competitive

Sole-Source

► There is a stronger mix of new

HR buyers, half of which are

seeking HR Technology only

► 50% of new buyers seek

technology only; the other half

expect HRO services

► A diverse mix of buyers seeks HR technology with and without outsourced services

� Dotted lines estimate comparable size deals signed directly by HR SaaS providers

► HRO renewal activity is frequently sole-sourced where buyers are satisfied

n = 24

HR Buyers

New

Renewal

► HRO buyers rely on the HRO

provider to solution the best HR

platform

► One in three HR technology

outcomes was reversed or

delayed due to the business case

76%

18%6%

Platform Selection

Bid by HRO

Client

DictatedConcurrent

RFPs

© 2013 Information Services Group, Inc. All Rights Reserved 5

HR Technology Outcome

58%12%

17%

13%

% of HR Buyers

No HRIT Change TBD

Move to SaaS Move to ERP

HR Client Results – HR Technology Only

Results may surprise you. Despite the frenzied activity in the market, large HR

clients are moving with caution and recognize value in “letting the dust settle”

►A majority of HR buyers (68%) are highly

motivated to buy HR technology

� Without a current version HR system,

most seek to upgrade or buy new

►Less than one third of HR buyers (29%)

chose to buy or upgrade HR technology

� Four had custom legacy HRIS to replace

� Two were new M&A entities with no HRIS

� One replaced vendor’s extinct platform

►1 in 4 “wait and see” buyers chose contract

extension or some other tactic that

postpones an HRIS decision two years (2015)

HR SaaS providers decline to provide stats to confirm deals with 10,000+ seats in 2012-2013

and remain elusive during client pursuits. ISG can point to only a handful of announced deals.

© 2013 Information Services Group, Inc. All Rights Reserved 6

SaaS Market Trends

Workday’s quick growth and maturity are credited with breathing life back into a

stagnant HRO market and SaaS is touted as a disruptive technology.

► HR buyers were among the earliest adopters of SaaS, beginning with talent

management, learning and recruiting platforms and now progressing to HCM

► Workday’s native SaaS platform has solidified from a U.S.-centric mid-market platform

to a formidable global market leader for HR cloud technology

� Client base has grown from 105 clients at the end of 2010 to close to 500+ clients

� Most Workday implementations (75%+) are handled by systems integrators

� Workday inundated with marketing requests; until certain the buyer is “serious” do not expect

any meaningful negotiation on fees or terms and conditions

► Oracle Fusion and SAP Employee Central are playing catch up based on their 2012

acquisitions of Taleo and SuccessFactors, respectively

� Current race to expand SaaS talent platforms acquired to include core HR/Payroll

� Incumbent providers must articulate the path to upgrade or replace the current ERP cash-cow

� Experience with ERP predecessor platforms is widespread, but there is no army of dedicated

systems integrators comparable to the Workday model

► Buyers are quickly sold on the usability, analytics and simpler infrastructure delivered

by SaaS, but less prepared for contracting and deal terms which are unlike ERP

© 2013 Information Services Group, Inc. All Rights Reserved 7

Disrupting the Disruptor

Watch for messaging from technology and service providers alike which is designed

to further drive HR buyer behavior as they shop for HR Cloud solutions

► Oracle Fusion continues to extend the trajectory of its various ERP platforms

(PeopleSoft, EBS, Fusion) in hopes of creating a smoother evolution to SaaS

► SAP has begun informal communications to suggesting there will be little or no

investment to future releases for EC6 as new product dollars fund its SaaS offering

� Until formally announced, this rumour may serve to tip the scale to SaaS for HR

buyers who already favour cloud solutions and clarify SAP’s EC6 expected life span

� Provides a strong incentive for HRO providers to consider a jump to a SF Employee

Central cloud platform to avoid transitioning clients to a “dead end” platform

► HR buyers face ambiguous options for Payroll which is limited by geography, does not

include payroll administration and tax services, or is not multi-tenant SaaS

� Global payroll providers NGA (euHReka) and ADP (GlobalView) aggressively pursue

regional and global clients that are driven by concerns to solve for multi-country

payroll and that offer proprietary HR multi-tenant technology

� Workday provides SaaS payroll for North America only, plus sophisticated

CloudConnect interfaces to global payroll providers for rest-of-world payroll

� Oracle and SAP continue to draw on their country payroll templates in ERP,

generally deployed in a single tenant model

© 2013 Information Services Group, Inc. All Rights Reserved 8

Talent and Core HR: Travel with Caution

Clients struggle today with a roadmap for integrated HR delivery and often travel

different paths depending on their focus. What happens when they meet?

Business Case

Technology

Delivery Model

Business Case

Focus on TalentFocus on Talent

Technology

► SuccessFactors, Fusion (Taleo), and

other SaaS modules offering deep

functionality & broad client base

Population / Delivery Model

► Focus on salaried workforce and top

talent with similarly limited scope

of hierarchy, self service, and

workflow for talent only

Business Case

► Expected “return on talent” with

softer business value measures

► Impacts populations most visible to

executive sponsors

Focus on Core HRFocus on Core HR

Technology

► Workday SaaS or ERP upgrades to

newly evolving SaaS modules

(Oracle Fusion, SAP/SF EE Central)

Population / Delivery Model

► Include all workforce populations

with broad support of employee

master data changes, portal/call

center & global payroll integration

Business Case

► Expected reduction in cost; focus

on hard dollar budget savings

► HR process transformation to COE

and shared services delivery

Optimize Workforce Performance

Leverage mature SaaS talent

platforms; add recruiting/learning

modules and predictive analytics

Optimize HR Operations

Deploy a single HCM for global

leverage of headcount, employee

data, and payroll integration

© 2013 Information Services Group, Inc. All Rights Reserved 9

HR Technology & Services Outcome

25%

4%

41%

17%

13%

% of HR Buyers

No Services TBD

Same HRO Switch HRO

New HRO

HR Client Results – HR Technology & Services

HRO clients want SaaS technology, but are not willing to lose their existing HR

administration support and service channels (e.g., portal, chat, contact center)

►A majority of large HR buyers (71%) chose to outsource HR technology AND services

� All but one looked to the HRO provider to propose the HR technology platform

� Workday demand has driven all HRO providers to articulate a Workday offering

►All 5 clients dissatisfied with their current HRO provider continued HR outsourcing

� No HRO clients left the outsourced model to delivery services in-house

►HRO providers are quickly productizing services around other HR technology options

HR buyers who begin their journey with a technology-only selection will ultimately struggle to

determine whether it is possible to create their own HR Shared Services delivery or outsource

© 2013 Information Services Group, Inc. All Rights Reserved 10

Value and Appeal of Combined HR Technology & Services

► The HRO delivery model is poised to become a strong channel for SaaS HCM adoption

among large global clients (7,500+ employees)

� Workday is the only SaaS system deployed to date in an HRO delivery model by

Aon Hewitt who has transitioned 3 clients and signed 5-6 more in 2013

� IBM and NorthgateArinso both have Workday clients and services in transition

► HRO clients are accustomed to a “seamless” user experience, which requires portal

capabilities and other integration that is part of the HRO’s proprietary offering

� Integrated case management, email, and chat inquiry channels

� Integrated access to online knowledgebase and policy/procedures repository

� Integration of 3rd party applications and portals (i.e., Learning, Payroll, Benefits)

� Back office administration (data entry, errors) and ongoing systems configuration

� Access to reports and analytics that combine data within the core HRIS with data

from other HR point solutions

► Clients who have already outsourced payroll for large populations have little or no

interest to bring payroll administration back in house

� Watch for HR service offerings delivered on SaaS as stand-alone payroll support

© 2013 Information Services Group, Inc. All Rights Reserved 11

HR Buyer Demand

Supplier markets are moving quickly to capitalize on filling the gaps that are of

greatest interest to HR buyers

HR SaaS Market GapsHR SaaS Market Gaps

HRO / Portal Gaps

• Adapted HRO offerings to include “thin portal” and standard services

Payroll Gaps

Shared Services / Portal Gaps

• SaaS module development• Payroll SaaS offerings• Global payroll providers

ISG believes the

combinations and

depth of SaaS-BPO

solutions will expand

significantly over the

next five years as

leading HR suppliers

productize their IP

into standard

offerings.

Provider MarketsProvider Markets

Systems Perspective

• Portal tool providers• Consulting for shared

services and org design

SaaS Deployment Gaps

• Systems integrators

Services Perspective

© 2013 Information Services Group, Inc. All Rights Reserved 12

Practical Lessons from HR Buyers

► Each HR engagement is unique and requires a carefully

thought roadmap - don’t lose focus on overall HR

� Solving for one set of HR challenges can limit or

significantly affect cost and fit in other HR areas

� Plan your timeline to select a systems integrator

► The factors that most influence HR buyer approach and

results include

� Existing HR, payroll and talent platforms

� Currently outsourced HR/Payroll services

► Capital investment in HR is hard to come by – plan for

evolving products/services and multi-year funding asks

► Contracting SaaS is a very different animal from ERP

� Data is not widely available to HR buyers for use in

vendor selection or negotiations

� Security and risk challenges to move from on-

premise to SaaS require involvement outside HR

The ISG client sample is a reflection of the incredibly diverse needs, approaches,

and outcomes that are taking place in the market today.

HR Buyer Demand for SaaSHR Buyer Demand for SaaS

HR SaaS Platform

• RFX & feature comparisons• Business case, negotiations• Systems integrator RFX• Portal platform selection

HRO Technology & Services

• HR strategy, renewal & RFX• Benchmarking• Platform change• Global payroll• Business case, negotiations

HR Services

• HR transformation, shared services strategy, research

• Process harmonization

www.isg-one.com