Embed Size (px)

Citation preview

Surviving the “Big Crunch” with insight-enabled decisions inside the plant gate

June 2, 2015

Copyright © 2015 Accenture All rights reserved.

2Copyright © 2015 Accenture All rights reserved.

Objectives

Review Accenture/ICIS survey results to understand how Chemical executives are preparing for the “Big Crunch” that often comes on the heels of a Big Bang

Preview specific actions that organizations are/should take to address OT gaps and drive Digital Plant improvements

Underscore the important role that Operational Technology (OT) will play in better positioning businesses and assets for the “Big Crunch”

Highlight industry factors that are indicative of a "Big Bang Disruption” for global chemical companies

3Copyright © 2015 Accenture All rights reserved.

The North American chemical industry appears to have solid fundamentals – with rising operating rates and profitability.

Investing in new technologies now will position organizations to be more reliable, efficient and safer later.

2002

2004

2006

2008

2010

2012

2014

50

55

60

65

70

75

80

US chemicals capacityutilization, %

Source: US Bureau of Census, ICIS Consulting, Accenture Note: Based on data from 30 chemical companies headquartered in North America

US Ethylene capacity is expected to increase by

+40% by 2020

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

50

60

70

80

90

100

110

120

130

140

North American chemical company profit index

3Q08

= 1

00

4Copyright © 2015 Accenture All rights reserved.

Despite higher utilization rates, many segments are also experiencing greater reliability issues & subsequent lost production.

Unplanned lost production for US ethylene (% of capacity)

Source: Mark W. Woods, Ethylene Strategies International, LP; 832-233-9593

Apr-10 Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-150%

2%

4%

6%

8%

10%

12%

• In an effort to capture margin and push higher utilization rates, many organizations are deferring key maintenance activities

• Unfortunately immature maintenance and reliability practices result in reactive behavior

• Excessive sweating of the assets can lead costly unplanned shutdowns, higher operating losses and even disastrous consequences

Copyright © 2015 Accenture All rights reserved. 5

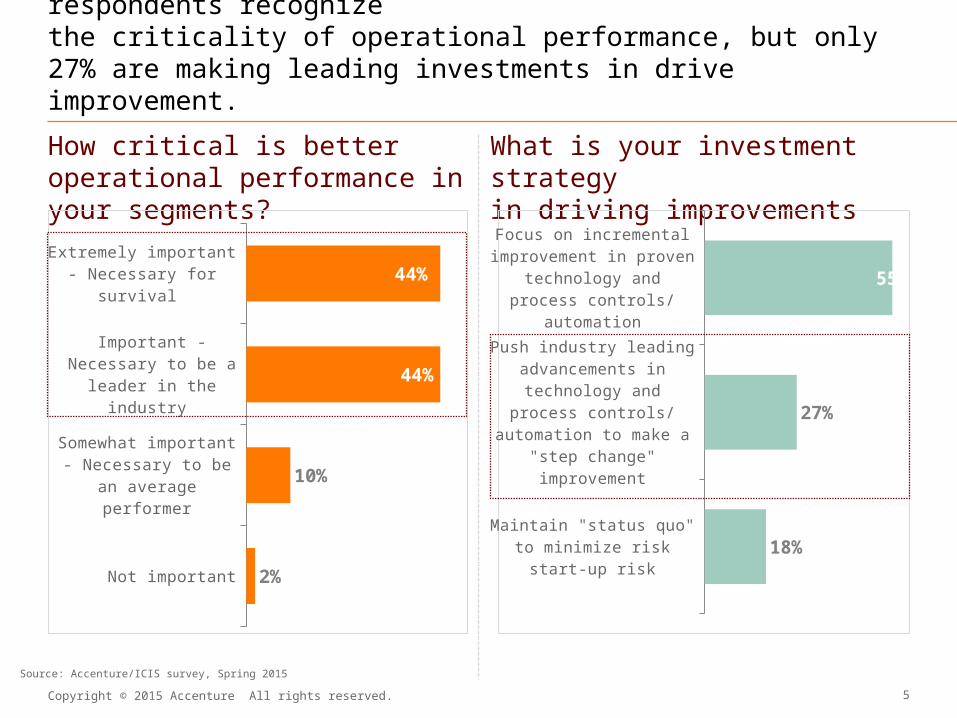

Survey results intuitively show that 88% of the respondents recognize the criticality of operational performance, but only 27% are making leading investments in drive improvement.

How critical is better operational performance in your segments?

What is your investment strategyin driving improvements

Focus on incremental improvement in proven technology and process controls/automation

Push industry leading advancements in technology and process controls/automation to make a "step change" improvement

Maintain "status quo" to minimize risk start-up risk

55%

27%

18%

Extremely important - Necessary for survival

Important - Necessary to be a leader in the industry

Somewhat important - Necessary to be an average performer

Not important

44%

44%

10%

2%

Source: Accenture/ICIS survey, Spring 2015

Copyright © 2015 Accenture All rights reserved. 6

There are challenges to achieving the step change improvements in operations enabled by technology.

Challenges affecting Operational Technology:

Lack of investment

Recent IT spending has been directed at the enterprise layer

Fractured Vendors

Consisting of a series of niche providers that focus on single capability elements, not end-to-end solutions

Governance

Operational Technologyhas historically not been underthe IT domain

Immaturity

Victim of immature life cycle management and support processes

Architecture

Plagued by antiquated point-to-point interfaces resulting in poor integration and data management

Disparate and Disconnected

Menagerie of applications resulting from repetitive acquisitions and divestments

7Copyright © 2015 Accenture All rights reserved.

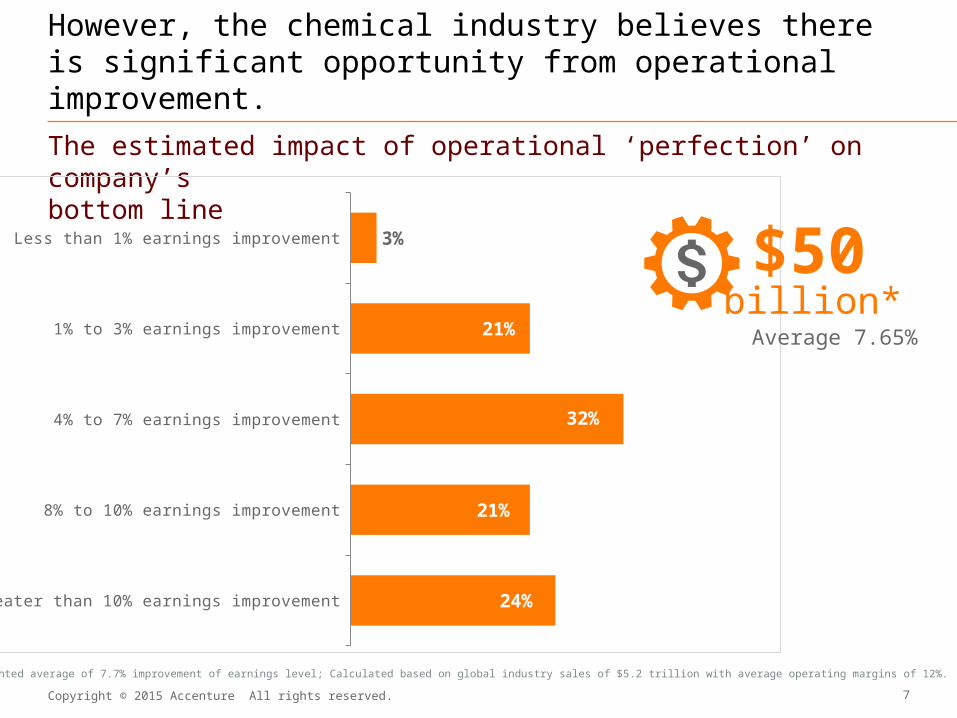

However, the chemical industry believes there is significant opportunity from operational improvement.

The estimated impact of operational ‘perfection’ on company’s bottom line

Less than 1% earnings improvement

1% to 3% earnings improvement

4% to 7% earnings improvement

8% to 10% earnings improvement

Greater than 10% earnings improvement

3%

21%

32%

21%

24%

Average 7.65%

*Based weighted average of 7.7% improvement of earnings level; Calculated based on global industry sales of $5.2 trillion with average operating margins of 12%..

$50billion*

Copyright © 2015 Accenture All rights reserved.

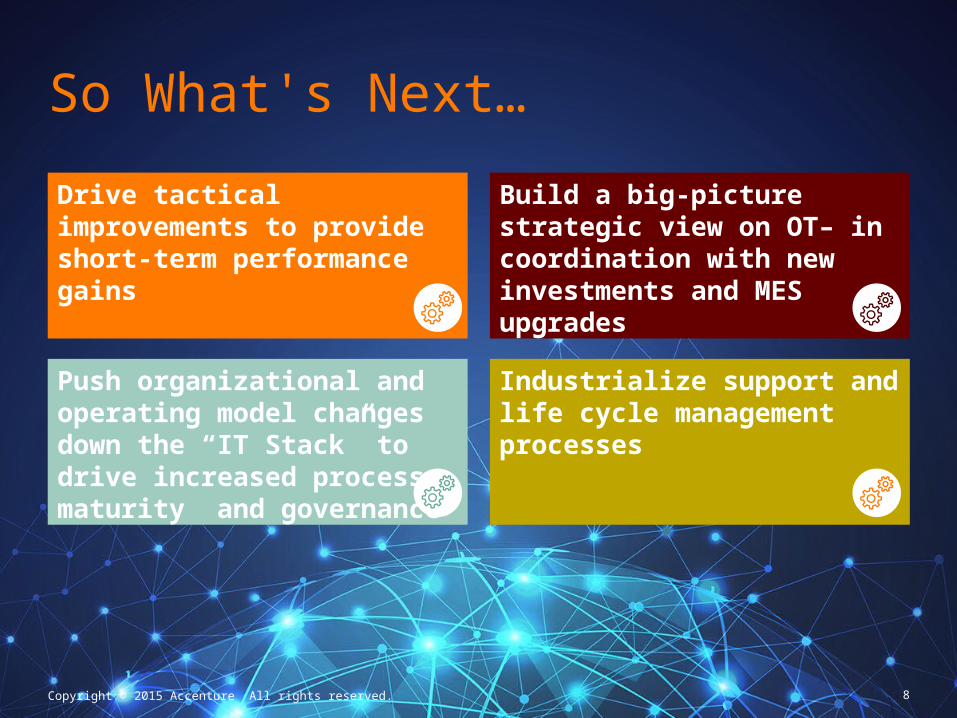

So What's Next…

8

Build a big-picture strategic view on OT– in coordination with new investments and MES upgrades

Push organizational and operating model changes down the “IT Stack” to drive increased process maturity and governance

Industrialize support and life cycle management processes

Drive tactical improvements to provide short-term performance gains

9Copyright © 2015 Accenture All rights reserved.

Digital Plant

Digital Foundation

Control Tower

Digital Workers

Digital Asset Management

Digital Operations

Talent Development & Learning

ISA-95 Lvl 2: Automation Systems

ISA-95 Lvl 1: Device I/O& Controls

ISA-95 Lvl 3: Manufacturing Ops & Control

Engineering Collaboration

OEM/MROSuppliers

Whse & ShippingContract

MFG

Contract MFG

The Digital Chemical Plant is coming.

Digital Supply Chain

FeedstockSupply

Digital Supply Chain

Sister SitesSister Sites

Offsite Pkg

Copyright © 2015 Accenture All rights reserved.

Read more:

The Digital Plant: Reaping the Rewards of Disruptionhttp://www.accenture.com/us-en/Pages/insight-digital-plant-reaping-rewards-disruption.aspx

Follow us:

10

@AccentureChems

Accenture Chemicals