Embed Size (px)

Citation preview

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance Asia markets were mixed Wednesday, following a weaker finish on Wall Street overnight as as traders await the US Federal Reserve decision due later in the US and news from the National People's Congress meeting in China. The US central bank is widely expected to stand pat on policy, but analysts will be closely watching the wording of the Federal OMC's statement for cues on the direction ahead. That un-certainty is helping to keep markets constrained. Healthcare and materials stocks pulled Wall Street lower on Tuesday in a second straight day of quiet trading as in-vestors cautiously awaited news from the US Federal Re-serve's two-day policy meeting. While the Fed is not ex-pected to raise interest rates at its meeting ending on Wednesday, investors will scour Fed Chair Janet Yellen's comments for clues indicating a path for future rate hikes. European shares retreated on Tuesday, led lower by com-modity stocks, after the Bank of Japan left policy un-changed but presented a bleaker view of the country's economy. The STOXX Europe 600 Basic Resources index fell 4.7 percent, the top sectoral decliner, as copper prices dipped. The European oil and gas index was also down 1.8 percent as crude oil prices slipped. Previous day Roundup Fall in global peers and oil prices dragged Indian equity benchmarks 1 percent Tuesday ahead of Federal Reserve's two-day meeting that will begin tonight. Pharma, FMCG, technology and HDFC group stocks were under pressure. The Sensex fell 253.11 points to 24551.17 and the Nifty declined 78.15 points to 7460.60. The broader markets also caught in bear grip as the BSE Midcap and Smallcap indices slipped 0.8% and 0.6%, respectively. On the global front, European equities were under pressure with FTSE, CAC and DAX falling around a percent, tracking a shaky lead in Asia where markets were mostly lower. The BoJ decided to keep its monetary policy steady rather than increasing its firepower. Japan's Nikkei and Hong Kong's Hang Seng fell 0.7% each while Shanghai gained 0.2%. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 2.44pts], Capital Goods [down 26.59Pts], PSU [up 19.34pts], FMCG [down 116.61Pts], Realty [down pts], Power [down pts], Auto [down 121.26Pts], Healthcare [down 482.50Pts], IT [down 92.27pts], Metals [up 14.17Pts], TECK [down 54.47pts], Oil& Gas [up 25.11pts].

World Indices

Index Value % Change

D J l 17251.53 +0.13

S&P 500 2015.93 -0.18

NASDAQ 4728.67 -0.45

FTSE 100 6139.97 -0.56

Nikkei 225 17051.37 -0.38

Hong Kong 20283.07 -0.03

Top Gainers

Company CMP Change % Chg

SBIN 185.05 3.30 1.82

BANKBARODA 143.50 2.55 1.81

PNB 83.35 1.05 1.28

BOSCHLTD 18,190.00 199.00 1.11

TATASTEEL 300.00 3.00 1.11

Top Losers

Company CMP Change % Chg

LUPIN 1,725.10 144.10 -7.71

HDFC 1,113.15 45.55 -3.93

ZEEL 384.85 15.65 -3.91

DRREDDY 3,133.00 100.65 -3.11

ITC 316.80 8.25 -2.54

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

DHAMPURSUG 83.80 9.25 12.41

DWARKESH 207.45 17.45 9.18

OUDHSUG 65.00 10.80 19.93

SASKEN 418.00 39.80 10.52

SUPREMEIND 773.90 3.90 0.51

Indian Indices

Company CMP Change % Chg

NIFTY 7460.60 -78.15 -1.04

SENSEX 24551.17 -253.11 -1.02

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

IPCALAB 535.90 -6.70 -1.23

GLOBOFFS 260.50 -11.00 -4.05

SPECIALITY 81.60 0.80 0.99

ORBTEXP 270.00 -0.45 -0.17

PRESTIGE 140.15 -1.90 -1.34

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH] 3. JUBILNT LIFE SCIENCE

JUBILANT LIFE SCIENCE facing profit booking at higher level in last two session it created greavstone doji on daily chat, since volatility is high so we advise to sell it on rise around 385 with strict stop loss of 391 for target of 375 360 and below 355 target may extend up to 340 MACRO NEWS See 10-12% growth in FY18; rev to touch Rs 7200 cr:

Crompton OMCs to approach govt, EC over petrol, diesel price hike RIP: 33-yr old Vicks Action 500 Extra no more on safety

grounds Reverse merger of NICE, NECE with BF Utilities in 6

mnths: Kheny SC directs Swamy to amend petition against Jet-Etihad

deal Mozambique LNG discusses gas export with Indian com-

panies GSFC inks in-principle agreement with KRN for debt fi-

nancing L&T bags orders worth Rs 1,672 crore Lupin receives 9 observations from USFDA for Goa plant AuroPharma gets final USFDA nod for osteoporosis drug P&G stops selling Vicks Action500 Extra in India after ban Glenmark gets final USFDA nod for migraine drug Go vt Gets Bids For 7.2 mmscmd In 3rd Round Of Auction Gulf Oil International Signed 3-Year Multi Million Dollar

Deal With Man United Theoretically possible to cut rates to -0.5%: BOJ's Kuroda GMR, GVK, Lanco to get a slice of Rs 1,200-cr gas subsidy Govt imposes anti-dumping duty on plastic-processing

imports Sebi allows FPIs to invest in REITs, corp bonds under de-

fault

STOCK RECOMMENDATIONS [FUTURE] 1. ENGINERIND [FUTURE]

ENGINERSIND Future is near to last one week support of 160. in last session it consolidate in range of 162-160 since the market taken reversal from resistance of 7600 for that we can see more weakness in upcoming days so sell it below 160 for target of 158 155.50 with stop loss of 162 2. ADANIPORTS [FUTURE]

ADANIPORTS faced profit booking near breakout level of 233 before last session it cross these level but it finished with doji candle in last session it breached around 1.50% which is confirmation of trend reversal so we advise to sell it around 231-232 with strict stop loss of 235 for target of 228 225.

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 7,600 48.00 2,49,684 61,58,250

NIFTY CE 7,700 22.55 1,93,923 66,77,925

BANKNIFTY CE 16,000 86.10 57,841 6,76,350

CROMPGREA CE 50 1.05 5,663 37,44,000

SBIN CE 190 4.50 3,895 41,34,000

SBIN CE 185 6.70 2,586 22,52,000

TATASTEEL CE 300 11.00 2,445 22,34,000

LUPIN CE 1,800 29.15 2,336 1,84,800

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 7,400 65.40 2,29,631 50,64,600

NIFTY PE 7,500 103.40 2,28,928 40,55,950

BANKNIFTY PE 15,000 150.10 46,888 5,87,580

LUPIN PE 1,700 42.80 3,139 1,25,700

SBIN PE 180 3.75 2,010 24,64,000

CROMPGREA PE 40 1.40 1,957 14,31,000

TATASTEEL PE 290 6.40 1,805 13,00,000

LUPIN PE 1,750 63.50 1,489 57,300

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 35287 1892.96 25150 1339.28 308544 16937.29 553.68

INDEX OPTIONS 413802 22716.74 398207 21843.26 1391184 76774.47 873.48

STOCK FUTURES 60762 2838.58 75739 3522.18 1036854 46603.35 -683.60

STOCK OPTIONS 34451 1611.78 34731 1616.60 79887 3648.18 -4.82

TOTAL 738.75

STOCKS IN NEWS

HDFC tanks 4%, Goldman Sachs downgrades on corpo-rate lending biz

TVS eyes 10% sales growth in domestic two-wheeler next fiscal

ICICI Bank launches contactless mobile pay solution 'iTap'

Cairn India gets over `29000 cr tax demand Reliance Capital eyes Indian assets of JP Morgan AMC Wipro Partners With Schneider Electric Adani Enterpries’ coal project gets Queensland parlia-

ment’s nod Crompton sheds 74% as consumer pdts biz demerger

takes effect

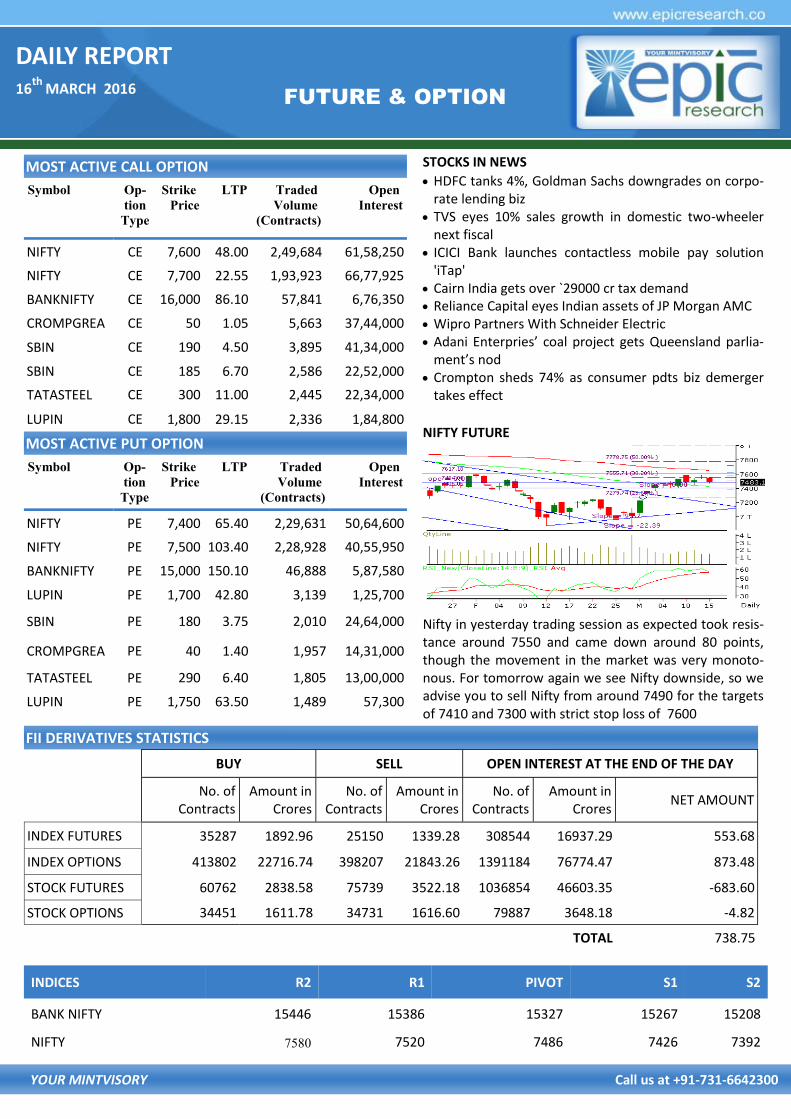

NIFTY FUTURE

Nifty in yesterday trading session as expected took resis-tance around 7550 and came down around 80 points, though the movement in the market was very monoto-nous. For tomorrow again we see Nifty downside, so we advise you to sell Nifty from around 7490 for the targets of 7410 and 7300 with strict stop loss of 7600

INDICES R2 R1 PIVOT S1 S2

BANK NIFTY 15446 15386 15327 15267 15208

NIFTY 7580 7520 7486 7426 7392

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

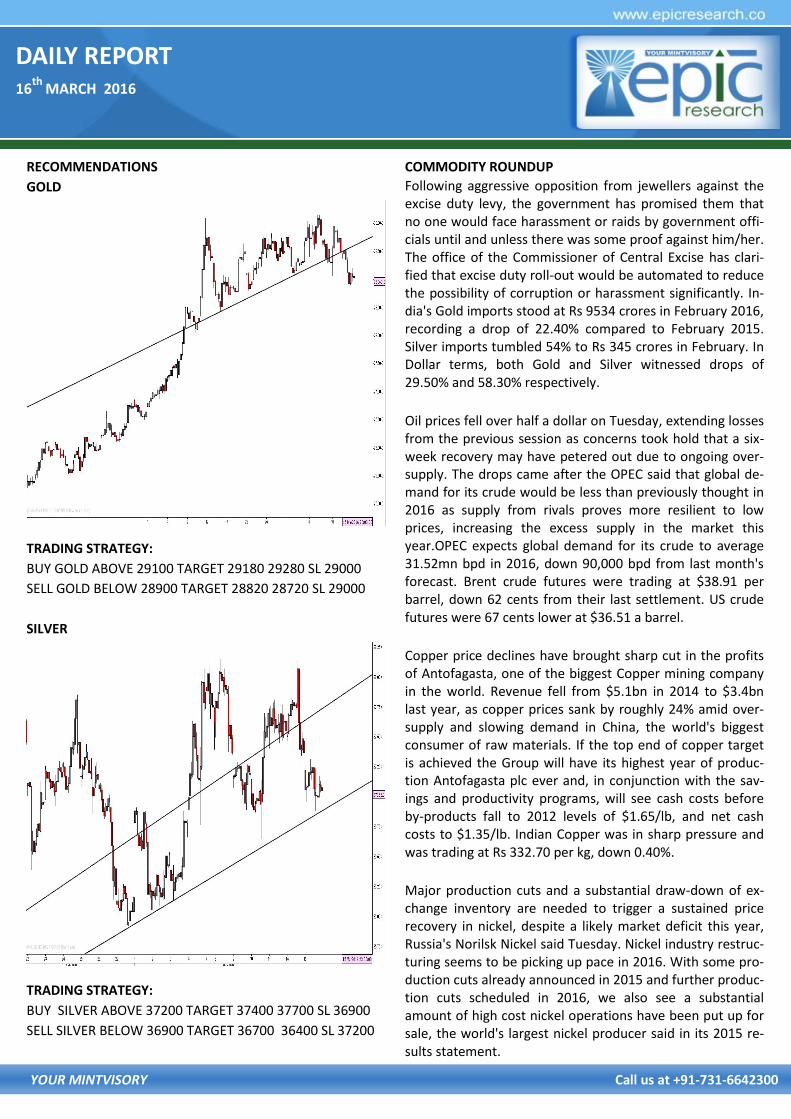

GOLD

TRADING STRATEGY:

BUY GOLD ABOVE 29100 TARGET 29180 29280 SL 29000

SELL GOLD BELOW 28900 TARGET 28820 28720 SL 29000

SILVER

TRADING STRATEGY:

BUY SILVER ABOVE 37200 TARGET 37400 37700 SL 36900

SELL SILVER BELOW 36900 TARGET 36700 36400 SL 37200

COMMODITY ROUNDUP

Following aggressive opposition from jewellers against the excise duty levy, the government has promised them that no one would face harassment or raids by government offi-cials until and unless there was some proof against him/her. The office of the Commissioner of Central Excise has clari-fied that excise duty roll-out would be automated to reduce the possibility of corruption or harassment significantly. In-dia's Gold imports stood at Rs 9534 crores in February 2016, recording a drop of 22.40% compared to February 2015. Silver imports tumbled 54% to Rs 345 crores in February. In Dollar terms, both Gold and Silver witnessed drops of 29.50% and 58.30% respectively.

Oil prices fell over half a dollar on Tuesday, extending losses from the previous session as concerns took hold that a six-week recovery may have petered out due to ongoing over-supply. The drops came after the OPEC said that global de-mand for its crude would be less than previously thought in 2016 as supply from rivals proves more resilient to low prices, increasing the excess supply in the market this year.OPEC expects global demand for its crude to average 31.52mn bpd in 2016, down 90,000 bpd from last month's forecast. Brent crude futures were trading at $38.91 per barrel, down 62 cents from their last settlement. US crude futures were 67 cents lower at $36.51 a barrel.

Copper price declines have brought sharp cut in the profits of Antofagasta, one of the biggest Copper mining company in the world. Revenue fell from $5.1bn in 2014 to $3.4bn last year, as copper prices sank by roughly 24% amid over-supply and slowing demand in China, the world's biggest consumer of raw materials. If the top end of copper target is achieved the Group will have its highest year of produc-tion Antofagasta plc ever and, in conjunction with the sav-ings and productivity programs, will see cash costs before by-products fall to 2012 levels of $1.65/lb, and net cash costs to $1.35/lb. Indian Copper was in sharp pressure and was trading at Rs 332.70 per kg, down 0.40%.

Major production cuts and a substantial draw-down of ex-change inventory are needed to trigger a sustained price recovery in nickel, despite a likely market deficit this year, Russia's Norilsk Nickel said Tuesday. Nickel industry restruc-turing seems to be picking up pace in 2016. With some pro-duction cuts already announced in 2015 and further produc-tion cuts scheduled in 2016, we also see a substantial amount of high cost nickel operations have been put up for sale, the world's largest nickel producer said in its 2015 re-sults statement.

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX INDICES

Index Value % Change

CHANA 4379 -2.21

CORIANDER 6681 -0.54

COTTON SEED 2130 -1.98

GUAR SEED 3074 -1.57

JEERA 14815 +0.37

MUSTARDSEED 3923 -0.68

SOY BEAN 3662 -0.76

SUGAR M GRADE 3302 +0.76

TURMERIC 9228 -0.65

WHEAT 1627 +2.97

RECOMMENDATIONS

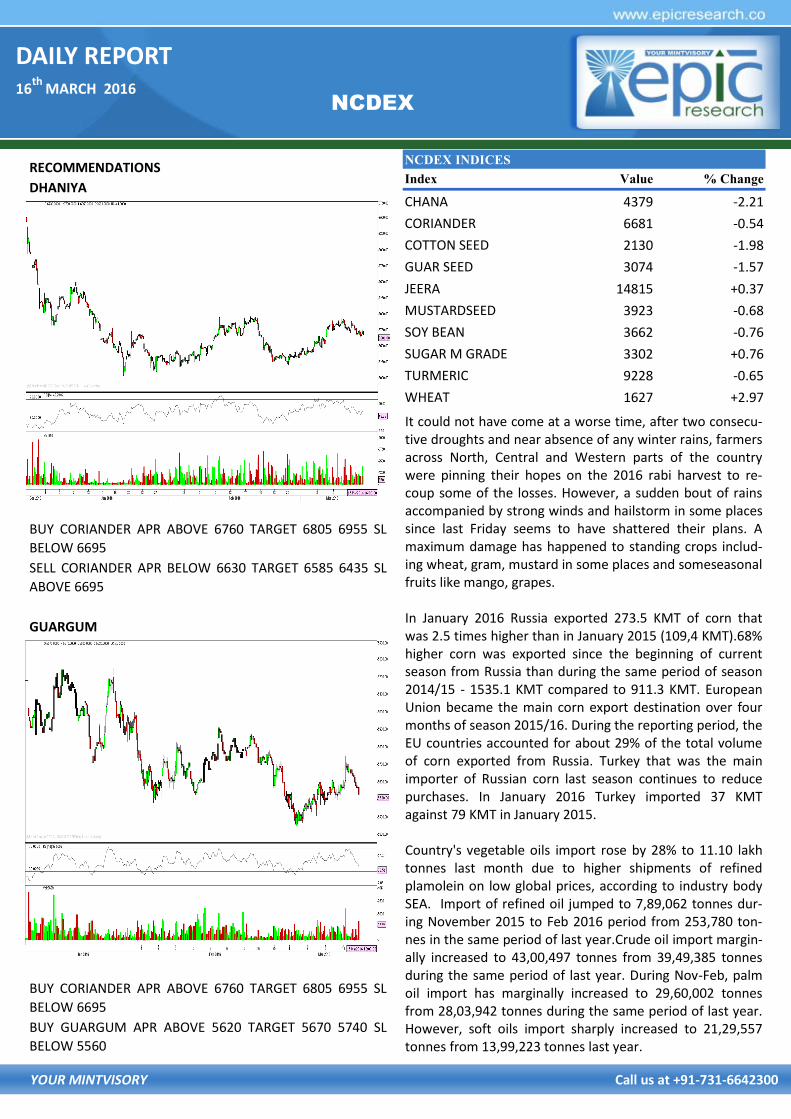

DHANIYA

BUY CORIANDER APR ABOVE 6760 TARGET 6805 6955 SL

BELOW 6695

SELL CORIANDER APR BELOW 6630 TARGET 6585 6435 SL

ABOVE 6695

GUARGUM

BUY CORIANDER APR ABOVE 6760 TARGET 6805 6955 SL

BELOW 6695

BUY GUARGUM APR ABOVE 5620 TARGET 5670 5740 SL

BELOW 5560

It could not have come at a worse time, after two consecu-tive droughts and near absence of any winter rains, farmers across North, Central and Western parts of the country were pinning their hopes on the 2016 rabi harvest to re-coup some of the losses. However, a sudden bout of rains accompanied by strong winds and hailstorm in some places since last Friday seems to have shattered their plans. A maximum damage has happened to standing crops includ-ing wheat, gram, mustard in some places and someseasonal fruits like mango, grapes. In January 2016 Russia exported 273.5 KMT of corn that was 2.5 times higher than in January 2015 (109,4 KMT).68% higher corn was exported since the beginning of current season from Russia than during the same period of season 2014/15 - 1535.1 KMT compared to 911.3 KMT. European Union became the main corn export destination over four months of season 2015/16. During the reporting period, the EU countries accounted for about 29% of the total volume of corn exported from Russia. Turkey that was the main importer of Russian corn last season continues to reduce purchases. In January 2016 Turkey imported 37 KMT against 79 KMT in January 2015. Country's vegetable oils import rose by 28% to 11.10 lakh tonnes last month due to higher shipments of refined plamolein on low global prices, according to industry body SEA. Import of refined oil jumped to 7,89,062 tonnes dur-ing November 2015 to Feb 2016 period from 253,780 ton-nes in the same period of last year.Crude oil import margin-ally increased to 43,00,497 tonnes from 39,49,385 tonnes during the same period of last year. During Nov-Feb, palm oil import has marginally increased to 29,60,002 tonnes from 28,03,942 tonnes during the same period of last year. However, soft oils import sharply increased to 21,29,557 tonnes from 13,99,223 tonnes last year.

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 67.2290 Yen-100 59.3100

Euro 74.6444 GBP 95.9223

CURRENCY

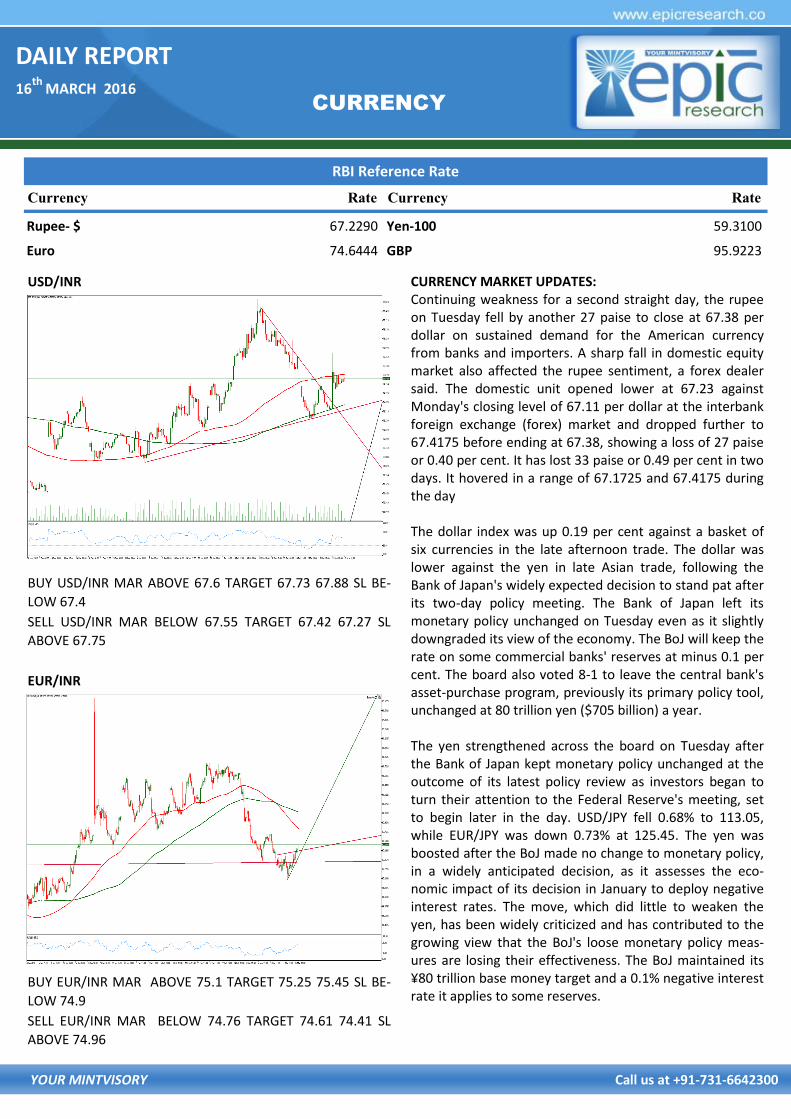

USD/INR

BUY USD/INR MAR ABOVE 67.6 TARGET 67.73 67.88 SL BE-

LOW 67.4

SELL USD/INR MAR BELOW 67.55 TARGET 67.42 67.27 SL

ABOVE 67.75

EUR/INR

BUY EUR/INR MAR ABOVE 75.1 TARGET 75.25 75.45 SL BE-

LOW 74.9

SELL EUR/INR MAR BELOW 74.76 TARGET 74.61 74.41 SL

ABOVE 74.96

CURRENCY MARKET UPDATES: Continuing weakness for a second straight day, the rupee on Tuesday fell by another 27 paise to close at 67.38 per dollar on sustained demand for the American currency from banks and importers. A sharp fall in domestic equity market also affected the rupee sentiment, a forex dealer said. The domestic unit opened lower at 67.23 against Monday's closing level of 67.11 per dollar at the interbank foreign exchange (forex) market and dropped further to 67.4175 before ending at 67.38, showing a loss of 27 paise or 0.40 per cent. It has lost 33 paise or 0.49 per cent in two days. It hovered in a range of 67.1725 and 67.4175 during the day The dollar index was up 0.19 per cent against a basket of six currencies in the late afternoon trade. The dollar was lower against the yen in late Asian trade, following the Bank of Japan's widely expected decision to stand pat after its two-day policy meeting. The Bank of Japan left its monetary policy unchanged on Tuesday even as it slightly downgraded its view of the economy. The BoJ will keep the rate on some commercial banks' reserves at minus 0.1 per cent. The board also voted 8-1 to leave the central bank's asset-purchase program, previously its primary policy tool, unchanged at 80 trillion yen ($705 billion) a year. The yen strengthened across the board on Tuesday after the Bank of Japan kept monetary policy unchanged at the outcome of its latest policy review as investors began to turn their attention to the Federal Reserve's meeting, set to begin later in the day. USD/JPY fell 0.68% to 113.05, while EUR/JPY was down 0.73% at 125.45. The yen was boosted after the BoJ made no change to monetary policy, in a widely anticipated decision, as it assesses the eco-nomic impact of its decision in January to deploy negative interest rates. The move, which did little to weaken the yen, has been widely criticized and has contributed to the growing view that the BoJ's loose monetary policy meas-ures are losing their effectiveness. The BoJ maintained its ¥80 trillion base money target and a 0.1% negative interest rate it applies to some reserves.

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

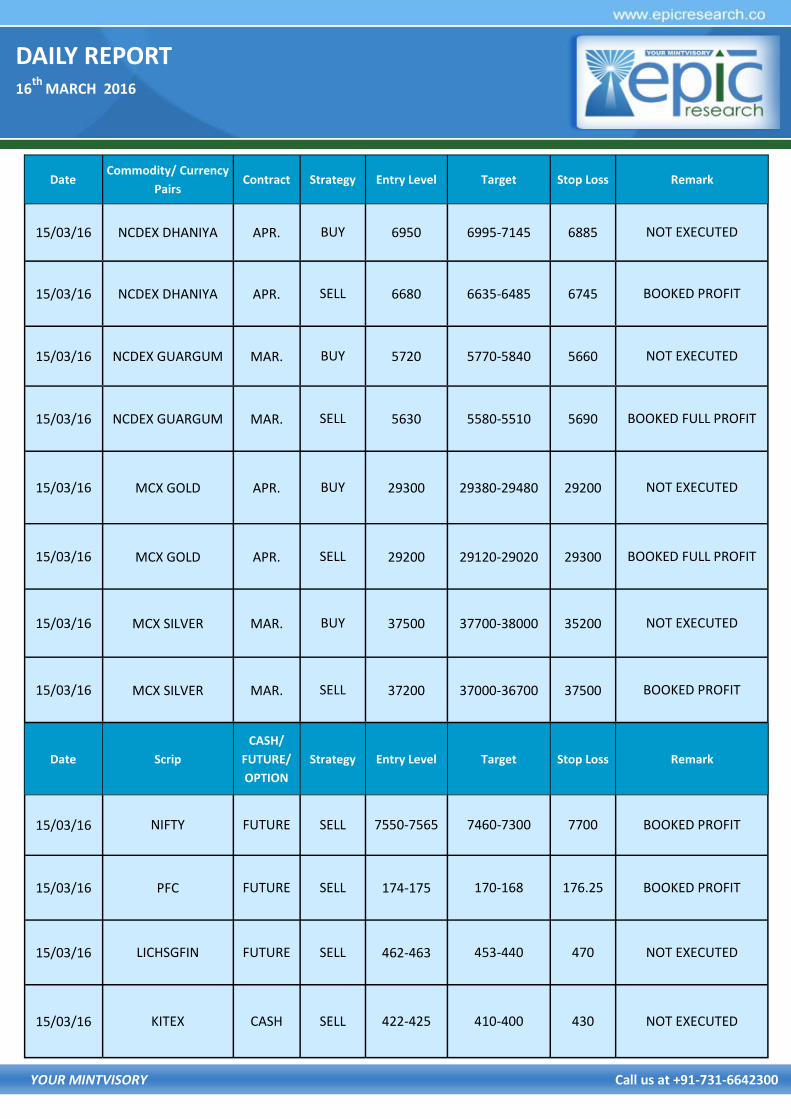

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

15/03/16 NCDEX DHANIYA APR. BUY 6950 6995-7145 6885 NOT EXECUTED

15/03/16 NCDEX DHANIYA APR. SELL 6680 6635-6485 6745 BOOKED PROFIT

15/03/16 NCDEX GUARGUM MAR. BUY 5720 5770-5840 5660 NOT EXECUTED

15/03/16 NCDEX GUARGUM MAR. SELL 5630 5580-5510 5690 BOOKED FULL PROFIT

15/03/16 MCX GOLD APR. BUY 29300 29380-29480 29200 NOT EXECUTED

15/03/16 MCX GOLD APR. SELL 29200 29120-29020 29300 BOOKED FULL PROFIT

15/03/16 MCX SILVER MAR. BUY 37500 37700-38000 35200 NOT EXECUTED

15/03/16 MCX SILVER MAR. SELL 37200 37000-36700 37500 BOOKED PROFIT

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

15/03/16 NIFTY FUTURE SELL 7550-7565 7460-7300 7700 BOOKED PROFIT

15/03/16 PFC FUTURE SELL 174-175 170-168 176.25 BOOKED PROFIT

15/03/16 LICHSGFIN FUTURE SELL 462-463 453-440 470 NOT EXECUTED

15/03/16 KITEX CASH SELL 422-425 410-400 430 NOT EXECUTED

DAILY REPORT 16

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, MARCH 14

- -

TUESDAY, MARCH 15

8:30 AM RETAIL SALES FEB. -0.3% 0.2%

8:30 AM RETAIL SALES EX-AUTOS FEB. -0.3% 0.1%

8:30 AM PRODUCER PRICE INDEX FEB. -0.1% 0.1%

8:30 AM EMPIRE STATE INDEX MARCH -10.0 -16.6

10 AM HOME BUILDERS' INDEX MARCH -- 58

10 AM BUSINESS INVENTORIES JAN. 0.0% 0.1%

WEDNESDAY, MARCH 16

8:30 AM CONSUMER PRICE INDEX FEB. -0.2% 0.0%

8:30 AM CORE CPI FEB. 0.2% 0.3%

8:30 AM HOUSING STARTS FEB. 1.158MLN 1.099MLN

8:30 AM BUILDING PERMITS FEB. 1,205MLN 1.202MLN

9:15 AM INDUSTRIAL PRODUCTION FEB. -0.7% 0.9%

9:15 AM CAPACITY UTILIZATION FEB. 76.6% 77.1%

2 PM FOMC ANNOUNCEMENT

2:30 PM JANET YELLEN PRESS CONFERENCE

THURSDAY, MARCH 17

8:30 AM WEEKLY JOBLESS CLAIMS 3/12 N/A N/A

8:30 AM PHILLY FED MARCH -4.0 -2.8

8:30 AM CURRENT ACCOUNT Q4 -- -$124BLN

FRIDAY, MARCH 18

10 AM CONSUMER SENTIMENT MARCH 92.2 91.7