Embed Size (px)

Citation preview

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

European shares fell on Monday, led lower by a slump in utility EDF after a senior executive quit, and by weaker bank stocks which were hit by some broker price target cuts. European stocks have rallied after a rocky start to 2016, as oil prices recovered and fears over a U.S. eco-nomic slowdown abated. Nevertheless, the pan-European FTSEurofirst 300 index remains down around 7% so far in 2016. JP Morgan Cazenove reduced its rating on equities to "underweight" for the first time since 2007, saying the re-cent market rebound was set to peter out. The FTSEuro-first, which reached one-month highs on Friday after three straight weeks of gains, closed 0.3% lower. The euro zone's blue-chip Euro STOXX 50 index fell 0.5%.

The Dow Jones industrial average and the S&P 500 index closed higher on Monday as a spike in energy shares offset sharp declines in large-cap technology names, which dragged down the Nasdaq. Crude prices, which have largely dictated the direction of the stock market this year, were up more than 5 percent. The S&P 500 energy sector .SPNY, up 2.4 percent, rose for the fifth consecutive session, a streak not seen since October. It is up more than 23 per-cent from its 2016 low in mid-January.

Japan's economy contracted less than initially estimated in the final quarter of 2015 but private consumption re-mained weak, underscoring the challenges facing premier Shinzo Abe in restoring growth amid intensifying overseas headwinds.

Previous day Roundup

Indian stock markets edged higher on Friday, posting their best weekly gain in more than four years, tracking gains in Asian markets and on improved risk appetite after the gov-ernment unveiled a fiscally prudent budget earlier this week. The Sensex was up 39.49 points at 24646.48, and the Nifty was up 9.75 points at 7485.35. About 1516 shares have advanced, 1087 shares declined, and 145 shares are unchanged. Bank Nifty posts biggest weekly gains in 10 years.

Index stats

The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 14.13pts], Capital Goods [up 11.15Pts], PSU [up 113.93pts], FMCG [up 7.96Pts], Realty [up 11.56pts], Power [up 19.90pts], Auto [up 35.09Pts], Healthcare [up 49.30Pts], IT [down 51.28pts], Metals [up 156.88Pts], TECK [down 24.11pts], Oil& Gas [up 34.26pts].

World Indices

Index Value % Change

D J l 17073.95 +67.18

S&P 500 2001.76 +1.77

NASDAQ 4708.25 -0.19

FTSE 100 6182.40 -17.03

Nikkei 225 16635.26 -276.06

Hong Kong 19954.69 -1.02

Top Gainers

Company CMP Change % Chg

PNB 83.35 4.35 5.51

BHEL 107.70 4.40 4.26

VEDL 87.15 3.20 3.81

SBIN 189.10 6.35 3.47

COALINDIA 325.00 10.90 3.47

Top Losers

Company CMP Change % Chg

HCLTECH 835.10 24.20 -2.82

TECHM 450.00 11.75 -2.54

IDEA 105.75 2.60 -2.40

ASIANPAINT 867.00 13.25 -1.51

SUNPHARMA 857.90 13.00 -1.49

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

JSWSTEEL 1,194.00 34.20 2.95

KELLTONTEC 215.40 19.55 9.98

MINDAIND 977.00 134.30 15.94

MINDTREE 1,595.95 20.55 1.30

- -

Indian Indices

Company CMP Change % Chg

NIFTY 7485.35 +9.75 +0.13

SENSEX 24646.48 +39.49 +0.16

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

MONSANTO 1,590.10 -39.00 -2.39

RAIREKMOH 112.00 -4.85 -4.15

SHOPERSTOP 334.30 -7.50 -2.19

VIDHIDYE 57.00 -0.95 -1.64

ZODIACLOTH 222.00 -10.55 -4.54

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH] 3. SINTEX

In SINTEX we have seen that it has crossed a good resis-tance level of 72 but closed below but strength is seen in the volume in the stock so breakout is expected in the stock above this level in next trading session, so it is sug-gested to buy stock around 72.50-72.60 with a strict stop loss of 71.50 for the targets up to 73.60-75. MACRO NEWS

Alkem's Mandva plant gets establishment nod from US-FDA

CBDT forms directorates to monitor taxpayer service

Nalco to invest Rs 900 crore in Kakrapar Atomic Power plant

FDI in food processing to act as catalyst: Minister

Siemens Board approves sale of healthcare undertaking for Rs 3,050 crore

Economic affairs secretary says -Looking at Rs 50,000 crore in total for bank recapitalization

Environment Ministry releases new categorisation of industries

Finance Ministry says jewellers with turnover of over Rs 12cr to pay 1% excise on non-silver jewellery

Nalco to invest Rs 900cr in Kakrapar Atomic power plant

Ajanta Pharma receives US FDA nod for Almotriptan Malate tablets

Chambal Fertilisers signs Rs 500 crore term loan, Rs 300 crore bank guarantee agreement with SBI

Direct benefit transfer for fertilisers a welcome step: RCF

CIL mines have not halted production; demand weak: Swarup

Pharma crusader Thakur takes India's drug regulators to court

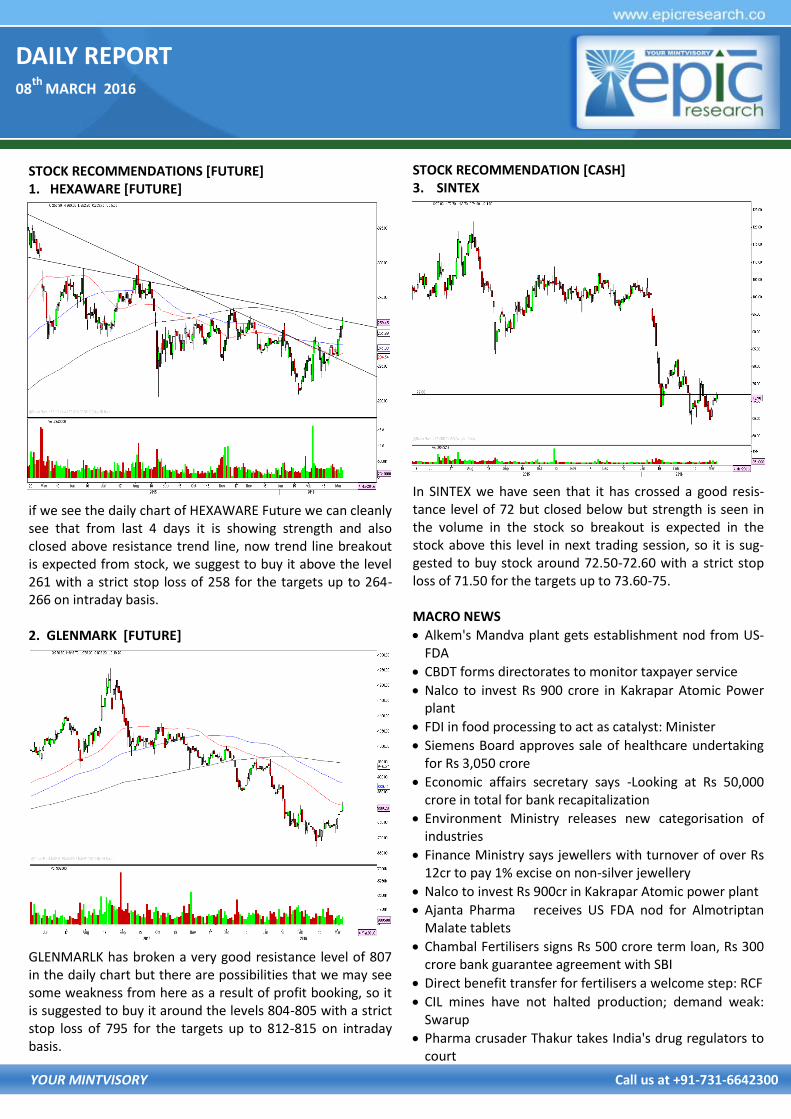

STOCK RECOMMENDATIONS [FUTURE] 1. HEXAWARE [FUTURE]

if we see the daily chart of HEXAWARE Future we can cleanly see that from last 4 days it is showing strength and also closed above resistance trend line, now trend line breakout is expected from stock, we suggest to buy it above the level 261 with a strict stop loss of 258 for the targets up to 264-266 on intraday basis. 2. GLENMARK [FUTURE]

GLENMARLK has broken a very good resistance level of 807 in the daily chart but there are possibilities that we may see some weakness from here as a result of profit booking, so it is suggested to buy it around the levels 804-805 with a strict stop loss of 795 for the targets up to 812-815 on intraday basis.

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,000 39.80 2,33,012 55,62,675

NIFTY CE 8,100 21.75 1,46,587 48,57,300

BANKNIFTY CE 17,000 151.35 42,269 4,86,780

TATASTEEL CE 280 7.40 4,327 14,86,000

IFCI CE 30 1.10 3,545 1,07,20,000

SBIN CE 230 2.65 3,161 54,84,000

LT CE 1,300 18.25 2,289 6,16,200

RELINFRA CE 620 25.00 2,289 5,82,400

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 7,700 87.50 1,61,166 44,92,800

NIFTY PE 7,800 125.85 1,52,661 42,26,850

BANKNIFTY PE 16,000 144.85 42,029 4,38,780

TATASTEEL PE 250 3.00 2,528 18,50,000

TATASTEEL PE 260 5.25 2,117 13,82,000

SBIN PE 220 7.50 1,885 17,92,000

SBIN PE 210 3.55 1,545 17,80,000

RELINFRA PE 600 22.50 1,402 5,53,800

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 34231 1818.40 32193 1670.98 277359 15048.14 147.42

INDEX OPTIONS 546312 29387.59 550980 29633.61 1268446 70402.85 -246.02

STOCK FUTURES 97883 4340.39 89914 4040.20 1075198 48210.67 300.19

STOCK OPTIONS 55229 2396.16 55559 2393.99 58622 2613.38 2.17

TOTAL

STOCKS IN NEWS

Tech Mahindra Bombay HC approves amalgamation of TechM BPO and New vC Services

L&T completes sale of Coimbatore casting manufactur-ing unit to Bradken

Ashok Leyland to invest USD 10mn to expand UAE manufacturing plant capacity

Jindal Photo Bombay High Court approves scheme of arrangement between Jindal Poly Films & Company

Sadbhav Engineering unit Rohtak Panipat tollway re-sumes toll operations

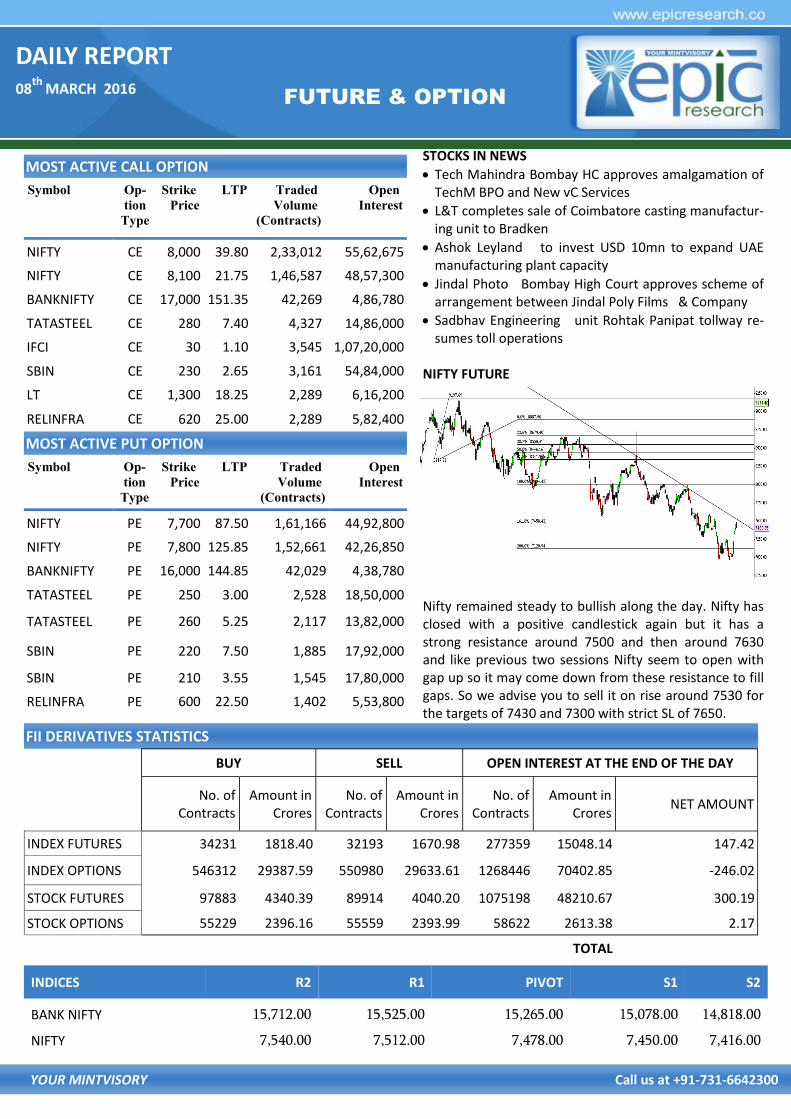

NIFTY FUTURE

Nifty remained steady to bullish along the day. Nifty has closed with a positive candlestick again but it has a strong resistance around 7500 and then around 7630 and like previous two sessions Nifty seem to open with gap up so it may come down from these resistance to fill gaps. So we advise you to sell it on rise around 7530 for the targets of 7430 and 7300 with strict SL of 7650.

INDICES R2 R1 PIVOT S1 S2

BANK NIFTY 15,712.00 15,525.00 15,265.00 15,078.00 14,818.00

NIFTY 7,540.00 7,512.00 7,478.00 7,450.00 7,416.00

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

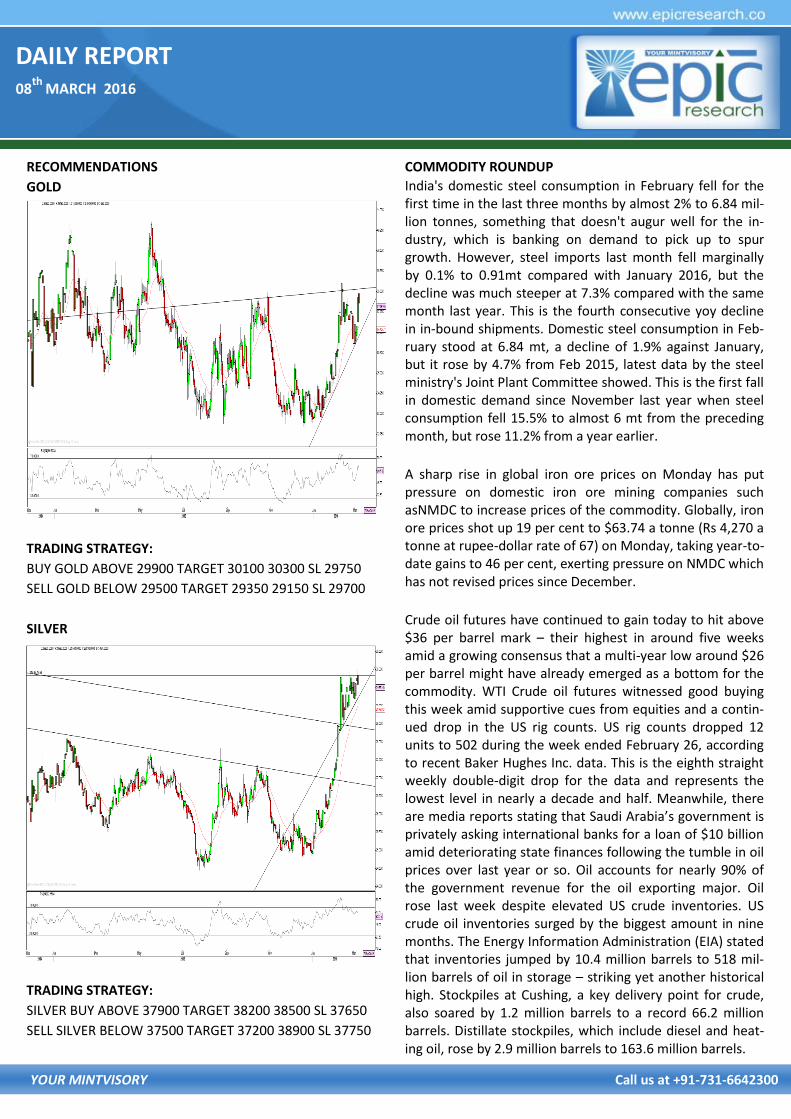

GOLD

TRADING STRATEGY:

BUY GOLD ABOVE 29900 TARGET 30100 30300 SL 29750

SELL GOLD BELOW 29500 TARGET 29350 29150 SL 29700

SILVER

TRADING STRATEGY:

SILVER BUY ABOVE 37900 TARGET 38200 38500 SL 37650

SELL SILVER BELOW 37500 TARGET 37200 38900 SL 37750

COMMODITY ROUNDUP

India's domestic steel consumption in February fell for the first time in the last three months by almost 2% to 6.84 mil-lion tonnes, something that doesn't augur well for the in-dustry, which is banking on demand to pick up to spur growth. However, steel imports last month fell marginally by 0.1% to 0.91mt compared with January 2016, but the decline was much steeper at 7.3% compared with the same month last year. This is the fourth consecutive yoy decline in in-bound shipments. Domestic steel consumption in Feb-ruary stood at 6.84 mt, a decline of 1.9% against January, but it rose by 4.7% from Feb 2015, latest data by the steel ministry's Joint Plant Committee showed. This is the first fall in domestic demand since November last year when steel consumption fell 15.5% to almost 6 mt from the preceding month, but rose 11.2% from a year earlier.

A sharp rise in global iron ore prices on Monday has put pressure on domestic iron ore mining companies such asNMDC to increase prices of the commodity. Globally, iron ore prices shot up 19 per cent to $63.74 a tonne (Rs 4,270 a tonne at rupee-dollar rate of 67) on Monday, taking year-to-date gains to 46 per cent, exerting pressure on NMDC which has not revised prices since December.

Crude oil futures have continued to gain today to hit above $36 per barrel mark – their highest in around five weeks amid a growing consensus that a multi-year low around $26 per barrel might have already emerged as a bottom for the commodity. WTI Crude oil futures witnessed good buying this week amid supportive cues from equities and a contin-ued drop in the US rig counts. US rig counts dropped 12 units to 502 during the week ended February 26, according to recent Baker Hughes Inc. data. This is the eighth straight weekly double-digit drop for the data and represents the lowest level in nearly a decade and half. Meanwhile, there are media reports stating that Saudi Arabia’s government is privately asking international banks for a loan of $10 billion amid deteriorating state finances following the tumble in oil prices over last year or so. Oil accounts for nearly 90% of the government revenue for the oil exporting major. Oil rose last week despite elevated US crude inventories. US crude oil inventories surged by the biggest amount in nine months. The Energy Information Administration (EIA) stated that inventories jumped by 10.4 million barrels to 518 mil-lion barrels of oil in storage – striking yet another historical high. Stockpiles at Cushing, a key delivery point for crude, also soared by 1.2 million barrels to a record 66.2 million barrels. Distillate stockpiles, which include diesel and heat-ing oil, rose by 2.9 million barrels to 163.6 million barrels.

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX INDICES

Index Value % Change

CHANA 4224 -0.75

CORIANDER 6575 -0.78

COTTON SEED 2141 -0.74

GUAR SEED 2983 -0.27

JEERA 14115 +0.89

MUSTARDSEED 3836 -0.52

SOY BEAN 3622 -0.30

SUGAR M GRADE 3222 -0.09

TURMERIC 8872 -0.27

RECOMMENDATIONS

DHANIYA

BUY CORIANDER APR ABOVE 6660 TARGET 6705 6855 SL

BELOW 6595

SELL CORIANDER APR BELOW 6530 TARGET 6485 6335 SL

ABOVE 6595

GUARGUM

BUY GUARGUM MAR ABOVE 5450 TARGET 5500 5570 SL

BELOW 5390

SELL GUARGUM MAR BELOW 5350 TARGET 5300 5230 SL

ABOVE 5410

The Govt agencies have procured 51,000MT of kharif pulses for the buffer stock against the target of 50,000MT. Now they have been asked to start procurement of Masoor, Gram dal and other Rabi pulses also which have the total target of 1 lakh MT. In an inter ministerial meeting chaired by Secretary of Department of Consumer Affairs, C Viswanath, prices and availability of essential commodities were reviewed. The meeting was informed that import of 8,500 MT dal already order is on the way. The representa-tive of Ministry of Agriculture and Farmer Welfare informed that area under production of oilseeds during 2015-16 has increased 2.1% and mustard production is expected to be hire by 6 lakh MT. The meeting also reviewed production of tomato in the country and its price trends. Tomato produc-tion is also expected hire by 11.6% during 2015-16. Efforts are being made to increase its cultivation in non-traditional areas by using advanced hybrid varieties. India's exports of oilmeal, largely used for bird and animal feed, dropped 52 per cent between April 2015 and Febru-ary 2016, due to lower domestic output as crushing mills reduced their operation capacity on disparity. The export of soybean meal is at a historical low of 70,390 tonnes during the first 11 months of 2015-16, compared to 613,676 tonnes in 2014-15 and 2,558,781 tonnes during the same period of 2013-14. Currently, export price of Indian soybean meal is quoted at $480 per tonne against Argen-tina origin soybean meal CIF (cost, insurance and freight) Rotterdam at $321 per tonne. Indian soybean meal is to-tally out-priced by $160 per tonne in the international mar-ket.

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 67.2713 Yen-100 59.1000

Euro 73.6688 GBP 95.2158

CURRENCY

USD/INR

SELL USD/INR MAR BELOW 67.28 TARGET 67.15 67 SL

ABOVE 67.48

BUY USD/INR MAR ABOVE 67.4 TARGET 67.53 67.68 SL BE-

LOW 67.2

EUR/INR

BUY EUR/INR MAR ABOVE 74.1 TARGET 74.25 74.45 SL BE-

LOW 73.9

SELL EUR/INR MAR BELOW 73.87 TARGET 73.72 73.52 SL

ABOVE 74.07

CURRENCY MARKET UPDATES:

The US dollar edged higher against a basket of currencies

on Monday, as Friday's employment rent still lent some

support, although lower expectations for a U.S. rate hike in

the near future continued to weigh. The dollar index,

which measures the greenback's strength against a trade-

weighted basket of six major currencies, was at 97.65. The

U.S. economy added 242,000 new jobs last month and the

unemployment rate held steady at an eight-year low of

4.9%. But average hourly earnings fell by 0.1% during Feb-

ruary, reversing the 0.5% rise seen in January. The weak

wage numbers indicated that consumer inflation is likely to

remain muted. Federal Reserve policymakers are watching

inflation closely as they try to determine when to raise

rates again.

The European unit came under pressure after data earlier

showed that German factory orders fell 0.1% in January,

adding to a 0.2% drop in December. Domestic orders fell

by 1.6% during the month, pointing to weakening demand

within the euro zone's largest economy. The single com-

mon currency dropped 0.43% to 1.0959 versus the green-

back. Investors were looking ahead to Thursday's European

Central Bank meeting after the bank disappointed expecta-

tions with a smaller-than-expected stimulus move at its

December meeting.

USD/JPY slid 0.30% to trade at 113.43. Bank of Japan Gov-

ernor underlined the positive aspects of the negative inter-

est rate policy adopted by the BoJ in January and which

took effect on February 16. As against the pound, dollar

was higher with GBP/USD down 0.58% at 1.4145.

The rupee rose to as much as 67.86 per dollar, its highest

since Feb. 10, from its closing level of 68.4250/68.4350 on

Monday. The RBI was forced to step in to prevent the ru-

pee from gaining too much, traders said, in a reversal of

just a week ago when the central bank was selling dollars

to prevent the currency from hitting a record low of 68.85

to the dollar.

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

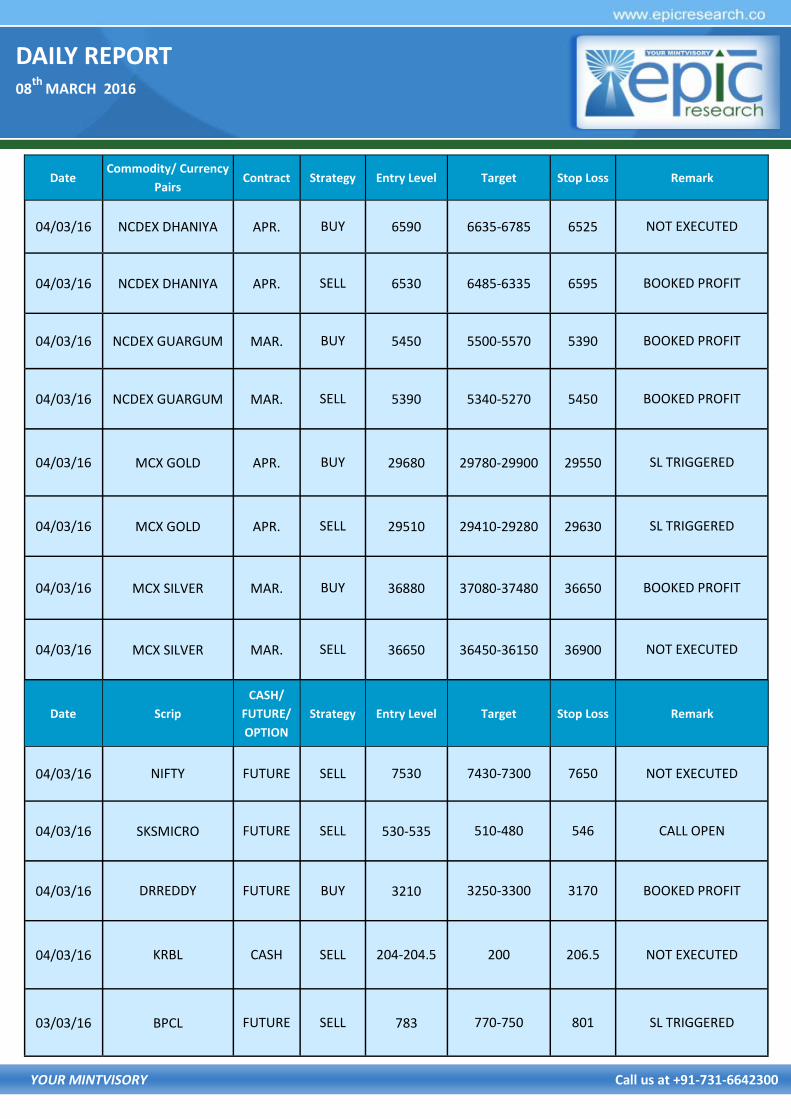

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

04/03/16 NCDEX DHANIYA APR. BUY 6590 6635-6785 6525 NOT EXECUTED

04/03/16 NCDEX DHANIYA APR. SELL 6530 6485-6335 6595 BOOKED PROFIT

04/03/16 NCDEX GUARGUM MAR. BUY 5450 5500-5570 5390 BOOKED PROFIT

04/03/16 NCDEX GUARGUM MAR. SELL 5390 5340-5270 5450 BOOKED PROFIT

04/03/16 MCX GOLD APR. BUY 29680 29780-29900 29550 SL TRIGGERED

04/03/16 MCX GOLD APR. SELL 29510 29410-29280 29630 SL TRIGGERED

04/03/16 MCX SILVER MAR. BUY 36880 37080-37480 36650 BOOKED PROFIT

04/03/16 MCX SILVER MAR. SELL 36650 36450-36150 36900 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

04/03/16 NIFTY FUTURE SELL 7530 7430-7300 7650 NOT EXECUTED

04/03/16 SKSMICRO FUTURE SELL 530-535 510-480 546 CALL OPEN

04/03/16 DRREDDY FUTURE BUY 3210 3250-3300 3170 BOOKED PROFIT

04/03/16 KRBL CASH SELL 204-204.5 200 206.5 NOT EXECUTED

03/03/16 BPCL FUTURE SELL 783 770-750 801 SL TRIGGERED

DAILY REPORT 08

th MARCH 2016

YOUR MINTVISORY Call us at +91-731-6642300

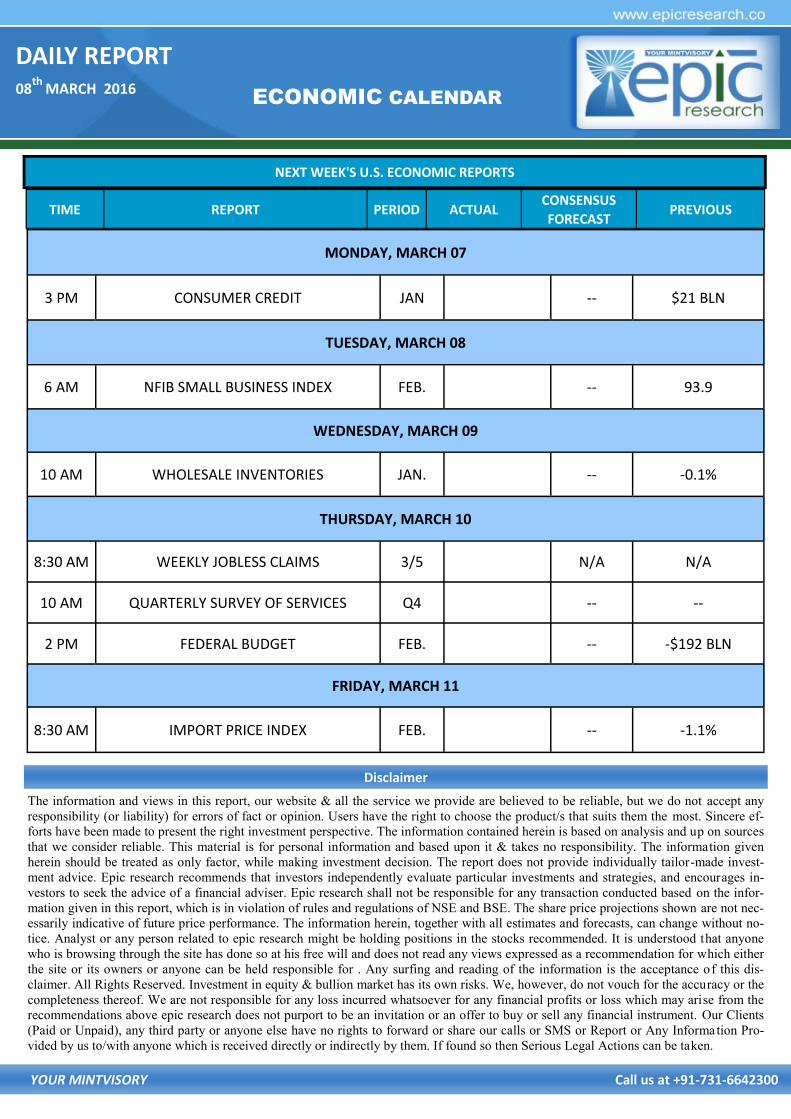

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, MARCH 07

3 PM CONSUMER CREDIT JAN -- $21 BLN

TUESDAY, MARCH 08

6 AM NFIB SMALL BUSINESS INDEX FEB. -- 93.9

WEDNESDAY, MARCH 09

10 AM WHOLESALE INVENTORIES JAN. -- -0.1%

THURSDAY, MARCH 10

8:30 AM WEEKLY JOBLESS CLAIMS 3/5 N/A N/A

10 AM QUARTERLY SURVEY OF SERVICES Q4 -- --

2 PM FEDERAL BUDGET FEB. -- -$192 BLN

FRIDAY, MARCH 11

8:30 AM IMPORT PRICE INDEX FEB. -- -1.1%