Embed Size (px)

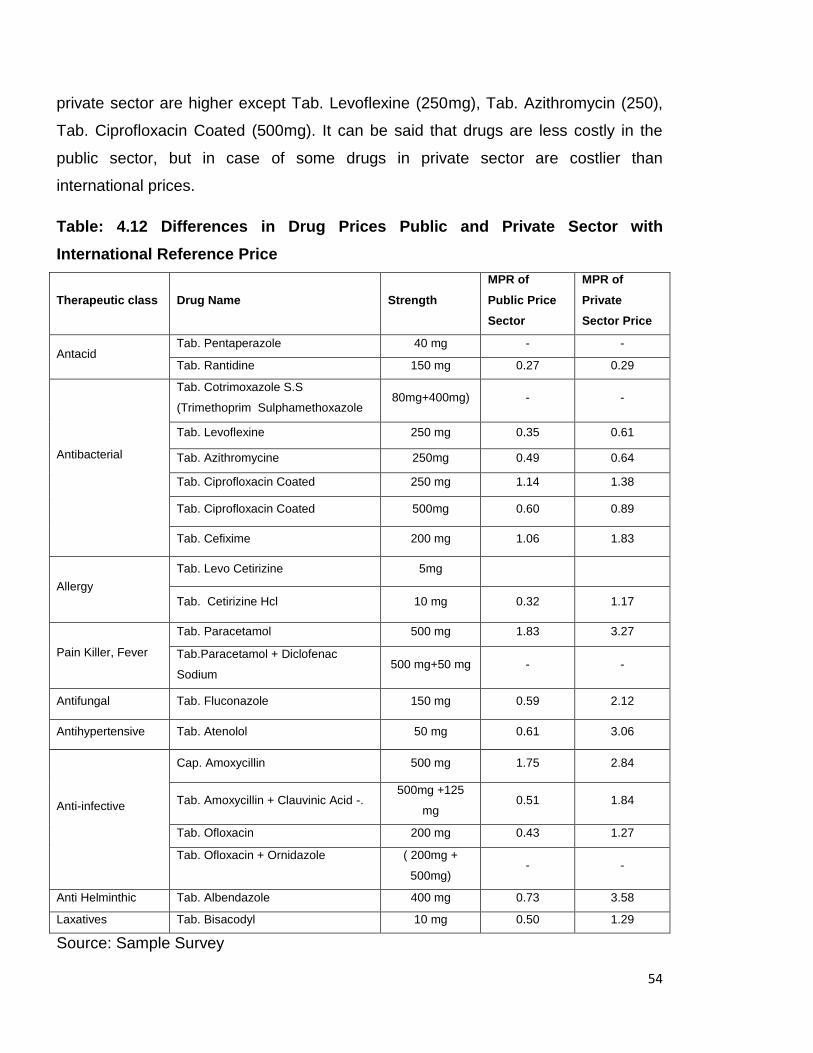

Citation preview

Availability, Affordability and Pricing of the Essential

Drugs: A Case Study of Bathinda City (Punjab)

Dissertation submitted to the Central University of Punjab

For the award of

Master of Philosophy

In

Economic Studies

By

Indu Bala

Supervisor

Dr. Sandeep Kaur Bhatia

Centre for Economic Studies

School of Social Science

Central University of Punjab, Bathinda

August, 2016

i

ABSTRACT

Availability, Affordability and Pricing of the Essential Drugs: A Case Study of

Bathinda city (Punjab)

Name of Student : Indu Bala

Registration Number : CUPB/MPH/SSS/CES/2014-2015/04

Degree for which submitted : Master of Philosophy

Name of Supervisor : Dr. Sandeep Kaur Bhatia

Centre : Centre for Economic Studies

School of Studies : School of Social Sciences

Key words : Drugs, Availability, Affordability, Prices

Differences, International Comparison of

Drugs Prices, Drug Price Control, Patent.

In recent times individual spending on health care is the common issue. This issue is

manifold as linked with the availability, affordability and pricing of drugs. The present

study evaluates these issues related to essential drugs in Bathinda city which is one

of the blocks of Malwa region. Availability, affordability and price differences are

examined across two types of drugs generic and, branded-generic at public and

private drug stores, using a primary survey of patients, drug retailers and wholesalers

mainly. The study also analyses the evolution of government drug pricing policies and

the impact of patents on drugs. Data on drug prices is collected of commonly used

essential drugs of different therapeutic classes. Affordability of the essential

medicines to the ordinary people is measured by comparing the treatment cost with

the wages earned by them. To compare the domestic prices with international

reference prices, median price ratios (MPR) are obtained by dividing the local public

and private sector median prices with international reference prices. The study

discovers that availability of essential drugs in the public sector is not sufficient to

meet the challenge of providing essential drugs to the entire population of the city.

The Private sector is dominating for providing drugs and better treatment which has

very less transparency in the pricing system and variations in the retail prices and

markups are very high. Affordability level of essential drugs for different treatments to

ii

the ordinary people is satisfactory but not for the people living below the poverty line.

Policies should be targeted to maintain a transparent pricing system and should be

affordable for all as well as making them more widely available. The drug price control

order should be properly implemented in fixing the MRP of branded-generic drugs.

(Indu Bala) (Dr. Sandeep Kaur Bhatia)

iii

ACKNOWLEDGEMENTS

First of all, I offer my humble thanks with folded hands and bowed head to the

almighty for his grace, kindness and blessing that gave me patience and motivation

during the course of my work.

I have the great honor to express my deep sense of gratitude and indebtedness to

my supervisor, Dr. Sandeep Kaur Bhatia, Assistant Professor, Center for Economic

studies, Central University of Punjab for her constant guidance, constant

encouragement, healthy criticism and generosity shown throughout the period of my

study and preparation of this manuscript.

I would like to give my special thanks to COC Dr. P.K Mishra, Dr. Naresh Singla, Dr.

J. K Parida, Centre for Economic Studies for their valuable suggestions pleasant

atmosphere of knowledge. I would also like to thanks Dr. R.K. Kohli, present Vice-

Chancellor of the university, Prof. Dr. P. Ramarao, Dean of academic affairs and Prof

A. K. Jain. Without their constant help, support and encouragement, this dissertation

would not have been possible.

I got immense pleasure to express my thanks to all my friends Jashanpreet Kaur

Jagdeep Kaur, Poonam Rani, Arif Gulzar Hajam, Zahoor Ahmad Paray, Harmeet

Kaur, Harpreet Kaur, Gagandeep Kaur, Sareena Goel for always supporting and

believing in me with enormous affection and valuable suggestions.

Finally, my family has supported and helped me along the course of this dissertation

by giving encouragement and providing the moral and emotional support I needed to

complete my dissertation. To them, I am eternally grateful.

Indu Bala

iv

Table of Contents

Sr. No. Contents Page No.

1 Chapter 1: Introduction 1-8

2 Chapter 2: Literature Review 9-18

3 Chapter 3: Data and Methodology 19-24

4 Chapter4: Availability, Affordability and Prices

Differences of Essential Drugs

25-55

5 Chapter 5: Evaluation of Indian Drug Pricing Policies

and TRIPS

56-67

6 Chapter 6: Conclusion 68-76

7 Bibliography 77-83

v

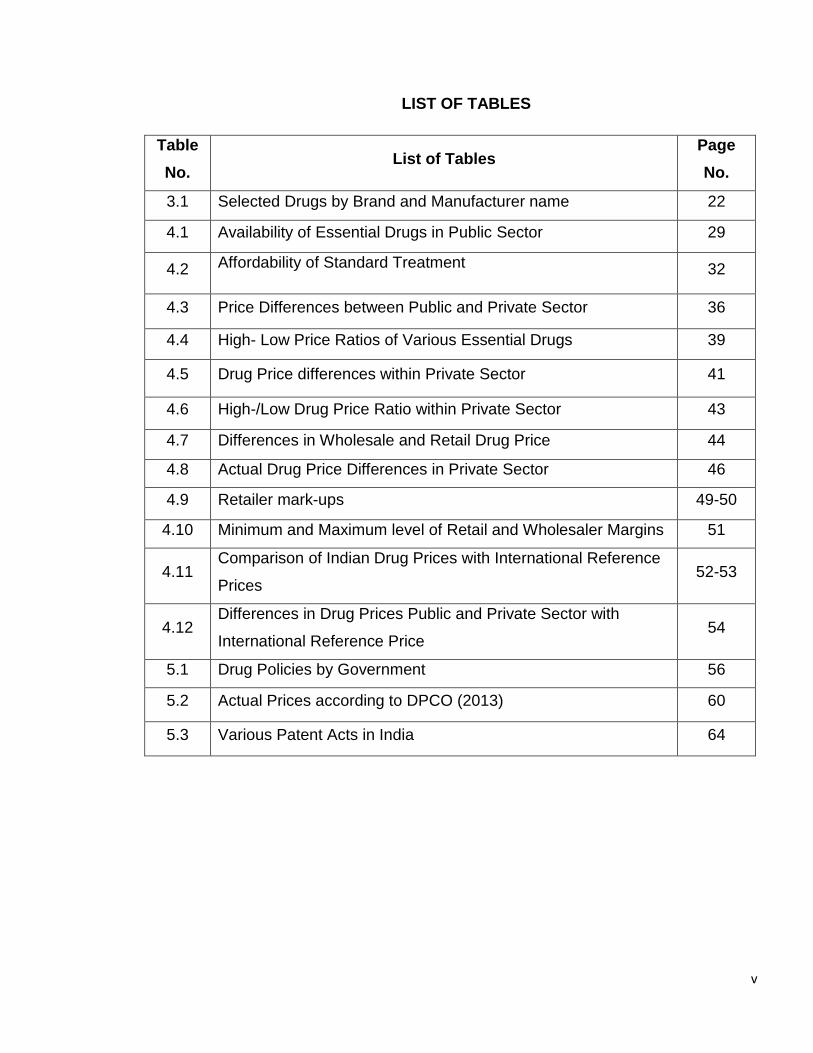

LIST OF TABLES

Table

No. List of Tables

Page

No.

3.1 Selected Drugs by Brand and Manufacturer name 22

4.1 Availability of Essential Drugs in Public Sector 29

4.2 Affordability of Standard Treatment 32

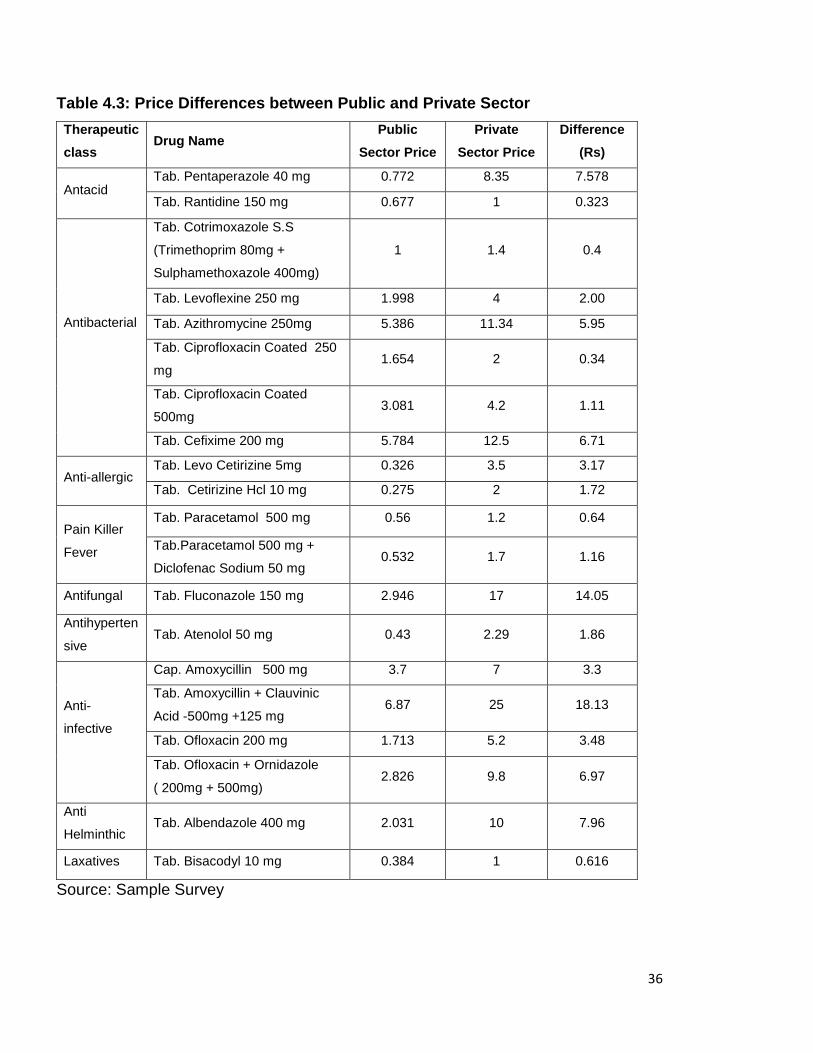

4.3 Price Differences between Public and Private Sector 36

4.4 High- Low Price Ratios of Various Essential Drugs 39

4.5 Drug Price differences within Private Sector 41

4.6 High-/Low Drug Price Ratio within Private Sector 43

4.7 Differences in Wholesale and Retail Drug Price 44

4.8 Actual Drug Price Differences in Private Sector 46

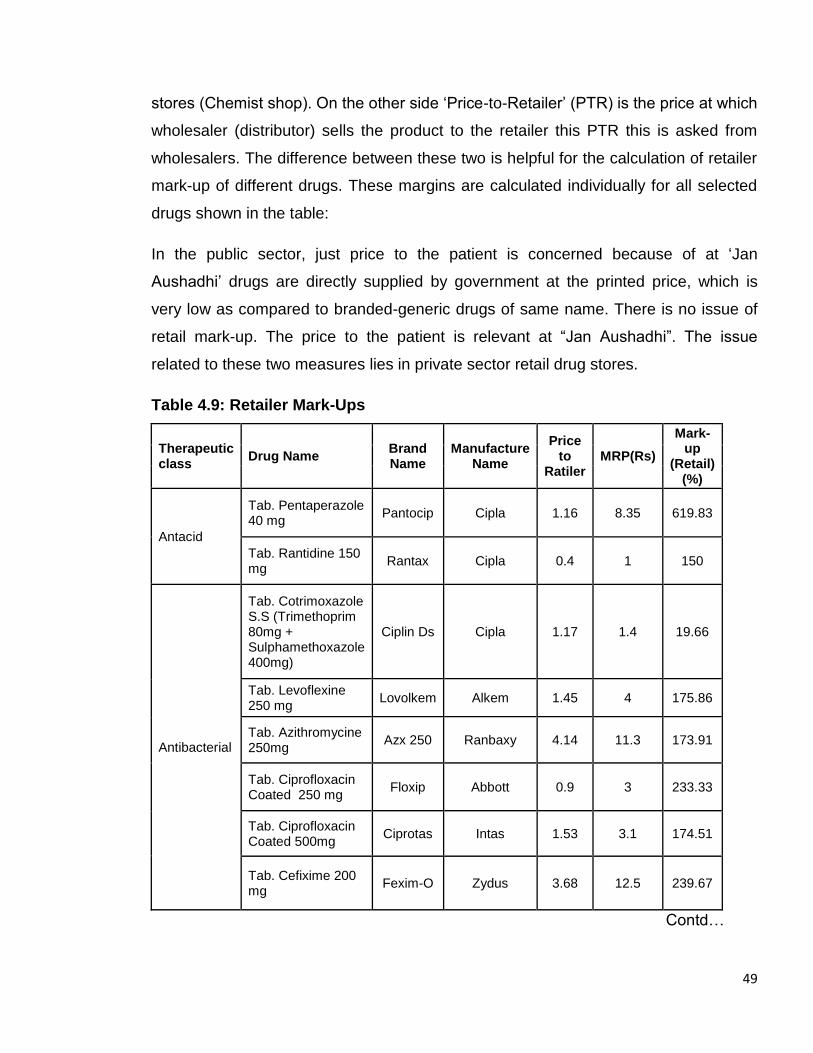

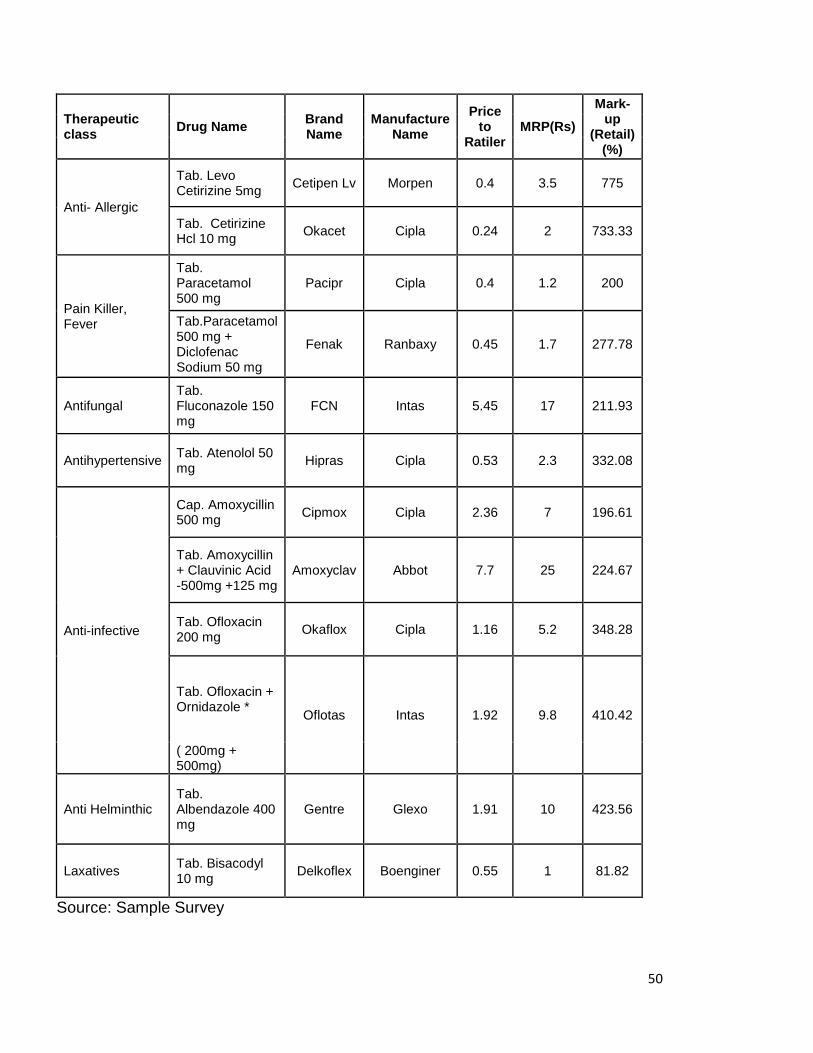

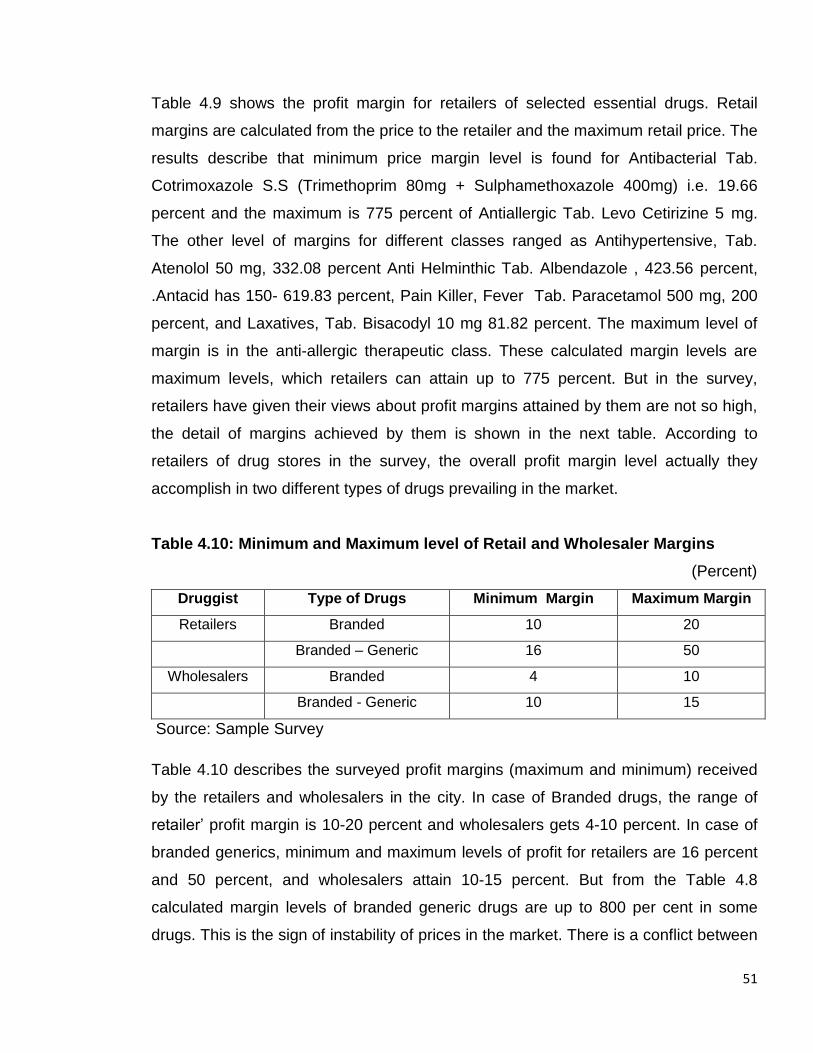

4.9 Retailer mark-ups 49-50

4.10 Minimum and Maximum level of Retail and Wholesaler Margins 51

4.11 Comparison of Indian Drug Prices with International Reference

Prices 52-53

4.12 Differences in Drug Prices Public and Private Sector with

International Reference Price 54

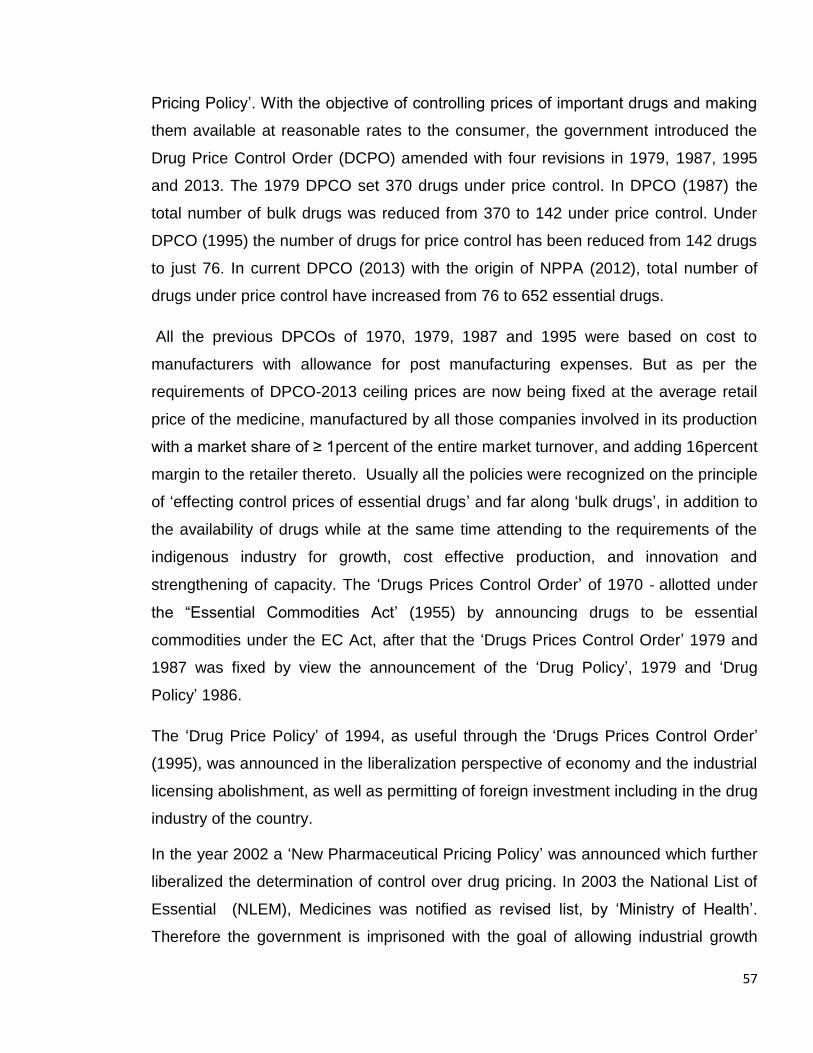

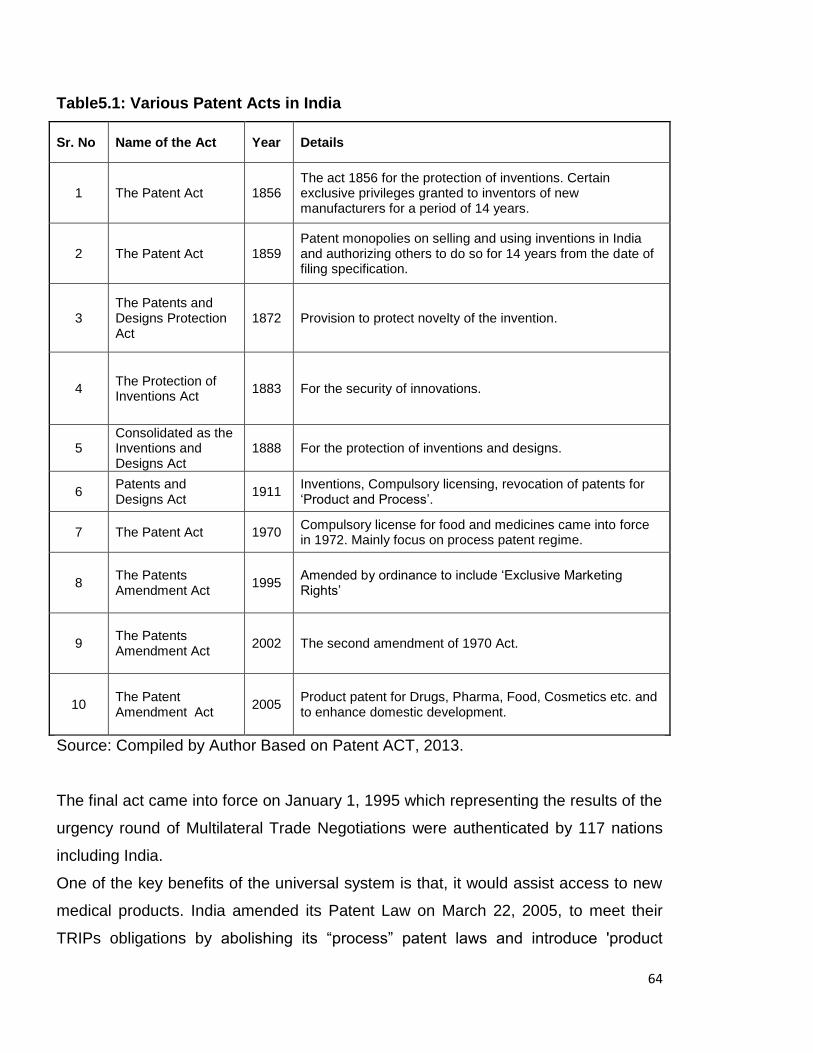

5.1 Drug Policies by Government 56

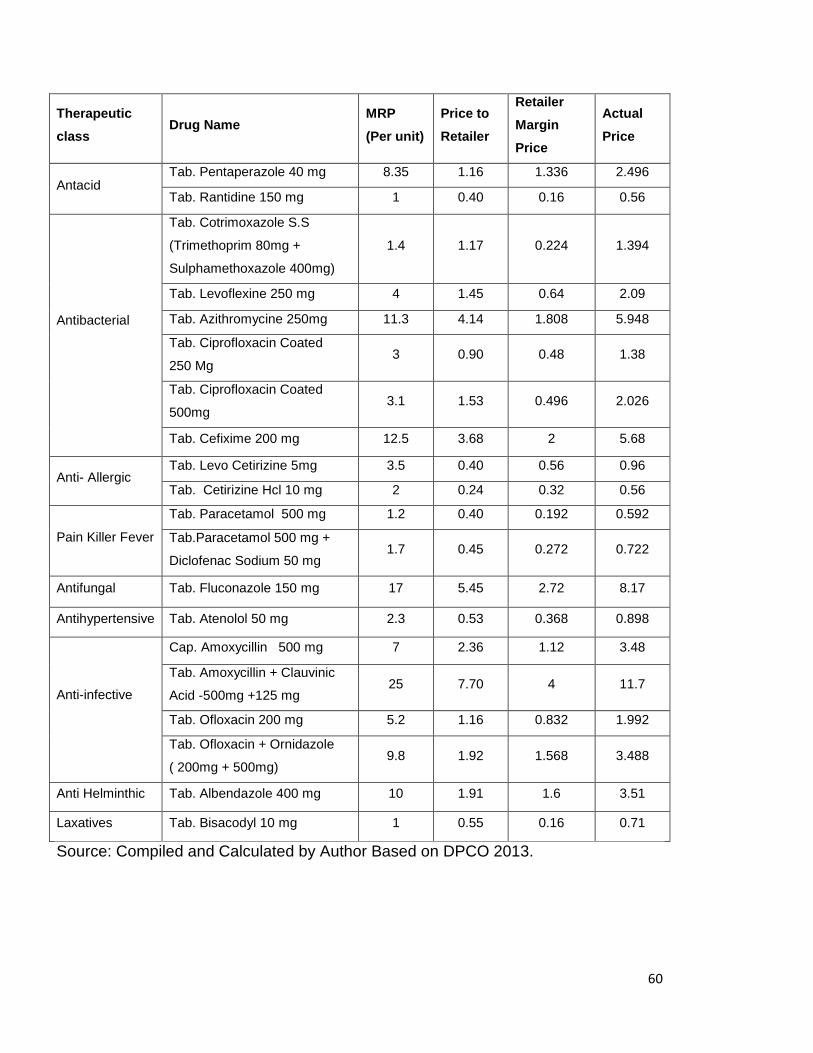

5.2 Actual Prices according to DPCO (2013) 60

5.3 Various Patent Acts in India 64

vi

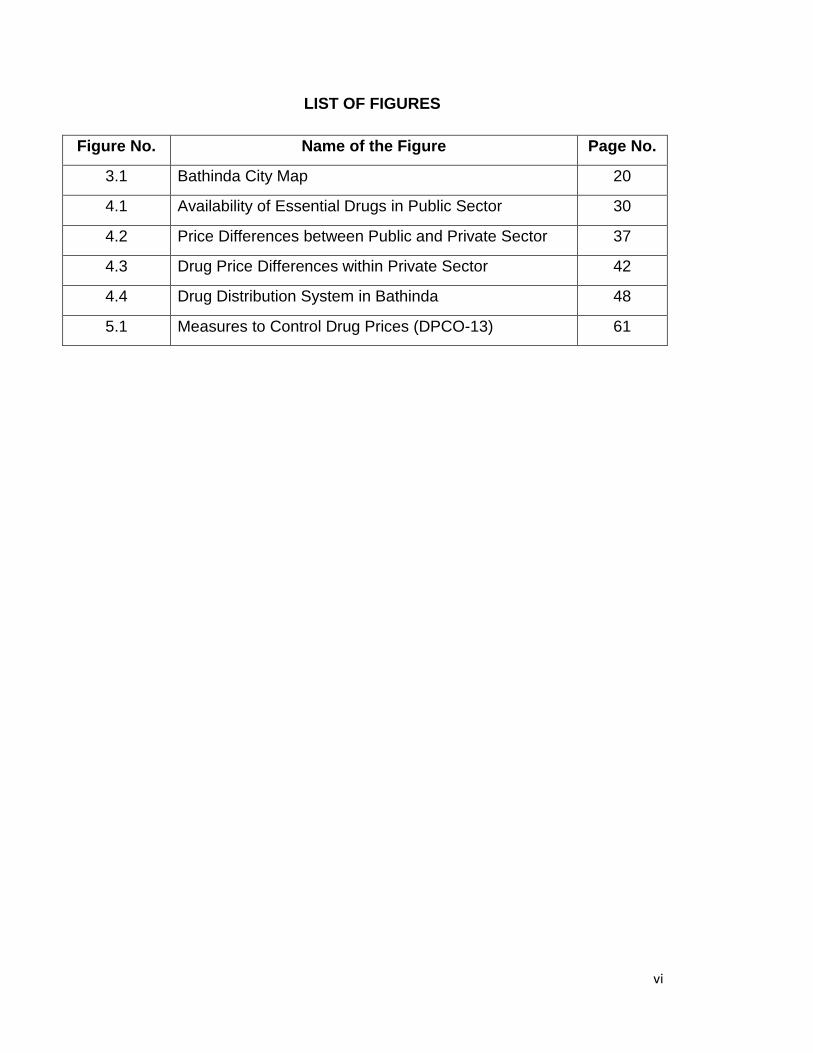

LIST OF FIGURES

Figure No. Name of the Figure Page No.

3.1 Bathinda City Map 20

4.1 Availability of Essential Drugs in Public Sector 30

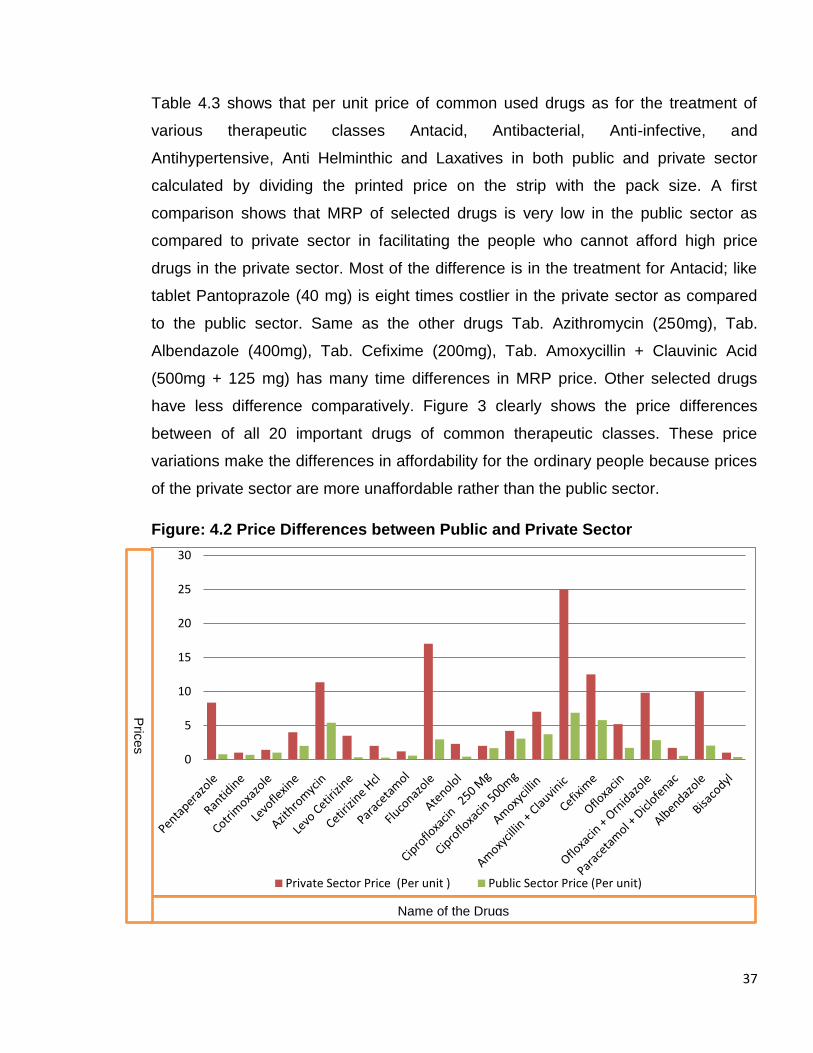

4.2 Price Differences between Public and Private Sector 37

4.3 Drug Price Differences within Private Sector 42

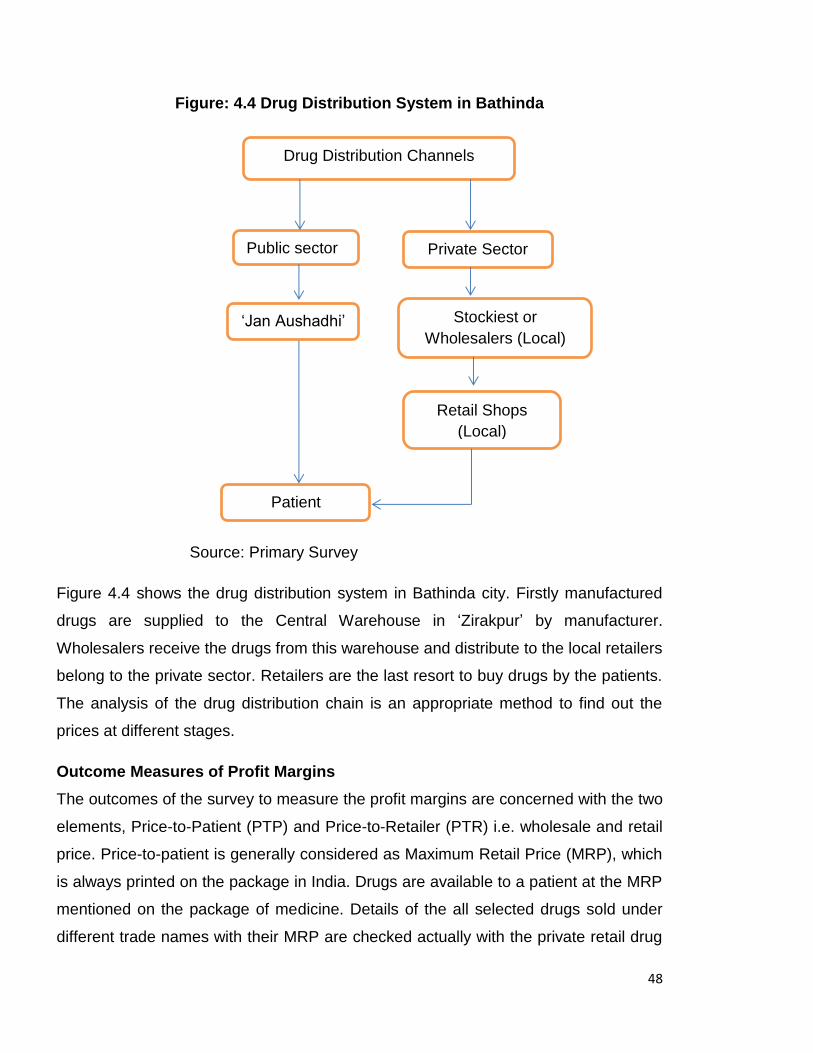

4.4 Drug Distribution System in Bathinda 48

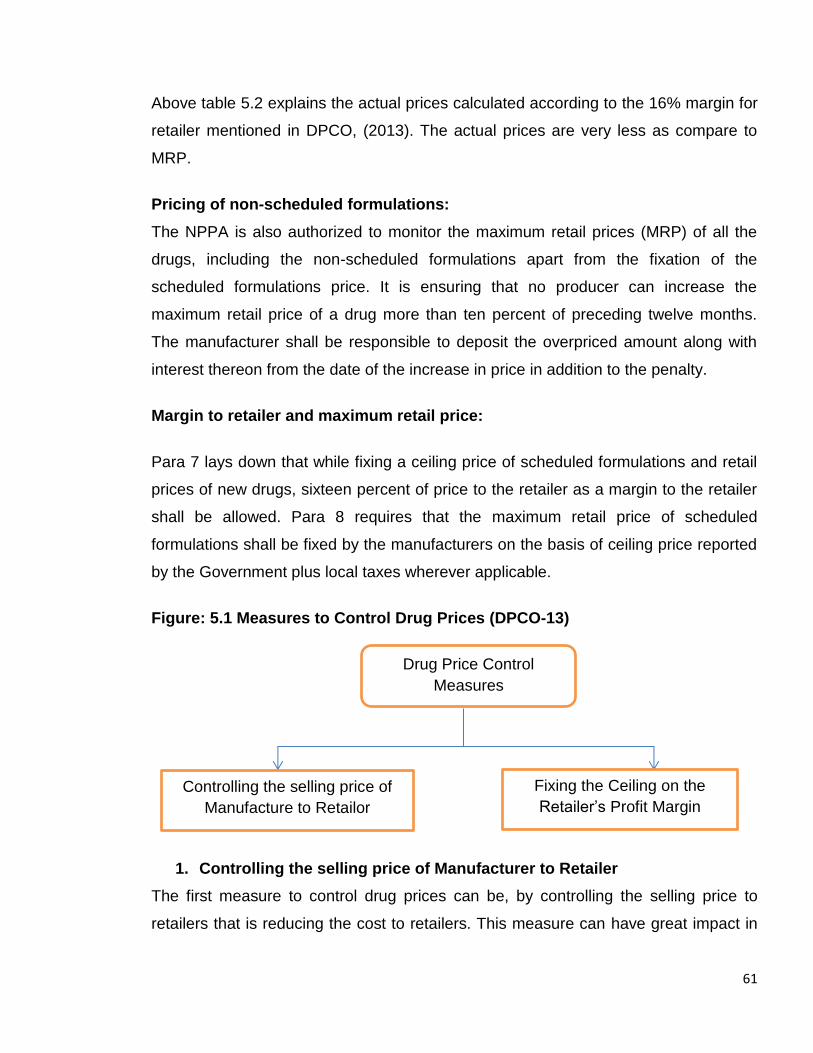

5.1 Measures to Control Drug Prices (DPCO-13) 61

vii

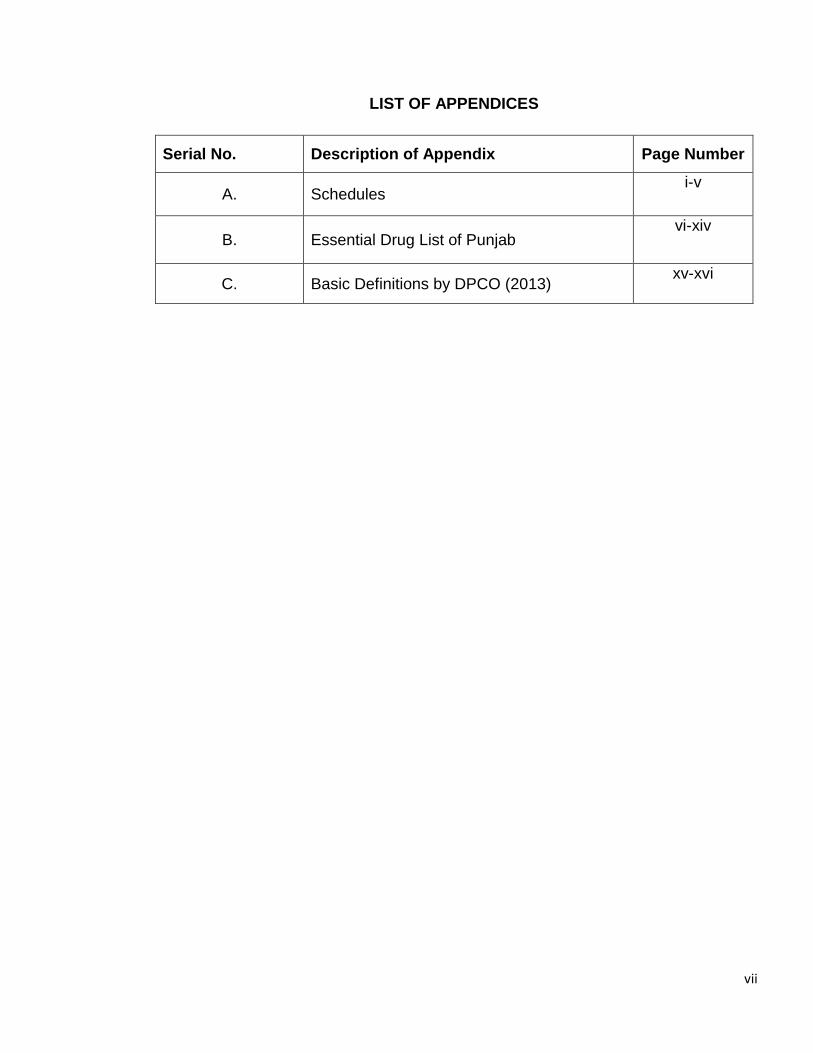

LIST OF APPENDICES

Serial No. Description of Appendix Page Number

A. Schedules i-v

B. Essential Drug List of Punjab vi-xiv

C. Basic Definitions by DPCO (2013) xv-xvi

viii

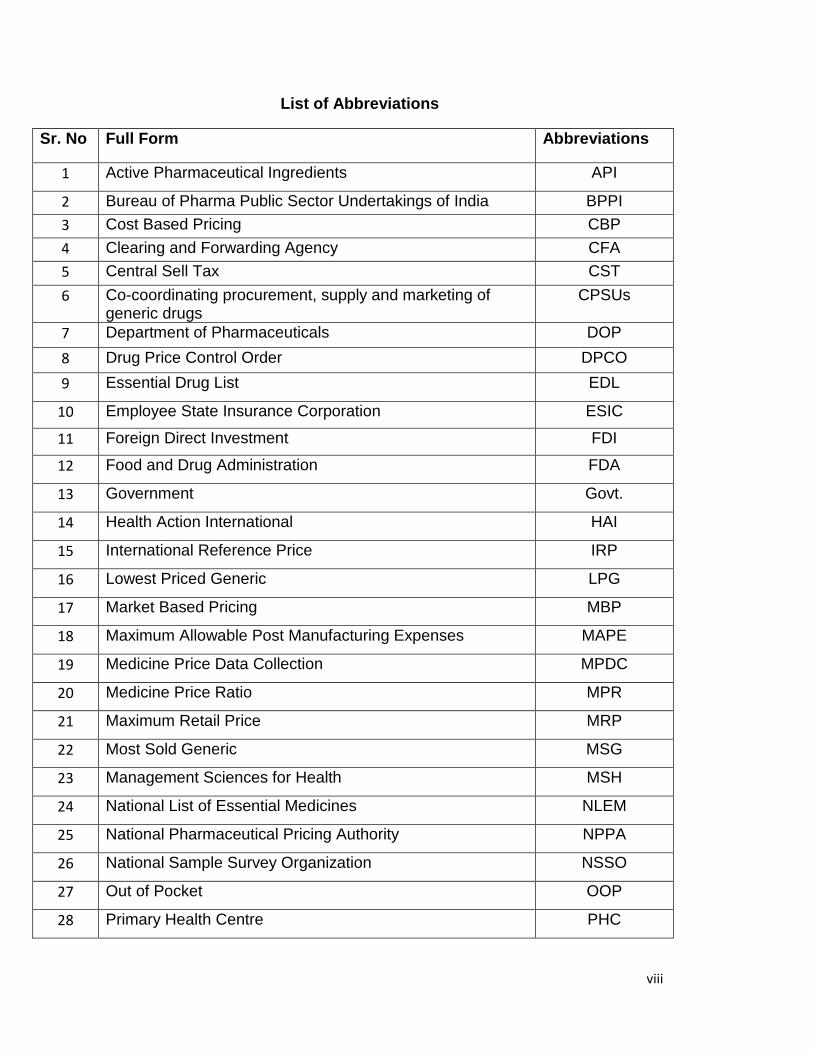

List of Abbreviations

Sr. No Full Form Abbreviations

1 Active Pharmaceutical Ingredients API

2 Bureau of Pharma Public Sector Undertakings of India BPPI

3 Cost Based Pricing CBP

4 Clearing and Forwarding Agency CFA

5 Central Sell Tax CST

6 Co-coordinating procurement, supply and marketing of generic drugs

CPSUs

7 Department of Pharmaceuticals DOP

8 Drug Price Control Order DPCO

9 Essential Drug List EDL

10 Employee State Insurance Corporation ESIC

11 Foreign Direct Investment FDI

12 Food and Drug Administration FDA

13 Government Govt.

14 Health Action International HAI

15 International Reference Price IRP

16 Lowest Priced Generic LPG

17 Market Based Pricing MBP

18 Maximum Allowable Post Manufacturing Expenses MAPE

19 Medicine Price Data Collection MPDC

20 Medicine Price Ratio MPR

21 Maximum Retail Price MRP

22 Most Sold Generic MSG

23 Management Sciences for Health MSH

24 National List of Essential Medicines NLEM

25 National Pharmaceutical Pricing Authority NPPA

26 National Sample Survey Organization NSSO

27 Out of Pocket OOP

28 Primary Health Centre PHC

ix

29 Price to Retailor PTR

30 Price to Patient PPP

31 Research And Development R&D

32 Trade Related Intellectual Property Rights TRIPS

33 Value Added Tax VAT

34 World Health Organization WHO

35 World Trade Organization WTO

1

CHAPTER - 1

INTRODUCTION

The large population in developing countries has been suffering from the health care

burden due to malnutrition, non-availability of facilities and lesser budget proposals

for health care in these countries. Indian Health Care Outlook (2015) reveals that in

developing countries, households usually have to purchase drugs and other health

facilities ‘Out of Pocket’ (OOP). The Indian health care system is also highly

dependent on personal spending as India is one of the world’s highest out-of-pocket

spending nations because of low government’s expenditures for health creating a

burden on patients and their families. World Health Organization (WHO) data reveals

that in 2012 only 33 percent of Indian health care expenditure originated from

government sources while remaining 86 percent was from private (Deloitte United

States, 2016).

Surveys conducted in six states during 2004–2005 sites involved Chennai (southern

India), Haryana (northern India), Karnataka (southern India), West Bengal (eastern

India), and two surveys sites in Maharashtra State (western India) through “World

Health Organization/ Health Action International” (WHO/HAI) a standardized

methodology exposes poor availability of drugs in public sector hospitals as only up

to 30 per cent . Therefore, low-income patients are enforced to buy more expensive

drugs from private sources or simply go without treatment. The main barrier to access

essential drugs makes health care unaffordable one is the low public sector

expenditure and other high medicine prices. In order to ensure availability at

reasonable prices, the Government of India (Ministry of Chemicals and Fertilizers)

has established an independent body of experts the National Pharmaceutical Pricing

Authority (NPPA) in 1997 which have the primary function of price determination,

revision, and related activities, such as updating the list of medicines under price

control by the inclusion and exclusion of drugs on the basis of established criteria and

guidelines. However, the NPPA monitors the prices of medicines sold in all sectors,

but still there are issues regarding the prices of drug (Kotwani et al., 2007).

2

Economic Health Care Scenario of Punjab State

According to a study by Chaudhuri (2012) examines that hospitalization and

outpatient services at public health facilities are quite low in Haryana (30 percent) and

in Punjab 20 percent. The specified reasons are the high cost of care including high

prices of drugs. In the Punjab, State the Health Systems Corporation includes public

hospitals and public clinics over which the poor people can access health facilities.

Two schemes were announced in 2008, to decrease out-of-pocket expenses for poor

families i.e. ‘Jan Aushadhi’ to provide inexpensive generic drugs through public health

care centers and ‘Rashtriya Swasthya Bima Yojna’ under which a family of five below

the poverty line would receive the cashless treatment maximum 30,000 annually.

PGRC Eighth Report (2013) viewed that health indicators in Punjab are slightly better

than many other states. It ranks third in the country in terms of birth rate (16.2 per

1000 population). The infant mortality rate of 30 per 1000 live births places it at fifth

rank. It has a maternal mortality ratio of 172 per 100,000 live births. Around 61

percent of deliveries are conducted in health institutions; the share of government and

private institutions stands at 22 percent and 39 percent respectively. A major concern

is the rising cost of medical care. The average expenditure for hospitalization in

Punjab is Rs. 15,431 which is one among the highest across the country. Even in

government health institutions, average out-of-pocket expenditure is Rs. 270/- per

OPD consultation and Rs. 7,700/- per hospitalization. User charges, inadequate

supply of medicines and other surgical supplies and lab reagents has led to an

escalation in the cost of medical care in government health institutions. The state

does not allocate adequate budget for medicines and supplies. At least 20 percent of

the health budget should be allocated for medical and surgical supplies. Clearly,

decreasing outlay on social sectors is responsible for a cut on soft items in the budget

such as medicines. A survey conducted by National Sample Survey Organization

(NSSO) in the first half of 2014, concluded that Punjab ranks top in terms of out-of-

pocket health expenditure because the people of Punjab spend a major portion of the

money income on medical treatment in the country. The out-of-pocket health

expenditure is any direct expenditure by households on drugs and health services

practitioners. It is a part of private health expenditure. According to head of School of

3

Public Health (PGIMER), people of Punjab bear the highest medical expenditure (in

terms of hospitalization), and in the area-wise break-up, the out-of-pocket health

expenditure in urban areas is Rs 29, 971 as compared to Rs 27,718 in rural areas of

the state. On an average in the Punjab state the expenditure of hospitalized per

person, Rs 28,539. In Haryana, Rs 24,000 against the national average of Rs 18,628.

Among union territories, Delhi and Chandigarh spend the highest with 34,604 and

34,658, respectively.

National Health Profile (2015) briefs Punjab’s per capita spending on health is Rs 728

and monthly per capita household out-of-pocket expenditure in the state is Rs 196.5.

In Haryana, it is Rs 131, Rs 95 in Jammu and Kashmir, Rs 134.5 in Himachal

Pradesh, Rs 103 in Chandigarh and Rs 132 in the national capital. The reason found

by experts of health expenditure burdens on common people that the lack of public

(government) expenditure. Punjab’s per capita spending on health is just Rs 728.The

state government is expensed on health are just 0.72 per cent of the gross state

domestic product. This profile of Punjab state shows the higher burden of health care

as compared to other states. (Bharti, 2016).

Role of Generic Drugs

India Pharmaceuticals position is well-known as ‘branded’ and ‘branded-generic and

most of the products are sold by a brand (trade) name. Till January 2005 all

medicines were the generic product when patents were not relevant in India. Branded

medicines were manufactured by multinational and good reputated manufacturers of

Indian. Branded medicines are promoted by manufacturers at higher prices while

almost all drugs easily available with trade-names. The public sector acquires drugs

as unbranded generics with the chemical or ‘International Nonproprietary Name’ on

the labeled product. The Indian pharmaceutical sector is communal under the

‘Ministries of Health and Family Welfare’ (Department of Chemicals and

Petrochemicals under the Ministry of Chemicals and Fertilizers) and the ‘Office of

Drugs Controller’. The government’s main thrust of pharmaceutical policies has been

on the manufacturing of the private sector and marketing of drugs and for the

common man there are not more improvements in accessibility of essential

medicines. The Indian health sector has been affected by structural adjustment,

4

economic liberalization reforms by the World Bank and increasing production cost in

pharmaceuticals (Roy et al., 2012).

Due to the high economic pressure on drug budgets the use of generic drugs is

progressively growing internationally because since they are usually substantially

lower in price than the innovative brands and these drugs provide the opportunity for

major savings in health care expenditure. However, physicians are apprehensive

regarding the quality of generic drugs and have concerns about their reliability as well

as interchange of certain drug categories. Although the generic medicines are bio-

equivalents of their innovator counterparts and are produced in similar facilities,

according to good manufacturing practices, these are widely believed as inferior in

their therapeutic efficacy and quality to branded products. Marketing practices

adopted by manufacturers of imported branded medicines also propagate the belief

that generics are inferior quality as reported from countries in Central and Eastern

Europe and independent countries emerged from the former Soviet Union. In India,

generic substitution is legally not allowed because of limited awareness about

generics to patents, and patients do not want pharmacist to change the trade name

written by doctor. Hence, consumer awareness for the generics, variety of trade

names available in the market and price variation is very limited. (Singal et al., 2011).

In developing countries, policymakers are confronted to increase the availability and

affordability of essential medicines. The government of India recently opened

‘Generic Drug Stores’ to make access to drugs, at some public channels of drug

distribution who sell generic drugs produced by the public sector. Their prices are

lower than market price. India also faces the task of equal access to affordable and

quality essential drugs for its own people despite pharmaceutical industry growth in

the last two decades, access to essential drugs remnants an issue of common

people. As for the poor population affordability remains to be the main barrier to

access to medicines. In April 2008, the ‘Department of Pharmaceuticals’ (DOP) under

the ‘Chairmanship of Minister of Chemicals and Fertilizer’ responsible for drug policy

and pricing launched a campaign to open generic drug stores called ‘Jan Aushadhi

stores’. Quality generic drugs are to be available at lower prices in these stores.

Opening generic drug stores and making essential medicines available at affordable

5

prices seems to be a step in the right direction. So far implementation of the policy

raises several concerns related to low availability (Kotwani, 2010).

Various drug policies are approved from time to time to manage the task of sustaining

balance between pharmaceutical, industrial growth and ensuring affordable and

reasonably priced medicines to the consumers at the same time, particularly the poor

common people. In India firstly control over the price of drugs was the outcome of the

Chinese aggression with the promulgation of the ‘Drugs Display of Prices Order’

(1962) and the Drugs Control of Prices Order, 1963. These were circulated under the

Act ‘Defenses of India’. With these orders, the prices of drugs were fixed from 1st

April, 1963. Consequently, arrangement of price control systems was notified through

various orders with different principles, in which the span of regulator of prices as well

as the nature of control of prices varied from order to order as per the respective drug

policies.

The latest Drug Price Control Order (DPCO-2013) was issued on 15.05.2013. All the

previous DPCOs, 1970, 1979, 1987 and 1995 were based on cost to manufacturers

with allowance for post manufacturing expenses. As per the provisions of DPCO

(2013) ceiling prices are now being fixed at the average retail price of the medicine,

produced by all those companies engaged in its production with a market share of ≥

1percent of the total market turnover, and adding 16percent margin to the

retailer. While most of the ‘Drug Pricing Policies’ in the past have been implemented

in light of various objectives, the 2012 National Pharmaceutical Policy is aimed mainly

at making drugs affordable. The main objective of the policy is to put in place a

regulatory basis to ensure the availability of essential drugs listed in the NLEM at

affordable prices (Arthapedia, 2016).

Availability and affordability of drugs is greatly affected by Intellectual Property Rights

(IPR) i.e. of India Patents Act (1970) and Amendments (2005). It has generated a

solid impression on the modern day life. These IPRs were encouraged in an ever

seen manner by the TRIPs agreement. The TRIPs agreement has directed its

member states to implement the requirements of the agreement in order to

encourage and protect IPRs. Members’ states are asked to provide protection to

different IPRs by making necessary amendments in their existing laws or enacting

6

new laws. India, being a member state of the TRIPs agreement brought changes in

its IPRs laws. The preceding fifteen years have seen many new IPR performances.

With globalization, liberalization and privatization, the field of IPR has grown multifold

and its importance has amplified, having a profound impact on commercial welfares

(Malik, 2013).

Although government increasing expending on public health facilities and managing

the drug prices polices to make drugs affordable, but the conditions of the health care

burden are not improving. A large part of the population depends upon the private

sector for heath treatment because of facilities available to patients, but the treatment

costs are mostly uncompromising for the ordinary people. As Indian’s generic drugs

are famous and demanded all over the world because of cheap prices. India can

achieve the highest level to provide availability of drugs for any health problem and

make them affordable to all.

Significance of the study

It is a matter of high concern that high prices of drugs directly make drugs beyond the

reach of million people in developing countries. Large numbers of the population in

India also do not have regular access to essential medicines. According to the

‘National Pharmaceutical Pricing Policy’ (NPPP) 2012 Indian Pharmaceutical industry

is producing drugs at 3rd position of by volume and 14th in terms of value at global

level. As India is very efficient in the pharmaceutical sector to produce drugs at very

cheap cost relative to world level and provide low price in the world, despite the fact

domestic consumers suffer from the high retail price of very cheap drugs. Commonly,

individuals have to bear the full cost of their drugs and health treatment, since drugs

are not fully subsidized through Indian government. To overcome this economic

burden of drugs the use of generic drugs is a good substitute but, consumer’s

awareness for the generics, variety of trade names available in the market, and price

variation is very limited. Hence, there is need to conduct a study that can analyze the

uses and price structure of pharma products manufactured in India. The study has

purposively selected Bathinda city situated in the Malwa region of Punjab, where the

health problem has major concern. High prices and price differences in the private

7

sector and low availability in the public sector are major barriers to the use of drugs

and better health. High prices of drugs is one of the issue, while as issues related to

the price differences within the same sector is another one. By keeping in view, the

present study is an attempt to discuss various issues related to h availability and

affordability of essential drugs Therefore the study has tried to examine the gap in

cost, wholesale, retail price and profit margin at different levels of distribution of drugs

from a manufacture unit to consumers of commonly demanded drugs in Bathinda city.

An attempt is also made to study the evaluation of drug policy and the impact of

TRIPS on drug prices. Therefore, keeping in view the above literature gap, the

present study attempts to carry out the following objectives to contribute the literature

and provide further knowledge about the subject.

Objectives of the Study

To evaluate the availability and affordability of essential drugs in a Bathinda

city.

To calculate the differences in drug prices at various stages of distribution in

different sectors i.e. public and private.

To evaluate the various Indian Drug Pricing Policies and TRIPS.

To give some policy suggestions for a sustainable and affordable health care

system.

Plan of the Present Study

The present study is scheduled into six chapters as:

The first chapter deals with the introduction about the problems related to the

essential drugs, health status of India and Punjab. Discussion about role of generic

drugs in the health care is also given. Objectives and significance of the present study

are explained.

The second chapter deals with a review of various studies related to the subject

matter of the study, which helps to deal with the research problem. By reviewing the

literature the research gap also given in this chapter.

8

The third chapter consists with the data and methodology used for analyzing the

objectives. In other words, it demonstrates source of data and different indices used

to know the facts related to different objectives of the study.

The fourth chapter deals with the analysis of the collected data related to the

availability, affordability, price differences and different markups of common essential

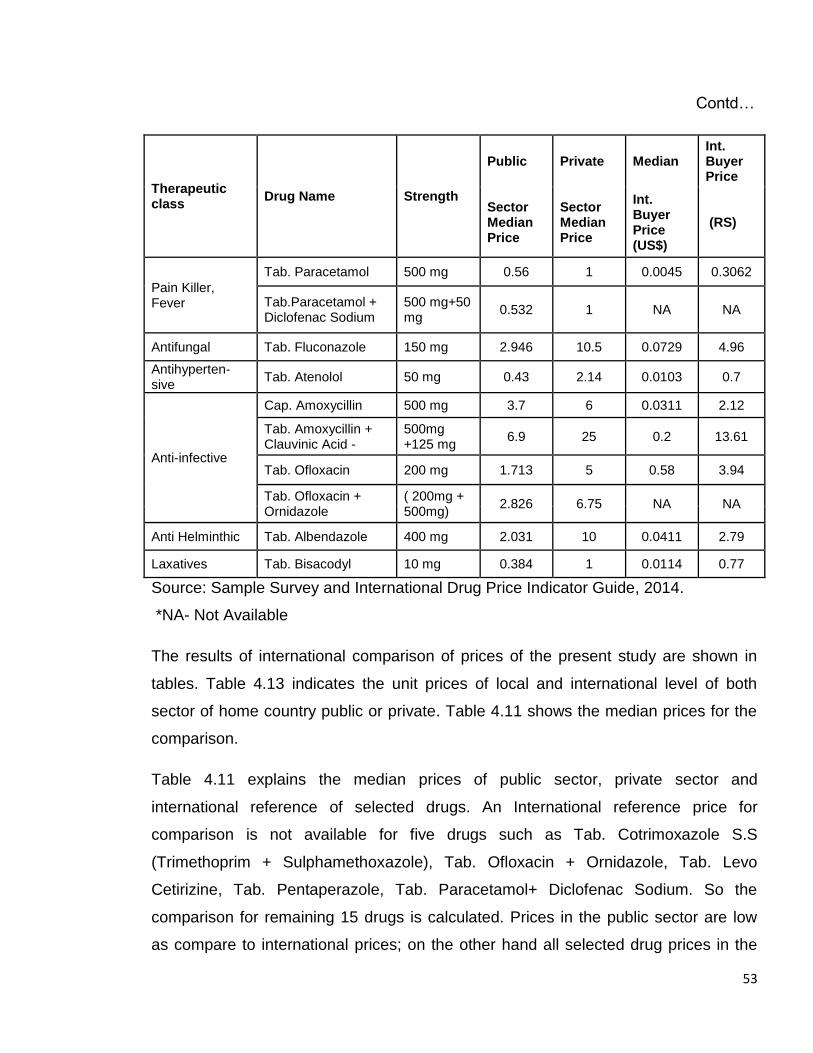

drugs. The international price comparisons are also taken into account.

The fifth chapter describes the evaluation of Indian drug price policies and current

drug price control order in detail also the impact of TRIPS on Indian pharmaceuticals.

The sixth chapter is an attempt to summarize the findings of the study. It also

includes some possible suggestions for policy building to access essential drugs for

ordinary people, stabilize the prices and to promote the generic affordable drugs.

9

CHAPTER - 2

LITERATURE REVIEW

The purpose of reviewing the literature is to study an overview of important literature

published on the subject of the study. Several studies have examined the Indian

pharmaceutical industry as per the availability of drugs, price differences and in a

different way as price mechanism, differences, and cost of production. In this context

an attempt has been made to review the related studies in a systematic order. First

section relates to availability, affordability and differences in drug prices and various

issues of usage of generic drugs in India. The second section deals with studies

related to drug control pricing policies and impacts of TRIPS.

Section I

Godwin and Varatharajan (2002) works on, differences in drug price across different

retail market settings in Thiruvananthapuram district of Kerala. The study determined

retail markup of 12 commonly used branded drugs with charged high drug prices is

estimated to capture the variability in mark-up across five different drug stores as

Government-owned drug stores, Private drug stores in a competitive setting, Society-

owned drug stores, Private drug stores in spatial monopoly setting, and Private drug

stores within hospitals. The sample was used as twelve Generic Name Paracetamol

,Ampicilin , Amoxycilin Mox, Ranitidine Rantac, Cetrizine Zetzine, Alprazolan Alprax ,

Penicillin G Voveran ,Atenolol Aten,Glyben Glamade Daoni,.Enaprel Envas,

Ciprofloxacilin. The results of study show there exists 32 percent price differential of

between different retail drug stores retailing the similar brand of the same drug; the

difference is huge as 120 percent of Amoxycilin. High difference in retail prices

attributable to the built-in markup in the MRP. However, retail margins in India are

estimated as near 32.7 percent (WHO/WTO, 2001). Studies also described a

difference of 150-200 percent between wholesale and retail prices. The formal and

informal factors as, Wholesale and retail markups, Import duties and taxes, can

double the price of a drug between manufacturers and consumer.

10

Kotwani (2003) works a report of medicine prices, availability, and affordability in the

state of Rajasthan on the basis of standardized methodology published by WHO/HAI

to analyses components of prices of a basket of essential medicines in the public,

private-for-profit and co-operative sectors. The results show that the government of

Rajasthan purchases medicines at a reasonable price for patients who are eligible for

free medicines at public health facilities. Almost half of medicines surveyed were

priced less than twice the international reference prices in private pharmacies. The

medicines such as albendazole, diazepam, diclofenace, amoxicilline, atenolol,

paracetamol, and hydrochlorothizide were expensive in the private sector. The prices

of albendazole, diazepam and diclofenac in the private was 8, 26 and 14 times the

procurement price in the public sector, including wholesale and retail margins are

very high or the manufacture prices are higher in the private sector than the public

sector. In case of public sector availability was low, so poor patients sometimes go

without treatment or buy medicines from private pharmacies forcefully. The availability

of medicines to treat HIV/AIDS was very low in all sectors.

Singal et al., (2011) examine the comparison between the quality and price of

generic (branded-generic) drug to their costly popular brand (branded) manufactured

by the same pharmaceutical company in India. The study considered materials and

methods on five medicines: alprazolam, cetirizine, ciprofloxacin, fluoxetine, and

pantoprazole which are commonly used and manufactured in branded and branded-

generic versions of the same company were selected. Price-to-patient and price-to-

retailers were found for five “pair” of medicines with results that retailer margin for

five branded medicines were in the range of 25-30percent, but for their branded-

generics version manufactured by the same company it was in the range of 201-1016

percent and price-to-patient for the branded version of cetirizine, fluoxetine,

ciprofloxacin, lansoprazole, and alprozolam was higher by 41percent, 33 percent, 20

percent, 14 percent, and 31percent than branded-generic. The study concludes that

the difference in price-to-patient was not as huge as it is expected for generics, but

the margins for retailer were very high for branded-generics. Quality of branded-

generics is same as for their branded version. It is suggested that there is a need to

modify the drug price policy, regulate the markups in the generic supply chain,

11

conduct and widely publicize the quality testing of generics for awareness of all

stakeholders.

Basak and Sathyanarayana (2012) depicts the evaluation of knowledge and

perceptions about generic medicines in community pharmacists' and drug retailers' in

two towns of Tamil Nadu, India, through a cross-sectional descriptive study, with a

questionnaire method, to survey community pharmacists and drug retailers working in

39 randomly selected private pharmacies from Among 66 respondents (pharmacists

and drug retailers), 39 (59.1percent) were drug retailers; 52 (78.8percent) were self-

employed; majority in the age group 31-40 (31.8percent); and mostly males

(83.3percent). Overall, 21 respondents (31.8percent) did not have knowledge about

generic drugs and 30 percent of the respondents believed that generic drugs are of

inferior quality compared to branded drugs. Only 63.6percent of the surveyed

pharmacists and drug retailers agreed that generic drugs can be considered

therapeutically equivalent with the branded ones. The majority of the respondents

(80percent) did not support generic substitution, even in case of approved drugs are

not available. Many community pharmacists and drug retailers have misconceptions

regarding generic medicines. It is concluded that lack of knowledge may negatively

affect the community pharmacists' support towards generic medicines in India and

this issue should be addressed by academicians and other relevant bodies.

Chaudhuri (2012) examines that hospitalization and outpatient services at public

health facilities are quite low as in Haryana (30percent) and in Punjab (20percent).

The specified reasons are the high cost of care including high prices of drugs. In the

Punjab, State the Health Systems Corporation includes public hospitals and public

clinics over which the poor people can access health facilities. Two schemes were

announced in 2008, to decrease out-of-pocket expenses for poor families. These two

schemes were ‘Jan Aushadhi’ where inexpensive generic drugs were made available

through public health care centers and ‘Rashtriya Swasthya Bima Yojna’ under which

a family of five below the poverty line would receive cashless treatment maximum

30,000 annually.

12

Roy et al., (2012) analysis the medicines cost and their affordability in private

pharmacies in Delhi (India), using a method of primary survey to measure the costs of

prescribed medicines and treatment of community acquired pneumonia (CAP), with

medicines purchased from 27 private pharmacies. Measurement of affordability is

taken by making a comparison of the monthly per capita expenditure, to the costs of

treatment (medicines). The results show observed costs of prescriptions (129.37+

217.99) in the cost of treatment of community acquired pneumonia varied huge

inconsistency from Rs. 34.50 to Rs.244.75 with azithromycin and Rs.72.20 to

Rs.277.30 with levofloxacin. The study finds show that there are large variations in

the costs of medicines are and economically not affordable for the poor in India.

Reforms in ‘National Pharmaceutical Policy’ are required immediately.

Eighth Report of PGRC (2013) observes that Punjab is somewhat better in health

indicators than many other states because of third rank in terms of birth rate (16.2 per

1000 population) in the country. The infant mortality rate of 30 per 1000 live births

places it at fifth rank. It has a maternal mortality ratio of 172 per 100,000 live births.

Around 61percent of deliveries are conducted in health institutions; the share of

government and private institutions stands at 22 percent and 39 percent respectively.

A major concern is the rising cost of medical care. The average expenditure for

hospitalization in Punjab is Rs. 15,431 which is one among the highest across the

country. Even in government health institutions, average out-of-pocket expenditure is

Rs. 270/- per OPD consultation and Rs. 7,700/- per hospitalization. User charges,

inadequate supply of medicines and other surgical supplies and lab reagents has led

to an escalation in the cost of medical care in government health institutions. The

state does not allocate adequate budget for medicines and supplies. At least

20percent of the health budget should be allocated for medical and surgical supplies.

Clearly, decreasing outlay on social sectors is responsible for a cut on soft items in

the budget such as medicines.

Hinsch et al., (2014) works on improving medicines price transparency and Price

information Mechanism through data collected during the course of a WHO project

focusing on the development of a vaccine price and procurement information

13

mechanism. The project collected information from six medicine price information

mechanisms and interviewed data managers and technical experts on key aspects as

well as observed market effects of these mechanisms. These include the uptake of

high quality medicines, more favorable results from contract negotiations, changes in

national pricing policies, and the decrease of prices in certain segments for countries

participating in or deriving data from the various mechanisms. In conclusion the

reviewed mechanisms avoid the methodological challenges observed

for medicine price comparisons that only use national price databases. It is suggested

that medicine price information mechanisms respond to the need for

increased medicine price transparency and have the potential to contribute to

improved access to medicines in developing countries.

Ahmad et al., (2015) examines that nearly half of India’s population has lack of

access to essential rugs in government hospitals due to the heavy dependency of

most of the patients in the private sector in spite of India’s greater exports in drugs to

more than 200 nations consisting of more than 20,000 manufacturers and with

3rd largest market by volume in the world. The main emphasis of in Indian

pharmaceutical, health policies is to focus on the progression of the industrial sector

rather than the issues of law availability, high pricing, and less affordability of drugs.

As it is a common view that drug prices in India are comparatively low, but studies

have reported that medications in India are costly and unaffordable. The margin on

drug sales across the same generic class is extremely high, often ranging from 1000

percent to 4000 percent. Since independence the objectives of the Indian

pharmaceutical industry have remained the same as the growth of domestic industry

and manufacture qualitative drugs. In India, more than 80 percent of healthcare

expenditure is borne by patients while the income of 70 percent of Indian population

is less than 2$. The most essential medications that are needed by the majority of the

Indian population should be reviewed for inclusion in the drug price control list. There

is a large difference in the prices of different branded drugs and generics that are

selling in the market even though they might characterize the same drug fragment.

Health experts should be advised to suggest cost-effective drugs in the attention of

the patients without being influenced by pharmaceutical companies. Consumer

14

knowledge about generics could be improved through effective educational

interferences. The issue of pricing needs an all-inclusive solution generated by the

coordinated efforts of stakeholders, pharmaceutical companies, and healthcare

professionals in order to catalyze equity in access to health care.

Rana and Roy (2015) examine the issues and relevance of generic drugs which are

bioequivalent to the innovator product in terms of dosage form, strength, and route of

administration, quality, safety, performance characteristics and intended use of global

health. Generic drugs are considered as a basis for providing affordable drugs to

patients. The major generic markets in the world include United States of America

(USA) followed by European Union (EU), Canada, Japan and Australia. The major

suppliers of generic medicines in China and India are showing fabulous growth in the

generic drugs sector. There are many legal and regulatory issues along with quality

concerns associated with the use of the generic products. Lately, bilateral

international agreements called Free Trade Agreements (FTA), delaying tactics by

originator companies like strategic patenting and litigations on generic manufacturers

have been a major setback for the generic medicine industry. These issues need to

be addressed to optimize use of generic Drugs. The sustainability of generic drugs in

public sector is crucial for improving access to essential medicines to the worldwide.

Section II

Lanjouw (1997) disclose the outcomes of a field survey conducted in order to

evaluate the impact of pharmaceutical product patents in India and her main

concludes that Indian firms, profit the level of generic drug production will decrease

for as they will possibly have to pay some of royals to the original innovators. An

increase in the incentives for investment in R & D in diseases relevant to developing

countries, as well as in the formation of innovations in general. However, this may be

basically due to the fact that the strategy of imitation is no longer available, rather

than being a direct incentive effect. Another impact can be that stronger IPR would

not enlarge the R & D activity of foreign firms in India, since in multinationals

pharmaceutical R & D is a highly centralized process, where cost is not the

paramount concern.

15

Lall (2003) reviews the case for uniform and strong IPR by developing country

groupings using various procedures of domestic technology imports and innovation.

This indicates that in India, "it is possible to argue, however, that India has now

reached a stage in pharmaceutical production where stronger IPRs would induce

greater innovation by local firms the benefits of which would have to be set off against

the closure of other firms.

Hoen (2003) examine that the causes for the shortage of access to essential

medicines are diverse, but in some cases of necessary treatments where drugs are

very costly are the major barrier. Unaffordability of drug prices can be the result of

strong intellectual property protection. While TRIPS does offer safeguards to remedy

the negative effects of patent protection or patent abuse, in practice it is unclear

whether and how countries can make use of these safeguards when patents

increasingly present barriers to medicine access. Public health supporters the Doha

Declaration as an important accomplishment because it gave dominance to public

health over private intellectual property on the other hand the Doha declaration did

not solve all of the problems associated with intellectual property protection and

public health. The recent failure of the WTO to resolve the outstanding issue to

ensure production and export of generic medicines to countries that do not produce

may even indicate that the optimism felt at Doha was premature.

Dhar and Gopakumar (2006) works to specify the performance of Indian

pharmaceutical firms by interacting the changes in the patent regime required by the

Agreement on TRIPS. In Post- TRIPS period the R & D spending of some of the top

firms as Ranbaxy and Dr Reddy’s has shown an increase which results, R&D

strengths of the firms have enhanced significantly.

Mani (2006) reveals a detailed mapping out of the sectoral system of innovation of

India’s pharmaceutical industry. The study shows that the TRIPS compliance of the

intellectual property right regime has not reduced the innovation capacity of the

domestic pharmaceutical industry, which has visualized an increase in both research

budget and patenting.

16

Chaturvedi and Chataway (2006) explain in the paper that Indian firms are investing

in R & D not only for innovative drug discovery also for developing capabilities to

assimilate and exploit knowledge available outside. Indian firms are acclimatizing to

the changing environments. R & D is predictable as the ‘survival kit’ in the post-TRIPs

scenario. They are also placing themselves as a partner of choice for technology

savvy national and multinational firms.

Birla and Gupta (2007) explain that Indian firms are increasing their innovative

capacity. The Indian Pharmaceutical Industry is moving, chances in Post- TRIPS

period. The participation of Indian generic companies are also growing their

participation in the progressive markets, particularly the US. R&D growth rate is also

increasing rapidly.

Manikandan and Gitanjali (2012) review the national list of essential medicines of

India. The Ministry of Health, Government of India revised the National List of

Essential Medicines of India (NLEMI 2011) in June 2011, eight years after the last

revision. The NLEMI 2011 contains 348 medicines and was prepared over one and a

half years by 87 experts. Though there are some positive aspects of the list such as

the documentation of a detailed description of the revision process, the inclusion of

many experts from various fields in the review committee, well written description of

the essential medicines concept and others, a critical review of the list reveals areas

of major and minor concerns. Improper medicine selection like the inclusion of a

nearly obsolete medicine such as ether, an anesthetic agent; non-inclusion of

pediatric formulations; spelling errors; and errors in the strengths of formulations

diminishes the significance of the NLEMI 2011. In its present form, the NLEMI 2011

did not align with the Indian Pharmacopoeia, and the National Health Programs as

well as the National Formulary of India 2010. Formatting errors, non-inclusion of an

index page, syntax and spelling errors may also undermine the usefulness of the

NLEMI 2011 as a reference material. An urgent revision of the NLEMI 2011 is

advised so as to avert misinforming the wider international and local readers.

17

Malik (2013) revises that TRIPs was one of the most contentious issues in the

Uruguay Round of multilateral trade negotiations, concluded in 1994 at Marrakesh.

India has decided to comply with all the instruments and annexes of GATT, including

Trade Related Aspects of Intellectual Property Rights (TRIPs) as a member of the

World Trade Organization (WTO), and having signed the General Agreement on

Tariff and Trade (GATT). Because of the WTO, India has to amend its intellectual

property laws. India was forced to comply with the TRIPs agreement. After the

formation of WTO in 1995, the India is being its member has to implement the TRIPs

agreement in to. The commitment under the TRIPs agreement compelled India to

amend its intellectual property laws.

Kumar (2014) view for comparison between old and latest systems in DPCO as

DPCO act 1995 and DPCO act 2013. The new pricing guideline, DPCO has come in

to effect from May 15, 2013. In past before implementing DPCO 2013, the prices of

74 bulk drugs are controlled by DPCO 1995, but when the DPCO 2013 has come into

effect, 652 new drugs are added to the list national list of essential medicines

(NLEM). It is required that the duty of government to make the lifesaving drugs

affordable to the common man. It is suggested for the implementation of new policies

that the government has to reduce the prices of the drug which is needful for common

man, to improve the research and development of new drugs, it has to be liberal in

fining the prices in such a way that the industries cannot be suffered and it has to

support the research in the nation. It controls the market prices of the drugs and it

supports research by exempting the price control of new drugs by giving the patent up

to 5 years.

Kanwar and Hall (2014) analyses the impacts of TRIPS Patents. TRIPS which are

the Agreement on Trade Related Aspect of Intellectual Property Rights attempt the

difficult assignment of balancing private and public rights. On one hand, it protects the

interest of the pharmaceutical companies that invest heavily in R and D of Drugs and,

on the other; it allows nations that belong to the WTO to promote public health in their

respective countries. However, patents on pharmaceutical products have adversely

affected industrially developing and least developed countries, hampering their ability

18

to formulate suitable public health policies that would enable their ailing citizen to

access medicines. For instance Pharmaceutical patents have raised the cost of life

saving drugs, effectively placing them out of the reach of the mainstream of the

World’s population.

Most of the studies are found which emphasized on availability, affordability and

prices in some states of India. Studies related to price differences are very few and

explained the only difference between the retail prices in different markets. Price

differences at different stages of distribution are not done in the earlier studies in India

and none of the study found in the Punjab. Therefore, the present study is an attempt

to examine the price differences at various stages from manufacture to consumer

along with the availability and affordability in the Bathinda city of Malwa region

(Punjab) known as health sensitive.

19

CHAPTER - 3

DATABASE AND METHODOLOGY

This chapter deals with the data collection and methodology used in the present study

for analyzing the availability, affordability and price differences of essential drugs in a

Bathinda city (Punjab).

Data Base

To achieve the different objectives of the present study, the study primarily relies on

the survey of the Bathinda city with the help of WHO/HAI methodology (2003),

described in the manual entitled ‘Medicine Prices – a new approach to measurement’

which has been designed to collect data, analyze and interpret the result in a

standardized way. To understand the methodology “International Drug Price indicator

Guide 2014” published by WHO is also used. This methodology helps in the present

study for selection of health facilities, the comparison of prices at international level

and to calculate affordability, and pricing components. The secondary data sources

have been used for:

1) The collection of Global Core and regional drug drugs lists, mentioned in the

WHO/HAI manual (2003) published for international price comparison.

2) To calculate the affordability minimum wages in the government sector of

Bathinda district is collected from ‘Labour Department of Punjab’ (Statistical

Section, 2013) and poverty estimates by (Tendulkar Method, 2011-12).

Selection of Area

Bathinda city is purposefully selected for primary survey. It is located in the Malwa

region in the state of Punjab which is known as health sensitive region. It is divided

into the 4 tehsils of Bathinda, Rampura Phul, Maur and Talwandi Sabo. These tehsils

are further divided into nine Blocks of Bathinda, Sangat, Nathana, Rampura, Phul,

Balianwali, Bhagta Bhaika, and Talwandi Sabo and there are total 21 cities and towns

in this district from which first Bathinda (Municipal Corporation) is selected

20

purposively because this is the only city of Malwa region where a government drug

store is established by central government.

For the primary survey the three main stakeholders, i.e. drug consumers as patients,

drug retailers as chemists, and the wholesalers are surveyed on the basis of random

sampling technique. The sample size for the patients is selected 150 from different

areas of the city to collect the general prescription of patients on the use of health

facilities, use of generic or branded drugs and the sources of purchasing drugs. The

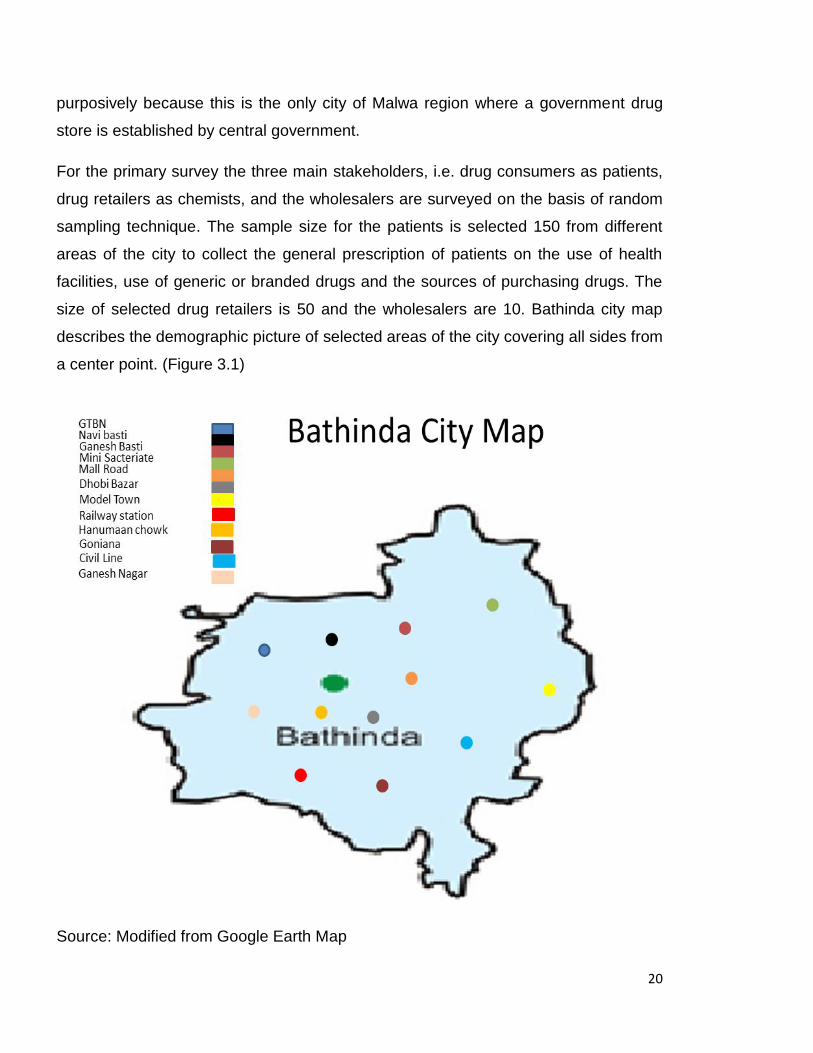

size of selected drug retailers is 50 and the wholesalers are 10. Bathinda city map

describes the demographic picture of selected areas of the city covering all sides from

a center point. (Figure 3.1)

Source: Modified from Google Earth Map

21

Two sectors are surveyed in the city for drug price comparison. The sectors are:

1) Public Sector Prices: Data for drug prices and drug availability are

collected from the public sector drug store in Bathinda city known as “Jan

Aushadhi” located in Civil Hospital Bathinda. This drug store works under a

Central government at very less price of essential medicines.

2) Private Sector Prices: Private sector drug prices are those, at which

patients pay for medicines to private retail drug stores. In this sector also

printed price, i.e. (MRP) maximum retail price is charged by retailers. So the

data on (MRP) prices in this sector are collected through printed price on the

strip.

In Public sector one drug store is available in the city “Jan Aushadhi drug” store and

profile of private drug distributors in the city is collected from the President of the

wholesalers and retailers of the Bathinda city. In private sector 50 retail drug stores

are randomly surveyed from the different areas such as retail drug stores near Civil

Hospital, Gandhi Market, Near Bus stand, Power house road, Ajit Road, Mall road,

Bibi wala road, Haji Rattan B.C.C road, Mati Das Nagar, Mini Sectriate, Guru Gobind

Singh Nagar. Famous wholesales who provide branded-generic drugs to different

private retail drug stores are also surveyed, because almost all the private retailers

buy medicines from local wholesalers and all the wholesalers provide the drugs at

the same prices to retailers.

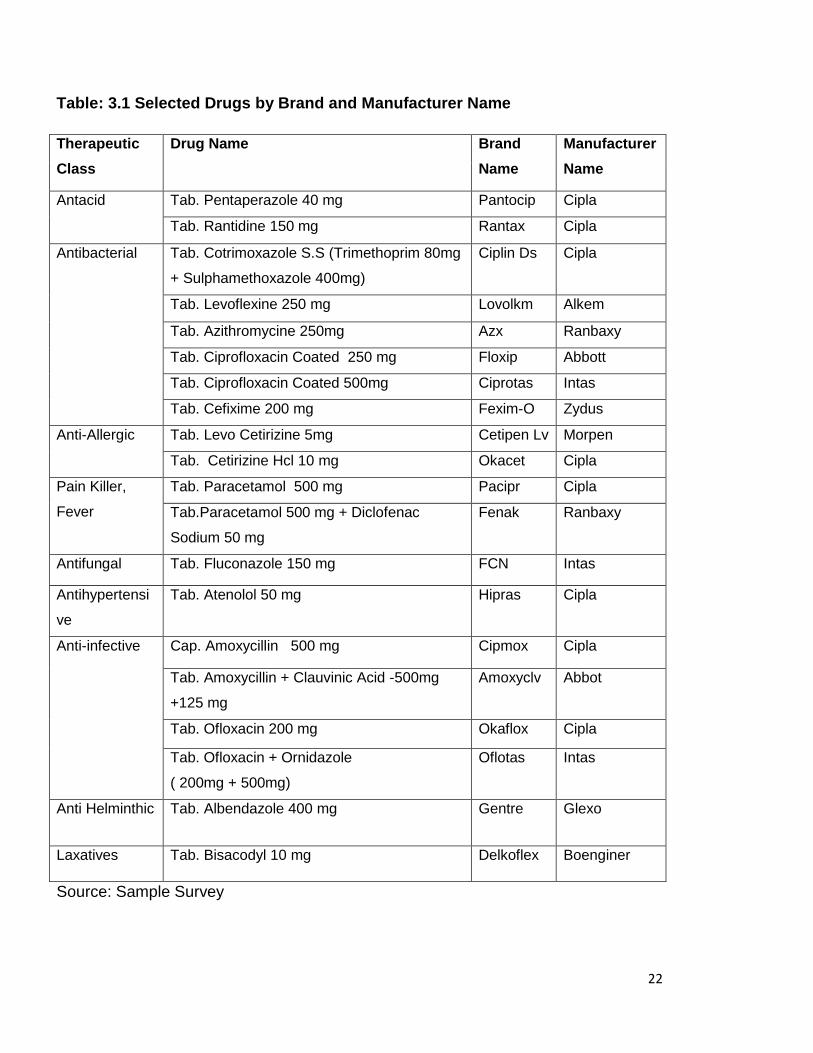

Selection of Drugs

In the Bathinda city number of medicines are purchased from private drug stores, the

selection of medicines is very difficult on the basis of patients’ views, so the common

medicines are sorted out on the basis of views of doctors and retailors, final selection

is made by comparing these common medicines with Punjab Essential Drug List

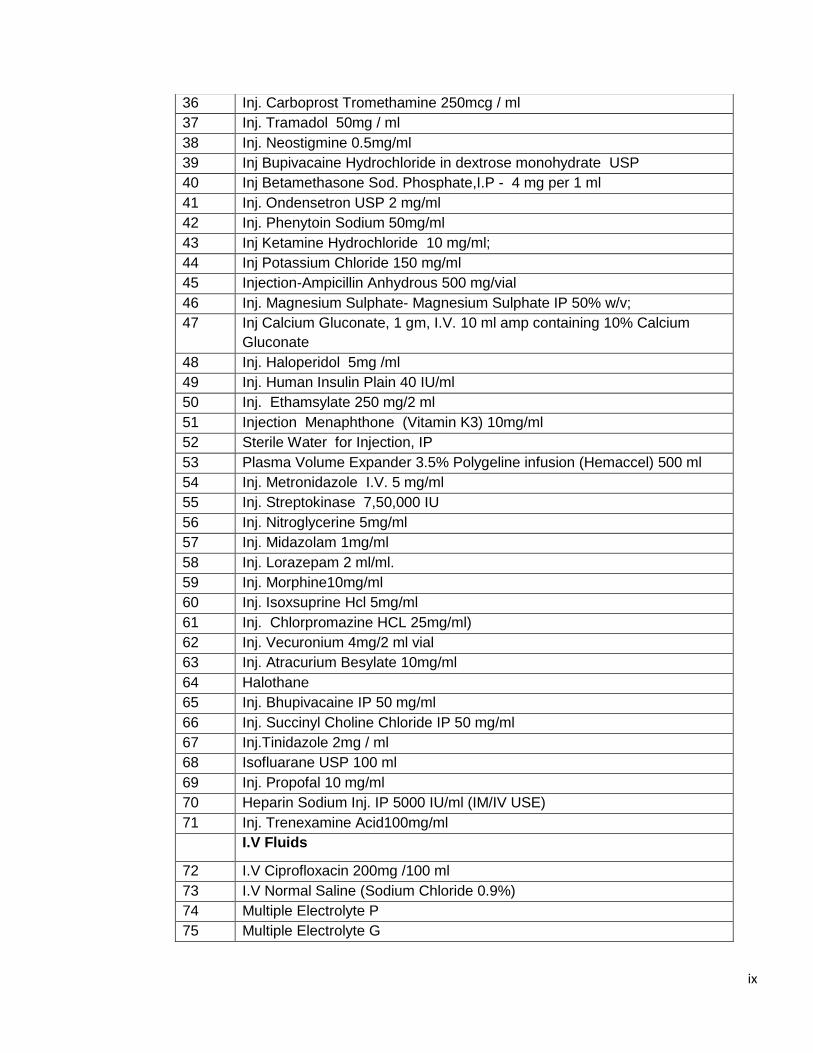

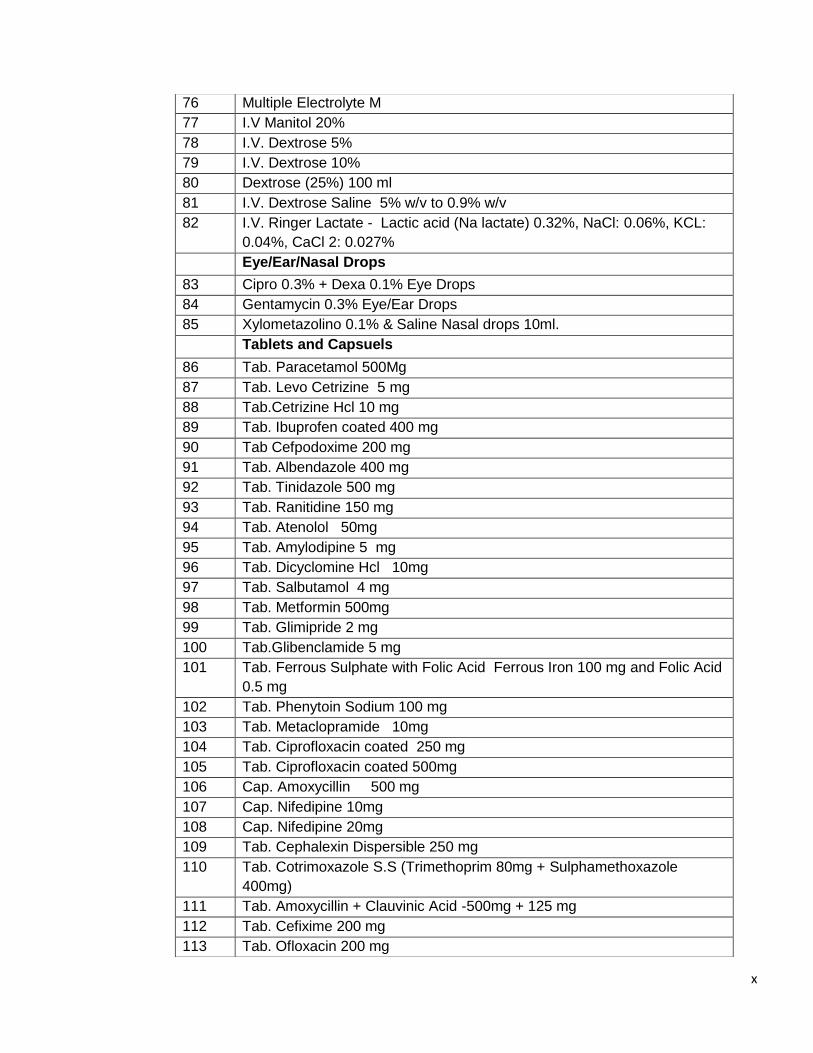

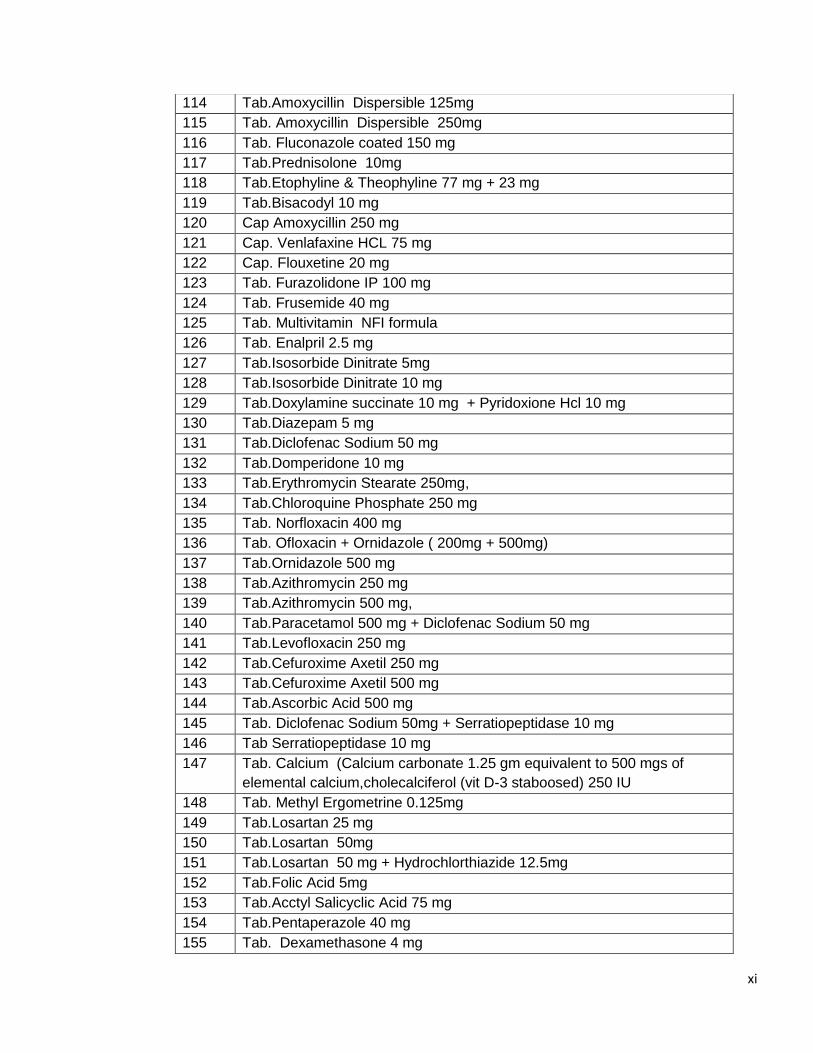

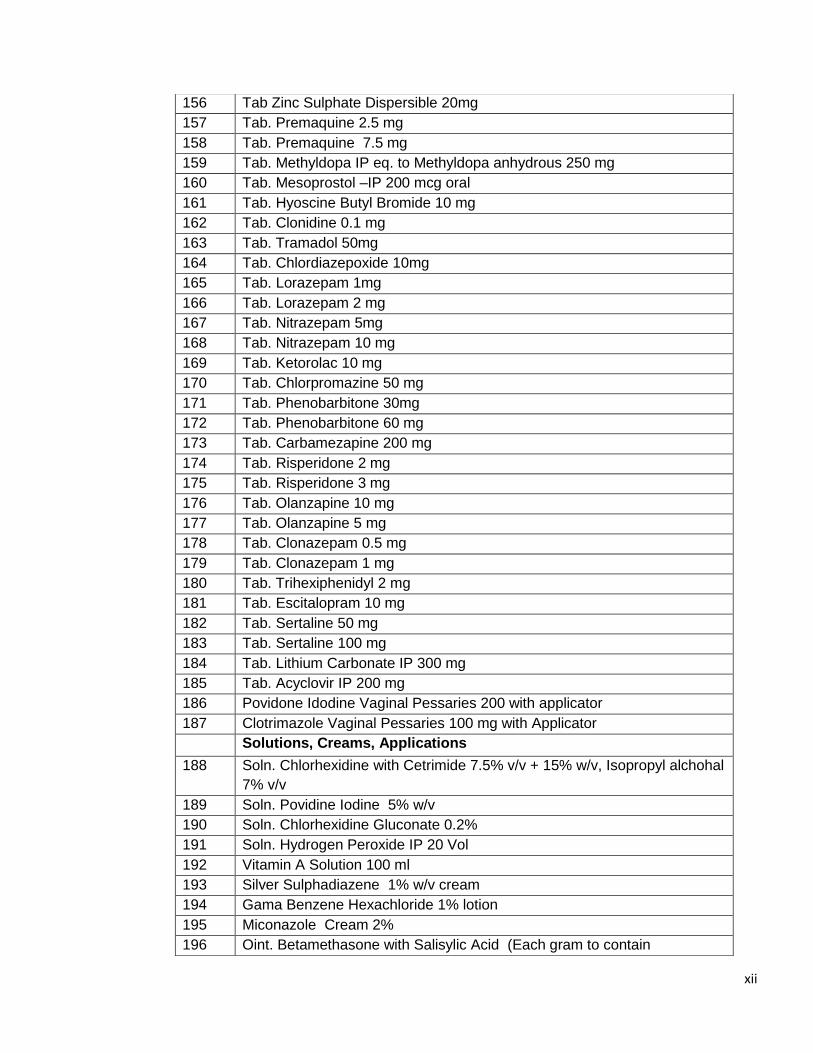

(EDL) containing (235) name of all types of drugs including injections, (1 to 71), I.V

Fluids (72 to 82) Eye/Ear/Nasal Drops, (83 to 85), Tablets and capsules, (86 to 187),

Solution, Creams, Applications (188 to 204), Syrup/ Suspension (205 to 235) The

selected medicines are under the number (86 to 187) tablets and capsules.

(Annexure-B)

22

Table: 3.1 Selected Drugs by Brand and Manufacturer Name

Therapeutic

Class

Drug Name Brand

Name

Manufacturer

Name

Antacid Tab. Pentaperazole 40 mg Pantocip Cipla

Tab. Rantidine 150 mg Rantax Cipla

Antibacterial

Tab. Cotrimoxazole S.S (Trimethoprim 80mg

+ Sulphamethoxazole 400mg)

Ciplin Ds Cipla

Tab. Levoflexine 250 mg Lovolkm Alkem

Tab. Azithromycine 250mg Azx Ranbaxy

Tab. Ciprofloxacin Coated 250 mg Floxip Abbott

Tab. Ciprofloxacin Coated 500mg Ciprotas Intas

Tab. Cefixime 200 mg Fexim-O Zydus

Anti-Allergic Tab. Levo Cetirizine 5mg Cetipen Lv Morpen

Tab. Cetirizine Hcl 10 mg Okacet Cipla

Pain Killer,

Fever

Tab. Paracetamol 500 mg Pacipr Cipla

Tab.Paracetamol 500 mg + Diclofenac

Sodium 50 mg

Fenak Ranbaxy

Antifungal Tab. Fluconazole 150 mg FCN Intas

Antihypertensi

ve

Tab. Atenolol 50 mg Hipras Cipla

Anti-infective

Cap. Amoxycillin 500 mg Cipmox Cipla

Tab. Amoxycillin + Clauvinic Acid -500mg

+125 mg

Amoxyclv Abbot

Tab. Ofloxacin 200 mg Okaflox Cipla

Tab. Ofloxacin + Ornidazole

( 200mg + 500mg)

Oflotas Intas

Anti Helminthic Tab. Albendazole 400 mg Gentre Glexo

Laxatives Tab. Bisacodyl 10 mg Delkoflex Boenginer

Source: Sample Survey

23

For each drug two types of products are surveyed, generic without any brand name,

i.e. Lowest Price Generic, (LPG) and the Most Sold brand Generic (MSG). Generic

drugs with the lowest price are available in the public store. The wholesale prices are

only surveyed in the private sector because of wholesalers are the part of the drug

distribution chain in the private sector only.

In the public sector the drugs are directly supplied by center government and there is

no issue of whole and retail prices. In the private sector, which is dominating to

provide each type of drugs has many issues regarding the price differences within

sector and high markups mostly in generic-branded drugs. Thus, the brand and

manufacture name is also asked of most sold medicines to compare the different

prices and markups.

Drug Price distribution channel

With the help of the drug distribution chain in Bathinda, drug price components are

analyzed to establish that how the retail price of a medicine is determined and how

different markups and taxes are contributing in the price.

The manufacturer provides medicines to the wholesalers through Clearing and

Forwarding Agents (CFA), and central warehouse, then supplied to substockist or

wholesalers who distribute to different retail stores, lastly patients purchased from

chemists. Thus the chain internally within the city is started from wholesaler to

patients. So to find information about prices in an accurate way, wholesalers and

retailers are contacted and asked to provide information on price components of

selected medicines

Analysis of Data and Outcome Variables

Primary survey is followed by data analysis. Data collected in this study has been

analyzed through:

(i) Appropriate statistical tools are used in computerized excel, such as

averages, percentage, price ratios, sector wise unit prices, minimum and

maximum.

24

(ii) To explain the international comparison ‘Median Price Ratios’ are calculated.

These ratios are the median unit prices across the facilities surveyed in a

sector (in local currency) divided by the international reference price (also in

local currency) to compare the external standard price.

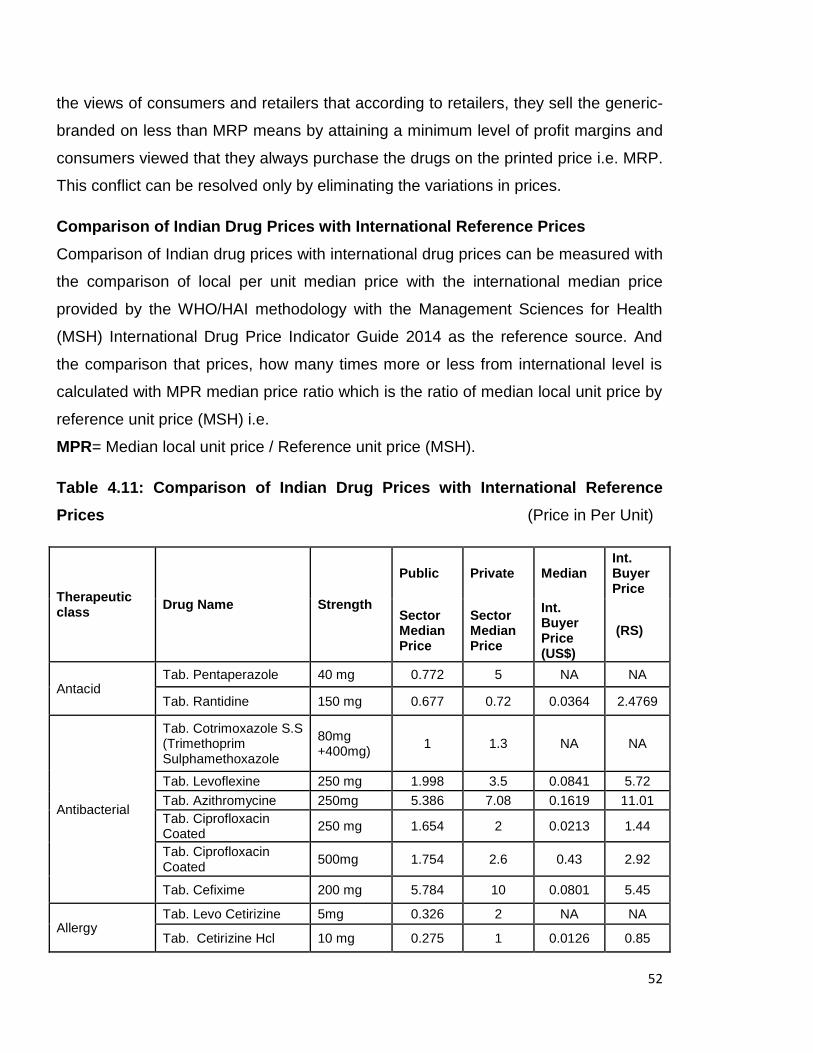

MPR= Median local unit price / Reference unit price (MSH).

The reference price serves as an external standard for evaluating local prices. WHO

and HAI recommend using the ‘Management Sciences for Health (MSH)

International Drug Price Indicator Guide 2014 as the reference source’.

Limitations of the Study

The study attempts to use the standardized methodology provided by WHO/HAI for

attaining the objectives, some guidelines of methodology cannot be satisfied.

According to WHO methodology originated brands of drugs are also surveyed, but in

the present study only commonly used brands are surveyed.

25

CHAPTER - 4

AVAILABILITY, AFFORDABILITY AND PRICING OF ESSENTIAL DRUGS

Introduction

This chapter is an attempt to examine the issues related to essential drugs, i.e.

availability, affordability and price differences, through the primary survey of Bathinda

city. The present survey is an amalgam of different respondents from various fields

suc h as doctors, druggists (wholesalers and retailers) and patients to verify and

examine the use of drugs from branded to generic and preference towards health

facilities. The present chapter is divided into two parts: first part explains the

availability and affordability of commonly used essential drugs in public and private

sector. The second part deals with the drug price differences between public and

private sectors, differences within the private sector and international price

differences i.e. international price comparison. Through prices differences, different

markups are also analyzed for reviewing the drug price policies to make them more

effective.

Overview of Respondents

The different respondents involved in the study are the first source to analyze the

issue of availability, affordability and price differences of common essential drugs by

surveying of doctors, patients and druggists in the city. Patient’s opinion towards

public sector health facilities is not adequate as the majority of the respondents about

68 percent are not interested to use the public sector health facilities and prefer to the

private sector health care facilities due to the availability of drugs and provision of

satisfactory treatment. The remaining respondents use the public facilities but not for

entire treatment and then go to private facilities because of they are not much

contented with the prevailing facilities due to low availability of drugs in the civil

hospital and then they have to purchase the drugs and health treatment from the

private sector out of pocket with a higher cost. The reason for the positive opinion

towards the private sector hospitals and drug stores instead of high cost is the

availability in a large number at any time this concludes that the majority of the

population in the city depends on private health care facilities with compensating the

26

higher cost of treatment for temporary and regular basis. Lack of knowledge of the

respondent’s about the public drug store ‘Jan Aushadhi’ for the drugs at very less

price is one of the reasons for preferring private drug stores while lack of availability

of all drugs is the second reason.

The patient’s perspective about prevailing drug prices indicates that nearly 30 percent

of the respondents are fully dissatisfied from prevailing prices of drugs, 27 percent are

somewhat satisfied, 16 percent are neutral, 22 percent are satisfied and only 7

percent are fully satisfied. It is observed that the fully satisfied respondents are with

higher income which is the main reason for not much burden of higher prices of drugs

to them and the around 30 percent respondents are dissatisfied bearing the health

care burden due to higher prices of drugs at private drug stores.

The results related to general prescription explain that patients do not have

knowledge about the generic drugs. Around 70 percent of the respondents do not

familiar with the term generic drugs, only distinguish that in generally known is, the

less cost of drugs in provided in the public sector. But because of low availability of

drugs in the hospital, doctors also prefer drugs from private retail shops. In this case,

it’s very difficult for any patient to substitute any type of generic which is less costly

than branded. Normally any individual cannot understand about the difference

between generic branded and branded medicines because of the same expression of

all drugs and patients have to choose the branded drugs as preferred by doctors

which results the high burden of drug prices is taken by the patients.

The perspective of doctors and druggists play a significant role for the prescription

about use of drugs because opinions of patients extremely depend upon these two for

use of any drug. Public sector doctors attempt to prefer generic drugs the most and

branded in very rare cases, on the other side private doctors favor to branded drugs

which are more expensive than generic drugs. The results of the present study depict

that 40 percent doctors in private sector favor only branded drugs because of their

quality and their belief generic drugs are less effective and not good in quality.

Remaining around 60 percent doctors have viewed that generics are good substitutes

for branded to make drugs more affordable and they prefer both types of drugs

27

according to the treatment for diseases. So doctors of different hospitals in the city

responses about the drug preference that, usually they prefer both branded and

generic, but ordinarily favor to the branded because of more effectiveness.

The perspective of the drug retailers (chemists) is also interrelated to the doctor’s

view. The patients make more demand of branded drugs from the druggist preferred

by the doctors to them. On the other side in public sector generic, drug store (Jan

Aushadhi) the generics without any brand name are sold. In private medical stores,

both branded and branded-generic are preferred to patient for both regular and

temporary basis. Around 60 percent retailers have viewed that there is a more

demand of branded drugs with a maximum 16 percent to 20 percent margin, but in

case of branded-generic drugs, there is a huge level of margin sometimes nearly

more than 100 percent. When retailers are asked about their views related to this

phenomenon of differences in margins, they expressed that we charge the prices with

a limit of margin according to patients can be minimum or maximum level of margins.

According to the drug wholesaler’s viewpoint, there is not much variation in the

demand of branded and branded generic drugs. The viewpoint of drug wholesalers is

that the print price of generic medicines is many times higher than the company price,

they contracted drugs from the company’s warehouses at very less price, then by

adding their profit margin maximum 10 percent according to drug’s price and drugs

distributed to the retailers in the city. Retailers have no link with wholesalers about

their margin levels, once the wholesalers distribute the drugs then its retailer’s own

choice of charge the price to patients.

The opinions of different respondents can be summed up that preference of branded

or generic drugs is not decided by patients because of lack of knowledge. It depends

upon the doctors or the chemists who suggests drugs. The reason for more

preference to branded drugs by doctor’s views is the better quality and the chemists

prefers to generic drugs because of two reasons, first the low price of generic and

patients can easily afford, secondly the margin level is many times higher than

branded. The differences in mark-up levels of branded generic drugs are the reason

of price difference in the markets. By considering the opinions of different

28

respondents discussed above the present study is an exertion to disclose the

differences in prices and markups charged by retailers which shows the non-

transparency and variations of drug prices in the market.

Availability of Essential Drugs

Availability of essential drugs is one major part of health care in the society. Essential

drugs availability is required in both public as well as in private sectors. By reviewing

the opinions of patients, it comes out that low availability of drugs is the issue of

public sector. As in private sector, there are number of sources available for the

patients to purchase drugs, i.e. medical stores in a large number almost in every

area, but they provide mainly very costly drugs and private doctors also prefer

branded drugs which are costlier than generics. Generics with different brand names

are available in the private sector, which are also sold at the printed price i.e.

maximum retail price (MRP). The generic drugs with lowest price are available in the

public sector drug store known as “Jan Aushadhi” within a civil hospital in Bathinda

city. This generic, drug store is working under the central government to provide

cheaper non-branded essential drugs. There is always issue of lower availability in

the public sector rather than the private sector because of profit- oriented strategy of

the private sector. The insufficient availability issue relates to the public sector is the

reason to select the public sector in the study.

The availability of all essential drugs mentioned in survey is listed from “Drug

essential list of Punjab” (2011) including (235) number of different items of drugs,

which including injections, (1 to 71), I.V Fluids (72 to 82) Eye/Ear/Nasal Drops, (83 to

85), Tablets and capsules, (86 to 187), Solution, Creams, Applications (188 to 204),

Syrup/ Suspension (205 to 235) are surveyed. None of the brands are available in the

drug store. Only generics with salt name are provided there. The price which is

printed on the strip of drug is charged similarly. Overall availability of essential drugs

is found very less only 28.51percent. When patients found the low availability of drugs

in public sector facilities, they forcefully have to purchase drugs from the private drug

stores with high prices, which may also lead to excessive out-of-pocket spending.

29

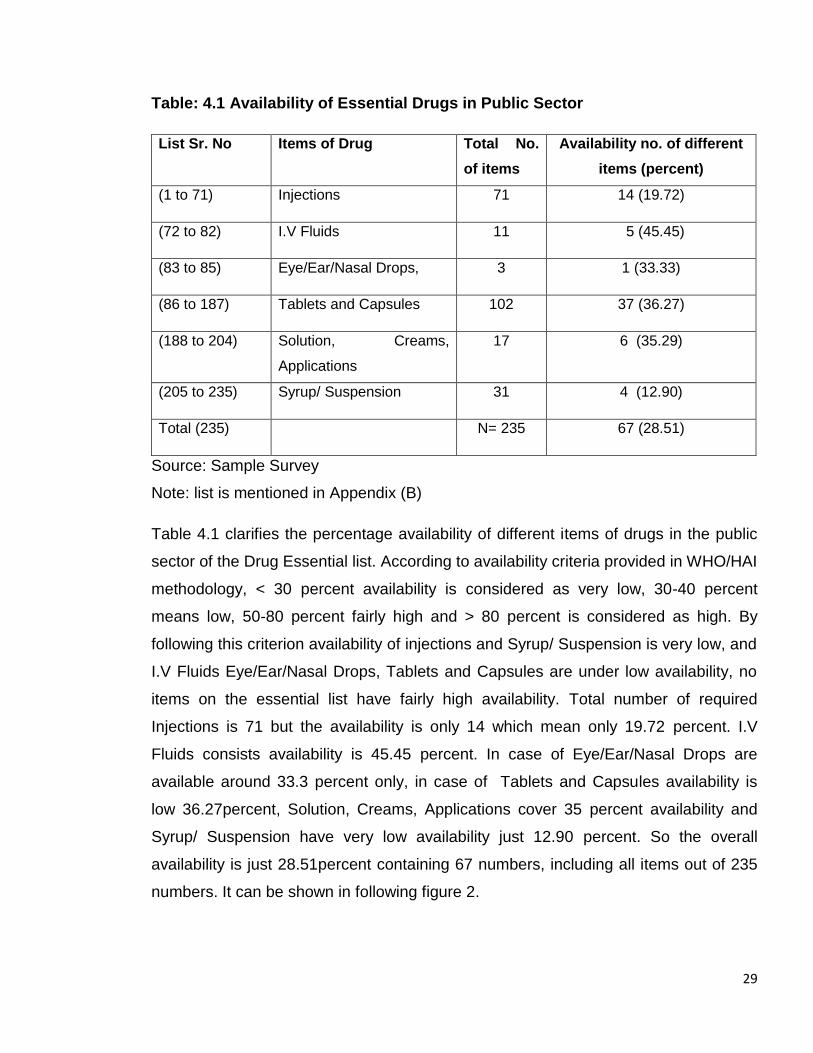

Table: 4.1 Availability of Essential Drugs in Public Sector

List Sr. No Items of Drug Total No.

of items

Availability no. of different

items (percent)

(1 to 71) Injections 71 14 (19.72)

(72 to 82) I.V Fluids 11 5 (45.45)

(83 to 85) Eye/Ear/Nasal Drops, 3 1 (33.33)

(86 to 187) Tablets and Capsules 102 37 (36.27)

(188 to 204) Solution, Creams,

Applications

17 6 (35.29)

(205 to 235) Syrup/ Suspension 31 4 (12.90)

Total (235) N= 235 67 (28.51)

Source: Sample Survey

Note: list is mentioned in Appendix (B)

Table 4.1 clarifies the percentage availability of different items of drugs in the public

sector of the Drug Essential list. According to availability criteria provided in WHO/HAI

methodology, < 30 percent availability is considered as very low, 30-40 percent

means low, 50-80 percent fairly high and > 80 percent is considered as high. By

following this criterion availability of injections and Syrup/ Suspension is very low, and

I.V Fluids Eye/Ear/Nasal Drops, Tablets and Capsules are under low availability, no

items on the essential list have fairly high availability. Total number of required

Injections is 71 but the availability is only 14 which mean only 19.72 percent. I.V

Fluids consists availability is 45.45 percent. In case of Eye/Ear/Nasal Drops are

available around 33.3 percent only, in case of Tablets and Capsules availability is

low 36.27percent, Solution, Creams, Applications cover 35 percent availability and

Syrup/ Suspension have very low availability just 12.90 percent. So the overall

availability is just 28.51percent containing 67 numbers, including all items out of 235

numbers. It can be shown in following figure 2.

30

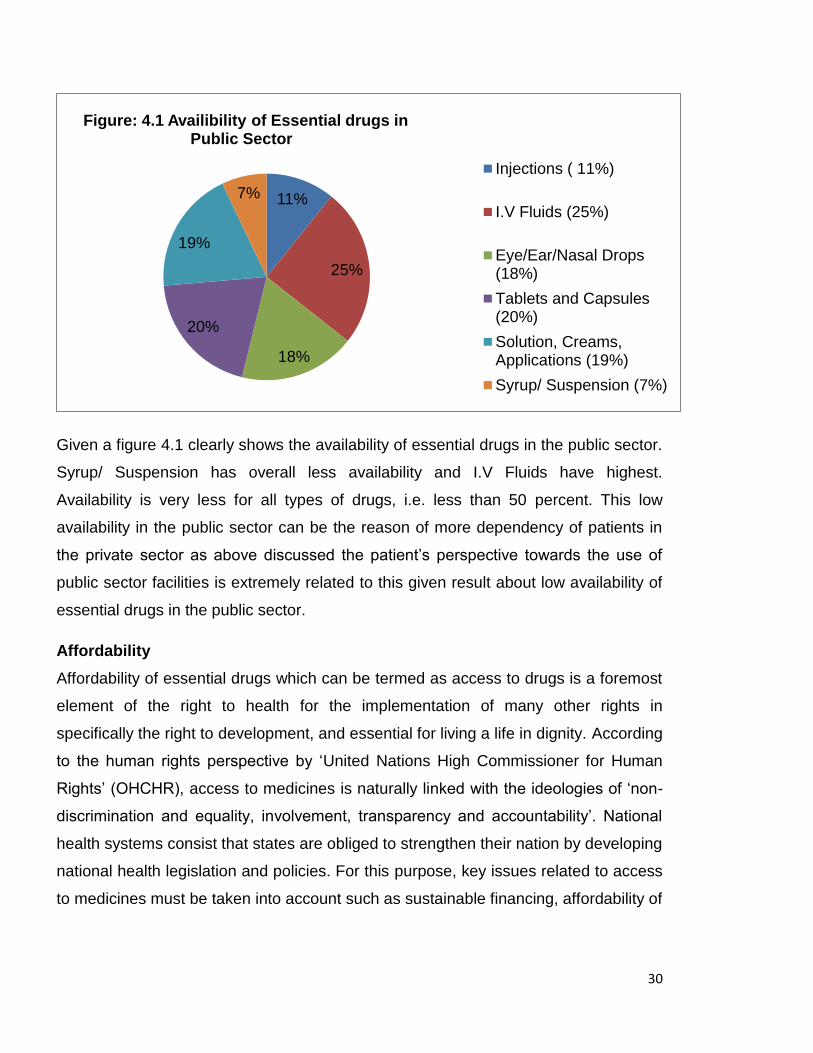

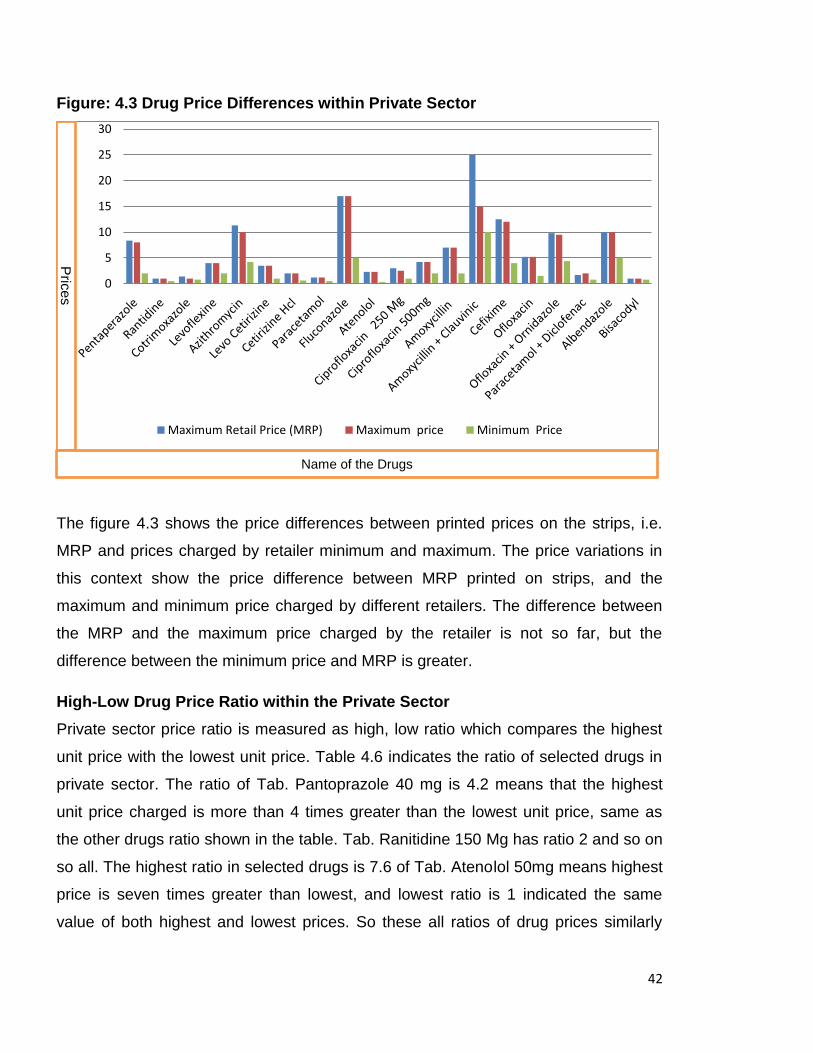

Given a figure 4.1 clearly shows the availability of essential drugs in the public sector.

Syrup/ Suspension has overall less availability and I.V Fluids have highest.

Availability is very less for all types of drugs, i.e. less than 50 percent. This low

availability in the public sector can be the reason of more dependency of patients in

the private sector as above discussed the patient’s perspective towards the use of

public sector facilities is extremely related to this given result about low availability of

essential drugs in the public sector.

Affordability

Affordability of essential drugs which can be termed as access to drugs is a foremost

element of the right to health for the implementation of many other rights in

specifically the right to development, and essential for living a life in dignity. According

to the human rights perspective by ‘United Nations High Commissioner for Human

Rights’ (OHCHR), access to medicines is naturally linked with the ideologies of ‘non-

discrimination and equality, involvement, transparency and accountability’. National

health systems consist that states are obliged to strengthen their nation by developing

national health legislation and policies. For this purpose, key issues related to access

to medicines must be taken into account such as sustainable financing, affordability of

11%

25%

18%

20%

19%

7%

Figure: 4.1 Availibility of Essential drugs in Public Sector

Injections ( 11%)

I.V Fluids (25%)

Eye/Ear/Nasal Drops(18%)

Tablets and Capsules(20%)

Solution, Creams,Applications (19%)

Syrup/ Suspension (7%)

31

essential drugs, price and quality control, dosage and efficacy of drugs, procurement

practices and procedures, supply chains, etc.

One method to measure the affordability is used given in the WHO/HAI methodology.

This comparison is given to the ordinary people, i.e. lowest paid unskilled government

worker. This is measured by comparing the treatment cost with the wages they earn.

The salary of the lowest paid government worker is identified by the government

source. It determines the number of days of wages required by this worker for

purchasing medicines for a standard duration of treatment for a common condition.

The wage rate in Bathinda of the lowest paid unskilled government worker is Rs.

219.20 on the daily basis. The lowest paid unskilled worker in the private sector or

unorganized sector could be earning more or less.

The second method is used to determine the affordability, by considering the number

of poor people. In Punjab, according to Tendulkar methodology (2011-12) the

population below poverty line is 7.66 percent in rural areas, 9.24 percent in urban

areas and 8.26percent overall which means no. of persons are 23.18 (lakhs). Punjab

state has poverty lines limit in monthly per capita (RS) 1,054 for rural and 1,155 for

urban. This means 35.13 Rs per day in rural and 38.5 in urban areas. So the

affordability of the essential medicines for 23.18 (lakhs) people is very low in Punjab.

The poverty status in the district Bathinda 32141 families are living below the poverty

line in addition to 6491 families in even more miserable conditions i.e. having an

income equal to half of the BPL families, thus making a total of 38632 families in all in

the BPL category. In the profile of city Bathinda 5177 families are living below the

poverty out of which 1093 families having the status of the poorest of the poor and

4084 families are poor who have less than Rs 47 per day spending.(2011-12) Even

the treatment cost of minor health problems is burden for these poor people. The

essential drugs surveyed have calculated the treatment cost both in public and private

sector by daily dose and duration of days for treatment.

32

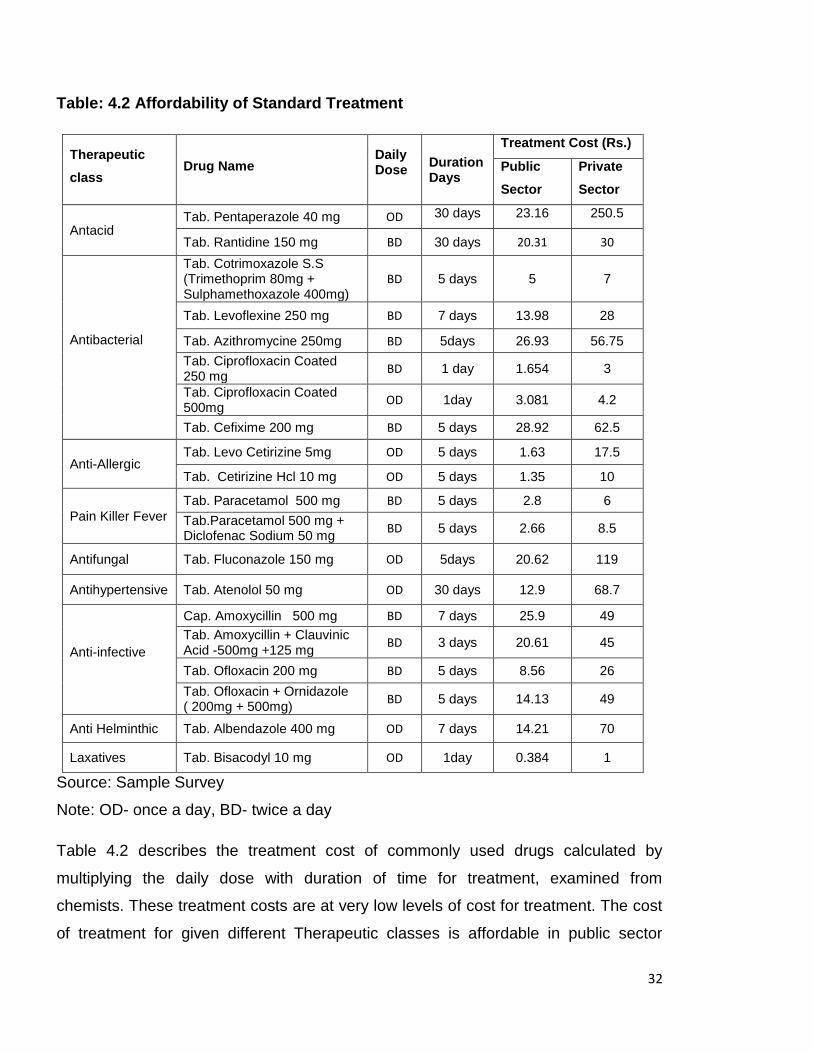

Table: 4.2 Affordability of Standard Treatment

Therapeutic

class Drug Name

Daily Dose

Duration Days

Treatment Cost (Rs.)

Public

Sector

Private

Sector

Antacid Tab. Pentaperazole 40 mg OD 30 days 23.16 250.5

Tab. Rantidine 150 mg BD 30 days 20.31 30

Antibacterial

Tab. Cotrimoxazole S.S (Trimethoprim 80mg + Sulphamethoxazole 400mg)

BD 5 days 5 7

Tab. Levoflexine 250 mg BD 7 days 13.98 28

Tab. Azithromycine 250mg BD 5days 26.93 56.75

Tab. Ciprofloxacin Coated 250 mg

BD 1 day 1.654 3

Tab. Ciprofloxacin Coated 500mg

OD 1day 3.081 4.2

Tab. Cefixime 200 mg BD 5 days 28.92 62.5

Anti-Allergic Tab. Levo Cetirizine 5mg OD 5 days 1.63 17.5

Tab. Cetirizine Hcl 10 mg OD 5 days 1.35 10

Pain Killer Fever Tab. Paracetamol 500 mg BD 5 days 2.8 6

Tab.Paracetamol 500 mg + Diclofenac Sodium 50 mg

BD 5 days 2.66 8.5

Antifungal Tab. Fluconazole 150 mg OD 5days 20.62 119

Antihypertensive Tab. Atenolol 50 mg OD 30 days 12.9 68.7

Anti-infective

Cap. Amoxycillin 500 mg BD 7 days 25.9 49

Tab. Amoxycillin + Clauvinic Acid -500mg +125 mg

BD 3 days 20.61 45

Tab. Ofloxacin 200 mg BD 5 days 8.56 26

Tab. Ofloxacin + Ornidazole ( 200mg + 500mg)

BD 5 days 14.13 49

Anti Helminthic Tab. Albendazole 400 mg OD 7 days 14.21 70

Laxatives Tab. Bisacodyl 10 mg OD 1day 0.384 1

Source: Sample Survey

Note: OD- once a day, BD- twice a day

Table 4.2 describes the treatment cost of commonly used drugs calculated by

multiplying the daily dose with duration of time for treatment, examined from

chemists. These treatment costs are at very low levels of cost for treatment. The cost

of treatment for given different Therapeutic classes is affordable in public sector

33

comparing the private sector. It can be affordable to those who earn enough for the

surviving the basic needs but not affordable to those who lives the life with very low

income or below poverty line. These costs are also affordable for the ordinary people

defined in WHO/HAI methodology which are lowest unskilled government workers

because they earn wages Rs. 219.20 per day and the treatment cost of these

common drugs is slightly affordable, but the wages in unorganized sector of unskilled

workers are lower than the public sector and the 5177 families which are poor having

less than Rs. 47 per day spending has never afforded the treatment costs in the

private sector, and have difficulty to pay the treatment cost in the public sector. The

conclusion of the affordability issue is the treatment of these diseases are affordable

for only the higher income or slightly for the people employed in the government

sector, drugs are not affordable for the low income and or people because these

costs are only included drug costs, other costs as doctor’s consultation fees and

diagnostic tests will likely mean that the total cost to the patient may be considerably

higher.

Drug Prices

Price of any drug is known by MRP printed on the strip of the drug. MRP is the

maximum retail price, which a retailer can charge. Mostly in all of the retail shops the

drugs are sold on this printed price, according to the general phenomena of Indian

market this is identified to charge the printed price, which includes all the costs, such

as manufacturing, distributing, taxes etc. and the consumers also give the opinion