Embed Size (px)

Citation preview

Changes, problems and challenges ofaccounting education in Libya

NASSR S. AHMAD and SIMON S. GAO�

Napier University Business School, Edinburgh, Scotland, UK

Received: June 2002

Revised: February 2003; May 2003

Accepted: September 2003

Abstract

While accounting education has existed in Libya for over 45 years, knowledge about it is scarceamong Western accounting academics. This paper reports the development of accountingeducation and curricula since Libya’s independence in the 1950s and examines its currentproblems during a decade of United Nations (UN) sanctions. Following an introduction to theaccounting profession in Libya, the paper provides an overview of the changes to accountingeducation since 1957 and analyses major issues currently faced by Libyan accounting educators,including: a shortage of qualified accounting academics; inappropriateness of imported syllabusesto the peculiarities of the economy; the unfit marriage of academic teaching and professionaltraining in the accounting curricula; and inadequate accounting research. The paper concludes thatsocial and economic characteristics must be fully taken into account in the case of Libya inimporting accounting education systems from the West.

Keywords: accounting education, accounting profession, accounting research, curriculum, Islamicaccounting, Libya

Introduction

Accounting is very important for not only market systems, but also other forms of economic

systems (American Accounting Association (AAA), 1978). Accounting and accountants have

played a very important role in Muslim societies since the Middle Ages (Zaid, 2000).

Despite accounting education having existed in Libya for over 45 years, very few studies of

the issues it entails have been conducted. Knowledge of the subject is generally scarce among

Western accounting educators because, as far as the authors are aware, the only major study pub-

lished in a Western journal was Bait-El-Mal et al. (1973), which has been overtaken by signifi-

cant changes in social, political and economic systems over the last three decades. Indeed, while

a few Libyans in the West have produced PhD theses concerning accounting in Libya (e.g.,

Kilani, 1988; Bakar, 1997; Buzied, 1998), it appears that this broader subject area is also

largely overlooked in the Western literature.

The aim of this paper is to bring this deserted area to the attention of Western academics by

reporting the development of accounting education in Libya, analysing the changes of accounting

�Address for correspondence: Professor Simon S. Gao, School of Accounting and Economics, Napier University

Business School, Napier University, Sighthill, Edinburgh EH11 4BN, Scotland, UK. E-mail: [email protected]

Accounting Education 13 (3), 365–390 (September 2004)

Accounting EducationISSN 0963-9284 print/ISSN 1468-4489 online # 2004 Taylor & Francis Ltd

http://www.tandf.co.uk/journalsDOI: 10.1080/0963928042000273825

curricula since the 1970s, and highlighting some contemporary issues in Libya’s accounting edu-

cation. The rest of the paper is organized as follows: the next section provides a brief review of the

Libyan context. The third section is devoted to background information on the status of the

accounting profession. The fourth section reports the accounting education system covering pro-

fessional education and university-level education, and compares the curricula under two eras with

a view to understanding the change in accounting education over time. The fifth section provides

an analysis of current problems of accounting education. Finally, a conclusion is presented.

Libyan context

Libya is a developing Arab state located in the north-central part of Africa. Islam is the state

religion and about 97% of Libyans are Sunni Muslim. The country occupies an area of

almost 1.8 million square kilometres with a population of 5.5 million (Central Bank of Libya,

2001b). Arabic is the official language, while English and Italian are also used in business

and trade. The Libyan social environment is characterized by the extended family, clan, tribe,

village and Islamic religion. These play a major role in the community’s life and people’s

relationships (Agnaia, 1997). The economy of Libya is unique in many aspects, accompanied

by peculiar characteristics of its political regime.

The Great Socialist People’s Libyan Arab Jamahria (GSPLAJ) is the official name of Libya.

The GSPLAJ was established according to the ‘Third Universal Theory’ of the Green Book by

Colonel Muammar Al Qathafi (1981).1 The alteration from a monarchy to the present system

began when it became the Libyan Arabic Republic following the Fatah Revolution on 1 Septem-

ber 1969. Several actions (e.g., nationalizing foreign companies that were operating in Libya,

and establishing public-owned enterprises) were taken by the new administration to restructure

the economy. The private sector and foreign companies disappeared and a wide range of

public-owned enterprises were formed (Kilani, 1988). In the spring of 1972, a new political,

administrative and legislative system was introduced as part of the People’s Revolution,

which established a socialist state, to be governed only by the people. After the Declaration

of the People’s Authority in 1977, Libya became a ‘State of the Mass’ or a Jamahria.

The Libyan economy, like that of other Arab states, was agriculture-based until not long ago. In

the early 1970s, the government began a drive for economic development (Agnaia, 1997). Over

the past 30 years, the expansion in the hydrocarbon sector has driven the country’s economy,

with the contribution of oil to GDP at over 50% in the 1970s and early 1980s. While the

economy has largely depended on oil as the main source of wealth, the country has allocated a

large amount of money to establishing industrial companies in non-oil sectors over the last two

decades, following the government’s Development Plans2 of 1980. Thus, the non-oil sectors

increased significantly, contributing over 70% of GDP. Nevertheless, the country still faced

difficulty in being able to produce enough capital goods and consumer goods to achieve ‘self-

sufficiency’ and ‘self-reliance’ (Agnaia, 1996). These trends are evident from Table 1.

The country’s socialist philosophy has affected the economy largely in terms of the ownership of

a business and controlling of business objectives. Libyan industrial companies are predominantly

1The Green Book is a political work edited by Colonel Muammer al Qaddafi, the leader of Libya, covering pol-

itical, economic and social problems and solutions in Libya. The book has been used widely in Libyan society as

the solution guidance. Earlier versions were published in Arabic. The English version was published in 1981.2The objective of the development plans was to achieve 10.3% annual growth of the non-oil sector and 17.2% for

the whole economy (Secretariat of Planning, 1980, p.57).

366 Ahmad and Gao

Table 1. Libyan GDP by the industrial sectors 1970–1999 (millions LD: 1LD ¼ US$1.64)

Economic sectors 1970 1971 1977 1980 1986 1991 1995 1999

Agriculture and fishing 33 33 90 183 320 678 947 1547Petroleum and gas 813 923 328 6571 1784 3054 2468 3254Mining and quarrying 17 8 29 49 49 73 149 215Manufacturing 23 25 125 192 402 706 800 944Electricity and water 6 7 26 50 112 177 217 269Construction 88 117 602 936 895 1320 484 738Trade, restaurants and hotels 47 47 292 490 486 1042 1254 1966Transport and communication 43 87 220 356 396 812 893 1276Banking and insurance 13 29 144 246 285 371 286 476Ownership of housing 60 69 157 210 252 315 391 507General services 98 135 362 611 920 1031 823 1239Education services 40 47 173 221 388 534 736 927Health services 16 22 80 115 214 331 294 488Other services 8 9 37 47 75 172 308 440Total GDP 1288 1587 5613 10 277 6577 10 615 10 049 14 286Petroleum and gas (%) 63.1 58.2 58.4 63.9 27.1 28.8 24.6 22.8Other sectors (%) 36.9 41.8 41.6 36.1 72.9 71.2 75.4 77.2

Source: Central Bank of Libya (1994, 1995, 1998, 2001a); Ganous et al., (1994, 1999).

Acco

un

ting

edu

catio

nin

Lib

ya3

67

owned by the state, and controlled and supervised by government institutions. While those enter-

prises are financed in different ways in relation to their activity, nature and objective, most of

them have received their funding (e.g., launching grant) from the government. Currently, there

are over 190 large public enterprises (Libyan Commercial, Industrial and Agricultural Chamber

(LCIAC), 2002). The main objective of those enterprises is to offer services and goods to the

public rather than to make a profit. Based on the state socialist philosophy, employees were given

the right to set up self-management in their enterprises. Most companies are currently managed

by people’s committees; each committee has the responsibility of running the business and achieving

all the enterprise’s objectives. The people’s committees are also required to implement all the finan-

cial regulations and control (including accounting activities), to follow all the instructions and guide-

lines provided by their relevant secretariats (ministries), and provide these secretariats with all

reports (including annual reports) and information they demand. All companies are required to

prepare annual reports including income statements and balance sheets. The government has total

authority over, for example, imports or exports of a company and even the company’s location.

Many senior appointments to Libyan companies are in the hands of politicians and civil servants.

As a result, Libyan companies, as public enterprises, are very sensitive to any change in the govern-

ment’s policies regarding economic, political and social issues (Agnaia, 1997). The central authority

often directs companies’ day-to-day operations in the areas of organizational structure, location or

site, responsibilities, authorized budgets, employment conditions and management appointments.

In 1992, Law No. 9 on partnerships provided a new basis for individuals to engage in manufac-

turing, agriculture, professional service and other ventures as sole owners or in partnerships,

leading to the emergence of private businesses. Moreover, in 1997, Law No. 5 relating to encoura-

ging foreign capital investment was enacted by the General People’s Congress (GPC) (the highest

legislative authority in Libya) for the purpose of attracting foreign investments and accelerating

social and economic development. In line with the implementation of ‘the Development Plans’

of 1980, the emergence of a private sector, the growth of foreign investment and the effect of glo-

balization, there is a strong demand for change to accounting and accounting education.

Although the Libyan economy is not considered a market economy per se, accounting has

played an important role for over a half century. Resource allocation, monitoring social and

economic development plans and the establishment of the product pricing system all depend

on accounting information (rather than the mechanism of market forces). The users of account-

ing information are predominantly the state and state agencies. This is fundamentally different

from the Western market economies where private investors and creditors are among the major

users of accounting information.

Management training and development programmes have been established to achieve more

independence and self-sufficiency of the national economy under the Development Plans of

1980. Accounting education has received considerable attention and the size of the provision

of accounting education has largely expanded since the 1980s. Indeed, the recent economic

expansion has resulted in a growing demand for both qualified accountants and reliable account-

ing information. However, there are only 1369 qualified and partially-qualified accountants in

Libya (Libyan Association of Accountants and Auditors (LAAA), 2002). For a country with

a population of over 5.5 million, clearly, there is an acute shortage of qualified accountants.

The accounting profession in Libya

The links between accounting education and the domestic accounting profession are usually

determined by the development of the latter (Enthoven, 1981; Gao, 1995). Mature accounting

368 Ahmad and Gao

professions in developed countries have significantly influenced their accounting education

(Puxty et al., 1994; Melancon, 1998; Ainsworth, 2001). However, the accounting profession

in developing countries has been considered weak (Wallace, 1990; Wallace and Briston,

1993). Libya as a developing country is no exception. As a result, the influence of the profession

on accounting education is trivial.

Up to Libya’s independence in 1952,3 there was no domestic accounting profession and most of

the business firms depended upon foreign accounting firms from Italy and the UK (Bait-El-Mal

et al., 1973). No formal accounting education or training was available locally, and so, when inde-

pendence came, there was even a shortage of personnel to fill clerical and technical positions in the

administrative and public services. This was one of the country’s most serious handicaps and

meant that, throughout the 1950s, it relied greatly on advisors from the UK, USA and UN to estab-

lish rudimentary accounting systems. Indeed, at that time, many foreign agencies from the UK and

the USA (e.g., the Libyan Public Development and Stabilisation Agency, the Libyan American

Reconstruction Commission, the Libyan and American Joint Service) flooded into the country

to carry out various projects. These agencies were all administrated by non-Libyans and,

through them, the British and Americans implemented their own accounting models, significantly

influencing the accounting system (Buzied, 1998).

The discovery of oil in the early 1960s provided the country with financial resources to develop

business activities leading to a significant growth of the economy. Accordingly, there were increas-

ing needs from investors, creditors, business managers and governmental agencies for financial

information and resultant accounting services. Subsequently, many foreign accounting firms

from Egypt, the USA and the UK opened branches in Libya, predominantly providing audit ser-

vices. Following the People’s Revolution and the major transformation of the country’s political

system, Libya moved away from the UK and USA colonial system of recognizing and producing

professional accountants by putting a strong emphasis on university education and qualifications.

Similar to other countries, such as Singapore (Tan et al., 1994; Wijewardena and Yapa, 1998),

Libya accredited a university degree as an adequate qualification for professional recognition

without requiring further examinations, subject only to acquiring practical experience. In the

1970s, with the increase of accounting graduates from the University of Libya and the return of

many Libyan graduates from abroad, many Libyan-run accounting firms were established.

As a result of the increase of accounting firms in both number and size, and the lack of regu-

larity in accounting and auditing standards and practices, there was an urgent need to set up a

professional body, to take the responsibility for developing a general framework of accounting.

To meet the demand, Law No. 116 was enacted in 1973. This is the first law to govern accoun-

tancy and related areas. It covers: (1) the establishment of the LAAA; (2) registration of accoun-

tants; (3) exercise of profession; (4) fees; (5) pension and contribution fund; (6) obligations of

accountants and auditors; (7) penalties; and (8) general and transitional provisions. The LAAA

was established in June 1975 with the following objectives:

. to organize and improve the conditions of the accounting profession and to raise the stan-

dards of accountants and auditors professionally, academically, culturally and politically;

. to organize and participate in conferences and seminars related to accounting internally and

externally and to keep in touch with new events, scientific periodicals, lectures and so on;

3Before the country’s independence, the colonizers (Turkey from 1551 to 1911, Italy from 1911 to 1943, and Britain

and France from 1943 to 1952) were responsible for running the country’s affairs and implemented their laws.

Accounting education in Libya 369

. to establish a retirement pension fund for its members;

. to increase co-operation between its members and to protect their rights; and

. to take action against members who violate the traditions and ethics of the profession.

In addition to the LAAA, the State Accounting Bureau (SAB) has also played a key role in the

development of an accountancy profession. The SAB was established by the Law No. 31 of 1955

under the responsibility of the Ministry of Treasury. To guarantee its dependence, the SAB

became responsible directly to the whole Ministries’ Council of Libya under the Audit

Bureau Law of 1966. The Revolutionary Government of 1969 changed the government structure

to consist of an executive branch and a legislative branch represented by the Revolutionary

Command Council (RCC). Accordingly, the SAB was changed under Law No. 79 of 1975 to

become responsible directly to the RCC.4 Article No. 1 of the SAB Law of 1973 states the inde-

pendence and objectives of the Bureau as follows: the SAB is an independent agency affiliated to

the RCC; its purpose is to apply effective control over the public funds. Since the RCC trans-

ferred its authority to the GPC in 1977, the SAB has become responsible directly to this new

legislative body.

Following the Law No. 7 of 1988, the SAB was combined with the Central Institute for General

Administration Control. The new body was initially called the Institute for Public Follow-Up but

in 1996 was renamed as the Institute of Public Control (IPC). Initially, it was responsible for audit-

ing all the state agencies, departments, organizations aided by or in receipt of loans from the gov-

ernment and any other corporations to which the state contributes more than 25% of the capital.

The purpose of the audits was to ensure that these organizations were running according to the

financial regulations and guidelines set up by their relevant secretariats (ministries) and meeting

the social and economic objectives. The IPC’s responsibilities have been extended to include

the auditing of foreign companies and joint ventures operating in Libya, with the purpose of ensur-

ing that these companies operated in accordance with Libya’s laws and regulations. Although there

are legal requirements for the auditing of these enterprises, no specific guidelines for carrying out

such audits are given by the authorities. The audit process and administration are largely subject to

the rules set by the IPC in line with the existing economic policy, regulations and Libyan laws. Due

to a dearth of staff, the IPC was not able to complete its task on time and the delay in the auditing of

the accounts of the above organizations has become a serious problem. Consequently, much audit-

ing of state enterprises’ reports has had to be outsourced to public accountants, which in turn

increased the demand for qualified public accountants.

The primary professional qualification of accountancy in Libya is membership of the LAAA.

Table 2 shows the numbers of registered members in 2002. Accountants who want to qualify as

members must meet the following requirements:

. Hold Libyan nationality

. Have a bachelor’s degree in accounting

4The general broad function of the SAB, as stated in the law No. 79 of 1975, is to exercise effective control over

public resources. In order to undertake its responsibilities, the SAB performs four main tasks: (1) post-audit of

government revenues; (2) post-audit of government expenditures; (3) pre-audit of government obligations; and

(4) reporting of audit findings. Particularly, according to part 2, article 18, of the Law No. 79 of 1975, the

SAB is responsible for the examining and auditing of the accounts of the state, organizations and public agencies.

In addition, the SAB is responsible for auditing government-owned companies and any account or entity assigned

for government audit by the RCC.

370 Ahmad and Gao

. Have five years experience of accountancy-related jobs in an accounting office after

obtaining the bachelor’s degree

. Be active over political and civil rights

. Be of good conduct, reputation and respectability, commensurate with the profession.

An accountant who has a bachelor’s degree in accounting without experience and intends to

practise accountancy may be registered as an assistant accountant in practice. During the first

two years, an assistant accountant can practise in the profession by joining a firm of accountants.

After two years of experience, an assistant accountant has the right to practise in the profession

in his area with some limitations. He may only certify (a) accounts and balance sheets of firms

with no shares; (b) audit and certify accounts of taxpayers who are subject to taxes on incomes

from commerce, industry and independent professions whose capital does not exceed 20 000 LD

(US$32 800) or whose annual net income does not exceed 5000 LD (US$8200); and (c) audit

and certify accounts of taxpayers who are subject to general tax on income and whose

revenue does not exceed 10 000 LD (US$16 400). Other registered accountants who have a

bachelor’s degree in accounting with no practice experience and do not intend to practise in

the profession are listed in the register of assistant accountants not in practice. Accountants

who hold a degree higher than a bachelor’s degree in accounting are exempt from the experience

requirement if the higher degree requires four or more years of study and training.

Accountants who are registered in the list of accountants in practice have the right to certify

accounts and balance sheets of all types of firms and taxpayers. Accounting firms in Libya,

which are required to be licensed by the LAAA, can offer services in such areas as preparing

financial reports, auditing, tax services, bankruptcy, management consulting, system design

and installation. Because of a shortage of expertise and experience in many service areas,

along with low demands from companies and organizations for other services, most of the

public accountants are predominantly occupied in auditing and preparing financial reports.

Other services are seldom provided (Buzied, 1998).

The secondary professional accounting qualification available in Libya is membership of the

IPC. An accountant who wants to qualify as a member must meet the following requirements:

. Hold Libyan nationality

. Have a bachelor’s degree in accounting

. Have five years of accountancy experience in the IPC

. Be active over political and civil rights

. Be of good conduct, reputation and respectability, commensurate with the profession;

and swear to do work with complete honesty and sincerity.

Table 2. Registered accountants in the Libyan Association of

Accountants and Auditors in 2002

Types of membership Number

Accountants in practice 945Assistant accountants in practice 307Assistants who are not in practice 117Total 1369

Source: LAAA (2002).

Accounting education in Libya 371

Just as admittance to full membership of the LAAA and the IPC does not require any study

beyond a bachelor’s degree, only practical experience, so, after becoming a member of the

LAAA, no continuing professional training is required. For this reason, accounting firms nor-

mally do not conduct any training programmes for their accounting staff. These circumstances

bring the competence of Libyan professional accountants into question, on the basis of Dewing

and Russell’s (1998) contention that competence in accounting is ultimately recognized not only

by completing a period of ‘apprenticeship’ but also by passing the examinations of a pro-

fessional accountancy body; possession of a university degree in accounting is insufficient. Simi-

larly, Annisette (2000) argues that ‘professional education, examination and certification play

important roles in demarcating and defining the boundaries of a profession both in terms of

its membership and in terms of its knowledge-base’ (p.654). Doubts about the capability of

Libyan universities to offer accounting programmes that can meet the dual objectives of attain-

ing both academic scholarship and professional competence, which arose when Libya moved

away from professional education and examinations following the 1969 Revolution, are dis-

cussed below.

Regarding how professional accountants practice, business accounting and reporting is influ-

enced, first, by regulatory and institutional frameworks that consist of rules, regulations and

institutions inherited from the American, British and Italian periods (Bait-El-Mal et al., 1973;

Kilani, 1988), and included in the 1953 Libyan Commercial Code (LCC); and, second, by

prevailing income tax law. Although the LCC has been partially modified from time to time

to meet the changing needs of society, the accounting systems and reporting methods in use

in Libyan companies reflect those passed down by the country’s former colonial masters

(Buzied, 1998). Under the LCC, all companies are required to prepare an annual report, includ-

ing an income statement and a balance sheet, but there is no formal set of Libyan accounting

standards about the form and content of the annual reports, nor any requirements about

what foreign accounting principles and standards should be adopted (Bait-El-Mal et al., 1973;

Kilani, 1988; Buzied, 1998). Thus, significant differences arise in the ways in which accounting

principles, rules, methods and procedures are applied within different companies, even ones in

the same industry. The variety of accounting practices causes enormous problems for accounting

education in trying to fulfil the dual objectives enumerated above and discussed in the next

sections.

Accounting education in Libya

During the 400 years that Libya was a colony of various powers there was little education pro-

vision. When independence came in 1952, more than 90% of the population was illiterate; very

few Libyans had studied at university level or qualified as professional accountants. A general

education system from primary level to university level was established, and included account-

ing education. As in other areas, Libya relied heavily on advisors from Britain, American and the

UN to implement this system, and so, much was imported from the first world (International

Bank for Reconstruction and Development, 1960; Stanford Research Institute, 1969; Kilani,

1988; Buzied, 1998). This is reflected in the system now which, as shown in Table 3, is

broadly divided into four levels, namely pre-school, fundamental education, middle education

and training, and higher education.

Initially, accounting education focused entirely on the intermediate level (pre-university),

with the establishment of the first School of Public Administration in 1953, aim of which was

372 Ahmad and Gao

to develop graduate clerks and book-keepers (Buzied, 1998). Accounting education at university

level started in 1957 with the establishment of the Accounting Department in the Faculty of

Economics and Commerce at the University of Libya (now called Garyounis University)5

(Kilani, 1988; Bakar, 1997; Buzied, 1998). Thus, the accounting education system after indepen-

dence is divided into two levels: pre-university and university levels. This section investigates

these two levels with more attention being given to the latter. The analysis of the university level

is based on the old (1957–1976) and new (since 1976) accounting programmes of Garyounis

University. However, before dealing with that it is useful to explain skill and competency

requirements within the Libyan social, political and economic context.

Skill and competency requirements

Fundamental principles and standards with respect to competencies, skills, and learning and

development have been proposed by the International Federation of Accountants (IFAC).

The International Education Guideline No. 9 defines the goal of accounting education as

producing ‘competent professional accountants capable of making a positive contribution

over their lifetime to the profession and society in which they work’ (IFAC, 1996, para. 1).

It emphasizes ‘the need to maintain professional competence in the face of the changes

that accountants increasingly encounter and requires that an attitude of learning be developed

and maintained’ (para. 1). IFAC defines competence as ‘. . . the ability to perform the tasks

and roles expected of a professional accountant, both newly qualified and experienced,

to the standard expected by employers and the general public’ (para. 3). Furthermore

international educational standards for professional accountants covering general education,

professional skills and experience requirements have been issued in 2003 (IFAC, 2003).

Although circumstances in Libya differ from the West, the above fundamental principles

and standards can be applied. The functions of accounting are increasingly similar to those

in Western economies, following the recent growth of the private sector, the changing of

business environments and the increasing influences of globalization. The complexity of the

economy (because of the expansion of the non-oil sectors) means that accounting is increas-

ingly recognized as an important part of management and control, and can be used to manage

the economy more effectively. Even within the state-owned sectors, under the system of

people’s committees, the growing demand for state (or social) accountability, in respect of

Table 3. Libya’s education levels

Pre-school Fundamental

Middle educationand training

(pre-university level) Higher education

Age 4–5 Primary (age 6–12) Secondary (age 16–18) University (age 19þ)Preparatory (age 13–15) Technical (age 16–18)

Colleges (age 16–18)

5The University of Libya was founded in Benghazi in 1957, with a branch in Tripoli. In 1973, the two campuses

became the Universities of Benghazi and Tripoli, and in 1976, they were renamed as Garyounis University and

El-Fatah University.

Accounting education in Libya 373

both economic and social performance, requires a broad role to be played by professional

accountants, not only recording and reporting business activity and performance at the enter-

prise level, but also improving macro-control and implementing the state’s social and econ-

omic plans. Professional accountants must incorporate the state’s national economic policy

into their practice and place an emphasis on the implementation of the laws, regulations

and economic policies of the state. These wide functions require accountants to possess profes-

sional competencies and broad skills, and be able to make ‘a positive contribution over

their lifetime to the profession and society’ (IFAC, 2003, p.27). Professional accountants are

therefore required to possess a range of skills, ‘including technical and functional skills,

organisational and business management skills, personal skills, interpersonal and communi-

cational skills, a variety of intellectual skills and skills in forming professional judgements’

(IFAC, 2003, p.52).

Accounting education programmes should prepare students to become professional accoun-

tants, not to be professional accountants (Flaherty and Diamond, 1996). Deppe et al. (1991)

suggest that accounting education needs to provide an opportunity for students to develop com-

petencies in seven areas: (1) communication skills, (2) information development and distribution

skills, (3) decision-making skills, (4) knowledge of accounting, auditing, and tax, (5) knowledge

of business and environment, (6) professionalism, and (7) leadership development. In the

context of Libya’s social and economic system, these skills and competencies can be explained

as follows.

1. Communication skills – to be able to communicate accounting information effectively

with various stakeholders of enterprises (the government and public agencies, the IPC,

employees, people’s committees, the general public including religious groups, consu-

mers, suppliers, etc.).

2. Information development and distribution skills – to be able to collect, select and

collate information and data, prepare financial accounts and statements, and report

them and other accounting information to the government, public agencies and other

users, within required time limits.

3. Decision-making skills – having adequate skills to analyse business environments and

compare business options and consequences; to plan business and financial strategies;

and to make decisions for a given objective and environment.

4. Knowledge of accounting, auditing and tax – understanding the principles and prac-

tices of accounting, auditing and tax, and being able to follow and initiate the advance-

ment of these areas within their professional field.

5. Knowledge of business and environment – understanding the complexity and oper-

ations of business, and how business and social, political and economic environments

interact; and being able to adapt to the changes in business and its environment.

6. Professionalism – following principles of conduct generally associated with, and

deemed essential in, defining the distinctive characteristics of professional behaviour,

in the interests of the state and the mass, and for fostering state (or social) accountabil-

ity; being capable of incorporating the state’s national economic policy into practice;

and placing an emphasis on the implementation of the laws, regulations and economic

policies of the state.

7. Leadership development – pursuing role models within society and the organization,

based on participation, responsibility and spiritual authority; and showing personal

commitment to the values and goals established in the organization and society.

374 Ahmad and Gao

Pre-university level

Pre-university level academic education extends over 3–4 years of study. It is subdivided into

general baccalaureate, specialized baccalaureates, technical and vocational institutes and

centres. This level of education is made up of over 30 commercial institutes, colleges and

secondary commercial schools. Most of them were established to meet the increasing demand

for bookkeepers, accountants, clerks and secretaries for both governmental and private

sectors. Students must complete the third part of fundamental education before they can study

at these institutions. The diploma programmes they offer normally last three years and have

common core accounting subjects (e.g., fundamentals of accounting, cost accounting,

governmental accounting, insurance and bank accounting, principles of auditing, and taxation

accounting), complemented by subjects in other areas of business (e.g., principles of economics,

statistics, mathematics of finance, methods of commerce and typewriting by computer in Arabic

and English languages). In addition, the programmes require other subject knowledge, such as

religion, and Arabic and English languages.

University level

Since its inception in 1957, the Accounting Department in the Faculty of Economics and Com-

merce at Garyounis University has been the most influential force in accounting education in

Libya. During 1957–1981, it was the only faculty that offered accounting education at the uni-

versity level. The growing demand for accountants and accounting services in the 1980s

increased the need for the provision of accounting education at the higher education level. As

a result, a few other universities also began to offer accounting programmes.6

As a result of the increasing number of accounting departments and degree programmes in

accounting, there was an acute shortage of academic accounting staff. To overcome this

problem, lecturers from different Arabic countries were recruited to teach at these institutions.

In addition, these universities and higher institutes created part-time positions. It was very

common that an accounting department had only one or two full-time lecturers and the remain-

der of the staff were working part-time from other universities or industry. In most cases, the

founding lecturers of these newly-established accounting departments came from the Account-

ing Department of Garyounis University and these newly-established departments have more or

less the same accounting programmes and delivery systems as Garyounis; even textbooks are a

carbon-copy of those used at Garyounis University (Buzied, 1998). For this reason, the remain-

der of this section concentrates to the accounting education programmes offered by the account-

ing department at Garyounis University.

Undergraduate programme

The old accounting education curriculum of 1957–1976 was greatly influenced by the British edu-

cation system, as Libya was administered by Britain during the period 1943–1952, and many Gar-

younis accounting faculty members were educated in the UK before they came to Libya to teach.

The academic year was a nine-month year. A bachelor degree programme was offered over a

period of four years. In the first two years, which were common years for all three departments

6These comprise the Faculty of Economics at El-Fatah University, and the Faculty of Accounting at Al-Jabal Al-

iGarbi University. An additional set of new higher institutes and universities was created in the early 1990s and

many new accounting faculties and departments were opened at Sebha University, Omar El-mukhtar University,

Nasser University, Seventh of April University and Al-Tahaddi University.

Accounting education in Libya 375

in the University’s Faculty of Economics and Commerce, students were required to obtain general

background knowledge of accounting and related disciplines, such as economics, management and

statistics. In the final two years, students focused on a specialist area in one of the departments.

Overall, accounting students had to take 32 courses, distributed as shown in Table 4 (Garyounis

University, 1972). Twelve (almost 40%) were core accounting subjects, six (nearly 20%) were

in the economics area, three (10%) were management-related subjects, and 11 (over 30%) were

divided between statistics, mathematics, law, English language and geography.

A key feature of this course structure was its emphasis on specialized accounting topics and

professional technical expertise. The load given to accounting subjects (40%) was far heavier

than the 27% suggested by the American Accounting Association (Enthoven, 1981) and the

25% suggested by IFAC (Needles et al., 2001). Additionally, the programme devoted inadequate

attention to management accounting and cost accounting, with less than 15% of teaching hours

in accounting subjects specifically for these. The main accounting textbooks used alongside this

curriculum were generally British (e.g., Bigg, 1970) or Arabic, either translated from English or

Table 4. Undergraduate accounting programmes – the old programme (at Faculty of Economics and

Commerce, Garyounis University)

Subjects

Teachinghours per

week Subjects

Teachinghours per

week

First year Second yearAccounting Principles 5 Corporate Accounting

(Partnership and Financial)5

Principles of Economics 3 Production Management 2Management Principles 3 Micro-Economics 2Pure and Financial

Mathematics (1)3 Statistics (2) 2

Statistical and ResearchMethods (1)

2 Pure Mathematics (2) 3

Geographical Economics 2 Principles of Civil Law 2English Language 4 Money and Banking 2Total hours 22 English Language 4

Total hours 22Third year – Accounting Major Fourth year – Accounting

MajorCost Accounting 3 Accounting for Financial and

Insurance Companies3

Taxation Accounting 2 Accounting for Oil and Gas 3Applied Accounting 3 Auditing 3Commercial Law 2 Management Accounting 2Macroeconomics 2 Insurance 2Public Finance 2 Financial Statement Analysis 2Personnel Management 2 Government Accounting 2Libyan Economy 2 Financial Management 2Total hours 18 Research Project 2

Total hours 21

Source: Garyounis University (1972).

376 Ahmad and Gao

written by Arabian writers who graduated from British universities (Kilani, 1988; Bakar, 1997).

The lowest qualification for teaching was a master degree from any officially recognized university

around the world.7 The majority of the accounting faculty up to the early 1970s were Egyptians or

Syrians educated in the UK, with a few Britons, Canadians and Americans. The official language

of teaching was Arabic.

The Garyounis University accounting programme shifted to an American model in 1979,

based on two 16-week semesters instead of a full nine monthly academic year (Garyounis Uni-

versity, 1979). Students are evaluated according to earned credit hours, and are required to earn

123 credit hours in order to graduate, usually over eight semesters. The broad selection of

accounting and non-accounting subjects (164 credit in-class hours) that students choose from

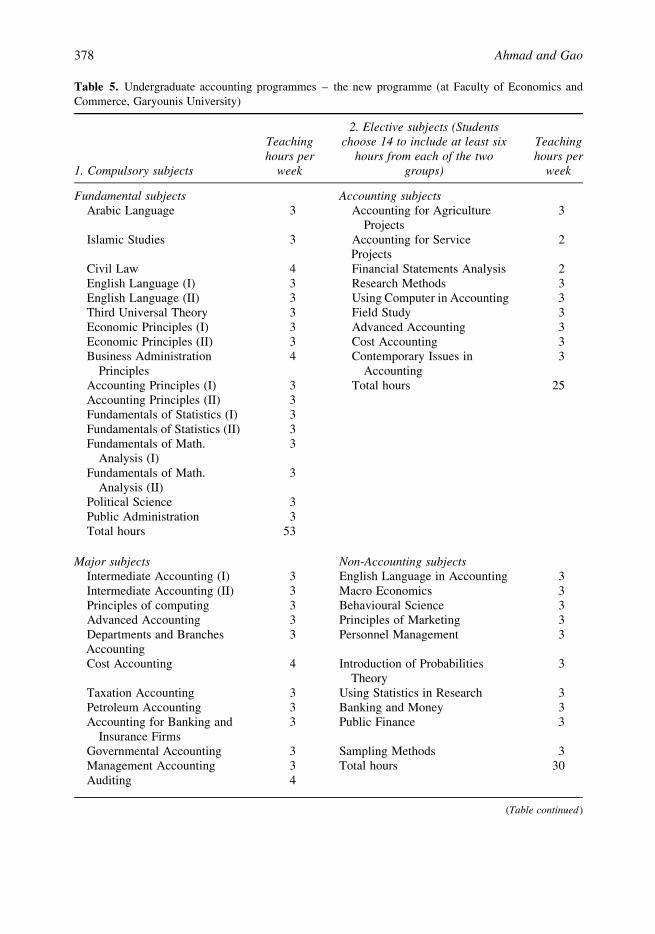

is shown in Table 5. Compulsory accounting comprise 44 credit hours and compulsory non-

accounting subjects comprise 65 credit hours; and elective subjects comprise 14 credit hours,

of which at least six and not more than eight must be in accounting. The main contents of the

accounting subjects are shown in Table 6.

By the early 1980s, the majority of accounting faculty were Libyans who had graduated from

the USA; and most textbooks were either American (e.g., Niswonger et al., 1977; Bodnar, 1980;

Helmkamp et al., 1983), Arabic books translated from American books (e.g., Dou and Domuan,

1983; Al-Hasey et al., 1988; El-Sharif et al., 1995), or written by Arabic authors who graduated

from US universities (Bakar, 1997).

As the old curriculum did, the new programme focuses heavily on financial accounting topics, in

particular on the technical or mechanical aspects of accounting, dealing with external reporting,

taxation and external auditing. This was designed to satisfy the requirement of equipping students

with professional technical expertise, as graduates are expected to perform accountancy jobs

without further professional training. Examining the syllabuses of the accounting programme, it

seems that most of the subjects are based on accounting concepts and principles from the West;

and that they cover many concepts either not known in Libya or which are interpreted differently

there (e.g., profit, interest, cost of capital, market value, prudence, materiality, substance over form,

realization).8 It is also apparent that the syllabuses do not cover some areas or subjects that are con-

sidered to be directly related to the characteristics of Libya. Three important omissions in our view

are accounting under Islamic Shari’a, accounting for the enterprises managed by people’s commit-

tees, and the application and practice of accounting and auditing in the context of state (social)

accountability. The likely reasons for these being missing are that limited research has been

done in the subjects, as discussed in the next section, and the difficulty of incorporating these

areas into the existing ‘Western’ accounting principles and models.

Postgraduate programme

The Department of Accounting at Garyounis University has been offering a master’s programme

since 1988.9 The programme is organized into three components: core subjects, electives and

7For instance, the first three Libyan accounting teachers who joined the accounting department in 1967 had their

master degrees from American universities.8This applies to wider economic indicators. For example, The Economist reported that, when asked, neither

the head of the Libyan Central Bank nor his director of research knew what the country’s inflation rate was

(Anderson, 2001).9The master’s programme has also been offered by the Postgraduate Studies Academy in Tripoli and the Faculty

of Accounting at al-Jabal al-Gharbi University in Gahrian since the 1990s with almost the same textbooks and a

similar curriculum to those of Garyounis University.

Accounting education in Libya 377

Table 5. Undergraduate accounting programmes – the new programme (at Faculty of Economics and

Commerce, Garyounis University)

1. Compulsory subjects

Teachinghours per

week

2. Elective subjects (Studentschoose 14 to include at least six

hours from each of the twogroups)

Teachinghours per

week

Fundamental subjects Accounting subjectsArabic Language 3 Accounting for Agriculture

Projects3

Islamic Studies 3 Accounting for ServiceProjects

2

Civil Law 4 Financial Statements Analysis 2English Language (I) 3 Research Methods 3English Language (II) 3 Using Computer in Accounting 3Third Universal Theory 3 Field Study 3Economic Principles (I) 3 Advanced Accounting 3Economic Principles (II) 3 Cost Accounting 3Business Administration

Principles4 Contemporary Issues in

Accounting3

Accounting Principles (I) 3 Total hours 25Accounting Principles (II) 3Fundamentals of Statistics (I) 3Fundamentals of Statistics (II) 3Fundamentals of Math.

Analysis (I)3

Fundamentals of Math.Analysis (II)

3

Political Science 3Public Administration 3Total hours 53

Major subjects Non-Accounting subjectsIntermediate Accounting (I) 3 English Language in Accounting 3Intermediate Accounting (II) 3 Macro Economics 3Principles of computing 3 Behavioural Science 3Advanced Accounting 3 Principles of Marketing 3Departments and BranchesAccounting

3 Personnel Management 3

Cost Accounting 4 Introduction of ProbabilitiesTheory

3

Taxation Accounting 3 Using Statistics in Research 3Petroleum Accounting 3 Banking and Money 3Accounting for Banking and

Insurance Firms3 Public Finance 3

Governmental Accounting 3 Sampling Methods 3Management Accounting 3 Total hours 30Auditing 4

(Table continued)

378 Ahmad and Gao

a dissertation. It includes five core subjects of accounting and accounting-related subjects, plus a

minimum of three electives from six choices, among which must be at least one from manage-

ment postgraduate subjects, one from economics postgraduate subjects and a dissertation (see

Table 7).

Each subject is taught over 14 weeks in weekly lecture-cum-seminar sessions each of three

hours. The majority of the faculty are Libyans who graduated from the USA or the UK and

most textbooks are either American and British (e.g., Mautz and Sharaf, 1961; Drury, 1983),

or Arabic books translated from American and British books (e.g., Hajaj and Saeud, 1989) or

written by Arabic authors (e.g., Al-Nage, 1992; Holwa, 1992) who graduated from US or UK

universities.

Until now, there has been no PhD programme in accounting in Libya, even though this is con-

sidered very important for the advancement of the accounting faculty and the development of

accounting research. Staff members with a PhD are either foreigners or Libyans who studied

in the USA, UK or elsewhere. The lack of a PhD programme is one of the main factors that

have contributed to the slow development of accounting education and research in Libya.

Problems and challenges in Libya’s accounting education

A major problem with accounting education in Libya is that it is centred on Western accounting

theories that lack validity not only because of the different system of economics and value they

espouse compared to those found in Libya but also because in an Islamic society such as

Libya, the philosophy and institutional framework in which accounting and reporting are prac-

tised is different from those found in the West. It is clear from the previous discussion that the

Libyan accounting education system is strongly influenced by other foreign systems. It was

TABLE 5 Continued

1. Compulsory subjects

Teachinghours per

week

2. Elective subjects (Studentschoose 14 to include at least six

hours from each of the twogroups)

Teachinghours per

week

Accounting Systems Design 3Total hours 41

Non-major subjects (elective)Commercial Law 3Micro Economics 3Production Management 3Financial Management 3Operations Research 3

Total hours 15

Grand total ¼ 164 teaching hours per weekNumber of hours required for graduation ¼ 123 taught hours over eight semesters

Source: Garyounis University (2002).

Accounting education in Libya 379

Table 6. The main contents of some accounting subjects offered for undergraduates at Garyounis

University

Subject Arabic English

AccountingPrinciples (1)

This course covers the definition ofaccounting, the development ofaccounting and its relationshipwith other sciences, generallyaccepted accounting principles,accounting cycle, dataprocessing, journalizing, postingto ledger, the preparation of trialbalance and financial statements,and closing entries.

AccountingPrinciples (2)

This course comprises adjustmentsprocessing and entries, assistantjournals, accounting methods andinternal control system.

IntermediateAccounting (1)

It covers in depth the conceptualframework of financialaccounting, concepts of time-value-of money and theirapplications in accounting, and adetailed study of measurementissues and disclosure of assets(inventory, cash, short-terminvestments, and fixed assets).

IntermediateAccounting (2)

It covers long-term investments, adetailed study of measurementissues and disclosure of liabilities,correction of accounting errors,and changing of prices and itseffects on the financialstatements.

CompaniesAccounting (1)

This course aims to introduceaccounting for partnershipsincluding formation of apartnership, changes in partners,and liquidation of a partnership.

CompaniesAccounting (2)

This course covers: the accountingprinciples used for corporations,such as accounting treatments ofshares, accounting treatments ofstocks, accounting forcorporations including formationof a corporation, liquidation of acorporation; and amalgamation ofcorporations.

(Table continued)

380 Ahmad and Gao

TABLE 6 Continued

Subject Arabic English

Cost Accounting(1)

This course is designed to introducethe student to cost accountingincluding the development of costaccounting and its relation to othersciences, classification of costs,different theories of costs, andaccounting treatments of costelements (materials, labour, andother direct and indirect costs).

Cost Accounting(2)

It includes cost behaviour patterns,the various approaches to costestimation and using ofquantitative models in costaccounting.

ManagementAccounting

It includes the definition ofmanagement accounting,budgeting and variance analysisreports, the relevance conceptin decision making andits application in somedecision (short- and long-termdecisions), and performanceassessment.

Auditing This course is designed to givestudents knowledge about thedefinition of auditing, auditingstandards, planning for audit,evaluating the internal controlsystem, accumulating the relevantamount and quality of evidence,analytical auditing procedures,audit in a computerizedenvironment, statistical models inauditing and auditor’s report.

AccountingInformationSystems

This course includes the basicstructure and principles ofaccounting systems, introductionto both manual and computerizedaccounting information systems,and case studies.

FinancialStatementsAnalysis

It covers the definition of financialanalysis and its importance, thetools and techniques for analysingand interpreting financialstatements.

(Table continued)

Accounting education in Libya 381

TABLE 6 Continued

Subject Arabic English

GovernmentalAccounting

This course aims to teach studentsthe definition of governmentalaccounting and its objectives, itsdifferences from financialaccounting, accounting system inpublic organizations, how toprepare administrative anddevelopment budgets in Libya,and the preparation of domesticproduction statement.

Table 7. Composition of the master’s degree in accounting at Faculty of Economics, Garyounis University

1. Compulsory courses 2. Elective courses

Subjects

Teachinghours per

week Subjects

Teachinghours per

week

Operations Research 3 Accounting subjects (at least 3):Applied Statistics 3 Financial Statements Analysis 3Accounting Theory 3 Social Accounting 3Advanced Management

Accounting3 Applied Accounting 3

Seminars in Auditing 3 Seminars in FinancialAccounting

3

Total hours 15 International Accounting 3Accounting Information

Systems Design3

Taxation Accounting 3Total accounting hours required 9Dissertation 6At least one subject from

management postgraduatesubjects

3

At least one subject fromeconomics postgraduateprogramme subjects

3

Total hours 21Overall hours required to graduate ¼ 36

Source: Garyounis University (1994).

382 Ahmad and Gao

brought mainly from Britain and North America during the latter years of the colonial period

and through the UN after independence. This accords with Yapa’s (2000) finding that almost all

developing countries that have been colonies under powerful Western rulers have inherited their

accounting education from a colonial system. Even if many Western accounting courses intro-

duced into Libya in the past have had a positive impact on students’ knowledge and accounting

practices, these courses, using (translations of) Western accounting textbooks, were not easily

understood by Libyan students. For example, as enterprises in Libya are largely owned and

managed by the masses, the agent–principal problem that has emerged in the West seems

absent in Libya, and so students find it very difficult to understand the agency issues at the

heart of many Western accounting and finance textbooks.

The accounting system in Libya is based on Islamic philosophy and is quite different from the

one prevailing in the West. Under the principles of the Shari’a, which claims the unity of God,

the community and the environment, a form of social accountability is required, rather than the

predominant personal accountability found in Western societies and accounting practices. Thus,

accounting should embody the Islamic principle of full disclosure of accounting information to

serve the objective of state (or social) accountability, rather than what is disclosed and not dis-

closed being the outcome of a political process (Karim, 1995; Baydoun and Willett, 2000).10

This is illustrated in Baydoun and Willett’s comparison of financial reports between the

Western accounting and Islamic systems as shown in Table 8. The state (or ‘the mass’ in

Libya’s political terminology) is the ultimate user of accounting reports, and organizations

must serve the interest of the socialist state (or the mass). Therefore, the accounting profession

(regardless of internal or external functions) has to give priority in how it practises to the state’s

national economic policy, and place a strong emphasis on the implementation of the laws, regu-

lations and economic policies of the state, when they prepare and audit annual reports and

provide accounting services.

Not only have these matters been neglected in the accounting curriculum but also too little

effort is being made to close the gap and align the curriculum to the needs of society and the

economy. We argue that, since the Libyan economic and business systems vary considerably

from those of economies in the first world, simply teaching accounting subjects imported

from the first world is not desirable. Western accounting courses should not be taught mechani-

cally; they must be adapted in accordance with accounting reality of Libya. A further point is

that if the situation was to change, one problem that would arise is that laws, regulations and

policies in Libya are frequently changing, and so accounting teaching materials would require

regular modification. This might be extremely difficult for accounting faculty, as they are

heavily burdened with teaching already because accounting programmes are continuing to

expand. Indeed, we acknowledge that efforts to achieve the fundamental change outlined

above are hampered by a shortage of accounting academics and accounting research (see

below).

10We appreciate the comment by an anonymous reviewer on the similarity of accounting in Libya and the one in

Egypt under Nasser. ‘Both were socialist and Islamic regimes. Egypt had a uniform accounting system with

public sector audit, both external and internal, performed by the National Audit Office. Within such a system

the demand for accounting services is very different from that in a capitalist economy’. Clearly, it would be inter-

esting for international accounting to compare the two accounting systems as suggested by the reviewer. As the

focus of this paper is on accounting education in Libya, however, it would be beyond the scope to give a com-

parison on accounting systems in these two countries.

Accounting education in Libya 383

Another major problem with accounting education in Libya is that the curricula do not offer a

foundation for lifelong learning, which elsewhere is now considered as a fundamental objective

of accounting education. IFAC (1996) stresses that a programme of accounting education and

experience must emphasize a set of knowledge, skills and professional values broad enough

to enable adaptation to change: individuals who become qualified professional accountants

should be characterized by striving constantly to learn and apply what is new. Lifelong learning

is characterized by the notion of learning to learn or self-directed learning, which is defined as

developing skills and strategies that help one learn more effectively and using these effective

learning strategies to continue to learn throughout one’s lifetime (Needles et al., 2001).

However, in Libya, the traditional approach to accounting education is still ascendant, with

the emphasis on the transfer of knowledge, and with learning defined and measured strictly in

terms of knowledge of principles, standards, concepts, facts, and procedures at a point in

time. It seems that both the accounting profession and accounting educators have overlooked

this important element of developing students’ ability to adapt to change. Moreover, there is

no evidence in the curricula of sufficient attention being given to general skills and professional

values as defined by IFAC (1996). The importance of cultivating critical thinking skills, empha-

sized by the IFAC as an essential learning outcome in accounting educational programmes, has

largely been ignored in the design of the accounting curricula.

Three other general areas are frequently identified as problematic in Libyan accounting

education:

. A shortage of qualified accounting academics and educators. Since Libya began her

ambitious development plans in the 1980s, the country has experienced tremendous

Table 8. The differences in Islamic and Western accounting systems

CharacteristicsWestern financial accounting

system Islamic corporate reports

Philosophical viewpoint Economic rationalism Unity of GodPrinciples Secular Religious

Individualistic CommunalProfit maximization Reasonable profitSurvival of fittest EquityProcess Environment

Criteria Based upon moderncommercial law -permissive rather thanethical:

Based upon ethical laworiginating in the Qur’an:(Islamic law, As-Sunnah)

Limited disclosure (provisionof information subject topublic interest)

Full disclosure (to satisfy anyreasonable demand forinformation in accordancewith the Shari’a)

Personal accountability(focus on individuals whocontrol resources)

Public accountability (focuson the community whoparticipate in exploitingresources)

Adapted from Baydoun and Willett (2000, p.82).

384 Ahmad and Gao

changes, an important aspect being the strategic focus on the non-oil sectors. Large

sums have been allocated to establishing industrial companies in these non-oil

sectors. This and other private sector expansion has increased the demand for quali-

fied accountants, as discussed above and, in turn, this has led to an increase of

accounting education programme provision. However, it has not been possible to

recruit enough accounting academics in line with this expanded provision. This short-

age has been worsened since UN sanctions made it almost impossible to recruit from

overseas and for foreign experts to visit and teach in Libya. The sanctions have

made it very difficult for Libyan academics to attend conferences and courses over-

seas that would have been important for staff professional development and academic

advance.

. The unfit marriage of academic teaching and professional training in the accounting

curriculum. Obviously, the designing of a good curriculum plays a crucial role in

any kind of education, accounting education being no exception. A key feature of

Libyan accounting education is its emphasis on technical expertise and techni-

cally-oriented training. As a result, the curricula for accounting students heavily con-

centrate on accounting (mainly bookkeeping and reporting) alone, inter alia,

financial accounting and auditing; there is too much concern with specific accounting

techniques in the curricula; and large numbers of accounting courses focus on

detailed accounting procedures. Although the new curricula have increased the cov-

erage of non-accounting subjects and general knowledge and skills, the coverage is

inadequate, as the curricula would be expected to meet both academic standards and

the needs of professional qualification for the LAAA. It has been argued (e.g., IFAC,

1996) that the changes in accounting education need to meet the dynamically

expanding demands of the profession, and entrants to the accounting profession

should be more broadly educated, including training in basic competence and learn-

ing skills. This will require a switch in focus from one of simply learning a body of

knowledge to one of developing a process of continuing learning. It will also require

accounting classes that focus broadly on information development and dissemination,

not on a narrow definition of accounting (Sundem and Williams, 1992). There is no

evidence that adequate attention has been given to these changes and focuses in

Libya.

. Inadequate accounting research. It is undisputed that accounting research is a power-

ful source of improving accounting practice, teaching and learning, and so is an

important element of accounting education. It can serve as a gateway for a country’s

development in accounting education and the profession. In Libya, accounting

research is almost non-existent, first, because the shortage of faculty means they

have to spend most of their time in the classrooms to deliver programmes; and sec-

ondly, because much effort has been expended on translating Western accounting

writings and textbooks. Technically, most Libyan accounting research has concen-

trated on basic accounting concepts and been limited to qualitative interpretations,

thus fostering some practical applications and deriving some abstract generalizations.

Most accounting researchers (e.g., Dou and Domuan, 1979; Kilani, 1990) have tried

to induce an accounting framework based on the principles of political economy of

the Green Book, antimarket rhetoric and Islamic wisdom. For example, in the paper

entitled ‘Accounting under the Green Book’s Philosophy of the Partners, not Wage

Workers’, Duo and Domuan argue that the principles of Western accounting do

Accounting education in Libya 385

not fit the Green Book’s philosophy.11 They go on to propose what they call the

‘points system’ to distribute income among the partners (workers) rather than

‘wages’. Clearly, the quality of teaching depends on the competence of the faculty,

which in turn hinges on the faculty members’ schooling and communication skills.

Since there is no PhD programme in Libya, most accounting faculty nationwide have

received no schooling beyond a master’s degree.12 As a result, faculty members have

not gained essential research methods and skills. This situation is likely to change as

recently the Libyan government has managed to send many young faculty members

overseas to study for research degrees.

As an isolated developing country under the UN sanctions for a decade, Libya has been facing

great challenges in its accounting education. Obviously, it needs to produce sufficient numbers

of accountants to meet the increasing demand for accountancy from the non-oil industries and

the rise of the private sector. However, the expansion of accounting education programmes at the

university level has been blocked by the shortage of accounting educators who were traditionally

trained overseas.

Moreover, the uniqueness of the Libyan current political, social and economic systems

requires localization of accounting curricula and counts on developing accounting theories to

meet its own characteristics of the ‘mass’ economic system; clearly those curricula and account-

ing theories could not be imported from the first world, or any other country. However, there is no

evidence that such an issue has been considered in the designing of accounting curricula. In

addition, there is a need to establish a proper partnership between the universities and the

accounting profession in order to foster a more effective system of education and training future

accountants; the importance of such a partnership has not been widely recognized in Libya.

Conclusions

The purpose of this paper has been to report on the development of accounting education in

Libya, analysing the changes in accounting curricula since the 1970s and highlighting some con-

temporary issues in Libya’s accounting education. To put this analysis into context, an overview

of the Libyan social, political and economic context and accounting profession was provided.

The paper highlights that the Libyan accounting profession was influenced by British and Amer-

ican accounting standards and practices. The influence came through their owned or managed oil

and non-oil firms operating in the country during the colonial period and through their advisers

11The Green Book states: ‘If we analyse the economic factors of production from ancient times till now we always

find that they are composed of these essentials: raw materials, an instrument of production and a producer. The

natural rule of equality is that each of the factors has a share in this production, for if any of them is withdrawn,

there will be no production. Each factor has an essential role in the process of production and production comes to

a halt without it. As long as each factor is essential and fundamental, they are all equal in their essential character

within the process of production. Therefore, they all should be equal in their right to what is produced. The

encroachment of one factor on another is opposed to the natural rule of equality, and is an attack on the right

of others. Each factor, then, has a share regardless of the number of factors. If we find a process of production,

which can be performed by only two factors, each factor shall have half of the production. If it is carried out by

three factors, each shall have a third of the production’ (Qathafi, 1981, pp. 47–8).12Although some Libyans sent to the USA and UK in the 1970s and 1980s returned with a PhD degree, the number

was very small and has been decreasing. Particularly during the decade of UN sanctions, very few Western

countries granted visas to Libyan students to study.

386 Ahmad and Gao

to Libyan firms and governmental organizations after independence. Such influence was

extended to Libyan accounting education through the use of British education programmes

and textbooks in the period from 1957 to 1976, and American programmes and textbooks

since 1976 (new system). Therefore, the current Libyan accounting education system and

accounting profession are oriented toward the accounting environment and the private sector

of the UK and USA.

In contrast, we have argued that Libyan accounting education and practices should focus on

national information needs and emphasize the use of accounting not only to business enterprises

but also to state and economic development activities. Social and economic characteristics must

be fully taken into account in importing accounting education systems and curricula from the

West. Owing to current economic realities in Libya, accounting practice and education

remain under-developed. We have also highlighted other problematic areas of Libya’s account-

ing education, including the inappropriateness of the syllabuses to the needs of the economy, a

shortage of qualified accounting academics and educators, the unfit marriage of academic teach-

ing and professional training in the accounting curricula, and inadequate accounting research.

Notwithstanding these continuing weaknesses, accounting education has contributed to

training accounting personnel and promoting advances in accounting practice and business

management in Libya. There are now more than ten universities with accounting departments

or programmes and numbers of accounting students have significantly increased over the last

decade. However, as the current economic development plan progresses, the demand for com-

petent accountants will keep growing. To satisfy this growing need, accounting education will

play an even greater role, and so accounting educators face several challenges as alluded to in

this paper. Further wider issues include the UN removing its sanctions, the challenge of world

economic integration and other globalization issues, not forgetting moves to globalize

accounting.

Acknowledgement

The authors are grateful to Rashad Abdel-khalik, Keith Dixon, Gordon Guo, Omneya Abd El-

Salam, Iain Wright, Jane Zhang, Brian Windram, participants at the Accounting and Finance

Research Conference held at Napier University in March 2002 and the two anonymous referees

for their valuable comments and suggestions made on earlier versions of this paper.

References

Agnaia, A.A. (1996) Assessment of management training needs and selection for training: the case ofLibyan companies, International Journal of Manpower 17 (3), 31–51.

Agnaia, A.A. (1997) Management training and development within its environment: the case ofLibyan industrial companies, Journal of European Industrial Training 21 (3), 117–23.

Ainsworth, P. (2001) Changes in accounting curricula: discussion and design, Accounting Education:an international journal 10 (3), 279–97.

Al-Hasey, J., Be Garbeua, S. and Bait-El-Mal, M. (1988) Intermediate Accounting. Benghazi:Garyounis University Publications.

Al-Nage, M. (1992) Studies in Accounting Theory. Egypt: Al-Jala Al-Jeddah Library.American Accounting Association (1978) Accounting Education and the Third World: A report by

the Committee on International Operations and Education. Sarasota, FL: American AccountingAssociation.

Accounting education in Libya 387

Anderson, L. (2001) Muammar al-Qaddafi: the ‘King’ of Libya, Journal of International Affairs 54(2), 515–17.

Annisette, M. (2000) Imperialism and the professions: the education and certification of accountantsin Trinidad and Tobago, Accounting, Organizations and Society 25, 631–59.

Bait-El-Mal, M.M., Smith, C.H. and Taylor, M.E. (1973) The development of accounting in Libya,International Journal of Accounting 8, 83–101.

Bakar, M.M. (1997) Accounting and the economic development of oil and gas in Libya: historicalreview, theoretical analysis and empirical investigation. Unpublished PhD thesis, Universityof Dundee, UK.

Baydoun, N. and Willett, R. (2000) Islamic corporate reports, Abacus 36 (1), 71–90.Bigg, W.W. (1970) Cost Accounting. London: MacDonald and Evans.Bodnar, G.H. (1980) Accounting Information Systems. Boston, MA: Allyn & Bacon.Buzied, M.M. (1998) Enterprise accounting and its context of operation: the case of Libya.

Unpublished PhD thesis, University of Durham, UK.Central Bank of Libya (1994) Economic Bulletin, Vol. 34, 1st Quarter. Tripoli: Research and

Statistics Department.Central Bank of Libya (1995) Economic Bulletin, Vol. 35, 1st Quarter. Tripoli: Research and

Statistics Department.Central Bank of Libya (1998) Economic Bulletin, Vol. 38, 1st Quarter. Tripoli: Research and

Statistics Department.Central Bank of Libya (2001a) Economic Bulletin, Vol. 41, 1st Quarter. Tripoli: Research and

Statistics Department.Central Bank of Libya (2001b) Economic Bulletin, Vol. 41, 2nd Quarter. Tripoli: Research and

Statistics Department.Deppe, L.A., Sonderegger, E.O., Stice, J.D., Clark, D.E. and Streuling, G.F. (1991) Emerging

competencies for the practice of accounting, Journal of Accounting Education 9 (2), 257–90.Dewing, I.P. and Russell, P.O. (1998) Accounting education and research: Zeff’s warnings reconsid-

ered, British Accounting Review 30 (3), 291–312.Dou, K. and Domuan, F. (1979) Accounting According to the Green Book’s Philosophy of the

Partners, Not Wage Workers. Tripoli: Public Firm of Publication and Distribution.Dou, K. and Domuan, F. (1983) An Introduction to Financial Accounting. Tripoli: Public Firm of

Publication and Distribution.Drury, C. (1983) Management and Cost Accounting, 1st edn. London: Chapman and Hall.El-Sharif, Y., Bait-El-Mal, M. and Ehshad, Y. (1995) Principles of Financial Accounting. Benghazi:

Garyounis University Publications.Enthoven, A.J.H. (1981) Accounting Education in Economic Development Management. Amsterdam:

North-Holland.Flaherty, R.E. and Diamond, M.A. (1996) Position and Issues Statements of the Accounting

Education Change Commission, Accounting Education Change Commission and AmericanAccounting Association (Accounting Education Series, Vol. No. 13). Sarasota, FL: AmericanAccounting Association.

Ganous, S., Tabouli, B., Shembesh, A., Al-Hamali, A., Barasi, O., AL-Mahdawi, M., Abou-Snina, M.and Sheredi, A. (1994) Libya: the Revolution in 25 years (in Arabic). Tripoli: General People’sCommittee for Information and Culture.

Ganous, S., Tabouli, B., Shembesh, A., Al-Hamali, A., Barasi, O., AL-Mahdawi, M., Abou-Snina, M.and Sheredi, A. (1999) Libya: the Revolution in 30 years (in Arabic). Tripoli: General People’sCommittee for Information and Culture.

Gao, S.S. (1995) Accounting education and practice in China–perceived problems and solutions. InJ. Blake and S.S. Gao (eds) Perspectives on Accounting and Finance in China, pp. 299–318.London: Routledge.

Garyounis University (1972) Prospectus of Garyounis University. Benghazi: Garyounis University.

388 Ahmad and Gao

Garyounis University (1976) Prospectus of Garyounis University. Benghazi: Garyounis University.Garyounis University (1979) Prospectus of Garyounis University. Benghazi: Garyounis University.Garyounis University (1994) Prospectus of Garyounis University. Benghazi: Garyounis University.Garyounis University (2002) Prospectus of Garyounis University. Benghazi: Garyounis University.Hajaj, A. and Saeud, K. (1989) Auditing Between Theory and Practice. Saudi Arabia: Dar Al-Marek

for Publication.Helmkamp, J.G., Imdieke, L.F. and Smith, R.E. (1983) Principles of Accounting. New York: John