Embed Size (px)

Citation preview

INTRODUCTION

CIMB Group is a leading ASEAN universal bank, the largest Asia

Pacific investment bank and one of the world's largest Islamic

banks. CIMB is headquartered in Kuala Lumpur, Malaysia and offers

consumer banking, wholesale banking, Islamic banking and asset

management. This group retail branch network is the widest in the

region with 1,060 retail branches with its core market being in

Malaysia, Indonesia, Singapore, Thailand and Cambodia. This group

has about 43,000 staffs located in 17 countries.

The group’s geographical reach and its products and services are

complemented by partnerships. Its partners include the Principal

Financial Group, Bank of Tokyo-Mitsubishi UFJ, Sun Life

Assurance, Allianz Insurance, Thai Life Insurance, Sri Ayudhya

General Insurance, and Mapletree Investments at which the

products and the services complemented by this companies. The

offices in ASEAN's main markets and in Bahrain, Colombo, Hong

Kong, Melbourne, Mumbai, Shanghai, Seoul, Sydney and Taipei are

the largest in Asia Pacific through its investment bank.

As the second largest commercial bank in Malaysia, CIMB Bank

holds significant market share across all consumer banking

products. It was named Best Domestic Bank in Malaysia 2009. CIMB

basically operate business on a dual banking basis through three

main brand entities which are CIMB Bank, CIMB Investment Bank and

CIMB Islamic that giving customer a choice of both conventional

and Islamic solutions.

1

CORPORATE PROFILE

TYPE : Public

INDUSTRY : Financial service

HEADQUARTERS : Kuala Lumpur, Malaysia

CHAIRMAN : Tan Sri Dato’ Md Nor Yusof

CHIEF EXECUTIVES : Datuk Seri Nazir Razak

2

PRODUCTS : Consumer banking, corporate banking,

investment banking,

Islamic banking, Asset management,

insurance and takaful.

TOTAL ASSETS : RM 321.8 billion (September 2012)

EMPLOYEES : over 43,000

HISTORY

CIMB was started their business as a merger since their

existence. It starts from the first bank known as Bian Chiang

Bank by Wee Kheng Chiang on the year of 1924 in Kuching, Sarawak,

Malaysia. During these early days, the bank’s activities were

mainly related to business financing and issuance of bill of

exchange which is an unconditional order in writing, addressed by

one person to another, signed by the person giving it, requiring

the person to whom it is addressed to pay on demand or at a fixed

3

or determinable future time a sum certain in money to or to the

order of a specified person, or to bearer.

On 17 September 1935, Ban Hin Lee Bank Bhd founded by “Towkay”

Yeap Chor Ee was established in Penang, Malaysia and formally

incorporated as a private limited company. This bank originally

focuses to serve local businesses in their trade and merchant

activities. By 1948, Bank Lippo was founded in Tangerang,

Indonesia that been controlled by Mochtar Riady with Lippo Group.

In 1955, Bank Niaga has been founded in Indonesia and established

as a national private bank and well known for their excellent to

gained great deal of trust from its customers and on the well-

being and professionalism of its employees.

In 1960, Ban Hin Lee Bank Bhd branched into real estate and home

financing. During 1965, Southern Bank Bhd was founded from humble

roots in Penang and quickly expanded to other parts of Malaysia.

This bank was later renamed as Southern Banking Ltd and gain

opportunities being as an important player in wealth management

products, credit cards and SME lending. This bank was also is the

first bank in Malaysia that set up MEPS and ATM machine. In the

same year, Bank Bumiputra Malaysia Bhd was incorporated in line

with government initiatives in order to increase Bumiputra

participation in the Malaysia economy.

In 1971, the prominent Wee family of Bian Chiang Bank became more

famous as founding members of the United Overseas Bank (UOB) in

Singapore. A year after, United Asian Bank Bhd completely

4

establish in Kuala Lumpur at which being started as a banking

joint-venture between Malaysia and India as it is a merger of

three Indian owned banks which are Indian Overseas Bank Ltd,

Indian Bank Ltd and United Commercial Bank Ltd. This United Asian

Bank Bhd took over the operations of the Malaysian branches of

these Indian banks. It was mainly directed at small businesses

and individuals.

On April 1974, Pertanian Baring Sanwa Multinational Berhad

incorporated by Bank Pertanian of Malaysia, Baring Brothers,

Multinational Bank of the United Kingdom and Sanwa Bank of Japan.

Under management of Baring Brothers, Pertanian Baring Sanwa

Multinational Berhad have been provided corporate advisory and

funding services to multinationals and undertook corporate

restructuring, merger and acquisition activities for Malaysian

companies. Under this year, Bank Niaga have been expanded and

become a full service bank.

The purchased of Bian Chiang Bank by Fleet Group have led to the

formation of Bank of Commerce Bhd in November 1979. This new bank

had a strong focus on system and transparency from the very

beginning and reflecting the management style of co-shareholder,

JP Morgan. This bank has been pushed forward by an aggressive

performance driven work culture and this led the bank a one of

the most progressive banks in the industry.

5

By 1980s, Bank Bumiputra Malaysia Bhd becomes the largest bank in

the country in term of assets. Their banking facilities been

provided access by infrastructure and contribute to the growth of

small scale enterprise and investment in rural areas. Bank

Bumiputra Malaysia Bhd was the first Malaysian bank that operates

in New York, London, Tokyo, Bahrain and Hong Kong. Two years

after that, it was listed as the largest bank in Southeast Asia

by Asian finance magazine. At the same time, after three years of

the incorporation of Bian Chiang Bank their total assets have

become MYR367 million and total shareholders fund is MYR12.8

million for a one-branch bank.

As the controlling shareholder of Pertanian Baring Sanwa

Multinational Berhad, Bank of Commerce replaced it in the year

1986 and renamed as Commerce International Merchant Bankers Bhd

(CIMB). The new shareholders retained their focus on corporate

finance and IPOs. Three years after operation, CIMB emerged as

Malaysia top advisor for new listings. By the added of

stockbroking in order to complement its advisory and listing

expertise, establishment of award-winning reputation as an

equities broker and IPO house led this bank in increasing of

their profit at a high amount in early 1990. CIMB then win

rewards as an excellent position from the exponential bond market

growth.

6

In the same year, Ban Hin Lee Bank Bhd had become a modern and

thriving financial position in their headquarters at Penang and

operation throughout Malaysia and Singapore. On 7 January 1991,

it becomes a public listed company on Kuala Lumpur Stock Exchange

(KLSE). On November 1991, Bank of Commerce acquired United Asian

Bank and created Bank of Commerce (M) Bhd. Then, this listed

company was renamed Commerce Asset Holdings Berhad (CAHB). Bank

of Commerce branch network then increasing year by year.

In October 1999, Bank Bumiputra Malaysia Bhd emerged from Asian

financial crisis and other financial problem. Bank of Commerce

emerges with this bank and become the largest merger in

Malaysia’s banking history. Under the control of CAHB bank, they

formed Bumiputra-Commerce Bank and became the bank of choice to

many multinational and local corporations, government

organizations and individuals.

1 July 2000, Southern Bank acquired Ban Hin Lee Bank, United

Merchant Finance, Perdana Finance Bank and Cempaka Finance Bhd.

During a year 2002, Commerce Asset Holdings Bhd became the

majority shareholders in Bank Niaga. This was actually the

strategic policies that taken by Indonesian government in

response to the banking and economic crisis. This acquisition

provided more opportunities for CAHB to acquire a majority stake

in Indonesian banking franchise.

January 2003, CIMB have been listing on the main board of the

Kuala Lumpur Stock Exchange (KLSE) and exceed the expectations of

7

their investors and employees. But, it was just listed for three

years due to upcoming developments. On June 2003, CIMB Islamic

was officially launched by Malaysia’s Bank Negara Governor, Tan

Sri Dato’ Dr Zeti Akhtar Aziz.

CIMB acquired 70% of Commerce Trust Bhd and commerce Asset fund

managers Sdn Bhd from Commerce Assets Holdings Bhd. This led to

the formation of CIMB-Principal Asset Management Bhd and joint

venture with Principal Financial Group of USA in 2004. In 2005,

CIMB acquires G K Goh Securities Pte Ltd pf Singapore and led to

the formation of CIMB- GK Securities Pte Ltd. In June, CIMB

announces acquisition of Bumiputra-Commerce Group in order to

create a universal bank by combining its consumer and investment

banks. January 2006, CIMB group made a transition to a full

service banking provider serves a range of customers from

corporates to individuals. After negotiations with Southern Bank,

in March 2006 CIMB Groups acquired tgis bank to combine the

extensive resources and reach of Bumiputra-Commerce.

The Prime Minister of Malaysia, Dato’ Seri Abdullah Ahmad Badawi

was launched the new CIMB Group as a regional universal bank in

September 2006 signifying the three way merger of Commerce

International Merchant Bankers, Bumiputra-Commerce Bank and

Southern Bank. As a universal bank, it has the full range of

banking and financial services, conventional and Islamic to serve

everyone from the smallest retail client to the largest companies

and institution.

8

In November 2007, in order to carry out the Group corporate

social responsibilities and philanthropic initiative, CIMB

Foundation has been created. Its focus more on sustainable

programmed in community development, education and sports. In

2008, CIMB entered into an agreement for a stake in the Bank of

Yingkou, China. During this time, CIMB Group created the sixth

largest bank in Indonesia between the merger of PT Bank Niaga Tbk

and PT Bank Lippo Tbk with the initiative of Khazanah Nasional

Bhd.

In the same year, CIMB Group and the Principal Financial Group

strengthened their partnership with the launch of CIMB-Principal

Islamic Asset Management. CIMB entered into an agreement with the

Financial Institution Development Fund to purchased stake in Bank

Thai Pcl and renamed as CIMB Thai when officially launched in

2009 by Khun Korn Chatikavanji, Thailand’s Minister of Finance.

The 39-storey Menara Bumiputra-Commerce houses CIMB Group’s

consumer banking franchises officiated by Seri Paduka Baginda

Yang di-Pertuan Agong Tuanku Mizan Zainal Abidin Ibni Al-Marhum

Sultan Mahmud Al-Muktafi Billah Shah and Seri Paduka Baginda Raja

Permaisuri Agong Tuanku Nur Zahirah.

In September 2009, CIMB Group set up their banking service in

Singapore to bring the innovative products that maximize value

for money in a competitive environment. CIMB Group then tries to

expand their power to Cambodia on 19 November 2010 in Pnom Penh.

In 2011, CIMB Group starts CIMB 2.0 an organizational to

9

recalibrate and accelerate its businesses. The Group rebrands to

a red logo through all divisions and launches a new tagline of

‘ASEAN For You.’ In order to support ASEAN economic integration,

the Group also launches the CIMB ASEAN Research Institute and the

CIMB ASEAN Conference series. In 2012, CIMB Group reaches Asia

Pacific and beyond such as Royal Bank of Scotland, Sydney,

Melbourne, Seoul, Taipei and many more.

COMPANY VISION AND MISSION

Vision

To be the leading ASEAN company.

Mission

To provide universal banking services as a high-performing,

institutionalised and integrated company located in ASEAN and key

market beyond, and to champion the acceleration of ASEAN

integration and the region’s links to the rest of the world.

10

CORPORATE ENTITIES OF CIMB

CIMB Group today operates across ASEAN under several corporate

entities including CIMB Investment Bank, CIMB Bank, CIMB Islamic,

CIMB Niaga, CIMB Securities International and CIMB Thai.

CIMB

Bank

11

CIMB Bank is the Group’s consumer bank in Malaysia. It has four

main operating markets that located in Malaysia, Indonesia,

Singapore and Thailand, plus a growing presence in Cambodia and

Philippines that are role as main subsidiaries.. Besides that,

CIMB Bank has opened their branch in London and representative

offices in Shanghai, Yangon and Mumbai. In Malaysia, CIMB Bank

had 312 branches, 8.6 Million customers and 2,284 ATM’s at the

end of 2012 and the number are still growing. As the second

largest consumer bank in Malaysia, CIMB Bank managed to open two

branches in Singapore and eleven branches in Cambodia.

CIMB Niaga

Established in 1955 as Bank Niaga, CIMB Niaga is the group’s

banking franchise in Indonesia. It was the fifth largest bank in

Indonesia by assets at the end of 2012 and has been listed on the

12

Indonesia Stock Exchange since 1989. CIMB Niaga offers a

comprehensive range of conventional and Shariah products and

services. At the end of 2012, they had 509 branches, 3.8 Million

and 2,257 ATMs around Indonesia. CIMB Group had 97.9% stake in

CIMB Niaga at the end of 2012.

CIMB Investment Bank

CIMB Investment Bank is the investment banking with offices in

Malaysia and ASEAN’s main market, China (Hong Kong and Shanghai),

Bahrain, Colombo, London, Australia (Melbourne and Sydney),

Mumbai, New York, Seoul, and Taipei. The product and service that

been offered by this investment banking franchise are

institutional and retail brokerage, placements and underwriting,

and corporate finance advisory services. Throughout year 2012,

CIMB Investment Bank has shown rapid growth by maintaining market

dominance in Malaysia and improving in rankings in Singapore and

Thailand. In Malaysia, the Investment Bank was No.1 in

stockbroking.

13

CIMB Islamic

CIMB Islamic is the global Islamic banking and finance that

conduct under CIMB Group. It offers full complement of Shariah-

compliant financial solutions in investment banking, consumer

banking, asset management, takaful, private banking and wealth

management. It also was operating in parallel with the Group’s

objective. CIMB Islamic Shariah Comittee was responsible to guide

and monitor the operation to make sure it follows and abide all

Shariah principles. In Malaysia, CIMB Islamic is the second

largest Islamic bank after Bank Islam. Besides that, CIMB Islamic

is also recognised as a pioneer in Islamic financial markets.

CIMB Thai

14

CIMB Thai is CIMB Group’s banking franchise in Thailand. It was

the tenth largest bank in Thailand at the end of the year 2012

and has been listed on the Stock Exchange of Thailand since 1978.

The total assets at the end of 2012 approximately THB201.5

Billion (RM 20.1 Billion) and have 164 branches, 1.1 Million

customers and 509 ATMs in Thailand. CIMB Group had a 93.7% stake

in CIMB Thai at the end of 2012.

15

KEY INTERNAL CONTROL PROCESS

Key internal control process in CIMB is the process that the

board has established in reviewing the performance and the

integrity of the system that had been implemented or want to be

implemented in internal control such as compliance with

applicable laws, regulations, rules, directives and guidelines,

directives and guidelines. The committees under key internal

control are as follows:

Audit Committee

One of the key processes that the board was established is The

Group of Audit Committee (Group AC). The Group Audit Committee

(Group AC) comprises independent Non-Executive Directors. It is a

Board-delegated committee charged with oversight of financial

reporting, disclosure, regulatory compliance, risk management and

monitoring of internal control processes in the Group. Senior

Management, internal auditors and external auditors report to the

Group AC on the effectiveness and efficiency of internal

controls.

All significant and material findings by the internal auditors,

external auditors and regulators are reported to the Group AC for

review and deliberation. The Group AC reviews and ensures the

implementation of Senior Management’s mitigation plans to

safeguard the interests of the Group and upkeep proper

16

governance. Management of business and support units that are

rated as ‘Above Average Risk’ or ‘High Risk’ are counselled by

the Group AC.

The Group AC also reviews all related party transactions, audit

and non-audit related fees proposed by the external auditors of

the Group. The Group AC makes field visits to bank branches and

operating subsidiaries of the Group whenever necessary. This

enables the Group AC to actively interact with the relevant

Senior Management staff on the expectations of the Group with

regard to compliance, internal controls and risk management.

Presentations of business plans, current developments,

operations, risks of the business and controls to lessen the

risks are made by the relevant business and support units as and

when deemed necessary by the Group AC.

Risk Committees

The Board has established various risk committees within the

Group with distinct lines of responsibility and functions, which

are clearly defined in the terms of reference. These committees

have the authority to examine matters within the scope and report

pertinent issues and recommendations to the Board.

17

The Board Risk Committee determines the Group’s risk policy

objectives and assumes responsibility on behalf of the Board for

supervision of risk management. The Board Risk Committee reports

directly to the Board of the Group. They also provides strategic

guidance and reviews decisions made by the various Risk

Committees.

The responsibility of the supervision of the risk management

functions is delegated to the Group Risk Committee, which reports

directly to the Board Risk Committee. The Group Risk Committee,

comprising of Senior Management of the Group, performs the

oversight function on overall management of risks, within the

risk appetite approved by the Board.

The Group Risk Committee is supported by specialised sub-

committees like Group Wholesale Banking Risk Committee, Regional

Liquidity Risk Committee, Regional Credit Committee and Consumer

Banking Credit Committee.

Group Shariah Committee

The Group Shariah Committee (the Shariah Committee) which is in

compliance with BNM’s Guidelines on Shariah Governance Framework

for Islamic Financial Institutions is responsible for overseeing

all Shariah matters of the Group in accordance with the relevant

regulatory frameworks in the jurisdictions where the Group

operates in. The Shariah Committee among others ensures that the

Shariah rulings relating to Islamic banking and capital market

18

products and services comply with the Shariah resolutions of the

relevant Shariah authorities.

The Shariah Committee is assisted by the Group Shariah Department

that functions as the internal adviser on Shariah matters to all

business and support units within the Group in the carrying out

of their Islamic banking capital market and finance activities.

It serves as the intermediary between such units and the Shariah

Committee. In addition to recommending the relevant and

appropriate Shariah policies and procedures for the Shariah

Committee’s approval, the Shariah Department also provides

training across the Group on the Shariah Governance Framework

(the SGF).

The Shariah Department facilitates the implementation of Shariah

Research & Secretariat, whilst Shariah Review, Shariah Risk

Management and Shariah Audit functions are performed by Group

Compliance, Group Risk and Group Internal Audit, respectively.

The Group Management Committee

The Group Management Committee (GMC) assists the Group Managing

Director/Chief Executive Officer (Group Chief Executive Officer)

in ensuring that the daily operations of the Group are conducted

19

in accordance with the corporate objectives, strategies, approved

annual budget, applicable laws and regulations as well the

Group’s internal policies and procedures, that goes to the heart

of how the Group conducts business. The Group has established a

number of policies and procedures which are designed to enhance

the integrity of the system of internal control and mitigate

risks. Delegated Authority and authority limits are established

to facilitate smooth daily banking and financing operations,

trading activities, extension of credit facilities,

restructuring, investments as well as acquisitions and disposals

of assets. The results of operating units are reported monthly at

GMC meetings and compared with approved budget.

The GMC members review their respective business plans and report

to the Group Chief Executive Officer the performance of their

respective business divisions in line with the Group’s strategy

and other matters as directed by the Board and the Group Chief

Executive Officer.

PEST ANALYSIS

20

Political and legal

Corporate governance

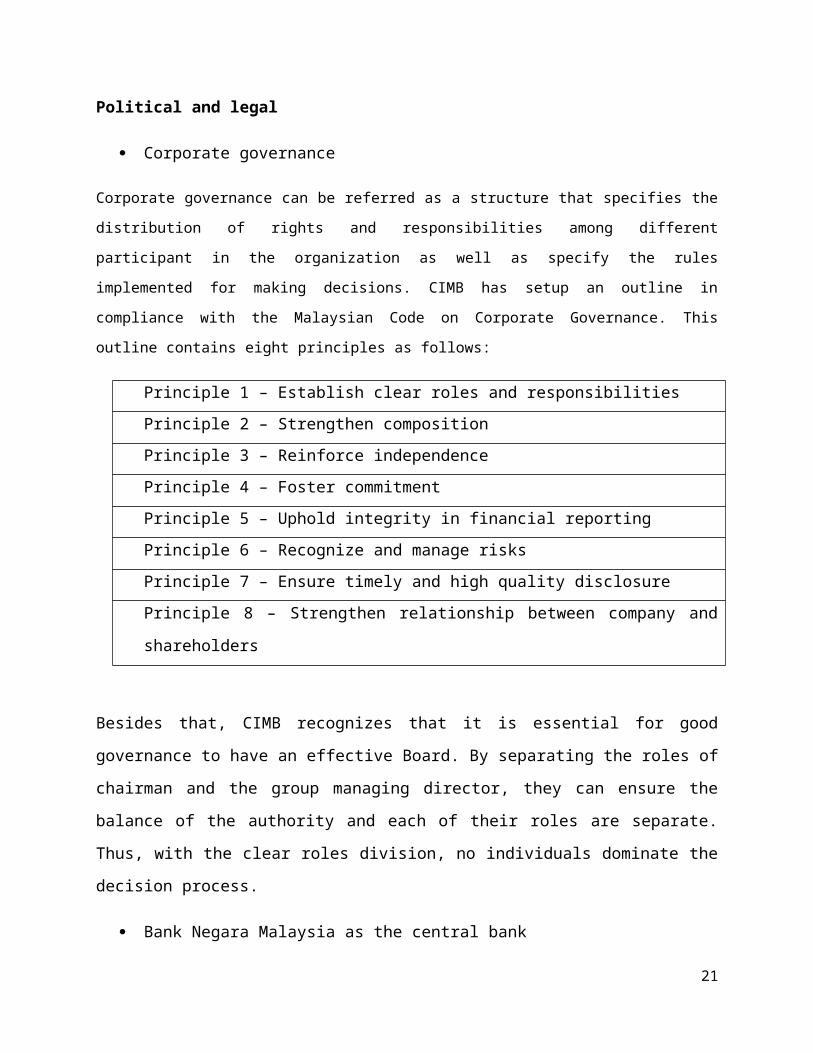

Corporate governance can be referred as a structure that specifies the

distribution of rights and responsibilities among different

participant in the organization as well as specify the rules

implemented for making decisions. CIMB has setup an outline in

compliance with the Malaysian Code on Corporate Governance. This

outline contains eight principles as follows:

Principle 1 – Establish clear roles and responsibilitiesPrinciple 2 – Strengthen compositionPrinciple 3 – Reinforce independencePrinciple 4 – Foster commitmentPrinciple 5 – Uphold integrity in financial reportingPrinciple 6 – Recognize and manage risksPrinciple 7 – Ensure timely and high quality disclosurePrinciple 8 – Strengthen relationship between company and

shareholders

Besides that, CIMB recognizes that it is essential for good

governance to have an effective Board. By separating the roles of

chairman and the group managing director, they can ensure the

balance of the authority and each of their roles are separate.

Thus, with the clear roles division, no individuals dominate the

decision process.

Bank Negara Malaysia as the central bank

21

Bank Negara Malaysia (BNM) as the central bank is responsible to

regulate the law and rules for all the banking institution in

Malaysia. Thus, CIMB is also tied under the rules and regulations

set by BNM. The example of such law and regulations are, Anti-

Money Laundering Act 2001 (AMLA) and Insurance Act 1996. Besides

that, BNM also responsible in setting the base lending rate (BLR)

which banks cannot exceed the range that have been setup.

On the other hand, BNM also is playing the role for promoting the

monetary stability. For example, this is where all the banks in

Malaysia including CIMB are restricted to implement the strategy

to control their position during economic downturn or even during

inflation.

Large number of shareholders

Until now, CIMB has at least 30 largest shareholders as the

leading shareholder is Khazanah Nasional Berhad which holds a

total of 29.9 per% of share. This followed by Employee Provident

Fund Board and Mitsubishi UFJ Financial Group which hold a total

of 12.92% and 5% respectively. Having a large number of

shareholders whom has big name in their industry could help CIMB

in recruiting another new relationship with the organization.

This is because, as CIMB strengthening their relationship with

the existing shareholder, at the same time they could gain trust

from the outsider. Thus, this could lead CIMB to access to the

opportunity of expanding their market in the country other than

22

the ASEAN countries. Besides that, at the same time CIMB can

increase their reputation in the eyes of the other organizations.

Economic

For the whole of 2012, Malaysia’s real GDP grew by 5.6 per cent

compared with 5.1 per cent in 2011. Malaysia is a developing

economy in Asia which, in recent years, has successfully

transformed from an exporter of raw materials into a diversified

economy. The largest sector of the economy is services,

accounting for around 54 percent of GDP.

After a benign inflation environment in 2012, BNM estimates

headline inflation to average 2-3% in 2013. The drivers of

inflation in 2013 are expected to come from higher global prices

of selected food commodities, the adjustments to domestic

administered prices as the government resumes its subsidy

rationalization and the moderate impact of the minimum wage

policy on companies’ total costs.

Malaysia remains attractive to private capital inflows. Foreign

direct investment (FDI) inflows have maintained their momentum

since rebounding from a slump in 2009. Malaysia was assessed for

the first time under the Financial Sector Assessment Program

(FSAP) in 2012, which is conducted jointly by the International

Monetary Fund and the World Bank. The outcome of the assessment

reaffirmed the strength and resilience of the country's banking

23

sector, which is backed by a high level of compliance to domestic

regulatory and supervisory framework.

Therefore, CIMB Group has to take advantage of the economic

stability that is present in Malaysia. Malaysia’s economic

condition itself has provided a platform for the Group to present

themselves as an attractive investment towards their prospective

investor.

Social

Corporate social responsibility (CSR)

CIMB realizes that it is a part of virtuous circle to support

people in the communities, workplace, marketplace and environment

in order to help building the social sustainability in the long

term period. This is where CIMB giving back to the community and

contribute for the betterment of the society. CIMB has supported

the community in terms of health, education as well as sport and

recreation.

CIMB Foundation has funded the project of prevention of blindness

and mobile health clinics for the society health awareness.

Besides that, this foundation also funded the sponsorship

programmes, sponsorship of PINTAR schools and also the courses to

improve English and ICT capacity. All of this has been done to

improve the education level of the rural children across the

region. On the hand, CIMB also strongly encourage their staff to

take part in sport by holding the CIMB SEA Games which open to

24

all staff in Malaysia, Indonesia, Singapore, Thailand and

Cambodia.

Cultural differences among countries

Having located in various countries around the Southeast Asia,

CIMB has to consider the differences of the culture practiced by

the people living there. This is because every country has its

own culture practice and belief. For example, there are

differences between the cultures in CIMB Thai ad CIMB Malaysia.

Malaysian tends to be specific on time compare to the Thai

employees. Besides that, in Malaysia organizational structure,

employees believe that they have to settle the assigned task on

time. In contrast, Thais are more flexible which if work is not

done on time, it is okay to postpone it to another day. Because

of such differences in their culture, CIMB must find the best

alternatives in order to adapt to the different culture.

Technology

In order to compete with other banks, CIMB must aware to the

technological changes that may influence its performance in the

banking industry. Thus, CIMB had introduced their online banking

that can be accessed through CIMB Clicks. Besides transaction of

25

money, their customer also can experience the self service

banking.

The new service offered by CIMB is Kwik Account. It is an account

that can be opened online, anywhere, without going into a branch.

On the other hand, CIMB customers can immediately use the

account. Through this newly introduced Kwik Account, customers

able to do online shopping, sending money using only mobile

numbers, reload their prepaid, send money overseas and pay their

bills.

With the services provided by CIMB, customers now can access to

their services wherever they are. It is a great opportunity for

CIMB to use the technological advances as people nowadays are

mostly own smart phones which allow them to access Internet

anytime.

26

SWOT ANALYSIS

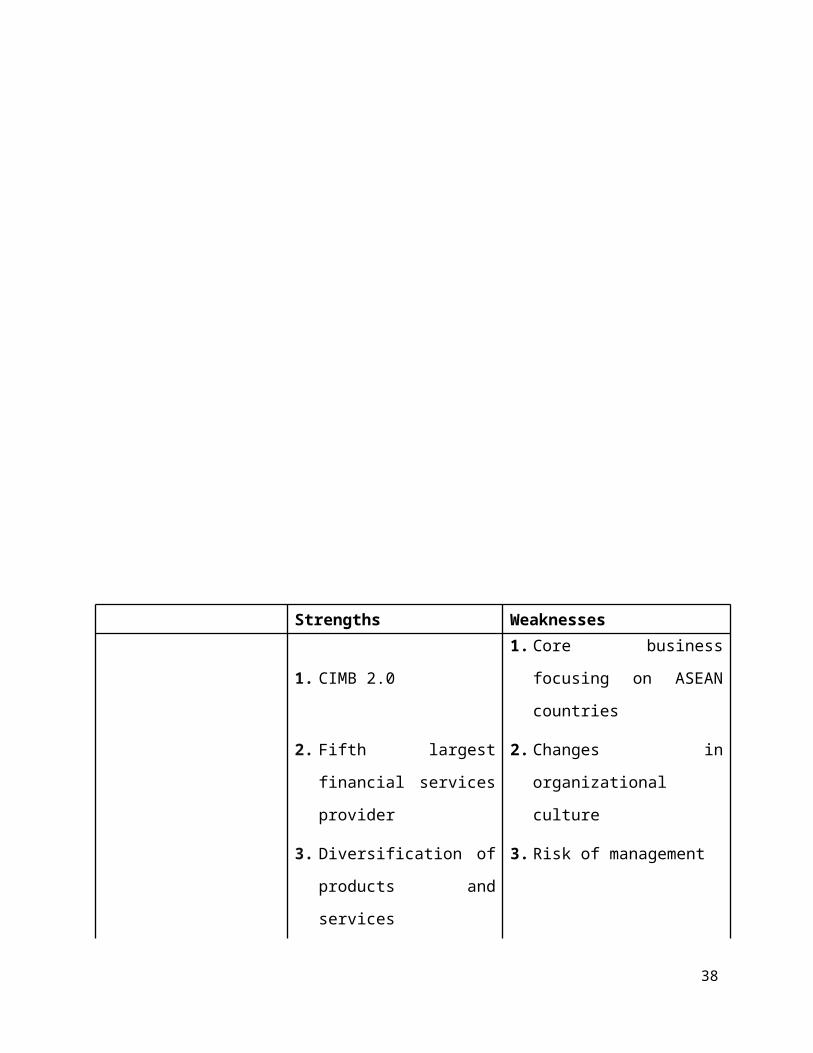

Strength

CIMB 2.0

CIMB 2.0 is CIMB Group’s internal organizational restructuring

that would leverage the various components of banking, treasury

and the markets launched at the end of 2011 and the

implementation of the change are still considered as an ongoing

process. These changes include the merger of the corporate

banking and treasury operations, the acquisition of Royal Bank of

Scotland (RBS) by CIMB and the streamlining of businesses at the

commercial bank. CIMB 2.0 primary focus is to achieve scale

economies, engage in stronger cost management and portfolio

optimization at all levels of business and geographies.

Furthermore, this move also allowed for the operations to move to

a regional perspective, improve product offerings and teamwork as

well as generate operational efficiencies.

Fifth largest financial services provider

27

Being Malaysia’s fifth largest banking and one of Southeast

Asia’s leading universal banking groups by assets in Southeast

Asia, CIMB Group has proved their worth as one of the major

player in the financial market to their customer. Their long

history of enlistment in the Bursa Malaysia has further

solidified their position as one of the leading universal banking

groups in the industry. With their strong position in market, it

directly develops trust on behalf of their current and potential

customers to utilize the services that are provided to by CIMB

Group.

Diversification of products and services

By offering a wide range of financial products and services,

covering corporate and investment banking, consumer banking,

treasury, insurance and asset management, CIMB Group have serve

their customers throughout the regions. Their diversification

would lead to the increase in profits as well as attracting

potential investors. With the diversification of product and

services, customers would have more choices in what they want to

invest their money in.

Weakness

Core business focusing on ASEAN countries

28

Until now, CIMB only exist in the ASEAN countries. This is such a

great disadvantage for CIMB as days passed there are many other

growing banks around the world. Customers nowadays are seeking

for services that are very convenient for them. Customers from

this countries will it find hard for them to access for CIMB

services when they intend to travel outside overseas. This is

because when they are plan to travel to the country which did not

provide CIMB, they need to deal within their country first

regarding the money transaction, exchange of currency and so on.

Changes in organizational culture

CIMB need to endure the changes occurs in their organizational

culture because of the merging done. The people whom working in

CIMB before has to adapt to new environment because of there were

changes happened. Besides that, employees have to make themselves

comfortable with the new management that may be different from

before.

Mergers and acquisition done by CIMB also means that there will

be new employees hired or being relocated. Thus, this change

tends to make them uncomfortable as the risk of being unemployed

would always present in their mind.

High interest rate

CIMB Group interest rate can be considered as one of the banks

that offered a high interest rate towards its customer. With its29

base interest rate amount to 6.60% (similar to AmBank Berhad and

Maybank Berhad), their customer would turn their back from CIMB

and go to other banks that could offer lower interest rate such

as Bank Muamalat Malaysia Berhad (6.35% p.a) and Al-Rajhi Bank

(Malaysia) Berhad (6.30%).

Opportunities

Growth in international banking will increase customer base

As technology are rapidly growing in these few years, internet

access are provided almost everywhere throughout the world with

the exception of third world countries. Availability of internet

access makes it easier to engage in business transaction without

face-to-face meeting. Therefore, potential investors that are

located in the countries which do not have any CIMB offices could

invest through the internet services that are provided by the

CIMB Group.

Malaysia’s economic growth

Malaysia’s robust economic growth in the 4th quarter of 2012 has

boosted the country’s 2012 GDP growth to 5.6%, much higher than

the 5.1% registered in 2011. The growth was supported by the

continued strength in domestic demand despite the challenging

30

global economic environment. Due to continuing low interest

rates in the US and Europe and with balance sheets of most Asian

economies expected to remain strong, there is an insurgence of

investors tilting towards Asia as compared to developed

economies. Therefore, it is beneficial for the Group to invest in

both local and foreign bonds to take advantage of high demand for

bonds, especially Asian bonds.

Political stability

Malaysia’s political stability environment would encourage more

investors to invest in Malaysian companies. The Government has

also pledged to implement the appropriate policies and provide

its support for the creation of a conducive environment for

business and investment. This allows investors to rest assured of

Government that is firm yet flexible enough to accommodate their

needs. Political stability would provide a platform for CIMB

Group to attract prospective investors and partners that are

looking forward to investing their money in politically low risk

country.

Large customer base

31

Their strong presence in these countries has created a large

customer base of about 13.5 million customers in over 19

countries, with the potential of adding more to the number. The

Group’s retail banking branch network is the widest in the

Southeast region with a total of 1,080 retail branches in

Malaysia, Indonesia, Singapore, Thailand and Cambodia. While

their investment bank is the largest in Asia Pacific (excluding

Japan) with offices and ASEAN’s main markets and in Bahrain,

Colombo, Hong Kong, Melbourne, Mumbai, Shanghai, Seoul, Sydney

and Taipei. In addition it has equity sales operations in London

and New York. Their strategic company placement has allowed them

to serve their customer better thus, creating a large customer

base in the region.

Threat

Competition from international banks

Being as one of the top ten banks in Asia gives the opportunity

for the CIMB in competing with the other existing international

banks. For example, they have to compete with the AmBank Group

and DBS Bank. As days pass, they are more banks growing and this

has added the number of the CIMB’s competitors.

Because of the existing competition, it also causes the CIMB

itself to have a limited market growth. CIMB has to prove

themselves so that they stand out and can offers better than

32

other existing international banks. Besides that, a huge number

of competitors make it hard for CIMB to expand its market share.

Fluctuation of foreign exchange rate

As an institution which also is dealing with the exchange rate,

CIMB need to face the risk of the unstable foreign exchange rate.

This happens because of the foreign exchange rate always change

depends on the current situation all around the world. Besides

that, this situation will lead to uncertainty as customer may be

unsure of how much money they will receive when they are selling

abroad, for example. This usually arises between the exporter and

the importer because the prices may be affected as they can be

more expansive or cheaper.

On the other hand, this uncertainty will lead to the lack of

investment from the customers in CIMB. Deposits from the customer

are the largest contribution to one bank. Thus, when this

happens, customer will feel reluctant to invest at CIMB because

of the exchange rate that always changes from time to time. It is

a worrisome especially for the risk averse.

Same business segment

This is another threat that needs to be faced by CIMB which the

competitors also provide the same services to their customers.

For instance, CIMB introduces the CIMB Islamic and at the same

time Public Bank also provides the Islamic Banking to their33

customers. Because of this, customer will have the options to

choose which service they want to use. Besides that, the existing

customers of CIMB may also turn their back from CIMB and choosing

the rivals.

Financial liberalization

Financial liberalization refers to reduction of any sort of

regulations on the financial industry of a given country. CIMB

Group must constantly be aware of the changes in government

regulations, especially regarding the financial market. Under

control, financial liberalization would improve the economic

growth of a country. However, in an uncontrollable environment,

financial liberalization will lead to a country’s financial

crisis.

34

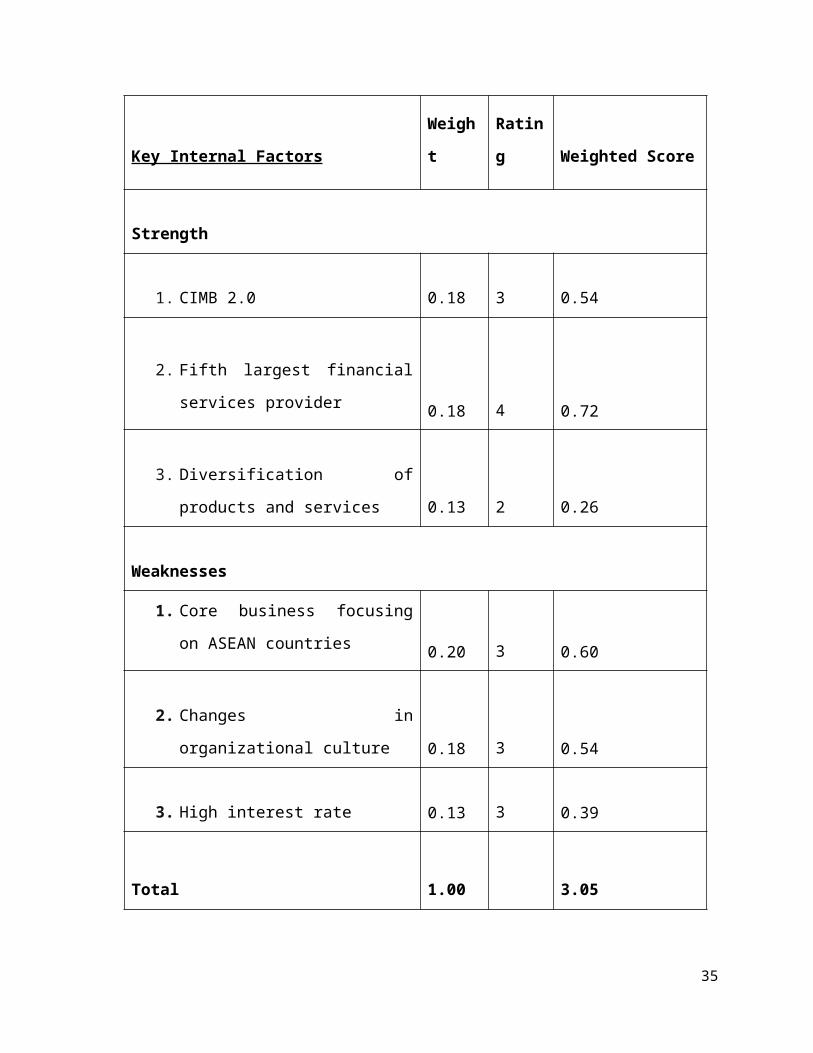

Key Internal Factors

Weigh

t

Ratin

g Weighted Score

Strength

1. CIMB 2.0 0.18 3 0.54

2. Fifth largest financial

services provider 0.18 4 0.72

3. Diversification of

products and services 0.13 2 0.26

Weaknesses

1. Core business focusing

on ASEAN countries 0.20 3 0.60

2. Changes in

organizational culture 0.18 3 0.54

3. High interest rate 0.13 3 0.39

Total 1.00 3.05

35

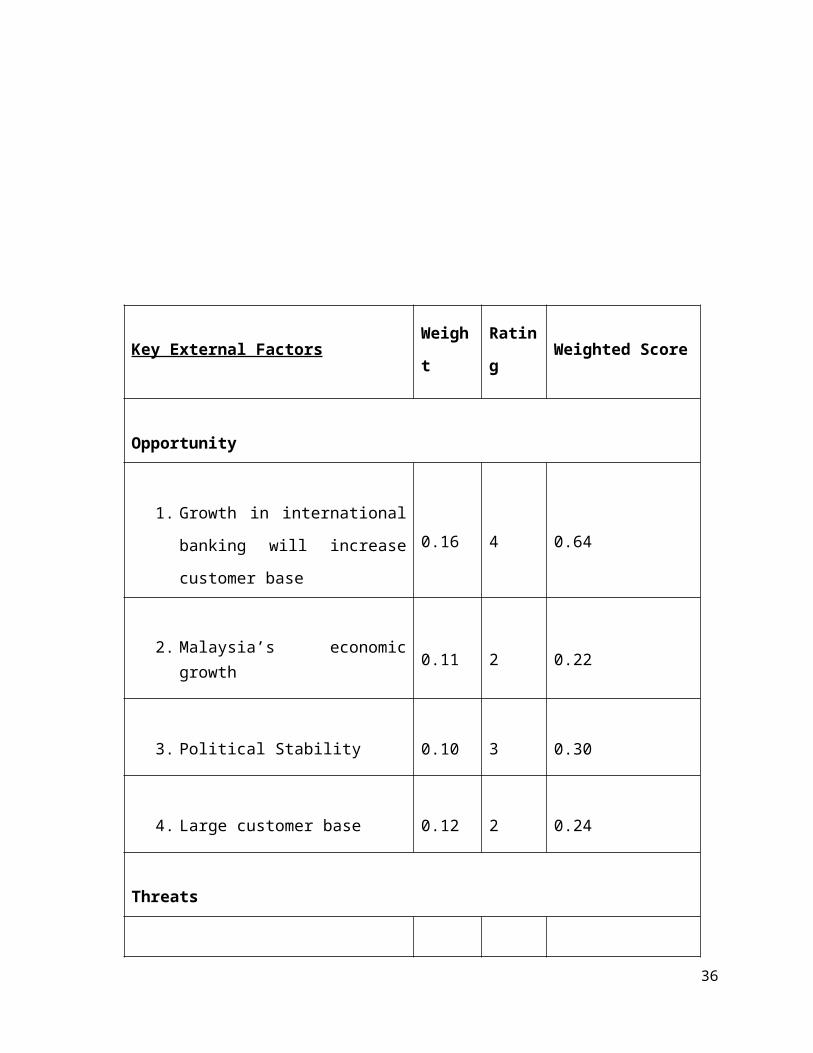

Key External FactorsWeigh

t

Ratin

gWeighted Score

Opportunity

1. Growth in international

banking will increase

customer base

0.16 4 0.64

2. Malaysia’s economicgrowth 0.11 2 0.22

3. Political Stability 0.10 3 0.30

4. Large customer base 0.12 2 0.24

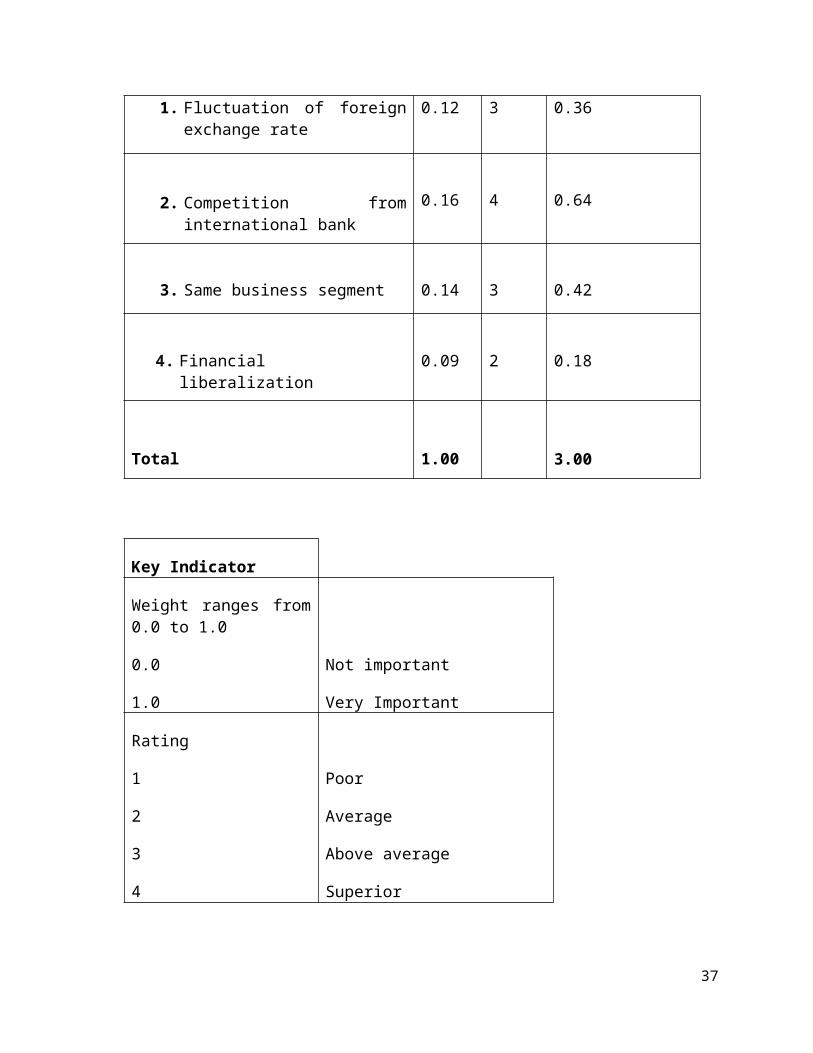

Threats

36

1. Fluctuation of foreignexchange rate

0.12 3 0.36

2. Competition frominternational bank

0.16 4 0.64

3. Same business segment 0.14 3 0.42

4. Financialliberalization

0.09 2 0.18

Total 1.00 3.00

Key Indicator

Weight ranges from0.0 to 1.0

0.0

1.0

Not important

Very Important

Rating

1

2

3

4

Poor

Average

Above average

Superior

37

Strengths Weaknesses

1. CIMB 2.0

1. Core business

focusing on ASEAN

countries

2. Fifth largest

financial services

provider

2. Changes in

organizational

culture

3. Diversification of

products and

services

3. Risk of management

38

4. Large customer

base

Opportunities SO Strategies WO Strategies

1. Growth in

international

banking will

increase

customer base

1. Regional expansion

(S2, S4, O2)

1. Appoint an

experienced manager

to monitor foreign

branches (W3, O3)

2. Offer low interest

rate to ASEAN

customer (S4, O2)

2. Malaysia’seconomic growth

3. PoliticalStability

Threats ST Strategies WT Strategies

1. Fluctuation offoreign exchangerate

1. Strengthening

position in ASEAN

through social

banking (S2, T2)

2. Build specialized

institution for

future skilled

workers (S3, T3)

1. Joint venture with

international bank

(W1, T2)

2. Competition from

international

bank

3. Same businesssegment

4. Financialliberalization

39

Strength – Opportunities

Regional expansion

(S2. Fifth largest financial services provider, S4. Large

customer base, O2. Malaysia’s economic growth)

Being the fifth largest financial services provider with a large

customer base in ASEAN countries, they could expand their market

by conquering other countries regionally. Taking advantages of

the booming Asian’s economic growth, they could start looking

towards expanding their markets to Asia-Pacific countries instead

of only ASEAN countries.

Weakness – Opportunities.

Offer low interest rate to ASEAN customer

(S4. Large customer base, O2. Malaysia’s economic growth)

By offering low interest rate to CIMB’s ASEAN customers, it would

provide an opportunity for CIMB Group to retain as well as

increasing their customer base. As CIMB is headquartered in

Malaysia, they could take advantage of the economic growth by

40

inducing the ASEAN customer to make loans. Thus, they could gain

profits in terms interest rate payments.

Strength – Threat

Strengthening position in ASEAN through social banking

(S2. Fifth largest financial services provider, T2. Competition

from international bank)

Southeast Asia is among the countries with the world most

Facebook users. This fact provides a good opportunity for CIMB to

utilize the potential Facebook users in ASEAN to experience

social banking via social network. CIMB Group would be the first

bank in Southeast Asia that provides social banking features with

the utilization of social networking. They will able to

strengthen its position especially in the ASEAN market.

Build specialized institution for future skilled workers

(S3. Diversification of products and services, T3. Same business

segment)

CIMB Group could build a specialized institution for those who

are interested in financial and banking course. By setting up on

building this institutions, they will be able to differentiate

themselves with others financial institutions. With this

institution, they will have their own skilled workforce that are

able to serve in their company in the future.

41

Weakness - Threat

Joint venture with international bank

(W1. Core business focusing on ASEAN countries, T2. Competition

from international bank)

As CIMB Group main focus is their businesses in ASEAN countries,

they are faced with competitors from international banks that

have a larger customer base compared to the Group. Those

international banks such as Standard Chartered have a wide

coverage of customers from all over the world. By joining venture

with those international banks, they could reduce their

competitors as well as gaining access to customers

internationally and the knowledge of those international banks.

42

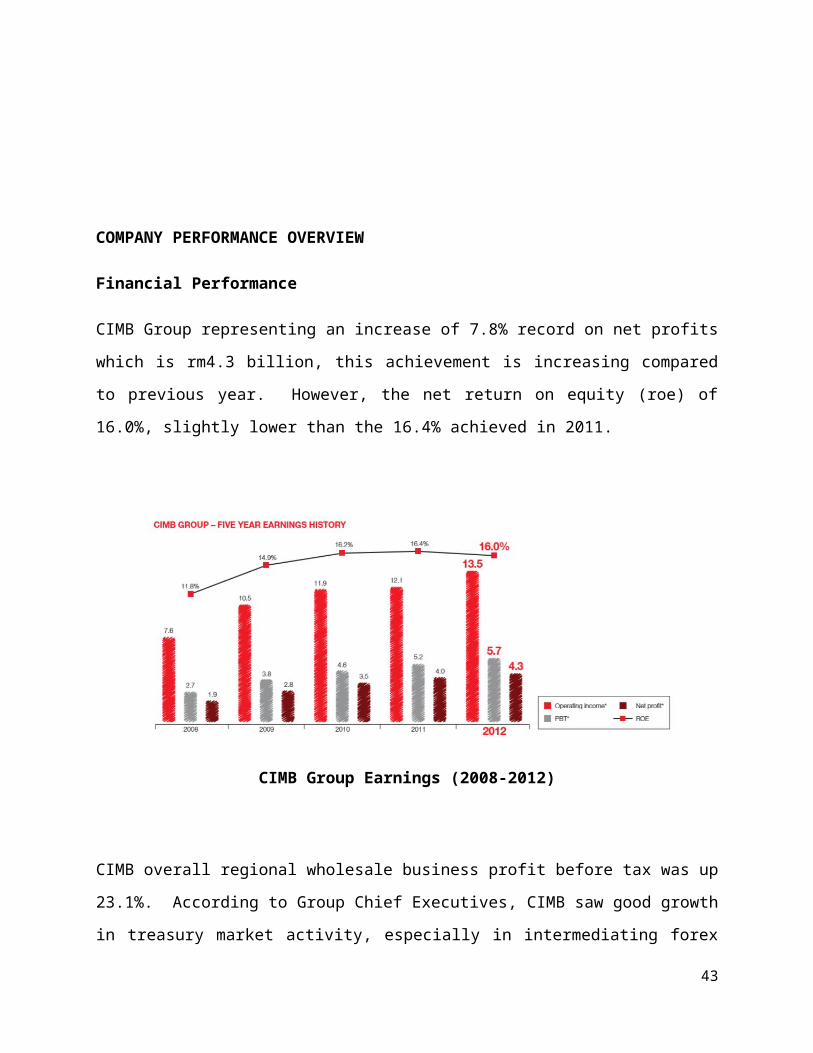

COMPANY PERFORMANCE OVERVIEW

Financial Performance

CIMB Group representing an increase of 7.8% record on net profits

which is rm4.3 billion, this achievement is increasing compared

to previous year. However, the net return on equity (roe) of

16.0%, slightly lower than the 16.4% achieved in 2011.

CIMB Group Earnings (2008-2012)

CIMB overall regional wholesale business profit before tax was up

23.1%. According to Group Chief Executives, CIMB saw good growth

in treasury market activity, especially in intermediating forex

43

flows across the region and had an excellent year in regional

capital markets. Even though the profit before tax of CIMB

Niaga, CIMB Thai and CIMB Singapore grew but the CIMB Singapore

securities operations lost RM8 million due to low market volumes

and higher cost. In 2012, the higher growth rates of CIMB mainly

from non-Malaysian entities as the total non-Malaysian profit

before tax increased to 41% of the Group’s total compared to 36%

recorded in the previous year. In conclusion, CIMB have recorded

good performance by the increasing of operating income and net

profit from year 2008 until the year 2012, as the CEO Dato’ Sri

Nazir Razak have been awarded a second ranking in Institutional

Investor’s survey for Asia’s Best CEO (Bank) in 2008 and in 2012

he has been awarded a “LIFETIME ACHIEVEMENT AWARD” due to his

contribution to Asian banking and finance.

Investment Banking

CIMB maintained position as ASEAN’s top investment bank while

revenues increased by 16.1% and profit before tax by 18.3% in

year 2012. CIMB led three of the global top 10 initial public

offerings (IPO) in 2012. These were the RM10.4 billion IPO for

state-run palm oil planter Felda Global Ventures (also the

largest IPO in Malaysia), RM6.7 billion IPO for Asian hospital

operator integrated Healthcare and RM4.6 billion IPO for cable TV

operator Astro Malaysia.

In 2012, expand the business through acquisitions. These new

acquisitions are involving lots of cost but CIMB is convinced

44

that they will prove astute as leverage on the enlarged platform

not only for investment banking revenues but also in synergies.

CIMB integrated operations after the acquisition of the Royal

Bank of Scotland (RBS) and Asia Pacific Investment Banking (APAC

IB) platform, they win in the bookrunners in Singapore’s as

second largest IPO, for religare Health Trust of india, which

raised SGD511 million, and China machinery engineering Corp’s

HKD4.4 billion IPO.

CIMB maintained as market leadership in 2012 by topping the

league table in stock broking, IPO and equities Capital markets

(ECM). In Singapore CIMB good progress as number one in IPO and

stock broking as well as in Thailand CIMB also topped the IPO

league table. Thus, in 2012, CIMB were the number one in IPO and

ECM in ASEAN.

Share Price Performance

Although management is pleased with the Group’s performance and

financial results, CIMB share price continued to underperform.

Over 2012, CIMB Group’s share price increased by only 2.6% from

RM7.44 on January 2012 to RM7.63 on 31 December 2012. CIMB share

price underperformed against the KLCi and KL financial index

(KLfin) by 7.8% and 9.5% respectively.

The reason of CIMB weak stock performance is the key valuation

matrices relative to peers. CIMB have to improve expectations of

near term roes and key ratios especially those relating to cost,

capital and asset quality. At the same time though, they unable

45

compromise on long term value creation which sometimes draws on

near term costs and capital and adds uncertainties and

complexities to the business.

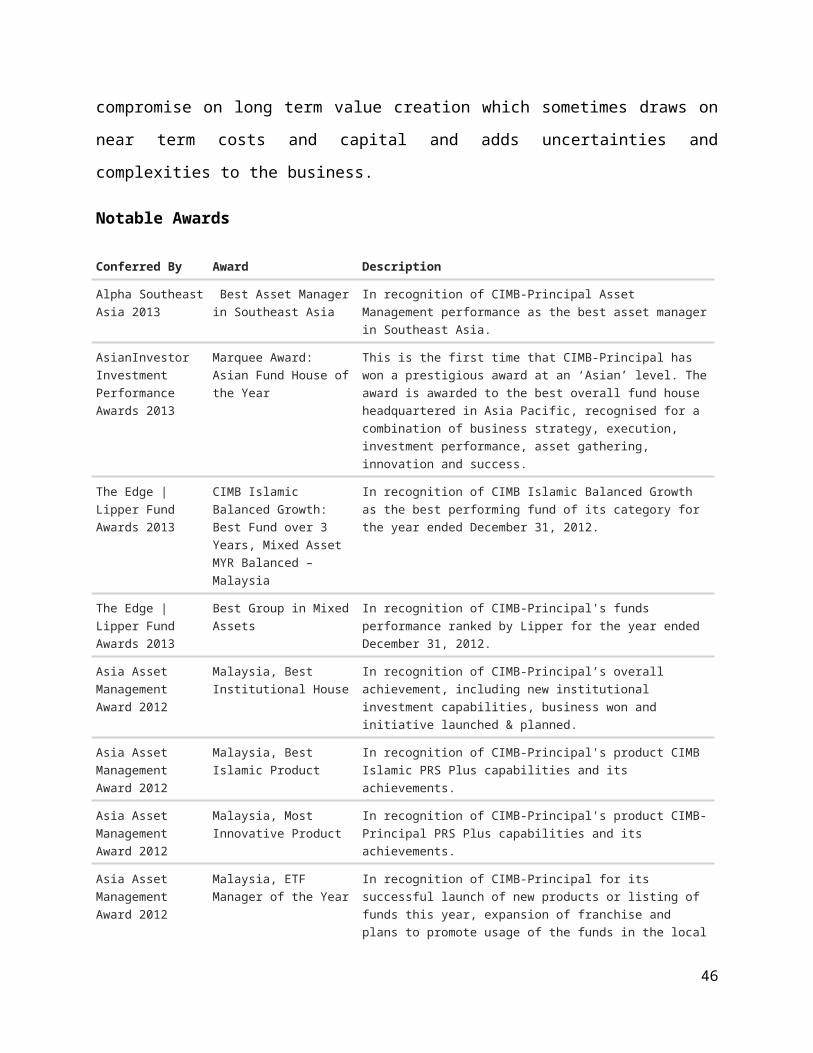

Notable Awards

Conferred By Award Description

Alpha SoutheastAsia 2013

Best Asset Managerin Southeast Asia

In recognition of CIMB-Principal Asset Management performance as the best asset managerin Southeast Asia.

AsianInvestor Investment Performance Awards 2013

Marquee Award: Asian Fund House ofthe Year

This is the first time that CIMB-Principal has won a prestigious award at an ‘Asian’ level. Theaward is awarded to the best overall fund house headquartered in Asia Pacific, recognised for a combination of business strategy, execution, investment performance, asset gathering, innovation and success.

The Edge | Lipper Fund Awards 2013

CIMB Islamic Balanced Growth: Best Fund over 3 Years, Mixed Asset MYR Balanced – Malaysia

In recognition of CIMB Islamic Balanced Growth as the best performing fund of its category for the year ended December 31, 2012.

The Edge | Lipper Fund Awards 2013

Best Group in MixedAssets

In recognition of CIMB-Principal's funds performance ranked by Lipper for the year ended December 31, 2012.

Asia Asset Management Award 2012

Malaysia, Best Institutional House

In recognition of CIMB-Principal’s overall achievement, including new institutional investment capabilities, business won and initiative launched & planned.

Asia Asset Management Award 2012

Malaysia, Best Islamic Product

In recognition of CIMB-Principal's product CIMB Islamic PRS Plus capabilities and its achievements.

Asia Asset Management Award 2012

Malaysia, Most Innovative Product

In recognition of CIMB-Principal's product CIMB-Principal PRS Plus capabilities and its achievements.

Asia Asset Management Award 2012

Malaysia, ETF Manager of the Year

In recognition of CIMB-Principal for its successful launch of new products or listing of funds this year, expansion of franchise and plans to promote usage of the funds in the local

46

market and how the firm is promoting the greateruse of ETFs in general.

Leveraging Social Media

CIMB Group continues to have the largest facebook fan base in

ASEAN, at over 1.5 million, and is the most ‘liked’ bank in the

region. Social media has become a crucial channel for CIMB to

engage with their customers. CIMB leveraged on the platform of

internet banking portal, CIMB clicks, to create octopay, ASEAN’s

first banking service on facebook.

Octopay leverages on social interactions with users of CIMB

Clicks on facebook by providing innovative services such as money

transfers, airtime reloads and internet reloads. CIMB Group

achieved another milestone in the social media space when we

launched the Savings Circle, the world’s first fully integrated

bank deposit campaign on facebook. Leveraging on facebook,

Savings Circle attracts facebook users with prizes and reward

them and their friends for saving together.

47

RECOMMEDATION

Expand their banking service

CIMB group is a universal bank headquarters in Kuala Lumpur and

now operating in high growth economies in ASEAN. Meaning now all

of their banking service is primary focus at the ASEAN countries.

As now, the company has penetrate almost all the countries in

ASEAN. It is important for the company to expand their banking

service outside their own territory turf. They should try to

further their service into other region such as the European and

48

South American region to increase their company revenue. The

European and South American can be considered as one of the big

emerging market in the banking service, so CIMB group has to take

this opportunity to expand their business in that region.

Enhanced their corporate alliance

It is very important for a company to have a great alliance with

another company to strengthen their company. Besides that, by

having a partnership the CIMB group geographical reach and its

product or service can be improved and this can be complemented

by their partnership. As now the group partnership includes the

Principal Financial Group, Bank of Tokyo-Mitsubishi UFJ, Standard

Bank and Daewoo Securities. In 2012, the company has joined force

with new partner that is the Rohatyn Group. Touch ‘n Go, and also

John Keells Stock Brokers. All of this partnership is very

important to realising the company to expand their business

further.

Effective risk management

As a big entity company, it is only natural a company such as the

CIMB group itself to face a risk in their line of business. A

robust and effective risk management system is critical for a

company to achieve continues profitability and to sustain their

growth in the international market and increased their market

share. For a company that focuses in the banking service and

involve with a lot of money, there are many risk that can affect

them such as credit risk, liquidity risk, and operational risk

49

and also in the interest rate risk. The company has to make sure

that they have an effective strategy in avoiding those risks.

CONCLUSION

CIMB group is a company that involve in the business of banking

service. The group is a regional universal bank that focuses on

ASEAN as it core market. Through recent year, they have

strengthened their business in all the ASEAN regions. With their

various banking service such as the Islamic banking and the

investment service that they have provided has made them a very

popular choice among the people not only in Malaysia but also the

foreign people to perform their banking service.

As for now, the group have already has their own branch in almost

of the ASEAN countries. The group now has to make several

strategies to expand their market share in another region such as

the European and also the South American. This region is

considered to have many opportunities that can allow them to

further expand their business. By doing this, not only they can

compete with other big company in the banking service but also

will be well known throughout the world.

50

51

REFERENCES

CIMB Group Holdings Berhad, 2008, CIMB Annual Reports. CIMB

Group.

CIMB Group Holdings Berhad, 2009, CIMB Annual Reports. CIMB

Group.

CIMB Group Holdings Berhad, 2010, CIMB Annual Reports. CIMB

Group.

CIMB Group Holdings Berhad, 2011, CIMB Annual Reports. CIMB

Group.

CIMB Group Holdings Berhad, 2012, CIMB Annual Reports. CIMB

Group.

Bank CIMB Niaga, 2009, Merger Process and Achievement Report.

CIMB< 2012, CIMB Completes Asia Pacific Investment Banking Platform

with RBS Acquisition.

Hunger, David J. & Wheelen, Thomas L., 2010, Strategic Management and

business policy, Upper Saddle River, N.J : Pearson Prentice Hall

Firdaus Ghalba and Harimukti Wandebori, 2013, Propose Business

Strategy Formulation For CIMB Niaga Syariah, The Indonesian Journal Of

Business Administartion.

CIMB Official Website, 2013. Retrieved from

http://www.cimbbank.com.my

52

53