Embed Size (px)

Citation preview

1

STRATEGIC MANAGEMENT AND DEVELOPMENT OF STRATEGIC

MANAGEMENT APPROACH IN TURKEY

Hasan CANPOLAT Governor, Deputy Undersecretary Ministry of Interior Ankara-TURKEY Tel: +90 312 425 4282 [email protected] Ahmet KESĐK Director General of Strategy Development Unit Ministry of Finance Ankara-TURKEY Tel: +90 312 415 12 17 [email protected]

Abstract

Public finance became one of the most important areas in Turkey where structural

reforms were put into implementation. Public Financial Management and Control Law No.

5018 was enacted in 2003. Radical changes were made in the public financial management

system which have been in effect for long years.

This paper examines the development of the “strategic management” concept which is

one of the most important parameters that has evolved in line with the objective of “endowing

public sector with a competitive structure in accordance with the requirements of the global

economy” in the world for the past 25 years and in Turkey since the 2000’s and the process of

realization of this concept in Turkey.

Keywords: Accountability, Budgeting, Public Management, Public Sector Reform,

Strategy

Word Count: 7752

2

STRATEGIC MANAGEMENT AND DEVELOPMENT OF STRATEGIC

MANAGEMENT APPROACH IN TURKEY

Introduction

One of the main issues that have been discussed in Turkey and many other countries

for the last fifty years is the question of how to adapt to unprecedentedly rapid global changes.

Within this framework, public management reforms came to the fore among the current

issues.

On the other hand, the mechanisms for transition to the minimal state from the

interventionist state which emerged in the post-war period were provided by the reforms

resulting from the New Public Management (NPM) approach of which the intellectual basis

was largely formed by the new right and which is widely accepted in many countries.

The basic approach of the new right ideology which was highly visible in the 1970s is

that the state should define the rules of the game in the market and put them under the

protection of laws, but it should not intervene into the market by providing goods and

services.

The NPM model that was shaped on the basis of these basic approaches is also a

market-based model and the main purposes of the NPM reforms are as follows (Hughes,

1994: 3):

• To improve public service quality

• To ensure more effective, economic and efficient public services

• To reduce public expenditures

• To improve and develop state-citizen relations

• To meet citizens’ increasing demand for public services

3

• To endow the public sector with a competitive structure in line with the

requirements of the global economy

The NPM which is considered as a solution to many problems experienced in public

management offered important instruments in the early globalization period for especially

privatization practices and transition to the minimal state. In this context, a series of reforms

were launched in Europe, the USA, Australia and especially the UK as of the 1980s. These

reforms were then spread from these countries to many developing countries with the help of

international organizations.

However, the states that faced serious problems due to the spread of the global crisis

throughout the world as of the 2000s when the globalization gained momentum and that failed

to overcome these problems and thus the new public management and its arguments started to

be criticized intensively.

The financial crisis that broke out in the USA in the summer of 2007 turned into a

global economic crisis in the second half of 2008. During the global crisis, the world economy

experienced the worst contraction in 60 years and the world trade faced the worst contraction

in 80 years. Unemployment rates nearly doubled in many developed countries in the last two

years. Capital flows to the developing countries was in negative territory for the first time

after 24 years.

State intervention was regarded as the only solution for an effective fight against the

global crisis and many countries increased their public expenditures to an unprecedented

extent in recent years. The share of public expenditures in the GDP has increased by at least 5

points in many countries in the last two years.

In addition, public revenues decreased sharply due to economic contraction; the share

of public debt stock in the GDP has increased by 20 points in the last two years; and the bank

4

balance sheet problem faced at the beginning of the crisis has eventually become the public

sector balance sheet problem.

It is seen that during the crisis the state interfered in private markets to this extent for

the first time in the last quarter, injected capital to banks in order to resolve the balance sheet

problem of the banks and became a partner in failing companies in order to save these

companies.

As a result, it is understood that it will take a long time to decrease extraordinary

budget deficits and public debt stocks to the pre-crisis levels and it is required to review the

functions of the state and thereby the key concepts of strategic planning, strategic

management and public financial management that frequently come to the fore recently.

In this respect, when the pre-crisis period is considered, it is seen that the strategic

management principles were superficially put into effect in many countries, and countries

allocated large amounts of resources for service sector, R&D, innovation and infrastructure in

order to increase economic growth, welfare and competitiveness of the economy in a period

when liquidity was abundant, expectations peaked and the global economic growth

continuously increased. So it can be said that the worm was in the apple from the start.

However, in that period effectiveness and efficiency which are the basic elements of

strategic management approach were ignored, fiscal spaces were created in the budgets,

transparency was ignored and accounts were fiddled and input-output relation in the use of

public resources disappeared. In addition, strong organizational structures were weakened for

sake of minimal state or in some countries such a structure could never be established and

thus the importance of a strong and effective public management that can implement and

supervise rules was ignored.

5

1. Efforts for Transition to an Effective Financial Management in Turkey

Efforts for a systematic reform to public management in Turkey can be dated back to

the 19th century. The reform efforts launched in that period continued in a stronger way with

the proclamation of the Republic in 1923 and many important regulations were made in this

scope. However, the regulations made before the plan period of the early 1960s cannot be

considered as part of a systematic programme based on strategic objectives, but as efforts to

solve problems based on reports prepared by domestic and foreign experts on the required

subjects.

During the plan period, on the other hand, it was decided to prepare a strategic plan

based on comprehensive research reports, but this decision could not be successfully put in

effect. As a result, such problems as over-centralization and organizational over-growth,

corruption, inefficiency, introversion, non-accountability and visionlessness that were

detected in public management became greater in time and had considerable effects on public

management service quality.

However, it can be said that during public management reforms period in Turkey the

most comprehensive and consistent approach introduced by the NPM approach was the Law

on Basic Principles and Restructuring of Public Management (KYTK).

The use of “a different language” in the KYTK shows that the Law is different and

that the public management reform was made with a new approach. The use of “public

management” concept instead of the traditional “administration” concept in the draft law is a

clear sign of that. It was not until the KYTK that this term was used in any Constitution or

law. The use of public management concept in the new Law points to the direct effect of the

“new public management” approach and the Anglo-American public management model on

the reforms and to divergence from the Continental Europe in terms of management tradition

(Azrak, 2004: 225).

6

In addition to the use of public management concept instead of administration concept,

the draft law included lots of concepts which are new in the administrative legislation despite

being frequently used by public management experts. For example, concepts like transparent,

accountable and participatory management driven by human rights and freedoms that are

frequently used by pubic managers and considered among the basic operational principles of

the administration are listed in the first article of the KYTK as the basic principles of public

management that should be established.

In addition, “determination of duties, authorities and responsibilities of central and

local administrations for fair, rapid, good quality, effective and efficient delivery of public

services” is mentioned in the remaining part of the article. The use of such concepts in legal

texts shows that the draft law has “a different language” that is inspired from the new public

management approach (Demir, 2008).

It is possible to make some points when the public management reforms that gained

momentum in the late 1980s and the KYTK were considered together. Firstly, it is obvious

that these reforms were inspired from the NPM approach which is accepted worldwide.

Secondly, due to the conditions pertaining to Turkey, reforms were not based on an approach

that directly gets to the bottom of problems and produces permanent structural solutions, but

an approach based on a more effective public financial management and on economic

liberalization. Within the framework of this approach, the reforms to economic management

significantly accelerated and realization of “minimal state” approach by reducing intervention

of the state in the economy became one of the most basic economic policies within the reform

period of the last 30 years.

When the reforms that accelerated in the 2000s were considered as a whole, the

desired results can be summarized as follows:

7

• Improving the processes of planning, policy-making, decision-making and

resource allocation,

• Strengthening accountability and transparency in public management,

• Increasing operational capacity of public agencies and ensuring cost-efficiency,

• Focusing on regulatory and supervisory function of the public sector,

• Rationalizing commercial activities of public enterprises,

• Strengthening local structures.

2. Restructuring of Public Financial Management

The early 1990s when public management reforms were discussed intensively in

Turkey is a period when budget deficits rose to higher levels, borrowing requirements of the

government increased and inflation rate reached historical high levels.

It can be said that in this period discipline could not be maintained in public finance

and almost half of the budgetary expenditures were made through off-budget schemes without

parliamentary control (Kesik, 1999: 97-98).

Under these circumstances, awareness was created on restructuring of public financial

management and the Public Financial Management Project was launched to this end in 1993

under the coordination of the Ministry of Finance. Within the scope of this project, efforts

were made and proposals were offered in various fields like budget scope, budget execution,

debt management, accounting, financial statistics and management information system, but no

step could be taken in terms of reforms due to lack of sufficient political will.

The structural reform process in Turkey started with the IMF stand-by agreement

signed in the late 1999 and the PEIR (Public Expenditures and Institutional Review) prepared

by the World Bank together with the public bureaucracy in 2000, and it gained momentum as

of the 2002 year-end.

8

After lessons learned from this process, public finance became one of the most

important areas where structural reforms were put into implementation, and the Public

Financial Management and Control Law No. 5018 enacted at the end of 2003 brought about

radical changes in the public financial management system which had been in effect for many

years in Turkey. Within this scope, extra-budgetary funds were included in the budget and

cleared as of 2000 and special income and special appropriation incurred by these funds were

terminated as of 2005.

Moreover legal and institutional infrastructure of public debt management was

strengthened and guarantee and borrowing limits were defined with the Law on Regulation of

Public Financing and Debt Management. In this regard, Treasury guarantee was set as a

condition for external borrowing of public agencies and risk account was put into

implementation. Transparency was increased through envisaging regular reporting of public

debt management results to the Parliament and the public.

The Law No. 5018 aims at ensuring budget unity, to underlining fiscal transparency

and accountability as well as efficient, effective and economic use of public resources and

establishing strategy-oriented organizations by bringing a long term perspective to public

management. As a result of this, medium term programme and plan, strategic plan,

performance programme and multi-year budgeting, accountability, transparency, efficient,

effective and economic use of resources, and forecasts based on sound and accurate are

considered as the important novelties introduced by the new system.

The Law No. 5018 was designed in a way to include new financial management and

control principles which are tried to be implemented in the OECD and EU countries, and

provides important tools for public managers in terms of managerial responsibility for

efficient and economic use of resources and medium term allocation and use of public

resources.

9

3. Increasing Predictability: Evolution of the Medium Term Expenditure System

The regulation on the medium term expenditure system is involved in the Law No.

5018 in Turkey. The Law sets forth the fundamental components of the medium term

programme1, medium term fiscal plan2, strategic plans, performance programmes and the

medium term expenditure system.

Furthermore, the Law No. 5018 makes several references to the multi-year budgeting.

The Law stipulates that:

• The budgets shall be prepared, implemented and controlled in conformity with the

policies, targets and priorities envisaged in the development plans and programmes, and

according to the strategic plans, performance criteria and cost-benefit analysis of the

administrations.

• Budgets shall be negotiated and evaluated together with the budget estimations of

the next two years by considering strategic plans.

• Central government budget law shall include revenue and expenditure estimations

of the first year and following two years.

• Multi-year budgetary approach consistent with strategic plans of public

administrations shall be taken into account in developing revenue and expenditure proposals.

• Last two years’ budget realizations and next two years’ revenues and expenditures

estimates of public administrations within the scope of general government shall be attached

to the central government budget draft law.

The necessary legal ground for the medium term programme and medium term fiscal

plan, which are the most important components of the medium term expenditure system, is

constituted with the Law No.5018. Pursuant to the legislation, public administrations should

prepare their budgets for the next three-year period by determining their own institutional

priorities and within the framework drawn with the medium term programme and medium

10

term fiscal plan. However, in practice, public administrations are seen to prepare their budgets

for the next two years by just increasing their appropriations at certain rates instead of

adopting a multi-year perspective and approach. Moreover only the budget for the next year is

negotiated and evaluated during draft budgets negotiations with central institutions and in

budget negotiations in the Turkish Grand National Assembly (TGNA), whereas budget

estimates for the following two years are not discussed.

4. Search for an Efficient Management: Strengthening Strategic Planning Process

Functionality of strategic plans depends on whether the strategic plan goals and

objectives requiring a certain cost among the others are involved in the budgets. Priorities of

the governments take their places in strategic plans. Preparation of budgets on the basis of

strategic plans also means that governmental priorities are correlated with resource allocation.

Furthermore, strategic plans should be prepared in line with the priorities determined

in development plans, medium term programmes and plans and regional and sectoral plans

and programmes, i.e. in top policy papers. In other words, administrations should include

goals and objectives that will ensure realization of policies and priorities defined in the top

policy papers in their strategic plans.

So far, such regulations have been perceived as an aim rather than a tool in many

countries including Turkey and taken their places within the public management in this sense.

In this regard, it is necessary to dwell on results of perception of such institutional regulations

developed in order to ensure efficiency in public sector as an aim rather than a tool. When

these regulations are perceived as an aim, this topic transforms into a document management

issue, new applications are developed which are very successful technically and have internal

consistency, studies are carried out and documents are prepared in accordance with the

conditions (like SWOT analysis) determined through the legislations required by the new

11

strategic management system, and best practices and then these studies and documents are

publicized.

However such a problem emerges here that these documents cannot go further than a

document that is not shared by all horizontal and vertical management processes, is not

internalized by the public administration, handles the issues in relatively shorter terms,

focuses on activities rather than strategy (such as number of meetings, number of conferences

to be held, number of employees to attend trainings, and etc.) and much more importantly that

includes routine activities that the organization is readily making.

However, strategic management process should be an application that covers strategic

priorities. What should be asked here is what these strategic priorities are. These strategic

priorities should focus on the areas that make life easy for everyone in the country by

analyzing global economy and global competitive system that include real risks at state and

society level and by producing solutions that can serve critical priorities (improvement of

income distribution, opportunities provided for the elderly, objectives for the children in the

poor section of the society, measures against global warming, objectives for improving

business environment, educational objectives, etc.) on the scale of state and agency to

predefined long term challenges.

Therefore, if we want to get the expected result from strategic management in Turkey,

we should avoid wrong implementations listed above. Otherwise, confidence in the

mechanisms introduced by the new approach may weaken.

Another matter that should be elaborated is that strategic priorities are overabundant.

Overabundance of strategic priorities may transform the strategic objectives into a list of

intent. 600 objectives that were set in England many years ago were first decreased to 160,

then 120 and now to 30 (Barber, 2007: 132-134). These objectives are national and distributed

among the institutions by relevance.

12

Distribution of responsibility here is determined as the institution which is mainly in

charge, and the institutions to be cooperated. These objectives are embraced not only by

central administration but also by local administrations and even non-governmental

organizations. Such low number of objectives ensures the institution to focus on specific and

few objectives both in terms of public resources and policies, activities and institutional

capacity.

In Turkey, there are many policy papers such as development plan, medium term

programme, medium term fiscal plan and annual program. In fact, the opportunity of focusing

on fewer objectives can be created, efficiency of public resources can be enhanced, and more

effective results can be achieved from public activities by decreasing the number of policy

papers and combining other policy papers, except for development plan.

On the other hand, current problems cannot be differentiated from global problems

and developments. Economic power balances in the world necessarily affect the policies of

each country. However, what draws our attention here is the fact that challenges resulting

from both internal and external conditions (social security, social protection, healthcare,

education, industry, SMEs, etc.) will affect national economies for many years. Thus, it is

necessary to design policies with 40-50-year perspectives, to determine objectives and

accordingly, to develop public organizations.

Even though the Law No. 5018 envisages strategic plans for a five-year period, the

capacity of Turkey to make much longer term strategic plans on specific strategic priorities

will foster solution of certain problems in an easier and shorter manner. For instance, Ireland

is among the leading countries on the quality of educational services. On the other hand, it is a

widely known fact that its physical infrastructure is inadequate. For this reason, this country

has considered 3-year strategic plan as sufficient for the department of education while

making 30-year strategic plan for the department of transportation.

13

Thus, it is necessary to act in a strategic manner by means of utilizing available public

administration instruments according to the strategic priorities in order to achieve results in a

sounder way in terms of each institution and each sector. Otherwise, making 5-year plans only

to comply with the legislation will not go beyond fulfilment of formal terms of the legislation.

As indicated in the example above, investments in the transportation sector have become

strategic for Ireland, and preparation of a 30-year plan has become necessary for the state

welfare and development. For this reason, strategic management cannot be performed only to

comply with the legislation.

4.1. Institutional Strategic Plans

Public administrations are envisaged to prepare strategic plans with participatory

methods in order to define their missions and visions for the future; to determine strategic

goals and measurable objectives; to measure their performances in line with the indicators

defined previously, and to monitor and evaluate this process within the framework of

development plans, programmes, relevant legislation and basic principles they adopt.

The Undersecretariat of State Planning Organization is authorized to determine public

administrations to be responsible for preparing strategic plans and the schedule for transition

to strategic plan, and other principles and procedures for strategic plan. Pursuant to this

authority, the Undersecretariat issued By-Law on the Procedures and Principles for the

Strategic Planning in Public Administrations and Strategic Planning Guide.

Strategic Planning Guide provides a general framework for the strategic planning

process, and scope and content of the strategic plans. The concept of strategic planning is used

in a broad sense in a way to involve the whole strategic management process and expressed in

four steps. Public administrations are envisaged to shape the titles and subtitles by considering

their own structures whereas they should adhere to main principles in and general structure of

the guide. Thus, it starts with the question of where we are; then states where we want to go;

14

continues with how we can move from today to the desired future; and measures the success

attained at the final stage.

In Turkey, public administrations prepare and publicize their strategic plans as

required by the legislation. However, in some public administrations, top management

perceives the strategic plans as an intent document that should be prepared as envisaged by

the Law rather than a policy paper that will steer activities.

Failure of the top management to embrace the strategic plans damages faith and

confidence of the staff in the strategic plan and decreases their motivation. In addition,

difficulties experienced by the staff in adoption of the new mentality and behaviours

introduced by the strategic management approach should not be ignored.

4.2. Institutional Performance Programmes

It is resolved that public administrations will prepare performance programmes that

include activities and projects they will carry out and required resources, and their

performance objectives and indicators. In this respect, it is also resolved that public

administrations will prepare their budgets in consistent with the mission, vision, strategic

goals and objectives defined in their strategic plans and in a performance-based way. In

accordance with the relevant article, the Ministry of Finance is authorized to make the

necessary regulations for the performance-based budgeting. Pursuant to this authority, the

Ministry issued By-law on the Performance Programmes to be Prepared by the Public

Administrations and Performance Programme Preparation Guide.

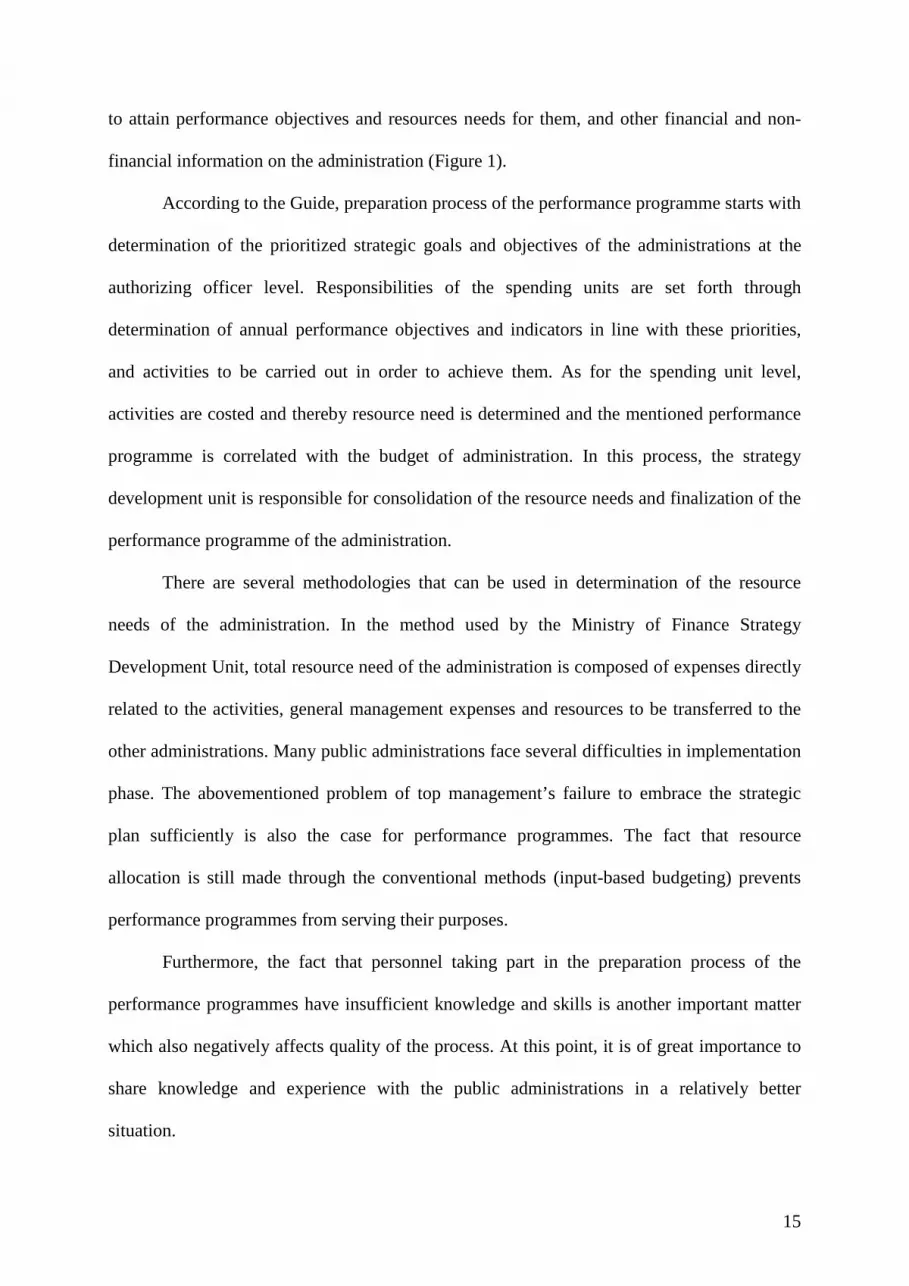

As required by the By-law on the Performance Programmes to be Prepared by the

Public Administrations, it is envisaged that performance programmes shall be prepared by the

top manager at the administration level in coordination with the strategy development unit and

with the participation of authorizing officers in a way to include performance objectives and

indicators of the administration for the programme period, activities to be carried out in order

15

to attain performance objectives and resources needs for them, and other financial and non-

financial information on the administration (Figure 1).

According to the Guide, preparation process of the performance programme starts with

determination of the prioritized strategic goals and objectives of the administrations at the

authorizing officer level. Responsibilities of the spending units are set forth through

determination of annual performance objectives and indicators in line with these priorities,

and activities to be carried out in order to achieve them. As for the spending unit level,

activities are costed and thereby resource need is determined and the mentioned performance

programme is correlated with the budget of administration. In this process, the strategy

development unit is responsible for consolidation of the resource needs and finalization of the

performance programme of the administration.

There are several methodologies that can be used in determination of the resource

needs of the administration. In the method used by the Ministry of Finance Strategy

Development Unit, total resource need of the administration is composed of expenses directly

related to the activities, general management expenses and resources to be transferred to the

other administrations. Many public administrations face several difficulties in implementation

phase. The abovementioned problem of top management’s failure to embrace the strategic

plan sufficiently is also the case for performance programmes. The fact that resource

allocation is still made through the conventional methods (input-based budgeting) prevents

performance programmes from serving their purposes.

Furthermore, the fact that personnel taking part in the preparation process of the

performance programmes have insufficient knowledge and skills is another important matter

which also negatively affects quality of the process. At this point, it is of great importance to

share knowledge and experience with the public administrations in a relatively better

situation.

16

Using performance programmes as an instrument for approval and auditing of the

public administration budgets by the TGNA may carry these documents to the mentioned

critical and significant position. Otherwise, performance programmes cannot go beyond

creating an additional workload for the public administrations and public administrations

cannot get the expected benefit from them.

4.3. Monitoring and Evaluation

Public administrations measure their performances according to the predetermined

indicators; and monitor and evaluate this process.

In practice, monitoring and evaluation practices only take place on the paper; impacts

and outcomes of the activities, projects, programmes and policies are not evaluated; and cost-

effectiveness analyses are not conducted.

Major problems experienced in practice are as follows: some difficulties are

experienced in obtaining performance information during monitoring and evaluation process;

all stages for the process of service delivery cannot be involved into the scope; managerial

responsibility is overshadowed by the financial responsibility; a certain methodology is not

determined for the monitoring and evaluation and finally results obtained from the monitoring

and evaluation process are not taken into account in decision-taking process.

Monitoring and evaluation should be beneficial for all partners; should focus on some

critical points of the performance; should be simple, cost-effective, available and practical;

and should be implemented in a way to include both financial and nonfinancial information.

5. The Ministry of Finance Case

Considering both regulatory role of the Ministry of Finance and its leading position, it

will be beneficial to touch upon practices of the MoF for medium term expenditure system at

the administration level.

17

MoF handles the medium term expenditure system with a systematic approach on the

institutional basis. In general, MoF Strategic Management System includes the followings:

• Strategic plans prepared in five-year periods

• Performance programmes which are annual implementation of the budgets prepared

in accordance with the strategic plans,

• Monitoring and evaluation of the performance objectives and indicators envisaged

in the performance programmes, and

• Accountability reports indicating performance results of the Ministry (Figure 2).

In the MoF, strategic management practices are carried out through the MoF SGB.net

system. “Performance budget module” constituting infrastructure of the performance

information system within the SGB.net system has a cascading structure beginning from the

mission and vision of the Ministry and descending to the activities defined in the performance

programmes.

Ministry of Finance Strategic Plan for 2008-2012, which is the first component of the

strategic management system of the MoF, includes medium and long term objectives of the

ministry and strategic indicators for measuring these objectives. In preparation of the Ministry

of Finance Strategic Plan, both top policy papers and administrative priorities were taken into

consideration; and each strategic objective was correlated with the axes in the Ninth

Development Plan (Figure 3).

Ministry of Finance Performance Programmes, which is the second component of the

strategic management system, have been prepared and publicized within the budget process

since 2008. In the performance programme of the Ministry, performance objectives and

indicators, and activities of the ministry and costs for these activities are determined; and

plan-programme-budget relation is tried to be set forth.

18

It is of utmost importance to exhibit and evaluate implementation results in order to

increase efficiency of the strategic planning and performance programme processes. In this

regard, monitoring and evaluation system is an important part of the strategic management

system of the MoF.

Within the scope of monitoring and evaluation, performance objectives of the Ministry

units and realization values of the performance indicators they determined for these objectives

in the performance programme are entered into the MoF SGB.net system by the units

quarterly in a year. Monitoring and Evaluation Reports prepared as a result of evaluation of

the performance information are submitted to the top management.

Furthermore, an application was developed in order to monitor and evaluate activities

carried out within the scope of the performance programme and expenditures related to these

activities. Therefore, it will be possible to immediately monitor expenditures related to

activities in a year and to connect periodical realizations of the performance indicators with

the expenditures.

Final component of the strategic management system is the accountability reports. In

the Ministry of Finance Accountability Report for 2008, realization status of the objectives

and indicators defined in the performance programme, deviations from them and reasons for

deviations have been included for the first time; and thereby an important step was taken in

terms of accountability.

Furthermore, the Strategy Development Unit started to implement a structure

(Cascading) which descends from operational planning, which is an important step of the

strategic management system, and terms of reference as well as aims and objectives referred

in the strategic plan to the duties and responsibilities to be fulfilled on the basis of units. After

this system is put into effect by other units of the Ministry, the authorizing officers will be

able to follow-up business processes and personnel’s responsibilities. At the end of this

19

process, it is aimed to measure performance in the public administrations on the basis of

works and persons and thus, to establish a structure which will enable performance

contracting.

It will be possible to measure effectiveness of the abovementioned practices

implemented with the strategic management system through the data to be obtained as a result

of the monitoring and evaluation system. This brings forward a question on the effectiveness

of monitoring and evaluation. The fact that the framework of the legislation on the monitoring

and evaluation system is not determined and there is not a system accepted in this area

constitutes one of the most important challenges of the monitoring and evaluation system

implemented in the Ministry. In addition, it became impossible to obtain comparative data

because target values of the performance indicators are revised and redesigned annually and

indicators followed-up for one year are excluded from the scope of monitoring and evaluation

the following year.

6. Strategic Management and Change Management

Within the framework of the public financial management reform, it became necessary

that public administrations prepare their strategic plans in compliance with the national plans

and strategies, in this way, express their policies and strategies clearly, prepare budgets

consistent with these policies and strategies and measure their success by means of the

performance indicators to be developed. Transition from input-oriented traditional budgeting

to output/outcome-oriented budgeting has become the natural outcome of this approach in the

public financial management (Figure 4).

It is necessary to firstly develop administrative capacity and to establish the new

organizational culture in order to fulfil the purpose of ensuring efficiency and effectiveness in

the allocation and utilization of public resources. Otherwise, establishing institutions and rules

merely will not be enough.

20

In Turkey, public administrations need to complete newly introduced concepts with an

effective implementation. It is very important to comprehend and apply a new system in terms

of its meaning and content. The new financial management and control system should be dealt

as a management system, rather than a financial system. It will be possible to make a

considerable progress by elaborating and clarifying responsibilities of the financial

management and control concept.

Therefore, public administrations have important roles for applying the public

financial management system delegated to the Ministry of Finance for years in accordance

with the new approach. Furthermore, it should be highlighted that the Court of Accounts has a

significant task in the proper functioning of the new public financial management system.

It is possible to model efficient and effective utilization of the resources in public

administrations on three basic processes as policy formation, planning and budgeting in terms

of managerial success.

Policy-Plan Relation: Even though the policy formation responsibility belongs to

political authorities, the relation between policies and plans at the institution level is

established by means of strategic plans at the institutional level. The strategic plans

become top framework declarations as they are the basic documents which refer to the

aims and objectives of the institution in medium and long term. In the Turkish case,

institutionalization of the strategic plans in public administrations and their guidance

for the subsequent programs and budget documents are in the transition period yet. In

this sense, it is very important for the administrations to prepare their strategic plans as

top plan documents, which correspond to their visions and missions and guide their

activities, in accordance with the current resources and capacities in a dynamic

manner. These plans should be considered as the plan of its own administration, not

another one, and should be embraced.

21

Strategic Plan-Activity/Project Relation: This is the stage where the plans are

related with the activities and turned into concrete. Thanks to a practice based upon a

medium-term expenditure system, the budget is placed upon outputs after the activities

are determined. In this manner, as it was before, outputs, not inputs, will be focused in

the new system, and it will be possible to ensure allocation and utilization in

accordance with the aims and objectives of the administrations. Thus, the performance

programme will put the budget on a better ground.

Activity/Project Cost (Budget) Relation: In this stage, in establishing the activity-

budget relation, it is aimed to prepare the budget environment which will enable the

use of analysis like cost-benefit and cost-effectiveness for the selection of activities

and projects. The basic activities in this stage in the budget can be evaluated under two

subtitles;

•••• Firstly, choosing the best alternative through the cost-effectiveness and cost-

benefit analyses of the activities and projects which are pre-determined to

serve to the institutional strategic plan

•••• Secondly, revising activities/projects in the event that total costs of the

activities/projects exceed the budget ceiling, and thus prioritizing and

finalizing the program.

In conclusion, the model is based on an interrelated and coherent process which goes

from top policy declaration to the institutional strategic plan, from institutional strategic plan

to activities/projects, from activities/projects to budget. Therefore, what is important in the

budget process is not the inputs but to what extent that these inputs serve the policies,

objectives and activities and at which level that the related public agency produces service at

the end of the day. This should be considered important in terms of demonstrating how

service performance and financial performance are achieved in a measurable way.

22

Today’s strategic management approach envisages that the ministries determine their

priorities within the framework of long-term policies, allocate their resources in accordance

with institutional goals and objectives and set targets for enhancing their capabilities in terms

of basic policy and management capacity. The strategic plans set in accordance with the Law

No.5018 should be prepared in a manner that they cover the institutional policy priorities and

they are accessible. They should be put forward in compliance with the resource framework

and institutional capacity and prepared in such a way that they guide the subsequent periods.

The strategic management approach envisages that priorities and resources focus on

medium and long term policies in the administrations. Thus, it enables development of result-

oriented initiatives for the future, rather than solution of daily problems.

In this framework, strategic management in the ministries anticipates a system in

which administrative and financial responsibilities are determined in a structure that cascades

from top policy paper at government level to the business processes in the public

administration (Figure 5). The institutional responsibility framework for the realization of the

policy objectives in top policy papers is determined with the strategic plans prepared at

institution level. The public administration, on the other hand, should put forward the service

and responsibility framework of the units by means of the performance programs and work

plans prepared in parallel to the strategic plans. Compliance of the activities at unit level with

the objectives and priorities at top level is important in terms of the cascading hierarchical

structure of the strategic management.

For the ministries, it is very significant to relate goals and objectives with the service

units in the ministries. In this sense, the current implementation shows that the service units

cannot establish a relation between the administrative capacity and economic resource, and

the institutional goals and objectives. In this context, performance programs establish the

relation between strategic plan and budget. Distribution of the resources according to the

23

strategic priorities in the administrations is adversely affected by the fact that the activities

envisaged in the performance programs are not set in a manner that they serve goals and

objectives and that the program is not prepared on unit basis. To this end, the administrations

need to deal with the performance programs differently from their traditional manner of

working and to prepare their budgets on the basis of activities and in accordance with their

performance objectives.

Furthermore, establishment of the relation between the activities carried out on the

unit basis and the personnel in those units constitutes an important stage of this process. The

units should determine terms of reference, roles and responsibilities of the personnel and their

individual performance indicators through the work plans they will prepare. Thus, in order to

attain the objectives in the policy papers, responsibility framework of the personnel working

in the units will be determined.

In the measurement of the institutional financial performance and service performance

during the budget execution process and decisiveness of the policies within the period, it is

aimed to utilize resources according to the prioritized services.

What is important in the new budgeting approach is not the amount of the resource

allocated but achievement of the outputs and results obtained after the activities.

Accountability is based on this fact. In this sense, that the administrations relate the utilized

resources with the obtained outputs and results, in other words, the created public value will

help them departing from input-oriented approach.

The fact that the strategic management approach is part of the management processes,

this cannot be changed by means of legislative arrangements and this process requires a

change in mentality constitutes the most important challenges for the administrations. For this

reason, it is important to perceive the new structure as tools that will ensure administrative

effectiveness, rather than a requirement stipulated by the legal legislation.

24

After the strategic management is put into practice in the public administrations, it is

necessary to spread mentality change experienced in the top management to the rest of the

institution and thus, to re-define the existing business processes. For this reason, finalization

of this transformation will only be possible by adoption of the process by authorizing officers

under the leadership of the top management.

Conclusion

Even though the global crisis has been on the agenda for a long time, democratization,

transparency, accountability, predictability, an effective state structure which cannot be

fulfilled in many countries are not outdated, on the contrary, have become more important.

In this sense, taking into account the reforms which began to accelerate in the 1980s

and widened and deepened during the 2000s, Turkey needs to set a new reform strategy in

early 21st century. This reform strategy will be able to carry the country to the new century if

its assessments and directions are decided in an accurate way.

Developing a New and Comprehensive Reform Strategy: The Turkish bureaucracy

came into prominence by arguing that it would be founder of the system and pioneer for the

modernization. On the other hand, it could dedicate itself to maintaining the current situation

because of both the structural reasons that stem from the system and subjective ones that

result from the historical process. What needs to be questioned while putting public

administration into effect and what should be the subject of the reform is the role of

guardianship of the bureaucratic class and the conservative nature of the institutional

structures produced by this role.

The most important reason why comprehensive structural reforms cannot be made in

the public administration in Turkey is that the strict and conservative nature of the

bureaucratic structure has never been the target of the reforms. In other words, without

analyzing the position of the bureaucracy in the Turkish political structure in a healthy

25

manner3 and following a reform strategy which will save bureaucracy from the role as the

owner of the system and transform it to a legal-rational mechanism and ensuring

democratization of the state, it is inevitable for all reform attempts that start with goodwill to

fail, like in the example of KYTK4.

Developing the Capacity of Strategic Management: With top policies, a more

powerful relation between budget and execution has been established when compared to pre-

reform period, policy-making capacity has been increased in the public administrations and a

partial improvement has been achieved in the utilization of the public resources in accordance

with the strategic priorities. In this scope, Strategy Development Units (SDU) were

established in the central management and local administrations with the aim of strengthening

institutional infrastructure of the strategic planning. However, there is a problem in terms of

personnel capacity in the related units even though the institutional and legal infrastructure

has been established. In this sense, it is necessary to develop expertise capacity of the

administrations quantitatively and qualitatively in the areas of medium and long-term strategy

and policy setting, strategy developing and performance management. According to the SDU

research results for 2007, improvement is necessary in the areas of leadership of managers,

good command and compliance of the new financial management and organization required

by the reform (Usta, 2010:11).

In May 2010, 137 of 145 central public administrations and 17 of 19 state economic

enterprises prepared strategic plans for the first time. Moreover, almost 320 local

administrations prepared their second strategic plans. Within the framework of the budget

preparations for 2011, the institutions will prepare performance programs on the basis of

strategic plans. However, the plans were not costed sufficiently and they are poorly binding

(Usta, 2010:10).

26

Making Accountability Widespread to the Public Sector: In the public

management, the relation between budget, strategic plan and performance management could

not be established adequately. Furthermore, the arrangements for strengthening accountability

and transparency could not produce the desired results.

27

Figure 1. Performance Programme Preparation Process

Formulation of Performance Programme

of the Ministry

Determination of general government expenses and resources to be transferred to the other administrations

Consolidation of the resource needs (Activities, performance objectives, general government expenses and resources to be transferred to the other

administrations )

Top Management - Authorizing

Officers

Spending Units

Strategy Development

Unit

Determination of prioritized strategic goals and objectives

Determination of performance objectives and indicators

Determination of activities

Determination of costs that can directly be related to the activities

Source: Ministry of Finance, Performance Programme Preparation Guide, 2009, p. 12.

Figure 2. Ministry of Finance Strategic Management Model

Strategic Plan Performance Programme

Monitoring & Evaluation

AccountabilityReports

Management Information System

Internal Control

28

Figure 3. Ministry of Finance Strategic Management Framework

STRATEGIC GOAL STRATEGIC OBJECTIVE PERFORMANCE OBJECTIVE ACTIVITY

Budget Management

Financial Control

Economic and Sectoral Analysis

Accounting Reporting

Leasing and Property Related Fees

AcquisitionConstitution of Servitude

Allocation Transactions

Sale Transactions

Transfer and Abandonment

Legal Advisory for the State

Audit and Advisory Services

Audit

Strategy Development

Central Harmonization

THEME

Rational use of public immovables will be ensured.

POLICY

EXECUTION

To ensure effectiveness, efficiency, accountability and transparency in the

utilization of public resources To increase value added to the Turkish economy

by rational utilization of public immovables

Support for Accounting

To establish a financial management system in compliance with international standards

To provide legal services for the state in a rapid, effective and efficient manner

Revenue Budget Preparation and Tax Revenue Reporting

To prevent the informal economy and corruption

POLĐ

CY

DEVELOPMENT

Revenue policies which will promote economic growth, social justice, employment and international competitiveness will be developed.

To form revenue policies that promote economic growth, social justice, employment and

international competitiveness

Allocation of public resources will be ensured to be in accordance with the public priorities and in line with the spending policies which protect fiscal discipline.

To form spending policies which protect fiscal discipline and to allocate public resources in

accordance with public prioritiesTo create a robust and rule-

based financial structure

A model for financial services management will be formed as stipulated in the Law No. 5018 and secondary legislation.

The accounting system which is in compliance with the international standards will be strengthened.

A financial management system in compliance with the international standards will be established.

Accounting Audit

AUDIT AND

ADVISORY

Legal Proceedings

Fight against laundering of proceeds of crime and financing of terrorism

Informal economy and corruption will be prevented.

Efficiency in fight against laundering proceeds of crime and financing of terrorism will be ensured.

To prevent laundering proceeds of crime and financing of terrorism

To prevent black economy, corruption and informal

economy

To protect the rights of the state by providing an effective legal service

Legal services for the state will be provided in a rapid, effective and efficient manner.

29

Figure 4. Plan-Programme and Budget Relation Model

Source: MoF Strategy Development Unit

Figure 5. Cascading

Source: MoF Strategy Development Unit

30

1 According to Article 16 of the Law No. 5018, medium-term programme is prepared in accordance with the

requirements of developments plans, strategic plans and general economic conditions in a way to cover macro

policies, principles and basic economic figures in forms of objectives and indicators. The medium term

programme is prepared by the Undersecretariat of State Planning Organization and approved by the Council of

Ministers which gathers by the end of May.

2 The second document in the medium term budgeting process is the medium term fiscal plan which is in

compliance with the medium term programme and which includes total revenue and expenditure forecasts,

deficit and borrowing targets, appropriation proposal ceilings of public administrations for the coming three

years. The medium term fiscal plan is prepared by the Ministry of Finance and decided on by the High Planning

Council until 15 June. One of the most important elements of the medium term fiscal plan is determination of

appropriation proposal ceilings of public administrations. This enables to put an upper limit on appropriation

proposals of public administrations within the scope of central government excluding regulatory and supervisory

agencies at the first level of economic classification. Limiting appropriation proposals aims at making sure that

public administrations propose their appropriations based on strategic goals and objectives set out in strategic

plan and preventing unnecessarily high proposals (Mutluer et. al., 2006: 215).

3 It should be noted that bureaucratic structure and mentality is not represented organizationally only by the

bureaucracy itself. According to a research made on the prominent Turkish politicians, leading staff of the

parliaments between the period of 1924 – 1950 was composed of bureaucrats at a rate of 66 percent in the 2nd

Parliament, 61 percent in the 3rd Parliament, 60 percent in the 4th Parliament, 65 percent in the 5th Parliament, 61

percent in the 6th Parliament and finally 50 percent in the 7th Parliament; and this fact can only be explained by

the weakness of the entrepreneurial class and that people having received a contemporary education could not

find a job apart from the governmental positions (see Gencay Şaylan, Türkiye’de Kapitalizm, Bürokrasi ve

Siyasal Đdeoloji (Ankara: V Yay., 1986), p. 76. ).

4 For a healthy analysis of the Turkish political structure, see Hasan Bülent Kahraman, Türk Siyasetinin Yapısal

Analizi-I,Kavramlar-Kuramlar-Kurumlar (Đstanbul: Agora Kitaplığı, 2008), a contemporary study developing

Şerif Mardin’s sociological analysis based on centre-environment dilemma and adapting it for today. This study

evaluated the Turkish political structure in terms of the conflict among the military-intellectuals called as the

historical block and who represent the centre; the provincial bourgeoisie who represent bureaucracy and

environment; immigrants who started to settle down in the large city centres; and the vast majorities of public.

31

BIBLIOGRAPHY

Azrak, Ülkü (2004), “Türk Đdaresinde Reform Girişimlerinin Değerlendirilmesi”, Hukuk ve

Adalet Dergisi 2: 223-236.

Barber, Michael (2007), Instruction To Deliver, Tony Blair, Public Services And The

Challenge Of Achieving Targets. London: Politico’s.

Demir, O. (2008), “Kamu Yönetiminin Yeniden Yapılandırılması ve Kamu Yönetimi Temel

Kanunu Tasarısı”,

http://www.geocities.com/guvencetin/kamuyonetimininyenidenyapilandirilmasi.html.,

Erişim Tarihi: 20.12.2008.

Hughes, Owen E. (1994), Public Management And Administration: An Introduction. London:

The Macmillan Press.

Kesik, Ahmet (1999), “Fon Sistemi ve Devam Eden Sorunlar”, Maliye Dergisi 131: 59-101.

Maliye Bakanlığı, Performans Programı Hazırlama Rehberi (2009).

Mutluer, M. Kamil and Öner, Erdoğan and Kesik, Ahmet (2006), Bütçe Hukuku. Đstanbul:

Đstanbul Bilgi Üniversitesi Yayınları.

Usta, Erhan (2010) Kamu Mali Yönetimi Sempozyumu, Word Bank, 25 Mayıs 2010, Ankara.