Embed Size (px)

Citation preview

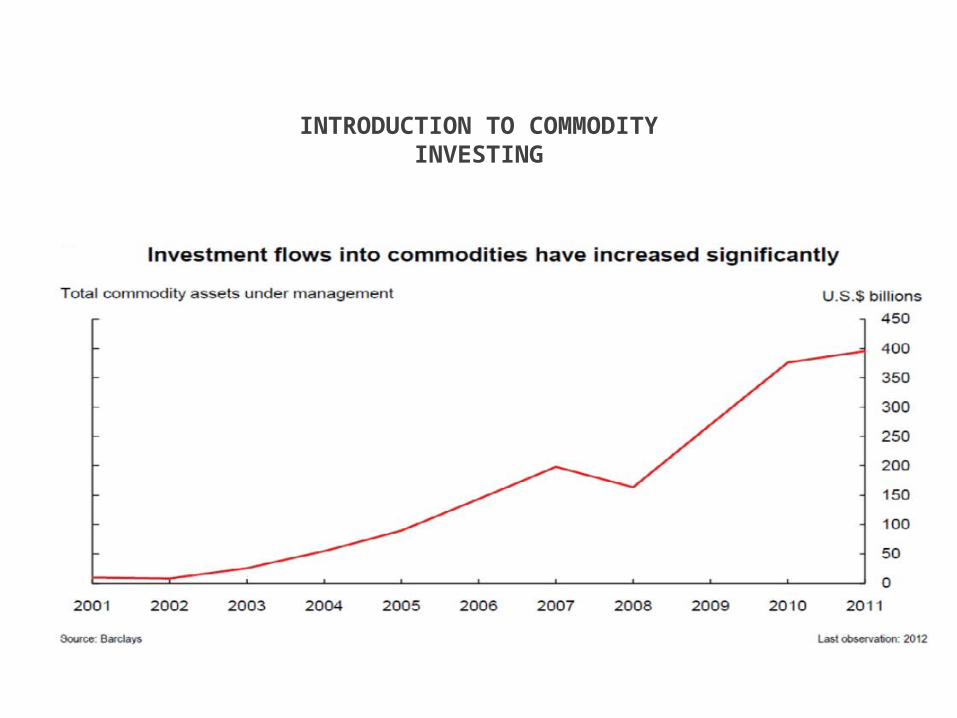

INTRODUCTION TO COMMODITY INVESTING

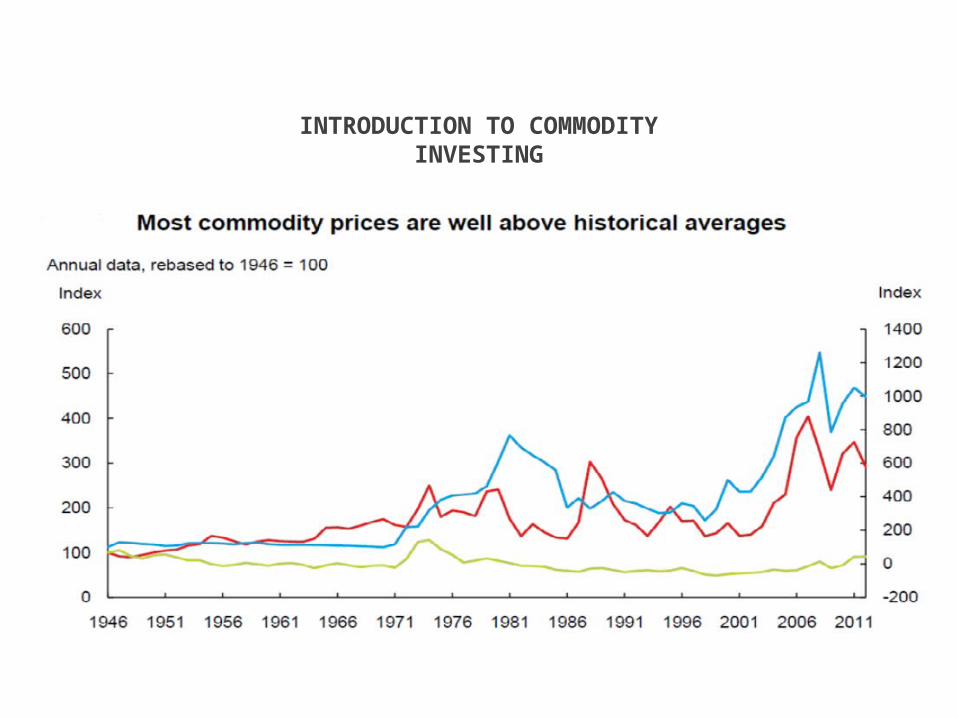

INTRODUCTION TO COMMODITY INVESTING

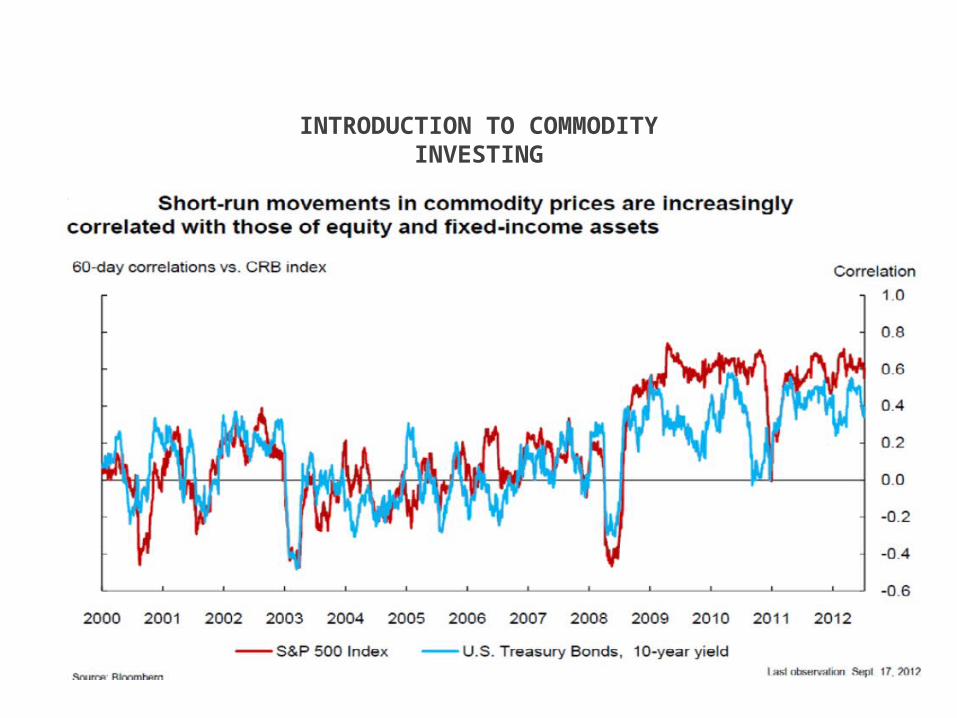

INTRODUCTION TO COMMODITY INVESTING

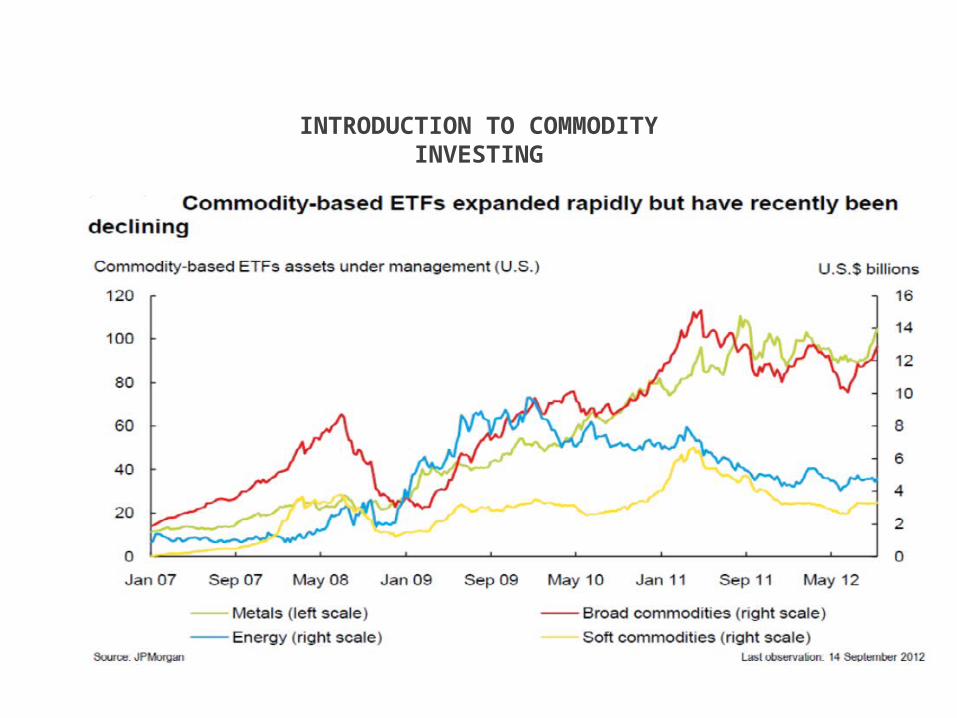

INTRODUCTION TO COMMODITY INVESTING

METHODS OF INVESTING IN COMMODITY

•Buy Share of Companies whose business is Commodity related such as Reliance,Tata Steel,Rio Tinto,Vedanta,BP.•Buy Physical Commodity•Financial assets where the underlying is commodity:

•Commodity Futures.•Commodity Indices•Total Return Swap•Commodity Linked Structured Products

COMMODITY INDICES

•Payout linked to a basket of commodities as opposed to a single commodity. Physical ownership of commodity not required, increasing convenience and reducing transaction cost for the investor.Ex:S&P GSCI.•The weights of the individual commodity in the index are decided by an Index Committee with their decision being driven by USD value of global production of the commodity on a rolling 5 year period.•S&P GSCI is composed of three sub indices:

•Spot Index:Price movement of future contracts of commodity included in the index.•Excess Return Index: Returns on Spot positions plus profit(or loss) attributable to rolling of futures position at delivery date.•Total Return Index: This incorporates the excess return plus the interest earned on fully collateralised contract position on all commodity future included in the index

The return on such indices is based on futures, but since some investors are not allowed to invest in leveraged structures, the returns are calculated on a deleveraged basis. For investment in futures only the margin amount(which is a small portion of the nominal exposure) is required. However, the investor would have to pay the amount equivalent to the nominal exposure. The difference between the margin and the nominal is assumed to be invested in risk free securities

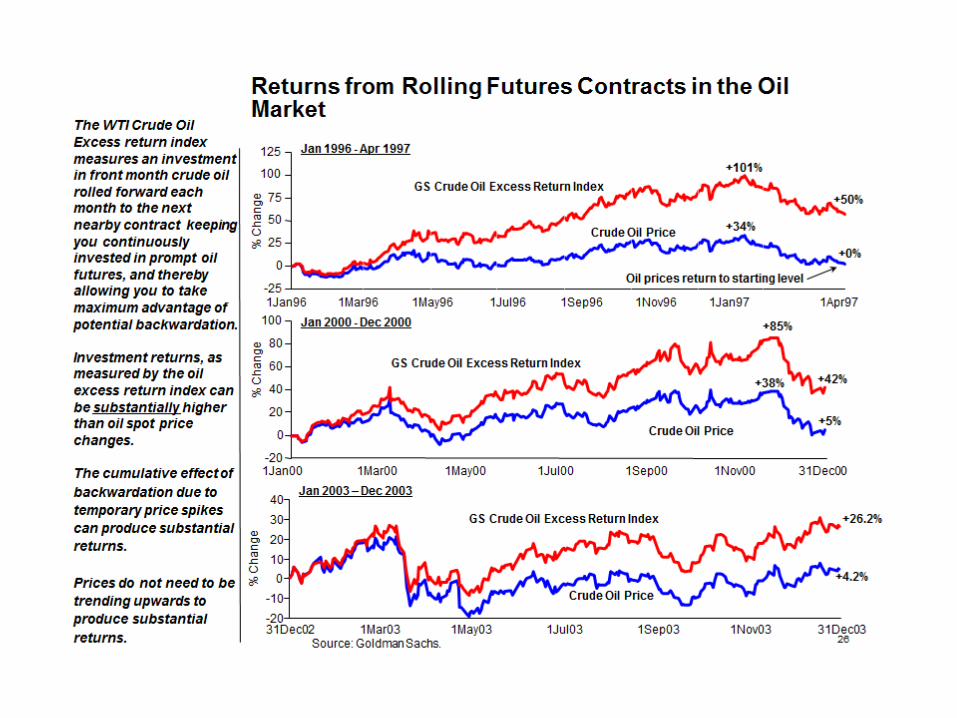

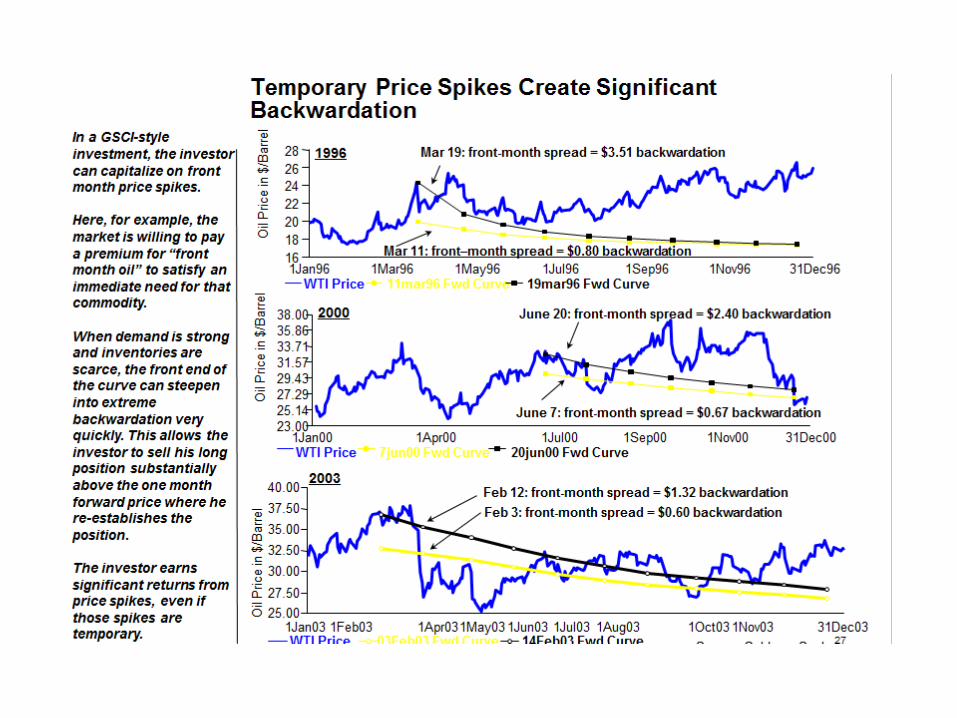

ROLL YIELD

Rolling the future contract involves selling out the existing long position as it approaches maturity and simultaneously buying whichever future is next to mature(Prompt).Roll yield arises from the possibility that certain commodities experience prolonged period of backwardation.General Forward Contract Pricing Method:Forward Price= Spot Price + Net Carry;Net Carry= Libor(Finance Cost) – Convenience Yield + Storage Cost;Example: Spot Copper at USD 7100/ton, three month future delivery at USD 7050/ton. An investor could buy the future and with time the future price may rise to the level of the spot( supported by the argument that at delivery future and spot price converge). In such a scenario, the future position will generate a profit of USD 50/tonne. The investor may choose to continue with the exposure to copper by purchasing at delivery a new 3 month future contract, which may be lower than the spot price(assuming backwardation continues) around the time of delivery.If during the life of the future, the spot price rises profitability will improve, while a fall is spot price will reduce profitability.

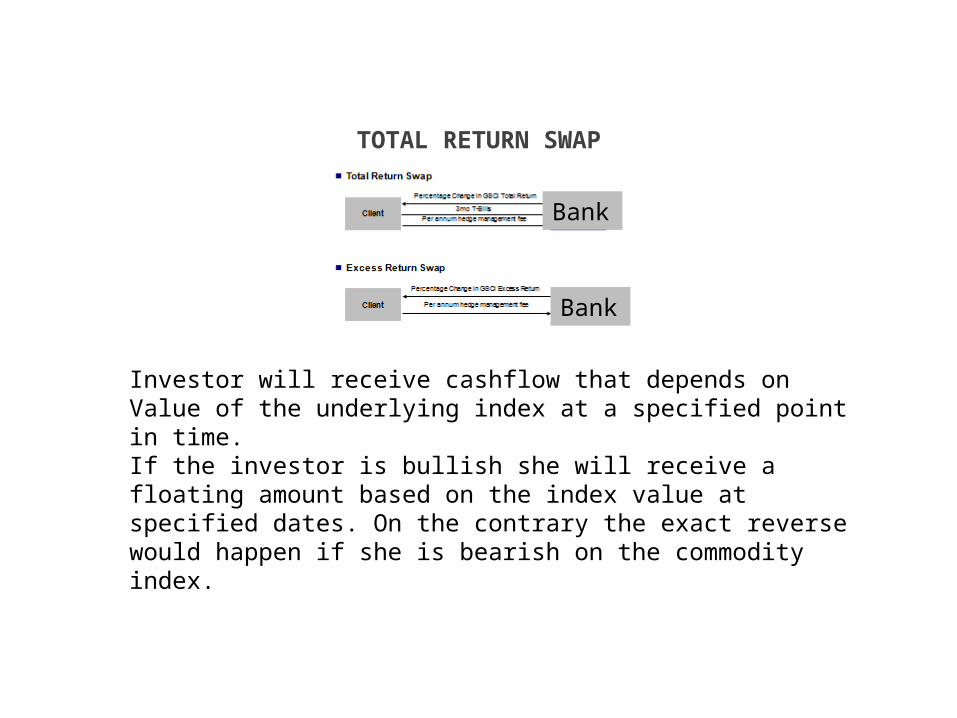

TOTAL RETURN SWAP

Bank

Bank

Investor will receive cashflow that depends on Value of the underlying index at a specified point in time.rIf the investor is bullish she will receive a floating amount based on the index value at specified dates. On the contrary the exact reverse would happen if she is bearish on the commodity index.

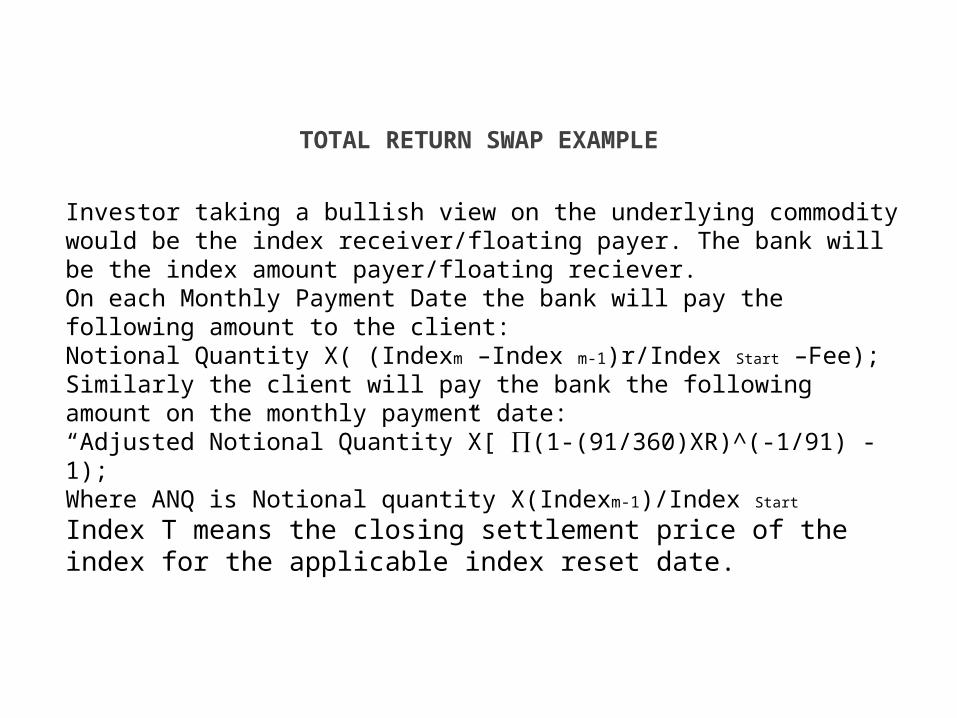

TOTAL RETURN SWAP EXAMPLE

Investor taking a bullish view on the underlying commodity would be the index receiver/floating payer. The bank will be the index amount payer/floating reciever.On each Monthly Payment Date the bank will pay the following amount to the client:Notional Quantity X( (Indexm –Index m-1)r/Index Start –Fee);Similarly the client will pay the bank the following amount on the monthly payment date:“Adjusted Notional Quantity”X[ (1-(91/360)XR)^(-1/91) -∏1);Where ANQ is Notional quantity X(Indexm-1)/Index StartIndex T means the closing settlement price of the index for the applicable index reset date.

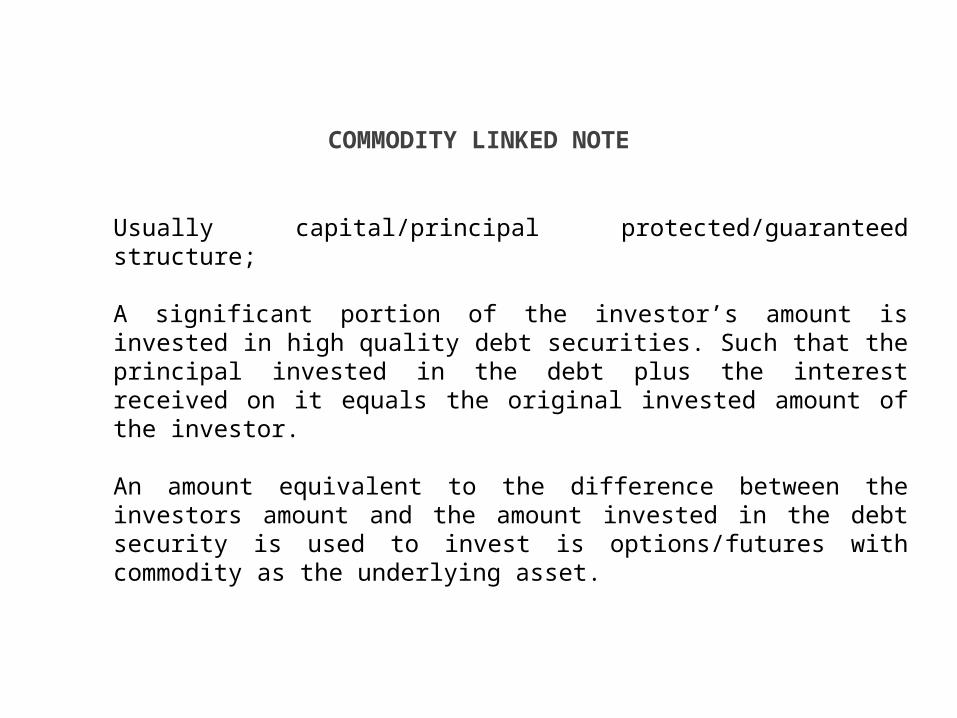

COMMODITY LINKED NOTE

Usually capital/principal protected/guaranteed structure;

A significant portion of the investor’s amount is invested in high quality debt securities. Such that the principal invested in the debt plus the interest received on it equals the original invested amount of the investor.

An amount equivalent to the difference between the investors amount and the amount invested in the debt security is used to invest is options/futures with commodity as the underlying asset.