Embed Size (px)

Citation preview

I

Anja Kuhn

Mart.Nr: 11722464

Corporate Psychopaths and their effect on leadership and

corporate culture

A guideline how to cope with psychopathy in a corporation

Masterarbeit

zur Erlangung des akademischen Grades

eines Master of Science

der Studienrichtung Betriebswirtschaft

an der Karl-Franzens-Universität Graz

Betreuer: Univ.-Prof. Dipl.-Ing. Dr. techn. Michael Kopel

Institut: Organisation und Institutionenökonomik

Graz, April 2020

II

Table of content

1 Introduction ....................................................................................................................... 1

Description of the case study samples ................................................................................. 4

2 Scientific Relevance .......................................................................................................... 8

Literature Review ................................................................................................................. 8

Current State of the Art ....................................................................................................... 9

Structure of Content ........................................................................................................... 10

3 Corporate Psychopaths and the “Dark Triad” ............................................................... 11

Definition ............................................................................................................................. 11

“Dark Triad” ....................................................................................................................... 15 3.2.1 Machiavellianism ........................................................................................................................... 15 3.2.2 Narcissism ...................................................................................................................................... 16 3.2.3 Psychopathy .................................................................................................................................... 17

Common features and differences ..................................................................................... 17

Distribution within different sectors ................................................................................. 19 3.4.1 Distribution within the hierarchy of a corporation ......................................................................... 20

4 Case Study Design ........................................................................................................... 20

Analytical Framework........................................................................................................ 20 4.1.1 Behavioural Agency Theory ........................................................................................................... 21 4.1.2 Corporate Governance .................................................................................................................... 23

Methodology ........................................................................................................................ 25 4.2.1 Criteria of the deliberate sample ..................................................................................................... 25 4.2.2 Target setting of the Design ........................................................................................................... 26

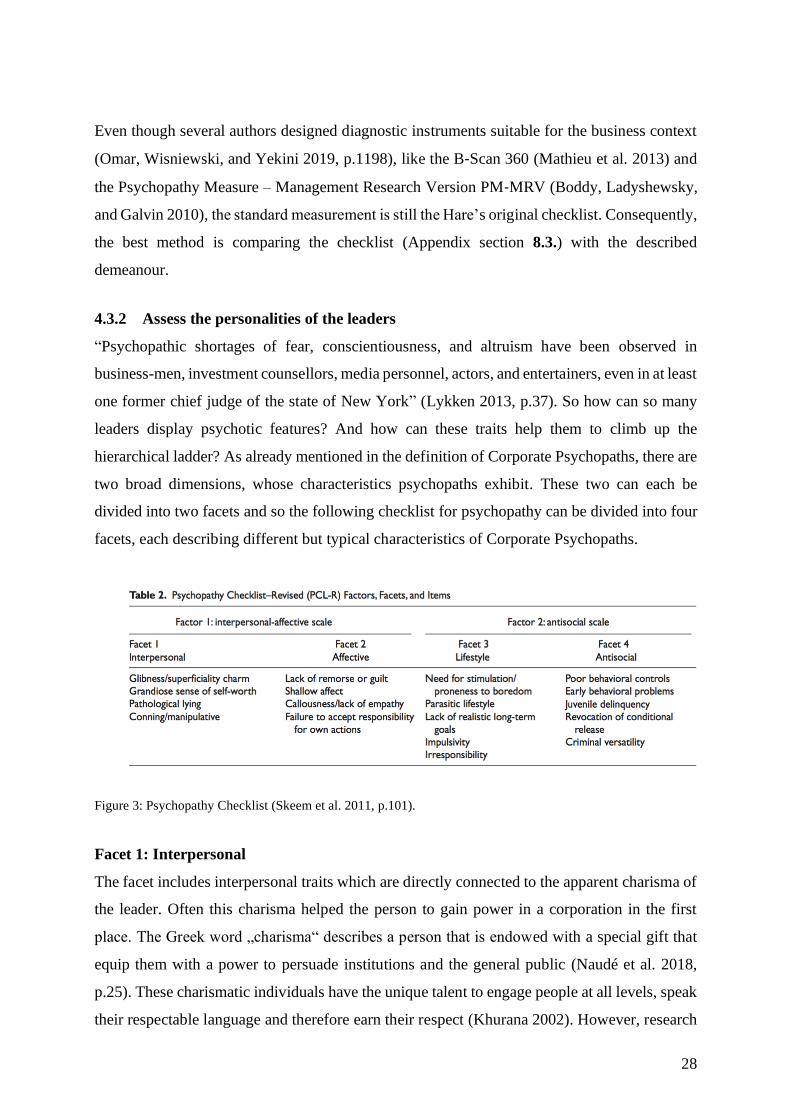

Psychopathy Measure ......................................................................................................... 27 4.3.1 Traits of Corporate Psychopaths .................................................................................................... 27 4.3.2 Assess the personalities of the leaders ............................................................................................ 28 4.3.3 Collation ......................................................................................................................................... 32

Corporate Psychopaths as Leaders ................................................................................... 38 4.4.1 Psychopaths rising within corporations .......................................................................................... 38 4.4.2 Leadership mechanisms & its Impact ............................................................................................. 40 4.4.3 Pay for performance & Behavioural Agency Theory ..................................................................... 44 4.4.4 Collation ......................................................................................................................................... 46

Multiplier Effects of Corporate Psychopaths................................................................... 51 4.5.1 Intra-organizational ganging dynamics/ Corporate Culture ........................................................... 51 4.5.2 Key characteristics of corporations as psychopaths ....................................................................... 53 4.5.3 Passive Board of Directors ............................................................................................................. 56 4.5.4 Corporate Governance .................................................................................................................... 57 4.5.5 Collation ......................................................................................................................................... 58

Corporate Fraud ................................................................................................................. 63 4.6.1 White Collar Crimes ....................................................................................................................... 65 4.6.2 Audit Failure ................................................................................................................................... 67 4.6.3 Collation ......................................................................................................................................... 68

5 Cross-Case Analysis ........................................................................................................ 73

6 Guideline to cope with Corporate Psychopaths.............................................................. 76

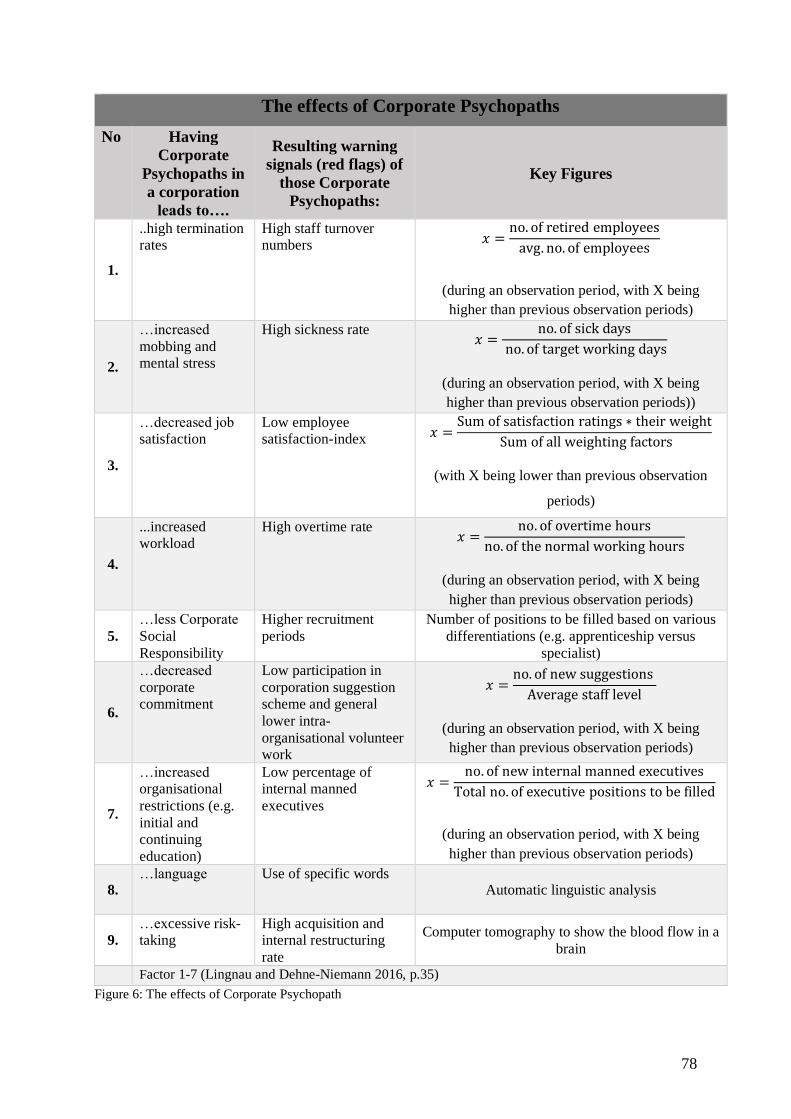

Recognition of psychopathic traits within a corporation ................................................ 77

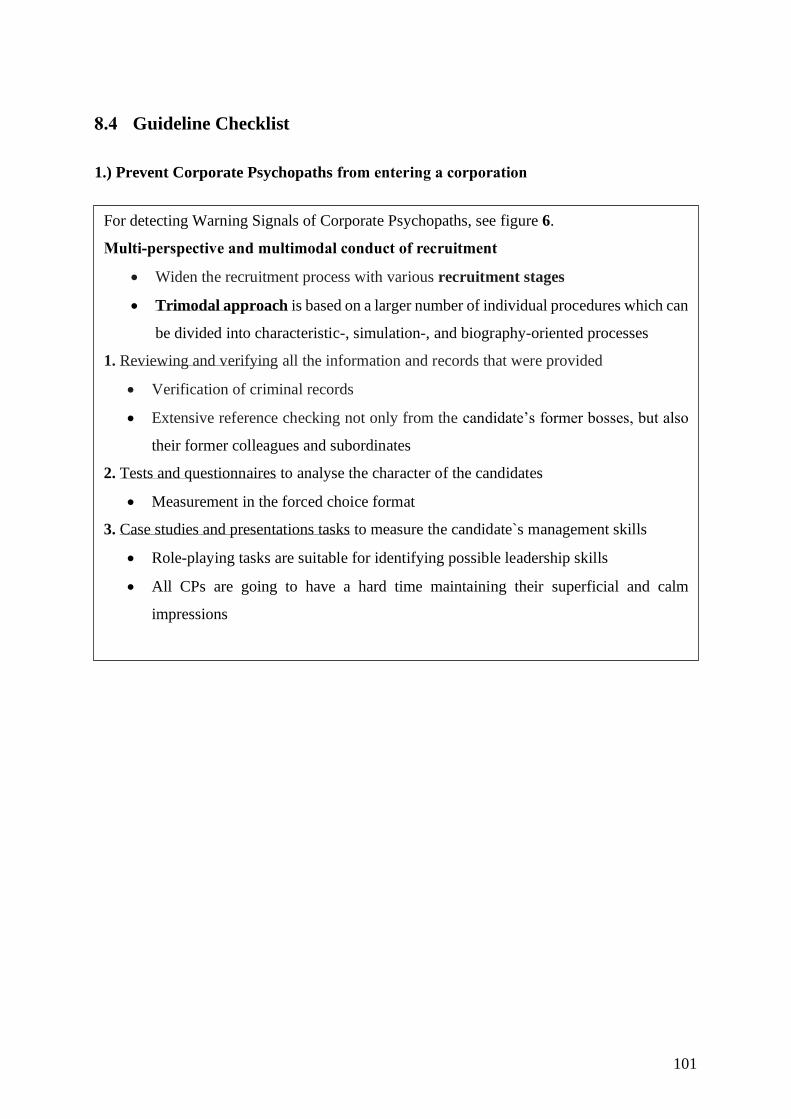

Prevent Corporate Psychopaths from entering a corporation ....................................... 81

III

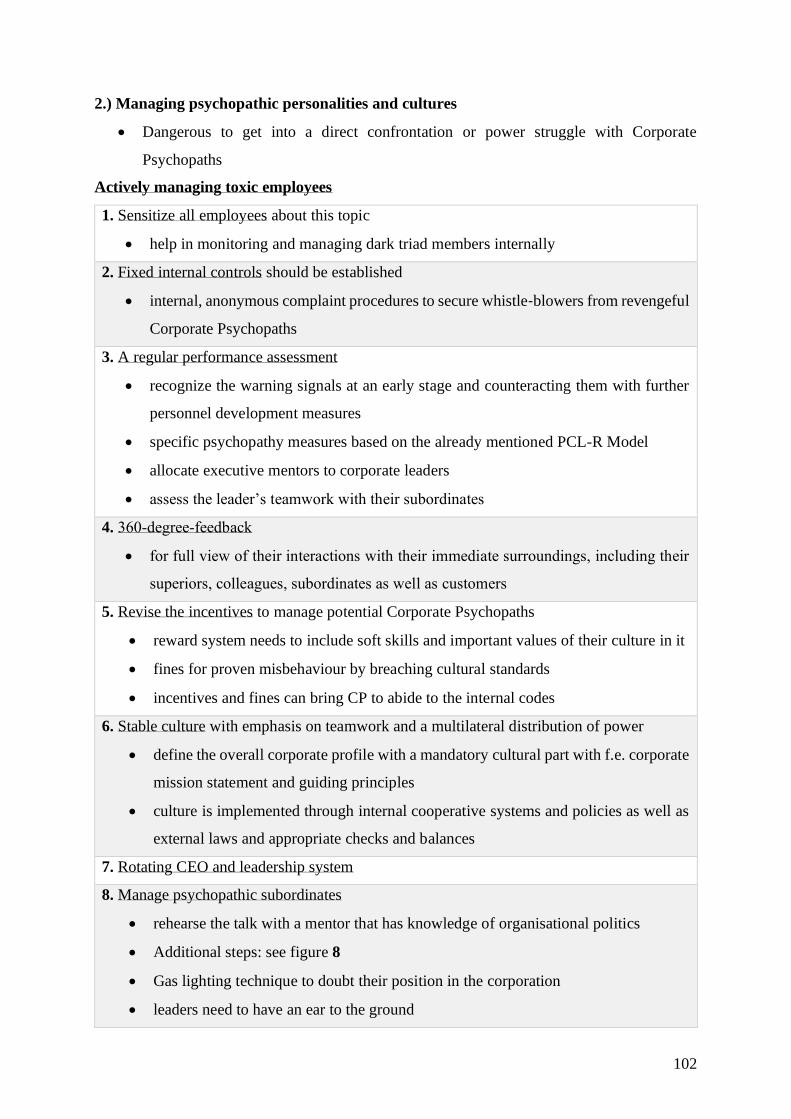

Managing psychopathic personalities and cultures ......................................................... 83 6.3.1 Manage psychopathic subordinates ................................................................................................ 86

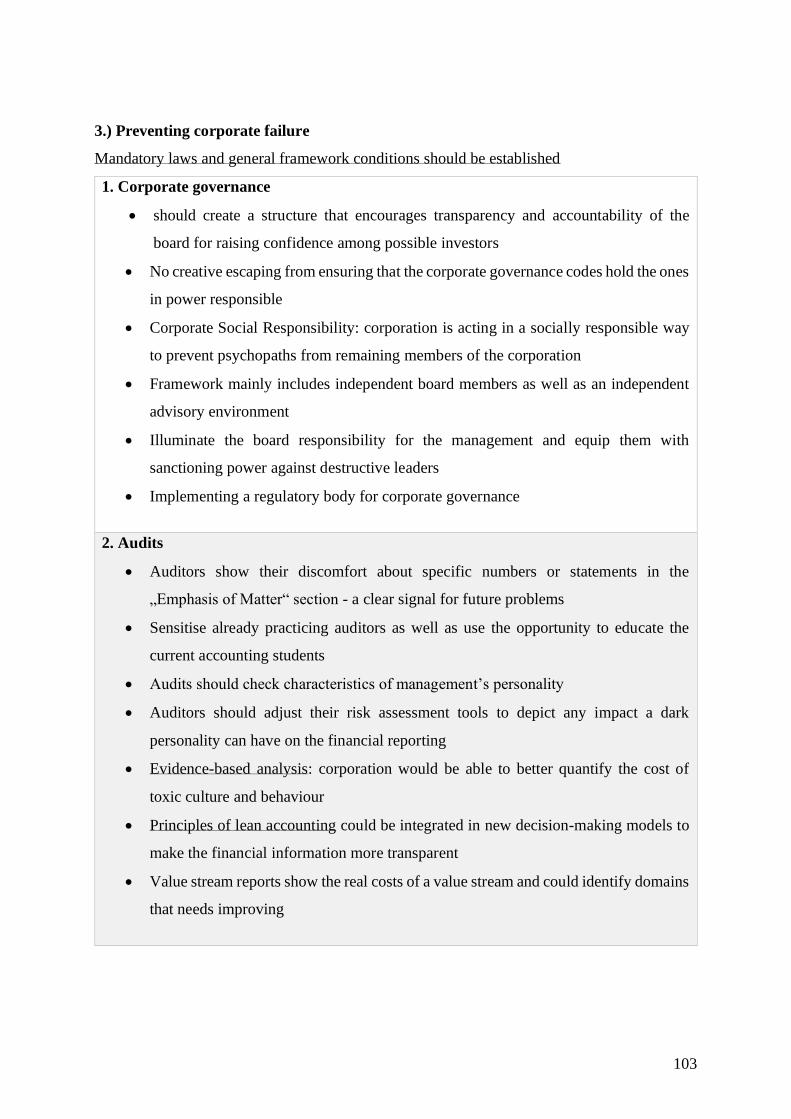

Preventing corporate failure .............................................................................................. 88 6.4.1 Corporate Governance .................................................................................................................... 88 6.4.2 Auditing Methods ........................................................................................................................... 89

Lessons learned ................................................................................................................... 90

7 Conclusion ....................................................................................................................... 91

Reflection ............................................................................................................................. 93

Limitations .......................................................................................................................... 94

Implications for further research ...................................................................................... 94

8 Appendix .......................................................................................................................... 96

Table of possible candidates .............................................................................................. 96

Criteria check of the used examples.................................................................................. 98

Hare’s original checklist for psychopathy summarized: .............................................. 100

Guideline Checklist ........................................................................................................... 101

9 Bibliography .................................................................................................................. 104

Table of figures

Figure 1: The dark triad (Boddy 2010, p.303). ....................................................................... 17

Figure 2: Experience of Corporate psychopaths in the workplace (Boddy 2010, p.307). ...... 19

Figure 3: Psychopathy Checklist (Skeem et al. 2011, p.101).................................................. 28

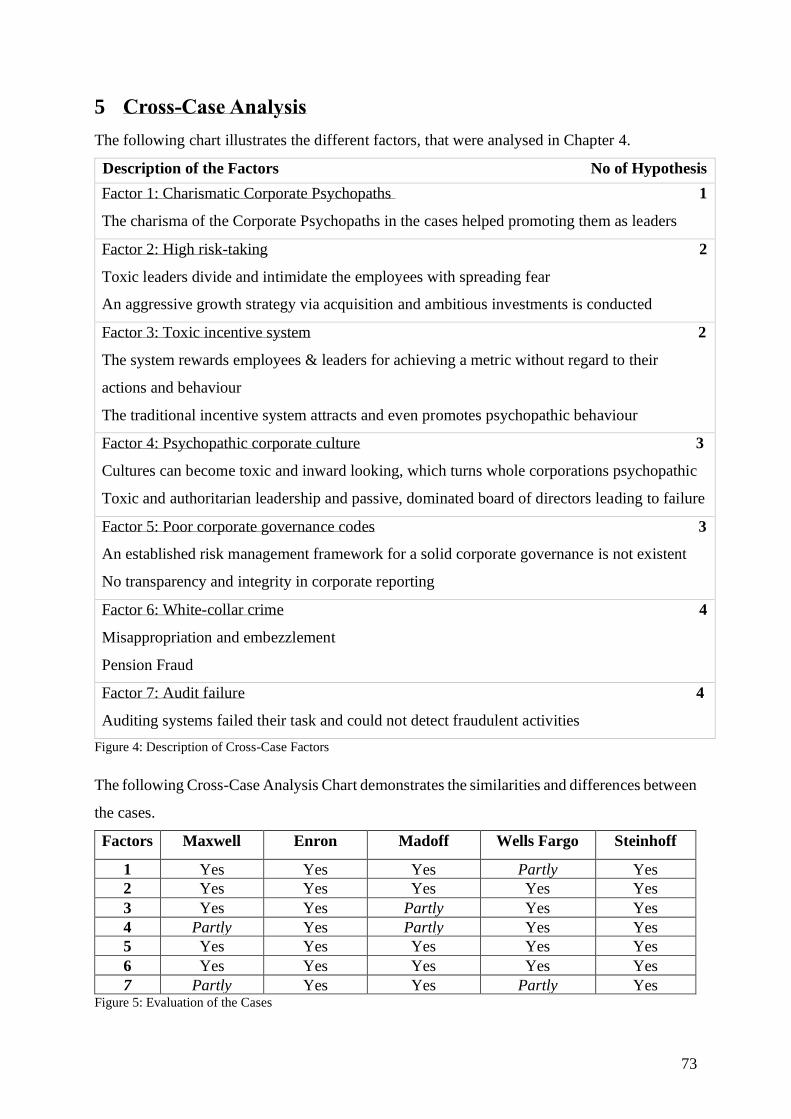

Figure 4: Description of Cross-Case Factors .......................................................................... 73

Figure 5: Evaluation of the Cases............................................................................................ 73

Figure 6: The effects of Corporate Psychopath ....................................................................... 78

Figure 7: Trimodal approach (Externbrink and Keil 2018, p.68). .......................................... 82

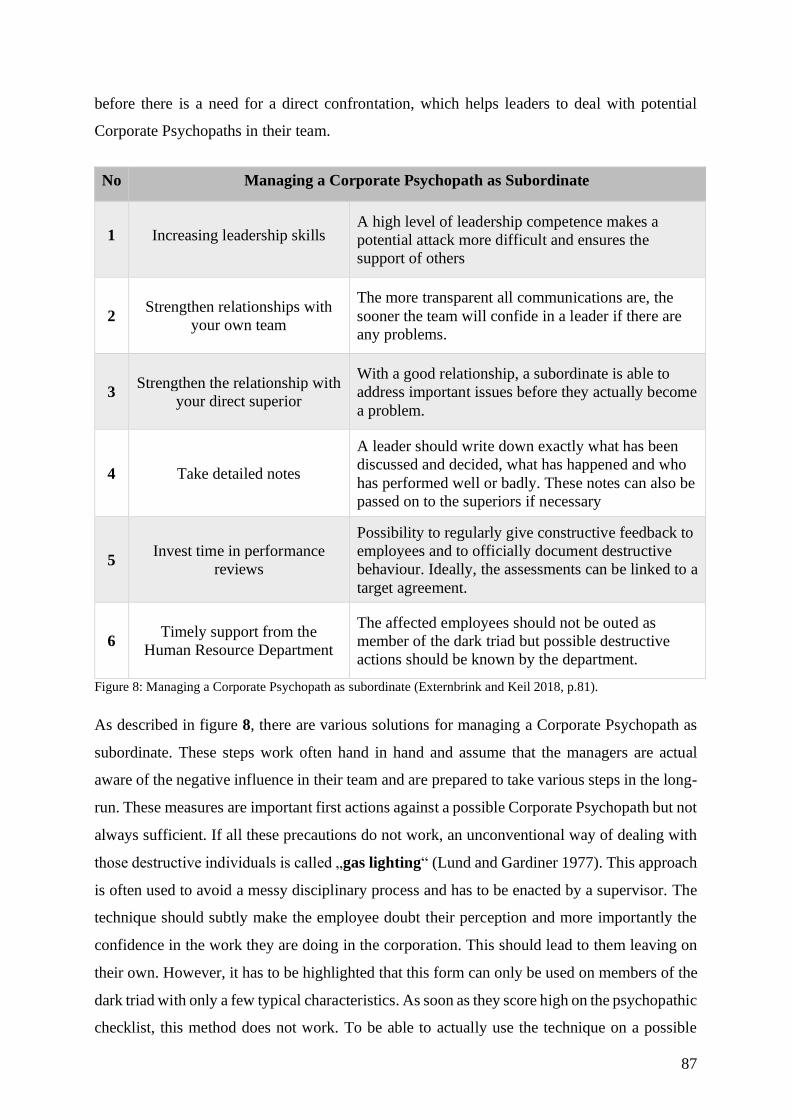

Figure 8: Managing a Corporate Psychopath as Subordinate (Externbrink and Keil 2018,

p.81).......................................................................................................................................... 87

1

1 Introduction

“This world, ladies and gentlemen, is not a sandbox with children building castles. No, this

world is tough competition that in a very sobering way only knows winners and losers.”

Wendelin Wiedeking (*1952) former CEO of Porsche AG. (Forschelen 2017, p.762).

The competitive intelligence expert Marc Barry would agree with this testimony and specifies

it for the economic world by saying, “If you’re a CEO, do you think your shareholders really

care whether you’re Billy Buttercup or not? (..) I don’t think so. I think people want money.

That’s the bottom line.” (Bakan 2012, p.30). As greed and moral indifference define today’s

corporate culture, the pressure that is put on CEOs to expand shareholder value no matter what

is steadily increasing (Bakan 2012, p.30).

But how does this subject of a harsher and emotionless tone in corporations affect all of us?

Over the last 100 years the corporation has become the world´s dominant economic institution

and the trend toward dominance of the “corporate system” has continued persistently (Berle

and Means 2017, p.20). According to the UN, corporations employed 54 million people in 2002

(Assadourian 2005, pp.18f). The average market capitalization of corporations tripled since

1975 and exceeds now $6 billion (Doidge et al. 2018, p.11). A more recent report also showed

that 59 per cent of the world’s 150 largest economic entities are in fact corporations (Tombs

and Whyte 2015, p.5). As the wealth of today´s largest corporations exceed the wealth of many

national governments, the dominance of modern corporations in the economic world also has a

vast effect on our society, so the public is inevitably surrounded by their ideas and culture

(Tombs and Whyte 2015, p.3).

The permanent corporate presence in our lives shapes not only our personal ideology, but also

influences society by fixing prices, altering laws and is furthermore able to dictate the decisions

in government (Bakan, 2012, p.7). Today´s corporations are able to govern our lives as they

have the capacity to combine economic power and a seemingly unlimited number of people.

They are central to all systems of social- or health-care, criminal justice, education, energy and

transport. Furthermore, the problem is not only the size of today´s corporations but also their

market concentration. In the recent years, academic studies even tend to argue that multinational

corporations are replacing states as the most powerful forms of actors in globalization (Tombs

and Whyte 2015, p.16).

2

However, these results help the public forget their morality or their offences. This error can

have significant consequences, as elite offenses cause sufficiently bigger harm than street-level

offences which are called violent crimes. The so-called white-collar crimes are defined as

“nonviolent crime for financial gain committed by means of deception” (Blickle et al. 2006,

p.221) and often occur due to the lack of requirements for corporations to pay the costs of their

damaging activities. As corporations are focusing entirely on maximizing profits for the

corporation’s shareholders, they are trying to externalize as many of their social and

environmental costs as possible without being held accountable for it (Assadourian 2005). This

is mainly due to the system used in accounting practice in which corporate balance sheets

normally only reflect particular costs without accounting for the long-term damage caused by

their activities (Tombs and Whyte 2015, p.14). As corporations become more powerful,

demands for accountability from an increasingly anxious public arise (Bakan 2012, p.16). Even

though there is an increasing global regulatory focus on trying to end fraud and the phenomenon

of too big to fail corporations, they have the underlying problem of moral hazard, where the

responsible people are protected from the negative consequences of their risky actions

(Schwarcz 2017, p.761).

As the corporation’s defined mandate is to pursue its own aim of increasing its value, regardless

of the harmful consequences it might cause unethical actions (Bakan 2012). As a result ruthless

traits and behaviours have been normalised and in some cases even appreciated among

corporate leaders (Pardue, Robinson, and Arrigo 2013, pp.166f). In a personal environment

most people would find these personality traits abhorrent but are willing to accept it in the most

powerful institutions (Bakan 2012, p.18). So no wonder that according to Peter Jürgen Dormann

(*1940), CEOs are dangerous animals (Forschelen 2017, p.770). However, the concrete

consequences of these dangerous characteristics for the affected employees or the entire

corporations are rarely brought to the public. One reason might be that unethical actions mostly

happen in secret and as soon as it becomes public, the scandal of hazardous leadership is usually

given more attention than the analysis of the components that originally led to the problems

(Huber and Scheytt 2017).

A main reason for these growing threats from corporations might be the existence of so-called

Corporate Psychopaths. The term Corporate Psychopath (Boddy 2011, p.256) describes a

combination of the term psychopath from the field of psychology and corporate from the

business literature. In a nutshell, psychopaths can be explained as people without any

3

conscience. Due to this lack of conscience, psychopaths can often end up committing offences

and end up in prison (Hare 1999b, p.181). The correlation between psychopathy and street-

level offenses has been proven (Walsh, Swogger, and Kosson 2009, p.416) and valid methods

for identifying violent psychopaths has been developed (Boddy, Ladyshewsky, and Galvin

2010, p.122). However, psychopathic characteristics among corporate offenders are still rarely

explored. In general, there is scarcity of research to explore the relationship between

psychopathy and acts of elite offences (Pardue, Robinson, and Arrigo 2013, p.116).

So, what happens when Corporate Psychopaths reach corporate leadership positions? It can

cause low levels of ethical decision making (Boddy, Ladyshewsky, and Galvin 2010, p.122) as

these destructive leaders are mostly concerned with their own achievements and value them

over the success and wellbeing of the corporation they work for. Boddy (2015, p.2413)

postulates that whenever a corporation has been infiltrated by corporate psychopaths it has

resulted in a handful of people on the top becoming wealthy by taking high risks to improve

their position, while neglecting any social responsibility connected with their actions. Hansen

& Wernerfelt (1989, p.399) described the building of an effective human organisation as a

critical aspect for the corporation’s success. Corporate Psychopaths can directly affect the

whole human organisation due to their disruptiveness (Clarke 2005), as well as their negative

influence on the behaviour of colleagues (Goldman 2006). However, having Corporate

Psychopaths within a corporation is nearly unavoidable as psychopaths represent an estimated

1% of the population and it is therefore likely that every corporation employing more than 100

people will employ at least one psychopath (Boddy et al. 2015, p.534). In this thesis Corporate

Psychopath is used as an umbrella term for the three main socially-aversive attributes:

psychopathy, narcissism and Machiavellianism (Furnham, Richards, and Paulhus 2013, p.199).

These three form the so called “Dark Triad” (DeShong, Grant, and Mullins-Sweatt 2015, p.55).

This term originates from the negative association of these socially-aversive attributes and their

link to counter-productive behaviour (Furnham, Richards, and Paulhus 2013).

Dark-side tendencies often reveal themselves in ruthless efforts to get ahead and thus lead the

way to behaviour that acquires short-term benefits but with long-term costs as a result (Kaiser,

LeBreton, and Hogan 2015). Empirical analysis supports the hypothesis that dark triad

tendencies are particularly destructive for shareholder wealth (Omar, Wisniewski, and Yekini

2019, p.1221). However, having Corporate Psychopaths in a corporation leads mainly to

indirect productivity losses (Michalak and Ashkanasy 2018). Even though not directly

4

measurable, it can be safely assumed that Corporate Psychopaths in leadership roles contribute

to the 12 billion missed working days due to anxiety and depressive disorders (WHO 2016). So

even though Corporate Psychopaths are often considered high flyers within their corporations

(Furnham 2016), it becomes obvious that Corporate Psychopathy and bad leadership are

undeniably linked.

In order to understand the immense impact of Corporate Psychopaths on societal values and

economic norms and to be able to create guidelines to deal with them, this thesis aims to analyse

exemplary high ranking Corporate Psychopaths that can be directly linked to corporate failings

(Boddy 2006, p.1467). As scandals of failing corporations combined with bad leadership

accumulated within the last decade, more awareness has been paid to culture and the impact of

the tone at the top on organizational outcomes. Consequently, a general comprehension of

Corporate Psychopaths not only aids in constructing guidelines but also in answering the

question of how global corporations end up with Corporate Psychopaths as leaders (Boddy,

Ladyshewsky, and Galvin 2010, p.121).

Description of the case study samples

The idea of linking proven psychopathic CEOs with the failure of corporations came up after

several of these collapses could be directly related to their senior management (Boddy 2015,

p.2413). In the aftermath of different corporate failures, a high number of potential Corporate

Psychopaths have been proposed by various authors (Deutschman 2005). But even though

the tendency to white collar crimes and the lack of guilt of the responsible leaders is visible

in most of these cases, not all collapses can be clearly linked to a psychopathic leader.

Nevertheless, the following examples give historical evidence of collapses due to the effect of

Corporate Psychopaths in their ranks.

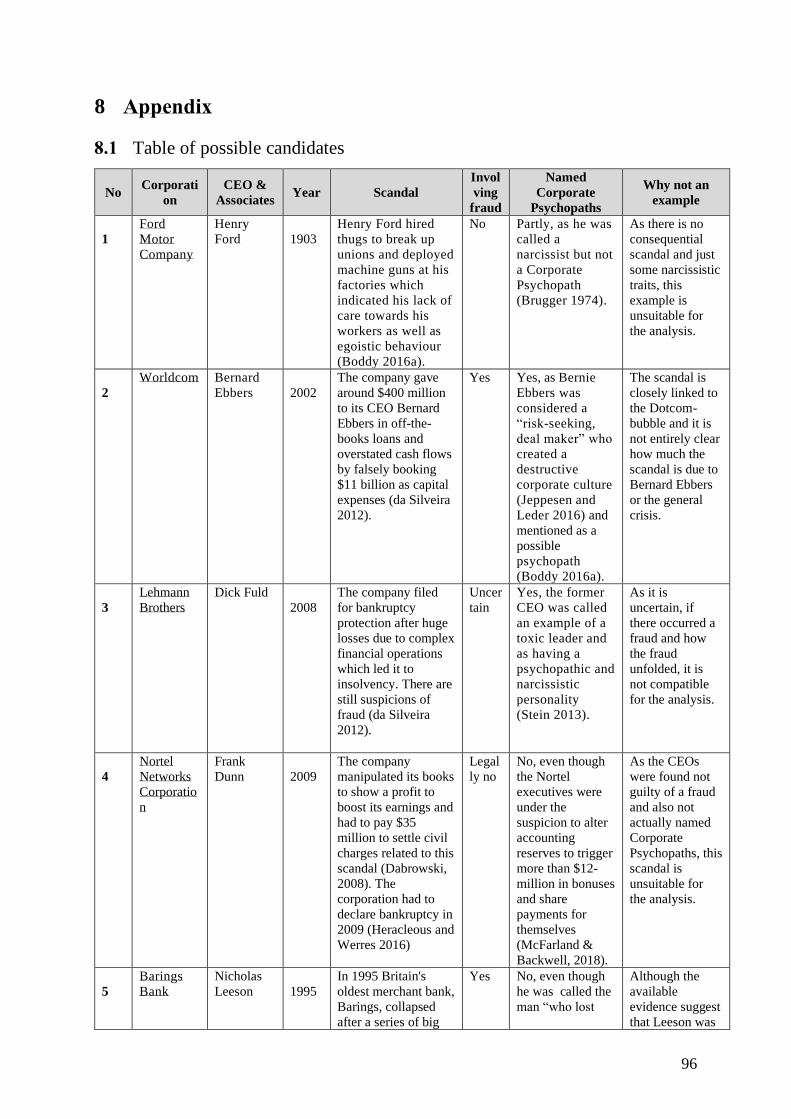

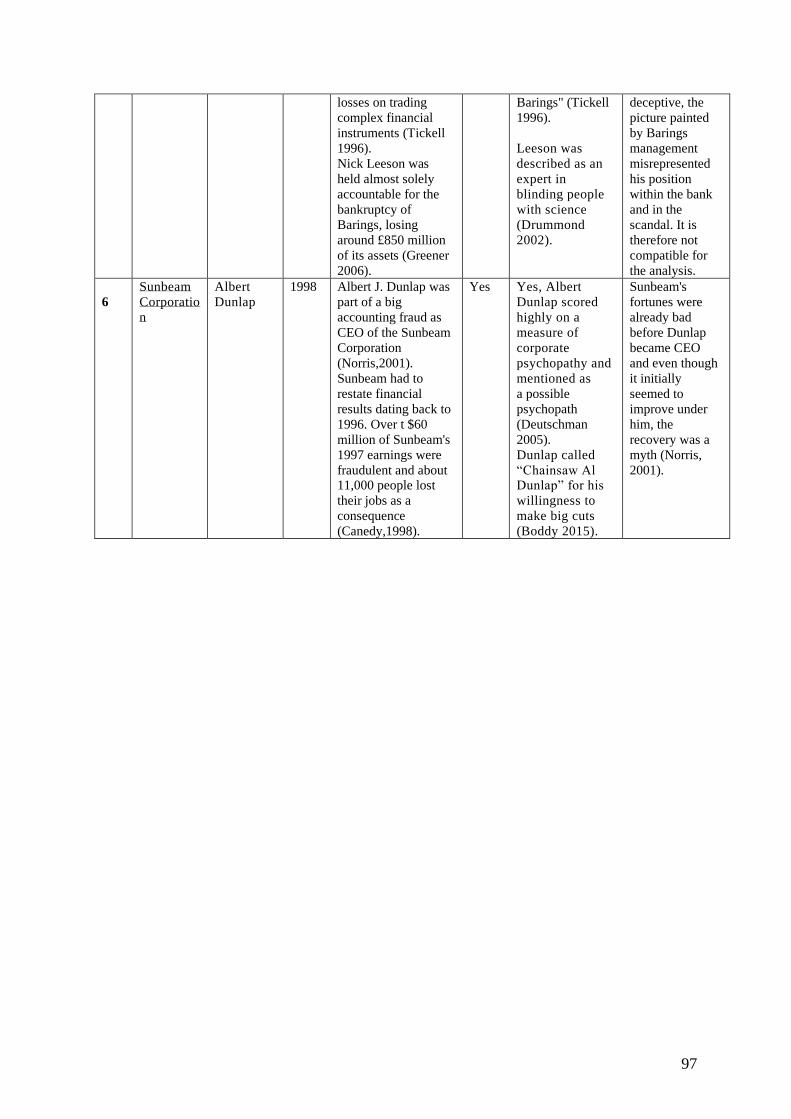

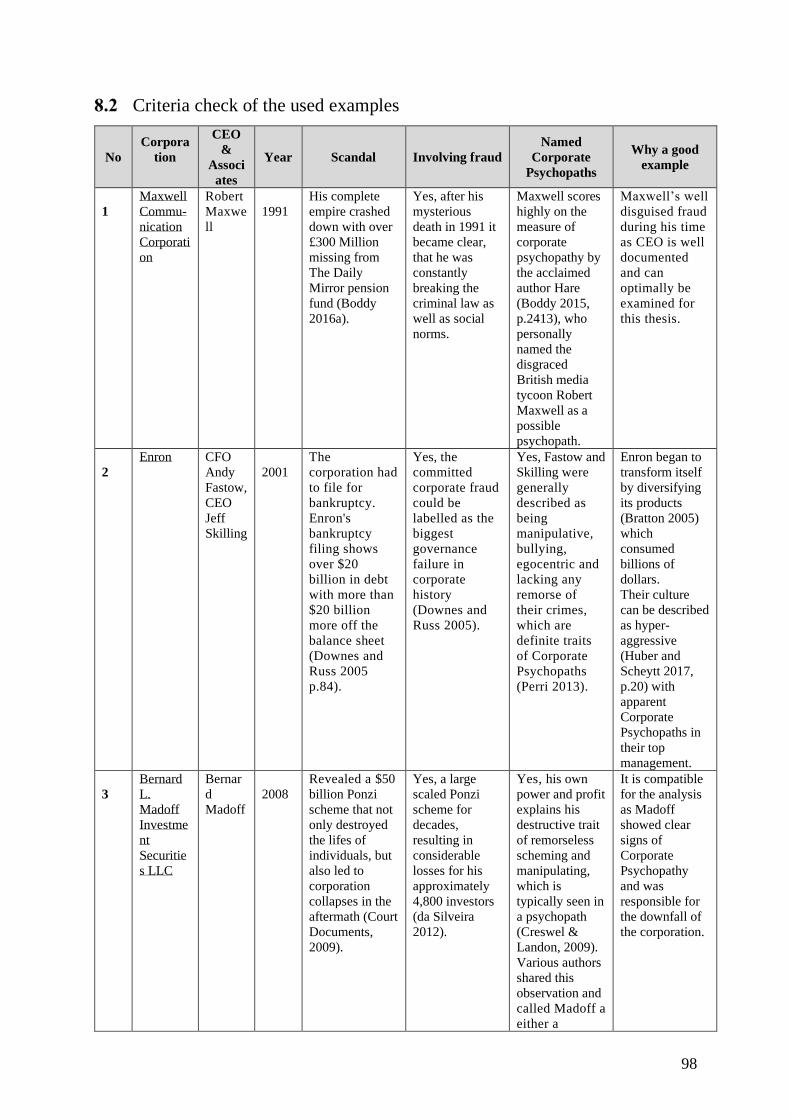

1. Maxwell Communication Corporation

The first and oldest case is also the first one that led to a public discussion about the effects

of bad leadership by a seemingly charismatic and competent CEO. The famous business

figure Robert Maxwell was well-known as a media tycoon, owning the Maxwell

Communication Corporation with newsletters like The Daily Mirror or The New York Daily

News while simultaneously influencing society as a member of the British parliament (Smith

2013).Thus he was a respected leader during his lifetime (Boddy 2016a). After his mysterious

death in 1991 he left his media corporations in a complex web of the covert links between all

5

his investments and his Maxwell Communication Corporation causing his complete empire to

crash down with over £300 Million missing from The Daily Mirror pension fund. It soon

became obvious that he was constantly breaking the criminal law (Clarke 1992, p.463). The

bankruptcy of his corporation was subject to many historical reports. As a result, Maxwell’s

well disguised fraud during his time as CEO is well documented and can optimally be

examined for this thesis.

Maxwell scores highly on the measure of corporate psychopathy by the acclaimed author

Robert Hare (Boddy 2015, p.2413), who personally named the disgraced British media tycoon

Robert Maxwell as a possible psychopath. He reportedly said "I'm not saying Maxwell was a

psychopath…but he sure had psychopathic tendencies." (Boddy 2005, p.33).

2. Enron

The second case of the famous Enron scandal publicly started a conversation of the socially-

aversive characteristics by the dark triad within their leaders after its spectacular crash in 2001.

Just a few years earlier Enron was celebrated as “America's Most Innovative Company”

(Wang et al. 2007, p.229) by Fortune magazine due to its great short-term profits and it

showed a high efficiency in actively disguising the already ongoing fraud. Ultimately, the

corporation had to file for bankruptcy and their committed corporate offence could be

labelled as the biggest governance failure in corporate history (Downes and Russ 2005a).

Enron's bankruptcy filing shows over $20 billion in debt with additionally more than $20

billion off the books (Downes and Russ 2005 p.84). Their responsible leaders CFO Andy

Fastow, together with CEO Jeff Skilling, chairman Jay Kenneth and 27 other Enron leaders

sold their shares before the corporation collapsed (Downes and Russ 2005a). To gain more

profit for themselves, these leaders set up fraudulent entities to keep several liabilities off the

books and therefore displaying a cheating personality (Boddy 2016a). Consequently the

members of the senior management were identified as potential Corporate Psychopaths (Naudé

et al. 2018, p.29). In this case especially Fastow and Skilling were described as being

manipulative, bullying, egocentric and lacking any remorse for their crimes, which are

definite traits of Corporate Psychopaths (Perri 2013). Enron’s collapse clearly showed what

happens when the ruthless characteristics we normally accept in corporate leaders are pushed

to the extreme (Bakan 2012, p.32).

6

3. Madoff Investment Securities

Corporate bankruptcy rates soared during and after the Financial Crisis and between 2007 and

2010 the bankruptcy rates rose by 87.2% (Flynn and Kearns 2011, p.2). Among those corporate

collapses were numerous multinationals, once leading corporations (Heracleous and Werres

2016, p.491), but the example of Bernard Madoff and his Ponzi scheme stands out as the

biggest investment scam in history (Azim and Azam 2016, p.122). Bernard Madoff was the

CEO and founder of the investment corporation Bernard L. Madoff Investment Securities LLC

and ultimately confessed to running a large scaled Ponzi scheme for decades, resulting in

considerable losses for his 4,800 investors (da Silveira 2012, p.29). He was a prominent Trader

and Chairman of Nasdaq, a competitor to the New York Stock Exchange (Hurt 2009,

p.953), before the customers withdrew their deposits in the wake of the financial crisis.

The investigation following the crumbling of his empire revealed a $50 billion Ponzi

scheme that not only destroyed the life of individuals, but also led to corporation collapses in

the aftermath (Court Documents, 2009).

His motive of increasing his own power and profit explains his destructive trait of remorseless

scheming and manipulating, which is typically seen in a psychopath (Creswel & Landon 2009).

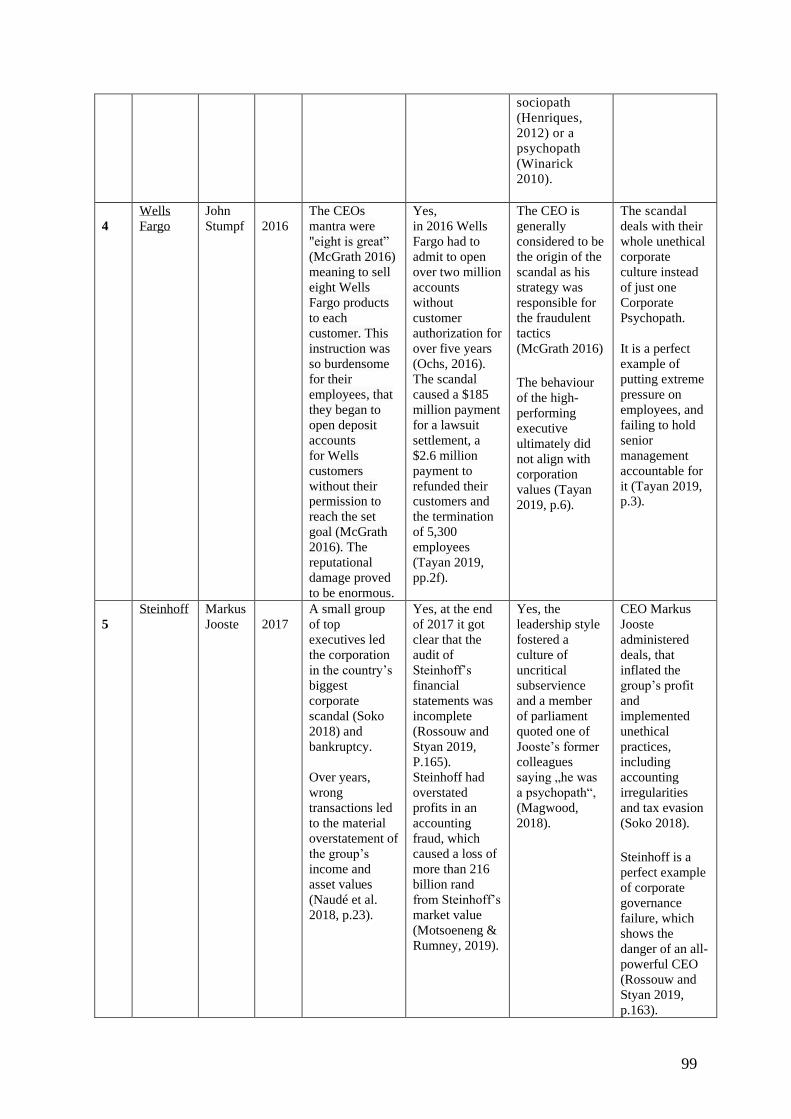

Various authors shared this observation and called Madoff either a sociopath (Henriques,

2012) or a psychopath (Winarick 2010). Even though Madoff and his actions within his

investment group have been named potentially psychopathic (Perri 2013) before the scandal

went down with many personal tragedies as its aftermath, questions arise why the fraud could

not be detected despite clear warning signs and eligible whistle-blowers.

4. Wells Fargo

The case of Wells Fargo is the only example where the discussed scandal did not lead to

a complete bankruptcy of the corporation. It also deals with their whole unethical corporate

culture instead of just one Corporate Psychopath. The Wells Fargo cross-selling scandal

illustrates the tensions that can emerge between corporate culture, financial incentives, and the

resulting employee behaviour (Tayan 2019, p.1). Even though Wells Fargo has been ranked as

“Great Places to Work” for several years (Tayan 2019, p.2), the CEO’s mantra was "eight is

great” (McGrath 2016) meaning to sell eight Wells Fargo products to each customer. This

instruction proved so demanding for bank employees, that they began to open deposit accounts

for Wells customers without their permission to reach the set goal (McGrath 2016). The high

pressure that was introduced by top management, made the employees desperate trying to meet

minimum goals to keep their jobs. A lawsuit against Wells Fargo later proved “employees who

7

failed to resort to illegal tactics were either demoted or fired as a result.” (Hill 2017, p.76).

Finally, in 2016 Wells Fargo had to admit to opening over two million accounts without

customer authorization over a time-span of five years (Ochs, 2016).

But even though the employees created those fake bank accounts, the CEO is generally

considered to be the origin of the scandal as his strategy was responsible for the fraudulent

tactics (McGrath 2016). Even though some complaints of the immoral activities reached the

CEO, they were ignored or downplayed, thus preventing an end to the scheming or even just

getting an insight into the extent of the growing scandal (Sison, Ferrero Muñoz, and Guitián

2018). Through this ongoing disguise of a large scaled fraud Wells Fargo became

„organizationally psychotic“ (McKay, 2016). In the end, the scandal caused a $185 million

payment to resolve a lawsuit by regulators, a $2.6 million payment that was refunded to

customers and the termination of 5,300 employees (Tayan 2019, pp.2f). The Wells Fargo

scandal is a perfect example of a toxic corporate culture that emphasizes fraud to create profit.

5. Steinhoff

The most recent is the Steinhoff Collapse in 2017. The South African retailer Steinhoff was

first thrust into a financial crisis in December 2017 after the resignation of its influential Chief

Executive Markus Jooste (Rossouw and Styan 2019a). In recent years, suspicions of possible

fraud grew due to the rapid pace of Steinhoff’s acquisitions (Naudé 2018). CEO Markus Jooste

administered deals, that inflated the group’s profit and implemented unethical practices, such

as tax evasion, accounting irregularities and in general low corporate standards (Soko 2018).

His leadership style created a culture of uncritical conformity and ultimately led the multi-

billion dollar corporation to the country’s biggest corporate scandal (Soko 2018). An

independent report found out that Steinhoff had overstated profits in an $7.4 billion accounting

fraud, with only the top leaders knowing of it. This caused a loss of more than 216 billion South

African Rand from Steinhoff’s market value (Motsoeneng & Rumney, 2019). When Jooste had

to appear in Parliament due to his criminal misconducts, a member of parliament quoted one of

Jooste’s former colleagues saying „he was a psychopath“, (Magwood, 2018) and asked Jooste

directly for his thoughts on this testimony about his character. The former CEO was entirely

unfazed and said „not in a position to comment on that“ (Magwood, 2018). The collapse can

be seen as the result of a failure in corporate governance and highlights the risks of a dominant

Chief Executive Officer (Sewpersadh 2019).

8

All these featured cases have been extensively analysed in the past but not in direct comparison

with each other. Even though the CEOs and their implemented corporation cultures have

already been identified as psychopathic before, they were never analysed to find specific

patterns connected with their dark traits.

2 Scientific Relevance

Literature Review

The first consideration of the literature research is the relationship between the characteristics

of Corporate Psychopaths and organizational performances within corporations. As

Corporate Psychopaths aim to become leaders, leadership in general and the setting of their

incentives in particular play an essential role in the performance of the corporation. The

literature on leadership and how to set the right incentives to get the leaders to align with the

goals of the corporation is extensive. However, as in finance the assumption is that everyone

is economically rational, leaders are seemingly distinct from their subordinates by possessing

traits that enable them to rightfully manage the future and convincingly be in control.

Consequently, much of the literature on leadership maintains the common belief in their ability

to predict the right future rather than questioning this trait. Critical articles of the common

concept of leadership started challenging the mainstream literature, arguing that it is also

important to consider the effects of leadership on the collective rather than simply on the

individual (Drath et al. 2008) and to examine “asymmetrical power relations and insecurities”

(Bryman et al. 2011, p.184) within the hierarchy. Another critical aspect is the incentive setting

of leaders, as it is likely the most crucial strategic factor for an organization. It is used to direct

managerial decisions and channel the behaviour of subordinates (Gomez-Mejia et al. 2014).

But in today´s corporation, especially the payments of CEOs can often lead them to make short

term decisions and manipulate corporation results. This phenomenon of moral hazard could be

encouraged by the typical characteristics of Corporate Psychopaths.

The current state of the literature about Corporate Psychopaths is not only provided by

psychology researchers but is also an interesting topic for the economic field of study. The

issues of the dark triad have been primarily dealt with by psychology papers but due to the

common traits within their characteristics, their economic effects got increasingly interesting

from the corporation´s point of view. Particularly after the Global Financial Crisis, economists

like Clive R. Boddy started to research to what extent leaders, that were directly linked to past

corporate failures, might be Corporate Psychopaths (Boddy 2011). The reviewed research

9

suggests that each dark triad member has their own facets but the published studies in each field

tend to combine their dark characteristics summarizing it in the term Corporate Psychopath

(Furnham, Richards, and Paulhus 2013).

Current State of the Art

The different research directions surrounding Corporate Psychopaths and their impact

demonstrate the increasing importance of this subject. As the size of modern corporations is

constantly growing, the effect of Corporate Psychopaths as leaders is naturally expanding but

has in fact received relatively little academic attention (Tombs and Whyte 2015, p.2). But how

do Corporate Psychopaths affect the leadership and culture within a corporation and what are

typical characteristics of failing corporations that are attributable to those Psychopaths? In

most of the research, the consequences of them as part of corporations is not included. However,

further studies of destructive characteristics may lead to a better understanding of leadership in

general (Kellerman 2004). It is a particularly important aspect as research across different

domains implicates that negative people and experiences always have a stronger effect than

positive ones (Kaiser, LeBreton, and Hogan 2015). Even though there is existing research of

Corporate Psychopaths, Harms et al. (2011) already noted that the nature of the dark side of a

person and their resulting behaviour appears “far more complex than originally thought”

(Harms, Spain, and Hannah 2011, p.508). There is still a lot of research necessary to figure out

all the similarities and differences between Corporate Psychopaths but even more critical is the

link between their characteristics and their behaviour as leaders. It will take a great deal of

further research in order to understand how it actually affects leadership (Kaiser, LeBreton, and

Hogan 2015). Additionally, several economists have previously highlighted the far‐reaching

effects on their employees and the corporate governance issue Corporate Psychopaths present

(Boddy 2017). And as most organizations have a pyramidal structure, the tone at the top likely

has a multiplier effect throughout all segments of the corporation. Hence, the top managements

control of organizational resources and their decision-making power for important strategic

choices within a corporation have an enormous effect on the company´s future (Gomez-Mejia

et al. 2014).

But what measures could help to control dark traits of leaders within a corporation?

Behavioural Agency Theory is a theoretical basis for dealing with incentive setting strategies.

Even though it is an established theory based on Agency Theory (Pepper and Gore 2015,

p.1046), only more recent literature started to address the evolution of incentives regarding

10

their impact after multiple corporate failures. However, it could be a relevant theoretical basis

for discussing strategic ways of managing dark characteristics in a corporation. Another

relevant aspect when dealing with Corporate Psychopaths as CEOs is Corporate Governance.

In essence, Corporate Governance is about the way power is performed over corporate entities

and setting a framework for those managing it (du Plessis, Hargovan, and Harris 2018). The

global financial crisis raised fundamental questions about the functions of Corporate

Governance (Tricker and Tricker 2015, p.18) and how it could help to prevent unpredicted

corporate collapses. Consequently, research regarding the application of Behavioural Agency

Theory and Corporate Governance in the actual business areas of today´s complex organization

of corporations has become more and more relevant and should be expanded. The question

which now arises is how does the knowledge of these help modern corporations detect or

prevent misalignment of the agent or even corporate failure?

This thesis will cover Corporate Psychopaths, leadership and the link between them in order to

create a valuable contribution to both research areas and their impact on corporations as a

whole. In order to do so, it is only reasonable to link leaders of the dark triad to corporate

failures in order to figure out which characteristics of a corporation indicate a possible threat.

This combination has not yet been evaluated in this way and could provide a great insight into

signs of corporate failure due to Corporate Psychopaths.

Structure of Content

After introducing the topic together with relevant examples in chapter 1, the scientific relevance

is described in chapter 2, followed by defining the terms Corporate Psychopath and ‘dark triad’

in chapter 3. Chapter 4 explains the case study design starting with the analytical framework of

Behavioural Agency Theory in combination with the Corporate Governance Aspect, followed

by the methodology of this design. The section furthermore highlights the specific criteria of

the deliberate sample and the target setting is explained. The deliberate samples are explained

with a particular emphasis on why they are representative of Corporate Psychopaths as CEOs

and psychopathic cultures in corporations. Part 4.3 uses psychopathy measures to figure out

if considerable overlap exists between reported behaviour and the measure of psychopathy

applied (Boddy 2016a). Thereafter in section 4.4 the topic of why psychopaths are rising up

within corporations is treated as well as their leadership mechanisms to influence their

employees. In accordance with that the multiplier effect of the behaviour of leaders along

with possible intra-organizational ganging dynamics and key characteristics of whole

11

corporations as psychopaths are examined in section 4.5. The risk of corporate fraud

occurring due to Corporate Psychopaths is explored in section 4.6. Consequently, wrapping up

the research is done by a cross-case analysis of the findings in Chapter 5.

With the help of the described findings, it is possible to create guidelines how to handle

Corporate Psychopaths in chapter 6. The first step is figuring out how to recognize any

psychopathic traits within a corporation, whether in a whole culture or just one individual. As

a result, the second point is how to manage the recognized personalities. The third and most

important point is how to prevent casualties of their characteristic traits for the corporation or

even prevent those Corporate Psychopaths from entering it. The last point is describing the

lessons learned from the numerous cases of historic corporation failures. The thesis ends with

a reflection, as well as its limitations and implications for further work that has to be done.

3 Corporate Psychopaths and the “Dark Triad”

Definition

The general expression of a sociopathic personality first emerged during the 1930s (Lykken

2006, p.4). Based on this, the work of the psychiatrist Cleckley (1941) shaped the idea of the

pathological condition psychopathy. His research firstly identified key criteria including lack

of anxiety and guilt, poverty of emotions, and most importantly lack of empathy (Pardue,

Robinson, and Arrigo 2013, p.131). An official approach to defining the term psychopathy

comes from ‘A Dictionary of Psychology’, which describes it as “a mental disorder roughly

equivalent to antisocial personality disorder, but with emphasis on affective and interpersonal

traits such as superficial charm, pathological lying, egocentricity, lack of remorse, and

callousness.” (Colman, 2001, p.618). Therefore, it is possible to conceal psychopathy and

appear normal, to an extent where psychopaths can easily gain the trust of their surroundings.

Due to their manipulative qualities they are generally perceived as competent and well-meaning

(Pardue, Robinson, and Arrigo 2013, p.131).

However, some psychopaths tend to use instrumental violence like robbery to get what they

desire, resulting in a high number of psychopaths in prison (Kiehl and Hoffman 2011, p.1).

Most psychopaths lack a moral compass resulting in going through life taking what they want.

They tend to rationalize and justify their own behaviour, often not accepting the responsibility

for their own activities and finding a way to blame others for it (Pardue, Robinson, and Arrigo

2013, p.134). This is the reason why psychopathy is generally seen as the most dangerous of

12

personality disorders (Babiak et al. 2012, p.1). Yet, some of them have a better ability to control

their impulses which enables them to strive for a corporate instead of a criminal career (Boddy

et al. 2015, p.532). Although Cleckley (1941) regarded psychopaths as pathological, he already

noticed some adaptive characteristics such as social poise when he wrote about a psychopathic

business man who exploited his interpersonal charm for his own occupational success (Smith,

Watts, and Lilienfeld 2014, p.507). Consequently, psychopaths can differ vastly from one

another, and their condition can range in severity and therefore also in their personality traits

(Babiak et al. 2012).

The modern literature has different expressions for the phenomenon of a psychopath working

and operating in an organizational area (Boddy 2005), like executive, or organizational

psychopaths/sociopaths (Pech and Slade 2007). As previously stated, the most used one is the

phrase „Corporate Psychopath“ (Boddy 2011, p.256) which is a combination of the term

‘psychopath’ from the area of psychology and the term ‘corporate’ from the business literature.

Measurement

In general the term psychopathy refers to a personality disorder that covers interpersonal,

affective, lifestyle, and antisocial traits and behaviours (Babiak et al. 2012, p.1) and is

determined by two dimensions, whose characteristics psychopaths highly exhibit. The first

dimension consists of lack of affection and interpersonal manipulation. The lack of affect factor

describes psychopaths as cold-hearted humans without remorse but also physical and social

fearlessness (Smith, Watts, and Lilienfeld 2014, p.507). As they strive for their personal wealth,

they might be unable to have real emotions or empathy but are capable of simulating feelings.

The second factor of interpersonal manipulation expands this attribute by indicating that they

are usually perceived as completely normal (Lingnau and Dehne-Niemann 2016). The second

dimension is divided into erratic lifestyle and antisocial behaviour and therefore contains the

behavioural features of psychopathy. Here, erratic lifestyle refers to the extremely impulsive

nature of psychopaths. As psychopaths normally have very limited self-control they can be

provoked quickly and tend to short but violent outbursts of anger (Lingnau and Dehne-Niemann

2016). A more detailed description of the two dimensions and its traits can be found in Chapter

4.3.2.

The two most widely used psychopathy measures, the interview-based Psychopathy Checklist-

Revised (PCL-R) (Neumann, Johansson, and Hare 2013) as well as the Psychopathic

Personality Inventory-Revised (PPI-R) (Koglin and Petermann 2009) are both based on these

13

broad dimensions. The two-dimension composition carries important implications for the

different display of psychopathy (Smith, Watts, and Lilienfeld 2014, p.507). As so-called

successful psychopaths, Corporate Psychopaths often do not have all four of the factors. Unlike

psychopathic criminals, they tend to have little or no trait of the secondary psychopathy

dimension, which helps them to apparently fit into society.

Origin

Understanding psychopathy starts with knowing the fundamental principles about personality.

The personality represents who an individual is and results not only from genetics but also from

the upbringing. Therefore it reflects how individuals see and experience their surrounding

(Babiak et al. 2012, p.1). A personality is officially defined as “the set of psychological traits

and mechanisms within the individual that are organized and relatively enduring and that

influence his or her interactions with, and adaptations to, the intrapsychic, physical, and social

environments” (Larsen and Buss 2005, p.4). Individuals’ personalities evolve only until roughly

their late 20s (Babiak et al. 2012, p.1), which is why psychopathic behaviours typically begin

in childhood and continue in adolescence. Just like any personality this lifelong disorder is a

result of connections between biological and temperamental predispositions but also social

drives (Babiak et al. 2012, p.1). Therefore it can occur as a consequence of physical or cultural

factors but in their study of male twins, Taylor et al. (2003, pp.633f) found that psychopathic

traits were primarily associated with genetic factors. The dominant physical factor is abnormal

brain connectivity, especially in the orbitofrontal cortex regions (Finger et al. 2011, p.152)

which results in the inability to experience empathy. As the orbitofrontal cortex regions is the

region of the brain that is responsible for emotion, any disturbance of its functions can lead to

socially inappropriate behaviour (Wernke and Huss 2008, p.231), especially when making

moral judgments. Since Corporate Psychopaths have no real sense of emotion they are able to

make very rational decisions without any sign of delusions or nervousness where other people

would maybe make different choices based on their emotions (Boddy 2006, p.1468). Even

though psychopathy might arise from genetic factors, environmental factors need to be

considered, too. Contributing factors to the disorder are poor parenting, child abuse and the use

of drugs (Gao et al. 2010, pp.7f).

But whether to physical or cultural factors, psychopathy exists in all societies. Psychopathy can

occur in both males and females within all race, cultures and socioeconomic backgrounds.

Psychopaths may themselves even be married and have a family (Babiak et al. 2012). In

14

general, researchers agree that psychopaths understand right from wrong but willingly disregard

society’s rules to pursue their own interests (Babiak et al. 2012). There is also a consensus

among these experts that psychopaths should be carefully managed rather than treated, as

psychopathy is not curable and treatments not available at present (Harris and Rice 2006,

p.568).

Development in a corporation

Even with today´s knowledge of psychopaths, they have no problems in joining the business

world of politics, law enforcement, government, and academia. In our society they are part of

all areas of work, from executive to blue-collar position (Babiak et al. 2012, p.2). In the

recruitment phase, such individuals tend to impress as they appear calm and charming due to

their limited range of emotions. Psychopaths try to win over their superiors, whilst

simultaneously exploiting their subordinate and colleagues, often taking credit for their work

(Boddy 2005, p.37). They appear sophisticated, and can be very successful in a corporation

(Boddy 2011, p.256). As accomplished manipulators, they find gaining promotions relatively

easy, as their lack of empathy and their callousness allow them to make difficult business

decisions, such as mass dismissals, without any moral consideration (Omar, Wisniewski, and

Yekini 2019, p.1198). Kühn (2012) came to the conclusion that the personality of the described

„Homo oeconomicus“ widely overlaps with that of a Corporate Psychopath. After reaching

supervisory positions, they refuse to share information and introduce self‐serving rules and

procedures (Boddy, Galvin, and Ladyshewsky 2011, p.17) as Corporate Psychopaths are mostly

concerned with their own goals of money and power and value them over the success and

longevity of the corporation they work for. These actions result in reduced employee job

satisfaction (Mathieu et al. 2014, p.87) with over 30% of bullying in corporations being

accounted for by the behaviour of Corporate Psychopaths (Boddy 2014, p.113). Research

shows that psychopathy is additionally associated with the use of hard negotiation tactics and

poor management skills (Smith, Watts, and Lilienfeld 2014, p.509). Corporate Psychopaths

disregard any kind of corporate social responsibility and can destroy the reputation of their

employer (Boddy 2012, p.79). Their constant need for stimulation can also induce excessive

risk-taking, which can put entire corporations in crisis (Omar, Wisniewski, and Yekini 2019,

p.1198).

Corporate Psychopaths create deliberate chaos in a corporation to deflect the blame for their

failure and to hide their unlawful activities. The relatively chaotic nature of a modern

corporations is helping them to rise quickly in their hierarchy unnoticed. Today’s global

15

corporations are used to rapid change and thus also to a constant turnover of staff. These rapidly

changing conditions within a corporation make it hard to spot Corporate Psychopaths (Boddy

2011, p.257). Consequently Corporate Psychopathy has been described as “the most important

forensic concept of the early 21st century.”(Babiak et al. 2012, p.3).

“Dark Triad”

Despite individual theoretical roots on the three socially aversive personalities: Narcissism,

Machiavellianism, and Psychopathy, the distinctions grew blurred over time (Jones and Paulhus

2014, p.28). As a result, Paulhus and Williams (2002) formulated the term Dark Triad to

encourage studying the three traits together to be able to clarify their common features as well

as their differences. The three personalities can all be found under the term Corporate

Psychopaths. They are named the Dark Triad due to their common socially undesirable traits,

and conceptual similarities (Rauthmann 2012, p.487). Indeed, studies have shown considerable

positive correlations between measures of the traits of the Dark Triad and counterproductive

workplace behaviour (O’Boyle et al. 2012, p.569). However, the analysis also showed, that

each characteristic trait of the Dark Triad exhibits different behaviour therefore recent research

often focuses on their individual diversified impact on corporations (Perry 2015). As

Machiavellians are more linked with interpersonal forms like maltreatment of co-workers and

outcomes predicted by a strategic orientation (Jones and Paulhus 2014, p.30), Narcissists are

more associated with workplace behaviour for ego-promoting outcomes such as bullying and

white-collar crimes. And finally, psychopathy is often involving reckless, violent and

aggressive workplace behaviour (DeShong, Grant, and Mullins-Sweatt 2015). However, the

goals of the different Dark Triad members frequently align as they all display a common

callousness and way of thinking (Jones and Figueredo 2013). To varying degrees, they all show

tendencies to self-promotion and aggressiveness (Paulhus and Williams 2002, p.557).

3.2.1 Machiavellianism

Christie and Geis (1970) were the first to introduce the concept of Machiavellianism into the

characteristic literature and it was mainly based on the political strategist, Niccolo Machiavelli

(1513-1981). The construct emerged from a selection of statements from Machiavelli´s original

books (Paulhus and Williams 2002, p.556), especially from a book entitled Il Principe (The

Prince) from 1532. The Prince was addressed to kings and lords and advises them to secure

their power, if necessary even through methodically planned immoral deeds, including the

removal of rivals (Muris et al. 2017). Christie and Geis constructed these statements into a

selection of personality attributes to be able to measure Machiavellianism. Further research

16

showed that respondents who agreed to the summarised, twenty-point measure of

Machiavellianism (Boddy 2010, p.301), were more likely to behave in a calculating and cold

fashion (Christie & Geis, 1970). The measurement also includes traits like a cynical worldview,

especially of human nature (Jones and Paulhus 2014, p.29), a general immoral outlook (Spurk,

Keller, and Hirschi 2016, p.113) and self-beneficial motives with strategic planning

(Rauthmann 2012, p.487). Machiavellians are known for planning ahead, building alliances,

and trying to maintain a positive reputation. They are strategic rather than impulsive (Jones and

Paulhus 2011).

Overall there are differing results on how Machiavellians are perceived by others. In general

young Machiavellians appear to be liked by their colleagues (Hawley 2003) but Machiavellian

behaviours are often rejected (Falbo 1977), and individuals judge Machiavellians more

negatively after an extended involvement with them (Rauthmann 2012, p.488).

Machiavellianism within corporations describes a ruthless and selfish approach to management.

3.2.2 Narcissism

The general theory of Narcissism was developed by Freud and named after the myth of

Narcissus, a beautiful man who was cursed by a goddess to fall into unreturned love. He fell in

love with his own reflection and unable to leave his image, he died of starvation (Holme, 1981).

The construct of Narcissism emerged from Raskin and Hall (1979), who invented the

Narcissistic Personality Inventory (NPI). Facets from this clinical syndrome are characterized

by a high self-love with desire of control, admiration and most importantly success (Paulhus

and Williams 2002, p.557). The basic characteristics of narcissists include grandiosity,

entitlement, dominance, and a high level of arrogance (Özsoy 2018, p.743) Especially

grandiosity can lead narcissistic characters on a pursuit for ego-boosting (Morf and Rhodewalt

2001), frequently ending in self-destructive behaviours (Vazire and Funder 2006). Narcissistic

grandiosity also promotes a sense of entitlement and can even turn into aggression as soon as

the own grandiosity is threatened (Jones and Paulhus 2014, p.30).

Therefore, a narcissist has since been seen as someone “who loves themselves too much for

their own good” (Boddy 2010, p.302). Narcissists demand the admiration of others but have

difficulties in maintaining any relationships due to their general lack of trust and also affliction

for others (Spurk, Keller, and Hirschi 2016, p.113). They even tend to belittle others or are

vengeful against colleagues (Omar, Wisniewski, and Yekini 2019, p.1203). Narcissists can be

popular, and liked at first but are seen not favourably as interactions progress (Back, Schmukle,

17

and Egloff 2010), as their arrogant and hostile behaviour causes the loss of their previously

positive reputation (Rauthmann 2012, p.488).

3.2.3 Psychopathy

The adaptation of clinical psychopathy is the most recent of the Dark Triad (R. D. Hare 1985).

The previously mentioned self-report psychopathy scale was first assembled by Hare (1985)

and later expanded in the generally accepted Psychopathy Checklist, which is still the standard

measurement of psychopathy (Paulhus and Williams 2002, p.557). Psychopathy is defined by

the impulsivity of that person, a lack of guilt or remorse about their actions as well as a belief

in the superiority of oneself (Spurk, Keller, and Hirschi 2016, p.113) and might include criminal

activities (DeShong, Grant, and Mullins-Sweatt 2015). They tend to lie for instant rewards,

even if it compromises the general long-term interests (Jones and Paulhus 2014). Thus

psychopaths act impulsively, have a tendency to thrill-seeking, and due to their callousness pay

little attention to their reputations (R. D. Hare and Neumann 2008).

Due to their manipulative behaviour, they can appear similar to narcissists at first until their

antisocial behaviours come to light. However, due to their lack of empathy and impulsiveness

some of them seem repulsive from the beginning (Rauthmann 2012, p.488). Of the three

personality disorders, psychopaths are the most studied and apparently the most dangerous ones

as well (Paulhus, Williams, and Harms 2001, p.5).

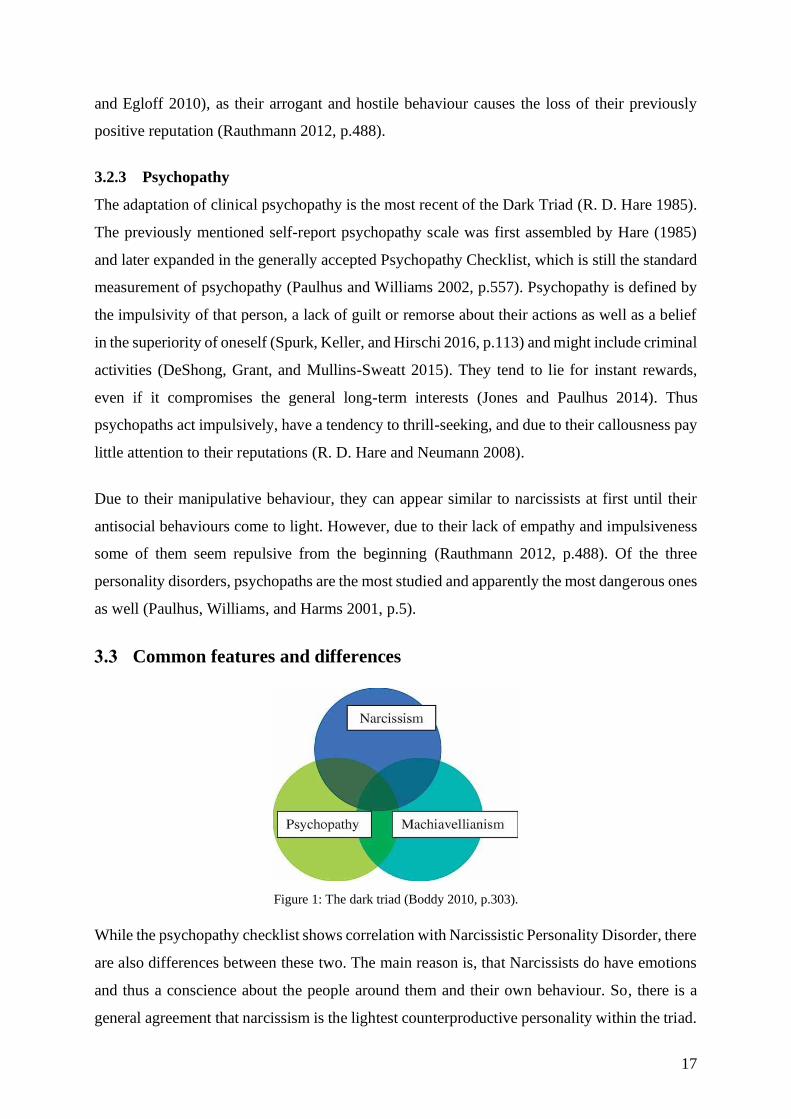

Common features and differences

Figure 1: The dark triad (Boddy 2010, p.303).

While the psychopathy checklist shows correlation with Narcissistic Personality Disorder, there

are also differences between these two. The main reason is, that Narcissists do have emotions

and thus a conscience about the people around them and their own behaviour. So, there is a

general agreement that narcissism is the lightest counterproductive personality within the triad.

18

The minimal anxiety and their lack of real emotions make psychopaths the most treacherous of

the three, even though Machiavellianism and psychopathy appear very similar (Boddy et al.,

2015, p.533). The various studies of Paulhus & Williams have shown that especially

interpersonal manipulation and callous affect are common traits within all the Dark Triad

personalities. This evidence shows, that the core of the Dark Triad is generally based on the

talent of interpersonal manipulation (DeShong, Grant, and Mullins-Sweatt 2015). The members

of the Dark Triad share a common core of disagreeableness over time and consequently of a

social destructiveness in their environment (Paulhus and Williams 2002, p.561). Indeed, dark

personalities exhibit behaviours aimed at getting ahead instead of getting along, which reflects

their anti-sociality (Rauthmann 2012, p.488).

But there are also clear differences, as Jones and Paulhus (2012) concluded that egoistic goals

drive narcissistic behaviour, whereas instrumental goals or material gain motivate

Machiavellians and psychopaths (Jones and Paulhus 2014, p.30). Machiavellianism

distinguishes itself from psychopathy with respect to the element of impulsivity (Jones and

Paulhus 2014, p.29). Narcissists also exhibit the most self-enhancement, followed by

psychopaths. In contrast, Machiavellians showed no sign of self-enhancement, as they are more

reality-based (Paulhus and Williams 2002, p.561).

The following statements are used for a SD3 (Short Dark Triad) Test. Items should be kept in

the same order, reversals are indicated with (R) here and the statements can be evaluated from

Disagree strongly to Agree strongly (1-5). It reflects the dark triad and their differences (Jones

and Paulhus 2014). All of those traits can be seen in Corporate Psychopaths.

Machiavellianism

1. It’s not wise to tell your secrets.

2. I like to use clever manipulation to get my way.

3. Whatever it takes, you must get the important people on your side.

4. Avoid direct conflict with others because they may be useful in the future.

5. It’s wise to keep track of information that you can use against people later.

6. You should wait for the right time to get back at people.

7. There are things you should hide from other people to preserve your reputation.

8. Make sure your plans benefit yourself, not others.

9. Most people can be manipulated.

Narcissism

1. People see me as a natural leader.

2. I hate being the center of attention. (R)

3. Many group activities tend to be dull without me.

4. I know that I am special because everyone keeps telling me so.

5. I like to get acquainted with important people.

19

6. I feel embarrassed if someone compliments me. (R)

7. I have been compared to famous people.

8. I am an average person. (R)

9. I insist on getting the respect I deserve.

Psychopathy

1. I like to get revenge on authorities.

2. I avoid dangerous situations. (R)

3. Payback needs to be quick and nasty.

4. People often say I’m out of control.

5. It’s true that I can be mean to others.

6. People who mess with me always regret it.

7. I have never gotten into trouble with the law. (R)

8. I enjoy having sex with people I hardly know

9. I’ll say anything to get what I want.

(Jones and Paulhus 2014, p.31).

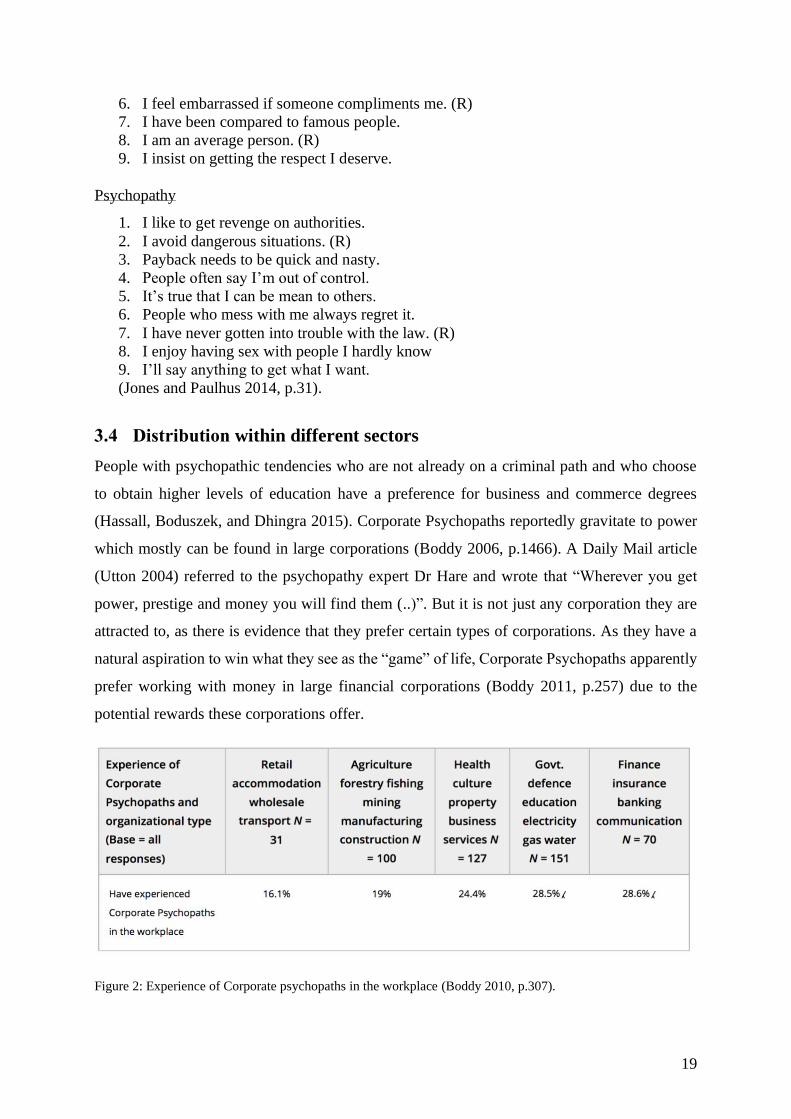

Distribution within different sectors

People with psychopathic tendencies who are not already on a criminal path and who choose

to obtain higher levels of education have a preference for business and commerce degrees

(Hassall, Boduszek, and Dhingra 2015). Corporate Psychopaths reportedly gravitate to power

which mostly can be found in large corporations (Boddy 2006, p.1466). A Daily Mail article

(Utton 2004) referred to the psychopathy expert Dr Hare and wrote that “Wherever you get

power, prestige and money you will find them (..)”. But it is not just any corporation they are

attracted to, as there is evidence that they prefer certain types of corporations. As they have a

natural aspiration to win what they see as the “game” of life, Corporate Psychopaths apparently

prefer working with money in large financial corporations (Boddy 2011, p.257) due to the

potential rewards these corporations offer.

Figure 2: Experience of Corporate psychopaths in the workplace (Boddy 2010, p.307).

20

The research of Boddy (2010) provides evidence that Corporate Psychopaths appear at a

greater level in the financial service sector and the civil service in comparison to primary

industries and retail services. On the other hand, professions that are dedicated to serving others

like social work seem way less attractive to individuals whose main motivation is always an

egoistic one which is the case for Machiavellians, Psychopaths and Narcissists (Boddy 2010).

3.4.1 Distribution within the hierarchy of a corporation

As already mentioned in the definition of Corporate Psychopaths, those individuals often end

up in positions of power, as there exists significant incidence of the emotional components of

psychopathic personality disorder in a sample of senior managers (Omar, Wisniewski, and

Yekini 2019, p.1198). Even though it contradicts general management principles, dark triad

managers are able to rise through the ranks into those positions with high power. Due to their

skills in manipulation they can hide possible performance shortfalls by using bullying tactics

(Pech and Slade 2007). In a study of nearly two hundred executives, 3.5 % of the top senior

executives were psychopathic as measured by the Psychopathy Checklist (Boddy,

Ladyshewsky, and Galvin 2010, p.127).

4 Case Study Design

This thesis focuses specifically on the issue of Corporate Psychopaths and their destructive

effects within a corporation. However, even with exact measurements and clear guidance on

how to diagnose a dark triad personality disorder (Hare, 1991) executives will be unwilling to

participate in surveys, particularly if those could expose the dark side of their character.

Therefore a more practical approach is to collect information in a more discrete way by going

through archived data (Omar, Wisniewski, and Yekini 2019, p.1197). In order to provide

concrete correlations between Corporate Psychopaths as leaders and their corporate

destructiveness it is necessary to select exemplary collapses or scandals of big corporations in

the past. Combining those real examples with a theoretical background should enable the setup

of hypotheses about typical characteristics within a failing corporation due to Corporate

Psychopaths.

Analytical Framework

The theoretical framework emphasizes that top executives affect corporate goals, values, and

actions and therefore may exhibit certain psychological traits which become a strong driving

force and shape the whole corporation. As Corporate Psychopaths are disproportionally

21

represented within higher managerial positions (Babiak, Neumann, and Hare 2010), their

decisions and behaviour have a concrete influence on broader society (Omar, Wisniewski, and

Yekini 2019, p.1197). On the basis of the argument that behavioural agency theory and

corporate governance codes are both based on the agency theory, combining them may improve

the explanatory value of agency-based models of the executive behaviour as well as insight into

how these behaviours could be controlled. This combination also takes the modern structures

of corporations as well as the risk of having Corporate Psychopaths as leaders into account.

4.1.1 Behavioural Agency Theory

In essence, information asymmetry permits Corporate Psychopaths as executives to disguise

the actual motives for their behaviour. Even though not all leaders pursue managerial

opportunism, shareholders do not have any way of knowing which person is going to exhibit

such tendencies in advance. Unfortunately, the temptation to make up profits as well as hiding

losses is extensively too great for those whose jobs and wealth depend on the results (Downes

and Russ 2005, p.94).

The standard agency framework centres on monitoring costs and incentive setting as the basic

theoretical assumption is the misalignment of agents and principals, which often leads to moral

hazard. In contrast, the behavioural agency theory sets the agent performance at the centre of

its concept, declaring that the interests of shareholders and agents can be aligned if the

responsible leaders are motivated to work to the best of their own abilities (Pepper and Gore

2015, p.1045). Consequently, the main theoretical background on the conduct of Corporate

Psychopaths as leaders is Behavioural Agency Theory, developed by Wiseman and Gomez-

Mejia (1998). This theory is often seen as a progression of the traditional agency theory, since

the model integrates concepts from the behavioural theory of the firm (March and Shapira 1992)

and agency theory (Gomez-Mejia et al., 2015). In this model elements of internal corporate

governance are combined with the incorporate ideas from prospect theory (Tversky and

Kahneman 1992) in order to explain executive risk-taking behaviour of different kinds of

leaders (Wiseman and Gomez-Mejia 1998, p.133). The Behavioural Agency Theory is based

on four key factors which affect their strategic decision making (Camerer, Loewenstein, and

Rabin 2011). These components are loss aversion, preferences linked to uncertain outcomes,

temporal discounting, and lastly fairness as well as inequity aversion (Pepper and Gore 2015,

p.1047).

22

Considering these factors, the importance of the agent’s intrinsic and extrinsic work motivation

is not to be underestimated. The Behavioural Agency Theory questions the idea that intrinsic

and extrinsic motivation are independent or even additive. Frey and Jegen (2001) have

described this phenomenon as “crowding-out“, arguing that unpredictable monetary rewards

might even cause a reduction in intrinsic motivation (Deci and Ryan 1985). The first factor of

behavioural agency theory presumes that especially senior executives are primarily loss averse

and just secondary risk averse, since losses linked to their future pay pose a significant threat

to their perceived wealth, and to the executives standard of living (Wiseman and Gomez-Mejia

1998, p.140). Principally it means, that decision makers are generally more concerned about

losing wealth than to increasing it (Wiseman and Gomez-Mejia 1998). This component

explains why decision makers act conservatively when facing gains but almost always take

greater risks when facing a loss, as there is nothing more to lose than the general loss itself.

Consequently, the second factor of preferences relating risky and uncertain outcomes also

depend on the loss aversion, as when forecasted performance is unsatisfactory, executives may

anticipate losses to wealth and thus consider taking greater strategic risks (Wiseman and

Gomez-Mejia 1998, p.137). Below an individual reference point, agents will be loss averse but

above the reference point they will traditionally be risk averse. Specifically, senior executive's

risk preferences are revealed through their strategic choices on behalf of the corporation.

Extensive research has shown that risk bearing mediates the relationship between how the

situation facing an executive is framed and the amount of risk the executive is willing to take

(Gomez-Mejia et al., 2015). These choices hold important implications for the firm's

performance and the agent's general compensation risk (Wiseman and Gomez-Mejia 1998,

p.135), especially when dealing with Corporate Psychopaths.

The third factor is linked to agent´s time preferences. Within behavioural agency theory, the

assumption is that agents discount time to a hyperbolic discount function, rather than an

exponentially one (Ainslie & Haslam, 1992). It implies that possible future rewards are

deliberately discounted even though the actual discount rate is individual. The fourth and last

component is the perception of equitable compensation of the agent. If they feel like their input

and skills are valued and adequately rewarded the agents will be motivated to contribute to the

corporation´s success at a high level (Adams 1965). However, if this is not the case and the

output is not proportionate, the agent will become demotivated. The agent’s equity criterion is

individual according to the proper market standards and personal assessment. Fehr and Schmidt

(1999, p.819) call this important factor “inequity aversion.”

23

An important assumption of behavioural agency theory is that the top executive teams have a

vital impact on firm performance. This is especially important when dealing with Corporate

Psychopaths in this group of chief executive officers (CEO), the chief operating officers (COO),

the chief financial officers (CFO), or divisional heads (Pepper and Gore 2015, pp.1050f ). They

are responsible for defining and executing the corporation’s strategy (Carpenter, Geletkancz,

and Sanders 2004) and usually receive a lot of monetary compensation for their work. However,

in the last decades there has been considerable discussions about the structure of top

management compensation in large corporations, on whether it is rightfully designed to lead

executive decision making toward maximizing the general performance (Finkelstein and

Hambrick 1988).

Behavioural agent theory argues that any high management team needs a balanced set of reward

strategies with a combination of fixed and variable pay and short- and long-term incentives to

maximize the agent´s motivation to optimize their own job performance in regard to the best

interest of the corporation. To maximize the overall corporation performance, the selected

strategy must be valid for all the agents in the top management team. Identifying the optimal

reward strategy for the corporation requires an understanding of all the top executives agents

and their individual risk tolerances (Pepper and Gore 2015, p.1063), which makes it even more

important to identify members of the dark triad in their ranks.

4.1.2 Corporate Governance

The idea of behavioural agency theory is also closely linked to the general aspect of Corporate

Governance, as agency theories are used as the implicit theoretical background to study

governance issues (Jensen and Meckling 1976). It is an umbrella term which covers the

activities and composition of the board of directors, compensation policies (Cuomo, Mallin,

and Zattoni 2016), the relationships with the shareholders, with those managing the corporation

as well as with external regulators, auditors and other legitimate stakeholders. In essence,

Corporate Governance is the framework of rules and processes by which authority is managed

and controlled within a corporation and covers the mechanisms by which those in control

should be held accountable (du Plessis, Hargovan, and Harris 2018).

Corporate governance codes can be formulated at three different hierarchical levels. The first

level is the international one, where codes are developed by institutions such as Pan‐European,

Commonwealth or OECD, in order to increase governance standards in a whole geographic

24

region. The second level is national. Codes are issued by institutions like the government or the

stock exchange within individual countries to be able to positively influence corporate

governance practices in a specific national environment. The last is the individual firm level,

where codes are established by corporations to communicate to share- and stakeholders their

governance principles (Cuomo, Mallin, and Zattoni 2016). In case of the corporation´s level the

board of directors should generally be responsible for supervising the management and also for

its decisions and performance (Tricker & Tricker, 2015), which is especially important when

dealing with Corporate Psychopaths as CEOs. The corporate governance code of a corporation

should press the board of directors to take on an active role in controlling the behaviour of the

top executives. But contrary to other forms of regulation, governance codes are "formally

nonbinding and voluntary in nature " (Haxhi and Aguilera 2015, p.2), which allow firms the

flexibility to select which corporate governance structure they adopt in order to pursue their

objectives, while simultaneously guaranteeing better transparency (Cuomo, Mallin, and Zattoni

2016, p.223). The „comply or explain“ application (Mallin 2013, p.36) provides a voluntary

method for improvement and innovation of the applied corporate governance practices. The

individual corporations all have the option to comply with the codes’ recommendations or they

have to explain the reasons why they could not (Cuomo, Mallin, and Zattoni 2016, p.223).

However, despite the positive effect this voluntarily approach can have, there also is doubt on

its actual effectiveness (Pietrancosta 2010). In contrast to hard law regulations, corporate

governance codes are not able to enforce good business practices from corporations as they

have the option to not comply. Empirical evidence exhibits that corporations comply with

codes’ recommendations more in form than in substance (Krenn 2014). However, at the same

time hard law regulation can also have negative implications for governance practices, as recent

studies revealed increased costs of compliance with regulation (Sasseen and Weber 2006),

which can be especially high for small corporations (Engel, Hayes, and Wang 2007).

The accumulated corporate scandals over the last two decades have underlined the failure of

the existing governance mechanisms, like appropriate and equal governance codes for all

(Cuomo, Mallin, and Zattoni 2016, p.224). Especially after the Enron debacle in 2002 almost

all advancing economies added further strands to corporate governance policy as codes have

become a popular method of increasing corporation’s accountability (Mallin 2013). The second

phase of expanding national codes development occurred after various corporate scandals led

to the global financial crisis. Consequently the amount of corporate governance codes increased

exponentially after this (Cuomo, Mallin, and Zattoni 2016, p.222). Simultaneously, the

25

establishment of new corporate governance codes always occurred alongside with stricter legal

standards aimed at increasing investor protection.

These increasing demands of corporate governance codes and new legal norms for transparency

and reporting are all in their core responses to the agency dilemma. Indeed, the conceptual

framework of corporate governance codes is the need to respond to the agency problem as

wherever there is a separation between the members and the governing body, the agency

dilemma could arise and corporate governance issues could occur (Tricker and Tricker, 2015).

Therefore, the main goal of corporate governance is to find the right mechanisms to align the

agents with the interests of the responsible principals and consequently with the corporation

(Wiseman and Gomez-Mejia 1998, p.133). As a result of the increasing globalization,

supranational institutions are gaining importance to implement governance codes to avoid

massive corporate frauds in the future and to stimulate regular revision (Cuomo, Mallin, and

Zattoni 2016).

Methodology

4.2.1 Criteria of the deliberate sample

As part of understanding the cultural context of a corporation in relation to the individuals of

the dark triad, the method is to pursue a qualitative research approach in term of a case study

design. The research is primarily an exploratory research and therefore used to acquire an