Embed Size (px)

Citation preview

ARTICLE IN PRESS

Journal of Financial Economics 81 (2006) 255–281

0304-405X/$

doi:10.1016/j

$This pap

of the Banco

paper signific

seminar for t

Repullo. Com

and in the E

J. Dermine,

J. Segura for

Department

authors’ own�CorrespoE-mail ad

www.elsevier.com/locate/jfec

Determinants of collateral$

Gabriel Jimeneza, Vicente Salasa,b, Jesus Saurinaa,�

aBanco de Espana, C/Alcala 48, 28014 Madrid, SpainbUniversidad de Zaragoza, Spain

Received 12 December 2003; received in revised form 24 February 2005; accepted 17 June 2005

Available online 25 January 2006

Abstract

We estimate a comprehensive model of the determinants of collateral in loans extended to business

firms. We use a panel data on a sample of bank loans to Spanish firms from 1984 to 2002. Consistent

with theories that view collateral as a solution to adverse selection problems, our results provide

direct evidence of a negative association between collateral and a borrower’s risk. We also present

evidence on previously unexplored determinants of collateral such as credit market competition,

lender type, and the business cycle.

r 2005 Elsevier B.V. All rights reserved.

JEL classification: G21; D43; E32

Keywords: Collateral; Asymmetric information; Relationship banking; Competition; Business cycle

- see front matter r 2005 Elsevier B.V. All rights reserved.

.jfineco.2005.06.003

er is the sole responsibility of its authors and the views presented here do not necessarily reflect those

de Espana. We appreciate the detailed comments made by the referee, which helped us improve the

antly. Moreover, we thank everyone at a Centro de Estudios Monetarios y Financieros (CEMFI)

heir numerous comments and suggestions, in particular, M. Arellano, S. Bentolila, O. Bover, and R.

ments from participants at the Second International Conference on Credit Risk held at Montreal

uropean Finance Association meetings held in Maastrich, in particular, those from E. Altman,

M. Levonian, and K. Roszbach were likewise gratefully received. We also thank A. Almazan and

their very detailed comments on previous drafts, as well as our colleagues at the Financial Stability

at Banco de Espana for their helpful suggestions. Any errors that remain are, however, entirely the

.

nding author. Tel.: +3491 3385080; fax: +34 91 3386104.

dress: [email protected] (J. Saurina).

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281256

1. Introduction

What determines the use of collateral in credit contracts? Drawing from current theories,we examine this question empirically by hypothesizing that the use of collateral is afunction of characteristics of the borrower (credit quality), the lender (specialization), thecredit market (competition), the nature of the borrower–lender relationship (duration), theloan (size), and macroeconomic conditions (business cycle). We test our comprehensivespecification of the determinants of collateral with panel data on financial loans extendedto business firms by Spanish banks from 1984 to 2002. Thus, our test control for borrowerfixed effects and for time-varying factors such as macroeconomic conditions. Thanks to aunique data set, we are able to examine as-of-yet-unexplored determinants of collateral,and we provide a new, sharper test of the relation between collateral use and a borrower’scredit risk.1

Collateral requirements are common terms in loan contracts, together with the interestrate, maturity, and size and possible covenants. Credit market research explains the use ofcollateral as a consequence of adverse selection (Bester, 1985; Chan and Kanatas, 1985;Besanko and Thakor, 1987a, b), and/or moral hazard (Boot et al., 1991), which problemsarise in transactions between borrowers and lenders. The nature of the borrower–lenderrelationshipo, i.e., transactional or relationship lending (Sharpe, 1990; Rajan, 1992), thelevel of competition in the credit market (Besanko and Thakor, 1987a), and the net cost(benefits) of a thorough screening of borrowers (Manove and Padilla, 1999, 2001) can alsoexplain why some loans are secured whereas others are granted without collateral.Moreover, theories that relate the use of collateral to credit market competition and to

other determining factors have not yet been empirically tested. Little is known about howmacroeconomic conditions (the business cycle and the risk-free interest rate) affect the useof collateral in business loans. Finally, the empirical literature has not yet settled importantissues such as whether collateral signals a riskier or a safer loan, or whether relationshipincreases or decreases the requirements for obtaining a loan.The data we use is the Credit Register database of Banco de Espana, which allows us to

group borrowers into three risk classes according to their public record in the Register.Specifically, these three groups comprise those borrowers that have a loan in default at thetime they obtain a new one, those that do not have a loan in default at the time the newloan is granted but that do default in the near future, and all other borrowers. Thisgrouping of borrowers provides the appropriate setup for testing the theories that link theuse of collateral to the credit risk of the borrower and to information conditions in thecredit market. For the group that has a public record of a past default, and thus has lowcredit quality, theory predicts that the likelihood of these borrowers pledging collateral isthe highest among all borrowers (Berger and Udell, 1990; Boot et al., 1991). For thoseborrowers with no record of default when they obtain a loan their credit quality, which canbe high or low, can be observed or it may be private information. In the case of observedcredit quality, the likelihood of collateral will be higher for low-quality borrowers than for

1Note that we focus only on external collateral, i.e., the assets pledged to secure the loan that are external to the

firm, because casual observation of the data suggests that this is the most frequent form of collateral. However, we

do not know the precise nature of the collateral, and we cannot rule out the possibility that, in some cases,

collateral is internal to the firm. While, the use of internal collateral is useful in solving asset-substitution problems

(Smith and Warner, 1979) and Mayers’s under investment problem (Stulz and Johnson, 1985), internal collateral

can only be effective if its value can be monitored (Rajan and Winton, 1995).

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 257

high-quality borrowers (those that are not likely to default) and will be similar to thatobserved for the group with a default record at the time the loan is granted.

However, if credit quality is private information, then the theory of collateral predictsthat borrowers who consider themselves to be of high credit quality will use collateral tosignal their quality and thereby secure a lower interest rate on their loans (Bester, 1985;Chan and Kanatas, 1985; Chan et al., 1986; Besanko and Thakor, 1987a, b). Thus, withinthe group of borrowers of unknown credit quality (those with no loans in default whenthey receive a new loan), the use of collateral will be more likely to be pledged by high-quality borrowers (those that do not default in the next period) than by low-qualityborrowers (those that do default next period). This means that to the extent that collateralserves as a signal of credit quality, the likelihood of collateral use among borrowers thatdefault one year after the loan was granted is expected to be lower than that among theborrowers that do not default.

We find that the likelihood of collateral usage is higher both among borrowers who have aloan in default prior to obtaining a new loan and among borrowers who default after receivingthe loan than it is among borrowers that do not default before or after receipt of the loan. Thisresult confirms that observed risk matters in decisions about the terms of a loan. But we alsofind, however, that among borrowers that default after the current loan is granted, theincremental likelihood of their pledging collateral (relative to the likelihood of collateral useamong borrowers who do not default) increases with the age of the borrower. Moreover,among younger borrowers, the likelihood of pledging collateral is lower within the group ofborrowers that default after the current loan is granted than it is among those that do notdefault. As expected, the lender’s ability to estimate borrower risk is better for older borrowers.The possibility of using collateral to signal credit quality therefore occurs mainly among youngborrowers who have no previous record of financial or commercial activity; this is the groupfor which the asymmetric information effect is likely to be the strongest. Our paper is the firstto present empirical evidence in support of theories that explain collateral as a signal of aborrower’s credit quality, and as a solution to adverse selection problems in credit markets.

The structure of the paper is as follows. Section 2 describes our empirical model of thedeterminants of collateral usage in loans, and presents our main hypotheses, which arebased on previous theoretical models and empirical research. In Section 3 we describe thedata, variables, and method we use to test the main hypotheses. We present the results ofour empirical analysis in Section 4, and Section 5 concludes.

2. Empirical model and main hypotheses

Theories of collateral analyze the information asymmetries that arise between borrowersand lenders, the costs and benefits of relationship lending, the competitive conditions in thecredit market, the inclination of lenders to substitute collateral for a thorough screening ofthe borrower, and the characteristics of the loan. Taking all of this into account, weformulate the following empirical model on the use of collateral:

PrðCollateralijklt ¼ 1Þ ¼ F ða0 þ a1Defaultlt�1 þ a2Defaultltþ1

þ a3Defaultltþ1 x Age as Borrowerlt�1

þ a4Durationjlt�1 þ a5Defaultl;t�1 x Durationjlt�1

þ a6Scopejlt�1 þ a7Number of Lenderslt�1

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281258

þ a8Herfidahlkt þ a9Herfindahlkt x Durationjlt�1

þ a10Specializationjt þ a11Size of Lenderjt

þ a12Bankj þ a13Control Variablesijklt þ ZlÞ, ð1Þ

where i, j, k, l, and t denote the loan, bank, market, firm (borrower), and time period(year), respectively, Zl represent borrower fixed effects, F(.) is the logistic distributionfunction and Collateralijklt is a dummy variable that takes a value of one if the loan hascollateral, and zero otherwise. We define each of the variables in Eq. (1) as we develop ourhypotheses. Note that this model captures the predictions from the theory.We now present our hypotheses:

Hypothesis 1 (H1). The likelihood of using collateral in loans is higher among borrowerswith observed lower credit quality.

Boot et al. (1991) show that when lenders can observe a borrower’s credit quality, low-quality borrowers obtain loans with collateral and high-quality borrowers obtain loanswithout having to pledge collateral. In Eq. (1), the variable DEFAULTlt�1 is a dummy thattakes the value of one when, according to the Credit Register, the borrower who is granteda loan has a loan in default at the beginning of the year, and zero otherwise. We define thevariable in this way because the information that lenders receive from the Credit Registeronly consist of the number of loans the borrower has in default at the time of the inquiry.Thus, we predict a positive coefficient for a1.

Hypothesis 2 (H2). Among borrowers whose credit quality is private information (i.e.,unobserved), the likelihood of using collateral is higher among those of higher creditquality.

We base this hypothesis on the use of collateral as a signal of high credit quality insituations of adverse selection in which borrowers know their credit quality but lenders donot (Bester, 1985; Chan and Kanatas, 1985; Besanko and Thakor, 1987a). To test thisprediction, we require information on the ex post credit quality of the borrowers. Weproxy for this information using the variable DEFAULTlt+1, which takes the value of oneif a borrower did not have a loan in default in t�1 but defaults in t+1, and zero otherwise.This variable allows us to identify those borrowers with no defaults when they obtain aloan but that default after obtaining the loan. If high-quality borrowers use collateral tosignal credit quality in t, then we expect a negative sign for a2, the coefficient onDEFAULTlt+1, since collateral theory predicts that low-quality borrowers are less likely topledge collateral than are high-quality borrowers. The drawback of this test is that we donot know if borrowers that default in t+1 belong to the observed risk group or to theprivate information group. Most likely, there will be a mix of the two situations, with thesign of the coefficient on DEFAULTlt+1 depending on which proportion of casespredominates.To address the above ambiguity, we introduce AGE AS BORROWERlt�1, which we

define as the number of years since the borrower obtained its first registered loan, as of thebeginning of the year in which the loan is made. This measure can identify borrowerssorted by observed risk or private information. Ideally, the age variable should be thenumber of years since the firm was created; however, this information is not available inthe database. Note that AGE AS BORROWERlt�1 coincides with the age of the firm if thefirm gets a loan, and thus is registered in the CIR database, in the year it is created.

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 259

Otherwise, it is a lower bound of the firm’s age. We prefer this variable to, for instance, thenumber of years since the borrower has been with the bank that grants the loan,DURATION, because the borrower could have had previous relationships with otherbanks.

We develop our prediction for AGE AS BORROWERlt�1 as follows. Young borrowersstart with scant information in their commercial and financial records, but as time goes by,information accumulates that can be used by lenders to update their credit qualityassessments (e.g., Diamond, 1991). Since private information is more likely to prevailamong young borrowers, the use of collateral to signal credit quality will be more frequentamong young borrowers than among old borrowers. Thus, as borrowers age the likelihoodof being classified as more or less risky increases.

Accordingly, our hypothesis is that within the group that defaults in t+1, theproportion of borrowers sorted by observed risk in t should increase with the age of theborrower, that is, the coefficient on DEFAULTt+1 is not constant, but rather increasingwith borrower age. Therefore, in model (1), the coefficient on DEFAULTt+1 is written asa2+a3 AGE AS BORROWER. If the data support these predictions, then we expect to finda negative sign for a2, as we discuss above, and a positive sign for a3.

Turning now to our next set of hypotheses, loan maturity is also an indicator of loansmade according to the differences in private information. We expect the informationadvantage of the borrower over the lender to be higher for long-term loans than for short-term loans, since the lender is less forward-looking than the borrower, who will use thelong-term loan to finance a long-term project. In our empirical analysis, we classify loansas short- and long-term loans. We expect that the results that pertain to privateinformation compared to those that pertain to observed risk will be more relevant to long-term loans than to short-term loans.

Hypothesis 3a (H3a). The likelihood of using collateral decreases with the duration ofborrower–lender relationship if the benefits of relationship lending dominate, and increaseswith the duration of the relationship if the cost of the ‘‘hold-up’’ problem associated withrelationship lending dominate.

The above hypothesis summarizes the predictions in studies on relationship lending(Boot, 2000; Berger and Udell, 2002) on the likelihood of collateral. In addition, Boot et al.(1991) observe that collateral can be a solution to problems of moral hazard, and Boot andThakor (1994) show that repeated interactions between borrowers and lenders help tobuild trust and reduce moral hazard. From these predictions the sign of a4, the coefficienton DURATIONjlt�1, which equals the number of years the lender has had a relationshipwith the borrower who receives the loan, should be negative. On the other hand, a longerduration can be associated with a higher likelihood of collateral use, i.e., positive a4, iflonger-term relationships reflect more severe hold-up problems (Greenbaum et al., 1989;Sharpe, 1990; Rajan, 1992; Farinha and Santos, 2002). The empirical results will tell uswhich of the above two situations prevails in the data.

Hypothesis 3b (H3b). On the one hand, if a longer borrower–lender relationshipcontributes to the development of trust, then duration will be negatively related to thelikelihood of collateral usage for all borrowers. On the other hand, if a longer relationshipsimply means that lenders can more accurately sort borrowers by credit quality, then the

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281260

likelihood of using collateral will be independent of duration for borrowers whose creditquality is known at the time of the loan.

An increase in the length of the borrower–lender relationship can decrease the likelihoodof collateral use because it facilitates builds trust (Boot and Thakor, 1994). Alternatively,Berger and Udell (1995) argue that the likelihood of using collateral decreases with theduration of a relationship because lenders collect better information about borrowers andthus can more properly sort them in terms of credit quality.2 Note, however, that bettersorting is relevant only for those borrowers whose credit quality is not known at the timethe loan is granted. Borrowers that have a loan in default at the time they receive a newloan are known to have low credit quality, in which case, under the better sortingexplanation, the likelihood of collateral use will be independent of DURATIONjlt�1 forthese borrowers. Hypothesis 3b determines which of these explanations prevails.In model (1) the coefficient on DURATIONjlt�1 is written as a function of

DEFAULTt�1: a4+a5DEFAULTt�1. Under the Berger and Udell (1995) explanation ofthe advantages of relational lending, the coefficient on DURATION is zero whenDEFAULTt�1 ¼ 1 and the prediction is a4 þ a5 ¼ 0. If longer relationships also build trust(Boot and Thakor, 1994), however, then a4+a5 will be still be negative, as trust is expectedto lower the likelihood of collateral to all borrowers.

Hypothesis 4a (H4a). The likelihood of using collateral decreases with the concentration ofthe credit market.

Besanko and Thakor (1987b) show that Competition lowers the rents of lenders in allthe states of the world, and suggest that the use of collateral is more likely withcompetition than monopoly. Accordingly, we assume that credit market concentrationreduces competition among lenders. Thus, this hypothesis summarizes the effects of creditmarket competition on the use of collateral. If competition is inversely related toconcentration, then coefficient a8 on the Herfindahl index of concentration, HERFIN-

DAHLkt, will be negative.3

Hypothesis 4b (H4b). The reduction in the likelihood of using collateral as a result oflonger borrower–lender relationships will be higher (lower) in more concentrated marketsif the value of information obtained in the relationship decreases (increases) withcompetition in the credit market.

Competition shortens the borrower–lender relationship and reduces the incentives toinvest in information (Chan et al., 1986; Diamond, 1991; Petersen and Rajan, 1995).However, Boot and Thakor (2000) argue that banks respond to greater competition bydeveloping closer relationships with their clients, increasing differentiation and loyalty.If the value of the investment in borrower-specific information decreases with

competition, the same duration will imply more investment and lower likelihood ofcollateral in more concentrated credit markets. However, if competition and the incentivesto differentiation foster this investment, the reverse will be true. The variable

2Diamond (1991) and Petersen and Rajan (1994) present models in which the loan’s interest rates decrease over

time as lenders learn more about the attributes and decisions of the borrowers. Their results can be partially

extended to the case of collateral.3Inderst and Muller (2004) offer an additional explanation of why credit market competition increases the

likelihood of collateral use.

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 261

HERFINDAHLkt x DURATIONjlt�1 accounts for this cross-effect in the empirical model.A negative sign for a9 would support the theories that predict higher investment inrelationship-specific information in less competitive, more concentrated credit markets,since the same duration would result in a greater reduction in the likelihood of collateraluse in highly concentrated credit markets than in less concentrated credit markets.However, a positive sign would support Boot and Thakor’s (2000) prediction that in morecompetitive markets, banks invest more to increase customer loyalty.

Hypothesis 5 (H5). The use of collateral requirements in loans will be more likely if theloan is granted by a lender with a low level of expertise in evaluating loan applications.

Banks with less expertise (in particular, new product or regional market entrants) andfewer resources for evaluating the economic risk of a loan will have a greater incentive touse collateral as a substitute for such evaluation (Manove and Padilla, 1999, 2001).Moreover, may exist differences in lending practices across financial intermediaries, giventheir specialization (Carey et al., 1998) and their ownership structure (Saunders et al., 1990;Gorton and Rosen, 1995).

Our sample banks reflect different degrees of specialization and vary in size and type(commercial compared to savings bank). Larger banks and those that specialize more inbusiness loans should have a comparative advantage in terms of evaluating borrower risk.Thus, we expect that such banks will rely on collateral less than will other banks, implyinga negative sign for the coefficients of the variables SPECIALIZATIONjt, a10, and SIZE

OF THE LENDERjt, a11.Savings banks, traditionally providing loans to households, have only recently expanded

into business loans. Moreover, savings banks are generally more conservative institutions,since they are under the control of their managers and workers who are interested inavoiding possible financial distress and keeping their jobs. The probability of usingcollateral in a loan should, therefore, be higher among savings banks than amongcommercial banks. For this reason, we expect to find a negative coefficient on the variableBANKj, a12, which takes the value of one if the lender is a commercial bank and zerootherwise.

Hypothesis 6 (H6). The amount of collateral in a loan will increase with the risk-freeinterest rate and decrease with the size of the loan.

This hypothesis concerns the amount of collateral required, once the decision to pledgecollateral is already made. Boot et al. (1991) show that under moral hazard, once thelender chooses to ask for collateral, the amount of collateral increases with the real interestrate and decreases with the size of the loan and with a reduction in the dissipative cost ofthe collateral. Allowing the increase in the risk-free real interest rate to translate into ahigher collateral requirement rather a higher interest rate on the loan helps to reduce theagency costs of the transaction. Loans of a larger size reduce the amount of collateralbecause they imply a higher payoff for the lender in the good states of the world. We knowof no previous empirical work, however, that uses loan-level data to explain the amount ofcollateral.

In assigning control variables, little is known about the impact of macroeconomicconditions, such as the business cycle or monetary policy on the decision to pledgecollateral, and we know of no previous empirical work on these potential determinantsof the use of collateral. We introduce gross domestic product growth, GDP GROWTH,

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281262

and the real interest rate, REAL INTEREST RATE, to account for macroeconomicconditions.The duration of the relationship of the borrower with a particular bank,

DURATIONjlt�1, is jointly determined with the number of operations a borrower haswith the bank, SCOPEjlt�1, and with the number of banks with which the borrower isworking, NUMBER OF LENDERSlt�1. Thus, we test the hypothesis on the variableDURATIONjlt�1 controlling for the variables SCOPEjlt�1 and NUMBER OF

LENDERSlt�1. In principle, more loans with the same bank imply more relationshipsand in turn more opportunities for the lender to improve its knowledge of the borrower.As the number of banks a borrower works with increases, the relationship with each bankwill become weaker, thereby reducing the value of any individual bank’s investment ininformation (Thakor, 1996). From these arguments we might expect a negative coefficientfor SCOPEjlt�1 and a positive coefficient for NUMBER OF LENDERSlt�1 if the benefitsof relationship lending are higher than the costs. However, these two variables can berelated to other unobserved borrower characteristics, such as credit quality (Petersen andRajan, 1994) or availability of assets to be used as collateral (Farinha and Santos, 2002).Therefore, the specific predictions on these variables require a deeper analysis than ispossible in this paper.The borrower’s debt, DEBTlt�1, at the time the new loan is granted is a control variable

to account for the size of the borrower. Given a loan’s SIZE, DEBTlt�1 also indicates alender’s relative increase in credit risk. We also include the controls PROVINCEk andGEOGRAPHIC RISKkt�1 in our model, because many borrowers conduct business inlocal markets. Specifically, PROVINCEk is a dummy variable for each of the 50 Spanishprovinces, and GEOGRAPHIC RISKkt�1 is the proportion of bad loans over total loans inthe province at the time the new loan is granted. Differences in technology, production,and marketing conditions across industries might at least partially account for possibledifferences in the risk of projects financed with the new loan, and for differences inborrowers’ economic risks. The dummy variable INDUSTRY controls for these effects foreach of the 11 industries in which firms are grouped.The observable characteristics of the borrowers (business firms) in the sample are limited

to total bank debt, the number of years in the Credit Register, and the record of defaults.We cannot observe variables such as total assets, number of years since the firm wascreated, accounting statements, credit ratings, training and experience of the managementteam, assets that can be pledged as collateral, etc. Since these omitted variables might becorrelated with our model’s explanatory variables of the collateral decision, it is importantto control for unobserved fixed borrowers’ effects in the estimation of model (1). We,therefore, include these fixed effects among the explanatory variables of the model.

3. Database and methodology

Most of the data we use to test the hypotheses above come from the Credit Register ofBanco de Espana (CIR). The CIR database contains detailed monthly information on allloans over h6,000 granted by any credit institution in Spain. Reporting institutions thatwish to study the credit record of any applicant have access to the CIR database, but onlyat an aggregate level and without the possibility to obtain the borrower’s history. For eachloan, the CIR registers information on the instrument type, currency, maturity, collateral,default situation, and amounts drawn and available. The CIR also records characteristics

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 263

of the borrower, namely, whether it is a person or a firm, and the borrower’s industry (forfirms) and province. We are also able to determine whether the loan uses collateral, and ifit does, whether it is fully secured (i.e., 100% collateralized) or partially secured (between50% and 100% collateralized).

For each year between December 1984 and December 2002, we focus on all newfinancial loans4 granted to firms by any Spanish commercial or savings bank (95% marketshare among credit institutions), which result in approximately two million loans. Weconcentrate only on financial loans and exclude other types of debt (such as commercialloans, leases, factoring operations, and off-balance sheet commitments) because we wish toensure homogeneity in the conditions of the loan transaction. Previous research (e.g.Berger and Udell, 1995), finds that loan terms can differ depending on the type ofoperation, even if the transactions are between the same borrowers and lenders. The CIRdatabase does not have a code for each loan. Thus, it is difficult to track a loan over time.Since we wish to know the precise year in which the loan was granted, we limit our finalsample to those loans for which we can estimate the year it was made. We exclude loansthat mature in less than one year because it is impossible to know whether such facilitiesare new or an extension of a loan made in the past.

We estimate Eq. (1) using a logit model with fixed effects. The econometric procedure weuse to introduce borrower fixed effects (Greene, 1993) is based on a conditional likelihoodapproach implemented in a logit model in which it is possible to find a sufficient statisticfor the fixed effect. After conditioning on this statistic, our results have properties similarto those that obtain by differentiating the data in conventional time and cross-sectionaldata panels. Specifically, we write the model as

PrðCollaterallt ¼ 1jxl1; . . . ;xlT ; ZlÞ ¼expðxltbþ ZlÞ

1þ expðxltbþ ZlÞ, (2)

where Zl denotes the borrower-specific effect.The logit model with borrower-specific effects works for samples in which each

individual has at least a collateralized loan and loan without collateral. This constraintreduces the sample of observations in relation to the entire available population of loans.Nevertheless, the number of usable observations is around 550,000 loans.

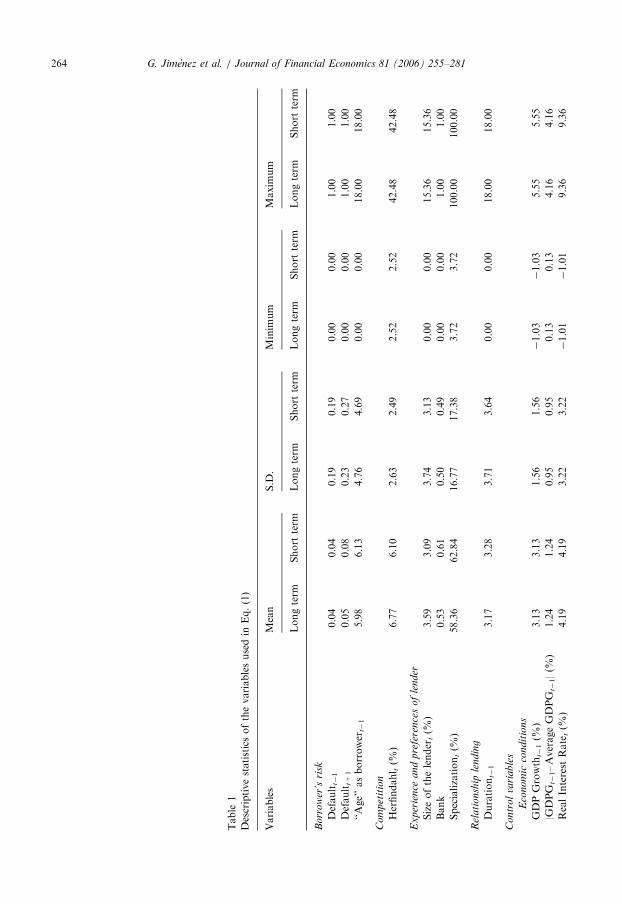

Table 1 presents summary statistics for the dependent and explanatory variables of themodel that we obtain from the sample of usable observations. We present separatestatistics for long-term loans (maturity over three years), which account for almost 80% ofthe sample, and for short-term loans (less than three years). We winsorize the primary dataso that we can substitute the values of the continuous variables above (below) the 99th(1st) percentile with the respective percentile values of the variable. The statisticscorrespond to the winsorized data.

The average size of the loan in the short-term group is 70% of that in the long-termgroup. This result is as might be expected given that short-term loans can be renewed overtime. Commercial banks typically offer a greater proportion of short-term loans then dosavings banks, while the reverse is true for long-term loans. The variables DURATIONjlt�1

and AGE AS BORROWERlt�1 show similar patterns for short- and long-term loans. The

4Financial loans are 60% of the total number of loans in the CIR. We do not know whether the loan is

effectively committed, but commitments are very rare in Spain (i.e., commitments are usually unilaterally

cancelable by the bank).

ARTICLE IN PRESS

Table

1

Descriptivestatisticsofthevariablesusedin

Eq.(1)

Variables

Mean

S.D

.Minim

um

Maxim

um

Longterm

Short

term

Longterm

Short

term

Longterm

Short

term

Longterm

Short

term

Borr

ow

er’s

risk

Default

t�1

0.04

0.04

0.19

0.19

0.00

0.00

1.00

1.00

Default

t+1

0.05

0.08

0.23

0.27

0.00

0.00

1.00

1.00

‘‘Age’’asborrower

t�1

5.98

6.13

4.76

4.69

0.00

0.00

18.00

18.00

Co

mp

etit

ion

Herfindahl t(%

)6.77

6.10

2.63

2.49

2.52

2.52

42.48

42.48

Ex

per

ience

and

pre

fere

nce

sof

lender

Sizeofthelender

t(%

)3.59

3.09

3.74

3.13

0.00

0.00

15.36

15.36

Bank

0.53

0.61

0.50

0.49

0.00

0.00

1.00

1.00

Specialization

t(%

)58.36

62.84

16.77

17.38

3.72

3.72

100.00

100.00

Rel

ati

onsh

iple

ndin

g

Duration

t�1

3.17

3.28

3.71

3.64

0.00

0.00

18.00

18.00

Co

ntr

ol

vari

ab

les

Eco

nom

icco

nd

itio

ns

GDPGrowth

t�1(%

)3.13

3.13

1.56

1.56

�1.03

�1.03

5.55

5.55

|GDPG

t�1–AverageGDPG

t�1|(%

)1.24

1.24

0.95

0.95

0.13

0.13

4.16

4.16

RealInterest

Rate

t(%

)4.19

4.19

3.22

3.22

�1.01

�1.01

9.36

9.36

G. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281264

ARTICLE IN PRESSGeographic

Risk

t�1(%

)4.37

4.46

3.75

3.54

0.48

0.48

28.34

28.34

Bo

rro

wer

’sch

ara

cter

isti

cs

Debt t�1

4.28

4.67

15.52

11.03

0.00

0.00

94.21

49.82

Scope t�1

1.54

1.77

1.61

1.63

0.00

0.00

6.00

6.00

Number

oflenders t�1

4.03

5.23

4.67

5.06

0.00

0.00

23.00

20.00

Lo

an

’sch

ara

cter

isti

cs

Sizeoftheloan

0.46

0.36

1.11

0.73

0.01

0.01

6.67

3.51

Dep

end

ent

vari

ab

le

Collateral

0.51

0.31

0.50

0.46

0.00

0.00

1.00

1.00

%Fullycollateralized

92.45

86.65

Mean,standard

deviation(S.D

.),minim

um,andmaxim

um

values

ofthevariables.Oursample

ofloansconsist

ofloansto

borrowerswithatleast

oneloanwith

collateralandonewithoutcollateralthatweregrantedbySpanishbanksin

theperiod1984to

2002.

Lo

ng

(sh

ort

)te

rmloansare

loanswithmaturity

over

threeyears

(betweenoneandthreeyears).

Def

au

ltt�

1is

adummyvariable

thattakes

thevalueofoneiftheborrower

thatreceives

theloanhasaloanin

defaultandzero

otherwise.

Def

au

ltt+

1isadummyvariablethattakes

thevalueofoneiftheborrower

does

nothavealoanin

defaultatthetimetheloanisgrantedbutdefaultsayear

after.

Ag

ea

sb

orr

ow

ert�

1isthenumber

ofyears

theborrower

hasbeenin

theCreditRegisterpriorto

theyearin

whichwhen

itreceives

theloan.

Her

fin

da

hl tisthe

index

ofcreditmarket

concentrationequalto

thesum

ofbanks’squaredmarket

sharesin

loansmadein

each

oneofthe50Spanishprovincesin

year

t.S

ize

of

the

len

der

tistheratiooftheassetsofthebanksthatgranttheloanover

totalassetsofallbanks.

Ba

nkisadummyvariablethattakes

thevalueofoneifthelender

isa

commercialbankandzero

ifitisasavingsbank.

Sp

ecia

liza

tio

ntistheproportionofloansto

firm

sover

totalloansmadebythelender

inyear

t.D

ura

tio

nt�

1isthe

number

ofyears

oflender—

borrower

relationshipspriorto

when

theloanismade.

GD

Pg

row

tht�

1istherate

ofgrowth

ingross

domesticproduct

inrealterm

sone

yearpriorto

when

theloanismade.|G

DP

gro

wth

t�1–

Ave

rag

eG

DP

gro

wth

t�1|istheabsolute

difference

betweenGDPgrowth

andaveragegrowth.

Rea

lin

tere

stra

tet

isthenominalmoney

market

interestrate

minustheinflationrate

(Consumer

Price

Index)in

year

t.G

eogra

ph

icri

skt�

1istheproportionofbadloansover

totalloans

intheprovince

inwhichtheloanisgrantedthepreviousyear.

Deb

t t�1istotaloutstandingbankdebtoftheborrower

atthetimeoftheloan(inmillionsofEuros).

Nu

mb

ero

fle

nd

ers t�1isthenumber

ofbankstheborrower

hasloanswithpriorto

when

theloanismade.

sco

pe t�1isthenumber

ofloanstheborrower

haswiththe

lender

priorto

when

theloanismade.

Siz

eo

fth

elo

anistheamountoftheloangrantedin

millionsofEuros.

Deb

tandsi

zeo

fth

elo

anare

atconstantpricesof2002.

Co

lla

tera

lisadummyvariablethattakes

thevalueofoneiftheloanhascollateralandzero

otherwise.

Loans

full

yco

llate

rali

zedare

theproportionoftotalloansfor

whichcollateralsecures100%

oftheloan;thedifference

from

100istheproportionofloansthatare

partiallycollateralized.

G. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 265

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281266

proportion of borrowers with a loan in default at the time they obtain a new loan,DEFAULTlt�1, is 4% for both long- and short-term loans. Among those borrowers thatare not in default when they obtain a short-term loan, 5% (8%) default in the followingyear if the last loan is a long-term (short-term) loan. Finally, the proportion of loans withcollateral is 30.5% in short-term loans and 50.8% for long-term loans.5 The differences wefind between the terms and characteristics of loans of different maturity suggest that topreserve homogeneity, we should estimate model (1) separately for each maturity.The model that tests the predictions on the amount of collateral, partial or total, is a

multinomial logit model in which the dependent variable falls under one of threecategories: no collateral, partial collateral (i.e., more than 50% of the loan is secured), andtotal collateral (i.e., 100% secured).6

Because we expect decreasing marginal effects on the impact of each variable in theprobability of collateral use in a particular loan, DEBT, AGE AS BORROWER,DURATION, SCOPE, NUMBER OF LENDERS, and SIZE OF THE LOAN enter intothe models in natural logs.7

4. Empirical results

4.1. The use of collateral

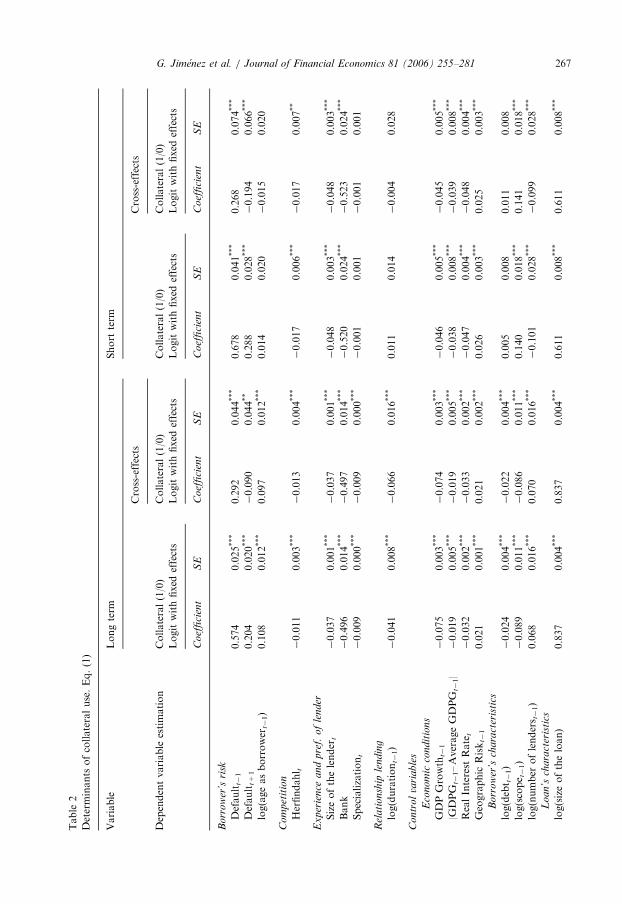

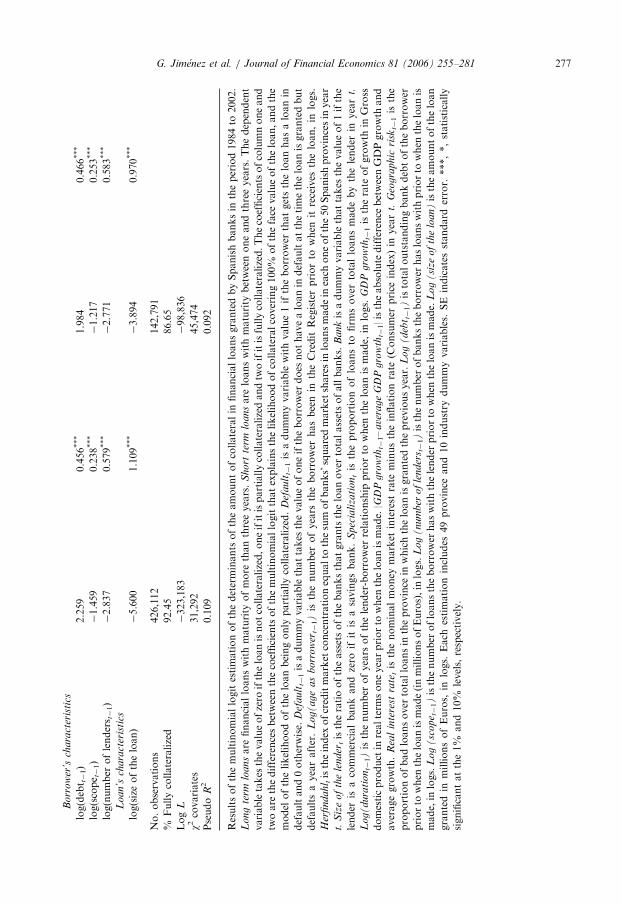

Table 2 shows the fixed effects logit model estimations of model (1) for both long-(columns one and two) and short-term (columns three and four) loans. The null hypothesisof borrowers’ fixed effects in the explanation of the use of collateral cannot be rejected. Inboth cases, the Hausman test of fixed versus random effects rejects the null hypothesis of anon-systematic difference in coefficients with a p-value of zero.The positive and significant coefficient of DEFAULTt�1 in all estimations confirms H1.

Borrowers with lower credit quality are more likely to pledge collateral to obtain a loanthan are other borrowers. Since information on the borrower’s record in the CreditRegister is available to all lenders, it is realistic to assume that the bank that grants the loanin year t knows the borrower’s record. Therefore, all borrowers for whom DEFAULTt�1

takes the value of one reasonably belong to the group with lower credit quality.

5It is interesting to compare data above with the data presented by Berger and Udell (1995) for the U.S., and by

Harhoff and Korting (1998) for Germany, bearing in mind that these two papers deal only with credit line data. In

the U.S. sample, 53% of the loans have collateral while in the German sample this figure is 62%. In the U.S., 78%

of the time borrowers obtain their line of credit from the bank with which they first engaged in their activity (11.4

years of DURATION and 14.1 years of AGE AS BORROWER), while for the German sample the percentage is

70% (12 and 17.5 years, respectively). In our sample AGE AS BORROWER is the time since each borrower

obtains its first loan, and the ratio of loyalty to the lender is 53% (3.2 of DURATION over 6 of AGE AS

BORROWER). Almost 30% of the firms in the German sample had been in financial distress during the past five

years, while the average number of lenders with which they have relationships with is 1.82. The German and U.S.

samples consider only small firms, while we have the population of Spanish firms as well as the whole population

of financial loans.6We note that when one or more of the explanatory variables is endogenous, for example, loan SIZE, the most

appropriate model to use is the probit model. Our use of the multinomial logit model here should be taken as an

approximation.7Except for SIZE OF THE LOAN, we add one to all these variables before we take logs in order to avoid the

variable approaching �N.

ARTICLE IN PRESSTable

2

Determinants

ofcollateraluse.Eq.(1)

Variable

Longterm

Short

term

Cross-effects

Cross-effects

Dependentvariable

estimation

Collateral(1/0)

Collateral(1/0)

Collateral(1/0)

Collateral(1/0)

Logitwithfixed

effects

Logitwithfixed

effects

Logitwithfixed

effects

Logitwithfixed

effects

Co

effi

cien

tS

EC

oef

fici

ent

SE

Co

effi

cien

tS

EC

oef

fici

ent

SE

Borr

ow

er’s

risk

Default

t�1

0.574

0.025***

0.292

0.044***

0.678

0.041***

0.268

0.074***

Default

t+1

0.204

0.020***

�0.090

0.044**

0.288

0.028***

�0.194

0.066***

log(ageasborrower

t�1)

0.108

0.012***

0.097

0.012***

0.014

0.020

�0.015

0.020

Co

mp

etit

ion

Herfindahl t

�0.011

0.003***

�0.013

0.004***

�0.017

0.006***

�0.017

0.007**

Ex

per

ien

cea

nd

pre

f.o

fle

nder

Sizeofthelender

t�0.037

0.001***

�0.037

0.001***

�0.048

0.003***

�0.048

0.003***

Bank

�0.496

0.014***

�0.497

0.014***

�0.520

0.024***

�0.523

0.024***

Specialization

t�0.009

0.000***

�0.009

0.000***

�0.001

0.001

�0.001

0.001

Rel

ati

onsh

iple

ndin

g

log(duration

t�1)

�0.041

0.008***

�0.066

0.016***

0.011

0.014

�0.004

0.028

Co

ntr

ol

vari

ab

les

Eco

nom

icco

nd

itio

ns

GDPGrowth

t�1

�0.075

0.003***

�0.074

0.003***

�0.046

0.005***

�0.045

0.005***

|GDPG

t�1–AverageGDPG

t�1|

�0.019

0.005***

�0.019

0.005***

�0.038

0.008***

�0.039

0.008***

RealInterest

Rate

t�0.032

0.002***

�0.033

0.002***

�0.047

0.004***

�0.048

0.004***

Geographic

Risk

t�1

0.021

0.001***

0.021

0.002***

0.026

0.003***

0.025

0.003***

Bo

rro

wer

’sch

ara

cter

isti

cs

log(debt t�1)

�0.024

0.004***

�0.022

0.004***

0.005

0.008

0.011

0.008

log(scope t�1)

�0.089

0.011***

�0.086

0.011***

0.140

0.018***

0.141

0.018***

log(number

oflenders t�1)

0.068

0.016***

0.070

0.016***

�0.101

0.028***

�0.099

0.028***

Lo

an

’sch

ara

cter

isti

cs

log(sizeoftheloan)

0.837

0.004***

0.837

0.004***

0.611

0.008***

0.611

0.008***

G. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 267

ARTICLE IN PRESSTable

2(c

onti

nu

ed)

Variable

Longterm

Short

term

Cross-effects

Cross-effects

Dependentvariable

estimation

Collateral(1/0)

Collateral(1/0)

Collateral(1/0)

Collateral(1/0)

Logitwithfixed

effects

Logitwithfixed

effects

Logitwithfixed

effects

Logitwithfixed

effects

Co

effi

cien

tS

EC

oef

fici

ent

SE

Co

effi

cien

tS

EC

oef

fici

ent

SE

Cro

ss-e

ffec

ts

Default

t�1*log(duration

t�1)

——

0.208

0.028***

——

0.310

0.047***

Herfindahl t*log(duration

t�1)

——

0.002

0.002

——

0.000

0.004

Default

t+1*log(ageasborrower

t�1)

——

0.185

0.025***

——

0.302

0.038***

No.observations

426,112

426,112

142,791

142,791

%collateralized

50.85

50.85

30.50

30.50

Log

L�141,565

�141,513

�44,865

�44,814

w2covariates

58,146

58,251

10,011

10.111

Pseudo

R2

0.170

0.171

0.100

0.101

Resultsoftheborrowers’fixed

effectslogitestimationofmodel

(1)ondeterminants

ofcollateralin

financialloansgrantedbySpanishbanksin

theperiod1984to

2002.

Lon

gte

rmlo

an

sare

financialloanswithmaturity

over

threeyears

(columnsoneandtw

o).

Sh

ort

term

loa

nsare

loanswithmaturity

betweenoneandthreeyears

(columnsthreeandfour).Thedependentvariable

Co

lla

tera

ltakes

thevalueofoneiftheloanhascollateralandzero

otherwise.Explanatory

variablesin

columnsone

andthree:

Def

au

ltt�

1isadummyvariable

withvalue1iftheborrower

thatgetstheloanhasaloanin

defaultand0otherwise,

Def

au

ltt+1isadummyvariable

that

takes

thevalueofoneiftheborrower

does

nothavealoanin

defaultatthetimetheloanisgrantedbutdefaultsayearafter,

Lo

g(

age

as

bo

rrow

ert�

1)isthenumber

of

years

theborrower

hasbeenin

theCreditRegisterpriorto

when

itreceives

theloan,in

logs,

Her

find

ah

l tistheindex

ofcreditmarket

concentrationequalto

thesum

of

banks’squaredmarket

sharesin

loansmadein

each

oneofthe50Spanishprovincesin

year

t,si

zeo

fth

ele

nder

tistheratiooftheassetsofthebanksthatgrantsthe

loanover

totalassetsofallbanks,

Ba

nkisadummyvariablethattakes

thevalueof1ifthelender

isacommercialbankandzero

ifitisasavingsbank,

Sp

ecia

liza

tio

nt

istheproportionofloansto

firm

sover

totalloansmadebythelender

inyear

t,L

og

(d

ura

tio

nt�

1)isthenumber

ofyears

ofthelender-borrower

relationship

priorto

when

theloanis

made,

inlogs,

GD

Pg

row

tht�

1is

therate

ofgrowth

ingross

domesticproduct

inrealterm

soneyearpriorto

when

theloanis

made,

|GD

P

gro

wth

t�1–

ave

rag

eG

DP

gro

wth

t�1|istheabsolute

difference

betweenGDPgrowth

andaveragegrowth,

rea

lin

tere

stra

tetisthenominalmoney

market

interest

rate

minustheinflationrate

(consumer

price

index)in

year

t,G

eog

rap

hic

risk

t�1istheproportionofbadloansover

totalloansin

theprovince

inwhichtheloanisgranted

thepreviousyear,

Lo

g(

deb

t t�1)is

totaloutstandingbankdebtoftheborrower

priorto

when

theloanis

made(inmillionsofEuros),in

logs,

Lo

g(

nu

mb

ero

f

len

der

s t�1)isthenumber

ofbankstheborrower

hasloanswithpriorto

when

theloanismade,in

logs,

Log

(sc

op

e t�1)isthenumber

ofloanstheborrower

haswith

thelender

priorto

when

theloanismade,

Log

(si

zeo

fth

elo

an

)istheamountoftheloangrantedin

millionsofEuros,in

logs.Columnstw

oandfourpresentcross-

effectsofthevariables

Def

au

ltt+1

an

dL

og

(a

ge

as

bo

rrow

ert�

1),

Def

au

ltt�

1,

an

dL

og

(d

ura

tio

nt�

1)and

Her

fin

da

hl t

an

dlo

g(

du

rati

on

t�1).Each

estimationincludes

49

province

and10industry

dummyvariables.

SEindicatesstandard

error.***,**,statisticallysignificantatthe1%

and5%

levels,respectively.

G. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281268

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 269

Table 2 reports that for the average borrower, DEFAULTt+1 has a positive andsignificant coefficient in columns one and three. The likelihood that borrowers will berequired to pledge collateral is higher for borrowers with a clean record of no defaults atthe time of the new loan (but who later reveal themselves as having low credit quality) thanit is for borrowers who do not default. Lenders also have other sources of informationbeyond the CIR with which they can sort borrowers (i.e., accounting statements, creditratings and so on). Thus, our findings confirm the conclusion reached in previous work(Berger and Udell, 1990, 1995; Jimenez and Saurina, 2004) that observed credit risk is thedominant mechanism for sorting borrowers at the time the loan is granted. However, theex ante and ex post credit risk variables that we use in this paper to distinguish amongborrowers of different credit quality permit a sharper test of the hypothesis than do thevariables used in the previous studies.8

We also find that the estimated coefficient of DEFAULTt+1 is significantly lower thanthat of DEFAULTt�1. One possible explanation for this result is that among borrowersthat have a record of no defaults at the time they receive a new loan, some are sorted underobserved risk and some are sorted under private information. Among the latter group,high-credit-quality borrowers use collateral to signal their high quality and thereby obtaina lower interest rate on the loan. Therefore, in the pool of all borrowers, some on high- andlow-credit-quality borrowers simultaneously pledge collateral. The positive coefficient onDEFAULTt+1 is the net result of the two, pointing out that the proportion of borrowerssorted by observed risk is higher than the proportion of those sorted by privateinformation. Nevertheless, one can also argue that the lower estimated coefficient forDEFAULTt+1 compared with that for DEFAULTt�1 is due to the fact that the informationthat lenders use to sort borrowers in the group with defaults differs from that used to sortborrowers in the group with no defaults; in the first case, there is a direct and objectivemeasure of credit risk, whereas and in the second case, there is not.9

To further explain the observed differences in the estimated coefficients of DEFAULTt�1

and DEFAULTt+1, in Section 2 we postulate that the coefficient on DEFAULTt+1 is anincreasing function of the borrower’s experience, since more experienced borrowers havegreater opportunities to learn about their credit qualities. Table 2, columns two and four,reports a positive sign for the coefficient of the variable DEFAULTt+1 x Log(AGE AS

BORROWER), consistent with our prediction.Moreover, column two of Table 2 shows that for long-term loans, for example, the coeffi-

cient on DEFAULTt+1 with cross-effects, is –0.090+0.185Log(AGE AS BORROWER), as

8Other papers look at the relation between collateral and risk. In some, risk is measured by the risk premium in

the interest rate of the loan (Berger and Udell, 1990; Degryse and Van Cayseele, 2000). However, the risk

premium in the interest rate can be a measure of the risk of the project to be financed with the loan, while the

theory links the use of collateral to the risk of the borrower, not to the risk of the project. Harhoff and Korting

(1998) find a positive association between use of collateral and observed low borrower credit quality, but they do

not consider future defaults.9Borrowers’ fixed effects will also control for the fact that ratings of bonds issued by firms are another source of

information on the quality of the borrowers. However, in Spain, the number of firms that issue public debt is

limited. Moreover, the number of non-financial firms with rated debt is much lower (21 firms had rated debt at the

beginning of 2004). In addition, John et al. (2003) show that the credit ratings of bond issues by U.S. firms are not

sufficient statistics for determining credit risk. If these results apply to Spain and to bank loans, it could mean that

credit ratings will not be sufficient statistics for the risk of the bank loan and the use of collateral will still depend

on other explanatory variables. Similarly, Altman et al. (2005) argue that the loan market is more informational

efficient than the bond market around default dates.

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281270

H2 predicts under the sorting-by-private information explanation of collateral. This resultimplies that for young borrowers, i.e., those with Log(AGE AS BORROWERS) close tozero, the coefficient on DEFAULTt+1 is negative and statistically significant. Theconclusion is the same for short-term loans, where for Log(AGE AS BORROWER) ¼ 0,the coefficient on DEFAULTt+1 is �0.194. Therefore, among young borrowers, thelikelihood of pledging collateral is positively associated with credit quality because thoseborrowers who reveal lower credit quality ex post are less likely to pledge collateral thanare those who do not default. This evidence is the first that we are aware of that isconsistent with the theory that explains collateral as a signalling device in response toadverse selection problems (H2).While relationship lending lowers the likelihood of collateral for long-term loans,

duration does not have a significant effect on short-term loans (H3a). The coefficients onLog(DURATION) are negative and statistically significant in columns one and two ofTable 2, but not significant in columns three and four.The control variables SCOPE and NUMBER of LENDERS also show that the

coefficients change signs based on loan maturity. For long-term loans, the evidence thatboth an increase in the number of relationships and a greater concentration of thoserelationships in a reduced number of banks lower the likelihood of collateral use reinforcesour earlier result that relationship lending yields better loan terms than transactionallending, particularly for long-term loans. However, the opposite is true for short-termloans, for which transactional lending (fewer relationships with each of many banks)results in a lower likelihood of collateral use.An important conclusion that emerges from these results is that we cannot assume that

differences in loan terms across relationship and transactional lending are unaffected by loanmaturity. It is possible that banks specialize along two dimensions, in particular, relationshipversus transactional lending, and short-term versus long-term lending. These results are alsoconsistent with the finding of Berger and Udell (1995) that for credit-line loans, such as ourlong-term loans, relationship lending improves the terms of the loan, while for other loans,as reported by Petersen and Rajan (1994), it does not.10 Thus, examining the determinants ofcollateral separately for short- and long-term loans, appears to be a better approach thansimply using loan maturity as an additional explanatory variable in a pooled model.The evidence for H3b indicates that borrowers with a loan in default at the time they

obtain a new loan do not benefit from longer relationships with the lender. Rather, forthese borrowers, duration increases the likelihood of collateral: among long-term loans(column two), the coefficient of Log(DURATION) for borrowers with DEFAULTt�1 ¼ 1is 0.142 (�0.066+0.208). Thus, for borrowers with known low credit quality, longerrelationships seem to turn into a hold-up situation. This result provides stronger supportfor Berger and Udell’s (1995) hypothesis that duration improves the sorting of borrowersin terms of credit quality than for Boot and Thakor’s (1994) hypothesis that a longerduration implies higher trust and less moral hazard.The negative estimated coefficient on HERFINDAHL is consistent with the prediction

in H4a. If we assume that competition and rivalry are lower in more concentrated creditmarkets, then the results support the hypothesis that competition increases the likelihood

10In short-term loans, reputation and relationship effects are less important than those associated with the

forward commitment to provide future financing that are embodied in a line of credit (Berger and Udell, 1995,

p. 356).

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 271

of collateral use. However, the coefficient of the cross-effect between the duration of theborrower–lender relationship and market concentration is not statistically significant. Wemust, therefore, conclude that credit market concentration does not change the effect thatrelationship duration has on the likelihood of collateral use. This may be because there arecountervailing forces when it comes to the impact of credit market concentration on banks’investments in borrower-specific information, as in H4b.

The data confirm H5, which predicts more use of collateral in loans granted by lenderswith lower expertise in credit operations and higher risk aversion. Larger banks that areprivately owned (commercial) and that specialize more in business loans are less likely torequire collateral in loans than are smaller banks, savings banks, and banks that are moreoriented toward retail banking. This conclusion is true for both long- and short-term loans.Thus, the empirical evidence is consistent with the theories that explain the use of collateralas a substitute for a thorough screening of the borrower’s credit risk (Manove and Padilla,1999, 2001).

Macroeconomic conditions such as the business cycle and monetary policy have aneconomically significant effect on the use of collateral. During downturns, lenders are morelikely to ask for collateral. In fact, since we observe a different impact depending onwhether output growth is above or below its average trend (captured by the variable |GDP

GROWTH—Average GDP GROWTH|), our analysis actually shows that output growthhas an asymmetric effect on the use of collateral: the likelihood of collateral use decreasesmore in upturns (GDP growth is above the trend) than it increases in downturns (GDPgrowth is below the trend). In periods of tighter monetary policy or higher real interestrates, borrowers are less likely to use collateral than they are in periods of loose monetarypolicy.

We know of no theory or any previous evidence on the relation between the use ofcollateral and macroeconomic conditions. A possible explanation of our results could bethat banks take into account the evidence that bad loans are inversely related to GDPgrowth, and that higher interest rates coincide with periods of more restrictive monetarypolicy. If the availability of credit is limited, then banks will prefer high-quality borrowersto low-quality ones in granting credit.

The rest of the control variables indicate that larger borrowers are less likely to pledgecollateral than are smaller ones, especially if the loan granted is a long-term loan. Whenfixed effects are included among of the explanatory variables, the variable DEBT, whichwe use as a proxy for size, has a negative and significant coefficient for long-term loans.Controlling for the size of outstanding debt, the likelihood of collateral increases with thesize of the loan, both for short-term and long-term loans. The coefficient of AGE AS

BORROWER is positive and significant for long-term loans but insignificant for short-term loans. Our empirical evidence differs from that of Berger and Udell (1995), who find anegative effect of borrower age in the likelihood of collateral use. Therefore, improvementsin loan terms, if any, come from the private information obtained by the bank through aclose relationship with the borrower (duration).

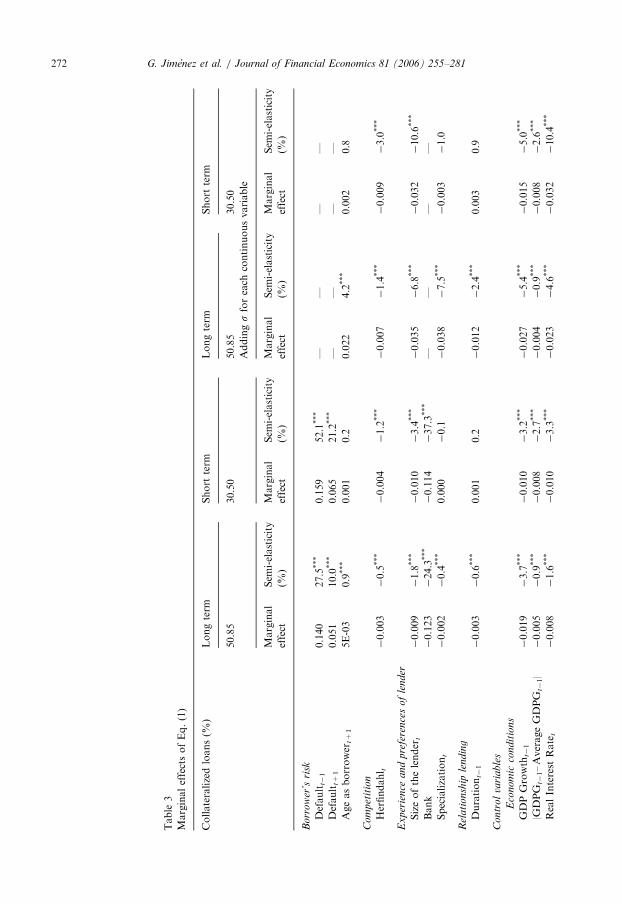

4.2. Marginal effects

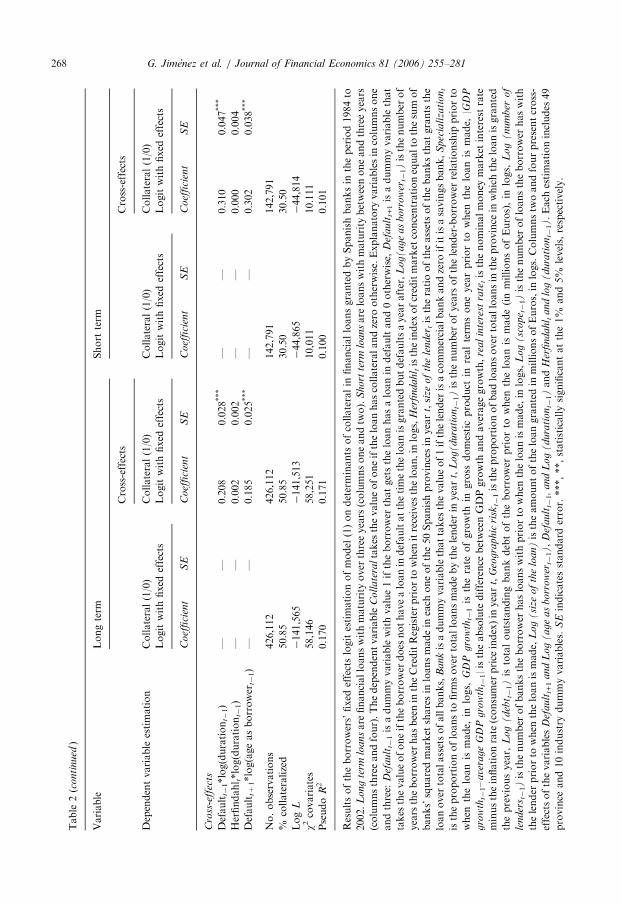

Table 3 shows the marginal effects of changes in the values of the explanatory variableson the probability of collateral use. We obtain our results from the logit estimations ofTable 2. We estimate the mean of the fixed effects so that F ðbxÞ is close to its observed

ARTICLE IN PRESS

Table

3

MarginaleffectsofEq.(1)

Collateralizedloans(%

)Longterm

Short

term

Longterm

Short

term

50.85

30.50

50.85

30.50

Addingsforeach

continuousvariable

Marginal

effect

Sem

i-elasticity

(%)

Marginal

effect

Sem

i-elasticity

(%)

Marginal

effect

Sem

i-elasticity

(%)

Marginal

effect

Sem

i-elasticity

(%)

Borr

ow

er’s

risk

Default

t�1

0.140

27.5

***

0.159

52.1

***

——

——

Default

t+1

0.051

10.0

***

0.065

21.2

***

——

——

Ageasborrower

t+1

5E-03

0.9

***

0.001

0.2

0.022

4.2

***

0.002

0.8

Co

mp

etit

ion

Herfindahl t

�0.003

�0.5

***

�0.004

�1.2

***

�0.007

�1.4

***

�0.009

�3.0

***

Ex

per

ience

and

pre

fere

nce

sof

lender

Sizeofthelender

t�0.009

�1.8

***

�0.010

�3.4

***

�0.035

�6.8

***

�0.032

�10.6

***

Bank

�0.123

�24.3

***

�0.114

�37.3

***

——

——

Specialization

t�0.002

�0.4

***

0.000

�0.1

�0.038

�7.5

***

�0.003

�1.0

Rel

ati

onsh

iple

ndin

g

Duration

t�1

�0.003

�0.6

***

0.001

0.2

�0.012

�2.4

***

0.003

0.9

Co

ntr

ol

vari

ab

les

Eco

nom

icco

nd

itio

ns

GDPGrowth

t�1

�0.019

�3.7

***

�0.010

�3.2

***

�0.027

�5.4

***

�0.015

�5.0

***

|GDPG

t�1–AverageGDPG

t�1|

�0.005

�0.9

***

�0.008

�2.7

***

�0.004

�0.9

***

�0.008

�2.6

***

RealInterest

Rate

t�0.008

�1.6

***

�0.010

�3.3

***

�0.023

�4.6

***

�0.032

�10.4

***

G. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281272

ARTICLE IN PRESSGeographic

Risk

t�1

0.005

1.0

***

0.006

1.8

***

0.020

3.9

***

0.020

6.5

***

Bo

rro

wer

’sch

ara

cter

isti

cs

Debt t�1

�1E-08

0.0

***

0.000

0.0

�0.022

�4.3

***

0.003

0.9

Scope t�1

�0.014

�2.8

***

0.017

5.6

***

�0.023

�4.6

***

0.028

9.1

***

Number

oflenders t�1

0.004

0.8

***

�0.004

�1.4

***

0.020

3.9

***

�0.021

�6.9

***

Lo

an

’sch

ara

cter

isti

cs

Sizeoftheloan

5E-04

0.1

***

4E-04

0.1

***

0.504

99.1

***

0.263

86.2

***

Changein

thelikelihoodofcollateraluse

inresponse

tochanges

intheexplanatory

variablesoftheborrowers’fixed

effectsmodel(1)attheirrespectivesamplemeans.

Thefirstfourcolumnscorrespondto

marginalchanges

inthevalues

ofthevariablesandthelast

fourto

changes

when

addingonestandard

deviationofthe

explanatory

variableto

thesamplemean.Themarginaleffect

istheactualchangein

thelikelihoodvalueandSem

ielasticityindicatesrelativechanges

withrespectto

thelikelihoodofcollateraluse

when

variablesare

valued

attheirsamplemeans.

Lon

gte

rmlo

an

sare

financialloanswithmaturity

over

threeyears

(columnsoneand

three).

Sh

ort

term

loa

nsare

loanswithmaturity

betweenoneandthreeyears

(columnstw

oandfour).

Def

au

ltt�

1isadummyvariablethattakes

thevalueofoneifthe

borrower

thatreceives

theloanhasaloanin

defaultandzero

otherwise.

Def

au

ltt+1isadummyvariablethattakes

thevalueofoneiftheborrower

does

nothavea

loanin

defaultatthetimetheloanisgrantedbutdefaultsayearafter.

Ag

ea

sb

orr

ow

ert�

1isthenumber

ofyears

theborrower

hasbeenin

theCreditRegisterpriorto

theyearin

whichwhen

itreceives

theloan.

Her

fin

da

hl tistheindex

ofcreditmarket

concentrationequalto

thesum

ofbanks’squaredmarket

sharesin

loansmadein

each

oneofthe50Spanishprovincesin

year

t.S

ize

of

the

len

der

tistheratiooftheassetsofthebanksthatgranttheloanover

totalassetsofallbanks.

Ban

kisa

dummyvariablethattakes

thevalueofoneifthelender

isacommercialbankandzero

ifitisasavingsbank.

Spec

iali

zati

on

tistheproportionofloansto

firm

sover

totalloansmadebythelender

inyear

t.D

ura

tio

nt�

1isthenumber

ofyears

oflender—borrower

relationshipspriorto

when

theloanismade.

GD

Pg

row

tht�

1isthe

rate

ofgrowth

ingross

domesticproduct

inrealterm

soneyearpriorto

when

theloanismade.

|GD

Pg

row

tht�

1–

ave

rage

GD

Pg

row

tht�

1|istheabsolute

difference

betweenGDPgrowth

andaveragegrowth.

Rea

lin

tere

stra

tetisthenominalmoney

market

interest

rate

minustheinflationrate

(consumer

price

index)in

year

t.

Geo

gra

phic

risk

t�1istheproportionofbadloansover

totalloansin

theprovince

inwhichtheloanisgrantedthepreviousyear.

Deb

t t�1istotaloutstandingbankdebt

oftheborrower

atthetimeoftheloan(inmillionsofEuros).

Nu

mb

ero

fle

nder

s t�1isthenumber

ofbankstheborrower

hasloanswithpriorto

when

theloanismade.

Sco

pe t�1isthenumber

ofloanstheborrower

haswiththelender

priorto

when

theloanismade.

Siz

eo

fth

elo

anistheamountoftheloangrantedin

millionsof

Euros.Theestimatedprobabilityatsamplemeaniscomputedas

Fðb

xÞ,where

xdenotesthemeansofallthevariablesandbdenotestheestimatedparameters.We

compute

themarginaleffect

asd½Probðy¼

1jx�=d

xk¼

fðb

xÞb

kforallthevariablesexceptforDebt,A

ge

as

bo

rrow

er,D

ura

tio

n,S

cope,N

um

ber

of

len

der

sandS

ize

of

the

loa

n,whichisðfðb

xÞb

kÞ=

xk,to

recover

theeffect

ofthesevariablesin

levels.Forthebinary

variablesitisPrð

coll

ate

ral¼

1jx�;d¼

1Þ�

Prð

coll

ate

ral¼

1jx�;d¼

0Þ,

where

x�denotesthemeansofalltheother

variables.

F(.)denotesthelogisticdistributionfunctionand

f(.)isitsdensity

function.***statisticallysignificantat1%

level.

G. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 273

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281274

value. The magnitude of these effects helps to calibrate the economic significance of theresults in Table 2, which in most cases is rather high.For borrowers who are in default at the time they obtain a new loan, the likelihood of

collateral use for the new long- (short-) term loan is 27.5% (52.1%) higher than forborrowers who have no default at all. Moreover, the increase in the likelihood of collateraluse for a borrower that defaults next period is 10% (21%) for a long- (short) term loan,compared to a borrower with no default at all. Among borrowers whose AGE AS

BORROWER equals one, those in the group that defaults in period t+1 observe a lowerlikelihood of collateral, 4% (14%), compared to borrowers that do not default.If the values of the Herfindahl index are one standard deviation higher than the sample

mean, then the likelihood of using collateral for the loan is 1.4% (3%) lower than the meanvalue for long-term (short term) loans. On the one hand, while a one-standard deviationincrease of the variable DURATION decreases the likelihood of collateral use by 2.4% forlong-term loans, the likelihood of collateral is unchanged if the loan is a short-term loan.On the other hand, a one-standard deviation increase in the NUMBER OF LENDERS

raises the likelihood of collateral use by 3.9% if the new loan is a long-term loan andreduces it by 6.9% if it is a short-term loan. If the loan is a long-term (short-term) loan, thelikelihood that it will use collateral is 24.3% (37.3%) lower if a commercial bank, ratherthan with a savings bank, grants the loan.Macroeconomic conditions affect the likelihood of collateral use in an economically

significant way for all the cases we consider. A one-additional percentage point increase inGDP growth lowers the likelihood of collateral in long-term loans by 3.7 percentage points(pp). If the loan is granted in a year in which GDP grows at a rate above the long-termtrend, then the probability of using collateral falls by an additional 0.9 pp for long-termloans and 2.7 pp for short-term loans. The reduction in the likelihood of collateral use dueto marginal increases in the real interest rate ranges between 1.6% for long-term loans to3.3% for short-term loans.

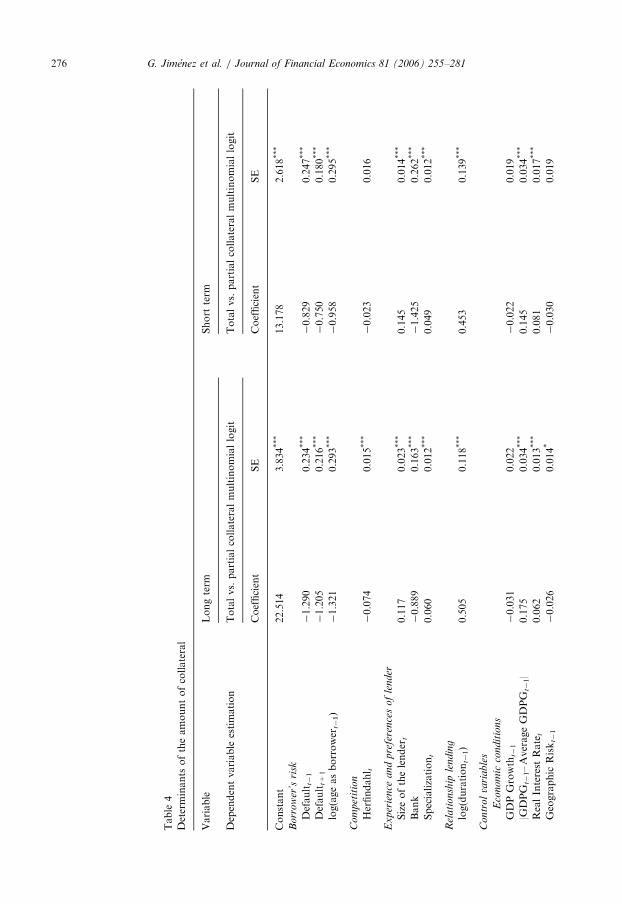

4.3. Amount of collateral

Table 4 presents the results of the multinomial logit model on the determinants of theamount of collateral for the same sample of loans used to estimate the models that explainthe use of collateral. The model has the same explanatory variables as the model of thedeterminants of the use of collateral, but we now limit the theoretical predictions to theREAL INTEREST RATE and the SIZE of the loan. We obtain the results by using a two-stage conditional maximum likelihood estimation. This method accounts for the fact thatSIZE is likely to be endogenous because it is jointly determined with other loan terms suchas the interest rate and the use of collateral.11 Since loan SIZE is one of the variables weuse to test H6, it is important to reduce potential bias in performing the tests.In Table 4, columns one and two show that, for long-term and short-term loans,

respectively, the estimated values, standard errors, and levels of significance for thedifferences between the coefficients of the multinomial logit that explains the likelihood ofcollateral covering 100% of the face value of the loan and the model of the likelihood ofthe loan being only partially covered by the collateral. A positive value indicates that an

11The technical details, of the two-stage estimation procedure are in Rivers and Vuong (1988). Jimenez et al.

(2004) provide a more detailed explanation of the procedure.

ARTICLE IN PRESSG. Jimenez et al. / Journal of Financial Economics 81 (2006) 255–281 275

increase in the corresponding variable increases the likelihood that the bank will requirethe use of full collateral as opposed to partial collateral.

Our results are consistent with the predictions by Boot et al. (1991) that the amount ofcollateral pledged in a particular loan will increase if the loan is granted in a period ofhigher real interest rates, and will decrease with the size of the loan. Thus, the empiricalevidence confirms H6 and explanations of the use of collateral now deal with problems ofmoral hazard. In situations in which the risk-free interest rate is high, the additional riskpremium in the interest rate of the loan will aggravate the moral hazard problem. Usingcollateral instead of charging higher interest rates reduces the moral hazard problem andthereby increases efficiency.

4.4. Robustness of the results

We obtain statistics such as those presented in Table 1 for the whole population of short-term and long-term loans. The total number of loans of each maturity is similar, so thedifference between usable and total loans is especially important for the group of short-term loans. Not surprisingly, then, the main differences between the statistics for thevariables from the sample and from the population correspond with the short-term loans.For example, DEBTlt�1 and SIZE are up to five times larger in the sample of short-termloans than in the population of loans. Moreover, short-term loans with collateral as aproportion of the total number of short-term loans is 8.5%, compared to 30.5% for thesample of usable observations.

To verify that the process with which we select usable sample does not distort the mainconclusions of the study, we perform a robustness exercise by estimating model (1) for theentire population of loans, although in this case we use a different estimation method.Here, we estimate Eq. (1) for the whole population of loans by using a two-step probitmodel to check the robustness of the results.

The two-step probit estimation leaves the main results unchanged, although it producesdifferent signs for coefficients of control variables such as SCOPE, NUMBER OF