Embed Size (px)

Citation preview

1

Published in: Mann, S. (ed.), Sectors Matter - Exploring Mesoeconomics,

Springer, Heidelberg, Dordrecht, London, New York, 2011, 55-102

Economic Growth Through

The Emergence Of New Sectors Andreas Pyka, University of Hohenheim, Economics Institut, , D-70593 Stuttgart, Germany.

Pier Paolo Saviotti, UMR GAEL, Université Pierre Mendès-France, PO Box 47, F-38040

Grenoble, Cedex 9 , France, and CNRS GREDEG, Sophia Antipolis, France.

SEPTEMBER 2010

Abstract:

The basic theme underlying this chapter is the qualitative change taking place during

economic development. Qualitative change is represented by the emergence of new entities,

qualitatively different from those that preceded them. Qualitative change gives rise to changes

in the composition of the system. In turn, these changes in composition amount to something

very similar to structural change. In the model presented in this chapter qualitative change is

created by the emergence of new sectors, each of which produces an output that is

qualitatively different to, and thus distinguishable from, the outputs of all the other sectors.

Each sector produces a differentiated output. Typically such output will be an heterogeneous

multicharacteristics product. The output of each sector is produced by a population of firms,

whose processes of entry and exit are modelled as part of the dynamics of the sector. The

initial stimulus to the creation of the sector comes from an important innovation that creates

an adjustment gap, that is, a potential market that when the innovation is created is empty.

The model has a strong Schumpeterian flavour in that the first entrepreneur entering a market

enjoys a temporary monopoly. This temporary monopoly is eroded by the entry of imitators,

which gradually increases the intensity of competition. When the intensity of competition

becomes sufficiently high there is no more inducement for anyone to enter the population of

firms and there starts being an incentive for incumbent firms to exit the sector. The sector is

saturated. The saturation is reinforced as the demand for what was a new product comes to be

completely satisfied. In this way the adjustment gap initially created by the innovation is

gradually eliminated, thus transforming a niche into a mature market, which becomes one of

the routines of the economic system. The saturation of a sector is thus determined by the

increasing intensity of competition and by the saturation of demand. Furthermore, exit is also

determined by mergers and acquisitions, themselves dependent on returns to adoption. As

soon as a sector becomes saturated there is an increasing inducement for incumbent firms to

exit and to create a new niche, where once more they will have a temporary monopoly. The

same life cycle, constituted by entry, imitation, increasing intensity of competition, saturation

of demand, exit will be repeated all over again for each new sector. At the end of it what was

a highly profitable niche will become a standard, saturated market. In order for new niches to

be created the negative inducements determined by the saturation of a population must be

accompanied by some positive inducements for the creation of a new niche. Search activities

create innovations and determine the differential fitness of the new technology and the

2

expected differentiation of the niche. Financial availability is another factor required for the

creation of firms in a new niche. Different populations of firms thus interact in their evolution.

As one pre-existing population saturate,s it creates inducements for the creation of new

populations. In this sense the creation of new niches becomes the vehicle for variety growth

and for the expansion of the economic system.

1. Introduction

For many countries economic development has created an enormous amount of wealth

increasing the welfare of most members of their populations. In many growth models the

representation of economic development underlying formal modelling exercises assumed that

technical progress would in the course of time increase the productivity of all existing

processes, thus leading to the possibility of a greater output per unit of resources employed in

production. Economic growth would arise because more final goods would thus be available

for each member of the population. Even the most casual observation tells us that this

representation does not correspond to what happened in one important respect. Both the types

of output ad the activities used to produce them are qualitatively different from those that

were previously used in the economy. We can thus say that the composition of the economic

system changed during economic development. Here by composition we mean the list of all

objects (products or services), activities and actors (individual ad institutional) that are

required to describe the economic system at a given time. Furthermore, qualitative change

necessarily entails structural change, although the two phenomena are not identical. Structural

change only results from the emergence of new sectors, from the extinction of old ones, and

from the changing weights of surviving sectors. Qualitative change can occur at lower levels

of aggregation, for example in the internal composition of a sector or even in that of the

technical objects or of the activities within each sector. The two phenomena are, however,

closely related.

The importance of the previous considerations changes drastically depending on whether

qualitative change is only an effect of previous economic development or also a determinant

of subsequent economic development. In the latter case changes in the composition of the

economic system should become one of the important variables in models of economic

growth and development. Our knowledge of the relationship between economic development

and qualitative change is very limited. With our model of economic development by the

creation of new sectors we attempt to shed light on some important aspects of the role played

by qualitative change in economic development, by laying the foundations of a model in

3

which changes in the composition of the economic system are endogenously generated by the

evolution of the system itself and, in turn, affect its future development. To put it in another,

slightly different, form, we can say that economic development is a process in which new

activities emerge, old ones disappear, the weight of all economic activities and their patterns

of interaction change.

Most existing models of growth are macroeconomic models. Thus they do not take the

composition of the economic system into account. This does not mean that it is impossible for

any macroeconomic growth model to derive some of the implications of changing

composition. However, it means that this possibility is limited. For example, in Romer’s

models (1987, 1990) one of the outcomes of R&D activities is to increase the number of

sectors producing capital goods. Obviously, this amounts to a change in the composition of

the economic system. In Aghion and Howitt’s (1998) multisectoral extension of their

endogenous growth model the existence of several sectors producing intermediate outputs and

of their interactions are examined. However, the number of sectors does not change in the

course of time. In general, in these models there is no indication of what the new capital

goods could be or of their potential interactions with the consumer goods sectors. In fact

consumer goods and services are the really missing character from all these models. This is

probably due to the use of production functions that, while admitting many inputs, can

produce only one output. In particular, the implications of these models for the variety of the

economic system are unclear. In Romer’s models we can expect variety to increase, although

we do not know under what circumstances and in what directions. In Aghion and Howitt’s

models variety is likely to remain constant. Thus we can see here that endogenous growth

models, while being an important improvement with respect to the Solow-Swann vintage, still

have difficulties in coping with the dynamics of qualitative change taking place in the

economy. Macroeconomic growth models are useful precisely because they do away with all,

or some of the complexities inherent in the composition of the economic system. The

simplification that they achieve in this way helps these models to achieve in a parsimonious

and elegant way some important results, but limits their ability to deal with the composition of

the economic system. Of course, such limitation is much more serious in the long than in the

medium or short run, since changes in composition affect the macroeconomic level rather

slowly. Thus, the more profound limitation of macroeconomic growth models is likely to be

their ability to analyse long term trends in economic development.

4

Another type of research relevant for design of our model is that on structural change.

Important examples of this research are the work by Salter (1960), by Cornwall (1977), and

more recently by Fagerberg (2000) and by Fagerberg and Verspagen (1999). These works are

mostly empirical, but an important attempt to formulate a theoretical model linking structural

change and economic growth was made by Pasinetti (1981,1993). The work of all these

authors takes structural change into explicit account and they provide an important inspiration

for our work. However, this past work on structural change still leads to a number of

problems, at least some of which we aim at overcoming. First, the definition of structural

change used by the previously quoted authors refers to the emergence of new sectors, to the

disappearance of older ones and to their changing weights in the economic system. Aspects of

qualitative change taking place at a lower level of aggregation, although having impacts at the

sectoral level, are not taken into account. In this chapter the term qualitative change refers to a

wider range of changes in the composition of the economic system. Second, the possibility to

detect structural change and to study its effects depends heavily on the availability of

statistical data about production and above all on the definition of industrial sectors used.

Statistical classifications of production are changed infrequently and in ways that do not

necessarily reflect the real changes taking place in the economy. Thus, as it emerges clearly

from the work of Fagerberg and Verspagen (1999, 2000) the industrial classification that they

have to use in order to compare a large number of countries hides some types of structural

change. Third, these studies on structural change have remained somewhat separate with

respect to the macroeconomic growth models. Fourth, even the most sophisticated model

linking structural change and economic growth, that of Pasinetti, has very limited dynamic

features: it leads us to the conclusion that in the long run the economic system cannot follow a

balanced growth path unless new sectors emerge and ‘absorb’ the resources potentially

displaced by the evolution of older sectors, but it does not tell us anything about the dynamics

of emergence of new sectors or about their relationship to older ones.

Our chapter is introducing into the details of a model of economic development that includes

qualitative change amongst its main determinants. Thus, we hope to contribute to a better

understanding of the role of qualitative change and to bridge the gap between macroeconomic

growth models and structural change studies. In what follows the conceptual nature of the

present model will be explained, followed by the presentation of the more technical aspects of

the model. One section of this chapter introduces to a selection of results of simulation

5

experiments. The final section concludes and gives a brief outlook for future extensions of the

model which are on our research agenda.

2. A model of economic development by the creation of new sectors

Our model of economic development by the creation of new sectors has been developed over

the past seven years and has already undergone a number of modifications (see Saviotti, Pyka,

2004a, 2004b, 2004c, 2008a, 2008b, 2009, 2010). We will first give a brief verbal description

of the model and then introduce the equations.

2.1 A narrative description of the model

In the model, each sector is generated by an important innovation. Such innovation creates a

potential market and gives rise to what we call an adjustment gap. The term adjustment gap is

due to the fact that, as soon as a potential market is created, it is in fact empty: neither the

productive capacity nor the demand for the innovation is present. They are gradually

constructed during the life cycle of the new sector. As the new sector matures, the adjustment

gap is continuously closed: a productive capacity, which in the end matches demand, is

created. When this happens, the sector enters its saturation phase. The productive capacity is

generated by Schumpeterian entrepreneurs establishing new firms initially induced by the

expectation of a temporary monopoly and related extraordinary profits. The success of the

innovation gives rise to a band wagon of imitators. The number of firms in the new sector

gradually rises, but this also raises the intensity of competition in the sector, thus gradually

reducing the inducement to further entry. After the intensity of competition in the new sector

reaches levels comparable to those of established sectors, the new sector is no longer

innovating but becomes part of the circular flow. When a sector achieves maturity in the way

described above, an inducement exists for Schumpeterian entrepreneurs to set up a new niche,

which can eventually give rise to the emergence of a new industry. In other words, the

declining economic potential of maturing sectors induces the creation of newer and more

promising ones. Competition plays a very important role in this process of creation of new

industries. Entrepreneurs are induced to establish new firms by the expectation of a temporary

monopoly, that is, by the absence of competition. However, the new sector could not achieve

its economic potential unless imitative entry took place. As a result, the intensity of

competition rises, thus reducing the inducement to further entry. An additional contribution is

made to the dynamics of our artificial economic system by inter-sector competition. Inter-

6

sector competition arises when two sectors produce comparable services. Inter-sector

competition is an important component of contestable markets (Baumol et al. 1982) and can

keep the overall intensity of competition of the economic system high, even when each sector

achieves very high levels of industrial concentration.

In our model, the variety of the economic system plays an essential role. Economic variety is

approximated by the number of different sectors. By raising variety, the creation of new

sectors provides the mechanism whereby economic development can continue in the long run.

In this way, the economic system can escape the trap generated by the imbalance between

rising productivity and saturating demand (Pasinetti, 1982, 1993; Saviotti, 1996), which

would occur in a system at constant composition. This also affects the macroeconomic

employment situation: In particular, this artificial economic system can keep generating

employment, even when employment creation is falling within each sector (Saviotti, Pyka,

2004b).

In order to illustrate qualitatively the developments generated by our model, figure 1a shows

the development of the number of firms in a certain industry. Within a wide range of

conditions, the number of firms in each sector grows initially, reaches a maximum and then

falls to a fairly low value. Within these conditions, each sector seems to follow a life cycle,

similar to the ones detected by Klepper (1996), Jovanovic and MacDonald (1984), Utterback

and Suarez (1993). However, in our model, this industry life cycle is created by variables very

different from those used by the previous authors in their models which include increasing

returns to R&D, radical innovations and the emergence of dominant designs. In our case, the

cyclical behavior is caused only by the combined dynamics of competition and of market

saturation. We do not wish to say that cyclical behavior cannot arise under the conditions

identified by the previous authors. We simply say that cyclical behavior can arise also from

the interplay of competition and of market saturation. Figure 1b then shows the course of

development of employment in single industries - which first strongly increases, but in the

shake-out period also is reduced considerably – and the trend of the aggregate employment on

the macroeconomic level, which can be positive despite the decrease of sectoral employment.

Figure 1c displays the overall income development in our economic system. Despite the

severe shake-out processes reducing drastically both the number of firms in mature industries

and sectoral employment, figures 1b and 1c illustrate a decisive advantage of our approach of

numerically modelling industry evolution. By aggregating the various figures we can not only

7

observe the sectoral developments but also the macroeconomic figures, thereby detecting

overall beneficial or disadvantageous developments.

-

50

100

150

200

250

300

1 251 501 751

number of f irms

t-

50

100

150

200

250

300

350

1 251 501 751

sectoral employment and linear trend of

aggregate employment

t

figure 1a) number of firms figure 1b) employment

-

10

20

30

40

50

60

1 251 501 751

income development

t

figure 1c) income

2.2. The simulation model

In the following paragraphs, we describe the formal aspects of our model in detail. Two

remarks are necessary to ease the understanding of this formal description: First, to illustrate

the implemented relationships we display figures which document the results of one

numerical experiment we have labelled the standard scenario. In the results section we

introduce further experiments where we modify the various constants. The second remark

concerns these constants, which frequently can be found in our model. Basically they all serve

as weights for the different factors which play a role for economic development. To shorten to

some extent the following description we summarize these constants in a table in the

appendix.

Equation (1) is the central equation. It describes the change in the net number of firms dNit in

each sector i in the course of time. Accordingly Nit is the number of firms in sector i at time t.

The change in the net number of firms is the result of the processes of entry and exit into and

out of the sectors. The term k1FAitAGi

t describes the rate of entry, the two terms -ICit and -

MAit describe processes of exit. The variables determining the rate of entry, FAi

t and AGit, are

the financial availability and the adjustment gap respectively; the variables determining the

8

exit are the intensity of competition ICit and mergers and acquisitions MAi

t. The four entry

and exit terms are graphically displayed in figures 2a-d. Their meanings and how they are

computed is described immediately below. Figure 1a represents graphically the change in the

number of firms in different sectors. As it can be seen, the number of firms rises at first,

reaches a maximum and then falls to a low value. As already mentioned, the number of firms

in subsequent industries indicates the shape of an industry life cycle in our standard scenario.

t

i

t

i

t

i

t

i

t

iMAICAGFAkdN

1 (1)

This specific pattern emerges from the interplay of the four variables on the right hand side of

equation (1). FAit is the term for financial availability, a variable we expect to contribute

positively to industry development. In the standard scenario displayed in figure 2a the

financial availability for previous sectors is endangered with the emergence of a follow-up

industry with high growth rates (see Saviotti and Pyka, 2009).

AGit (figure 2b) is the adjustment gap at time t and describes the potential size of a market.

When a new industry emerges a new adjustment gap is opened up which is positively

influenced by the search activities in an industry and negatively influenced by an increasing

sectoral productivity and saturated demand.

ICit (figure 2c) is the intensity of competition at time t composed of two influences stemming

from intra-industry and from inter-industry competition. The intensity of competition

increases and declines with the number of firms in the respective industry and is influenced

positively by the emergence of subsequent industries later on (see Saviotti and Pyka, 2008a).

Finally, the term MAit (figure 2d) is the number of mergers and acquisitions at time t. During

industry development a consolidation process fed by mergers and acquisitions and failures

shapes the evolution (see Saviotti, Pyka, Krafft, 2007).

-

0.2

0.4

0.6

0.8

1.0

1.2

1 251 501 751 t

financial availability

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1 251 501 751 t

adjustment gaps

9

figure 2a) financial availability figure 2b) adjustment gaps

-

2

4

6

8

10

12

14

1 251 501 751 t

intensity of competition

-

0.1

0.2

0.3

0.4

0.5

0.6

1 251 501 751

mergers & acquisitions

t

figure 2c) intensity of competition figure 2d) mergers and acquisitions

- Financial Availability

Financial availability represents the amount of financial resources which are available for

investment in sector i. It is not just the amount of resources in the economic system. It reflects

also the knowledge required to estimate the economic development potential of new

industries. In fact it is the fraction of the financial resources of the whole economic system

which investors are prepared to invest in sector i. Thus, FAit depends on the expectations of

the market potential of given innovations. We can expect growing financial availability to

accelerate the rate of entry of firms into a sector. The comparison of different constant levels

of financial availability will only tell us that an economic system able to invest more in an

emerging sector will have a higher rate of growth of firms in the sector but it will not give us

a realistic picture of the dynamics of investment in emerging sectors. Thus, it is possible to

assume that financial operators will observe the behaviour of the economic system and spot

the potential of emerging sectors. If they notice that some aspects of an emerging sector, for

example the rate of creation of new firms, grow more rapidly than average for the whole

economic system, they can invest more heavily in the emerging than in the average - and

typically more mature - sector in the expectation to enjoy higher than average (supranormal)

rates of profit. This kind of behaviour is represented by equation 2:

)](1[ 32 j

t

jt

it

idt

dN

dt

dNkkFA (2)

Equation 2 is a form of replicator dynamics and it tells us that the investment in sector i

(FAit) depends on the extent to which the rate of growth of the number of firms in sector i is

above that for the average in the rest of the economic system. However, for a given difference

between the rate of growth of the number of firms in sector i and in the rest of the economic

system the amount of FAit will depend on the two parameters k2 and k2, where k2 is the

10

amount of financial resources available in the whole economic system, and k3 is the optimism

(or over optimism) of financial operators with respect to the development potential of sector i.

A typical development of FAit is displayed in figure 2a.

- Adjustment Gap

The term adjustment gap AGit indicates the expected size of the market created by a pervasive

major innovation. The term gap indicates something to be compensated or filled. In fact, as

the innovation emerges there is neither a demand nor a production capacity for it. Potential

users and consumers do not know about its existence and properties and entrepreneurs have

not yet had the time to invest in new production facilities. As demand grows and production

facilities are built the gap is gradually closed giving rise to a saturated market. The gap may

never be completely closed if the output of the sector keeps changing in a qualitative way. An

example of this change would be today's cars compared to those of Henry Ford's era. In

today's cars there are many new internal structures and functionalities, supplying new

services, which were completely absent in much older cars. The implication of this is that

while a sector can saturate in volume terms it will not necessarily saturate in value terms

(Saviotti, Pyka, Krafft, 2007). Also, we cannot expect the size of the adjustment gap to fall at

all times after the emergence of a new sector. During the life cycle of the sector innovations,

the result of search activities (SEit, see later) have two effects: (i) they increase efficiency,

thus reducing costs and prices, (ii) they increase the services supplied by the product (Yit, see

later) and the degree of product differentiation (ΔYit, see later). As a consequence of both (i)

and (ii) the population of potential adopters of the output of sector i grows. Thus AGit can

even grow in the intermediate phases of the life cycle of the sector. Eventually, even if no

complete saturation takes place, the size of AGit will fall below its maximum. We can then

distinguish in the life cycle of each sector an early and more entrepreneurial period in which

there are high rates of dNit, of profit etc. and a more mature and more managerial period

during production which processes would become relatively more routine like. AGit can be

defined as the difference between maximum demand and instant demand (equation 3). Fig 2b

shows the dynamics of the adjustment gaps of different sectors in the system.

t

i

t

i

t

i DDAG max (3)

- Demand and Prices

11

In our model demand depends on product price pit, on the services Yi

t supplied by the product,

on product diversification ΔYit and the disposable income for purchases in this sector Dispoi

t

relative to the macroeconomic overall income (Incomet) according to equation (4). We can

expect demand to increase as pit (product price) falls and as Yi

t (services supplied by the

product) and ΔYit (product differentiation) rise. Also, pi

t can be expected to fall due to

growing efficiency of production processes and to rise due to growing product quality or to

growing product differentiation. The relative share of income available for sector i

(Dispoit/Incomet) exerts a positive influence as well and is of particular importance when the

new sector emerges. Equation (4) describes the formal relationship for demand in our model.

The constant kipref is introduced in order to investigate the influence of changing demand

preferences concerning the output of a sector.

t

i

t

i

t

i

t

t

ii

pref

t

ip

YY

Income

DispokkD

4 (4)

-

0.2

0.4

0.6

0.8

1.0

1 251 501 751

demand

t

Figure 3: Demand

The development of the sectoral demand in our standard scenario is displayed in figure 3.

Demand first strongly increases due to an increasing production efficiency which leads to

decreasing product prices. An enlargement of the services provided and the product

differentiation increases demand as well. Saturation tendencies and competition from other

sectors finally decreases sectoral demand.

The services Yit supplied by a given product i (equation 5) and the product differentiation ΔYi

t

(equation 6) can be expected to vary in the course of time due the effect of sectoral search

activities SEit. We expect Yi

t and ΔYit to rise according to a logistic equation. Only search

activities can lead to their growth, although this will occur at different rates due to the

effectiveness of search activities in different sectors. This differential effectiveness is

12

described in the model by the parameters k5 and k6 for services, k7 and k8 for product

differentiation.

)](exp[1

10

65

0

SESEkkyY

t

i

t

i

(5)

)]([1

10

87

0

SESEkkExpyY

t

i

t

i

(6)

-

0.2

0.4

0.6

0.8

1.0

1.2

1 251 501 751 1001 1251 1501 1751

product services

t

Figure 4: Product Services

Again for the standard scenario the development of product services Yit is displayed in figure

4. In early periods the potential for improvements of services is large and the service level

increases accelerated. In later periods the possibilities for further improvements are

increasingly exhausted and the respective development slows down and finally stops. The

development of the product differentiation ΔYit looks similar in dependence of the respective

constants.

Prices pit are calculated in equation (7) as unit costs uci

t plus a mark up kMU in equation (8).

Unit costs are determined by labour costs (labourit wi

t (wit:=wages in sector i at time t)),

physical capital costs (Investmentit i (i:=interest rate)), and by the effects of increasing

services and increasing product differentiation. The mark up kMU in the standard scenario is

fixed at 20% of unit costs.

t

iMU

t

i uckpp 0 (7)

t

i

t

i

t

i

t

i

t

i

t

i YkYkiInvestmentwlabourkuc

1211

1

9 exp)(1 (8)

t

i

t

i

t

i

wages

t

i

t

ilabour

PQkwages

11 (9)

t

iwages

t

i wageskwagesk 1100 (10)

13

Sectoral wages wagesit are determined by the industry turnover from the previous period

Qit-1Pi

t-1 and the size of the sectoral workforce labourit (equation 9). Furthermore, the weight

ktiwages is composed of a constant wages0 and a part which leads to higher wages in

consecutive sectors.

-

0.5

1.0

1.5

2.0

1 251 501 751

unit costs

t

5

6

6

7

7

8

1 251 501 751 t

prices

Figure 5a) Unit Costs Figure 5b) prices

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1 251 501 751 t

w ages

Fig 5c) Wages

In figure 5a) the development of unit costs is displayed. Unit costs start to increase first driven

by increasing wages (displayed in figure 5c). The increasing wages are finally

overcompensated by an increased productivity, which leads to falling unit costs again. The

development of the prices (figure 5b) follows unit-costs closely.

- Search Activities

Search activities SEit are an important component in our model. They are a considered to be a

generalized analogue of R&D. Search activities include all the activities which scan the

external environment to look for alternatives to existing routines. Search activities can be

fundamental or sectoral. We can expect search activities to be affected by demand (equation

11). In particular, sectoral search activities rise with the accumulated demand Daccit (equation

14 and figure 6a) for the output of the same sector (equation 12 and figure 6b).

)]exp(1[ 1413

0 t

i

t

i DacckkSESE (11)

14

t

t

i

t

i DDacc (12)

-

100

200

300

400

500

600

1 251 501 751 t

accumulated demand

-

5

10

15

20

1 251 501 751

search activities

t

Figure 6a: Accumulated Demand Figure 6b: Sectoral Search Activities

The maximum demand Dmax,it defines the maximum possible size of the market for sector i.

The above described concept of adjustment gap AGit is defined as the difference between

maximum and instant demand. Since at time zero (creation of the new market) instant demand

Dit is equal to zero Dmax,i

t represents the maximum possible size of the market for i at the time

of the creation of the market. This maximum size is influenced by the technological

opportunities already exploited for this industry TIit which again are a function of search

activities and described in equation (13).

)]([1

10

1615 SESEkkExpTI

t

i

t

i

(13)

The maximum demand Dmax,it the is defined as the ratio between instant demand Di

t and

exploited opportunities TIit (equation 14). Figure 7a displays the exploitation of sectoral

opportunities. Figure 7b shows the development of maximum demand.

t

i

t

it

iTI

DD max (14)

-

0.1

0.2

0.3

0.4

0.5

1 251 501 751

Exploitation of sectoral opportunities

t-

0.5

1.0

1.5

2.0

1 251 501 751 t

maximum demand

Figure 7a: The exploitation of sectoral opportunities Figure 7b: Maximum Demand

- Income and Disposable Income

15

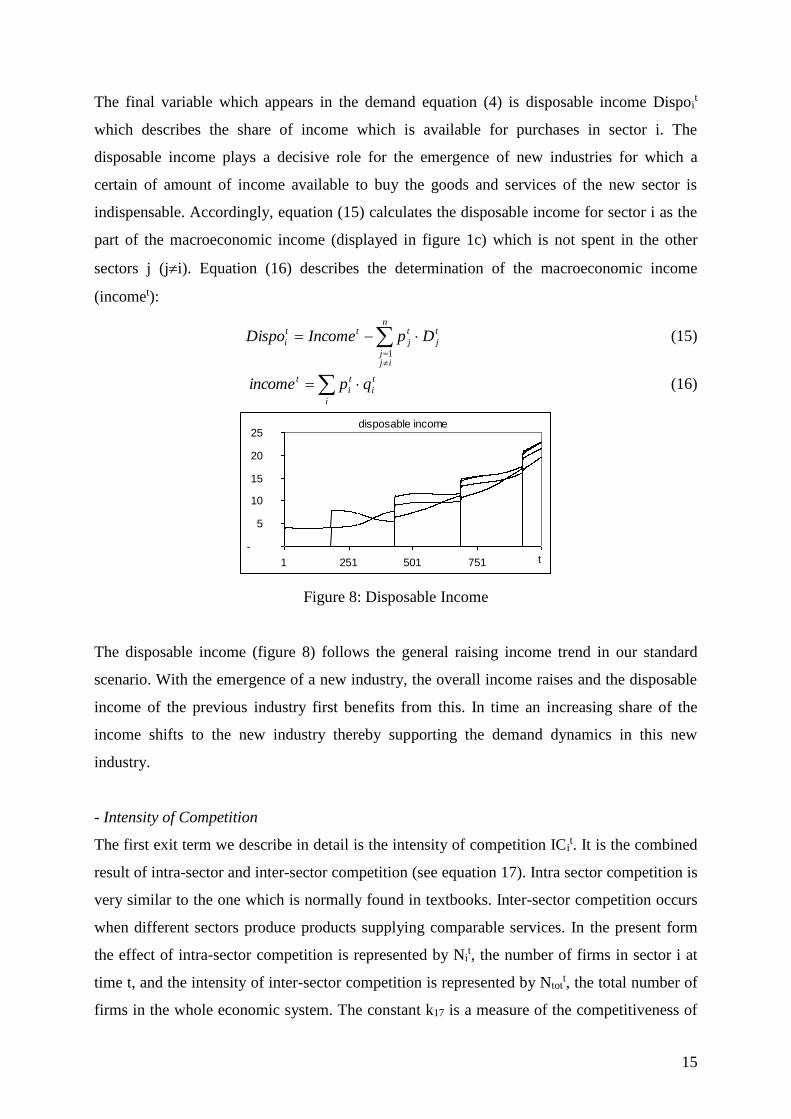

The final variable which appears in the demand equation (4) is disposable income Dispoit

which describes the share of income which is available for purchases in sector i. The

disposable income plays a decisive role for the emergence of new industries for which a

certain of amount of income available to buy the goods and services of the new sector is

indispensable. Accordingly, equation (15) calculates the disposable income for sector i as the

part of the macroeconomic income (displayed in figure 1c) which is not spent in the other

sectors j (ji). Equation (16) describes the determination of the macroeconomic income

(incomet):

n

ijj

t

j

t

j

tt

i DpIncomeDispo1

(15)

i

t

i

t

i

t qpincome (16)

-

5

10

15

20

25

1 251 501 751

disposable income

t

Figure 8: Disposable Income

The disposable income (figure 8) follows the general raising income trend in our standard

scenario. With the emergence of a new industry, the overall income raises and the disposable

income of the previous industry first benefits from this. In time an increasing share of the

income shifts to the new industry thereby supporting the demand dynamics in this new

industry.

- Intensity of Competition

The first exit term we describe in detail is the intensity of competition ICit. It is the combined

result of intra-sector and inter-sector competition (see equation 17). Intra sector competition is

very similar to the one which is normally found in textbooks. Inter-sector competition occurs

when different sectors produce products supplying comparable services. In the present form

the effect of intra-sector competition is represented by Nit, the number of firms in sector i at

time t, and the intensity of inter-sector competition is represented by Ntott, the total number of

firms in the whole economic system. The constant k17 is a measure of the competitiveness of

16

the economic system, as determined, for example, by anti-monopoly laws etc. The constant

RII is the ratio between inter- and intra-sector competition. When k18 = 0 there is only intra-

sector competition and as k18 grows inter-sector competition raises its importance. This is an

approximate form since we can expect the intensity of competition to be affected also by the

extent of product differentiation.

t

total

t

i

t

total

t

it

iNkN

NNkIC

18

1

1

17 (17)

The intensity of competition for the various sectors we observe in our standard simulation is

displayed in figure 2c. We see that due to the strong entry in the entrepreneurial period of an

industry the intensity of competition raises strongly driven by the increasing number of firms

in a sector. It slows down after a peak is reached and is shifted moderately higher when new

sectors enter the scene, which indicates the impact of inter-industry competition.

- Failure, Mergers and Acquisitions

The merger and acquisitions term MAit which is the second exit variable in equation 1

describes the failure and consolidation process during the shake-out period of an industry life

cycle. In figure 2d we see that MAit first strongly increases in young industries indicating a

high rate of failure in the entrepreneurial period. It slows down again with the coming up of a

dominant design and the establishment of the industry. Formally, equation (18) describes

MAit in dependence of the marginal costs MCi

t and the search activities SEit as well as instant

demand Dit. Marginal costs MCi

t so far are simply a constant although easily other

relationships are conceivable.

t

i

t

i

t

it

i

t

iDSE

MCNkMA

1

19 (18)

0MCMCti ; 10 constMC (19)

- Production

On the supply side the sectoral output Qit is determined by the sectoral search activities SEi

t,

the physical capital stock CSphysicalit and the level of human capital HCi

t as described in

equation (20):

)]exp(1[)1( 24232120

0 t

i

t

i

t

i

t

ci

t

i HCkCSphysicalkSEkkQQ (20)

17

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1 251 501 751 t

output

-6

-4

-2

-

2

4

6

1 251 501 751

excess demand

t

Figure 8a: Output Figure 8b: Excess Demand

-0.6

-0.4

-0.2

-

0.2

0.4

0.6

1 251 501 751t

alpha

Figure 8c: adjustment parameter

To adjust the supply side with the demand side of our sectoral economic system we calculate

the excess demand EXDit in each period (equation 21) as the difference between demand and

output. The excess demand displayed in figure 8b then is used to determine an adjustment

variable it. This adjustment variable (figure 8c) is limited to an upper and lower value (0.5 in

the standard scenario) which does not allow for extreme reactions. This value is accumulated

in equation (23) to the production adjustment variable tci used in the output equation (20).

t

i

t

i

t

it

iD

QDEXD

(21)

2)EXD( t

i

t

i (22)

t

t

i

t

ci (23)

- Investment and Basic Research

Besides the search activities SEit which are responsible for increasing production efficiency,

the production Qit is also determined by the physical capital stock CSphysicali

t and the level

of human capital HCit which follow the investment decisions in our economic system. The

overall periodical volume of investment Total_Investmentt (equation 24) is a fraction (ms :=

marginal savings rate) of the macroeconomic income (incomet) displayed in figure 1c. The

investment is distributed on the different sectors following the relative size of the sectors

share_sectorit (equation 25).

18

tt IncomemsInvestmentTotal _ (24)

ms:= const = 0.25 (marginal saving rate)

t

t

i

t

it

iIncome

Qptorshare

sec_ (25)

The physical capital stock is then the accumulated and depreciated outcome of the sectoral

investment as described in equation (26) and displayed in figure 9.

-

50

100

150

200

250

300

350

400

1 251 501 751

physical capital stocks

t

Figure 9: Physical Capital Stocks

tt

i

t

i

t

i InvestmentTotaltorsharephysicalshareCSphysicalCSphysical _sec__)1( 1 (26)

Besides the physical capital stock, also human capital HCit matters for production. The level

of human capital is determined by the investment in human capital which determines the

capital stock of investment in human capital (CSed,it) in equation (27) and together with the

quantitative size of the labour force (labourit) determines the level of human capital HCi

t in

equation (28) and displayed in figure 10.

t

ied

t

i CSkh 22 (27)

t

i

t

i

t

i hlabourHC (28)

1

1

25

t

i

t

it

iQ

Nklabour (29)

i

t

i

t labouremployment (30)

-

20

40

60

80

100

120

1 251 501 751

Level of sectoral Human Capital

t

Figure 10: Level of sectoral human capital

19

The sectoral labour force is an important figure for the observation of macroeconomic trends

in our economic system. As we can aggregate the sectoral employment figures to a

macroeconomic employment figure (see figure 1b) we can not only make propositions on the

sectoral level but also on the aggregate level. The sectoral labour force labourit is determined

by the number of firms in the previous period Nit-1 and the sectoral output of the previous

period Qit-1 (equation 29). The overall employment variable is calculated in equation (30).

Besides sectoral research in our economic system fundamental research activities SEFt focus

on the exploration of new technological opportunities which might lay the foundation for new

industries. Investment in fundamental research activities depend on the share of investment in

fundamental research shareRD and the overall investment Total_Investmentt. Equation (31)

describes the calculation of fundamental research activities:

t

RD

t InvestmentTotalshareSEF _ (31)

- The Emergence of New Industries

One of the most distinctive features of our economic system is the endogenously variable

number of sectors. The creation of a new sector is induced by the previous dynamics of the

economic system. For a new industry i to emerge a few conditions need to be fulfilled. First,

sector i-1 has to become saturated; this is indicated by an adjustment gap of the sector i-1

which starts to close (AGt-1i-1 > AGt

i-1). A closing adjustment gap is indicating declining

opportunities for growth, and profit-oriented entrepreneurs start searching for new

opportunities. With a closing adjustment gap in industry i-1 we start a stepwise increasing

counter variable (counterit) which simply counts the periods of declining opportunities in

sector i-1. Each period then an entry threshold is calculated which decreases with increasing

accumulated fundamental research activities (equation 32):

)( 2726

tt

i SEFkkholdEntryThres (32)

Always when the condition counterit > EntryThresholdi

t is fulfilled, the new industry i starts to

work and a new industry life cycle is set up.

20

-

10

20

30

40

1 251 501 751

entry threshold (bold) and counter variable

t

Figure11: Entry threshold and counter variable

In figure 11 the development of the sectoral entry threshold is displayed. In periods with

increasing fundamental research activities the threshold decreases. Figure 11 also displays the

counter variable which starts to increase when the adjustment gap of a previous industry starts

to decline.

Figure 12: Structure of the model

Figure 12 summarizes the complex interdependent structure of our model. It has to be

mentioned for this graphical representation of the model that circular connections are to be

disbanded. In the simulation model this is done by a sequential structure for the various

calculations; so for example the various investment decisions in one period, which are

determined by the income in this period, start to exert their influences only one period later.

Nit dNi

t

AGit

FAit

MAit

Dmax,it

Dit

Dispoit

Yit,

Yit, pi

t

SEit

ucit

labourit

investmentit

incomeit

SEFit

Qit

ICit

21

3. Simulation Experiments

In this section we give an overview on the various experiments we have performed so far.

Before going into detail a few remarks concerning the numerical experiments are necessary.

Usually, for experiments one or several parameters are varied and the results are compared

with a standard scenario. Obviously, the model has to be tested for stability and robustness.

This has been done in several papers (Saviotti, Pyka, 2004b and Saviotti, Pyka 2008a) and

also new methodologies for robustness checks have been developed. The model is supposed

to produce qualitative stable results for the experiments which in some circumstances might

none the less mean that the corridor of possible values of single figures can be broad. As we

have not used any stochastic formulation in the model we can dispense Monte-Carlo

simulations.

The following seven experiments were chosen to illustrate the broad applicability of our

model to the analysis of a wide set of questions which deal with structural change, economic

development and growth. The first three experiments taken from Saviotti and Pyka (2004a)

deal with very general aspects of the model (variation of technological opportunities, variation

of learning rates and variation of production efficiencies) and allow to gain a better

understanding on the basic dynamics generated by our model. Experiment 4 (Saviotti and

Pyka, 2004c) then tackles already a macro-economic question and analyzes the relationship of

sectoral development and macroeconomic employment figures. Experiment 5 highlights the

important relationship between variety and economic development we allows us to confirm in

Saviotti and Pyka (2004c) the decisive role of a heterogeneous industrial structure for growth

and development which is inaccessible in traditional models of economic growth. In a similar

vein experiment 6 performed in Saviotti and Pyka (2008a) shed light on the inter-sectoral

coordination on the macroeconomic level, i.e. the critical question of the timing concerning

the emergence of new sectors. The final experiment 7 (Saviotti and Pyka, 2009) is used to

demonstrate one of the decisive advantages of our numerical model of economic development

by the emergence of new industry, namely the investigation of co-evolutionary processes

which introduce a high degree of complexity. In particular the relationship between the real

sphere of technology development and the monetary sphere of financial availability is

analyzed and it is shown that due to the co-evolutionary dynamics, there is scope for chaotic

developments.

22

3.1 Experiment 1: Varying technological opportunity

The constant k13, which appears in equation (11) for search activities SEit, measures the extent

of technological opportunity of the technology that created a new sector. In the standard

scenario k13 had the same value for the different populations. In this experiment we varied the

values of k13 for different populations. We explored the situation in which the technological

opportunity of each subsequent population is higher than that of the pre-existing one.

Although there is no guarantee that such a condition is going to apply systematically to all

new emerging sectors, it is also not an implausible one in particular cases. In the past it was

considered that agriculture had an intrinsically lower potential for productivity improvement

than manufacturing. Electronics and information based sectors seem to manifest a higher rate

of productivity growth than historically displayed by mechanical sectors. With these

considerations we do not want to prove that the pattern of increasing technological

opportunity by subsequent populations of firms is of general applicability, but simply that

there are a number of cases in which this could happen. We are exploring a scenario in which

technological opportunity increases for each subsequent population. In the experiment we

used two sets of values, corresponding to experiments 1a and experiment 1b respectively

(Table 1).

Table 1

Values of the constant k13 used in experiments 1a and 1b,

and different from those of the standard scenario.

Experiment 1a Experiment 1b

k131= 40 k13

1= 40

k132= 50 k13

2= 60

k133= 60 k13

3= 80

These changes (Figure 13) lead to an earlier start of the life cycle of populations 2 and 3, to a

higher maximum number of firms at the peak of the life cycle, to an increase in the steady

state level of demand of each population with respect to the pre-existing ones (Figure 14) and

to an increase of the maximum level of demand of each population with respect to the pre-

existing ones (Figure15). These effects are qualitatively the same, but greater in experiment

1b), where the increase in technological opportunity is even greater.

23

0

5

10

15

20

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

number of f irms in a population (standard scenario)

0

5

10

15

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

number of f irms in a population (experiment 1a)

0

5

10

15

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

number of f irms in a population (experiment 1b)

Figure 13: Influence of technological opportunity on the number of firms.

0

5

10

15

20

25

30

35

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

demand (standard scenario)

0

10

20

30

40

50

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

demand (experiment 1a)

0

10

20

30

40

50

60

70

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

demand (experiment 1b)

Figure 14: Influence of technological opportunity on demand

24

0

0,05

0,1

0,15

0,2

0,25

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

intensity of competition (standard scenario)

0

0,05

0,1

0,15

0,2

0,25

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

intensity of competition (experiment 1a)

0

0,05

0,1

0,15

0,2

0,25

0,3

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

intensity of competition (experiment 1b)

Figure 15: Influence of technological opportunity on the intensity of competition

Summarising, we could say that the effect of an increase in technological opportunity of each

new sector with respect to pre-existing ones, is an acceleration of the process of economic

development, determined by a faster emergence of new sectors, and an increase in the scope

of economic development, as shown by the increase in the number of firms that each sector

can support and by the higher levels of demand eventually achieved in each sector.

3.2 Experiment 2: Varying the rate of learning

In this experiment we varied the value of the constant k14 for different populations with

respect to the standard scenario. K12 takes a higher value for each subsequent population, that

is k141 k14

2 . k143. The values used are indicated in Table 2. Given the meaning of k14, this

experiment is equivalent to increase firms’ rate of learning. Three versions of the experiment

are performed.

25

Table 2: Values of k14 used in experiment 2 and different

from those of the standard scenario.

Experiment 2a

Experiment 2b

Experiment 2c

k141= 0.005 k14

1= 0.005 k141= 0.005

k142= 0.01 k14

2= 0.015 k142= 0.025

k143= 0.015 k14

3= 0.025 k143= 0.05

The consequence of increasing firms’ rate of learning is to accelerate the emergence of

populations 2 and 3 with respect to the standard scenario. This has an equivalent effect of the

number of firms and on demand. Entry in population 2 takes place earlier when the rate of

learning for population 2 increases relative to that of population 1. The same type of change

takes place for population 3, whose emergence is also accelerated by an increase of its rate of

learning relative to that of population 2 (Figure 16). Remembering that in our model a

population corresponds to an industrial sector, we can see that a faster rate of learning can

lead to an earlier emergence of a sector. Contrary to what happened in experiment 1, in this

case only the time path of the number of firms seems to be affected, not its value. The

maximum number of firms in each of the three populations remains approximately equal to

that of the standard scenario, but it begins to increase earlier for populations 2 and 3.

26

Figure 16: Influence of the rate of learning on the number of firms

The behaviour of sectoral demand is affected in a similar way (figure 17). The demand for

each sector output begins to rise more rapidly when we increase the rate of learning, up to the

point where the demand for the output of sector 2 can overtake that of sector 1. Long run

demand for the output of a sector does not seem to be affected by a change in learning rate.

This leads us to expect that the aggregate number of firms and the aggregate demand will

grow faster the faster the rate of learning. However, in our model a faster rate of learning does

not bring joy for everyone. While the system may display a faster growth the number of firms

in population 1 begins to fall sooner, due to the inter-sector competition provided by the

increased number of firms in populations 2 and 3. If the development of the system can be

described by means of the life cycles of different sectors, these life cycles follow a time path

that is determined both by the intrinsic features of each sector and by its interactions with

other sectors in the economy. We can observe that in the most extreme case considered here

(experiment 2c), when the rates of learning of populations 2 and 3 are the highest with respect

to population 1, the number of firms and the sectoral demand of population 2 very soon

overtakes those of populations 1 and 3.

0

5

10

15

20

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

number of firms in a population (standard scenario)

0

5

10

15

20

1 163 325 487 649 811 973 1135 1297 1459

populat ion 1 populat ion 2 populat ion 3

number of f irms in a population (experiment 2a)

0

5

10

15

20

1 163 325 487 649 811 973 1135 1297 1459

populat ion 1 populat ion 2 populat ion 3

number of f irms in a population (experiment 2c)

0

5

10

15

20

1 163 325 487 649 811 973 1135 1297 1459

populat ion 1 populat ion 2 populat ion 3

number of f irms in a population (experiment 2b)

27

0

5

10

15

20

25

30

35

1 251 501 751 1001 1251

populat ion 1 populat ion 2 populat ion 3

demand (standard scenario)

0

5

10

15

20

25

30

35

1 163 325 487 649 811 973 1135 1297 1459

population 1 population 2 population 3

demand (experiment 2a)

Figure 17: Influence of the rate of learning on demand

If we compare the results of experiments 1 and 2, we can see that the general effect of an

increase in technological opportunity (Experiment 1) is both, to accelerate the creation of new

sectors and to increase their scope, that is, to increase the maximum number of firms in each

sector, demand and maximum demand. On the other hand, an increase in the rate of learning

of one sector relative to the others only influences the time path of the emergence of new

sectors and not their size, as measured either by the number of firms or by demand. Thus

technological opportunity is seen as having a greater expansive effect on the development of

the whole system than an increase in the rate of learning. However, an increase in the rate of

learning can also lead to an overall faster growth for the whole system, but this growth is

obtained more by greater efficiency than by an expansion of the markets of the various

sectors. In both cases the general improvement of the growth potential of the economic

system leads to a collective improvement, but some agents in the system may suffer. Thus an

emergence of new sectors may mean faster growth, but it also leads to an earlier and faster

emergence of competition for pre-existing (traditional) sectors.

All the analysis so far has been based on individual if interacting populations of firms. The

model can also help us to understand the consequences of sectoral dynamics for aggregate

growth. The total number of firms and aggregate demand for the whole economy are

represented in figure 18.

0

5

10

15

20

25

30

35

1 163 325 487 649 811 973 1135 1297 1459

populat ion 1 populat ion 2 populat ion 3

demand (experiment 2b)

0

5

10

15

20

25

30

35

1 163 325 487 649 811 973 1135 1297 1459

populat ion 1 populat ion 2 populat ion 3

demand (experiment 2c)

28

figure 18: Aggregate curves with the results of experiments 1 and 2. Fig 18a shows the

influence of technological opportunity and of the rate of learning on demand; figure 18b

shows the influence of technological opportunity and of the rate of learning on the number of

firms in each sector

Here we can see that aggregate demand is stimulated more by an increase in technological

opportunity than by an increase in the rate of learning. The total number of firms grows more

rapidly if the technological opportunity or the rate of learning of successive populations are

increased with respect to the standard scenario. However, in this case we can see that if the

economy were not to generate any more new sectors after sector 3, the number of firms would

converge irrespective of the technological opportunity or of the rate of learning. We have to

bear in mind that the behaviour of the system after the ‘maturity’ of sector 3 is artificial in the

sense that we expect new sectors to emerge. The experiment is valuable nevertheless because

it tells us that if the emergence of new sectors were to slow down, for example due to the

influence of particular economic policies, the overall number of firms in the economy would

fall. Increasing intensity of competition, failures, mergers and acquisitions would tend to

reduce continuously the number of surviving firms. The total number of firms can only

increase or at least remain constant if new sectors are continuously created. Conversely from

these results we can expect that in absence of new sectors the system will converge on a set of

0

20

40

60

80

100

120

140

1 251 501 751 1001 1251

standard scenario experiment 1b experiment 2b

fig. 18a) aggregate demand

0

5

10

15

20

25

30

35

1 251 501 751 1001 1251

standard scenario experiment 1b experiment 2b

fig. 18b) total number of firms

29

monopolies, their number being equal to that of the surviving sectors. The same cannot be

said about aggregate demand. Here the higher growth path that is established by an increase

of either technological opportunity or of the rate of learning persists beyond the maturity of

sector 3. By combining these two results we can expect that the output per firm will

continuously increase after the maturity of sector 3.

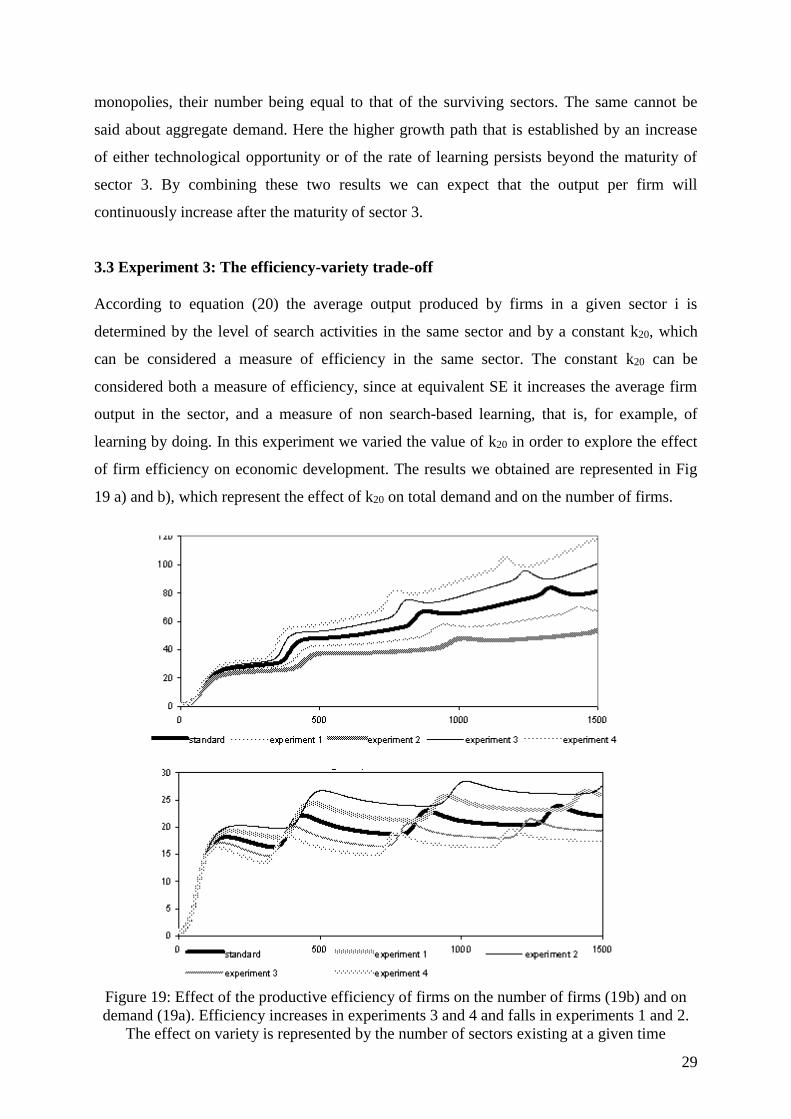

3.3 Experiment 3: The efficiency-variety trade-off

According to equation (20) the average output produced by firms in a given sector i is

determined by the level of search activities in the same sector and by a constant k20, which

can be considered a measure of efficiency in the same sector. The constant k20 can be

considered both a measure of efficiency, since at equivalent SE it increases the average firm

output in the sector, and a measure of non search-based learning, that is, for example, of

learning by doing. In this experiment we varied the value of k20 in order to explore the effect

of firm efficiency on economic development. The results we obtained are represented in Fig

19 a) and b), which represent the effect of k20 on total demand and on the number of firms.

Figure 19: Effect of the productive efficiency of firms on the number of firms (19b) and on

demand (19a). Efficiency increases in experiments 3 and 4 and falls in experiments 1 and 2.

The effect on variety is represented by the number of sectors existing at a given time

30

The results of this experiment are as follows:

Rate of creation of new sectors: The higher the value of k20 and thus the higher the efficiency

of a sector i, the faster the rate of creation of subsequent sectors. If we were to call the time at

which each sector first appears ti,0, then ti,0 would be inversely proportional to k20. Thus the

effect of generally increasing firms productive efficiency in all the sectors of the economic

system would be to accelerate the 'tempo' of economic development. This behaviour can be

explained by means of the inducement that the saturation of a given sector provides for the

creation of subsequent sectors. In turn, this inducement is determined by increasing intensity

of competition and by the saturation of demand. On the whole, a higher efficiency in sector i

leads to a faster saturation of the same sector, thus triggering the creation of the next one

(i+1).

Total demand: The total demand for each sector, and thus for the whole economic system,

increases with increasing k20. This is due to two reasons: first, since each sector emerges

earlier, at any subsequent time the number of sectors in the economic system is greater for a

greater value of k20. Second, the steady state level of demand achieved within each sector

increases with k20. Thus total demand at any time t will be greater because there are more

sectors in the economic system and because each sector has a higher steady state demand.

The number of firms in each sector: The maximum number of firms achieved in each sector at

the peak of the life cycle falls with increasing k20. The total number of firms in the economic

system (Figure 19a) increases more slowly when the average efficiency of each sector is

higher. A faster rise in output, corresponding to a higher intensity of competition, leads to

more exit and to more mergers and acquisitions. Thus the maximum number of firms reached

in the life cycle of each sector falls with the increasing efficiency of the same sector. Thus the

steady state rate of growth in the total number of firms (Figure 19a) falls with increasing

efficiency. In our calculations so far we varied by the same extent the efficiency of all sectors.

Of course, this does not need to be the case in a real economic system. In fact we expect

efficiency and its rate of growth to vary differentially amongst sectors, thus leading to

structural change. This possibility will be explored in subsequent experiments.

The results described above provide a considerable if not definitive confirmation for the

hypothesis about the complementarity between variety growth and efficiency growth

31

(Saviotti, 1996). A greater efficiency allows the more rapid creation of new sectors, and leads

to a greater net number of sectors in the economic system at a given time, that is to a higher

variety.

These results have some interesting implications for economic development. First, if we

consider the general development of the world system without focusing on any particular

country, we can see that the rate of growth of the economic system increases with the

increasing efficiency of each sector. We have to bear in mind at this point that the calculations

that we performed so far attribute the same value of k18 to all the sectors. Thus the

development we have analysed is a proportional form of development, in which all sectors

progress in the same way. Within this framework the saturation of any given existing sector

accelerates the rate of creation of subsequent ones. This type of development and structural

change takes place because new sectors are continuously (in the long run) added to the

economic system. Thus the composition of the system changes and this change in

composition drives its rate of growth. A clear relationship exists in our artificial economic

system between structural change and changes in the composition of the system on the one

hand, and the rate of growth of the system on the other hand. However, as pointed out before,

this type of structural change is not the only possible one. As pointed out above, a different

efficiency of each sector would add another component to the process of structural change by

making some sectors with high values of k20 grow more rapidly than others. This second

component of structural change has not yet been analysed in our experiments.

3.4 Experiment 4: Sectoral Employment and Productivity

Sectoral and total employment calculated for the standard scenario is shown in figure 20. The

dynamics of sectoral employment follows closely that of firm creation, with the rate of

employment growth being particularly high in the early phases of the life of a new sector and

then declining gradually. In figure 20 an aggregate representation has been superimposed on

the sectoral curves by adding up the contributions to employment of the different sectors at

each time. This aggregate representation is particularly useful if we are more interested in the

impact of variables such as productive efficiency, technological opportunity, rate of learning

etc. on the aggregate properties of the system than in the internal mechanisms of each sector.

What is immediately clear is that employment creation within each sector tends to decline and

that overall employment can keep growing only due to the emergence of new sectors. Thus,

the process of qualitative and structural change is a determinant of employment growth. This

32

conclusion is reinforced by figure 21, which displays the output shares of different sectors. As

the shares of old sectors declines that of emergent ones rises first and then starts declining as

the once new sectors move towards maturity. An interesting implication following from figure

20 is that a relatively stable macroeconomic growth pattern is produced by a much more

turbulent micro-economic evolution of individual sectors. To the extent that the patterns of

sectoral evolution described here are common, the achievement of a stable macroeconomic

growth pattern can only be obtained by creating new sectors that is by changing the

composition of the economic system. In this sense the flexibility required of the economic

system is the ability to create new sectors, or its creativity.

Figure 20. Evolution of sectoral and total employment in the standard scenario

Figure 21. Evolution of the sectoral output shares with the emergence of new sectors.

We can also notice (Figure 22) that productive efficiency and employment change in opposite

directions during the development of each sector: productivity rises as employment falls.

0

10

20

30

1 251 501 751 1001 1251

sectoral employment total employment

L

t

sectoral & total employment (linear trend)

0%

25%

50%

75%

100%

time 500 1000

sector 1 sector 2 sector 3 sector 4

33

0 250 500 750 1000 1250

productivity sectoral employment

# of

w orker

s

produc-

tivity

productivity and employment development in a sector

Figure 22. Productivity and employment development in a sector.

3.5 Experiment 5: Variety

Going back to our hypotheses about variety and efficiency, we find a further confirmation of

our hypothesis on the complementarity of increasing efficiency and increasing variety for

economic development. Not only an adequate succession of new sectors can compensate for

the growing inability of older ones to provide employment but faster entry of new sectors

leads to a higher rate of growth of variety and to a higher rate of growth of employment.

Starting from the sectoral shares displayed in figure 21, we calculated the varieties of each

sector and the aggregate variety of the economic system by means of the informational

entropy function. As we can see in figure 23, the variety of the economic system generally

increases during economic development as a consequence of the creation of new sectors.

However, there are short periods during which variety remains approximately constant or

falls. These periods correspond to the conjunction of the decline of mature sectors and of the

growth of emerging ones. As it was previously pointed out, the birth of a new sector is

triggered by the saturation of a previous one. Such a condition, amounting to an almost

perfect inter-temporal coordination, is not necessarily present in real economic systems. It is

possible for a new sector to emerge either before or after the complete saturation of a pre-

existing one. In the former case we expect both employment and variety to grow at a faster

pace than in our results, in the latter we expect employment and variety growth to slow down.

The latter case would be an example of poor inter-temporal coordination in which the new

sectors are not 'ready' when required. In order to display a greater number of sectors in the

calculations performed to obtain this figure we accelerated the process of development with

34

respect to that of the standard scenario by increasing the rate of learning k14 (see experiment

2).

Figure 23: Change in aggregate variety during the development of the economic system. A

higher rate of learning than in the standard scenario has been used to display a greater number

of sectors.

Figure 24 shows the relationship between employment and variety. There is a general trend

towards increasing employment as variety grows, but employment may fall during short

periods, presumably when the rate of variety growth is lower. In fact, the periods of negative

growth of employment in figure 24 correspond to the periods when variety is either growing

very slowly or falling in figure 23. Thus, this figure seems to confirm the generally positive

relationship between the variety of the economic system and the level of employment it can

sustain.

Figure 24: The relationship between employment and variety.

In order to further test the relationship between variety and employment creation we

calculated dL/dt as a function of variety. Different values of variety were obtained by varying

technological opportunity, the rate of learning and productive efficiency. The rate of creation

of new sectors, and thus the rate of variety growth, is accelerated by increasing each of these

variables, but by different mechanisms. Increasing the rate of learning accelerates the

15

25

0 0,2 0,4 0,6 0,8 1 1,2 1,4 1,6 1,8 2 2,2

relationship betw een variety and employment (k5 = 0.025)

employment

variety

0,00

0,40

0,80

1,20

1,60

2,00

2,40

0 500 1000 1500

variety

time

35

emergence of new sectors but leaves almost unchanged the maximum demand of each sector.

Increasing technological opportunity accelerates the rate of creation of new sectors and the

maximum demand in each sector. Increasing productive efficiency accelerates the rate of

creation of new sectors but reduces the number of firms that can supply even an increasing

demand. We can expect variety growth obtained by these different mechanisms to have

different effects on employment creation. If we remember that in this model variety depends

on the number of distinguishable sectors in the economic system, we can understand that a

higher level of demand or a lower number of firms can lead to different employment levels at

equivalent variety. Figures 25 and 26 show the effect of variety on the rate of employment

creation and figures 27 and 28 the effect of variety growth on the rate of employment

creation. Both higher levels of variety and higher rates of variety growth have a generally

positive effect on the rate of employment creation, except for the case in which variety is

increased by raising productive efficiency. In this case the positive effect of variety due to the

increasing number of economic activities corresponding to the sectors is more than

compensated by the rise in productive efficiency. As a result of these experiments our

hypothesis N° 1 may need to be slightly modified. Variety growth is likely to be a necessary

requirement for the continuation of long term economic development, and in most of the

situations we explored it contributes positively to employment creation, but it is not a

sufficient condition under all circumstances. It is still possible for productive efficiency to

increase fast enough to compensate the positive effect of variety growth.

Figure 25: Effect of variety on employment creation. The changes in variety are here obtained

by changing the rate of learning.

0,005

0,01

0,1 0,2 0,3 0,4 0,5 0,6 0,7

variety (av.)

dL/dt

36

Figure 26: Effect of variety on the rate of on employment creation. The changes in variety are

here obtained by changing k20, the rate constant for learning by doing.

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008

0.009

0.01

0.0006 0.001 0.0014 0.0018

dL/dt

dH/dt

increasing k14 from 0.005 to 0.04 (step-size: 0.005)

Figure 27: The effect of variety growth on employment creation. Variety is changed by

changing k14, the rate of learning.

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0.016

0.018

0.02

0.0009 0.001 0.0011 0.0012 0.0013 0.0014 0.0015 0.0016 0.0017

dL/dt

dH/dt

increasing k13 from 25 to 250 (step-size: 25)