Embed Size (px)

Citation preview

Financial Management in Not-for-Profit Businesses

30-1

30

Consider the following organizations: thousands of municipal utilities ranging fromLos Angeles Power & Light and the New York Power Authority to tiny rural electric au-thority (REA) cooperatives; all private colleges and universities; about 85 percent of allU.S. hospitals, nursing homes, and other health care facilities; and even tourist attrac-tions such as the Baltimore and Tampa aquariums. These are not-for-profit businesses,defined as corporations that charge a fee for their services and are expected to gen-erate enough revenues to cover costs, but that have neither outstanding stock norstockholders.

These tens of thousands of not-for-profit firms employ millions of people andprovide vital services, so it is important that they be operated efficiently. To maintainefficiency, the not-for-profits require financial management skills similar to those ofinvestor-owned firms, but with an important difference: the not-for-profits do not havestockholders, hence their goal is not shareholder wealth maximization. As we discussin the chapter, this difference in goals between profit and not-for-profit businessesleads to some interesting contrasts in the financial management of the two types oforganizations.

*CH30_Web_Brigham_859011 10/17/01 2:59 PM Page 30-1

For-Profit (Investor-Owned) versus Not-for-Profit Businesses

When the average person thinks of a business, he or she thinks of an investor-owned,or for-profit, firm. The IBMs and General Motors of this world are investor-ownedfirms. Investors become owners of such companies by buying the firms’ commonstock, either when the company first sells its shares to the public, in an initial publicoffering (IPO); when it issues additional shares, in the primary market; or in the sec-ondary market.

Investor-owned firms have three key characteristics: (1) The owners (stockholders)are well-defined, and they exercise control by voting for the firm’s board of directors.(2) The firm’s residual earnings belong to its stockholders, so management is respon-sible to this single, well-defined group of people for the firm’s profitability. (3) Thefirm is subject to taxation at the federal, state, and local levels. However, if an organi-zation meets a set of stringent requirements, it can qualify as a tax-exempt, or not-for-profit, corporation.1 Tax-exempt status is granted to corporations that fit thedefinition of a charitable organization and hence qualify under Internal Revenue Ser-vice (IRS) Tax Code Section 501(c)(3). Thus, such corporations are also known as501(c)(3) corporations.2

The Tax Code defines a charitable organization as any corporation, communitychest, fund, or foundation that is organized and operated exclusively for religious,charitable, scientific, public safety, literary, or educational purposes. Because thepromotion of health is commonly considered a charitable activity, a corporation thatprovides health care services, provided it meets other requirements, can qualify fortax-exempt status. In addition to being organized for a charitable purpose, a not-for-profit corporation must be administered so that (1) it operates exclusively for the pub-lic, rather than private, interest; (2) none of the profits are used for private inurement;(3) no political activity is conducted; and (4) if liquidation occurs, the assets will con-tinue to be used for a charitable purpose.3

For example, hospital corporations that qualify for tax-exempt status exhibit thefollowing characteristics: (1) Control rests in a board of trustees composed mostly ofcommunity leaders who have no direct economic interest in the organization. (2) Theorganization maintains an open medical staff, with privileges available to all qualifiedphysicians. (3) If the hospital leases office space to physicians, such space can be leasedby any member of the medical staff. (4) The hospital operates an emergency room ac-cessible to the general public. (5) The hospital is engaged in medical research and ed-ucation. (6) The hospital undertakes various programs to improve the health of thecommunity.

Conversely, any of the following activities may disqualify a hospital from tax-exempt status: (1) The hospital is controlled by members of the medical staff. (2) The

30-2 CHAPTER 30 Financial Management in Not-for-Profit Businesses

1In the past, tax-exempt corporations were commonly called nonprofit corporations, but today the term not-for-profit corporation is more common. For more information on financial management in not-for-profithealth care corporations, see Louis C. Gapenski, Understanding Health Care Financial Management: Text,Cases, and Models (Ann Arbor, MI: AUPHA Press/Health Administration Press, 1996).2For additional information on obtaining and maintaining tax-exempt status, see the summer 1988 issue ofTopics in Health Care Financing, titled “Tax Management for Exempt Providers.”3Private inurement means personal benefit from the profits (net income) of the corporation. Since individu-als cannot benefit from not-for-profit corporations’ profits, such organizations cannot pay dividends. Note,however, that prohibition of private inurement does not prevent parties to not-for-profit corporations, suchas managers, from benefiting through salaries, perquisites, and the like. For example, in 1992 it was dis-closed that the national chairman of the United Way received an annual salary plus perquisites thatexceeded $400,000 in value. He was forced to resign in part because this level of compensation was consid-ered too high for an employee of a not-for-profit charity.

*CH30_Web_Brigham_859011 10/17/01 2:59 PM Page 30-2

hospital restricts staff privileges to controlling physicians. (3) The hospital leasesoffice space to some physicians at less than fair market value. (4) The hospital limitsthe use of its facilities. (5) The hospital has contractual agreements that provide directeconomic benefit to controlling physicians. (6) The hospital provides only a negligibleamount of charity care.

Not-for-profit corporations differ significantly from investor-owned corporations.Because not-for-profit businesses have no shareholders, no group of individuals hasownership rights to the firm’s residual earnings. Similarly, no outside group exercisescontrol of the firm; rather, control is exercised by a board of trustees that is not con-strained by outside oversight. As we noted earlier, not-for-profit corporations are gen-erally exempt from taxation, including both property and income taxes, and they havethe right to issue tax-exempt debt. Finally, individual contributions to not-for-profitorganizations can be deducted from taxable income by the donor, so not-for-profitbusinesses have access to tax-advantaged contributed capital.

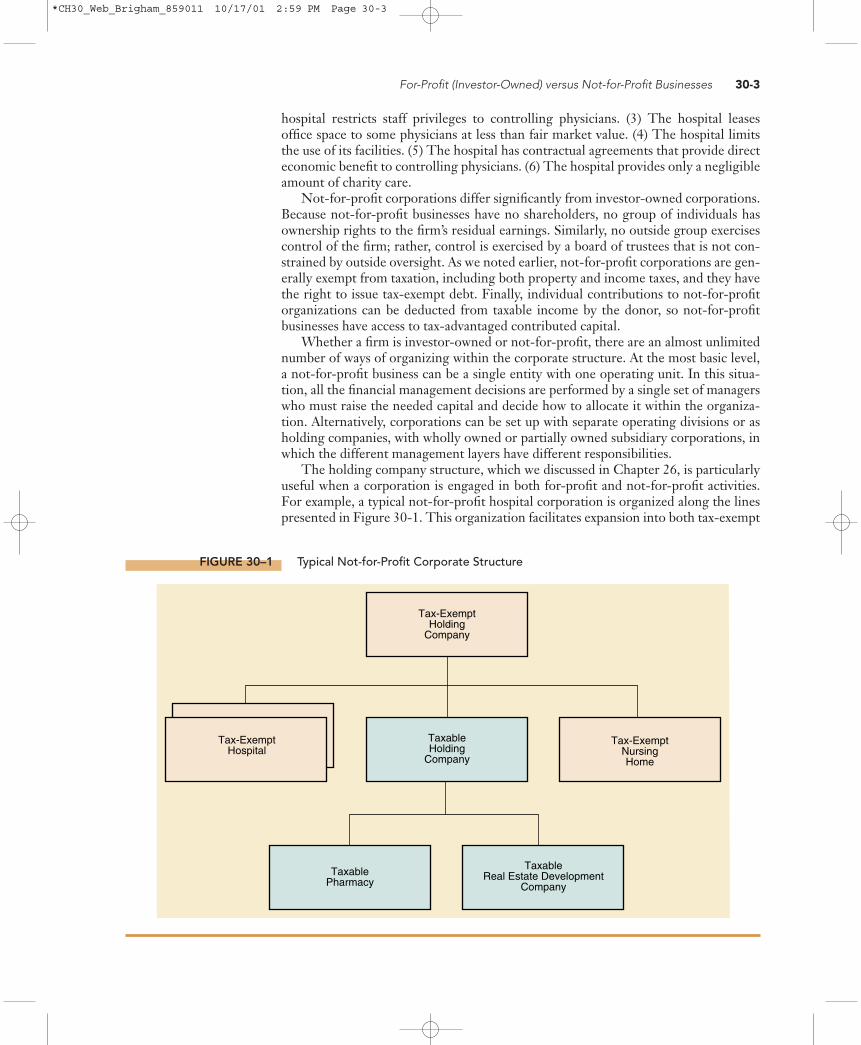

Whether a firm is investor-owned or not-for-profit, there are an almost unlimitednumber of ways of organizing within the corporate structure. At the most basic level,a not-for-profit business can be a single entity with one operating unit. In this situa-tion, all the financial management decisions are performed by a single set of managerswho must raise the needed capital and decide how to allocate it within the organiza-tion. Alternatively, corporations can be set up with separate operating divisions or asholding companies, with wholly owned or partially owned subsidiary corporations, inwhich the different management layers have different responsibilities.

The holding company structure, which we discussed in Chapter 26, is particularlyuseful when a corporation is engaged in both for-profit and not-for-profit activities.For example, a typical not-for-profit hospital corporation is organized along the linespresented in Figure 30-1. This organization facilitates expansion into both tax-exempt

For-Profit (Investor-Owned) versus Not-for-Profit Businesses 30-3

Tax-ExemptHolding

Company

Tax-ExemptHospital

TaxableHolding

Company

Tax-ExemptNursingHome

TaxablePharmacy

TaxableReal Estate Development

Company

FIGURE 30–1 Typical Not-for-Profit Corporate Structure

*CH30_Web_Brigham_859011 10/17/01 2:59 PM Page 30-3

and taxable activities well beyond patient care. However, the tax-exempt holding com-pany must ensure that all transactions between taxable and tax-exempt subsidiaries areconducted at arm’s length; if business is not transacted in this way, the tax-exemptstatus of the parent holding company and its not-for-profit subsidiaries could bechallenged.

The inherent differences between investor-owned and not-for-profit organiza-tions have profound implications for many elements of financial management, includ-ing defining the goals of the firm and making financing and capital budgeting deci-sions. The remainder of this chapter will be devoted to these issues.

Define the following terms:

(1) Investor-owned firm

(2) Not-for-profit business

(3) 501(c)(3) corporation

(4) Private inurement

(5) Board of trustees

What are some major differences between investor-owned and not-for-profitbusinesses?

Goals of the Firm

From a financial management perspective, the primary goal of investor-owned firms isshareholder wealth maximization, which translates to stock price maximization. Be-cause not-for-profit businesses do not have stockholders, shareholder wealth maxi-mization cannot be the goal of such organizations. Rather, not-for-profit businessesserve and are served by a number of stakeholders, which include all parties that havean interest (financial or otherwise) in the organization. For example, a not-for-profithospital’s stakeholders include its board of trustees, managers, employees, physicians,creditors, suppliers, patients, and even potential patients (i.e., the entire community).While managers of investor-owned companies can focus primarily on the interests ofone class of stakeholders—the stockholders—managers of not-for-profit businessesface a different situation. They must try to please all the stakeholders because there isno single, well-defined group that exercises control.4

Typically, the goal of a not-for-profit business is stated in terms of some mission.For example, the mission statement of Ridgeway Community Hospital, a 300-bed,not-for-profit hospital, is as follows:

Ridgeway Community Hospital, along with its medical staff, is a recognized, innovativehealth care leader dedicated to meeting the needs of the community. We strive to be thebest comprehensive health care provider possible through our commitment to excel-lence.

Although this mission statement provides Ridgeway’s managers and employees with aframework for developing specific goals and objectives, it does not provide much

30-4 CHAPTER 30 Financial Management in Not-for-Profit Businesses

4Many people argue that managers of not-for-profit firms do not have to please anyone at all, because theytend to dominate the board of trustees that is supposed to exercise oversight. However, we would argue thatmanagers of not-for-profit firms must please all the firms’ stakeholders to a greater or lesser extent because allare necessary to the well-being of the business. Similarly, managers of investor-owned firms should not treatany of their other stakeholders unfairly, because such actions are ultimately detrimental to stockholders.

*CH30_Web_Brigham_859011 10/17/01 2:59 PM Page 30-4

insight about the goals of financial management. For Ridgeway to accomplish its mis-sion, the hospital’s managers have identified five specific financial management goals:

1. The hospital must maintain its financial viability.2. The hospital must generate sufficient profits to permit it to expand along with the

community and to replace plant and equipment as it wears out or becomes obsolete.5

3. The hospital must generate sufficient profits to invest in new medical technologiesand services as they become available.

4. Although the hospital has an aggressive philanthropy program in place, it does notwant to be overly dependent on this program, or on government grants, to fund itsoperations.

5. The hospital will strive to provide services to the community as inexpensively aspossible, given the above financial requirements.

In effect, Ridgeway’s managers are saying that to achieve the “commitment to ex-cellence” mentioned in its mission statement, the hospital must remain financiallystrong and reasonably profitable. Financially weak organizations cannot continue toaccomplish their stated missions over the long run. Note that in many ways Ridge-way’s five goals for financial management are not much different from the financialmanagement goals of for-profit hospitals. In order to maximize shareholder wealth,the managers of for-profit hospitals must also maintain financial viability and obtainthe financial resources necessary to provide new services and technologies.

What is the primary goal of investor-owned firms? Of not-for-profit businesses?

From a financial management perspective, what are the major similarities anddifferences between the objectives of investor-owned and not-for-profit firms?

Cost of Capital Estimation

As we discussed in Chapter 11, a firm’s weighted average, or overall, cost of capital(WACC) is a blend of the costs of the various types of capital it uses. In general, costof capital estimation for not-for-profit businesses parallels that for investor-ownedfirms, but there are two major differences. First, since not-for-profit businesses pay notaxes, there are no tax effects associated with debt financing.6 Second, investor-ownedfirms raise equity capital by selling new common stock and by retaining earningsrather than paying them out as dividends. Not-for-profit businesses raise the equiva-lent of equity capital, which is called fund capital, in three ways: (1) by earning prof-its, which by law must be retained within the business; (2) by receiving grants fromgovernmental entities; and (3) by receiving contributions from individuals and compa-nies. Since fund capital is fundamentally different from equity capital, this questionarises: How do we measure the cost of fund capital?

Cost of Capital Estimation 30-5

5Technically, not-for-profit firms earn an “excess of revenues over expenses” rather than “profits.” But tokeep consistent terminology, we will generally use the term profits or net income for this excess, as domost people who work in not-for-profit firms.6However, most not-for-profit firms can issue tax-exempt bonds through municipal financing authorities.Thus, the cost of debt disadvantage of not being able to deduct interest expense from taxable income isoffset for the most part by issuing lower-cost tax-exempt debt. We will discuss tax-exempt debt in detail ina later section.

*CH30_Web_Brigham_859011 10/17/01 3:00 PM Page 30-5

Because the weighted average cost of capital is used primarily for capital budgetingdecisions, it represents the opportunity cost of using capital to purchase fixed assetsrather than for alternative uses. For investor-owned firms, the opportunity cost asso-ciated with equity capital is apparent—if available capital is not needed for investmentin fixed assets, it can be returned to the stockholders by either paying dividends or re-purchasing stock. For not-for-profit businesses, which do not have this option, the op-portunity cost of fund capital is more controversial. Historically, at least four positionshave been taken with regard to the cost of fund capital:7

1. It has been argued that fund capital has zero cost. The rationale here is (a) that con-tributors do not expect a monetary return on their contributions, and (b) that thefirm’s other suppliers of fund capital, especially the patients who pay more forservices than is warranted by the firm’s tangible costs, do not require an explicitreturn on the capital retained by the firm.

2. The second position also assumes a zero cost for fund capital, but here it is recog-nized that, when inflation exists, fund capital must earn a return sufficient to enablethe organization to replace existing assets as they wear out. For example, assumethat a not-for-profit firm buys a building that costs $1,000,000. Over time, the costof the building will be recovered by depreciation, so, at least in theory, $1,000,000will be available to replace the building when it becomes obsolete. However, be-cause of inflation the new building now might cost $1,500,000. If the firm has notincreased its fund capital by retaining earnings, the only way to finance the addi-tional $500,000 will be through grants and contributions, which may not be avail-able, or by increasing its debt and hence its debt ratio, which might not be desirableor even possible. Thus, just to maintain its existing asset base over time, a not-for-profit firm must earn a return on fund capital equal to the inflation rate, hence thisrate must be built into the firm’s cost of capital estimate. Of course, if the asset basemust increase to provide additional services, retained earnings above those neededto keep up with inflation will be required.

3. The third position is that fund capital has some cost but that it is not very high.When a not-for-profit firm either receives contributions or retains earnings, it canalways invest those funds in marketable securities rather than purchase real assets.Thus, fund capital has an opportunity cost that should be acknowledged, and thiscost is roughly equal to the return available on a portfolio of short-term, low-risksecurities such as T-bills.

4. Finally, others have argued that fund capital to not-for-profit businesses has aboutthe same cost as the cost of retained earnings to similar investor-owned firms. Therationale here also rests on the opportunity cost concept, but the opportunity costis now defined as the return available from investing the fund capital in alternativeinvestments of similar risk.

Which of the four positions is correct? Think about it this way: Suppose RidgewayCommunity Hospital expects to receive $500,000 in contributions in 2001 and alsoforecasts $1,500,000 in earnings, so it expects to have $2,000,000 of new fund capitalavailable for investment. The $2 million could be used to purchase assets related to itscore business, such as an outpatient clinic or diagnostic equipment; the money couldbe temporarily invested in securities with the intent of purchasing real assets some

30-6 CHAPTER 30 Financial Management in Not-for-Profit Businesses

7For one of the classic works on this topic, see Douglas A. Conrad, “Returns on Equity to Not-for-ProfitHospitals: Theory and Implementation,” Health Services Research, April 1984, 41–63. Also, see the follow-uparticles by Pauly; Conrad; and Silvers and Kauer in the April 1986 issue of Health Services Research.

*CH30_Web_Brigham_859011 10/17/01 3:00 PM Page 30-6

time in the future; it could be used to retire debt; it could be used to pay managementbonuses; it could be placed in a non-interest-bearing account at the bank; and so on. Ifit uses the capital to purchase real assets, Ridgeway is deprived of the opportunity touse this capital for other purposes, so an opportunity cost must be assigned.

The hospital’s investment in real assets should return at least as much as the returnavailable on securities investments of similar risk.8 What return is available on securi-ties with similar risk to hospital assets? Generally, the best answer is the return thatcould be expected from investing in the stock of an investor-owned hospital company,such as Columbia/HCA. After all, instead of using fund capital to purchase real assets,Ridgeway could always use the funds to buy the stock of an investor-owned hospitaland thus generate additional funds for future use. Therefore, the cost of fund capitalfor a not-for-profit corporation can be proxied by estimating the beta coefficient of asimilar investor-owned corporation and then using Hamada’s equation as discussed inChapter 16 to adjust for leverage and tax differences.

In general, the opportunity cost principle applies to all fund capital—this capitalhas a cost that is equal to the cost of retained earnings to similar investor-owned firms.However, contributions that are designated for a specific purpose, such as a children’shospital wing, may indeed have a zero cost: since the funds are restricted to a particu-lar project, the firm does not have the opportunity to invest them in other alternatives.

Although the opportunity cost concept is intuitively appealing, some fundamentalproblems are inherent in using a publicly held for-profit hospital corporation’s cost ofequity as a proxy for a not-for-profit hospital’s cost of fund capital. First and foremost,the market risk to equity investors is probably less than the risk imbedded in fund cap-ital because stockholders can eliminate a large portion of their investment risk byholding well-diversified portfolios. Stakeholders such as managers, patients, physi-cians, and employees, on the other hand, do not have the same opportunities to diver-sify their hospital-related activities. Furthermore, investor-owned companies tend tohave wide geographic and patient diversification, while not-for-profit hospitals tend tobe stand-alone concerns with little risk-reducing diversification. In spite of these con-cerns, it is reasonable to assign a cost of fund capital based on opportunity costs, andthe best estimate is the cost of equity to a similar for-profit business.

What is fund capital, and how does it differ from equity capital?

How does the cost of capital estimation process differ between investor-ownedand not-for-profit businesses?

Capital Structure Decisions

When making capital structure decisions within not-for-profit businesses, managersmust be concerned with two issues: Is capital structure theory, particularly the tax-benefits-versus-financial-distress-costs trade-off theory, applicable to not-for-profitbusinesses? And are there any characteristics of not-for-profit businesses that preventthem from following the guidance prescribed by theory?

Capital Structure Decisions 30-7

8We do not mean to imply here that not-for-profit firms should never invest in a project that will losemoney. Not-for-profit firms do invest in negative-profit projects that benefit their stakeholders, but theirmanagers must be aware of the financial opportunity costs inherent in such investments. We will have moreto say about this issue when we discuss capital budgeting decisions.

*CH30_Web_Brigham_859011 10/17/01 3:01 PM Page 30-7

No rigorous research has been conducted into the optimal capital structures ofnot-for-profit businesses, but some loose analogies can be drawn. Although not-for-profit businesses do not pay taxes and hence cannot reduce the cost of debt by

many of these businesses have access to the tax-exempt debt market. As aresult, not-for-profit businesses have about the same effective cost of debt as doinvestor-owned firms.

As discussed in the previous section, a not-for-profit firm’s fund capital has an op-portunity cost that is roughly equivalent to the cost of equity of an investor-ownedfirm of similar risk. Thus, we would expect the opportunity cost of fund capital to riseas more and more debt financing is used, just as it would for an investor-owned firm.Not-for-profit businesses are subject to the same types of financial distress and agencycosts that are borne by investor-owned firms, so these costs are equally applicable.Therefore, we would expect the trade-off theory to be applicable to not-for-profitbusinesses, and such businesses should have optimal capital structures that are defined,at least at first blush, as a trade-off between the costs and benefits of debt financing.Note, however, that the asymmetric information theory is not applicable to not-for-profit businesses because such businesses do not issue common stock.

Although the trade-off theory may be conceptually correct for not-for-profit busi-nesses, a problem arises when applying the theory. For-profit firms have relatively easyaccess to equity capital. Thus, if a for-profit firm has more capital investment oppor-tunities than it can finance with retained earnings and debt financing, it can generallyraise the needed funds by a new stock offering.9 Further, it is relatively easy for investor-owned firms to alter their capital structures. For example, if a firm is under-leveraged it can simply issue more debt and use the proceeds to repurchase stock, or ifit has too much debt it can issue additional shares and use the proceeds to retire debt.

Not-for-profit businesses do not have access to the equity markets—their solesource of “equity” capital is through government grants, private contributions, andprofits. Thus, managers of not-for-profit businesses do not have the same degree offlexibility in either capital investment or capital structure decisions as do their coun-terparts in for-profit firms. For this reason, it is often necessary for not-for-profit busi-nesses (1) to delay new projects because of funding insufficiencies and (2) to use morethan the theoretically optimal amount of debt because that is the only way that neededservices can be financed. Although these actions may be unavoidable, managers mustrecognize that such strategies do increase costs. Project delays result in needed ser-vices not being provided on a timely basis, and using more debt than the optimal levelpushes the firm beyond the point of the greatest net benefit of debt financing, whichincreases its capital costs. Therefore, if a not-for-profit firm is forced into a situationwhere it is using more than the optimal amount of debt financing, its managers shouldplan to reduce the level of debt as soon as the situation permits.

The ability of not-for-profit businesses to obtain government grants, to attract pri-vate contributions, and to generate excess revenues plays an important role in estab-lishing the firm’s competitive position. A firm that has an adequate amount of fundcapital can operate at its optimal capital structure and thus minimize capital costs. Ifsufficient fund capital is not available, a not-for-profit firm may be forced to rely tooheavily on debt financing, resulting in higher capital costs. Also, its weakened financialcondition may prevent it from acquiring capital equipment that would increase its ef-ficiency and improve its services, thus hampering its overall operating performance.

(1 � T),

30-8 CHAPTER 30 Financial Management in Not-for-Profit Businesses

9According to the asymmetric information theory of capital structure, managers may not want to issue newstock, but the capability is there, and circumstances do arise in which managers issue new equity to obtainneeded financing.

*CH30_Web_Brigham_859011 10/17/01 3:01 PM Page 30-8

Imagine two not-for-profit businesses that are similar in all respects except thatone has more fund capital and can operate at its optimal capital structure, while theother has insufficient fund capital and thus must use more debt than its optimum. Thefinancially strong firm has a significant competitive advantage because it can either of-fer more services at the same cost or it can offer matching services at lower costs.

Is the trade-off theory of capital structure applicable to not-for-profit businesses? Explain.

What impact does the inability to issue common stock have on capital structuredecisions within not-for-profit businesses?

Capital Budgeting Decisions

In this section, we discuss the effect of not-for-profit status on three elements of capi-tal budgeting: (1) appropriate goals for project analysis, (2) cash flow estimation/decision methods, and (3) risk analysis.

The Goal of Project Analysis

The primary goal of a not-for-profit business is to provide some service to society, notto maximize shareholder wealth. In this situation, capital budgeting decisions mustconsider many factors besides the project’s profitability. For example, noneconomicfactors such as the well-being of the community must also be taken into account, andthese factors may outweigh financial considerations.

Nevertheless, good decision making, designed to ensure the future viability of theorganization, requires that the financial impact of each capital investment be fully rec-ognized. Indeed, if a not-for-profit business takes on unprofitable projects that are notoffset by profitable projects, the firm’s financial condition will deteriorate, and if thissituation persists over time it could lead to bankruptcy and closure. Obviously, bank-rupt businesses cannot meet community needs.

Cash Flow Estimation/Decision Methods

In general, the same project analysis techniques that are applicable to investor-ownedfirms are also applicable to not-for-profit businesses. However, two differences do ex-ist. First, since some projects of not-for-profit businesses are expected to provide a so-cial value in addition to a purely economic value, project analysis should consider so-cial value along with financial, or cash flow, value. When social value is considered, thetotal net present value (TNPV) of a project can be expressed as follows:10

(30-1)

Here, NPV is the standard net present value of the project’s cash flow stream, andNPSV is the net present social value of the project. The NPSV term clearly differen-tiates capital budgeting in not-for-profit businesses from that in investor-owned firms,and it represents the firm’s assessment of the project’s social value as opposed to itspure financial value as measured by NPV.

TNPV � NPV � NPSV.

Capital Budgeting Decisions 30-9

10For more information on the social value model, see John R. C. Wheeler and Jan P. Clement, “CapitalExpenditure Decisions and the Role of the Not-For-Profit Hospital: An Application of the Social GoodsModel,” Medical Care Review, Winter 1990, 467–486.

*CH30_Web_Brigham_859011 10/17/01 3:01 PM Page 30-9

A project is deemed to be acceptable if its Not all projects have socialvalue, but if a project does, this value should be recognized in the decision process. Notethat to ensure the financial viability of the firm, the sum of the NPVs of all projects initi-ated in a planning period, plus the value of the unrestricted contributions received,must equal or exceed zero. If this restriction were not imposed, social value could dis-place financial value over time, but this would not be a sustainable situation because afirm cannot continue to provide social value unless its financial integrity is maintained.

NPSV can be defined as follows:

(30-2)

Here, the social values of a project in every Year t, quantified in some manner, are dis-counted back to Year 0 and then summed. In essence, the suppliers of fund capital to anot-for-profit firm never receive a cash return on their investment. Instead, they re-ceive a return on investment in the form of social dividends, such as charity care, med-ical research and education, and myriad other community services that for various rea-sons do not pay their own way. Services provided to patients at a price equal to orgreater than the full cost of production are assumed not to create social value. Simi-larly, if governmental entities purchase care directly for beneficiaries of a program orsupport research, the resulting social value is attributed to the governmental entity,not to the provider of the services.

In estimating a project’s NPSV (that is, in evaluating Equation 30-2), it is neces-sary (1) to quantify the social value of the services provided by the project in each yearand (2) to determine the discount rate that is to be applied to those services. First, con-sider how we might quantify the social value of services provided in the health care in-dustry. When a project produces services to individuals who are willing and able to payfor those services, the value of those services is captured by the amount the individualsactually pay. Thus, one approach to valuing the services provided to those who cannotpay, or to those who cannot pay the full amount, is to use the average net price paid byindividuals who do pay. This approach has intuitive appeal, but there are four pointsthat merit further discussion:

1. Price is a fair measure of value only if the payer has the capacity to judge the truevalue of the services provided. Many who are knowledgeable about the health careindustry would argue that information asymmetries between the provider and thepurchaser reduce the ability of the purchaser to judge true value.

2. Because most payments for health care services are made by third parties, price dis-tortions may occur. For example, insurers might be willing to pay more for servicesthan an individual would pay in the absence of insurance. Or the existence ofmonopsony power, say, by Medicare, might result in a net price that is less than in-dividuals would actually be willing to pay.

3. The amount that an individual is willing to pay might be more or less than theamount a contributor or other fund supplier would be willing to pay for the sameservice.

4. Finally, there is a great deal of controversy over the true value of treatment in manyhealth care situations. If we are entitled to whatever health care is available regard-less of its cost, and if we are not individually required to pay for the care (even thoughsociety, as a whole, is), then we may demand a level of care that is of questionablevalue. For example, should $100,000 be spent to keep a comatose 87-year-old per-son alive for 15 more days? If the true social value of such an effort is zero, then itmakes little sense to assign a $100,000 value to the care just because that is its cost.

NPSV � an

t�1 Social valuet

(1 � ks)t .

TNPV � 0.

30-10 CHAPTER 30 Financial Management in Not-for-Profit Businesses

*CH30_Web_Brigham_859011 10/17/01 3:01 PM Page 30-10

In spite of potential problems mentioned here, it still seems reasonable to assign a so-cial value to many (but not all) health care services on the basis of the price that othersare willing to pay for those services.11

The second element required to estimate a project’s NPSV is the discount ratethat is to be applied to its annual social value stream. As with the required rate of re-turn on equity for not-for-profit businesses, there has been considerable controversyover the proper discount rate to apply to future social values. However, it is clear thatcontributors of fund capital can capture social value in two ways. First, note that con-tributions can be made directly to not-for-profit organizations. Second, note thatcontributors could always invest the funds in a portfolio of securities and then use theproceeds to purchase the health care services directly. In the second situation, therewould be no tax consequences on the portfolio’s return because the contributedproceeds would qualify for tax exemption; however, the contributor would lose the taxexemption on the full amount of the funds placed in the portfolio. Because the sec-ond alternative exists, it is reasonable to argue that providers should require a returnon the social value stream that approximates the return available on the equity in-vestment in for-profit firms offering the same services.

The net present social value model formalizes the capital budgeting decisionprocess applicable to not-for-profit businesses. Although few organizations attempt toquantify NPSV for all projects, not-for-profit businesses should at least subjectivelyconsider the social value inherent in projects under consideration.

Another important difference between investor-owned and not-for-profit busi-nesses involves the amount of capital available for investment. Standard capital bud-geting procedures assume that firms can raise virtually unlimited amounts of capitalto meet investment requirements. Presumably, as long as a firm is investing the fundsin profitable (positive NPV) projects, it should raise the debt and equity needed tofund the projects. However, not-for-profit businesses have limited access to capital—their fund capital is limited to retentions, contributions, and grants, and their debtcapital is limited to the amount that can be supported by their fund capital base.Thus, not-for-profit businesses are likely to face periods in which the cost of desir-able new projects will exceed the amount that can be financed, so not-for-profitbusinesses are often subject to capital rationing, a topic we discussed in detail inChapter 13.

If capital rationing exists, then, from a financial perspective, the firm should acceptthat set of capital projects that maximizes aggregate NPV without violating the capitalconstraint. This amounts to “getting the most bang from the buck,” and it involves se-lecting projects that have the greatest positive impact on the firm’s financial condition.However, in a not-for-profit setting, priority may be assigned to some low-profit oreven negative NPV projects. This is acceptable as long as these projects are offset bythe selection of positive NPV projects, which would prevent the low-profit, priorityprojects from eroding the firm’s financial integrity.

Capital Structure Decisions 30-11

11The issue of interpersonal values also arises—is the value of a heart transplant the same to a 75-year-oldin poor health as to a 16-year-old in otherwise good health? An even more controversial issue has to do withthe ability to pay—if someone can afford a Rolls Royce and he or she wants to buy one, he or she can, eventhough someone else may think the car is not worth the cost. To what extent is health care different fromcars—or food, shelter, and clothes? Hence, to what extent should the health care industry be insulated fromthe kinds of economic incentives that operate in other industries? To date, our society has not come to gripswith this issue, but with health care costs rising at a rate that would make it exceed the gross national prod-uct in less than 50 years, something must be done, and fairly soon.

*CH30_Web_Brigham_859011 10/17/01 3:01 PM Page 30-11

Risk Analysis

As we discussed in Chapter 14, three separate and distinct types of project risk can bedefined: (1) stand-alone risk, which ignores portfolio effects and views the risk of aproject as if it were held in isolation; (2) corporate risk, which views the risk of a proj-ect within the context of the firm’s portfolio of projects; and (3) market risk, whichviews a project’s risk from the perspective of a shareholder who holds a well-diversifiedportfolio of stocks. For investor-owned firms, market risk is the most relevant,although corporate risk should not be totally ignored.

For not-for-profit businesses, stand-alone risk would be relevant if a firm had onlyone project. In this situation, there would be no portfolio consequences, either at thefirm or individual investor level, so risk could be measured by the variability of fore-casted returns. However, most not-for-profit businesses offer a myriad of differentproducts or services; thus, they can be thought of as having a large number (hundredsor even thousands) of individual projects. For example, most not-for-profit healthmaintenance organizations (HMOs) offer health care services to a large number of di-verse employee groups in numerous service areas. In this situation, the stand-alonerisk of a project under consideration is not relevant because the project will not beheld in isolation. Rather, the relevant risk of a new project is its corporate risk, whichis the contribution of the project to the firm’s overall risk as measured by the impact ofthe project on the variability of the firm’s overall profitability.

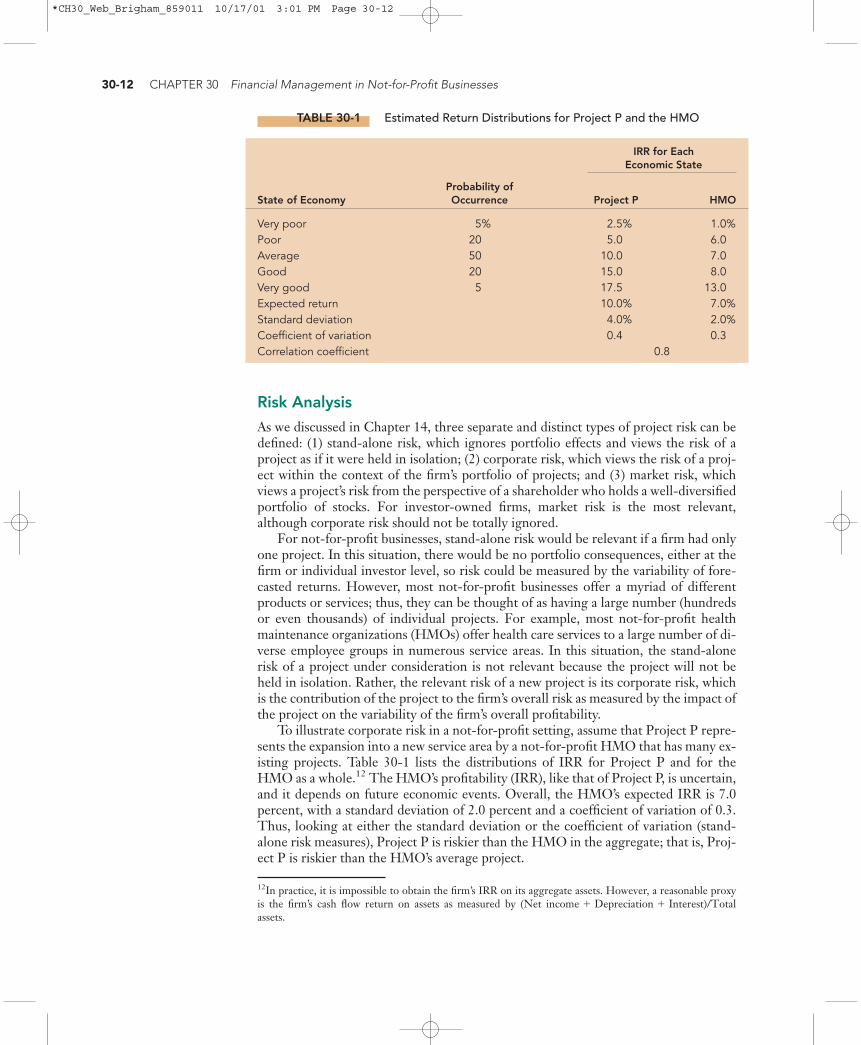

To illustrate corporate risk in a not-for-profit setting, assume that Project P repre-sents the expansion into a new service area by a not-for-profit HMO that has many ex-isting projects. Table 30-1 lists the distributions of IRR for Project P and for theHMO as a whole.12 The HMO’s profitability (IRR), like that of Project P, is uncertain,and it depends on future economic events. Overall, the HMO’s expected IRR is 7.0percent, with a standard deviation of 2.0 percent and a coefficient of variation of 0.3.Thus, looking at either the standard deviation or the coefficient of variation (stand-alone risk measures), Project P is riskier than the HMO in the aggregate; that is, Proj-ect P is riskier than the HMO’s average project.

30-12 CHAPTER 30 Financial Management in Not-for-Profit Businesses

TABLE 30-1 Estimated Return Distributions for Project P and the HMO

IRR for EachEconomic State

Probability ofState of Economy Occurrence Project P HMO

Very poor 5% 2.5% 1.0%Poor 20 5.0 6.0Average 50 10.0 7.0Good 20 15.0 8.0Very good 5 17.5 13.0Expected return 10.0% 7.0%Standard deviation 4.0% 2.0%Coefficient of variation 0.4 0.3Correlation coefficient 0.8

12In practice, it is impossible to obtain the firm’s IRR on its aggregate assets. However, a reasonable proxyis the firm’s cash flow return on assets as measured by (Net assets.

income � Depreciation � Interest)/Total

*CH30_Web_Brigham_859011 10/17/01 3:01 PM Page 30-12

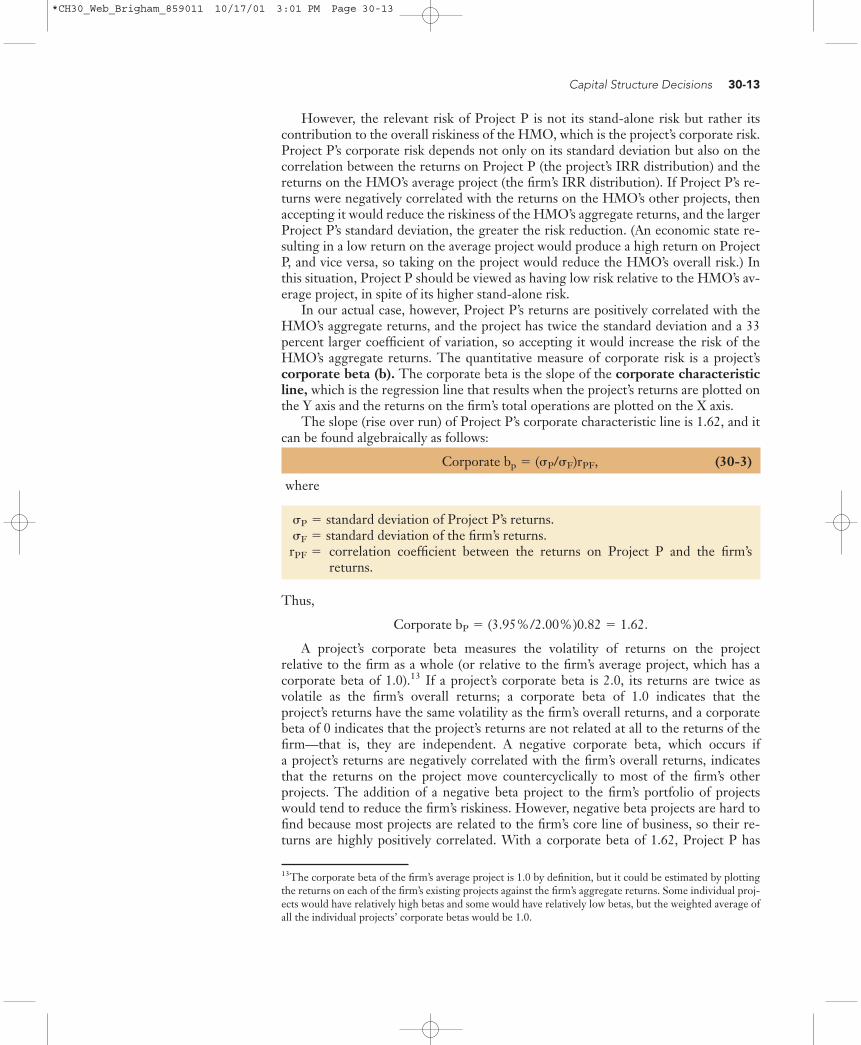

However, the relevant risk of Project P is not its stand-alone risk but rather itscontribution to the overall riskiness of the HMO, which is the project’s corporate risk.Project P’s corporate risk depends not only on its standard deviation but also on thecorrelation between the returns on Project P (the project’s IRR distribution) and thereturns on the HMO’s average project (the firm’s IRR distribution). If Project P’s re-turns were negatively correlated with the returns on the HMO’s other projects, thenaccepting it would reduce the riskiness of the HMO’s aggregate returns, and the largerProject P’s standard deviation, the greater the risk reduction. (An economic state re-sulting in a low return on the average project would produce a high return on ProjectP, and vice versa, so taking on the project would reduce the HMO’s overall risk.) Inthis situation, Project P should be viewed as having low risk relative to the HMO’s av-erage project, in spite of its higher stand-alone risk.

In our actual case, however, Project P’s returns are positively correlated with theHMO’s aggregate returns, and the project has twice the standard deviation and a 33percent larger coefficient of variation, so accepting it would increase the risk of theHMO’s aggregate returns. The quantitative measure of corporate risk is a project’scorporate beta (b). The corporate beta is the slope of the corporate characteristicline, which is the regression line that results when the project’s returns are plotted onthe Y axis and the returns on the firm’s total operations are plotted on the X axis.

The slope (rise over run) of Project P’s corporate characteristic line is 1.62, and itcan be found algebraically as follows:

(30-3)

where

standard deviation of Project P’s returns.standard deviation of the firm’s returns.correlation coefficient between the returns on Project P and the firm’s returns.

Thus,

A project’s corporate beta measures the volatility of returns on the project relative to the firm as a whole (or relative to the firm’s average project, which has acorporate beta of 1.0).13 If a project’s corporate beta is 2.0, its returns are twice asvolatile as the firm’s overall returns; a corporate beta of 1.0 indicates that the project’s returns have the same volatility as the firm’s overall returns, and a corporatebeta of 0 indicates that the project’s returns are not related at all to the returns of thefirm—that is, they are independent. A negative corporate beta, which occurs if a project’s returns are negatively correlated with the firm’s overall returns, indicatesthat the returns on the project move countercyclically to most of the firm’s other projects. The addition of a negative beta project to the firm’s portfolio of projectswould tend to reduce the firm’s riskiness. However, negative beta projects are hard tofind because most projects are related to the firm’s core line of business, so their re-turns are highly positively correlated. With a corporate beta of 1.62, Project P has

Corporate bP � (3.95%/2.00%)0.82 � 1.62.

rPF � �F � �P �

Corporate bp � (�P/�F)rPF,

Capital Structure Decisions 30-13

13The corporate beta of the firm’s average project is 1.0 by definition, but it could be estimated by plottingthe returns on each of the firm’s existing projects against the firm’s aggregate returns. Some individual proj-ects would have relatively high betas and some would have relatively low betas, but the weighted average ofall the individual projects’ corporate betas would be 1.0.

*CH30_Web_Brigham_859011 10/17/01 3:01 PM Page 30-13

significantly more corporate risk than the HMO’s average project, and the HMO’sWACC should be increased to reflect the differential risk prior to evaluating the project.

As with investor-owned firms, in most situations it is very difficult, if not impos-sible, to develop accurate quantitative assessments of projects’ corporate risk. There-fore, managers are often left with only an assessment of a project’s stand-alone riskplus a subjective notion about how it fits into the firm’s other operations. Generally,the project under consideration will be in the same line of business as the firm’s (ordivision’s) other projects; in this situation, stand-alone and corporate risk are highlycorrelated, and hence a project’s stand-alone risk will be a good measure of its cor-porate risk. This suggests that managers of not-for-profit businesses can get a feel forthe relevant risk of most projects by conducting scenario, simulation, and/or decisiontree analyses.

Ultimately, capital budgeting decisions in not-for-profit organizations require theblending of objective and subjective factors to reach a conclusion about a project’s risk,social value, effects on debt capacity, profitability, and overall acceptability. Theprocess is not precise, and often there is a temptation to ignore risk considerations be-cause they are so nebulous. Nevertheless, a project’s riskiness should be assessed andincorporated into the decision-making process.14

Why is it necessary for not-for-profit businesses to worry about the profitabilityof proposed projects?

Describe the net present social value model for making capital budgeting decisions. How might social value be measured?

Which are more likely to experience capital rationing: investor-owned businessesor not-for-profit businesses? Why?

What project risk measure is most relevant for investor-owned businesses? For not-for-profit businesses?

What is a corporate beta? How does a corporate beta differ from a market beta?

Long-Term Financing Decisions

Not-for-profit businesses have access to many of the same types of capital as doinvestor-owned firms, but there are two major differences: (1) not-for-profit firms canissue tax-exempt debt, but (2) they cannot issue equity, although they can solicit tax-exempt contributions, and their earnings are not taxable and must be retained.

Long-Term Debt Financing

Regarding debt financing, the major difference between investor-owned and not-for-profit businesses is that not-for-profit businesses can issue tax-exempt, or municipal,bonds, generally called munis.15 There are several types of munis. For example,

30-14 CHAPTER 30 Financial Management in Not-for-Profit Businesses

14Risk considerations are generally much more important than debt capacity considerations because a proj-ect’s cost of capital is affected to a much greater degree by differential risk than by differential debt capacity.15Municipal bond is the name given to long-term debt obligations issued by states and their political subdivi-sions, such as counties, cities, port authorities, toll road or hospital authorities, and so on. Short-term munici-pal notes are issued primarily to meet temporary cash needs, and long-term municipal bonds are usually usedto finance capital projects.

*CH30_Web_Brigham_859011 10/17/01 3:02 PM Page 30-14

general obligation bonds are secured by the full faith and credit of a governmentunit (that is, they are backed by the full taxing authority of the issuer), whereas specialtax bonds are secured by a specified tax, such as a tax on utility services. Of specific in-terest to not-for-profit businesses are revenue bonds, where the revenues derivedfrom such projects as roads and bridges, airports, water and sewage systems, and not-for-profit health care facilities are pledged as security for the bonds. Most municipalbonds are sold in serial form, which means that a portion of the issue comes due peri-odically, generally every six months or every year, over the life of the issue. Theshorter maturities are essentially equivalent to sinking fund payments on corporatebonds, and they help to ensure that the bonds are retired before the revenue-producing asset has been fully depreciated. Munis are typically issued in denomina-tions of $5,000 or multiples of $5,000, and although most are tax exempt, some thathave been issued since 1986 are taxable to investors.

In contrast to corporate bonds, municipal issues are not required to be registeredwith the Securities and Exchange Commission (SEC). Information about municipalissues is found in each issue’s official statement, which is prepared before the issue isbrought to market. To assist buyers and sellers of municipal bonds in the secondarymarket, the SEC recently adopted rules that require issuers of municipal bonds toprovide an audited annual report on their current financial condition, and to release ina timely fashion information that is “material” to the credit quality of their outstand-ing debt.

Whereas the majority of federal government and corporate bonds are held by in-stitutions, close to 50 percent of all municipal bonds outstanding are held by individ-ual investors. The primary attraction of most municipal bonds is their exemption fromfederal and state (in the state of issue) taxes. For example, the interest rate on an AAA-rated long-term corporate bond in January 2001 was 6.4 percent, while the rate on atriple-A muni was 5.0 percent. To an individual investor in the 40 percent federal-plus-state tax bracket, the muni bond’s equivalent taxable yield is

It is easy to see why high-tax-bracket investors often prefer mu-nicipal bonds to corporates.16

To illustrate the use of municipal bonds by a not-for-profit hospital, consider theJune 1995, $56 million issue by the Orange County (Florida) Health Facilities Au-thority. The authority is a public body created under Florida’s Health Facilities Authorities Law, and it issues health facilities municipal revenue bonds and then givesthe proceeds to the qualifying health care provider. For this particular bond issue, theprovider was the Citrus Medical Center, a not-for-profit hospital, and the primarypurpose of the issue was to raise funds to build and equip a children’s hospital facil-ity. The bonds were secured solely by the revenues of Citrus Medical Center, so theactual issuer—the Orange County Health Facilities Authority—had no responsibilityregarding the interest or principal payments on the issue. The bonds were rated AAA,not on the basis of the financial strength of Citrus Medical Center but rather be-cause the bonds were insured by the Municipal Bond Investors Assurance (MBIA)Corporation.17 Table 30-2 shows the maturities and interest rates associated with theissue.

5.0%/0.6 � 8.3%.5.0%/(1 � 0.40) �

Long-Term Financing Decisions 30-15

16For more information on tax-exempt financing by not-for-profit firms, see Bradley M. Odegard, “Tax-Exempt Financing under the Tax Reform Act of 1986,” Topics in Health Care Financing, Summer 1988.Also see Kenneth Kaufman and Mark L. Hall, The Capital Management of Health Care Organizations(Ann Arbor, MI: Health Administration Press, 1990), Chapter 5.17Municipal bond insurance, which is called credit enhancement, will be discussed in more detail later in thesection.

*CH30_Web_Brigham_859011 10/17/01 3:02 PM Page 30-15

Note the following points regarding the Citrus Medical Center municipal bondissue:

1. The issue is a serial issue; that is, the $56,000,000 in bonds are composed of 13 se-ries, or individual issues, with maturities ranging from about 2 years to 30 years.

2. Because the yield curve was normal, or upward sloping, at the time of issue, theinterest rates increase as the series’ maturities increase.

3. The bonds that mature in 2010, 2015, and 2025 are called “term bonds,” and theyhave sinking fund provisions that require the hospital to place a specified dollaramount with a trustee each year to ensure that funds are available to retire the is-sues as they become due. The trustee may either buy up the relevant bonds in theopen market or call the bonds at par for redemption. If interest rates have fallen,and the bonds sell at a premium, the trustee will call the bonds, but if rates haverisen, the trustee will make open market purchases.

4. Although it is not shown in the table, Citrus’s debt service requirements—the to-tal amount of principal and interest that it has to pay on the issue—are relatively con-stant over time, at about $4 million per year. In effect, the debt payments are spreadrelatively evenly over time. The purpose of structuring the series in this way is tomatch the maturity of the asset with the maturities of the bonds. Think about it thisway: The children’s hospital has a life of about 30 years. During this time, it will begenerating revenues more or less evenly, and its value will decline more or lessevenly. Thus, the issuer has structured the debt series so that the debt service re-quirements can be met by the revenues associated with the children’s hospital. At theend of 30 years, the debt will be paid off, and Citrus will probably be planning for areplacement facility that would be funded, at least in part, by a new bond issue.

One feature unique to municipal bonds is credit enhancement, or bond insur-ance, which is a relatively recent development used for upgrading an issue’s rating toAAA. Credit enhancement is offered by several credit insurers; the two largest are theMunicipal Bond Investors Assurance (MBIA) Corporation and AMBAC Indemnity

30-16 CHAPTER 30 Financial Management in Not-for-Profit Businesses

TABLE 30-2 Citrus Medical Center Municipal Bond Issue: Maturities, Amounts, and Interest Rates

Maturitya Amount Interest Rate

1997 4.35%1998 740,000 4.451999 785,000 4.602000 825,000 4.752001 880,000 4.902002 925,000 5.002003 985,000 5.102004 1,050,000 5.202005 1,115,000 5.302006 1,190,000 5.402010 5,590,000 5.802015 9,435,000 5.902025 6.00

aAll serial issues mature on June 1 of the listed year.

Source: Orange County Health Facilities Authority Official Statement.

$56,000,00031,775,000

$ 705,000

*CH30_Web_Brigham_859011 10/17/01 3:02 PM Page 30-16

Corporation. Currently, about 40 percent of all new municipal issues carry bondinsurance.

Here is how credit enhancement works. Regardless of the inherent credit rating ofthe issuer, the bond insurance company guarantees that bondholders will receive thepromised interest and principal payments. Thus, bond insurance protects investorsagainst default by the issuer. Because the insurer gives its guarantee that payments willbe made, the bond carries the credit rating of the insurance company, not of the issuer.For example, in our previous discussion on the bonds issued by the Orange CountyHealth Facilities Authority on behalf of Citrus Medical Center, we noted that thebonds were rated AAA because of MBIA insurance. The hospital itself has an A rating;hence, bonds issued without credit enhancement would be rated A. The guarantee byMBIA resulted in the AAA rating.

Credit enhancement gives the issuer access to the lowest possible interest rate, butnot without a cost—bond insurers typically charge an upfront fee of about 0.7 to 1.0percent of the total debt service over the life of the bond. Of course, the lower the hos-pital’s inherent credit rating, the higher the cost of bond insurance. Additionally, bondinsurers typically will not insure issues that would have a rating below A if uninsured.

To illustrate credit enhancement, again consider the Citrus Medical Center bonds.The total debt service (principal and interest) on the bonds amounts to roughly $140million on the $56 million issue (interest adds up quickly). Assuming an insurance costof 1.0 percent, the fee for the insurance would be $1.4 million. Is it worth it? CitrusMedical Center apparently thought so. To perform an analysis, simply discount the in-terest savings that result from the AAA rating (as opposed to the uninsured A rating)back to the present, and compare this present value with the insurance cost. If thepresent value of the savings exceeds the cost of the bond insurance, then insuranceshould be purchased.

Equity (Fund) Financing

Investor-owned firms have two sources of equity financing: retained earnings and pro-ceeds from new stock offerings. Not-for-profit businesses can, and do, retain earnings,but they cannot sell stock to raise equity capital. They can, however, raise equity cap-ital through charitable contributions. Individuals as well as firms are motivated tocontribute to not-for-profit businesses for a variety of reasons, including concern forthe well-being of others, the recognition that often accompanies large contributions,and tax deductibility.

To illustrate, consider not-for-profit hospitals, most of which received their initial,startup equity capital from religious, educational, or governmental entities (some hos-pitals also receive ongoing funding from these sources). Since the 1970s, these sourceshave provided a much smaller proportion of hospital funding, forcing many not-for-profit hospitals to rely more on retained earnings and charitable contributions. Fur-ther, federal programs—such as the Hill-Burton Act, which provided large amounts offunds for hospital expansion following World War II—have been discontinued.

On the surface, it appears that investor-owned firms have a significant advantage inraising equity capital because new common stock can in theory be issued at any timeand in any amount. Conversely, charitable contributions are much less reliable—pledges are not always collected, so funds that were counted on may not be available.Furthermore, the planning, solicitation, and collection periods can take years. Also,whereas the proceeds of new stock offerings may be used for any purpose, charitablecontributions are often restricted, which means that they can be used only for adesignated purpose. Note, however, that managers of investor-owned firms do nothave complete freedom to raise capital in the equity markets—if market conditions are

Long-Term Financing Decisions 30-17

*CH30_Web_Brigham_859011 10/17/01 3:02 PM Page 30-17

poor and the stock is selling at a low price, then a new stock issue can be harmful to thefirm’s current stockholders. Also, as we discussed in Chapter 16, a new stock offeringmay be viewed by investors as a signal by management that the firm’s stock is over-valued, so new stock issues tend to have a negative effect on the firm’s stock price,which discourages their use.

Define the following terms:

(1) Municipal bonds

(2) Revenue bonds

(3) Serial bonds

(4) Official statement

(5) Debt service requirements

(6) Credit enhancement

Do municipal financing authorities that issue revenue bonds generally have anyobligations regarding the payment of interest and principal? Explain.

How could a not-for-profit firm’s financial manager evaluate whether or not tobuy bond insurance?

Financial Analysis, Planning, and Forecasting

The general procedures for financial analysis, planning, and forecasting discussed inChapters 3 and 4 pertain to both investor-owned and not-for-profit businesses. Theprimary difference is the accounting procedures used, which affects the “look” of thefinancial statements.

For illustrative purposes, consider the health care industry again. As in all indus-tries, financial reporting in health care follows a set of standards (established by theaccounting profession) called generally accepted accounting principles (GAAP).18

The two primary organizations that promulgate standards for the health care industryare the Financial Accounting Standards Board (FASB), which deals with issues per-taining to private organizations, and the Government Accounting Standards Board(GASB), which deals with issues related to governmental entities. Generally, the prin-ciples promulgated by FASB and GASB relate to issues that are relevant to most indus-tries, while industry-specific issues are addressed by the various industry committees ofthe American Institute of Certified Public Accountants (AICPA). In 1972, the AICPAHealth Care Institutions Committee issued the first of six editions of the Hospital AuditGuide, which became the bible for those preparing hospital financial statements. In1990 the committee, which is now called the Health Care Committee, published an en-tirely new guide entitled Audits of Providers of Health Care Services, which superseded theold guides. Here are some of the more important provisions of the new guide:19

1. The new guide applies to all private organizations providing health care services toindividuals. Thus, it applies to both investor-owned and private not-for-profit

30-18 CHAPTER 30 Financial Management in Not-for-Profit Businesses

18For more information on the various organizations involved in setting accounting principles for thehealth care industry, see Woodrin Grossman and William Warshauer, Jr., “An Overview of the StandardSetting Process,” Topics in Health Care Financing, Summer 1990, 1–8.19For a more detailed review of the new audit guide, see Robert G. Colbert, “The New Health Care Auditand Accounting Guide,” Topics in Health Care Financing, Summer 1990, 14–23; and J. William Tillett andWilliam R. Titera, “What AICPA Audit Guide Revisions Mean for Providers,” Healthcare Financial Man-agement, July 1990, 52–62.

*CH30_Web_Brigham_859011 10/17/01 3:03 PM Page 30-18

organizations such as hospitals, nursing homes, managed care plans, home healthagencies, medical group practices, and clinics.20

2. The new guide contains complete sets of sample financial statements, includingfootnote disclosures, for the major types of providers.

3. Prior to the issuance of the new guide, providers reported revenues on the incomestatement on the basis of charges (gross revenues), whether or not the charges wereexpected to be collected. Then, the various deductions from charges, such as con-tractual allowances (discounts), bad debt losses, and charity care, were subtractedfrom gross revenue. The new guide prescribes that only net revenue should beshown on the income statement, because charges not billed or not expected to becollected do not represent expected revenue to the provider. Bad debt losses con-stitute an operating expense and continue to be shown directly on the incomestatement, but contractual allowances and charity care are now reported in thefootnotes.21

4. The new guide blurs the distinction between operating and nonoperating cashflows. Essentially, operating revenues and expenses occur because of an organi-zation’s central mission and operations. On the other hand, nonoperating gainsand losses result from transactions that are incidental or peripheral to the organi-zation’s mission. Considerable latitude exists in what an organization defines as itscentral mission and operations, but most organizations classify most revenues andexpenses as operating. In general, only contributions, investment income, andgains and losses on financial transactions such as bond refundings are classified asnonoperating.

5. The new guide validates cash flows as the best measure of transactions. Thus, thestatement of cash flows has become a standard financial statement for not-for-profit health care providers.

6. Finally, the new guide contains detailed guidance on issues that are unique tothe health care industry. Examples include the reporting of third-party pay-ments from insurance companies such as Blue Cross/Blue Shield and malpracticeinsurance.

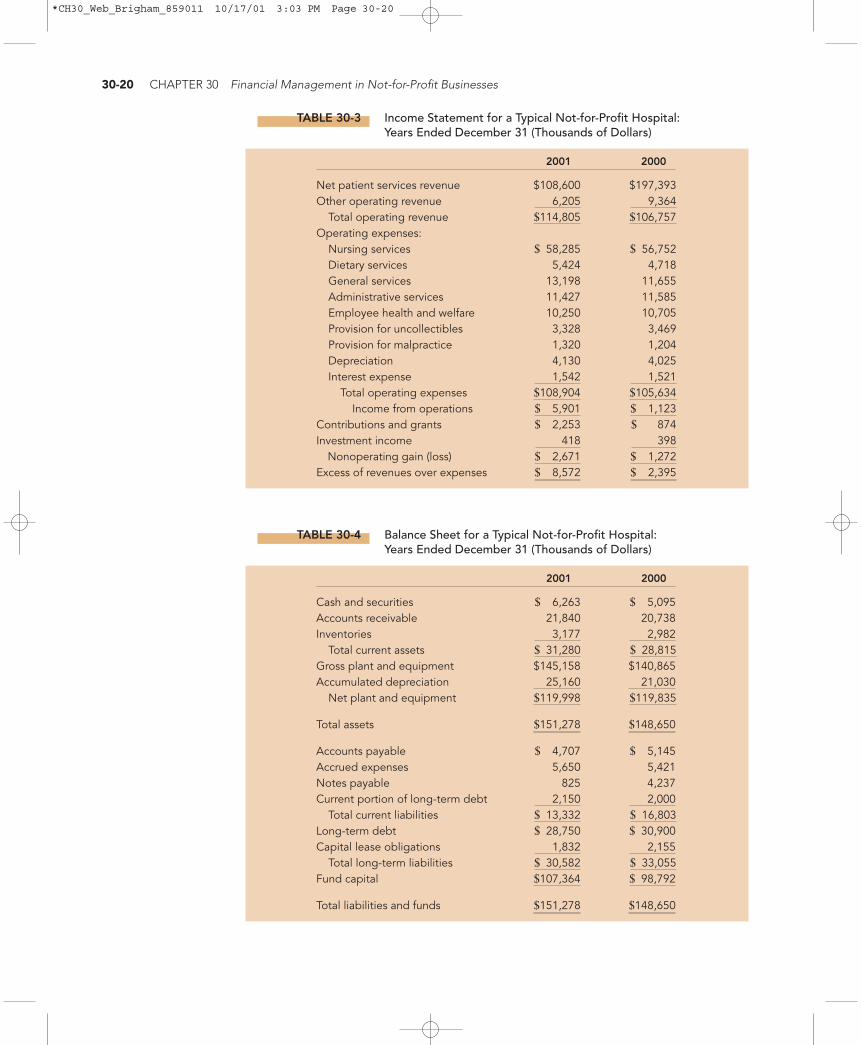

Tables 30-3 and 30-4 show the 2000 and 2001 income statements (also called state-ments of revenues and expenses) and balance sheets for a typical not-for-profit hospital.Three points about the statements are worth noting. First, the formats for the state-ments are similar to those of investor-owned firms. Second, the hospital had an excessof revenues over expenses (or net income) of $8,572,000 in 2001. Of course, being anot-for-profit firm, the hospital paid no taxes or dividends, so it retained all of its$8,572,000 in net income. Third, the claims against assets are of two types: liabilities, ormoney the company owes, and fund capital. Fund capital is a residual. Thus, for 2001:

Fund capital is the not-for-profit equivalent of equity capital and serves essentiallythe same function. A balance sheet fund account for a not-for-profit business is built upover time primarily by retentions and contributions but is reduced by operating losses.

Assets$151,278,000

�

�Liabilities

($13,332,000 � $30,582,000)� Fund capital.� $107,364,000.

Financial Analysis, Planning, and Forecasting 30-19

20Most governmental providers will also have to follow the new guide, but GASB statements will haveprecedence over the guide when conflicts occur.21If a provider does not expect to collect for services rendered, the care is classified as charity care and doesnot constitute revenue. However, if a provider expects to collect for services rendered but fails to do so, thenthe expected revenue becomes a bad debt loss.

*CH30_Web_Brigham_859011 10/17/01 3:03 PM Page 30-19

30-20 CHAPTER 30 Financial Management in Not-for-Profit Businesses

TABLE 30-3 Income Statement for a Typical Not-for-Profit Hospital: Years Ended December 31 (Thousands of Dollars)

2001 2000

Net patient services revenue $108,600 $197,393Other operating revenue

Total operating revenueOperating expenses:

Nursing servicesDietary services 5,424 4,718General services 13,198 11,655Administrative services 11,427 11,585Employee health and welfare 10,250 10,705Provision for uncollectibles 3,328 3,469Provision for malpractice 1,320 1,204Depreciation 4,130 4,025Interest expense

Total operating expensesIncome from operations

Contributions and grantsInvestment income

Nonoperating gain (loss)Excess of revenues over expenses $ 2,395$ 8,572

$ 1,272$ 2,671398418

$ 874$ 2,253$ 1,123$ 5,901$105,634$108,904

1,5211,542

$ 56,752$ 58,285

$106,757$114,8059,3646,205

TABLE 30-4 Balance Sheet for a Typical Not-for-Profit Hospital: Years Ended December 31 (Thousands of Dollars)

2001 2000

Cash and securitiesAccounts receivable 21,840 20,738Inventories

Total current assetsGross plant and equipment $145,158 $140,865Accumulated depreciation

Net plant and equipment

Total assets

Accounts payableAccrued expenses 5,650 5,421Notes payable 825 4,237Current portion of long-term debt

Total current liabilitiesLong-term debtCapital lease obligations

Total long-term liabilitiesFund capital

Total liabilities and funds $148,650$151,278

$ 98,792$107,364$ 33,055$ 30,582

2,1551,832$ 30,900$ 28,750$ 16,803$ 13,332

2,0002,150

$ 5,145$ 4,707

$148,650$151,278

$119,835$119,99821,03025,160

$ 28,815$ 31,2802,9823,177

$ 5,095$ 6,263

*CH30_Web_Brigham_859011 10/17/01 3:03 PM Page 30-20

What organizations prescribe standards for reporting by not-for-profit busi-nesses?

How do the financial statements of investor-owned and not-for-profit businessesdiffer?

Short-Term Financial Management

The basic concepts of short-term financial management developed in Chapters 22 and 23 can be applied without modification to not-for-profit businesses.

SummaryThis chapter focuses on financial management within not-for-profit businesses. Thekey concepts covered are listed below:

� Although most finance graduates will go to work for investor-owned firms, many fi-nancial management professionals work for or closely with not-for-profitorganizations, which range from government agencies such as school districts andcolleges to charities such as the United Way and the American Heart Association.

� If an organization meets a set of stringent requirements, it can qualify for tax-exempt status. Such organizations, which must be incorporated, are callednot-for-profit corporations. One type of not-for-profit organization is the not-for-profit business, which sells goods and/or services to the public but whichhas not-for-profit status.

� The goal of a not-for-profit business is typically stated in terms of some missionrather than shareholder wealth maximization.

� Not-for-profit businesses raise the equivalent of equity capital, which is calledfund capital, in three ways: (1) by earning profits, which by law are retainedwithin the business, (2) by receiving grants from governmental entities, and (3) byreceiving contributions from individuals and companies.

� In not-for-profit businesses, the weighted average cost of capital is developed inthe same way as in investor-owned firms. Although there is no direct tax benefit tothe issuer associated with debt financing, there is a benefit to investors because in-terest received is often tax exempt; thus, the net cost of debt is similar for investor-owned and not-for-profit businesses.

� For cost of capital purposes, fund capital has an opportunity cost that is roughlyequal to the cost of equity of similar investor-owned firms.

� The trade-off theory of capital structure generally applies to not-for-profitfirms, but such firms do not have as much financial flexibility as investor-ownedfirms because not-for-profit firms cannot issue new common stock.

� The social value version of the net present value model recognizes that not-for-profit businesses should value social contributions as well as cash flows.

� In general, the relevant capital budgeting risk for not-for-profit businesses is cor-porate risk rather than market risk. Corporate risk is measured by a project’s cor-porate beta.

� Many not-for-profit organizations can raise funds in the municipal bond market.� Credit enhancement upgrades the rating of a municipal bond issue to that of the

insurer. However, issuers must pay a fee to obtain credit enhancement.� With minor exceptions, the financial statement formats of investor-owned and

not-for-profit businesses are the same.� Short-term financial management is generally unaffected by the ownership type.

Summary 30-21

*CH30_Web_Brigham_859011 10/17/01 3:04 PM Page 30-21

Questions

What is the major difference in ownership structure between investor-owned and not-for-profitbusinesses?

Does the asymmetric information theory of capital structure apply to not-for-profit businesses?Explain.

Does a not-for-profit firm’s marginal cost of capital (MCC) schedule have a retained earningsbreak point? Explain.

Assume that a not-for-profit firm does not have access to tax-exempt (municipal) debt and thusgains no benefits from the use of debt financing.a. What would be the firm’s optimal capital structure according to the cost-benefit trade-off

theory?b. Is it likely that the firm would be able to operate at its theoretically optimal structure?

Describe how social value can be incorporated into the NPV decision model. Do you think not-for-profit firms would normally try to quantify net present social value, or would they merelytreat it as a qualitative factor?

Why is corporate risk the most relevant project risk measure for not-for-profit businesses?

If all markets were informationally efficient, meaning that buyers and sellers would have easyaccess to the same information, would firms gain any cost advantage by purchasing bond insur-ance (credit enhancement)?

30–7

30–6

30–5

30–4

30–3

30–2

30–1

30-22 CHAPTER 30 Financial Management in Not-for-Profit Businesses

Sandra McCloud, a finance major in her last term of college, is currently scheduling her place-ment interviews through the university’s career resource center. Her list of companies is typicalof most finance majors: several commerical banks, a few industrial firms, and one brokeragehouse. However, she noticed that a representative of a not-for-profit hospital is scheduling in-terviews next week, and the position—that of financial analyst—appears to be exactly what San-dra has in mind. Sandra wants to sign up for an interview, but she is concerned that she knowsnothing about not-for-profit organizations and how they differ from the investor-owned firmsthat she has learned about in her finance classes. In spite of her worries, Sandra scheduled an ap-pointment with the hospital representative, and she now wants to learn more about not-for-profit businesses before the interview.

To begin the learning process, Sandra drew up the following set of questions. See if you canhelp her answer them.a. First, consider some basic background information concerning the differences between

not-for-profit organizations and investor-owned firms.(1) What are the key features of investor-owned firms? How do a firm’s owners exercise

control?(2) What is a not-for-profit corporation? What are the major control differences between

investor-owned and not-for-profit businesses?(3) How do goals differ between investor-owned and not-for-profit businesses?

b. Now consider the cost of capital estimation process.(1) Is the weighted average cost of capital (WACC) relevant to not-for-profit businesses?(2) Is there any difference between the WACC formula for investor-owned firms and that

for not-for-profit businesses?(3) What is fund capital? How is the cost of fund capital estimated?

c. Just as in investor-owned firms, not-for-profit businesses use a mix of debt and equity(fund) financing.(1) Is the trade-off theory of capital structure applicable to not-for-profit businesses? What

about the asymmetric information theory?

CDSee Ch 30 Show.ppt and Ch 30 Mini Case.xls.

*CH30_Web_Brigham_859011 10/17/01 3:06 PM Page 30-22

Selected Additional References 30-23

(2) What problem do not-for-profit businesses encounter when they attempt to implementthe trade-off theory?

d. Consider the following questions relating to capital budgeting decisions.(1) Why is capital budgeting important to not-for-profit businesses?(2) What is social value? How can the net present value method be modified to include the

social value of proposed projects?(3) Which of the three project risk measures—stand-alone, corporate, and market—is rele-

vant to not-for-profit businesses?(4) What is a corporate beta? How does it differ from a market beta?(5) In general, how is project risk actually measured within not-for-profit businesses? How

is project risk incorporated into the decision process?e. Not-for-profit businesses have access to many of the same long-term financing sources as do

investor-owned firms.(1) What are municipal bonds? How do not-for-profit health care businesses access the mu-

nicipal bond market?(2) What is credit enhancement, and what effect does it have on debt costs?(3) What are a not-for-profit business’s sources of fund capital?(4) What effect does the inability to issue common stock have on a not-for-profit business’s

capital structure and capital budgeting decisions?f. What unique problems do not-for-profit businesses encounter in financial analysis and plan-

ning? What about short-term financial management?

Selected Additional References

Easley, David, and Maureen O’Hara, “The Economic Roleof the Nonprofit Firm,” Bell Journal of Economics, Autumn1983, 531–538.

Hansmann, Henry B., “The Role of Nonprofit Enterprise,”Yale Law Review, April 1980, 835–901.

*CH30_Web_Brigham_859011 10/17/01 3:08 PM Page 30-23