Embed Size (px)

Citation preview

1

This is a pre-review, pre-copyedit author version, not for redistribution of the article Carballo-Penela, A., Mateo-Mantecón, I., Doménech, J. L., & Coto-Millán, P. (2012). From the motorways of the sea to the green corridors' carbon footprint: the case of a port in Spain. Journal of Environmental Planning and Management, 55(6), 765-782. Doi 10.1080/09640568.2011.627422 Published by Taylor & Francis. From the motorways of the sea to the green corridors’ carbon footprint: the case of a port in Spain Adolfo Carballo-Penelaa1 , Ingrid Mateo-Mantecónb, Juan Luis Doménech Quesadac, Pablo Coto-Millánb aDepartment of Business Organization, University of Santiago de Compostela, Santiago de Compostela Spain.

Facultade de CC Económicas e Empresariais, Avd. Burgo das Nacións s/n. CP.15782. Tel: +34981563100 ext.11649 Fax : +34981 54 70 36. E-mail : [email protected] bDepartment of Economics, University of Cantabria, Santander, Spain.

Avd/ de los Castros s/n. CP. 39005. Santander Tel: +34942201567. Fax: +34942201603. Tel: + 34942201653. Fax: +34942201603. cDepartment of Environment. Port of Gijón, Gijón, Spain.

C/Claudio Alvargonzález 32, CP. 33201 Gijón. Tel: +34985 179600. Fax: +34 985 179696.

Abstract

Green Corridors are a European concept denoting long-distance freight transport corridors where advanced technology and co-modality are used to achieve energy efficiency and reduce environmental impact. Green corridors consider all kind of agents acting in the door-to-door co-modality chains, including ports. Carbon footprints (CF) provide companies, customers and other agents with information related to greenhouse gas (GHG) emissions from the supply chain of products, identifying key points, potential risks and opportunities of improvement. Its application in both the logistic networks and all modes of transport would allow for the creation of green corridors and sustainable motorways of the sea. This paper describes the method composed of financial accounts (MC3) used to estimate the CF of a port. The paper shows the effects of the method on the Port of Gijón (PAG), which steers the existing Gijón/Nantes/Saint-Nazaire motorway of the sea. The extension of the system to all nodes of the shipping line and other transport modes will lead in the long run to a carbon-neutral green corridor. Our findings show the importance of looking at indirect emissions in order to become a carbon neutral port.

Keywords: motorways of the sea; carbon footprint.

1 Corresponding author. Email: [email protected]

2

1. Introduction

Nowadays, the control of greenhouse emissions is a key tool in order to measure the

environmental impact of organizations and freight. The application of this measure at all

points and for every logistic agent involved in a green supply chain (Yenning and Sheu

2009; Zhu et al. 2008) would make possible to plan the reduction of emissions in the

chain, aiming to minimize emissions in the whole network. Thus, the main objective of

the so-called green corridors, reducing the emissions of freight passing through the net,

would be achieved. Such corridors are being promoted by the Directorate- General

Energy and Transport of the European Commission.

More concisely, since the publication of the White Book on Transport in 2001,

and its intermediate revision in 2006, the role of co-modality to achieve transport

sustainability in the EU has been strongly stressed (McEldowney et al., 2005). One of

the measures adopted was the European Motorways of the Sea, because they may

constitute key shipping routes between Member States, with regular services of high

quality, which combined with other transport modes can offer a more sustainable

alternative to the pure road transport.

With a ten year perspective, looking at the European Commission forecasts

about the success of the motorways of the sea, the objectives settled have not achieved,

because there are only a few motorways of the sea on use (the Gijón-Nantes is one of

them).

However, despite this modest development further to the measures designed to

achieve this aim, the European Commission adopted in October 2007 the so-called

“Freight transport Logistics Action Plan” to improve both efficiency and sustainability

3

of Freight Transport. One of the Plan’s proposals was the promotion of Green

Corridors, defined as an integrated transport concept where Short Sea Shipping, rail,

inland waterways and road, complement each other to enable the choice of an

environmentally friendly transport (European Commission Studies 2009).

Green supply corridors can be achieved through the appliance of strategies of

continuous emission reduction in a) ports b) vessels of the shipping line c) logistic

agents d) the other modes of transport up to the client. This allows establishing

connections with the industry which are aimed to extend the chain up to the extraction,

production and processing centres. The establishment of networks and alliances based

on sustainability seems to be an appropriate strategy to accomplish the objectives of the

Product Integrated Policy, which is one of the pillars of the Sustainable Development

Strategy of the European Union1.

The ecological and environmental added value of green corridors is derived

from its ability to provide an optimal framework for all kind of agents acting in the

door-to-door co-modality chains to achieve common arrangements and objectives (Van

Agtamaal and Swahn 2009).

As this is a newly established tool, the following information provides a short

summary of some specified milestones related to Green Corridors (Mulder 2009).

2006: Green Corridors idea developed in action group ENT7 from ERANET

Transport project.

2007, 3rd July: Green Corridors idea presented to Ben van Houtte/ DG Tren at

Dutch Transport Ministry.

2007, October: EU Action plan for Green Freight Corridors.

2007, November: Several Green Corridor DG Tren calls in FP7.

2008, December: Green Corridors in ENT+ proposal, cancelled 2009.

4

2009, October: Swedish Green Corridor Programme/ Initiative.

2009, 9th December: Green Corridor Conference, preparing for 2010 FP7 calls.

Events such as Green Port Logistics 2010, or Stockholm 2010, deal exclusively with

carbon management, as there is a growing demand by all sectors of the logistics supply

chain to reduce carbon emissions and implement a carbon neutral strategy. The success

of this initiative is not only determined by the level of investment but also by the

agents’ compromise and effort as well as by their ability to work together (European

Commission 2009).

One of the measures taken were the motorways of the sea. One way to promote the

motorways of the sea and to the stakeholders involved, is becoming more competitive

and contributing to their development, through the use of sustainability measures and

“carbon zero” strategies. These measures shall be implemented in ports, terminals,

shipping lines and other logistics agents. It is also one of the necessary steps for the

logical development of the motorways of the sea to the green corridors.

Therefore, it is not surprising that some of the most relevant ports have already

adopted this strategy. For example, the Port of New York has determined carbon direct

emissions derived from their activities and operations and found out they amount to

298,000 CO2 Tons2.

The Port of Oslo also determined its emissions on the basis of the ISO 14064-1

standard, by including direct emissions (456 t), indirect energetic emissions (49 t) and

other indirect emissions related to subcontracts, business and trips from home to work

(199 t). The total amounts to a 704 t CO2/year. Through the same method, the Port of

Rotterdam showed direct emissions of 8,960 t CO2/year, indirect energetic emissions of

7,230 tCO2 and other indirect emissions of 20,100 t (total: 36,290 CO2/year) (WPCC

2008).

5

These ports have already addressed strategic plans to reduce emissions. As an

example of this, both the port and the city of Rotterdam have carried out an ambitious

plan to diminish CO2 emissions –The Rotterdam Climate Initiative- the first phase of

which will end in 2025.

The European Sea Ports Organization (ESPO) has included these

recommendations in its latest statements, for instance, in the Policy statement on

reduction of Green House Gas emissions in port, of 15 May 2009, by means of which,

under the umbrella of the International Association of Ports and Harbours (IAPH), it

coordinates the regional implementation of the World Ports Climate Declaration

(WPCD) and endorses the technical developments of the projects of the Worlds Ports

Climate Initiative (WPCI), which is the follow-up initiative of WPCD. The

recommendations made by the ESPO on this issue are the following: 1) calculation of a

port’s CO2 footprint; 2) reduction of CO2 emissions from port operations and

development; 3) reduction of CO2 emissions by promoting usage renewable energy; 4)

reduction of CO2 emissions of hinterland transport; 5) reduction of CO2 emissions of

ocean going shipping (ESPO 2009).

The Climeport Project and other recent initiatives have joined together several

important Mediterranean ports such as Valencia (Spain), Algeciras (Spain), Marseille

(France), El Pireo (Greece), Koper (Slovenia) and Livorno (Italy), in order to determine

their Carbon Footprint and establish measures to reduce the impacts of climate change

(Climeport 2009).

The success of these initiatives depends on the existence of robust tools for

assessing greenhouse gas emissions from green corridors. This paper proposes the

application of Carbon Footprint to ports, vessels, maritime lines, agents and others

modes of transport that configure green corridors and motorways of the sea with the aim

6

to continuously reduce greenhouse gas (GHG) emissions until they become carbon

neutral3.

We describe one of the available methodological approaches for assessing

Carbon Footprints of organizations, goods, and services, the method composed of

financial accounts (MC3). The main goal of this study is to clarify how to apply this

method to estimate the carbon footprint of a part of a green corridor showing what kind

of results are available with this methodological approach. The paper includes a case

study, assessing the carbon footprint of the Port of Gijón (PAG), which steers the

existing Gijón/Nantes/Saint Nazaire motorway of the sea. This case study permits

checking the utility of the obtained information at this level, being a first step in order to

apply this method to a whole green corridor.

2. The Carbon Footprint: Material and Methods

2.1 From ecological footprint to corporate carbon footprint

The ecological footprint (EF) is a well-known index designed at the beginning of the

90’s by Mathis Wackernagel and William Rees to determine biological resources use

and waste generation in terms of the appropriate ecosystem surface, comparing them

with the biosphere’s capacity in a certain year (Wackernagel and Rees 1996).

Present definitions remark that the ecological footprint can be applied not only

to individuals and populations, but also to different types of activities such as goods and

organizations (Global Footprint Network 2007). A large number of works (e. g.

Wackernagel and Rees, 1996, Ewing et al. 2010) lay out in detail index’s concept,

theoretical basis of the calculation method, objectives, use and evolution over time. In

addition, there is a considerable debate, with regards to both the potential of the index

and the interpretation of the corresponding results (e.g., Van der Bergh and Verbruggen

1999, Rees 2006, Fiala 2008 or Kitzes et al. 2008, Ewing et al. 2010).

7

The carbon footprint (CF)concept is far more recent and much less defined than

the EF’s. The carbon footprint is orphan, which allows the existence of different

interpretations of the index. Some of the main differences are related to: i) gases which

emissions are present in the index; ii) the relationship with analysis of the ecological

footprint.

In the first case, some studies consider that the CF should include several

greenhouse gases, so it should be expressed in CO2equivalent tones (Doménech 2004,

Carbon Trust 2007, BSI 2008),while others (Global Footprint Network 2007,

Wiedmann and Minx 2008) prefer to stick to only one gas, CO2.

On the other hand, applying the index to certain realities, such as organizations

and their products, brings up new issues that should be taken into account. Several

studies recommend limiting the footprint of goods and services to the direct emissions

of the company which generates them. In other cases, indirect emissions are also

considered, by including the emissions of the company’s chain of suppliers (Wiedmann

and Minx 2008).

All these matters cause important differences in the proposed definitions. For

example, Global Footprint Network, reference body for ecological footprint analysis,

provides the following definition of CF: "The demand on biocapacity required to

sequester (through photosynthesis) the carbon dioxide emissions from fossil fuel

combustion" (Global Footprint Network 2007, p. 1). The definition by Carbon Trust is

much wider as it includes: “the total emission of greenhouse gases in carbon equivalents

from a product across its life cycle from the production of raw material used in its

manufacture, to disposal of the finished product (excluding in-use emissions)” (Carbon

Trust 2007, p.4).

8

For this study, it has been considered that the determination of the ecological

footprint, specially the carbon footprint of organizations, companies and their related

goods and services, presents special features which have to be examined (Carballo-

Penela and Domenech 2010). The expressions corporate ecological footprint (CEF) and

corporate carbon footprint (CCF) have been chosen as these clearly show that the

footprint estimated refers to the enterprises field. The Kyoto Protocol establishes goals

for emission reduction for six gases: CO2, N2O, CH4, HFC, PFC and SF6. The inclusion

of emissions of these gases in the CCF analysis increases their utility for those

companies that have goals of emissions linked to this and post-Kyoto Protocol

international agreements.

Finally, CEF and CCF should not be limited to direct or on-site effects, as it is

useful to take into account the emissions along the whole chain of suppliers of the goods

and services produced. This assumption i) prevent the index from excluding relevant

impacts ii) promote joint decision making processes of companies which belong to the

same chain of suppliers and which aim to reduce product footprint and search for new

business opportunities iii) make possible for the indicator to be used in order to create

an ecolabel. This ecolabel informs the final consumer about the surface/emissions which

have been used up to the time of purchase iv) the approach applied is in line with the

integrated product policy, one of the main bases of the European Sustainable

Development Strategy (EC, 2006).

2.2 Calculation methods for the estimation of the CCF

During the last decade, several methodologies aimed to calculate the carbon footprint

have been developed. Unlike simple methods, they do not only estimate the emissions

produced by certain activities but in most cases they are intended to estimate all or most

company emissions on the basis of a single calculation method.

9

The achievement of a standard method, applicable to different types of activities

and different types of companies (size, activity, etc), is a key issue due to the

requirements of both the Kyoto Protocol and the post-Kyoto period, for which there is

still no consensus. The existing standards for information concerning generated

emissions (WRI/WBCSD 2004, AENOR 2006 etc) do not solve the lack of

standardization, as they do not set specific guidelines for the calculation. The ecological

footprint standards drawn up by Global Footprint Network do not solve the problem

either, as they allow the use of different methodologies (Global footprint Network

2009).

The use of input-output techniques to determine the CCF (Wiedmann and

Lenzen 2009, Wiedmann et al. 2009), the Publicly Available Specification (PAS) 2050

(BSI 2009, Carbon Trust 2008a) or the the method composed of financial accounts

(MC3) (Doménech, 2004, Carballo-Penela and Doménech 2010) are some of the most

relevant methodological approaches. Next, the method applied in this paper, the MC3 is

briefly described.

2.3 The method composed of financial accounts (MC3)

The MC3 was developed between 2000 and 2002 by biologist J. L. Doménech. The

original method, including guidelines for assessing the CEF-CCF of organizations

(Carballo Penela and Doménech, 2010), was published by the Spanish Association for

Standardisation and Certification (AENOR) (Doménech 2007). This method has been

improved through the cooperation with five Spanish universities, and the results of this

work have been published in several papers (e.g., Marañon et al. 2008, Carballo-Penela

and Doménech, 2010, Coto et al. 2010).

10

Carballo-Penela (2009, 2010) has recently developed a method to estimate the

CEF-CCF of goods and services along the suppliers’ chain, from the raw materials to

the final consumer. In this paper it is described how the MC3 can be used to determine

the organizations’ footprint, the one used for the members of a green corridor, focusing

on the Gijón Port Authority.

The information to determine the CCF through the MC3 is mainly obtained from

accounting documents such as the balance sheet and the profit and loss account, so all

activities linked to each organization are perfectly defined. The MC3 calculates the

footprint of all goods and services included in the accounts, waste derived from the

acquisition of such goods and services and space occupied by the company, premises

which are included in the accounts4.

The CCF is estimated on the basis of the calculation sheet, which works as a

consumption land use matrix (CLUM) which applies the consumption of goods and

services needed by companies (Carballo-Penela et al., 2011).

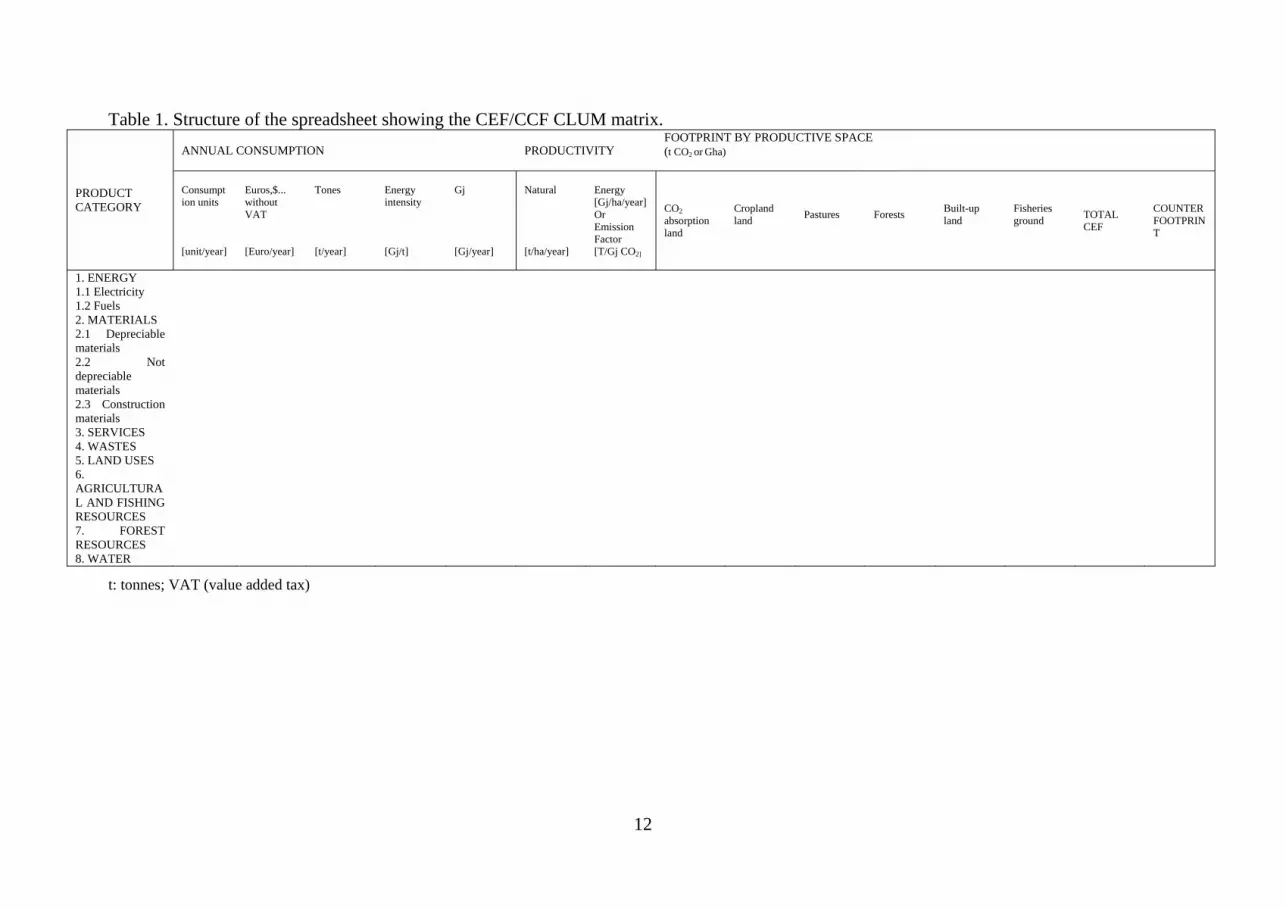

The rows of the CLUM matrix show the footprints for each category of

good/service consumed. Columns include, amongst several other elements, relevant

categories of productive space, according to the ecological footprint analysis (see Table

1).

Columns are divided in 6 groups. The first group (column 1) stands for the

different types of consumables. They are classified in 8 main categories, energy

consumption, divided in two subcategories (electricity and fuels), materials, subdivided

in 3 subgroups (depreciable material, non-depreciable materials and construction

materials), services, residues and waste, land use, agricultural and fishing resources,

forest resources and water. Each category can include as many products as desired.

11

The second group, columns 2-6, shows the consumption of each product, in

specific units. The first column relates to product characteristics. The second column

shows consumption values in monetary units, while the third one gives consumption in

tons. The fifth column shows the amount of energy per consumption unit, in gigajoules

(Gj), by means of multiplying the tons of each product (third column) by the amount of

energy/ton used to produce it (Gj/t) (forth column).

The energy intensity factors show the amount of energy used to produce all the

products included in the CLUM matrix, considering a standard life cycle. At present,

the main sources used are Wackernagel et al. (2000), Simmons et al. (2006) and

European Commission (2007).

The third group of columns (columns 7 and 8) shows good productivity. Column

7 deals with natural productivity, which is used to calculate the CEF, in tons per

hectare. Column 8 shows energy productivity, in Gj per hectare. Energy productivity

shows how many tons of each fuel were needed to generate the CO2volume which can

be absorbed per hectare on an annual basis, applying an absorption rate per hectare/year

of 5.21 t CO2/ha/year (IPCC 1997)5.

The fourth group includes six columns (9-14), which give a breakdown of the

footprint by productive spaces. Those are the ones used to calculate the population

ecological footprint (CO2 absorption land, Cropland, Pastures, Forest, Built-up land and

Fisheries ground).

12

Table 1. Structure of the spreadsheet showing the CEF/CCF CLUM matrix.

PRODUCT CATEGORY

ANNUAL CONSUMPTION PRODUCTIVITY FOOTPRINT BY PRODUCTIVE SPACE (t CO2 or Gha)

Consumption units [unit/year]

Euros,$... without VAT [Euro/year]

Tones [t/year]

Energy intensity [Gj/t]

Gj [Gj/year]

Natural [t/ha/year]

Energy [Gj/ha/year] Or Emission Factor [T/Gj CO2]

CO2 absorption land

Cropland land

Pastures

Forests

Built-up land

Fisheries ground

TOTAL CEF

COUNTER FOOTPRINT

1. ENERGY 1.1 Electricity 1.2 Fuels 2. MATERIALS 2.1 Depreciable materials

2.2 Not depreciable materials

2.3 Construction materials

3. SERVICES 4. WASTES 5. LAND USES 6. AGRICULTURAL AND FISHING RESOURCES

7. FOREST RESOURCES

8. WATER

t: tonnes; VAT (value added tax)

13

Finally, the last column shows the counter footprint. The concept of counter

footprint is based on the fact that even though it is desirable for companies and

organizations to reduce their footprint by becoming more efficient and reducing their

consumption, it is also positive for companies to invest in natural capital. Thus, natural

capital investments reduce their footprint. In such a way, the index encourages the

private sector to preserve natural areas, which is positive in terms of sustainability. By

deducting the counter footprint from the CCF the net CCF is obtained (Carballo-Penela

et al., 2011).

The consumption of both goods and services and energy and natural productivity

allows calculating the CEF-CCF for acquired goods, as shown in figures 1 and 2.

Figure 1. Energy Footprint.

Figure 2. Natural Footprint.

The footprint of non biotic goods is due to the energy used in their production.

As regards the consumption of natural and biotic resources, which can be transformed

into surface dividing tons consumed by natural productivity, it does also include the

energy used in order to produce them, which is determined by applying an energy

intensity factor to the consumption of agricultural, fisheries and forestry resources.

The focus will be now placed on the CCF calculation. The latter includes not

only the CO2 emissions generated by the company premises or by its means of

productions (for example those derived from solid-fuel consumption) but also emissions

generated by the energy used in the production of goods and services acquired by the

14

company, independently of whether or not they are used in the production process. In

the latter case the Gj used in the production of a certain good (Figure 1) is transformed

into CO2 emissions by applying emission factors (t CO2/Gj) from The

Intergovernmental Panel on Climate Change6 (IPCC 1997).

The CCF includes emissions from wood and derived products, which are linked

to the “Forests” as area, as the emissions which are not absorbed by the forest area

needed to produce the wood included in the demanded products are also considered. In

the next future it will include all the greenhouse gas emissions subject to the Kyoto

Protocol able to be transformed into CO2 equivalent tons by applying the Global

Warming Potential7 (GWP) with a 100 year horizon (IPCC 2007).

2.3.1 Differences between the CCF calculation methods.

Despite sharing the same objective, the existing CCF calculation methods use different

means to reach it.

Table 2. The MC3 and other methodological approaches

Table 2. The MC3 and other methodological approaches

Concept Input-Output Techniques

PAS 2050

CBA MC3

Calculation method Input-output analysis/

Process LCA

Component-based approach/LCA

MC3 is based on Compound-Method

Activities included in CCF All the activities by an organization

All the production activities

Relevant activities

All the activities by an organization

Organization source of information

Basically, finacial accounts

Maps of processes/ LCA inventories

Basically, finacial accounts

Basically, financial accounts

Transformation of financial information into mass unit data

No needed. The method uses monetary input-output coefficients

No needed Needed. No explicit method

Needed. Explicit method

Equivalence and yield factors Yes No No Yes Is the required software accessible?

No No No Yes

Source: Carballo-Penela et al., (2011).

15

These methods differ on issues such as the activities that must be included in the

CCF, the use of equivalence and performance factors, energy intensity and related

conversion factors applied, or how to convert consumption expressed in monetary units

into physical units (Table 2). In any case, even if consensus was achieved on these

issues, the different nature of the calculation methods would lead to different results.

All these methods show strengths and weaknesses, but it has been not

considered expedient to carry out a detailed analysis in this paper. For the aim of this

work, it is more useful to stress the reasons which favor the use of MC3 at an

organization level (Carballo-Penela et al., 2009; Carballo-Penela and Doménech, 2010;

Carballo-Penela et al., 2011).

The MC3 is a comprehensive method, which includes the footprint of goods and

services consumed by organizations, independently of whether or not they are

linked to the production process. The CCF related to waste is also included by

taking into account the emissions generated by its treatment and removal

processes.

It is based on the composed method developed by Wackernagel and Rees, a

solid technique well known by ecological footprint researchers.

It is a technically viable method, as it is not necessary to possess a specific

knowledge. Any person able to use a calculation sheet can determine CCF.

The MC3 is a transparent method. Both the calculation sheet and the information

necessary to calculate the CCF, including energy intensities and emission

factors, are available at: http://www.huellaecologica.com, which includes all

sources of information.

16

It is a flexible method. The calculation sheet allows for the possibility of adding

or modifying the factors used, by adapting to the characteristics of different type

of companies.

It is a complete method, which collects the footprint from the consumption of all

goods and services and wastes generated by a company, including direct and

indirect emissions.

The method is constantly being updated and improved by a working group

formed by members of 5 Spanish universities which is in charge of problem-

solving. The MC3 approach has been recognized by the Spanish Observatory for

Sustainability as a valid methodology for assessing and reducing GHG

emissions arising from companies under the frame of the Spanish GHG

Voluntary Reduction Agreement.

At present, the method can be applied to both organizations and their products,

having a great potential on products and services ecolabelling issues.

There are also some remarkable advantages for supply chain analysis:

The footprint of every member of a supply chain, e.g. a green corridor, is assigned to the

produced goods by that organization. The fact that each company covers a complete

phase of the chain 1) implies lower economic and time costs; 2) clearly delimits the

activities under analysis, favouring the collection of information obtained from each

company; 3) avoids dealing cut-off criteria.

The theoretical presentation of the method requires determining the participants in the

supply chain. In practice, every company obtains the environmental information of the

purchased goods/services from their suppliers. This fact makes possible the integration

of the environmental information in the market in a practical way, thus avoiding high

communication costs (Carballo Penela et al., 2011).

17

3. Results

The MC3 is applied to the Port Authority of Gijón from 2004 to 2008. Located on the North coast of Spain, the Port of Gijón (PAG) is part of the state-owned

Spanish ports and harbours system is managed by 28 Port Authorities. The Port of Gijón

is the Spanish leader in moving bulk solids, mainly linked to coal, iron and cement, with

the movement of goods, around 20 million tons. Figure 3 shows the evolution of the

main traffics between 2004 and 2008.

Figure 3. Evolution of PAG’s traffics. Period 2004 to 2008.

The Port of Gijon is a part of the Gijon-Nantes motorway of the sea, being the only

European port present in the SuperGreen project (see endnote 1). The resulting footprint

is derived from both solid-fuel consumption carried out by the organization and

emissions generated by the electricity consumed in its premises as well from those

derived from both the acquisition of goods and services and waste generated by the Port

Authority.

Table 3. Evolution of PAG’s nets CCF and CEF. Period 2004 to 2008. Indicador 2004 2005 2006 2007 2008 Income(€) * 35,948,895 40,970,804 38,752,272 39,914,840 39,201,740 Goods moved (T) 20,060,466 21,790,871 20,488,293 20,782,000 19,331,000 Net CCF (tCO2/year) 30,426 32,097 30,194 29,485 32,408 Net CEF (Gha/year) 5,298 6,693 6,182 6,167 6,148

* Net turnover

18

Table 3 show that the net CCF in 2004 is 30,426 tCO2, and it follows the following

pattern: it shows a 5.5% decrease from 2004 to 2005, it decreases by 5.9% in 2006 and

by 1.2% in 2007, to subsequently increase by 8.6% in 2008. Table 3 also shows the

evolution of the net CEF, which increases considerably from year 2004 to 2005

(26.3%), decreases by 7.6% in 2006, 0.24% in 2007 and 0.3% in 2008.

Table 4 shows the breakdown of the PAG’s net CCF by consumption categories.

The greatest port impact, which took place in 2008, with an 81.8% increase in the gross

CCF, stands for materials’ footprint (70.2% of them being building materials and 11.6%

the rest of the materials). Electricity footprint follows (11.7%), then services and service

contracts, fuel (1.7%), forest resources and water (1.6%), agricultural resources (0.5%)

and waste (0.08%).

Table 4. Evolution of PAG’s CCF broken down by categories (t CO2/year)

Category 2004

2005

2006

2007

2008

Electricity 5,040 (16.5%)

3,909 (12.2%)

3,893 (12.9%)

3,815 (12.8%)

3,801 (11.7%)

Fuels 676 (2.2%)

705 (2.2%)

839 (2.8%)

578 (1.9%)

550 (1.7%)

Materials 4,036 (13.2%)

3,916 (12.2%)

3,795 (12.5%)

3,728 (12.5%)

3,756 (11.6%)

Building materials 16,281 (53.4%)

19,000 (59.1%)

19,113 (63.2%)

19,411 (64.9%)

22,772 (70.2%)

Services and contract services 786 (2.6%)

1,447 (4.5%)

1,197 (4.0%)

1,247 (4.2%)

863 (2.7%)

Waste 1.143 (3.7%)

1.250 (3.9%)

10 (0.0%)

59 (0.2%)

27 (0.1%)

Agricultural resources 410 (1.3%)

521 (1.6%)

449 (1.5%)

490 (1.6%)

159 (0.5%)

Forest resources and water 2,113 (6.9%)

1,401 (4.4%)

950 (3.1%)

569 (1.9%)

532 (1.6%)

Gross Footprint 30,485 32,148 30,245 29,896 32,460 Counter Footprint 59 51 51 51 52 Net Footprint 30,426 32,097 30,194 29,845 32,408

The net CCF increased in year 2005, due to a considerable rise in the port

activity and to the corresponding rise in the movement of goods, for which it is

necessary to use more electricity, fuels, materials and services, etc. A record 21.8

19

million tons of goods moved was reached during 2005, and the extension of port

facilities (up to date, the largest investment in a public work carried out in Asturias)

began.

Nevertheless, during year 2006 the Port Authority reached again around 20

million tons of goods, similarly to previous years, which has the effect of reducing

slightly the footprints in terms of ecoefficiency (figures 4 and 5). Due to this fact,

during 2006 a reduction of the net CCF in several consumption types (electricity,

materials, services, agricultural resources, forest resources and water) was registered, in

addition to the considerable cut in solid-fuel production, consequence of the separation

of vessels and other users of the port, which were once included. During 2007 good

consumption restraint remained and so did the footprint which even decreased slightly.

During year 2008 the restraint on consumption remained for almost every

category and it even decreased for some of them, such as agricultural resources.

Nevertheless, there is an increase in building materials, due to the execution of several

works, which increases the footprint compared to the previous year.

As it has already been pointed out, this absolute values are linked to port activity

so comparison between ports must be carried out in relative terms, that is, in terms of

ecoefficiency. The latter is determined by dividing business activity (in terms of

business or amount of goods) by the environmental impact (net CCF). Figures 4 and 5

show the results of these ecoefficiency indexes.

Even though ecoefficiency has improved in the period 2004-2007 (better

incomes and more goods moved per carbon footprint unit), it worsens in 2008 in terms

of freight. The reasons behind this fact are to be found in an increase of emissions in

absolute terms due to building works, which is not corresponded by an increase in

income or goods moved, which in fact, decreased. During year 2008, there is a decrease

20

of 100 tons of goods moved per ton of CO2 and of 127 Euros less than in 2007 (Figures

4 and 5).

Figure 4. Ecoefficiency in terms of annual income per ton emitted CO2 (€/tCO2)

Figure 5. Ecoefficiency in terms of goods moved annually per ton emitted CO2 (t/tCO2)

4. Discussion

The analysis of the CCF in the aforementioned port shows some interesting results:

From 2004 to 2006 PAG emissions increase/decrease as the traffic of goods of

Port Authorities increases/decreases (Table 3). This does not mean that traffic

has to be reduced in order to reduce the CCF. It actually means that issues such

as promoting transport efficiency, clean technologies, etc, would lead to reduce

21

the CCF, even when traffic increases as it happens from 2006 to 2007. The CCF

is increased 2008 due to building works for new facilities for the port.

As regards the PAG for the relevant period, the importance of the footprint

derived from both materials and building materials becomes evident, as all of

them show significant annual investments (Table 4). This impact is not yet

declared in the bottom line reporting by almost any port.

The net CCF derived from direct emissions (those derived from fuel

combustion) is insignificant. It represents 1.7% of the total in 2008 (Table 4).

Some carbon footprint calculation methods only include this category of

consumptions, which shows that existing methodologies are still incomplete.

The waste footprint is even more insignificant in relation to the total, 0.1% in

2008 (Table 4), which demonstrates the need to improve and extend through the

consumption footprint the current waste-oriented port environment management.

The minimum CCF of the period reaches 19,331 tCO2 (Table 3). That means that

the measures set in place to reduce CCF and improve ecoefficiency in the

relevant period are not sufficient to become a carbon neutral port. Such

measures consisted in installing solar panels for hot sanitary water (HSW) in the

logistic area; solar energy for channel buoying; presence detectors in multiple

use buildings; heating and cooling regulation; replacing luminaries; dock

lighting regulation; replacing old transformers; replacing boilers; detecting water

leaks in the network, investments aimed to reduce water network losses; switch

off of non-operating premises; purchase of two electrical vehicles; improvement

of energy saving in buildings (reduction of 17% in the central multi-use

building). These results show that both stronger actions and more significant

22

investment should be carried out to achieve a lower footprint and higher

ecoefficiency.

5. Conclusions

Carbon neutral strategies will be key to the success and differentiation of green

corridors. ESPO joins the international demand for carbon emission reduction and

promotes measures aimed to achieve a 20% carbon footprint reduction by year 2020.

Port Authorities, local and regional governments, logistic agents and port stakeholders

should also contribute to it.

Nowadays, different standards like ISO 14040, ISO 14044 or Global Footprint

Network Standards, contain guidelines for the assessment of the CCF of products and

organizations. These standards provide sufficient flexibility to allow different

approaches to suit the specified requirements they contain, existing relevant differences

in terms of the calculation method and some assumptions involved in the estimation of

the indicator.

This paper describes one of the existing approaches the method composed of

financial accounts (MC3). MC3 offers useful information for sustainable development,

carbon management of organizations and sustainable consumption, being a flexible,

transparent, and easy-to-apply method. MC3 can be applied to motorways of the sea and

also to green corridors, fitting the needs of carbon footprint calculation of ports, means

of transport and other agents of the logistic network. We have chosen a port, the Port

Authority of Gijon, included in the Gijón/Nantes/Saint-Nazaire motorway of the sea and

the green corridors SuperGreen project has been chosen, as an example of how carbon

footprint can be calculated for all the stakeholders involved in it.

Our findings show the importance of looking at indirect emissions in order to

become a carbon neutral port. Emissions from electricity, materials, building materials,

23

services and contract services, wastes, agricultural resources and forest resources and

water reaches an average of 30,324 tCO2 in the studied period (97.84% of the CCF).

Several researchers also remark the importance of indirect CCF (Carballo Penela, 2010;

Wiedmann et al., 2009).

Measures to reduce both fuels and electricity emissions, commonly considered

by other CCF methodological approaches, are needed but only affect to 15.38 % of the

CCF in the studied period. In other words, carbon neutrality requires measures beyond

reducing electricity and fuel emissions. In this context, completeness of methods for

carbon footprinting is a key factor in order to implement carbon Neutral strategies.

Regarding PAG results, this port has reduced emissions from 2004 to 2007 in both

absolute and relative terms. Building works for new port facilities have increased the

CCF in 2008. However, building materials footprint should be lessen when new

facilities are finished. A bigger port will probably move more goods, being positive in

terms of ecoefficiency.

PAG should pay attention to absolute emissions, since is quite far from being a carbon

neutral port. Efficiency in the use of materials and replacing the electricity supplier by

one producing renewable energy would contribute to the reduction of the CCF of the

port. The footprint of materials and building materials used buy PAG would also be

decreased if the ecolabelling systems supply information on the CCF of each material.

In this case, this port could choose those with a lower footprint.

24

Appendix: Acronyms and Abbreviations

CF: Carbon footprintCCF: Corporate carbon footprint

CEF: Corporate ecological footprint

CLUM: Consumption land use matrix

EF: Ecological footprint

ESPO: European sea ports organization

Gha: Global hectare

GHG: Greenhouse gas

GWP: Global warming potential

HSW: Hot sanitarywater

IAPH: Association of ports and harbours

IPCC: Intergovernmental Panel on Climate Change

MC3: Method composed of financial accounts (from Spanish “Método compuesto de

las cuentas constables”)

PAG: Port of Gijón (from Spanish “Autoridd Portuaria de Gijón”)

UNEP: United Nations environment programme

WMO: World meteorological organization

WPCD: World ports climate declaration

WPCI: World ports climate initiative

WRI: World resources institute

WBCSD: World business council for sustainable development

25

Notes section

1 Initiatives as SuperGreen Green corridors Project promote the Green Corridors concept in Europe in order to improve energy efficiency and to reduce the environmental footprint of the transport sector. Launched at the beginning of 2010, the project SuperGreen is a key tool to assist the European Commission with developing the Green Corridor idea.

2 The Port of New York was one of the first ones to set the objective “carbon neutral” for 2010, and reduce its environmental footprint through both an ambitious strategic plan and an aggressive plan of investments which amounts to several million dollars in the next few years (Port Authority of New York and New Jersey 2008).

3 That is having a zero carbon footprint by balancing a measured amount of carbon released with an equivalent amount sequestered or offset.

4 That is the origin of the name “method composed of financial accounts”. Provision of information on certain topics (waste generation, land use, etc) linked to other company departments can be necessary in cases when such information does not appear in the accounts.

5 Starting from 2010, a 3.67 tCO2 /ha/year rate will be applied (IPCC 2007). 6 The Intergovernmental Panel on Climate Change (IPCC) is the leading international body for

the assessment of climate change. It was established by the United Nations Environment Programme (UNEP) and the World Meteorological Organization (WMO) to provide the world with a clear scientific view on the current state of knowledge in climate change and its potential environmental and socio-economic impacts.

7 Global-warming potential (GWP) is a relative measure of how much heat a greenhouse gas traps in the atmosphere. It compares the amount of heat trapped by a certain mass of the gas in question to the amount of heat trapped by a similar mass of carbon dioxide.

References

AENOR, 2006 UNE-EN ISO 14044: 2006. Gestión ambiental. Análisis de ciclo de

vida. Requisitos y directrices. Madrid: AENOR Ediciones.

British Standards Institute (BSI), 2008. PAS 2050: 2008. Specification for the

assessment of the life cycle greenhouse emissions of goods and services. London:

British Standards Institute.

Carballo-Penela, A., 2009. A pegada ecolóxica de bens e servizos: desenvolvemento dun

método de cálculo e aplicación ao ciclo de vida do mexillón en conserva en Galicia.

Thesis (Ph.D).University of Santiago de Compostela.

26

Carballo Penela, A., Doménech, J.L., 2010. Managing the carbon footprint of products:

the contribution of the method composed of financial statements (MC3). International

Journal of life Cycle Assessment, 15, 962-969.

Carballo Penela, A., Doménech, J.L., García-Negro, M.C., 2011. Environmental supply

chain management with MC3: the case of canned mussels in Galicia (Spain). Journal of

Cleaner Production (in revision)

Carballo-Penela, A., M.C. García-Negro, Doménech, J.L., 2009. A methodological

proposal for the corporate carbon footprint: an application to a wine producer company

in Galicia (Spain). Sustainability, 1, 302-318.Carbon Trust, 2006. Carbon footprints in

the supply chain: the next step for business. London: The Carbon Trust.

Carbon Trust, 2007. Carbon footprint measuring methodology 1.3. London: The Carbon

Trust.

Climeport, 2009. Second Technical meeting of Climeport. Available from:

http://www.climeport.com/en/documentation/doc_details/11-second-technical-meeting-

of-the-climeport-project-in-pireo-greece.html. [Accessed 6 Dec 2010]

Coto-Millán, P., Mateo-Mantecón I., Doménech J.L, Carballo-Penela A., Pesquera

M.A., 2010. Evaluation of Port Externalities: The Ecological Footprint of Port

Authorities. In: P. Coto-Millán, M.A. Pesquera, J. Castanedo, eds. Essays on Port

Economics. Berlin: Springer Physica-Verlag 323-340.

Doménech JL 2004. Huella ecológica portuaria y desarrollo sostenible. Puertos, 114,

26-31.

Doménech, J.L., 2007. Huella ecológica y desarrollo sostenible. 2nd ed. Madrid:

AENOR Ediciones.

27

European Commission, 2006. Making product information work for the environment.

Final Report of the Integrated Product Policy Working Group on Product Information.

Brussels: European Commission.

European Commission, 2007. Whel-to-wheels Analysis of Future Automotive Fuels and

Powertrains in the European Context. Brussels: European Commission.

European Commission, 2009. Evaluation of the Common Transport Policy (CTP) of the

EU from 2000 to 2008 and analysis of the evolution and structure of the European

transport sector in the context of the long-term development of the CTPReview of the

Common Transport Policy. Appendix A. Task 1 reports (on specific policy areas). Task

1.3. Logistics, inter- and co-modality. Brussels: European Commission.

European Commission Studies, 2009. Evaluation of the Common Transport Policy

(CTP) of the EU from 2000 to 2008 and analysis of the evolution and structure of the

European transport sector in the context of the long-term development of the CTP.

Brussels: European Commission.

European Sea Ports Organization (ESPO), 2009. Policy statement on reduction of Green

House Gas emissions in ports [online]. Available from:

http://www.espo.be/downloads/archive/ba3fecf0-7a1a-4c8f-9bbf-06805ea34022.pdf

[Accessed 20 Feb 2010]

Ewing, B., Reed, A., Galli, A., Kitzes, J., Wackernagel, M., (2010) Calculation

Methodology for the National Footprint Accounts, 2010 Edition. Oakland: Global

Footprint Network.

Fiala, N. 2008. Measuring sustainability: why the ecological footprint is bad economics

and bad environmental science. Ecological Economics, 67, 519–525.

28

Global Footprint Network, 2007. Footprint term glosary. Oakland: Global Footprint

Network.

Global Footprint Network, 2009. Ecological Footprint Standards 2009. Oakland:

Global Footprint Network.

IPCC, 1997. Revised 1996 IPCC Guidelines for National Greenhouse Gas Inventories

reporting Instructions, 1997 [online]. Available from: http://www.ipcc-

nggip.iges.or.jp/public/gl/invs1.htm. [Accessed 23 March 2009].

IPCC, 2007. IPCC Fourth Assessment Report (AR4) Changes in Atmospheric

Constituents and in Radiative Forcing [online]. Available from: http://ipcc-

wg1.ucar.edu/wg1/Report/AR4WG1_Print_Ch02.pdf. [Accessed 26 Jan 2009]

Kitzes, J., Galli, A., Riz, S.M., Reed, A., Wackernagel, M., 2008. Guidebook to the

National Footprint Accounts: 2008 Edition. Oakland: Global Footprint Network.

Marañón, E., Iregui, G., Doménech, J.L., Fernández-Nava, I., González-Arenales, M.,

2008. Propuesta de índices de conversión para la obtención de la huella de los residuos

y los vertidos. OIDLES, 1, 56-72.

McEldowney, M., Ryley, T., Scott, M., Smyth, A., 2005. Integrating Land-use Planning

and Transportation in Belfast: A New Policy Agenda for Sustainable Development?.

Journal of Environmental Planning and Management, 48, 507-526.

Mulder, F., 2009. Advanced technologies in green transport corridors. The Green

corridors conference towards climate neutral freight transport, 9 December 2009

Brussels.

Port Authority of New York and New Jersey, 2008. Port Authority of New York and

New Jersey Aims to be Carbon Neutral by 2010 [online]. Available from:

29

http://www.panynj.gov/press-room/press-item.cfm?headLine_id=971. [Accessed 12 Jan

2010].

Rees, W.E., 2006. Ecological footprints and bio-capacity: essential elements in

sustainability assessment. In: J. Dewulf, H.V. Langenhove, eds. Renewables-Based

Technology:Sustainability Assessment. New Jersey: John Wiley and Sons, 143-156.

Rotterdam Climate Initiative, 2007. The World Capital of CO2-free energy. Project

Group Rotterdam Climate Initiative [online]. Available from: http://

www.rotterdamclimateinitiative.nl. [Accessed 15 Feb 2010].

Simmons, C., González, I., Lewis, K., 2006. Methodology for determining global

sectoral material consumption, carbon dioxide emissions and Ecological Footprints

[online]. WWF, One Planet Business; Review Version 12. Available from:

http://www.bestfootforward.com/OPB/Methodology%20Report%20-

%20Review%20v12.PDF. [Accessed 7 Dec 2010].

Van Agtmaal, E., Swahn, M., 2009. How to assess eco-efficiency of green corridors.

The Green corridors conference towards climate neutral freight transport, 9 December

2009 Brussels.

Van Den Bergh, J.C.J.M., Verbruggen, H., 1999. Spatial sustainability, trade and

indicators: an evaluation of the ecological footprint. Ecological Economics, 29, 61-72.

Wackernagel, M., Dholakia, R., Deumling, D., Richardson, D., 2000. Redefining

Progress, Assess your Household's Ecological Footprint V 2.0 [online]. Available from:

http://greatchange.org/ng-footprint-ef_household_evaluation.xls. [Accessed 12 Feb

2006].

30

Wackernagel, M., Rees, W., 1996. Our ecological footprint. Reducing human impact on

Earth. Gabriola Island: New Society Publishers.

World Resources Institute (WRI)/World Business Council for Sustainable Development

(WBCSD), (ed) 2004. The greenhouse gas protocol: a corporate accounting and

reporting standard, revised edition. WRI/WBCSD, Washington DC

Wiedmann, T., Lenzen, M., 2009. Unravelling the impacts of supply chains. A new

Triple-Bottom-Line Accounting Approach. In: S. Schaltegger, M. Bennett, R. Burrit, C.

Jasch, eds. Environmental Management Accounting for Cleaner Production.

Amsterdam: Springer Netherlands, 65-90.

Wiedmann, T., Minx, J.C., 2008. A Definition of 'Carbon Footprint'. In: C.C. Petsovam,

ed. Ecological Economic Research Trends. New York: Nova Science Publishers, 55-65.

Wiedmann, T., Lenzen, M., Barret, J., 2009. Companies on the Scale: Comparing and

Benchmarking the Footprints of Businesses. Journal of Industrial Ecology, 13, 361-383.

WPCC, 2008. Developing a carbon footprint. Port of Oslo & Port of Rotterdam. The

C40 World Ports Climate Conference. 9-11 July 2008 Rotterdam.

Yenming, J.C., Sheu, J.B., 2009. Environmental-regulation pricing strategies for green

supply chain management. Transportation Research Part E, 45, 667-677.

Zhu, Q., Sarkis, J., Lai, K-H., 2008. Green supply chain management implications for

“closing the loop” Transportation Research Part E, 1-18

31

![[Document subtitle] [DATE] - Environmental Footprint Institute](https://img.pdfslide.net/doc/110x75/631ca10e7051d371800f901d/document-subtitle-date-environmental-footprint-institute.jpg)