Embed Size (px)

Citation preview

Revamping the Regional Railway Systems in Eastern and Southern AfricaMark Pearson and Bo GiersingRegional Integration Research Network Discussion Paper (RIRN/DP/12/01)

Mineral Resource Based Growth Pole Industrialisation Growth Poles and Value Chains

Regional Integration Research NetworkOpen Dialogues for Regional Innovation

C.C. Callaghan

Mineral Resource Based Growth Pole Industrialisation – Value Chains Report

Page i

Preface

Since its establishment in 2009, Trade Mark Southern Africa (TMSA) has supported the

Tripartite of the Common Market of Eastern and Southern Africa (COMESA), the Southern

African Development Community (SADC) and the East African Community (EAC), in

developing and implementing its regional integration agenda. This involves supporting the

design and planned implementation of the Tripartite Free Trade Area (FTA), improving the

economic competitiveness of the region and reducing costs of cross-border transactions

through a transport corridor approach addressing both trade facilitation issues and

infrastructure constraints.

Focused industrial development is essential in the COMESA-EAC-SADC Tripartite region to

fundamentally change the economy and to promote high yield sectors. Such development

brings not only an improvement in the GDP and job provision, but promotes knowledge

accumulation and technological sophistication that have far reaching benefits for the

economy.

This research was conducted under the topic “Tripartite ‘Growth Pole’ Diagnostic Reports:

Analysis of Potentials and Prospects for Minerals-Based Industrialisation.” The research is

packaged in four (4) Sub-Sector Reports on hydrocarbons, ferrous metals, base metals and

phosphates and a Consolidated ‘Growth Poles’ Report. The reports profile and prioritise a

number of potential regional ‘growth poles’ throughout eastern and southern Africa. In the

‘first sort’ each known minerals deposit was analysed through three (3) filters as follows:

1. By size of deposit (size of known indicated resource);

2. By status of deposit (levels of investment in developing the deposit); and,

3. By ‘expert group’ assessment (market conditions and supporting infrastructure).

The research reviewed available information on mineral deposits and the status of their

development and analysed the extent to which realisable mining and mineral development

opportunities can contribute to and enhance regional development. Data constraints limited

the research to the Eastern and Southern Africa region and defined a limited number of

plausible ‘growth poles’, which could provide a platform to accelerate industrialisation in the

region.

The results from these three filters were then combined through a ‘second sort’, which

enhanced the analysis by clustering minerals within a defined locality into potential ‘growth-

pole’ value chains. In line with ‘growth pole’ theory the basis for any prioritisation was

Page ii

whether the initial ‘critical mass’ of investment had been achieved. The minimum critical level

of investment is considered to be achieved when five key pre-conditions have been met,

namely:

1. A recognised global multi-national corporation (MNC) has made a significant

investment in developing a mineral deposit or a cluster of mineral deposits;

2. Such an investment commitment reflects that the regulatory environment for trade

and investment in sufficiently robust to support large-scale projects;

3. Similarly, this size of investment in developing a world-class resource confirms that

the long term global market outlook for the target commodity is equally robust;

4. It also acknowledges that any supply-side infrastructure constraints can be overcome

by the projects cash-flows and that infrastructure development itself represents an

opportunity for the lead developer, in the transport and energy sectors for example;

and,

5. Finally, the participation of a strong ‘anchor’ investor substantially strengthens the

prospects for developing upstream linkages to local suppliers and new downstream

industries as a result of the presence of and initial investment by the global mining

company.

In addition to these pre-conditions the research also considers two additional criteria to

prioritize ‘growth-pole’ potential. The first was the extent to which the value-chain could be

developed given prevailing market conditions, and the second was whether value-chain

linkages straddle national borders to assume a regional posture.

Based on these considerations the following seven (7) regional growth poles were prioritised

in order of potential:

1. Tete, Mozambique – Southern Malawi (Hydrocarbons, Ferrous Metals and

Phosphates);

2. Copperbelt, Zambia – Copperbelt, DRC (Base Metals);

3. Cabinda, Angola – Bas Congo, DRC – Soyo, Angola (Hydrocarbons and

Phosphates);

4. Rovuma Basin, Mozambique – Ruvuma and Songo-Songo Basins, Tanzania

(Hydrocarbons);

5. Lephalale, South Africa – Morepule, Botswana (Hydrocarbons);

6. Kabanga, Tanzania – Musongati, Burundi (Base Metals); and,

7. Central Zimbabwe – Central Mozambique (Hydrocarbons and Ferrous Metals).

Page iii

An initial scoping study is currently being conducted to develop a fuller picture of the Tete,

Mozambique – Southern Malawi ‘Growth Pole’, which has been expanded to include

Eastern, Zambia, in collaboration with the World Bank and the governments of Malawi,

Mozambique and Zambia.

TMSA, under its Regional Integration Research Network initiative, commissioned Chris

Callaghan to conduct the research. Chris Callaghan is an independent consultant whose

career includes stints as a Mining Sector Specialist at the Development Bank of Southern

Africa (DBSA) and a Senior Manager at MINTEK South Africa, the state-run Mining

Technology Research Institute. The TMSA lead was Graham Smith, TMSA Programme

Manager - Corridors. The study benefited particularly from guidance and inputs by Dr.

Judith Fessehaie, TMSA Industrial Development Expert and Mr. Bo Giersing, TMSA Ports

and Railway Specialist, Mr. Jurgens Van Zyl, an independent Mining and Development

Finance Specialist, currently under contact to Business Leadership South Africa (BLSA) and

Dr. Paulo Fernandes, a Logistics Specialist at Mott MacDonald/PDNA South Africa. These

individuals ‘peer reviewed’ the prioritisation methodology, which underpinned the selection of

the Growth-Poles. Other TMSA colleagues provided some early inputs into the terms of

reference for the study.

More Information

The reports can be downloaded on the TMSA website at

www.trademarksa.org/publications/mineral-resource-based-growth-pole-industrialisation

Reports include the Consolidated Growth Poles and Value-Chains Report and four (4) Sub-

Sector Minerals Reports on Hydrocarbons (Coal, Oil and Gas), Ferrous Metals (Iron and

Steel), Base Metals (Chrome, Manganese, Nickel, Vanadium, Copper, Zinc and Lead) and

Phosphates report.

Page iv

Table of abbreviations

Billion cubic metres per annum bcmpa

Billions of tonnes bt

Billions of tonnes per annum btpa

Chrome Cr

Copper Cu

Direct shipping ore DSO

Empresa Nacional de Hidrocarbonetos ENH

Iron Fe

Ferrochrome FeCr

Gross domestic product GDP

Gigajoule GJ

Growth Pole based Programme GPBP

Global Value Chain GVC

Information and communications technology ICT

Liquefied natural gas LNG

Liquefied petroleum gases LPG

Million British Thermal Units MMbtu

Manganese Mn

Millions of tonnes Mt

Millions of tonnes per annum Mtpa

Manufacturing value add MVA

Normal cubic meters per hour NCMH

Natural gas liquids NGL

Nickel Ni

Phosphorous P

Lead Pb

Sulphur S

Special economic Zone SEZ

Tonnes t, ton

Terms of reference TOR

Tonnes per annum tpa

Wet High Intensity Magnetic Separator WHIMS

Zambia-China Cooperation zone ZCCZ

Zinc Zn

Page v

Table of Definitions

LNG Liquefied natural gas (largely methane cooled to -161°C for transport in specially designed tankers)

LPG Liquefied petroleum gases (propane, butane or mixtures of the two)

NCMH Normal cubic meters per hour is a measure of flow rate. It is equal to one cubic meter under "normal" conditions,

defined as 0°C and 1 atmosphere (101.3 kPa).

NGL Natural gas liquids (largely Ethane and heavier hydrocarbons, cooled to -101°C for transport to a tetrochemical

plant or refinery

MMbtu Million British Thermal units equal to the international ISO standard of 1.055056 GJ

Page vi

Table of Contents

1 Introduction .......................................................................................................... 1 1.1 Terminology ............................................................................................................... 8 1.2 The real ability to grow an economy on a minerals base .................................... 13

1.2.1 United States ....................................................................................................... 14 1.2.2 South Africa ......................................................................................................... 15

1.3 Linkages ................................................................................................................... 17 1.3.1 Monetary and Fiscal linkages .............................................................................. 17 1.3.2 Employee consumption linkages ......................................................................... 17 1.3.3 Production linkages ............................................................................................. 18

1.4 Basis for the focus areas ....................................................................................... 22

2 Methodology ...................................................................................................... 24 2.1 Screening and clustering to define growth poles around mineral potential ..... 24 2.2 Initial screening ....................................................................................................... 24 2.3 First sort ................................................................................................................... 26 2.4 Expert group rating ................................................................................................. 27 2.5 Infrastructure component ...................................................................................... 30 2.6 Challenges ............................................................................................................... 35 2.7 Value Chains ............................................................................................................ 35

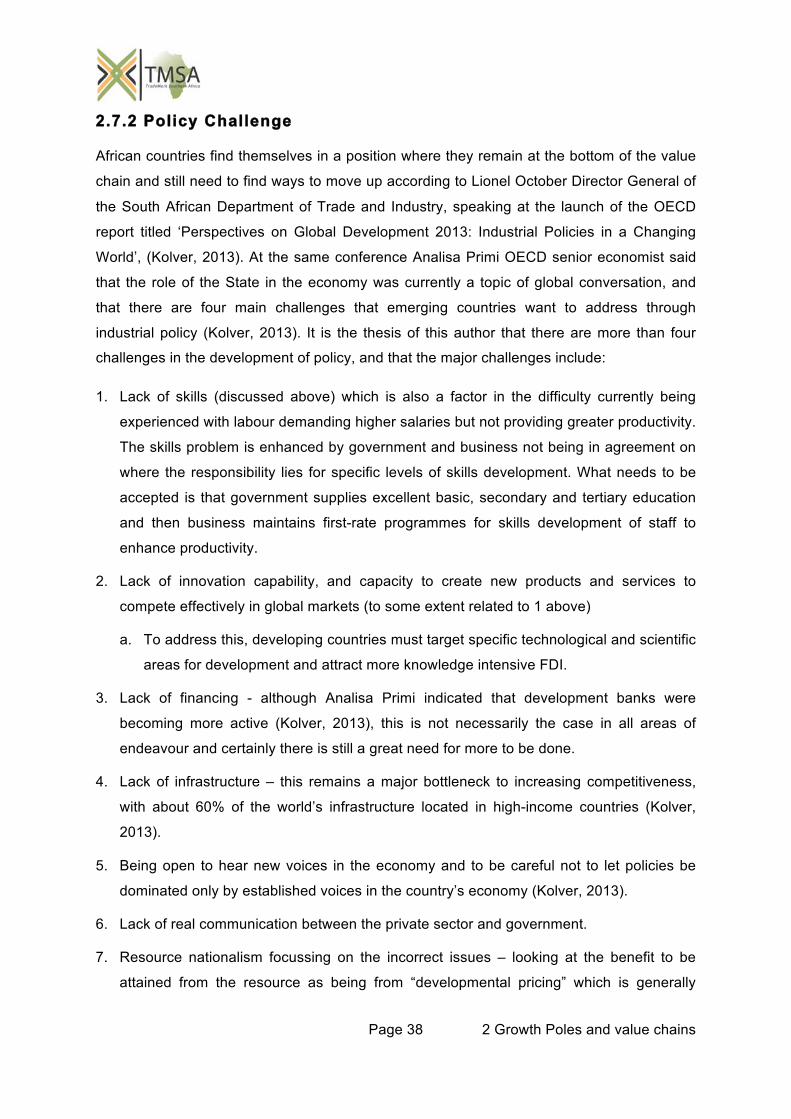

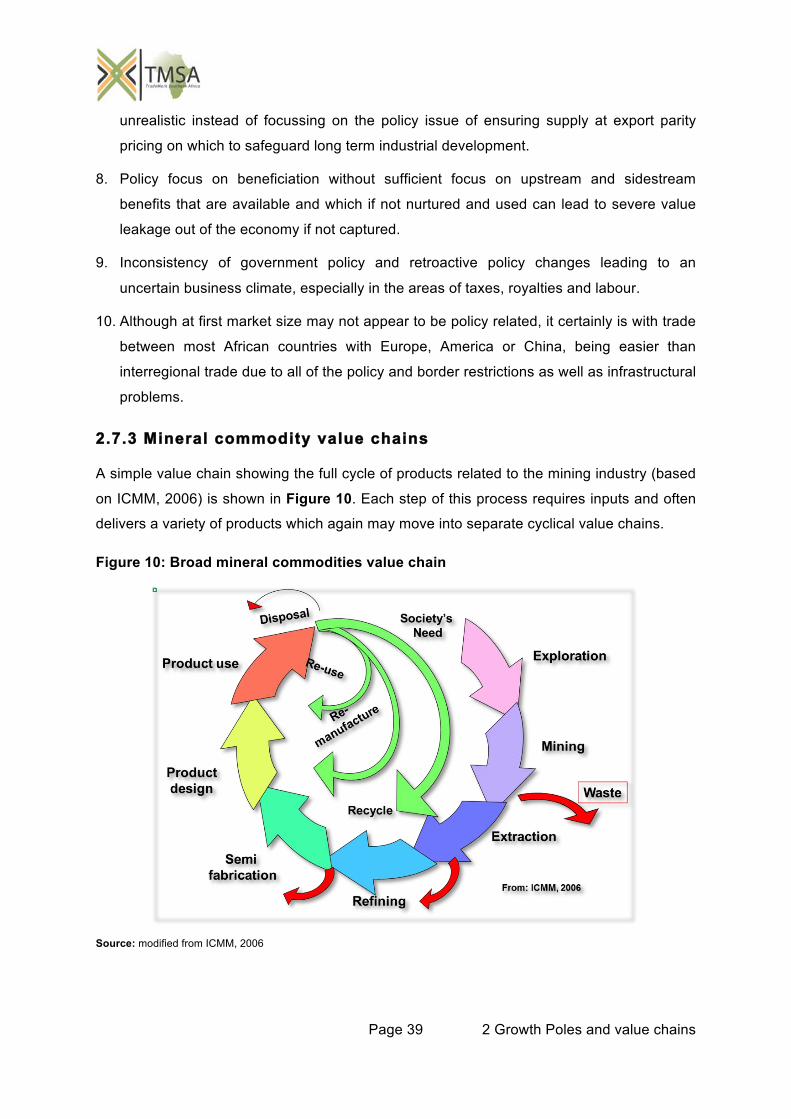

2.7.1 First step in developing value chains .................................................................. 36 2.7.2 Policy Challenge ................................................................................................. 37 2.7.3 Mineral commodity value chains ......................................................................... 38 2.7.4 The importance of developing value chains ........................................................ 39 2.7.5 Global Value Chains ........................................................................................... 41

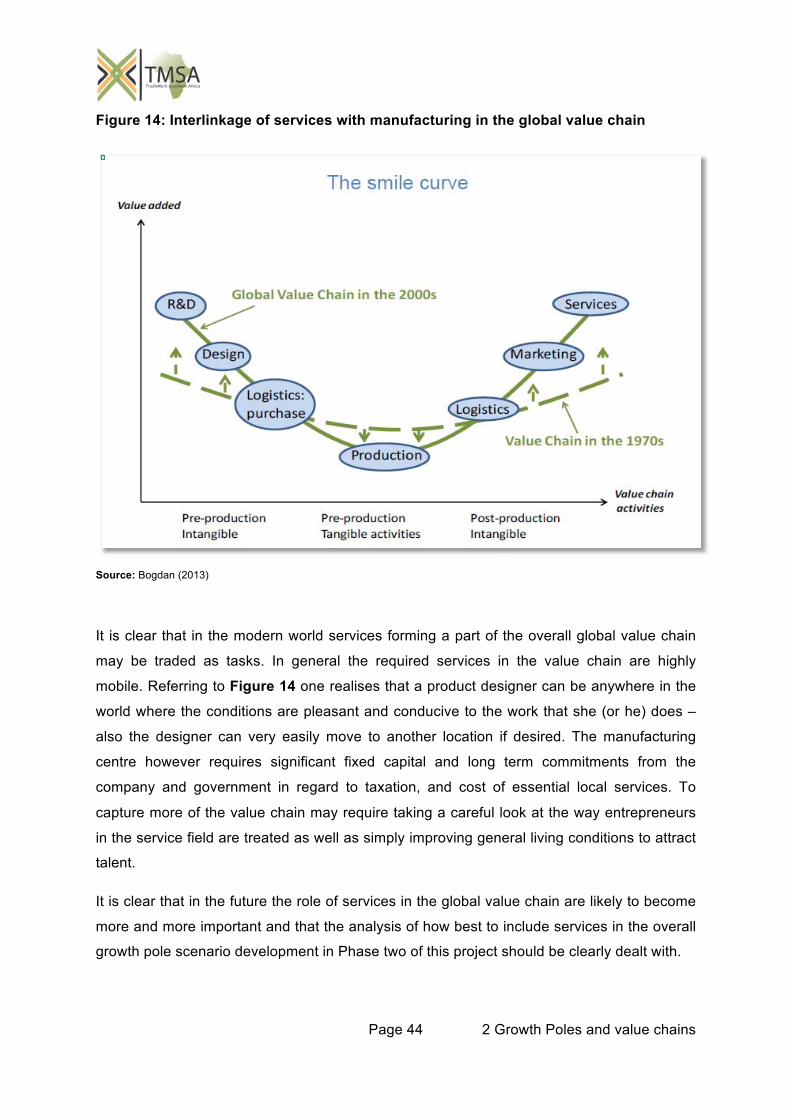

2.8 The JICA report ....................................................................................................... 44

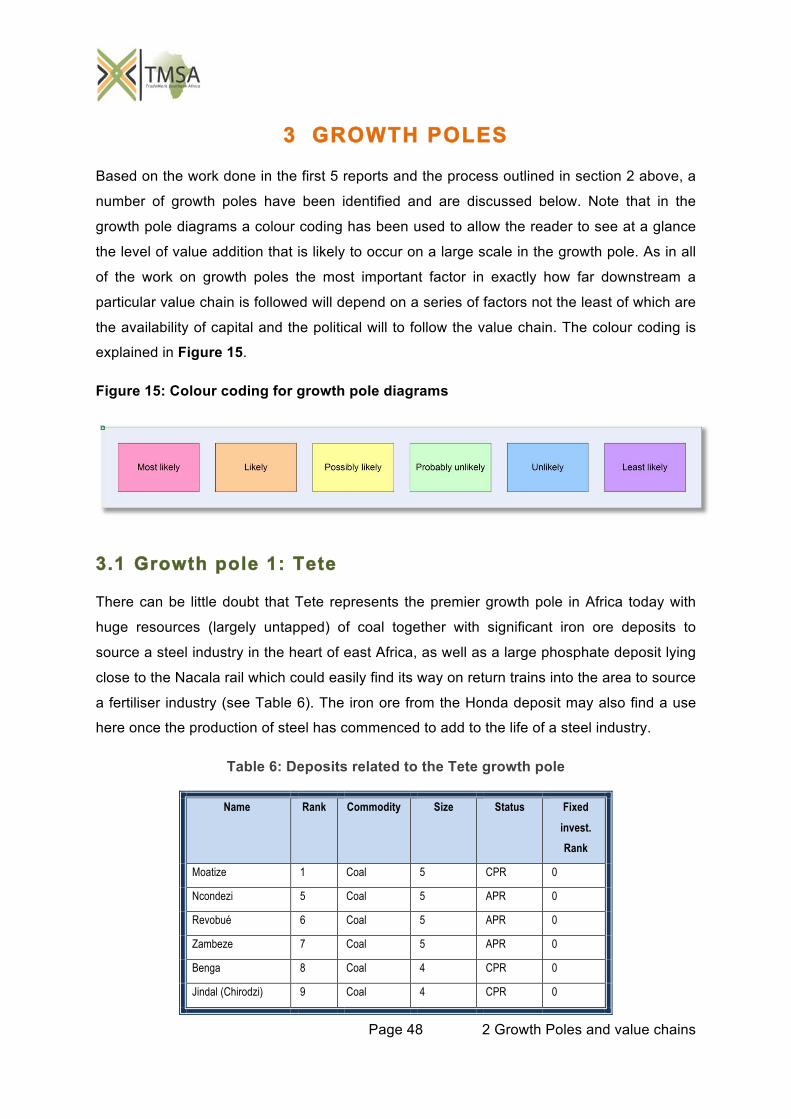

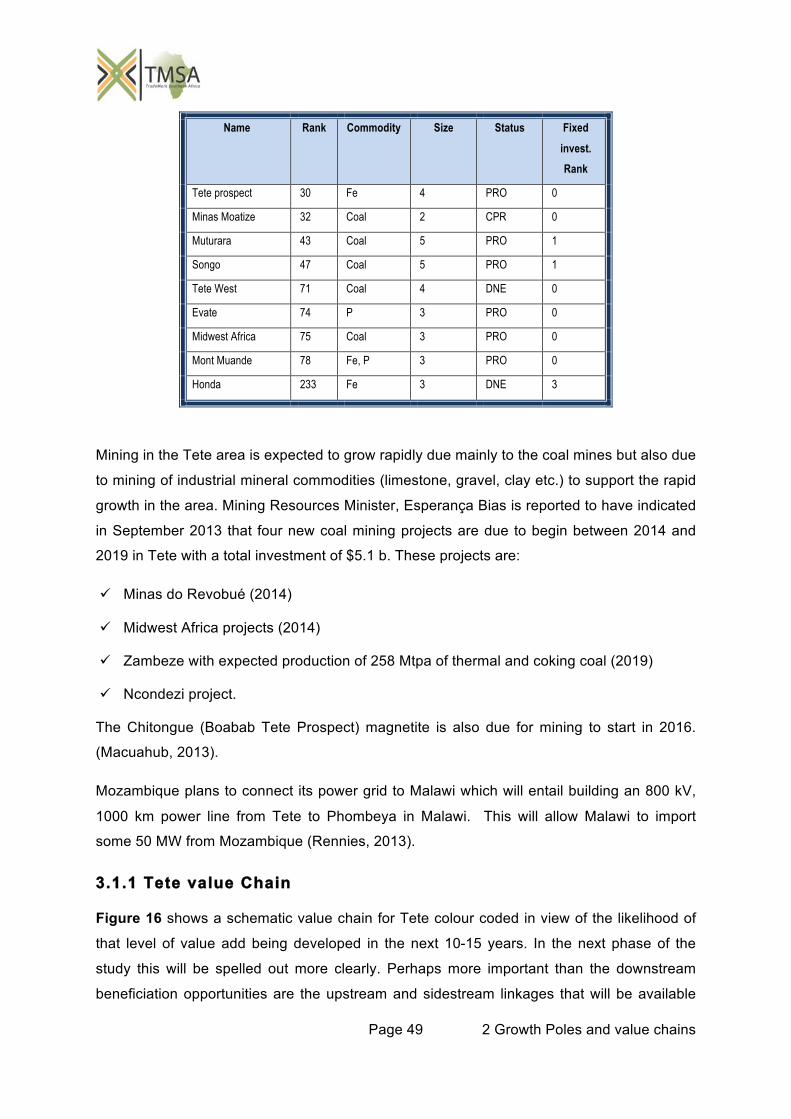

3 Growth Poles ...................................................................................................... 47 3.1 Growth pole 1: Tete ................................................................................................. 47

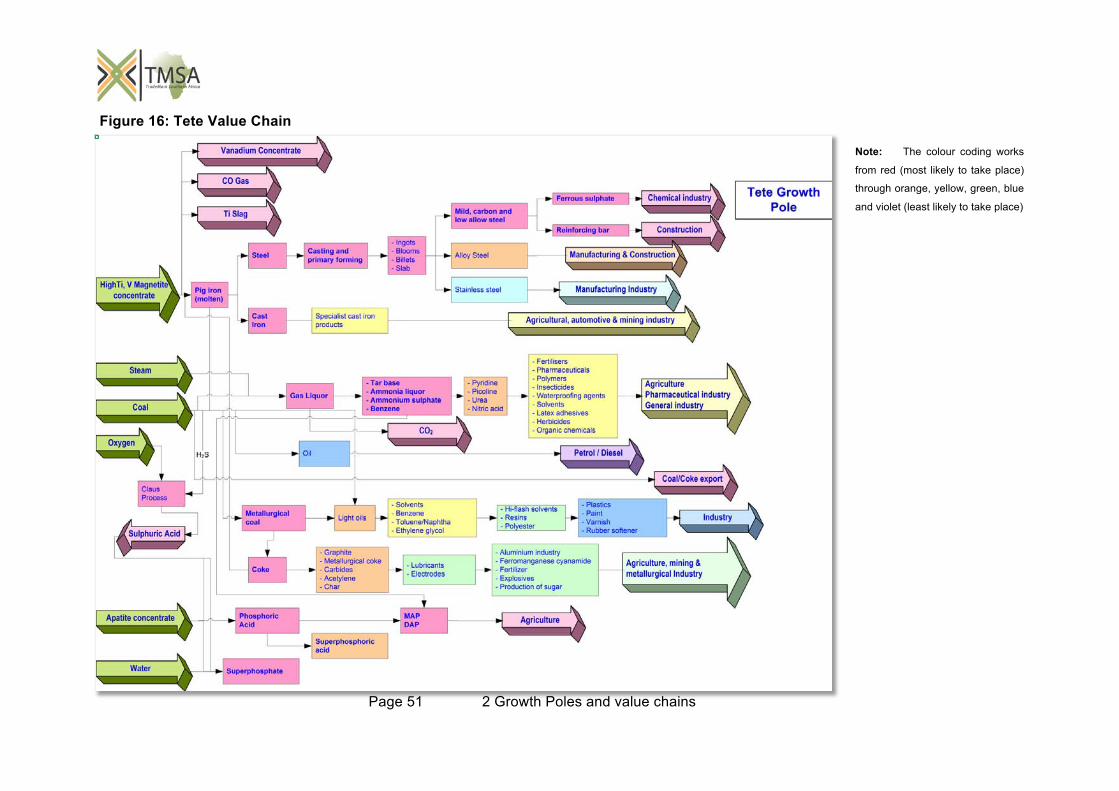

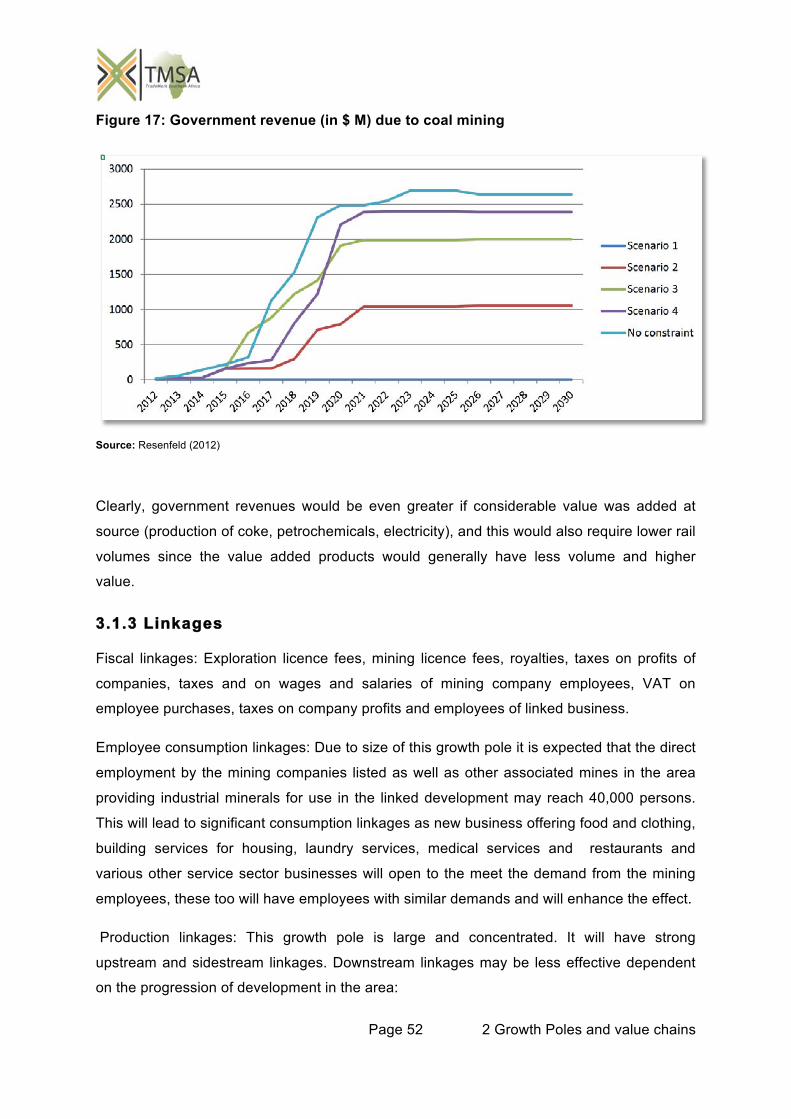

3.1.1 Tete value Chain ................................................................................................. 48 3.1.2 Government revenue from coal mining ............................................................... 49 3.1.3 Linkages .............................................................................................................. 51

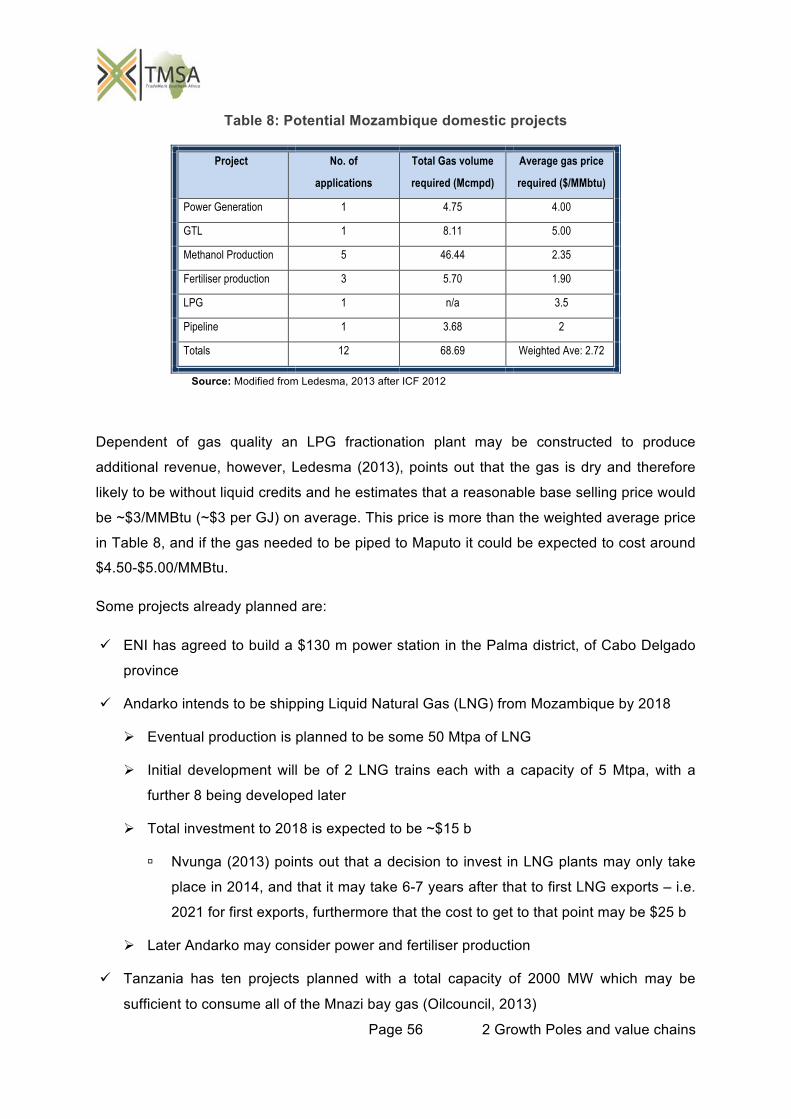

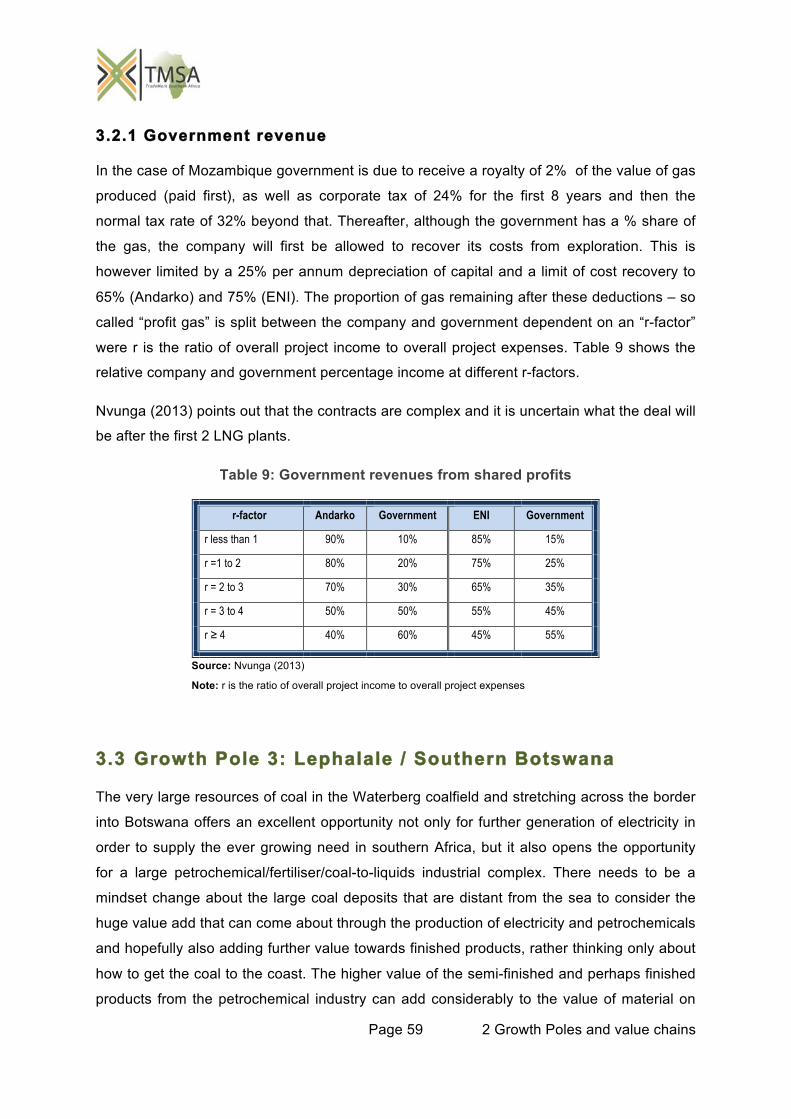

3.2 Growth Pole 2: Rovuma / Mtwara .......................................................................... 53 3.2.1 Government revenue .......................................................................................... 58

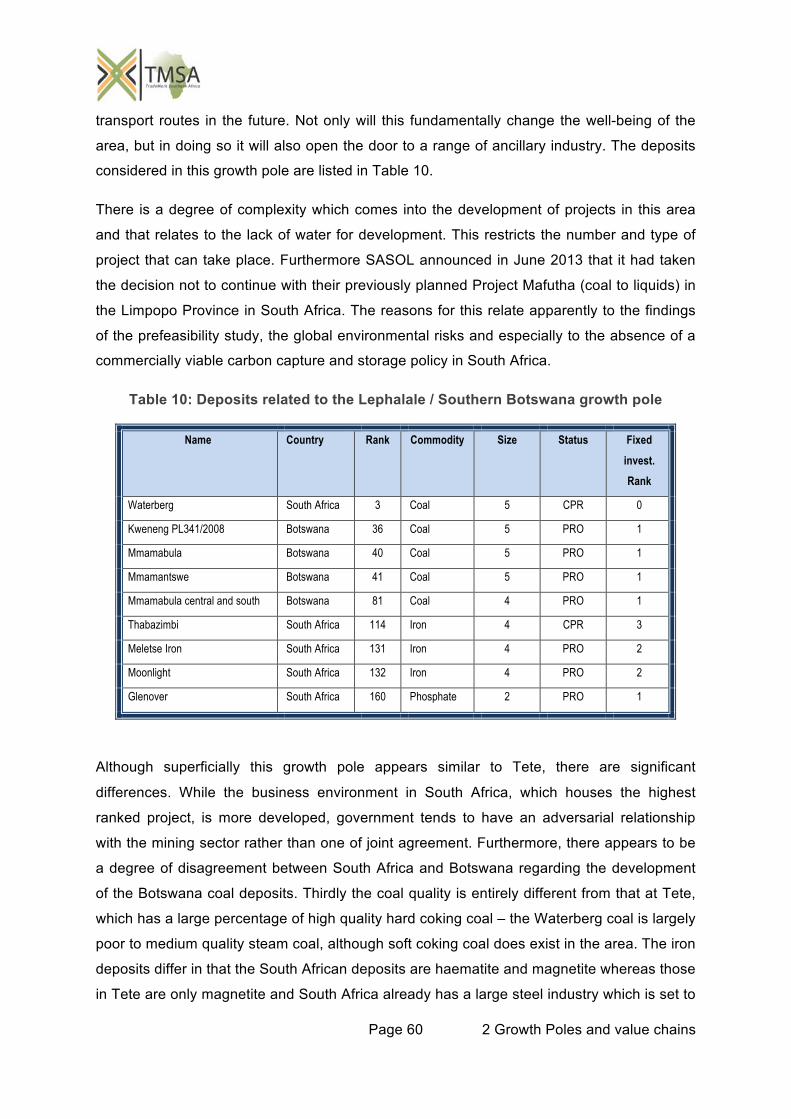

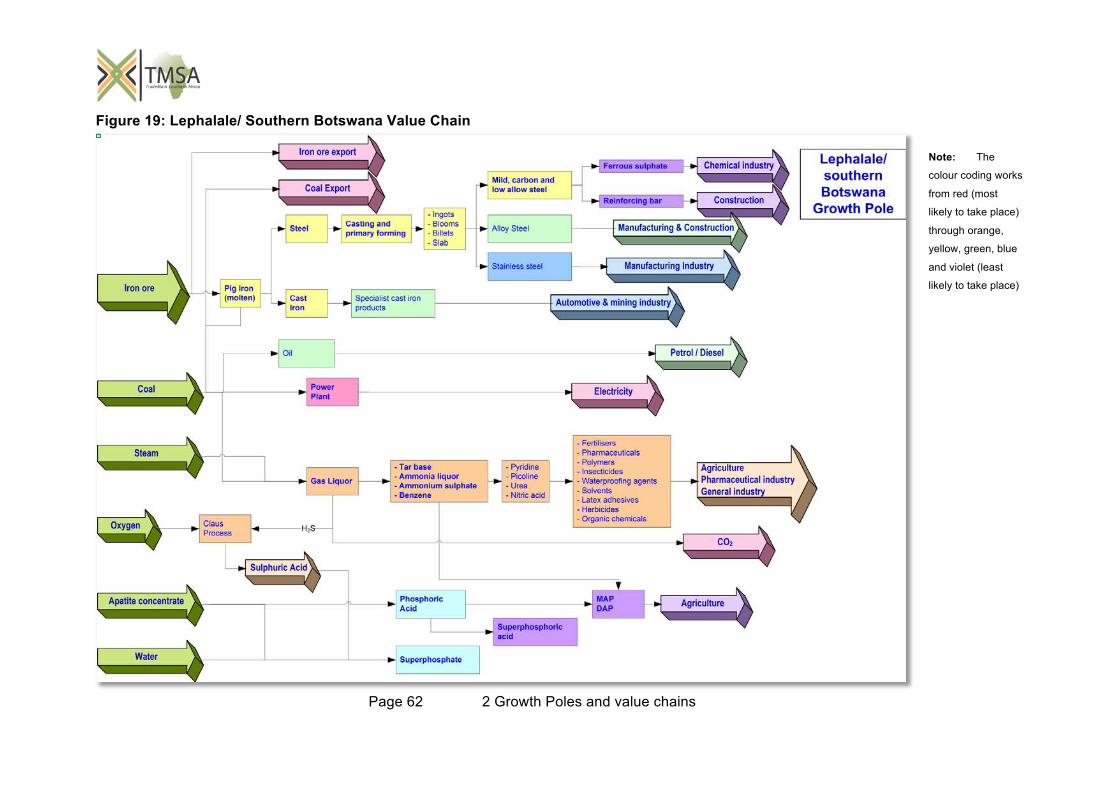

3.3 Growth Pole 3: Lephalale / Southern Botswana .................................................. 58

Page vii

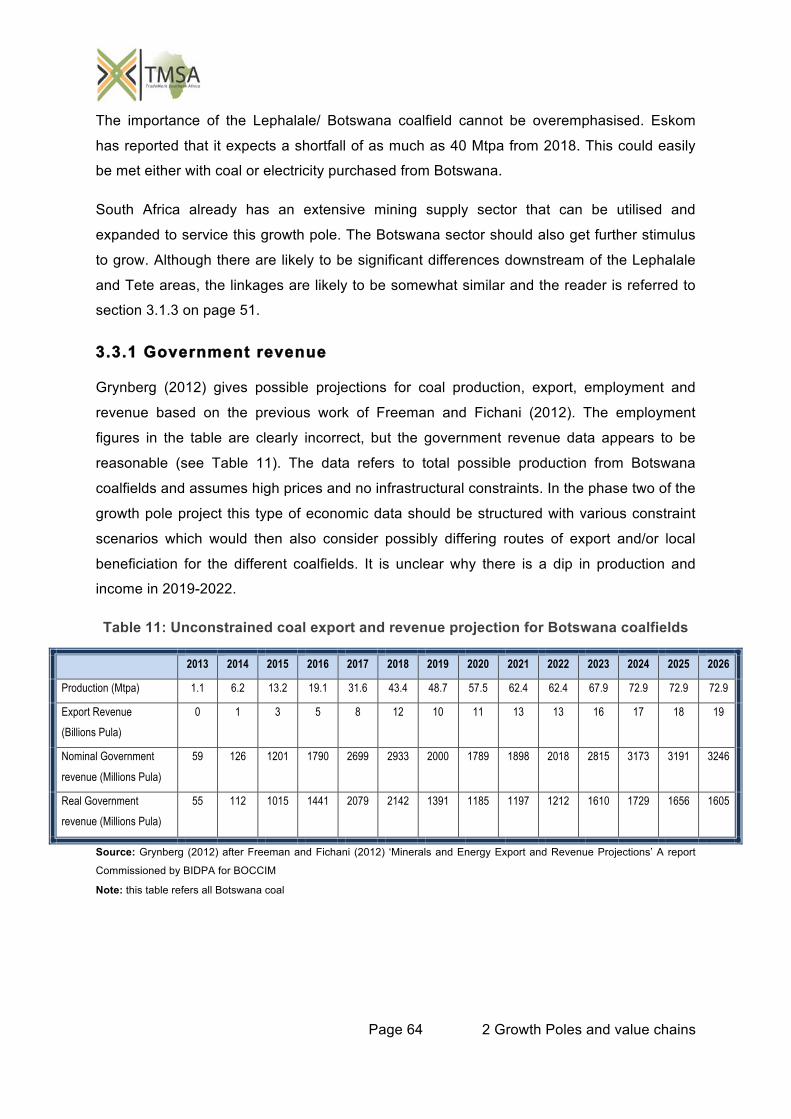

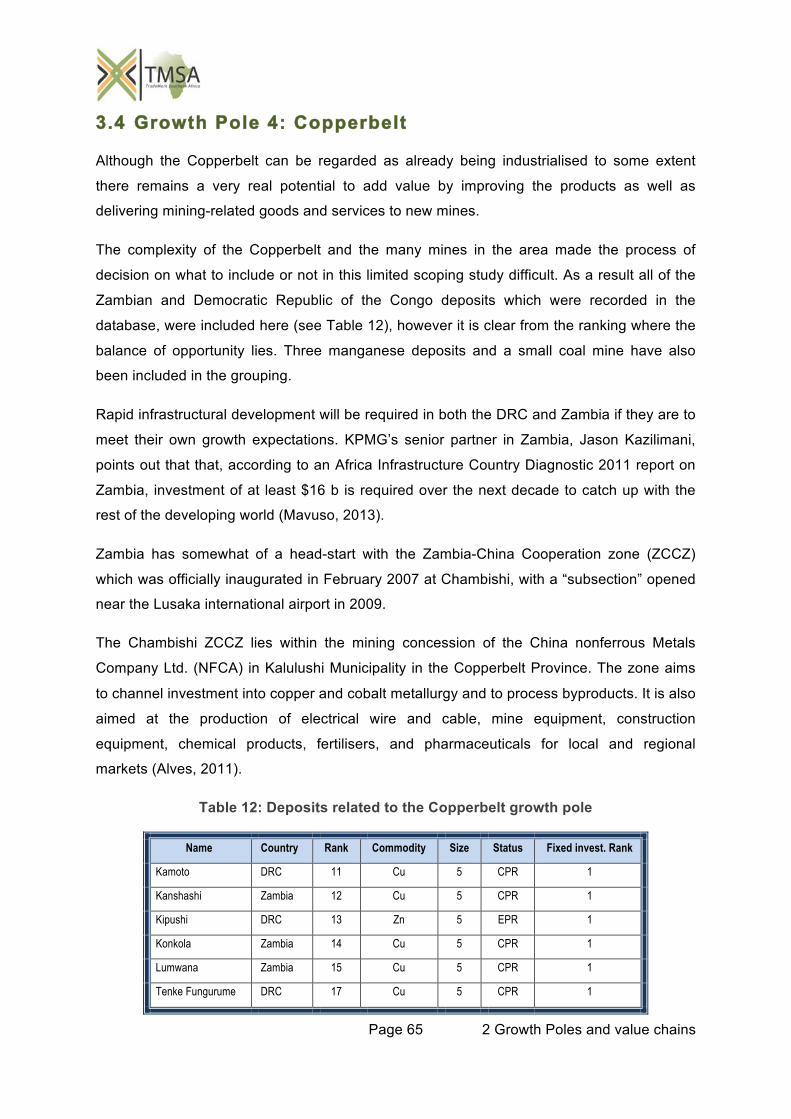

3.3.1 Government revenue .......................................................................................... 63 3.4 Growth Pole 4: Copperbelt ..................................................................................... 64

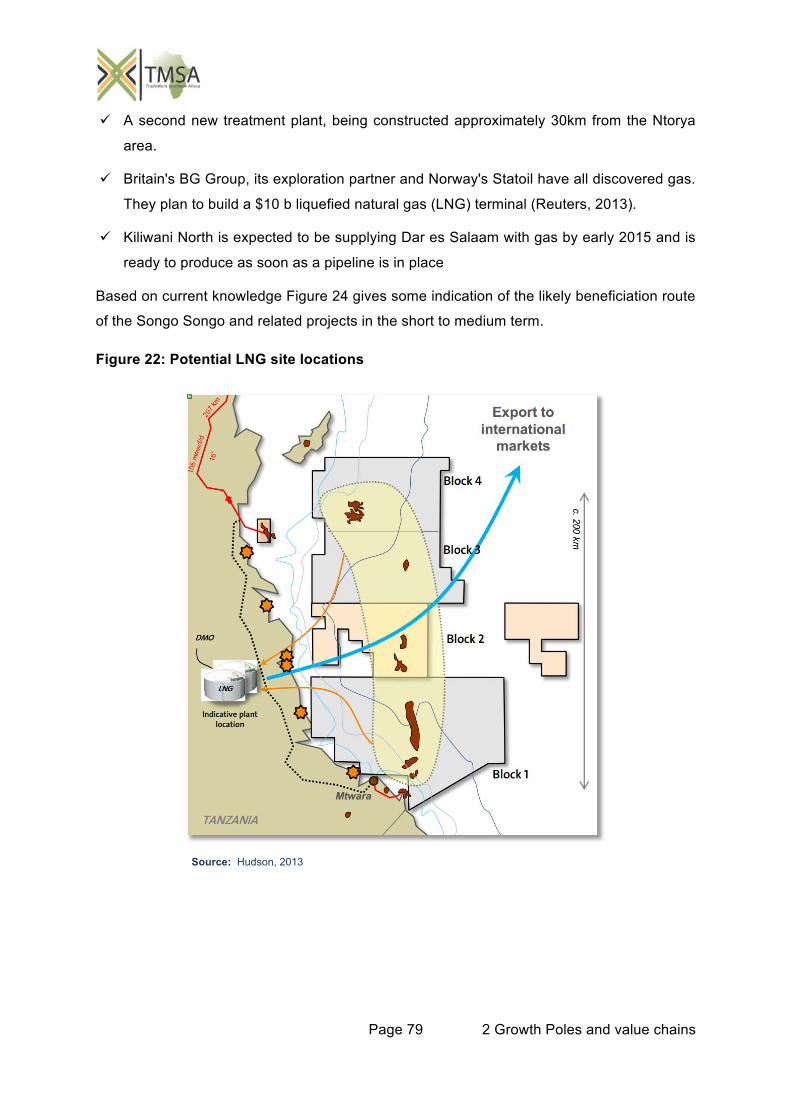

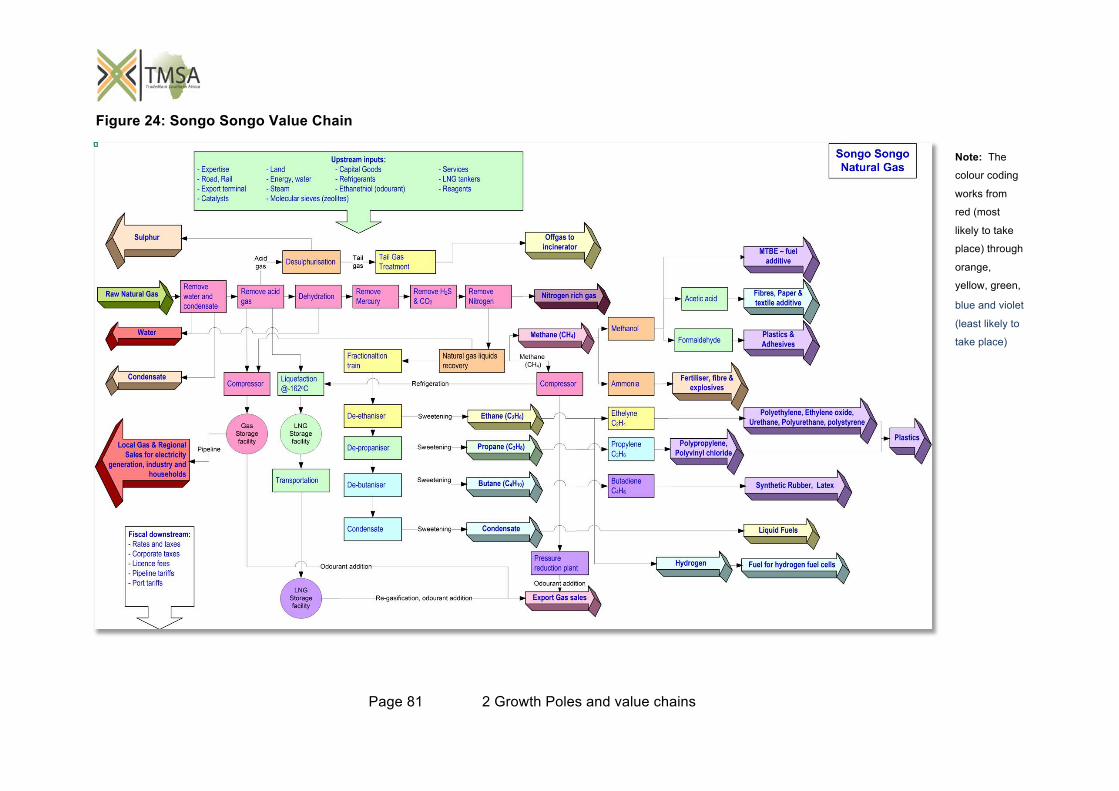

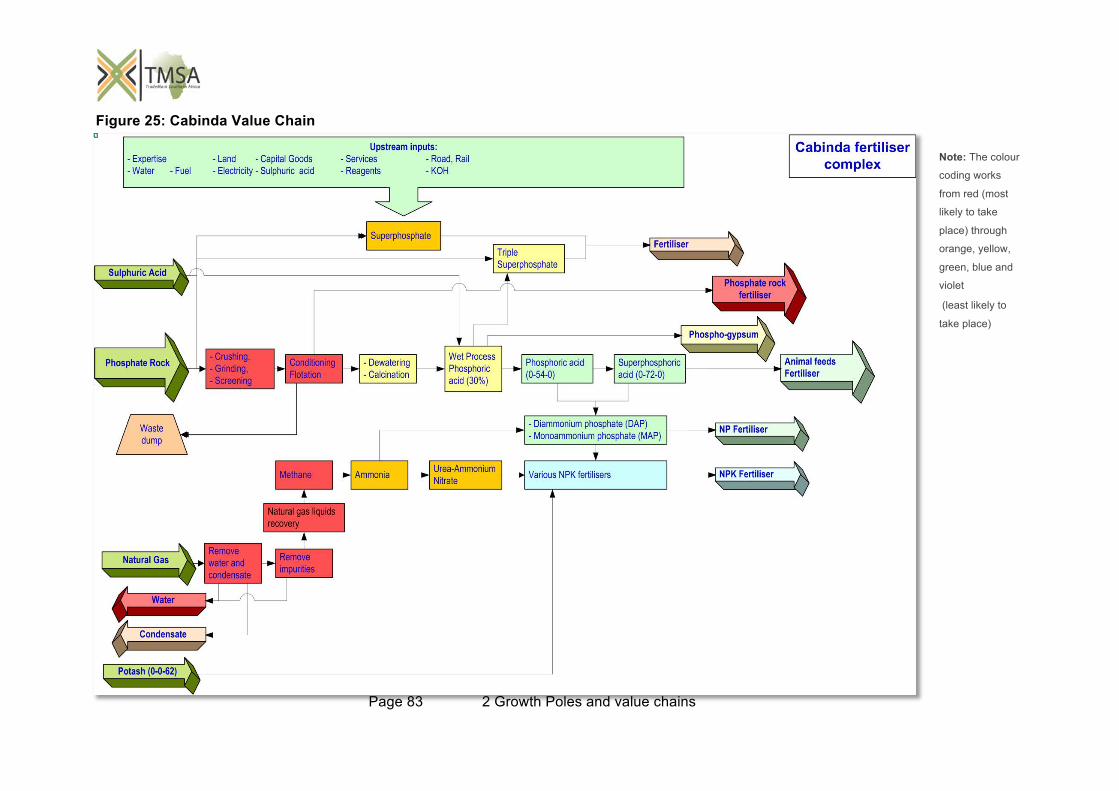

3.4.1 Linkages .............................................................................................................. 69 3.5 Growth pole 5: Zimbabwe steel ............................................................................ 71 3.6 Growth Pole 6: Northern Cape iron/manganese .................................................. 74 3.7 Growth pole 7: Songo-Songo Central Tanzania ................................................... 76 3.8 Growth Pole 8: Cabinda / Bas Congo DRC Oil / Phosphate ................................ 81 3.9 Growth pole 9: Kabanga / Burundi nickel growth pole ....................................... 83

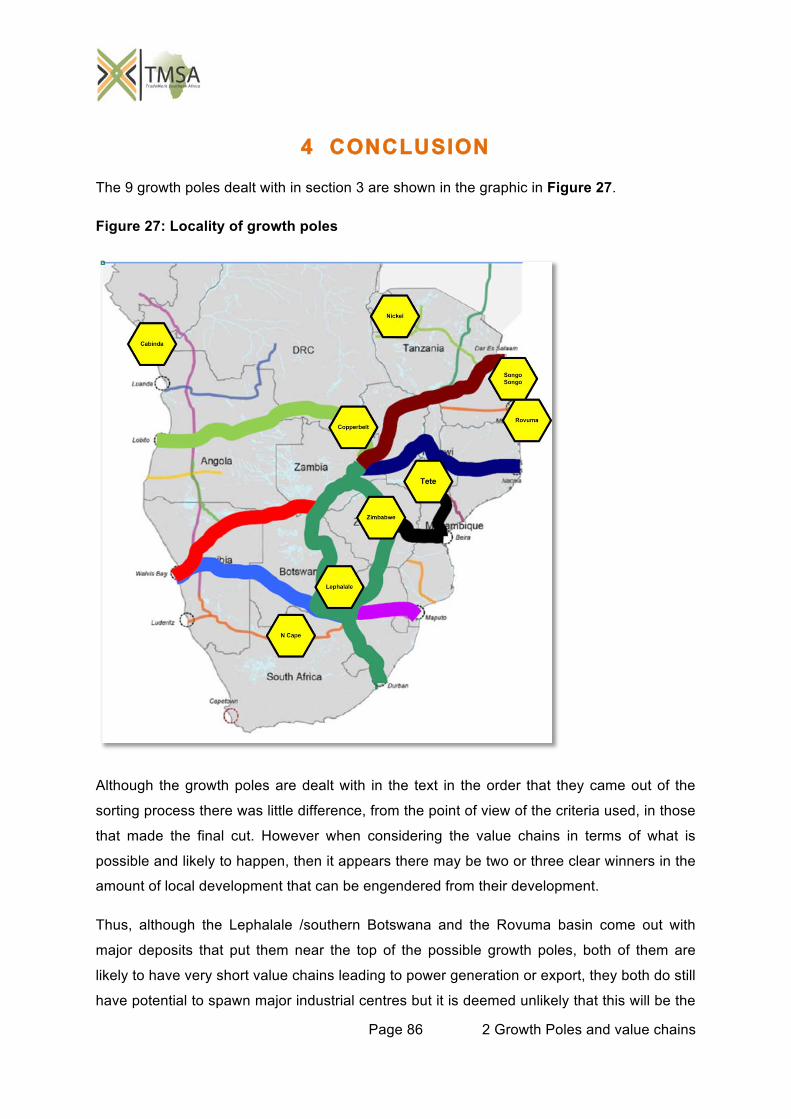

4 Conclusion ......................................................................................................... 85

Appendix A Energy content .................................................................................. 92

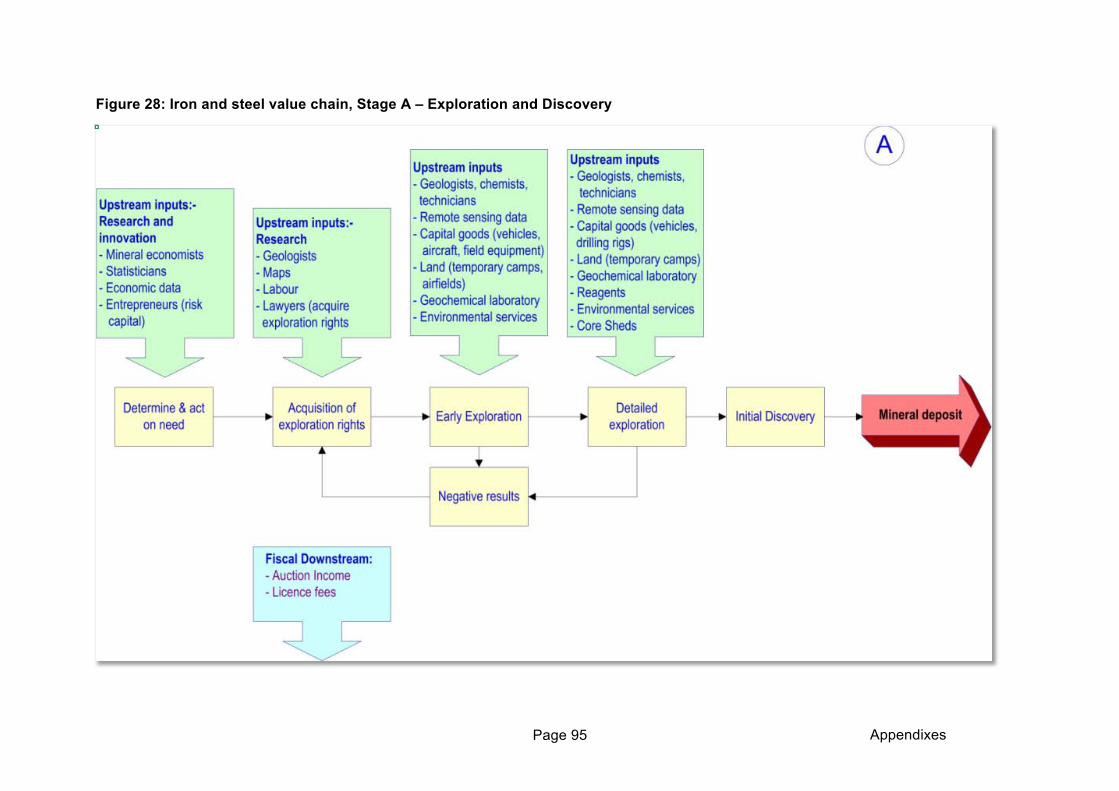

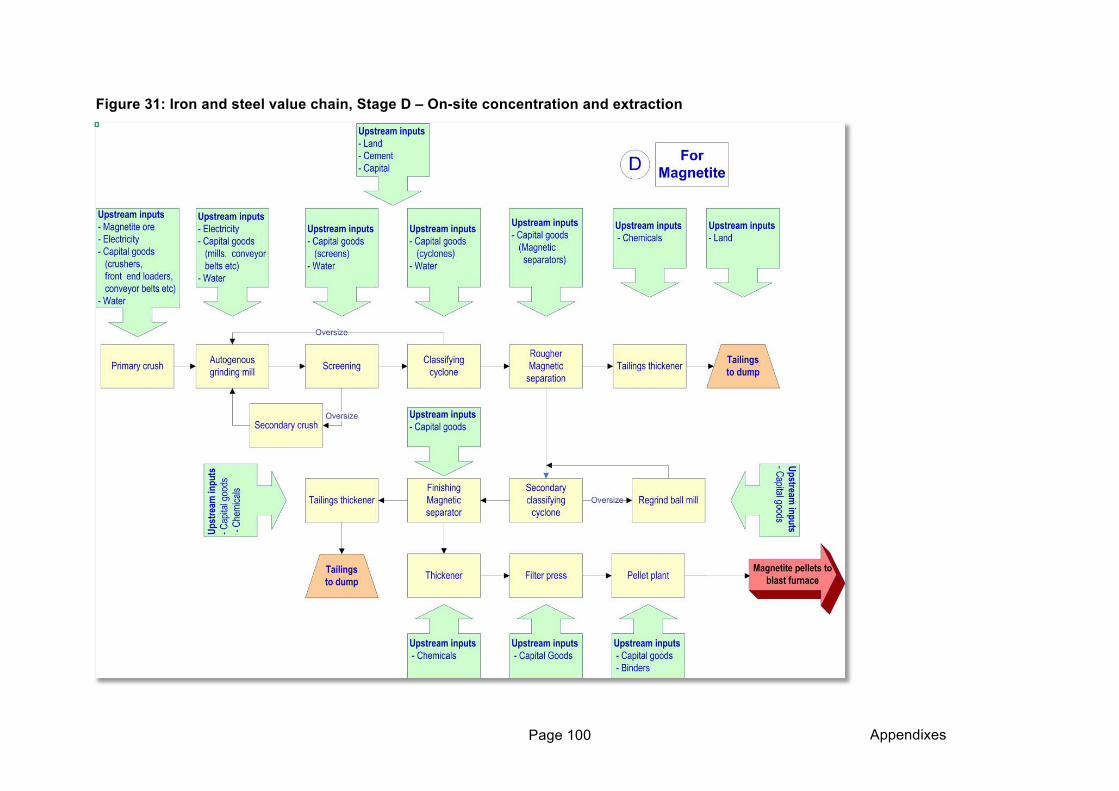

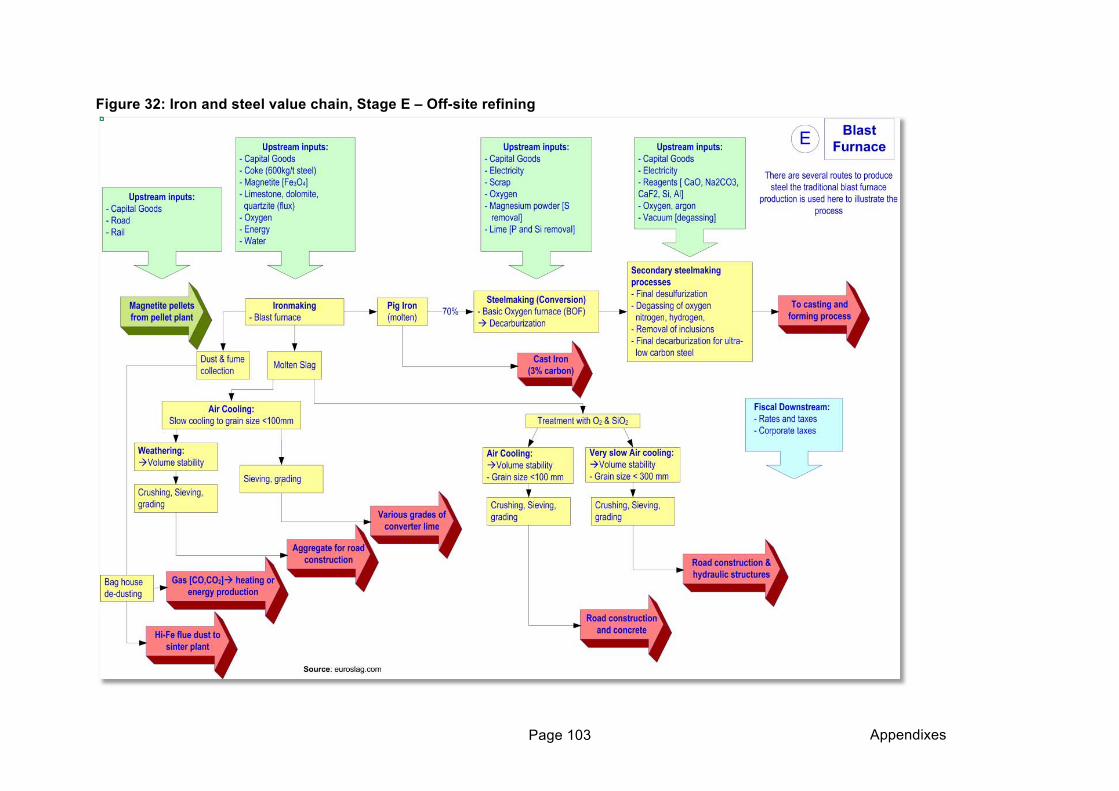

Appendix B Iron and steel value chain ................................................................ 93

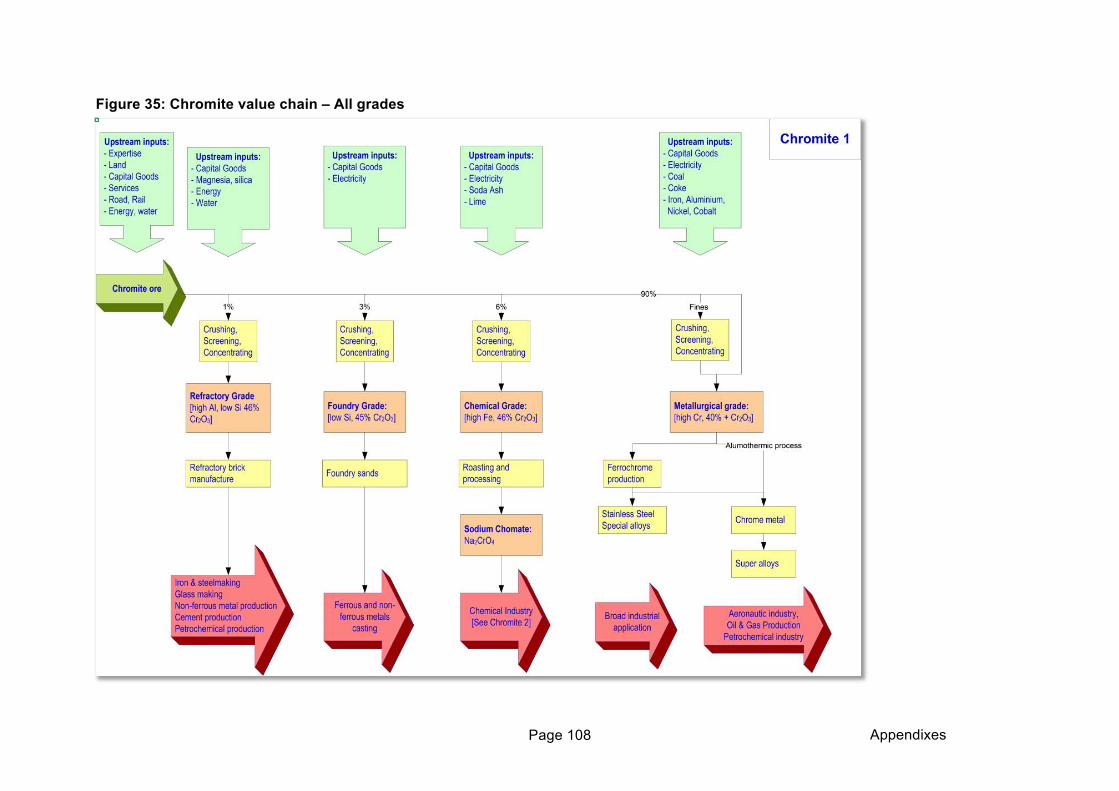

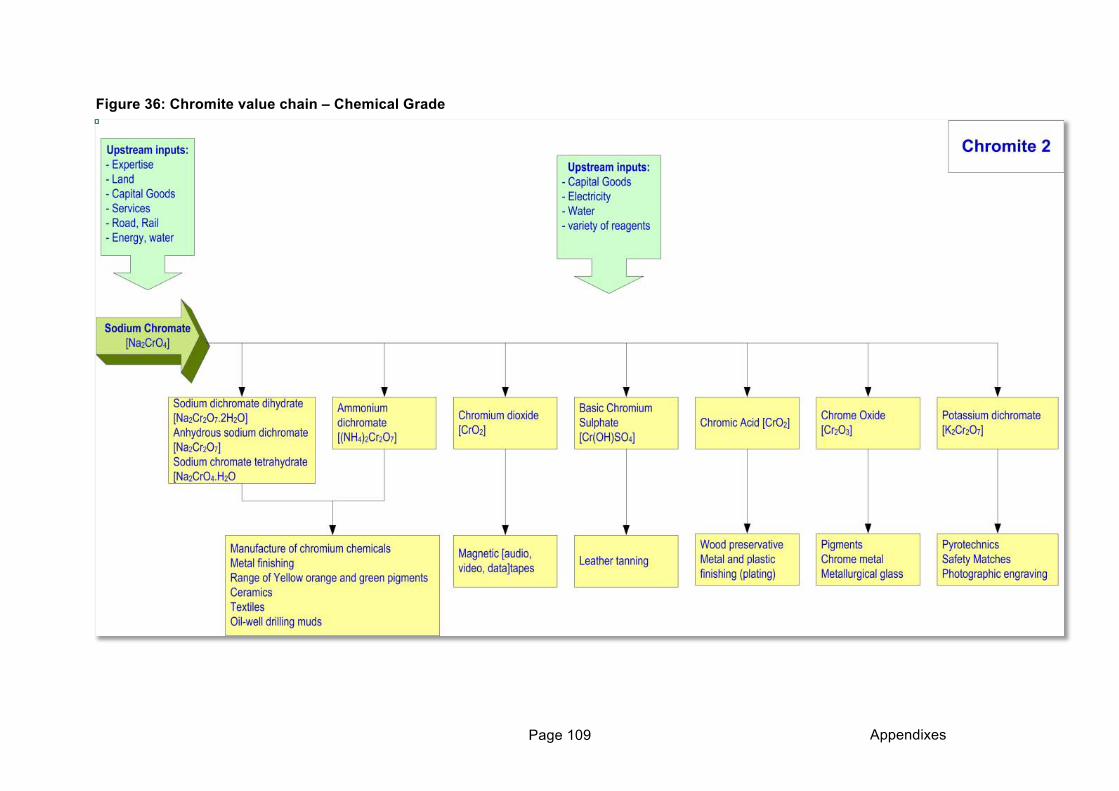

Appendix C Chrome value chain ........................................................................ 107

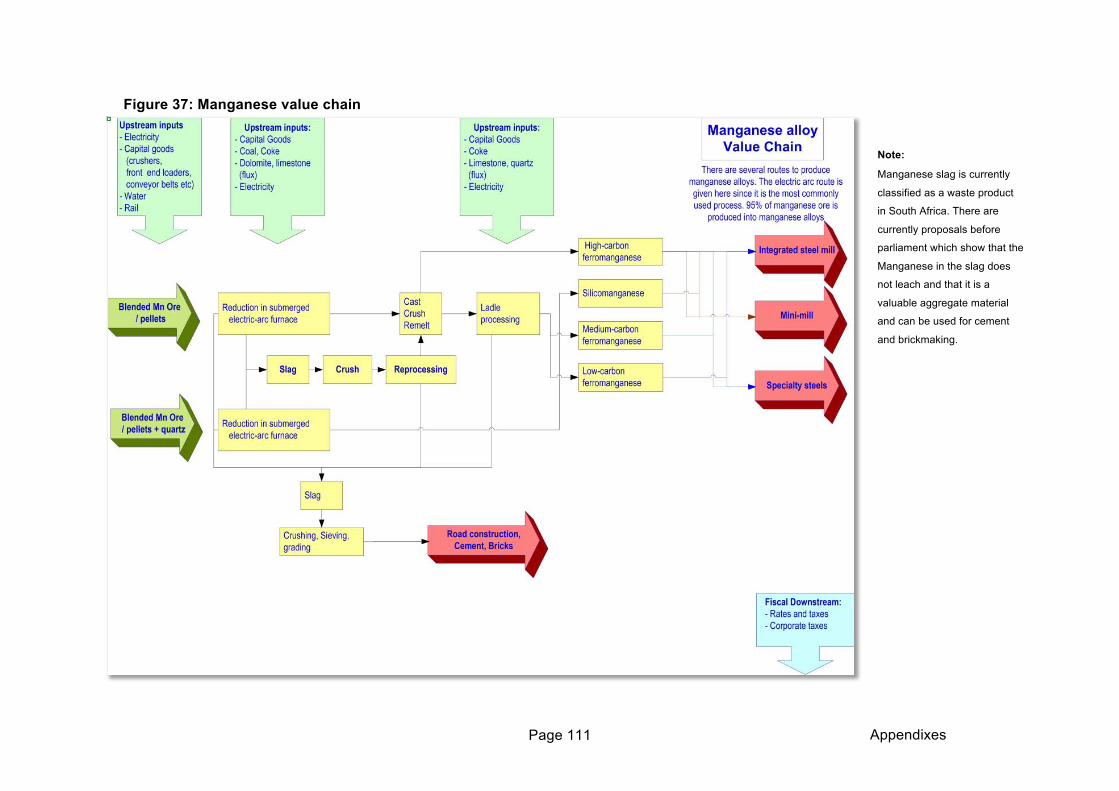

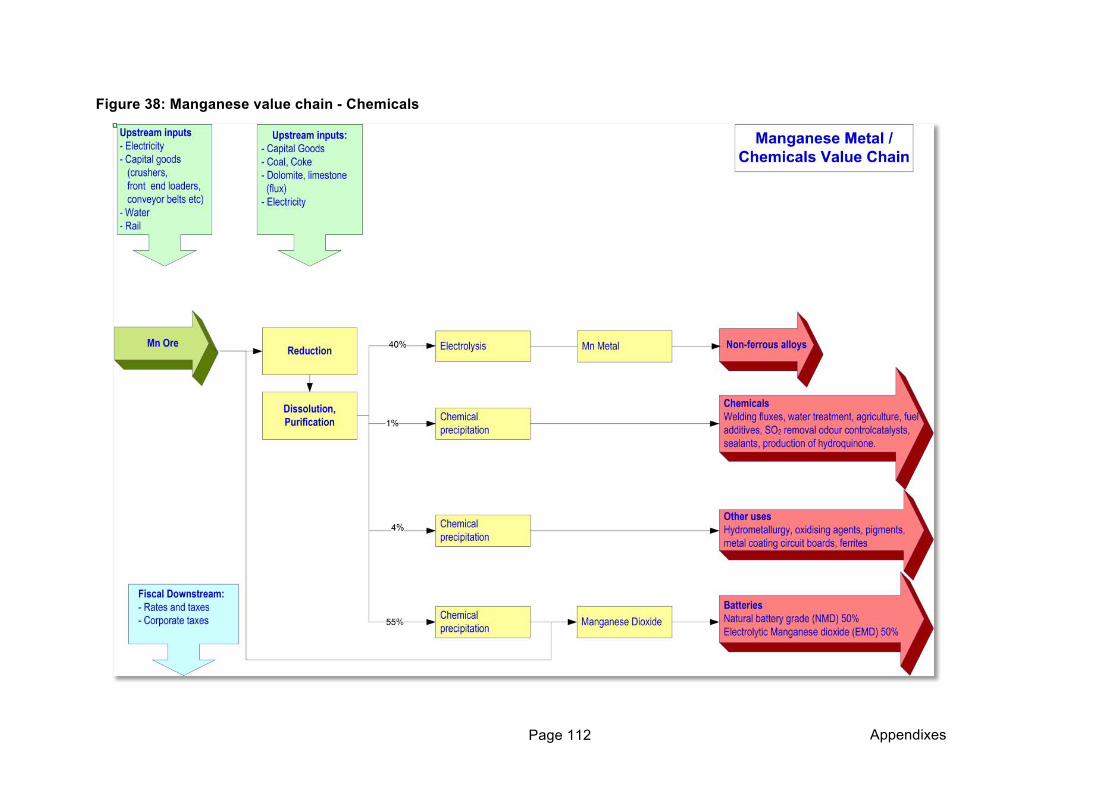

Appendix D Manganese value chain ................................................................. 110

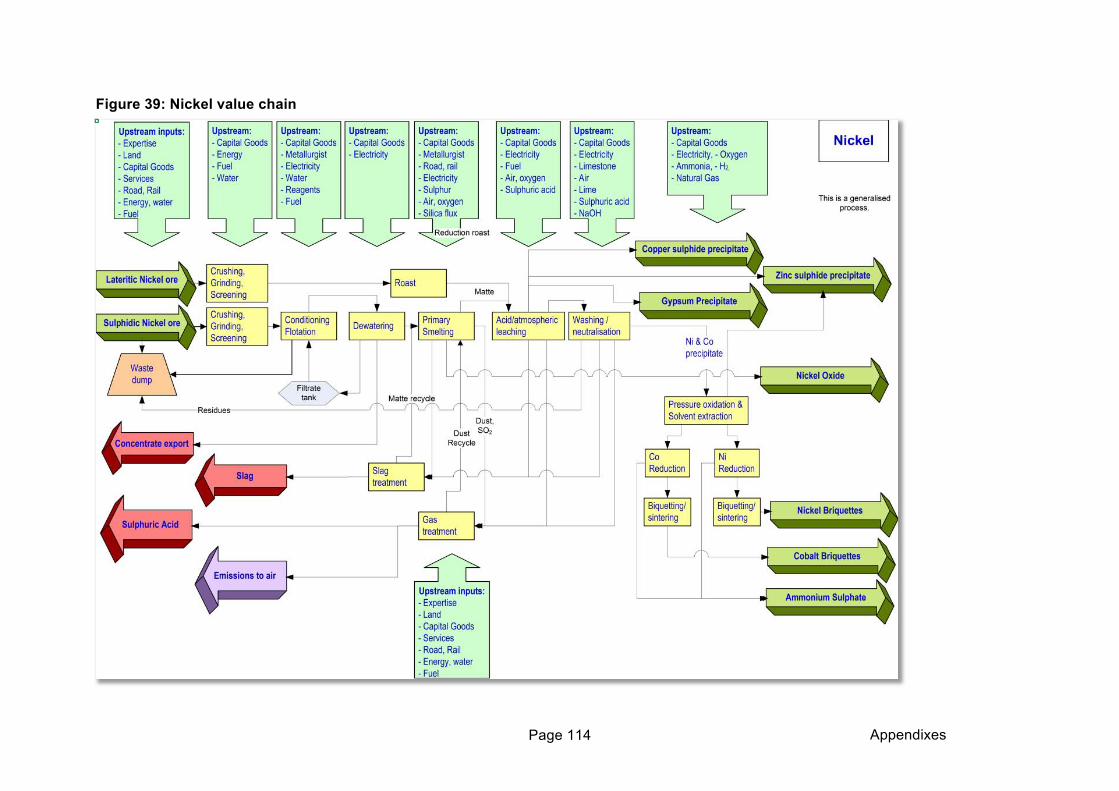

Appendix E Nickel value chain ........................................................................... 113

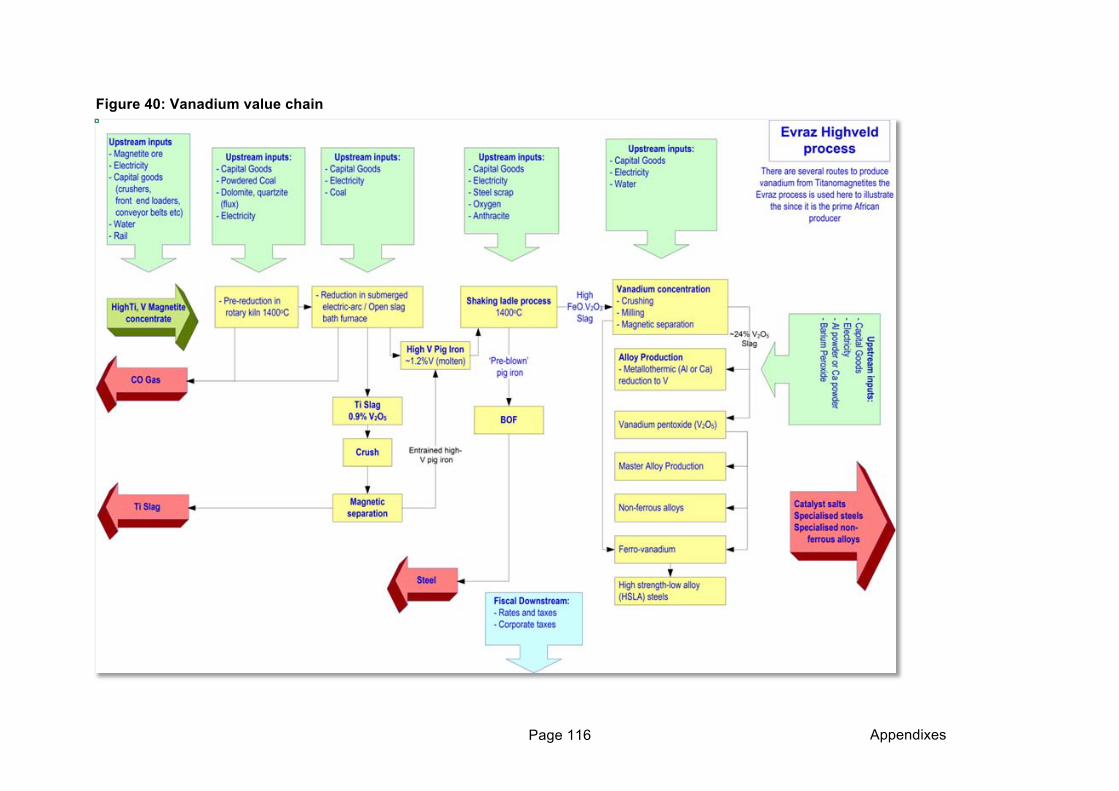

Appendix F Vanadium value chain .................................................................... 115

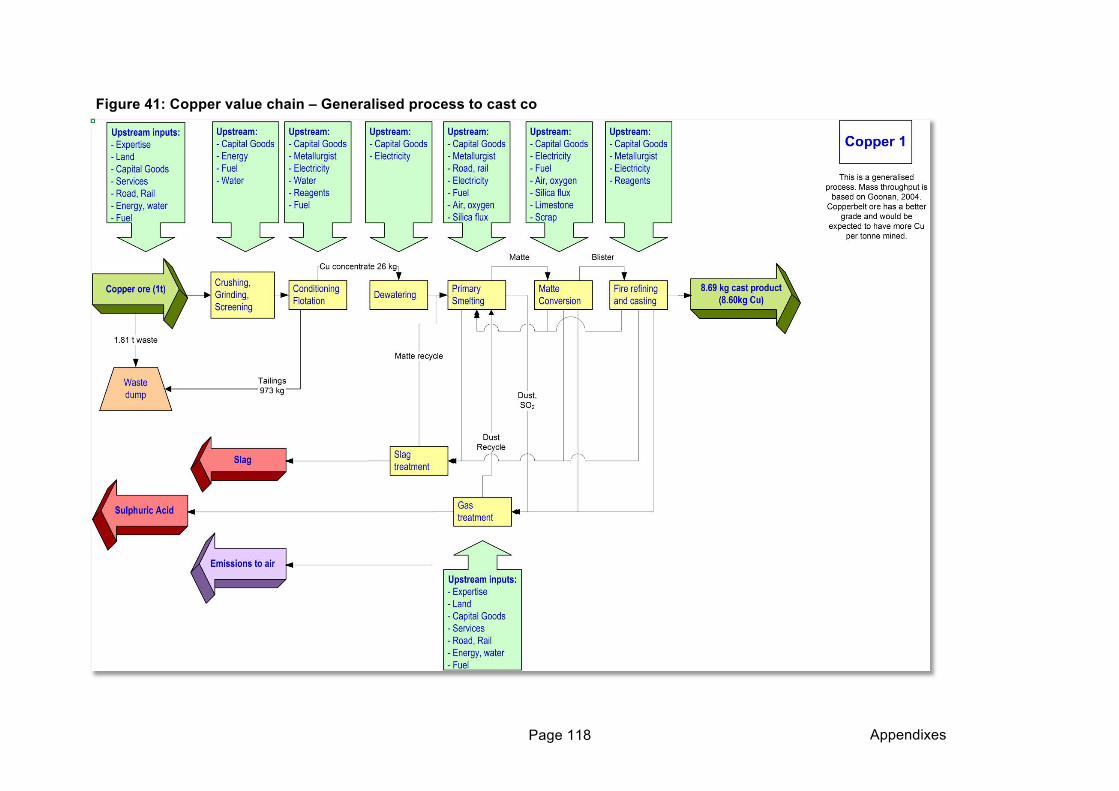

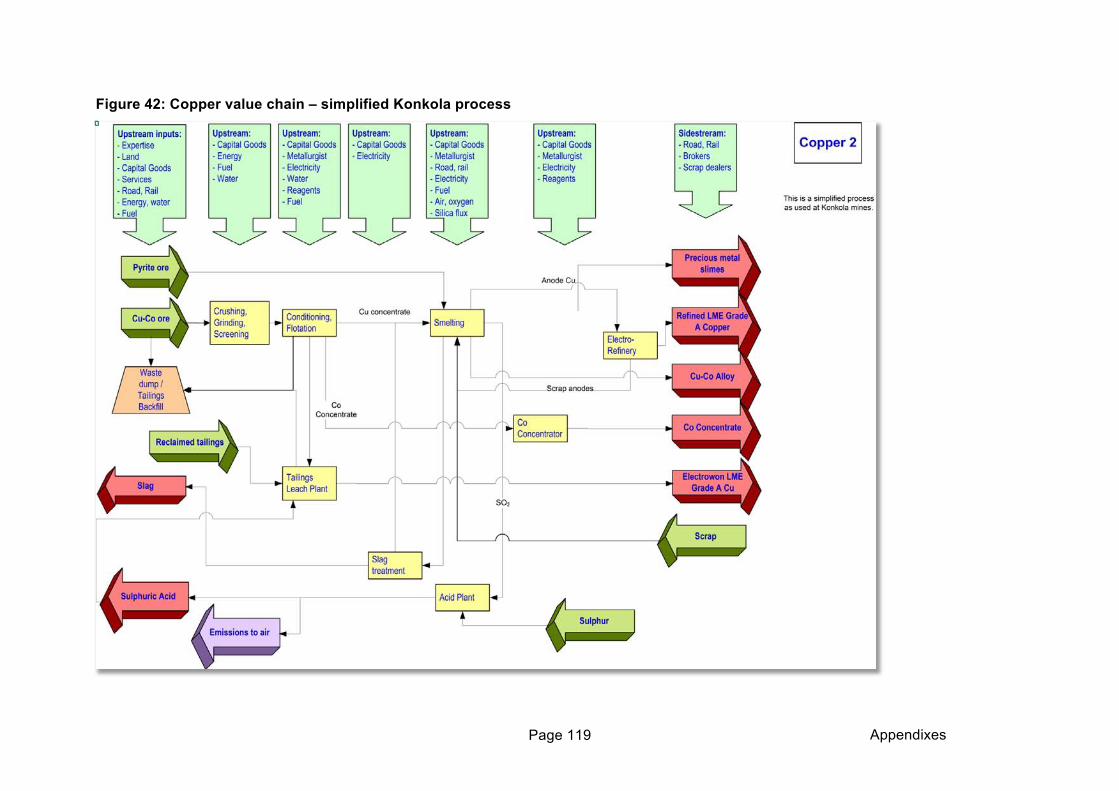

Appendix G Copper Value Chain ........................................................................ 117

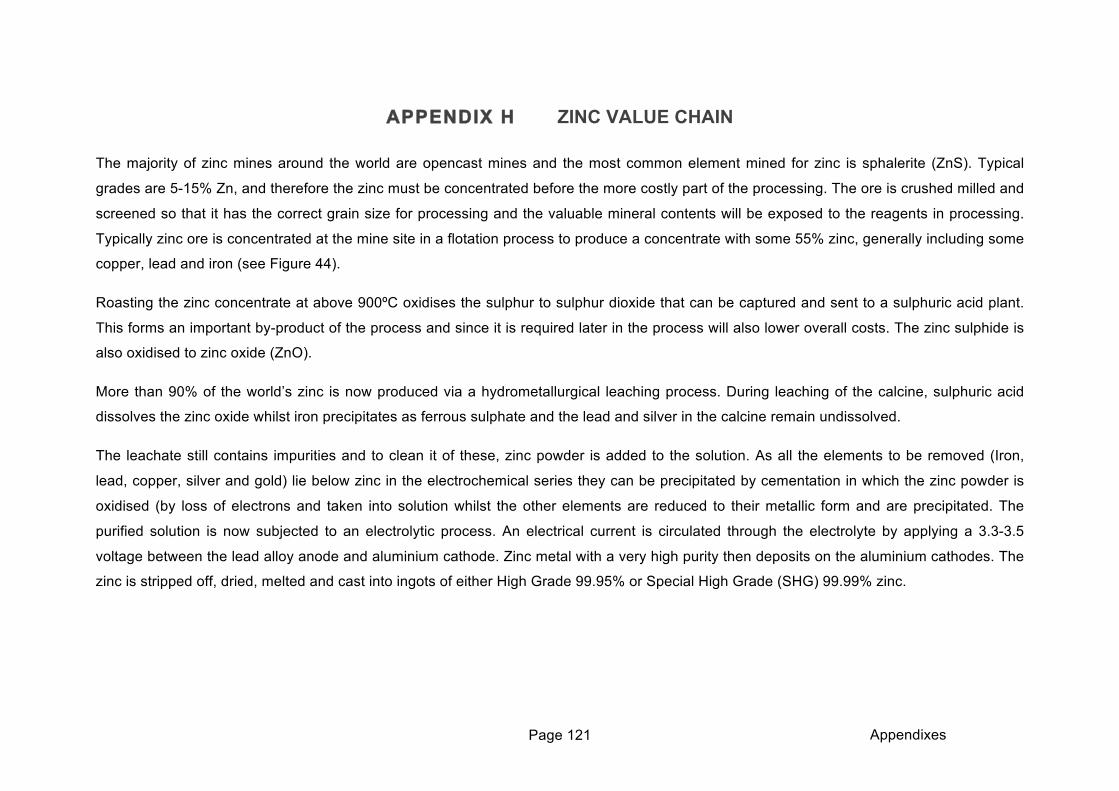

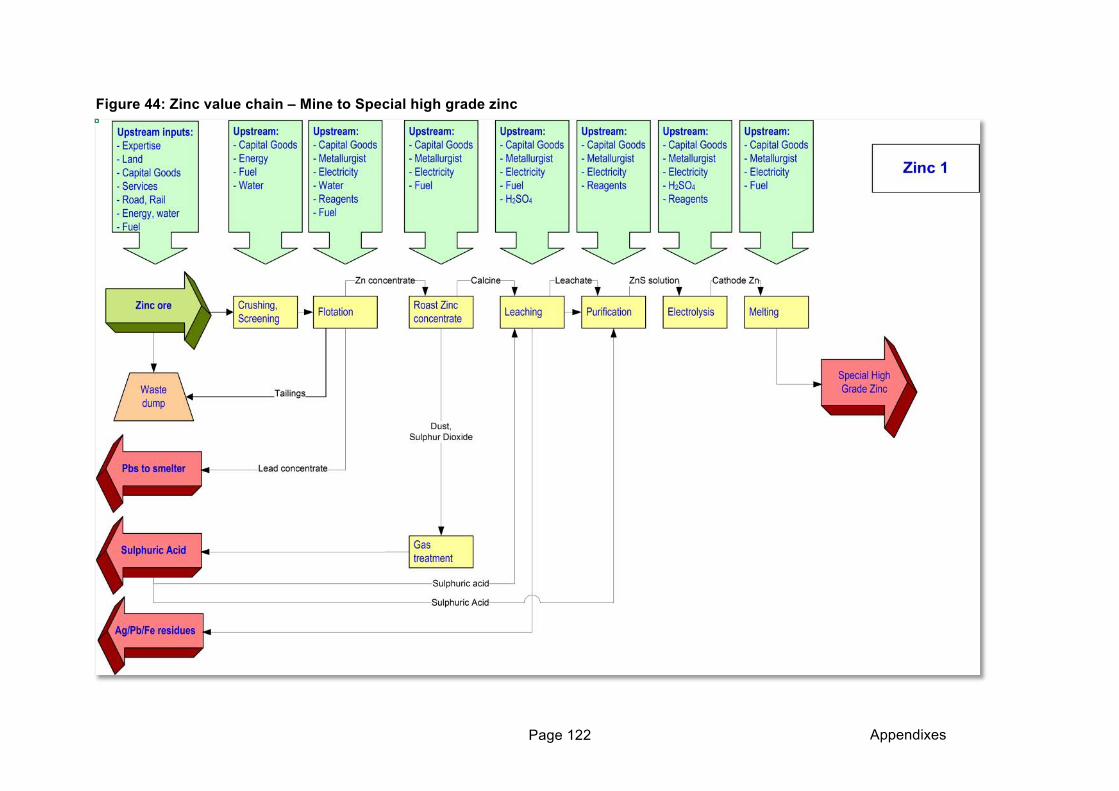

Appendix H Zinc Value Chain ............................................................................. 121

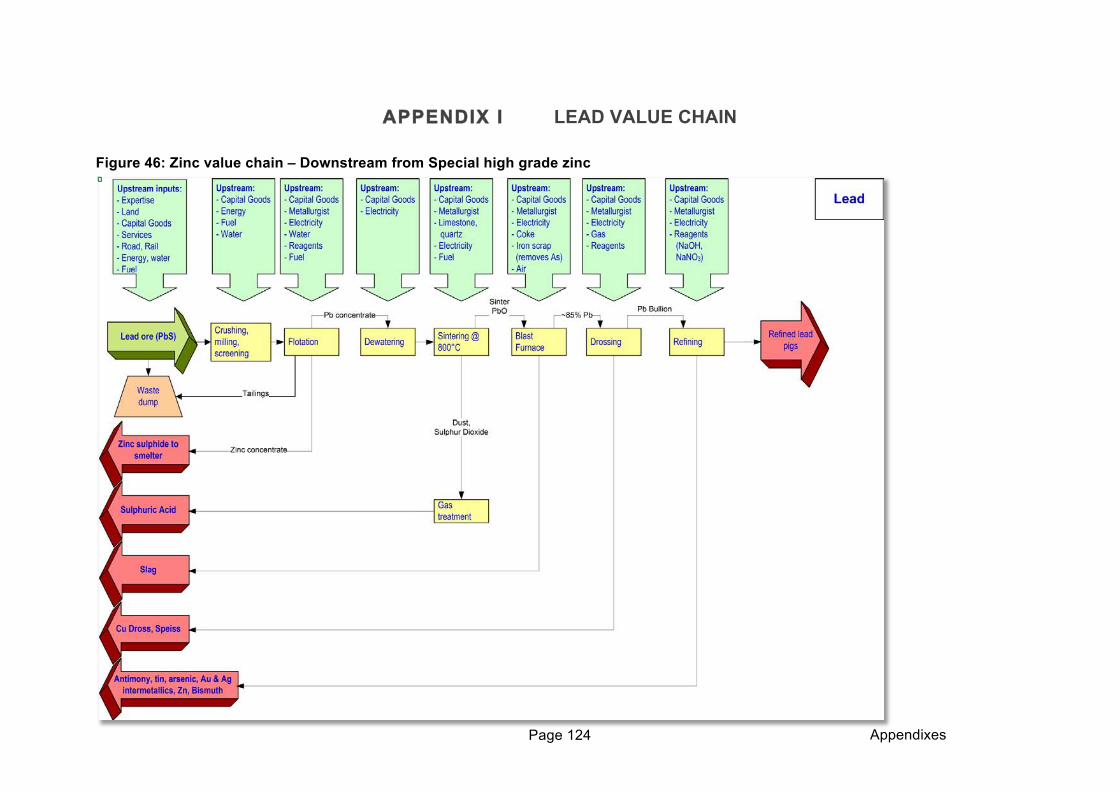

Appendix I Lead Value Chain ............................................................................. 124

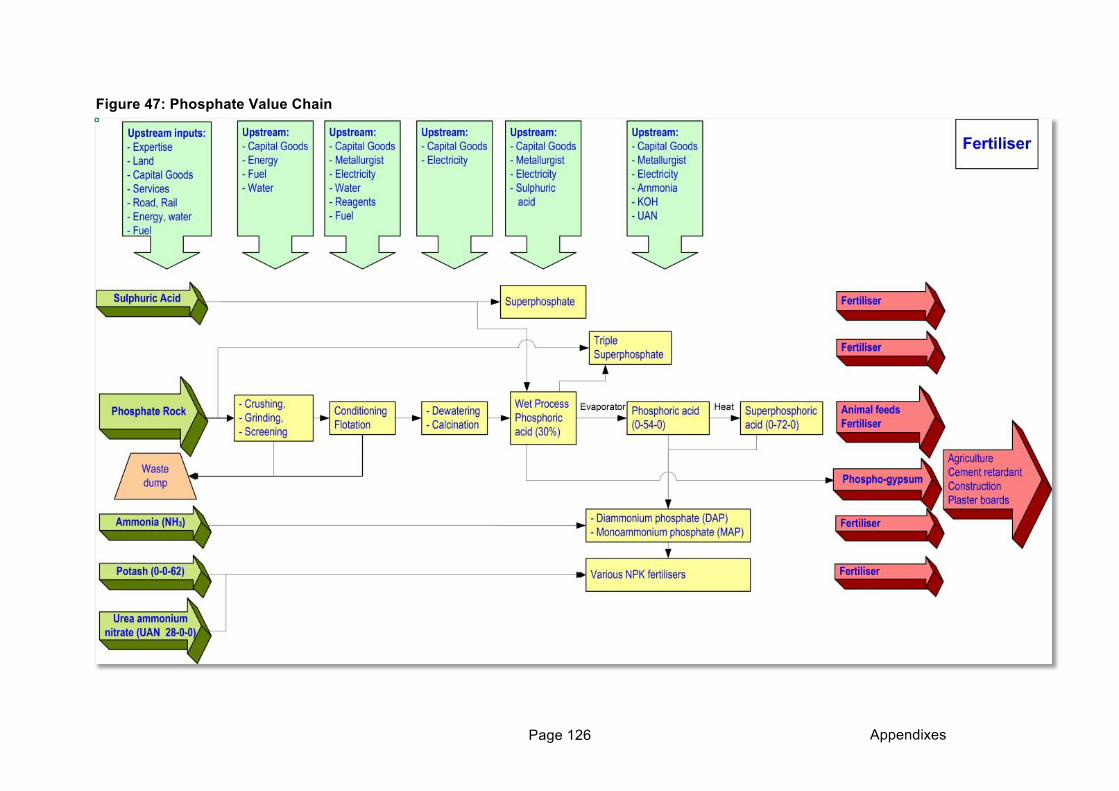

Appendix J Phosphate Value Chain ................................................................... 125

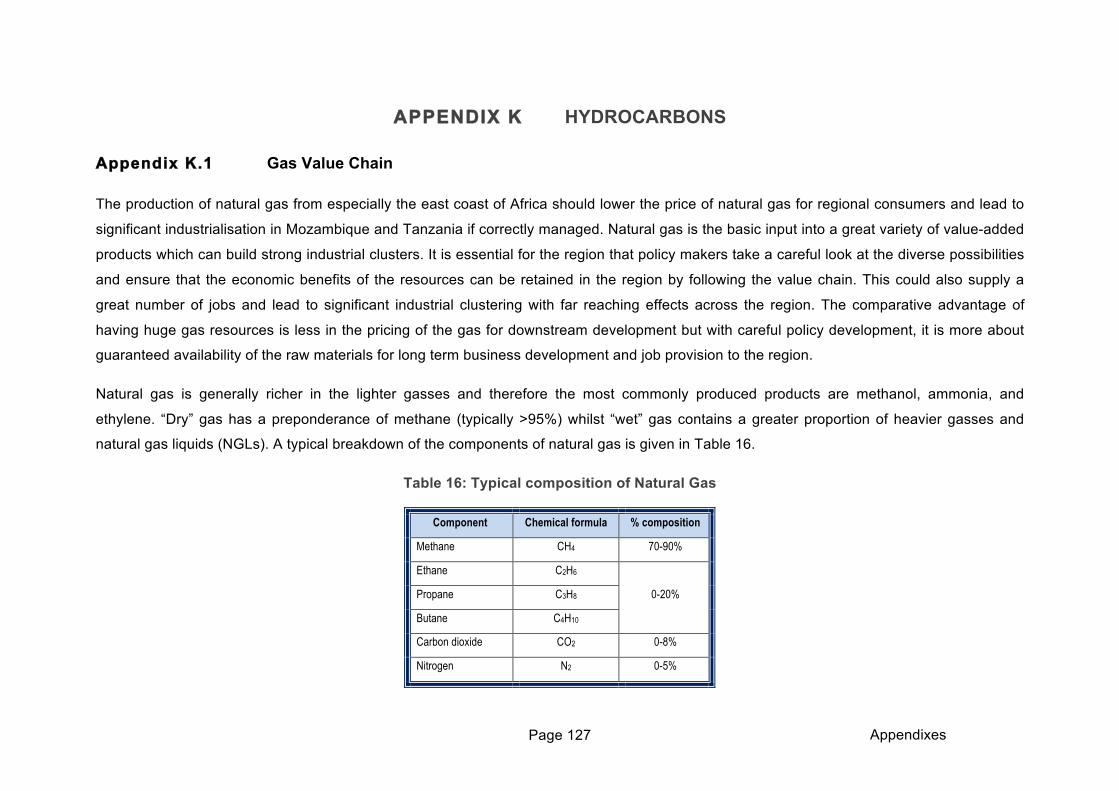

Appendix K Hydrocarbons ................................................................................. 127

Appendix L Direct opportunities ........................................................................ 139

Page viii

List of Figures

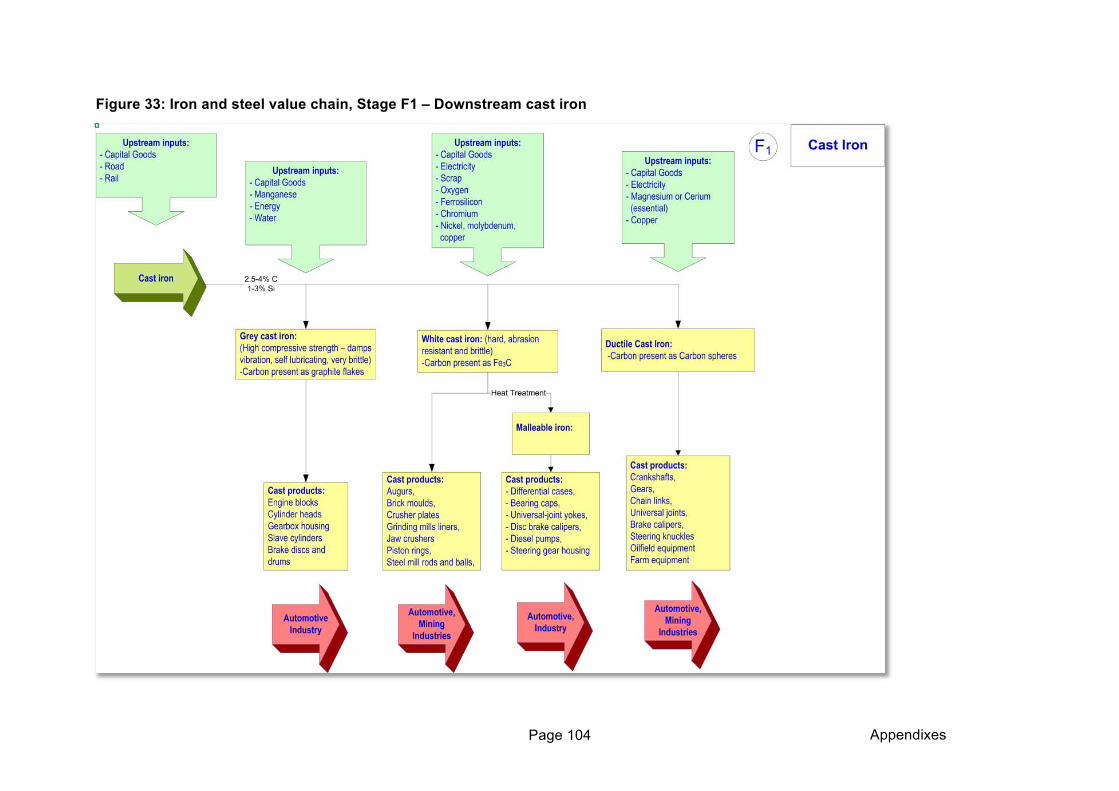

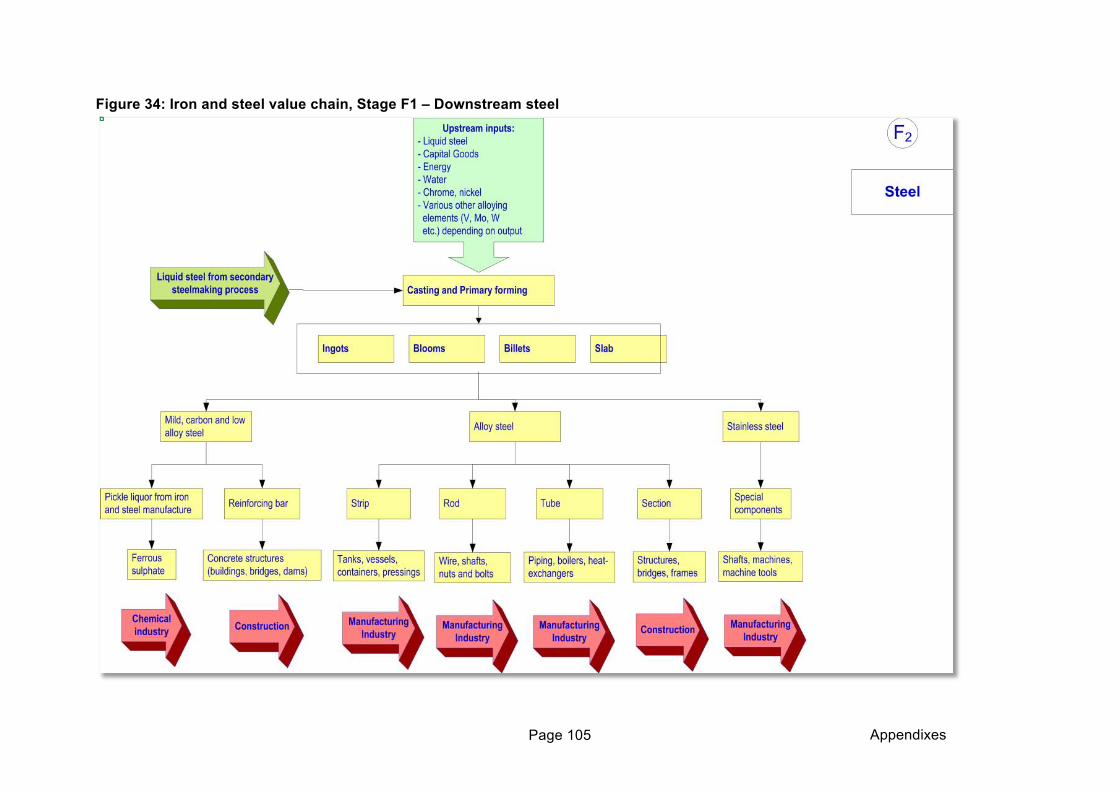

Figure 1: Relative Australian Wage levels ............................................................................... 3 Figure 2: Terms of trade for commodities versus manufactured goods .................................. 5 Figure 3: Primary commodity Prices and their piecewise linear trends, 1900-2010 ................ 5 Figure 4: Linkages in the wood and timber sector ................................................................... 9 Figure 5: Chamber of Mines four stage beneficiation process .............................................. 10 Figure 6: Resource related Gross Value Added (Australia) ................................................... 12 Figure 7: Mining industry expenditure (ZAR ‘M), *2011 ......................................................... 17 Figure 8: Monetary and fiscal linkages .................................................................................. 19 Figure 9: Proposed gas pipeline ............................................................................................ 33 Figure 10: Broad mineral commodities value chain ............................................................... 38 Figure 11: Generic mineral commodities value chain with broad inputs ................................ 39 Figure 12: Manufacturing contribution to GPD ...................................................................... 40 Figure 13: Economy wide impact of the South African mining sector in 2012 ....................... 40 Figure 14: Interlinkage of services with manufacturing in the global value chain .................. 43 Figure 15: Colour coding for growth pole diagrams ............................................................... 47 Figure 16: Tete Value Chain .................................................................................................. 50 Figure 17: Government revenue (in $ M) due to coal mining ................................................ 51 Figure 18: Rovuma Value Chain ............................................................................................ 57 Figure 19: Lephalale/ Southern Botswana Value Chain ........................................................ 61 Figure 20: Copperbelt Value Chain ....................................................................................... 67 Figure 21: Zimbabwe steel Value Chain ................................................................................ 73 Figure 22: Potential LNG site locations ................................................................................. 78 Figure 23: Possible direct, indirect and induced employment from LNG production ............. 79 Figure 24: Songo Songo Value Chain ................................................................................... 80 Figure 25: Cabinda Value Chain ............................................................................................ 82 Figure 26: Kabanga / Burundi Growth pole ........................................................................... 84 Figure 27: Locality of growth poles ........................................................................................ 85 Figure 28: Iron and steel value chain, Stage A – Exploration and Discovery ........................ 95 Figure 29: Iron and steel value chain, Stage B – Proving discovery and development ......... 97 Figure 30: Iron and steel value chain, Stage C – Mining ....................................................... 99 Figure 31: Iron and steel value chain, Stage D – On-site concentration and extraction ...... 100 Figure 32: Iron and steel value chain, Stage E – Off-site refining ....................................... 103 Figure 33: Iron and steel value chain, Stage F1 – Downstream cast iron ........................... 104 Figure 34: Iron and steel value chain, Stage F1 – Downstream steel ................................. 105

Page ix

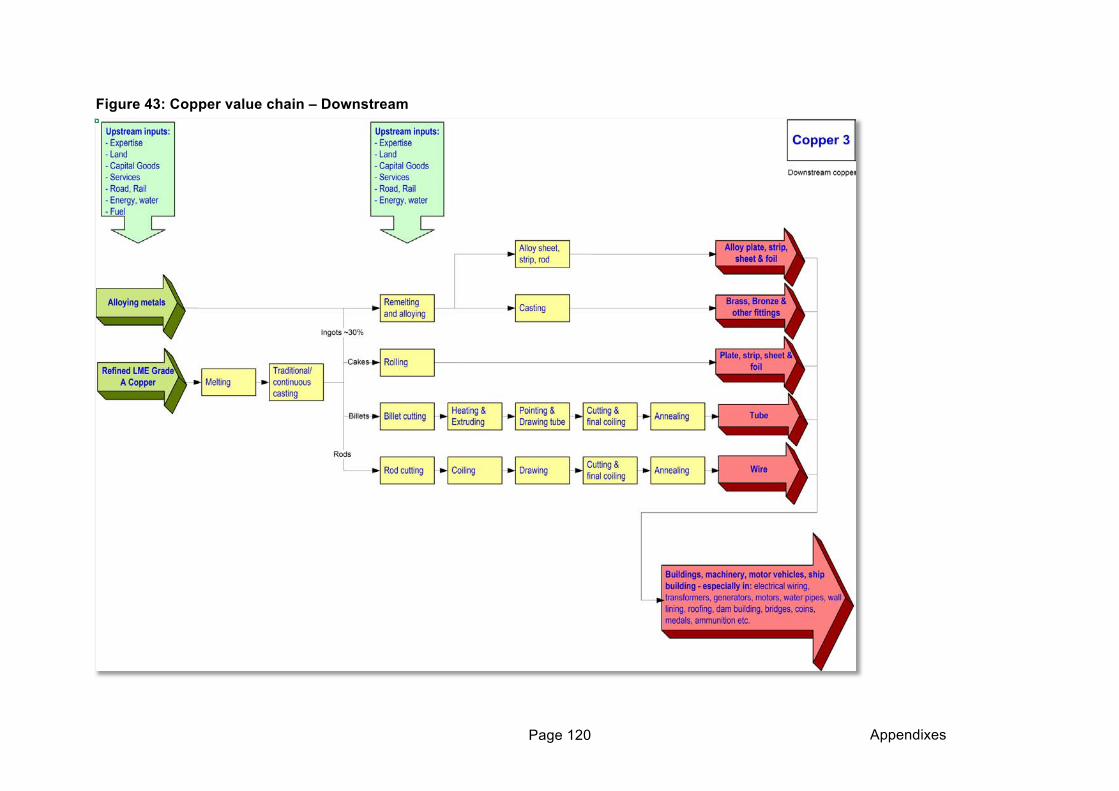

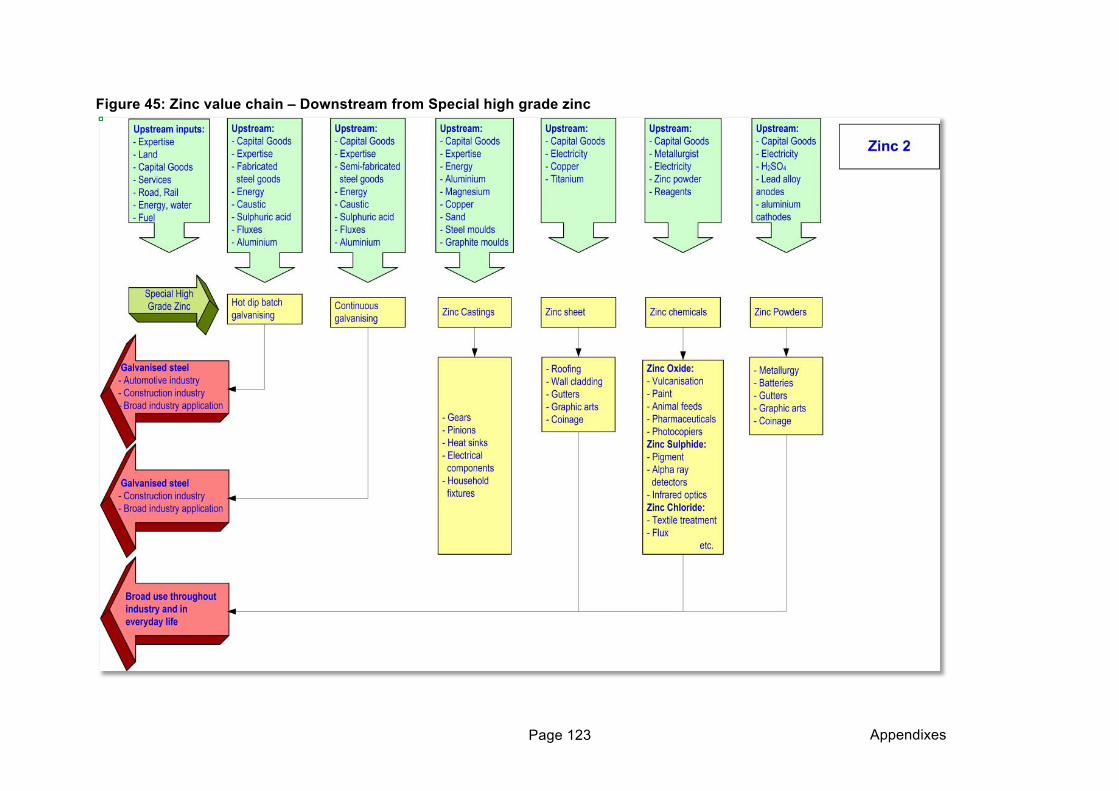

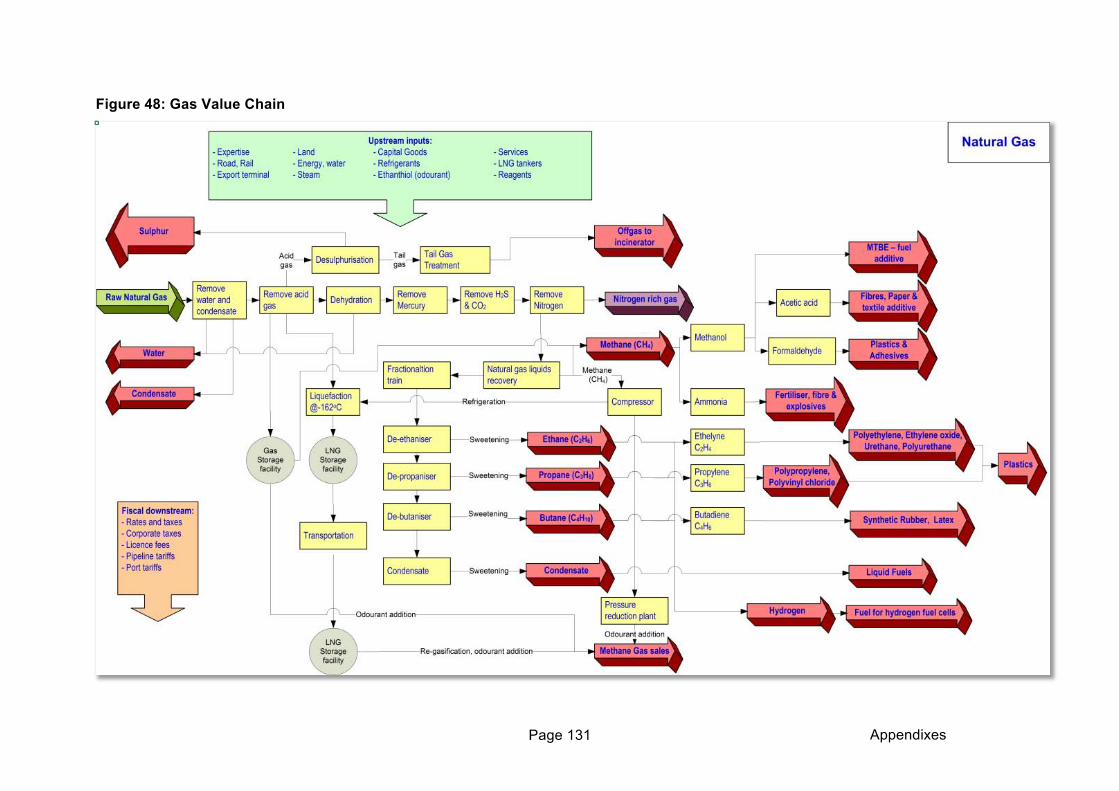

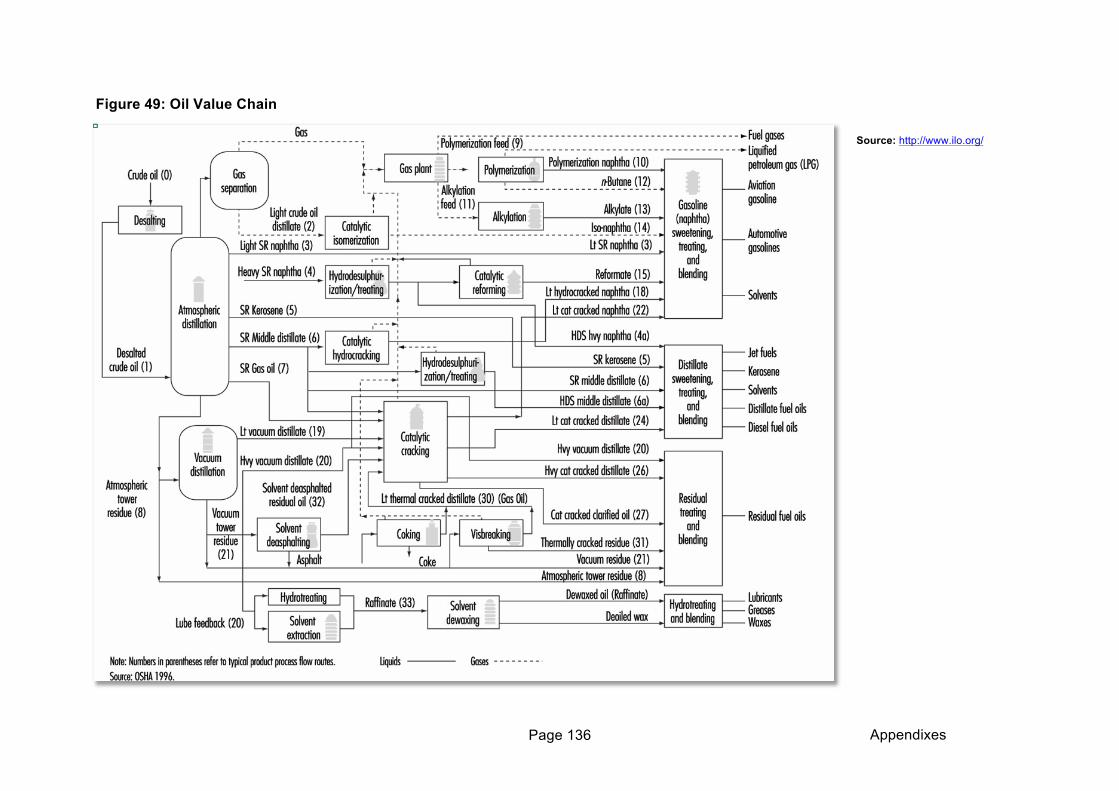

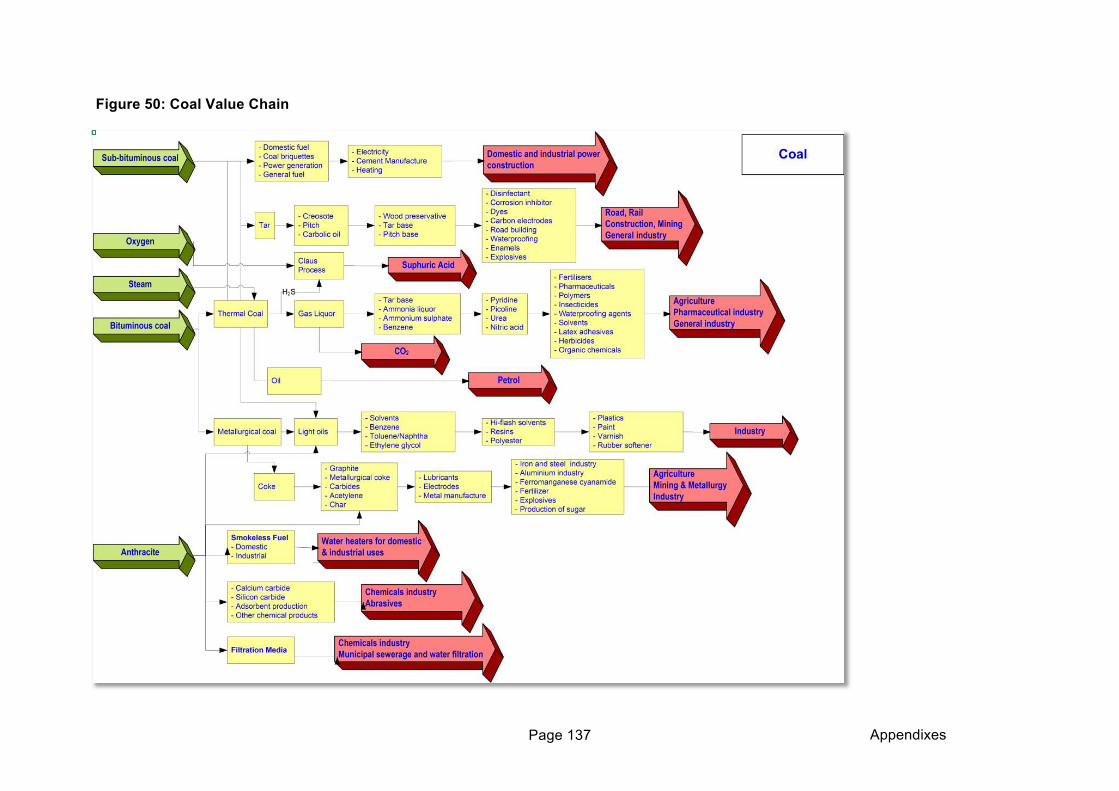

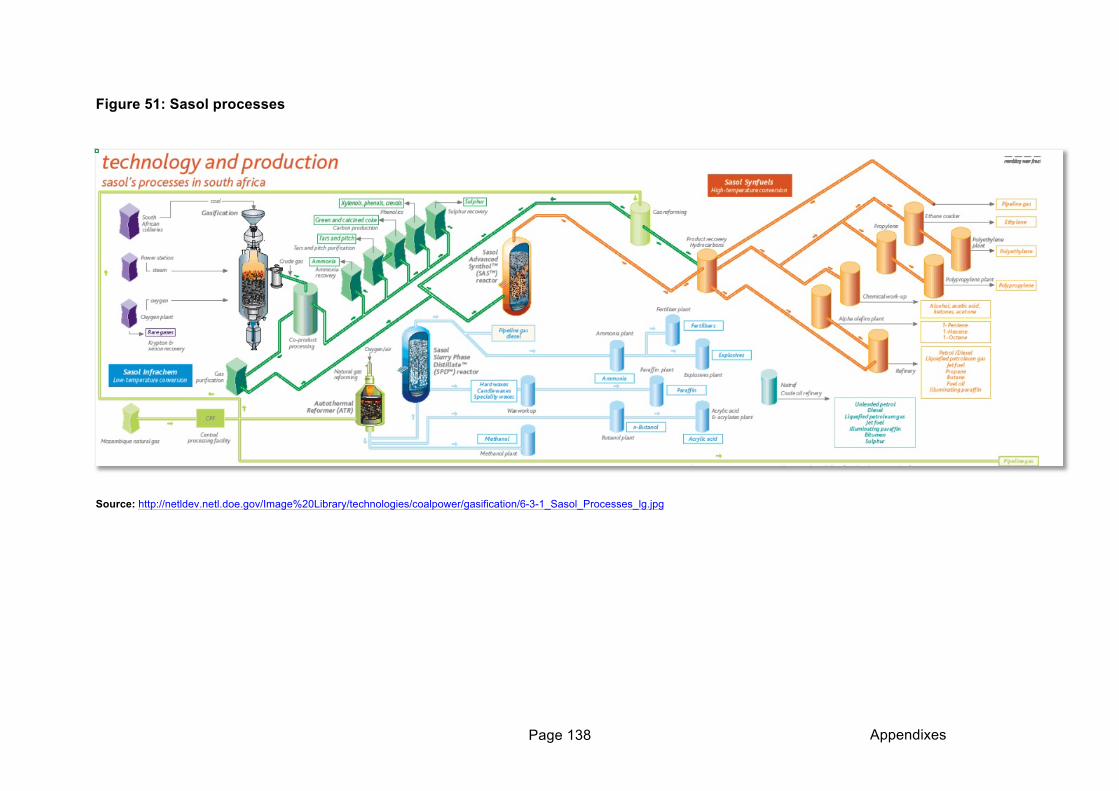

Figure 35: Chromite value chain – All grades ...................................................................... 108 Figure 36: Chromite value chain – Chemical Grade ............................................................ 109 Figure 37: Manganese value chain ...................................................................................... 111 Figure 38: Manganese value chain - Chemicals .................................................................. 112 Figure 39: Nickel value chain ............................................................................................... 114 Figure 40: Vanadium value chain ........................................................................................ 116 Figure 41: Copper value chain – Generalised process to cast co ....................................... 118 Figure 42: Copper value chain – simplified Konkola process .............................................. 119 Figure 43: Copper value chain – Downstream .................................................................... 120 Figure 44: Zinc value chain – Mine to Special high grade zinc ............................................ 122 Figure 45: Zinc value chain – Downstream from Special high grade zinc ........................... 123 Figure 46: Zinc value chain – Downstream from Special high grade zinc ........................... 124 Figure 47: Phosphate Value Chain ...................................................................................... 126 Figure 48: Gas Value Chain ................................................................................................ 131 Figure 49: Oil Value Chain ................................................................................................... 136 Figure 50: Coal Value Chain ................................................................................................ 137 Figure 51: Sasol processes ................................................................................................. 138

Page x

List of Tables

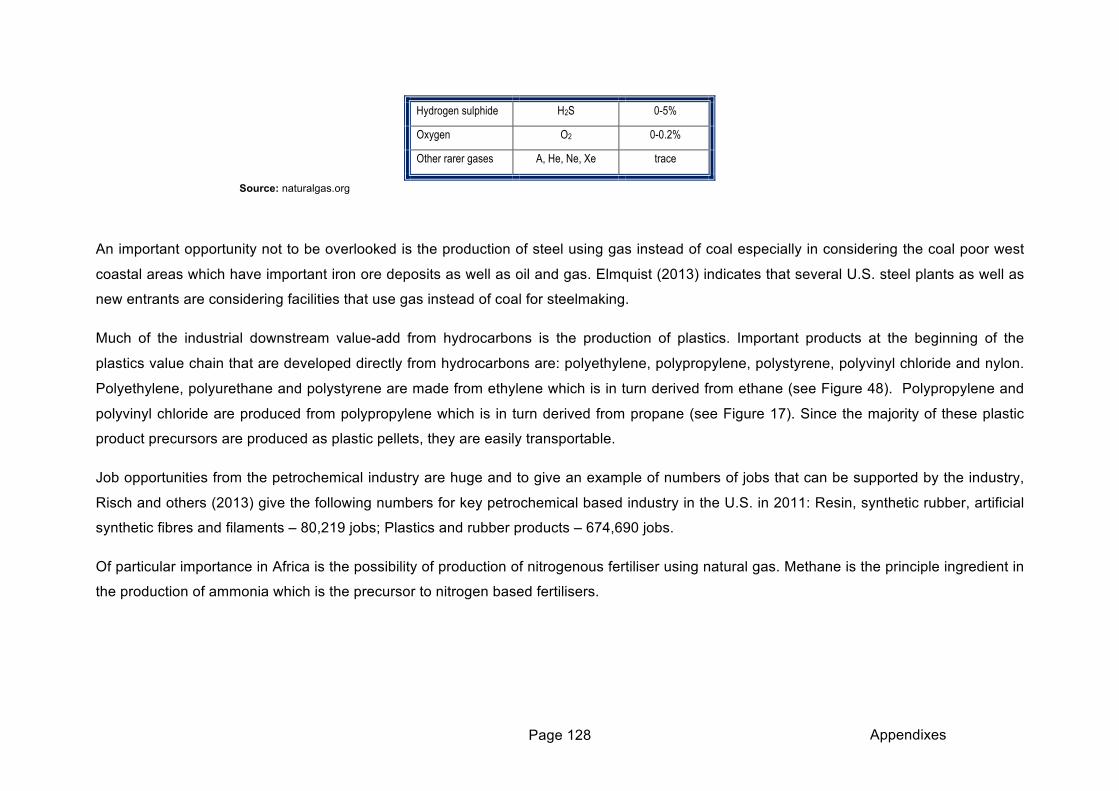

Table 1: Size Ratings ............................................................................................................. 25 Table 2: Status Ranking ........................................................................................................ 26 Table 3: First sort ................................................................................................................... 27 Table 4: Expert rating by likelihood of attracting new fixed investment ................................. 27 Table 5: Second sort .............................................................................................................. 28 Table 6: Deposits related to the Tete growth pole ................................................................. 47 Table 7: Deposits related to the Rovuma/ Mtwara growth pole ............................................. 54 Table 8: Potential Mozambique domestic projects ................................................................ 55 Table 9: Government revenues from shared profits .............................................................. 58 Table 10: Deposits related to the Lephalale / Southern Botswana growth pole .................... 59 Table 11: Unconstrained coal export and revenue projection for Botswana coalfields ......... 63 Table 12: Deposits related to the Copperbelt growth pole ..................................................... 64 Table 13: Deposits related to the Zimbabwe iron and steel growth pole ............................... 72 Table 14: Deposits related to the Northern Cape growth pole ............................................... 74 Table 15: Deposits related to the Songo Songo growth pole ................................................ 77 Table 16: Typical composition of Natural Gas ..................................................................... 127

Page 1 2 Growth Poles and value chains

1 INTRODUCTION

This introductory section reviews some of the topics that have led to the formulation of the

industrial growth pole project.

Over time there have been several attempts at understanding the development of diverse

industrialised economies, none of which appear to have been able to adequately explain all

development around the world. The need to understand and progress economic

diversification and industrial development in low to middle income economies is critical for

Africa, to assist the process of rapid development, to supply much needed jobs, and to

protect Africa from ongoing poverty and civil strife. A recent book by Morris, Kaplinsky and

Kaplan (2012), has taken an in-depth look at industrialisation and it proposes that the most

should be made of the commodity boom to promote industrialisation on the continent. The

thinking that is behind this book is seen to be largely in line with that of the author and it

represents a clear and concise summary of the discussion on African industrialisation.

Notwithstanding the results of the recently published work of Martinez and Mlachila (2013) in

which they showed that, broadly speaking, the quality of growth has “unambiguously”

improved in Sub Saharan Africa over the past 15 years, now being “stronger, less volatile,

accompanied by productivity improvements, more broad-based, and more export-oriented”;

Africa still has a long way to go especially in relation to the nature of its exports.

Morris and others (2012) also point out that Africa's situation with regard to industrial

potential and GDP has shown signs of real change since the turn of the century, with GDP

growth between 2000 and 2010 at 4.7%, outstripping the global growth rate which was only

2.5%. Referring to Farooki and Kaplinsky (2012), they indicate that regardless of price

volatility, they expect commodity prices to continue being robust in the future "for some

years to come".

In the long term, and notwithstanding price booms, commodities have shown a relative drop

in price relative to manufactured goods. Morris and others (2012) support this traditional

view and give a short history of its development. They also recognise the recent reversal in

the terms of trade. However, in reviewing papers written over the past couple of decades on

the Resource Curse and Dutch Disease, they come to the conclusion that the real problem

affecting commodity rich countries may be rather a "commodities specialisation in an

economy with little or no history of industrial development". In this argument the leading

thinking of Wright and Czelusta (2004) is important; they state that most of the papers

Page 2 2 Growth Poles and value chains

advocating a resource curse equate mineral exports with resource abundance. They also

indicate that resource intensity was a pervasive feature in the industrial and technological

development of the United States, and furthermore that the minerals sector remains linked

today to technological knowledge and advances.

“Resource abundance was a significant factor in shaping if not propelling the U.S. path to

world leadership in manufacturing.” Wright and Czelusta (2004)

The path the U.S. followed was one of large scale investment in exploration and

transportation built on geological knowledge, with the concomitant development of mineral

extraction, refining and manufacturing technology (Wright and Czelusta, 2004). America

industrialised from a minerals base. Regardless of how the problem is couched in theory, the

result for Africa in practical terms is similar; Africa must industrialise and must do so soon,

since it is unlikely that any other route will lead to long term, steady economic growth and, as

stated by the Commission on Growth and Development (2008), it is only economic growth

that

“…can spare people en masse from poverty and drudgery. Nothing else ever has.”

The declining trend in the commodities : manufactured goods terms of trade (the Prebisch-

Singer hypothesis) has become weaker since around 2000, as the relative prices of primary

commodities increased (Yamada and Yoon, 2013) and appears to have been arrested, and

possibly reversed, because of improvement in commodities pricing due to enhanced

demand (Morris et al 2012). Add to this the fact that in many cases the best and easiest-to-

access deposits of minerals are coming to an end, and the fact that there tends to be a long

period before new (especially large, low grade) deposits can come on stream, and the future

looks positive for demand-driven pricing to remain robust. As to the reasons for the

increasing costs of exported commodities, one must not ignore the huge cost pressure

(especially due to labour and energy costs) of the last few years on miners throughout the

world – but perhaps most clearly in southern Africa.

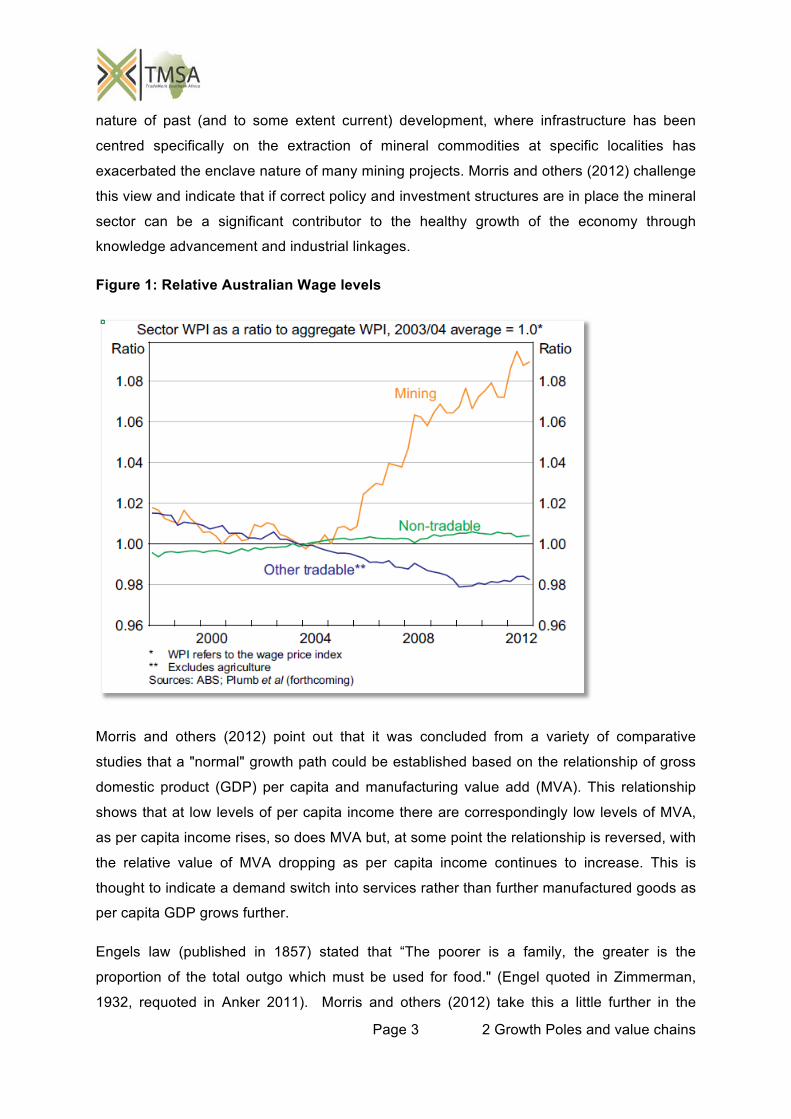

Bishop and others (2013) provide an excellent graphic summary of the wage increase in the

Australian mining sector relative to other sectors in the economy (see Figure 1). The higher

cost of mining now, relative to the 1990’s, indicates that it is unlikely that the price of

commodities will fall again to the levels seen pre 2000.

Morris and others (2012) discuss the contribution of Singer (1950) in which he hypothesised

the idea of enclave economies in which there was little scope for commodity driven linkages

in the low income, low technology, developing country in which the mining took place. The

Page 3 2 Growth Poles and value chains

nature of past (and to some extent current) development, where infrastructure has been

centred specifically on the extraction of mineral commodities at specific localities has

exacerbated the enclave nature of many mining projects. Morris and others (2012) challenge

this view and indicate that if correct policy and investment structures are in place the mineral

sector can be a significant contributor to the healthy growth of the economy through

knowledge advancement and industrial linkages.

Figure 1: Relative Australian Wage levels

Morris and others (2012) point out that it was concluded from a variety of comparative

studies that a "normal" growth path could be established based on the relationship of gross

domestic product (GDP) per capita and manufacturing value add (MVA). This relationship

shows that at low levels of per capita income there are correspondingly low levels of MVA,

as per capita income rises, so does MVA but, at some point the relationship is reversed, with

the relative value of MVA dropping as per capita income continues to increase. This is

thought to indicate a demand switch into services rather than further manufactured goods as

per capita GDP grows further.

Engels law (published in 1857) stated that “The poorer is a family, the greater is the

proportion of the total outgo which must be used for food." (Engel quoted in Zimmerman,

1932, requoted in Anker 2011). Morris and others (2012) take this a little further in the

Page 4 2 Growth Poles and value chains

explanation of the "normal" pattern of growth, indicating that as per capita income increases

consumers can add a greater amount of manufactured goods and ultimately services to their

spend. They also point out that the price elasticity of demand is an important part of the

equation, with substitutes often causing a drop in demand for primary commodities, if the

price becomes an incentive for such technological development. Furthermore, lack of skills

and technological barriers tend to slow down the progress of a nation from the production of

commodities to the production of industrialised goods. Following a similar path to other

economies that have made the transition (from commodity producer to manufactured goods

producer) in the past, may be difficult. There are a number of barriers, such as the cost of

transportation and the hurdle of trade liberalisation policies. Furthermore, the route of export

oriented industrial development becomes less and less attractive as each new nation comes

into competition, simply because the competition is too great especially when one competes

with a nation the size of China (Morris et al 2012).

In general, manufacturing and services are more labour intensive than mining and the first

stages of beneficiation (Morris and others (2012) call this "processing"). Furthermore, the

common occurrence of kleptocracy and violence indicates the urgency for resource rich

economies to build out their resource value chain and diversify outputs. The apparent terms

of trade reversal (see Figure 2) bodes well for low and middle income countries, since it

provides an opportunity to use the resource rents resulting from relatively good commodity

prices to fund diversification of the economies into new mineral commodities as well as the

production of industrial goods and the provision of services from the base of knowledge

developed in the minerals industry. It is important to note that the effect of this diversification

and movement into industrial commodities will lead to much more certainty in the economies

since it is well known that prices for value added goods tend to be much less volatile than

those for the raw materials. However, to use the opportunity requires quick and centred

reaction since it has no guarantee of lasting. As an example of this reversal, the Australian

terms of trade increased by 82% between 2003/4 and September 2011, from which time it

has again dropped by 17%. The improvement in Australia’s terms of trade has already given

rise to a surge of resource investment to meet demand and make best use of the opportunity

(Bishop et al, 2013).

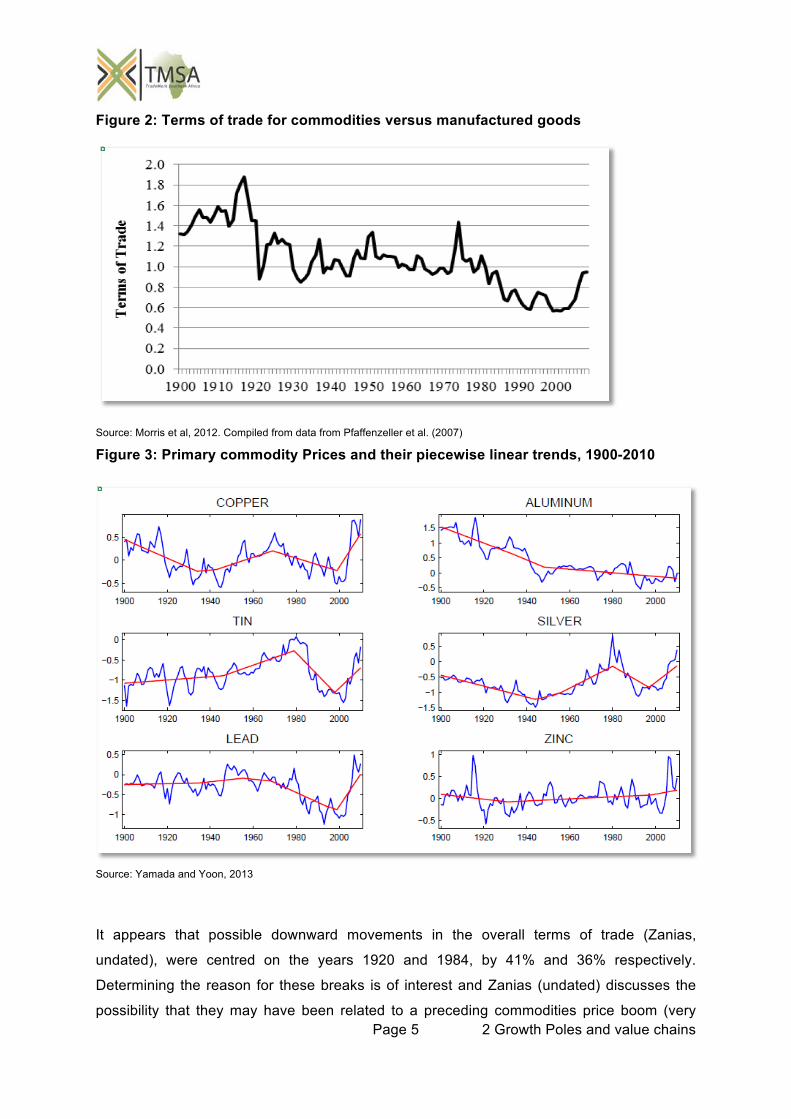

In discussing the change in terms of trade between commodities and manufactured goods, it is important to understand that

this was possibly not just a gentle decline over time, but rather that the relationship may have changed historically in “structural

breaks” (Zanias, undated). Yamada and Yoon (2013) have had another look at the Prebisch-Singer hypothesis with the Grilli

and Yang (1988) dataset extended to 2010. They conclude that there is little evidence that the Prebisch-Singer hypothesis

holds all of the time, but that it does hold sometimes for primary commodities. Their primary commodity prices and piecewise

linear trends for mineral commodities are given in

Page 5 2 Growth Poles and value chains

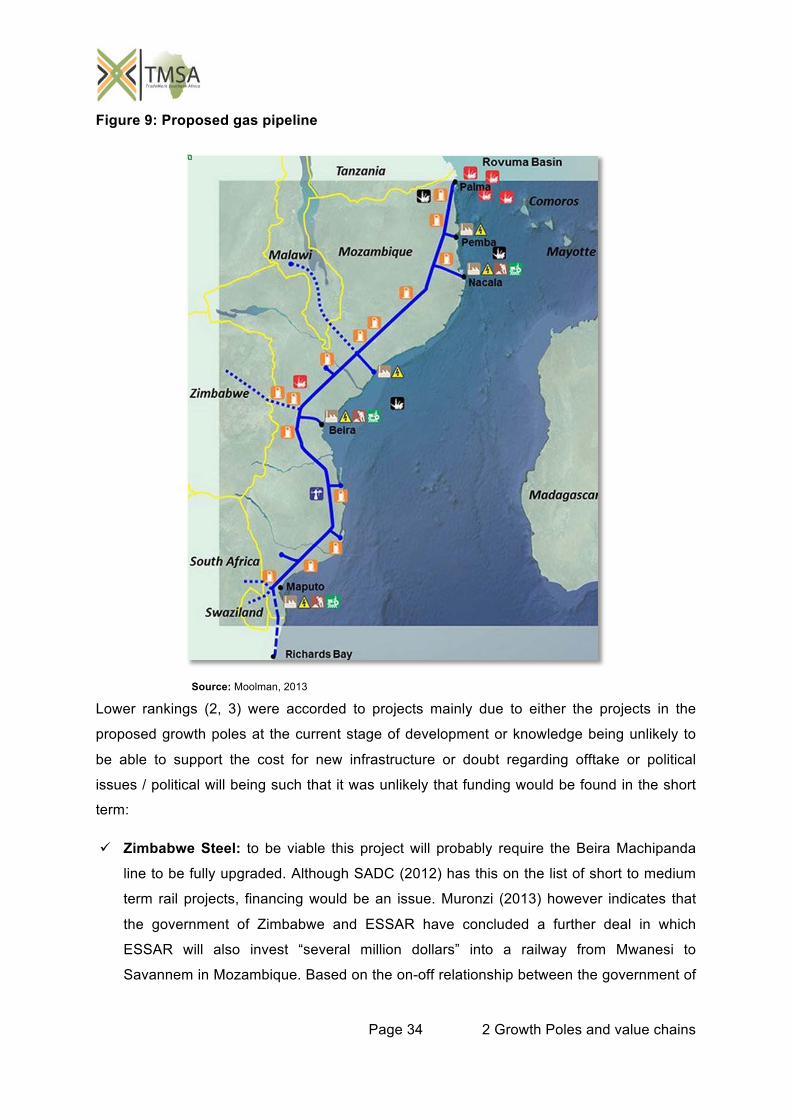

Figure 2: Terms of trade for commodities versus manufactured goods

Source: Morris et al, 2012. Compiled from data from Pfaffenzeller et al. (2007)

Figure 3: Primary commodity Prices and their piecewise linear trends, 1900-2010

Source: Yamada and Yoon, 2013

It appears that possible downward movements in the overall terms of trade (Zanias,

undated), were centred on the years 1920 and 1984, by 41% and 36% respectively.

Determining the reason for these breaks is of interest and Zanias (undated) discusses the

possibility that they may have been related to a preceding commodities price boom (very

Page 6 2 Growth Poles and value chains

clear in Figure 2). However the graph in Figure 2 extends into the current commodities price

boom – something Zanias did not have – and, if Zanias’ thesis is correct the questions that

then arise are:

How long will the boom last? and,

Does this imply another structural break? and if so,

Will it necessarily indicate that commodities prices will once again fall significantly

relative to manufactured goods? or,

Does the reversal in the terms of trade indicate a fundamental change due to increasing

global scarcity of commodities to support the burgeoning world population?

Regardless of the answers to the above questions the advice of Zanias (undated) remains

that developing resource intensive economies must diversify exports to reduce risk and

increase revenue. The challenge, as indicated by Morris and others (2012), is to "determine

which industrial and service sectors provide the greatest possibilities for development." It is

this challenge that is at the core of the current study.

It is perhaps pertinent to note here that the advice to diversify the economy of commodity

based countries is not universal. Tilton (2012) adds a word of caution in that some

economists may not, in his opinion, be looking at the full picture. He argues that the reason

for the long term falling terms of trade may be that costs in the production of primary

commodities have dropped. At the same time the improvements in manufactured products

produced may not be sufficiently taken into account by economists. Since a movement away

from the production of primary commodities would be counterproductive where production

costs are falling fast enough to counter the price drop, he advises that the suggestion that

countries should diversify away from such production “may very well be counterproductive,

encouraging countries to abandon what is a promising path to faster economic

development.” Tilton (2012). Contrary to this thinking, Pascal Lamy said, at the Hague on the

7th March 2013 at the “Conference on International Cooperation in 2020”, that virtually all

development and poverty reduction has included a high average rate of sustained growth,

inclusive of participation in international trade. He added that the essential ingredient for

resilient growth is “diversified productive capacity” (WTO News, 2013).

The call to diversify should not be seen as a call to diversify away from the production of

primary commodities, but rather an opportunity to use the comparative advantage to support

Page 7 2 Growth Poles and value chains

investment to allow diversification of the total offering, and also to be in the best position to

take the opportunity of increasing demand in future from developing economies that move

naturally to demand more manufactured goods and later more services. To add to this,

Bishop (2013) following the case made by Gregory (2011) points to a clear three-phased

structure to the resources boom, which he indicates is already in its second phase. The

three phases (which may overlap) are:

The boom in the terms of trade and the appreciation of the exchange rate;

The surge in resource investment; and

The subsequent growth in the production and export of resources.

Considering Bishop and others (2013) assessment of the phase of the boom and Zanias’

(undated) thesis on structural breaks, could lead to the view that it is likely that another

downward structural break is possible since the surge in resource investment may well lead

to a future oversupply as the Chinese market moves into a more evenly paced demand

scenario and eventually to a greater demand for services. This leads to further questions

regarding the vast numbers in China that would still aspire to move to cities. Kaplinsky and

Farooki (2010) estimate that the urbanised population in China will grow from 594 million in

2007 to 684 million in 2015 and 890 million in 2030, as well as the timing of a similar

developmental surge in India and later in Africa itself.

Notwithstanding any of these events, the movement in Africa into a more diversified offering,

especially one based on the beneficiation of its resources, still appears to make the best

case for future prosperity. Further supporting this conclusion is the work of Arezki and others

(undated) in which they find mixed support for the Prebish-Singer hypothesis, but with the

majority of piecewise regressions having a downward slope. In their work covering data

since 1650 they find a considerable number of structural breaks as well as clear volatility

especially in recent years. Amongst their remedies for the decline of relative primary

commodity prices is “to diversify into manufactures and services for which the country

concerned has comparative advantages” (Arezki et al, undated).

It is interesting to note that, notwithstanding Bishop and others (2013) description of what is

happening in the Australian environment, Ventyx (2012) indicates that the industry as a

whole is cautious in regard to the strength of the global economic recovery after the

Eurozone shock, and that investment in the mining sector is focussed more on expansion of

existing sites than on development of new sites. Furthermore, rather than finding qualified

workers at any cost, the industry is focussing on safety and training of the current workforce

Page 8 2 Growth Poles and value chains

thus also improving performance. At the same time industry is moving in the direction of a

greater reliance on information technology and automation to improve efficiency in the face

of declining grades and increasing cost.

1.1 Terminology

In their discussion of linkages Morris and others (2012), refer to the work of Hirschman

(1981). Hirschman considered three types of linkages: fiscal linkages, consumption linkages

and production linkages. These linkages are variously interpreted within the literature but

here they will be seen as follows:

Fiscal linkages will be seen to include royalties and licence fees on companies as well

as taxes on profits of companies and on wages and salaries to their employees,

Consumption linkages refer to the demand generated by employees, based on earned

incomes, for outputs of the commodities and other sectors,

Production linkages are inclusive of

Upstream or backwards linkages, referring to inputs to be used in the commodities

sector and,

Downstream or forwards linkages, referring to production of outputs of commodities

through various stages of value addition into semis, intermediate and finished products

for use in the industrial sector or final usage

Sidestream or horizontal linkages, referring to linkages developed directly from the core

business, or its upstream or downstream components, which develop the capability to

move into other value chains, inclusive of services, power and transport infrastructure

(rail, roads and ports)

This study will concentrate on production linkages.

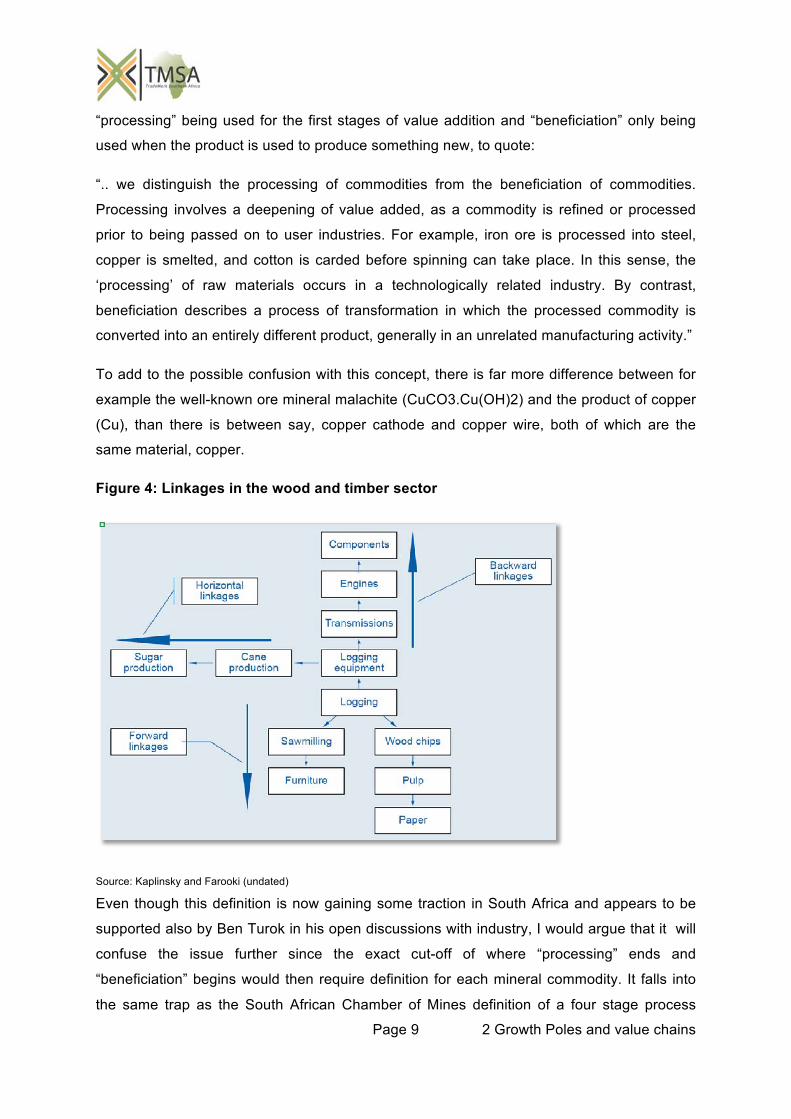

Production linkages are well illustrated by the logging example given in Kaplinsky and

Farooki (undated), and shown here in Figure 4.

Morris and others (2012), try to draw a line between “processing” and “beneficiation” in a

way that may be confusing, since it does not accord with general understanding of these

terms. Generally in the Southern African minerals sector the term “beneficiation” applies to

any stage of value addition to an ore or mineral mined. Throughout much of the rest of the

world the term “beneficiation” applies only to that part of the value addition chain which takes

place on the mine. Morris and others (2012), however, use the concepts differently with

Page 9 2 Growth Poles and value chains

“processing” being used for the first stages of value addition and “beneficiation” only being

used when the product is used to produce something new, to quote:

“.. we distinguish the processing of commodities from the beneficiation of commodities.

Processing involves a deepening of value added, as a commodity is refined or processed

prior to being passed on to user industries. For example, iron ore is processed into steel,

copper is smelted, and cotton is carded before spinning can take place. In this sense, the

‘processing’ of raw materials occurs in a technologically related industry. By contrast,

beneficiation describes a process of transformation in which the processed commodity is

converted into an entirely different product, generally in an unrelated manufacturing activity.”

To add to the possible confusion with this concept, there is far more difference between for

example the well-known ore mineral malachite (CuCO3.Cu(OH)2) and the product of copper

(Cu), than there is between say, copper cathode and copper wire, both of which are the

same material, copper.

Figure 4: Linkages in the wood and timber sector

Source: Kaplinsky and Farooki (undated)

Even though this definition is now gaining some traction in South Africa and appears to be

supported also by Ben Turok in his open discussions with industry, I would argue that it will

confuse the issue further since the exact cut-off of where “processing” ends and

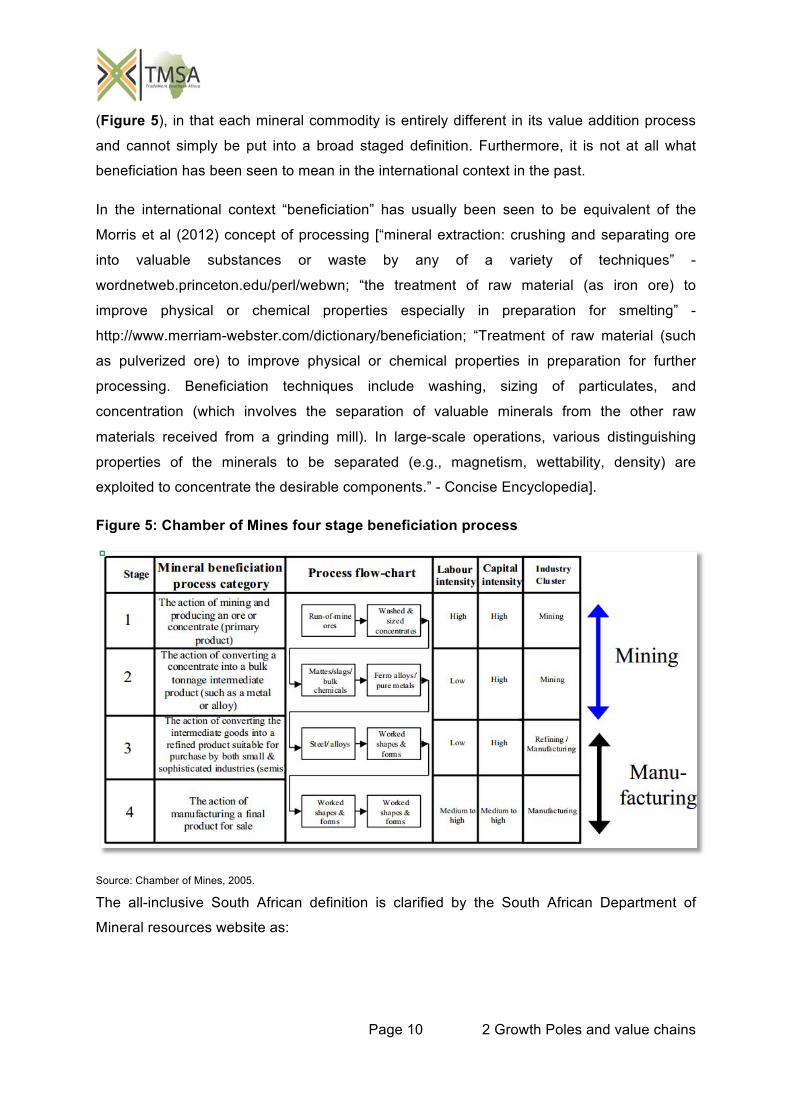

“beneficiation” begins would then require definition for each mineral commodity. It falls into

the same trap as the South African Chamber of Mines definition of a four stage process

Page 10 2 Growth Poles and value chains

(Figure 5), in that each mineral commodity is entirely different in its value addition process

and cannot simply be put into a broad staged definition. Furthermore, it is not at all what

beneficiation has been seen to mean in the international context in the past.

In the international context “beneficiation” has usually been seen to be equivalent of the

Morris et al (2012) concept of processing [“mineral extraction: crushing and separating ore

into valuable substances or waste by any of a variety of techniques” -

wordnetweb.princeton.edu/perl/webwn; “the treatment of raw material (as iron ore) to

improve physical or chemical properties especially in preparation for smelting” -

http://www.merriam-webster.com/dictionary/beneficiation; “Treatment of raw material (such

as pulverized ore) to improve physical or chemical properties in preparation for further

processing. Beneficiation techniques include washing, sizing of particulates, and

concentration (which involves the separation of valuable minerals from the other raw

materials received from a grinding mill). In large-scale operations, various distinguishing

properties of the minerals to be separated (e.g., magnetism, wettability, density) are

exploited to concentrate the desirable components.” - Concise Encyclopedia].

Figure 5: Chamber of Mines four stage beneficiation process

Source: Chamber of Mines, 2005.

The all-inclusive South African definition is clarified by the South African Department of

Mineral resources website as:

Page 11 2 Growth Poles and value chains

“Beneficiation, or value-added processing, involves the transformation of a primary material

(produced by mining and extraction processes) to a more finished product, which has a

higher export sales value. Beneficiation involves a range of different activities including:

Large-scale, capital-intensive activities, such as smelting;

Sophisticated refining plants; and

Labour-intensive processes, such as craft jewellery, metal fabrication and ceramic

pottery.

Each successive level of processing permits the product to be sold at a higher price than the

previous intermediate product or original raw material and adds value at each stage.”

For the purposes of this study the following definitions will apply:

Mineral processing: that stage of adding value to the mined mineral or ore that typically

takes place at the mine site to make it saleable to manufacturers. This may vary in type of

process and the level of purity achieved and is dependent on the market.

Beneficiation: any process of recovering, extracting, concentrating, refining or further

processing of a mineral or ore into a mineral product with a higher value and / or utility. This

is inclusive of mineral processing, smelting and refining as well as value addition to the point

that an entirely new product is formed which does not owe its value primarily from the

mineral commodity, and is ready for sale on the open market.

This definition can still be considered to be variable across mineral commodities, it is

perhaps more useful than some of the narrower versions given above.

The concept of depth and breadth of linkages as discussed by Morris et al (2012) is useful.

The depth of the linkage relates to the degree of value that is added through the linkage,

whilst the breadth of the linkage refers to the range of connected activities feeding into or

from the linkage.

In the discussion by Morris and other (2012) on staples theory, they conclude that resource

extraction inevitably does lead to the development of infrastructure and, as a result, to

horizontal linkages which can benefit from the infrastructural build. They also argue that the

“Staples trap” of being caught in commodity specialisation is not inevitable and that a degree

of industrial development with forward and backward linkages usually results from resource

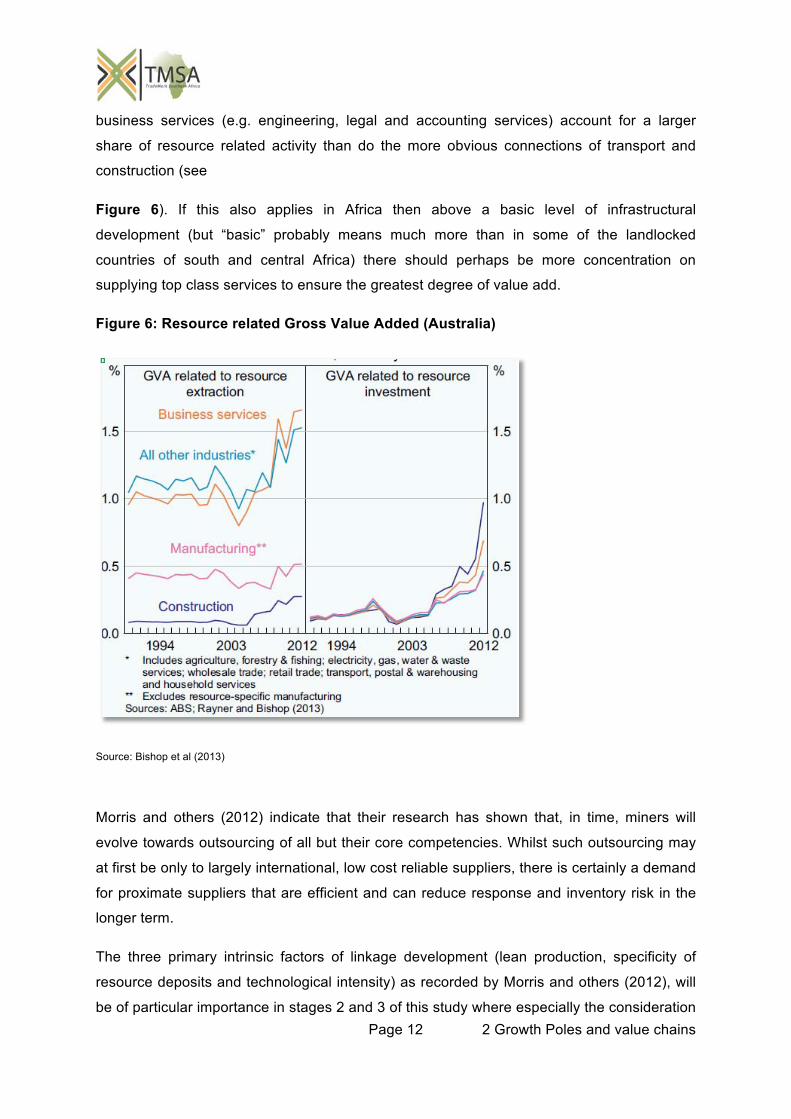

exploitation. Interesting here is the recent paper by Bishop et al (2013) which clarifies the

resource related gross value addition (GVA) in Australia. It is clear from their data that

Page 12 2 Growth Poles and value chains

business services (e.g. engineering, legal and accounting services) account for a larger

share of resource related activity than do the more obvious connections of transport and

construction (see

Figure 6). If this also applies in Africa then above a basic level of infrastructural

development (but “basic” probably means much more than in some of the landlocked

countries of south and central Africa) there should perhaps be more concentration on

supplying top class services to ensure the greatest degree of value add.

Figure 6: Resource related Gross Value Added (Australia)

Source: Bishop et al (2013)

Morris and others (2012) indicate that their research has shown that, in time, miners will

evolve towards outsourcing of all but their core competencies. Whilst such outsourcing may

at first be only to largely international, low cost reliable suppliers, there is certainly a demand

for proximate suppliers that are efficient and can reduce response and inventory risk in the

longer term.

The three primary intrinsic factors of linkage development (lean production, specificity of

resource deposits and technological intensity) as recorded by Morris and others (2012), will

be of particular importance in stages 2 and 3 of this study where especially the consideration

Page 13 2 Growth Poles and value chains

of specificity of resource will be important. The other two factors of lean production and

technological intensity are more generic to the development of linkages within the sector.

In framing the overall concept for this study it is important to see infrastructural attributes of

linkage development in their broadest sense and to be aware of the advantages that may

flow through from centred investment to not only the physical infrastructure (road, rail, ports,

pipelines, telecommunication and electricity networks) but also to the softer social

infrastructure (regulatory regime, administrative networks, educational facilities, institutional

development).

1.2 The real ability to grow an economy on a minerals base

The resource curse is both real and imaginary. It is real because, where governments do not

put the correct policy in place, or become corrupt, resource riches exported in an

unbeneficiated form from insular development leads to the negative effects of the Dutch

disease. However, it is imaginary in the sense that the effect is not due to the natural

resource wealth in itself, but rather to the attitudes that develop around the wealth and the

resultant lack of appropriate measures to ward off the negative effects which can come from

an over-reliance on the natural resource to build the economy. The problem in essence

relates to the fact that any other project will use a resource that has a raw material input cost

as well as capital and production costs. The raw material costs of an industry are supportive

of other industry. In the case of the production of natural resources this is not so and

therefore industries based on natural resources pass less direct external benefits to other

industry (Gylfason, 2001). The Dutch disease therefore does not exist where the state,

through careful and sensible policy and control measures ensures that the economic benefit

of the raw materials mined are ploughed back into the economy through the development of

backward linkages to related industry, local beneficiation of raw materials and taxation

policies which promote knowledge development and industrial growth. In discussing the

failure of most resource rich low to middle income countries to benefit significantly from

resource based development, Barbier (undated) states:

“The conditions for ensuring successful development have simply not been met. That is, in

most of today’s developing economies, frontier expansion has been symptomatic of a

pattern of economy-wide resource exploitation that generates little additional economic

rents, and what rents are generated, have not been reinvested in more productive and

Page 14 2 Growth Poles and value chains

dynamic sectors, such as resource-based industries and manufacturing, or in education,

social overhead projects and other long-term investments.”

The question may remain in the minds of readers: “But has it ever been done?”, and the

answer is simply “Yes, many times.” Most modern economies have at some point in the past

used their natural resource wealth to boost economic growth and development. Barbier

(undated) states that:

“Exploiting or converting new sources of relative abundant resources for production

purposes can be a dynamic process that causes economies to “take off.”

Two of these, The United States and South Africa will be briefly described.

1.2.1 United States

Wright and Czelusta (2004) show that successful resource based development is not

primarily a matter of geological endowment. In the late 19th and early 20th century when the

US became the world’s leading manufacturer, it was already the leading mineral economy.

US technological and industrial development was based on its resource endowment.

Large scale investments in exploration, transportation, geological and metallurgical

knowledge allowed early development of the countries mineral potential and lead to the

development of an industrial economy based on the knowledge and technological expertise

built on the mineral sector.

Where resource based economies have performed poorly, it has not been due to an

overemphasis of mineral wealth but rather due to a failure to properly develop their mineral

potential through appropriate policy (Wright and Czelusta, 2004).

Wright and Czelusta (2004) quote Benjamin Franklin as having said that there are no mines

in North America in 1790, however by 1913 the US was the dominant producer in the world

of most industrial minerals used at the time. During the period 1879-1914 the resource

intensity of the US exports increased at the same time as it was becoming the leading

manufacturing hub of the world. During this time the U.S. share of mineral production was far

in excess of its relative reserve potential. Wright and Czelusta (2002) refer to the essence of

the US success with their mineral endowment as follows:

“The American economy may have been resource abundant, but Americans were not

rentiers living passively off of their mineral royalties. Clearly the American economy made

something of its abundant resources. Nearly all major US manufactured goods were closely

Page 15 2 Growth Poles and value chains

linked to the resource economy in one way or another: petroleum products, primary copper,

meat packing and poultry, steel works and rolling mills, coal mining, vegetable oils, grain mill

products, sawmill products, and so on. The only items not conspicuously resource-oriented

were various categories of machinery. Even here, however, some types of machinery

serviced the resource economy (such as farm equipment), while virtually all were

beneficiaries in that they were made of metal. These observations by no means diminish the

country’s industrial achievement, but they confirm that American industrialization was built

upon natural resources.”

Herein also lies the blueprint for Africa today and the motivation for a project of this nature

which will attempt to find just those links that can assist the growth of an industrialised

economy based on a mineral endowment.

Referring to the 1997 paper by David and Wright, Wright and Czelusta (2004) indicate that

the rise of the US economy can be ascribed to:

An accommodating legal environment

Investment in infrastructure and public knowledge

Education in mining, minerals and metallurgy.

1.2.2 South Africa

South Africa changed in the late 19th Century from an essentially agricultural society to an

industrial society. This change took place at the same time (and as a result of) as the

discovery of diamonds and more significantly the discovery in 1886 of gold on the

Witwatersrand. Within 10 years of the discovery of gold, Johannesburg existed, 20 years

later it was already South Africa’s largest city and today it is the largest city and industrial

hub in Africa. The mining sector’s contribution to continued industrialisation of South Africa

has led to it being the most industrialised country in Africa at present.

This contribution by mining to the structural transformation of South Africa has been and can

still be significant. However, it requires constant attention to the regulatory and institutional

environment. Of particular importance is the removal of barriers (real and perceived) to the

development of new mines and especially to the expansion of a full value chain industry

based on mining in South Africa.

Mining in South Africa today is a well organised and highly regulated industry which makes a

significant contribution to national and regional development. In terms of job creation, mining

provided more than 513,211 direct jobs as well as an estimated 160,000 jobs directly linked

Page 16 2 Growth Poles and value chains

to the beneficiation of mineral commodities in 2011. This does not account for the number of

indirect jobs created. Generally indirect job development related to mining exceeds direct

employment (World Bank, 2002).

Economic growth already achieved due to mining in South Africa is best understood by

considering the size and overall vibrancy of the Gauteng region which is the largest inland

hub in the world built on the foundations of the mining industry.

The South African mining sector accounted for about 20% of private sector investment and

12.3% of total investment in 2011. Furthermore it made up some 29% of the allshare index

on the JSE (which itself has its roots in the mining sector). Since South Africa has had a

healthy growth of secondary and tertiary industry - largely based on mining - the overall

relative contribution to the GDP has contracted over the past two decades to 8.8% in 2011,

although it is close to 18% if services and associated industries are included (COM, 2012).

Total primary mineral exports accounted for 38% of South Africa’s total merchandise exports

(COM, 2012). If secondary beneficiated minerals are added then the minerals complex

accounted for about 50% of South Africa’s total merchandise exports (COM 2011).

Although much more can and should be done it is important to note that South Africa does

beneficiate a good deal of its mining output. A good example is the cement industry which

supplies more than 95% of local demand from locally mined limestone, gypsum and coal. In

the same way the steel industry which supplies about 80% of local demand from locally

mined iron, manganese, chromite, coal and coke, albeit at prices that could see

improvement. The furnaces involved in the steel making process are 95% powered by

electricity from coal fired power stations using locally mined coal. More than 30% of South

Africa’s liquid fuel requirements are produced from locally mined coal and more than 95% of

electricity is generated in coal fired power plants using locally mined coal. Furthermore, the

majority of domestic chemicals, fertilisers, waxes, polymers and plastics are fabricated using

locally mined mineral commodities and 13% of the world’s platinum catalytic converters are

produced locally (COM, 2012). In the case of gold and silver, South Africa has capacity to

produce pure gold and silver products both from local and imported concentrates. However,

although the COM estimated that, in 2010, some R200 b of value was added to South

African mineral products (COM, 2011), there is no doubt that there is still significant loss of

value by exporting mineral commodities too high up the value chain.

The value of mining in building an industrial society with backwards and horizontal linkages

as well as direct fiscal linkages is clarified in Figure 7.

Page 17 2 Growth Poles and value chains

1.3 Linkages

In each of the top chosen growth poles there will be a discussion of any particular linkage

opportunities that exist for the growth pole itself and which need directed attention. However

many linkages are generic to mining and these will not be generally repeated, rather they are

mentioned here as an overview of the type of linkage to consider. In the second stage of the

greater project specific project linkages should be unravelled in much more detail.

1.3.1 Monetary and Fiscal linkages

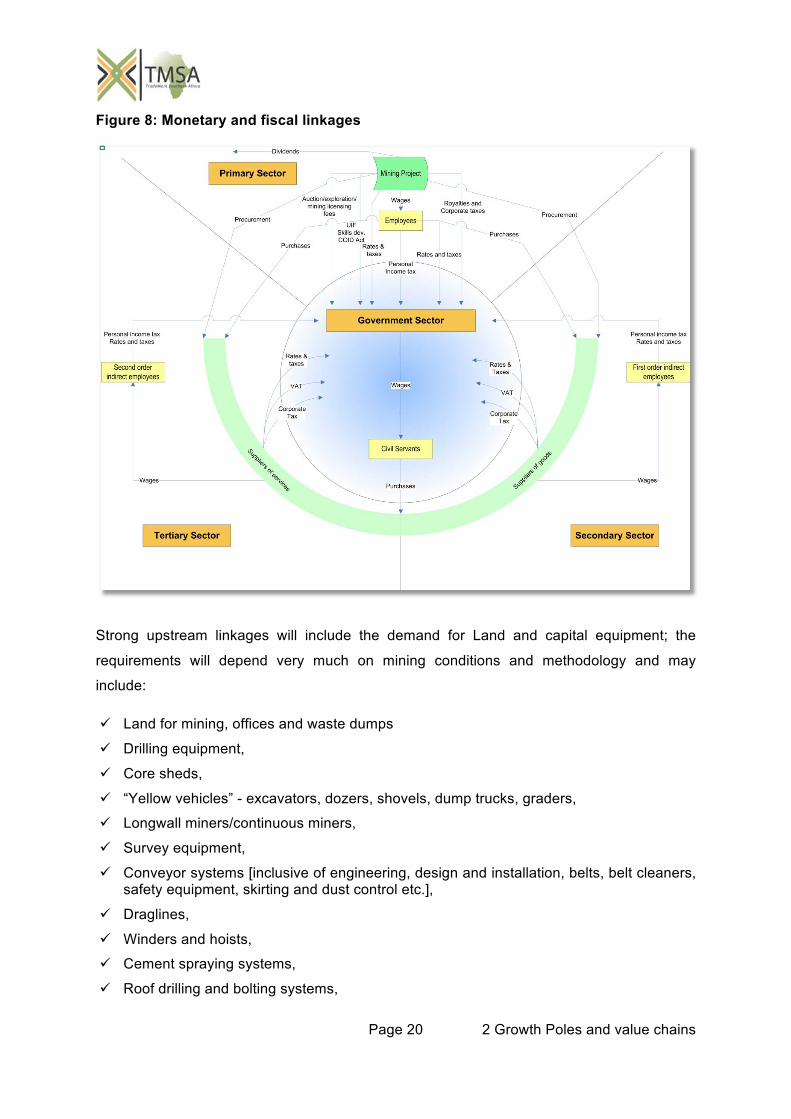

Exploration licence fees, mining licence fees, royalties, taxes on profits of companies, taxes

and on wages and salaries of mining company employees, VAT on employee purchases,

taxes on company profits and employees of linked business.

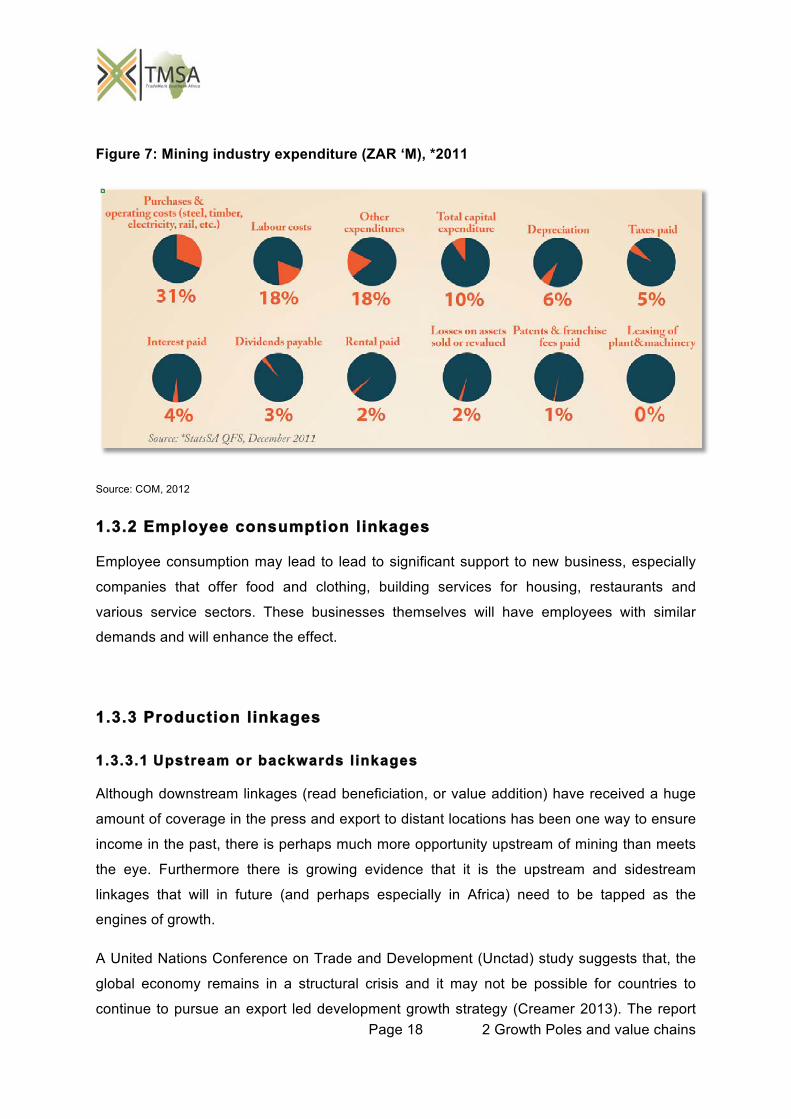

The monetary and fiscal linkages will vary somewhat from country to country dependent on the local taxation systems. An overview of possible linkages is shown in Figure 8.

Page 18 2 Growth Poles and value chains

Figure 7: Mining industry expenditure (ZAR ‘M), *2011

Source: COM, 2012

1.3.2 Employee consumption linkages

Employee consumption may lead to lead to significant support to new business, especially

companies that offer food and clothing, building services for housing, restaurants and

various service sectors. These businesses themselves will have employees with similar

demands and will enhance the effect.

1.3.3 Production linkages

1.3.3.1 Upstream or backwards linkages

Although downstream linkages (read beneficiation, or value addition) have received a huge

amount of coverage in the press and export to distant locations has been one way to ensure

income in the past, there is perhaps much more opportunity upstream of mining than meets

the eye. Furthermore there is growing evidence that it is the upstream and sidestream

linkages that will in future (and perhaps especially in Africa) need to be tapped as the

engines of growth.

A United Nations Conference on Trade and Development (Unctad) study suggests that, the

global economy remains in a structural crisis and it may not be possible for countries to

continue to pursue an export led development growth strategy (Creamer 2013). The report

Page 19 2 Growth Poles and value chains

argues that export led strategies are no longer viable. Instead a strategy, geared towards

generating a greater role for domestic and regional demand, should be pursued.

It is therefore essential to plan regional trade but especially to ensure that the upstream and

sidestream linkages related to the Tripartite’s comparative strength in mineral commodities is

captured wherever possible within the region. The increased regional wealth that will result

from a lower leakage into world markets will also increase the regional buying power and

thus improve the odds of growth led by trade within the region.

Page 20 2 Growth Poles and value chains

Figure 8: Monetary and fiscal linkages

Strong upstream linkages will include the demand for Land and capital equipment; the

requirements will depend very much on mining conditions and methodology and may

include:

Land for mining, offices and waste dumps

Drilling equipment,

Core sheds,

“Yellow vehicles” - excavators, dozers, shovels, dump trucks, graders,

Longwall miners/continuous miners,

Survey equipment,

Conveyor systems [inclusive of engineering, design and installation, belts, belt cleaners, safety equipment, skirting and dust control etc.],

Draglines,

Winders and hoists,

Cement spraying systems,

Roof drilling and bolting systems,

Page 21 2 Growth Poles and value chains

Refrigeration and ventilation systems,

Compressors,

Fans,

Explosive drilling and packing systems,

Backfill technology and equipment,

Communication systems,

Personnel transport [underground and surface],

Pulleys,

Pumps,

Battery packs and lighting systems for personnel,

Loading equipment,

Cranes,

Comminution and screening systems,

Tanks,

Piping,

Mine scheduling software,

Hydraulic valves,

Stockyard handling systems and equipment,

Tailings dam systems and equipment,

Rail siding equipment,

Railway coaches,

Laboratory analysis equipment,

Automated scanners (to monitor production quality),

Scales ,

Employee time management systems (clocking-in devices).

Mining is also an important purchaser of consumables such as:

Cables,

Cement,

Clay bricks (building),

Copper wire,

Electricity,

Explosives,

Fuel (mainly diesel),

First aid and emergency supplies and equipment,

Page 22 2 Growth Poles and value chains

Miners clothing and safety equipment supply, gloves, safety shoes, hard hats, reflective gear, earplugs, safety goggles etc.),

Oxygen,

Refractory Bricks (furnaces),

Roof supports and roof bolts,

Tyres,

Steel (various forms),

Vehicle spares,

Water.

1.3.3.2 Downstream or forwards linkages

Downstream linkages will depend mainly on the particular mineral commodities being

developed. See section 2.7 Value Chains as well the Appendices for a generic view of the

downstream linkages.

1.3.3.3 Sidestream or horizontal l inkages

Sidestream and horizontal linkages are likely to be reasonably specific for each growth pole

even at this concept level. In general these linkages will include rail, roads, ports, electrical

and water supply networks, information and communications technology (ICT) networks. A

strong banking sector and international trade sector will develop to directly serve the mining

companies; these will be available for the wider community. Hospitals and clinics may be

directly built by the mining sector or developed to serve them and these are likely to be

available to the wider community. This is also true of good schools and even possibly

technical colleges and universities, which although primarily developed to serve the families

of miners will be available for widespread use.

Besides being a major employer, the mining sector is also an important user of contracted

expertise in the services sector. Many of these services can be used across different

business types and therefore are seen as sidestream linkages. This may include services

such as:

Administrative services,

Builders,

Computer engineers, computer programmers, data typists,

Electricians and electrical engineers,

Environmental services,

Geological consultants,

Page 23 2 Growth Poles and value chains

Human resources consultants,

Insurance experts,

Laundry and repair services,

Lawyers,

Logistics systems and services,

Mechanical engineers, mechanics,

Plumbers,

Refrigeration engineers and artisans,

Security services.

1.4 Basis for the focus areas

The focus areas considered in this project relate to hydrocarbons (coal, oil and gas), ferrous

metals (iron, chrome, nickel and vanadium) and base metals (copper, lead and zinc) as well

as phosphates.

Hydrocarbons will still in the foreseeable future supply the majority of energy in the tripartite

and are known to have excellent backwards and forwards linkages if linked to industrial

development. Likely world demand for the raw materials from the east is also projected to

remain strong for many years to come from China and especially from India.

Ferrous metals make the backbone of any economy with iron being the most important metal

traded in the world today. Rapid development of the tripartite will require large quantities of

steel and the benefits of producing the steel locally are huge. Furthermore, the tripartite has

all the required raw materials for basic steel and stainless steel manufacture as well as the

manufacture of a host of special grades of stainless steel.

Base metals and in particular copper are also highly in demand in countries moving strongly

up the development curve since it is used in water and electrical installations in housing

developments. Again the demand in the east is strong, and in the case of copper this is

particularly the case in China and Japan.

Iron ore and coal in particular are high bulk materials and where these are to be exported

they will demand a considerable infrastructure build. The feedback loop of this infrastructural

development will greatly increase the demand for the chosen minerals commodities.

Phosphates may seem to be outside of the general grouping, but due to the expected rapid

growth of the African population the requirement for food and hence fertilisers in the future

will be considerable. Since the hydrocarbons can be used to develop ammonia and related

Page 24 2 Growth Poles and value chains

nitrogenous fertilisers the consideration of phosphates, in which Africa is particularly rich and

which forms an essential part of complete fertilisers becomes straightforward.

Page 25 2 Growth Poles and value chains

2 METHODOLOGY

2.1 Screening and clustering to define growth poles around mineral potential

In order to identify those deposits most likely to display economic potential, the most up to

date mineral deposit data that could be accessed was captured into a database and

subjected to an iterative screening process. This entailed searching for deposits in which

there has been some interest by companies in the literature and on the internet as well as

following up leads based on older databases that are available from various sources, prior

knowledge as well as personal communication with contacts in the field. In this process,

deposits were ranked by major commodity, deposit size and deposit status. The purpose of

the screening was to select deposits that could act as growth centres for the growth poles

and which are significant enough in themselves or together with others in the area to act as

growth poles. From these would then be chosen three projects to study at a more detailed

level in a second phase of the greater project.

2.2 Initial screening

In putting the database together there was an attempt to consider mainly those projects

where there is current private sector attention. This is not always a straightforward process,

since it is common practice to put projects “on hold”, especially in difficult economic times

such as we are currently experiencing. As a result projects in which the private sector has

lost interest or those which have not yet attracted real investment may also be included, but

certainly the majority of deposits in the database are currently producing mines or being

pursued by companies or have been actively pursued within the last five years. As a basis

for the synthesis and ranking of the mineral occurrences and deposits in the compiled

database, the following decisions were made:

Due to the size and time frame allowed for this project in certain cases areas of

mineralisation where recorded in the database rather than individual “deposits”. This is

especially true of the hydrocarbons, which are, to some extent, continuous over large

areas. However where only a few economic zones were known in such areas at this

stage the individual deposits were recorded, especially where information could be

gleaned on the project. This is also true where, for example, coal is known to be

Page 26 2 Growth Poles and value chains

preserved in localized graben structures rather than being widespread over an entire

coalfield.

Although the majority of the projects that made it onto the database are large, once on

the database projects of any size would be considered provided they had the promise of

being turned to account, as a part of a cluster of developments.

In the second stage of the growth pole study the greater project areas chosen as growth

pole possibilities should be scoured for other mineral opportunities which although

perhaps smaller or further from development will make a significant contribution to the

industrial development of the area.

The purpose of the exercise was not to generate high-risk exploration targets but to

identify prospects that are already being developed or have a good chance of being

developed within a relatively short space of time. Consequently, prospects for which

there were very little exploration information and did not hold much promise were given

a low ranking.

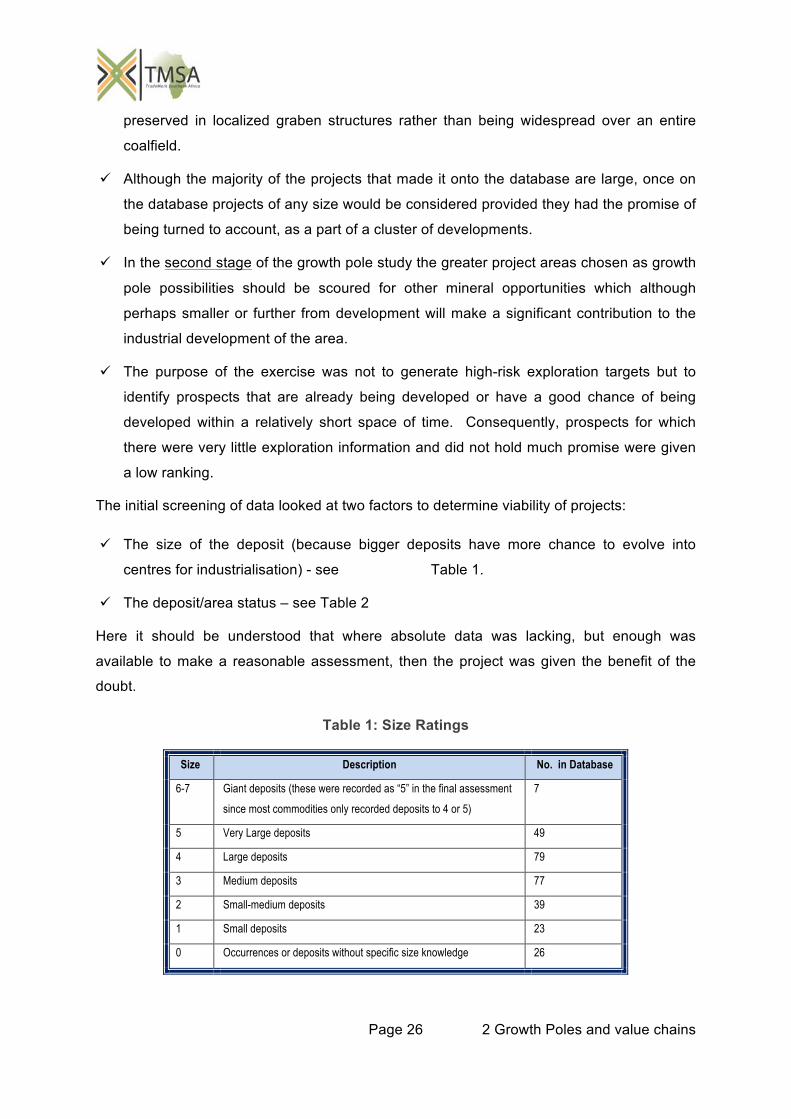

The initial screening of data looked at two factors to determine viability of projects:

The size of the deposit (because bigger deposits have more chance to evolve into

centres for industrialisation) - see Table 1.

The deposit/area status – see Table 2

Here it should be understood that where absolute data was lacking, but enough was

available to make a reasonable assessment, then the project was given the benefit of the

doubt.

Table 1: Size Ratings

Size Description No. in Database

6-7 Giant deposits (these were recorded as “5” in the final assessment

since most commodities only recorded deposits to 4 or 5)

7

5 Very Large deposits 49

4 Large deposits 79

3 Medium deposits 77

2 Small-medium deposits 39

1 Small deposits 23

0 Occurrences or deposits without specific size knowledge 26

Page 27 2 Growth Poles and value chains

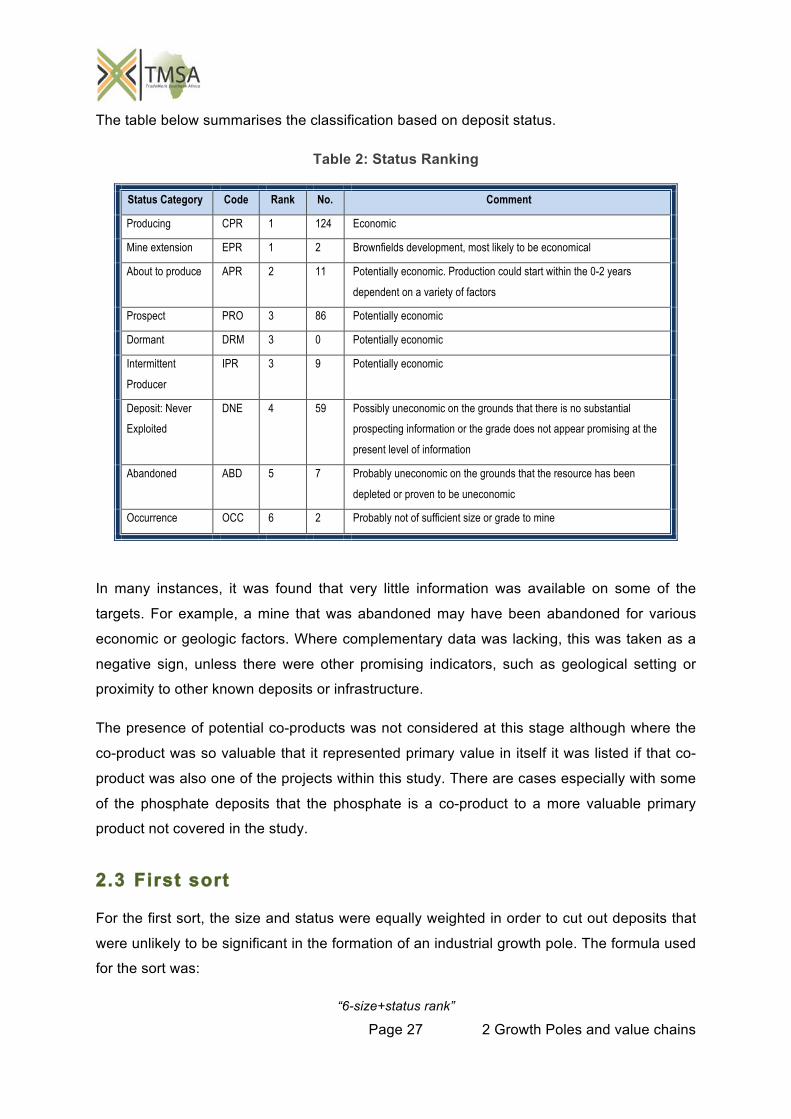

The table below summarises the classification based on deposit status.

Table 2: Status Ranking

Status Category Code Rank No. Comment

Producing CPR 1 124 Economic

Mine extension EPR 1 2 Brownfields development, most likely to be economical

About to produce APR 2 11 Potentially economic. Production could start within the 0-2 years

dependent on a variety of factors

Prospect PRO 3 86 Potentially economic

Dormant DRM 3 0 Potentially economic

Intermittent

Producer

IPR 3 9 Potentially economic

Deposit: Never

Exploited

DNE 4 59 Possibly uneconomic on the grounds that there is no substantial

prospecting information or the grade does not appear promising at the

present level of information

Abandoned ABD 5 7 Probably uneconomic on the grounds that the resource has been

depleted or proven to be uneconomic

Occurrence OCC 6 2 Probably not of sufficient size or grade to mine

In many instances, it was found that very little information was available on some of the

targets. For example, a mine that was abandoned may have been abandoned for various

economic or geologic factors. Where complementary data was lacking, this was taken as a

negative sign, unless there were other promising indicators, such as geological setting or

proximity to other known deposits or infrastructure.

The presence of potential co-products was not considered at this stage although where the

co-product was so valuable that it represented primary value in itself it was listed if that co-

product was also one of the projects within this study. There are cases especially with some

of the phosphate deposits that the phosphate is a co-product to a more valuable primary

product not covered in the study.

2.3 First sort

For the first sort, the size and status were equally weighted in order to cut out deposits that

were unlikely to be significant in the formation of an industrial growth pole. The formula used

for the sort was:

“6-size+status rank”

Page 28 2 Growth Poles and value chains

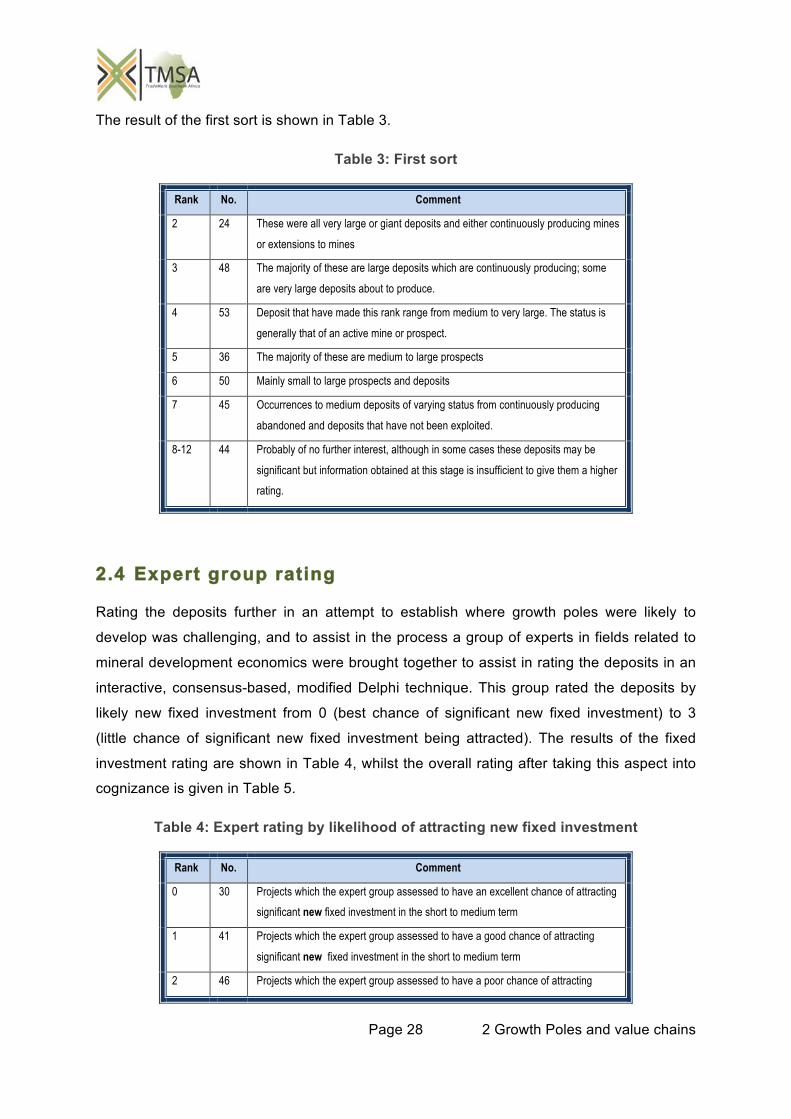

The result of the first sort is shown in Table 3.

Table 3: First sort

Rank No. Comment

2 24 These were all very large or giant deposits and either continuously producing mines

or extensions to mines

3 48 The majority of these are large deposits which are continuously producing; some

are very large deposits about to produce.

4 53 Deposit that have made this rank range from medium to very large. The status is

generally that of an active mine or prospect.

5 36 The majority of these are medium to large prospects

6 50 Mainly small to large prospects and deposits

7 45 Occurrences to medium deposits of varying status from continuously producing

abandoned and deposits that have not been exploited.

8-12 44 Probably of no further interest, although in some cases these deposits may be

significant but information obtained at this stage is insufficient to give them a higher

rating.

2.4 Expert group rating

Rating the deposits further in an attempt to establish where growth poles were likely to

develop was challenging, and to assist in the process a group of experts in fields related to

mineral development economics were brought together to assist in rating the deposits in an

interactive, consensus-based, modified Delphi technique. This group rated the deposits by

likely new fixed investment from 0 (best chance of significant new fixed investment) to 3

(little chance of significant new fixed investment being attracted). The results of the fixed