Embed Size (px)

Citation preview

etap_478 831..852

Whitetracks Design, Inc.Hugh GroveTom Cook

Whitetracks Design, Inc. is one of the leading U.S. manufacturers of snowshoes. The busi-ness is owned by three individuals who are contemplating whether it should be sold now orcontinue to be operated for a later sale at a potentially enhanced business value. All theWhitetracks owners are now in their early 60s and are hoping for a comfortable retirement.Whether they retire sooner or later is dependent upon the proceeds from selling the busi-ness. Prior to selling, the owners want an accurate determination of the firm’s value toensure proper returns for years of hard work and personal investment. From an entrepre-neurial standpoint, this case raises the issues of how private companies can be valued sothat they can be subsequently managed for value creation. This is important as a 2005survey found that only 60% of private company managers had at least some idea of theirfirms’ value, and two thirds of these managers said that such firms’ value was based uponmanagement estimates or wishful thinking. To assist with determining the value of theirbusiness, the Whitetracks owners hired a merger and acquisition consultant, who is acoauthor of this case. The consultant will assist the owners in valuing the business and inmaking the decision to sell now or continue to operate the business.

Whitetracks Design, Inc.

In mid-2005, Jay Gruber, Betty Boyd, and Doug Jones, the owners of WhitetracksDesign, and Bob Moore, the company’s chief executive officer (CEO), were meeting withGary Grange, executive vice president of International Business Group (IBG), whom theyhad hired to advise them about valuing their company. Located in Denver, Colorado, IBGwas the third-largest merger and acquisition sell-side consulting firm in the United States.All four Whitetracks owners/managers were in their early 60s and were thinking aboutretirement. The owners had wanted to sell their company in 2001, but its sales flattened,and its earnings declined following the terrorist attacks on September 11. At that time, Mr.Grange had persuaded the owners to wait because Whitetracks’ financial performance wasdeclining.

In 2005, the company’s financial performance was improving, and the owners onceagain asked Mr. Grange if they should sell. Had the last 4 years of his free consulting madethe company ready for sale, or should they continue to operate Whitetracks for a subse-quent sale at a potentially higher business value? Betty Boyd worried about having mostof her assets and income tied up in the company. She thought that if they waited too longto sell, she might miss the opportunity to spend her retirement years traveling the world.She also worried about the owners’ personal guarantees of the corporate debt. Jay Gruberwas anxious to sell and move on to other ventures. He noted that industry experts werevery positive about the future of the snowshoe industry and so concluded that now wouldbe a good time to sell.

Please send correspondence to: Hugh Grove, tel.: (303) 871-2026; e-mail: [email protected].

PTE &

1042-2587© 2011 Baylor University

831July, 2011DOI: 10.1111/j.1540-6520.2011.00478.x

Gary Grange explained how IBG, one of the leading merger and acquisition advisoryfirms for privately owned companies, could help in the decision. IBG’s extensive networkof potential buyers would be able to review the Whitetracks’ prospectus that Mr. Grangeput together and indicate possible interest in buying the company now. Mr. Grange wouldrecast the financial statements to enhance the business value and selling price of thecompany.

Doug Jones was against using IBG. He thought that its fees were too high, and thatGary Grange had a conflict of interest. Mr. Jones wanted the owners to sell the companyon their own. Mr. Gruber reminded the others that Mr. Grange had not recommendedselling the company 4 years earlier and argued that if Mr. Grange had been interested onlyin his fee, he could have recommended a sale then. Based on their discussion, the ownersdecided to continue working with Mr. Grange. It was now up to him to get back to theowners quickly with a recommendation on whether to sell now or continue to operatethe business. Although IBG did not offer formal company valuations, Gary Grange knewthat the owners needed an idea of what the company was worth in 2005.

Whitetracks Design, Inc. Background

History and OwnershipIn 1988, Whitetracks Design, Inc. was founded in Denver by John Brown, a triathlete

looking for a way to exercise during his snowbound winter months. In the same year, thecompany introduced a unique, V-shaped tail on its first five models as the industry’s firstlightweight running and racing snowshoe. The V-shaped tail created a more streamlineddesign than its competitors’ snowshoes and made the Whitetracks’ shoes less awkward forwalking or running (see Figure 1).

The three current owners bought Whitetracks from Mr. Brown in 1994. Whitetrackscontinued to improve existing models and create new snowshoes for a variety of users. In1996, the U.S. Army Research, Development, and Engineering Center chose Whitetracksto introduce “new concepts and equipment improvements that will help the soldiers’ground mobility.” Also, Whitetracks’ Blackhawk model was designated as theofficial snowshoe of the Austrian, German, and Belgian armies. Unit sales in 2004exceeded 41,000 pairs sold primarily in the United States but also in Canada, Europe,Japan, and Korea. Based on estimated unit snowshoe sales as reported by the SnowsportsIndustry Association and the Whitetracks selling memorandum, in 2005, Whitetracks held15% of the U.S. market.

Jay Gruber, a venture capitalist who owned 52.6% of the company and served on itsboard of directors, was an avid outdoorsman. In 1994, he had seen his investment inWhitetracks as a chance to combine his passion for winter sports with an opportunity tomake some money. His investment had not turned out to be as profitable as he hadexpected, and now he was ready to sell. In a conversation with one of the case authors, Mr.Gruber said, “I want to get my money out while the spotlight is still on the growing market(for snowshoes). I am hungry to cash in my chips and move on to greener pastures.”

Betty Boyd owned 33.76% of Whitetracks and served awhile as the senior vicepresident of marketing. After graduating from the University of Texas, Ms. Boyd movedto Denver and worked for Qwest Communications as a marketing manager, but she alwayswanted to work for a smaller firm. In 1994, she took early retirement from Qwest andinvested a sizable portion of her retirement fund in Whitetracks. In 2002, she started to cutback her time at Whitetracks. “Whatever business you are into, you have to have a passionfor it. Small business can have a lot of ups and downs, and you have to be willing to ride

832 ENTREPRENEURSHIP THEORY and PRACTICE

them out. I lost that passion some time ago and have stepped back from an active role inthe company. Also, we have not able to arrange a succession within the business so I don’tknow what else we can do but sell,” she said to one of the case authors.

Doug Jones owned 13.76% and became the CEO, upon investing in the company in1994. Mr. Jones brought senior management experience with other small companies to his

Figure 1

Whitetracks Design Inc. Product Images(A) V-tail Adult Snowshoe; (B) V-tail Youth Snowshoe

A

B

833July, 2011

position. After 7 years of working hard to get Whitetracks in a solid financial andcompetitive position, he got tired of being the CEO and stepped aside for Bob Moore in2001. Mr. Jones was eager to sell but did not see why the owners needed IBG. He said toMr. Grange, “Why should we pay a large selling fee if we can sell the business on ourown? If we wait, we can increase profits and attract our own buyers. Why pay IBG topackage what we already know to be a pretty good thing?”

Bob Moore, a retired U.S. Air Force colonel, had headed a logistics command. Afterhis retirement, Mr. Moore moved to Denver and began looking for a job that would enablehim to use the management skills he developed in the Air Force. He joined the companyas a production manager in 1998 and became the general manager in 2000. In 2003, hemarried Betty Boyd.

Mr. Moore supported his wife’s decision to sell and was also ready to retire. He saidto Mr. Grange, “All the actual detail in managing a small business is a tough thing to dowith no resources. You’ve got to make many things work. While Whitetracks is a fantasticbrand, an icon in the industry, we thought that we could make it stronger, but it’s toughwithout deep pockets. Besides, Betty wants to move back to Texas, so this is a good timefor us to sell.” Mr. Moore thought that Whitetracks’ reputation for quality, excellentcustomer service, and good market penetration offered a lot of value to a buyer. Hethought the highest value for Whitetracks would probably come from a strategic buyer.Aligning Whitetracks with a large sporting goods company, one looking to add a snow-shoe line, could provide the investments in working capital, marketing, and research anddevelopment (R&D) necessary to increase the market share of the Whitetracks brand andto make it more competitive with the other larger snowshoe manufacturers.

OperationsWhitetracks was a seasonal business, shipping 90% of its orders between October and

February. Snowshoe models were designed by various consultants with great familiaritywith the snowshoe industry, and all materials were obtained from local suppliers. Allassembly and quality control took place at Whitetracks’ manufacturing plant, a leased,12,000 square foot, one-story building in an industrial park in Denver. Whitetracks had anoption to terminate the lease if the company were sold.

The manufacturing of snowshoes involved a four-stage process: (1) bending andcutting the frame tubing; (2) die cutting the decking and hinge material; (3) assemblingand mounting the bindings; and (4) final inspection and packaging.

The company purchased precut lengths of seamless, aluminum alloy tubing and useda machine called a bender to create the frame of the shoe. The benders were designed forthe specific finished shape and diameter of the snowshoe frame. The bender tightly lockedaround the tubing and exerted force to make the bend. When removed from the bender, thetubing was shaped exactly as needed for the snowshoe frame. Whitetracks owned andoperated two bending machines.

Powder coating of the frames was outsourced to a local company. The aluminumframes were electrically charged and then sprayed with dry, finely powdered plastic thatclung to the charged frame. The frames were then heated, and the plastic melted onto theframe. Once the frames returned from the powder-coating shop, they were ready for finalassembly.

Decks (the main part of the shoe) and bindings were cut from large rolls of material.Workers unrolled the material and fed it into Whitetracks’ die press. The press containedrazors mounted in the outline of the deck shape and cut a finished deck in one motion. Silkscreening of the decks was outsourced to a local company.

834 ENTREPRENEURSHIP THEORY and PRACTICE

The last steps in manufacturing the shoe were to attach the deck to the frame, to installcleats on the bottom of the shoe, and to fit the bindings and heel strap. All these parts wereriveted together through the deck with a single rivet. The shoes were then ready to beboxed and sent to retailers.

Whitetracks’ managers were pleased with the quality control they achieved by pro-ducing locally. All raw materials for the snowshoes were inspected as they came into theplant, and workers checked for problems at each step of the manufacturing process.Because snowshoe components fit so precisely, any fault in the process was usuallynoticed immediately. For example, an incorrectly cut deck could not be fastened to theframe. Manufacturing snowshoes was also a slow process, thus allowing for visualinspection throughout. The worker who tagged the completed snowshoes and preparedthem for shipping acted as the final inspector.

Customer service set Whitetracks apart from its competitors, its owners believed.Managers also thought that their high-quality products enabled the company to be the firstto offer original purchasers a limited lifetime warranty against defects in materials andworkmanship on all of its snowshoes and accessories. Competitors had only recentlybegun offering similar warranties on their own products. Whitetracks’ managers wereuncertain that they could maintain this tight quality control if production were outsourcedto China, as competitors had done.

MarketingWhitetracks had limited funds for direct advertising and promotion but did place

occasional advertisements in sports publications and on the Resort Sports Network(RSN).1 Other avenues of marketing consisted of providing a newsletter to dealers,engaging a public relations firm to generate media coverage, setting up meetings betweensales representatives and store-level buyers, and participating annually in several tradeshows. Whitetracks also sponsored approximately 20–30 promotional events each year.Many of these events had a charitable emphasis such as supporting the Special Olympicsby providing snowshoes for athletes and coaches. Whitetracks partnered with the NationalCenter for Disabled Skiers and donated equipment to enable individuals with disabilitiesto participate in snowshoeing. Whitetracks also used the Internet as part of their marketingstrategy. The web gave them cheap and quick advertising by simply taking a picture of anew product and posting it to the company website. Funding for promotional budgets wassmall, making it difficult to compete with larger competitors.

InnovationWhitetracks was known as a cutting-edge firm with a long-established, formal R&D

program. The company was recognized as a leader in the design and distribution ofhigh-tech, lightweight snowshoes. It held two design patents (a snowshoe binding and asnowshoe hinge) and had a long record of being the first company in the industry to offerinnovations. For example, Whitetracks had introduced children’s snowshoes, V-shapedtails, easy-on-and-off bindings, and a hinge that reduced fatigue by allowing people towalk with a normal stride. The R&D program used independent product developers anddesign consultants that specialized in the snowshoe industry. The time from initial product

1. RSN was created in 1986 and creates and distributes outdoor lifestyle programming in 105 resorts and innine markets across the United States. Source: http://en.wikipedia.org, accessed 12 December 2008.

835July, 2011

design to manufacturing and distribution was about 2 or 3 years. Whitetracks’ limitedfunding contributed to a longer product development cycle. Managers believed that failureto continue new product development would be a severe blow to Whitetracks’ competitiveposition.

ProductsOf all the brands in the market, Whitetracks’ snowshoes were the sportiest.2 They

were known as the shoe of choice by winter runners, athletes, and outdoor enthusiasts.3

Their unique V-shaped tail created less stress on the knees and ankles than did similarmodels made by competitors.

In 2005, the company sold 11 models and 31 combinations of snowshoes and bind-ings. Whitetracks increased revenues by offering high-margin accessories such as snow-shoe poles, talon kits, carry bags, t-shirts, and hats. But in spite of its multiple models andthe accessories it offered, Whitetracks was still essentially a single-product enterprise thatdepended for success on snowy winters around the globe.

Customers and MarketsCustomers were primarily outdoor recreational products dealers located in the snowy

regions of the United States, Canada, Europe, Japan, and Korea. The company sold to over400 dealers using sales representatives and commissioned sales agents. The three largestcustomers were Sierra Trading Post (22% of total sales), Recreational Equipment Incor-porated (REI) (13%), and The Sports Authority (13%). No other customer accounted formore than 9% of sales. Other customers were ski rental shops. For example, Whitetrackssnowshoes were the only brand available at the Winter Park Ski Area, Copper Mountain,and Smuggler’s Notch resort ski shops. A portion of sales came from institutional andgovernmental customers such as armed forces and schools.

The company’s three largest customers had a history of stretching their payments toWhitetracks well beyond the net 30 days policy, causing the company to scramble to meetworking capital requirements during its peak season. In contrast, the ski rental shopstypically paid on time. Because these three customers represented such a large proportionof its sales, Whitetracks had accepted their behavior as a cost of doing business. BobMoore, the CEO, expressed his frustration: “It makes me mad as hell that they don’t payon time. We make calls and send letters to them, but they pay when they want to anyway.We just have to put up with it.”

Whitetracks had a significant user base with strong brand loyalty. For instance, usercomments included: “I liked the sport snowshoe with the V-tail which made for a lighterand faster hike.” “Weight, shape and size: I love them. The best pair of snowshoes I haveowned thus far—the best, hands down.” “They are a great price, have a great appearanceand features and have a very cool name!” “I like the women’s design and sizing.”

CompetitionWhitetracks’ largest competitors for mid- and high-end snowshoes were located in the

United States. The Tubbs and Atlas brands, both manufactured by K2, had a combined

2. “Whitetracks Confidential Business Report: IBG Strategic Acquisition Candidate #6709,” IBG BusinessServices, Inc., p. 11, May 24, 2005.3. “Whitetracks Confidential Business Report: IBG Strategic Acquisition Candidate #6709,” IBG BusinessServices, Inc., p. 11, May 24, 2005.

836 ENTREPRENEURSHIP THEORY and PRACTICE

50% share of the domestic snowshoe market while Cascade Designs had a 20% share.These competitors outsourced the manufacturing of their snowshoes to China, leavingWhitetracks as the only remaining major U.S. manufacturer of snowshoes with a 15%market share. The industry was characterized by price cutting, which reduced profitmargins for all firms. Also, Whitetracks competed directly with a smaller competitor,Yukon Charlie, for low-priced shoes.

Management believed that snowshoes made in the United States had a special appealbut knew that features and service closed the sale. Serving customers quickly and effi-ciently was much easier to do when employees and facilities were in the United States.The downside to local, small-scale manufacturing was that Whitetracks had to producesnowshoes well ahead of the winter season, which could leave unsold inventory whendemand was lower than expected. “Last year the snowfall in Europe was below averageand several buyers canceled or reduced their orders,” said Bob Moore.

EmployeesDue to the seasonality of the snowshoe business, Whitetracks’ employment varied

from a seasonal high of 25 to a year-round staff of 10 nonunion factory employees and 6sales and administrative personnel. Factory employees were paid an average of $8.50 perhour and received paid vacation time and health-care benefits. The full-time factoryworkers had an average tenure with the company of approximately 4 years. Some of theseasonal employees returned each year to work and ski during the winter months. Theowners of Whitetracks had decided to try to help the full-time employees keep their jobsin the event of a sale, but layoffs would not be a deal breaker.

The Colorado economy was rebounding from 3 years of job losses following the“dot.com” bubble of 2001. Employment grew by 1.4% in 2004 and was projected to growby 2.5–3.0% in 2005. Approximately 40% of all new jobs state-wide were in the Denver–Aurora metro area. Also, the winter sports industry throughout the state was expected tocontinue to grow. Six of the top 10 U.S. ski resorts listed in Ski magazine in 2004 werelocated in Colorado.

Financial InformationIn 2001, Whitetracks sales and pretax earnings were $2.5 million and $264,000,

respectively, but in 2002, they fell to $2.1 million and $165,000. In 2003, one largeaccount did not place an order, and sales fell to $1.8 million with pretax earnings below$20,000. In 2004, the company replaced the lost order with larger orders from severalother accounts and sales, and pretax earnings recovered to $2.2 million and $79,000.Whitetracks struggled to fund necessary advertising, marketing, design, and productdevelopment because of insufficient working capital. However, in 2004, the companyobtained and used a $200,000 short-term line of credit and a $425,000 long-term bankloan. Historical income statements and balance sheets are shown in Tables 1 and 2.

The Snowshoe Industry

Snowshoes allow people to walk on deep snow by distributing the walker’s weightacross a large surface area. People have been snowshoeing for over 6,000 years (thepractice probably originated in Central Asia), and as early as the eighteenth century,

837July, 2011

snowshoeing had become a recreational and fitness sport.4 In the late 1950s, a Canadiancompany, Magline, used magnesium to construct the first metal frame, with webbingmade from airplane cable encased in nylon.5 At about the same time, a Vermont-basedcompany, Tubbs, created the first modern snowshoe, using a shorter length and narrowerwidth than the traditional wooden shoe design. In 1972, Gene and Bill Prater created thealuminum snowshoe as it is known today, with a short frame made of aluminum tubing,a nylon decking (the portion of the shoe that holds the foot), hinged binding, and cleats onthe bottom of the shoe.6 The Sherpa Snowshoe Company began manufacturing these“Western” shoes, and the “short and narrow” design became the industry standard.Figure 2 shows photographs of traditional wooden snowshoes and the modern design.

The total number of snowshoe participants in the United States was 5.5 millionin 2005, compared with the marquee winter sports of skiing and snowboarding with

4. http:ww.madehow.com/Volume-6/Snowshoe.html, accessed 5 December 2007.5. http:ww.madehow.com/Volume-6/Snowshoe.html, accessed 5 December 2007.6. http://en.wikipedia.org/wiki/Snowshoe, accessed 5 December 2007.

Table 1

Whitetracks Design, Inc. Income Statementsfor Years 2002–2004

— 2004 2003 2002

Sales $2,248,511 $1,789,429 $2,050,742Units sold 41,300 30,172 31,800Cost of goods sold

Material 771,007 596,194 693,945Direct labor 251,120 185,736 207,823Rent allocation 25,719 26,921 18,374Depreciation allocation 11,131 12,434 19,110Other 77,157 62,723 95,798

Total cost of goods sold 1,136,134 884,008 1,035,050Gross profit $1,112,377 $905,421 $1,015,692Operating expenses

Owners/management compensation 138,238 151,000 133,000CEO bonus compensation 23,900 4,270 20,327Salaries and wages 22,331 29,395 139,523Professional fees 47,422 99,177 45,131Rent allocation 23,912 24,447 20,793Commissions 122,089 154,430 71,815Bad debts 32,551 0 14,000Advertising and promotion 104,310 74,302 94,304Trade shows 25,162 25,184 29,021Research 4,008 24,582 14,224Depreciation allocation 1,995 2,814 3,901Amortization—purchase debt 12,600 12,600 12,600Interest 107,534 19,517 42,310Other expense 367,186 264,125 210,169

Total operating expenses 1,033,238 885,843 851,118Operating profit $79,139 $19,578 $164,574

CEO, chief executive officer.

838 ENTREPRENEURSHIP THEORY and PRACTICE

approximately 12.5 million participants.7 More than 30 firms manufactured snowshoes,but the industry was dominated by K2 (which owned both Tubbs and Atlas) and CascadeDesigns with total market shares of 50% and 20%, respectively.

Firms in the industry competed by either adopting a niche strategy or pursuing a massmerchandising strategy. Niche producers sold a small number of high-quality shoes andfocused on experienced users such as racers, avid snowshoers, and others who spent time

7. Snowshoe information from Snowsports Industries Association on the National Ski AreaAssociation website: http://www.nsaa.org/nsaa/press/0506/facts-about-skiing-and-snowboarding.asp,accessed 2 December 2008.

Table 2

Whitetracks Design, Inc. Balance Sheets forYears 2003–2004

— 12/31/2004 12/31/2003

Current assetsCash $503,443 $391,347Accounts receivable (net 5,000) 613,485 610,525Inventory 852,343 654,684Prepaid expenses 0 33,035Total current assets $1,969,271 $1,689,591

Property, plant, and equipmentLeasehold improvements 5,120 5,120Furniture and fixtures 33,075 73,138Machinery and equipment 263,045 254,681Vehicles 24,109 24,109Total PPE 325,349 357,048Accumulated depreciation -305,296 -323,812Net PPE 20,053 33,236

Other assetsPatent and trademark costs 15,262 15,262Non-compete agreement 189,000 189,000Loan fees 4,375 0Accumulated amortization -80,850 -68,250Total other assets 127,787 136,012Total assets $2,117,111 $1,858,839

Current liabilitiesAccounts payable $80,937 $71,367Sales tax payable 17,972 10,639Accrued commissions 21,639 18,404Accrued interest 90,156 163,310Line of credit payable 200,000 21,500Total current liabilities 410,704 285,220

Long-term liabilitiesNote payable-bank 425,000 129,685Shareholder loans 637,193 837,478Total long-term liabilities 1,062,193 967,163Total stockholders equity 644,214 606,456Total liabilities and equity $2,117,111 $1,858,839

PPE, property, plant, and equipment.

839July, 2011

in deep snow. Manufacturers from mass merchandisers to specialty companies sold a widerange of snowshoe models at prices between $20 and $300.

Although demand in most of the snowsports industry was flat in 2005, snowshoeingwas booming. Participation grew by 15% between 2004 and 2005, and between 8% and24% annually over the period from 2001 to 2004.8 Unit sales of snowshoes grew 9.2%,21.3%, and 10.2% over the years 2003, 2004, and 2005, respectively.9 Dollar sales grewat comparable rates, and the average retail price for a pair of snowshoes over the sameperiod varied between $142.30 and $148.95.

One of the biggest draws to the sport was the ease of mastering it. No fancy techniqueswere required, and snowshoes could be used in many different types of snow conditions,regardless of the weather. The saying in the industry was, “If you can hike, you cansnowshoe.” Snowshoeing was a crossover sport that offered a low-impact, aerobicworkout that also included strength training and muscle endurance. Research showed thatadults burnt up to 700 calories an hour snowshoeing. People who substituted snowshoeingfor running during the winter improved their overall fitness.10 Snowshoeing exercisedsimilar muscles to those used in walking and hiking. Carry Porter of Mountain SafetyResearch pointed out, “It’s the number one growing winter sport. Kids love it, women loveit, it’s easy to get into, it’s relatively inexpensive . . . why wouldn’t you want a pair ofsnowshoes?”11

8. http://www.winterfeelsgood.com/winterfeelsgood.php?section=news&page=basic_stats__06, accessed27 October 2007.

9. “SIA Resort Shop Abstracts, March 2003-March 2004”, Snowsports Industry Association.10. http://www.winterfeelsgood.com/winterfeelsgood.php?section=news&page=fact_snow-shoe, accessed27 October 2007.11. Mandel, P. “American Made: Does it Matter?,” Snowshoe Magazine, March 22, 2005.

Figure 2

Whitetracks Design, Inc. Traditional and Modern Snowshoe Images(A) Traditional Snowshoe; (B) Modern Snowshoe

Toe barToe hole

Toe cord

Pivot rod

Clow

Located beneath

binding

Heel bar

Heel strop

Decking

Tail area

Pull strap

Inside edge

(left snow shoe)

Strike plate

Step-in binding

Toe

Outside frame

TailWebbingFrame

A B

Traction device

(fastened to bottom)

840 ENTREPRENEURSHIP THEORY and PRACTICE

The industry was going through some fundamental changes because of a period ofconsolidation, and outsourcing manufacturing to China. Several small manufacturers shutdown, and others were acquired by larger competitors. Many industry experts believedthat the consolidation was driven by consumer and retailer demands for lower pricedsnowshoes. But others like Jake Thamm, president of Crescent Moon, a small high-endsnowshoe company in Boulder, Colorado, thought that the shakeout of small companiesstemmed from their failure to offer uniquely designed snowshoes or otherwise differen-tiate themselves from competitors. According to Mr. Thamm, to stay in business, smallerU.S. companies had to offer innovative designs and superior customer service.

In the mid-1990s, Yukon Charlie became the first snowshoe company to move a largepart of its manufacturing to China. As in other industries, the trend toward offshoring inChina accelerated over time. All of Atlas’ snowshoes were made in China in 2005, andTubbs planned to import all of its snowshoes from China in 2006. Much of the pressureto move overseas came from consumers demanding lower priced snowshoes and retailerspushing that demand back onto the manufacturers. Snowshoe manufacturing was expen-sive, said Richard Havlick of Havlick Snowshoes in Mayfield, New York: “Take a kid’sshoe. It costs the same to make as a full size shoe but you can’t sell it for the same price.”According to Karen Rightland of Tubbs, the advantages of outsourcing to China wereclear: “A lower-cost product is just a reality. Lower-cost manufacturing makes it possiblefor Tubbs to offer discounted family pricing on their snowshoes. Also, we can hurlresources at quality assurance problems, we can dedicate ourselves to making fixes andimprovements in a way we just couldn’t do when we were in the United States.”

The R&D of new products was done in the United States, and then the products weremanufactured offshore. Lead times for offshore manufacturing of 4 or 5 months combinedwith the logistics of shipping large quantities through limited port facilities to require thatsnowshoe production for the next season start early each year. The minimum efficientorder size from China was approximately 10,000 units.12

Some consumers were concerned about the quality and performance of snowshoesmade in China. Chinese snowshoes had a reputation for being heavy but cheap. However,although American shoppers might ask where a shoe was manufactured, the answer didnot seem to be critical to most of them. According to Bob Dion of Dion Snowshoes inReadsboro, Vermont, “Consumers say they want a U.S.-made product, but come shoppingtime, that’s not what happens. They do all their homework in their local stores andshopping malls, then go to the Internet and see where they can get the product for thelowest price.”13 However, Whitetracks’ managers thought that competitors’ overseas out-sourcing gave Whitetracks’ “Made in USA” products a certain cachet that increased sales.

For many years, women and children were offered only unisex products that did notfit properly. By 2005, all manufacturers had age- and gender-specific products. MelJanaes, a sales associate with Eastern Mountain Sports said, “Gender, weight, versatilityare now factors in how snowshoes are made.”14 Whitetracks, for example, was offeringnew V-tail models designed for a woman’s walking and running strides that were light andeasy to handle. Their bindings used quick release buckles with easy-to-use strap systemsthat were designed to form to a woman’s foot. Other snowshoes were designed specifi-cally for children.

12. Mandel, P. “American Made: Does it Matter? Part II,” Snowshoe Magazine, April 21, 2005.13. Mandel, P. “American Made: Does it Matter? Part II,” Snowshoe Magazine, April 21, 2005.14. Allford, R. “The Changing Landscape of the Snowshoe Industry: A Conversation with Mel Janaes,”Snowshoe Magazine, March 15, 2004.

841July, 2011

Growth Opportunities for the Snowshoe Industry

The 2004 Outdoor Participation Study (The Study) published by the Outdoor Indus-try Foundation suggested several future growth opportunities for aggressive, well-financed companies.

1. The market for snowshoes would be increasing.15 The Study reported a total U.S.outdoor recreation population of 145.7 million. Participants were younger (median age35), slightly more diverse (20% non-White), and consisted of more families (50% ofhouseholds have a child under 18) than in 1998. Snowshoeing was one of four activitiesshowing the largest percentage increase in “participants” since 1998, with 3 millionnew participants, a 203.4% increase. Respondents were looking for activities that wereeasy to access and to learn, could be done in a day, and did not require specializedtechnical gear. Snowshoe industry experts recognized that this group was critical forgrowth in the sport.

2. Young adults was a rapidly growing market segment.16 According to The Study,among young adults aged 16–24, snowshoeing had greater participation rates in 2005than in 1998, and a third of all snowshoers were between 16 and 24. The challenge withthis overall age-group was changing their perception that snowshoeing was an“uncool” activity for young people and suited only to older people. In the words of aNew York Times reporter,

To understand the problem facing snowshoe makers today, look no further than thesnowboarding prodigy Shaun White. He wows. His wild orange hair flops beneath asticker-bedecked helmet. He has an acrobatic repertoire of 360s, McTwists andMethod Airs that children instinctively want to ape. It’s enough to make the snowshoeindustry scream. After the under-18 crowd has admired the jumps, twists and turns ofthe talented Mr. White, why would they be satisfied to simply plod through snow?17

None of the firms spent much on advertising to the under-18 group. Even the industryleader Tubbs only spent $25,000 on advertising to this market segment in 2004.

3. Young Hispanics and African/Americans were a new market segment.18 The Studyalso found that Hispanics and African Americans represented a new generation ofoutdoor participants. Over 60% of the males in each group, and over 40% aged 16–24in each group participated in outdoor activities during the sample period.

4. Women are a growing market segment. The Study also found that over 74 millionwomen participated in outdoor activities, and the growth of female participation insnowshoeing increased substantially from 2004 to 2005.

5. Snowshoeing is a low-impact aerobic exercise. A final growth opportunity was toincrease the awareness of snowshoeing as a means of improving physical fitness. Poordiet and sedentary lifestyles were contributing to almost two thirds of American adults

15. “2006 Outdoor Recreation Participation Study,” Outdoor Industry Foundation. http://www.outdoorindustryfoundation.org.16. Allford, R. “Dude, Snowshoeing Kicks A**! How the Youth Make a Difference,” Snowshoe Magazine,November 15, 2004.17. Melekian, B., “Thank You for Snowshoeing,” The New York Times, December 14, 2006.18. “2006 Outdoor Recreation Participation Study,” Outdoor Industry Foundation. http://www.outdoorindustryfoundation.org.

842 ENTREPRENEURSHIP THEORY and PRACTICE

or more than 123 million people being overweight or obese.19 Dr. William Klish of theBaylor College of Medicine noted that for the first time in over 100 years, children hada shorter life expectancy than their parents.20 The winter months contributed to inac-tivity as well as to poor eating habits. Snowshoeing could improve fitness levels byoffering a noncompetitive, social activity for all members of the family.

Recast Financial Statements for Whitetracks Design, Inc.

Gary Grange told the owners that Whitetracks’ financial statements should be recast,or “normalized,” to prepare the company for sale. Because privately owned companiestended to minimize reported profits for income tax purposes, he said that financialrecasting was important for understanding a company’s earning capacity and cash flowand making meaningful comparisons with other companies. Mr. Grange told the ownersthat financial recasting eliminated such items as excessive or discretionary expenses(especially personal expenses) and nonrecurring revenues and expenses. He said thatrecasting also removed debt and interest expense because they reflect the financingdecisions of the current owner, not of a new owner. Furthermore, recasting the financialstatements often identified off-balance sheet assets and liabilities. Mr. Grange pointed outthat the Whitetracks balance sheet did not recognize product liability for snowshoesalready sold, a liability that the company’s owners had ignored. He told them, “We needto unwind your income statements to get at the real economic earning power of thecompany. Every dollar that we can add to your earnings will increase your business valueby $5 (using the typical “EBITDA times 5” approach).”

Mr. Grange also told the three owners that all recasting adjustments must belegitimate, to pass review by the buyers’ Certified Public Accountants (CPAs) duringtheir due diligence process. With his coaching, the owners volunteered the informationthat is shown in panel A of Table 3. Panel B shows Mr. Grange’s recast income state-ments for 2004 and 2003 based on the first seven proposed adjustments listed in panelA. For 2004, recast operating profit increased 127% from $79,139 to $179,429 and in2003 by 559% from $19,578 to $128,996. Panel C of Table 3 shows the recast balancesheet for 2004 based on the last four proposed adjustments in panel A. The net effectof these balance sheet adjustments was to increase the stockholders’ equity by 116%from $644,214 to $1,392,621.

Setting the Value of Whitetracks Design, Inc.

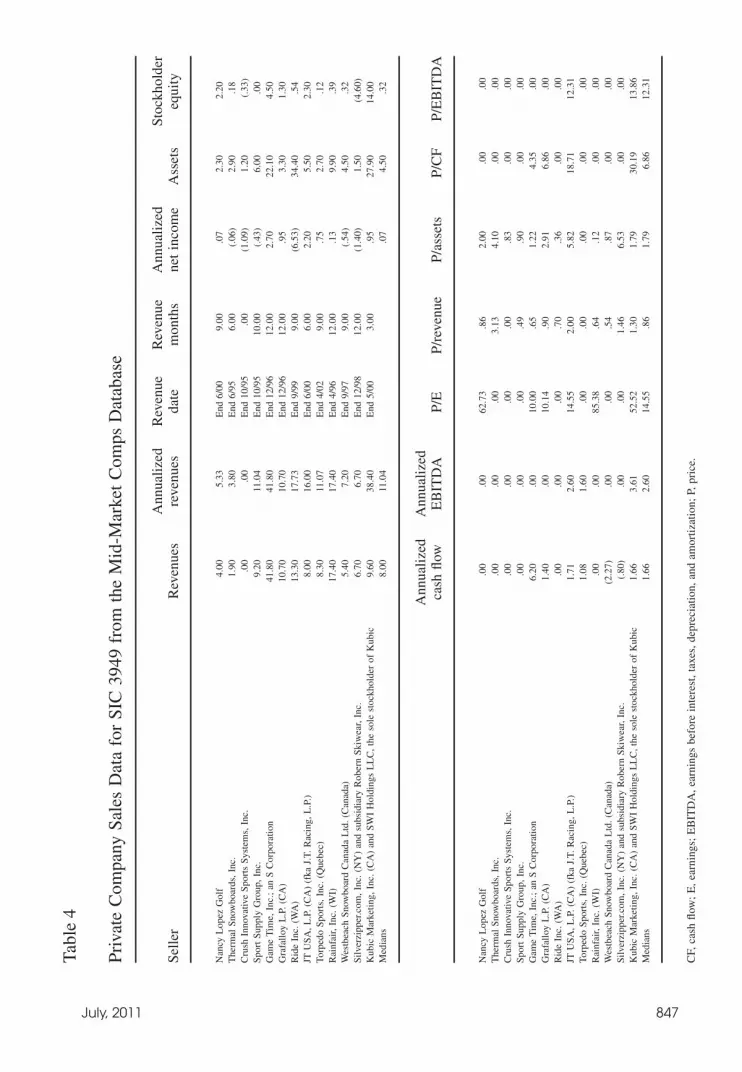

When valuing private companies for sale, Mr. Grange typically followed the industrypractice of using a multiple of 5 times the most recent historical earnings before interest,taxes, depreciation, and amortization (EBITDA) on a recast basis. As one check on thisEBITDA approach, he considered information from the John Wiley subscription database,Mid-Market Comps, for the sale of similar private companies in Whitetracks’ StandardIndustry Classification (SIC) code. This database was organized by industry and containedthe actual selling price as well as partial income statement and balance sheet information

19. Tarallo, M.J., “Take Another Look at Winter—Snowshoe Programs Work at Fitness Issues,” Perspective,July, 2004.20. Tarallo, M.J., “Take Another Look at Winter—Snowshoe Programs Work at Fitness Issues,” Perspective,July 2004, p. 29.

843July, 2011

Table 3

Whitetracks Design, Inc. Recast Financial Statements for 2003 and 2004

Panel A: Tentative Recasting Adjustments for Whitetracks

Adjustmentnumber Tentative adjustment

1 The total owners/management compensation for both the chief executive officer (CEO) and senior vice president (VP)positions for 2004 and 2003 was $138,238 and $151,000, respectively. The owner doing the senior VP job was justin an oversight role and the same duties were being performed by a VP of sales and marketing who was beingcompensated normally. The market compensation for the CEO position at similar companies was estimated to be$80,000 per year.

2 The CEO bonus compensation for 2004 and 2003 was $23,900 and $4,270, respectively. This bonus was normallybased upon 10% of unadjusted operating profits.

3 Excess or one-time expenses for attorneys and consultants were incurred for $37,000 in 2004 and $89,000 in 2003 fora business acquisition, real estate transactions, and software training.

4 In 2004, excess overtime of $14,000 was incurred due to a new production manager.5 Bad debt expense could be adjusted to normalize this expense at 1% of sales.6 Whitetracks carried no product liability insurance, which would cost $35,000 per year.7 The income tax rate is estimated to be 40%. This adjustment assumes that the new buyer would have to pay corporate

income taxes. Whitetracks is currently an S Corporation.8 To calculate an adjusted EBITDA, depreciation, amortization, interest, and taxes need to be added back to net income.9 Also, for the adjusted EBITDA, capital expenditures were normally $10,000 per year.

10 In reviewing Whitetracks’ 2004 balance sheet with the owners, $25,000 of scrap inventory still on the books.11 Accelerated depreciation had been used for income tax purposes but straight-line depreciation would be have been

$198,845 less over the years of fixed assets’ ownership.12 None of the other assets, except the patent and trademark costs (net book value of $10,000), had any future value to

potential buyers.13 All the accrued interest payable related to the shareholder loans that would all be reclassified as stockholders equity if

the company was sold.

EBITDA, earnings before interest, taxes, depreciation, and amortization.

Panel B: Whitetracks Design, Inc. Recast Income Statements for 2003–2004

— 2004 2003

Operating profit $79,139 $19,578Recasting adjustments: adjustment no.*

1. Actual owners/management salaries 138,238 151,000Reasonable managers’ salary -80,000 -80,0002. Actual CEO bonus 23,900 4,270Recalc.: 10% operating profit -7,914 -1,9583. Excess or one-time expense 37,000 89,0004. Excess overtime expense 14,000 05. Actual bad debt expense 32,551 0Normalized: 1% sales -22,485 -17,8946. Product liability insurance -35,000 -35,000Earnings before taxes $179,429 $128,9967. Income taxes (40%) 71,772 51,598Earnings $107,657 $77,3988. Interest 107,534 19,5178. Income taxes 71,772 51,5988. Depreciation 13,126 15,2488. Amortization 12,600 12,6009. Capital expenditures -10,000 -10,000

844 ENTREPRENEURSHIP THEORY and PRACTICE

Table 3

Continued

Panel B: Whitetracks Design, Inc. Recast Income Statements for 2003–2004

— 2004 2003

EBITDA: Recast $302,689 $166,361EBITDA: Not recast:

Operating profit $79,139 $19,578Interest 107,534 19,517Depreciation 13,126 15,248Amortization 12,600 12,600EBITDA: Not recast $212,399 $66,943

Note: * Adjustment No. corresponds to the adjustment number shown in panel A.CEO, chief executive officer; EBITDA, earnings before interest, taxes, depreciation, and amortization.

Panel C: Whitetracks Design, Inc. Recast Balance Sheets for 2004

—

Unadjusted

Adjustment*

Recast

12/31/2004 12/31/2004

Current assetsCash $503,443 $503,443Accounts receivable 613,485 613,485Inventory 852,343 (10) -25,000 827,343Prepaid expenses 0 0Total current assets $1,969,27 $1,944,271

Property, plant, and equipmentLeasehold improvements 5,120 5,120Furniture and fixtures 33,075 33,075Machinery and equipment 263,045 263,045Vehicles 24,109 24,109Total PPE 325,349 325,349Accumulated depreciation -305,296 (11) 198,845 -106,451Net PPE 20,053 218,898

Other assetsPatent and trademark costs 15,262 -5,262 10,000Non-compete agreement 189,000 (12) -189,000 0Loan fees 4,375 -4,375 0Accumulated amortization -80,850 80,850 0Total other assets 127,787 10,000Total assets $2,117,111 $56,058 $2,173,169

Current liabilitiesAccounts payable $80,937 $80,937Sales tax payable 17,972 17,972Accrued commissions 21,639 21,639Accrued interest 90,156 (13) -90,156 0Line of credit payable 200,000 200,000Product liability 0 35,000 35,000Total current liabilities 410,704 355,548

Long-term liabilitiesNote payable-bank 425,000 425,000Shareholder loans 637,193 (13) -637,193 0

845July, 2011

for the company in fiscal year before the sale. Financial statement data and variousbusiness valuation multiples for each company sold, such as Price/Earnings, Price/Revenue, Price/Cash Flow, and Price/EBITDA are shown in Table 4.

This historical EBITDA approach assumed no or few capital expenditures or workingcapital requirements for cash flows. Therefore, Mr. Grange also considered the free cashflow method of business valuation. He estimated revenues by forecasting total market sizefor the snowshoe industry for each of the next 5 years and assuming a constant marketshare for Whitetracks. He thought that the average wholesale price of Whitetracks’snowshoes would keep up with inflation, which he expected to average about 3% per yearover the planning period.

The owners told him that each year’s capital expenditures would approximate the sumof depreciation and amortization. Mr. Grange also decided to use the build-up method tofind a weighted average cost of capital (WACC) for Whitetracks. Table 5 contains finan-cial market data that Mr. Grange would use to find the WACC. To estimate the value ofWhitetracks to a C-Corporation, he used a 40% corporate income tax rate. Finally, Mr.Grange knew that strategic buyers would likely come from current manufacturers ofwinter sports equipment who would add the Whitetracks line to their existing products.Discussions with industry experts and managers at Whitetracks helped him to estimate thecost savings another manufacturer could realize by acquiring Whitetracks. These savingsfrom both economies of scale and scope are shown in Table 6. The major savings wouldcome from reduced wages and salaries, lower rent, and the elimination of subcontractedservices.

The owners were willing to stay on after the sale to help during the transition to newownership. Mr. Grange estimated that a buyer would pay upfront for both a $100,000non-compete agreement and a $50,000 consulting agreement, totaling $150,000 to bedivided equally among the three owners.

The three owners were anxiously awaiting Mr. Grange’s recommendation on whetherto sell the company now or continue to operate it for a future sale at a higher businessvalue. Mr. Grange had gathered all his notes and working papers together and wasconsidering the various tasks that lay before him. He knew that the financial statementrecasting was the starting point for a company business valuation. To attract buyers, he

Table 3

Continued

Panel C: Whitetracks Design, Inc. Recast Balance Sheets for 2004

—

Unadjusted

Adjustment*

Recast

12/31/2004 12/31/2004

Total long-term liabilities 1,062,193 425,000Total stockholders equity 644,214 748,407 $1,392,621Total liabilities and equity $2,117,111 $56,058 $2,173,169

Note: * The numbers in parentheses correspond to the adjustment numbers shown in panel A.PPE, property, plant, and equipment.

846 ENTREPRENEURSHIP THEORY and PRACTICE

Tabl

e4

Priv

ate

Com

pany

Sale

sD

ata

for

SIC

3949

from

the

Mid

-Mar

ket

Com

psD

atab

ase

Selle

rR

even

ues

Ann

ualiz

edre

venu

esR

even

ueda

teR

even

uem

onth

sA

nnua

lized

net

inco

me

Ass

ets

Stoc

khol

der

equi

ty

Nan

cyL

opez

Gol

f4.

005.

33E

nd6/

009.

00.0

72.

302.

20T

herm

alSn

owbo

ards

,Inc

.1.

903.

80E

nd6/

956.

00(.

06)

2.90

.18

Cru

shIn

nova

tive

Spor

tsSy

stem

s,In

c..0

0.0

0E

nd10

/95

.00

(1.0

9)1.

20(.

33)

Spor

tSu

pply

Gro

up,I

nc.

9.20

11.0

4E

nd10

/95

10.0

0(.

43)

6.00

.00

Gam

eT

ime,

Inc.

;an

SC

orpo

ratio

n41

.80

41.8

0E

nd12

/96

12.0

02.

7022

.10

4.50

Gra

fallo

yL

.P.(

CA

)10

.70

10.7

0E

nd12

/96

12.0

0.9

53.

301.

30R

ide

Inc.

(WA

)13

.30

17.7

3E

nd9/

999.

00(6

.53)

34.4

0.5

4JT

USA

,L.P

.(C

A)

(fka

J.T.

Rac

ing,

L.P

.)8.

0016

.00

End

6/00

6.00

2.20

5.50

2.30

Torp

edo

Spor

ts,I

nc.(

Que

bec)

8.30

11.0

7E

nd4/

029.

00.7

52.

70.1

2R

ainf

air,

Inc.

(WI)

17.4

017

.40

End

4/96

12.0

0.1

39.

90.3

9W

estb

each

Snow

boar

dC

anad

aL

td.(

Can

ada)

5.40

7.20

End

9/97

9.00

(.54

)4.

50.3

2Si

lver

zipp

er.c

om,I

nc.(

NY

)an

dsu

bsid

iary

Rob

ern

Skiw

ear,

Inc.

6.70

6.70

End

12/9

812

.00

(1.4

0)1.

50(4

.60)

Kub

icM

arke

ting,

Inc.

(CA

)an

dSW

IH

oldi

ngs

LL

C,t

heso

lest

ockh

olde

rof

Kub

ic9.

6038

.40

End

5/00

3.00

.95

27.9

014

.00

Med

ians

8.00

11.0

4.0

74.

50.3

2

Ann

ualiz

edca

shflo

wA

nnua

lized

EB

ITD

AP/

EP/

reve

nue

P/as

sets

P/C

FP/

EB

ITD

A

Nan

cyL

opez

Gol

f.0

0.0

062

.73

.86

2.00

.00

.00

The

rmal

Snow

boar

ds,I

nc.

.00

.00

.00

3.13

4.10

.00

.00

Cru

shIn

nova

tive

Spor

tsSy

stem

s,In

c..0

0.0

0.0

0.0

0.8

3.0

0.0

0Sp

ort

Supp

lyG

roup

,Inc

..0

0.0

0.0

0.4

9.9

0.0

0.0

0G

ame

Tim

e,In

c.;

anS

Cor

pora

tion

6.20

.00

10.0

0.6

51.

224.

35.0

0G

rafa

lloy

L.P

.(C

A)

1.40

.00

10.1

4.9

02.

916.

86.0

0R

ide

Inc.

(WA

).0

0.0

0.0

0.7

0.3

6.0

0.0

0JT

USA

,L.P

.(C

A)

(fka

J.T.

Rac

ing,

L.P

.)1.

712.

6014

.55

2.00

5.82

18.7

112

.31

Torp

edo

Spor

ts,I

nc.(

Que

bec)

1.08

1.60

.00

.00

.00

.00

.00

Rai

nfai

r,In

c.(W

I).0

0.0

085

.38

.64

.12

.00

.00

Wes

tbea

chSn

owbo

ard

Can

ada

Ltd

.(C

anad

a)(2

.27)

.00

.00

.54

.87

.00

.00

Silv

erzi

pper

.com

,Inc

.(N

Y)

and

subs

idia

ryR

ober

nSk

iwea

r,In

c.(.

80)

.00

.00

1.46

6.53

.00

.00

Kub

icM

arke

ting,

Inc.

(CA

)an

dSW

IH

oldi

ngs

LL

C,t

heso

lest

ockh

olde

rof

Kub

ic1.

663.

6152

.52

1.30

1.79

30.1

913

.86

Med

ians

1.66

2.60

14.5

5.8

61.

796.

8612

.31

CF,

cash

flow

;E

,ear

ning

s;E

BIT

DA

,ear

ning

sbe

fore

inte

rest

,tax

es,d

epre

ciat

ion,

and

amor

tizat

ion;

P,pr

ice.

847July, 2011

thought that Strengths, Weakness, Opportunities, and Threats (SWOT) and Porter’s FiveForces analyses would be helpful as well as ratio analysis. Concerning the businessvaluation task, he wanted to estimate both what Whitetracks would be worth to a buyerfrom outside the industry and its value to a strategic buyer. He knew that such a task wouldbe a real challenge since there was little comparable valuation data available from thecompany’s two major competitors. Also, he thought that forecasting cash flows forbusiness valuation would be challenging but important in presenting a final recommen-dation to the owners.

Hugh Grove is a Professor in the Daniels College of Business at the University of Denver.

Tom Cook is a Professor in the Daniels College of Business at the University of Denver.

Table 5

Financial Market Data

Component Rate

Risk-free interest rate .051Equity risk premium .072Industry risk premium (SIC 39) -.033Company-size risk premium .098

Source: SBBI Valuation Edition 2004 Yearbook, Chicago: IbbotsonAssociates.SIC, Standard Industry Classification.

Table 6

Projected Savings if Whitetracks MergedWith Another Snowshoe Manufacturer

—Estimated

annual savings

1. Factory (15%) using current productionworkers already employed

40,000

2. Management compensation 185,0003. Reduced rent 57,0004. Utilities (50% of current) 6,0005. Telephone (20% of current) 2,0006. Subcontracted operations

Silk screening 50,000Injection molding 181,000

848 ENTREPRENEURSHIP THEORY and PRACTICE

Note to Instructors: Whitetracks Design, Inc.

IntroductionWhitetracks Design, Inc. was a leading U.S. manufacturer of snowshoes. Its three

owners were deciding whether to sell the company now or to operate it for a later sale ata potentially enhanced business value. All of the Whitetracks owners were in their early60s and hoping to retire. To assist with determining the value of their business, they hiredGary Grange, a merger and acquisition consultant with International Business Group(IBG) Business Services, who is also a coauthor of this case. Mr. Grange would assist theowners in valuing Whitetracks and in deciding whether to sell the company.

The owners had wanted to sell Whitetracks in 2001, but its sales flattened andearnings declined following the terrorist attacks on September 11. At that time, Mr.Grange had persuaded the owners to wait because Whitetracks’ financial performancewas declining. In 2005, the company’s financial performance was improving, and theowners once again asked Mr. Grange if they should sell. Some of the owners worriedabout having most of their assets and income tied up in the company. Others thoughtthat if they waited too long to sell, they might miss the opportunity to spend theirretirement years traveling the world. They also worried about the owners’ personalguarantees of Whitetracks’ corporate debt. Whether they could retire sooner or laterdepended upon the proceeds from selling the company. Prior to selling, the ownerswanted an accurate determination of their firm’s value to ensure proper returns for theiryears of hard work and personal investment.

Key Issues and Discussion PointsThis case raises the issue of how to value privately held companies. This is important

because a 2005 survey1 found that only 60% of private company managers had at leastsome idea of their firms’ value; two thirds of these managers said their idea of the firms’value was based upon management estimates or wishful thinking. The case also aims tointroduce students to the interdisciplinary nature of business valuation through an industryanalysis and the recasting of financial statements preceding the valuation. Good businessvaluations require sound fundamentals in business strategy, accounting, and finance.Among the more interesting aspects of the case are the small size of the company, the lackof comparable companies for the valuation, and the paucity of good financial informationon which to make a decision to sell or not.

With the emergence of global competition and “world-flattening” technology, evenprivate companies should be managed for value by making decisions with the goal ofcreating business value and measuring performance by the change in value from 1 year tothe next. Eighty percent of a typical private business owner’s net worth is tied up in his orher business.2 As a result, an accurate determination of the firm’s value is essential toensure proper returns for years of hard work and personal investment. This firm’s value iscomputed using various business valuation methods with various assumptions about thefirm’s operations.

The major opportunities for student learning are:

1. Leitner, P., “The Fallacy of Safe Harbors: Managing for Value in the Private Firm,” Strategic Finance, April2006, p. 32.2. Good, D. “Business Valuation of Private Firms,” Presentation at the Association of Corporate GrowthAnnual Meeting, Denver, Colorado, June 2005.

849July, 2011

1. To understand a company’s strengths, weaknesses, opportunities, threats, and thecompetitive forces of its industry.

2. To analyze recastings (financial accounting adjustments) for their impacts on reportedearnings, financial condition, cash flows, and business valuation.

3. To construct pro forma income statements and free cash flows for business valuationpurposes.

4. To apply various business valuation methods to understand their impacts on the valueof a business.

5. To consider both financial and nonfinancial factors in making a final recommendationwhether to offer a company for sale.

Potential Audiences and UsesWhitetracks Design, Inc. is intended for both senior-level undergraduate and advanced

graduate case courses in accounting, finance, and entrepreneurship. It should be used laterin these courses after business valuation methods are covered. Students are challenged toanalyze the industry, make adjustments to the reported financial statements, and applyseveral different valuation methods. As such, the case provides an opportunity for studentsto perform these tasks in a real-world setting where the financial information is far fromperfect.

Suggested Teaching ApproachThis case has been used in an Master’s of Business Administration (MBA) course

with finance majors and some accounting students and general MBAs. Instructors willhave to be sensitive to the students’ academic preparation and be prepared to offerdifferent background readings tailored to individual students. It is likely that financestudents will excel with the business valuation approaches but will have some challengeswith the various industry analysis techniques. The opposite results are likely for manage-ment or entrepreneurship students. Thus, industry analysis techniques may need emphasisto finance students, and major business valuation methods may need emphasis to man-agement students before the case is assigned.

We have found that the finance students needed more lecture information on theindustry analysis methods for their impacts on reported earnings, financial condition, cashflows, and business valuation. Both finance and management students did well construct-ing pro forma income statements and free cash flows for business valuation purposes. Butthe management students needed more lecture information on the business valuationapproaches and methods. Both finance and management students did well evaluating bothfinancial and nonfinancial factors in making a final recommendation.

To facilitate a case discussion, the instructor could review major concepts of alterna-tive business valuation methods from any of a number of excellent books on businessvaluation, such as Damodaran (2002) and Pratt (2001). Whitetracks is very flexible;instructors can tailor it to the needs of their individual courses. The case can be taught asa full analysis of all the key issues and discussion points as we do at the University ofDenver, assigning three or four students to each group, giving 1 week for student prepa-ration, and employing a 2-hour class period for discussion. Alternatively, for instructorsnot wanting to devote as much time to all of the issues in the case, selected issues (orvarious combinations thereof) could be taught separately as stand-alone sections. Forexample, solutions to the pro forma free cash flows could be provided to the students to

850 ENTREPRENEURSHIP THEORY and PRACTICE

focus on the business valuation decisions rather than on financial forecasting. Similarly,solutions to the financial statement recastings are already included in the case exhibits.

We use the following assignment questions for students:

1. Perform a SWOT analysis for Whitetracks. Use Porter’s Five Forces model to analyzethe industry.

2. Perform a financial analysis of Whitetracks using financial ratios and common-sizefinancial statements.

3. Estimate earnings before interest, taxes, depreciation, and amortization (EBITDA),earnings before interest and taxes (EBIT), net operating profit after taxes (NOPAT),and free cash flows for Whitetracks over the next 5 years.

4. Use the build-up method to estimate a cost of equity capital for Whitetracks. Estimatea weighted average cost of capital (WACC) for Whitetracks.

5. Estimate the enterprise value and common stock values for Whitetracks using free cashflows. Estimate the terminal value at the end of year 5 using both a constant growthassumption as well as a multiple of EBITDA.

6. Estimate Whitetracks’ enterprise value and a value for all of its common stock usingIBG’s primary private company approach of a multiple times historical recast EBITDAand other methods of comparables or multiples given in the case. Use both trailing andleading year values for EBITDA. Conduct a sensitivity analysis of the value ofWhitetracks to different levels of the multiples.

7. Using Excel Data Tables, perform a sensitivity analysis on the value of Whitetracks by:• Varying WACC and the Terminal Value EBITDA Multiple• Varying the growth rate in total-market size and Whitetracks market share• Varying inventory turnover and days sales outstanding

8. Estimate the value of Whitetracks to a strategic buyer who is able to realize the costsavings given in the case and to improve Whitetracks’ working capital position.Assume that a strategic buyer could lower days sales outstanding (DSO) to 60 days andincrease inventory turnover to 3.8 times.

9. As Mr. Grange, make a final recommendation to the owners. Should Whitetracks besold now or should it be developed further to enhance its value for sale at a later date?

ReadingsInstructors might assign outside readings to assist students in understanding of busi-

ness valuation. Here are some suggested readings:

Damodaran, A. (2002). Investment valuation. New York: Wiley.

Pratt, S. (2001). Market approach to valuing businesses. New York: Wiley.

Role of the AuthorsThe two authors (business professors) have worked with IBG for several years. They

have published several case studies with other top executives at IBG. During the early partof 2006, Professors Grove and Cook met with Mr. Grange and obtained a copy of IBG’sselling book for Whitetracks. Following discussions with Mr. Grange, the professorsdeemed Whitetracks to be an excellent teaching vehicle. Follow-up phone calls, e-mail,and interviews with Mr. Grange and the owners of Whitetracks over the summer of 2006solidified the issues in the case and provided additional financial information on thecompany as well as personal information from the owners.

851July, 2011

![[solution] atkins physical chemistry 9th edition instructors solutions manual](https://img.pdfslide.net/doc/110x75/6348140ade40dd034d0905c7/solution-atkins-physical-chemistry-9th-edition-instructors-solutions-manual.jpg)