Embed Size (px)

Citation preview

2013

Cash Converter By Amanpreet Singh Monga - 430549193

[ANALYSING THE GLOBAL STRATEGY OF CASH CONVENTER]

Executive Summary

Cash Converters International is an organised second hand goods retail chain operated through

franchisee model and its own online e-commerce platform. The company also deals into micro

lending from $ 50 to $ 2000.

Founded in 1984 from Perth, Western Australia and with a presence of more than 140 outlets

in Australia, 700 outlets with representations in 21 countries; they are world’s largest second

hand goods dealer with revenues at AUD 2.34 billion and profits at AUD 29.4 million reported in

financial year ending 2012 (Cash Converter).

This report will focus on external environment analysis of India and then will discuss resources

and capabilities analysing firm’s performance, finally concluding with the suggestion of entry

mode for Cash Converters International Ltd into India in a phased approach with initial entry

mode with a master franchisee (identified partner - RJ Corp) and company owned subsidiary to

tackle financial regulation necessary to operate its micro finance business. Though the report

concludes with concerns of dependency of certain business units with external environment

but suggests India as a potential market for cash converters future growth.

1.0 Introduction

1.1 Brief background of the company and Rationale behind selection:

Cash Converters International originated from Western Australia in 1984 with a business model

of selling franchisee’s and second hand goods from franchisee outlets and its own greenfield

stores; it also offers secured loans to people with personal property as collateral, where one

can take back their collateral within 30 days at 30% premium levied (Cash Converter) and

(Allen, 2012). The rationale behind selection of this company is the business model because

pawn shops or second hand goods sale is a business which is said to do well in times when the

economy is good and even better when the economy is strained (Danubrata & Jittapong,

2013). Apart from the reason of business model, degree of internationalisation1 of the

organisation, highlighting company has a global mindset or capability of local adaptability,

makes it a company of choice for this report.

1.2 Brief assessment of India and reason of selection:

India is a market which already has this business model running from centuries as a highly

unorganised sector (giving gold for short term loan) to local jewellers / money lenders and

selling goods when not in use to kabadiwalas {scrap dealer} (Poduwal & Mehra, 2011). The

market size of this2 industry is estimated to be approx INR 75,000 crore (USD 136 billion

approx) with few organised players (Muthoot Finance and Mannapuram Finance) who just deal

in loans with gold as collateral (Philip, Ghatwai, & Mathew, 2012). Since gold is not an income

generating asset, the best way to monetise/capitalise on the gold lying in India is through

providing loan options; the average gold holding of total Indian households reported in various

articles mention it to be worth (USD 10909 billion approx)3 (Whitehead, 2011), (Keiser, 2012)

and (Pattanayak, 2012). Since Cash converters deal with second hand goods too, analysing the

article in a leading Indian business newspaper economic times by Poduwal & Mehra (2011),

1 Referring lecture “Becoming a global Company” by Dr. Chinmay Pattnaik and slide ‘Degree of Internationalisation’ on structura l Indicators –

the company has representation in 21 countries, listed in 2 stock exchanges (Australia & U.K), maximum proportion of non-capital involvement

abroad through franchisee. Governance Structure – 30% stake owned by U.S based Ezcorp, largest pawn shop operator in terms of market

capitalisation.

2 Giving gold for short term loan

3 Article states average 18,000 to 20,000 tonnes. The tonnes have been converted to grams and divided by average ROE of INR 55 per USD and

converted to billion.

which reports second hand goods industry without automobile estimated at INR 60,000 crore

(USD 109 billion), shows a huge poential market. Further National Council of Applied Economic

Reserach (NCAER) links this growth to product cycles getting shorter due to which the

replacement demands have gone up making second hand product a good subsitute and expects

a population of 267 million to fall in this purchasing category in the coming 5 years {2012-2016},

highlighting growing acceptability of this segment of business which is getting organised with

every passing year (Poduwal & Mehra, 2011).

2.0 External Environment Analysis

2.1 Political Analysis

India is currently being led by United Progressive Alliance (UPA) whose term ends in May 2014

and has been hit by series of corruption scandals during its tenure. These series of corruption

has led to growing frustration amongst the growing middle class and youth who have resorted

to mass protests on streets and through social media. The current Prime Minister (Dr.

Manmohan Singh) is said to have little say in decision making as the real political power resides

with the ruling party Chairman (Ms. Sonia Gandhi). This ambiguity in the powerhouse has led to

delays in policymaking and accountability amongst the officials. Though with the current

elections due in May 2014, it is forecasted that (UPA) will not come to power and BJP with Mr.

Narendra Modi as its prime ministerial candidate could come to power in the centre. If the BJP

comes with majority in the centre, it will be easier to push for economic reforms without

getting into deadlock with alliances and BJP per se to Congress alliance is considered more

business friendly as reported by The Economist (2013). So, it is a wait and watch situation till

the coming elections and it is expected that any economic reforms passed in the interim will

only be to create vote bank or for vested interest (The Economist, 2013) and (Mukherjee,

2013).

2.2 Economic Analysis

The Indian economy is currently going through the tough phase with decade low performance

of GDP @ 5% in 2012-13 which have been related to issues such as high public expenditure,

depleting investment & saving level, depreciation of the rupee and worsening current account

balance. Though these situations look concerning but these growth and slump phases in Indian

economy have been attributed to its gradual rise in foreign trade over years which has

integrated it with the global economy and the global uncertainty which is affecting the Indian

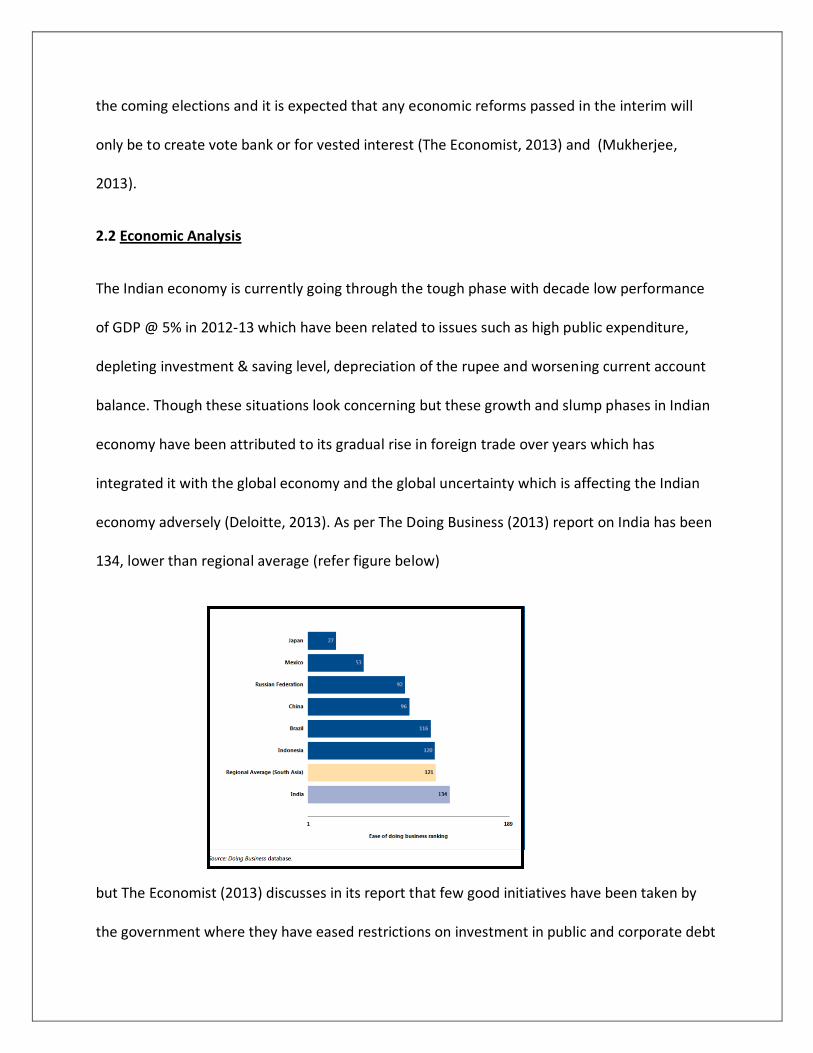

economy adversely (Deloitte, 2013). As per The Doing Business (2013) report on India has been

134, lower than regional average (refer figure below)

but The Economist (2013) discusses in its report that few good initiatives have been taken by

the government where they have eased restrictions on investment in public and corporate debt

by foreign institutional investors and more measures are expected to streamline investment

procedures in the coming years (2013-2017) by the government, where in general an automatic

approval process for foreign investment could be in place in line with guidelines of RBI, a step

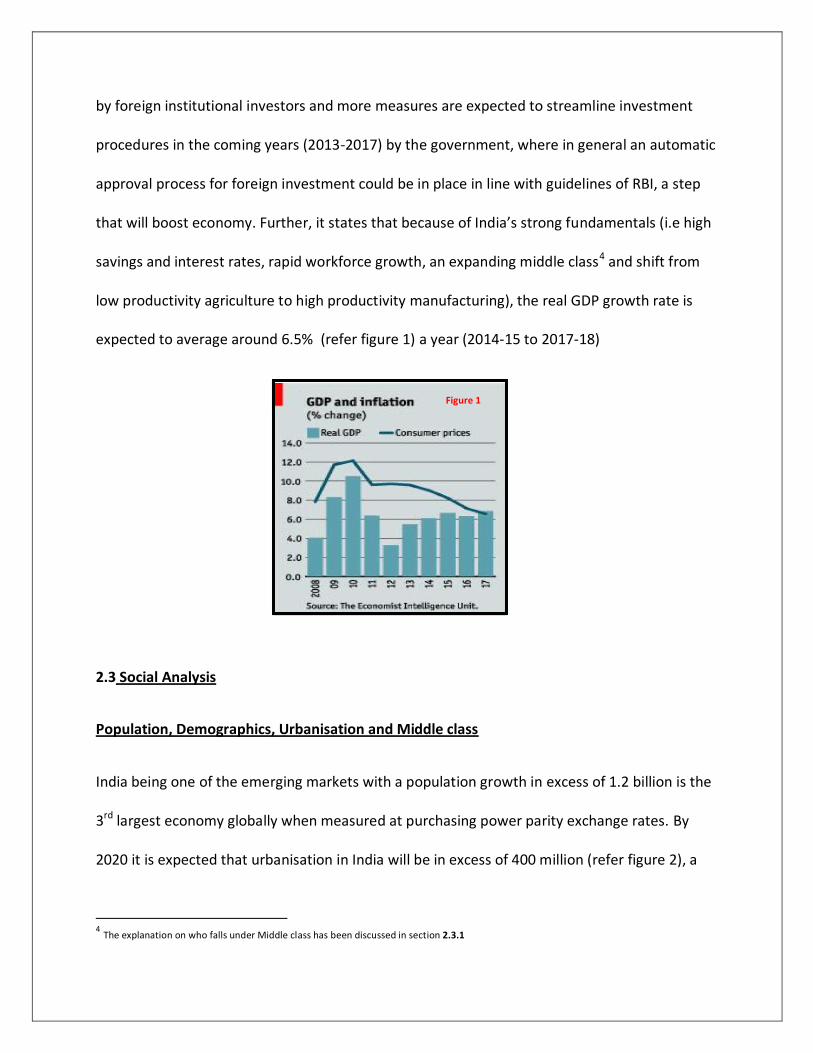

that will boost economy. Further, it states that because of India’s strong fundamentals (i.e high

savings and interest rates, rapid workforce growth, an expanding middle class4 and shift from

low productivity agriculture to high productivity manufacturing), the real GDP growth rate is

expected to average around 6.5% (refer figure 1) a year (2014-15 to 2017-18)

2.3 Social Analysis

Population, Demographics, Urbanisation and Middle class

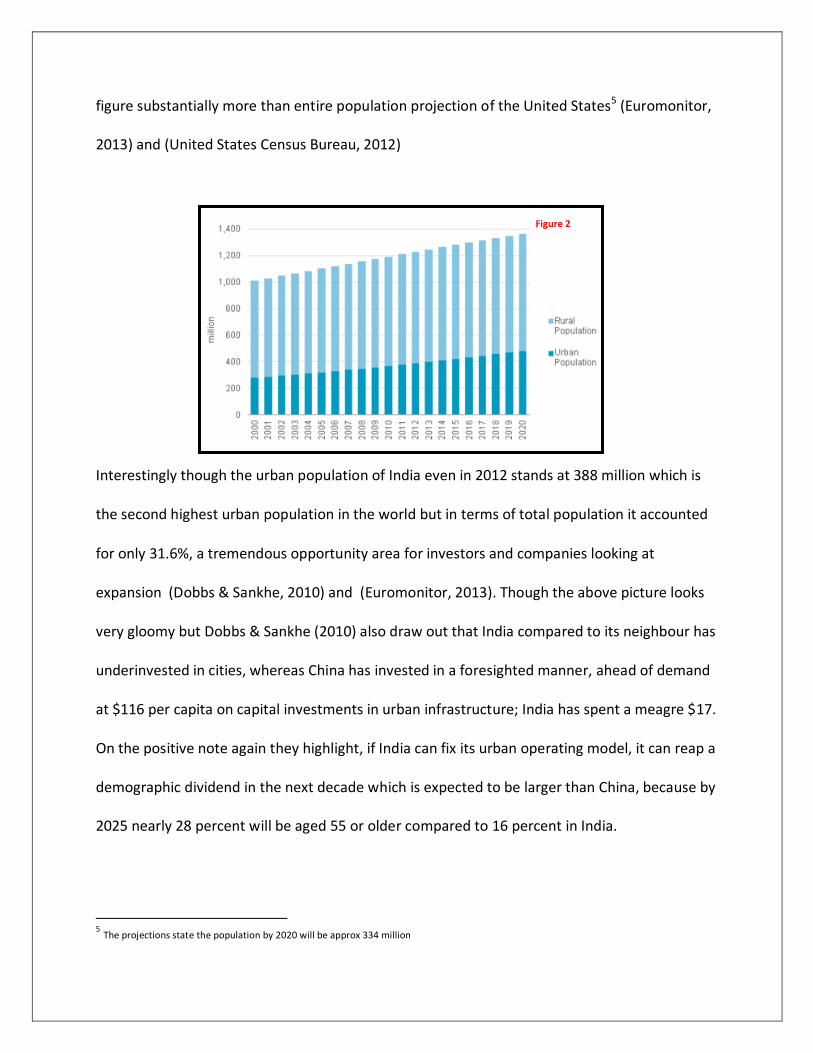

India being one of the emerging markets with a population growth in excess of 1.2 billion is the

3rd largest economy globally when measured at purchasing power parity exchange rates. By

2020 it is expected that urbanisation in India will be in excess of 400 million (refer figure 2), a

4 The explanation on who falls under Middle class has been discussed in section 2.3.1

Figure 1

figure substantially more than entire population projection of the United States5 (Euromonitor,

2013) and (United States Census Bureau, 2012)

Interestingly though the urban population of India even in 2012 stands at 388 million which is

the second highest urban population in the world but in terms of total population it accounted

for only 31.6%, a tremendous opportunity area for investors and companies looking at

expansion (Dobbs & Sankhe, 2010) and (Euromonitor, 2013). Though the above picture looks

very gloomy but Dobbs & Sankhe (2010) also draw out that India compared to its neighbour has

underinvested in cities, whereas China has invested in a foresighted manner, ahead of demand

at $116 per capita on capital investments in urban infrastructure; India has spent a meagre $17.

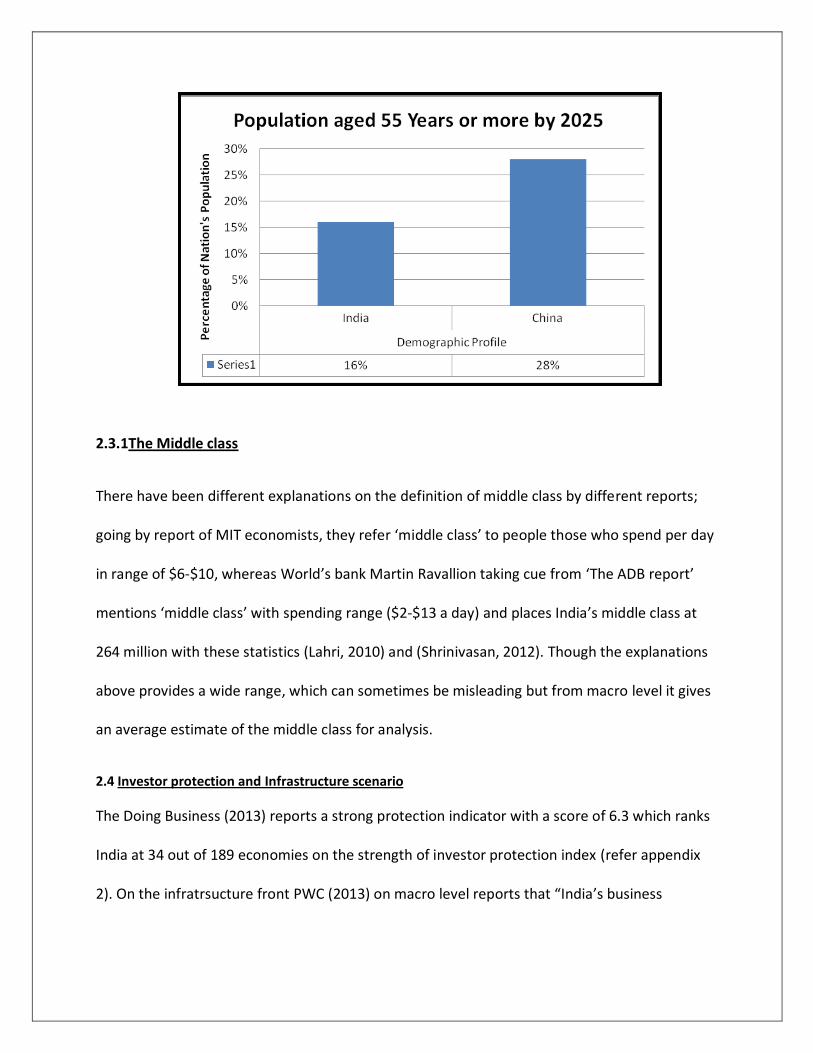

On the positive note again they highlight, if India can fix its urban operating model, it can reap a

demographic dividend in the next decade which is expected to be larger than China, because by

2025 nearly 28 percent will be aged 55 or older compared to 16 percent in India.

5 The projections state the population by 2020 will be approx 334 million

Figure 2

2.3.1The Middle class

There have been different explanations on the definition of middle class by different reports;

going by report of MIT economists, they refer ‘middle class’ to people those who spend per day

in range of $6-$10, whereas World’s bank Martin Ravallion taking cue from ‘The ADB report’

mentions ‘middle class’ with spending range ($2-$13 a day) and places India’s middle class at

264 million with these statistics (Lahri, 2010) and (Shrinivasan, 2012). Though the explanations

above provides a wide range, which can sometimes be misleading but from macro level it gives

an average estimate of the middle class for analysis.

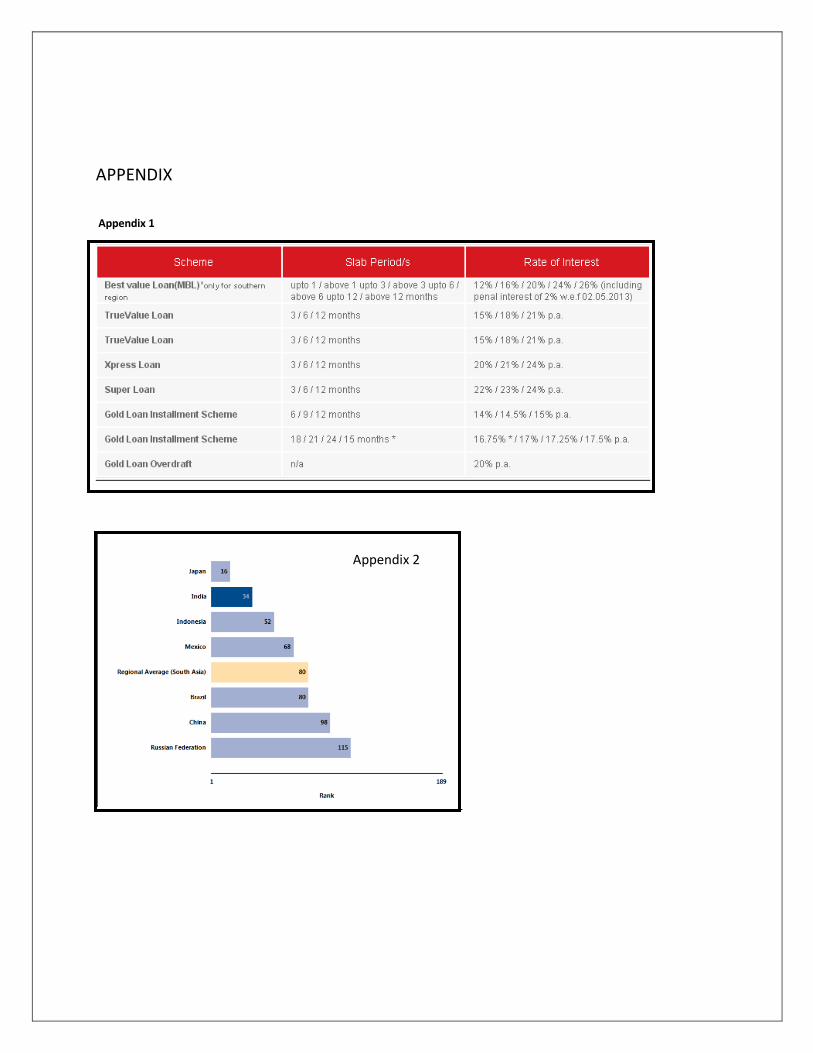

2.4 Investor protection and Infrastructure scenario

The Doing Business (2013) reports a strong protection indicator with a score of 6.3 which ranks

India at 34 out of 189 economies on the strength of investor protection index (refer appendix

2). On the infratrsucture front PWC (2013) on macro level reports that “India’s business

community repeatedly cites infrastructure as the single biggest hindrance to doing business,

well ahead of corruption and bureaucracy”; ranking India 84th out 144 countries6 evaluated.

Looking at infrastructure issues per se to retail industry Deloitte (2010) reports that finding the

right location with the right rental for stores is some what a challenge for all retailers because

rent forms a large portion of the expense from the profits.

3.0 Detailed Analysis of Retail industry – Franchisee market, Second hand goods & Micro Loan

Franchisee market:

The organised retail industry in India is reported by KPMG to be around USD 24 billion and just

2.5% of business is done through franchisee model compared to 50% done in U.S. It is further

discussed that Franchising industry will quadruple in volume in the coming five years (2013-

2017) that will account for almost 4% of India’s GDP (gross domestic product) (Narayan, 2013).

Further, analysing the report of Franchise Council of Australia, it provides a promising growth in

tandem with the KPMG report discussed above, mentioning a 35% growth annually in the

franchisee sector in India. Though the food franchisee is supposedly said to be the easier one to

introduce in India but interestingly micro level understanding of religion is not required for a

Cash Converter type business as in food franchisee, because to operate in India one must take

into consideration those factors. Overall it is said to be a promising franchisee market of future

( Franchise Business AU, 2011).

6 The report refers, The global competitiveness report 2012-2013 http://www3.weforum.org/docs/WEF_GlobalCompetitivenessReport_2012-

2013.pdf for further

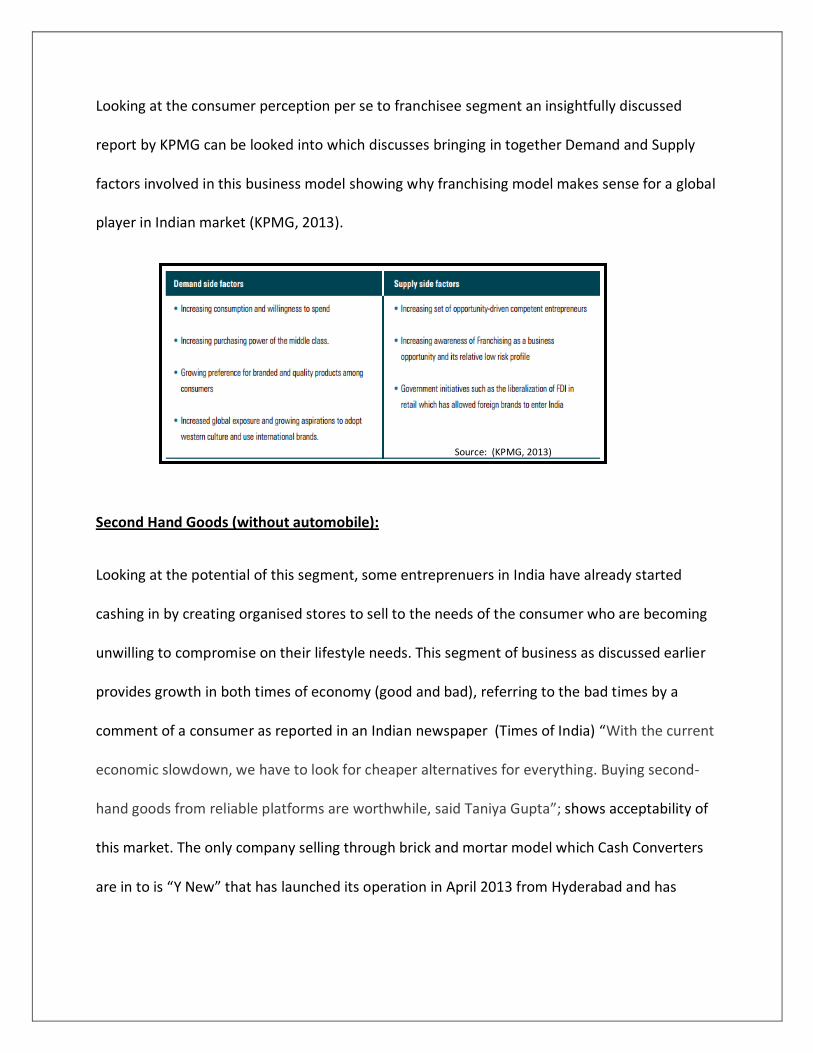

Looking at the consumer perception per se to franchisee segment an insightfully discussed

report by KPMG can be looked into which discusses bringing in together Demand and Supply

factors involved in this business model showing why franchising model makes sense for a global

player in Indian market (KPMG, 2013).

Second Hand Goods (without automobile):

Looking at the potential of this segment, some entreprenuers in India have already started

cashing in by creating organised stores to sell to the needs of the consumer who are becoming

unwilling to compromise on their lifestyle needs. This segment of business as discussed earlier

provides growth in both times of economy (good and bad), referring to the bad times by a

comment of a consumer as reported in an Indian newspaper (Times of India) “With the current

economic slowdown, we have to look for cheaper alternatives for everything. Buying second-

hand goods from reliable platforms are worthwhile, said Taniya Gupta”; shows acceptability of

this market. The only company selling through brick and mortar model which Cash Converters

are in to is “Y New” that has launched its operation in April 2013 from Hyderabad and has

Source: (KPMG, 2013)

already done business worth INR 45 lakhs (USD 81,000 approx) just from a single store as of

September 2013 (Banerjee, 2013).

Micro Loan or Credit:

Every country will have a different definition of micro credit or loan. From India’s perspective

going through definition level as per RBI Master Circular 2008 it is defined as “provision of

thrift, credit and other financial services and products of very small amount to the poor in rural,

semi-urban and urban areas for enabling them to raise their income levels and improve living

standards. Micro Credit Institutions are those, which provide these facilities” and from

regulatory point of view institutions that provide loans upto Rs 50000/- (USD 909), and in case

of loan for a dwelling unit, upto Rs 125000/- (USD 2270) are waived from RBI regulations which

are required for Banks as per (NOTIFICATION No. DNBS.138/CGM(VSNM)-2000 dated January

13, 2000) (Kothari & Gupta).

Entry Requirements:

Overseas Organisation as per RBI will have to furnish certificate of due diligence7 from an

overseas bank which in turn is subject to regulation of host-country regulator and adheres to

Financial Action Task Force (FATF) (Reserve Bank of India, 2011).

7 (i) that the lender maintains an account with the bank for at least a period of two years, (ii) that the lending entity is organized as per the local

law and held in good esteem by the business/local community and (iii) that there is no criminal action pending against it. For detailed guidelines and financial capping please refer [http://rbidocs.rbi.org.in/rdocs/notification/PDFs/59APDMFI191211.pdf]

Interest Charges on loan currently applicable for company evaluation:

In order to evaluate the interest charges that can be levied on the loan for gold or other

collateral as per the Cash Converters business model, the leading player in the field ‘Muthoot

Finance’ website was referred to, to understand the market trend in terms of interest rate that

can be levied and it showed an average range of 15% - 24% annual interest rate8 on diminishing

balance being levied to the consumer (Muthoot Finance) (refer appendix 1 for detailed

structure)

3.1 Analysis of Company’s Resources and Capabilities

The key resources and capabilities of Cash Converters Tangible – (financial capacity – AUD 27

million profits as of 2011 (Cash Converters International Limited, 2011)), which compared to

other small players gives them an edge to hold better and more quantity of stocks in the

company owned and operated outlets. The better financial capability will give an edge over

smaller players while promoting their brand, Intangible – (Brand Value), that the buyers will get

instant cash for their product and sellers will get product which has been evaluated by experts

at a competitive price and Human Resources – (Training, expereince and adaptability) with 28

years of experience and established systems and controls in place which have developed over

years with a sound track record of establishing and managing site network on a global basis

gives them an edge over other mom and pop stores or small unorganised retailers (Cash

Converters, February 2013), (Allen, 2012) and (Byline, 2006).

8 The interest rate is just for reference for any internal calculation required by the reader and is as of date (6.11.2013), subject to RBI

guidelines.

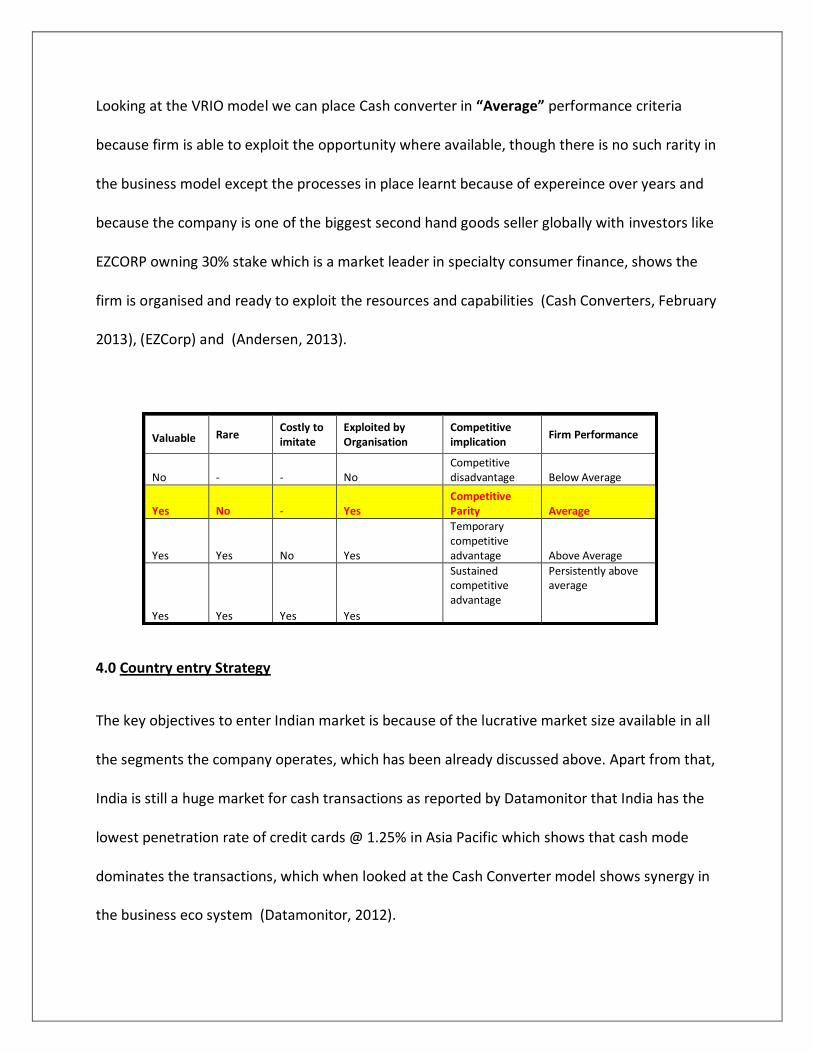

Looking at the VRIO model we can place Cash converter in “Average” performance criteria

because firm is able to exploit the opportunity where available, though there is no such rarity in

the business model except the processes in place learnt because of expereince over years and

because the company is one of the biggest second hand goods seller globally with investors like

EZCORP owning 30% stake which is a market leader in specialty consumer finance, shows the

firm is organised and ready to exploit the resources and capabilities (Cash Converters, February

2013), (EZCorp) and (Andersen, 2013).

Valuable Rare

Costly to imitate

Exploited by Organisation

Competitive implication

Firm Performance

No - - No Competitive disadvantage Below Average

Yes No - Yes Competitive Parity Average

Yes Yes No Yes

Temporary competitive advantage Above Average

Yes Yes Yes Yes

Sustained competitive advantage

Persistently above average

4.0 Country entry Strategy

The key objectives to enter Indian market is because of the lucrative market size available in all

the segments the company operates, which has been already discussed above. Apart from that,

India is still a huge market for cash transactions as reported by Datamonitor that India has the

lowest penetration rate of credit cards @ 1.25% in Asia Pacific which shows that cash mode

dominates the transactions, which when looked at the Cash Converter model shows synergy in

the business eco system (Datamonitor, 2012).

4.1 Entry Mode and Post Entry Strategy

The appropriate entry mode for the company should be through a mix of company subsidiary

and master franchisee model who should have the pan India rights to sell the franchisees. The

most suitable partner that has been identified is RJ Corp which runs subsidiaries like Devyani

International Limited, the reason to choose them is because of their expertise in handling

franchisee model for variuos F & B brands like (Pizza hut, KFC, Costa Coffee etc) and interests in

other mushrooming retail sectors (PTI, 2011).

The company can be seen as people centric from their vision statement and also from the

innovative policies that have been used inside organisation for which they were awarded

‘Breakthrough Bucket Award’ where they had launched 1st KFC store in Indian Subcontinent

with hearing and speech impaired team members. This shows company has a good image, is

people centric and focuses towards corporate social responsbility which will help Cash

Converters leverage from their strengths (Devyani International Limited).

Apart from ‘qualitative’ strengths, on the ‘quantitative’ front RJ Corp revenues in 2011-12 were

around USD 800 million from Indian operation and USD 1.2 billion including their Africa

operations (RJ Corp). With its international exposure, strong powerful management tools to

drive its operations and to motivate employees (i.e Balance score card, Employee profit and

loss management, Bench- Planning & Voice of Champions) and last but not least strong retail

presence through the franchisee model. Looking at these characteristics along with external

environment of India and resources & capabilities of Cash converters, RJ corp seems to be the

best fit as master franchisee partner.

The legal agreement should only exist between company and Rj Corp. Cash Converters should

clearly draft responsibilities of services, targets, investment in brand promotion in their

agreement with RJ Corp to avoid conflict when franchisee business comes at saturation level

and the company wants to enter with direct company owned/operated stores or when they

want to exit from the relationship with their master franchisee (ET Bureau, 2012).

Post Entry Strategy

The company should have two phased approach post entry strategy. The company should have

the approach in the lines of Yum! Brands Inc, where they launched their Pizza hut chains in

Phase -1 through master franchisee to kick start the business and enter directly with company

owned and operated stores in Phase-2 because of limited capcaity of the franchisee which

could not give them the growth in tandem with the growing market (ET Bureau, 2012). The

subsidiary should work as a support function to master franchisee and should monitor the

service levels and improvements in processes in accordance to the corporate strategy and

standards.

Brand Positioning

Since Cash converters has different models or streams of revenue, each revenue stream9 has to

be targeted seperately.

Franchisee – This should be positioned as a premium brand showcasing companies background,

financial capabilities and profitability model to capatalize maximum on franchisee fee.

9 Master franchisee as stream has not been taken into account, considering it will be a corporate level one time decision.

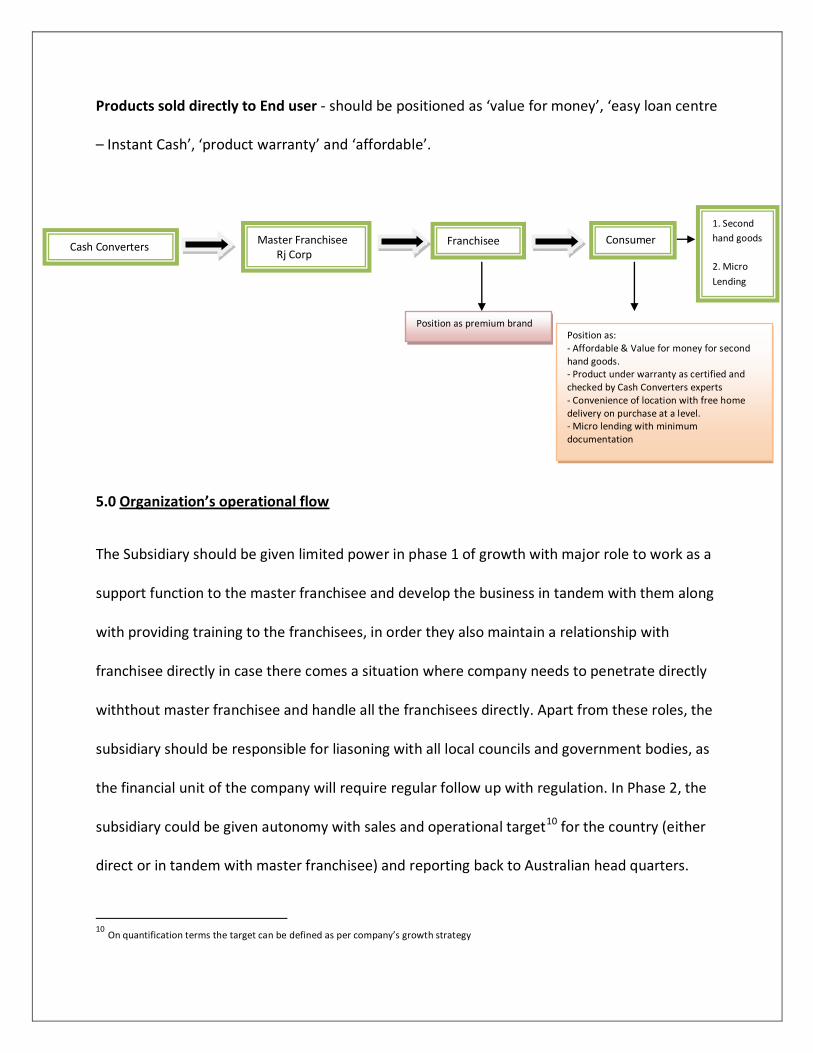

Products sold directly to End user - should be positioned as ‘value for money’, ‘easy loan centre

– Instant Cash’, ‘product warranty’ and ‘affordable’.

5.0 Organization’s operational flow

The Subsidiary should be given limited power in phase 1 of growth with major role to work as a

support function to the master franchisee and develop the business in tandem with them along

with providing training to the franchisees, in order they also maintain a relationship with

franchisee directly in case there comes a situation where company needs to penetrate directly

withthout master franchisee and handle all the franchisees directly. Apart from these roles, the

subsidiary should be responsible for liasoning with all local councils and government bodies, as

the financial unit of the company will require regular follow up with regulation. In Phase 2, the

subsidiary could be given autonomy with sales and operational target10 for the country (either

direct or in tandem with master franchisee) and reporting back to Australian head quarters.

10 On quantification terms the target can be defined as per company’s growth strategy

Cash Converters Master Franchisee Rj Corp

Franchisee Consumer

1. Second

hand goods

2. Micro

Lending

Position as premium brand Position as: - Affordable & Value for money for second hand goods. - Product under warranty as certified and checked by Cash Converters experts - Convenience of location with free home delivery on purchase at a level. - Micro lending with minimum documentation

6.0 Conclusion

Though the market size and potential is huge but the money lending business is too dependent

on external environment which we can analyse from the report of John Rolfe in ‘The Telegraph’,

where he discusses the impact of how tighter consumer credit rules by Australian minister

affected the Cash converters business in Australia which fell by 26% post the new consumer

credit rule came into place (Rolfe, 2013). The company needs to keep high visibility and brand

recall because the whole business model is dependent on end users as they are the suppliers

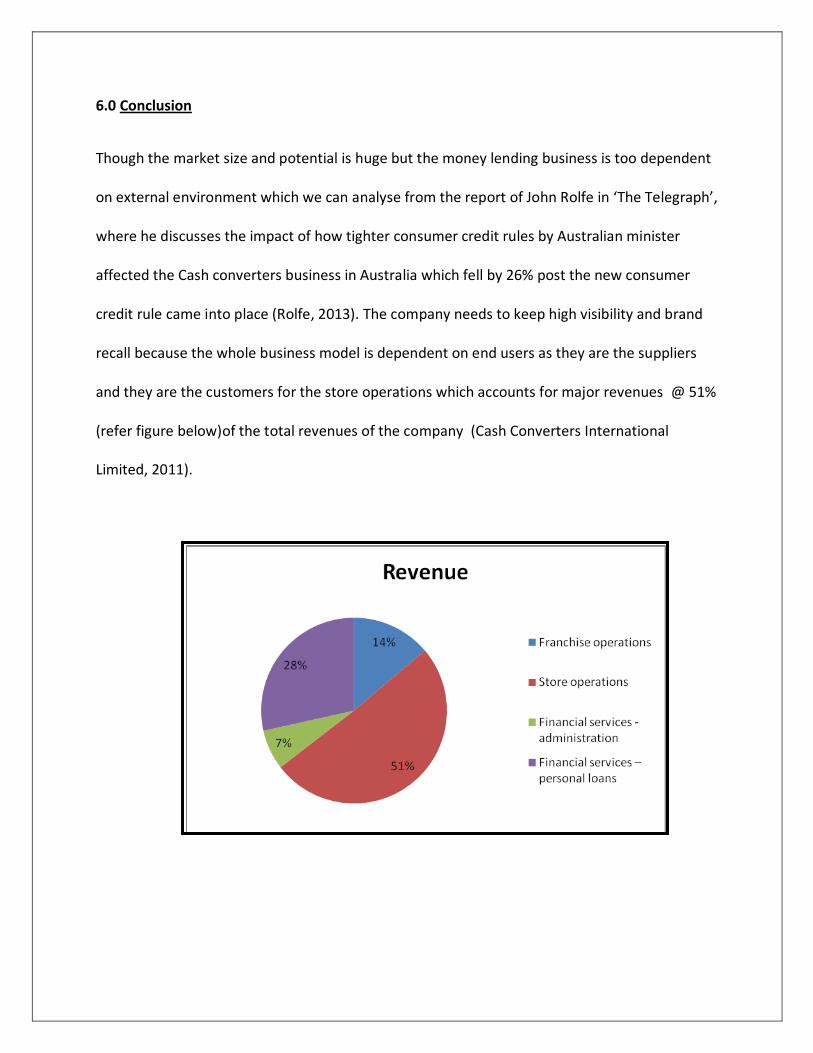

and they are the customers for the store operations which accounts for major revenues @ 51%

(refer figure below)of the total revenues of the company (Cash Converters International

Limited, 2011).

APPENDIX

Appendix 1

Appendix 2

References Franchise Business AU. (2011, 11 15). India’s franchising industry booms with many

opportunities for Australians. Retrieved 11 06, 2013, from Franchise Business:

http://www.franchisebusiness.com.au/c/Franchise-Business-AU/India-s-franchising-industry-

booms-with-many-opportunities-for-Australians-n914137

Allen, G. (2012, 01 16). Mail Online. Retrieved 11 03, 2013, from Mail Online:

http://www.dailymail.co.uk/news/article-2087290/Cash-Converters-buys-second-hand-goods-

rock-prices-adds-huge-mark-ups-selling-on.html

Andersen, P. (2013, 09 10). Cash Converters to raise some cash of its own. Retrieved 11 06,

2013, from 9 news Finance:

http://finance.ninemsn.com.au/newsbusiness/motley/8721121/cash-converters-to-raise-

some-cash-of-its-own

Banerjee, A. (2013, 09 24). Second-hand stores gaining popularity in Hyderabad. Retrieved 11

06, 2013, from The Times of India: http://articles.timesofindia.indiatimes.com/2013-09-

24/hyderabad/42359477_1_second-hand-market-6-lakh-gadgets

Byline, N. (2006, 10 02). Cash Converters cashes in: [CITY FINAL Edition]. Edinburgh, UK.

Cash Converter. (n.d.). Cash Converters. Retrieved 11 02, 2013, from Cash Converters:

http://www.cashconverters.com/

Cash Converter. (n.d.). Cash Converters International Limited. Retrieved 11 03, 2013, from Cash

Converters: www.cashconverters.com/Files/Download/972

Cash Converters International Limited. (2011). Annual Report 2011. Australia: Cash Converters

International Limited.

Cash Converters. (February 2013). Investor Presentation. Cash Converters.

Danubrata, E., & Jittapong, K. (2013, 09 10). Pawnshops hit paydirt as Southeast Asians sweat

before pay day. Retrieved 11 02, 2013, from Reuters:

http://www.reuters.com/article/2013/09/10/us-asia-pawnshops-idUSBRE98908520130910

Datamonitor. (2012, 02 17). Datamonitor. Retrieved 11 07, 2013, from Datamonitor:

http://www.datamonitor.com/store/News/indias_credit_card_market_holds_untapped_poten

tial?productid=5861ECB8-961F-48C1-BC5C-D42EC0824C56

Deloitte. (2013, February). Deloitte. Retrieved 11 04, 2013, from Deloitte:

http://www.deloitte.com/assets/Dcom-

India/Local%20Assets/Documents/Budget%202013/Budget_Publication_2013.pdf

Deloitte. (2010, 08). Indian Retail Market. Retrieved 11 07, 2013, from Deloitte:

http://www.deloitte.com/assets/Dcom-

India/Local%20Assets/Documents/Retail%20POV_low.pdf

Devyani International Limited. (n.d.). Devyani International Limited. Retrieved 11 07, 2013, from

Devyani International Limited: http://dil-rjcorp.com/awards.aspx

Dobbs, R., & Sankhe, S. (2010, 06). Comparing urbanization in China and India. Retrieved 11 05,

2013, from McKinsey & Company:

http://www.mckinsey.com/insights/urbanization/comparing_urbanization_in_china_and_india

ET Bureau. (2012, 09 28). The Economic Times. Retrieved 11 07, 2013, from The Economic

Times: http://articles.economictimes.indiatimes.com/2012-09-28/news/34148349_1_qsr-

chain-pizza-hut-largest-pizza-chain

Euromonitor. (2013, 05 09). India’s Rapid Unplanned Urbanisation Creates Opportunities and

Challenges - See more at: http://blog.euromonitor.com/2013/05/indias-rapid-unplanned-

urbanisation-creates-opportunities-and-challenges.html#sthash.4H9uwEC7.dpuf. Retrieved 11

05, 2013, from Euromonitor: http://blog.euromonitor.com/2013/05/indias-rapid-unplanned-

urbanisation-creates-opportunities-and-challenges.html

EZCorp. (n.d.). EZCorp. Retrieved 11 06, 2013, from EZCorp: http://www.ezcorp.com/about

Keiser, M. (2012, 11 29). Financial War Reports. Retrieved 11 03, 2013, from Financial War

Reports: http://www.maxkeiser.com/2012/11/indian-households-have-piled-up-as-much-as-

20000-tonnes-of-gold-worth-1-16-trillion-an-historic-high/

Kothari, V., & Gupta, N. (n.d.). Micro Credit in India:Overview of regulatory scenario. Retrieved

11 06, 2013, from CSC archive: http://eprints.cscsarchive.org/317/1/Micro_Credit_in_India-

Overview_of_the_Regulatory_Scenario.pdf

KPMG. (2013). Collaborating for Growth. Retrieved 11 06, 2013, from KPMG:

http://www.kpmg.com/IN/en/IssuesAndInsights/ArticlesPublications/Documents/Collaborating

_for_Growth.pdf

Lahri, T. (2010, 08 19). Much of Indian ‘Middle Class’ Is Almost Poor. Retrieved 11 05, 2013,

from The Wall Street Journal: http://wsj.com/indiarealtime/2010/08/19/majority-of-indian-

middle-class-is-almost-poor/

Mukherjee, A. (2013, 01 02). Reuters. Retrieved 11 04, 2013, from Reuters:

reuters.com/breakingviews/2013/01/02/india-braces-for-last-year-of-political-stability/

Muthoot Finance. (n.d.). Muthoot Finance. Retrieved 11 06, 2013, from Muthoot Finance:

http://www.muthootfinance.com/gold-loan/

Narayan, S. (2013, 07 04). Indian franchise business to grow fourfold by 2017: KPMG. Retrieved

11 06, 2013, from Live Mint & The Wall Street Journal:

http://www.livemint.com/Industry/rYk34sN037WIxS4tX9xP9H/Indian-franchise-business-to-

grow-fourfold-by-2017-KPMG.html

Pattanayak, B. (2012, 11 29). Indians hoard 20k tonnes gold worth record $1.16 trn. Retrieved

11 3, 2013, from The Financial Express: http://www.financialexpress.com/news/indians-hoard-

20k-tonnes-gold-worth-record-1.16-trn/1037761

Philip, S., Ghatwai, M., & Mathew, G. (2012, 01 23). Lining up to pawn the family gold.

Retrieved 11 04, 2013, from Indian Express: http://www.indianexpress.com/news/lining-up-to-

pawn-the-family-gold/903093/

Poduwal, S., & Mehra, M. (2011, 10 30). The story of India's Rs 60,000 cr second-hand market,

minus cars and bikes. Retrieved 11 03, 2013, from The Economic Times:

http://articles.economictimes.indiatimes.com/2011-10-30/news/30336718_1_second-hand-

market-incomes-product-cycles

PTI. (2011, 01 18). The Economic Times. Retrieved 11 07, 2013, from The Economic Times:

http://articles.economictimes.indiatimes.com/2011-01-18/news/28430321_1_rj-corp-

chairman-devyani-international-public-issue

PWC. (2013). India : A Snapshot. Retrieved 11 07, 2013, from PWC:

http://www.pwc.com/gx/en/capital-projects-infrastructure/assets/pwc_gridlnessnapshot-

india2013.pdf

Reserve Bank of India. (2011, 12 19). Reserve Bank of India. Retrieved 11 06, 2013, from

Reserve Bank of India: http://rbidocs.rbi.org.in/rdocs/notification/PDFs/59APDMFI191211.pdf

RJ Corp. (n.d.). RJ Corp. Retrieved 11 07, 2013, from RJ Corp: http://www.rjcorp.in/

Rolfe, J. (2013, 06 07). Bill has payday lenders by the Shorten curlies. Retrieved 11 07, 2013,

from The Telegraph: http://www.dailytelegraph.com.au/news/nsw/bill-has-payday-lenders-by-

the-shorten-curlies/story-fni0cx12-1226659159511

Shrinivasan, R. (2012, 12 01). Middle class: Who are they? Retrieved 11 05, 2013, from The

Times of India - Crest Edition: http://www.timescrest.com/society/middle-class-who-are-they-

9301

The Doing Business. (2013). Doing Business 2014. Doing Business - A world bank group

corporate Flagship.

The Economist. (2013, 08). ProQuest Central -The Economist Intelligence Unit. Retrieved 11 04,

2013, from The Economist Intelligence Unit:

http://search.proquest.com.ezproxy2.library.usyd.edu.au/docview/1428856724#

United States Census Bureau. (2012). Population Projection. Retrieved 11 05, 2013, from United

States Census Bureau:

http://www.census.gov/population/projections/data/national/2012/summarytables.html

Whitehead, J. (2011, 04 18). Pawn Business in India Thriving with Gold Boom. Retrieved 11 03,

2013, from Pawnshop Consulting Group, Inc.:

http://www.pawnshopconsultinggroup.com/pawn-business-in-india-thriving-with-gold-boom/