Embed Size (px)

Citation preview

1

Protected “Investor” and “Investment”

— A Perspective from the Greater Bay Area

Xueyu Yang and Zeyu Huang1

Abstract: The phenomenon of “Chinese disequilibrium” in investment arbitration has been

fading away in recent years. Six investor-State arbitrations initiated by investors domiciled or having residency in the Greater Bay Area (GBA) have contributed to the China-related investment arbitration jurisprudence by demystifying the notions of “investor” and “investment”. This paper aims to examine the peculiar notions of “investor” and “investment” in the context of the GBA by reviewing the treaty-based arbitrations initiated by Chinese investors. Keywords: Investor-State Arbitration, Investor, Investment, Greater Bay Area

I. Introduction

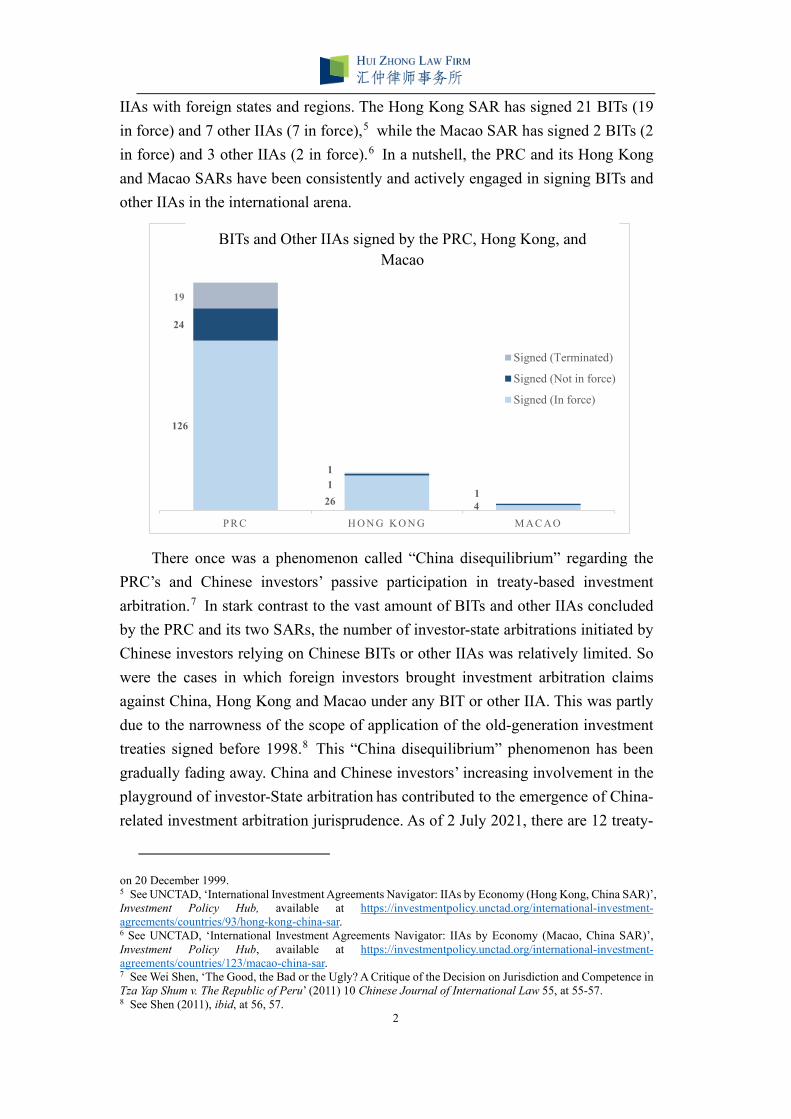

The People’s Republic of China (“PRC” or “China”) has been an active player in concluding bilateral investment treaty (“BIT”) and other international investment agreement (“IIA”) with investment provisions. As of June 2021, the PRC has already signed 145 BITs (107 in force) and 24 other IIAs (19 in force),2 including the most recent “RCEP”, i.e., the Regional Comprehensive Economic Partnership signed in 2020. 3 Besides, the Hong Kong and Macao Special Administrative Regions (“SARs”) of the PRC, by exercising the freedom of joining international agreements in their own names in economic and trade fields,4 have also concluded BITs or other

1 Xueyu Yang is a partner of Hui Zhong Law Firm based in Beijing. Ms. Yang has particular expertise in handling complex contentious matters involving multiple jurisdictions. Ms. Yang has advised both domestic and foreign clients in proceedings conducted at the ICSID, PCA, ICC, HKIAC, SIAC, CIEATC, BAC and different levels of domestic courts including the Supreme People’s Court of China. Zeyu Huang is an associate of Hui Zhong Law Firm based in Shenzhen. Mr. Huang obtained his LLB (Bachelor of Laws) degree from the Remin University of China Law School. He is also a PhD candidate & LLM and teaches private international law (legal practice) undergraduate course at the Faculty of Law in University of Macau. 2 See UNCTAD, ‘International Investment Agreements Navigator: IIAs by Economy (China)’, Investment Policy Hub, available at https://investmentpolicy.unctad.org/international-investment-agreements/countries/42/china. 3 See the Regional Comprehensive Economic Partnership, which was signed on 15 November 2020, with six Contracting Parties, namely, the Association of South-East Asian Nations (ASEN), Australia, China, Japan, New Zealand, and Korea. For more information, see the official website of the RCEP: https://rcepsec.org/. 4 See Article 151 of the Basic Law of the Hong Kong Special Administrative Region of the People’s Republic of China, which was promulgated by the National People’s Congress on 4 April 1990 and entered into force on 1 July 1997; Article 136 of the Basic Law of the Macao Special Administrative Region of the People’s Republic of China, which was promulgated by the National People’s Congress on 31 March 1993 and entered into force

2

IIAs with foreign states and regions. The Hong Kong SAR has signed 21 BITs (19 in force) and 7 other IIAs (7 in force),5 while the Macao SAR has signed 2 BITs (2 in force) and 3 other IIAs (2 in force).6 In a nutshell, the PRC and its Hong Kong and Macao SARs have been consistently and actively engaged in signing BITs and other IIAs in the international arena.

There once was a phenomenon called “China disequilibrium” regarding the PRC’s and Chinese investors’ passive participation in treaty-based investment arbitration.7 In stark contrast to the vast amount of BITs and other IIAs concluded by the PRC and its two SARs, the number of investor-state arbitrations initiated by Chinese investors relying on Chinese BITs or other IIAs was relatively limited. So were the cases in which foreign investors brought investment arbitration claims against China, Hong Kong and Macao under any BIT or other IIA. This was partly due to the narrowness of the scope of application of the old-generation investment treaties signed before 1998.8 This “China disequilibrium” phenomenon has been gradually fading away. China and Chinese investors’ increasing involvement in the playground of investor-State arbitration has contributed to the emergence of China-related investment arbitration jurisprudence. As of 2 July 2021, there are 12 treaty-

on 20 December 1999. 5 See UNCTAD, ‘International Investment Agreements Navigator: IIAs by Economy (Hong Kong, China SAR)’, Investment Policy Hub, available at https://investmentpolicy.unctad.org/international-investment-agreements/countries/93/hong-kong-china-sar. 6 See UNCTAD, ‘International Investment Agreements Navigator: IIAs by Economy (Macao, China SAR)’, Investment Policy Hub, available at https://investmentpolicy.unctad.org/international-investment-agreements/countries/123/macao-china-sar. 7 See Wei Shen, ‘The Good, the Bad or the Ugly? A Critique of the Decision on Jurisdiction and Competence in Tza Yap Shum v. The Republic of Peru’ (2011) 10 Chinese Journal of International Law 55, at 55-57. 8 See Shen (2011), ibid, at 56, 57.

126

26 4

24

11

19

P R C H O N G K O N G M A C A O

Signed (Terminated)

Signed (Not in force)

Signed (In force)

1

BITs and Other IIAs signed by the PRC, Hong Kong, and Macao

3

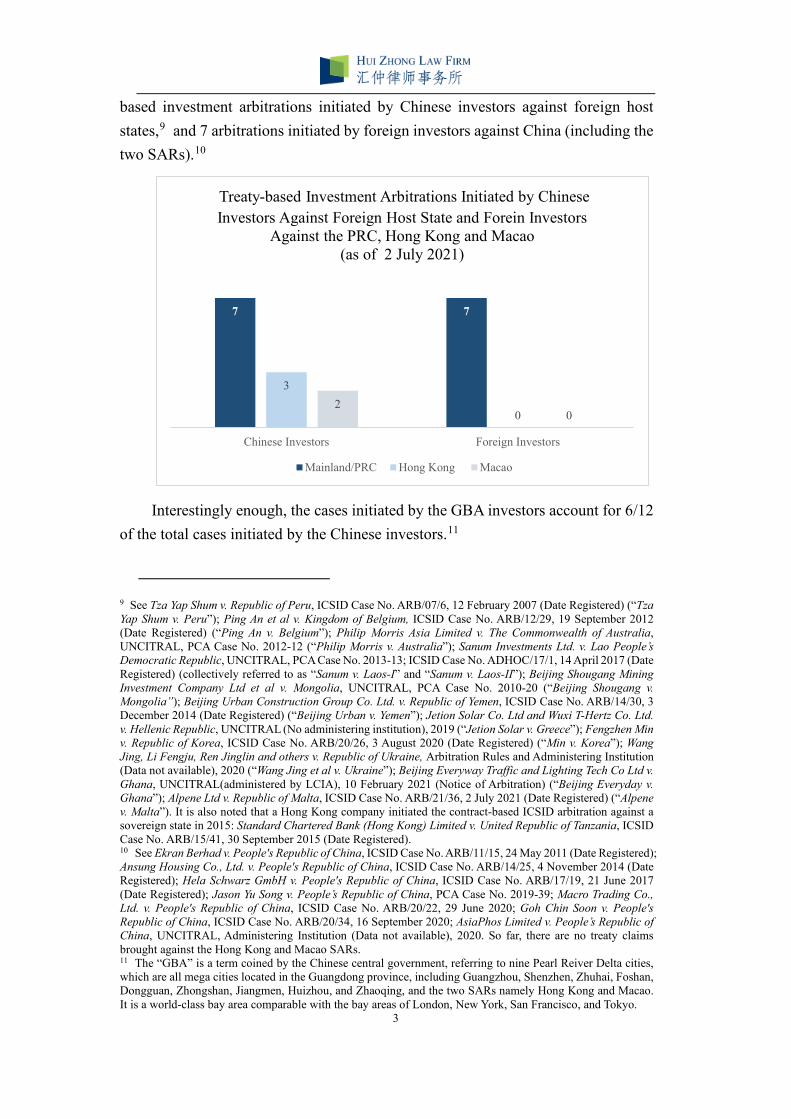

based investment arbitrations initiated by Chinese investors against foreign host states,9 and 7 arbitrations initiated by foreign investors against China (including the two SARs).10

Interestingly enough, the cases initiated by the GBA investors account for 6/12 of the total cases initiated by the Chinese investors.11

9 See Tza Yap Shum v. Republic of Peru, ICSID Case No. ARB/07/6, 12 February 2007 (Date Registered) (“Tza Yap Shum v. Peru”); Ping An et al v. Kingdom of Belgium, ICSID Case No. ARB/12/29, 19 September 2012 (Date Registered) (“Ping An v. Belgium”); Philip Morris Asia Limited v. The Commonwealth of Australia, UNCITRAL, PCA Case No. 2012-12 (“Philip Morris v. Australia”); Sanum Investments Ltd. v. Lao People’s Democratic Republic, UNCITRAL, PCA Case No. 2013-13; ICSID Case No. ADHOC/17/1, 14 April 2017 (Date Registered) (collectively referred to as “Sanum v. Laos-I” and “Sanum v. Laos-II”); Beijing Shougang Mining Investment Company Ltd et al v. Mongolia, UNCITRAL, PCA Case No. 2010-20 (“Beijing Shougang v. Mongolia”); Beijing Urban Construction Group Co. Ltd. v. Republic of Yemen, ICSID Case No. ARB/14/30, 3 December 2014 (Date Registered) (“Beijing Urban v. Yemen”); Jetion Solar Co. Ltd and Wuxi T-Hertz Co. Ltd. v. Hellenic Republic, UNCITRAL (No administering institution), 2019 (“Jetion Solar v. Greece”); Fengzhen Min v. Republic of Korea, ICSID Case No. ARB/20/26, 3 August 2020 (Date Registered) (“Min v. Korea”); Wang Jing, Li Fengju, Ren Jinglin and others v. Republic of Ukraine, Arbitration Rules and Administering Institution (Data not available), 2020 (“Wang Jing et al v. Ukraine”); Beijing Everyway Traffic and Lighting Tech Co Ltd v. Ghana, UNCITRAL(administered by LCIA), 10 February 2021 (Notice of Arbitration) (“Beijing Everyday v. Ghana”); Alpene Ltd v. Republic of Malta, ICSID Case No. ARB/21/36, 2 July 2021 (Date Registered) (“Alpene v. Malta”). It is also noted that a Hong Kong company initiated the contract-based ICSID arbitration against a sovereign state in 2015: Standard Chartered Bank (Hong Kong) Limited v. United Republic of Tanzania, ICSID Case No. ARB/15/41, 30 September 2015 (Date Registered). 10 See Ekran Berhad v. People's Republic of China, ICSID Case No. ARB/11/15, 24 May 2011 (Date Registered); Ansung Housing Co., Ltd. v. People's Republic of China, ICSID Case No. ARB/14/25, 4 November 2014 (Date Registered); Hela Schwarz GmbH v. People's Republic of China, ICSID Case No. ARB/17/19, 21 June 2017 (Date Registered); Jason Yu Song v. People’s Republic of China, PCA Case No. 2019-39; Macro Trading Co., Ltd. v. People's Republic of China, ICSID Case No. ARB/20/22, 29 June 2020; Goh Chin Soon v. People's Republic of China, ICSID Case No. ARB/20/34, 16 September 2020; AsiaPhos Limited v. People’s Republic of China, UNCITRAL, Administering Institution (Data not available), 2020. So far, there are no treaty claims brought against the Hong Kong and Macao SARs. 11 The “GBA” is a term coined by the Chinese central government, referring to nine Pearl Reiver Delta cities, which are all mega cities located in the Guangdong province, including Guangzhou, Shenzhen, Zhuhai, Foshan, Dongguan, Zhongshan, Jiangmen, Huizhou, and Zhaoqing, and the two SARs namely Hong Kong and Macao. It is a world-class bay area comparable with the bay areas of London, New York, San Francisco, and Tokyo.

7 7

3

02

0

Chinese Investors Foreign Investors

Treaty-based Investment Arbitrations Initiated by Chinese Investors Against Foreign Host State and Forein Investors

Against the PRC, Hong Kong and Macao (as of 2 July 2021)

Mainland/PRC Hong Kong Macao

4

Against such backdrop, this article is aimed at exploring two salient

jurisdictional issues arising from the China-related investment arbitrations initiated by Chinese investors as the claimants, especially for those domiciled or having residency in the GBA: (1) what kind of natural person or entity domiciled or having residency within the GBA is a qualified investor entitled to initiate a treaty-based investment arbitration? (2) what kind of commercial transaction carried out by these qualified Chinese investors qualifies as an investment?

II. Who Can Initiate a Treaty-based Investment Arbitration?

As a starting point, an investor claimant has the burden of proving a factual presumption of holding a valid nationality of a contacting party, other than the host state, to the applicable treaty. After the claimant discharging the burden, the burden of proof will shift onto the respondent party challenging the presumption of a valid nationality, which normally has a high threshold to overcome.12 The jurisdictional ratione personae issue of whether the investors, either a natural person or an entity in respect of the Hong Kong and Macao SARs, are covered by the definitions of “investor” in Chinese BITs, was heavily debated and assessed before the tribunals in the Tza Yap Shum and Sanum-I cases.

1. Tza Yap Shum case

12 See Ioan Micula, Viorel Micula, S.C. European Food S.A, S.C. Starmill S.R.L. and S.C. Multipack S.R.L. v. Romania, ICSID Case No. ARB/05/20, Decision on Jurisdiction and Admissibility of 24 September 2008, para.87 (“In that respect, there exists a presumption in favour of the validity of a State’s conferment of nationality. The threshold to overcome such presumption is high.”).

Ping An v. Belgium• Ping An el al. - Shenzhen, Guangdong Province• China-Belgium BIT (1986); Belgium-China BIT (2009)

Alpene v. Malta• Alpene Ltd - Hong Kong• Malta-China BIT (2009)

Tza Yap Shum v. Peru• Tza Yap Shum - Hong Kong• Peru-China BIT (1994)

Philip Morris v. Australia• Philip Morris Asia Ltd - Hong Kong• Hong Kong-Australia BIT (1993)

Sanum v. Laos-I • Sanum - Macao• China-Laos BIT (1993)

Sanum v. Laos-II• Sanum - Macao• China-Laos BIT (1993)

5

In Tza Yap Shum v. Peru, the investor Mr. Tza was a Chinese national with the

Hong Kong residency. Mr. Tza had made an investment of USD 400, 000 as a 90% indirect shareholder of TSG, a local fishmeal industrial company incorporated in Peru, through Linkvest which is a British Virgin Island (BVI) company.13 To prove Chinese nationality, Mr. Tza produced his Hong Kong identity card and passport albeit without producing the birth certificate as required by the tribunal.14 Peru challenged the standing of Mr. Tza to bring treaty claims under the Peru-China BIT (1994) by arguing that the passport and identity card issued by the Hong Kong SAR government were not sufficient to prove the individual investor’s Chinese nationality.15 The Tza Yam Shum tribunal held that the Hong Kong passport and identity card, which indicated that Mr. Tza’s place of birth was Fujian Province, sufficed to prove his Chinese nationality.16 The approach stems from the general rule and relevant case law that residence or any other geographic affiliation has little relevance in determining the individual’s nationality.17 Although it is recognized that “national certificates of nationality or passports or other documentation” have no binding force upon the tribunals, 18 passports, identity cards or any other certificate of nationality are accepted as prima facie and rebuttable evidence of nationality that should be given appropriate weight.19

However, the tribunal did not address the question whether Peru-China BIT (1994) technically did not apply to the Hong Kong SAR and its residents due to the “One Country, Two Systems” policy. Instead, it held that it was beyond the scope of the present dispute and thus unnecessary to determine whether the BIT applied to Hong Kong.20

2. Sanum-I case

13 See Tza Yap Shum v. Peru, ICSID Case No. ARB/07/6, Award of 7 July 2011, paras.59-60, 74, 98. For a summary in English of the Award, see Kenneth Juan Figueroa, ‘TZA YAP SHUM V. REPUBLIC OF PERU (ICSID CASE NO. ARB/07/6) AWARD’ (“Summary of the Award in Tza”), reported in International Arbitration Case Law, available at https://www.italaw.com/sites/default/files/case-documents/ita0882.pdf. 14 See Tza Yap Shum v. Peru, ICSID Case No. ARB/07/6, Decision on Jurisdiction and Competence of 19 June 2009, para.49. 15 See ibid, para.44. 16 See ibid, paras.58-61. 17 See Marvin Roy Feldman Karpa v. United Mexican States, ICSID Case No. ARB(AF)/99/1, Interim Decision on Preliminary Jurisdictional Issues of 6 December 2000, para.30 (“In particular, in matters of standing in international adjudication or arbitration or other form of diplomatic protection, citizenship rather than residence is considered to deliver, subject to specific rules, the relevant connection”). 18 See Hussein Nuaman Soufraki v. The United Arab Emirates, ICSID Case No. ARB/02/7, Decision of the Ad Hoc Committee on the Application for Annulment of Mr. Soufraki of 5 June 2007, para.64. 19 See Christoph H. Schreuer, The ICSID Convention: A Commentary (2nd edn, OUP 2009), at 268. See also Waguih Elie George Siag and Clorinda Vecchi v. The Arab Republic of Egypt, ICSID Case No. ARB/05/15, Decision on Jurisdiction of 11 April 2007, para.150-153. 20 See ibid, para.68.

6

The unsolved question in Tza Yan Shum was again hotly debated in Sanum v.

Laos-I. Sanum, an entity incorporated under the laws of the Macao SAR in the resort and gaming business, commenced an UNCITRAL ad hoc arbitration against the Lao People’s Democratic Republic (“Laos”) pursuant to the China-Laos BIT (1993).21 The tribunal convened by the parties to the dispute designated Singapore as the place of arbitration administered by the PCA as a Registry, and the UNCITRAL Arbitration Rules (2010) applied as the applicable procedural rules. 22 The substantial investments made by Sanum were crystalized into a majority shareholder’s rights and interest in three joint ventures and projects that were co-developed with the ST Group, a local company, under the Master Agreement dated 30 May 2007.23

At the jurisdictional stage, the main issue addressed by the tribunal was whether the claimant Sanum was covered by the China-Laos BIT (1993). Different from the omission of the Tza Yap Shum tribunal in discussing whether the applicable Chinese BIT applied to the Hong Kong SAR, the tribunal in the Sanum-I case observed that “[t]he question of the application or non-application of the [China-Laos BIT (1993)] to the Macao SAR is central to the question of jurisdiction”.24 Prior to concluding that the China-Laos BIT (1993) applied to the Macao SAR,25 the tribunal has used lots of ink in public international law analysis. To be specific, the tribunal had taken into careful consideration the 1999 Notification made by the PRC to the UN Secretary-General regarding the status of Macao in relation to deposited treaties,26 the 1969 Vienna Convention on the Law of Treaties (VCLT) 27 and customary international law codified in the 1978 Convention on the Succession of States in Respect of Treaties (VCST)28. The tribunal’s decision on this issue was explicitly contrary to the PRC Government’s public standing 29 and was rejected by the Singapore High Court.30 It was, however, finally confirmed by the Singapore Court

21 See Sanum Investments Ltd. v. Lao People’s Democratic Republic, PCA Case No. 2013-13, Decision on Jurisdiction of 13 December 2013, paras.1-3. 22 See ibid, para.5. 23 See ibid, paras.18-42. 24 See ibid, para.205. 25 See Sanum Investments Ltd. v. Lao People’s Democratic Republic, PCA Case No. 2013-13, Decision on Jurisdiction of 13 December 2013, para.300. 26 See United Nations, ‘Multilateral Treaties Deposited with the Secretary-General: Status as at 1 April 2009’, Volume I, Part I, Chapters I-VII, New York 2009, Note 3, at VIII-X. It is noted that Note 2 at VI-VIII of the same instrument was the counterpart notification made by the PRC regarding the status of the Hong Kong SAR in relation to deposited treaties. 27 See inter alia Article 29 of the VCLT. 28 See inter alia Article 15 of the VCST. 29 See the PRC Ministry of Foreign Affairs, ‘Foreign Ministry Spokesperson Hua Chunying's Regular Press Conference on October 21, 2016’, available at https://www.fmprc.gov.cn/mfa_eng/xwfw_665399/s2510_665401/t1407743.shtml. 30 See [2015] SGHC 15, paras.110-111.

7

of Appeal.31

3. A Look into the BITs and Other IIAs Signed by the Hong Kong and Macao SARs Borrowing from the argument made by the claimant in the Sanum-I case, the

fact that the Hong Kong and Macao SARs enjoyed the freedom of joining international treaties does not mean Chinese BITs and other IIAs should not apply to the territory of the two SARs.32 Instead, the BITs and other IIAs entered into by Hong Kong and Macao are perfectly considered as “a supplemental regime of protection for Macanese [and Hong Kong] investors, above and beyond that provided by the PRC treaties”.33

In the present authors’ view, this argument gives a sound summary of the relationship between Chinese BITs/other IIAs and the Hong Kong and Macao’s BITs/other IIAs. Theoretically speaking, the investors falling under the definitions of investors in both regimes of investment treaties can choose of their own will to rely on which treaty to initiate investment arbitration. For instance, Article 8 (2) of the Macao-Portugal BIT (2000) allows Macanese investors to have only recourse to a competent court of host state and the UNCITRAL ad hoc arbitration.34 However, the Chinese BIT concluded with Portugal in 2005 enables Macanese investors to have a third option – ICSID Arbitration – in addition to the two previous options.35 Therefore, if the China-Portugal BIT (2005) applies to the Macao SAR, a qualified Macanese investor under the two BITs can initiate an ICSID Arbitration; if not, he can only choose domestic litigation or an UNCITRAL ad hoc arbitration.

Some concerns have been raised against the concomitant application of Chinese BITs/other IIAs and the Hong Kong and Macao’s BITs/other IIAs. The respondent in the Sanum-I case argued that “the overlapping of the PRC and Macao BITs with the same third State would bring about ‘legal chaos for foreign investors’”. 36 However, both tribunals in the Tza Yap Shum and Sanum-I cases disregarded such concern as unnecessary and redundant. The Tza Yap Shum tribunal notes that it is not “necessarily redundant” for Hong Kong which enjoys the power to conclude

31 See [2016] SGCA 57, para.152. For a critical commentary on the judgment, see Mahdev Mohan & Siraj Shaik Aziz, ‘Construing A Treaty against State Parties’ Expressed Intentions: Sanum Investments Ltd v Government of the Lao People’s Democratic Republic’ (2018) 30 Singapore Academy of Law Journal 384. 32 See Claimant’s Response, para.48, cited in Sanum Investments Ltd. v. Lao People’s Democratic Republic, PCA Case No. 2013-13, Decision on Jurisdiction of 13 December 2013, para.292. 33 See ibid. 34 See Article 8(2) of the Macao-Portugal BIT (2000). 35 See Article 9(2) of the China-Portugal BIT (2005). 36 See Respondent’s Post-Hearing Submission, para.27, cited in Sanum Investments Ltd. v. Lao People’s Democratic Republic, PCA Case No. 2013-13, Decision on Jurisdiction of 13 December 2013, para.292.

8

international investment agreement to conclude BITs or other IIAs with the state which has also concluded an investment treaty with China.37 Instead, as observed by the Sanum-I tribunal, “the existence of two [invokable] treaties facilitates rather than hinders the fulfilment of the goals of the BITs, which are the protection of the foreign investors and the economic development of the host State”.38

III. What Commercial Transaction Qualifies an Investment?

The notion of “investment” in many Chinese BITs or other IIAs is defined very broadly. These broad asset-based definitions of “investment” have caused confusions and uncertainties in the tribunal’s assessing whether a protected investment exists. For instance, the Peru-China BIT (1994) provides for an encompassing definition of “investment”, comprising “every kind of asset” invested by investors of one contracting party in the territory of host state. 39 The other Chinese BITs that have been relied upon by Chinese investors to commence investor-State arbitrations also contain such an encompassing definition. 40 Therefore, a variety of cross-border commercial transactions might be covered by the term of “investment”.

On the one hand, such a broad definition of investment would encourage Chinese investors to seek treaty protection of their overseas commercial transactions having financial value. On the other hand, the definitions and terms are so broad that the tribunals usually need exercise a high degree of caution and prudence, for example, by adopting an objective test in deciding whether a specific business transaction falls under the protected investment.

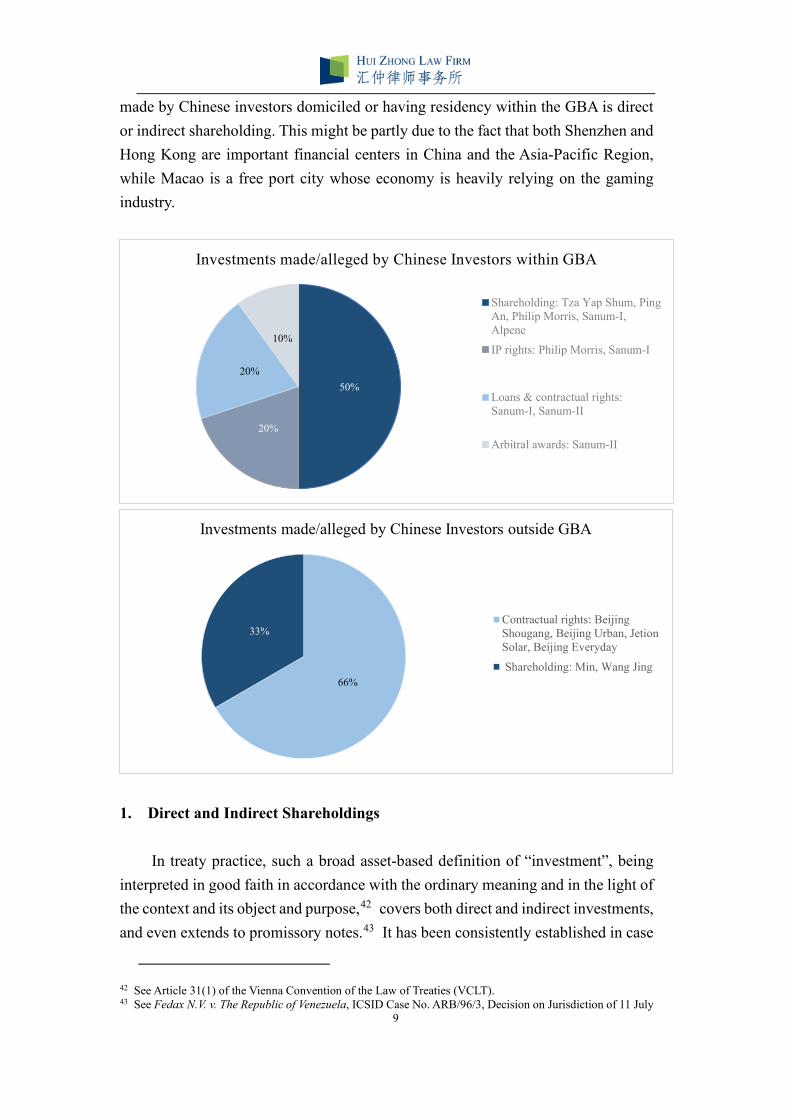

These rather broad definitions are detailed and clarified by incorporating a non-exhaustive list of assets or properties, which covers generic terms such as “movable and immovable property”, “shares, stock”, “any other kind of shareholdings”, “claims to money”, “intellectual property rights”, “know-how”, and “concessions”, etc. 41 Below are two charts illustrating the categories of investments made by Chinese investors from the GBA to foreign host states as well as those made by Chinese investors domiciled or having residency in the territory of the PRC outside the GBA. A glimpse of the charts indicates that the main category of investments

37 See Tza Yap Shum v. Peru, ICSID Case No. ARB/07/6, Decision on Jurisdiction and Competence of 19 June 2009, para.76. 38 See Sanum Investments Ltd. v. Lao People’s Democratic Republic, PCA Case No. 2013-13, Decision on Jurisdiction of 13 December 2013, para.295. 39 See Article 1(1) of the Peru-China BIT (1994). Cf. Article 126 of the Peru-China FTA (2009). 40 See Article 1(1) of the China-Laos BIT (1993) (“every kind of asset”); Article 1(1) of the China-Belgium BIT (1986) (“every kind of asset or property”); Article 1(1) of the Belgium-China BIT (2009) (“every kind of asset”); Article 1(e) of the Hong Kong-Australia BIT (1993) (“every kind of asset”). 41 See ibid.

9

made by Chinese investors domiciled or having residency within the GBA is direct or indirect shareholding. This might be partly due to the fact that both Shenzhen and Hong Kong are important financial centers in China and the Asia-Pacific Region, while Macao is a free port city whose economy is heavily relying on the gaming industry.

1. Direct and Indirect Shareholdings

In treaty practice, such a broad asset-based definition of “investment”, being

interpreted in good faith in accordance with the ordinary meaning and in the light of the context and its object and purpose,42 covers both direct and indirect investments, and even extends to promissory notes.43 It has been consistently established in case

42 See Article 31(1) of the Vienna Convention of the Law of Treaties (VCLT). 43 See Fedax N.V. v. The Republic of Venezuela, ICSID Case No. ARB/96/3, Decision on Jurisdiction of 11 July

50%

20%

20%

10%

Investments made/alleged by Chinese Investors within GBA

Shareholding: Tza Yap Shum, PingAn, Philip Morris, Sanum-I,Alpene

IP rights: Philip Morris, Sanum-I

Loans & contractual rights:Sanum-I, Sanum-II

Arbitral awards: Sanum-II

66%

33%

Investments made/alleged by Chinese Investors outside GBA

Contractual rights: BeijingShougang, Beijing Urban, JetionSolar, Beijing Everyday

Shareholding: Min, Wang Jing

10

law that direct and indirect shareholdings can meet the Salini test44 and the double-barreled test.45

In the Tza Yap Shum case, Peru had tried to defeat the tribunal’s jurisdiction by arguing that the Peru-China BIT (1994) did not intend to protect indirect investments, namely Tza’s indirect ownership of TSG through a BVI company, especially given that some other Chinese BITs explicitly excluded indirect investments. 46 Nevertheless, the tribunal dismissed the argument by opining that indirect investment was not excluded from the scope of protection under the BIT.47 In the tribunal’s view, the contracting parties to the BIT would have made clear the exclusion of indirect investments from the scope of covered investment if they intended to do so.48

The extension of treaty protection to indirect shareholdings controlled by qualifying investors was also sustained in other Chinese investor-State arbitrations. In the Sanum-I case, one of the objections ratione materiae brought before the tribunal were whether indirect investments qualified as an investment under the China-Laos BIT (1993).49 Laos contended that Sanum had not made an investment in Laos because it did not make any direct investment, and the contributions made to acquire the indirect shareholdings in local joint ventures were made in the form of loans.50 After examining the provisions in Article 1(1) of the applicable BIT, the tribunal concluded that indirect investments were not excluded and the indirect shareholdings obtained as a result of the “common business practice of foreign investors using local companies as vehicles to channel the investment” quailed as an investment protected by the BIT.51

2. Claims to Money, Loans, and Intellectual Property Rights (e.g., Business

Know-How, Trademarks, Brands) The other objection ratione materiae contended by Laos was concerned with

1997, paras.31-37. 44 See Salini Costruttori S.p.A. and Italstrade S.p.A. v. Kingdom of Morocco, ICSID Case No. ARB/00/4, Decision on Jurisdiction of 23 July 2001, para.52. 45 See Malaysian Historical Salvors, SDN, BHD v. The Government of Malaysia, ICSID Case No. ARB/05/10, Decision on Jurisdiction of 17 May 2007, para.55. See also Malicorp Limited v. The Arabian Republic of Egypt, ICSID Case No. ARB/08/18, Award of 7 February 2011, para.110. 46 See Tza Yap Shum v. Peru, ICSID Case No. ARB/07/6, Decision on Jurisdiction and Competence of 19 June 2009, paras.109, 110. 47 See ibid, para.106. 48 See ibid, para.107. 49 See Sanum Investments Ltd. v. Lao People’s Democratic Republic, PCA Case No. 2013-13, Decision on Jurisdiction of 13 December 2013, para.316. 50 See ibid. 51 See ibid, paras.317-318, 321.

11

“whether contributions made in the forms of loans to the local companies qualify as investments”.52 Pursuant to Article 1(1) of the China-Laos BIT (1993), the broad asset-based definition of investment not only covers “a claim to money or to any performance having an economic value”53, but also “know-how”54. In the tribunals’ view, such a definition is “wide-ranging and open”, being accompanied with a non-exclusive list of covered investments. Based on a subjective interpretation of Article 1(1) of the BIT, the tribunal held that Sanum’s loan to local companies and its alleged know-how in the hotel and gaming facilities industry qualified as investments in Laos.55

In Philip Morris v. Australia, as alleged by the claimant, the intellectual property rights enjoyed by its Australian subsidiary, namely Philip Morris Limited, constituted the core part of its entire business in Australia. 56 These intellectual property rights included “registered and unregistered trademarks, copyright works, registered and unregistered designs, and overall get up of the product packaging”, in particularly the recognition of its brands. 57 The claimant asserted that these intellectual property rights, its direct shareholding in Philip Morris Australia and indirect shareholding in Philip Morris Limited constituted qualified investment under Article 1(e) of the Hong Kong-Australia BIT (1993). 58 One of three preliminary objections advanced by Australia was that “neither the shares in PML nor PML’s assets [including the intellectual property rights] constitute investments for the purposes of the Treaty”. 59 However, the tribunal had not deemed this objection “suitable for consideration” and had only addressed the other jurisdictional objections (e.g. objection ratione temporis, and inadmissibility due to abuse of right, etc.).60 It implied that the intellectual property rights concerned and shareholdings were covered by the definition of “investment” under Article 1(e) of the Hong Kong-Australia BIT (1993).

3. Whether Arbitral Awards or Judicial Decisions Qualify as Protected

Investments?

52 See ibid, para.316. 53 See Article 1(1)(c) of the China-Laos BIT (1993). 54 See Article 1(1)(d) of the China-Laos BIT (1993). 55 See Sanum Investments Ltd. v. Lao People’s Democratic Republic, PCA Case No. 2013-13, Decision on Jurisdiction of 13 December 2013, paras.320-321. 56 See Philip Morris Asia Limited v. The Commonwealth of Australia, UNCITRAL, PCA Case No. 2012-12, Award on Jurisdiction and Admissibility of 7 December 2015, para.6. 57 See ibid. 58 See ibid, para.183. 59 See ibid, para.184. 60 See ibid, paras.185, 186.

12

Whether an arbitral award or a judicial decision arising from the investment is also a qualified investment covered by the term “claims to money” is also an interesting but controversial issue in investor-State arbitration case law.

In the Sanum v. Laos-II case which is conducted in accordance with the ICSID Additional Facility Rules, Sanum brought a new ancillary claim which was not included in its Notice of Arbitration. Sanum’s such a new ancillary claim related to the decision by the Lao courts not to enforce the 2016 SIAC Award which was in Sanum’s favor against a private party, the ST Group.61 Sanum contended that the new ancillary claim would qualify even under an ICSID Convention analysis, including the Salini Test or the double-barreled test, because the 2016 SIAC Award and other related claims arose out of the “very same investments”, i.e., “all of Claimant’s gaming investments in Laos” conducted under the Master Agreement in 2007.62

Laos rebutted the Sanum’s new claim that the 2016 SIAC Award did not fall within the definition of “investment” under the applicable BIT because it was “not an asset that was contributed to or invested in Laos” and “the award and the underlying investment ‘remain analytically distinct’”.63 Moreover, the SIAC Award “involves no contribution to, or relevant economic activity within, Laos”.64 While the tribunal rejected Sanum’s ancillary claim by holding that the agreement to the ICSID Additional Facility Rules was limited to the matters contained in Sanum’s Notice of Arbitration, the decision left Sanum free to pursue the claim separately through a new proceeding under the China-Laos BIT (1993).65

Even though tribunals might be divided in this regard, the majority of the tribunals agree on the principle that an arbitral award or a judicial decision can constitute an investment if, and only if, the commercial transaction underlying the investment is also a qualified investment made in host state.66 As regards the nature of arbitral award or judgment, as noted in the Petrobart case, any “Contract and the judgment are not in themselves assets but merely legal documents or instruments which are bearers of legal rights, and these legal rights, depending on their character, may or may not be considered assets.”67 Thus, whether the legal rights crystalized

61 See Sanum Investments Ltd. v. Lao People’s Democratic Republic, ICSID Case No. ADHOC/17/1, Procedural Order No.2 of 23 October 2017, paras.6, 12. 62 See ibid, para.13. 63 See Sanum Investments Ltd. v. Lao People’s Democratic Republic, ICSID Case No. ADHOC/17/1, Procedural Order No.2 of 23 October 2017, para.14. 64 See ibid. 65 See ibid, paras.32, 33. 66 See Jean-Pierre Harb, ‘Definition of Investments Protected by International Treaties: An On-Going Hot Debate’ (2011) 26 MEALEY’s International Arbitration Report 1, at 7. 67 See Petrobart Limited v. The Kyrgyz Republic, SCC Arbitration No. 126/2003, Award of 29 March 2005, at 71.

13

into an arbitral award or a judicial decision are derived from the underlying investment is a key prerequisite issue for deciding whether the award or judgement itself falls under a broad asset-based definition of investment. Following this principle, the arbitral award or judicial decision which is inextricably intertwined with “a simple one-off sales transaction”, such as a sales contract, does not constitute an investment either under the BIT or the ICSID Convention.68

IV. Concluding Remarks

Chinese investor-State arbitrations commenced by the investors within the GBA, such as Tza Yap Shum, Philip Morris, Sanum, Ping An et al, have made abundant contributions to the development of China-related investment arbitration jurisprudence. These cases, including the very recent case of Alpene v. Malta, would be undoubtedly conducive to wiping out the fogginess of peculiar notions of “investor” and “investment” in the context of the GBA. The investors within the GBA who are surely aware of their satisfaction of the notions of “investor” and “investment” are more likely to commence a treaty-based investment arbitration to protect qualified investments abroad. Moreover, with a proper understanding of the relationship between the Chinese BITs/other IIAs and those concluded by the Hong Kong and Macao SARs, the investors within the GBA, especially those domiciled or having residency in Hong Kong and Macao, may have more options to pursue potential investor-State arbitration to guard their rights and interest in investments made overseas.

68 See Romak S.A. v. The Republic of Uzbekistan, UNCITRAL, Award of 26 November 2009, paras.187, 211.