Embed Size (px)

Citation preview

Tax Reforms, Debt Shiftingand Corporate Tax Revenues:

Multinational Corporations in Canada

Vijay JogProfessor of Finance

School of Business, Carleton UniversityJianmin Tang

EconomistMicro-Economic Policy Analysis, Industry Canada

February 1998

WORKING PAPER 97-14Prepared for the

Technical Committee on Business Taxation

Working papers are circulated to make analytic work prepared for theTechnical Committee on Business Taxation available.

They have received only limited evaluation; views expressed are those of the authors and do not necessarily reflect the views of the Technical Committee,

or the Department of Finance.

Tax Reforms, Debt Shiftingand Corporate Tax Revenues:

Multinational Corporations in Canada

Vijay JogProfessor of Finance

School of Business, Carleton UniversityJianmin Tang

EconomistMicro-Economic Policy Analysis, Industry Canada

February 1998

WORKING PAPER 97-14Prepared for the

Technical Committee on Business Taxation

Comments on the working papers are invited and may be sent to:Paul Berg-Dick, Director

Business Income Tax DivisionDepartment of FinanceOttawa, Ont. K1A 0G5Fax: (613) 943-2486

e-mail: [email protected]

Vijay JogSchool of BusinessCarleton University

1125 Colonel By DriveOttawa, Ontario

K1S 5B6Fax: (613) 520-4427

Jianmin TangMicro-Economic Policy Analysis

Industry Canada235 Queen StreetOttawa, Ontario

K1A 0H5Fax: (613) 941-3859

For additional copies ofthis document please contact:

Distribution CentreDepartment of Finance

300 Laurier Avenue WestOttawa K1A 0G5

Telephone: (613) 995-2855Facsimile: (613) 996-0518

Also available through the Internet athttp://www.fin.gc.ca/

Cette publication est également disponible en français.

Abstract

An analysis of Canadian corporate income tax revenues during the 1984-94 period shows arelative shifting of tax revenue shares between Canadian and foreign-controlled corporations, anda substantial change in the debt levels of foreign-controlled corporations, as well asCanadian-based multinationals. In this paper, we explore the hypothesis that these changes indebt levels may have been associated with the tax reforms undertaken by the United States andCanada in the mid-1980s.

Our empirical analysis places special emphasis on the differences between Canadian-controlledcorporations and foreign-controlled corporations. We further separate these two groups into thosewith foreign affiliates and those without. We present evidence based on the universe of Canadiancorporations, as well as that from a longitudinal data set created especially for this paper. Wedevelop a theoretical two-country integrated model to show the directional impact of the taxreforms on the capital structure of corporations and the corresponding impact on Canadian taxrevenues. Our results are consistent with the predictions of our theoretical model.

Our data reveal that a significant shifting of debt by foreign-controlled firms in Canada, as wellas Canadian firms with foreign affiliates has occurred during the 1984-94 period. Also evident isa contemporaneous decline in Canadian corporate income tax revenues from multinationals asrevealed by taxes paid relative to operating income before interest and taxes. Analysis of ourlongitudinal sample and econometric analysis supports these conclusions. Except forCanadian-controlled corporations with no foreign affiliates, we observe a substantive increase inthe reliance on debt suggesting a corresponding decline in Canadian tax revenues. Since a largeproportion of the foreign controlled corporations is U.S.-controlled, tax reforms undertaken bythe United States in the 1980s could be a potential causal factor for this debt shifting. Our resultsimply that the relative change in the tax rates between Canada and the United States has had anegative impact on the Canadian corporate income tax base. Noting the fact that the debt levelsof the Canadian subsidiaries of multinationals are, on average, still much lower than theirCanadian counterparts, it is possible that the Canadian corporate income tax base may continueto remain under pressure due to further adjustments to the debt levels.

Table of Contents

1. Introduction ............................................................................................................................... 1

2. The U.S. and Canadian Tax Reforms ..................................................................................... 4

3. Theoretical Considerations....................................................................................................... 7

4. Empirical Analysis .................................................................................................................... 9

4.1 Data Source ......................................................................................................................... 10

4.2 Aggregate Evidence............................................................................................................. 10

4.3 Econometric Analysis.......................................................................................................... 13

5. Conclusions .............................................................................................................................. 17

Appendix: One-parent, One-foreign-subsidiary, Two-period Model .................................... 21

References .................................................................................................................................... 36

Tax Reforms, Debt Shifting and Corporate Tax Revenues 1

1. IntroductionThe 1980s saw significant tax reforms undertaken by Canada and the United States as well as

other Organization for Economic Co-operation and Development (OECD) countries. These tax

reforms have resulted in Canada becoming a relatively high-tax jurisdiction as compared with its

trading partners, particularly the United States. Although both Canada and the United States saw

an overall reduction in corporate tax rates, the degree of reduction reversed Canada’s position

from a relatively low-tax to a relatively high-tax jurisdiction as illustrated by Figure 1. For

example, the U.S. tax reform reduced the combined federal-state statutory U.S. corporate tax rate

from 50 to 39 percent. In contrast, Canadian tax reform reduced the comparable Canadian rate

from approximately 51 to 42 percent for non-manufacturing and 44 to 35 percent for

manufacturing. 1, 2

Furthermore, the tax reform in the United States has resulted in changes not only to the statutory

corporate tax rates but also to the tax rules for U.S. multinational corporations (MNCs) with

respect to the tax treatment associated with the income of their foreign subsidiaries. These

changes have been of particular importance to Canada, which has a significant number of

U.S.-controlled corporations (USCCs). For example, as of 1994, foreign-controlled corporations

(FCCs) represented 22 percent of total taxable income in Canada, 23 percent of total corporate

1 These statutory tax rates take into account the federal, as well as state and provincial tax rates. These rates are notfully representative of the situations faced by individual firms, as these would vary from state (province) to state(province) and, in certain instances, industrial sector (e.g. due to industry-specific tax provisions). The numbersshown in Figure 1 for Canada are based on statutory corporate tax rates faced by a sample of 457 large corporationsin Canada (the sample will be described in detail later on). These corporations represent both the manufacturing andthe non-manufacturing sectors but exclude the financial industry; therefore, the average rate represents a blend ofmanufacturing and non-manufacturing rates. The statutory corporate tax rate of each corporation is calculated as thesum of federal and provincial tax rates. The provincial tax rate is calculated as the average of the relevant provincialstatutory corporate tax rates, weighted by its taxable income in each province. Because of a lack of data, calculationsfor the U.S. tax rates are simply based on the formula: tax rate = federal rate + average state rate x (1-federal rate).We assume a reduction from 46 percent pre-reform to a 34 percent post-reform federal rate and a 7-percent averagestate tax.

2 It may be noted that, in addition to lowering statutory tax rates, tax reforms in both countries introduced severalbase-broadening measures. For example, the U.S. tax reform eliminated investment tax credits and imposedrestrictions on capital cost allowances through modifications to the accelerated cost recovery system (ACRS). InCanada, investment tax credits were effectively eliminated (except for R&D), and capital cost allowances werereduced and streamlined.

2 WORKING PAPER 97-14

tax revenues and 14 percent of total corporate assets.3 Although corresponding figures for

USCCs are not available, approximately 90 percent of foreign-controlled corporations are

U.S.-controlled.

The changes in corporate tax revenues attributed to FCCs along with their share of taxable

income and assets are shown in Table 1 and Figure 2. In Table 1, we list total taxable income,

total corporate income tax and total assets of all Canadian corporations, by control for 1984

through 1994. In 1984, FCCs represented 13 percent of total corporate assets in Canada rising

marginally to 14 percent in 1994. The corresponding figures for taxable income were 28 percent

in 1984 and 21 percent in 1994; whereas, for taxes paid, these figures were 33 percent in 1984

and 23 percent in 1994. Although the asset share of FCCs increased marginally, the taxable

income share of FCCs declined by 7 percentage points, and the tax share declined by

10 percentage points. Thus, over the sample period, FCC tax payments have been dramatically

reduced relative to those of their Canadian-controlled counterparts.

Figure 2 shows the corporate tax-to-assets ratio for the two groups over this 11-year period. For

Canadian-controlled corporations (CCCs) the value of the ratio fell from 0.46 percent to

0.39 percent, only a 15-percent reduction. For FCCs, this ratio fell dramatically from 1.55 percent

to 0.71 percent, a 54-percent reduction.4 If FCCs had maintained in 1994 the same corporate

tax-to-asset ratio as in 1984, Canadian tax revenues from FCCs would have been $6.4 billion

instead of the actual amount of $2.9 billion, a difference of $3.5 billion.

The main thrust of this paper is to investigate whether the changes in the relative tax rates

between the United States and Canada had an impact on debt levels of Canadian subsidiaries of

foreign multinationals as well as Canadian multinationals. If this is found to be the case, then this

debt shifting can also provide an explanation of significant changes in Canadian corporate

3 In the past, these numbers were available in the Statistics Canada publication #61-210. The publication waschanged significantly in the early 1990s, and no longer publishes this type of information for years after 1988.

4 Figure 2 shows that foreign-controlled corporations always have a higher tax-to-assets ratio thanCanadian-controlled corporations. This occurs because that the Canadian-controlled group contains manyCanadian-controlled private corporations (CCPCs), which enjoy a lower tax rate due to lower statutory tax rates andadditional tax deductions (e.g. R&D credits).

Tax Reforms, Debt Shifting and Corporate Tax Revenues 3

income tax revenues. The investigation is conducted by comparing the capital structure of CCCs

without foreign affiliates with that of all other corporations – that is CCCs with foreign affiliates

and FCCs/USCCs. Our hypothesis is that the increase in debt by USCCs (and Canadian

multinationals) occurred as a direct result of changes in relative tax rates. This debt shifting

resulted in higher deductions of interest, thereby resulting in lower tax payments in Canada,

everything else being equal.5 Note that such debt-shifting may affect both the amount of tax

revenues and their volatility.

This paper examines the debt-shifting behaviour of FCCs and CCCs by using a longitudinal data

set that was made available to us by Finance Canada. (The data set will be described in detail

later on). Our results suggest that the changes in tax systems resulting from U.S. tax reform

indeed influenced the financial policy of multinationals in Canada. Canadian corporate tax rate

also played a significant role in determining a corporation’s debt-to-asset ratio; the higher the

corporate tax rate faced by these corporations, the higher the debt-to-asset ratio. We show that,

from both theoretical and empirical perspectives, the tax difference between Canada and the

United States does have a positive impact on a corporation’s debt-to-asset ratio, indicating

a substantial debt-shifting response and a corresponding impact on Canadian corporate

tax revenues.

This paper is organized as follows. In the next section, we provide a brief overview of the tax

reforms in Canada and the United States. In Section 3, we conduct a brief review of the existing

literature and provide a theoretical analysis of changes to financial behaviour of a multinational

enterprise that is facing changes in tax regimes. In Section 4, we describe the data set used, our

econometric analysis and our results. Our conclusions are summarized in Section 5.

5 Three well-known instruments can be used by multinationals to minimize their tax payments. First, multinationalscan shift profits from high-tax countries to low-tax countries by manipulating transfer prices on cross-borderinterplant transactions. For instance, charging a below-cost price on products and services provided by a plant in ahigh-tax jurisdiction to a plant in a low-tax jurisdiction reduces the profit of the former and increases the profit of thelatter (Grubert, 1997). Second, multinationals can defer their home-country tax liabilities on repatriated foreigndividend income by reinvesting the profits that would have been used to pay such dividends, in active assets, passiveassets or both in host countries (Weichenrieder, 1996). Finally, multinationals can reduce their overall taxes byreallocating their debt from a low-tax jurisdiction to a high-tax jurisdiction to take advantage of the high interestdeduction in the high-tax jurisdiction. This third possibility is the subject of this paper.

4 WORKING PAPER 97-14

2. The U.S. and Canadian Tax Reforms 6

The U.S. tax reform of 1986 changed not only the statutory corporate tax rates in the United

States but also the tax treatment of U.S.-controlled foreign subsidiaries. The Canadian tax reform

in 1987 made changes to the statutory corporate income tax rates while broadening the base

subject to tax, but did not change the Canadian tax treatment of repatriated income from a USCC

to its parent. The results of these tax reforms resulted in three major changes affecting the tax

planning of a USCC from the viewpoint of its parent, and consequently Canadian corporate

tax revenues.

First, the post-reform period resulted in the reduction of the average combined federal-state U.S.

tax rate from 51 percent to 39 percent, a reduction of 12 percentage points. The Canadian tax

reforms resulted in a reduction of 7 percentage points, on average, from an overall pre-reform

rate of 51 percent to a post-reform rate of 44 percent for the non-manufacturing sector and 44 to

35 percent for the manufacturing sector. Although the exact rates applicable to individual firms

may vary, the direction of the change was clear. In the pre-reform period, Canadian tax rates were

lower than the U.S. tax rates whereas the post-reform period changed it in favour of the U.S.

Second, the U.S. tax reform changed the U.S. foreign tax credit (FTC) system. As these changes

have direct implications for the analysis in this paper, these deserve further elaboration. Prior to

the U.S. reform, the U.S. parent could average foreign-taxed income across low- and high-

(relatively) tax countries in an overall FTC basket calculation.7 This averaging implied that

excess foreign tax credits could be used to offset U.S. tax liability on income received from a

low-tax country. The U.S. tax reform made fundamental changes to this procedure. While

continuing to allow pooling of income across countries, it introduced new separate baskets for

determining the total FTC limitations. These separate baskets introduced additional restrictions

on the ability of the U.S. parent to minimize its U.S. tax liability on a worldwide basis.

6 As noted in the Introduction, this section provides only a brief overview of these two tax reforms. Detaileddescriptions of these reforms are available in many papers, including Ault and Bradford (1990), Bruce (1989),Hogg and Mintz (1991), and Jog and Mintz (1989).

7 The foreign tax credit includes the amount by which the creditable foreign income tax and withholding taxexceeded the U.S. tax on that income.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 5

Moreover, Canada moved from a low-tax country to a high-tax country. This change reduced the

incentive of the foreign parent not to repatriate income from its Canadian subsidiary.8 Thus, if

Canada was considered to be a ’foreign deficit tax credit’ country prior to the tax reform, it did

not remain so after the tax reform.9

Third, there were changes to the rules governing allocation of interest between U.S. and

foreign-source income for the purpose of calculating the FTC limitation. This limit is calculated

as notional U.S. tax payable on net foreign-source income.10 Prior to the tax reform, a taxpayer

could apportion interest either on the basis of the value of assets generating U.S. and

foreign-source income or on the basis of the amount of gross income generated. Corporate

groups filing consolidated returns could allocate interest on a separate company basis. This

provided scope to increase the amount of foreign tax credits available for the consolidated group.

Post-reform, the allocation of interest was made on the basis of the value of assets (for tax

purposes) and on a consolidated basis. Therefore, interest expense incurred by any member of a

corporate group proportionally reduced the U.S. and foreign-source income for all members of

the group on the basis of the value of assets generating income. Interest allocated against

foreign-source income was therefore apportioned to each of the FTC baskets. This approach,

which is based on the premise that money is fungible, limited the extent to which corporate

groups could engage in tax planning to maximize the amount of available foreign tax credits.

From the viewpoint of U.S. taxation, this rule was neutral with respect to the financing decisions

of the corporate group. This implied that, given the absence of any tax in the source country,

U.S. subsidiaries should be expected to have a capital structure that was more consistent with the

underlying business risk rather than a tax-planning perspective. These changes implied that the

Canadian subsidiaries were now likely to be capitalized at a higher debt-to-equity ratio and there

8 There are also non-tax reasons why dividend payments can increase. See Hines and Hubbard (1990).

9 The pre-tax reform case for not repatriating dividends due to the benefit of the deferral prior to the tax reform iswell described in Hines and Hubbard (1990), and Leechor and Mintz (1993).

10 See Altshuler and Mintz (1995), Arnold et al (1996) and Edgar (1987).

6 WORKING PAPER 97-14

would be an increase in dividend repatriation. The former would lead to a reduction in Canadian

tax revenues, since the interest expenses of the subsidiary would increase as well.11

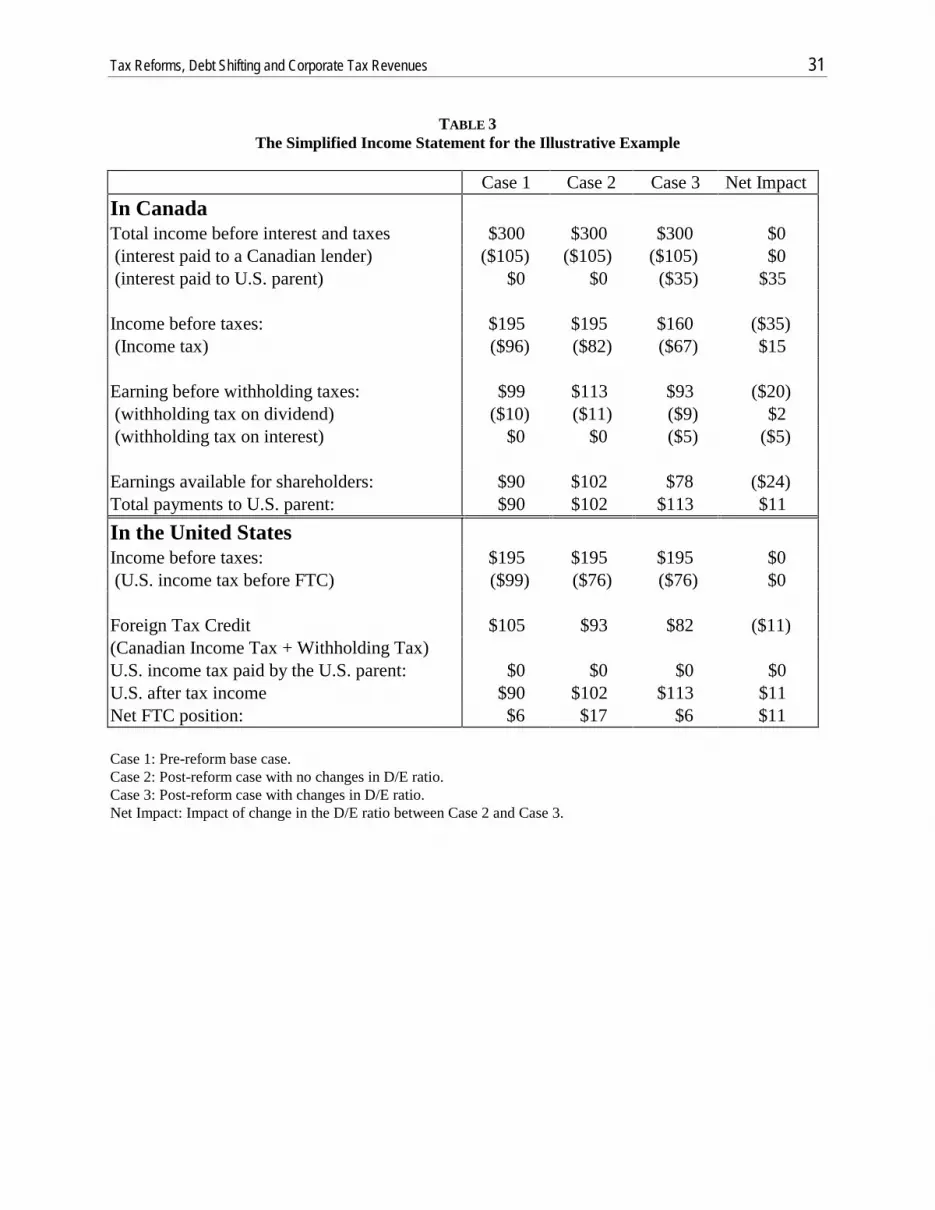

Tables 2 and 3 show an illustrative example of the impact of these changes on a USCC, assuming

some basic tax parameters, as viewed from its U.S. parent. Table 2 shows the values of the base

parameters used. Table 3 shows a simplified income statement for three cases: case 1 represents

pre-reform base case. Case 2 represents a post-reform situation with no changes in capital

structure. Case 3 represents a post-reform situation where the debt-to-equity ratio is changed so

as to revert back to the same FTC position as the pre-reform period. The example assumes that

the subsidiary has $3,000 in assets financed by 50-percent equity (parent contributions and

cumulative retained earnings) and 50-percent debt from Canadian sources (i.e. non-parent debt) –

Case 1. In all cases, all earnings are assumed to be paid out as dividends; this assumption has no

impact on the basic conclusions.

In Table 3, the first column (Case 1) in the simplified income statement provides the base case

(pre-reform) situation. In this case, the U.S. parent was, in effect, indifferent between the choice

of the capital structure for its Canadian subsidiary. One could even argue that, due to the small

positive difference between the U.S. and Canadian tax rates, the U.S. parent may have preferred

to: a) raise debt at the parent level; b) finance its Canadian subsidiary through equity investment;

and c) not withdraw dividends so as not to have an excess FTC position. Column 2 (case 2)

shows the simplified statement after the tax reform assuming no changes in the USCC

capitalization. As can be seen, the U.S. parent receives higher income (due to reductions in tax

rates in both countries), but increases its FTC from $6 to $17. However, it is possible for the

U.S. parent to further decrease the subsidiary's total tax payment by increasing the debt assumed

by the Canadian subsidiary. For example, if the U.S. parent was satisfied with the previous FTC

position, it can get to that position by increasing the subsidiary's debt to its U.S. parent. The

third column indicates that this would increase its interest deductions in Canada thereby further

reducing its Canadian taxes. Column 4 shows the net impact of this change in the capital

structure. Thus, if the U.S. parent chooses to maintain its pre-reform net tax position, this

11 The actual decision of the U.S.-based multinational would also depend on whether it faces an excess credit or anexcess limitation situation. For further details, see Hartman (1985) and Slemrod (1995).

Tax Reforms, Debt Shifting and Corporate Tax Revenues 7

would have an adverse impact on Canadian corporate tax revenues. For example, according to

the case in Table 3, the Canadian government would see a reduction of its total tax revenues (as a

result of debt shifting alone) to $67 from $82 – a reduction of approximately 18 percent.

Correspondingly, the U.S. parent’s after-tax income increases from $102 to $113, an increase

entirely at the expense of the Canadian government as a result of debt shifting. Clearly, the

negative impact described in this hypothetical example can be considered speculative at this

stage, although there is an incentive to move in the direction represented by the shift from Case 2

to Case 3.

It should also be noted here that the above discussion focusses mainly on the capital-structure

decisions of USCCs that may be affected by the tax reforms in both countries. There are, of

course, other important impacts of the tax reforms, including their impact on real (production and

investment) decisions by the U.S. parent in Canada, as well as their impact on transfer pricing

policies between the U.S. parent and its Canadian subsidiary.12 These changes in relative tax

rates also impact capital-structure decisions of Canadian multinationals with foreign affiliates. In

Section 4, we concentrate on the empirical evidence that allows investigation of the magnitude of

these impacts.

3. Theoretical ConsiderationsThe impact of changes to corporate taxation in home and host country on the behaviour of MNCs

has been a subject of great interest, especially in light of increasing globalization. The literature

has centred almost exclusively on the effect of a home-country tax system on a foreign

subsidiary’s investment decisions.13 In one of the earliest papers, Horst (1977) examined the

impact of changing U.S. tax policy (repealing deferral, increasing R&D charges to foreign

12 For the discussion of the impact on investment decisions, please see Hartman (1985); for transfer pricing issues,please see Grubert et al. (1991). Also see footnote 6.

13 There is a vast amount of literature on the impact of taxation on MNC decisions, including those related toinvestments, transfer pricing, tax competition, capital mobility, cost of capital and capital sourcing. There is also alarge body of literature on optimal capital structure from a purely domestic perspective. A complete review of thesestrands of literature is clearly beyond the scope of this paper. Some relevant papers are included in the list ofreferences at the end of the paper.

8 WORKING PAPER 97-14

subsidiaries and repealing the FTC) on U.S. MNCs. Sinn (1984) and Hartman (1985) studied the

effect of a home country tax system including deferral and an FTC on the mature subsidiary’s

investment decisions, and showed that the home-country tax system is irrelevant, once a

subsidiary has become mature. This area of study has since been extended in several directions.

Sinn (1993) has explored the investment decisions of an immature subsidiary, and concludes that

the overall taxes on cross-border profit repatriations tend to reduce the “birth weight” of a

subsidiary and increase the phase of its growth to maturity. Hines (1994) incorporates debt in

financing foreign subsidiaries and finds that the availability of debt finance makes it unlikely

that a home-country tax system reduces investments by subsidiaries, even in the early stages

of investments.14

With the exception of Horst (1977), there have been only a few studies that take into account the

interaction between a parent and its subsidiary. Unlike other studies that single out a subsidiary,

Horst considers both the parent and the subsidiary simultaneously and assumes that a

multinational enterprise strives to maximize its consolidated after-tax income. In his words,

“the consolidated after-tax income is the parent’s after-tax income (which includes dividend

income from its foreign subsidiary) plus the subsidiary’s retained earnings.” With the

consolidated after-tax income as the objective, his model captures some interaction between the

parent and its foreign subsidiary. The extent of its ability to do so, however, is limited by the

static nature of his model.

In this paper (and unlike Horst), we offer a two-period model of a multinational enterprise with a

parent and a foreign subsidiary, so that the dynamic relationship between the parent and its

subsidiary is captured. We also assume that the multinational enterprise strives to maximize its

consolidated after-tax income. This feature is important because intertemporal manipulation

(deferral, for example) is one of the main instruments used by the multinational to avoid tax

payments. Our simple model (see Appendix) allows us to evaluate the impact of tax-regime

changes in the home and host countries on the financing of multinational firms. The main

assumptions and conclusions from our theoretical model are as follows:

14 Note that most of these models assume that the repatriation tax on dividends is exogenous and constant over time.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 9

(i) The parent is financed in the first period as much as possible by the existing stock of equity

(or as little as possible by debt). The parent is assumed to be mature, and it is indifferent as

to whether debt or retained earnings finance its investment in the second period.

(ii) The foreign subsidiary is financed in the first period by as little equity or as much debt as

possible. When the tax is relatively high in the home country, the foreign subsidiary in the

second period is financed as much as possible by retained earnings. When the tax is

relatively low in the home country, it is financed in the second period as much as possible

by debt. All after-foreign-tax earnings are repatriated immediately as dividends.

(iii) Incentives exist for the multinational to finance the parent by borrowing through the

subsidiary, but not the opposite.

(iv) Withholding taxes are neutral and have no effect on the multinational’s investment

decisions.

Notwithstanding the fact that our simple model does not account for complex interactions among

the excess tax credit positions, a U.S. parent having subsidiaries in other countries in addition to

Canada, and the possibility of maximizing after-tax income on a global basis, a basic conclusion

seems inescapable. Given the general direction of the U.S. and Canadian tax reforms, there is a

greater incentive for a USCC to engage in debt shifting between its Canadian subsidiary and the

parent corporation.

4. Empirical AnalysisIn this section, we describe the results of our analysis of a longitudinal sample of Canadian-based

firms, which includes FCCs and CCCs, some with foreign affiliates and others without. The main

purpose of the analysis is to determine whether this sample confirms the theoretical conjectures

and the conclusions from the aggregate data.

10 WORKING PAPER 97-14

4.1 Data Source

To investigate debt shifting at the individual corporation level, a longitudinal data set was

constructed by Revenue Canada at the request of Finance Canada for the purpose of this study.15

It is composed of 525 Canadian-based large corporations that survived from 1984 to 1994. These

525 corporations are sampled from a universe that represents about 750,000 corporations.16 The

data set consists of both CCPCs and non-CCPCs. The latter are restricted to those with annual

sales greater than $20 million. Because the financial industry is predominantly Canadian-owned

and financial corporations’ financial behavior is more difficult to predict, we further exclude

financial corporations from the sample, which results in a sample of 457 Canadian non-financial

large corporations, of which 150, on average, are FCCs. For our econometric analysis, we also

exclude non-U.S. foreign corporations from the sample and retain those corporations that

survived from 1986 to 1994. Thus, the final sample for econometric analysis is composed of 388

Canadian non-financial large companies, of which 120, on average, are USCCs. Since USCCs

account for a large portion of FCCs, most of the conclusions regarding FCCs in the introductory

section reflect changes in the USCCs.

4.2 Aggregate Evidence

As indicated above, multinationals can reduce their tax payments by shifting debt from a low-tax

jurisdiction to a high-tax jurisdiction to take advantage of the high-interest deduction in the

high-tax jurisdiction. Tables 4a and 4b shows the values of main variables for the two samples:

CCCs and FCCs. The variables considered are total assets (net of accounts payable), fixed assets,

equity, total debt (long-term and short-term), revenues, operating earnings before interest and

taxes, taxable income as reported and taxes paid.

15 The identity of individual corporations was suppressed in the micro-level (company-level), longitudinal data setconstructed for this study.

16 We exclude Crown corporations, banks and trust companies, insurance corporations, co-operative corporations,credit unions, investment corporations, mutual-fund corporations, mortgage-investment corporations, exemptcorporations and non-resident corporations carrying on entertainment or travel business in Canada.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 11

Some interesting observations can be made from these tables. In 1984, taxes as a percentage of

revenues for CCCs were 2.7 percent, and this percentage was little changed by the end of the

10 years; the corresponding value for 1994 is 2.4 percent. During the 10-year period under

consideration, the assets, equity and debt levels of CCCs grew by about 75 percent, revenues by

50 percent and, operating earnings before interest and taxes by 79 percent, whereas taxable

income rose by 25 percent and total taxes paid by 33 percent. Thus, even for CCCs, taxable

income and taxes did not keep pace with the growth in revenues and operating earnings before

interest and taxes.

The picture for FCCs is, however, more dramatic. In 1984, the tax-to-revenue ratio for FCCs was

5.3 percent – almost double that of the CCCs. The primary reasons for this difference were their

higher operating margins – defined as profit before interest and taxes divided by revenues

(19 percent versus 15 percent), and a much lower reliance on debt (a 17-percent debt-to-total

asset ratio versus 34 percent for CCCs) thereby leading to a lower interest burden. However, the

1994 numbers tell a much different story. In 1994, the tax-to-revenue ratio is 1.7 percent for

FCCs, even lower than the corresponding number for CCCs. This decline is not because FCCs

had lower operating margins, but because they resorted to higher levels of debt financing, with a

corresponding increase in their interest burden. The operating margin in 1994 is 18.5 percent,

almost identical to that of the 1984 level. The drop in this tax-to-revenue ratio can be accounted

for, in major part, by the much lower taxable income-to-revenue ratio. In turn, the decline in this

ratio is at least partially a result of a much higher reliance on debt by FCCs. During the ten years

under consideration, the assets of FCCs rose by 72 percent, equity by only 29 percent, debt by

154 percent, operating margins rose by 41 percent, whereas taxable income declined by

36 percent and taxes declined by 52 percent. Figures 3 and 4 show these dramatic changes in the

tax-to-asset ratio and in the operating earnings before interest and taxes-to-asset ratio for the

CCC and FCC subsamples.

In terms of the potential impact on tax revenues, data in Table 4b can be used to make some

crude estimates. For example, if the debt-to-asset ratio of the sample FCCs in 1994 had remained

at the 1984 level, their debt would have been higher by $4.5 billion. At a 10-percent interest rate

and a 40-percent tax rate, the tax revenues from the sample corporations would have been higher

by $180 million. Since the assets represented by sample corporations are approximately

12 WORKING PAPER 97-14

13 percent of total assets (see Table 1) of all FCCs, this would have meant $1.3 billion in higher

taxes. If, on the other hand, we use the debt-to-fixed asset ratio as the variable for this analysis,

the corresponding numbers for the sample would be $320 million (i.e. potentially higher tax

revenues) for the sample corporations and $2.4 billion as an estimate for the universe (using the

numbers in Table 1).

Although not shown here, if one considers results for the Canadian-controlled corporation

without foreign affiliates (CC-NFA), Canadian-controlled corporation with foreign affiliates

(CC-FA), foreign-controlled corporation with foreign affiliates (FC-FA) and FC-NFA

sub-samples, except for CC-NFA, all groups show an increase in the debt-to-asset ratios and a

corresponding decrease in tax-to-revenue ratios compared to the operating margins. For example,

for the 126 or so foreign-controlled corporations with no foreign affiliates other than the parent

(FC-NFA), the operating margins increased by 50 percent whereas tax-to-revenue dropped by

40 percent. The unambiguous conclusion is that there has been a consistent increase in

debt-to-asset ratio in all categories of corporations except for those controlled by Canadian

parents with no foreign affiliates. Correspondingly, the taxes paid by the foreign-controlled

corporations, as well as those Canadian-controlled corporations with foreign affiliates have

declined significantly relative to their underlying operating earnings.

Figures 5 and 6 provide the subsample values of debt-to-asset ratios, which are consistent with

the aggregate evidence in Table 1.17 Figure 5 shows the debt-to-asset ratio for all CCCs and

FCCs, whereas Figure 6 shows the values for CC-FA, CC-NFA, FC-FA and FC-NFA.

A subgroup’s debt-to-asset ratio is defined as the subgroup aggregate debt to the subgroup

aggregate assets.18

This breakdown of CCCs and FCCs into those with and without foreign affiliates indicates that,

except for Canadian-controlled corporations without foreign affiliates, corporations in the three

other subgroups increased their debt-to-asset ratios, meaning an increasing reliance on debt.

17 Classification of corporations by whether or not they have foreign affiliates did not start until 1986, so Figure 6starts from 1986.

18 Debt equals the sum of both long-term and short-term debt and assets equal total assets minus accounts payable.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 13

This evidence is striking, since it suggests that the changes in the relative tax rates resulting from

the tax reforms may have had a strong impact on the financial structures of MNCs. Although

there was a reduction in the Canadian statutory corporate tax rate as a result of the Canadian tax

reform, by itself, this did not seem to have had a significant impact on the debt-to-asset ratio of

Canadian-controlled corporations with no foreign affiliates.19 This suggests that, even though

there was a decrease in Canadian tax rates, the decrease was overshadowed by the reversal in

relative tax positions between the United States and Canada. Since these results are based on the

aggregated data which may mask potential variation across corporations, an econometric

analysis, based on micro data, is in order.

4.3 Econometric Analysis

To estimate the effect of taxes on debt financing by comparing the financial policy of

Canadian-controlled corporations without foreign affiliates with the financial policy of all other

corporations which consist of Canadian-controlled corporations with foreign affiliates and

U.S.-controlled corporations, we specify the following regression models:20

(1)

=

+ P + SD

0 CCFA CCFA FCNFA FCNFA FCFA FCFA i t

t p i t i t i t

α α α α α τ

β τ β γ ετ

+ + + +

+ +

( )1 D D D

∆ ∆

Debt

Asset

i t

i t

(2)

DebtAsset

=

+ P + SD

i t

i t

0 CCFA CCFA FCNFA FCNFA FCFA FCFA i t

tUS

p i t i t i tUS

α α α α α τ

β τ β γ ετ

+ + + +

+ +

( )1 D D D

19 A standard extension of capital-structure theory would lead us to expect that a change in the Canadian tax rateswould reduce the incentive of CCCs to finance their operations with debt. However, we see no such reduction.

20 Although not reported here, we also attempted to model the impact of the tax loss carry-forward on thedebt-to-asset ratio. Theoretically, the availability of tax loss carry-forward will reduce a corporation’s effective taxrate. We tried different ways such as adding an extra explanatory variable, DLCF times the tax rate where DLCF is anannual loss carried-forward dummy with a value of one, where tax loss is carried-forward, and zero otherwise, or is asample-period dummy with a value of one, where there is a tax loss carry-forward in any year of the sample period,and zero otherwise. Neither of these approaches resulted in the corresponding coefficient being significant, and,therefore, the results are not included in the table.

14 WORKING PAPER 97-14

where Debti t = long-term and short-term debt of corporation i in year t;

Asseti t = total assets minus accounts payable of corporation i in year t;

D j , j = CC-FA, FC-NFA and FC-FA, is a control dummy;

τ i t = Canadian corporate tax rate (which combines provincial and federal rates) of

corporation i in year t;

∆τ t = the difference of the average industry corporate tax rates between Canada and

the United States for groups CC-FA, FC-NFA, and FC-FA. For CC-NFA, ∆τ t is zero;

τ tUS = the average tax rate in the United States, in each year, t;

Pi t = risk - adjusted operating performance of corporation i in year t;

SDi t = a vector of size dummies;

ε i t denotes the error term, assuming heteroskedasticity across corporations;

α, β, and γ are the parameters to be estimated. Note that γ is a vector.

The control dummies divide corporations into four groups according to ownership

(Canadian-controlled or U.S.-controlled) and the presence or absence of foreign affiliates. Unlike

Canadian-controlled corporations without foreign affiliates whose debt-to-asset ratios are

affected only by Canadian taxes, other corporations have incentives to change their debt-to-asset

ratios whenever there is a change in Canadian taxes or in relative tax rates between Canada and

the United States.

The risk-adjusted operating performance variable Pit is defined as a corporation’s operating

earnings (before interest and tax), scaled by the corporation’s assets in year t and divided by the

standard deviation of the corporation’s earnings across sample years. The standard deviation is

used to measure the risk of operating income of a corporation, and is assumed to be constant for

each year t for each corporation. There is a general consensus that the ability (cost) to borrow is

negatively related to the riskiness of the corporation’s operating performance, since more

profitable and less risky corporations can sustain higher debt levels.

The size dummies are introduced to capture the size effect on the debt-to-asset ratio, which,

to some extent, reflects a corporation’s vintage. We divide corporations based on assets into

Tax Reforms, Debt Shifting and Corporate Tax Revenues 15

four groups. The first group consists of corporations with assets not greater than $100 million;

the second group with assets larger than $100 million but not greater than $500 million; the third

group with assets larger than $500 million but not greater than $1 billion; the last group with

assets larger than $1 billion. The first group will be used as the base for regression.

Some comments on the variable ∆τ t in equation (1) and τ tUS in equation (2) are in order. Ideally,

we would have liked to model this variable at the individual firm level and for each year by

calculating (or estimating) the actual rates faced by the parent and its subsidiary. In addition, we

would have liked to model the excess foreign tax positions of the parent. Unfortunately, we do

not have access to the tax data of the U.S. parent or the foreign affiliate(s) of the Canadian

parent, and there is a multicollinearity problem (between τ tUS and ∆τ t ). Therefore, in

equation (1), we have used the Canadian industry average corporate tax rates (based on our

sample) minus the U.S. national average corporate tax rates to derive tax differentials that depend

on the type of the firm – CC-FA, CC-NFA, FC-NFA and FC-FA. Thus, the tax differential

estimate is the same for each firm in a group in a given year. The tax differential for group

CC-NFA is zero, since its financial policy should not be influenced by U.S. tax rates. To test for

the robustness and the impact of the tax-rate changes, we also use in equation (2) just the U.S.

tax rate instead of the ∆τ t to see whether the debt-to-asset ratio is sensitive to the U.S. tax

rate. Note that we cannot use both the variables in the same regressions due to the

multicollinearity problem.

Table 5 reports the results of estimating equations (1) and (2) using the longitudinal data set

consisting of 388 large Canadian-based non-financial corporations. Column (i) shows the results

for equation (1) but without the size dummies, column (ii) corresponds to the full specification,

column (iii) corresponds to equation specification 2. The regressions reported in column (i)

through (iii) suggest the following:

a) Canadian corporate tax rates have a significant impact on debt-to-asset ratios of

Canadian-based corporations. Canadian-controlled corporations without foreign affiliates

tend to be more sensitive to Canadian taxes than Canadian-controlled corporations with

foreign affiliates and U.S.-controlled corporations. This is because the financial policy of

16 WORKING PAPER 97-14

corporations with foreign affiliates or corporations controlled by U.S. parents is also

influenced by foreign tax systems.

b) The other key result is that the difference between Canadian and U.S. taxes correlates

with an increase in the debt-to-asset ratios of corporations other than those that are

Canadian-controlled without foreign affiliates. Under the column (ii) specification, the

coefficient for the differential tax rate is statistically significant and positive. That is, on

average, the debt-to-asset ratios of firms in groups other than CC-NFA increase as the

Canadian tax rates relative to U.S. tax-rates increase. Similarly, the results in column (iii)

indicate that even the simple U.S. tax-rate variable has the right sign and is also statistically

significant. What is remarkable about these statistically significant results is that neither of

these two specifications is exact. Ideally and as mentioned earlier, one would like to have

firm-level data for the U.S. parent and then use the matched differential tax rate in the

regression specification. Unfortunately, such data are unavailable.

c) Corporations with good operating performance have significantly higher debt-to-asset ratios.

This simply confirms the link between business risk and financial risk.

d) The size of corporations, which is measured by assets, also significantly influences their

debt-to-asset ratio. Large-size corporations have higher debt-to-asset ratios.

Overall, these results indicate that there has been a change in the debt-to-asset ratios of the

multinationals operating in Canada along with the relative shifts in the statutory tax rates

between the two countries. Although the Canadian tax reform reduced the statutory tax rates in

Canada, it was overshadowed by the declines in the U.S. tax rates.

Note that these results do not necessarily indicate that, by lowering its tax rate so as to

(potentially) lower the debt-to-asset ratio, Canada would achieve a net gain in its tax revenues.

This can be explored with illustrative calculations based on column (iii) of Table 5. Based on the

coefficients of FC-FAs and FC-NFAs, a one percentage point reduction in the Canadian

corporate tax rate would, on the margin, reduce the debt-to-asset ratio by 0.2689 percentage

points on average (weighted by the assets of FC-FAs and FC-NFAs in Table 1) for

foreign-controlled corporations. Given the 1994 data from Table 1 for the total assets of these

Tax Reforms, Debt Shifting and Corporate Tax Revenues 17

corporations, this implies a reduction in debt financing of $1.105 billion. Assuming an interest

rate of 10 percent for simplicity, this reduction in debt would imply a reduction of

$0.1105 billion in interest payments and a corresponding increase in total taxable income. Given

that the taxable income of these corporations was $12.355 billion in 1994 (Table 1), the total

change in tax revenue would be:

∆R = (12.355 +0.1105) (τ – 0.01) –12.355 τ = 0.1105 τ − 0.1246 < 0

Thus, although the interest deductions are potentially reduced, the reduction is not sufficient to

fully offset the overall one percentage point decline in the tax rate. In other words, no matter how

much the tax rate declines, the overall tax revenues will decline, although debt levels may

increase. In a similar vein, one may argue that an increase of one percent in the tax rate may

increase the overall tax revenues, all else being held constant. However, relatively higher tax

rates may encourage corporations to engage in other instruments (as in footnote 5) to minimize

their tax payments. Moreover, relatively high tax rates may induce Canadian multinationals to

invest abroad and may deter other FCCs from investing in Canada.

5. ConclusionsIn this paper, we concentrate on analysing debt-shifting behaviour of Canadian corporations with

a special emphasis on Canadian subsidiaries of foreign corporations and Canadian-controlled

corporations with foreign affiliates. We hypothesize that shifts in the relative tax rate faced by

corporations in the United States and Canada following the tax reforms undertaken by these two

countries have led these categories of corporations to increase their reliance on debt in Canada.

This debt shifting may be one explanation for the reduced Canadian corporate tax in the early

1990s. Our two-country integrated theoretical model also shows that, in a world where

host-country tax rates substantially exceed home-country tax rates, the home-country

multinational will choose to finance its subsidiary with a much higher portion of debt. This

would allow the multinational to maximize its overall after-tax income.

18 WORKING PAPER 97-14

Although many potential avenues for tax shifting across national borders are open to a typical

multinational, we hypothesize that the multinational will prefer debt shifting as a mechanism,

as it is potentially the least costly mechanism. More specifically, debt shifting is free from:

a) any audit consequences resulting from aggressive transfer pricing; and b) potential difficulty in

evaluating trade-offs between tax differentials and resource rents, or high cost due to the

irreversibility of investments.

Our empirical and econometric results confirm the significant changes that have occurred in debt

levels of multinationals in Canada. Our aggregate results clearly show a reduction in taxes from

FCCs in Canada as a proportion of total corporate revenues. Our sample of 457 large

corporations indicates that this reduction is consistent with the increase in debt-to-asset ratios of

FCCs in Canada following the U.S. and Canadian tax reforms, which significantly changed the

relative tax differential and made Canada a country with relatively high tax rates. Similar

increases in debt-to-asset ratios are also evident for Canadian-controlled multinationals. Our

econometric analysis also confirms these results, even though we do not have a direct measure of

firm-specific tax rates for the U.S. parent. In all cases, the debt-to-asset ratios at the firm level are

statistically significantly related to the Canadian tax rates as well as the tax differential.

Since USCCs control a significant fraction of Canadian corporate assets and operating income,

the impact on Canadian corporate tax revenues has been significant. In essence, the evident

debt-shifting policies adopted by USCCs have benefited the United States at the expense of

Canadian tax revenues. In aggregate, if FCCs had maintained, in 1994, the same corporate

tax-to-asset ratio as in 1984, Canadian tax revenues from FCCs would have been $6.4 billion

instead of the actual amount of $2.9 billion, a difference of $3.5 billion. Using the crude

estimates based on the sample corporations, this difference could be in the range of $1.3 to

$2.4 billion – still a significant number. These estimates exclude the potential loss of tax

revenues due to an increase in debt by Canadian-controlled corporations who now have an

incentive to finance their foreign (U.S.) affiliates by raising debt in Canada. Clearly, the impact

on Canadian tax revenues of debt shifting by both the FCCs and the CCCs with foreign affiliates

is significant. However, it should also be noted that our regression results suggest that tax

revenue losses as a result of debt shifting in response to changes in relative tax rates are

much lower than the impacts of changes in total corporate tax-to-asset ratios noted above.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 19

Although our results indicate that the debt shifting has indeed taken place during the post-reform

period and that it has affected Canadian tax revenues, three caveats are in order. First, one could

argue that the lower reliance on debt by U.S.-controlled Canadian subsidiaries during the

pre-reform period may have been accidental and temporary. Once the role of debt in reducing

taxes was discovered during the leveraged buy out (LBO) era of the 1980s, sooner or later, and

independent of any tax reform, multinationals in Canada would have increased the leverage of

their Canadian subsidiaries. We have no way to prove or disprove this assertion. Second, it can

be also argued that, if Canada had maintained the relative low tax rates, there would have been

relatively little debt shifting. In that case, the impact on Canadian taxes due to debt shifting could

have been smaller, but overall tax revenues would have declined due to the reduction in the

statutory tax rates as noted above. More specifically, although the relative tax differentials have

had an impact on debt levels and thereby on Canadian tax revenues, the extent of the decline in

taxable income is not large enough to suggest that, if Canadian tax rates had been lowered

further, overall Canadian tax revenues would have been higher. Third, it can be argued that

although there seems to be some stability in the debt-to-asset ratios of USCCs (Figures 5 and 6)

in the post-1990 period, their reliance on debt is still lower than their Canadian-controlled

counterparts. If the debt-to-asset ratio of CCCs is viewed as an “optimum” ratio, given the

business risk and tax benefits of debt, then the debt levels of USCCs can be considered below

that optimum especially when their overall operating profitability is better than their Canadian

counterparts (Figure 4 and Tables 4a and 4b). 21 Thus, one may expect a further increase in the

debt-to-asset ratio of USCCs and a corresponding decrease in the Canadian tax base.

Notwithstanding these caveats, the evidence presented in this paper highlights the

interdependence of the tax regime of countries that depend on foreign-based multinationals or

whose domestic multinationals are free to invest in foreign countries. Such countries must be

vigilant in analysing their tax regimes relative to those of their partner countries. Another

problematic issue is the potential policy response in the face of such debt shifting. 22

21 A simple calculation using the data in Table 4 shows that $4 billion of debt can be raised by FCCs to reachthe same debt-to-asset ratio of their Canadian counterparts.

22 See Edgar (1987) for a good exposition on the potential policy response to such erosion of the domestictax revenues.

20 WORKING PAPER 97-14

At the extreme, rules like thin capitalization may help, but not when the level of debt financing is

reasonable though higher than before. It may be possible to limit interest deductions by

complicated tracing rules such that, at the margin, the corporation faces the same marginal tax

rate on every incremental debt dollar. Although such mechanisms are possible, the complexities

in devising such rules should not be underestimated. Another alternative may be to ensure that

the domestic statutory tax rates remain in sync with the tax rates in the country’s most significant

trading partners; in the case of Canada, this would be the United States. One conclusion,

however, is inescapable: a change in the relative corporate income tax rates between Canada and

the United States in the 1980s has affected debt-to-asset ratios and thus Canadian tax revenues. If

this difference persists and if Canadian-controlled corporations continue to aggressively expand

abroad, the Canadian corporate tax base could experience further pressure.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 21

Appendix: One-parent, One-foreign-subsidiary, Two-period ModelA multinational enterprise that consists of a parent and a foreign subsidiary is at the end of

period 0 and is planning its coming two-period investment. The multinational has a total stock of

equity E0 (including retained earnings), which can be allocated to the parent, the subsidiary or

both. The technology used by the multinational requires only capital. The production function is

f K( ) , where K is the capital input, ′f K( ) >0 and ′′ <f K( ) 0.

The objective of the multinational is to maximize its two-period consolidated after-tax income,

which equals the parent’s after-tax income (including the dividend income from its foreign

subsidiary). For simplicity, we assume that the multinational does not issue new equity. Thus, the

multinational has a total equity E0 , which can be allocated between the parent (E ) and the

subsidiary (E * ). Because of high transaction costs, an allocation of E0 in the first period can not

be changed in the second period.23 Both the parent and the subsidiary borrow with one-period

maturity on the world market at the interest rate i to finance their extra investments. For

simplicity, we assume that there is no restriction on the debt-to-equity ratio of either the

subsidiary or the parent.

In the first period, the parent and the subsidiary invest E B+ 1 and E B* *+ 1 respectively, where

B1 and B1* are debts of the parent and the subsidiary, respectively. In the second period, both the

parent and the subsidiary can retain all or part of their after-tax earnings from the first period to

finance their investments. Thus, their investment in the second period are E B R+ +2 and

E B R* * *+ +2 , where B2 and R represent the debt and the retained earnings of the parent, and

B2*

and R* represent the debt and the retained earnings of the subsidiary. At the end of the

second period, the subsidiary repatriates all its after-foreign-tax earnings in the second period

plus the equity (E* ) and the retained earnings from the first period (R* ) to the parent.

The income of the multinational is subject to several taxes. The income from the parent is taxed

by the home country at the home country’s corporate tax rate,τ . The income from the subsidiary

is taxed by the foreign country at the foreign country’s corporate income tax rate,τ * . When the

23 This assumption is made purely for simplicity; it does not affect our results.

22 WORKING PAPER 97-14

dividend is repatriated from the subsidiary to the parent, the dividend is subject to a withholding

tax by the foreign country at the rate, w, and a tax from the home country if the multinational

is short of foreign tax credits. We assume that the home country has an international

double-taxation agreement with the foreign country, so that the parent can claim foreign tax

credits up to its home tax liability on the repatriated dividend.

Let θ denote the combined tax rate on dividend, which equals the sum of the host withholding

tax rate and the home tax rate. Let D denote the repatriated dividend. The total foreign tax

liability on the income related to the dividend is the sum of the foreign tax liability on the income

related to the dividend and the withholding tax on the dividend; that is, D wτ

τ

*

*1−+

(for a

discussion, see Hines and Hubbard, 1990, p. 164). The home tax liability (before foreign tax

credits) on the income related to the dividend is Dττ1−

*

. If ττ

ττ1 1−

≥−

+*

*

*w , then the

parent is short of foreign tax credits, so that the dividend is subject to a tax from the home

country at the rate τ τ

τ−−

−*

*1w . Thus, the combined tax rate on the repatriated dividend equals

θ τ ττ

τ ττ

= + −−

− = −−

w w*

*

*

*1 1. If

ττ

ττ1 1−

<−

+*

*

*w , then the parent has excess foreign tax

credits, and no home tax liability occurs on the repatriated dividend. In this case, the combined

tax rate just equals the foreign withholding tax rate w. In summary, the combined tax rate on

dividend is as follows:

(A1) θτ τ

τττ

ττ=

−

− −≥

−+

*

* *

*

*,

.1 1 1

if w

w otherwise

Tax Reforms, Debt Shifting and Corporate Tax Revenues 23

The multinational’s objective is to maximize the present value of its consolidated after-tax

income by choosing an optimal financial policy, a combination of E, B1 , R, B2 , B1* , R* and B2

* ,

subject to certain constraints as shown in the following equation. The mathematical

expression is:

(A2)

( )[ ]( )( ) ( )[ ]( ){ }

( )[ ]( ){ }( )( ) ( )[ ]( ){ }( )( )[ ]( ) ( )[ ]( ){ }( )( )[ ]( )

max

, , ,

, ,

* * * *

* * * * *

* * * *

* * * *

*

f E B i B R

r f E B R i B R

f E E B i B R

r f E E B R i B R

f E B i B f E E B i B R R

f E E B i B R

E B R B

E E B

+ − − −+ + + + − − +

+ − + − − − −

+ + − + + − − + −

+ − − + − + − − − − − ≥

− + − − − ≥≥

−

−

−

1 11

2 2

0 1 1

1

0 2 2

1 1 0 1 1

0 1 1

1 2

0 1

1

1 1

1 1

1 1 1

1 1 1 0

1 0

0

ττ

τ θ

τ θ

τ τ θ

τ

s.t.

R B* *, ,2 0≥

Where r is a discount factor and ( )r i= −1 τ , which is usually called the arbitrage condition and

has been used by Weichenrieder (1996), among others. In this model, the first constraint means

that the retained earnings of the parent are limited to the parent’s total after-tax earnings in the

first period that includes the parent’s after-tax earnings from home and the after-tax repatriated

dividend from the subsidiary. The second constraint means that the retained earnings by the

subsidiary in the first period cannot exceed its after-foreign-tax earnings.

The corresponding Lagrangian is:

(A3)

( )[ ]( )( ) ( )[ ]( ){ }

( )[ ]( ){ }( )( ) ( )[ ]( ){ }( )

( )[ ]( ) ( )[ ]( ){ }( ){ }( )[ ]( ){ }

L f E B i B R

r f E B R i B R

f E E B i B R

r f E E B R i B R

f E B i B f E E B i B R R

f E E B i B R

E B R B

d

d

E R

= + − − −+ + + + − − +

+ − + − − − −

+ + − + + − − + −

+ + − − + − + − − − − −

+ − + − − −+ + + +

−

−

1 11

2 2

0 1 1

1

0 2 2

1 1 0 1 1

0 1 1

1 1 2 2

1

1 1

1 1

1 1 1

1 1 1

1

ττ

τ θ

τ θ

λ τ τ θ

λ τλ λ λ λ

* * * *

* * * * *

* * * *

* * * * *

( )+ − + + +λ λ λ λE RE E B R B* * * * * * *.0 1 1 2 2

24 WORKING PAPER 97-14

The first-order conditions for an optimal solution are:

( )( ) ( )( ) ( )( )( )

( )( )( )[ ]( )( ) ( )( )( )[ ]

( )( ) ,01

111

111

1

1111

11

***10

*

**101

***20

**102

=−+−+−′−

−++−′−−+′+

−−++−′+

−

−−+−′−−++′+

+−+′=∂∂

EEd

d

BEEf

BEEfBEf

RBEEfr

BEEfRBEfr

BEfE

L

λλτλθττλ

θτ

θτττ

(A4)

( )( )[ ] ,0111

11 2 =−++−++′

++−=

∂∂

dRRBEfrR

L λλτ(A5)

(A6) ( )[ ]( ) ( )[ ]( ) ,011 1111

=+−−+′+−−+′=∂∂ λτλτ iBEfiBEfB

Ld

(A7) ( )[ ]( ) ,011

122

2

=+−−++′+

=∂∂ λτiRBEf

rB

L

(A8) ( ) ( )( )[ ]( ) ( ) ,011111

11 *****

20*=+−−−−+−++−′

++−−=

∂∂

RddRBEEfrR

L λλθλθτθ

(A9) ( )[ ]( )( ) ( )[ ]( )( )

( )[ ]( ) 01

1111

*1

**10

*

**10

**10*

1

=+−−+−′+

−−−+−′+−−−+−′=∂∂

λτλ

θτλθτ

iBEEf

iBEEfiBEEfB

L

d

d

(A10) ( )[ ]( )( ) ,0111

1 *2

***20*

2

=+−−−++−′+

=∂∂ λθτiRBEEf

rB

L

Tax Reforms, Debt Shifting and Corporate Tax Revenues 25

With the following Kuhn-Tucker conditions:

λd ≥ 0, [ f(E + B1) – iB1](1 – τ) + {[ f(E0 – E + B1*) – iB1

*](1 – τ*) – R*}(1 – θ ) – R ≥ 0(A11)

and λd {[ f(E + B1) – iB1](1 – τ) + {[ f(E0 – E + B1*) – iB1

*](1 – τ*) – R*}(1 – θ ) – R} = 0,

λd* ≥ 0, [ f(E0 – E + B1

*) – iB1*](1 – τ*) – R* ≥ 0

(A12)and λd

* {[ f(E0 – E + B1*) – iB1

*](1 – τ*) – R*} = 0,

(A13) λ λE dE E≥ ≥ =0 0 0, ,and

(A14) λ λ1 1 1 10 0 0≥ ≥ =, ,B B and

(A15) λ λR RR R≥ ≥ =0 0 0, ,and

(A16) λ λ2 2 2 20 0 0≥ ≥ =, ,B B and

(A17) ( )λ λE EE E E E* *, ,≥ − ≥ − =0 0 00 0 and

(A18) λ λ1 1 1 10 0 0* * * *, ,≥ ≥ =B B and

(A19) λ λR RR R* * * *, ,≥ ≥ =0 0 0 and

(A20) λ λ2 2 2 20 0 0* * * *, .≥ ≥ =B B and

We first consider a simple case of this model, where ( )′f E0 >i , ( )[ ]( )f E B i B+ − −1 1 1 τ

( )[ ]( ){ }( )+ − + − − − − −f E E B i B R R0 1 1 1 1* * * *τ θ >0 and ( )[ ]( )f E E B i B R0 1 1 1− + − − −* * * *τ >0

at the optimal point. The last two inequalities imply that λ λd d= =* 0 . The first inequality means

that it is profitable for the multinational to invest more than the amount of the existing stock of

equity in each country in the first period by borrowing to finance the extra amount (λ1 0= by

equation (A6)). We now proceed to discuss the optimal financial policy of the multinational

under this simple case.

26 WORKING PAPER 97-14

Look at the parent first. From equations (A5) and (A7), we have λ λR = 2 , which implies that the

multinational is indifferent to debt and retained earning to finance the parent’s investment in the

second period. Indeed, the capital cost of both financing means equals ( )r

r1+ . No matter what

is used to finance the investment, ( )( )′ + + − =f E B R r2 1 τ or ( )′ + + =f E B R i2 by the

arbitrage condition. We also have B1>0 and ( )′ + =f E B i1 from equation (A6). In summary, the

parent keeps a stable investment up to the point where the after-tax marginal profit

( ( ) ( )( )′ + − = ′ + + −f E B f E B R( )1 21 1τ τ ) equals the cost of capital ( )i 1− τ and the size of

investment depends only on interest. The multinational is indifferent to debt and retained

earnings in financing the parent’s investment. These results are independent of the home and

foreign taxes.

Next we turn to the subsidiary. From equations (A8) and (A10), we have 0 2≤ <λ λR* * if τ >τ * ,

which implies that B2 0* = and ( )( )′ − + − =f E E R r0 1* *τ ; we have λ R* > λ 2 0* ≥ if τ τ< * ,

which implies that R* = 0 and ( )′ − + =f E E B i0 2* . This is not surprising. The cost of one unit

of debt is ( )( )1

11 1

+− −

ri τ θ* and the cost of one unit of retained earnings is ( )r

r11

+− θ .

Their difference equals ( )i

r

11

−+

−θ τ τ *

, implying that if τ >τ * , the financing cost by debt is larger

than that by retained earnings; if τ τ< * , the opposite is true. As far as the first period is

concerned, we have B1* >0 and ( )′ − + =f E E B i0 1

* from equation (A9).

In summary, the subsidiary invests in the first period up to the point where the after-tax marginal

profit to the parent ( ( )( )′ − + − −f E E B( )* *0 1 1 1τ θ ) equals the cost of capital (( )( )i 1 1− −τ θ* ).

The investment in the second period is financed exclusively by the retained earnings from the

first period, if the home corporate tax rate is larger than the foreign corporate tax rate, and it is

financed exclusively by debt if the home corporate tax rate is smaller than the foreign corporate

tax rate. It is higher than that in the first period, if τ >τ * because of ( )′ − + <f E E R i0* ;

otherwise, it is the same.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 27

Extending this result to the U.S.-Canada situation, when Canadian tax rates are higher than

U.S. tax rates, a Canadian-controlled U.S. subsidiary will use as much debt financing as possible

in the first period, so that it can use as much of the retained earning financing as possible in the

second period, whereas the U.S.-controlled Canadian subsidiary will use as much debt financing

as possible in both periods. These results are independent of the foreign withholding tax.

Now we are ready to look at equation (A4), which links the parent and the subsidiary together.

Inserting the results from the last two paragraphs into this equation and arranging it by using the

arbitrage condition ( )r i= −1 τ , we arrive at:

(A21) ( ) ( )( )[ ]

( ) ( )( )[ ]1 1 1

10

2

11 1 1 0

− − − − ++

+ − = ≥

++

− − − − + − =

τ τ θ θ λ λ τ τ

τ τ θ λ λ

* * *

* *

r

r

ir

r

E e

E E

if

otherwise

It is not difficult to show that ( ) ( )( )[ ]1 1 1 0− − − − ≥τ τ θ* if τ τ≥ * and

( ) ( )( )[ ]1 1 1− − − −τ τ θ* >0 if τ <τ *, so that 0 ≤ <λ λE E

* under any situation. This implies that

E E= 0 .

In summary, all equity is used to finance the parent, and the subsidiary is completely financed by

debt and/or retained earnings, which are independent of the home and foreign taxes. This result

is surprising, but the intuition is very simple. When the corporate tax in the home country is

relatively high, the multinational finances its subsidiary in the first period by using debt, so that it

can reinvest its after-foreign-tax profits in the second period. This is driven by the incentive of

deferral of dividend repatriation to minimize its tax payments. When the corporate tax in the

home country is relatively low, the multinational uses debt exclusively to finance the subsidiary

in both periods, since it can take advantage of a higher interest-expenses deduction or the lower

cost of capital in the foreign country.

The model is set up in such a way that the parent does not borrow to finance the subsidiary and

vice versa. Is there any advantage for the parent to borrow to finance the subsidiary or for the

subsidiary to borrow to finance the parent? The answer is no to the former and yes to the latter.

28 WORKING PAPER 97-14

In each period, the cost of borrowing by the parent is ( )i 1− τ , and the cost of borrowing by the

subsidiary is ( )( )i 1 1− −τ θ* . They are the same if ( )τ τ τ≥ + −* *1 w ; otherwise, the cost of

borrowing by the parent is larger than that by the subsidiary. Clearly, if the home country’s

corporate tax is relatively low, then it is advantageous for the subsidiary to borrow to finance the

parent. This implies that, in the current situation, a U.S. subsidiary in Canada will borrow

heavily, if it is allowed, to finance its U.S. parent.

The above discussion is under the assumptions: ( )′f E0 >i , ( )[ ]( )f E B i B+ − −1 1 1 τ

( )[ ]( ){ }( )+ − + − − − − −f E E B i B R R0 1 1 1 1* * * *τ θ >0 and ( )[ ]( )f E E B i B R0 1 1 1− + − − −* * * *τ >0

at the optimal point. Now we relax these assumptions one at a time to see how our results

will change.

If ( )′ ≤f E0 i , then, from equations (A5)-(A6), no debt or retained earnings will be used by the

parent that is fully financed by equity up to a point where λ λE E= * (according to equation (A4)).

After that point, the rest of equity is used to finance the subsidiary. Clearly, our results under the

assumption ( )′f E0 > i are intact when this assumption is relaxed.

The constraint ( )[ ]( )f E B i B+ − −1 1 1 τ ( )[ ]( ){ }( )+ − + − − − − −f E E B i B R R0 1 1 1 1* * * *τ θ >0 is

not very interesting since the parent is indifferent to debt and the retained earnings to finance its

investment. So it is never binding.

In contrast, the constraint ( )[ ]( )f E E B i B R0 1 1 1− + − − −* * * *τ >0 is likely to be binding, because it

is optimal for the multinational to use the existing stock of equity to finance the parent first, and

only the leftover is allocated to the subsidiary, so that the subsidiary has the potential to use a

large amount of retained earnings whenever it is possible. If this constraint is binding, then

λ d* >0. It is clear from our earlier discussion that the subsidiary will use the retained earnings to

finance its investment in the second period, only when τ >τ * . In this case, the subsidiary will use

all its after-foreign-tax earnings and then borrow some to finance its investment to the point

where ( )′ − + + =f E E B R i0 2* * , which is different from ( )′ − + =f E E R r0

* when the

constraint is not binding. However, this difference does not affect our results.

Tax Reforms, Debt Shifting and Corporate Tax Revenues 29

FIGURE 1Statutory Average Corporate Tax Rates in Canada and the United States for Large Corporations

0.38

0.4

0.42

0.44

0.46

0.48

0.5

0.52

1983 1985 1987 1989 1991 1993 1995

Tax

Rat

e

Canadian Corporate Tax Rates U.S. Corporate Tax Rates

TABLE 1Taxable Income, Corporate Tax, and Assets

for Canadian Non-financial Corporations ($ billions)

Foreign-controlledCorporations

Canadian-controlledCorporations

All Corporations

YearTaxableIncome Tax Assets

TaxableIncome Tax Assets

TaxableIncome Tax Assets

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

10.851

14.324

11.560

10.488

12.490

13.345

11.017

11.058

8.712

9.241

12.355

2.977

4.242

3.456

3.023

3.465

3.455

2.865

2.878

2.264

2.366

2.912

191.9

205.2

214.8

247.5

290.6

319.5

324.4

357.7

364.7

375.6

411.0

27.673

27.945

28.001

34.464

38.781

45.649

39.237

37.229

33.785

38.469

44.027

5.950

6.001

6.234

7.941

8.599

9.409

8.366

8.406

7.731

8.700

9.553

1,285.7

1,330.7

1,422.4

1,596.1

1,806.8

1,934.0

2,100.5

2,332.2

2,194.0

2,338.6

2,460.7

38.524

42.269

39.561

44.952

51.272

58.993

50.255

48.287

42.497

47.710

56.383

8.927

10.243

9.690

10.963

12.064

12.964

11.231

11.284

9.995

11.066

12.464

1,477.6

1,535.9

1,637.2

1,843.6

2,097.5

2,253.5

2,424.9

2,689.9

2,558.7

2,714.2

2,871.7

Source: T2 Sample Summary Statistics, Finance Canada

Note: Total corporate tax includes Part I tax, net Part I.3 tax large corporations tax (LCT) and net Part VI tax. Net LCT equalsgross LCT minus the surtax credit. Net Part VI tax equals gross Part VI tax minus the Part I credit.

30 WORKING PAPER 97-14

FIGURE 2Corporate Tax-to-Assets ratio for Canadian Non-financial Corporations

TABLE 2Basic Parameters for an Illustrative Example

Basic ParametersRate of return on assets 10%Cost of debt 7%

Canada pre-reform statutory income tax rate 49%Canada post-reform statutory income tax rate 42%US pre-reform statutory income tax rate 51%US post-reform statutory income tax rate 39%

100% dividend payout

Capital Structure Cases 1 and 2 Case 3

$ of equity invested by U.S. parent in Canadian subsidiary $1,500 $1,000 $ of debt invested by U.S. parent in Canadian subsidiary $0 $500Total assets in Canadian subsidiary $3,000 $3,000

Debt/Equity Ratio 1 2

1983 1985 1987 1989 1991 1993 19950

0.005

0.01

0.015

0.02

0.025

Canadian-controlled Foreign-controlled

Tax

/Ass

ets

Tax Reforms, Debt Shifting and Corporate Tax Revenues 31

TABLE 3The Simplified Income Statement for the Illustrative Example

Case 1 Case 2 Case 3 Net Impact

In CanadaTotal income before interest and taxes $300 $300 $300 $0 (interest paid to a Canadian lender) ($105) ($105) ($105) $0 (interest paid to U.S. parent) $0 $0 ($35) $35