Embed Size (px)

Citation preview

1Akauntan NasionalDecember 2002

F R O M T H E E D I TO R

CONTRIBUTION OF ARTICLES

The Akauntan Nasional welcomes original and previously unpublished contributions which are of inte-rest to accountants, executives and scholars. Manuscripts should cover domestic or international accountingdevelopments. Lifestyle articles of interest to accountants are also welcomed.

Manuscripts should be submitted in English or Bahasa Malaysia and range from 2,500 to 5,000 words(double-spaced, typed pages). They should be submitted in hardcopy and diskette (3.5 inch) form in MicrosoftWord or Lotus Wordpro. Manuscripts are subject to a review procedure and the Editor reserves the right tomake amendments which may be appropriate prior to publication.

Letters to the EditorA key element in the world of publishing is what readers have to say.

We want to hear from you on just about anything that appears ineach issue of Akauntan Nasional. Why not drop us a line now?

1967

AKAUNTAN MALAYSIAINSTITUT

The Malaysian Institute of Accountants is a statutorybody set up under the Accountants Act, 1967 to regulateand develop the accountancy profession in Malaysia.

The functions of the Institute are, inter alia :

(a) To regulate the practice of the accountancyprofession in Malaysia;

(b) To promote in any manner it thinks fit, the interestsof the accountancy profession in Malaysia;

(c) To provide for the training and education by theInstitute or any other body, of persons practisingor intending to practise the profession;

(d) To determine the qualifications of persons foradmission as members; and

(e) To approve, regulate and supervise the conduct ofthe Qualifying examination.

MIA COUNCIL

PRESIDENTAbdul Samad Haji Alias (Dr.)

VICE-PRESIDENT Wong Mun Sum, Albert

ACCOUNTANT-GENERALYBhg. Datuk Siti Maslamah bt. Osman

Y.M. Raja Dato' Seri Abdul Aziz Raja Salim; Datuk Nur Jazlanbin Tan Sri Mohamed; Dato' Abdul Halim Mohyiddin; Dato'Lee Ow Kim; Dato' Nordin bin Baharuddin; Dato' Syed AminAl-Jeffri; Prof. Dr. Takiah bt. Mohd Iskandar; Prof. Madya Dr.Mohamad Ali bin Abdul Hamid; Prof. Madya Dr. Nafsiah bt.Mohamed; Prof. Madya Dr. Noorhayati bt. Mansor; Prof.Madya Dr. S. Susela Devi Selvaraj; Abdul Rahim bin AbdulHamid; Beh Tok Koay; Lam Fu Wing; Lam Kee Soon; LiewLee Leong, Raymond; Manjeet Singh s/o Santokh Singh; MohdNor bin Ahmad; Muhammad Ibrahim; Tuan Haji Muztazabin Mohamad; Nazlan Ozizi bin Ibrahim; Nik MohdHasyudeen bin Yusoff; Quek Jin Fong; Sudirman bin Masduki;Yeo Tek Ling; Zahrah bt. Abdul Wahab Fenner.

REGISTRARMohammad bin Abdullah

EXECUTIVE DIRECTORHo Foong Moi (Ms)

EDITORIAL BOARD

COMMITTEE : Raymond Liew, Chairman; Assoc. Prof.Dr. Jeyapalan Kasipillai; Chia Kum Cheng; Ghazalie Abdullah;Zahrah Abd Wahab Fenner; YM Raja Datuk Seri Abdul AzizRaja Salim; Prof. Madya Dr. Nafsiah Mohamed; Lam KeeSoon; Sudirman Masduki; Adelena Lestari Chong; TongChin Hoo

EDITORIAL TEAM : Iszudin Mohd Amin (Editor),Nirmala Ramoo (Asst. Manager), Rosliani Shafie(Communications/Admin. Assistant.)

PUBLISHING CONSULTANTExecutive Mode Sdn Bhd (317453-P)Tel : 03-7118 3200, 3205, 3230 Fax : 03-7118 3220e-mail : [email protected] : http://www.executivemode.com.my

PRINTERUltimate Print Sdn Bhd (62208-H)40 Jalan Penchala, 46050 Petaling JayaTel : 03-7787 5688 Fax : 03-7787 5609

PUBLISHED BYMalaysian Institute of AccountantsRegistered Office and AddressDewan Akauntan2 Jalan Tun Sambanthan 3, Brickfields50470 Kuala LumpurTel : 03-2279 9200 Fax : 03-2274 1783, 2273 1016e-mail : [email protected] : http://www.mia.org.my

Malaysian Institute of Accountants(Established under the Accountants Act, 1967)

AN

After decades of working quietly behind the sceneS, accountants who have been stereo-typed as boring bean counters suddenly found themselves shot into the public spotlightthis year. But it was publicity they neither desired nor sought. In the explosion of corpo-

rate scandals at giants like Enron and Worldcom, accountants were portrayed by the media asthe villains of the corporate world and accused of cooking the books.

The repercussions of these developments have been felt worldwide, and the accounting pro-fession in Malaysia has not been spared. Many questions have been raised about the ethicalconduct of accountants in commerce and industry as well as the profession as a whole. Much ofthe criticism centred on the perceived failure of accountants and external auditors to dischargetheir fiduciary responsibilities competently and to demonstrate the highest ethical practices.The accounting profession suffered serious damage to its reputation

But what got lost in all the publicity is the fact that it is an honourable profession bound by ethicsand morals. To be fair to accountants, the critics failed to focus on the internal factors as well as tounderstand how the process of financial disclosure is done. One of the primary misconceptionsprevalent, including within the Malaysian corporate sector and the media, is that the company’sexternal auditor is responsible for the financial statements of the company. If we go beyond themedia frenzy, a different picture emerges; the collapse of some of America’s corporate entities canbe blamed on a cast of characters. It is a corporate drama that has more than one villain.

As part of the corporate financial reporting team, accountants must always remember thatwe are the guardians of truth, fairness and due-diligence standards. To look at due diligencemerely as a compliance responsibility to fulfil legal obligations would be missing the point; duediligence practices should bring about higher professional standards, greater disclosure ofinformation and more accurate representations, without which the integrity of our professionwill be seriously undermined.

The core of a transparent and accountable corporate sector is the commitment to ethicalbehaviour by everyone involved in the financial reporting framework.

Future opportunities for the accounting profession depend very much on the maintenance ofpublic confidence. The profession has reached a critical period, being under constant publicscrutiny. This critical atmosphere should be understood by the accountants who must adjusttheir approach and attitude to it if their worthwhile contribution to society is to be maintainedand strengthened.

The task of upholding the reputation and well-being of the profession should not be left onlyto the Malaysian Institute of Accountants (MIA) but shared by all members equally. Upgradingthe code of ethics for accountants is but one way to attain this goal. More importantly, profes-sional survival must also rest on continuous educational training programmes.

Under such circumstances, the Institute with its vision of becoming ‘a globally recognisedand respected business partner committed to nation building’ has increased its efficiency andspeed to respond with flexibility to changes in the industry. In particular, we have bolstered ouroperations, improved our services, enhanced our Information Technology capabilities, as wellas strengthened our public relations activities. In short, we have strengthened our foundationfor service with excellence, while demonstrating MIA’s unique professionalism.

Over the next few years, it is expected that global competition will accelerate at an evengreater pace, due to many changes in business conditions, especially in the wake of globalisation.With the mission ‘to develop, support and monitor quality and expertise consistent with globalbest practice in the accountancy profession for the interest of stakeholders’ our focus will be ontaking the profession’s global expansion to a new level, by capitalising on members’ commit-ment, while achieving increased competitiveness in quality, cost and delivery.

As the year draws to a close, let us put our actions this year in perspective and act upon ourshortcomings, so that we are ready to take on the challenges of the future, a little wiser, a littlebolder.

Merry Christmas and A Happy New Year.

Editor

Accountants Speak Up

2 Akauntan Nasional December 2002

From the Editor

Notice to Practising Members

C O V E R

MIA Practice Review : Setting HighProfessional Standards

Statement on Practice Review,Review Procedures and Conduct ofMembers

Summary of Practice ReviewProcedures

M A N AG E M E N T A C C O U N T I N G

The BCP Budget and Business ImpactAnalysis

It’s Time Local Companies CameClean on Their EnvironmentalRecord

B U S I N E S S & A C C O U N T I N G

The Role of the Chief Financial Officerin 2010

Dividend Policy : Does it Matter?

Strategic Planning of AdvancedManufacturing Technology

TA X AT I O N

The Assessability of Interest Incomeas a Business Source

M A N A G E M E N T

Reviving Entrepreneurship in YourBusiness

K-Accountants — A HumanResource Perspective

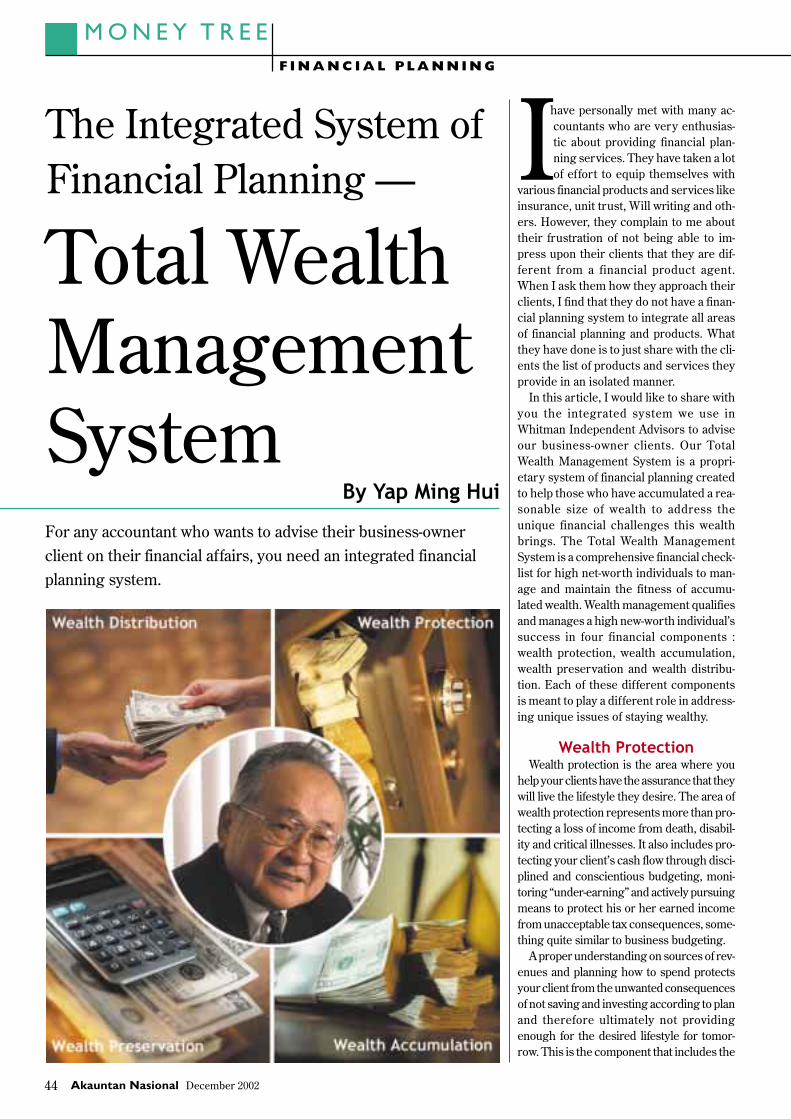

M O N E Y T R E E

The Integrated System of FinancialPlanning — Total WealthManagement System

B U S I N E S S W AT C H

Doing Business in the USA (Part 2)

I N T E R N AT I O N A L

IFAC Technical News

FASB & IASB Technical News

T R AV E L A N D L E I S U R E

Seoul’s Old and New

B E T T E R L I F E

Good Posture Prevents Backache

I N S T I T U T E N E W S

Penang Branch News

Sabah Branch News

Sarawak Branch News

MAAA News

C O L U M N S

Malaysian CFOs Have GreatestConcerns Over Non-Executives,Survey Shows

CIMA Graduation Joy

M E M B E R S ’ U P D AT E

MIA Resource Centre

Request for Address Update

Registration of Accountants

Readmission of Accountants

Reclassification of Accountants

Resignation of Accountants

CPE Calendar

1

3

4

7

13

16

22

24

26

30

34

40

41

44

The Akauntan Nasional is the official publication of the Malaysian Institute of Accountants (MIA) and is distributed to all members of theInstitute. The views expressed in this journal are not necessarily those of the MIA or its Council. Contributions including letters to the Editor andcomments on articles appearing in the journal are welcomed and should be sent to the Editor as addressed below. All materials appearing in theAkauntan Nasional are copyright and cannot be reproduced in whole or in part without written permission from the Editor.

Editor, Akauntan NasionalDewan Akauntan, 2 Jalan Tun Sambanthan 3, Brickfields, 50470 Kuala Lumpur, Malaysia

Tel : 03-2279 9200, Fax : 03-2274 1783, e-mail : [email protected] Homepage : http://www.mia.org.my

Seoul’s Old and New Pg 52

CONTENTSVolume 15, Number 11 DECEMBER 2002

The BCP Budget andBusiness Impact Analysis

Pg 16

46

48

51

52

54

56

57

58

60

62

63

64

64

65

67

67

67

68

The Role of the CFO in 2010Pg 24

3Akauntan NasionalDecember 2002

1967

AKAUNTAN MALAYSIAINSTITUT

VISION ANDMISSION

MIA’s Vision

• To be a globally recognised

and respected business

partner committed to

nation-building

MIA’s Mission

• To develop, support and

monitor quality and expertise

consistent with global best

practice in the accountancy

profession for the interest

of stakeholders

Malaysian Institute of Accountants(Established under the Accountants Act, 1967)

MIA BRANCHES

State : JohorLocation : Johor BahruChairman : Soh Siong Hoon, Sam

State : MelakaLocation : MelakaChairman : Lee Hin Kan

State : Negeri SembilanLocation : SerembanChairman : Chan Siew Tong

State : PahangLocation : KuantanChairman : Foo Tui Lee, Joseph

State : PenangLocation : PenangChairman : Teh Eng Hin, Steven

State : PerakLocation : IpohChairman : Soo Yuit Weng

State : SabahLocation : Kota KinabaluChairman : Alexandra Thien

State : SarawakLocation : KuchingChairman : Tiang Kung Seng, David

MIA CENTRES

State : Kedah & PerlisLocation : Alor SetarChairman : Por Lee Tee

State : KelantanLocation : Kota BahruChairman : Billy Kang

State : TerengganuLocation : Kuala TerengganuChairman : Su Lim

NOTICE TO PRACTISING MEMBERS

AN

AN

SMP. The good news about this ERP scheme is

that it allows various SMPs to come togetherto offer a tailored scheme to the respectivegroup of employees coming from differentpractices with minimum outlay but maximumpotential.

Besides financial incentives, the scheme alsooffers a free RM25,000 accidental death insur-ance coverage to seven employees for everyRM20,000 invested.

b Professional IndemnityInsurance (PII)

We have also invited a broker from State In-surance Broker Sdn Bhd to come and sharewith our practitioners on the various factorswhich should be considered when buying Pro-fessional Indemnity Insurance. Since 1998, ourInstitute has made it mandatory for all practi-tioners (both audit and non-audit) to have aminimum coverage of at least RM100,000 perpartner per practice.

EVENING TALK —INNOVATION SHOWCASE

As part of the innovation within the local ac-countancy profession, member firms are in-

vited to submit to the Practice Matters Depart-ment of the Institute, various innovative propos-als and schemes for the benefit of other practi-tioners or MIA members in commerce and in-dustry for our consideration. It can be in theform of new products or services that have al-ready been commercialised or are in the pro-cess of commercialisation. Once your innovativeproposal or scheme is accepted, it will be allowedto be demonstrated to fellow practitioners orother MIA members on a ‘free of charge’ basisat any one of our future evening talkprogrammes. Submission should be made toJohnny Yong (e-mail : [email protected]) fromthe Practice Matters Department with as muchdetails as possible to enable the Institute to makean informed decision. At minimum, the follow-ing information must be made available :

a) A synopsis of the proposal and/or scheme;

b) The possible benefits to the community andbusinesses;

c) Member’s name and contact details;

d) Firm’s name and contact details;

e) MIA membership number;

f) Ownership and claims of rights for the prod-ucts or services must be disclosed up-front.

CLARIFICATION ONSUBMISSION OF THE

ACCOUNTANTS’ REPORTFOR SOLICITOR’S

CLIENTS ACCOUNTSFur ther to our Notice in Akauntan

Nasional on Solicitor’s Clients Accounts, wewish to inform members of the following :

The Bar Council, in its letter to our Insti-tute dated 27 October 2002 (Ref.: BC/S/30/2002) clarified that, so long as solicitorshave branch offices of their practice/firmlocated in Peninsular Malaysia, they arerequired to submit the Accountants’ Reportfor their clients’ accounts irrespective ofwhether the clients’ accounts are operatedin East Malaysia only.

CALLING ALLPRACTITIONERS IN THE

KLANG VALLEY

As per our earlier announcement, we arelaunching our first evening talk for 2003

in the Klang Valley on 10 January (Friday). Thetalk will be held at the Main Boardroom,Dewan Akauntan, 2 Jalan Tun Sambanthan 3,Brickfields, Kuala Lumpur. It is scheduled tostart at 5.00 p.m. Members are required toregister with Janet Leong at Ext. 250 or SharonKoh at Ext. 125.

For the first in the series of evening talks,we are going to cover the following topics :

a Employee RetentionProgramme (ERP)

It is very common for small and medium-sized practices (SMPs) to suffer from highstaff turnover. Apart from the fact that somestaff may not see much potential in the SMPsdue to the limited scope for possible expan-sion, the lack of a financial incentive schemeto attract the staff’s loyalty could be anotherreason for such a vicious circle. For this pur-pose, fellow practitioners, especially from theSMPs sector should come forward and findout how an ERP programme can be imple-mented in the practice as a form of financialrewards for their loyal employees. We are for-tunate to get an expert from BHLB PacificTrust Management Bhd and its agent HazelOng to explain how unit trust can be used as aflexible instrument to retain employees of a

4 Akauntan Nasional December 2002

C O V E RP R AC T I C E R E V I E W

Through our involvement with the Inter-national Innovative Network (please seethe article in January/February 2003 issueof Akauntan Nasional), members in pub-lic practice may eventually be able to mar-ket their products and services in overseasmarkets through the local accountancyorganisation.

DEVELOPINGCONFIDENCE THROUGH

PUBLIC SPEAKING

Whether a practitioner is negotiatingan increase in his chargeable fees

with a difficult client or having to do a busi-ness presentation with the hope of secur-ing an important consultancy engagement,the ability to speak with confidence is ofparamount importance. On another level,an individual who is being interviewed fora new job also needs to outshine his poten-tial rivals in the department of confidence,all things being equal. And one of the sur-est ways to develop your confidence in frontof your clients and other VIPs is to masterthe skill of public speaking. It has beenquoted that people would prefer death thanto speak in public. However, public speak-ing like any other skill can be developed.For this reason, the Institute would like togauge members, especially the practitio-ners’ interest in this area. We will beorganising a series of ‘demo’ meetings atthe Institute’s premise to determine if thereis a need to cater for a special interest groupin public speaking. Members in Klang Val-ley are invited to join our first few demomeetings as scheduled below :

a) 6 March 2003 (Thursday) ;

b) 20 March 2003 (Thursday) ; and

c) 3 April 2003 (Thursday).

All meetings will start at 6 p.m. and willend at about 8.30 p.m. Should there beenough members keen in this area, thenthe Institute will consider setting up thisspecial group to promote the art of pub-lic speaking. Registration can be madethrough Sharon Koh at Ext. 125 (e-mail :[email protected])

Participation in the demo meeting isfree of charge and all sessions will carrytwo CPE hours.

AN

AN

Come 1 January 2003, theMalaysian Institute ofAccountants (MIA) willimplement the PracticeReview Programme that

will change the realm of public practice forall auditors in Malaysia. This initiative isnot new, having been on the drawing boardsince 1998, but recent events both locallyand internationally have fast tracked itsimplementation. The Institute believes thatthe launching of this important initiativeto cover all audit firms registered with it istimely and relevant in light of develop-ments in the international arena.

Since its activation in 1987, the Institutehas exercised its regulatory role through theinculcation of the ethical and professionalpractice of accountancy by continuous andlifelong education programmes as well asthrough the initiation of disciplinary proceed-ings against unethical members pursuant tothe powers conferred under the AccountantsAct, 1967. The Institute has since expandedits regulatory role, initially through the es-tablishment of financial statements reviewsand now, through the Practice Review.

What is Practice Review? To understandthe concept of Practice Review, we need torecognise the concept of auditing. In broadterms, auditing is a systematic process of

MIA Practice Review :

SETTINGHIGHPROFESSIONALSTANDARDSAudit firms are to be subject to practice review from 1 January2003. The move is aimed at maintaining, applying and observingstandards of the local auditing profession.

objectively obtaining and evaluating evi-dence on assertions about an entity’s eco-nomic actions and events. It ascertains thedegree of correspondence between thoseassertions and establishes the criteria andcommunicates the results to interested us-ers. Users of financial statements in mostcircumstances will not have access to first-hand knowledge about the entity and thus,depend on the opinions of independent au-ditors to give justified credibility to finan-cial statements. As such, the quality of anaudit is fundamental to ensure that accurate,complete and unbiased audited statementsare used for decision making by the users.Just as auditing is carried out in companiesto determine the state of their finances andoperating procedures, Practice Review is aprocess in which the activities of a practis-ing accountant are reviewed by anotherqualified member within the profession.Specifically, it is a process where the stan-dards and procedures of a member’s audit-ing practice are assessed by an independentmember of the same profession.

Impor tantly, the objective of thisProgramme is 3-pronged :(a) Firstly, to confirm members’ obligation

to follow the standards promulgated bythe Institute;

(b) Secondly, to undertake the regulatory

5Akauntan NasionalDecember 2002

role as provided under the AccountantsAct, 1967 as well as to be aligned withsome of the latest international devel-opments; and

(c) Thirdly, to enhance the confidence ofthe business community in our mem-bers’ standard of professional work.

Since August this year, various forumsinvolving members from different stateshave been conducted to enable them to of-fer their views in respect of the PracticeReview Programme. It is indeed encourag-ing to note that a significant number of mem-bers clearly see the value of implementingthis quality assurance programme.

The Practice Review Programme is a pro-active measure, which is intended to ensureall audit firms registered with MIA operateat least to the required minimum standards.It has to be pointed out that no new opera-tional and/or auditing standards are beingimplemented following the introduction ofPractice Review. Since the standards ex-

process that has led to significant fee de-pression) can be effectively addressed andrectified. By eliminating such illegal prac-tices, the Institute believes that its bona-fidemembers in public practice who operatetheir practices in accordance with the re-quired standards will eventually be able togenerate reasonable returns in terms of feesin their auditing practices. In addition, on15 November 2002, the Council approvedthe By-Law on Quality Assurance and Prac-tice Review as well as the Statement on Prac-tice Review, both of which have been dis-seminated to members. With a definitiveframework in place, the Institute is ready toset up a Practice Review Department. Apartfrom engaging in-house reviewers, the In-stitute will appoint suitably qualified practi-tioners to a panel of reviewers who will actas the Institute’s sub-contracted reviewersalongside those installed within the Prac-tice Review Department. A charge-out ratewill be imposed on the audit firms and basedon earlier estimates, a charge-out rate of RM200 per hour (still estimated only) is con-sidered as reasonable bearing in mind thatthe cycle of review is once every five years.

A Practice Review Committee (PRC) com-prising experienced practitioners has beenestablished to oversee the implementationprocess of the Practice Review Programme.Apart from Council members Dato’ NordinBaharuddin and Lam Kee Soon, who is alsochairman of the PRC, six non-Council mem-bers from large, medium and small firmshave been appointed to the PRC, whichwould be expanded in the future.

For details of the By-Law on Quality As-surance and Practice Review as well as theStatement on Practice Review, members ofthe public can download this informationfrom the Institute’s website atwww.mia.org.my. The PRC will be makingthe necessary disclosure on the detailedprocedures and processes of the PracticeReview Programme upon implementationthereof with effect from 1 January 2003.Further information will be released by thePRC from time to time. To date, the Insti-tute has held several talks in Kuala Lumpurfor members to explain the implementationprocess of Practice Review and to helpclear their doubts. The Institute plans tohold a series of similar talks in other statesin the near future.

pected of our members have always beenthere, the process of Practice Review is moreof a validation process undertaken by MIA.For firms which are found to be operating ata less than satisfactory level, the educationalside of this programme will help these firmsto improve their quality of work so as to raisestandards to that of the Institute’s minimum.This is an appropriate approach to generalrisk management within the auditing profes-sion. The commitment of the Council of MIAto the educational facet of the Practice Re-view programme is thus understandable. Inthe various forums with members, the inten-tion of the Institute to complete at least theinitial cycle of reviewing all firms within thenext five years with the emphasis on educat-ing members in public practice, has been wellreceived.

The Council of MIA foresees that throughthis programme, instances of MIA memberscollaborating with unqualified persons of-fering accounting and auditing services (a

AN

6 Akauntan Nasional December 2002

C O V E R

BY-LAW B-11 : QUALITY ASSURANCE AND PRACTICE REVIEW

Inserted : 15 November 2002; With ef fect from : 1 January 2003

B-11.1Every member in public practice shall ensure that hisfirm complies with all relevant professional standardsfor the purposes of assurance as to the quality of thepublic practice services provided by his firm whetherthrough himself, his partner(s) and/or his employees.In doing so, every member in public practice shallensure that his firm adopts and applies policies andprocedures designed to maintain adherence to pro-fessional standards.For the purposes of this by-law, the professional stan-dards required to be maintained, observed and ap-plied by a member in public practice to the extentapplicable to the type of public practice services pro-vided by that member or his firm, include:

(a) all standards and statements of professional conductand ethics in the form of the Institute’s By-Laws (OnProfessional Conduct & Ethics) in issue from time totime;

(b) all approved standards whether issued by the Councilor otherwise, and all guidelines, statements and/orcirculars of best practices issued or prescribed by theCouncil and/or the Institute from time to time.

B-11.2

All members in public practice and/or member firmsshall submit to the Institute’s Practice Reviewprogramme as established by the Council pursuant tothe Council’s Statement on Practice Review issued on15 November 2002 together with its supporting ap-pendices.Explanatory Note :

(i) The objectives of the Practice Review programme are :(a) to ensure that all members in public practice main-

tain, observe and apply the relevant professional stan-dards, so as to assure that those members in publicpractice, their firms and their employees are compe-tent, ethical, and exercise due professional care intheir professional work;

(b) to assist members in public practice to improve theirprofessional standards where necessary; and

(c) to identify areas where members in public practicemay require assistance in maintaining and observingprofessional standards.

(ii) The Practice Review programme does not set new pro-fessional standards. Rather, the professional standardsthat the members in public practice and/or their firms

are expected to maintain are those already pre-scribed by the Institute and which are summarisedfor convenience in by-law B-11.1(3) above.The Practice Review programme shall be conductedby the Institute through its Practice Review Com-mittee in accordance with the Statement on Prac-tice Review issued on 15 November 2002 with itssupporting appendices, any other directions issuedby the Council from time to time and in accor-dance with any other procedures and processes asmay be determined by the Practice Review Com-mittee.Each member in public practice and/or his firm shallcomply with the requirements contained in theStatement on Practice Review issued on 15 Novem-ber 2002 with its supporting appendices, any otherdirections issued by Council from time to time andwith any other procedures or requirements imposedby the Practice Review Committee for the purposesof carrying out the practice review pertaining tothat member’s firm.The Practice Review programme shall initially beconducted over a cycle of not more than five yearsin respect of member firms which are selected atrandom from the Institute’s records.Each member in public practice and/or his firmshall settle in full, the fees if any, in respect ofthe practice review conducted pertaining to hisfirm including any interim fees, as may be chargedand determined by the Practice Review Commit-tee for his firm. Such fees shall be due and pay-able within 30 days of the date of the bill raisedfor this purpose.

Explanatory Note :(i) The fees, if any, that are charged for the practice

review shall be based on hourly rates as approvedby the Council on the recommendation of the Prac-tice Review Committee.

(ii) The fees, if any, that are charged for the practicereview, shall be in respect of the time involved inthe planning, execution and reporting of the prac-tice review.

B-11.3

This by-law shall, unless otherwise determined bythe Council, only operate in respect of members inpublic practice and/or member firms who provideamong others, audit services.

1

2

3

1

2

3

4

5

7Akauntan NasionalDecember 2002

STATEMENT ON PRACTICE REVIEW

Review Procedures andConduct of Members

(Issued 15 November 2002)

1

2

3

4

5

6

7IntroductionParagraph (c) of Section 6 of the Accountants Act, 1967 (the

“Act”) provides for the Institute, as one of its objectives, to regulatethe practice of the profession of accountancy in Malaysia. Paragraph(f) of Section 6 of the Act further states that the Institute shall begenerally able to do such acts as it thinks fit for the purpose ofachieving its objectives, including that of regulating the profession.

In pursuance of the above, the Council of the Institute herebyissues this Statement on Practice Review for the purposes of imple-menting a practice review programme applicable to all membersin public practice as defined pursuant to the Rules and the By-Laws of the Institute.

The objective of the practice review programme is to ensure thatall members in public practice maintain, observe and apply the rel-evant professional standards. Primarily, the practice review programmeis intended to be educational and to help members in public practiceimprove their professional standards where necessary. Essentiallythrough a review of current engagement files, the practice reviewprogramme will identify areas where a member in public practice mayrequire assistance in maintaining professional standards.

The practice review programme does not set new standards.Rather, the standards that the member in public practice is expectedto maintain are those already prescribed by the Institute pursuantto the Act, the Rules and the By-Laws of the Institute including allethical standards in the form of the Institute’s By-Laws (On Profes-sional Conduct and Ethics), auditing standards in the form of theMalaysian Approved Standards on Auditing as well as the variousguidelines issued by the Institute in the form of RecommendedPractice Guides (RPG) and statements and circulars on best prac-tices issued by the Institute from time to time.

This Statement and its supporting appendices set out the con-duct and procedures of the practice review programme in gen-eral terms. This Statement also provides details of the require-ments of the practice review programme, what is expected of amember during the conduct of a practice review, and a brief de-scription of the practice review process.

This Statement comes into operation on 1 January 2003 andunless otherwise stated by the Council of the Institute, shall onlyoperate in respect of members in public practice and/or memberfirms who provide, among others, audit services. Compliance withthe requirements in this Statement is mandatory.

Definition of termsMember in public practice — a chartered accountant who, as asole proprietor or in a partnership, provides or is engaged in publicpractice services (as defined in the Malaysian Institute of Accoun-tants (Membership & Council) Rules 2001) in return for a fee orreward for such services otherwise than as an employee, and holdsa valid practising certificate. For the purpose of this Statement,this includes a member firm.

Practice review —9in relation to a member firm, means an exami-nation or review undertaken pursuant to this Statement and thesupporting appendices to determine whether professional standardsare being or have been observed, maintained and applied.

Practice Review Committee —9a committee established by theCouncil of the Malaysian Institute of Accountants (the Institute) toconduct practice reviews to determine whether professional stan-dards have been maintained, observed and applied.

Member firm —9for the purpose of this Statement, a firm of char-tered accountants where the sole-proprietor or all the partnersare members of the Institute, which is registered with the Insti-tute and which offers among others, audit services.

Professional standards — all those professional standards that arerequired to be maintained, observed and applied by members inpublic practice from time to time, and which are for the purposesof this Statement, set out in paragraph 11 below.

Reviewer —a. A member of the Institute who is appointed or engaged as an

employee by the Institute for the purpose of carrying out prac-tice reviews;

b. A member of the Institute having a valid audit licence and practis-ing certificate who is appointed to the Panel of Reviewers by theRegistrar for the purposes of carrying out practice reviews; and

c. Any other expert as the Practice Review Committee deems fitand who is appointed on an ad hoc basis to carry out the as-signment of practice reviews or any part thereof.

Practising certificate 9—the practising certificate issued pursuantto Rule 9 of the Malaysian Institute of Accountants (Membership &Council) Rules 2001.

Panel of Reviewers —9any member of the Institute having a validaudit licence and practising certificate, who is not an employee ofthe Institute and who has since been appointed by the Registrar tosuch a panel for the purposes of carrying out practice reviews onbehalf of the Institute.

8 Akauntan Nasional December 2002

C O V E R

ScopeMembers subject to review

All members in public practice offer-ing audit services are required to adhereto the standards prescribed by the Insti-tute. All members in public practice and/or member firms so engaged, must thussubmit to practice review, subject to para-graph 9 below.

ExemptionWhere a member in public practice

holding a practising certificate completesa declaration in prescribed form certifyingthat he/she is not engaged in public prac-tice services in so far as it pertains to auditengagements during the preceding 12months and does not intend to so practisefor the foreseeable future, or that he/shewill be discontinuing public practice in sofar as it pertains to audit engagements inthe immediate future (a maximum of threemonths from the random selection date),he/she may be exempted from practicereview at the discretion of the PracticeReview Committee.

Establishment and appointment ofPractice Review Committee

The Council of the Institute has man-dated the establishment and compositionof the Practice Review Committee to over-see the conduct of practice review as fol-lows :

a. The Practice Review Committee shallconsist of such number of members,being not less than 8, as the Councilshall determine and of whom, not morethan 2 shall also be members of theCouncil.

b. All the members of the Practice ReviewCommittee shall be members of theInstitute and a majority of them musthold a valid practising certificate andan audit licence currently in force.

c. A person shall not be a member of thePractice Review Committee and theInvestigation and Disciplinary Commit-tees as well as the Disciplinary AppealBoard at the same time.

d. The quorum for any meeting of thePractice Review Committee shall not beless than half of the total number of

members of the Practice Review Com-mittee for the time being.

e. The Practice Review Committee mayappoint sub-committees of its membersand may delegate to any such sub-com-mittee, with or without restrictions, anyof its functions or powers except thepower to make a complaint against amember in public practice or a mem-ber firm to the Investigation Commit-tee.

f. Members of the Practice Review Com-mittee are not eligible to be appointedto the Panel of Reviewers and vice-versa.

g. The Chairman of the Practice ReviewCommittee shall be a Council Memberof the Institute with a valid practisingcertificate and audit licence.

h. Subject to the provisions, if any, underthe Accountants Act, 1967 and any di-rections issued by the Council fromtime to time including those containedin this Statement and supporting ap-pendices, the Practice Review Commit-tee or any sub-committee thereof mayregulate its own procedures and pro-cesses as it thinks fit.

Directions of CouncilProfessional standards

The Council has from time to time, is-sued or specified the professional stan-dards which are to be maintained, ob-served and applied by members in publicpractice who offer, among others, auditservices. These professional standardsform the subject matter of the Institute’spractice review programme as herein con-tained. Practice review however, does notseek to redefine the scope and authorityof these professional standards but ratherseeks to enforce them within the param-eters so specified. For the time being andfor the purposes of this Statement, the pro-fessional standards which will be examinedunder practice review are as follows :a. all standards and statements of profes-

sional conduct and ethics in the formof the Institute’s By-Laws (On Profes-sional Conduct & Ethics) in issue fromtime to time, in so much as these ethi-cal standards and statements relate to

the conduct of audit engagements and/or that of the member firm;

b. all standards and statements of ac-counting in the form of the approvedstandards and pronouncements issuedby the Malaysian Accounting Stan-dards Board (MASB) from time to timein so far as significant departures there-from may affect the requirement for fi-nancial statements to give a true andfair view; and

c. all approved auditing standards, andguidelines and statements of best prac-tices in issue from time to time. Thiswill also include recommended prac-tice guides (RPG), statements andcirculars issued in relation to audit en-gagements and the practices of a mem-ber firm.

ScopeThe Council has directed the Practice

Review Committee to conduct practice re-views pursuant to this Statement and itssupporting appendices, in order to deter-mine that the professional standards speci-fied in paragraph 11 above are observed,maintained and applied by all memberfirms, subject to paragraph 9 above.

Extent of powersPractice reviews will be performed by

reviewers employed by the Institute and/or those who have been appointed to thePanel of Reviewers by the Registrar. In or-der to ensure proper administration of thepractice review process, the Practice Re-view Committee is allowed to exercise itsfull powers as provided in this Statementand pursuant to any other directives issuedby the Council without restriction.

Panel of ReviewersA Panel of Reviewers will be estab-

lished by the Institute to undertake thefunction of practice review in addition tothe reviewers so employed by the Instituteto conduct practice reviews. A person whois a member of the Institute and who holdsa valid audit licence and practising certifi-cate shall be eligible to be appointed to thePanel of Reviewers subject to the follow-ing provisions :

8

9

10

11

12

13

14

9Akauntan NasionalDecember 2002

a. The person must have successfullypassed an interview process conductedby the Practice Review Committee andsubsequently been recommended tothe Registrar by the Practice ReviewCommittee to be appointed to the Panelof Reviewers.

b. A person shall not be a member of thePanel of Reviewers and the Investiga-tion and Disciplinary Committees aswell as the Disciplinary Appeal Boardat the same time.

c. The tenure of the panel member shallnot be for a continuous period of morethan three years from the date of hisor her first appointment to the panel.Subsequent appointments cannot ex-ceed a continuous period of more thanthree years from the date of his or hersubsequent appointment.

d. A person currently under investigationby the Institute’s Investigation Commit-tee is not eligible to be appointed to bea member of the said Panel of Review-ers. An existing panel member who hasreceived a notice of complaint in re-spect of such an investigation must re-sign from the Panel of Reviewers assoon as practicable but in any event,within one month from the date thenotice of complaint is served on him/her at his/her last known registeredaddress with the Institute.

e. Each member of the Panel of Review-ers must undergo the process of prac-tice review within a year of his or herfirst appointment to the panel. Al-though member firms are selected ona random basis, the person who sits onthe Panel of Reviewers shall volunteerhis or her firm for the practice reviewwithin 6 months after the expiry of thefirst year of his or her appointment tothe Panel of Reviewers should his orher firm fail to be selected under thenormal random selection process.

f. The appointment to the Panel of Re-viewers must be validated by a letterof appointment signed by the Registrar.

g. All appointments to the Panel of Re-viewers shall automatically lapse on 31December of each calendar year unless

a letter of re-appointment issued underthe hand of the Registrar is sent to thepanel member’s last known registeredaddress with the Institute one monthor earlier before the expiry date of 31December of that calendar year.

h. As stated in paragraph 10 of this State-ment, a person cannot be a member ofthe Practice Review Committee and thePanel of Reviewers at the same timeand vice -versa.

i. Subject to sub-paragraph d. above, anadvance notice of one month should begiven to the Registrar prior to any res-ignation from the Panel of Reviewers.Any notice period of less than onemonth shall be accepted at theRegistrar’s own discretion.

Conduct of Practice ReviewsObjective

Essentially, a practice review entails,among other things, a review of currentaudit engagement files and related finan-cial statements to ascertain that the mem-ber firm is adhering to professional stan-dards. Where a member firm is not fol-lowing professional standards in certainsituations, suggestions and recommenda-tions for improvement may be made, andpossibly followed by a further review, inkeeping with the educational thrust ofpractice review. The number of currentaudit engagement files to be revieweddepends on:

a. The degree of reliance, if any, to beplaced on internal quality controls ofthe member firm; and

b. The size of the member firm being se-lected for review.

A summary of the practice review pro-cedures designed to meet the above objec-tive is contained in Appendix A herein.

Selection of member firms for reviewThe Registrar will randomly select

member firms for review and will deter-mine the order of review. A member firmwill not be selected until at least 18months have elapsed since the com-mencement of the member firm basedon the Institute’s records.

Upon the selection of the member firmto undergo the practice review process, themember firm will be duly notified within aweek in writing via registered post by theInstitute. The member firms will be givenan option to decide whether they wouldprefer to be reviewed by a reviewer em-ployed by the Institute or by a member ofthe Panel of Reviewers.

The member firm thus selected willhave to respond to the Registrar in writingwithin two weeks from the date of notifica-tion of selection as to which of the optionsthe firm intends to exercise. Once this op-tion is exercised, it cannot be reversedunless otherwise allowed by the Registraron the recommendation of the PracticeReview Committee.

In cases where a response to theInstitute’s notification of selection is notreceived within the stipulated time frame,the Registrar can proceed to assign suchreviewer at his discretion to the memberfirm that has been selected for the prac-tice review process.

The identity of the member firm shallbe kept confidential from all parties includ-ing the Practice Review Committee andthose staff of the Institute not directly in-volved in practice review, save for thoserelevant reviewers or members of thePanel of Reviewers (as the case may be)who are directly involved in the review ofthat member firm.

Where the member firm selected hasbranch offices or associated practices un-der more than one name, in so far as pos-sible, the practice review will be conductedto cover all these branches or associatedpractices at the same time. Members inpublic practice should ensure that the In-stitute is aware of all modes of practiceconducted by them in order that this canbe facilitated.

NotificationsMember firms will be notified by letter

as to whether their selected option hasbeen accepted. The option for reviewwhether by a reviewer employed by theInstitute or by a member of the Panel ofReviewers will be clearly stated in the no-

15

16

17

18

19

20

21

22

10 Akauntan Nasional December 2002

C O V E R

tification letter. In the latter case, thename of the member of the Panel of Re-viewers who has been appointed to dothe review as well as the firm which he/she is currently practicing under will bementioned in the notification letter. En-closed with the notification letter will bea Practice Review Questionnaire (theQuestionnaire). The member firm shouldcomplete the Questionnaire and returnthe same through the member firm’sdesignated practitioner (the sole practi-tioner, the senior partner or other part-ner designated as responsible for prac-tice review), along with all informationrequested, to the Institute within the re-quired period as may be stipulated in thenotification letter.

The reviewer assigned to the memberfirm will be responsible for arranging theon-site practice review visit, which will nor-mally be scheduled within six weeks ofsuch notification. The member firm shallnotify the Institute immediately if they con-sider the timing of the visit to be inconve-nient and shall specify the reasons thereto.Another date will be arranged by mutualconsent such that the review will be heldwithin four months of such notification.Any further extension is at the reviewer’ssole discretion and shall only be grantedfor valid reasons.

The member firm shall be given rea-sonable notice of the selection of clientfiles for inspection. The selection of cli-ent files is made by the reviewer from themost current client listing as provided bythe member firm. Such listing must becertified as complete by the member firmprior to the selection of sample files. As arule of thumb, the member firm shouldalways ensure that all current auditengagements which are representative ofthe operations of the firm should bereadily retrievable during the on-sitepractice review. For the purposes of thepractice review, such current audit en-gagement files refers to engagementswhich have been signed off in the past 18months up to the date of the on-sitepractice review or any other dates that canbe reasonably accepted by the revieweras a practical alternative.

Arrangements for reviewOn-site practice review visits will be

conducted at the member firm’s registeredoffice or other registered place of business.The member firm should ensure that thereviewer is given access to all offices ifthere are more than one and is given allreasonable assistance for the proper con-duct of the practice review. It is expectedthat the reviewer will be provided with ad-equate office facilities for him/her to per-form his/her work effectively and effi-ciently.

Access to documents(1) The following provisions shall

apply as regards to any practice review :

a) Any person, to whom this paragraph ap-plies, and who is reasonably believedby a reviewer to have in his/her pos-session or under his/her control anyrecord or other document which con-tains or is likely to contain informationrelevant to the practice review shall :

(i) produce to the reviewer or afford him/her access to, any record or documentspecified by the reviewer or any recordor other document which is of a classor description so specified and whichis in his/her possession or under his/her control being in either case arecord or other document which the re-viewer reasonably believes is or maybe relevant to the practice review,within such time and at such place asthe reviewer may reasonably require;

(ii) if so required by the reviewer, give tohim/her such explanation or furtherparticulars in respect of anything pro-duced in compliance with a require-ment under sub-paragraph (i) as thereviewer shall specify;

(iii) give to the reviewer all assistance inconnection with the practice review,which he/she is reasonably able togive.

b) Where any information or matter rel-evant to a practice review is recordedotherwise than in a legible form, anypower to require the production of anyrecord or other document conferredunder paragraph (a), shall include the

power to require the production of areproduction of any such informationor matter or of the relevant part of it ina legible form.

c) A reviewer may inspect, examine ormake copies of or take any abstract ofor extract from a record or documentwhich may be required to be producedunder paragraph (a) or (b). However,the making of copies should not beextended to cover those of the mem-ber firm’s current or previous clients’listings.

d) A reviewer exercising power under thisparagraph shall, if so requested by aperson affected by such exercise, pro-duce for inspection by such person acopy of the appointment furnished tohim/her prior to the commencementof the review.

2) Subsection (1)(a) applies to any mem-ber of the Institute employed or in-volved in the member firm to which theparticular practice review relates or toany person employed by or whose ser-vices are engaged by such firm.

Normally the reviewer will require acopy of the financial statements relating tothe client file reviewed. The financial state-ments will be used as a reference for thePractice Review Committee to assess theadequacy of auditing procedures in rela-tion to the materiality of the items con-cerned. Before the copy of the financialstatements is submitted to the PracticeReview Committee for consideration, allreferences to the client’s name or namesand references within the financial state-ments which could reveal the client’s or themember firm’s identity will be concealedby the reviewer.

Where it is considered necessary forthe proper completion of the review, a re-viewer may request copies of other docu-mentation. In such circumstances, theidentity of the client or references whichwould reveal the identity of the memberfirm will be concealed by the reviewer priorto the submission of these copies to thePractice Review Committee for consider-ation.

23

24

25

26

27

28

11Akauntan NasionalDecember 2002

Reporting

At the conclusion of the practice review,a reviewer is required to make a report tothe Practice Review Committee. In doingso, the reviewer shall not name any indi-vidual in the report except in a suitablycodified manner.

A reviewer shall, before making thereport required herein, send a dated draftof the reviewer’s report to the member firmconcerned, and to each individual (if any)who is named in the report by registeredpost or recorded delivery addressed to theregistered office or registered address ofthe member firm or the individual, as thecase may be.

The member firm, following the receiptof the draft report has 21 days beginningthe day after the day the dated draft is sentto make any submissions or representa-tions, in writing to the reviewer, concern-ing the dated draft of the reviewer’s report.

The reviewer is required to attach anywritten submission or representationmade, to the reviewer’s report in its finalform before submitting it to the PracticeReview Committee. The reviewer will de-lete any reference to the member firm’sidentity in these written submissions orrepresentations to preserve anonymity.

The reviewer will subsequently send tothe member firm a copy of the final reportas submitted to the Practice Review Com-mittee, by registered post or recorded de-livery.

Powers and Procedures of thePractice Review Committee

GeneralThe Practice Review Committee shall :

a. determine the practice and proceduresto be observed in relation to practicereviews to the extent not set out in thisStatement and supporting appendices;

b. issue instructions to any reviewer onany matter relating to practice reviewsor a particular practice review;

c. do or perform any other thing or act asmay be incidental to or which it con-siders necessary or expedient for the

performance of its functions or exer-cise of its powers under this Statement.

Review and ReportAfter completing the draft report pro-

cess, the reviewer will forward a copy ofthe reviewer’s report, any submissions orrepresentations from the member firm(suitably summarised and codified) to thePractice Review Committee for its review.

Follow-up actionOn receiving the report from a re-

viewer, the Committee, having regard tothe report and any submissions or repre-sentations attached to it, may:

a. make recommendations to the memberfirm concerned regarding its applica-tion or observance of (or lack thereof)professional standards;

b. i. issue an instruction to a reviewerto carry out, within such period as maybe specified in the instruction (whichperiod shall not commence earlier thansix months after the date on which theinstruction is issued), a further prac-tice review as regards the member firmto which the report relates; and

ii. specify in the instruction, thematters as regards which the review isto be carried out;

c. if it is of the opinion that any one ormore or all of the partners in the mem-ber firm subject to practice review mayhave failed to observe, maintain or ap-ply, as the case may be, professionalstandards, then subject to paragraph 37below, the Practice Review Committeemay make a complaint regarding suchpartner concerned or, in case there ismore than one such person concerned,a separate complaint in respect of eachof them, to the Investigation Commit-tee of the Institute.

Where :

a. there exists a potential complaint; and

b. immediately prior to the commence-ment of the relevant practice review

i. the proprietor or partner to whom thecomplaint relates had not previouslybeen a partner in any firm at any timewhen a practice review was carried out

as regards that firm; and

ii. a practice review had not previouslybeen carried out as regards his prac-tising on his own account, the PracticeReview Committee shall NOT refer thecomplaint to the Investigation Commit-tee UNLESS it is decided by a majorityof three quarters of its members for thetime being that, had the grounds ofcomplaint or any such ground or anymatter or matters complained of beenestablished, the relevant act or omis-sion by such proprietor or partnerwould have amounted to unprofes-sional conduct within the meaning pre-scribed pursuant to Rule 2 of the Ma-laysian Institute of Accountants (Dis-ciplinary) (No. 2) Rules 2002.

The Practice Review Committee shallmake recommendations to the memberfirm where :

a. it considers that the member firm hassatisfied all key control objectiveswhich the Practice Review Committeedetermines are required to maintainprofessional standards but where fur-ther improvements could be made tointernal quality control systems; and

b. it considers that the member firm hassatisfied the major key control objec-tives but some weaknesses exist in oth-ers. The member firm is then expectedto consider the recommendations forrectifying the weaknesses in controlsand take all necessary action to ensurethat all key control objectives areachieved. A follow up meeting will beconducted after 12 months or if pos-sible, even earlier to enquire about theprogress of the implementation of therecommendations.

A follow up review will be requiredwhere the member firm has not satisfiedthe Practice Review Committee that all thekey control objectives have been main-tained and where the deficiencies are likelyto materially affect the overall quality of anaudit engagement. In such cases the Prac-tice Review Committee will also make rec-ommendations, which it expects the mem-ber firm to implement in order to ensurethe maintenance of professional standards.

32

33

34

37

38

31

29

30

35

36

39

12 Akauntan Nasional December 2002

C O V E R

The implementation of these recommen-dations will be examined during the followup review.

It is clear that where a potential com-plaint relates to the first ever review of theindividual concerned, whether in the mem-ber firm which is the subject of the report,or in any other member firm previouslyreviewed, no complaint can be lodged withthe Investigation Committee unless theconditions set out in paragraph 41 beloware fulfilled. This provision is in line withthe educational thrust of practice reviewand the Council’s commitment to workwith members to improve professionalstandards.

The Practice Review Committee will,even on a first review, make a complaintagainst a member where the weaknessesin the performance of audit engagements,or the disregard of professional standardsamounts to, in its opinion, unprofessionalconduct within the meaning prescribedpursuant to Rule 2 of the Malaysian Insti-tute of Accountants (Disciplinary) (No. 2)Rules 2002. In subsequent reviews, thePractice Review Committee can make acomplaint where it is of the opinion thatthe member has failed (or has shown nocredible intention) to maintain, observe orapply the professional standards as ex-pected of him or her.

Where the Practice Review Commit-tee refers a complaint to the InvestigationCommittee, the reviewer shall disclosethe identity of the member(s) in publicpractice or the member firm as the casemay be, as well as submit all reports andfiles including working papers and corre-spondence pertaining to the review, to theInvestigation Committee for its investiga-tion.

Referral of disputesWhere a dispute arises over the pow-

ers of reviewers as regards to the accessto the documents etc. of the member firm,the reviewer or member firm or both mayrefer the dispute to the Practice ReviewCommittee. A member firm should refer adispute to the Practice Review Committeein writing via the Registrar.

Normally, the Practice Review Commit-tee will delegate the determination of sucha dispute to a sub-committee chaired by theChairman of the Practice Review Commit-tee. As far as possible the anonymity of themember firm will be maintained. The Reg-istrar will delete any references to themember firm’s identity from written com-munications before passing these on to thePractice Review Committee.

Where a dispute is referred, after con-sidering any submissions or representa-tions (which shall be in writing) made bythe relevant member firm and/ or the rel-evant reviewer, the Practice Review Com-mittee :

a. shall determine the dispute and com-municate such determination to eachof the parties to the dispute; and

b. may issue directions relating to thematter in dispute to such member firmor the reviewer concerned and requiresuch member or reviewer to complywith them.

Where a member firm or a member inpublic practice is required to comply witha direction given by the Practice ReviewCommittee and fails to comply with the saidrequirement, the Practice Review Commit-tee may make a complaint to the Investi-gation Committee regarding the memberfirm or member in public practice con-cerned on a simple majority basis.

ConfidentialityStrict confidentiality provisions shall

apply to all those involved in the practicereview process, namely the Registrar, re-viewers, members of the Practice ReviewCommittee, or any person holding a posi-tion who assists any of these parties.

Each person referred to in paragraph47 above shall :

a. at all times after his/her appointmentpreserve and aid in preserving secrecywith regard to any matter coming tohis/her knowledge in the performanceor in assisting in the performance ofany function;

b. not at any time communicate any suchmatter to any other person; and

c. not at any such time suffer or permitany other person to have any access toany record, document or other thingwhich is in his/her possession or un-der his/her control by virtue of his/herbeing or having been so appointed orhis/her having performed or havingassisted any other person in the per-formance of such a function; providedthat the above provisions do not applyin relation to disclosures made in rela-tion to or for the purpose of any inves-tigation and disciplinary proceedingsor criminal proceedings.

In order to enhance confidentiality andimpartiality, neither the identity of themember, the member firm or themember’s clients will be made known tothe Practice Review Committee. Any re-port prepared by the reviewer for the Prac-tice Review Committee will only identifythe member firm and its clients by codenumbers.

Where the final practice review reporthas been issued by the Practice ReviewCommittee and no further action is re-quired, the report, work papers and corre-spondence pertaining to the review shallbe destroyed after one year. Data requiredfor administration purposes shall be re-tained in order to evidence that a reviewrequiring no further action has been com-pleted and to identify the members and thefirm reviewed. Where the Practice ReviewCommittee decides that further action isnecessary, all files shall be retained untilsuch further action has been completed tothe satisfaction of the Practice ReviewCommittee.

Completeness of ReviewFor practical reasons, not all partners

of a member firm that have been selectedfor practice review will be reviewed indi-vidually as regard to the current audit en-gagement files.

However, in most circumstances, thesample of files selected for on-site practicereview should be reflective of the firms’overall operations and size. Appendix B onpage 15 sets out a flow chart of a generalindication of such file selection.

42

43

44

45

46

47

48

49

50

51

52

41

40

13Akauntan NasionalDecember 2002

considers necessary to facilitate the selec-tion of a sample of audit engagements, rep-resentative of the member firm’s clientportfolio, for review.

� Confirmation of visitIn consultation with the member firm, a

date will be set for the on-site review to becarried out. Flexibility will be permitted toensure that members in public practice arenot inconvenienced at especially busy peri-ods. The on-site review date will be arrangedby mutual consent such that the review willbe held within four months of notification.Further extension beyond four months willbe at the sole discretion of the reviewer.

ExecutionIt is estimated that at least a full day will

be needed to complete an on-site review fora member firm of a smaller size. However,this is based on the assumption that the mem-ber firm concerned hasmade all the necessary in-formation and documen-tation available to the re-viewer for his review. Re-views of larger firms maytake longer to complete.

� Initial meetingAn initial meeting will

be held between the re-viewer and a partner ofthe member firm desig-nated to deal with the re-view (designated part-ner). The primary pur-pose of this meeting is toconfirm the accuracy ofthe responses given onthe Questionnaire. Thedescription of the systemin the Questionnairemay not fully explain allthe relevant proceduresand policies adopted bythe member firm and

Summary ofPractice Review Procedures

IntroductionThe Practice Review Committee shall,

among other things, determine the de-tailed practice and procedures to be ob-served in relation to practice review. Theframework for the review procedures ascontained herein have been endorsed bythe Council and shall act as supplementalto the Statement on Practice Review issuedby the Council on 15 November 2002 andwhich comes into effect on 1 January 2003.These procedures are summarised belowand can be categorised into three stages— planning, execution and reporting.

Planning� Selection of member firms by Registrar

The Registrar will select member firmsrandomly from the register of member firmsmaintained by the Institute. Each memberfirm shall have an equal chance of beingselected. All member firms selected will becodified so as to ensure the identity of thefirms concerned remains confidential.

� Notification — Choice of ReviewersA member firm will be notified in writ-

ing about an impending practice reviewand will be required to state their prefer-ence — to be reviewed by a reviewer whois a staff of the Institute or by a person ap-pointed from the Panel of Reviewers.i) Notification — Enclosure of

QuestionnaireA Questionnaire will subsequently be

sent to the member firm for completionafter the option of review (see above) hasbeen confirmed by the Registrar.

� Return of completed QuestionnaireThe member firm should complete and

return the Questionnaire within one monthof receipt. The information will be used forthe planning of the review.

In addition, member firms are requiredto prepare a complete list of their audit cli-ents, suitably codified if desired, and toprovide any other information the reviewer

this initial meeting can provide additionalinformation. The reviewer should have afull understanding of the system and beable to form a preliminary evaluation of itsadequacy at the conclusion of the meeting.

Larger firms which have extensive docu-mentation regarding their practice and pro-cedures (i.e. formal of fice proceduresmanuals and audit manuals) will find it un-necessary to document all the controls andwill just cross reference the Questionnaireto the relevant sections of their manuals.For firms like these, an additional planningvisit will be arranged before the on-sitereview to review the relevant manuals.

� Compliance review — general controlsThe reviewer may carry out a compliance

review of the general controls of the mem-ber firm and evaluate the degree of relianceto be placed upon them. The degree of reli-ance will, ultimately, affect the sample size

14 Akauntan Nasional December 2002

of audit engagements to be reviewed.The following five key controls are in-

cluded in the Questionnaire :

● Independence;

● Maintenance of Professional Skill andStandards;

● Outside Consultation;

● Staff Supervision and Development; and

● Office Administration.

Member firms are expected to addresseach of the five key control areas.

In each key control area of the Question-naire, there are supplementary questionsand matters to consider. These are in-tended to indicate the kind of controls thatare expected to be installed and operatedwithin each firm.

All questions are not necessarily relevantto particular types of member firms be-cause of their size and culture etc. How-ever, member firms should still assess theirinternal control systems to ascer tainwhether they address the objectives underthe five key control areas.

� Selection of audit engagements to bereviewedThe number of audit engagements to be

reviewed depends upon :a. the number of partners involved in audit

engagements in the firms selected; andb. the degree of reliance placed, if any, on

general quality controls.

For the number of audit engagements tobe actually reviewed, please refer to theflowchart in Appendix B as provided hereinas a general guideline.

From the clients list as provided and certi-fied as complete, the reviewer, in consulta-tion with the member firm, will proceed toselect an actual sample of audit engagementsfor review. The engagements reviewedshould be a balanced sample from a varietyof different sized clients covering variousindustries so that they reflect the “overallperformance” of the said firm under review.Accordingly, if the reviewer considers thatthe actual sample is not representative of themember firm’s audit client portfolio, he mayproceed to choose an additional number offiles in excess of those as depicted in theenclosed flowchart in Appendix B.

The population from which files are se-lected for review will be audits completed

C O V E R

at least 6 months preceding the date of thenotification letter but not earlier than 18months prior to the selection date.

� Review of filesThe reviewer may adopt a compliance ap-

proach or substantive approach or a com-bination selection of both in the review ofaudit engagement files.

� Compliance approach —audit engagementsThe compliance approach is to assess

whether proper control procedures havebeen established by the member firm to en-sure that audits are performed in accordancewith approved Auditing Standards andGuidelines and such control procedures areconsistently adhered to by the member firm.

The following six key controls are in-cluded in the Questionnaire :

● Audit File Administration;

● Financial Statements Presentation;

● Review and Evaluation of System of In-ternal Controls;

● Substantive Tests;

● Audit Conclusion; and

● Audit Report.

� Substantive approach — audit engagementsA substantive approach will be employed

if the reviewer chooses not to place relianceon the member firm’s specific controls onaudit engagements or is of the opinion thatthe standard of compliance is not satisfactory.This approach requires a detailed review ofthe audit working papers in order to estab-

lish whether the audit work has been car-ried out in accordance with approved Audit-ing Standards and Guidelines. Such a reviewis similar to the type of review performed bythe engagement partner/manager duringnormal audit engagement procedures. Thisapproach is likely to take longer than thecompliance approach.

� Closing meetingAt the end of the on-site review, a draft re-

port of factual findings will be prepared fordiscussion with the designated partner of thefirm being reviewed or the sole practitioner.During the closing meeting, the designatedpartner/practitioner has the opportunity tomake representations, suggestions and rec-ommendations in relation to the matters

raised. The reviewer has the duty of explain-ing to the designated partner/practitionerthe advantages and benefits of implement-ing suggestions and recommendations forimprovements. At the conclusion of the clos-ing meeting, the designated partner/practi-tioner and the reviewer are required to signon the draft report of factual findings to sig-nify their agreement of its factual accuracy.

ReportingThe reviewer will prepare a report to the

Practice Review Committee (the reviewer’sreport), incorporating the report of factualfindings as discussed with the member firm.After review by the Practice Review Direc-tor (or Senior Manager) of the Institute, adated draft of the reviewer’s report will besent to the member firm for comments. Thisprocess should not take more than two

15Akauntan NasionalDecember 2002

Notes : i) The reviewer will decide how many audit engagements will be reviewed within a range at the planning stage. ii) The above table only gives a general indication of the number of audit engagements to be reviewed. The exact number and extent of review will be dependent on the individual firm's circumstances. iii) As a minimum guide, it is envisaged that the review of one audit engagement file per partner involved in provision of auditing services is to be conducted.

No. of No. of Audit No. of Audit No. of Audit partners in firm Engagements Engagements Engagements

1 3 ≥ 3 ≥ 42 - 5 ≥ 4 6 ≥ 8

6 and above ≥ 6 ≥ 10 ≥ 12

High

Degree of reliance to be placed on general controls

Compliance Review on generalcontrols. Do the results of the review indicate reliance can be placed ongeneral controls?

Medium to low

NO

YES

Have general controls been documented?

NO

NO

NO

YES

YES

Will the review be more efficiently executed by relying on general controls?

Is there any system of general controls?

YESYES

FILE Selection PROCESS

A P P E N D I X B

3

months after the closing meeting. Any com-ments made must be submitted in writingwithin 21 days. The reviewer will finalise his/her report upon the receipt of the submis-sions. In finalising the report, the reviewermay make changes to the dated draft he/she considers appropriate in the light of thesubmissions. The submissions will be at-tached (after properly codified) to thereviewer’s report before it is sent to the Com-mittee for consideration. A copy of thereviewer’s report will be sent to the memberfirm for its information and record.

The member firm will be allowed the op-por tunity to make its representationsthroughout the review process. It is ex-pected that the on-site closing meetingbetween the reviewer and the firm willprovide an excellent channel for thecommunication of views concerning thefindings and recommendations. In ad-dition, the member firm has 21 days toconsider the dated draft report andmake its formal submissions and rep-resentations to the Practice ReviewCommittee through the reviewer.

A meeting of the Practice Review Com-mittee will be held to consider thereviewer’s report and the member firm’ssubmissions. The Committee may issuea final report to the member firm and in-struct the reviewer to perform any follow-up action considered appropriate. The fi-nal report can be categorised as follows :

Such report may contain minor rec-ommendations for improvements tothe systems. The member firm mayexercise its discretion in consider-ing what course of action to betaken. The Institute will not performany follow-up procedures to ensurechanges are made.

A variation to the type of report asmentioned in (1) above is issuedwhere the member firm is found tohave achieved the major control ob-jectives but some weakness are foundin certain control areas which are con-sidered material enough to bring tothe attention of the firm. The said firmshould seriously consider the sugges-tions and recommendations and takeall necessary action (implementingnew procedures) to ensure the objec-

1

2

tives of the particular control areas areachieved. A brief review/meeting will bearranged with the member firm about 12months after the issue of the final reportto establish whether changes have beenimplemented.

Finally, there is also a report where amember firm is deemed to have failedto satisfy the Practice Review Commit-tee that it has sufficient controls to en-sure its audit work is consistently car-ried out in accordance with applicableprofessional standards. In such case,the Practice Review Committee will

order the reviewer to perform anotherpractice review no earlier than sixmonths after the issue of the final re-port. This will allow time for the mem-ber firm to take steps to improve itscontrols system as suggested.

It is possible that where the third type ofreport reveals extensive weaknesses amount-ing to unprofessional conduct within themeaning prescribed pursuant to the Malay-sian Institute of Accountants (Disciplinary)(No. 2) Rules 2002, the Practice Review Com-mittee can make a complaint to the Investiga-tion Committee for its investigations. AN

16 Akauntan Nasional December 2002

The Budget for Cost of RecoveryOften the daunting questions that haunts

a BCP Manager or BCP Project Team is :

does my organisation have a BCP bud-get?

if it does what is the amount and is itadequate?

what does my organisation invest itsdisaster recovery money in?

what is expected of my organisationfrom that kind of investment?

Total disaster recovery investments aresometimes obscure and hard to identify.The expenses can be hidden in normal pro-duction or operation and service support.The human resource cost portions may not

M A N A G E M E N T A C C O U N T I N GB C P & C R I S I S M G M T

The BCP BUDGETand BUSINESS IMPACTANALYSIS By Dr. Josef Eby Ruin

1

2

3

4

12

3

1

be properly tracked, or they are buried inother HR and department costs. Very of-ten it is not unusual to come acrossorganisations that are not able to meet their‘time-to-recover’, data protection objectivesor plain business recovery let alone conti-nuity with their current level of BCP ex-penditure-allocation. As a percentage oftheir budgets, financial institutions andservice providers like telecommunicationscompanies and airlines tend to be gener-ous in their investment on their disasterrecovery or business continuity. Othertypes of industries may not be that gener-ous or committed. One simple rule-of-thumb may be for an organisation to setaside about 10 per cent of its IT budget to

be dedicated as to its disaster recovery andbusiness continuity programmes.

The Many Costs orPrices of Crisis

A surprised power outage can causeorganisations to halt operations for an in-definite period of time. Some empiricalstudies reveal that nine out of 10organisations repor ted that during asystem’s failure they :

encounter productivity losses;

have bigger incidence of end-user andmanagement dissatisfaction, and

are confronted with deluge of customerdissatisfaction (and this is in fact verydamaging for the long-term survival ofthe organisation).

The costs of a disaster includes the costof :