Embed Size (px)

Citation preview

1© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Workers Compensation Update

Spring Midwestern Actuarial ForumMarch 7, 2008

Barry Lipton, Practice Leader and Senior ActuaryNCCI

Workers Compensation Update

Spring Midwestern Actuarial ForumMarch 7, 2008

Barry Lipton, Practice Leader and Senior ActuaryNCCI

2© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Workers Compensation Results

3© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

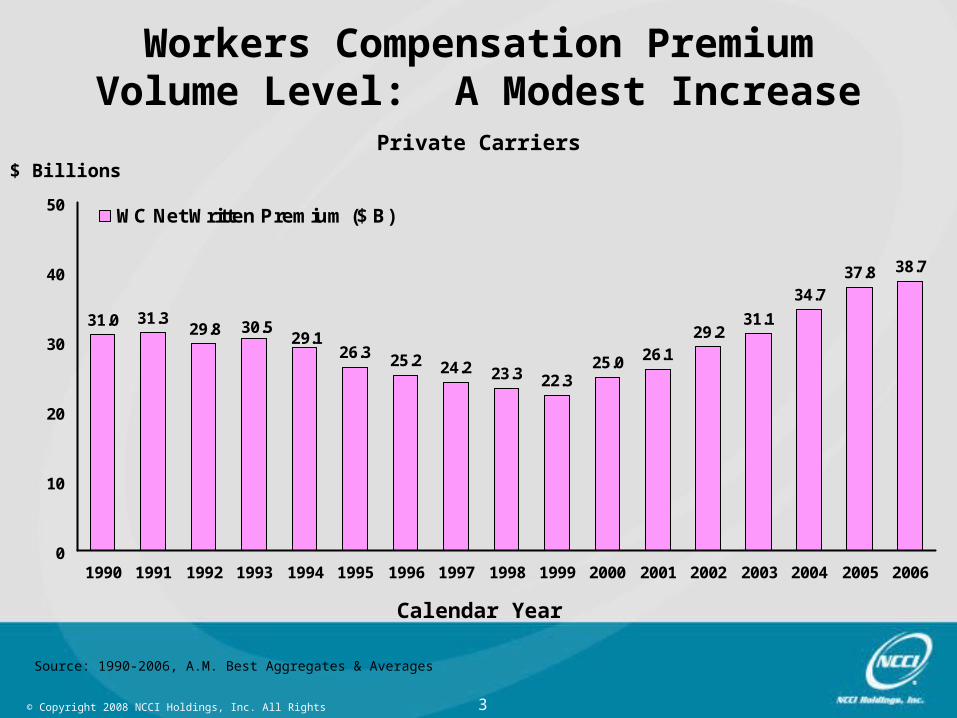

31.0 31.3

26.3 25.2 24.2 23.3 22.325.0 26.1

29.231.1

37.8 38.7

34.7

29.130.529.8

0

10

20

30

40

50

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

WC Net Written Premium ($ B)

Workers Compensation PremiumVolume Level: A Modest Increase

Private Carriers$ Billions

Calendar Year

Source: 1990-2006, A.M. Best Aggregates & Averages

4© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

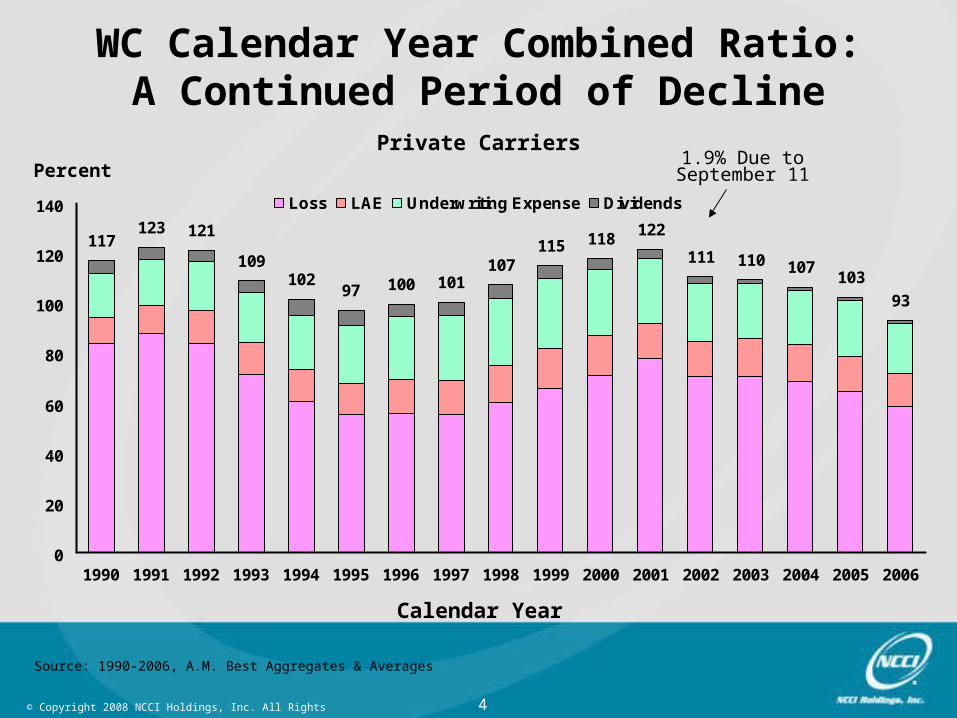

117123 121

109102

97 100 101107

115 118122

111 110 107103

93

0

20

40

60

80

100

120

140

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Loss LAE Underwriting Expense Dividends

1.9% Due to September 11Percent

WC Calendar Year Combined Ratio:A Continued Period of Decline

Private Carriers

Calendar Year

Source: 1990-2006, A.M. Best Aggregates & Averages

5© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

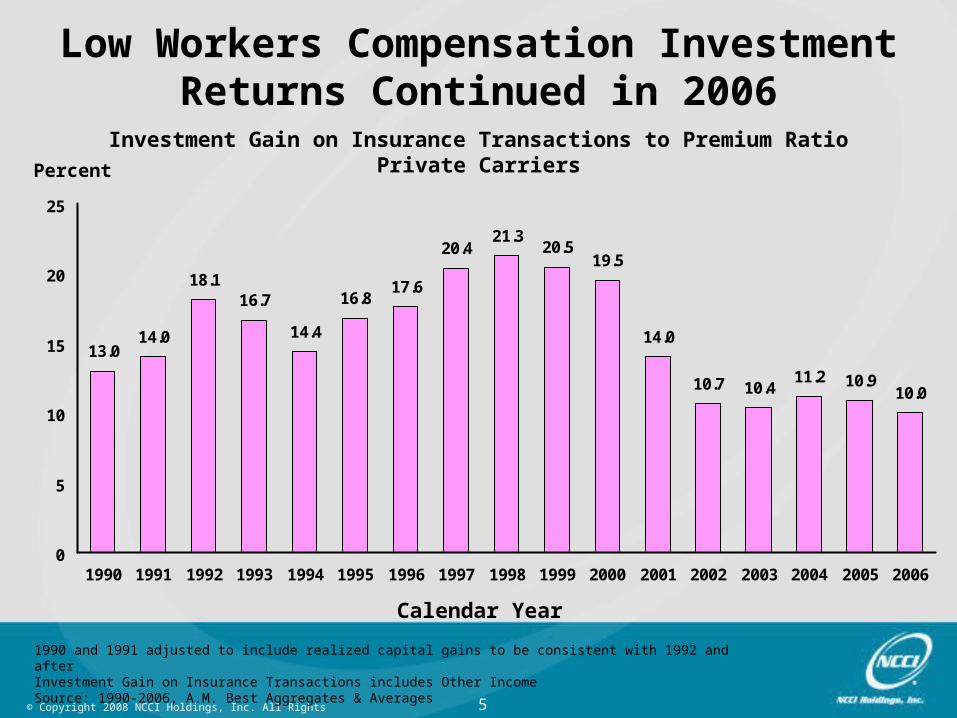

1990 and 1991 adjusted to include realized capital gains to be consistent with 1992 and afterInvestment Gain on Insurance Transactions includes Other IncomeSource: 1990-2006, A.M. Best Aggregates & Averages

13.014.0

18.116.7

14.4

16.817.6

20.421.3

20.519.5

14.0

10.7 10.4 10.910.0

11.2

0

5

10

15

20

25

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Percent

Low Workers Compensation InvestmentReturns Continued in 2006

Investment Gain on Insurance Transactions to Premium RatioPrivate Carriers

Calendar Year

6© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

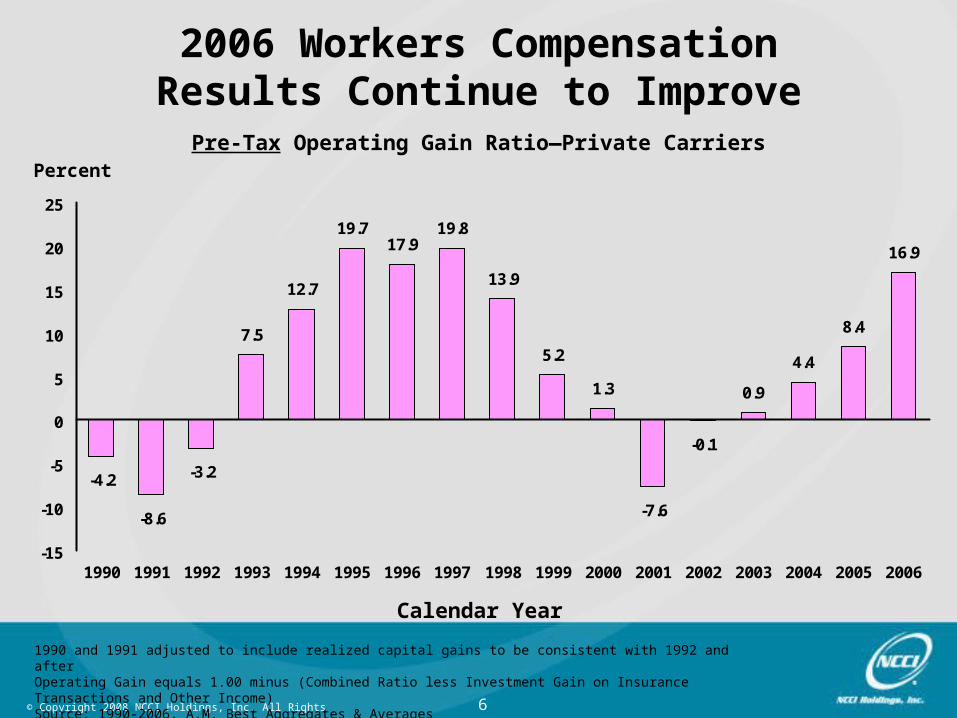

1990 and 1991 adjusted to include realized capital gains to be consistent with 1992 and afterOperating Gain equals 1.00 minus (Combined Ratio less Investment Gain on Insurance Transactions and Other Income)Source: 1990-2006, A.M. Best Aggregates & Averages

7.5

12.7

19.717.9

19.8

13.9

5.2

1.3 0.9

8.4

16.9

4.4

-0.1

-7.6

-3.2

-8.6

-4.2

-15

-10

-5

0

5

10

15

20

25

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Percent

Calendar Year

2006 Workers CompensationResults Continue to Improve

Pre-Tax Operating Gain Ratio—Private Carriers

7© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Workers CompensationResidual Market

8© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

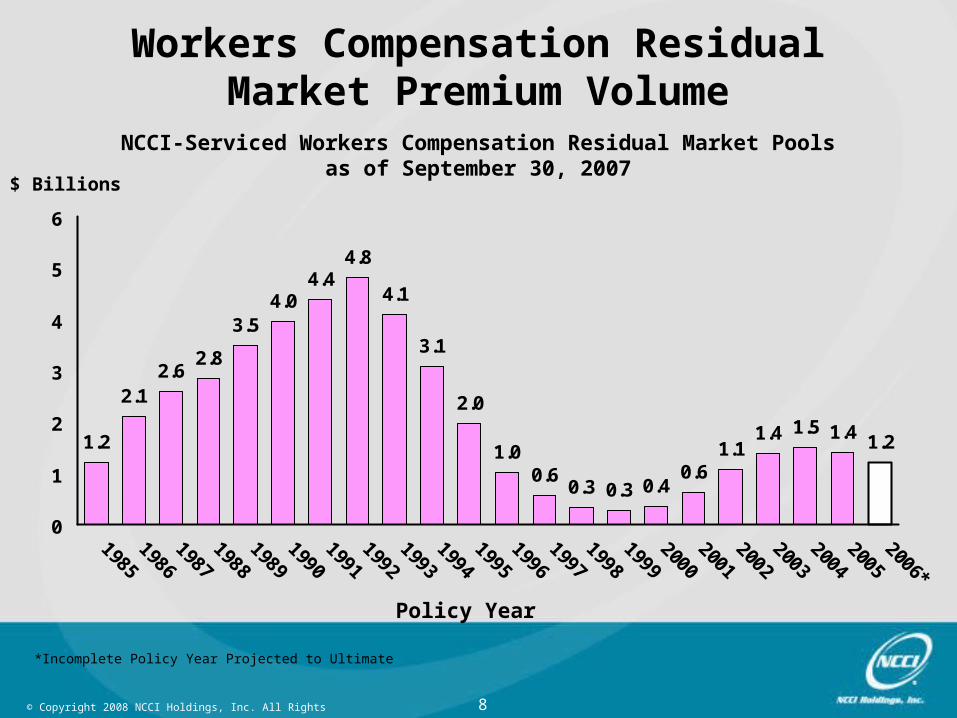

Workers Compensation Residual Market Premium Volume

NCCI-Serviced Workers Compensation Residual Market Poolsas of September 30, 2007

$ Billions

Policy Year

1.2

2.12.6

2.8

3.54.0

4.44.8

4.1

3.1

2.0

1.00.6

0.3 0.3 0.40.6

1.11.4 1.5

1.21.4

0

1

2

3

4

5

6

*Incomplete Policy Year Projected to Ultimate

9© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

*Incomplete Policy Year Projected to Ultimate

Workers Compensation Residual Market Combined Ratios

NCCI-Serviced Workers Compensation Residual Market Pools as of September 30, 2007

Percent

Policy Year

177

166 170167160

143

128

112104

98 95100103

117117 119

108 110108114115

108

80

100

120

140

160

180

200

10© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Workers Compensation

Accident Year ResultsAnd

Reserve Estimates

11© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

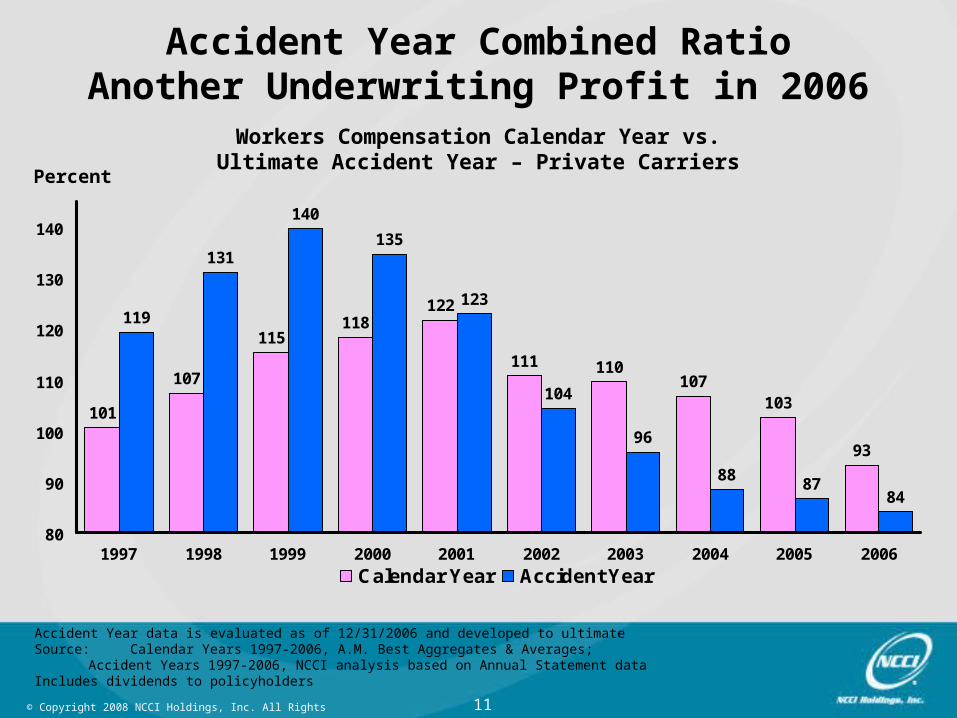

Accident Year Combined RatioAnother Underwriting Profit in 2006

Workers Compensation Calendar Year vs.Ultimate Accident Year – Private Carriers

Percent

101

107

115118

122

111 110107

103

119

131

140

135

123

104

96

8887

93

84

80

90

100

110

120

130

140

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Calendar Year Accident Year

Accident Year data is evaluated as of 12/31/2006 and developed to ultimateSource: Calendar Years 1997-2006, A.M. Best Aggregates & Averages;

Accident Years 1997-2006, NCCI analysis based on Annual Statement dataIncludes dividends to policyholders

12© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

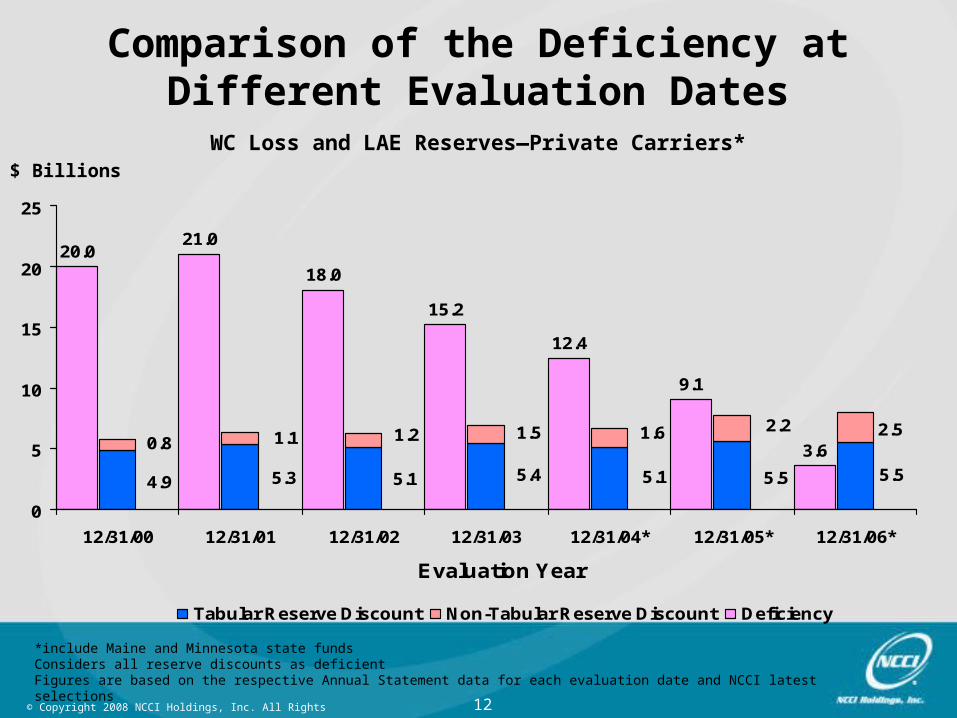

*include Maine and Minnesota state fundsConsiders all reserve discounts as deficientFigures are based on the respective Annual Statement data for each evaluation date and NCCI latest selections

$ Billions

Comparison of the Deficiency at Different Evaluation Dates

WC Loss and LAE Reserves—Private Carriers*

5.54.9 5.3 5.1 5.55.15.4

2.50.8 1.1 1.2

2.21.61.5

20.021.0

18.0

15.2

12.4

9.1

3.6

0

5

10

15

20

25

12/31/00 12/31/01 12/31/02 12/31/03 12/31/04* 12/31/05* 12/31/06*

Evaluation Year

Tabular Reserve Discount Non-Tabular Reserve Discount Deficiency

13© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

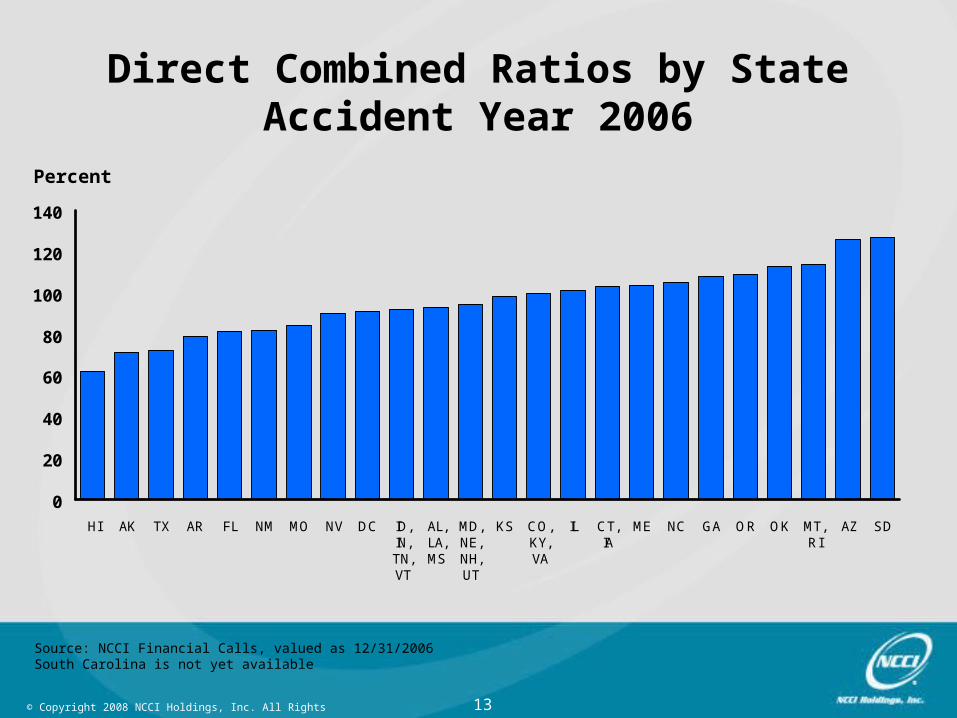

Direct Combined Ratios by StateAccident Year 2006

Percent

0

20

40

60

80

100

120

140

HI AK TX AR FL NM MO NV DC ID,IN,TN,VT

AL,LA,MS

MD,NE,NH,UT

KS CO,KY,VA

IL CT,IA

ME NC GA OR OK MT,RI

AZ SD

Source: NCCI Financial Calls, valued as 12/31/2006South Carolina is not yet available

14© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

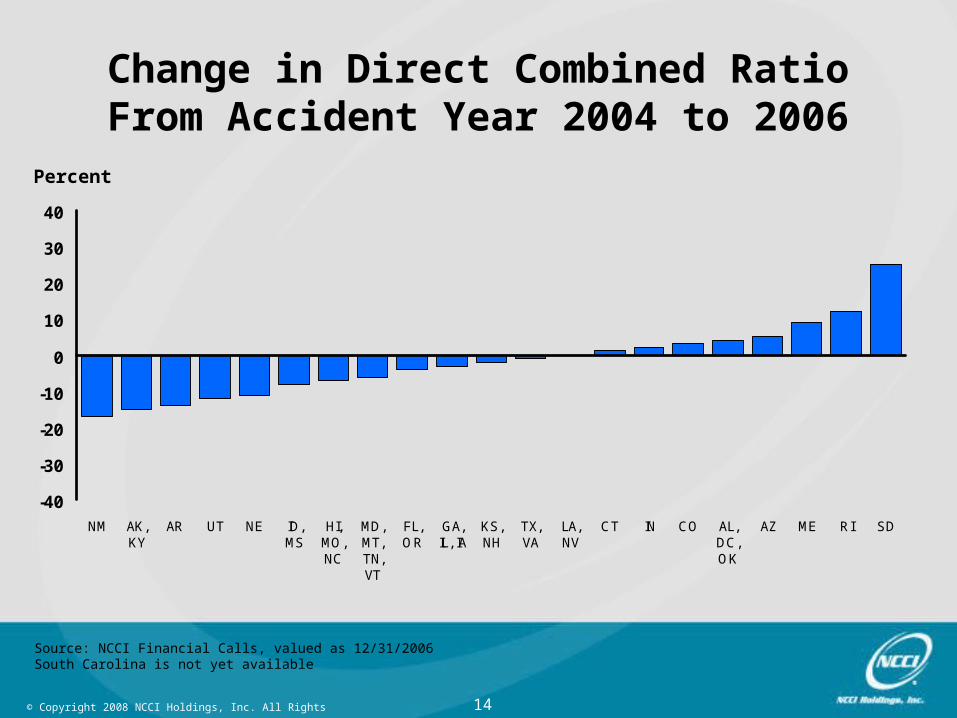

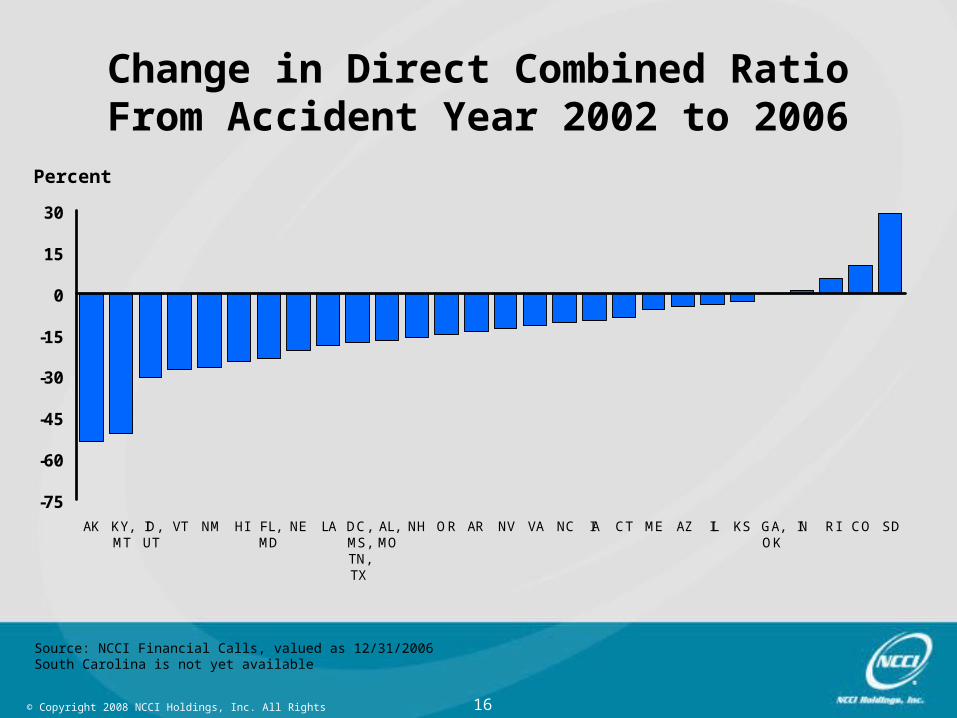

Change in Direct Combined RatioFrom Accident Year 2004 to 2006

Percent

-40

-30

-20

-10

0

10

20

30

40

NM AK,KY

AR UT NE ID,MS

HI,MO,NC

MD,MT,TN,VT

FL,OR

GA,IL, IA

KS,NH

TX,VA

LA,NV

CT IN CO AL,DC,OK

AZ ME RI SD

Source: NCCI Financial Calls, valued as 12/31/2006South Carolina is not yet available

15© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

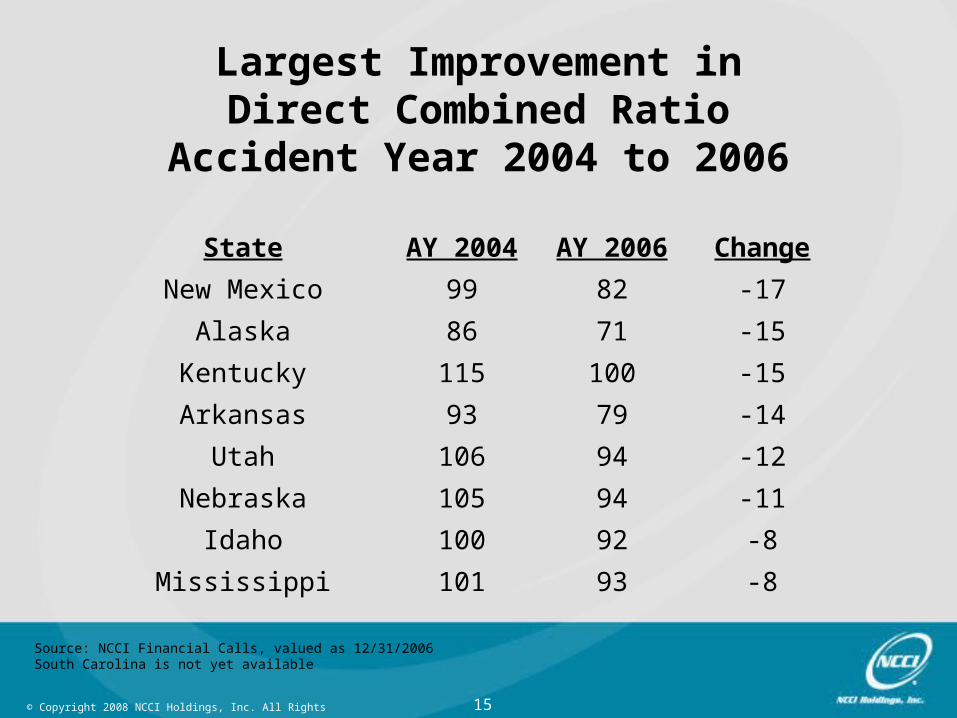

Largest Improvement inDirect Combined Ratio

Accident Year 2004 to 2006

Source: NCCI Financial Calls, valued as 12/31/2006South Carolina is not yet available

State AY 2004 AY 2006 Change

New Mexico 99 82 -17

Alaska 86 71 -15

Kentucky 115 100 -15

Arkansas 93 79 -14

Utah 106 94 -12

Nebraska 105 94 -11

Idaho 100 92 -8

Mississippi 101 93 -8

16© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Change in Direct Combined RatioFrom Accident Year 2002 to 2006

Percent

-75

-60

-45

-30

-15

0

15

30

AK KY,MT

ID,UT

VT NM HI FL,MD

NE LA DC,MS,TN,TX

AL,MO

NH OR AR NV VA NC IA CT ME AZ IL KS GA,OK

IN RI CO SD

Source: NCCI Financial Calls, valued as 12/31/2006South Carolina is not yet available

17© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Largest Improvement inDirect Combined Ratio

Accident Year 2002 to 2006

Source: NCCI Financial Calls, valued as 12/31/2006South Carolina is not yet available

State AY 2002 AY 2006 Change

Alaska 125 71 -54

Kentucky 151 100 -51

Montana 165 114 -51

Idaho 123 92 -31

Utah 125 94 -31

Vermont 120 92 -28

New Mexico 109 82 -27

Hawaii 87 62 -25

18© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Workers Compensation

Premium Drivers

19© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

-3.3

12.1

7.4

10.0

2.9 3.5

1.2

4.9

6.6

-2.0

-6.0

-2.6

-5.4

-8.0

-6.0

-3.2

-6.4

-5.1 -4.8

-10

-5

0

5

10

15

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007* 2008*

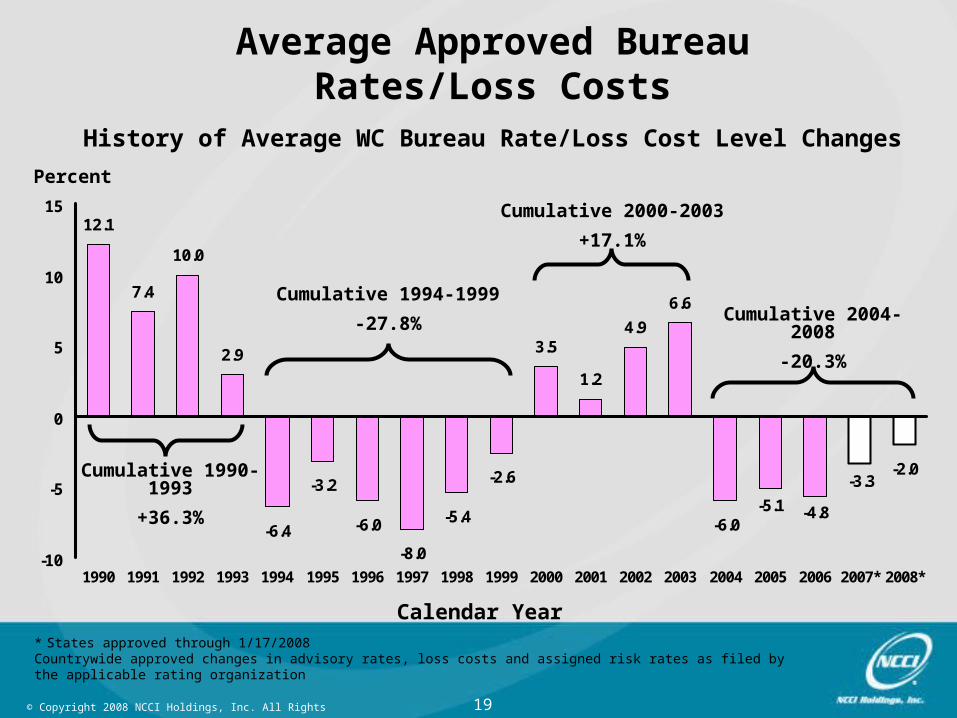

Cumulative 1990-1993

+36.3%

Cumulative 1994-1999

-27.8%

Average Approved BureauRates/Loss Costs

History of Average WC Bureau Rate/Loss Cost Level Changes

Percent

Cumulative 2000-2003

+17.1%

Cumulative 2004-2008

-20.3%

Calendar Year* States approved through 1/17/2008Countrywide approved changes in advisory rates, loss costs and assigned risk rates as filed by the applicable rating organization

20© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

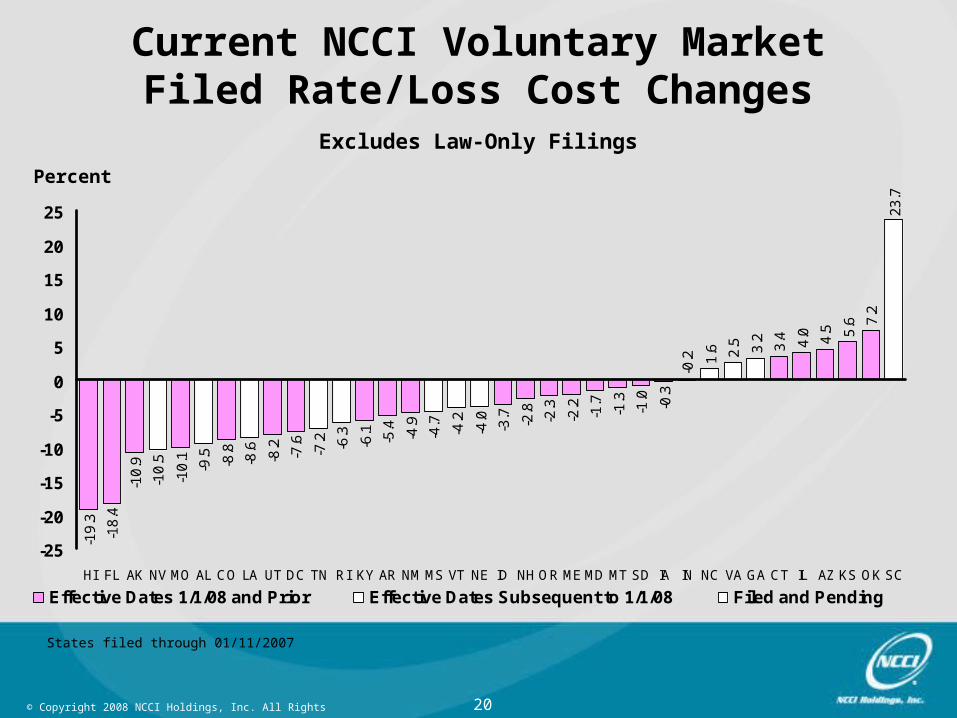

Current NCCI Voluntary MarketFiled Rate/Loss Cost Changes

Excludes Law-Only Filings

Percent

States filed through 01/11/2007

-19

.3

-18

.4

-10

.9

-10

.1 -8.8

-8.2

-7.6 -6

.1

-5.4

-4.9 -3

.7 -2.8

-2.3

-2.2

-1.7

-1.3

-1.0

-0.3

-0.2

3.4 4.0 4.5 5.6 7

.2

-9.5 -7

.2

-4.0

1.6 2.5 3.2

-10

.5 -8.6 -6

.3 -4.7

-4.2

23

.7

-25

-20

-15

-10

-5

0

5

10

15

20

25

HI FL AK NV MO AL CO LA UT DC TN RI KY AR NM MS VT NE ID NH OR ME MD MT SD IA IN NC VA GA CT IL AZ KS OK SC

Effective Dates 1/1/08 and Prior Effective Dates Subsequent to 1/1/08 Filed and Pending

21© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Percent

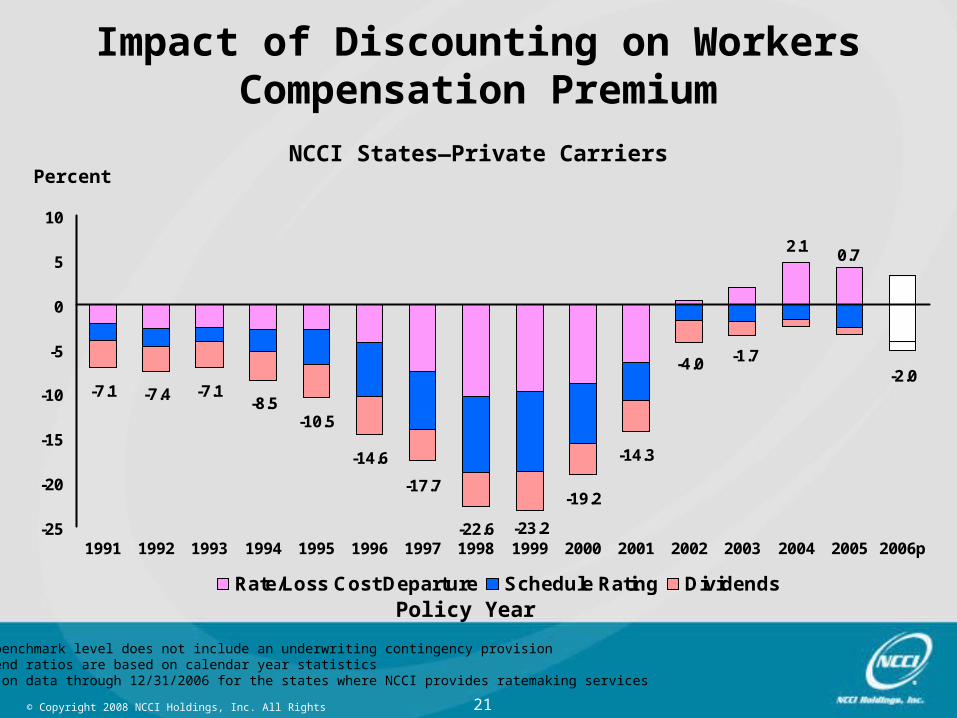

Impact of Discounting on Workers Compensation Premium

NCCI States—Private Carriers

NCCI benchmark level does not include an underwriting contingency provisionDividend ratios are based on calendar year statisticsBased on data through 12/31/2006 for the states where NCCI provides ratemaking services

Policy Year

-7.1 -7.4 -7.1-8.5

-10.5

-14.6

-17.7

-22.6

-19.2

-14.3

-4.0-2.0

-1.7

-23.2

2.10.7

-25

-20

-15

-10

-5

0

5

10

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006p

Rate/Loss Cost Departure Schedule Rating Dividends

22© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Workers Compensation

Loss Drivers

23© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

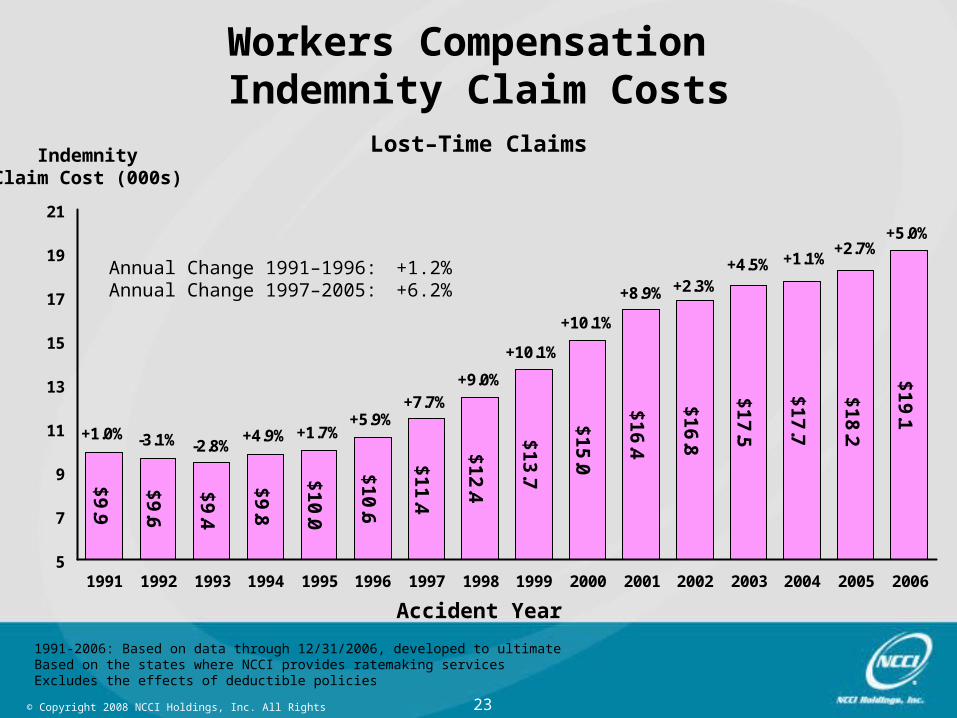

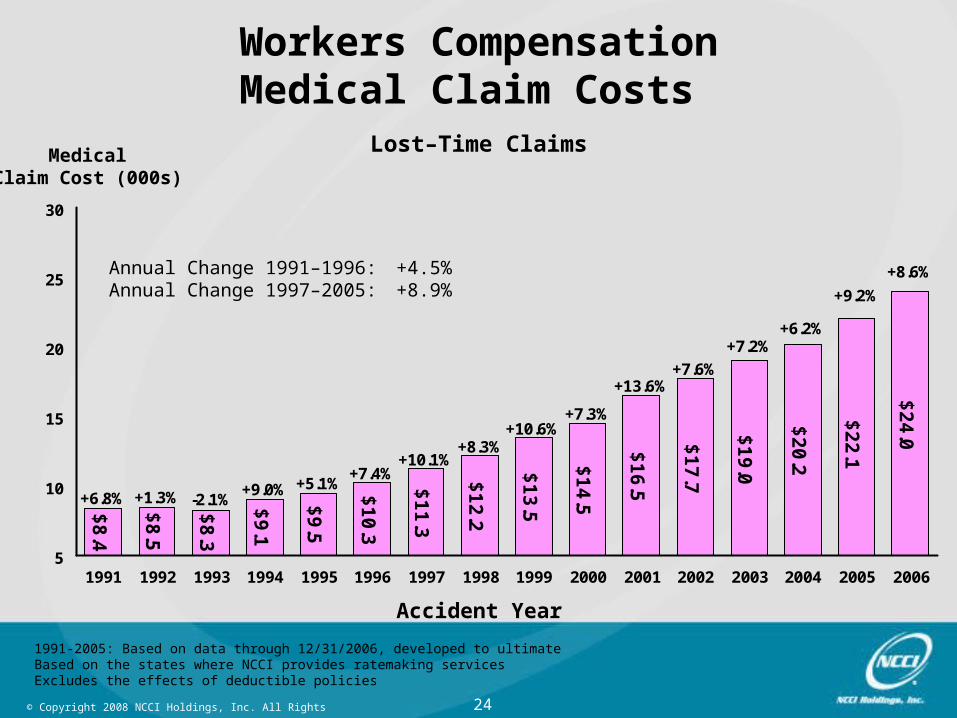

IndemnityClaim Cost (000s)

1991-2006: Based on data through 12/31/2006, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

Workers Compensation Indemnity Claim Costs

Lost–Time Claims

Accident Year

$9

.9

$9

.6

$9

.4

$9

.8

$1

0.0

$1

0.6

$1

1.4

$1

2.4

$1

3.7

$1

5.0

$1

6.4

$1

6.8

$1

7.5

$1

9.1

$1

7.7

$1

8.2

+5.0%

+1.0% -3.1% -2.8%+4.9% +1.7%

+5.9%+7.7%

+9.0%

+10.1%

+10.1%

+8.9% +2.3%+4.5% +1.1%

+2.7%

5

7

9

11

13

15

17

19

21

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Annual Change 1991–1996: +1.2%Annual Change 1997–2005: +6.2%

24© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

1991-2005: Based on data through 12/31/2006, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

Workers CompensationMedical Claim Costs

Lost–Time ClaimsMedicalClaim Cost (000s)

Accident Year

$8

.4

$8

.5

$8

.3

$9

.1

$9

.5

$1

0.3

$1

1.3

$1

2.2

$1

3.5

$1

4.5

$1

6.5

$1

7.7

$1

9.0

$2

4.0

$2

0.2

$2

2.1

+8.6%

+6.8% +1.3% -2.1%+9.0% +5.1%

+7.4%+10.1%

+8.3%+10.6%

+7.3%

+13.6%+7.6%

+7.2%+6.2%

+9.2%

5

10

15

20

25

30

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Annual Change 1991–1996: +4.5%Annual Change 1997–2005: +8.9%

25© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

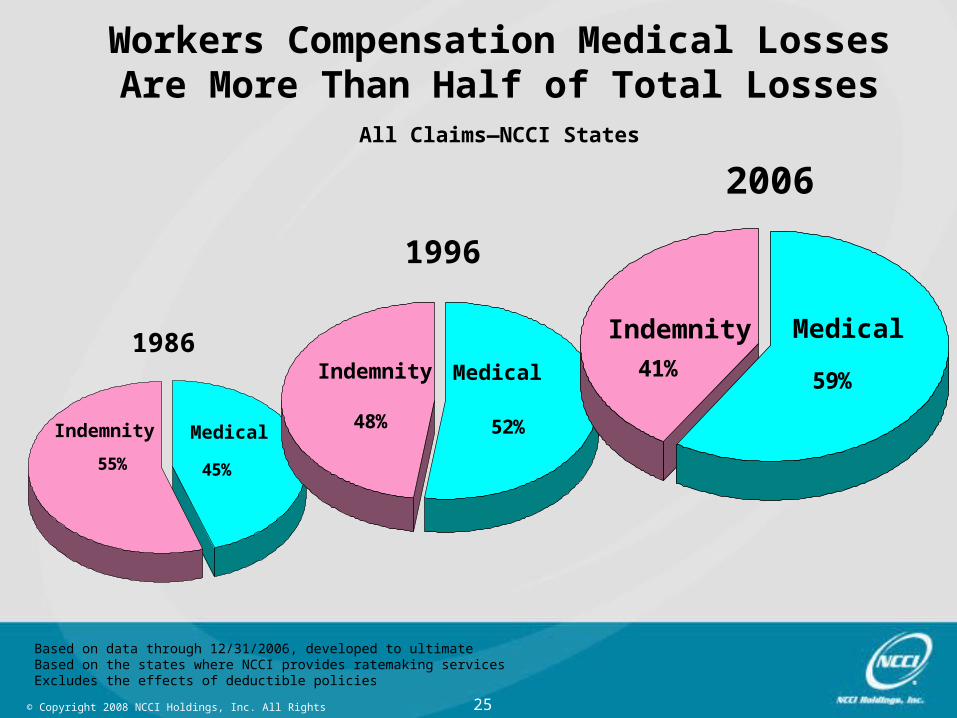

Workers Compensation Medical Losses Are More Than Half of Total Losses

All Claims—NCCI States

Based on data through 12/31/2006, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

45%55%

1986

MedicalIndemnity

1996

48% 52%

Indemnity Medical

2006

41% 59%

Indemnity Medical

26© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

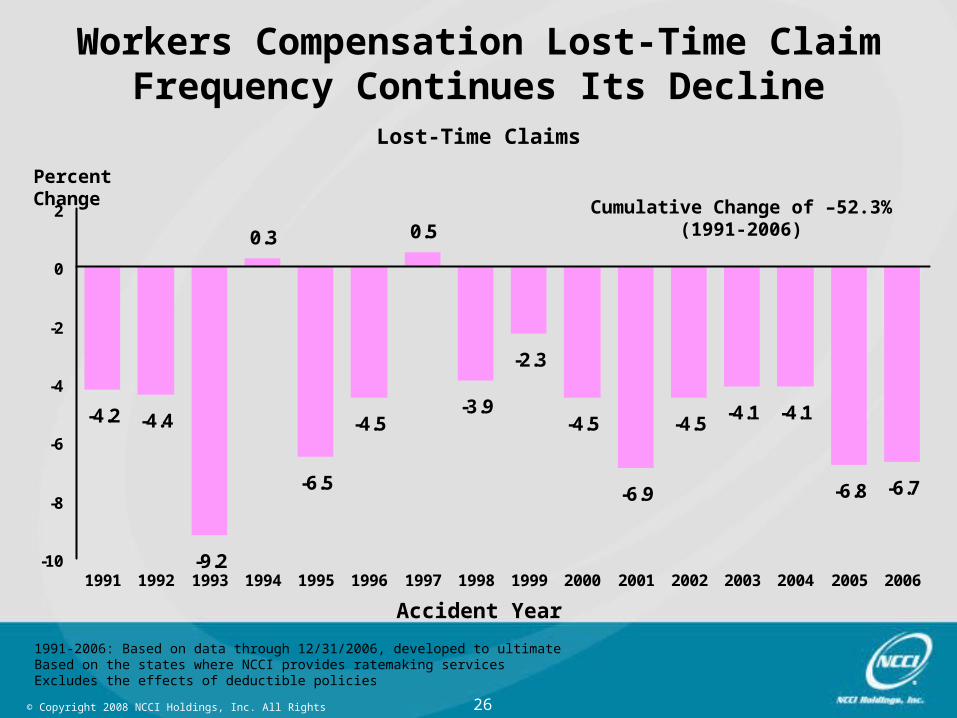

Percent Change

Workers Compensation Lost-Time Claim Frequency Continues Its Decline

Lost-Time Claims

Accident Year

1991-2006: Based on data through 12/31/2006, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policies

-4.2 -4.4

-9.2

-6.9

-4.5-4.1 -4.1

-6.7

0.3

-6.5

-4.5

0.5

-3.9

-2.3

-4.5

-6.8

-10

-8

-6

-4

-2

0

2

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Cumulative Change of –52.3%(1991-2006)

27© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Prescription Drug Study2007 Update

28© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

How Are Workers Compensation Drug Costs Changing?

What percentage of workers compensation (WC) medical costs are prescription drugs? How has the percentage changed over time?

Do WC prescription drug costs differ by state?

What types of drugs are prescribed most often?

29© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

WC Prescription Drug Cost Containment Options

Prescription drug-fee schedulesUsed in a majority of statesMany use Average Wholesale Price (AWP) Most also add a dispensing fee

Negotiation of lower prices

Mandated use of generic drugs

Pharmacy Benefit Managers (PBMs)

Formularies

30© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Key Findings

There are some signs that the WC prescription drug share of medical costs is leveling off, at least temporarily

Some states’ WC prescription drug costs vary significantly from average

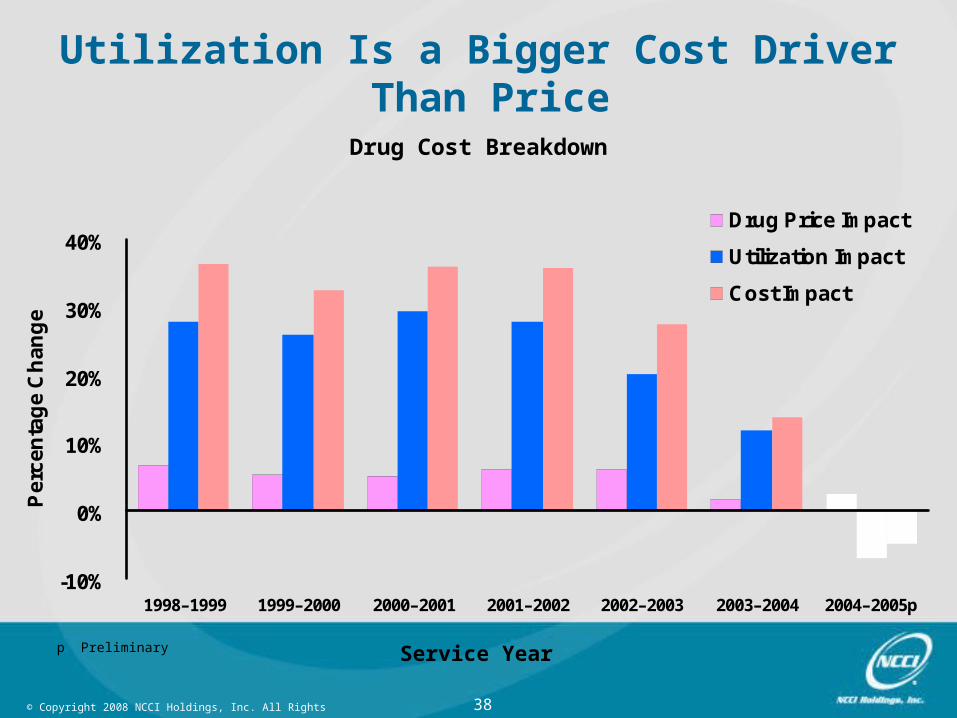

Utilization is the significant driving force behind total cost

31© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Key Findings

Anti-inflammatories and painkillers represent about half of total amount paid for drugs in 2005, and comprise 6 of the top 10 drugs

For drugs with generic equivalents, generics were prescribed 87% of the time in Service Year 2005

Additional savings of about 12% of total drug costs can be realized from using generic equivalents

32© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Study Design

Data includes a nationwide sample

Data covers claims from 1994 to 2005 and services from years 1996 to 2005

“Prescription drug” is defined as a transaction identified with a National Drug Code (NDC) or with carrier specialized codes

33© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Nationwide View

34© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

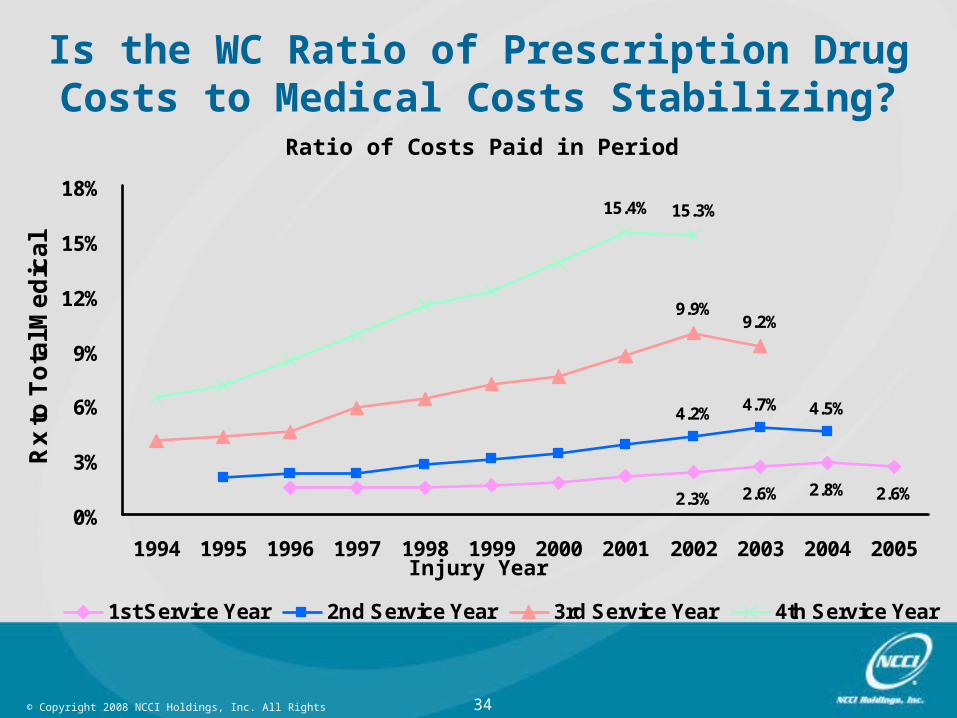

2.3% 2.6% 2.8% 2.6%

4.2% 4.7% 4.5%

9.2%9.9%

15.4% 15.3%

0%

3%

6%

9%

12%

15%

18%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Rx

to T

ota

l Me

dic

al

1st Service Year 2nd Service Year 3rd Service Year 4th Service Year

Is the WC Ratio of Prescription Drug Costs to Medical Costs Stabilizing?

Ratio of Costs Paid in Period

Injury Year

35© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

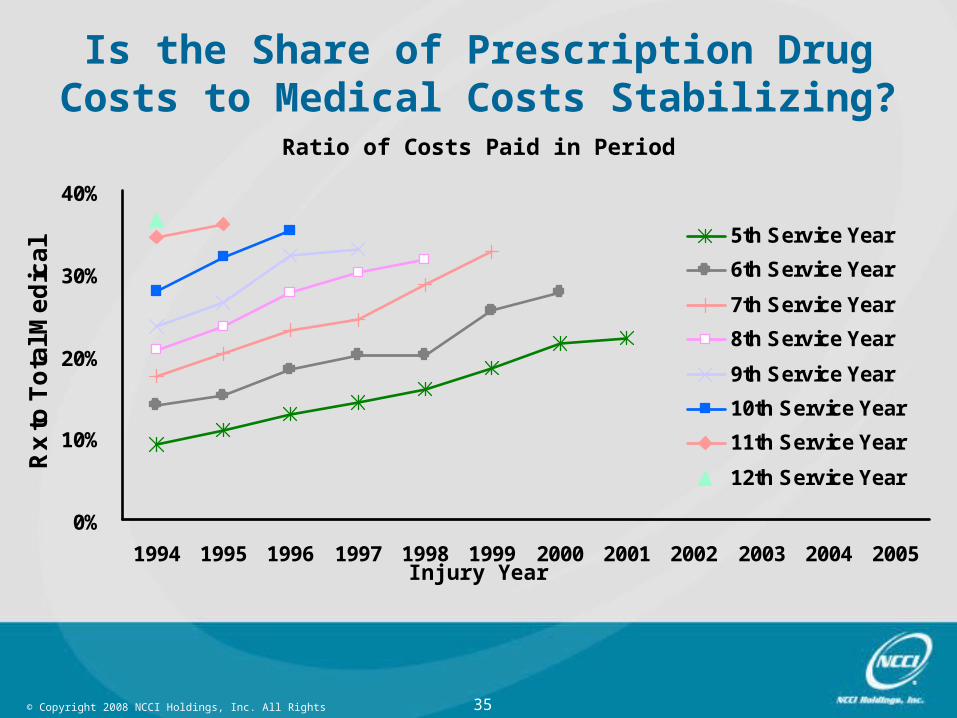

0%

10%

20%

30%

40%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Rx

to T

ota

l Me

dic

al 5th Service Year

6th Service Year

7th Service Year

8th Service Year

9th Service Year

10th Service Year

11th Service Year

12th Service Year

Is the Share of Prescription Drug Costs to Medical Costs Stabilizing?

Ratio of Costs Paid in Period

Injury Year

36© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Forecasting Rx Share of Medical Cost

Three scenarios naturally ariseLatest year is representative of the trendLatest year is an aberration; trend will continue at historical ratesTrends will continue at historical rates only after the fifth service year

We forecasted the Rx share under these three scenarios

37© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

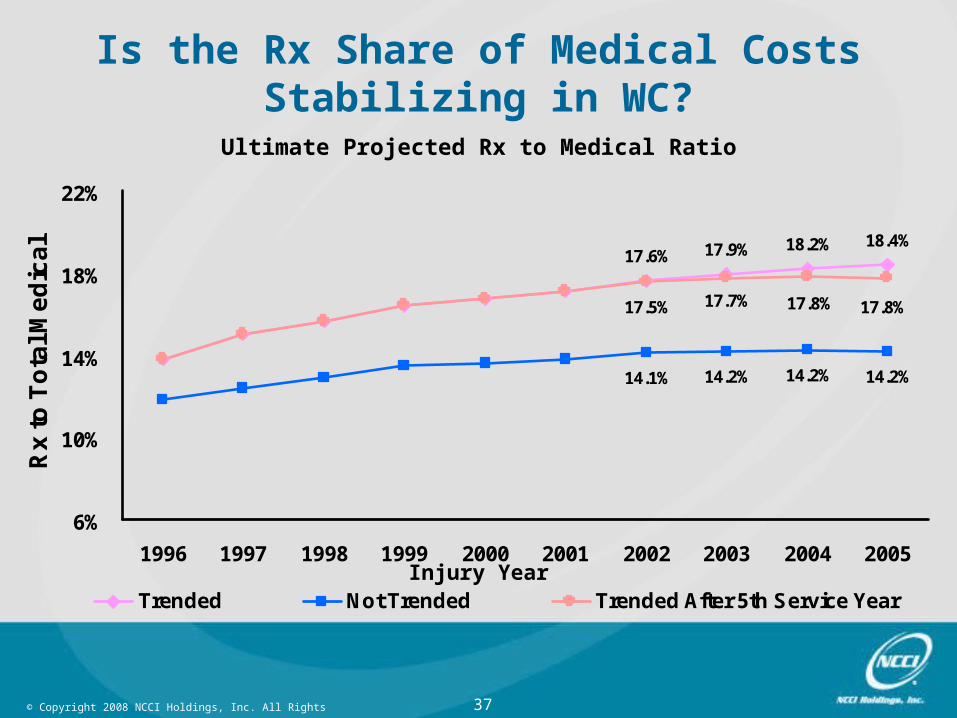

17.9%17.6%18.4%18.2%

14.1% 14.2% 14.2%14.2%

17.8%17.8%17.7%17.5%

6%

10%

14%

18%

22%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Rx

to

To

tal M

ed

ica

l

Trended Not Trended Trended After 5th Service Year

Is the Rx Share of Medical Costs Stabilizing in WC?

Ultimate Projected Rx to Medical Ratio

Injury Year

38© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

-10%

0%

10%

20%

30%

40%

1998–1999 1999–2000 2000–2001 2001–2002 2002–2003 2003–2004 2004–2005p

Pe

rce

nta

ge

Ch

an

ge

Drug Price Impact

Utilization Impact

Cost Impact

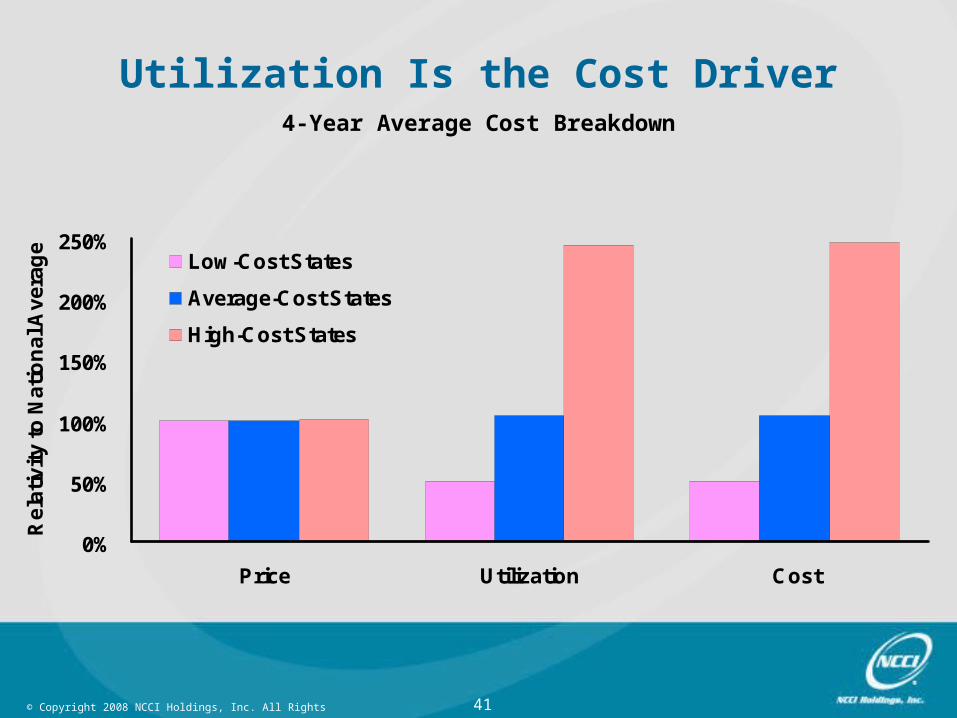

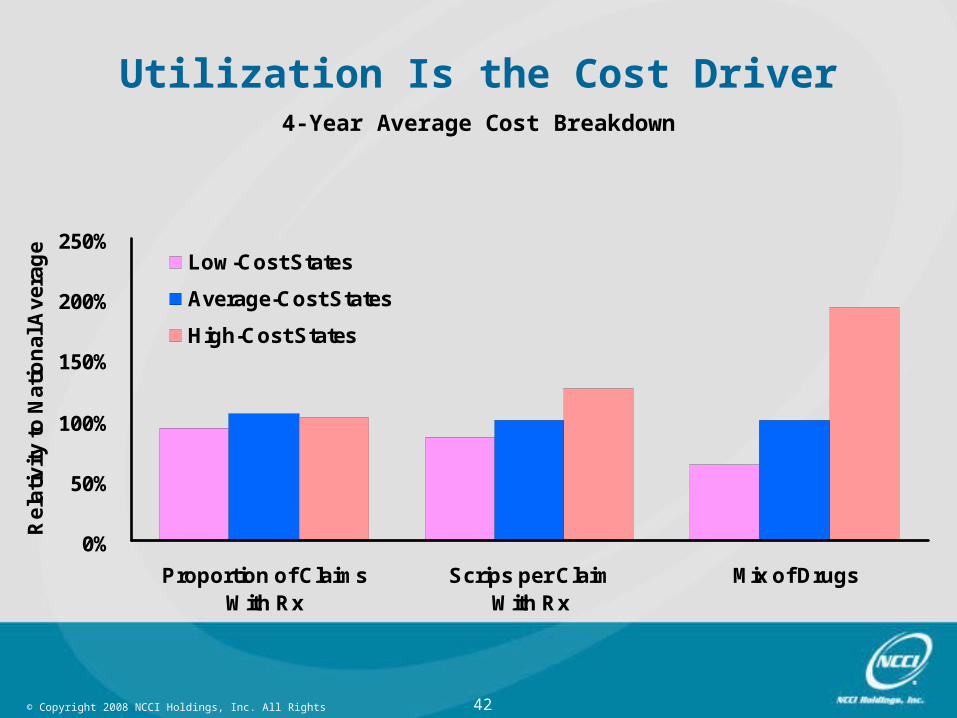

Utilization Is a Bigger Cost Driver Than Price

Drug Cost Breakdown

Service Yearp Preliminary

39© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Regional View

40© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

WC Rx Cost per Claim

Below Average

Average

Above Average

OR

MT

KS

NE

OK

LA

MS

KY

TN

FL

WI

IN

GA

MN

TX

CO

ID

UT

AR

AL

SC

VA

NC

AZ

IL

MI

IA

MO

CA

NH

MA

CT

MD

PA

DE

41© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

0%

50%

100%

150%

200%

250%

Price Utilization Cost

Re

lativ

ity

to N

atio

na

l Av

era

ge

Low-Cost States

Average-Cost States

High-Cost States

Utilization Is the Cost Driver4-Year Average Cost Breakdown

42© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

0%

50%

100%

150%

200%

250%

Proportion of ClaimsWith Rx

Scrips per ClaimWith Rx

Mix of Drugs

Re

lativ

ity

to N

atio

na

l Av

era

ge

Low-Cost States

Average-Cost States

High-Cost States

Utilization Is the Cost Driver4-Year Average Cost Breakdown

43© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Detailed View

44© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

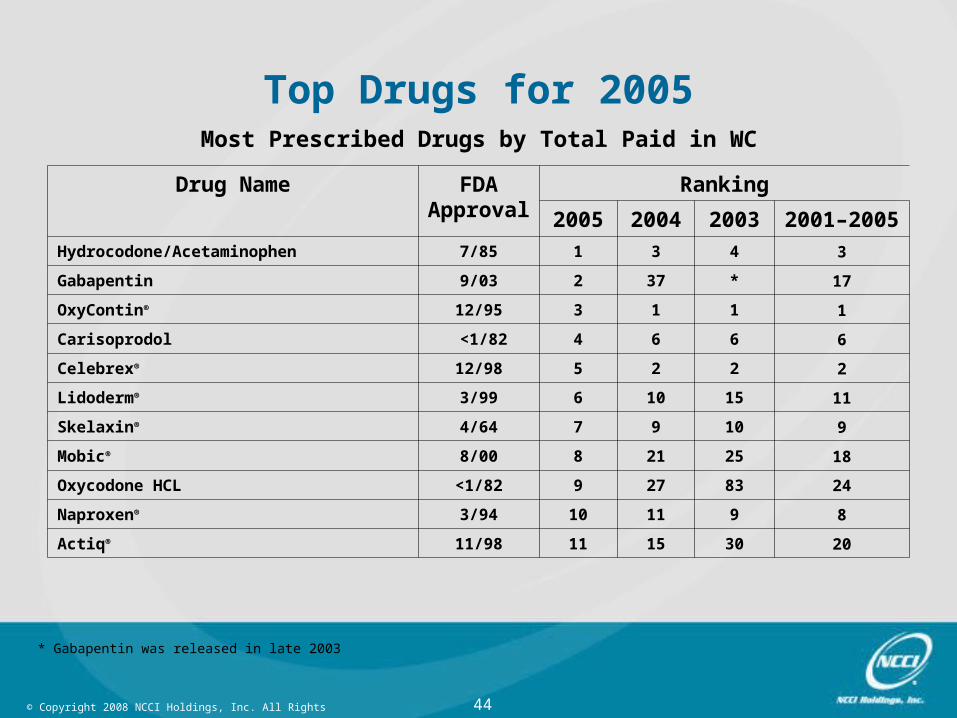

Top Drugs for 2005Most Prescribed Drugs by Total Paid in WC

Drug Name FDAApproval

Ranking

2005 2004 2003 2001–2005

Hydrocodone/Acetaminophen 7/85 1 3 4 3

Gabapentin 9/03 2 37 * 17

OxyContin® 12/95 3 1 1 1

Carisoprodol <1/82 4 6 6 6

Celebrex® 12/98 5 2 2 2

Lidoderm® 3/99 6 10 15 11

Skelaxin® 4/64 7 9 10 9

Mobic® 8/00 8 21 25 18

Oxycodone HCL <1/82 9 27 83 24

Naproxen® 3/94 10 11 9 8

Actiq® 11/98 11 15 30 20

* Gabapentin was released in late 2003

45© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

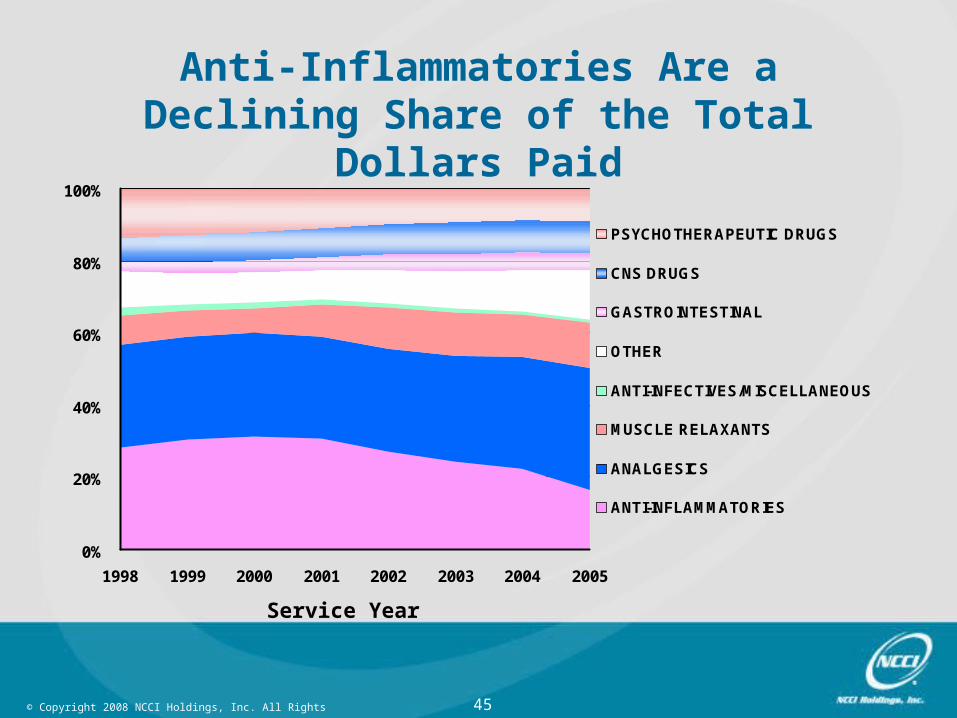

Anti-Inflammatories Are a Declining Share of the Total Dollars Paid

0%

20%

40%

60%

80%

100%

1998 1999 2000 2001 2002 2003 2004 2005

Service Year

PSYCHOTHERAPEUTIC DRUGS

CNS DRUGS

GASTROINTESTINAL

OTHER

ANTI-INFECTIVES/MISCELLANEOUS

MUSCLE RELAXANTS

ANALGESICS

ANTI-INFLAMMATORIES

46© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

0%

20%

40%

60%

80%

100%

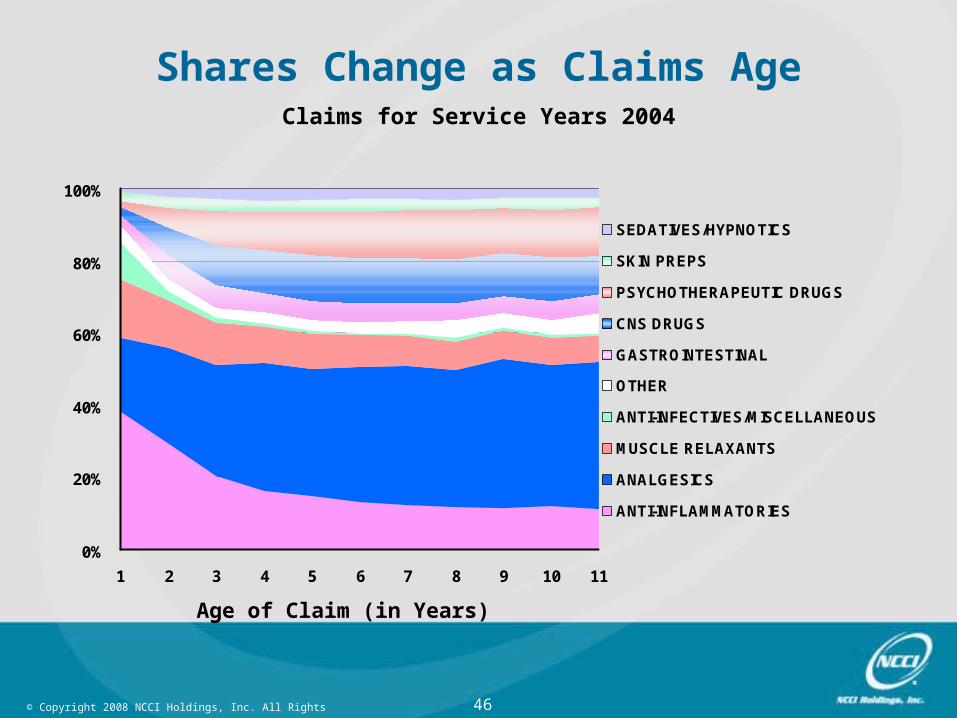

1 2 3 4 5 6 7 8 9 10 11

Age of Claim (in Years)

SEDATIVES/HYPNOTICS

SKIN PREPS

PSYCHOTHERAPEUTIC DRUGS

CNS DRUGS

GASTROINTESTINAL

OTHER

ANTI-INFECTIVES/MISCELLANEOUS

MUSCLE RELAXANTS

ANALGESICS

ANTI-INFLAMMATORIES

Shares Change as Claims AgeClaims for Service Years 2004

47© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

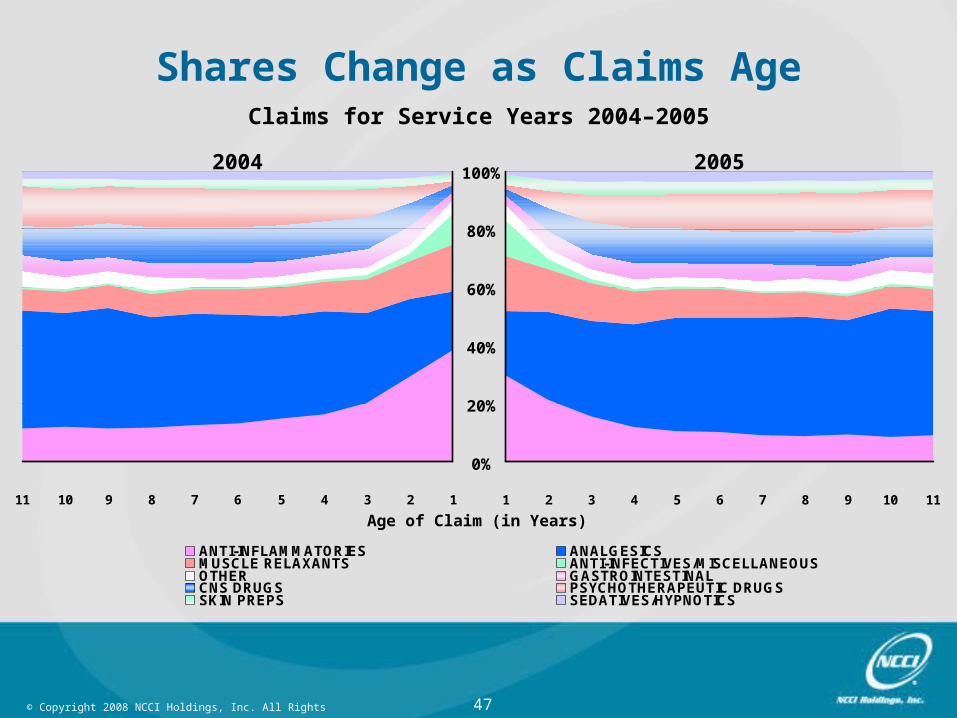

Shares Change as Claims AgeClaims for Service Years 2004–2005

ANTI-INFLAMMATORIES ANALGESICSMUSCLE RELAXANTS ANTI-INFECTIVES/MISCELLANEOUSOTHER GASTROINTESTINALCNS DRUGS PSYCHOTHERAPEUTIC DRUGSSKIN PREPS SEDATIVES/HYPNOTICS

1234567891011 1 2 3 4 5 6 7 8 9 10 11

Age of Claim (in Years)

100%

80%

60%

40%

20%

0%

2004 2005

48© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

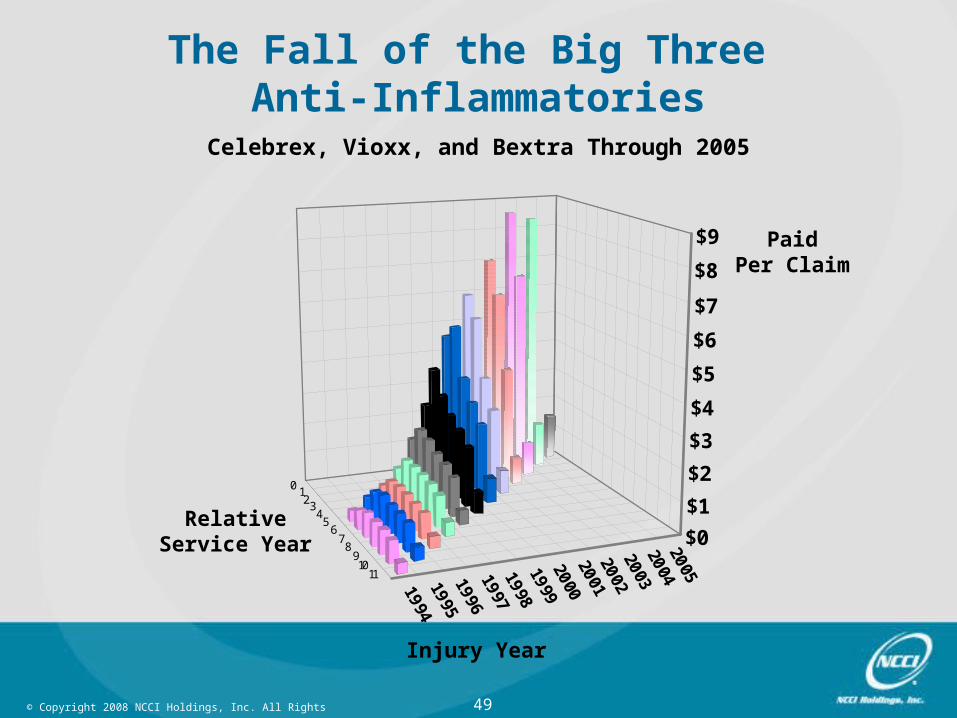

September 2004—Merck & Company voluntarily withdrew Vioxx® from the market

April 2005—At the request of the FDA, Pfizer voluntarily suspended sales of Bextra®

April 2005—The FDA allowed Pfizer to keep Celebrex® on the market, but with expanded risk information included in the labeling

The Fall of the Big Three Anti-Inflammatories

In 2003, Vioxx® ranked 5th, Bextra® ranked 7th, and Celebrex® ranked 2nd in terms of total dollars paid.

49© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

0123

45

678

910

11

199419951996199719981999200020012002200320042005

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

The Fall of the Big Three Anti-Inflammatories

Celebrex, Vioxx, and Bextra Through 2005

Injury Year

RelativeService Year

PaidPer Claim

50© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

012

345

67

8910

11199419951996199719981999200020012002200320042005

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

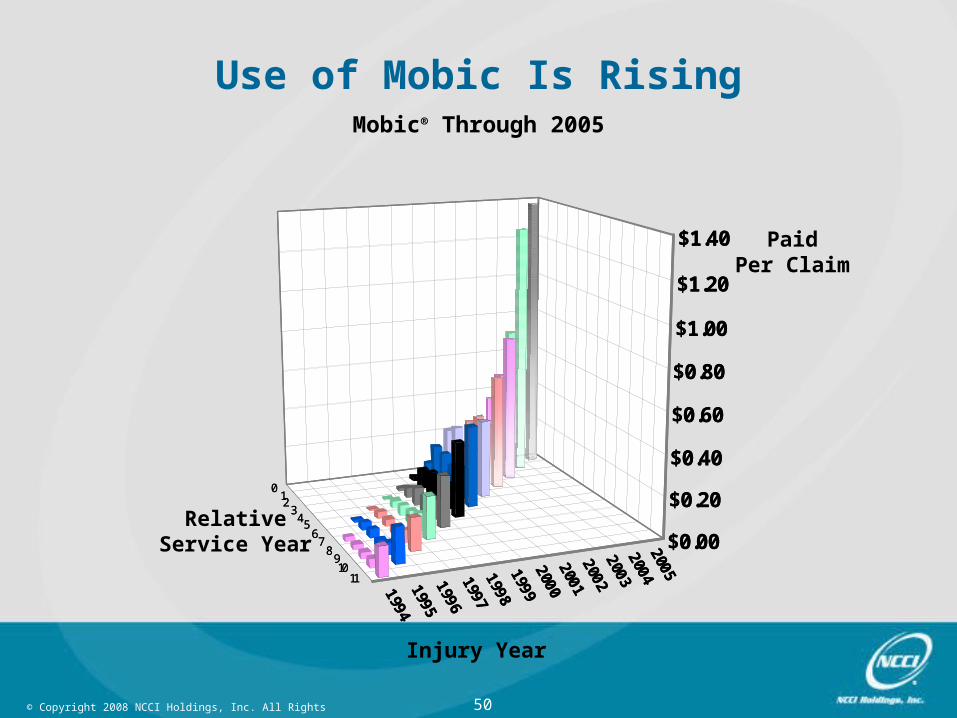

Use of Mobic Is RisingMobic® Through 2005

012

345

67

8910

11199419951996199719981999200020012002200320042005

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

Injury Year

RelativeService Year

PaidPer Claim

51© Copyright 2008 NCCI Holdings, Inc. All Rights Reserved.

Comments & DiscussionComments & Discussion

![Dynamic Reductions for Model Checking Concurrent Softwarealfons.laarman.com/slides/vmcai_2017_dynamic.pdf · Lipton Reduction [Lipton ’77, Lamport et al. ’89] Lipton Reduction](https://img.pdfslide.net/doc/110x75/5fd446796552407308296f61/dynamic-reductions-for-model-checking-concurrent-lipton-reduction-lipton-a77.jpg)