Embed Size (px)

Citation preview

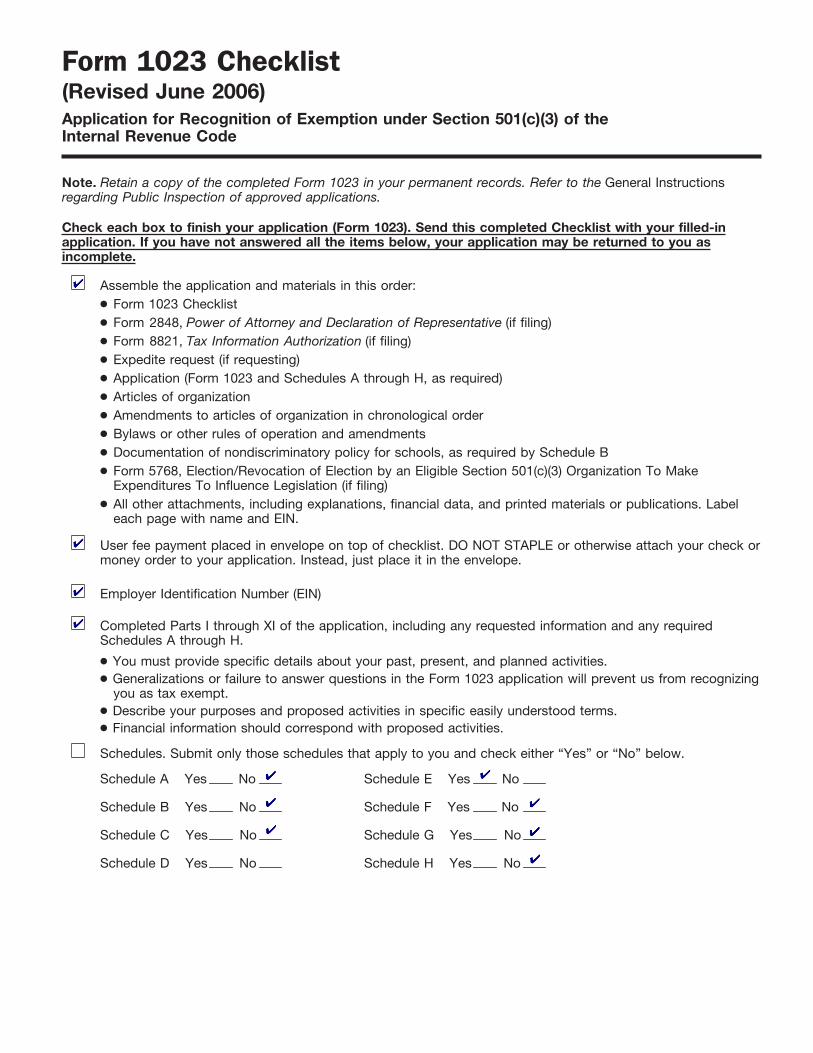

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

TLS, have youtransmitted all Rtext files for thiscycle update?

Date

Action

Revised proofsrequested

Date Signature

O.K. to print

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 1 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. June 2006)

Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code

OMB No. 1545-0056

Department of the Treasury Internal Revenue Service

Note: If exempt status is approved, this application will be open for public inspection.

For Paperwork Reduction Act Notice, see page 24 of the instructions. Cat. No. 17133K

Use the instructions to complete this application and for a definition of all bold items. For additional help, call IRS Exempt Organizations Customer Account Services toll-free at 1-877-829-5500. Visit our website at www.irs.gov for forms and publications. If the required information and documents are not submitted with payment of the appropriate user fee, the application may be returned to you.

Attach additional sheets to this application if you need more space to answer fully. Put your name and EIN on each sheet and identify each answer by Part and line number. Complete Parts I - XI of Form 1023 and submit only those Schedules (A through H) that apply to you.

Part I Identification of Applicant

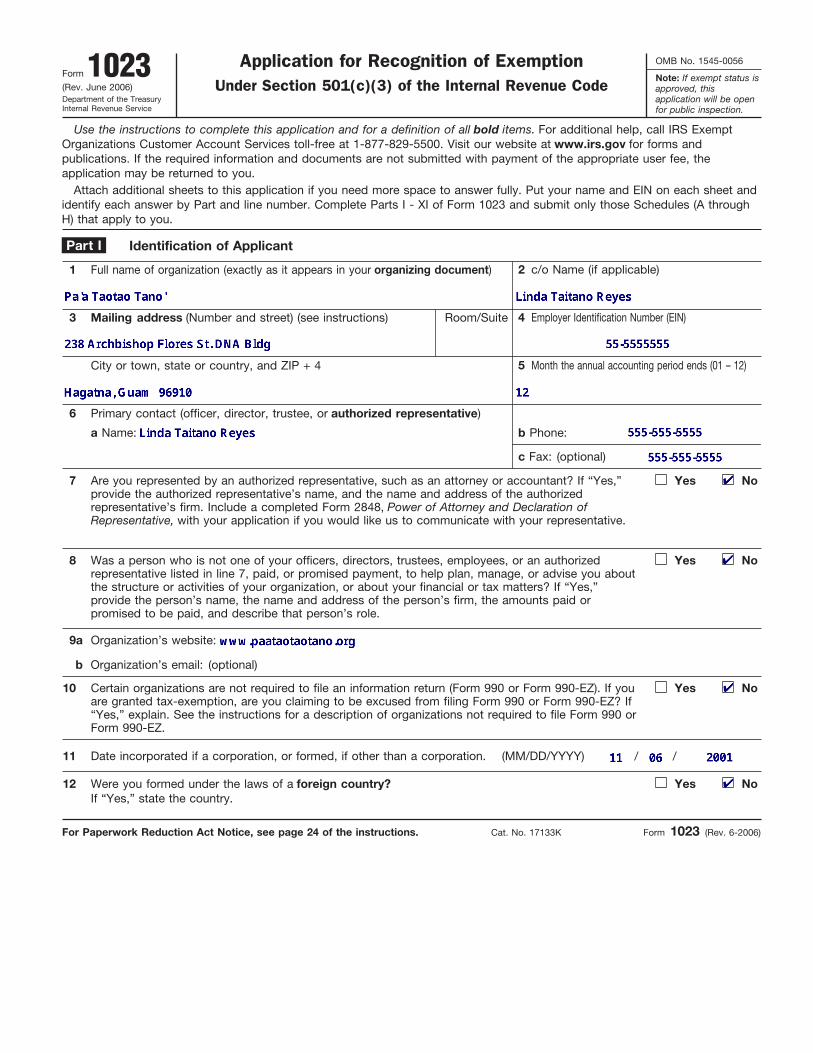

1 Full name of organization (exactly as it appears in your organizing document) 2 c/o Name (if applicable)

3 Mailing address (Number and street) (see instructions) Room/Suite

City or town, state or country, and ZIP + 4

4 Employer Identification Number (EIN)

5 Month the annual accounting period ends (01 – 12)

6 Primary contact (officer, director, trustee, or authorized representative)

a Name: b Phone:

c Fax: (optional)

7 Are you represented by an authorized representative, such as an attorney or accountant? If “Yes,” provide the authorized representative’s name, and the name and address of the authorized representative’s firm. Include a completed Form 2848, Power of Attorney and Declaration of Representative, with your application if you would like us to communicate with your representative.

Yes No

8 Was a person who is not one of your officers, directors, trustees, employees, or an authorized representative listed in line 7, paid, or promised payment, to help plan, manage, or advise you about the structure or activities of your organization, or about your financial or tax matters? If “Yes,” provide the person’s name, the name and address of the person’s firm, the amounts paid or promised to be paid, and describe that person’s role.

Yes No

9a Organization’s website:

b Organization’s email: (optional)

10 Certain organizations are not required to file an information return (Form 990 or Form 990-EZ). If you are granted tax-exemption, are you claiming to be excused from filing Form 990 or Form 990-EZ? If “Yes,” explain. See the instructions for a description of organizations not required to file Form 990 or Form 990-EZ.

Yes No

11 Date incorporated if a corporation, or formed, if other than a corporation. (MM/DD/YYYY) / /

12 Were you formed under the laws of a foreign country? Yes No If “Yes,” state the country.

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 2 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. 6-2006) Page 2Name: EIN: – Part II Organizational Structure

You must be a corporation (including a limited liability company), an unincorporated association, or a trust to be tax exempt. (See instructions.) DO NOT file this form unless you can check “Yes” on lines 1, 2, 3, or 4.

1 Are you a corporation? If “Yes,” attach a copy of your articles of incorporation showing certification of filing with the appropriate state agency. Include copies of any amendments to your articles and be sure they also show state filing certification.

Yes No

2 Are you a limited liability company (LLC)? If “Yes,” attach a copy of your articles of organization showing certification of filing with the appropriate state agency. Also, if you adopted an operating agreement, attach a copy. Include copies of any amendments to your articles and be sure they show state filing certification. Refer to the instructions for circumstances when an LLC should not file its own exemption application.

Yes No

3 Are you an unincorporated association? If “Yes,” attach a copy of your articles of association, constitution, or other similar organizing document that is dated and includes at least two signatures. Include signed and dated copies of any amendments.

Yes No

4a Are you a trust? If “Yes,” attach a signed and dated copy of your trust agreement. Include signed and dated copies of any amendments.

Yes No

b Have you been funded? If “No,” explain how you are formed without anything of value placed in trust. Yes No 5 Have you adopted bylaws? If “Yes,” attach a current copy showing date of adoption. If “No,” explain

how your officers, directors, or trustees are selected. Yes No

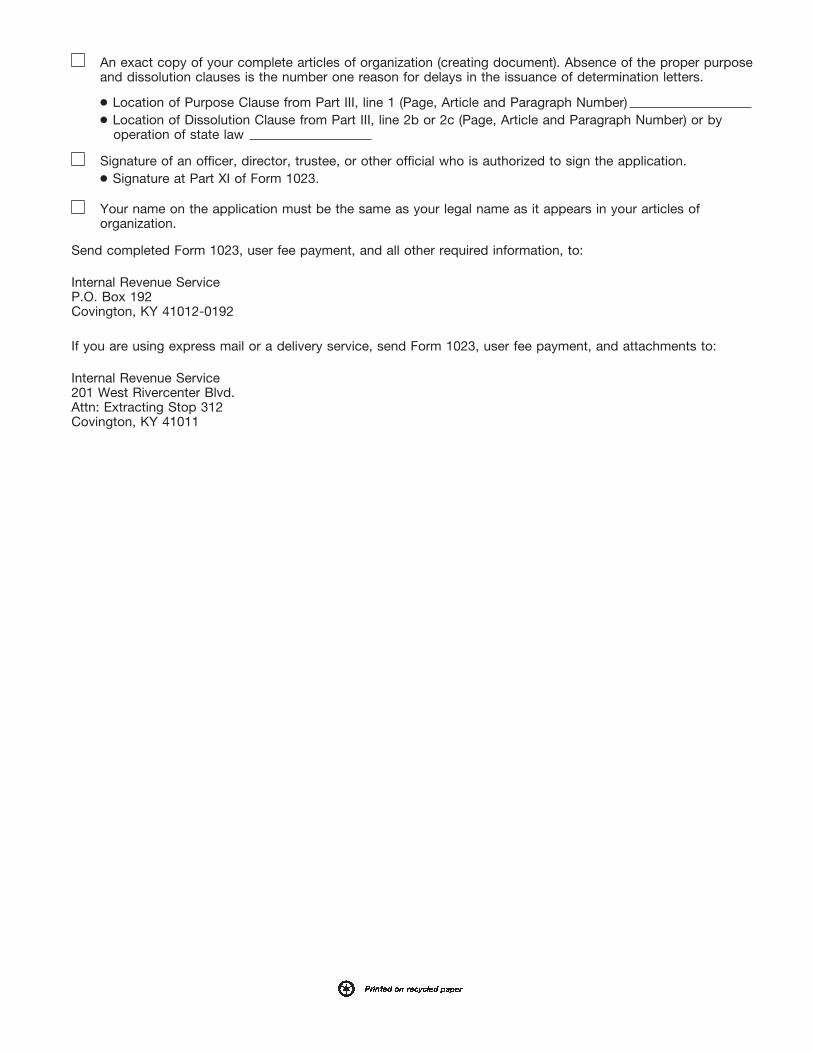

Part III Required Provisions in Your Organizing Document The following questions are designed to ensure that when you file this application, your organizing document contains the required provisions to meet the organizational test under section 501(c)(3). Unless you can check the boxes in both lines 1 and 2, your organizing document does not meet the organizational test. DO NOT file this application until you have amended your organizing document. Submit your original and amended organizing documents (showing state filing certification if you are a corporation or an LLC) with your application.

1 Section 501(c)(3) requires that your organizing document state your exempt purpose(s), such as charitable, religious, educational, and/or scientific purposes. Check the box to confirm that your organizing document meets this requirement. Describe specifically where your organizing document meets this requirement, such as a reference to a particular article or section in your organizing document. Refer to the instructions for exempt purpose language. Location of Purpose Clause (Page, Article, and Paragraph):

2a Section 501(c)(3) requires that upon dissolution of your organization, your remaining assets must be used exclusively for exempt purposes, such as charitable, religious, educational, and/or scientific purposes. Check the box on line 2a to confirm that your organizing document meets this requirement by express provision for the distribution of assets upon dissolution. If you rely on state law for your dissolution provision, do not check the box on line 2a and go to line 2c.

2b If you checked the box on line 2a, specify the location of your dissolution clause (Page, Article, and Paragraph). Do not complete line 2c if you checked box 2a.

2c See the instructions for information about the operation of state law in your particular state. Check this box if you rely on operation of state law for your dissolution provision and indicate the state:

Part IV Narrative Description of Your Activities

Using an attachment, describe your past, present, and planned activities in a narrative. If you believe that you have already provided some of this information in response to other parts of this application, you may summarize that information here and refer to the specific parts of the application for supporting details. You may also attach representative copies of newsletters, brochures, or similar documents for supporting details to this narrative. Remember that if this application is approved, it will be open for public inspection. Therefore, your narrative description of activities should be thorough and accurate. Refer to the instructions for information that must be included in your description.

Part V Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees, Employees, and Independent Contractors

1a List the names, titles, and mailing addresses of all of your officers, directors, and trustees. For each person listed, state their total annual compensation, or proposed compensation, for all services to the organization, whether as an officer, employee, or other position. Use actual figures, if available. Enter “none” if no compensation is or will be paid. If additional space is needed, attach a separate sheet. Refer to the instructions for information on what to include as compensation.

Name Title Mailing address Compensation amount (annual actual or estimated)

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 3 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

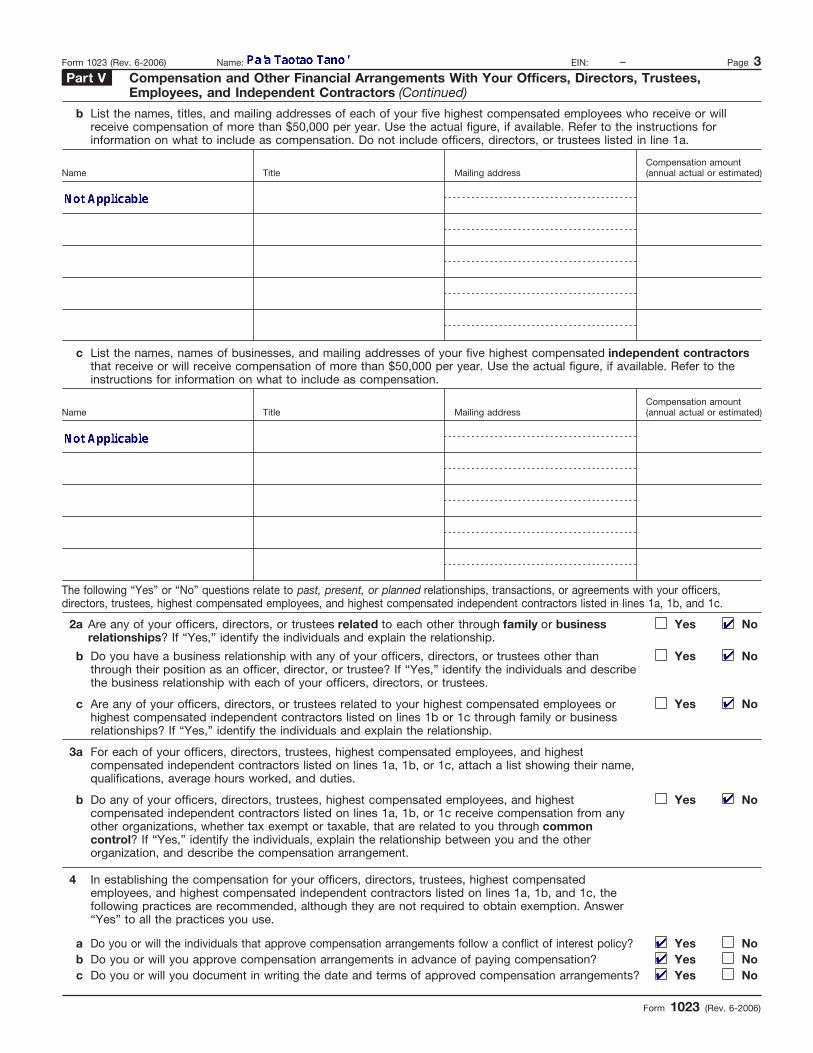

Form 1023 (Rev. 6-2006) Name: EIN: – Page 3 Part V Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees,

Employees, and Independent Contractors (Continued)

b List the names, titles, and mailing addresses of each of your five highest compensated employees who receive or will receive compensation of more than $50,000 per year. Use the actual figure, if available. Refer to the instructions for information on what to include as compensation. Do not include officers, directors, or trustees listed in line 1a.

Name Title Mailing address Compensation amount (annual actual or estimated)

c List the names, names of businesses, and mailing addresses of your five highest compensated independent contractors that receive or will receive compensation of more than $50,000 per year. Use the actual figure, if available. Refer to the instructions for information on what to include as compensation.

Name Title Mailing address Compensation amount (annual actual or estimated)

The following “Yes” or “No” questions relate to past, present, or planned relationships, transactions, or agreements with your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed in lines 1a, 1b, and 1c.

2a Are any of your officers, directors, or trustees related to each other through family or business relationships? If “Yes,” identify the individuals and explain the relationship.

Yes No

b Do you have a business relationship with any of your officers, directors, or trustees other than through their position as an officer, director, or trustee? If “Yes,” identify the individuals and describe the business relationship with each of your officers, directors, or trustees.

Yes No

c Are any of your officers, directors, or trustees related to your highest compensated employees or highest compensated independent contractors listed on lines 1b or 1c through family or business relationships? If “Yes,” identify the individuals and explain the relationship.

Yes No

3a For each of your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed on lines 1a, 1b, or 1c, attach a list showing their name, qualifications, average hours worked, and duties.

b Do any of your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed on lines 1a, 1b, or 1c receive compensation from any other organizations, whether tax exempt or taxable, that are related to you through common control? If “Yes,” identify the individuals, explain the relationship between you and the other organization, and describe the compensation arrangement.

Yes No

4 In establishing the compensation for your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed on lines 1a, 1b, and 1c, the following practices are recommended, although they are not required to obtain exemption. Answer “Yes” to all the practices you use.

a Do you or will the individuals that approve compensation arrangements follow a conflict of interest policy? Yes No b Do you or will you approve compensation arrangements in advance of paying compensation? Yes No c Do you or will you document in writing the date and terms of approved compensation arrangements? Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 4 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

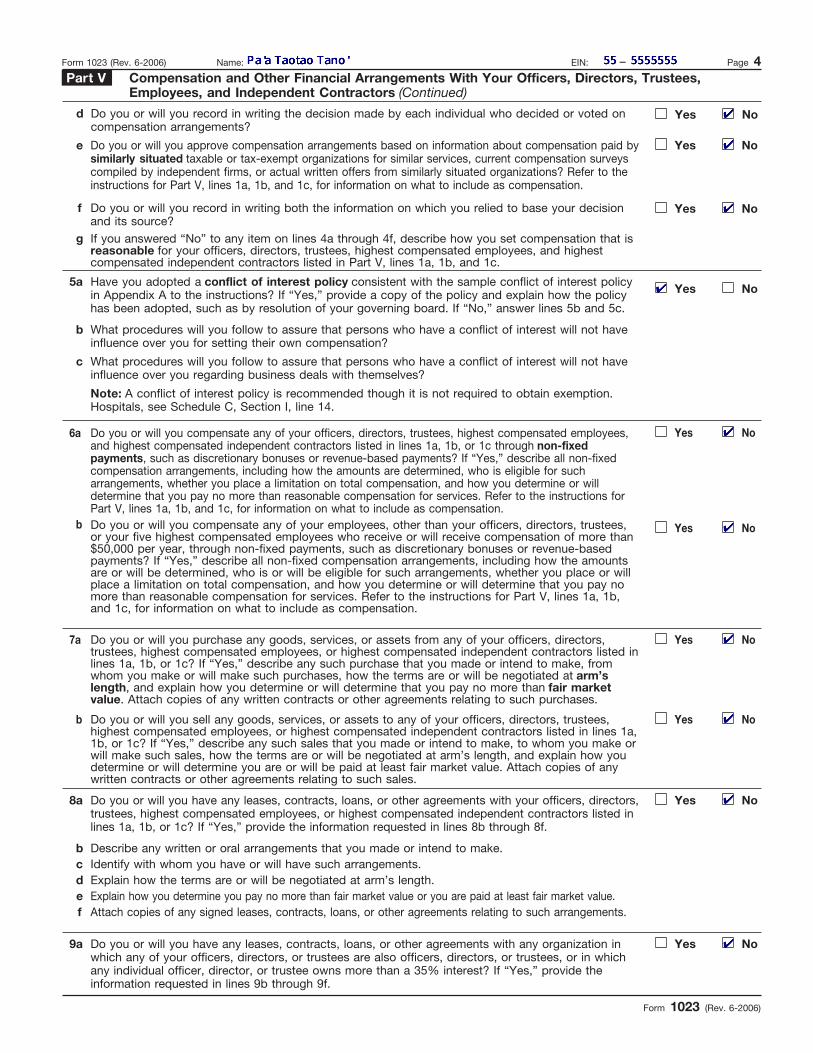

Form 1023 (Rev. 6-2006) Name: EIN: – Page 4 Part V Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees,

Employees, and Independent Contractors (Continued)

d Do you or will you record in writing the decision made by each individual who decided or voted on compensation arrangements?

Yes No

e Do you or will you approve compensation arrangements based on information about compensation paid by similarly situated taxable or tax-exempt organizations for similar services, current compensation surveys compiled by independent firms, or actual written offers from similarly situated organizations? Refer to the instructions for Part V, lines 1a, 1b, and 1c, for information on what to include as compensation.

Yes No

f Do you or will you record in writing both the information on which you relied to base your decision and its source?

Yes No

g If you answered “No” to any item on lines 4a through 4f, describe how you set compensation that is reasonable for your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed in Part V, lines 1a, 1b, and 1c.

5a Have you adopted a conflict of interest policy consistent with the sample conflict of interest policy in Appendix A to the instructions? If “Yes,” provide a copy of the policy and explain how the policy has been adopted, such as by resolution of your governing board. If “No,” answer lines 5b and 5c.

Yes No

b What procedures will you follow to assure that persons who have a conflict of interest will not have influence over you for setting their own compensation?

c What procedures will you follow to assure that persons who have a conflict of interest will not have influence over you regarding business deals with themselves?

Note: A conflict of interest policy is recommended though it is not required to obtain exemption. Hospitals, see Schedule C, Section I, line 14.

6a Do you or will you compensate any of your officers, directors, trustees, highest compensated employees, and highest compensated independent contractors listed in lines 1a, 1b, or 1c through non-fixed payments, such as discretionary bonuses or revenue-based payments? If “Yes,” describe all non-fixed compensation arrangements, including how the amounts are determined, who is eligible for such arrangements, whether you place a limitation on total compensation, and how you determine or will determine that you pay no more than reasonable compensation for services. Refer to the instructions for Part V, lines 1a, 1b, and 1c, for information on what to include as compensation.

Yes No

b Do you or will you compensate any of your employees, other than your officers, directors, trustees, or your five highest compensated employees who receive or will receive compensation of more than $50,000 per year, through non-fixed payments, such as discretionary bonuses or revenue-based payments? If “Yes,” describe all non-fixed compensation arrangements, including how the amounts are or will be determined, who is or will be eligible for such arrangements, whether you place or will place a limitation on total compensation, and how you determine or will determine that you pay no more than reasonable compensation for services. Refer to the instructions for Part V, lines 1a, 1b, and 1c, for information on what to include as compensation.

Yes No

7a Do you or will you purchase any goods, services, or assets from any of your officers, directors, trustees, highest compensated employees, or highest compensated independent contractors listed in lines 1a, 1b, or 1c? If “Yes,” describe any such purchase that you made or intend to make, from whom you make or will make such purchases, how the terms are or will be negotiated at arm’s length, and explain how you determine or will determine that you pay no more than fair market value. Attach copies of any written contracts or other agreements relating to such purchases.

Yes No

b Do you or will you sell any goods, services, or assets to any of your officers, directors, trustees, highest compensated employees, or highest compensated independent contractors listed in lines 1a, 1b, or 1c? If “Yes,” describe any such sales that you made or intend to make, to whom you make or will make such sales, how the terms are or will be negotiated at arm’s length, and explain how you determine or will determine you are or will be paid at least fair market value. Attach copies of any written contracts or other agreements relating to such sales.

Yes No

8a Do you or will you have any leases, contracts, loans, or other agreements with your officers, directors, trustees, highest compensated employees, or highest compensated independent contractors listed in lines 1a, 1b, or 1c? If “Yes,” provide the information requested in lines 8b through 8f.

Yes No

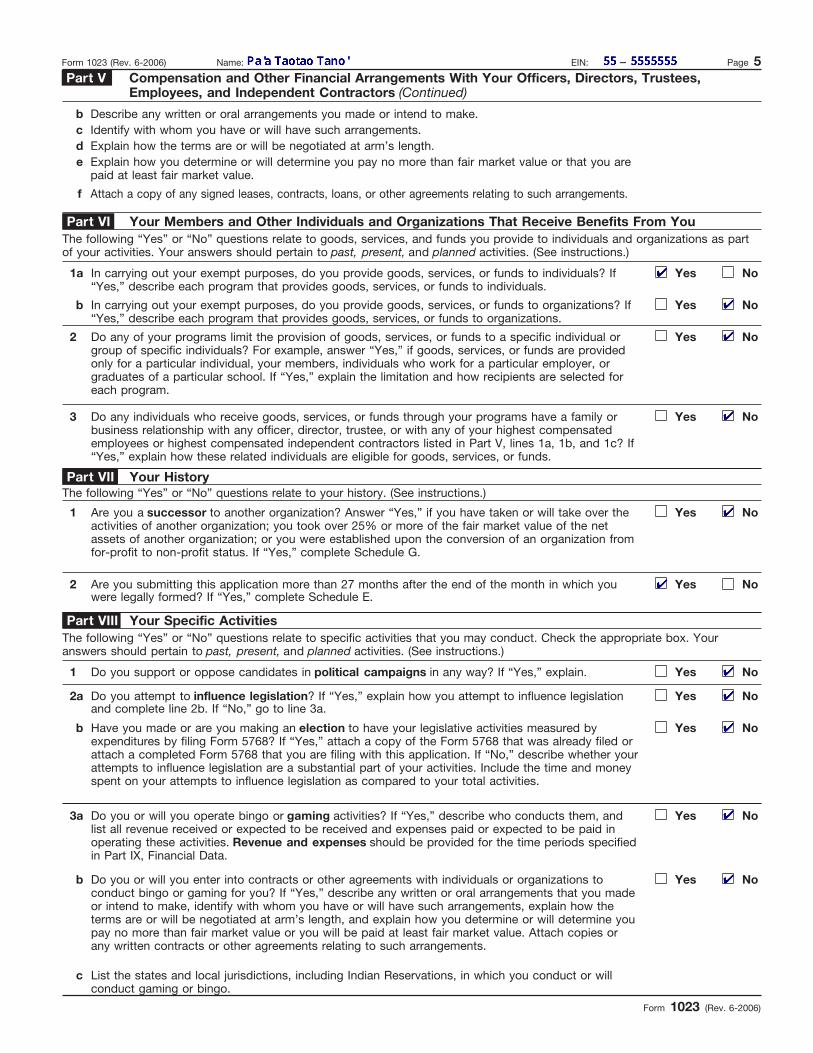

b Describe any written or oral arrangements that you made or intend to make. c Identify with whom you have or will have such arrangements. d Explain how the terms are or will be negotiated at arm’s length. e Explain how you determine you pay no more than fair market value or you are paid at least fair market value. f Attach copies of any signed leases, contracts, loans, or other agreements relating to such arrangements.

9a Do you or will you have any leases, contracts, loans, or other agreements with any organization in which any of your officers, directors, or trustees are also officers, directors, or trustees, or in which any individual officer, director, or trustee owns more than a 35% interest? If “Yes,” provide the information requested in lines 9b through 9f.

Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 5 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. 6-2006) Name: EIN: – Page 5 Part V Compensation and Other Financial Arrangements With Your Officers, Directors, Trustees,

Employees, and Independent Contractors (Continued)

b Describe any written or oral arrangements you made or intend to make. c Identify with whom you have or will have such arrangements. d Explain how the terms are or will be negotiated at arm’s length. e Explain how you determine or will determine you pay no more than fair market value or that you are

paid at least fair market value.

f Attach a copy of any signed leases, contracts, loans, or other agreements relating to such arrangements.

Part VI Your Members and Other Individuals and Organizations That Receive Benefits From You The following “Yes” or “No” questions relate to goods, services, and funds you provide to individuals and organizations as part of your activities. Your answers should pertain to past, present, and planned activities. (See instructions.)

1a In carrying out your exempt purposes, do you provide goods, services, or funds to individuals? If “Yes,” describe each program that provides goods, services, or funds to individuals.

Yes No

b In carrying out your exempt purposes, do you provide goods, services, or funds to organizations? If “Yes,” describe each program that provides goods, services, or funds to organizations.

Yes No

2 Do any of your programs limit the provision of goods, services, or funds to a specific individual or group of specific individuals? For example, answer “Yes,” if goods, services, or funds are provided only for a particular individual, your members, individuals who work for a particular employer, or graduates of a particular school. If “Yes,” explain the limitation and how recipients are selected for each program.

Yes No

3 Do any individuals who receive goods, services, or funds through your programs have a family or business relationship with any officer, director, trustee, or with any of your highest compensated employees or highest compensated independent contractors listed in Part V, lines 1a, 1b, and 1c? If “Yes,” explain how these related individuals are eligible for goods, services, or funds.

Yes No

Part VII Your History The following “Yes” or “No” questions relate to your history. (See instructions.)

1 Are you a successor to another organization? Answer “Yes,” if you have taken or will take over the activities of another organization; you took over 25% or more of the fair market value of the net assets of another organization; or you were established upon the conversion of an organization from for-profit to non-profit status. If “Yes,” complete Schedule G.

Yes No

2 Are you submitting this application more than 27 months after the end of the month in which you were legally formed? If “Yes,” complete Schedule E.

Yes No

Part VIII Your Specific Activities The following “Yes” or “No” questions relate to specific activities that you may conduct. Check the appropriate box. Your answers should pertain to past, present, and planned activities. (See instructions.)

1 Do you support or oppose candidates in political campaigns in any way? If “Yes,” explain. Yes No

2a Do you attempt to influence legislation? If “Yes,” explain how you attempt to influence legislation and complete line 2b. If “No,” go to line 3a.

Yes No

b Have you made or are you making an election to have your legislative activities measured by expenditures by filing Form 5768? If “Yes,” attach a copy of the Form 5768 that was already filed or attach a completed Form 5768 that you are filing with this application. If “No,” describe whether your attempts to influence legislation are a substantial part of your activities. Include the time and money spent on your attempts to influence legislation as compared to your total activities.

Yes No

3a Do you or will you operate bingo or gaming activities? If “Yes,” describe who conducts them, and list all revenue received or expected to be received and expenses paid or expected to be paid in operating these activities. Revenue and expenses should be provided for the time periods specified in Part IX, Financial Data.

Yes No

b Do you or will you enter into contracts or other agreements with individuals or organizations to conduct bingo or gaming for you? If “Yes,” describe any written or oral arrangements that you made or intend to make, identify with whom you have or will have such arrangements, explain how the terms are or will be negotiated at arm’s length, and explain how you determine or will determine you pay no more than fair market value or you will be paid at least fair market value. Attach copies or any written contracts or other agreements relating to such arrangements.

Yes No

c List the states and local jurisdictions, including Indian Reservations, in which you conduct or will conduct gaming or bingo.

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 6 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

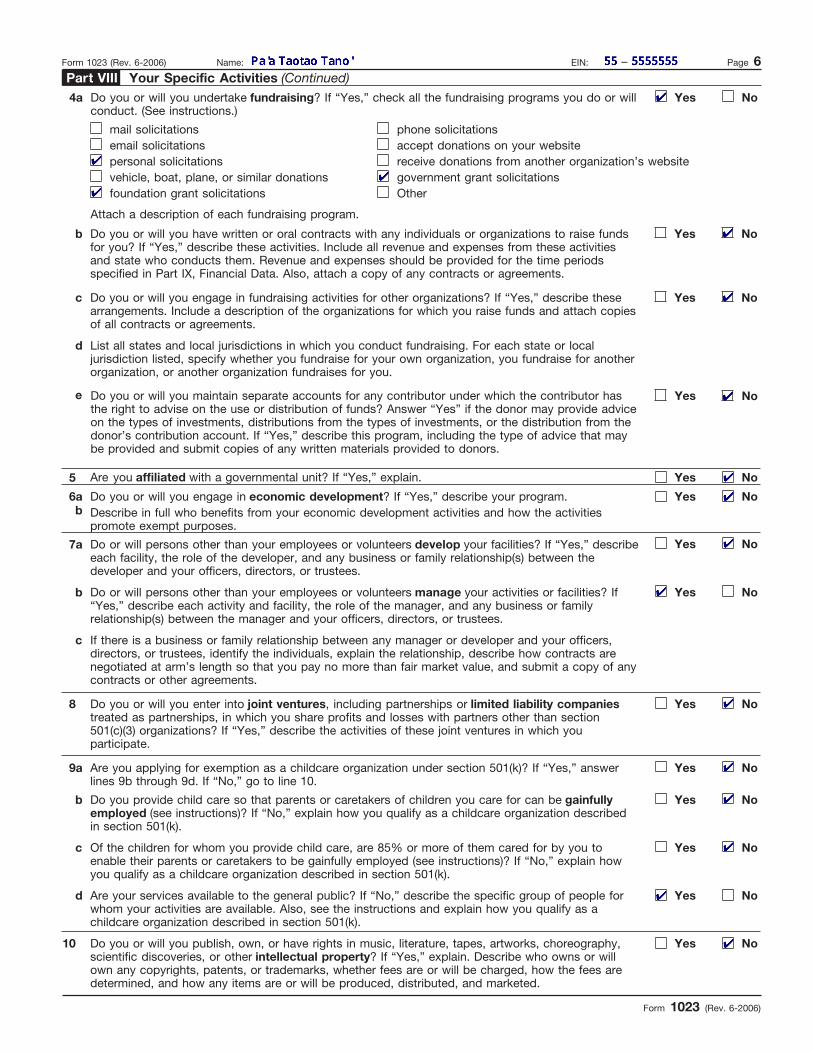

Form 1023 (Rev. 6-2006) Name: EIN: – Page 6 Part VIII Your Specific Activities (Continued) 4a Do you or will you undertake fundraising? If “Yes,” check all the fundraising programs you do or will

conduct. (See instructions.) Yes No

mail solicitations email solicitations personal solicitations vehicle, boat, plane, or similar donations foundation grant solicitations

phone solicitations accept donations on your website receive donations from another organization’s website government grant solicitations Other

Attach a description of each fundraising program.

b Do you or will you have written or oral contracts with any individuals or organizations to raise funds for you? If “Yes,” describe these activities. Include all revenue and expenses from these activities and state who conducts them. Revenue and expenses should be provided for the time periods specified in Part IX, Financial Data. Also, attach a copy of any contracts or agreements.

Yes No

c Do you or will you engage in fundraising activities for other organizations? If “Yes,” describe these arrangements. Include a description of the organizations for which you raise funds and attach copies of all contracts or agreements.

Yes No

d List all states and local jurisdictions in which you conduct fundraising. For each state or local jurisdiction listed, specify whether you fundraise for your own organization, you fundraise for another organization, or another organization fundraises for you.

e Do you or will you maintain separate accounts for any contributor under which the contributor has the right to advise on the use or distribution of funds? Answer “Yes” if the donor may provide advice on the types of investments, distributions from the types of investments, or the distribution from the donor’s contribution account. If “Yes,” describe this program, including the type of advice that may be provided and submit copies of any written materials provided to donors.

Yes No

5 Are you affiliated with a governmental unit? If “Yes,” explain. Yes No

6a Do you or will you engage in economic development? If “Yes,” describe your program. Yes No b Describe in full who benefits from your economic development activities and how the activities

promote exempt purposes.

7a Do or will persons other than your employees or volunteers develop your facilities? If “Yes,” describe each facility, the role of the developer, and any business or family relationship(s) between the developer and your officers, directors, or trustees.

Yes No

b Do or will persons other than your employees or volunteers manage your activities or facilities? If “Yes,” describe each activity and facility, the role of the manager, and any business or family relationship(s) between the manager and your officers, directors, or trustees.

Yes No

c If there is a business or family relationship between any manager or developer and your officers, directors, or trustees, identify the individuals, explain the relationship, describe how contracts are negotiated at arm’s length so that you pay no more than fair market value, and submit a copy of any contracts or other agreements.

8 Do you or will you enter into joint ventures, including partnerships or limited liability companies treated as partnerships, in which you share profits and losses with partners other than section 501(c)(3) organizations? If “Yes,” describe the activities of these joint ventures in which you participate.

Yes No

9a Are you applying for exemption as a childcare organization under section 501(k)? If “Yes,” answer lines 9b through 9d. If “No,” go to line 10.

Yes No

b Do you provide child care so that parents or caretakers of children you care for can be gainfully employed (see instructions)? If “No,” explain how you qualify as a childcare organization described in section 501(k).

Yes No

c Of the children for whom you provide child care, are 85% or more of them cared for by you to enable their parents or caretakers to be gainfully employed (see instructions)? If “No,” explain how you qualify as a childcare organization described in section 501(k).

Yes No

d Are your services available to the general public? If “No,” describe the specific group of people for whom your activities are available. Also, see the instructions and explain how you qualify as a childcare organization described in section 501(k).

Yes No

10 Do you or will you publish, own, or have rights in music, literature, tapes, artworks, choreography, scientific discoveries, or other intellectual property? If “Yes,” explain. Describe who owns or will own any copyrights, patents, or trademarks, whether fees are or will be charged, how the fees are determined, and how any items are or will be produced, distributed, and marketed.

Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 7 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. 6-2006) Name: EIN: – Page 7 Part VIII Your Specific Activities (Continued)

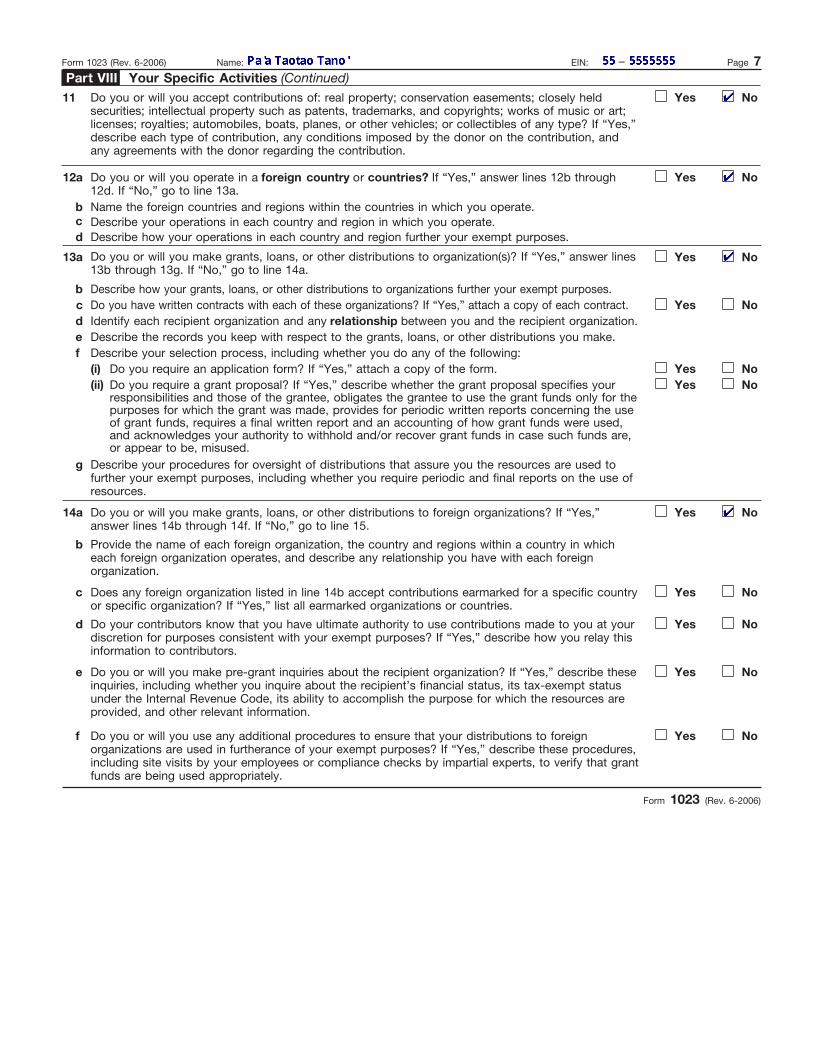

11 Do you or will you accept contributions of: real property; conservation easements; closely held securities; intellectual property such as patents, trademarks, and copyrights; works of music or art; licenses; royalties; automobiles, boats, planes, or other vehicles; or collectibles of any type? If “Yes,” describe each type of contribution, any conditions imposed by the donor on the contribution, and any agreements with the donor regarding the contribution.

Yes No

12a Do you or will you operate in a foreign country or countries? If “Yes,” answer lines 12b through 12d. If “No,” go to line 13a.

Yes No

b Name the foreign countries and regions within the countries in which you operate. c Describe your operations in each country and region in which you operate. d Describe how your operations in each country and region further your exempt purposes.

13a Do you or will you make grants, loans, or other distributions to organization(s)? If “Yes,” answer lines 13b through 13g. If “No,” go to line 14a.

Yes No

b Describe how your grants, loans, or other distributions to organizations further your exempt purposes. c Do you have written contracts with each of these organizations? If “Yes,” attach a copy of each contract. Yes No d Identify each recipient organization and any relationship between you and the recipient organization. e Describe the records you keep with respect to the grants, loans, or other distributions you make. f Describe your selection process, including whether you do any of the following:

(i) Do you require an application form? If “Yes,” attach a copy of the form. Yes No (ii) Do you require a grant proposal? If “Yes,” describe whether the grant proposal specifies your

responsibilities and those of the grantee, obligates the grantee to use the grant funds only for the purposes for which the grant was made, provides for periodic written reports concerning the use of grant funds, requires a final written report and an accounting of how grant funds were used, and acknowledges your authority to withhold and/or recover grant funds in case such funds are, or appear to be, misused.

Yes No

g Describe your procedures for oversight of distributions that assure you the resources are used to further your exempt purposes, including whether you require periodic and final reports on the use of resources.

14a Do you or will you make grants, loans, or other distributions to foreign organizations? If “Yes,” answer lines 14b through 14f. If “No,” go to line 15.

Yes No

b Provide the name of each foreign organization, the country and regions within a country in which each foreign organization operates, and describe any relationship you have with each foreign organization.

c Does any foreign organization listed in line 14b accept contributions earmarked for a specific country or specific organization? If “Yes,” list all earmarked organizations or countries.

Yes No

d Do your contributors know that you have ultimate authority to use contributions made to you at your discretion for purposes consistent with your exempt purposes? If “Yes,” describe how you relay this information to contributors.

Yes No

e Do you or will you make pre-grant inquiries about the recipient organization? If “Yes,” describe these inquiries, including whether you inquire about the recipient’s financial status, its tax-exempt status under the Internal Revenue Code, its ability to accomplish the purpose for which the resources are provided, and other relevant information.

Yes No

f Do you or will you use any additional procedures to ensure that your distributions to foreign organizations are used in furtherance of your exempt purposes? If “Yes,” describe these procedures, including site visits by your employees or compliance checks by impartial experts, to verify that grant funds are being used appropriately.

Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 8 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. 6-2006) Name: EIN: – Page 8 Part VIII Your Specific Activities (Continued)

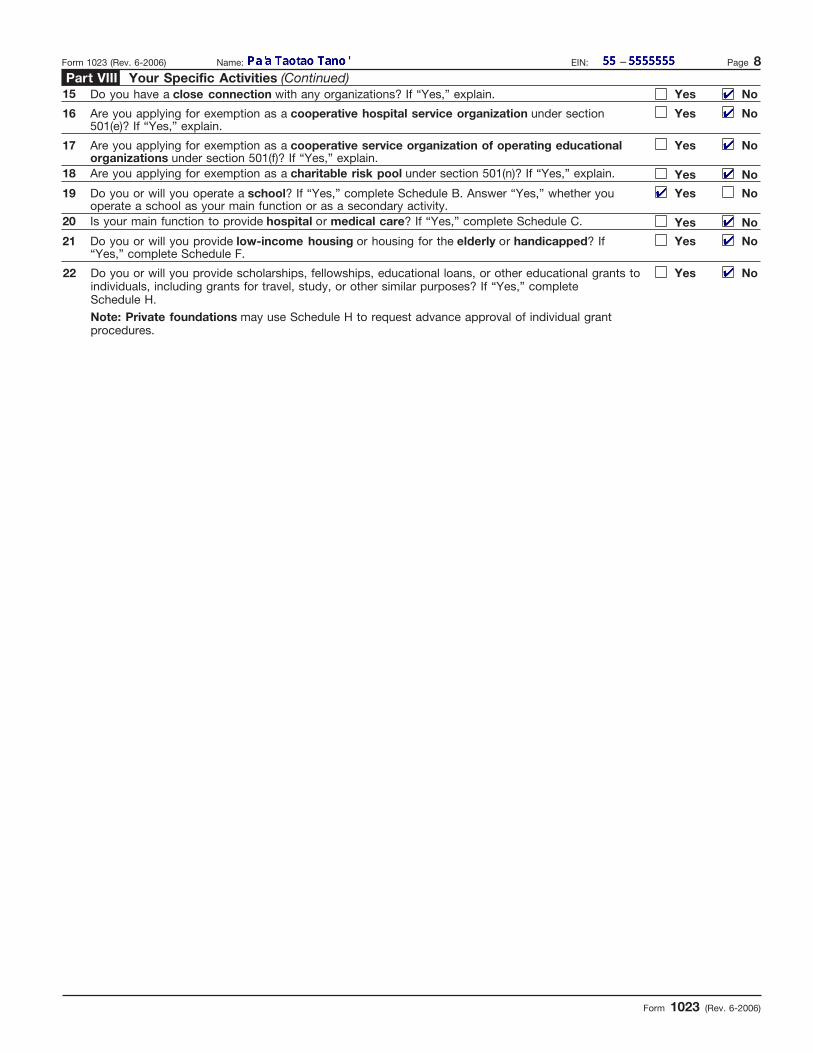

15 Do you have a close connection with any organizations? If “Yes,” explain. Yes No

16 Are you applying for exemption as a cooperative hospital service organization under section 501(e)? If “Yes,” explain.

Yes No

17 Are you applying for exemption as a cooperative service organization of operating educational organizations under section 501(f)? If “Yes,” explain.

Yes No

18 Are you applying for exemption as a charitable risk pool under section 501(n)? If “Yes,” explain. Yes No

19 Do you or will you operate a school? If “Yes,” complete Schedule B. Answer “Yes,” whether you operate a school as your main function or as a secondary activity.

Yes No

20 Is your main function to provide hospital or medical care? If “Yes,” complete Schedule C. Yes No

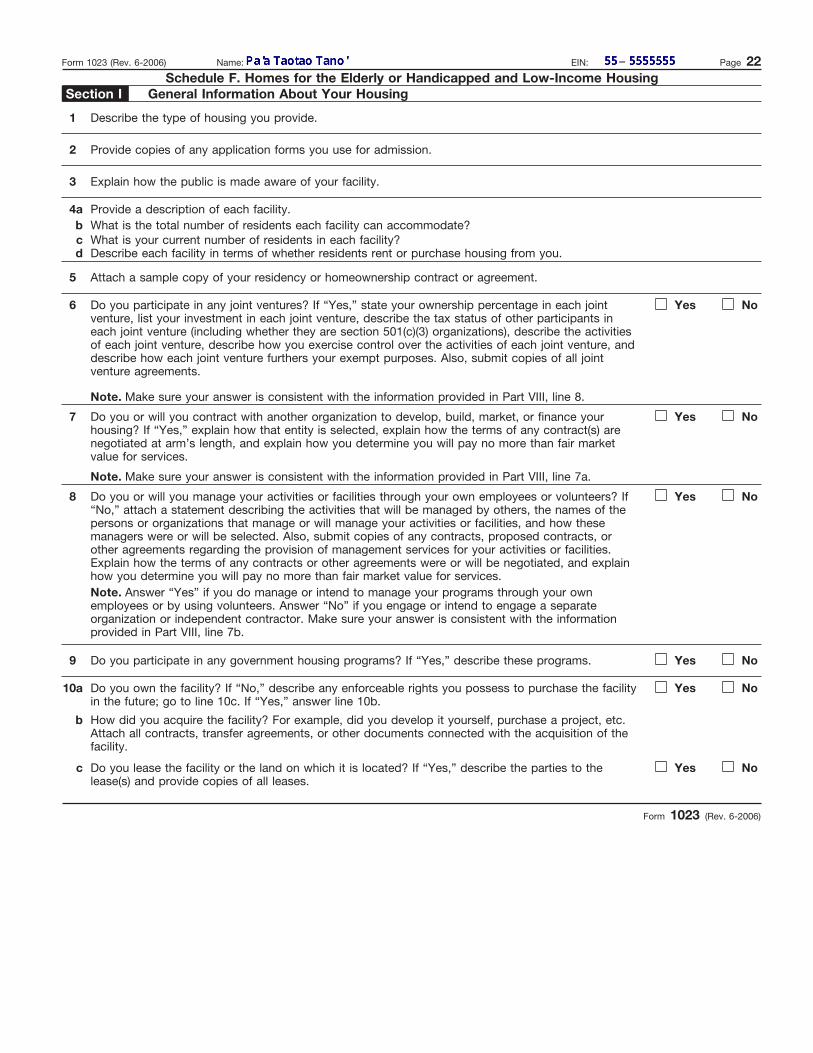

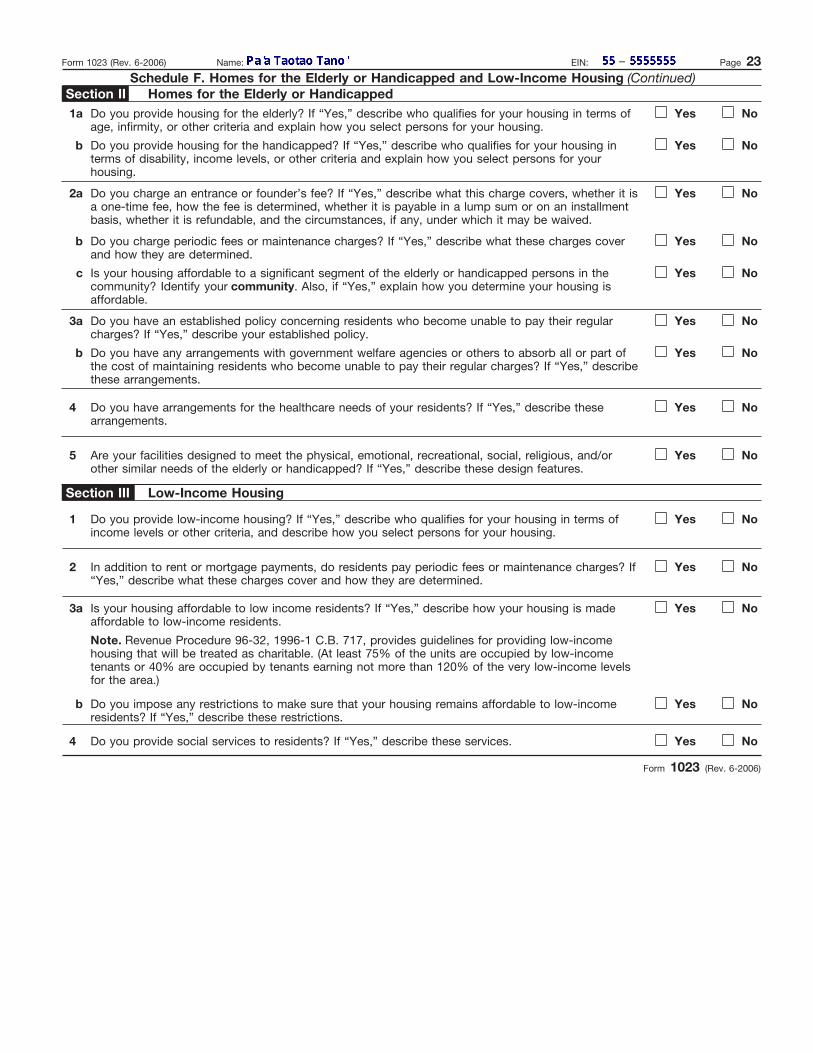

21 Do you or will you provide low-income housing or housing for the elderly or handicapped? If “Yes,” complete Schedule F.

Yes No

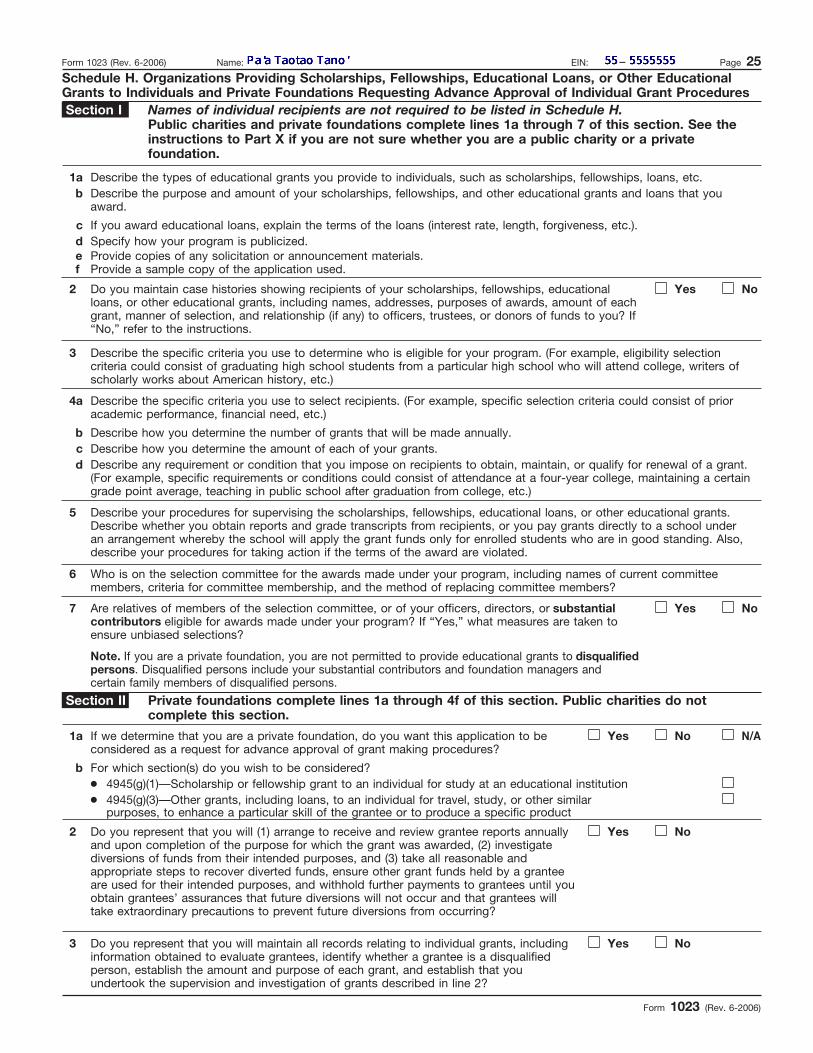

22 Do you or will you provide scholarships, fellowships, educational loans, or other educational grants to individuals, including grants for travel, study, or other similar purposes? If “Yes,” complete Schedule H.

Yes No

Note: Private foundations may use Schedule H to request advance approval of individual grant procedures.

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 9 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

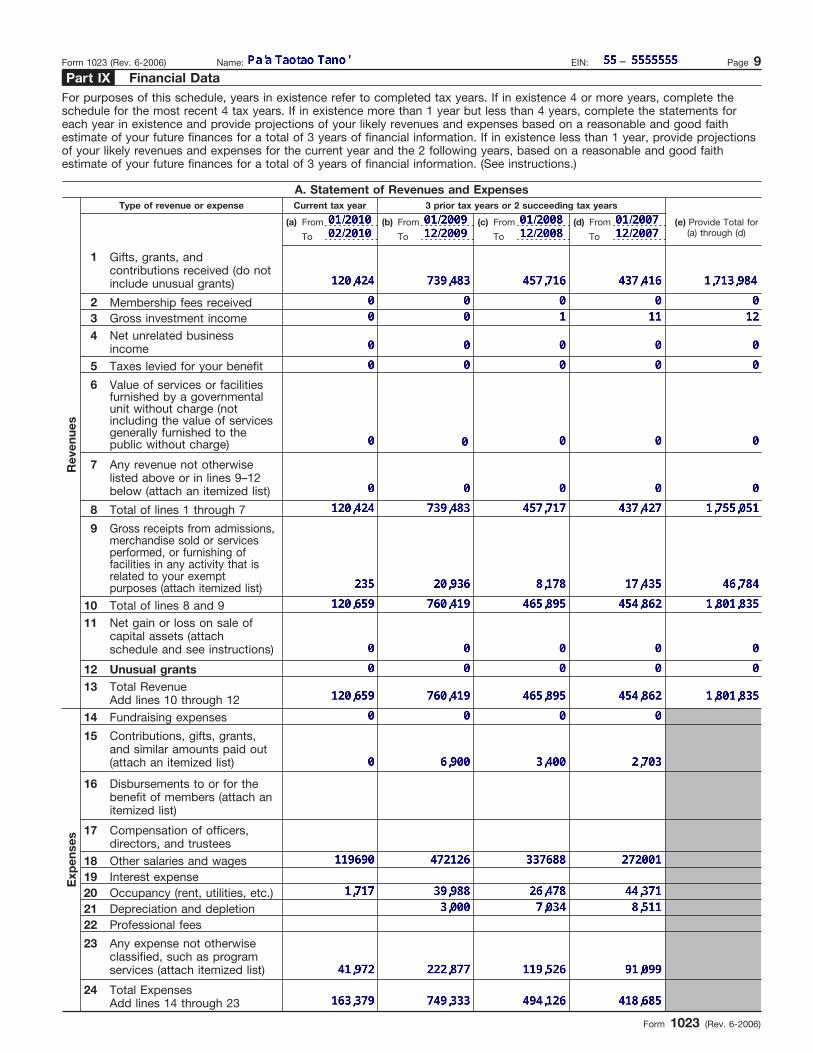

Form 1023 (Rev. 6-2006) Name: EIN: – Page 9 Part IX Financial Data

For purposes of this schedule, years in existence refer to completed tax years. If in existence 4 or more years, complete the schedule for the most recent 4 tax years. If in existence more than 1 year but less than 4 years, complete the statements for each year in existence and provide projections of your likely revenues and expenses based on a reasonable and good faith estimate of your future finances for a total of 3 years of financial information. If in existence less than 1 year, provide projections of your likely revenues and expenses for the current year and the 2 following years, based on a reasonable and good faith estimate of your future finances for a total of 3 years of financial information. (See instructions.)

A. Statement of Revenues and Expenses Type of revenue or expense Current tax year

(a) From

To

3 prior tax years or 2 succeeding tax years

(b) From

To

(c) From

To

(d) From

To

(e) Provide Total for (a) through (d)

Rev

enue

s

1 Gifts, grants, and contributions received (do not include unusual grants)

2 Membership fees received 3 Gross investment income 4 Net unrelated business

income 5 Taxes levied for your benefit

6 Value of services or facilities furnished by a governmental unit without charge (not including the value of services generally furnished to the public without charge)

7 Any revenue not otherwise listed above or in lines 9–12 below (attach an itemized list)

8 Total of lines 1 through 7

9 Gross receipts from admissions, merchandise sold or services performed, or furnishing of facilities in any activity that is related to your exempt purposes (attach itemized list)

10 Total of lines 8 and 9 11 Net gain or loss on sale of

capital assets (attach schedule and see instructions)

12 Unusual grants 13 Total Revenue

Add lines 10 through 12

Exp

ense

s

14 Fundraising expenses

15 Contributions, gifts, grants, and similar amounts paid out (attach an itemized list)

16 Disbursements to or for the benefit of members (attach an itemized list)

17 Compensation of officers, directors, and trustees

18 Other salaries and wages 19 Interest expense 20 Occupancy (rent, utilities, etc.) 21 Depreciation and depletion 22 Professional fees

23 Any expense not otherwise classified, such as program services (attach itemized list)

24 Total Expenses Add lines 14 through 23

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 10 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

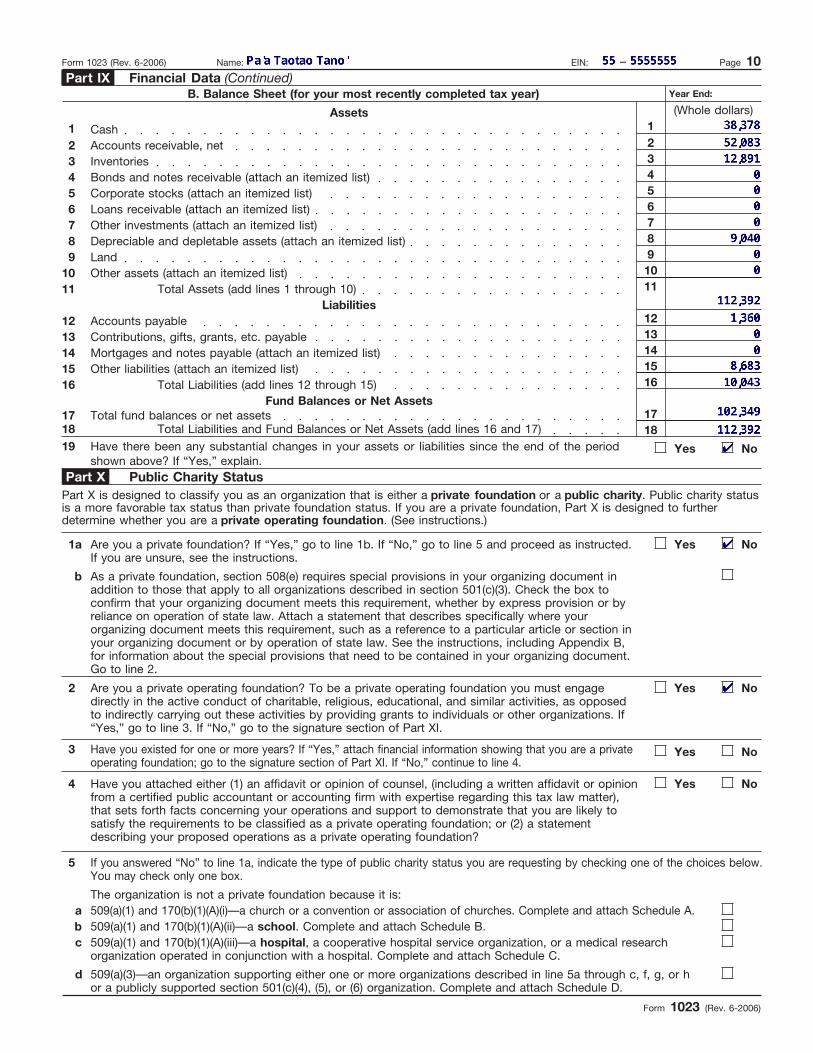

Form 1023 (Rev. 6-2006) Name: EIN: – Page 10 Part IX Financial Data (Continued)

B. Balance Sheet (for your most recently completed tax year) Year End:

(Whole dollars)Assets 1 Cash 1

2 Accounts receivable, net 2

3 Inventories 3

4 Bonds and notes receivable (attach an itemized list) 4

5 Corporate stocks (attach an itemized list) 5

6 Loans receivable (attach an itemized list) 6

7 Other investments (attach an itemized list) 7

8 Depreciable and depletable assets (attach an itemized list) 8

9 Land 9

10 Other assets (attach an itemized list) 10

11 Total Assets (add lines 1 through 10) 11

Liabilities 12 Accounts payable 12

13 Contributions, gifts, grants, etc. payable 13

14 Mortgages and notes payable (attach an itemized list) 14

15 Other liabilities (attach an itemized list) 15

16 Total Liabilities (add lines 12 through 15) 16

Fund Balances or Net Assets 17 Total fund balances or net assets 17 18 Total Liabilities and Fund Balances or Net Assets (add lines 16 and 17) 18 19 Have there been any substantial changes in your assets or liabilities since the end of the period

shown above? If “Yes,” explain. Yes No

Part X Public Charity Status Part X is designed to classify you as an organization that is either a private foundation or a public charity. Public charity status is a more favorable tax status than private foundation status. If you are a private foundation, Part X is designed to further determine whether you are a private operating foundation. (See instructions.)

1a Are you a private foundation? If “Yes,” go to line 1b. If “No,” go to line 5 and proceed as instructed. If you are unsure, see the instructions.

Yes No

b As a private foundation, section 508(e) requires special provisions in your organizing document in addition to those that apply to all organizations described in section 501(c)(3). Check the box to confirm that your organizing document meets this requirement, whether by express provision or by reliance on operation of state law. Attach a statement that describes specifically where your organizing document meets this requirement, such as a reference to a particular article or section in your organizing document or by operation of state law. See the instructions, including Appendix B, for information about the special provisions that need to be contained in your organizing document. Go to line 2.

2 Are you a private operating foundation? To be a private operating foundation you must engage directly in the active conduct of charitable, religious, educational, and similar activities, as opposed to indirectly carrying out these activities by providing grants to individuals or other organizations. If “Yes,” go to line 3. If “No,” go to the signature section of Part XI.

Yes No

3 Have you existed for one or more years? If “Yes,” attach financial information showing that you are a private operating foundation; go to the signature section of Part XI. If “No,” continue to line 4.

Yes No

4 Have you attached either (1) an affidavit or opinion of counsel, (including a written affidavit or opinion from a certified public accountant or accounting firm with expertise regarding this tax law matter), that sets forth facts concerning your operations and support to demonstrate that you are likely to satisfy the requirements to be classified as a private operating foundation; or (2) a statement describing your proposed operations as a private operating foundation?

Yes No

5 If you answered “No” to line 1a, indicate the type of public charity status you are requesting by checking one of the choices below. You may check only one box.

The organization is not a private foundation because it is: a 509(a)(1) and 170(b)(1)(A)(i)—a church or a convention or association of churches. Complete and attach Schedule A. b 509(a)(1) and 170(b)(1)(A)(ii)—a school. Complete and attach Schedule B. c 509(a)(1) and 170(b)(1)(A)(iii)—a hospital, a cooperative hospital service organization, or a medical research

organization operated in conjunction with a hospital. Complete and attach Schedule C.

d 509(a)(3)—an organization supporting either one or more organizations described in line 5a through c, f, g, or h or a publicly supported section 501(c)(4), (5), or (6) organization. Complete and attach Schedule D.

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 11 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

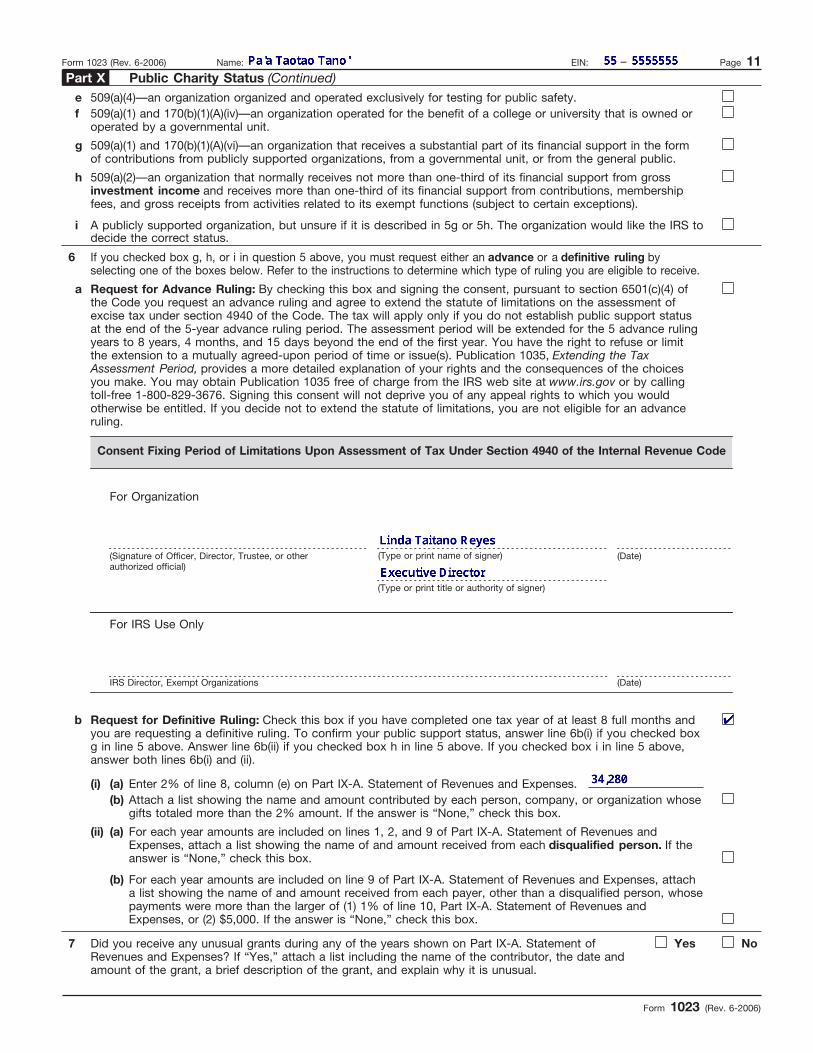

Form 1023 (Rev. 6-2006) Name: EIN: – Page 11 Part X Public Charity Status (Continued)

e 509(a)(4)—an organization organized and operated exclusively for testing for public safety. f 509(a)(1) and 170(b)(1)(A)(iv)—an organization operated for the benefit of a college or university that is owned or

operated by a governmental unit.

g 509(a)(1) and 170(b)(1)(A)(vi)—an organization that receives a substantial part of its financial support in the form of contributions from publicly supported organizations, from a governmental unit, or from the general public.

h 509(a)(2)—an organization that normally receives not more than one-third of its financial support from gross investment income and receives more than one-third of its financial support from contributions, membership fees, and gross receipts from activities related to its exempt functions (subject to certain exceptions).

i A publicly supported organization, but unsure if it is described in 5g or 5h. The organization would like the IRS to decide the correct status.

6 If you checked box g, h, or i in question 5 above, you must request either an advance or a definitive ruling by selecting one of the boxes below. Refer to the instructions to determine which type of ruling you are eligible to receive.

a Request for Advance Ruling: By checking this box and signing the consent, pursuant to section 6501(c)(4) of the Code you request an advance ruling and agree to extend the statute of limitations on the assessment of excise tax under section 4940 of the Code. The tax will apply only if you do not establish public support status at the end of the 5-year advance ruling period. The assessment period will be extended for the 5 advance ruling years to 8 years, 4 months, and 15 days beyond the end of the first year. You have the right to refuse or limit the extension to a mutually agreed-upon period of time or issue(s). Publication 1035, Extending the Tax Assessment Period, provides a more detailed explanation of your rights and the consequences of the choices you make. You may obtain Publication 1035 free of charge from the IRS web site at www.irs.gov or by calling toll-free 1-800-829-3676. Signing this consent will not deprive you of any appeal rights to which you would otherwise be entitled. If you decide not to extend the statute of limitations, you are not eligible for an advance ruling.

Consent Fixing Period of Limitations Upon Assessment of Tax Under Section 4940 of the Internal Revenue Code

For Organization

(Signature of Officer, Director, Trustee, or other authorized official)

(Type or print name of signer) (Date)

(Type or print title or authority of signer)

For IRS Use Only

IRS Director, Exempt Organizations (Date)

b Request for Definitive Ruling: Check this box if you have completed one tax year of at least 8 full months and you are requesting a definitive ruling. To confirm your public support status, answer line 6b(i) if you checked box g in line 5 above. Answer line 6b(ii) if you checked box h in line 5 above. If you checked box i in line 5 above, answer both lines 6b(i) and (ii).

(i) (a) Enter 2% of line 8, column (e) on Part IX-A. Statement of Revenues and Expenses. (b) Attach a list showing the name and amount contributed by each person, company, or organization whose

gifts totaled more than the 2% amount. If the answer is “None,” check this box.

(ii) (a) For each year amounts are included on lines 1, 2, and 9 of Part IX-A. Statement of Revenues and Expenses, attach a list showing the name of and amount received from each disqualified person. If the answer is “None,” check this box.

(b) For each year amounts are included on line 9 of Part IX-A. Statement of Revenues and Expenses, attach a list showing the name of and amount received from each payer, other than a disqualified person, whose payments were more than the larger of (1) 1% of line 10, Part IX-A. Statement of Revenues and Expenses, or (2) $5,000. If the answer is “None,” check this box.

7 Did you receive any unusual grants during any of the years shown on Part IX-A. Statement of Revenues and Expenses? If “Yes,” attach a list including the name of the contributor, the date and amount of the grant, a brief description of the grant, and explain why it is unusual.

Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 12 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

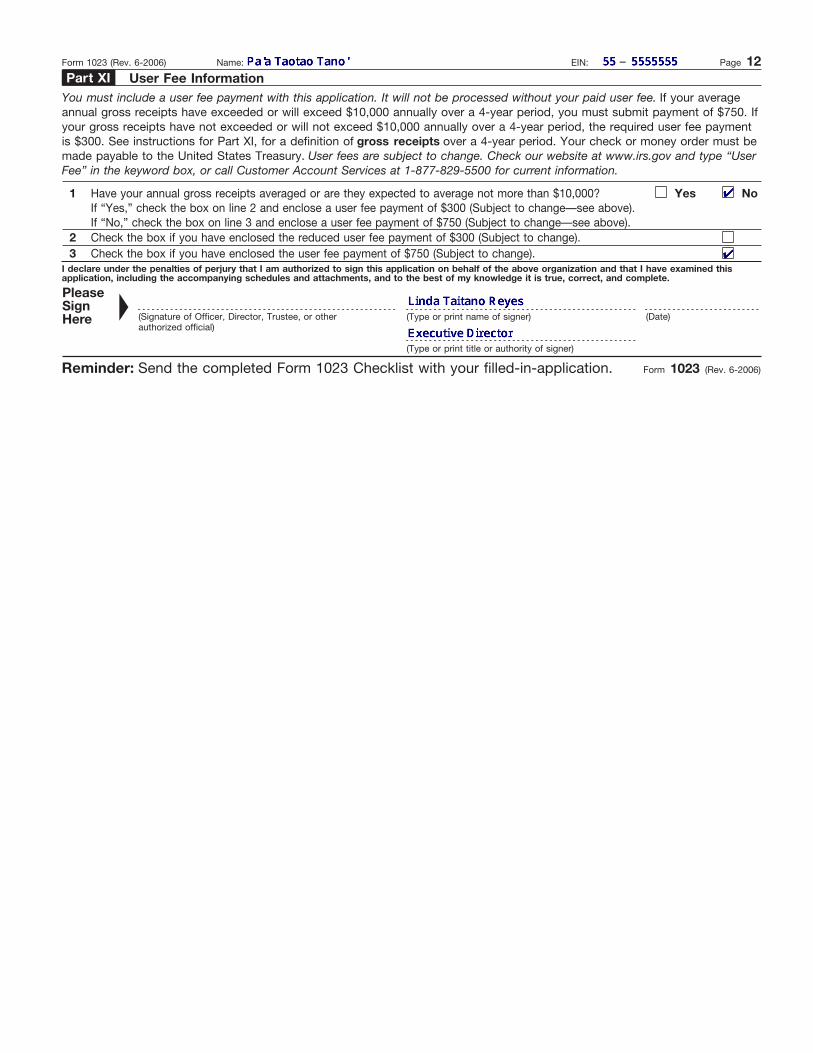

Form 1023 (Rev. 6-2006) Name: EIN: – Page 12 Part XI User Fee Information

You must include a user fee payment with this application. It will not be processed without your paid user fee. If your average annual gross receipts have exceeded or will exceed $10,000 annually over a 4-year period, you must submit payment of $750. If your gross receipts have not exceeded or will not exceed $10,000 annually over a 4-year period, the required user fee payment is $300. See instructions for Part XI, for a definition of gross receipts over a 4-year period. Your check or money order must be made payable to the United States Treasury. User fees are subject to change. Check our website at www.irs.gov and type “User Fee” in the keyword box, or call Customer Account Services at 1-877-829-5500 for current information.

1 Have your annual gross receipts averaged or are they expected to average not more than $10,000? Yes No If “Yes,” check the box on line 2 and enclose a user fee payment of $300 (Subject to change—see above). If “No,” check the box on line 3 and enclose a user fee payment of $750 (Subject to change—see above).

2 Check the box if you have enclosed the reduced user fee payment of $300 (Subject to change). 3 Check the box if you have enclosed the user fee payment of $750 (Subject to change).

I declare under the penalties of perjury that I am authorized to sign this application on behalf of the above organization and that I have examined this application, including the accompanying schedules and attachments, and to the best of my knowledge it is true, correct, and complete.

Please Sign Here

� (Signature of Officer, Director, Trustee, or other authorized official)

(Type or print name of signer) (Date)

(Type or print title or authority of signer)

Reminder: Send the completed Form 1023 Checklist with your filled-in-application. Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 13 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

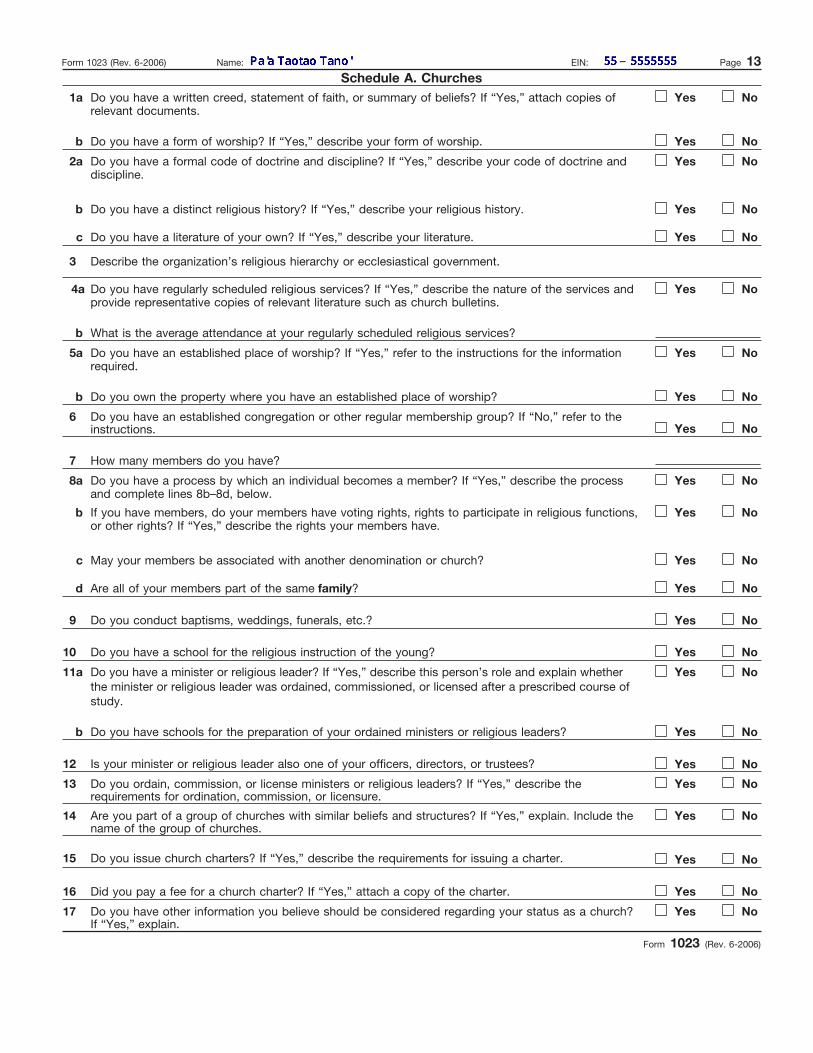

Form 1023 (Rev. 6-2006) Name: EIN: – Page 13 Schedule A. Churches

1a Do you have a written creed, statement of faith, or summary of beliefs? If “Yes,” attach copies of relevant documents.

Yes No

b Do you have a form of worship? If “Yes,” describe your form of worship. Yes No

2a Do you have a formal code of doctrine and discipline? If “Yes,” describe your code of doctrine and discipline.

Yes No

b Do you have a distinct religious history? If “Yes,” describe your religious history. Yes No

c Do you have a literature of your own? If “Yes,” describe your literature. Yes No

3 Describe the organization’s religious hierarchy or ecclesiastical government.

4a Do you have regularly scheduled religious services? If “Yes,” describe the nature of the services and provide representative copies of relevant literature such as church bulletins.

Yes No

b What is the average attendance at your regularly scheduled religious services?

5a Do you have an established place of worship? If “Yes,” refer to the instructions for the information required.

Yes No

b Do you own the property where you have an established place of worship? Yes No

6 Do you have an established congregation or other regular membership group? If “No,” refer to the instructions. Yes No

7 How many members do you have?

8a Do you have a process by which an individual becomes a member? If “Yes,” describe the process and complete lines 8b–8d, below.

Yes No

b If you have members, do your members have voting rights, rights to participate in religious functions, or other rights? If “Yes,” describe the rights your members have.

Yes No

c May your members be associated with another denomination or church? Yes No

d Are all of your members part of the same family? Yes No

9 Do you conduct baptisms, weddings, funerals, etc.? Yes No

10 Do you have a school for the religious instruction of the young? Yes No

11a Do you have a minister or religious leader? If “Yes,” describe this person’s role and explain whether the minister or religious leader was ordained, commissioned, or licensed after a prescribed course of study.

Yes No

b Do you have schools for the preparation of your ordained ministers or religious leaders? Yes No

12 Is your minister or religious leader also one of your officers, directors, or trustees? Yes No

13 Do you ordain, commission, or license ministers or religious leaders? If “Yes,” describe the requirements for ordination, commission, or licensure.

Yes No

14 Are you part of a group of churches with similar beliefs and structures? If “Yes,” explain. Include the name of the group of churches.

Yes No

15 Do you issue church charters? If “Yes,” describe the requirements for issuing a charter. Yes No

16 Did you pay a fee for a church charter? If “Yes,” attach a copy of the charter. Yes No

17 Do you have other information you believe should be considered regarding your status as a church? If “Yes,” explain.

Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 14 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

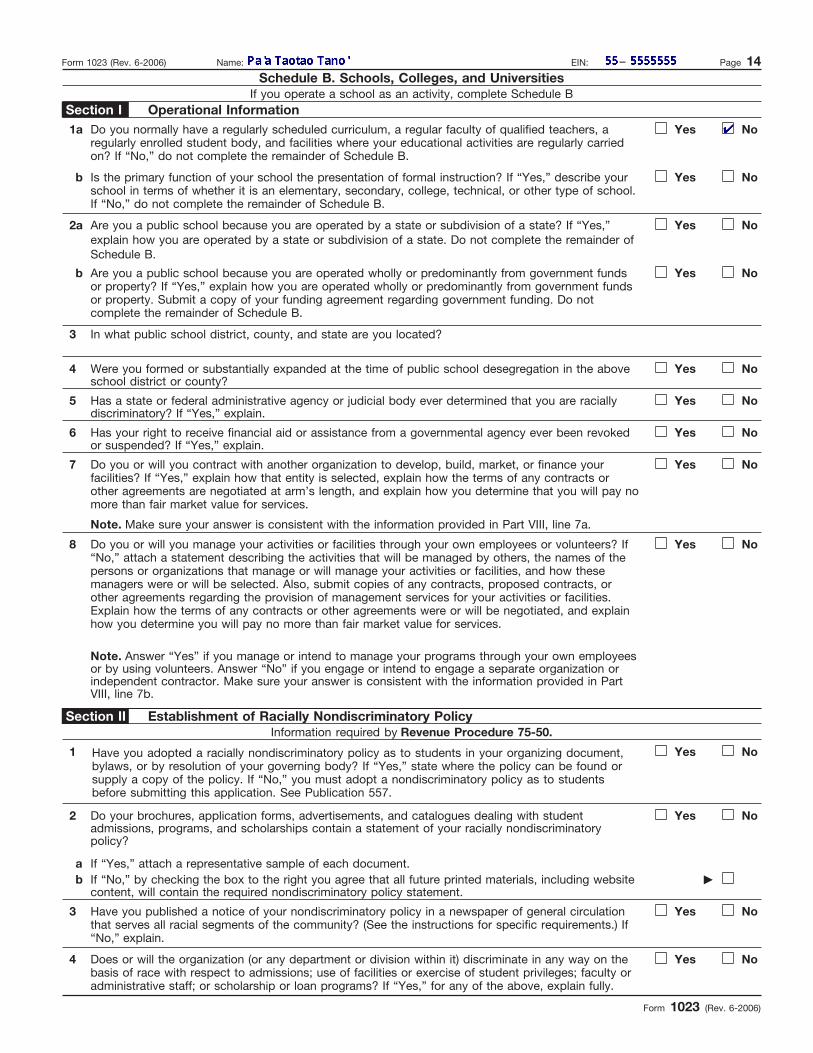

Form 1023 (Rev. 6-2006) Name: EIN: – Page 14 Schedule B. Schools, Colleges, and Universities

If you operate a school as an activity, complete Schedule B Section I Operational Information 1a Do you normally have a regularly scheduled curriculum, a regular faculty of qualified teachers, a

regularly enrolled student body, and facilities where your educational activities are regularly carried on? If “No,” do not complete the remainder of Schedule B.

Yes No

b Is the primary function of your school the presentation of formal instruction? If “Yes,” describe your school in terms of whether it is an elementary, secondary, college, technical, or other type of school. If “No,” do not complete the remainder of Schedule B.

Yes No

2a Are you a public school because you are operated by a state or subdivision of a state? If “Yes,” explain how you are operated by a state or subdivision of a state. Do not complete the remainder of Schedule B.

Yes No

b Are you a public school because you are operated wholly or predominantly from government funds or property? If “Yes,” explain how you are operated wholly or predominantly from government funds or property. Submit a copy of your funding agreement regarding government funding. Do not complete the remainder of Schedule B.

Yes No

3 In what public school district, county, and state are you located?

4 Were you formed or substantially expanded at the time of public school desegregation in the above school district or county?

Yes No

5 Has a state or federal administrative agency or judicial body ever determined that you are racially discriminatory? If “Yes,” explain.

Yes No

6 Has your right to receive financial aid or assistance from a governmental agency ever been revoked or suspended? If “Yes,” explain.

Yes No

7 Do you or will you contract with another organization to develop, build, market, or finance your facilities? If “Yes,” explain how that entity is selected, explain how the terms of any contracts or other agreements are negotiated at arm’s length, and explain how you determine that you will pay no more than fair market value for services.

Yes No

Note. Make sure your answer is consistent with the information provided in Part VIII, line 7a.

8 Do you or will you manage your activities or facilities through your own employees or volunteers? If “No,” attach a statement describing the activities that will be managed by others, the names of the persons or organizations that manage or will manage your activities or facilities, and how these managers were or will be selected. Also, submit copies of any contracts, proposed contracts, or other agreements regarding the provision of management services for your activities or facilities. Explain how the terms of any contracts or other agreements were or will be negotiated, and explain how you determine you will pay no more than fair market value for services.

Yes No

Note. Answer “Yes” if you manage or intend to manage your programs through your own employees or by using volunteers. Answer “No” if you engage or intend to engage a separate organization or independent contractor. Make sure your answer is consistent with the information provided in Part VIII, line 7b.

Section II Establishment of Racially Nondiscriminatory Policy Information required by Revenue Procedure 75-50.

1 Have you adopted a racially nondiscriminatory policy as to students in your organizing document, bylaws, or by resolution of your governing body? If “Yes,” state where the policy can be found or supply a copy of the policy. If “No,” you must adopt a nondiscriminatory policy as to students before submitting this application. See Publication 557.

Yes No

2 Do your brochures, application forms, advertisements, and catalogues dealing with student admissions, programs, and scholarships contain a statement of your racially nondiscriminatory policy?

Yes No

a If “Yes,” attach a representative sample of each document. b If “No,” by checking the box to the right you agree that all future printed materials, including website

content, will contain the required nondiscriminatory policy statement. �

3 Have you published a notice of your nondiscriminatory policy in a newspaper of general circulation that serves all racial segments of the community? (See the instructions for specific requirements.) If “No,” explain.

Yes No

4 Does or will the organization (or any department or division within it) discriminate in any way on the basis of race with respect to admissions; use of facilities or exercise of student privileges; faculty or administrative staff; or scholarship or loan programs? If “Yes,” for any of the above, explain fully.

Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 15 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

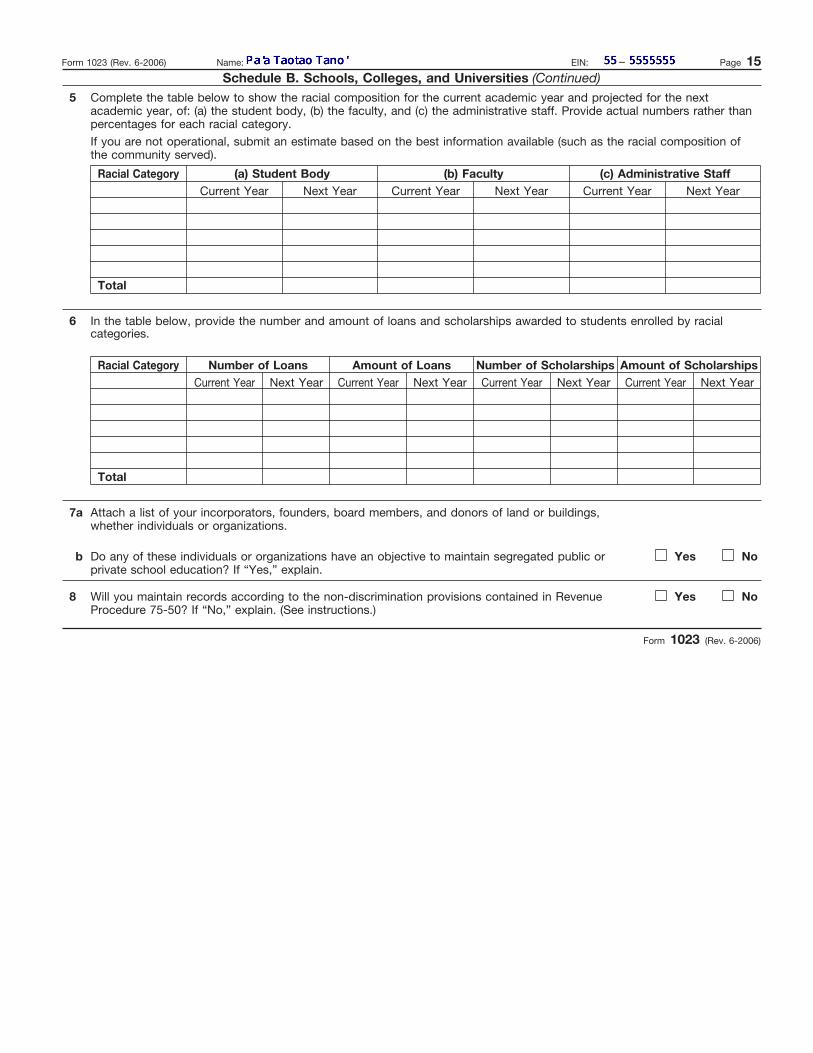

Form 1023 (Rev. 6-2006) Name: EIN: – Page 15 Schedule B. Schools, Colleges, and Universities (Continued)

5 Complete the table below to show the racial composition for the current academic year and projected for the next academic year, of: (a) the student body, (b) the faculty, and (c) the administrative staff. Provide actual numbers rather than percentages for each racial category.

If you are not operational, submit an estimate based on the best information available (such as the racial composition of the community served).

Racial Category (a) Student Body Current Year Next Year

(b) Faculty Current Year Next Year

(c) Administrative Staff Current Year Next Year

Total

6 In the table below, provide the number and amount of loans and scholarships awarded to students enrolled by racial categories.

Racial Category Number of Loans Amount of Loans Number of Scholarships Amount of Scholarships Current Year Next Year Current Year Next Year Current Year Next Year Current Year Next Year

Total

7a Attach a list of your incorporators, founders, board members, and donors of land or buildings, whether individuals or organizations.

b Do any of these individuals or organizations have an objective to maintain segregated public or private school education? If “Yes,” explain.

Yes No

8 Will you maintain records according to the non-discrimination provisions contained in Revenue Procedure 75-50? If “No,” explain. (See instructions.)

Yes No

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 16 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

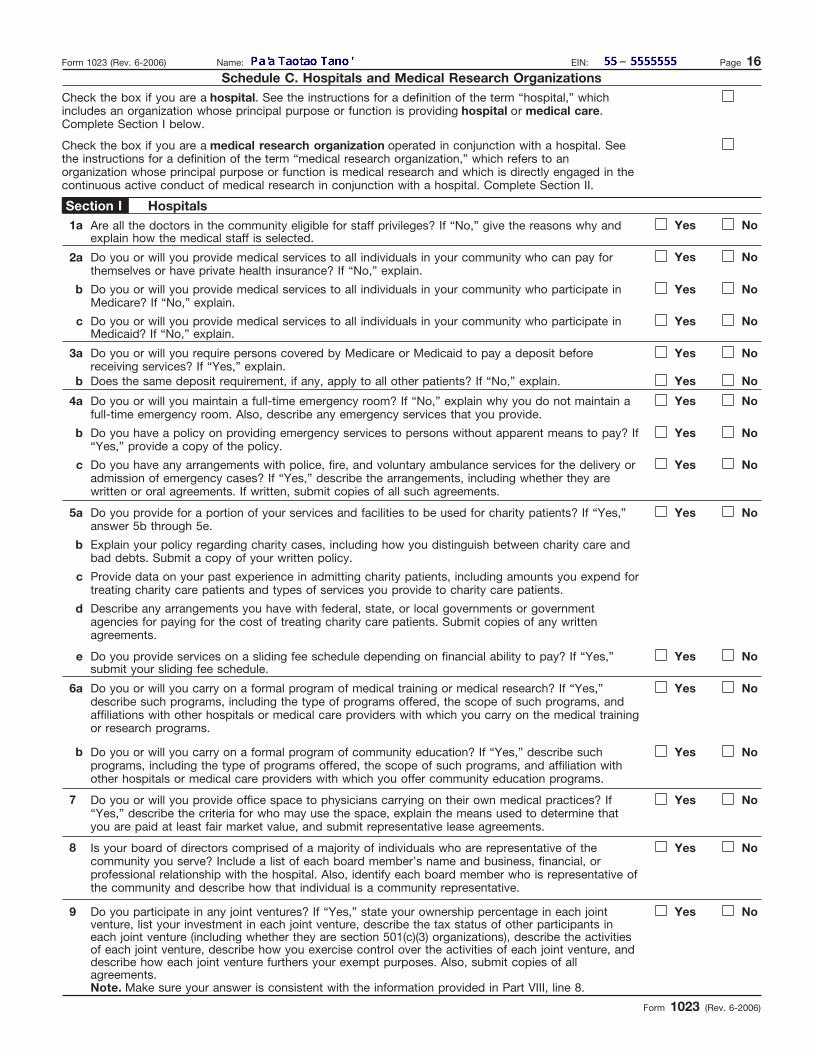

Form 1023 (Rev. 6-2006) Name: EIN: – Page 16 Schedule C. Hospitals and Medical Research Organizations

Check the box if you are a hospital. See the instructions for a definition of the term “hospital,” which includes an organization whose principal purpose or function is providing hospital or medical care. Complete Section I below.

Check the box if you are a medical research organization operated in conjunction with a hospital. See the instructions for a definition of the term “medical research organization,” which refers to an organization whose principal purpose or function is medical research and which is directly engaged in the continuous active conduct of medical research in conjunction with a hospital. Complete Section II.

Section I Hospitals 1a Are all the doctors in the community eligible for staff privileges? If “No,” give the reasons why and

explain how the medical staff is selected. Yes No

2a Do you or will you provide medical services to all individuals in your community who can pay for themselves or have private health insurance? If “No,” explain.

Yes No

b Do you or will you provide medical services to all individuals in your community who participate in Medicare? If “No,” explain.

Yes No

c Do you or will you provide medical services to all individuals in your community who participate in Medicaid? If “No,” explain.

Yes No

3a Do you or will you require persons covered by Medicare or Medicaid to pay a deposit before receiving services? If “Yes,” explain.

Yes No

b Does the same deposit requirement, if any, apply to all other patients? If “No,” explain. Yes No

4a Do you or will you maintain a full-time emergency room? If “No,” explain why you do not maintain a full-time emergency room. Also, describe any emergency services that you provide.

Yes No

b Do you have a policy on providing emergency services to persons without apparent means to pay? If “Yes,” provide a copy of the policy.

Yes No

c Do you have any arrangements with police, fire, and voluntary ambulance services for the delivery or admission of emergency cases? If “Yes,” describe the arrangements, including whether they are written or oral agreements. If written, submit copies of all such agreements.

Yes No

5a Do you provide for a portion of your services and facilities to be used for charity patients? If “Yes,” answer 5b through 5e.

Yes No

b Explain your policy regarding charity cases, including how you distinguish between charity care and bad debts. Submit a copy of your written policy.

c Provide data on your past experience in admitting charity patients, including amounts you expend for treating charity care patients and types of services you provide to charity care patients.

d Describe any arrangements you have with federal, state, or local governments or government agencies for paying for the cost of treating charity care patients. Submit copies of any written agreements.

e Do you provide services on a sliding fee schedule depending on financial ability to pay? If “Yes,” submit your sliding fee schedule.

Yes No

6a Do you or will you carry on a formal program of medical training or medical research? If “Yes,” describe such programs, including the type of programs offered, the scope of such programs, and affiliations with other hospitals or medical care providers with which you carry on the medical training or research programs.

Yes No

b Do you or will you carry on a formal program of community education? If “Yes,” describe such programs, including the type of programs offered, the scope of such programs, and affiliation with other hospitals or medical care providers with which you offer community education programs.

Yes No

7 Do you or will you provide office space to physicians carrying on their own medical practices? If “Yes,” describe the criteria for who may use the space, explain the means used to determine that you are paid at least fair market value, and submit representative lease agreements.

Yes No

8 Is your board of directors comprised of a majority of individuals who are representative of the community you serve? Include a list of each board member’s name and business, financial, or professional relationship with the hospital. Also, identify each board member who is representative of the community and describe how that individual is a community representative.

Yes No

9 Do you participate in any joint ventures? If “Yes,” state your ownership percentage in each joint venture, list your investment in each joint venture, describe the tax status of other participants in each joint venture (including whether they are section 501(c)(3) organizations), describe the activities of each joint venture, describe how you exercise control over the activities of each joint venture, and describe how each joint venture furthers your exempt purposes. Also, submit copies of all agreements.

Yes No

Note. Make sure your answer is consistent with the information provided in Part VIII, line 8.

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 17 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. 6-2006) Name: EIN: – Page 17 Schedule C. Hospitals and Medical Research Organizations (Continued)

Section I Hospitals (Continued) 10 Do you or will you manage your activities or facilities through your own employees or volunteers? If

“No,” attach a statement describing the activities that will be managed by others, the names of the persons or organizations that manage or will manage your activities or facilities, and how these managers were or will be selected. Also, submit copies of any contracts, proposed contracts, or other agreements regarding the provision of management services for your activities or facilities. Explain how the terms of any contracts or other agreements were or will be negotiated, and explain how you determine you will pay no more than fair market value for services.

Yes No

Note. Answer “Yes” if you do manage or intend to manage your programs through your own employees or by using volunteers. Answer “No” if you engage or intend to engage a separate organization or independent contractor. Make sure your answer is consistent with the information provided in Part VIII, line 7b.

11 Do you or will you offer recruitment incentives to physicians? If “Yes,” describe your recruitment incentives and attach copies of all written recruitment incentive policies.

Yes No

12 Do you or will you lease equipment, assets, or office space from physicians who have a financial or professional relationship with you? If “Yes,” explain how you establish a fair market value for the lease.

Yes No

13 Have you purchased medical practices, ambulatory surgery centers, or other business assets from physicians or other persons with whom you have a business relationship, aside from the purchase? If “Yes,” submit a copy of each purchase and sales contract and describe how you arrived at fair market value, including copies of appraisals.

Yes No

14 Have you adopted a conflict of interest policy consistent with the sample health care organization conflict of interest policy in Appendix A of the instructions? If “Yes,” submit a copy of the policy and explain how the policy has been adopted, such as by resolution of your governing board. If “No,” explain how you will avoid any conflicts of interest in your business dealings.

Yes No

Section II Medical Research Organizations 1 Name the hospitals with which you have a relationship and describe the relationship. Attach copies

of written agreements with each hospital that demonstrate continuing relationships between you and the hospital(s).

2 Attach a schedule describing your present and proposed activities for the direct conduct of medical research; describe the nature of the activities, and the amount of money that has been or will be spent in carrying them out.

3 Attach a schedule of assets showing their fair market value and the portion of your assets directly devoted to medical research.

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 18 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. 6-2006) Name: EIN: – Page 18 Schedule D. Section 509(a)(3) Supporting Organizations

Section I Identifying Information About the Supported Organization(s) 1 State the names, addresses, and EINs of the supported organizations. If additional space is needed, attach a separate

sheet. Name Address EIN

–

–

2 Are all supported organizations listed in line 1 public charities under section 509(a)(1) or (2)? If “Yes,” go to Section II. If “No,” go to line 3.

Yes No

3 Do the supported organizations have tax-exempt status under section 501(c)(4), 501(c)(5), or 501(c)(6)?

Yes No

If “Yes,” for each 501(c)(4), (5), or (6) organization supported, provide the following financial information:

● Part IX-A. Statement of Revenues and Expenses, lines 1–13 and ● Part X, lines 6b(ii)(a), 6b(ii)(b), and 7. If “No,” attach a statement describing how each organization you support is a public charity under section 509(a)(1) or (2).

Section II Relationship with Supported Organization(s)—Three Tests To be classified as a supporting organization, an organization must meet one of three relationship tests:

Test 1: “Operated, supervised, or controlled by” one or more publicly supported organizations, or Test 2: “Supervised or controlled in connection with” one or more publicly supported organizations, or Test 3: “Operated in connection with” one or more publicly supported organizations.

1 Information to establish the “operated, supervised, or controlled by” relationship (Test 1) Is a majority of your governing board or officers elected or appointed by the supported organization(s)? If “Yes,” describe the process by which your governing board is appointed and elected; go to Section III. If “No,” continue to line 2.

Yes No

2 Information to establish the “supervised or controlled in connection with” relationship (Test 2) Does a majority of your governing board consist of individuals who also serve on the governing board of the supported organization(s)? If “Yes,” describe the process by which your governing board is appointed and elected; go to Section III. If “No,” go to line 3.

Yes No

3 Information to establish the “operated in connection with” responsiveness test (Test 3) Are you a trust from which the named supported organization(s) can enforce and compel an accounting under state law? If “Yes,” explain whether you advised the supported organization(s) in writing of these rights and provide a copy of the written communication documenting this; go to Section II, line 5. If “No,” go to line 4a.

Yes No

4 Information to establish the alternative “operated in connection with” responsiveness test (Test 3) a Do the officers, directors, trustees, or members of the supported organization(s) elect or appoint one

or more of your officers, directors, or trustees? If “Yes,” explain and provide documentation; go to line 4d, below. If “No,” go to line 4b.

Yes No

b Do one or more members of the governing body of the supported organization(s) also serve as your officers, directors, or trustees or hold other important offices with respect to you? If “Yes,” explain and provide documentation; go to line 4d, below. If “No,” go to line 4c.

Yes No

c Do your officers, directors, or trustees maintain a close and continuous working relationship with the officers, directors, or trustees of the supported organization(s)? If “Yes,” explain and provide documentation.

Yes No

d Do the supported organization(s) have a significant voice in your investment policies, in the making and timing of grants, and in otherwise directing the use of your income or assets? If “Yes,” explain and provide documentation.

Yes No

e Describe and provide copies of written communications documenting how you made the supported organization(s) aware of your supporting activities.

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 19 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None

Form 1023 (Rev. 6-2006) Name: EIN: – Page 19 Schedule D. Section 509(a)(3) Supporting Organizations (Continued)

Section II Relationship with Supported Organization(s)—Three Tests (Continued) 5 Information to establish the “operated in connection with” integral part test (Test 3)

Do you conduct activities that would otherwise be carried out by the supported organization(s)? If “Yes,” explain and go to Section III. If “No,” continue to line 6a.

Yes No

6 Information to establish the alternative “operated in connection with” integral part test (Test 3) a Do you distribute at least 85% of your annual net income to the supported organization(s)? If “Yes,”

go to line 6b. (See instructions.)

If “No,” state the percentage of your income that you distribute to each supported organization. Also explain how you ensure that the supported organization(s) are attentive to your operations.

Yes No

b How much do you contribute annually to each supported organization? Attach a schedule. c What is the total annual revenue of each supported organization? If you need additional space,

attach a list.

d Do you or the supported organization(s) earmark your funds for support of a particular program or activity? If “Yes,” explain.

Yes No

7a Does your organizing document specify the supported organization(s) by name? If “Yes,” state the article and paragraph number and go to Section III. If “No,” answer line 7b.

Yes No

b Attach a statement describing whether there has been an historic and continuing relationship between you and the supported organization(s).

Section III Organizational Test 1a If you met relationship Test 1 or Test 2 in Section II, your organizing document must specify the

supported organization(s) by name, or by naming a similar purpose or charitable class of beneficiaries. If your organizing document complies with this requirement, answer “Yes.” If your organizing document does not comply with this requirement, answer “No,” and see the instructions.

Yes No

b If you met relationship Test 3 in Section II, your organizing document must generally specify the supported organization(s) by name. If your organizing document complies with this requirement, answer “Yes,” and go to Section IV. If your organizing document does not comply with this requirement, answer “No,” and see the instructions.

Yes No

Section IV Disqualified Person Test You do not qualify as a supporting organization if you are controlled directly or indirectly by one or more disqualified persons (as defined in section 4946) other than foundation managers or one or more organizations that you support. Foundation managers who are also disqualified persons for another reason are disqualified persons with respect to you.

1a Do any persons who are disqualified persons with respect to you, (except individuals who are disqualified persons only because they are foundation managers), appoint any of your foundation managers? If “Yes,” (1) describe the process by which disqualified persons appoint any of your foundation managers, (2) provide the names of these disqualified persons and the foundation managers they appoint, and (3) explain how control is vested over your operations (including assets and activities) by persons other than disqualified persons.

Yes No

b Do any persons who have a family or business relationship with any disqualified persons with respect to you, (except individuals who are disqualified persons only because they are foundation managers), appoint any of your foundation managers? If “Yes,” (1) describe the process by which individuals with a family or business relationship with disqualified persons appoint any of your foundation managers, (2) provide the names of these disqualified persons, the individuals with a family or business relationship with disqualified persons, and the foundation managers appointed, and (3) explain how control is vested over your operations (including assets and activities) in individuals other than disqualified persons.

Yes No

c Do any persons who are disqualified persons, (except individuals who are disqualified persons only because they are foundation managers), have any influence regarding your operations, including your assets or activities? If “Yes,” (1) provide the names of these disqualified persons, (2) explain how influence is exerted over your operations (including assets and activities), and (3) explain how control is vested over your operations (including assets and activities) by individuals other than disqualified persons.

Yes No

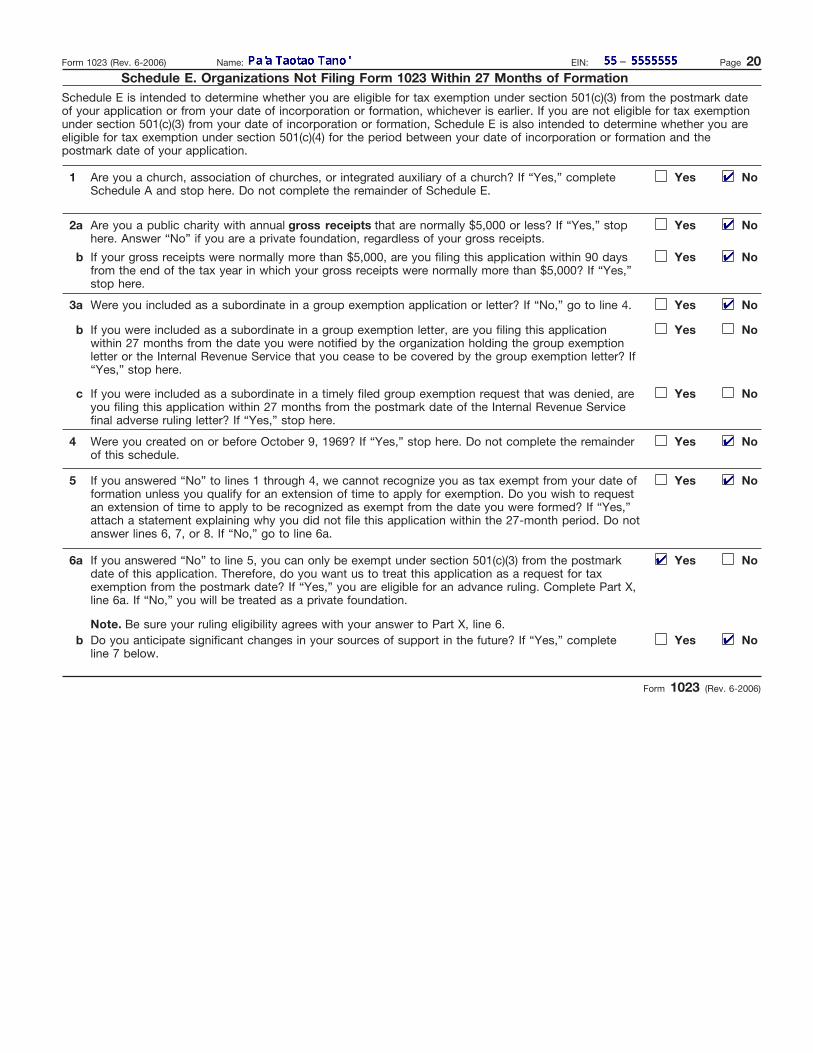

Form 1023 (Rev. 6-2006)

1I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

INSTRUCTIONS TO PRINTERSFORM 1023, PAGE 20 OF 28MARGINS; TOP 13mm (1/2"), CENTER SIDES. PRINTS: HEAD TO HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (8-1/2") x 279mm (11")PERFORATE: None