Embed Size (px)

Citation preview

1

Standard Costing and Variance Analysis

February 6th 2007

2

Lecture and Reading Objectives

• Outline the nature and purpose of an operational control system and the role of budgets, standards and variances.

• Explain how standard costs are set and define basic, ideal and currently attainable standards

• Compile flexible budgets and from these calculate labour, materials overhead and sales variances and reconcile actual profit with budgeted profit

• Identify the causes of variances and discuss the factors leading to the decision to investigate variances

• Discuss the limitations of traditional standard costing systems and assess alternatives

3

Essential Reading

• Drury Chapters 12, 15 and 16 (pages 461 and 468-482)

• Drury C (1999) ‘Standard costing: a technique at variance with modern management?’, Management Accounting, November

• Graham C, Lyall D and Puxty A (1992) ‘Cost control: the managers perspective’ Management Accounting, October

• Kaplan RS and Norton DP (2000) ‘The Balanced Scorecard – Measures that Drive Performance.’ Harvard Business Review, January-February, pages 71-79.

4

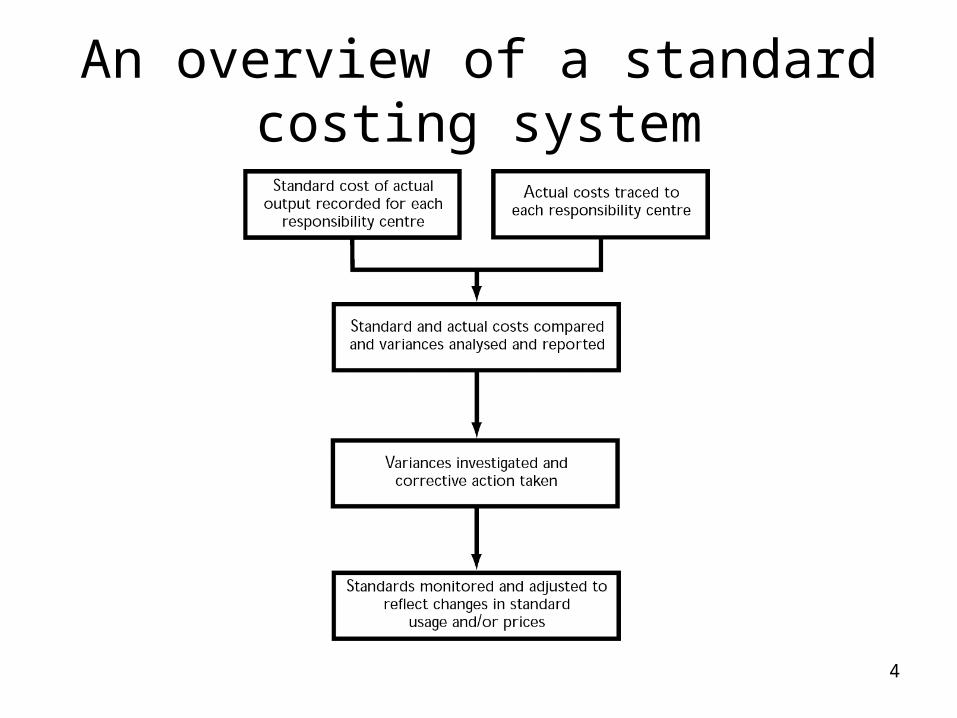

An overview of a standard costing system

5

Budgets & Standard Costs

• Prepare the budget using standard costs and budgeted prices

• Q: Should we compare the budgeted output with the actual output to calculate the variances?

• A: No, first flex the budget• Flex the budget for changes in activity level

(changes in units of output)• Calculate the differences between budget and

actual output – these are termed “variances”• Reconcile the original budgeted profit and actual

profit

6

Relationship between the budgeted and actual profit

(McLaney & Atrill 2002, page 398)

• Budgeted profit

• plus

• All favourable variances

• minus

• All adverse (unfavourable) variances

• equals

• Actual profit

7

What are standard costs and prices?

• Standard costs• These are predetermined costs. They are target

costs that should be incurred under efficient operating conditions…on a per unit basis (Drury, 2005, page 340)

• Standard costing is most suited for organisations where the activities are common or repetitive. The examples we shall use will be for manufacturing organisations.

8

Types of cost standard

• Basic cost standards • Left unchanged over long periods of time. Helps to

establish efficiency trends. Seldom used, as they do not represent current target costs, so not very useful for control.

• Ideal standards• Represent perfect performance. Minimum costs under

the most efficient operating conditions. Can be demotivating and unlikely to be used in practice.

• Currently attainable standards • Costs that should be incurred under efficient operating

conditions. Difficult, but not impossible, to achieve. Can be set at various levels of difficulty.

9

Numerical Example

• Example

10

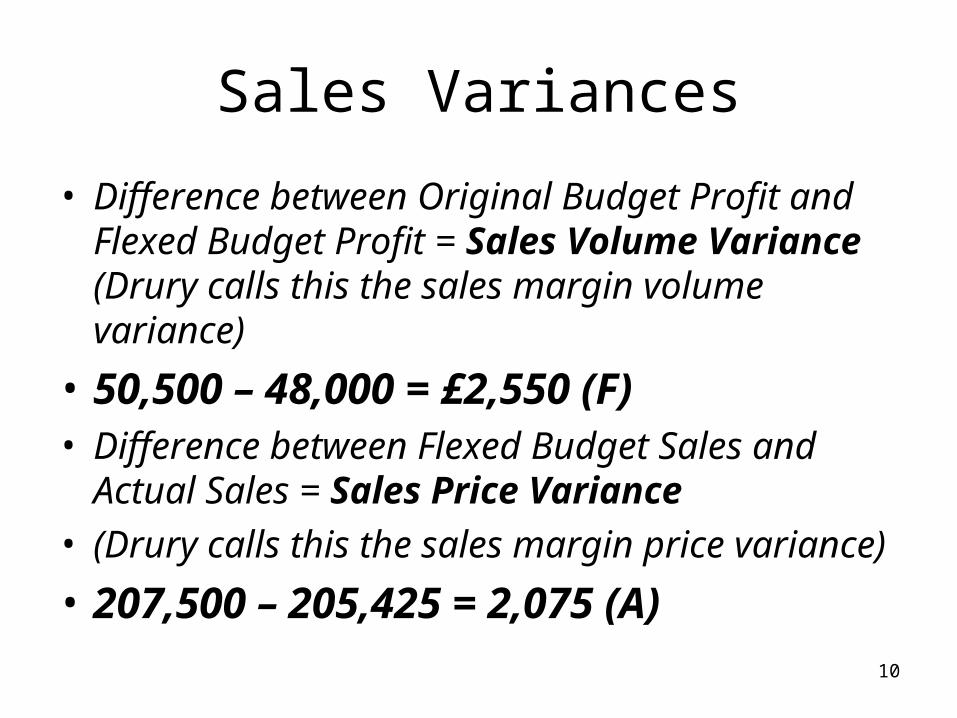

Sales Variances

• Difference between Original Budget Profit and Flexed Budget Profit = Sales Volume Variance(Drury calls this the sales margin volume variance)

• 50,500 – 48,000 = £2,550 (F)• Difference between Flexed Budget Sales and

Actual Sales = Sales Price Variance• (Drury calls this the sales margin price variance)

• 207,500 – 205,425 = 2,075 (A)

11

Materials Variances

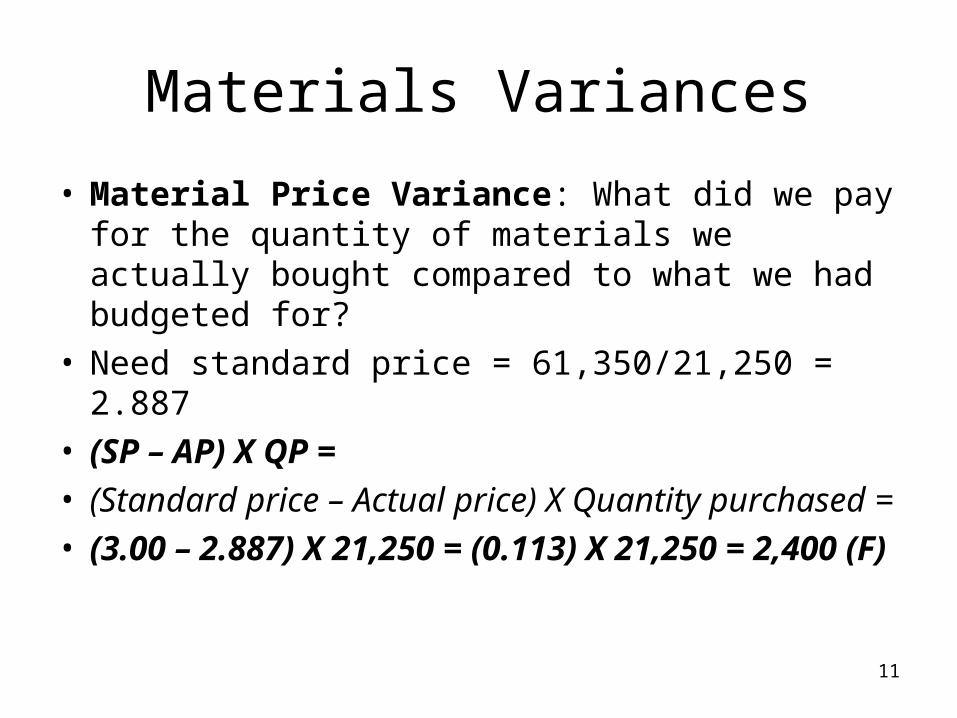

• Material Price Variance: What did we pay for the quantity of materials we actually bought compared to what we had budgeted for?

• Need standard price = 61,350/21,250 = 2.887• (SP – AP) X QP =• (Standard price – Actual price) X Quantity

purchased =• (3.00 – 2.887) X 21,250 = (0.113) X 21,250 =

2,400 (F)

12

Materials Variances

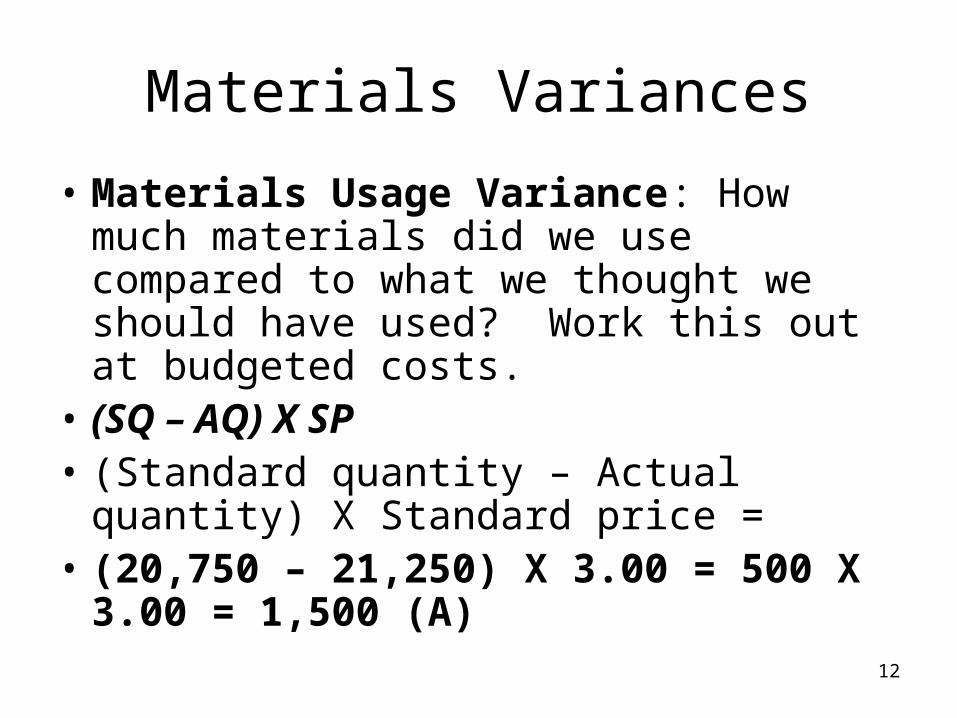

• Materials Usage Variance: How much materials did we use compared to what we thought we should have used? Work this out at budgeted costs.

• (SQ – AQ) X SP• (Standard quantity – Actual quantity) X

Standard price =• (20,750 – 21,250) X 3.00 = 500 X 3.00 =

1,500 (A)

13

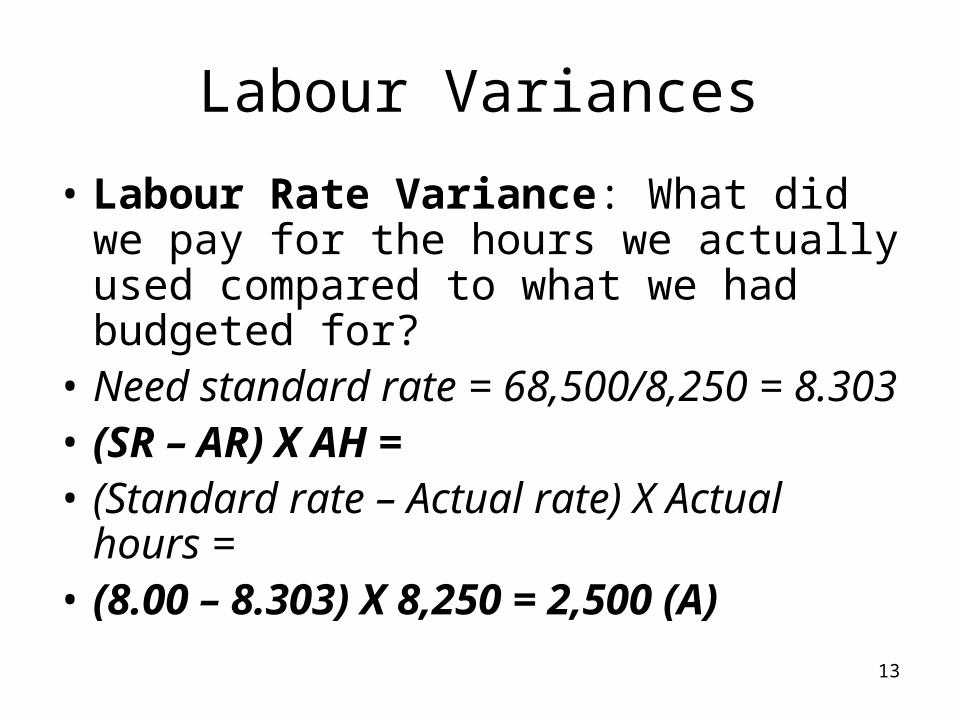

Labour Variances

• Labour Rate Variance: What did we pay for the hours we actually used compared to what we had budgeted for?

• Need standard rate = 68,500/8,250 = 8.303

• (SR – AR) X AH =• (Standard rate – Actual rate) X Actual

hours =• (8.00 – 8.303) X 8,250 = 2,500 (A)

14

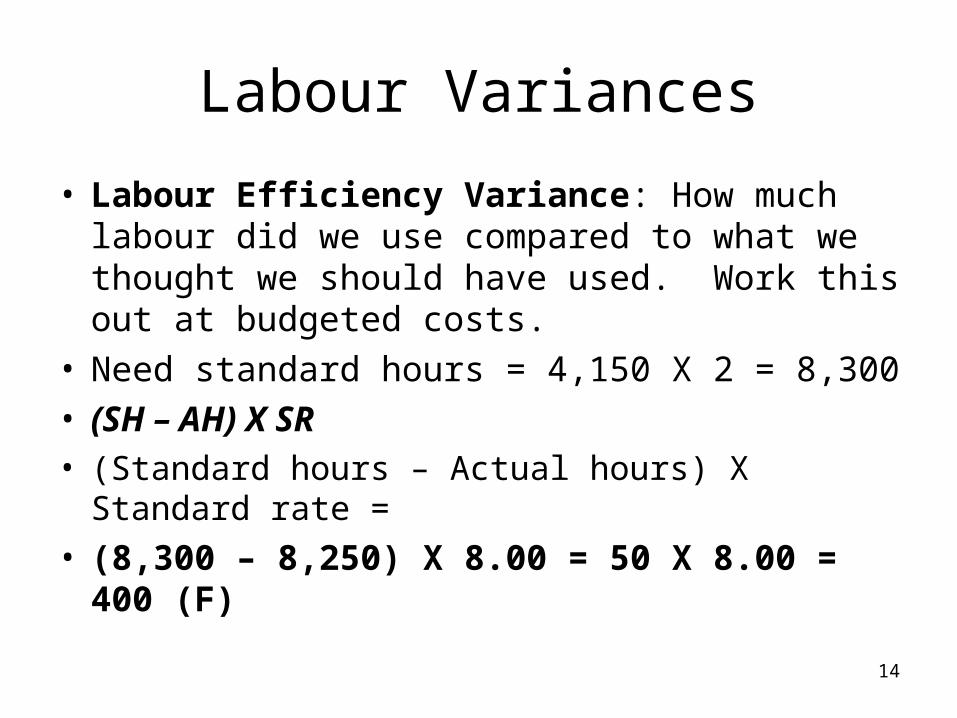

Labour Variances

• Labour Efficiency Variance: How much labour did we use compared to what we thought we should have used. Work this out at budgeted costs.

• Need standard hours = 4,150 X 2 = 8,300• (SH – AH) X SR• (Standard hours – Actual hours) X Standard rate =

• (8,300 – 8,250) X 8.00 = 50 X 8.00 = 400 (F)

15

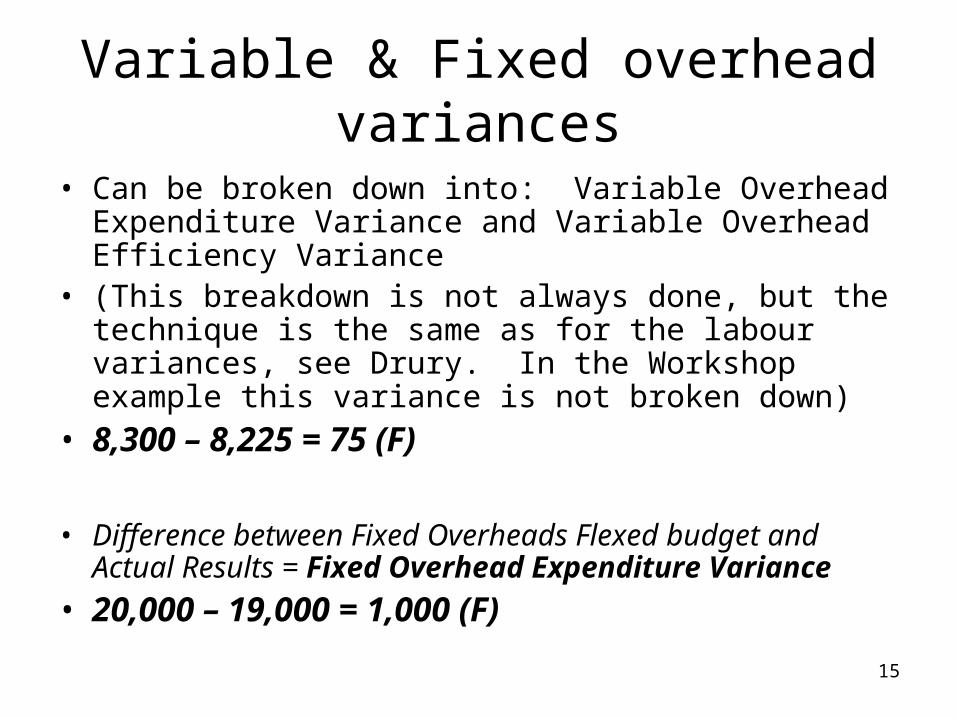

Variable & Fixed overhead variances

• Can be broken down into: Variable Overhead Expenditure Variance and Variable Overhead Efficiency Variance

• (This breakdown is not always done, but the technique is the same as for the labour variances, see Drury. In the Workshop example this variance is not broken down)

• 8,300 – 8,225 = 75 (F)

• Difference between Fixed Overheads Flexed budget and Actual Results = Fixed Overhead Expenditure Variance

• 20,000 – 19,000 = 1,000 (F)

16

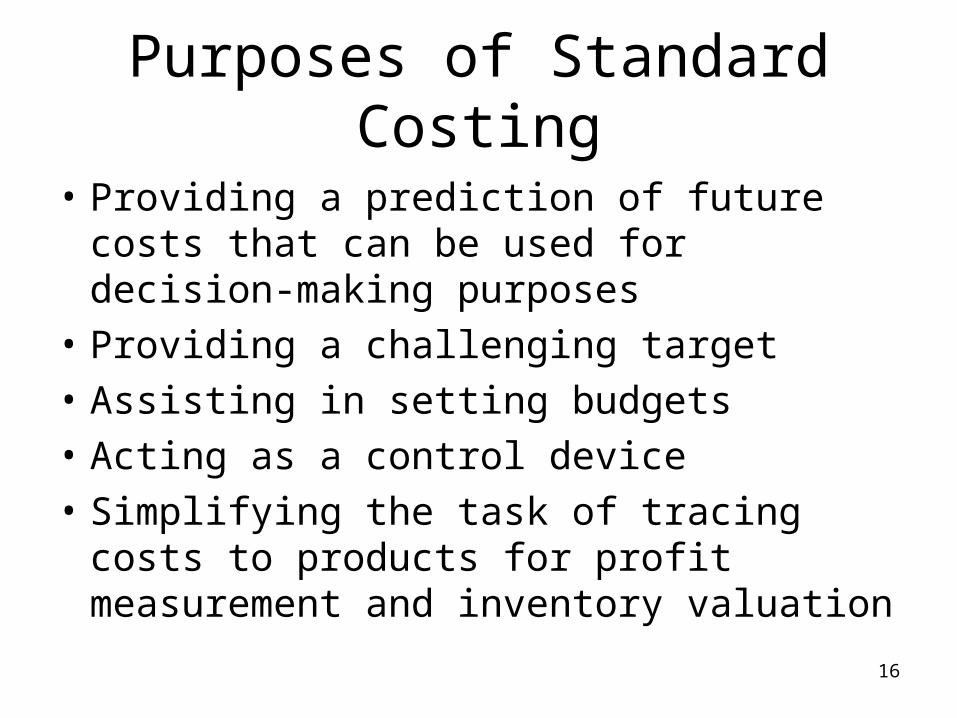

Purposes of Standard Costing

• Providing a prediction of future costs that can be used for decision-making purposes

• Providing a challenging target

• Assisting in setting budgets

• Acting as a control device

• Simplifying the task of tracing costs to products for profit measurement and inventory valuation

17

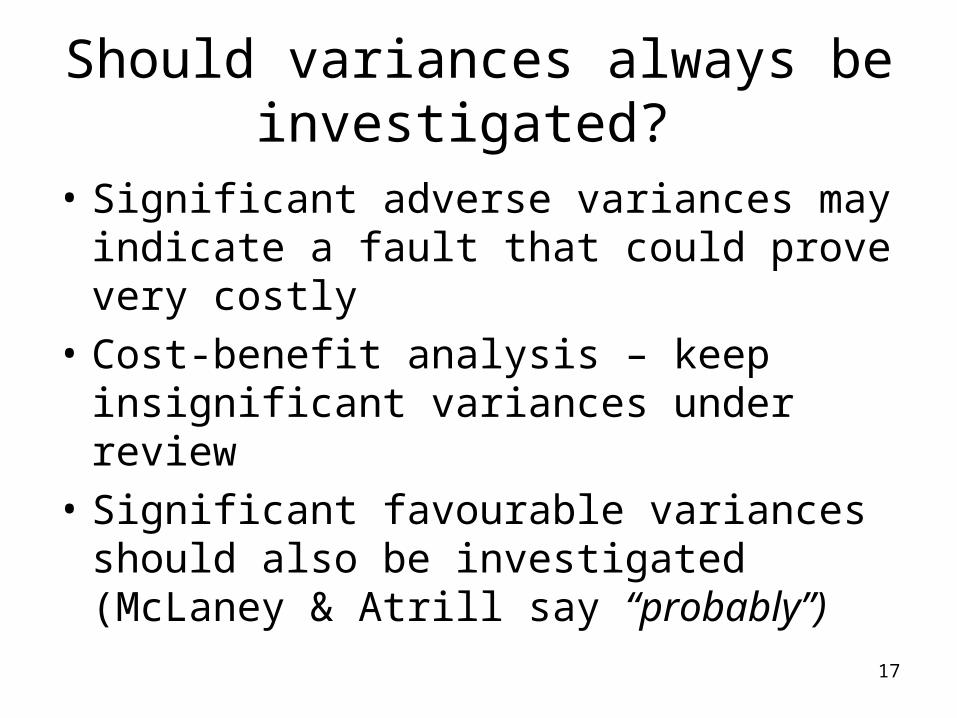

Should variances always be investigated?

• Significant adverse variances may indicate a fault that could prove very costly

• Cost-benefit analysis – keep insignificant variances under review

• Significant favourable variances should also be investigated (McLaney & Atrill say “probably”)

18

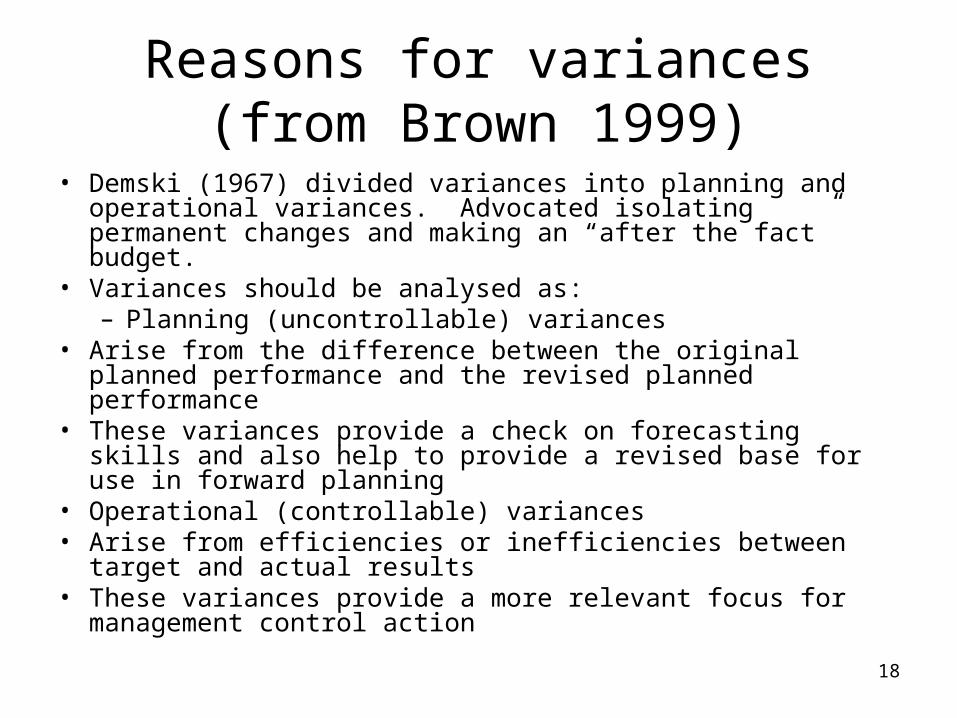

Reasons for variances (from Brown 1999)

• Demski (1967) divided variances into planning and operational variances. Advocated isolating permanent changes and making an “after the fact” budget.

• Variances should be analysed as:– Planning (uncontrollable) variances

• Arise from the difference between the original planned performance and the revised planned performance

• These variances provide a check on forecasting skills and also help to provide a revised base for use in forward planning

• Operational (controllable) variances• Arise from efficiencies or inefficiencies between target and

actual results• These variances provide a more relevant focus for

management control action

19

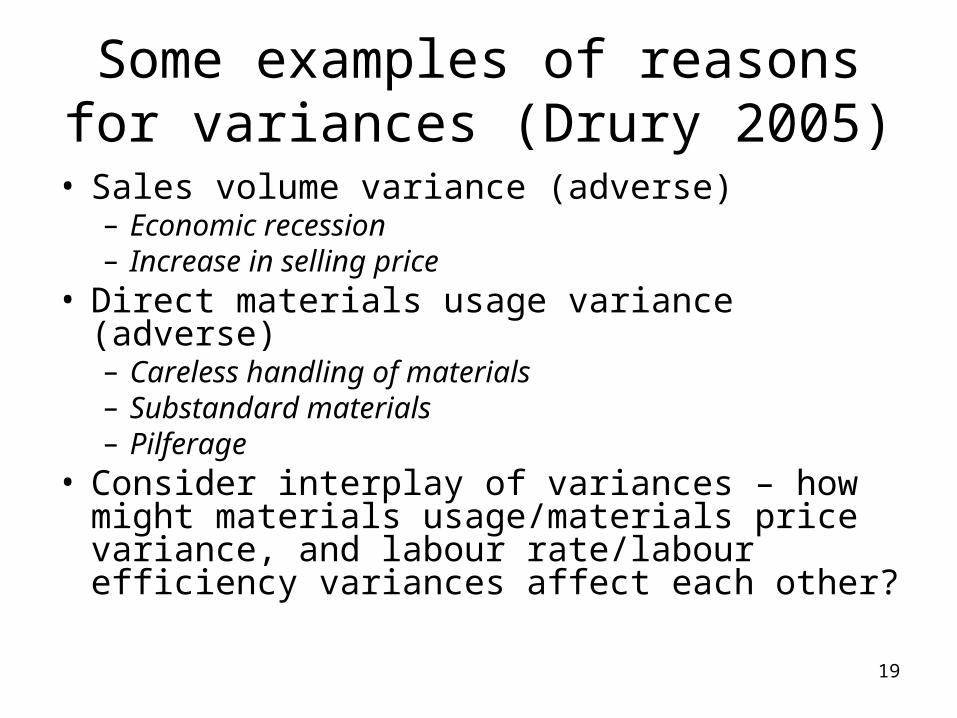

Some examples of reasons for variances (Drury 2005)

• Sales volume variance (adverse)– Economic recession– Increase in selling price

• Direct materials usage variance (adverse)– Careless handling of materials– Substandard materials– Pilferage

• Consider interplay of variances – how might materials usage/materials price variance, and labour rate/labour efficiency variances affect each other?

20

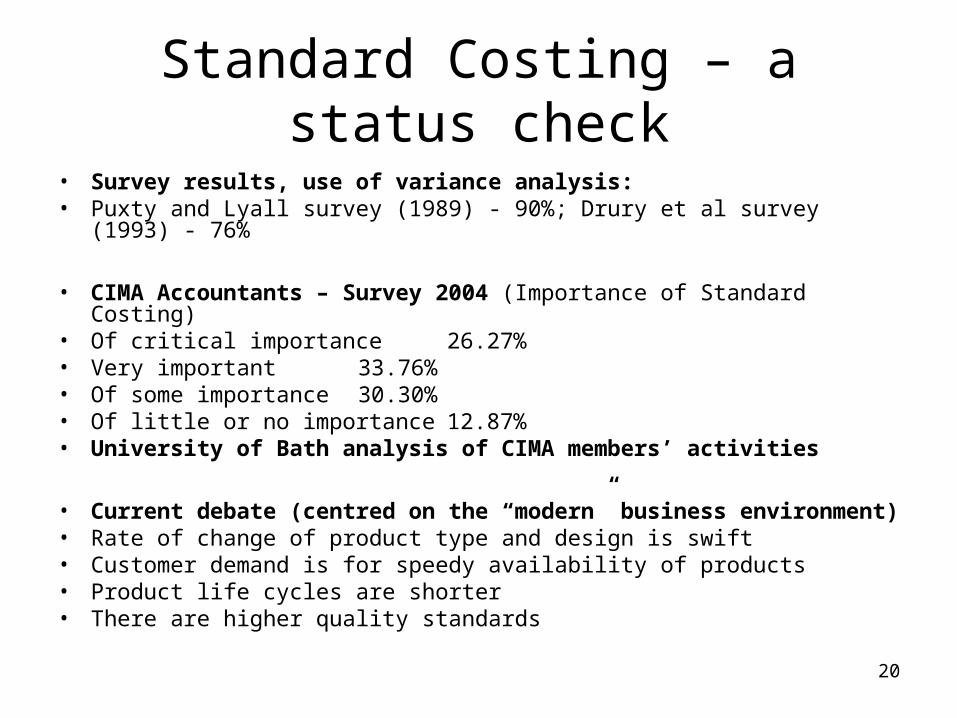

Standard Costing – a status check

• Survey results, use of variance analysis:• Puxty and Lyall survey (1989) - 90%; Drury et al survey (1993) - 76%

• CIMA Accountants – Survey 2004 (Importance of Standard Costing)• Of critical importance 26.27%• Very important 33.76%• Of some importance 30.30%• Of little or no importance 12.87%• University of Bath analysis of CIMA members’ activities

• Current debate (centred on the “modern” business environment)• Rate of change of product type and design is swift• Customer demand is for speedy availability of products• Product life cycles are shorter• There are higher quality standards

21

This has changed the way businesses operate, as follows:

• JIT systems allied to flexible manufacturing systems respond to customer demand

• TQM programmes aim at continuous improvement and effective provision of value-added activities

• Greater emphasis on the value chain• Changes to ABC and target costing• Improved speed and flexibility of information

availability e.g. online information in a computer integrated manufacturing environment

22

Criticisms of Standard Costing

• Impact of the changing cost structure - standard costing is most suited where there are direct and variable costs

• Inconsistency with a JIT philosophy (supplier chains, bulk purchases, effect on quality)

• Motivates behaviour that is inconsistent with TQM philosophy

• Overemphasises the importance of direct labour• Delay in feedback reporting• Standards are a static base against which actual events

are measured (standards can quickly become out of date; also see problem with TQM above)

23

More criticisms

• Their main objective is control, with conformance to standards and the elimination of any variances – this is seen as restrictive and inhibiting (problem for JIT and TQM systems)

• Can have adverse effects on performance if the link between cost and activity is not well understood, variances may be out of a manager’s control

• Areas of responsibility may not have clear lines of demarcation

• Even with these criticisms, there are still uses for standard costing and variance analysis – for a balanced view read Graham, Lyall and Puxty 1992

24

Points in favour of standard costing

• Planning • Standards may be useful as building blocks for

budgeting, which has to happen even in a TQM environment

• Control • Even where automated input of materials

occurs, it may still be relevant to analyse costs of changes from plan

• Decision making • Existing standards may be the starting point for

the estimated costs of new products

25

Points in favour of standard costing

• Performance measurement • When product mix is stable, performance monitoring

may be enhanced by the use of controllable standards• Product pricing • Use of standards can aid the construction of accurate

cost estimates for pricing. Target costs may be compared with current standards to highlight the “gaps” in costing – value engineering techniques might then be applied

• Improvement and change • Monitoring standards over time can help to identify

situations that are “out of control” (useful in TQM environments)

26

Kaplan & Norton – Balanced Scorecard

• Kaplan and Norton devised and later refined the notion of the “balanced scorecard”– Aim of the scorecard: to provide a comprehensive

framework for translating a company’s strategic objectives into a coherent set of performance measures

– Each organisation must decide what are its critical performance measures – this will vary over time and be linked to the strategy of the organisation

– Performance measures must be tied to strategies

27

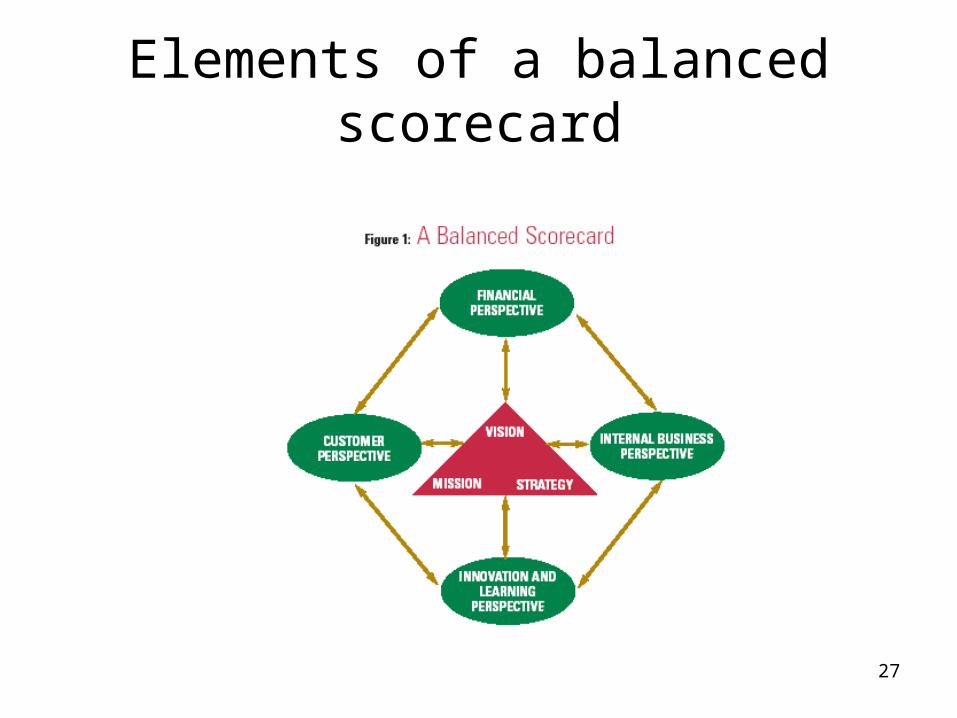

Elements of a balanced scorecard

28

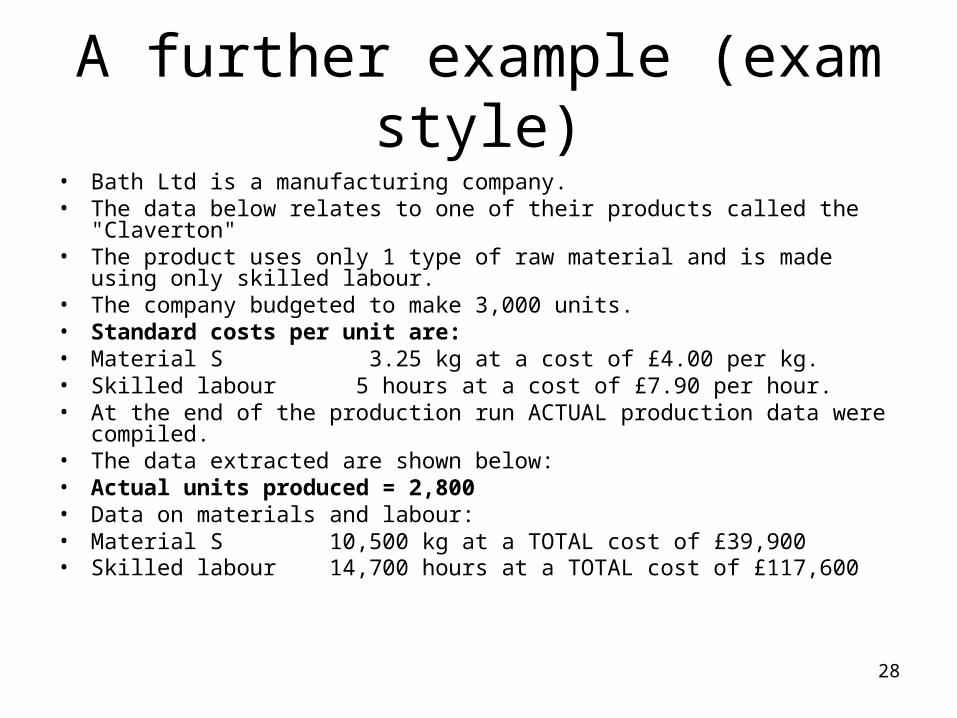

A further example (exam style)• Bath Ltd is a manufacturing company.• The data below relates to one of their products called the "Claverton"• The product uses only 1 type of raw material and is made using only skilled

labour. • The company budgeted to make 3,000 units.• Standard costs per unit are:• Material S 3.25 kg at a cost of £4.00 per kg.• Skilled labour 5 hours at a cost of £7.90 per hour.• At the end of the production run ACTUAL production data were compiled.

• The data extracted are shown below:• Actual units produced = 2,800• Data on materials and labour:• Material S 10,500 kg at a TOTAL cost of £39,900• Skilled labour 14,700 hours at a TOTAL cost of £117,600

29

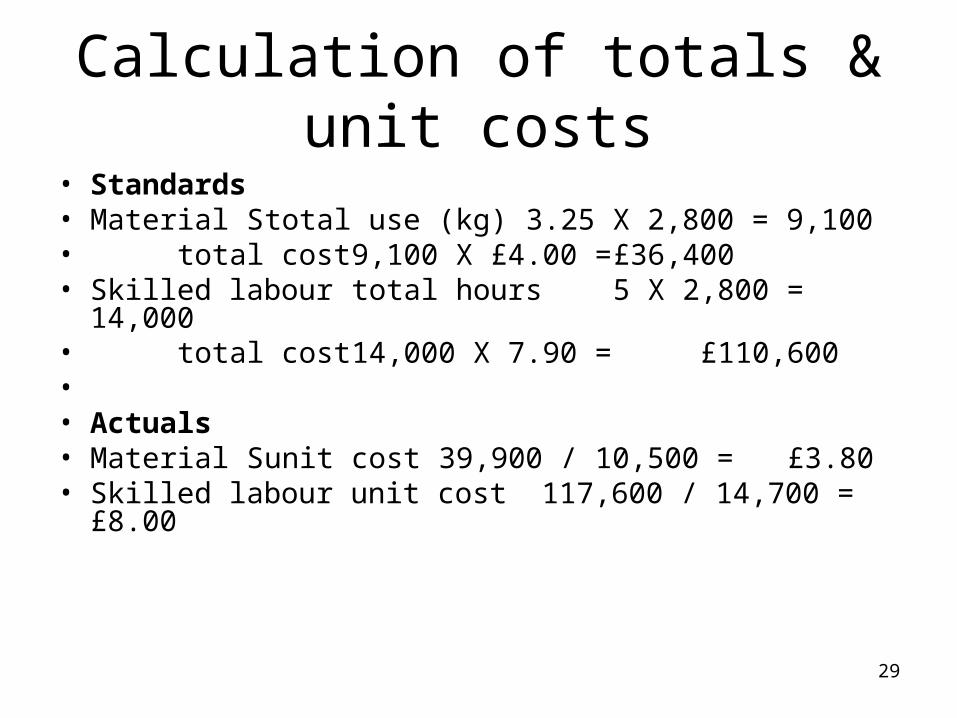

Calculation of totals & unit costs

• Standards• Material S total use (kg) 3.25 X 2,800 = 9,100• total cost 9,100 X £4.00 = £36,400• Skilled labourtotal hours 5 X 2,800 = 14,000• total cost 14,000 X 7.90 = £110,600•• Actuals• Material S unit cost 39,900 / 10,500 = £3.80• Skilled labour unit cost 117,600 / 14,700 = £8.00

30

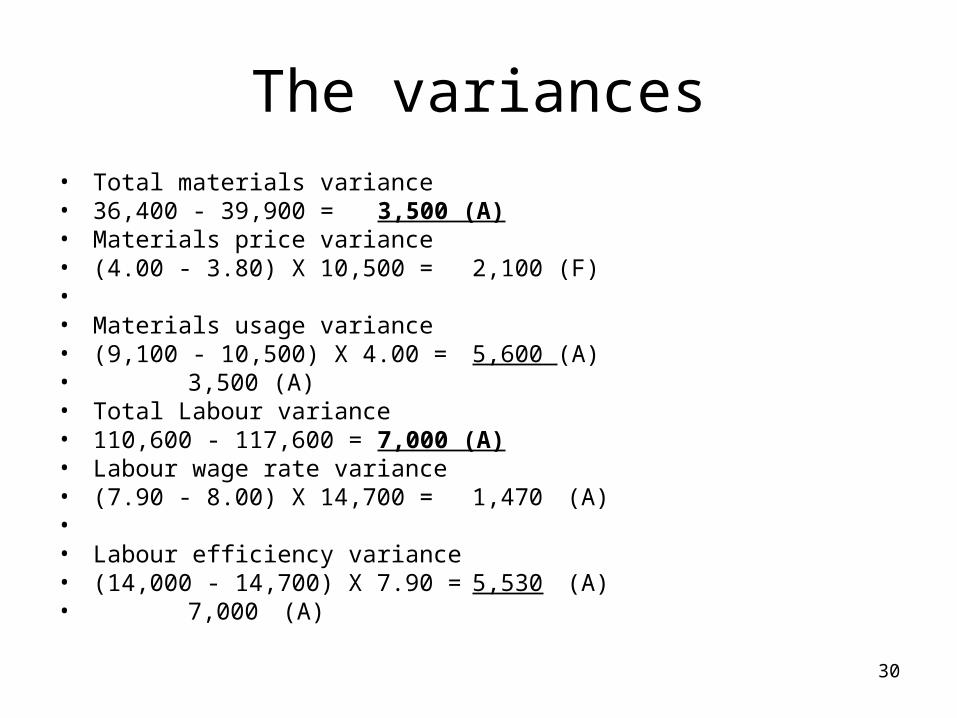

The variances• Total materials variance• 36,400 - 39,900 = 3,500 (A)• Materials price variance• (4.00 - 3.80) X 10,500 = 2,100 (F)•• Materials usage variance• (9,100 - 10,500) X 4.00 = 5,600 (A)• 3,500 (A)

• Total Labour variance• 110,600 - 117,600 = 7,000 (A)

• Labour wage rate variance• (7.90 - 8.00) X 14,700 = 1,470 (A)•• Labour efficiency variance• (14,000 - 14,700) X 7.90 = 5,530 (A)• 7,000 (A)