Embed Size (px)

Citation preview

Cerner Investment Community Meeting

Cerner Investment Community Meeting

February 24, 2009

Marc NaughtonSenior Vice President and Chief Financial Officer

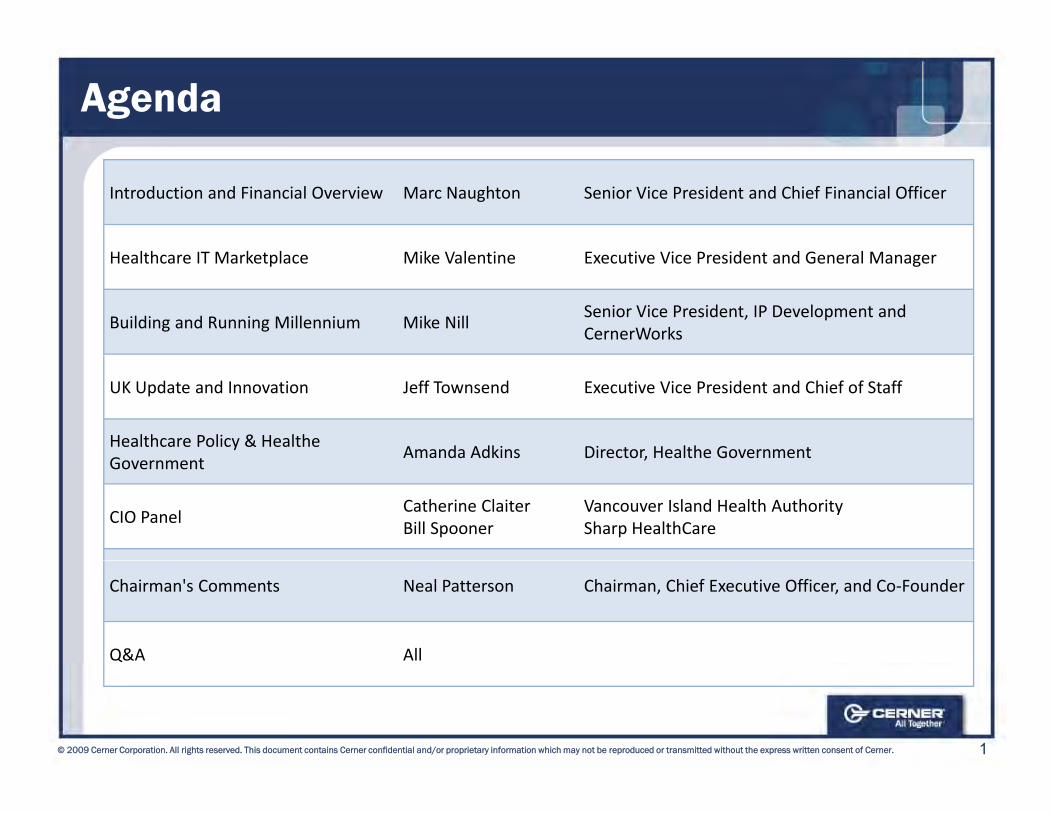

Agenda

Introduction and Financial Overview Marc Naughton Senior Vice President and Chief Financial Officer

H lth IT M k t l Mik V l ti E ti Vi P id t d G l MHealthcare IT Marketplace Mike Valentine Executive Vice President and General Manager

Building and Running Millennium Mike NillSenior Vice President, IP Development and CernerWorks

UK Update and Innovation Jeff Townsend Executive Vice President and Chief of Staff

Healthcare Policy & Healthe G

Amanda Adkins Director, Healthe GovernmentGovernment

a da d s ecto , ea t e Go e e t

CIO PanelCatherine ClaiterBill Spooner

Vancouver Island Health AuthoritySharp HealthCare

Chairman's Comments Neal Patterson Chairman, Chief Executive Officer, and Co‐Founder

Q&A All

1© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Safe Harbor StatementThis presentation may contain forward-looking statements that involve a number of risks and uncertainties. It is important to note that the Company’s performance, and actual results, financial condition or business could differ materially from those expressed in such forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to: (a) the possibility of product-related liabilities; (b) potential claims for system errors and warranties; (c) the possibility of interruption at our data centers or client support facilities; (d) our proprietary technology may be subject to claims for infringement or misappropriation of p p y gy y j g pp pintellectual property rights of others, or may be infringed or misappropriated by others; (e) risks associated with our global operations; (f) risks associated with our ability to effectively hedge exposure to fluctuations in foreign currency exchange rates; (g) risks associated with our recruitment and retention of key personnel; (h) risks related to our reliance on third party y p ; ( ) p ysuppliers; (i) risks inherent with business acquisitions; (j) changing political, economic and regulatory influences; (k) government regulation; (l) significant competition and market changes; (m) variations in our quarterly operating results; (n) potential inconsistencies in our sales forecasts compared to actual sales; and, (o) the volatility in the trading price of our p ( ) y g pcommon stock .

Additional discussion of these and other factors affecting the Company's business is contained in the Company's periodic filings with the Securities and Exchange Commission. The Company undertakes no obligation to update forward-looking statements to reflect

2© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

The Company undertakes no obligation to update forward looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes in future operating results, financial condition or business over time.

Cerner at a Glance

Founded in 1979, based in Kansas CityMost experienced healthcare IT managementLargest standalone healthcare IT company in world

Largest, most strategic worldwide healthcare IT client footprint

Over 6,000 hospital, health system, physician practice, clinic, laboratory, employer, government, and pharmacy client sitesclient sites

R&D Commitment and Clinical CultureOver $2B of cumulative R&DOver 900 CliniciansC l bl hiContemporary, scalable architectureMost comprehensive suite of healthcare solutions & services

2008 Revenues of $1,676M; Net Earnings of $180Mg10-year Revenue CAGR of 18% (mostly organic growth)10-year Earnings CAGR of 23%

7,600 Associates WorldwideOver 2 000 member Professional Services Organization

3© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Over 2,000 member Professional Services OrganizationOver 2,000 person Intellectual Property (IP) Organization

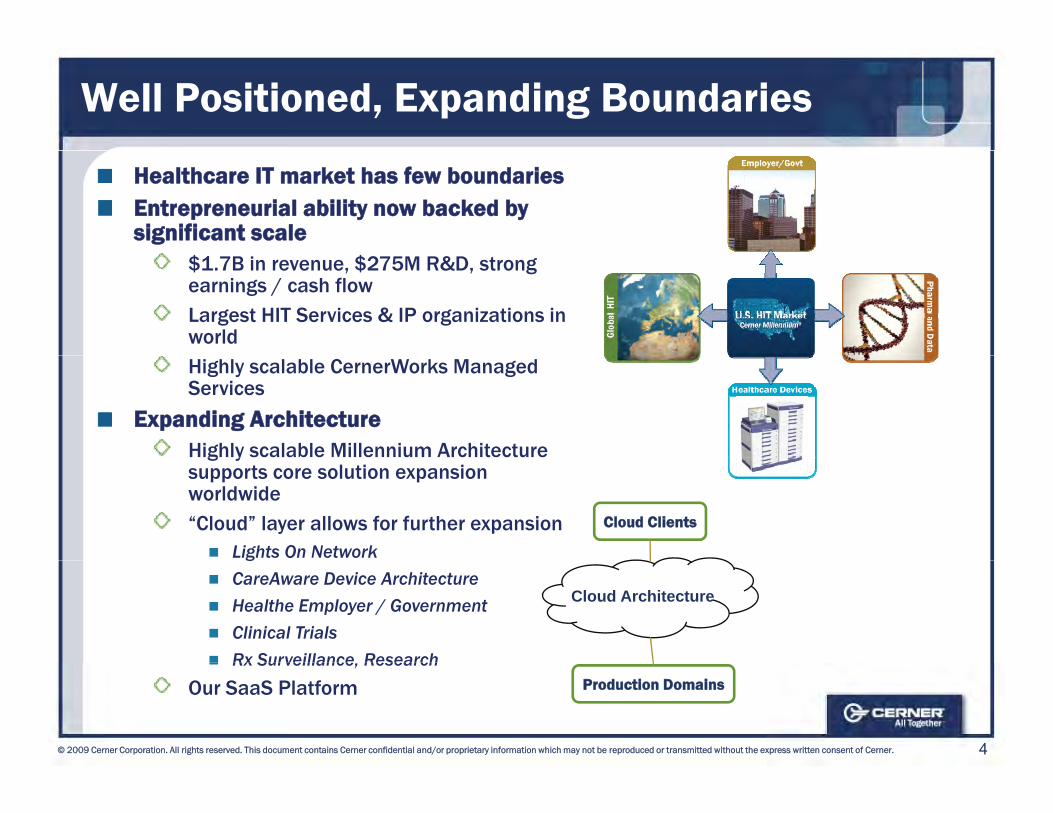

Well Positioned, Expanding Boundaries

Healthcare IT market has few boundaries Entrepreneurial ability now backed by significant scale

$1.7B in revenue, $275M R&D, strong earnings / cash flowLargest HIT Services & IP organizations in worldHighly scalable CernerWorks Managed Services

Expanding ArchitectureHighly scalable Millennium Architecture g ysupports core solution expansion worldwide“Cloud” layer allows for further expansion

Lights On Network

Cloud Clients

gCareAware Device ArchitectureHealthe Employer / GovernmentClinical TrialsRx Surveillance Research

Cloud Architecture

4© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Rx Surveillance, ResearchOur SaaS Platform Production Domains

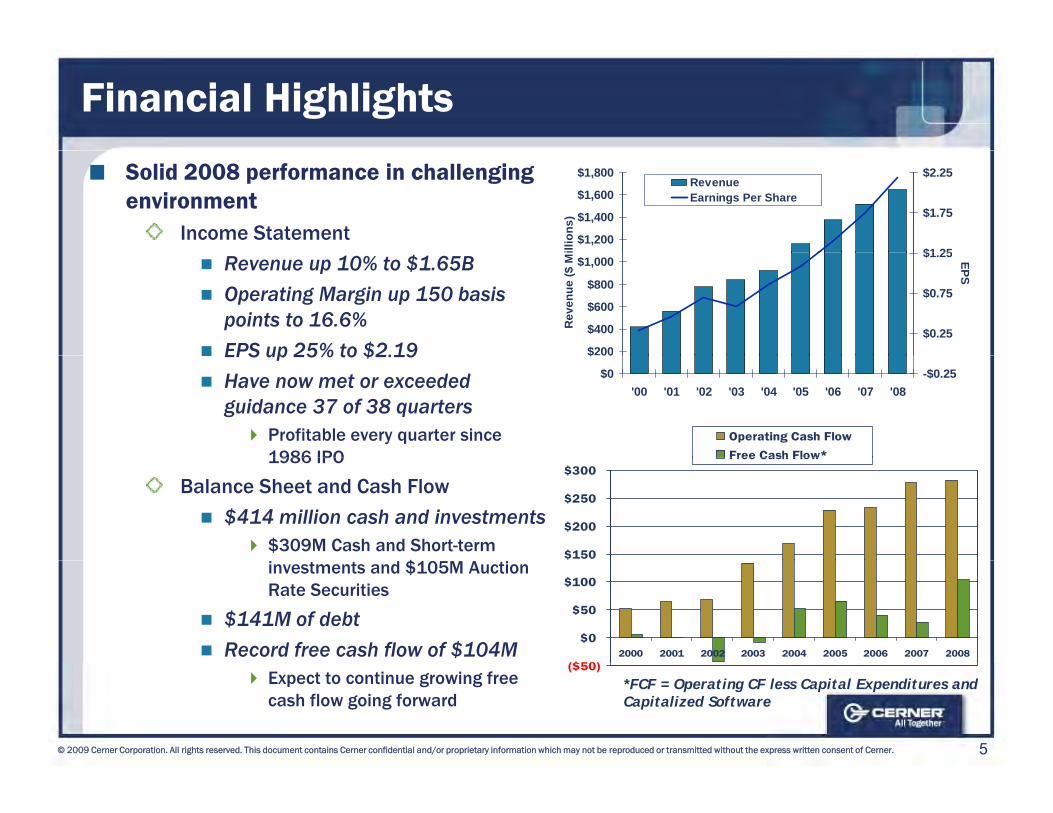

Financial Highlights

Solid 2008 performance in challenging environment

Income Statement $1,200

$1,400

$1,600

$1,800

illio

ns)

$1 25

$1.75

$2.25RevenueEarnings Per Share

Revenue up 10% to $1.65BOperating Margin up 150 basis points to 16.6%EPS up 25% to $2.19 $200

$400

$600

$800

$1,000

Rev

enue

($ M

$0.25

$0.75

$1.25 EPS

EPS up 25% to $2.19Have now met or exceeded guidance 37 of 38 quarters

Profitable every quarter since 1986 IPO

Operating Cash Flow

Free Cash Flow*

$0

$ 00

'00 '01 '02 '03 '04 '05 '06 '07 '08-$0.25

1986 IPO

Balance Sheet and Cash Flow

$414 million cash and investments$309M Cash and Short-term

$$150

$200

$250

$300Free Cash Flow

investments and $105M Auction Rate Securities

$141M of debtRecord free cash flow of $104M

($50)

$0

$50

$100

2000 2001 2002 2003 2004 2005 2006 2007 2008

5© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Expect to continue growing free cash flow going forward

($50)

*FCF = Operating CF less Capital Expenditures and Capitalized Software

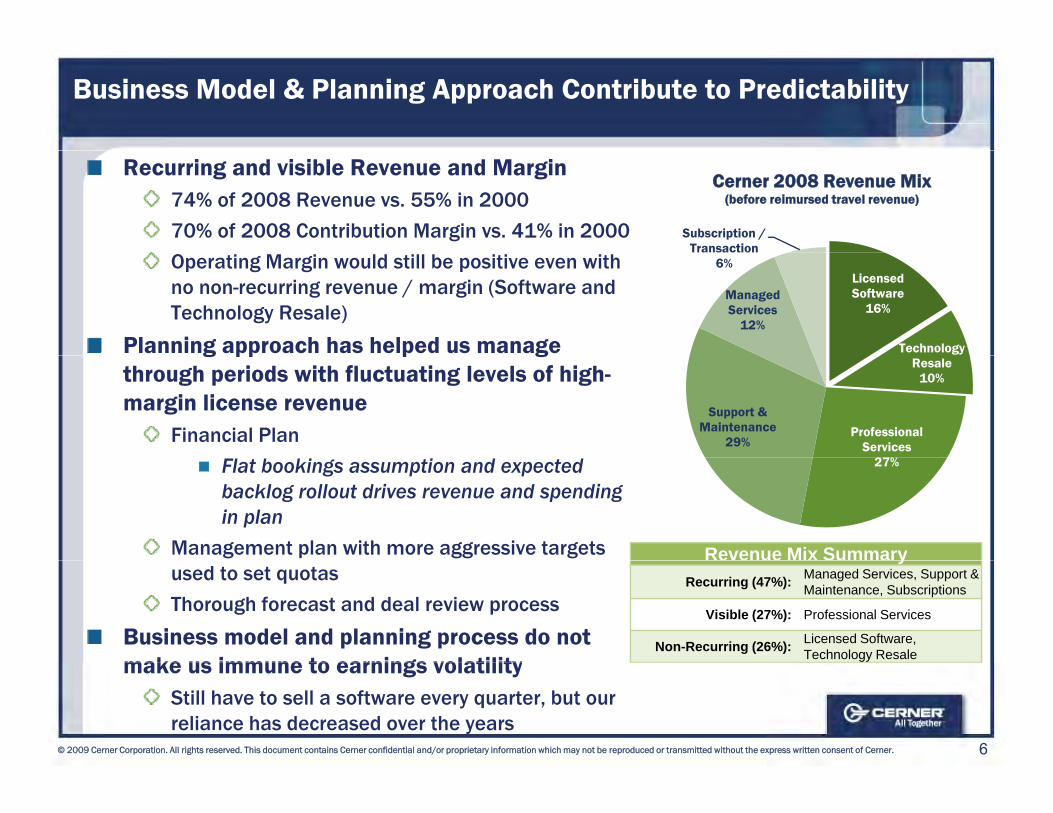

Business Model & Planning Approach Contribute to Predictability

Recurring and visible Revenue and Margin74% of 2008 Revenue vs. 55% in 2000

70% of 2008 Contribution Margin vs. 41% in 2000 Subscription / Transaction

Cerner 2008 Revenue Mix(before reimursed travel revenue)

Operating Margin would still be positive even with no non-recurring revenue / margin (Software and Technology Resale)

Planning approach has helped us manage

Licensed Software

16%

Technology

Managed Services

12%

6%

g pp p gthrough periods with fluctuating levels of high-margin license revenue

Financial Plan

Resale10%

Professional Services

27%

Support & Maintenance

29%

Flat bookings assumption and expected backlog rollout drives revenue and spending in plan

Management plan with more aggressive targets

27%

Revenue Mix Summaryused to set quotas

Thorough forecast and deal review process

Business model and planning process do not make us immune to earnings volatility

yRecurring (47%): Managed Services, Support &

Maintenance, Subscriptions

Visible (27%): Professional Services

Non-Recurring (26%): Licensed Software, Technology Resale

6© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

make us immune to earnings volatilityStill have to sell a software every quarter, but our reliance has decreased over the years

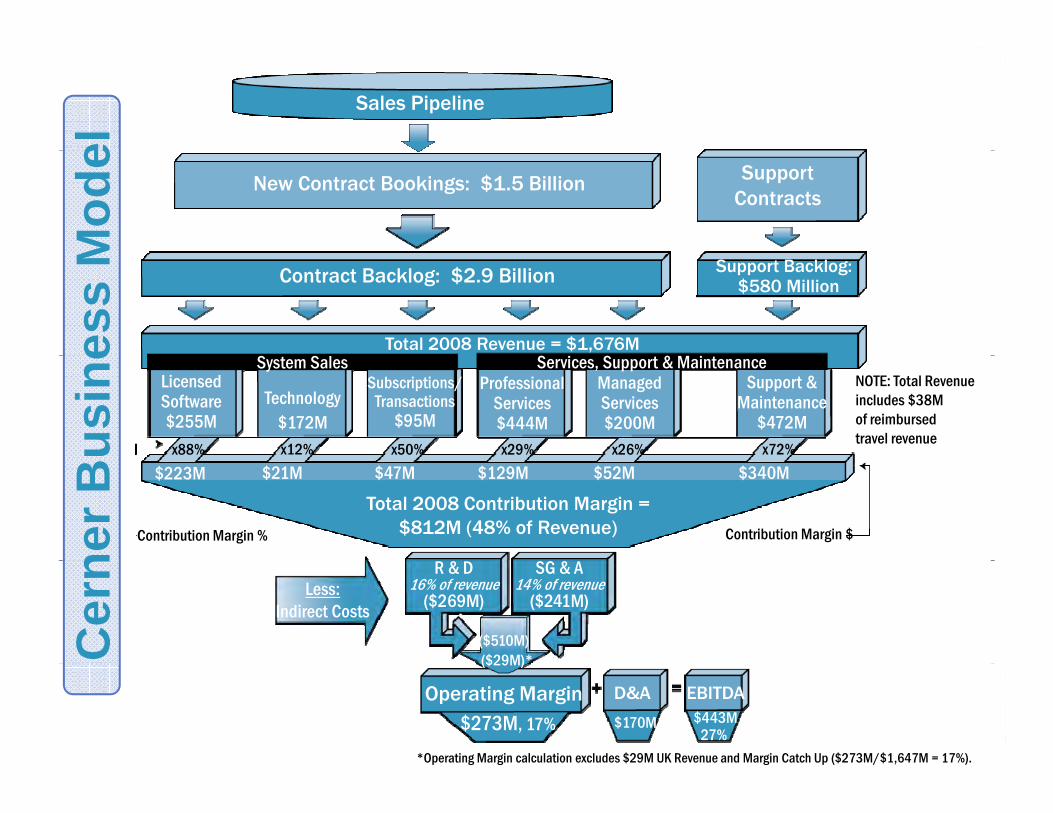

Sales Pipelineel

New Contract Bookings: $1.5 Billion SupportContracts

Mod

e

Contract Backlog: $2.9 Billion Support Backlog: $580 Million

Total 2008 Revenue = $1,676Mess

M

System Sales Services, Support & MaintenanceLicensedSoftware$255M

Subscriptions/Transactions

$95M

ProfessionalServices$444M

ManagedServices$200M

Support &Maintenance

$472Mx88% x12% x50% x29% x26% x72%

NOTE: Total Revenueincludes $38Mof reimbursedtravel revenue

Technology$172Mus

ine

Total 2008 Contribution Margin =$812M (48% of Revenue)Contribution Margin % Contribution Margin $

$223M $21M $47M $129M $52M $340M

ner B

Less:Indirect Costs

R & D16% of revenue

($269M)

SG & A14% of revenue

($241M)

($510M)($29M)*C

ern

7© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Operating Margin D&A EBITDA

$273M, 17% $170M $443M27%

*Operating Margin calculation excludes $29M UK Revenue and Margin Catch Up ($273M/$1,647M = 17%).

($29M)

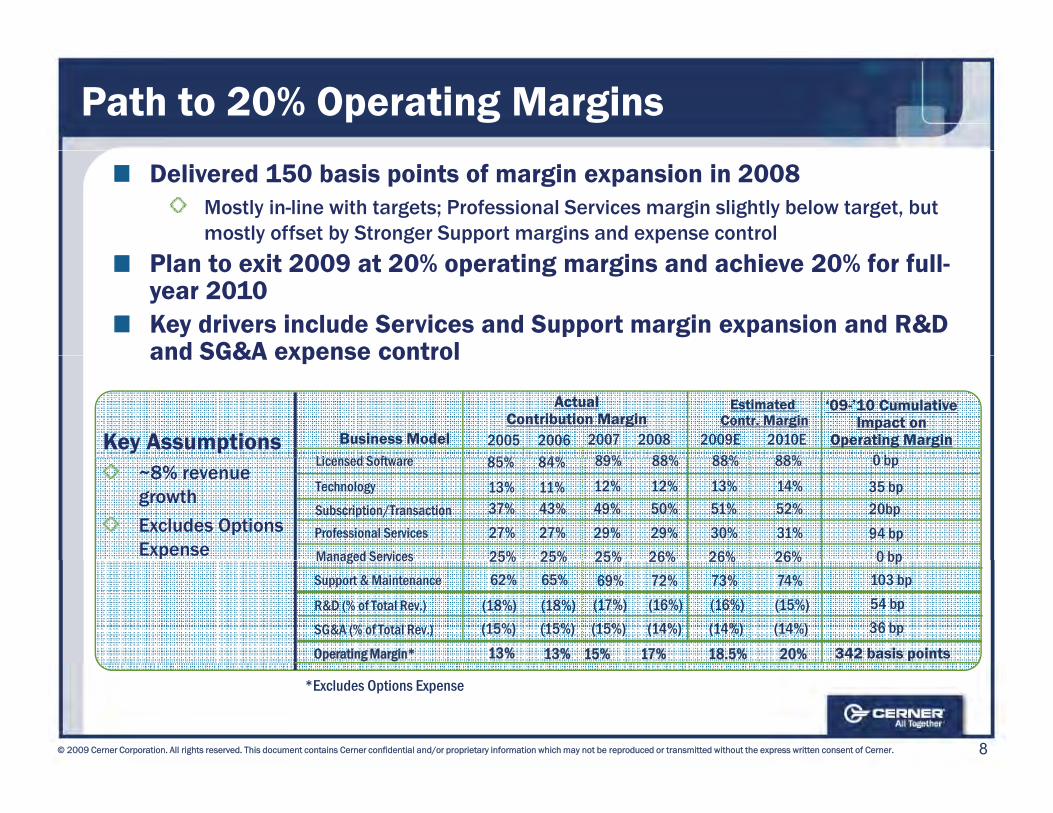

Path to 20% Operating Margins

Delivered 150 basis points of margin expansion in 2008Mostly in-line with targets; Professional Services margin slightly below target, but mostly offset by Stronger Support margins and expense control

Plan to exit 2009 at 20% operating margins and achieve 20% for full-year 2010Key drivers include Services and Support margin expansion and R&D and SG&A expense control

Key Assumptions

and SG&A expense control

Business Model

Actual Contribution Margin

Estimated Contr. Margin

‘09-’10 CumulativeImpact on

Operating Margin2005 200685% 84%

2007 2008 2009E 2010E89% 88% 88% 88%Li d S ft 0 bp

~8% revenue growth

Excludes Options Expense

85% 84%

37% 43%

89% 88% 88% 88%Licensed Software

Subscription/TransactionProfessional ServicesManaged Services

27% 27%25% 25%

49% 50% 51% 52%29% 29% 30% 31%25% 26% 26% 26%

13% 11% 12% 12% 13% 14%Technology

0 bp

35 bp20bp94 bp

0 bpManaged Services

Support & Maintenance

R&D (% of Total Rev.)

SG&A (% of Total Rev.)

25% 25%62% 65%

(18%) (18%)(15%) (15%)

25% 26% 26% 26%69% 72% 73% 74%

(17%) (16%) (16%) (15%)(15%) (14%) (14%) (14%)

0 bp103 bp54 bp36 bp

342 basis pointsOperating Margin* 13% 15% 17% 18.5% 20%13%

8© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

*Excludes Options Expense

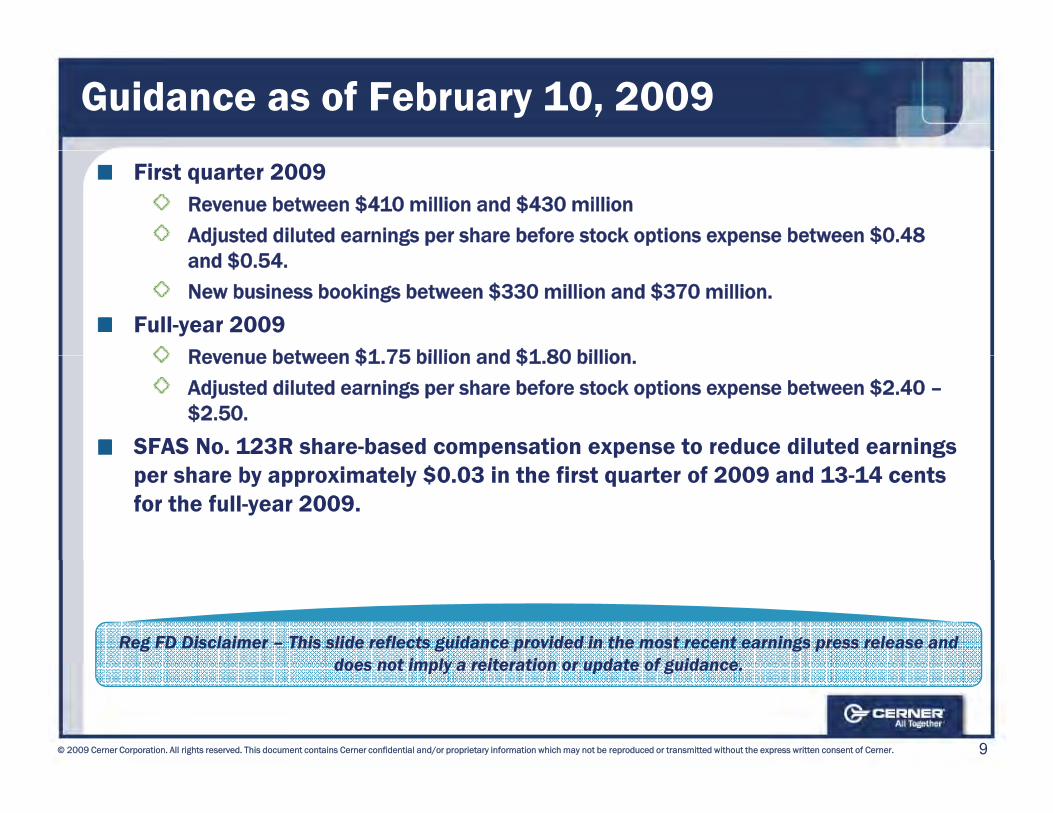

Guidance as of February 10, 2009

First quarter 2009Revenue between $410 million and $430 million

Adjusted diluted earnings per share before stock options expense between $0.48 $and $0.54.

New business bookings between $330 million and $370 million.

Full-year 2009Revenue between $1 75 billion and $1 80 billion Revenue between $1.75 billion and $1.80 billion.

Adjusted diluted earnings per share before stock options expense between $2.40 –$2.50.

SFAS No. 123R share-based compensation expense to reduce diluted earnings gper share by approximately $0.03 in the first quarter of 2009 and 13-14 cents for the full-year 2009.

Reg FD Disclaimer – This slide reflects guidance provided in the most recent earnings press release and does not imply a reiteration or update of guidance

9© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

does not imply a reiteration or update of guidance.

Healthcare IT Marketplace

Mike ValentineExecutive Vice President &General Manager

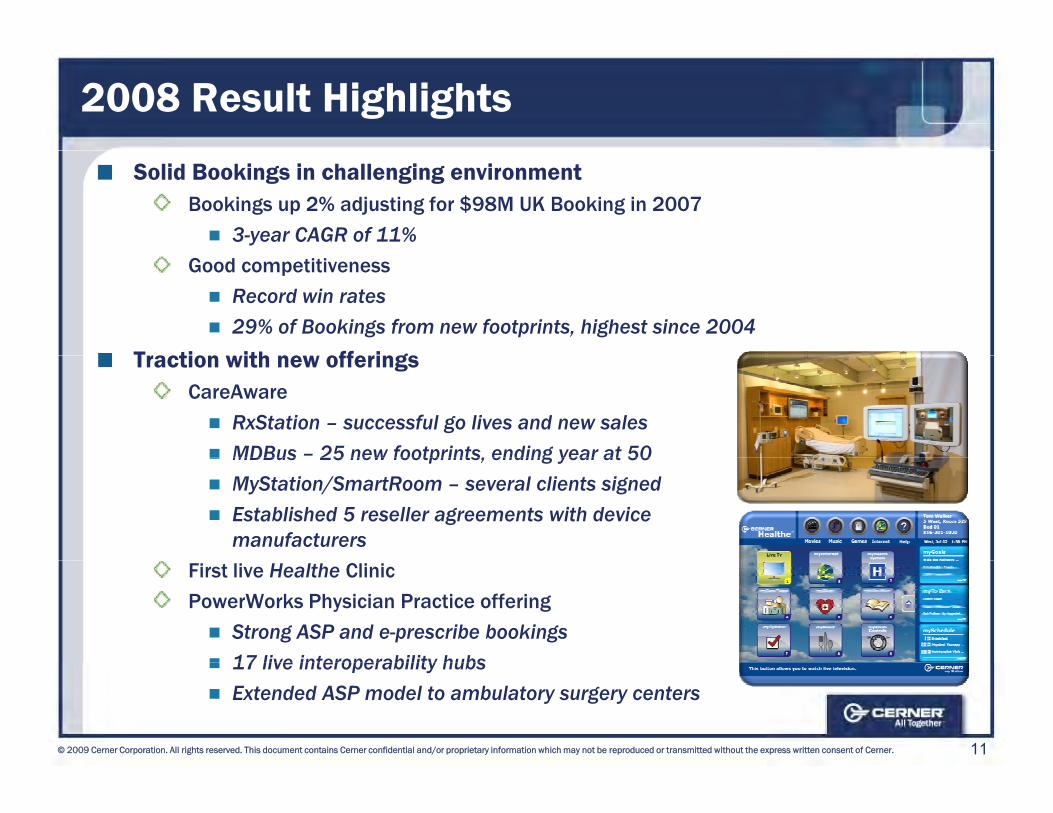

2008 Result Highlights

Solid Bookings in challenging environmentBookings up 2% adjusting for $98M UK Booking in 2007

3-year CAGR of 11%Good competitiveness

Record win rates29% of Bookings from new footprints, highest since 2004

Traction ith ne offeringsTraction with new offeringsCareAware

RxStation – successful go lives and new salesMDBus – 25 new footprints, ending year at 50MDBus 25 new footprints, ending year at 50MyStation/SmartRoom – several clients signedEstablished 5 reseller agreements with device manufacturers

First live Healthe Clinic

PowerWorks Physician Practice offering

Strong ASP and e-prescribe bookings17 live interoperability hubs

11© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

17 live interoperability hubsExtended ASP model to ambulatory surgery centers

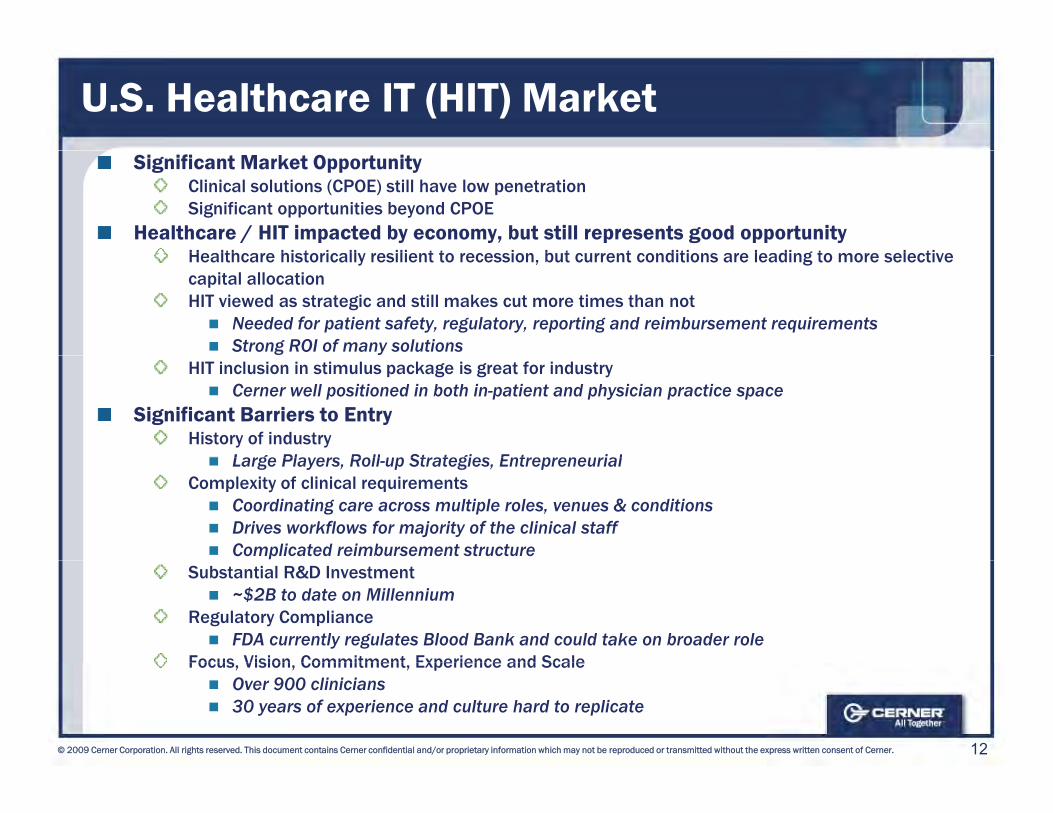

U.S. Healthcare IT (HIT) MarketSignificant Market Opportunity

Clinical solutions (CPOE) still have low penetrationSignificant opportunities beyond CPOE

Healthcare / HIT impacted by economy, but still represents good opportunityHealthcare historicall resilient to recession b t c rrent conditions are leading to more selecti e Healthcare historically resilient to recession, but current conditions are leading to more selective capital allocationHIT viewed as strategic and still makes cut more times than not

Needed for patient safety, regulatory, reporting and reimbursement requirementsStrong ROI of many solutions

HIT inclusion in stimulus package is great for industryCerner well positioned in both in-patient and physician practice space

Significant Barriers to EntryHistory of industry

Large Players Roll up Strategies EntrepreneurialLarge Players, Roll-up Strategies, EntrepreneurialComplexity of clinical requirements

Coordinating care across multiple roles, venues & conditionsDrives workflows for majority of the clinical staffComplicated reimbursement structure

Substantial R&D Investment~$2B to date on Millennium

Regulatory ComplianceFDA currently regulates Blood Bank and could take on broader role

Focus Vision Commitment Experience and Scale

12© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Focus, Vision, Commitment, Experience and ScaleOver 900 clinicians 30 years of experience and culture hard to replicate

Growth Opportunities

Playing OffenseSelling high ROI ‘whitespace’ solutions into installed baseReplace best-of-breed and unsuccessful suppliers

N M k t d S i

Whitespace & High ROIFocus Areas

AnesthesiologyClinical Process New Markets and Services

Physician Office, Retail PharmacyEmployer/Government

Personal Health Record

Clinical Process OptimizationCritical CareDevices, MDBus, Smart Room

Financial / Clinical HubsCondition ManagementBenefits / TPAFacilitated Network Model

Smart RoomEmergencyRevenue CycleSurgery

Facilitated Network ModelClinical TrialsRx Surveillance, ResearchCapture a larger portion of hospital IT spend with CernerWorks capabilities

Women’s Health

Application Management ServicesITWorks

Leveraging infrastructure to take on additional client IT workAccelerate white space, replace competitors

13© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Tightens alignment with key clients

Revenue Cycle MarketGeneral market observations

40% of healthcare organizations are planning to replace their legacy revenue cycle solutions, specifically the patient accounting application

Required to meet clinically-based pay-for-performance requirementsEmerging set of niche service suppliers and services based roll-upsO ffOutsourcing the business office

Most healthcare organizations are not staffed to manage the end-to-end processCommunity health systems are looking for cost containment; increased Community health systems are looking for cost containment; increased interest in hosted and service based models

Cerner’s opportunityRevenue cycle white space represents a $2B+ opportunityRevenue cycle white space represents a $2B opportunity50% of new business pipeline includes revenue cycle as a component70% of large installed clients have not licensed ProFit

14© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

70% of large installed clients have not licensed ProFitClinical and financial integration opportunity

Differentiated Services & OperationsIntegrated services create predictable outcomes and ongoing improvements

Professional Services

Implementation Learning Adoption ServicesImplementation, Learning, Adoption ServicesCenters

Solutions CenterUpgrade CenterpgExperience Center

Managed Services

Remote HostingApplication Management ServicesOperations ManagementLights On Network

Tools and Methodologies

Implementation Hours / Solution

Tools and Methodologies

Bedrock, MethodMMillennium Lighthouse® Clinical Process Optimization

15© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

These investments in operational efficiency position us well to handle stimulus surge

2005 2006 2007 2008

Significant Global Opportunity, Strong Results

Presence in 25 countries, 6 continentsMillennium available in 4 languages

Market share leader in United Kingdom, Middle East Canada Australia East, Canada, Australia

Market share leader in United Kingdom, Middle East, Canada, Australia

Growing presence in France, Spain, Ireland,

Germany Egypt South America Malaysia

$300

$350

$400

ions

) 20%

25%Global RevenuePercent of Total Revenue

Germany, Egypt, South America, Malaysia,

Singapore

Strong Financial Results$100

$150

$200

$250

Rev

enue

($ M

illi

10%

15%

% of Total

47% 5-year CAGR

$53M in 2003 to $368M in 20086% of revenue to 22% of revenue

Increasing profitability

$0

$50

$100

'02 '03 '04 '05 '06 '07 '08

R

0%

5%

Broadening diversity of revenueSix regions with more than $10M of revenue in 2008 including 4 with more than $20M

16© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

2008, including 4 with more than $20M

Building and Running Millennium

Mike NillSenior Vice President, IP ,Development & CernerWorks

Cerner Millennium Release 2007.18

Became generally available February 6, 2009Leverages Millennium 2007 platform to simplify migration pathOver 2,200 major enhancements

Continued focus on user interface and workflow enhancementsContinued focus on user interface and workflow enhancementsImproved quality

Major positive impact on clients by resolving 98% of priority issues from 2007 releaseHighlights

Women’s HealthWomen s HealthIntegrates all clinical information for mother and baby -- pregnancy through the post-partum

RadiologyImproved workflow and reporting

ImagingImagingAdditional multimedia types in clinical notes; image querying; MultiMedia Manager.

Bedside CareImproved point of care documentation; real time input of vital information

ePrescribingePrescribingEnhanced functionality and views of patients medication history and prescription plan

Medication ReconciliationImproved workflow, integration, and documentation

Cerner ProVision Document Imaging

18© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Cerner ProVision Document ImagingEnhanced integration with Powerchart increases intradepartmental communication

Improving Physician and Nurse Experience

Measure User EffortAdditional Lights On physician/nursing productivity measures

Measuring effort required to complete workflowsFocus on Orders/RXFocus on Orders/RX

Optimize Current SolutionsUtilize Lights On data to optimize existing Millennium Solutions

Audits assessing accuracy of build and best practice utilizationAudits assessing accuracy of build and best practice utilizationDrive improvements through Client Experience Center/Upgrade Center

Bedrock Reference Audits

Focus on Improved WorkflowsKnowledge at point of care

Workflow driver in the context of care

Quality Indicators dynamically satisfied

V i ffi i t i ti t lVoice as an efficient communication tool

Natural Language Processing

Automated Coding to assure appropriate reimbursement

Seamlessly Assure regulatory compliance

19© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Seamlessly Assure regulatory compliance

Minable data to change healthcare

Aligning and Measuring IP PerformanceClient and Business Alignment

Close, daily cooperation between the business needs and development – “Greater A f S l ti ”

IP Development Metrics

Accuracy of Solutions”Solution Partner programIP/Client Alignment BoardRelease summary/client interest

QualityDefects by Engineer/ReleasePackage Failure Rate/QtrSR Backlog Trend, Backlog Aging, Open/Close RatesRelease summary/client interest

Collaboration Rooms

Improving productivity and accountabilityMake quality assumed

g g pInnovation

# and % of Themes Delivered Per Release

On Time% of Scope Delivered On TimeMake quality assumed

Measuring quality of code by developer Accountability for defects

Increase quality upfront

% of Scope Delivered On Time% of Obligations Met/Qtr

StabilityCrashes per Client User/DayStability Defects per

Less rework and more cycles for productive development

Deliver capabilities once – limit patch backs

Engineer/ReleasePerformance

% of Client Transactions < 2 Seconds

Productivity

20© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

backs

Automated testingProductivity

Defect CRs Fixed per Engineer/MonthFeatures per Engineer/Release

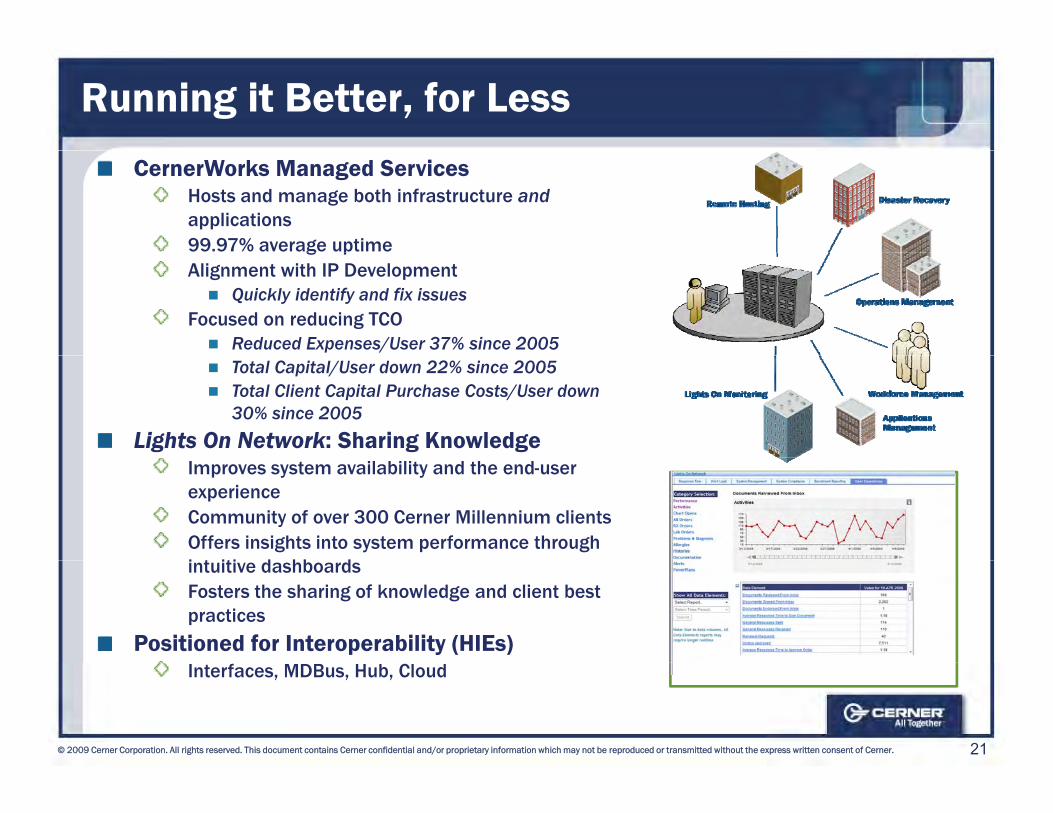

Running it Better, for Less

CernerWorks Managed ServicesHosts and manage both infrastructure andapplications99.97% average uptimeg pAlignment with IP Development

Quickly identify and fix issuesFocused on reducing TCO

Reduced Expenses/User 37% since 2005Total Capital/User down 22% since 2005 Total Client Capital Purchase Costs/User down 30% since 2005

Lights On Network: Sharing KnowledgeImproves system availability and the end-user experienceCommunity of over 300 Cerner Millennium clients Offers insights into system performance through i t iti d hb dintuitive dashboardsFosters the sharing of knowledge and client best practices

Positioned for Interoperability (HIEs)

21© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Interfaces, MDBus, Hub, Cloud

U.K. Update and Innovation

Jeff TownsendExecutive Vice President and Chief of Staff

U.K. Background and UpdateChoose and Book national e-scheduling solution

Selected in 2003 with Atos OrigonSystem now used for about half of all appointments; recently signed 2-year extension

Southern RegionBackground

Replaced prior software provider in 2005Prime contractor, Fujitsu, withdrew from program in 2008Transition agreement for 8 live trusts signed with Fujistu

UpdateBT, our prime contractor in London, is positioned to take over the 8 live trustsPending opportunities in remaining trusts

LondonBackground

Replaced prior software provider in 2006Overall solid progress, but there was a slowdown in activity in 2008

UpdateWorking closely with BT, closed gap on several issues by leveraging Cerner Millennium and our proven implementation methodologiesAfter a pause at many sites, given ‘green light’ to begin ramping activitiesAfter only recognizing revenue equal to our expense, we are now recognizing margin

$28 6M t h i d i Q408

23© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

$28.6M catch up recognized in Q408

Overall, positioned to make good progress in 2009

Innovation Campus - Collaboration Center

6 SuitesPhysical layout w/ help of Steelcase + Collaboration Design Rooms

Ph i iPhysicianConsumer (Home / Work /….)ICUWomen’s HealthImagingCareAware (Devices)In Process: Caregiver CenterStartup: Workforce & Enterprise Tracking

Focus is on Innovation & Real World design (“beyond the screen”)Other Collaboration Areas

Abilities Lab

HealthPresence (Cisco)

Collaboration Friday’s (Team Demonstrations)

24© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Demonstrations)

Café

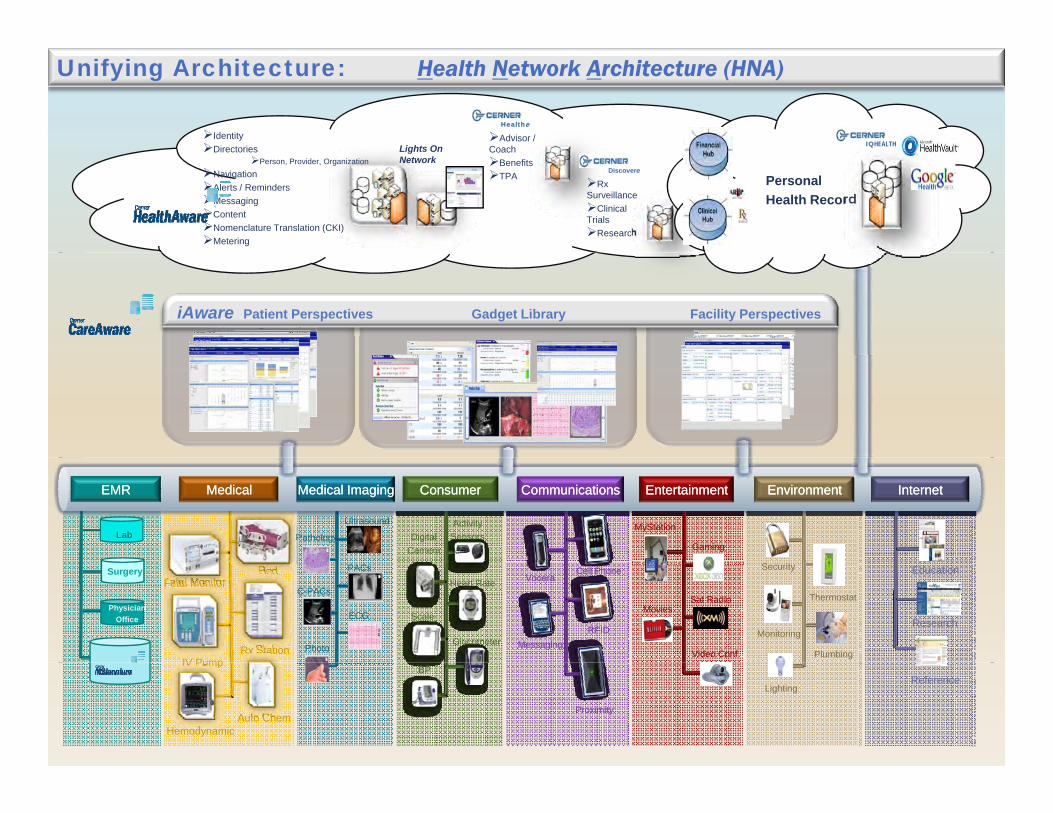

Unifying Architecture: Health Network Architecture (HNA)

IdentityDirectories Lights On

Advisor / Coach

Healthe

IQHEALTHDirectoriesPerson, Provider, Organization

NavigationAlerts / RemindersMessagingContentNomenclature Translation (CKI)Metering

Lights On Network

Rx Surveillance

Clinical Trials

Research

Discovere

CoachBenefitsTPA Personal

Health Record

iAware Patient Perspectives Gadget Library Facility Perspectives

PathologyLabActivitySensorsDigital

Camera Gaming

MyStation

EMREMR MedicalMedical Medical ImagingMedical Imaging ConsumerConsumer CommunicationsCommunications EntertainmentEntertainment EnvironmentEnvironment InternetInternet

Ultrasound

PACs

C-PACs

PhysicianOffice

Surgery Bed

Rx StationIV Pump

ECG

Photo

Vocera

Scale

Heart Rate

GlucometerRFID

Messaging

Cell Phone

Video Conf

Sat RadioMovies

Security

Thermostat

Monitoring

Plumbing

Education

Research

Fetal Monitor

25© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

HemodynamicAuto Chem

IV PumpBP

Proximity

LightingReference

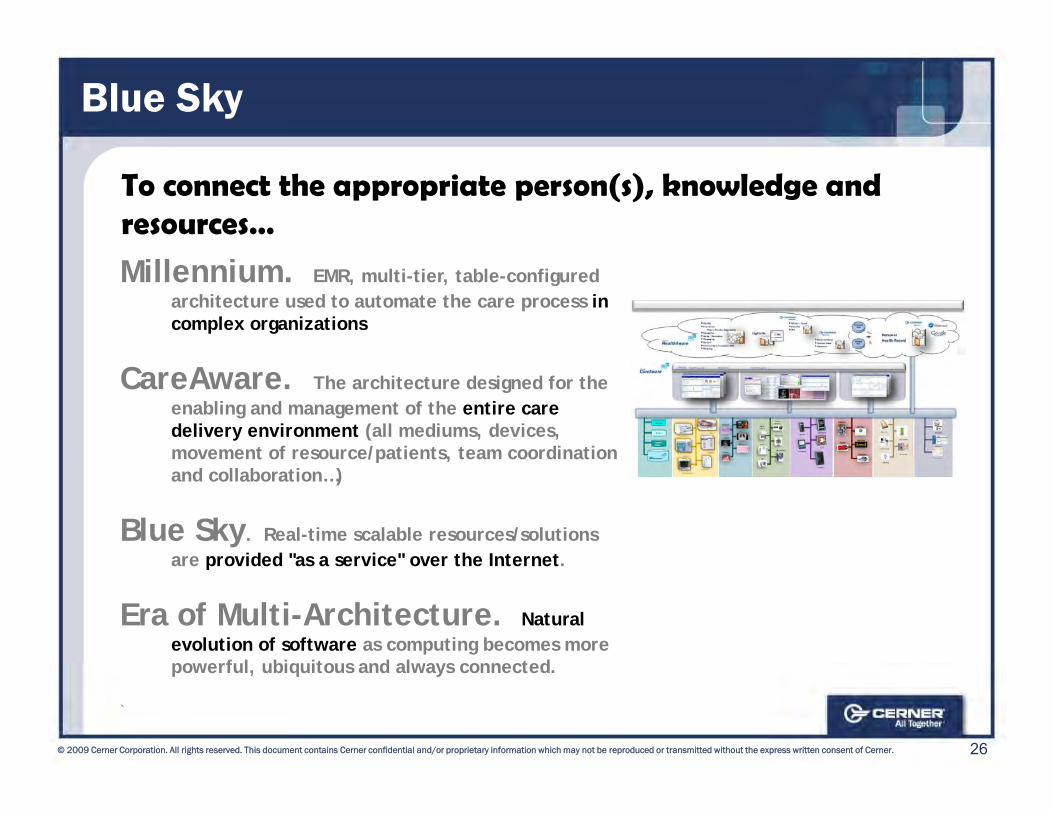

Blue Sky

To connect the appropriate person(s), knowledge and resources…

Millennium. EMR, multi-tier, table-configured architecture used to automate the care process in complex organizations

CareAware. The architecture designed for the enabling and management of the entire care delivery environment (all mediums, devices, movement of resource/patients, team coordination movement of resource/patients, team coordination and collaboration…)

Blue Sky. Real-time scalable resources/solutions are provided "as a service" over the Internetare provided as a service over the Internet.

Era of Multi-Architecture. Natural evolution of software as computing becomes more po erf l biq ito s and al a s connected

26© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

powerful, ubiquitous and always connected.

`

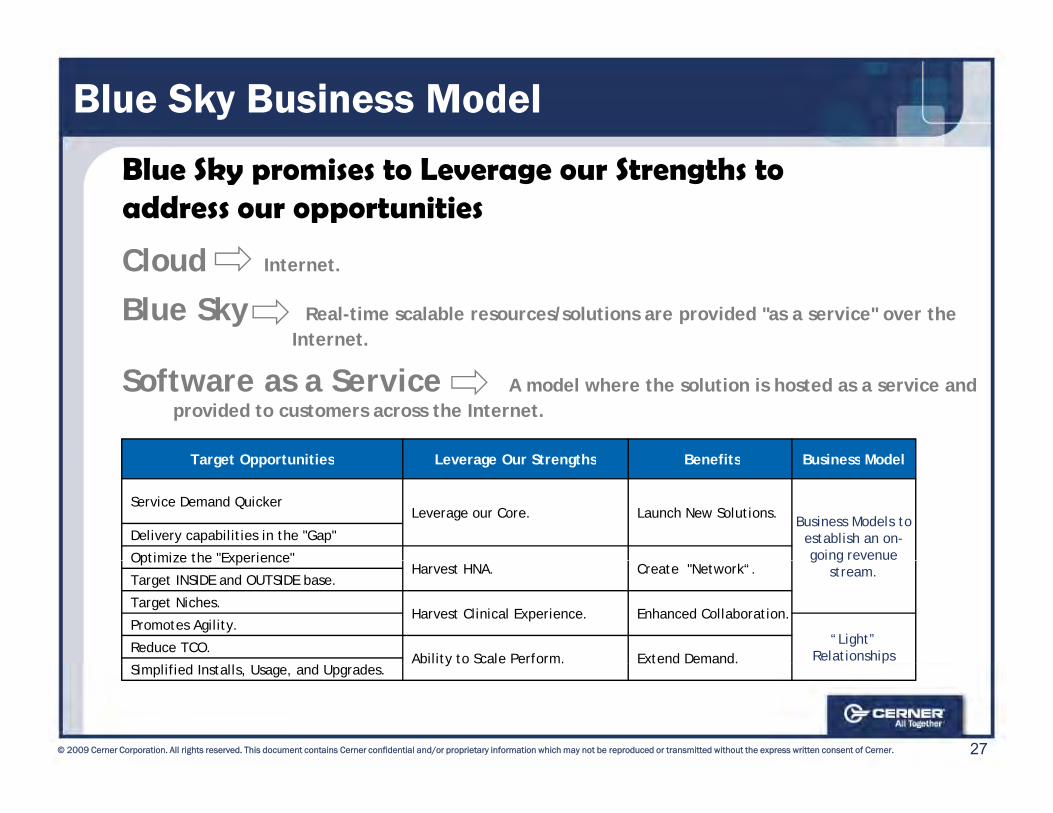

Blue Sky Business Model

Blue Sky promises to Leverage our Strengths to address our opportunities

Cl d Cloud Internet.

Blue Sky Real-time scalable resources/solutions are provided "as a service" over the Internet.

Target Opportunities Leverage Our Strengths Benefits Business Model

Software as a Service A model where the solution is hosted as a service and provided to customers across the Internet.

Target Opportunities Leverage Our Strengths Benefits Business Model

Service Demand Quicker Leverage our Core. Launch New Solutions.

Business Models to establish an on-going revenue

Delivery capabilities in the "Gap"

Optimize the "Experience" g gstream.

Optimize the ExperienceHarvest HNA. Create "Network“.

Target INSIDE and OUTSIDE base.

Target Niches.Harvest Clinical Experience. Enhanced Collaboration.

Promotes Agility.“Light”

RelationshipsReduce TCO.Ability to Scale Perform. Extend Demand.

27© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

pAbility to Scale Perform. Extend Demand.Simplified Installs, Usage, and Upgrades.

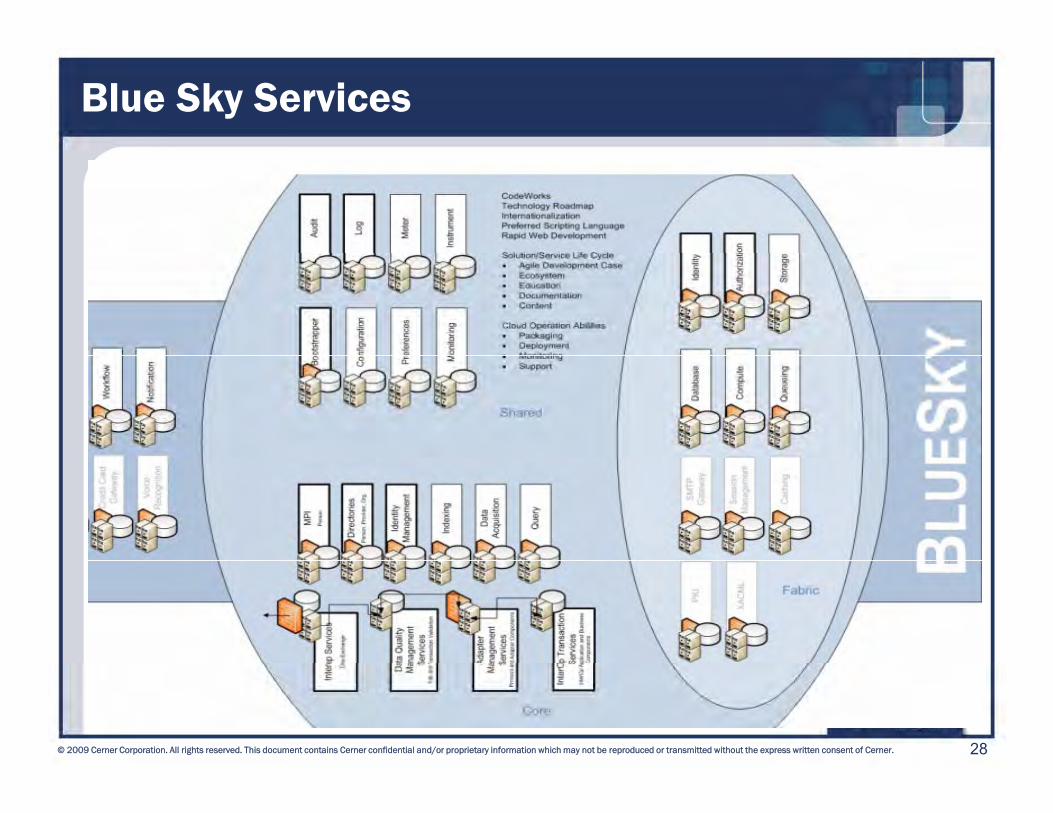

Blue Sky Services

28© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

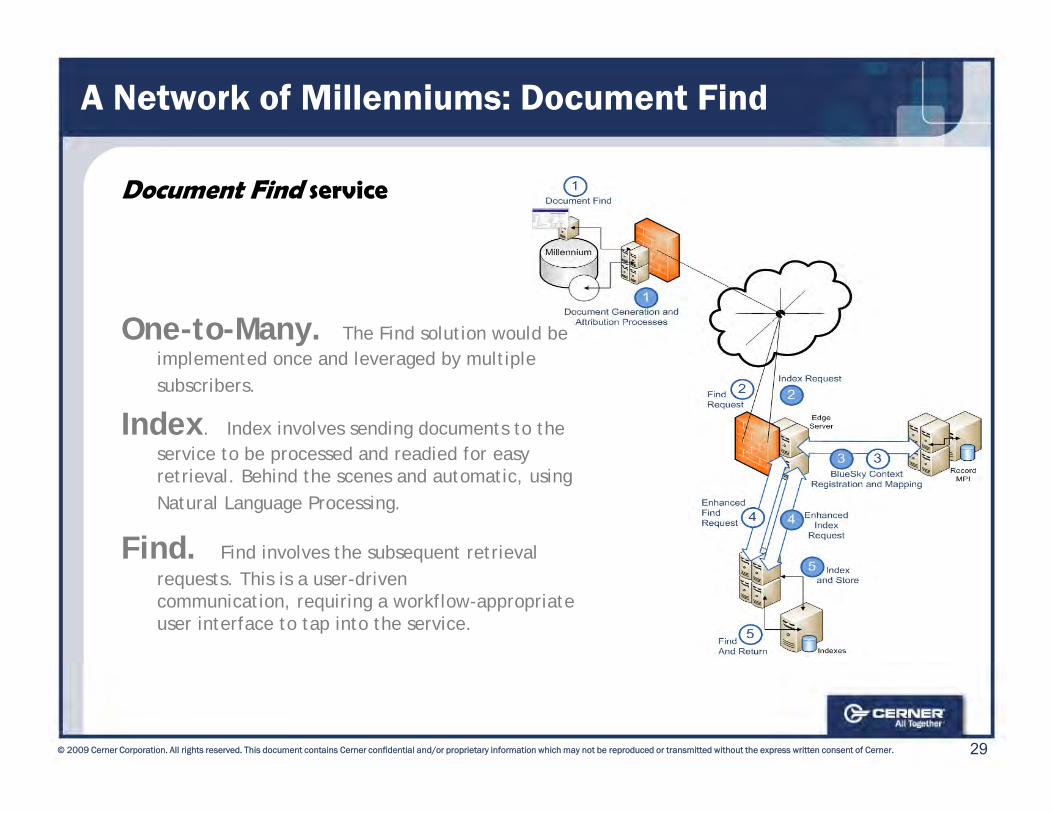

A Network of Millenniums: Document Find

Document Find service

One-to-Many. The Find solution would be implemented once and leveraged by multipleimplemented once and leveraged by multiplesubscribers.

Index. Index involves sending documents to the service to be processed and readied for easy service to be processed and readied for easy retrieval. Behind the scenes and automatic, usingNatural Language Processing.

Find. Find involves the subsequent retrieval qrequests. This is a user-driven communication, requiring a workflow-appropriate user interface to tap into the service.

29© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

A Network of Millenniums: Health Record

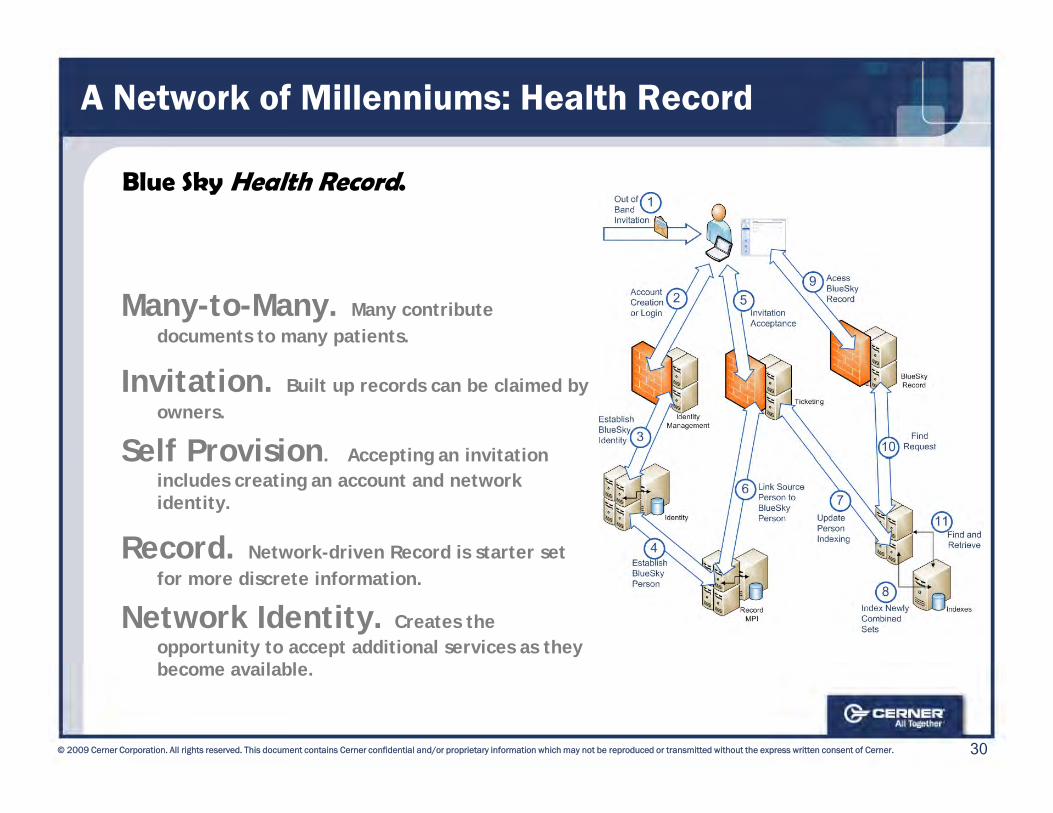

Blue Sky Health Record.

Many-to-Many. Many contribute documents to many patients.

Invitation. Built up records can be claimed by owners.

Self Provision Accepting an invitation Self Provision. Accepting an invitation includes creating an account and network identity.

Record. Network-driven Record is starter set for more discrete information.

Network Identity. Creates the opportunity to accept additional services as they b il bl

30© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

become available.

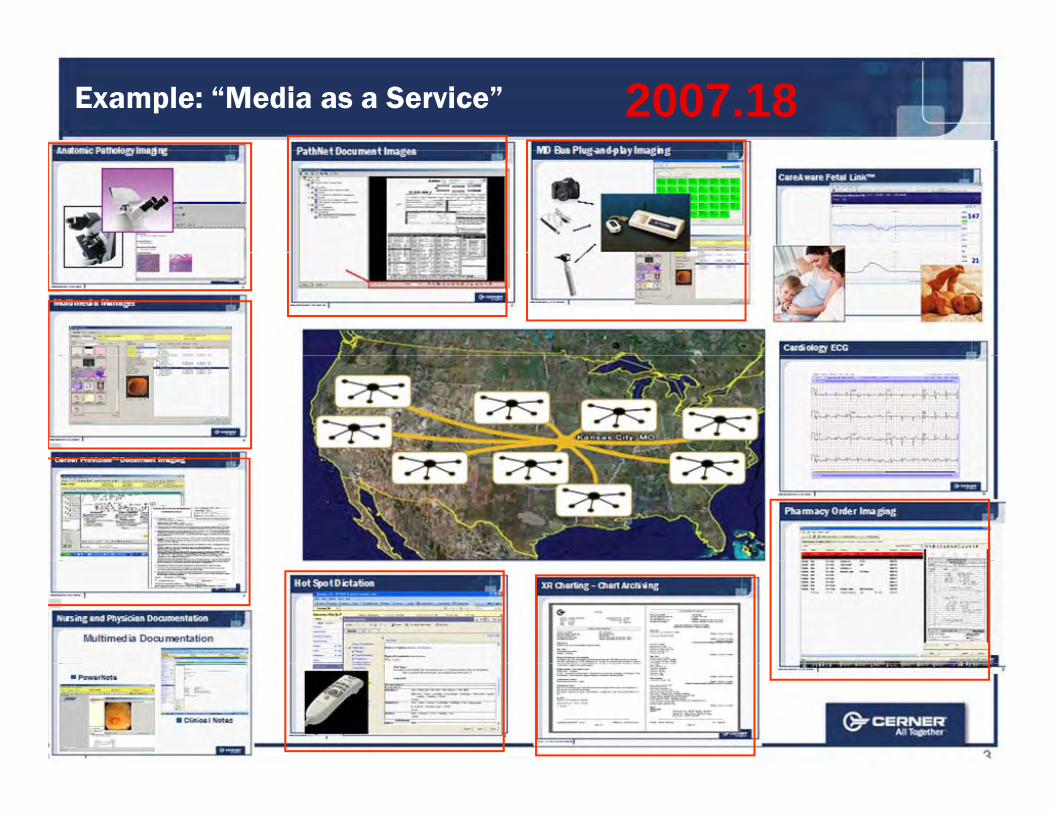

Example: “Media as a Service” 2007.18

31© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Healthcare Policy and Healthe Government

Amanda AdkinsDirector, Healthe Government,

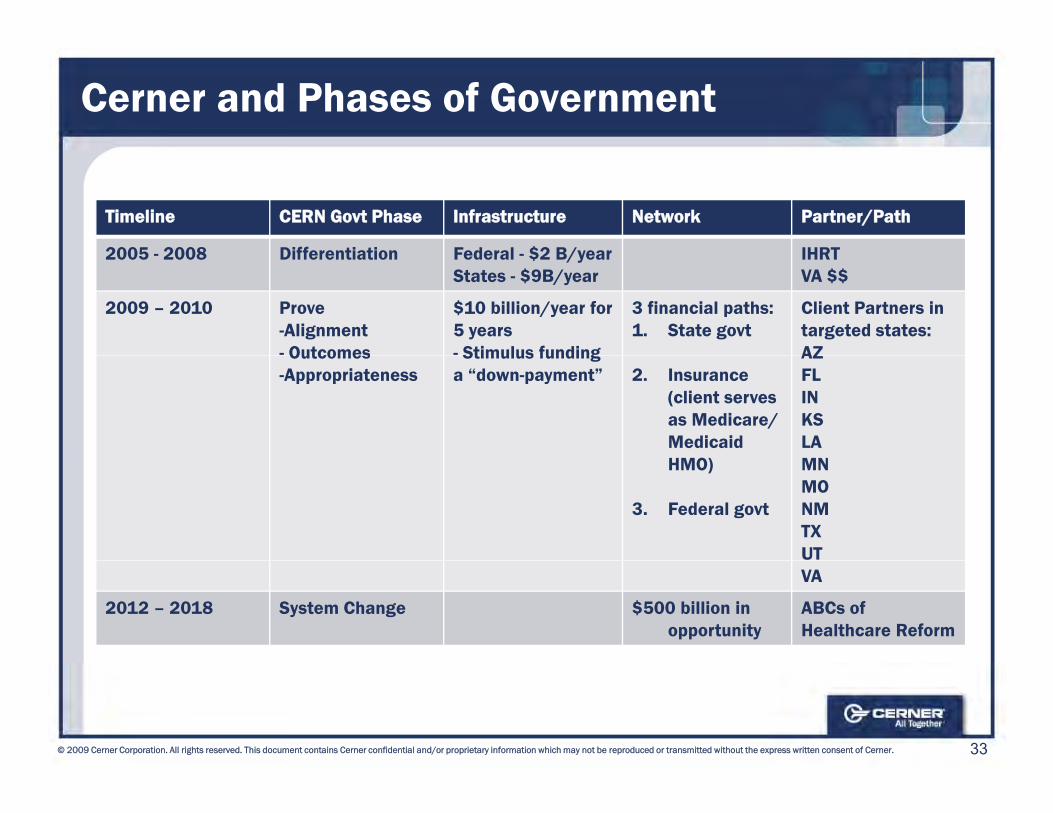

Cerner and Phases of Government

Timeline CERN Govt Phase Infrastructure Network Partner/Path

2005 2008 Differentiation Federal $2 B/year IHRT 2005 - 2008 Differentiation Federal - $2 B/yearStates - $9B/year

IHRT VA $$

2009 – 2010 Prove-Alignment- Outcomes

$10 billion/year for 5 years- Stimulus funding

3 financial paths:1. State govt

Client Partners in targeted states:AZOutcomes

-AppropriatenessStimulus funding

a “down-payment” 2. Insurance (client serves as Medicare/ Medicaid HMO)

AZFLINKSLAMNHMO)

3. Federal govt

MNMONMTXUTVA

2012 – 2018 System Change $500 billion in opportunity

ABCs of Healthcare Reform

33© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

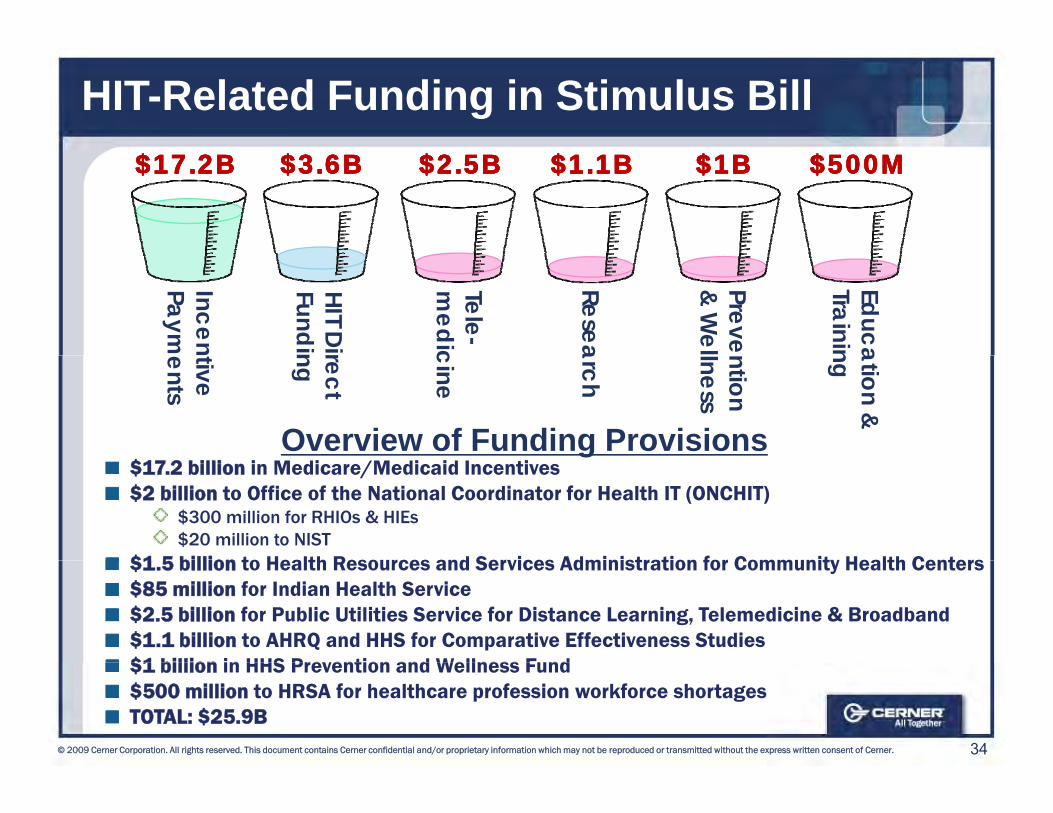

HIT-Related Funding in Stimulus Bill$17.2B$17.2B $3.6B$3.6B $2.5B$2.5B $1.1B$1.1B $500M$500M$1B$1B

IncenPaym

HIT DirFundin

Tele-m

edic

Resea

EducaTrainin

Preve& W

eltive ents

rect ng

cine

arch

ation & ngntion lness

Overview of Funding Provisions$17.2 billion in Medicare/Medicaid Incentives$2 billion to Office of the National Coordinator for Health IT (ONCHIT)

$300 million for RHIOs & HIEs$20 million to NIST

$1 5 billion to Health Resources and Services Administration for Community Health Centers$1.5 billion to Health Resources and Services Administration for Community Health Centers$85 million for Indian Health Service$2.5 billion for Public Utilities Service for Distance Learning, Telemedicine & Broadband$1.1 billion to AHRQ and HHS for Comparative Effectiveness Studies$1 billion in HHS Prevention and Wellness Fund

34© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

$1 billion in HHS Prevention and Wellness Fund$500 million to HRSA for healthcare profession workforce shortagesTOTAL: $25.9B

Cerner is Well Positioned

Requirements unknown, will be made known through regulatory process, but we feel we’re well positioned…

Certifications2007 CCHIT Certifications

Inpatient & Ambulatory

2008 CCHIT Certifications (planned)Emergency & Ambulatory

Staying in front of the regulatory process

Quality ReportingQ y p gLighthouse, PowerInsight

CMS-Certified PQRI Data Registry

SurveillanceSurveillanceLights On to aid in measuring compliance of use

Information Exchange

35© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Clinical Hub, Cerner Interchange and the Healthe Record

ABCs of Healthcare Reform: NY High Tech High Touch Health Home

Family History

High Tech, High TouchHealth Home

CC oordinate New York spends 75% of its $46 Billion Medicaid Budget on the Chronically ill.

Dx“SOAP”

My MedicalHistory

Eliminate: Variance,Error. Waste

MissingPerson, Medical Home,PHR, Funder, Compliance,N t iti A ti it

EE volve Partnership between Whitney M. Young Health Center (FQHC) and Cerner Corporation.

Rx OxEMR

Aligned Incentives

Trusted Agent

BB enefit

DDNutrition, Activity

Targeting 250 Chronically Ill Patients in Albany, New York.

Enrollees with receive a ll h i ti

isrupt

eClinicalworksHIXNY (RHIO)

cell phone as an incentive as well as to receive text reminders and other high touch interventions.

Any achieved savings will

Monthly Care Coordination Fee $272PMPM

AA utomate FF unding

Any achieved savings will be split between the State and the suppliers.

36© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

y $FFS through Whitney M.YoungShared Savings for Financial Outcomes$6M for Quality/Financial Incentives

CIO Panel

Catherine Claiter

Bill Spooner

Chairman’s Comments

Neal PattersonChairman, Chief Executive Officer ,and Co-Founder

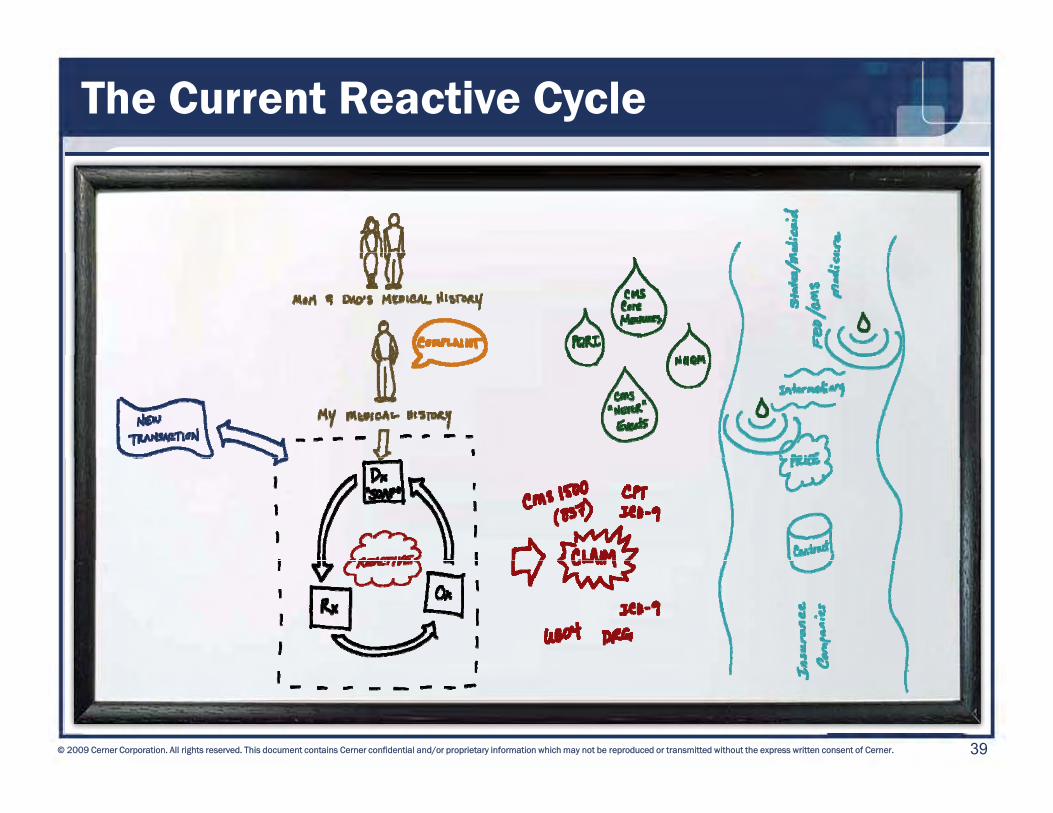

The Current Reactive Cycle

39© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

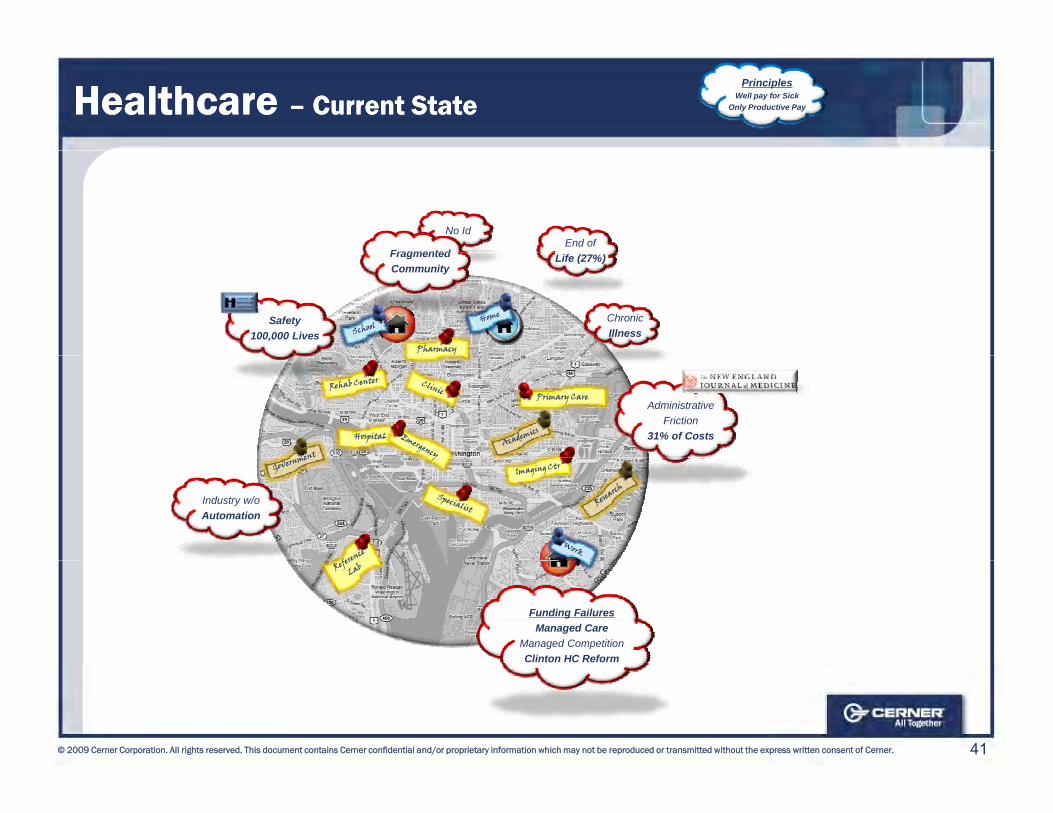

Healthcare Healthcare –– Current StateCurrent StatePrinciples

Well pay for SickOnly Productive Pay

PharmacyPharmacy

HospitalHospital

Primary CarePrimary Care

y

40© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Healthcare Healthcare –– Current StateCurrent StatePrinciples

Well pay for SickOnly Productive Pay

End ofNo Id

Fragmented

PharmacyPharmacy

Life (27%)

ChronicIllness

FragmentedCommunity

Safety100,000 Lives

HospitalHospital

Primary CarePrimary Care

y

AdministrativeFriction

31% of Costs

Industry w/oAutomation

Funding FailuresManaged Care

Managed CompetitionClinton HC Reform

41© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

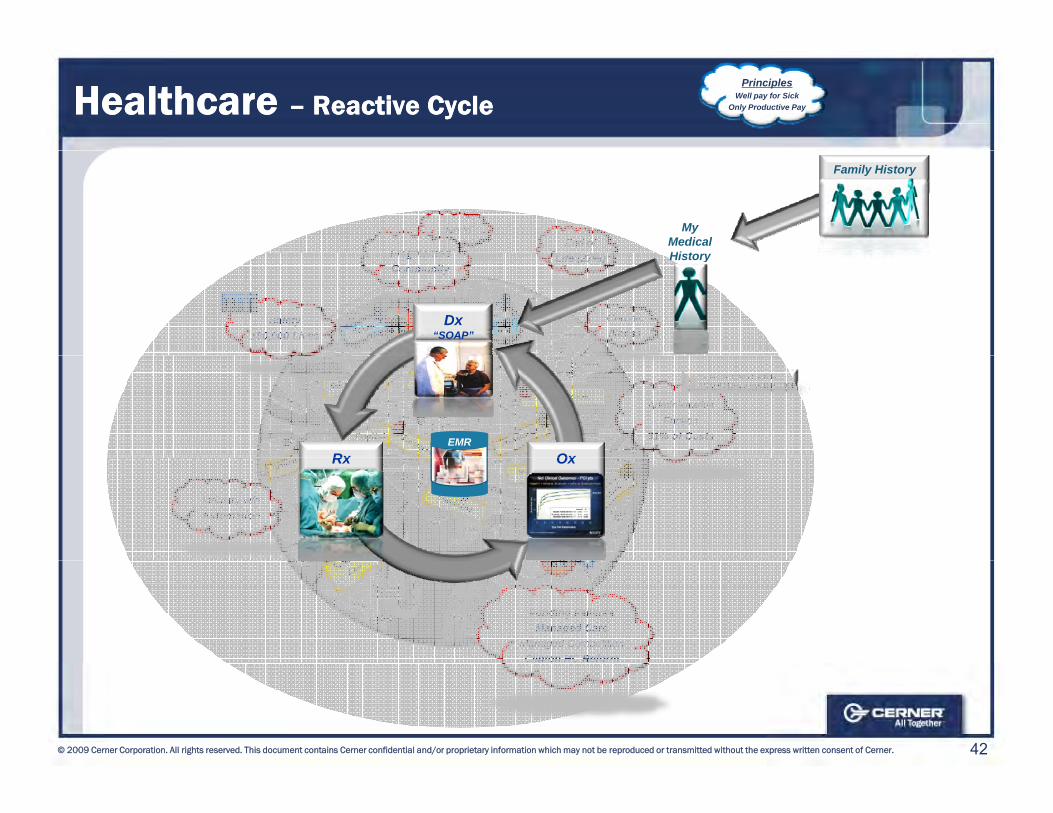

Healthcare Healthcare –– Reactive CycleReactive CyclePrinciples

Well pay for SickOnly Productive Pay

No IdEnd of

Fragmented

My MedicalHi t

Family History

PharmacyPharmacy

Safety100,000 Lives

Life (27%)

ChronicIllness

FragmentedCommunity

Dx“SOAP”

History

HospitalHospital

Primary CarePrimary Care

y

AdministrativeFriction

31% of Costs

Rx OxEMR

Industry w/oAutomation

Rx Ox

Funding FailuresManaged Care

Managed CompetitionClinton HC Reform

42© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

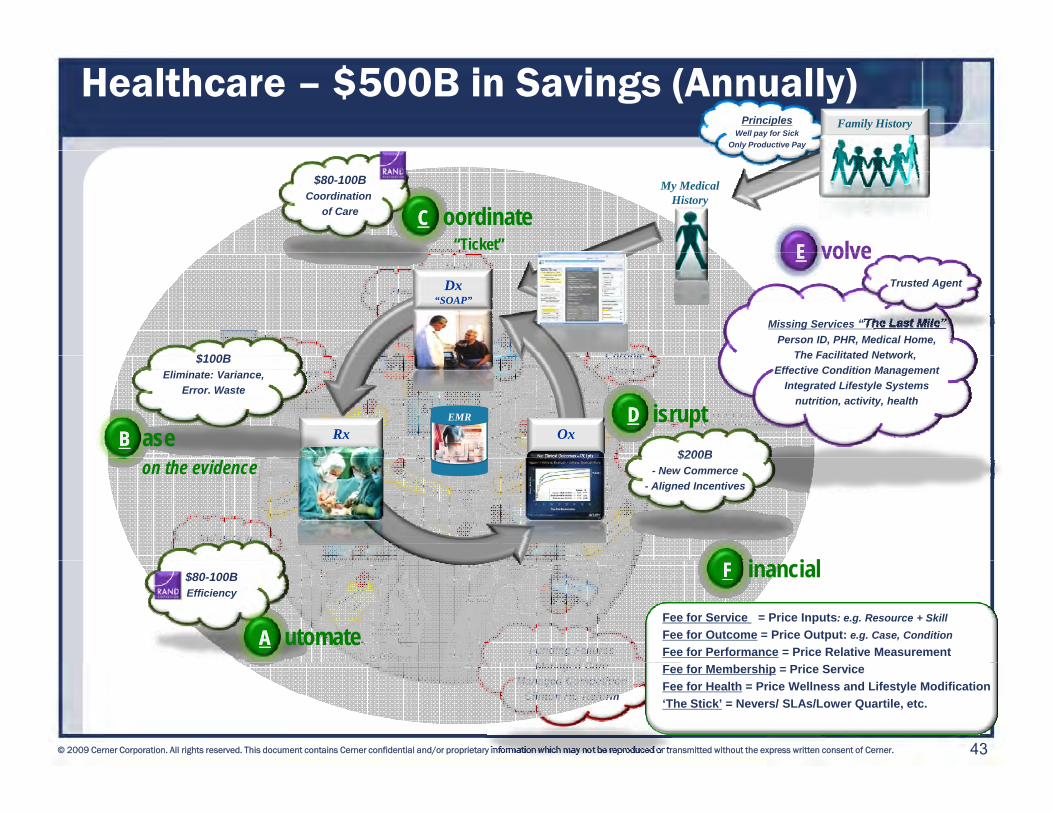

Healthcare – $500B in Savings (Annually)Principles

Well pay for SickOnly Productive Pay

Family History

My MedicalHistory

$80-100BCoordination

of Care CC oordinate“Ticket” EE volve

S f t

No IdEnd of

Life (27%)

Chronic

FragmentedCommunity

Dx“SOAP”

Missing Services “The Last Mile”Person ID, PHR, Medical Home,

The Facilitated Network$100B

Trusted Agent

EE volve

Primary CarePrimary Care

PharmacyPharmacy

Safety100,000 Lives

AdministrativeFriction

ChronicIllness

Rx OxEMR

The Facilitated Network, Effective Condition Management

Integrated Lifestyle Systemsnutrition, activity, health

$200B

$100BEliminate: Variance,

Error. Waste

BB aseDD isrupt

HospitalHospitalFriction

31% of Costs

Industry w/oAutomation

$200B- New Commerce

- Aligned Incentiveson the evidence

i i l

Funding FailuresM d C

Fee for Service = Price Inputs: e.g. Resource + SkillFee for Outcome = Price Output: e.g. Case, ConditionFee for Performance = Price Relative Measurement

$80-100BEfficiency

AA utomate

FF inancial

43© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Managed CareManaged Competition

Clinton HC Reform

Fee for Membership = Price ServiceFee for Health = Price Wellness and Lifestyle Modification ‘The Stick’ = Nevers/ SLAs/Lower Quartile, etc.

Chairman’s Comments

Neal PattersonChairman, Chief Executive Officer ,and Co-Founder

Questions

Q&A

Cerner Investment Community Meeting

February 24, 2009

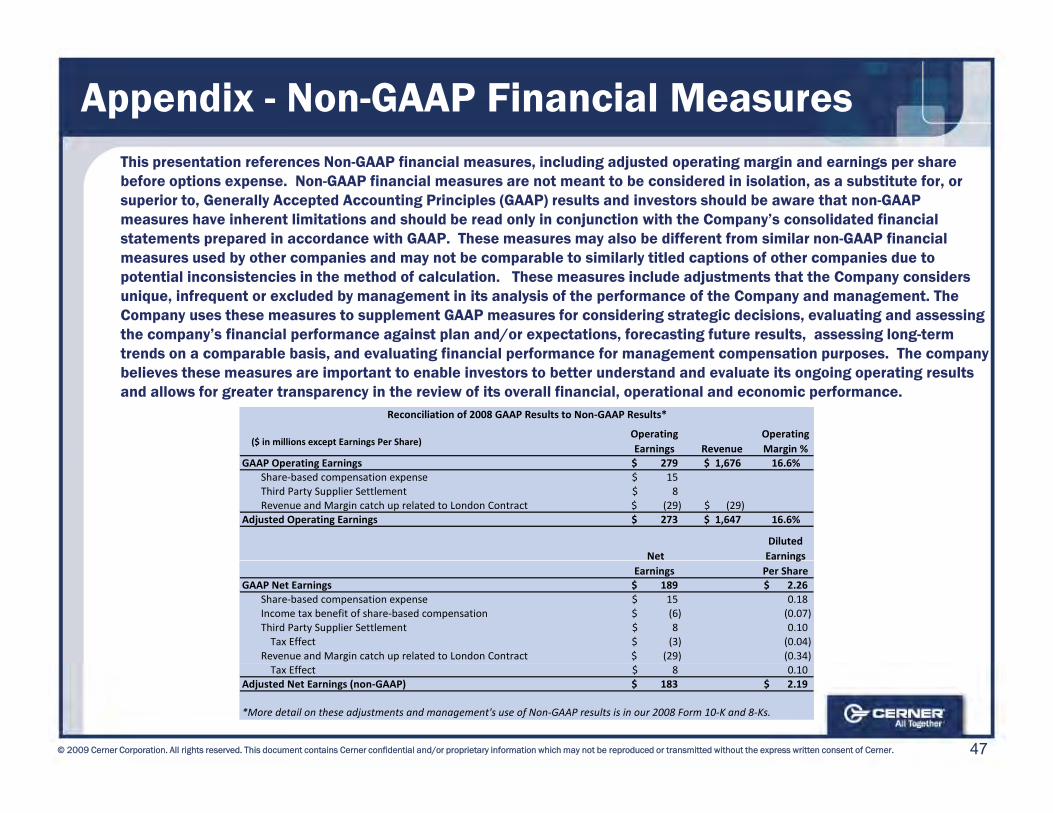

Appendix - Non-GAAP Financial MeasuresThis presentation references Non-GAAP financial measures, including adjusted operating margin and earnings per share before options expense. Non-GAAP financial measures are not meant to be considered in isolation, as a substitute for, or superior to, Generally Accepted Accounting Principles (GAAP) results and investors should be aware that non-GAAP measures have inherent limitations and should be read only in conjunction with the Company’s consolidated financial statements prepared in accordance with GAAP. These measures may also be different from similar non-GAAP financial

d b th i d t b bl t i il l titl d ti f th i d t measures used by other companies and may not be comparable to similarly titled captions of other companies due to potential inconsistencies in the method of calculation. These measures include adjustments that the Company considers unique, infrequent or excluded by management in its analysis of the performance of the Company and management. The Company uses these measures to supplement GAAP measures for considering strategic decisions, evaluating and assessing the company’s financial performance against plan and/or expectations, forecasting future results, assessing long-term trends on a comparable basis and evaluating financial performance for management compensation purposes The company trends on a comparable basis, and evaluating financial performance for management compensation purposes. The company believes these measures are important to enable investors to better understand and evaluate its ongoing operating results and allows for greater transparency in the review of its overall financial, operational and economic performance.

($ in millions except Earnings Per Share)Operating Earnings Revenue

Operating Margin %

Reconciliation of 2008 GAAP Results to Non‐GAAP Results*

GAAP Operating Earnings 279$ 1,676$ 16.6%Share‐based compensation expense 15$ Third Party Supplier Settlement 8$ Revenue and Margin catch up related to London Contract (29)$ (29)$

Adjusted Operating Earnings 273$ 1,647$ 16.6%

Net Diluted Earnings

Earnings g

Per ShareGAAP Net Earnings 189$ 2.26$

Share‐based compensation expense 15$ 0.18 Income tax benefit of share‐based compensation (6)$ (0.07) Third Party Supplier Settlement 8$ 0.10 Tax Effect (3)$ (0.04)

Revenue and Margin catch up related to London Contract (29)$ (0.34)

47© 2009 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner.

Tax Effect 8$ 0.10 Adjusted Net Earnings (non‐GAAP) 183$ 2.19$

*More detail on these adjustments and management's use of Non‐GAAP results is in our 2008 Form 10‐K and 8‐Ks.