Embed Size (px)

Citation preview

Investment Community Meeting HIMSS Orlando

Marc Naughton Executive Vice President and Chief Financial Officer

February 25, 2014 Health care is too important to stay the same.TM

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 2

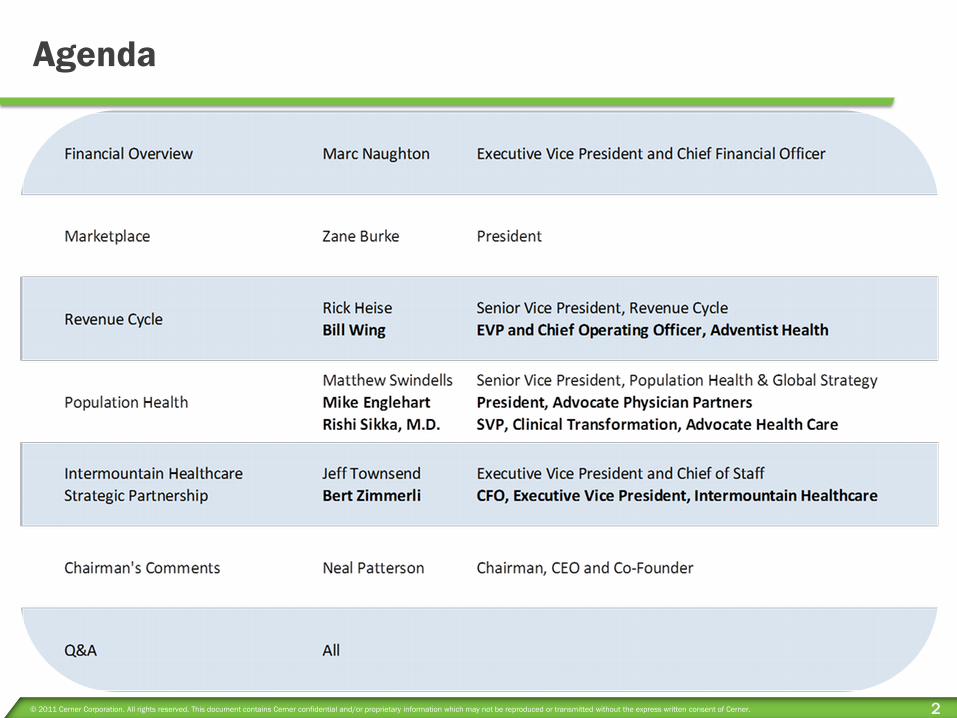

Agenda

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 3

Safe Harbor Statement

This presentation may contain forward-looking statements that involve a number of risks and

uncertainties. It is important to note that the Company’s performance, and actual results, financial

condition or business could differ materially from those expressed in such forward-looking

statements. Factors that could cause or contribute to such differences include, but are not limited to: (a) the possibility of product-related liabilities; (b) potential claims for system errors and warranties; (c) the possibility of interruption at

our data centers or client support facilities; (d) our proprietary technology may be subject to claims for infringement or misappropriation

of intellectual property rights of others, or may be infringed or misappropriated by others; (e) risks associated with our non-U.S.

operations; (f) risks associated with our ability to effectively hedge exposure to fluctuations in foreign currency exchange rates; (g) the

potential for tax legislation initiatives that could adversely affect our tax position and/or challenges to our tax positions in the United

States and non-U.S. countries; (h) risks associated with our recruitment and retention of key personnel; (i) risks related to our

dependence on third party suppliers; (j) risks inherent with business acquisitions; (k) the potential for losses resulting from asset

impairment charges; (l) risks associated with uncertainty in global economic conditions; (m) changing political, economic, regulatory and

judicial influences; (n) government regulation; (o) significant competition and market changes; (p) variations in our quarterly operating

results; (q) potential inconsistencies in our sales forecasts compared to actual sales; (r) the volatility in the trading price of our common

stock and the timing and volume of market activity; (s) our directors’ authority to issue preferred stock and the anti-takeover provisions in

our corporate governance documents; and (t) material adverse resolution of legal proceedings.

Additional discussion of these and other risks, uncertainties and factors affecting the Company's

business is contained in the Company's periodic filings with the Securities and Exchange

Commission. The reader should not place undue reliance on forward-looking statements, since the

statements speak only as of the date that they are made. The Company undertakes no obligation to

update forward-looking statements to reflect changed assumptions, the occurrence of unanticipated

events or changes in future operating results, financial condition or business over time. A

reconciliation of non-GAAP financial measures discussed in this presentation can be found in the

Appendix to this presentation and the Company’s most recent earnings release that was furnished to

the SEC and posted on the investor section of Cerner.com.

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 4

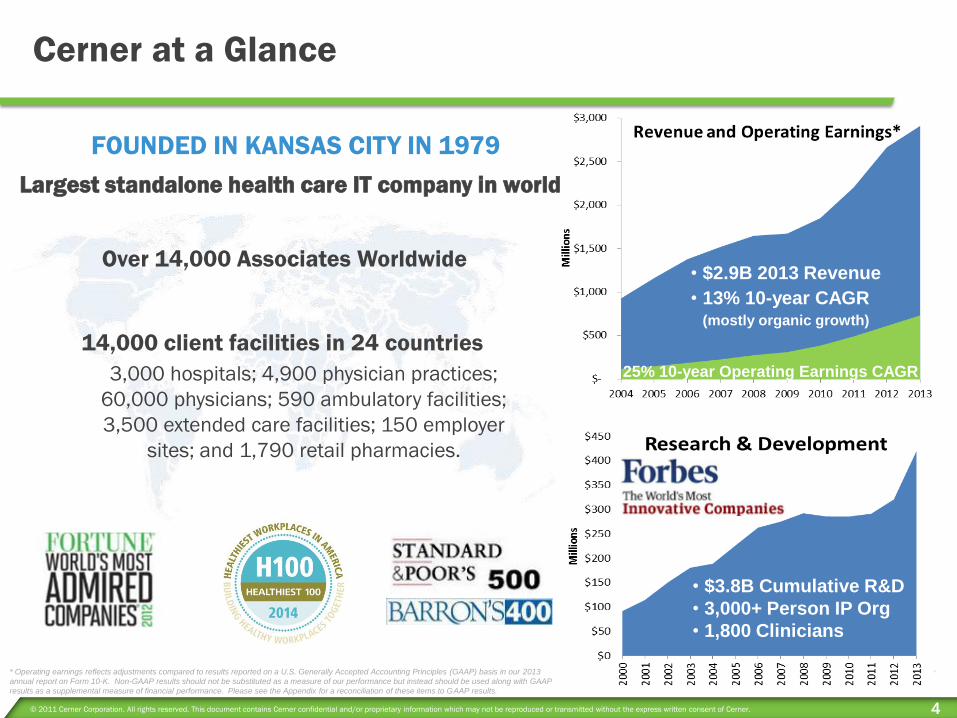

Cerner at a Glance

Over 14,000 Associates Worldwide

* Operating earnings reflects adjustments compared to results reported on a U.S. Generally Accepted Accounting Principles (GAAP) basis in our 2013

annual report on Form 10-K. Non-GAAP results should not be substituted as a measure of our performance but instead should be used along with GAAP

results as a supplemental measure of financial performance. Please see the Appendix for a reconciliation of these items to GAAP results.

• $3.8B Cumulative R&D

• 3,000+ Person IP Org

• 1,800 Clinicians

25% 10-year Operating Earnings CAGR

• $2.9B 2013 Revenue

• 13% 10-year CAGR (mostly organic growth)

14,000 client facilities in 24 countries

3,000 hospitals; 4,900 physician practices;

60,000 physicians; 590 ambulatory facilities;

3,500 extended care facilities; 150 employer

sites; and 1,790 retail pharmacies.

Largest standalone health care IT company in world

FOUNDED IN KANSAS CITY IN 1979

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 5

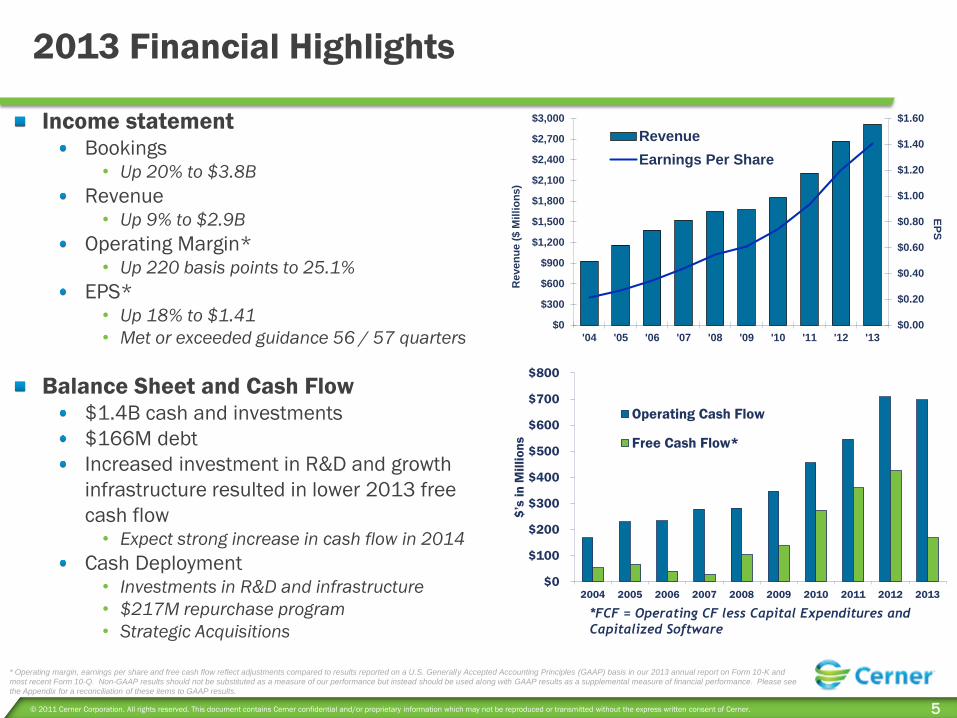

2013 Financial Highlights

Income statement Bookings • Up 20% to $3.8B

Revenue • Up 9% to $2.9B

Operating Margin* • Up 220 basis points to 25.1%

EPS* • Up 18% to $1.41

• Met or exceeded guidance 56 / 57 quarters

Balance Sheet and Cash Flow $1.4B cash and investments

$166M debt

Increased investment in R&D and growth

infrastructure resulted in lower 2013 free

cash flow • Expect strong increase in cash flow in 2014

Cash Deployment • Investments in R&D and infrastructure

• $217M repurchase program

• Strategic Acquisitions

$0

$100

$200

$300

$400

$500

$600

$700

$800

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$’s

in

Mil

lio

ns

Operating Cash Flow

Free Cash Flow*

*FCF = Operating CF less Capital Expenditures and

Capitalized Software

* Operating margin, earnings per share and free cash flow reflect adjustments compared to results reported on a U.S. Generally Accepted Accounting Principles (GAAP) basis in our 2013 annual report on Form 10-K and

most recent Form 10-Q. Non-GAAP results should not be substituted as a measure of our performance but instead should be used along with GAAP results as a supplemental measure of financial performance. Please see

the Appendix for a reconciliation of these items to GAAP results.

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$0

$300

$600

$900

$1,200

$1,500

$1,800

$2,100

$2,400

$2,700

$3,000

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13

EP

S

Reven

ue

($ M

illi

on

s)

Revenue

Earnings Per Share

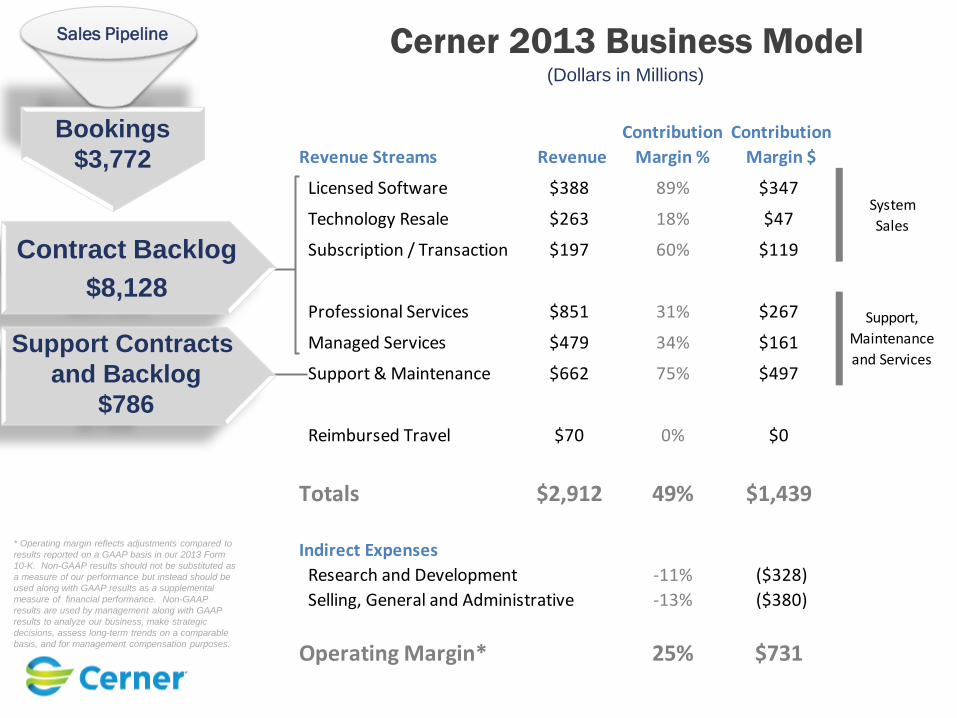

Bookings

$3,772

Cerner 2013 Business Model Sales Pipeline

Contract Backlog

$8,128

Support Contracts

and Backlog

$786

(Dollars in Millions)

* Operating margin reflects adjustments compared to

results reported on a GAAP basis in our 2013 Form

10-K. Non-GAAP results should not be substituted as

a measure of our performance but instead should be

used along with GAAP results as a supplemental

measure of financial performance. Non-GAAP

results are used by management along with GAAP

results to analyze our business, make strategic

decisions, assess long-term trends on a comparable

basis, and for management compensation purposes.

Revenue Streams Revenue

Contribution

Margin %

Contribution

Margin $

Licensed Software $388 89% $347

Technology Resale $263 18% $47

Subscription / Transaction $197 60% $119

Professional Services $851 31% $267

Managed Services $479 34% $161

Support & Maintenance $662 75% $497

Reimbursed Travel $70 0% $0

Totals $2,912 49% $1,439

Indirect Expenses

Research and Development -11% ($328)

Selling, General and Administrative -13% ($380)

Operating Margin* 25% $731

System

Sales

Support,

Maintenance

and Services

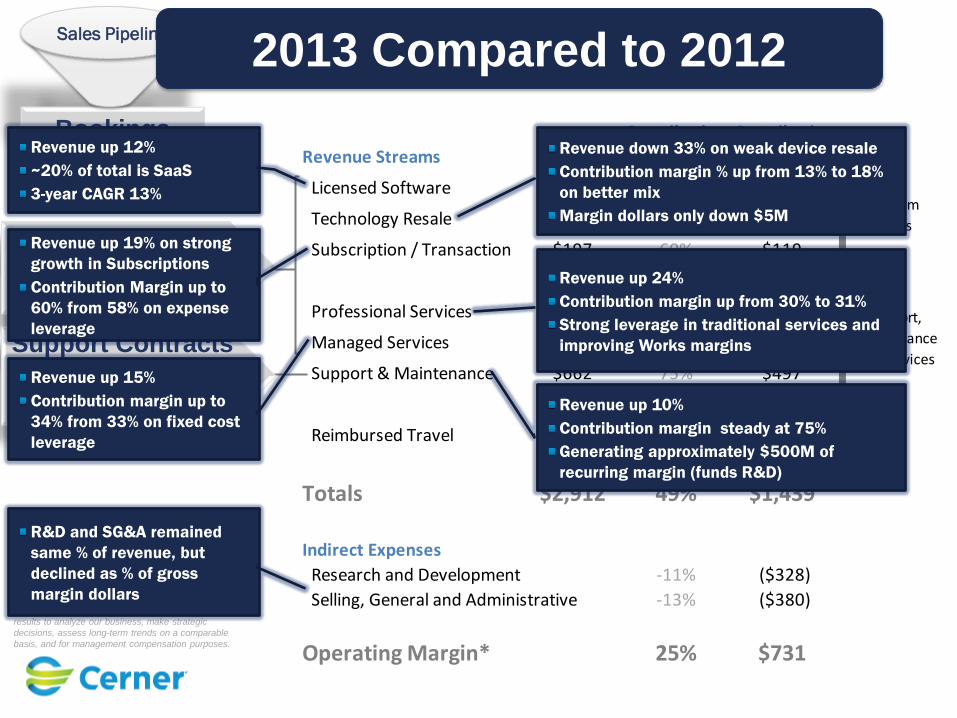

Cerner 2013 Business Model

Bookings

$3,772

Sales Pipeline

Contract Backlog

$8,128

Support Contracts

and Backlog

$786

(Dollars in Millions)

* Operating margin reflects adjustments compared to

results reported on a GAAP basis in our 2013 Form

10-K. Non-GAAP results should not be substituted as

a measure of our performance but instead should be

used along with GAAP results as a supplemental

measure of financial performance. Non-GAAP

results are used by management along with GAAP

results to analyze our business, make strategic

decisions, assess long-term trends on a comparable

basis, and for management compensation purposes.

Revenue Streams Revenue

Contribution

Margin %

Contribution

Margin $

Licensed Software $388 89% $347

Technology Resale $263 18% $47

Subscription / Transaction $197 60% $119

Professional Services $851 31% $267

Managed Services $479 34% $161

Support & Maintenance $662 75% $497

Reimbursed Travel $70 0% $0

Totals $2,912 49% $1,439

Indirect Expenses

Research and Development -11% ($328)

Selling, General and Administrative -13% ($380)

Operating Margin* 25% $731

System

Sales

Support,

Maintenance

and Services

Revenue up 12%

~20% of total is SaaS

3-year CAGR 13%

Revenue down 33% on weak device resale

Contribution margin % up from 13% to 18%

on better mix

Margin dollars only down $5M

Revenue up 19% on strong

growth in Subscriptions

Contribution Margin up to

60% from 58% on expense

leverage

Revenue up 15%

Contribution margin up to

34% from 33% on fixed cost

leverage

Revenue up 24%

Contribution margin up from 30% to 31%

Strong leverage in traditional services and

improving Works margins

Revenue up 10%

Contribution margin steady at 75%

Generating approximately $500M of

recurring margin (funds R&D)

2013 Compared to 2012

R&D and SG&A remained

same % of revenue, but

declined as % of gross

margin dollars

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 8

Increasing Visibility and Profitability

2013 Revenue Mix Summary

Recurring (47%): Managed Services, Support &

Maintenance, Subscriptions

Visible (30%): Professional Services

Non-Recurring (23%): Licensed Software, Technology

Resale

* Operating margin reflects adjustments compared to results reported on a GAAP basis in our 2013 Form 10-K. Non-GAAP results should not be substituted as a measure of our

performance but instead should be used along with GAAP results as a supplemental measure of financial performance. Non-GAAP results are used by management along with

GAAP results to analyze our business, make strategic decisions, assess long-term trends on a comparable basis, and for management compensation purposes.

Margin Growth and Visibility

Operating Margin 9% to 25% since 2003

Source of margin from 45% visible to 73%

Revenue Visibility Remains Strong

77% of Revenue Recurring or Visible

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 9

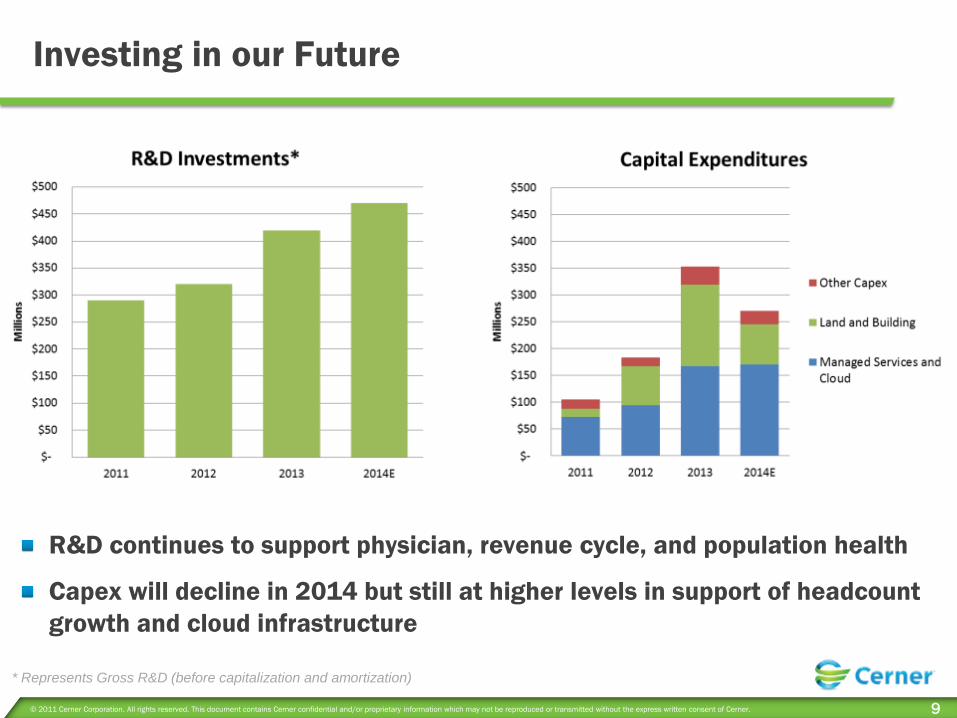

Investing in our Future

* Represents Gross R&D (before capitalization and amortization)

R&D continues to support physician, revenue cycle, and population health

Capex will decline in 2014 but still at higher levels in support of headcount

growth and cloud infrastructure

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 10

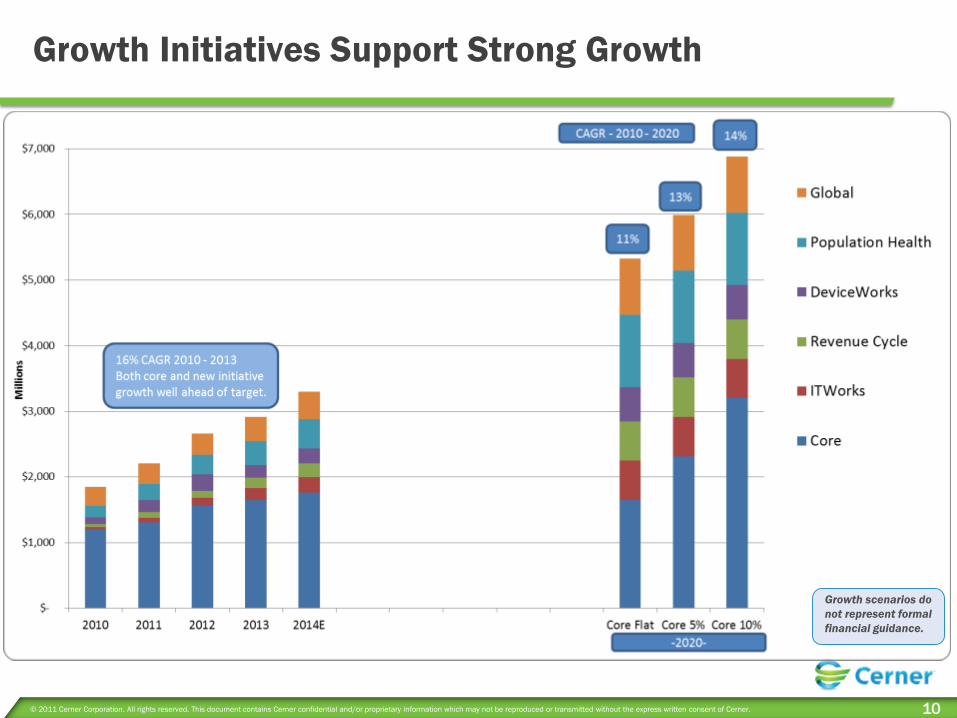

Growth Initiatives Support Strong Growth

Growth scenarios do

not represent formal

financial guidance.

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 11

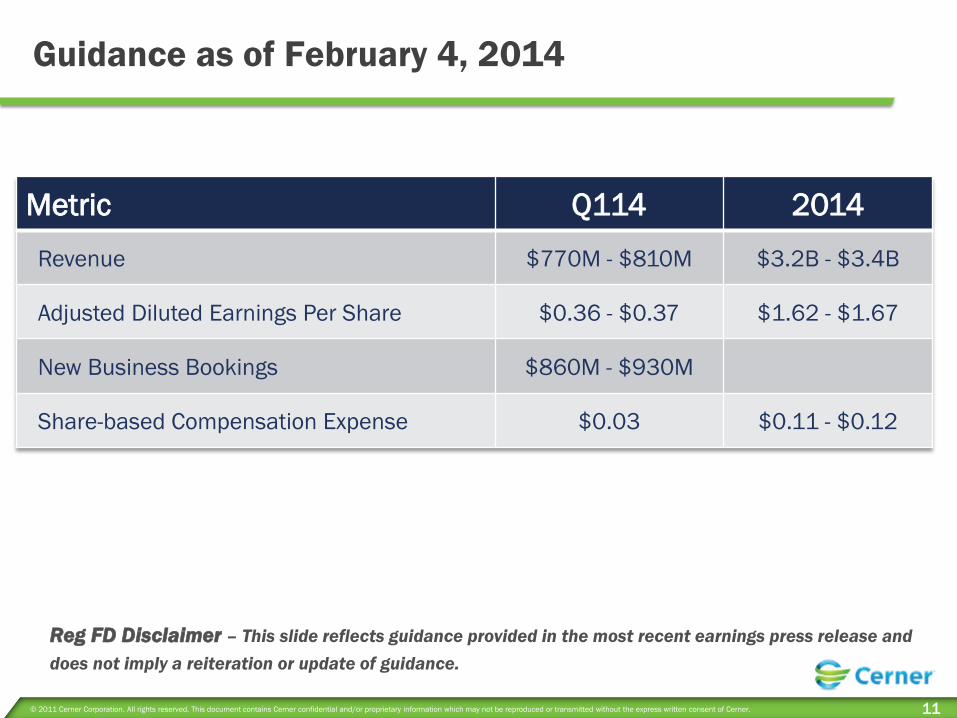

Guidance as of February 4, 2014

Reg FD Disclaimer – This slide reflects guidance provided in the most recent earnings press release and

does not imply a reiteration or update of guidance.

Metric Q114 2014

Revenue $770M - $810M $3.2B - $3.4B

Adjusted Diluted Earnings Per Share $0.36 - $0.37 $1.62 - $1.67

New Business Bookings $860M - $930M

Share-based Compensation Expense $0.03 $0.11 - $0.12

Marketplace

Zane Burke President

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 13

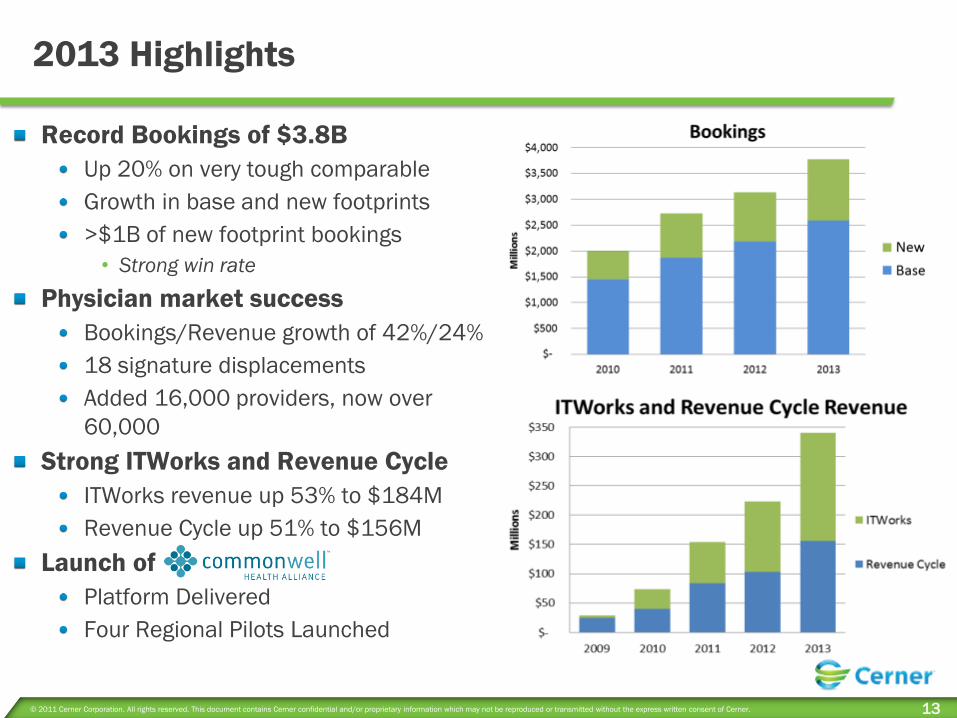

2013 Highlights

Record Bookings of $3.8B

Up 20% on very tough comparable

Growth in base and new footprints

>$1B of new footprint bookings

• Strong win rate

Physician market success

Bookings/Revenue growth of 42%/24%

18 signature displacements

Added 16,000 providers, now over

60,000

Strong ITWorks and Revenue Cycle

ITWorks revenue up 53% to $184M

Revenue Cycle up 51% to $156M

Launch of

Platform Delivered

Four Regional Pilots Launched

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 14

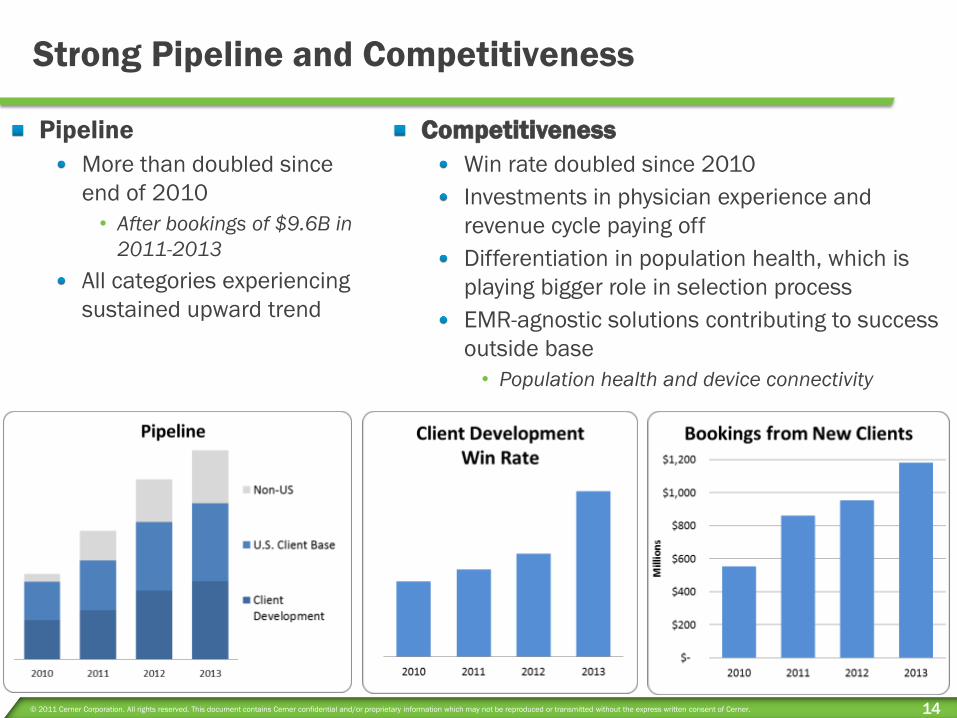

Strong Pipeline and Competitiveness

Pipeline

More than doubled since

end of 2010

• After bookings of $9.6B in

2011-2013

All categories experiencing

sustained upward trend

Competitiveness

Win rate doubled since 2010

Investments in physician experience and

revenue cycle paying off

Differentiation in population health, which is

playing bigger role in selection process

EMR-agnostic solutions contributing to success

outside base

• Population health and device connectivity

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 15

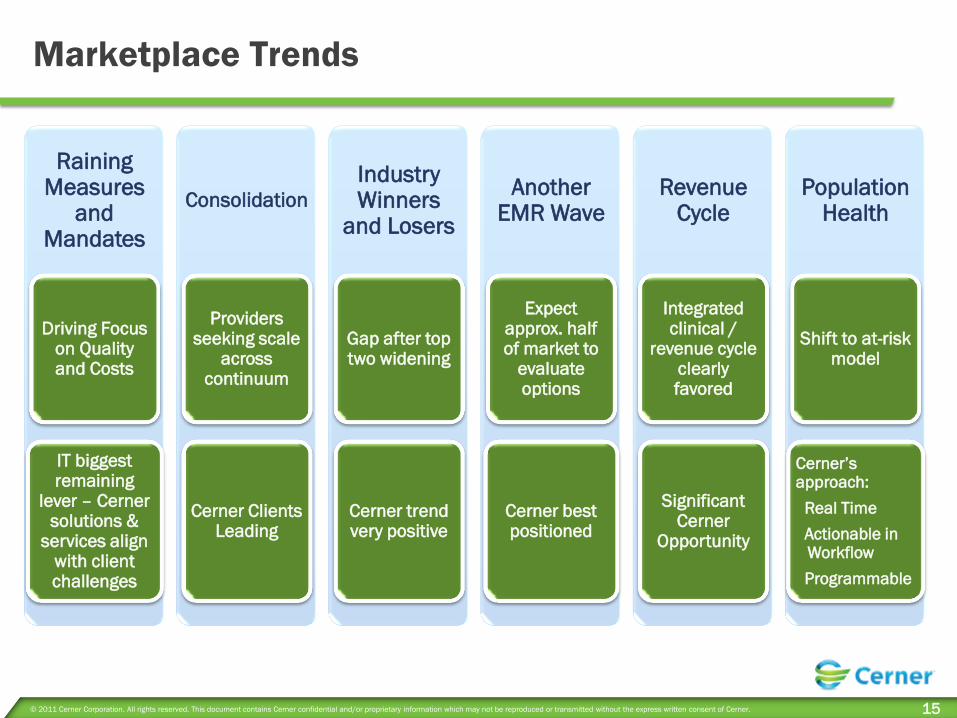

Marketplace Trends

Raining Measures

and Mandates

Driving Focus on Quality and Costs

IT biggest remaining

lever – Cerner solutions &

services align with client challenges

Consolidation

Providers seeking scale

across continuum

Cerner Clients Leading

Industry Winners

and Losers

Gap after top two widening

Cerner trend very positive

Another EMR Wave

Expect approx. half of market to

evaluate options

Cerner best positioned

Revenue Cycle

Integrated clinical /

revenue cycle clearly favored

Significant Cerner

Opportunity

Population Health

Shift to at-risk model

Cerner’s approach:

Real Time

Actionable in Workflow

Programmable

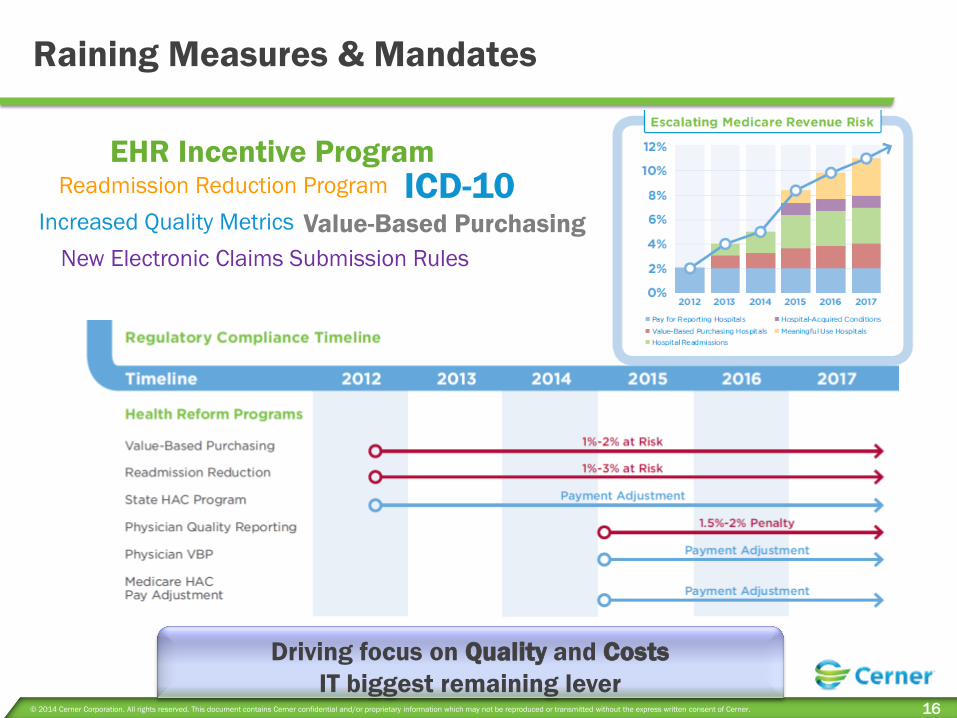

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 16

EHR Incentive Program

ICD-10 Value-Based Purchasing

Readmission Reduction Program

New Electronic Claims Submission Rules

Increased Quality Metrics

Raining Measures & Mandates

Driving focus on Quality and Costs

IT biggest remaining lever

© 2013 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 17

-30

-10

10

30

50

70

90

110

130128

26 23

12

2 6

116

24 18

-12 -13

-25

104

11

-7

Acq

uir

ed H

osp

ita

ls

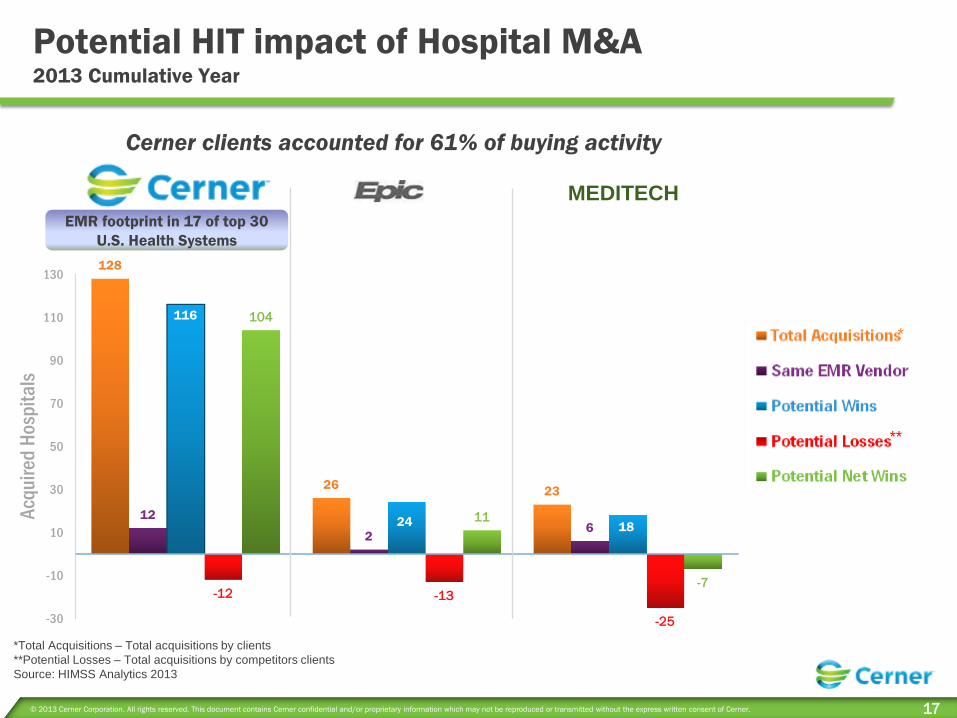

Potential HIT impact of Hospital M&A 2013 Cumulative Year

MEDITECH

Cerner clients accounted for 61% of buying activity

*Total Acquisitions – Total acquisitions by clients

**Potential Losses – Total acquisitions by competitors clients

Source: HIMSS Analytics 2013

**

*

EMR footprint in 17 of top 30

U.S. Health Systems

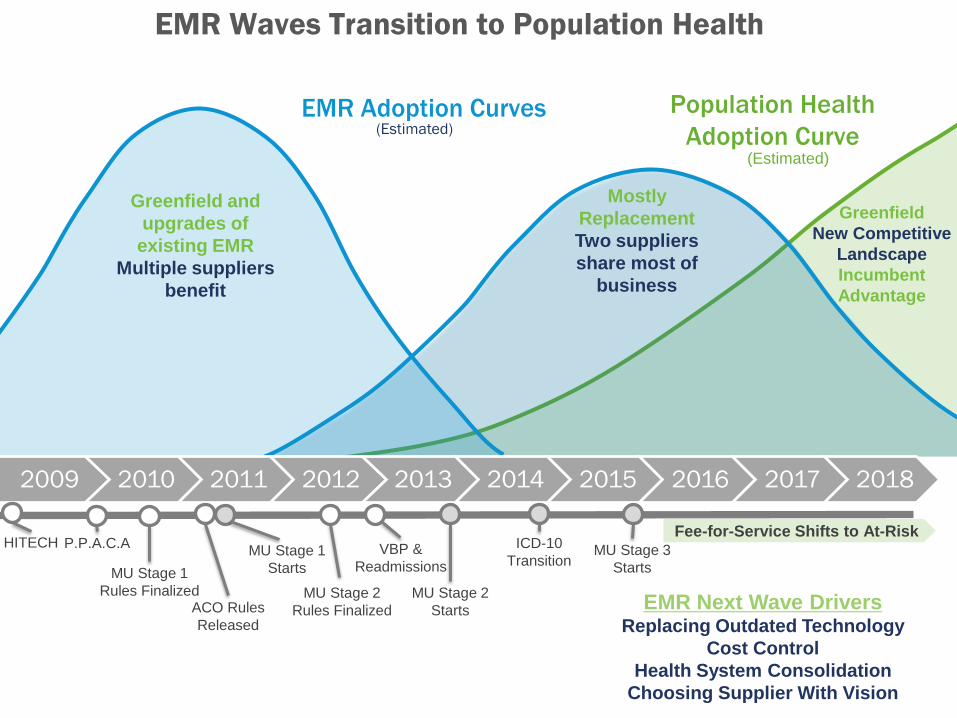

EMR Waves Transition to Population Health

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

HITECH MU Stage 1

Starts

VBP &

Readmissions

MU Stage 2

Starts

ICD-10

Transition MU Stage 3

Starts

P.P.A.C.A

MU Stage 1

Rules Finalized MU Stage 2

Rules Finalized ACO Rules

Released

Population Health

Adoption Curve (Estimated)

EMR Adoption Curves (Estimated)

EMR Next Wave Drivers Replacing Outdated Technology

Cost Control

Health System Consolidation

Choosing Supplier With Vision

Fee-for-Service Shifts to At-Risk

Mostly

Replacement

Two suppliers

share most of

business

Greenfield and

upgrades of

existing EMR

Multiple suppliers

benefit

Greenfield

New Competitive

Landscape

Incumbent

Advantage

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 19

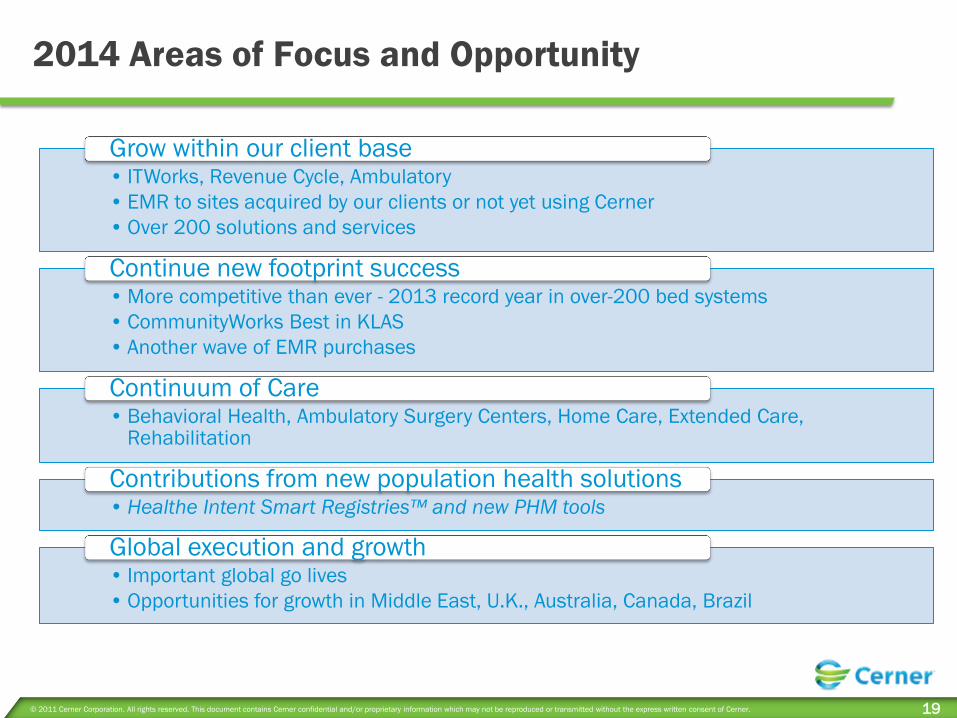

2014 Areas of Focus and Opportunity

• ITWorks, Revenue Cycle, Ambulatory

• EMR to sites acquired by our clients or not yet using Cerner

• Over 200 solutions and services

Grow within our client base

• More competitive than ever - 2013 record year in over-200 bed systems

• CommunityWorks Best in KLAS

• Another wave of EMR purchases

Continue new footprint success

• Behavioral Health, Ambulatory Surgery Centers, Home Care, Extended Care, Rehabilitation

Continuum of Care

• Healthe Intent Smart Registries™ and new PHM tools

Contributions from new population health solutions

• Important global go lives

• Opportunities for growth in Middle East, U.K., Australia, Canada, Brazil

Global execution and growth

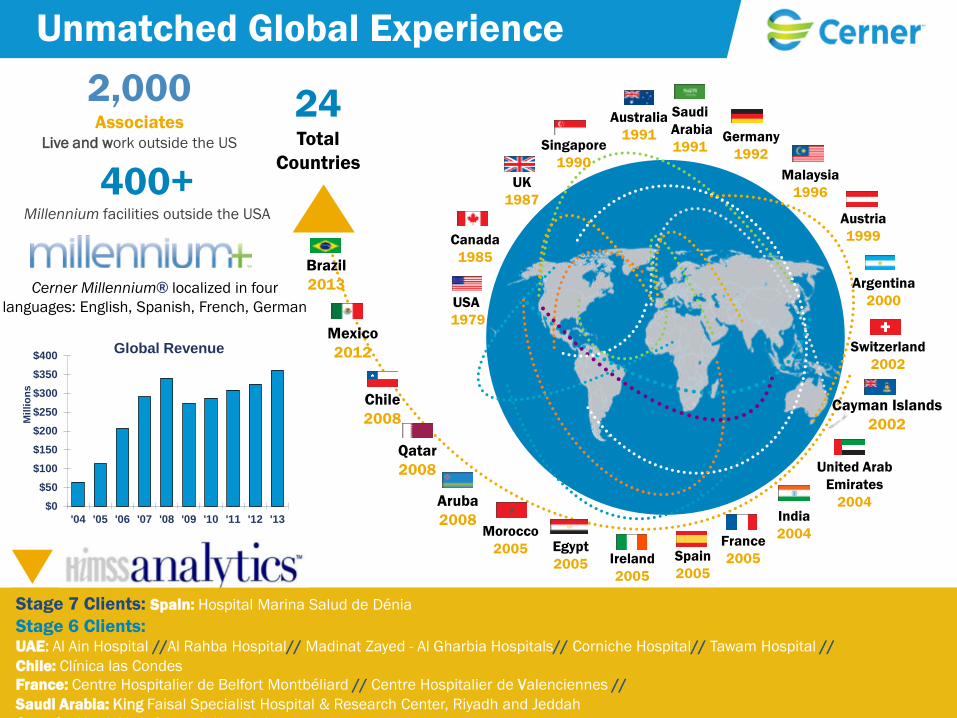

Cerner Millennium® localized in four

languages: English, Spanish, French, German

Stage 7 Clients: Spain: Hospital Marina Salud de Dénia

Stage 6 Clients: UAE: Al Ain Hospital //Al Rahba Hospital// Madinat Zayed - Al Gharbia Hospitals// Corniche Hospital// Tawam Hospital //

Chile: Clínica las Condes

France: Centre Hospitalier de Belfort Montbéliard // Centre Hospitalier de Valenciennes //

Saudi Arabia: King Faisal Specialist Hospital & Research Center, Riyadh and Jeddah

Canada: North York General Hospital

Malaysia: Prince Court Medical Centre

2,000 Associates

Live and work outside the US

400+ Millennium facilities outside the USA

USA

1979

Saudi

Arabia

1991 Germany

1992

Malaysia

1996

Australia

1991

Spain

2005 Ireland

2005

Egypt

2005

Chile

2008

Qatar

2008

France

2005

Canada

1985

24 Total

Countries

United Arab

Emirates

2004 India

2004

Argentina

2000

Austria

1999

Switzerland

2002

Cayman Islands

2002

Singapore

1990

UK

1987

Aruba

2008 Morocco

2005

Mexico

2012

Unmatched Global Experience

$0

$50

$100

$150

$200

$250

$300

$350

$400

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Mil

lio

ns

Global Revenue

Brazil

2013

Revenue Cycle

Rick Heise Senior Vice President, Revenue Cycle

Bill Wing Executive Vice President and Chief Operating Officer, Adventist Health

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 22

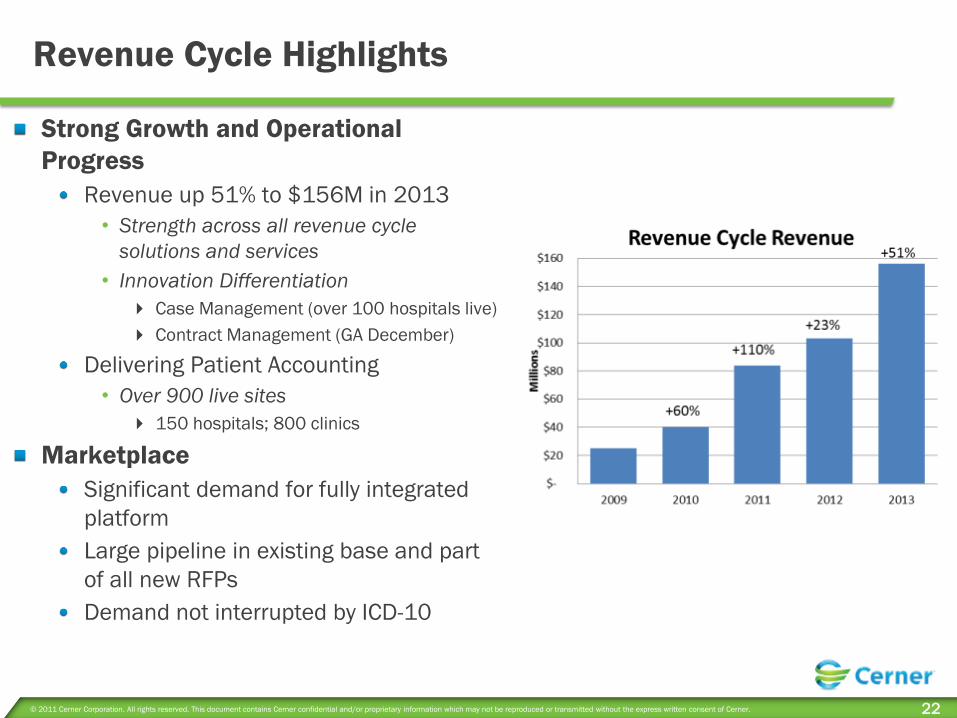

Revenue Cycle Highlights

Strong Growth and Operational

Progress

Revenue up 51% to $156M in 2013

• Strength across all revenue cycle

solutions and services

• Innovation Differentiation

Case Management (over 100 hospitals live)

Contract Management (GA December)

Delivering Patient Accounting

• Over 900 live sites

150 hospitals; 800 clinics

Marketplace

Significant demand for fully integrated

platform

Large pipeline in existing base and part

of all new RFPs

Demand not interrupted by ICD-10

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 23

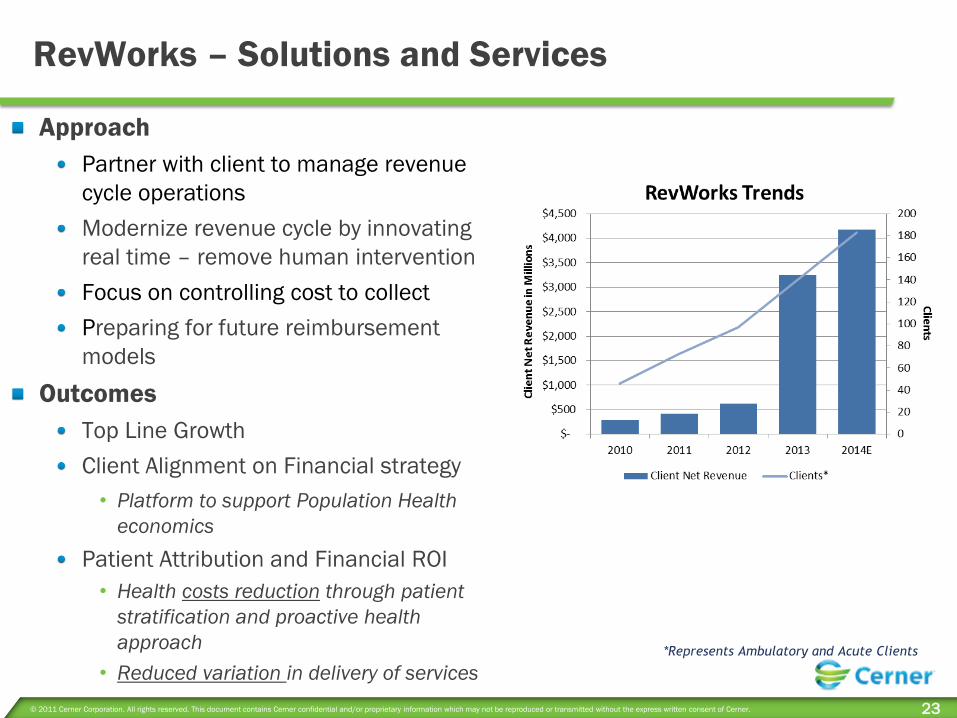

RevWorks – Solutions and Services

Approach

Partner with client to manage revenue

cycle operations

Modernize revenue cycle by innovating

real time – remove human intervention

Focus on controlling cost to collect

Preparing for future reimbursement

models

Outcomes

Top Line Growth

Client Alignment on Financial strategy

• Platform to support Population Health

economics

Patient Attribution and Financial ROI

• Health costs reduction through patient

stratification and proactive health

approach

• Reduced variation in delivery of services

*Represents Ambulatory and Acute Clients

Integrating to Win: The Power of Clinical and Financial Information

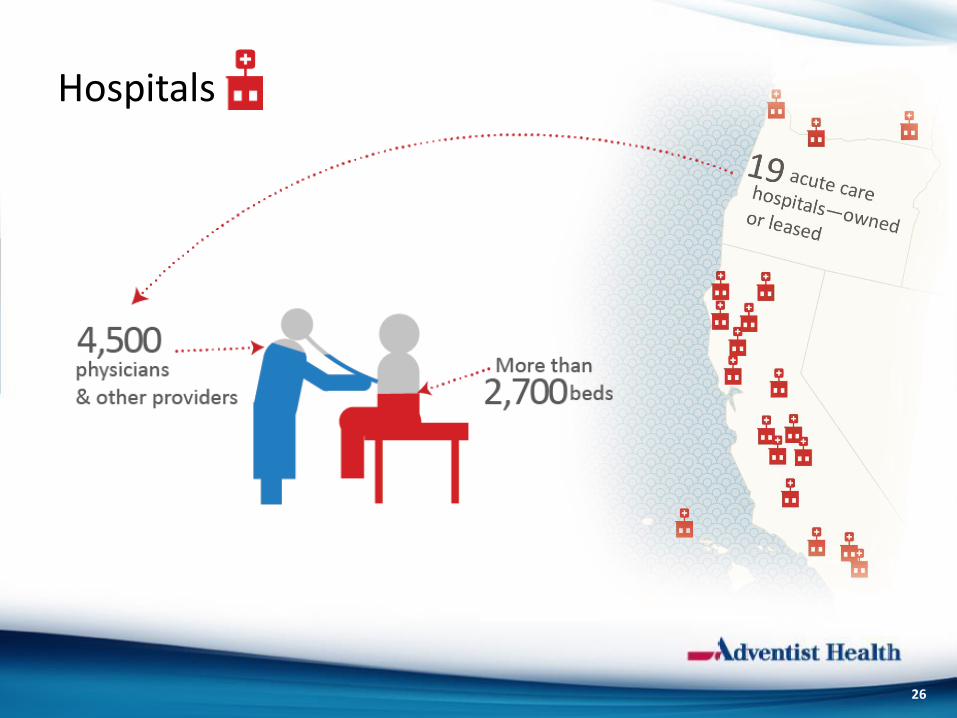

Who We Are

Hospitals

26

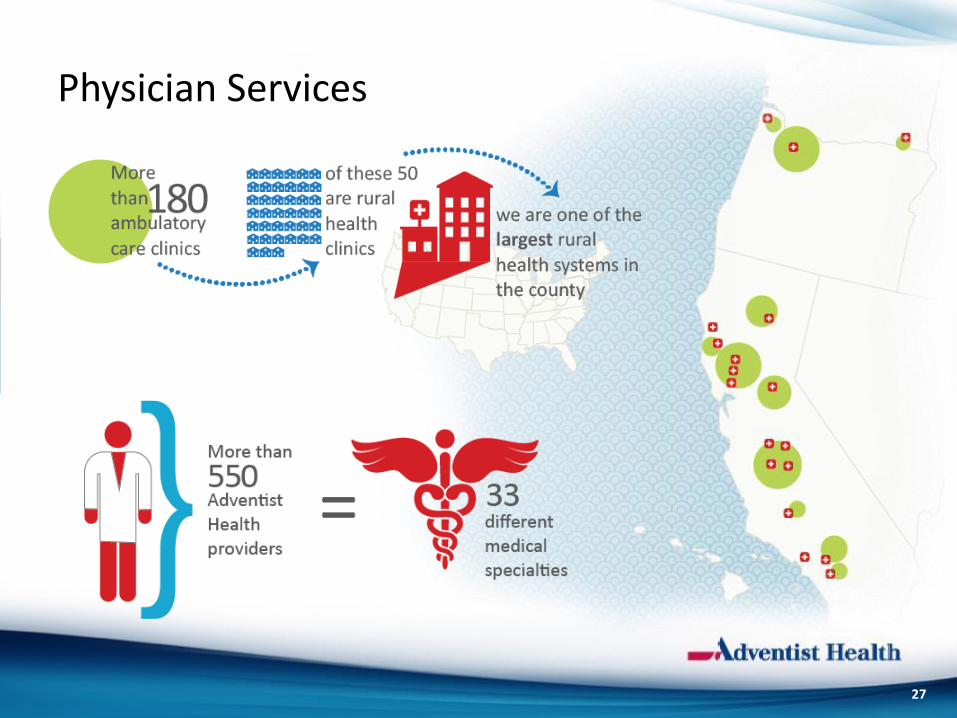

Physician Services

27

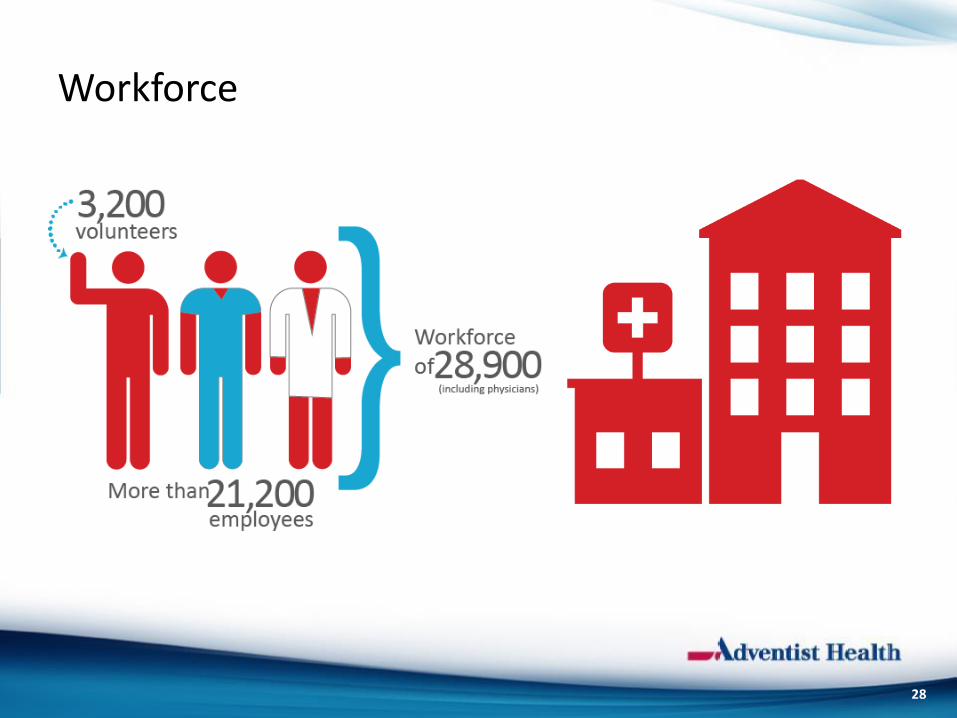

Workforce

28

Financials

Net Patient Revenue $2.7 billion

EBIDA $298.0 million

Net Income $133.1 million

Admissions 126,210

ED Visits 512,932

OP Visits 2,411,632

Rural Health Clinic Visits 817,900

Patient Days 569,530

Home Care Visits 227,662

Hospice Days 90,789

FYE 12/31/2012

29

Challenges Ahead

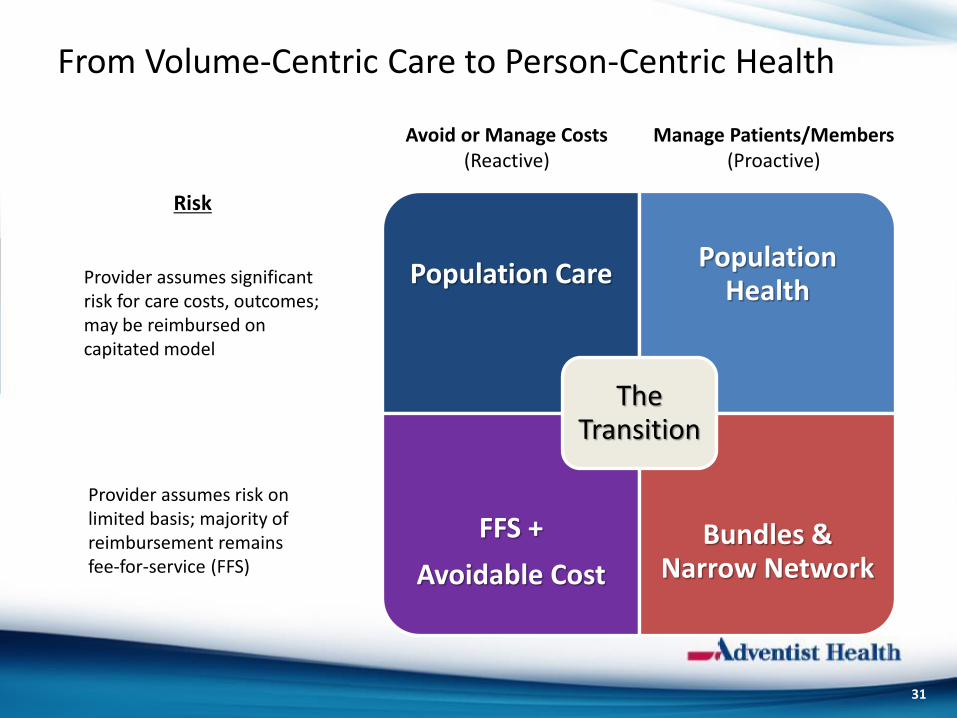

From Volume-Centric Care to Person-Centric Health

Population Care Population

Health

FFS +

Avoidable Cost

Bundles & Narrow Network

The Transition

Avoid or Manage Costs (Reactive)

Provider assumes risk on limited basis; majority of reimbursement remains fee-for-service (FFS)

Manage Patients/Members (Proactive)

Risk

Provider assumes significant risk for care costs, outcomes; may be reimbursed on capitated model

31

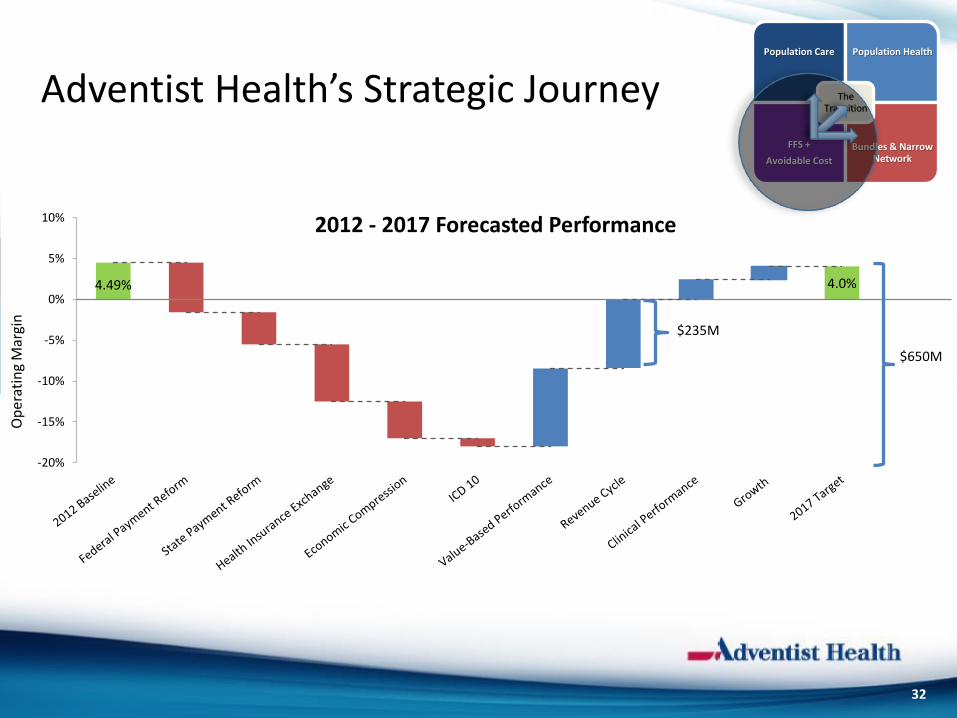

4.49% 4.0%

-20%

-15%

-10%

-5%

0%

5%

10% 2012 - 2017 Forecasted Performance

$235M

$650M

Adventist Health’s Strategic Journey

Op

erat

ing

Mar

gin

32

Population Care Population Health

FFS +

Avoidable Cost

Bundles & Narrow Network

The Transition

Value Based Performance

Care Transformation

Smart Growth

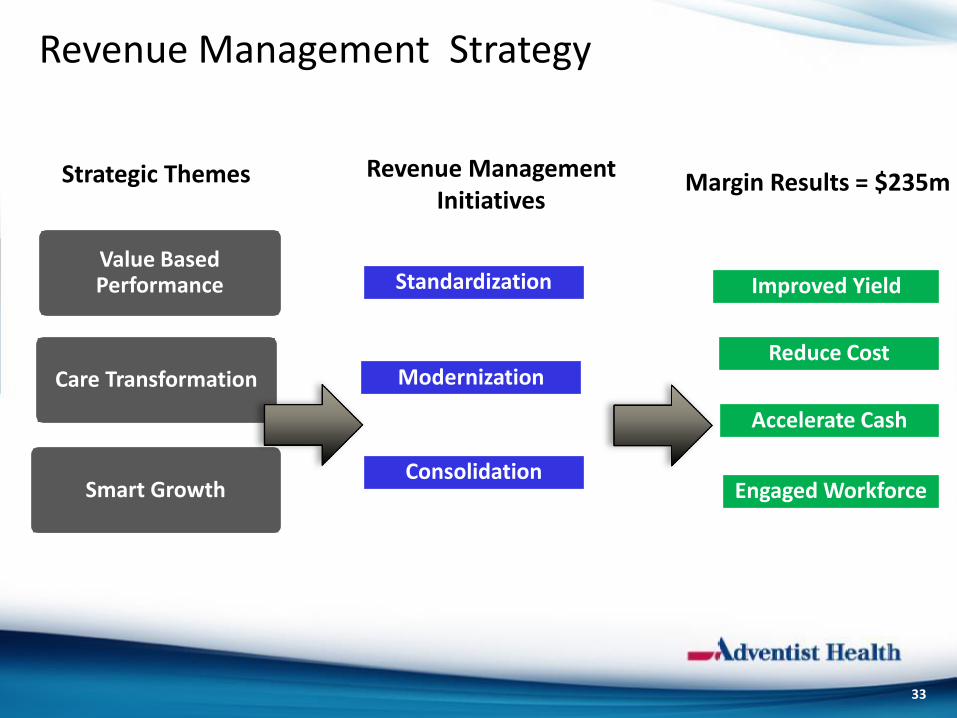

Strategic Themes Margin Results = $235m Revenue Management

Initiatives

Revenue Management Strategy

Operating Margin $235M

Consolidation

Modernization

Standardization

Reduce Cost

33

Accelerate Cash

Improved Yield

Engaged Workforce

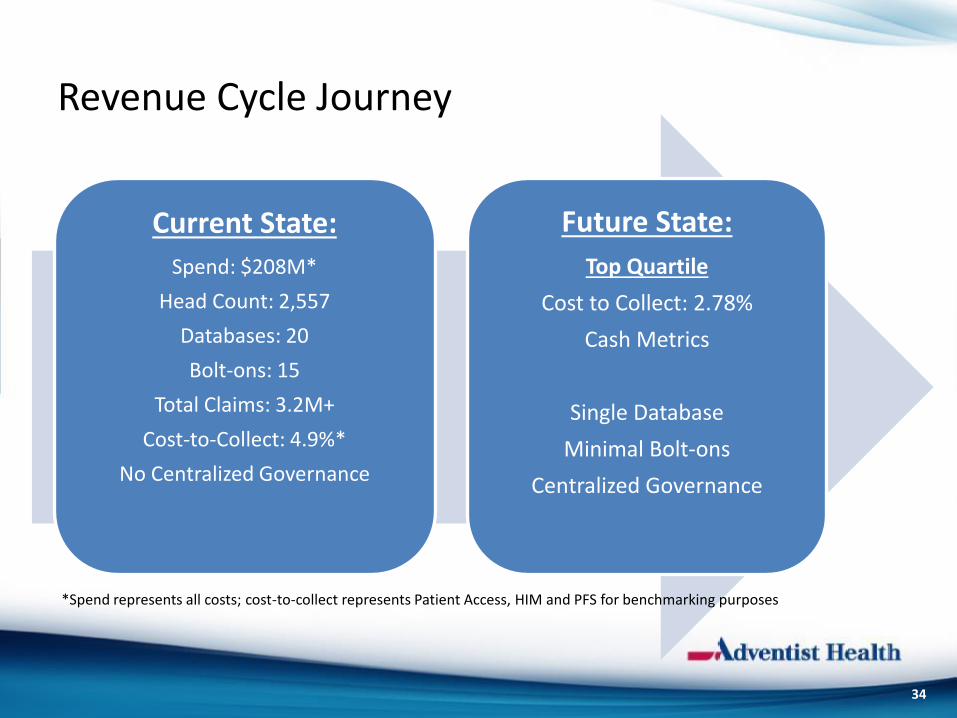

Current State:

Spend: $208M*

Head Count: 2,557

Databases: 20

Bolt-ons: 15

Total Claims: 3.2M+

Cost-to-Collect: 4.9%*

No Centralized Governance

Future State:

Top Quartile

Cost to Collect: 2.78%

Cash Metrics

Single Database

Minimal Bolt-ons

Centralized Governance

*Spend represents all costs; cost-to-collect represents Patient Access, HIM and PFS for benchmarking purposes

Revenue Cycle Journey

34

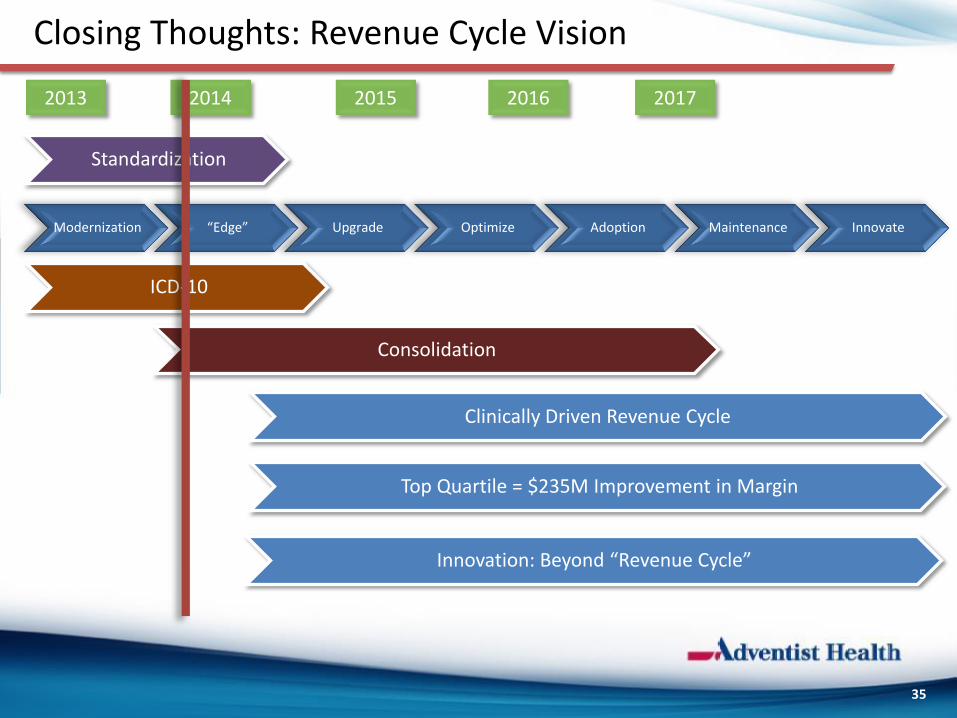

Closing Thoughts: Revenue Cycle Vision

Modernization “Edge” Upgrade Optimize Adoption Maintenance Innovate

2013 2016 2014 2015 2017

Standardization

Consolidation

Clinically Driven Revenue Cycle

Top Quartile = $235M Improvement in Margin

ICD-10

35

Innovation: Beyond “Revenue Cycle”

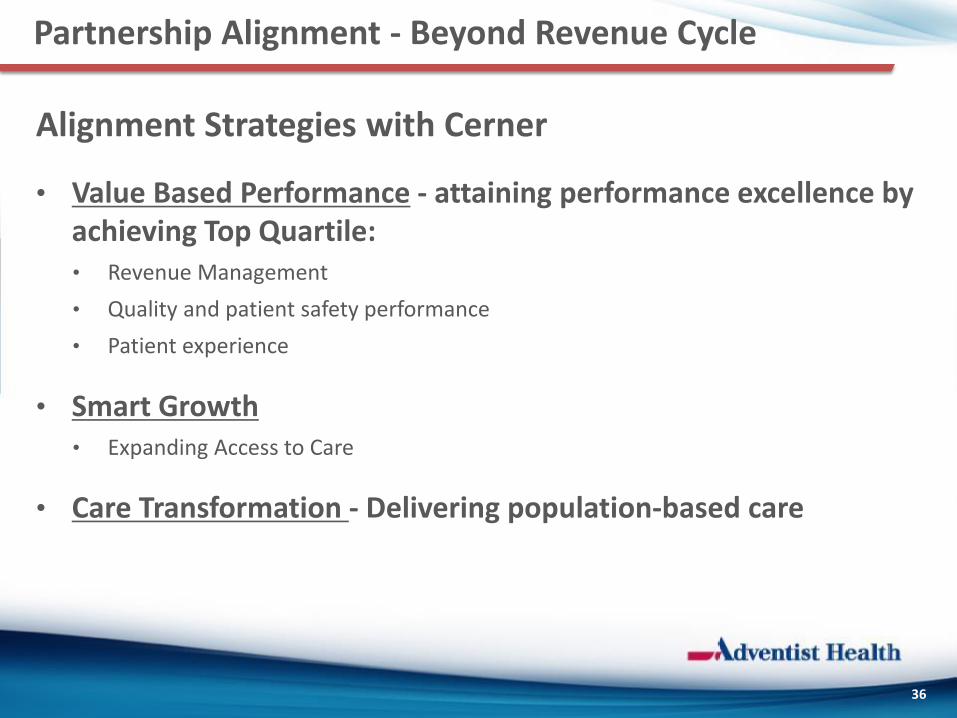

Partnership Alignment - Beyond Revenue Cycle

36

Alignment Strategies with Cerner

• Value Based Performance - attaining performance excellence by achieving Top Quartile: • Revenue Management

• Quality and patient safety performance

• Patient experience

• Smart Growth • Expanding Access to Care

• Care Transformation - Delivering population-based care

Advocate Cerner Collaboration Innovation in Population Health Management

Mike Englehart

President

Advocate Physician Partners

Rishi Sikka, MD

SVP, Clinical Transformation

Advocate Health Care

Matthew Swindells

SVP, Population Health & Global Strategy

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 38

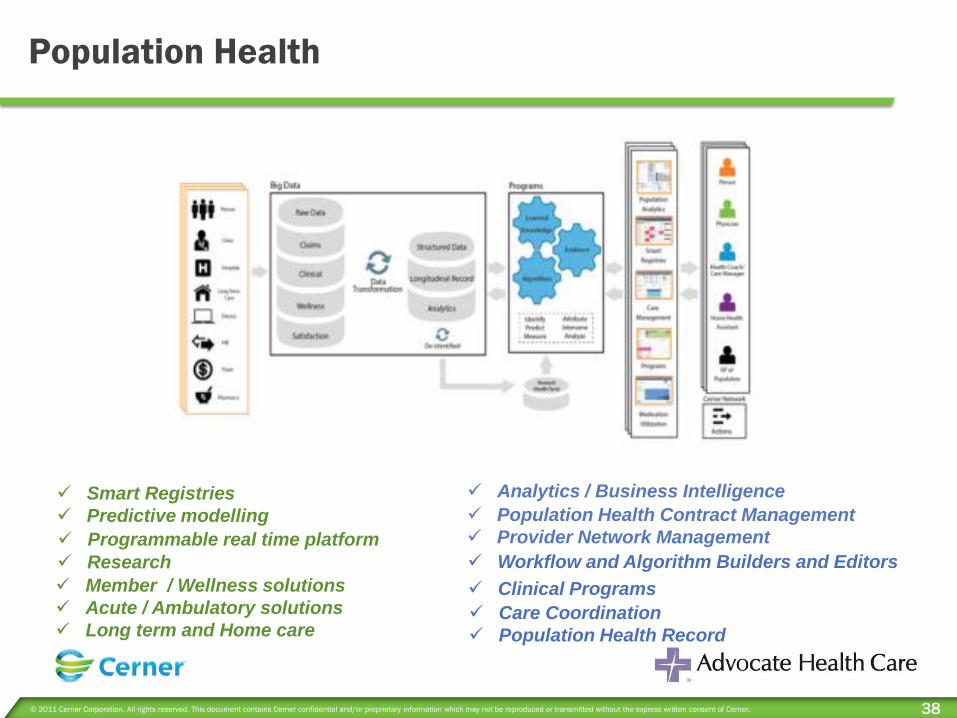

Population Health

Know Engage

Manage

Member / Wellness solutions

Acute / Ambulatory solutions

Long term and Home care

Research

Smart Registries

Predictive modelling

Programmable real time platform

Analytics / Business Intelligence

Care Coordination

Population Health Record

Clinical Programs

Population Health Contract Management

Provider Network Management

Workflow and Algorithm Builders and Editors

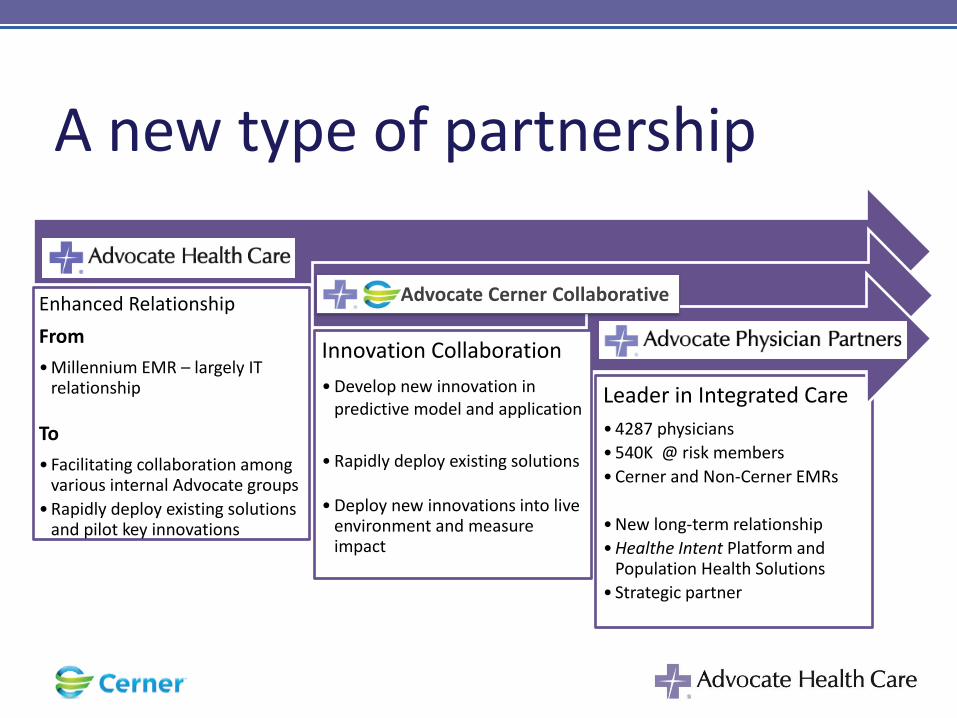

A new type of partnership

Enhanced Relationship

From

• Millennium EMR – largely IT relationship

To

• Facilitating collaboration among various internal Advocate groups

• Rapidly deploy existing solutions and pilot key innovations

Leader in Integrated Care

• 4287 physicians

• 540K @ risk members

• Cerner and Non-Cerner EMRs

• New long-term relationship

• Healthe Intent Platform and Population Health Solutions

• Strategic partner

Innovation Collaboration

• Develop new innovation in predictive model and application

• Rapidly deploy existing solutions

• Deploy new innovations into live environment and measure impact

Advocate Cerner Collaborative

Mike Englehart

President

Advocate Physician Partners

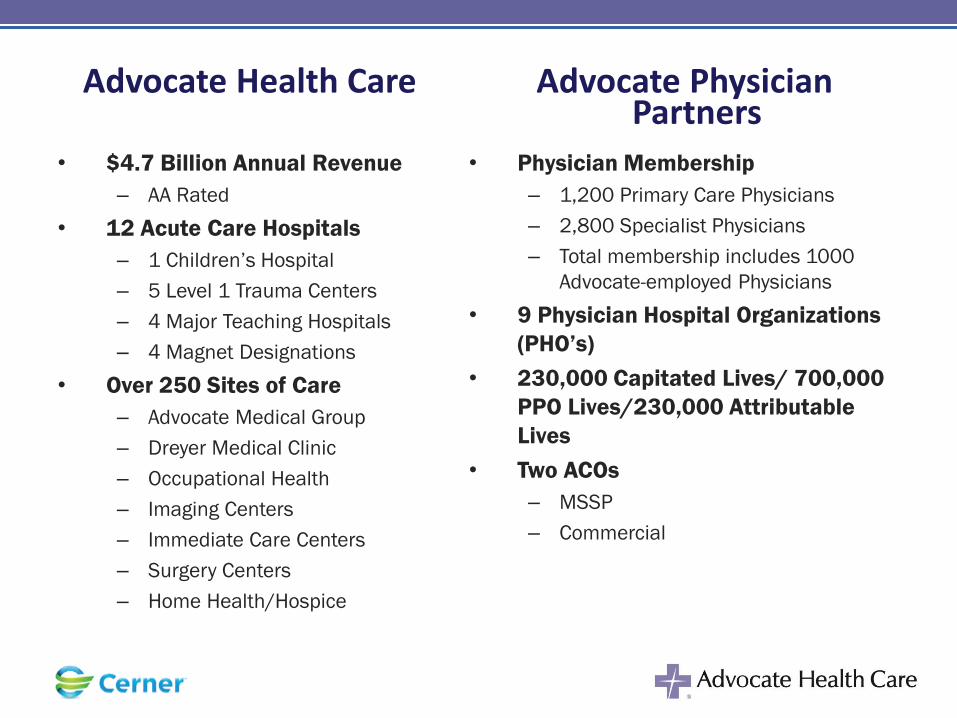

Advocate Health Care Advocate Physician Partners

• $4.7 Billion Annual Revenue

– AA Rated

• 12 Acute Care Hospitals

– 1 Children’s Hospital

– 5 Level 1 Trauma Centers

– 4 Major Teaching Hospitals

– 4 Magnet Designations

• Over 250 Sites of Care

– Advocate Medical Group

– Dreyer Medical Clinic

– Occupational Health

– Imaging Centers

– Immediate Care Centers

– Surgery Centers

– Home Health/Hospice

• Physician Membership

– 1,200 Primary Care Physicians

– 2,800 Specialist Physicians

– Total membership includes 1000

Advocate-employed Physicians

• 9 Physician Hospital Organizations

(PHO’s)

• 230,000 Capitated Lives/ 700,000

PPO Lives/230,000 Attributable

Lives

• Two ACOs

– MSSP

– Commercial

42

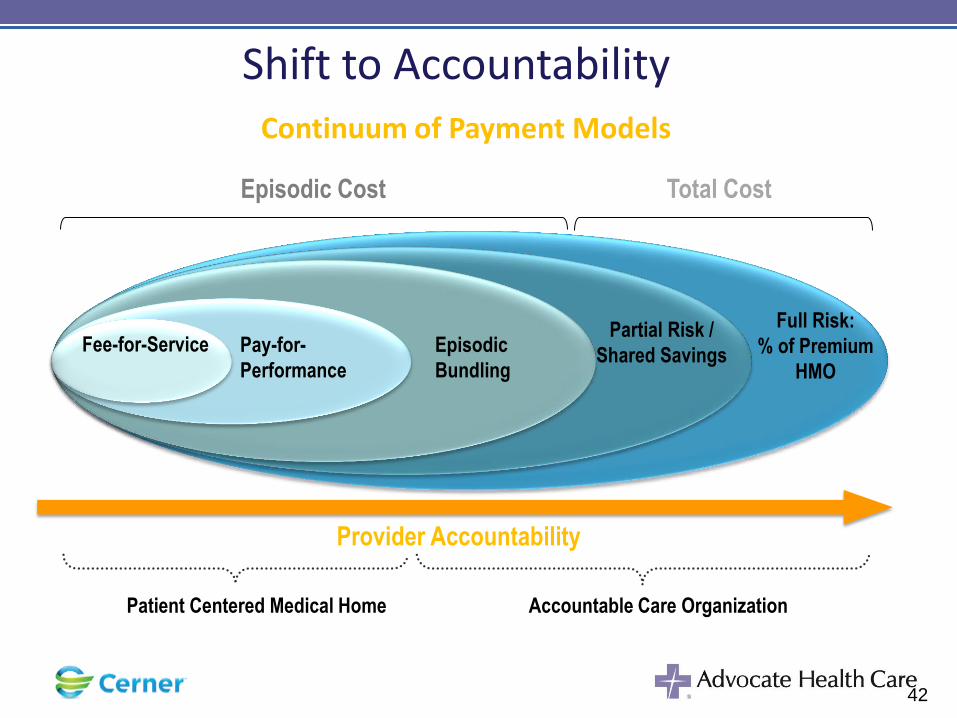

Shift to Accountability

Fee-for-Service Pay-for-

Performance

Episodic

Bundling

Partial Risk /

Shared Savings

Full Risk:

% of Premium

HMO

Episodic Cost Total Cost

Provider Accountability

Continuum of Payment Models

Patient Centered Medical Home Accountable Care Organization

43

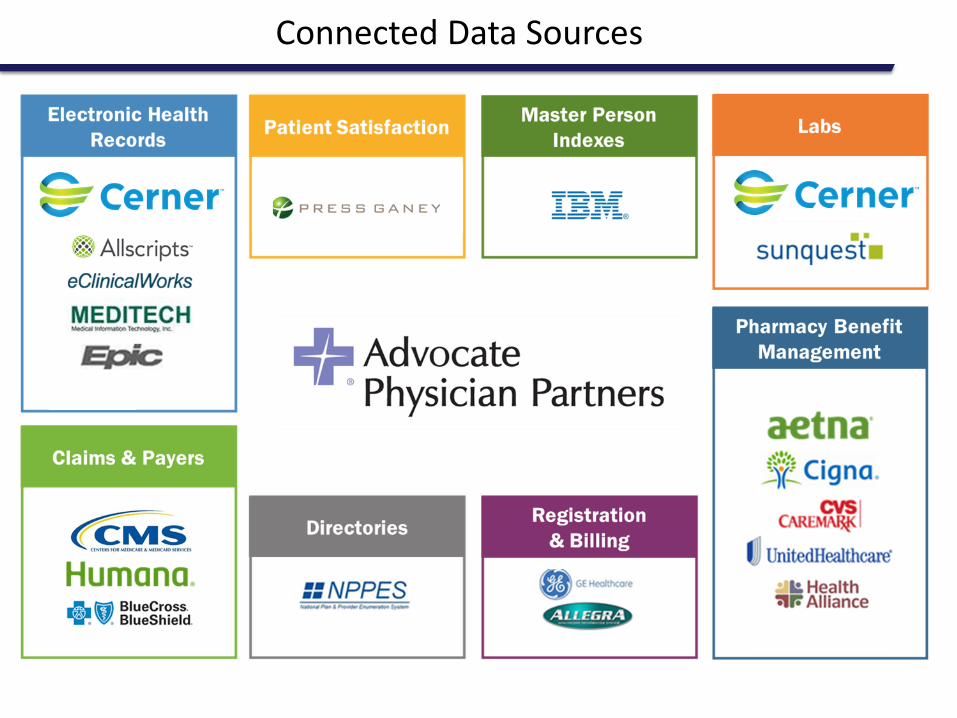

Connected Data Sources

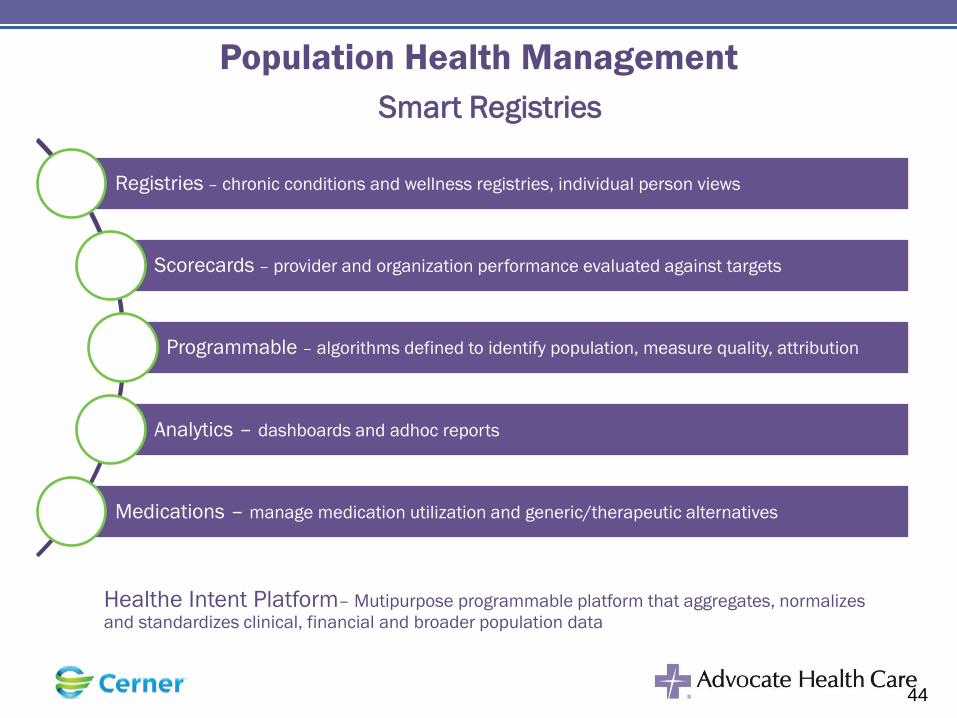

Population Health Management

Registries – chronic conditions and wellness registries, individual person views

Scorecards – provider and organization performance evaluated against targets

Programmable – algorithms defined to identify population, measure quality, attribution

Analytics – dashboards and adhoc reports

Medications – manage medication utilization and generic/therapeutic alternatives

Healthe Intent Platform– Mutipurpose programmable platform that aggregates, normalizes

and standardizes clinical, financial and broader population data

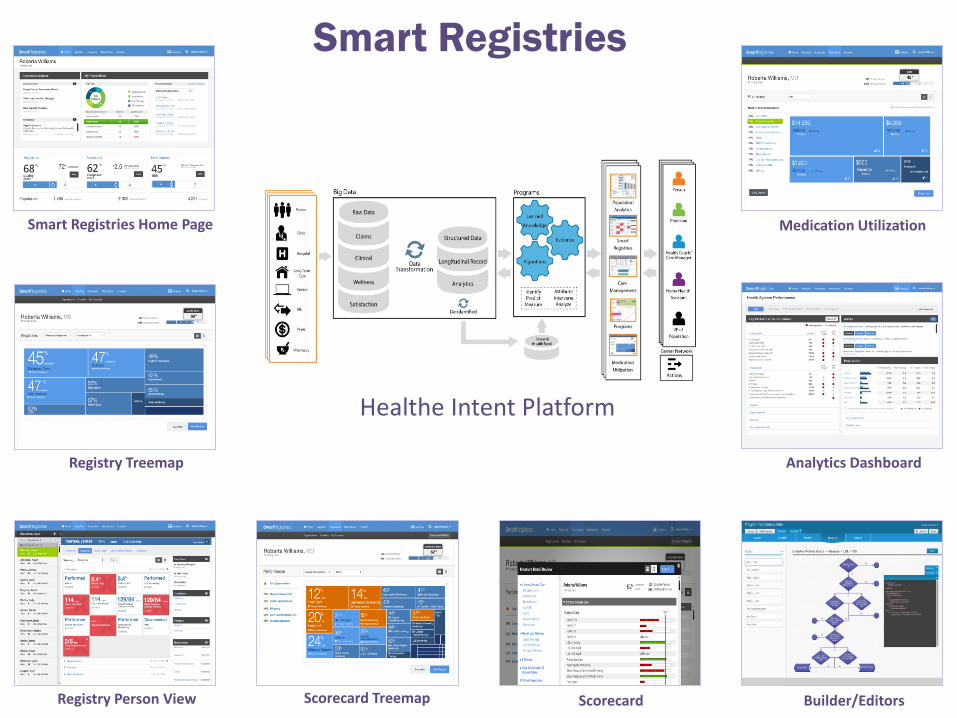

Smart Registries

44

45

46

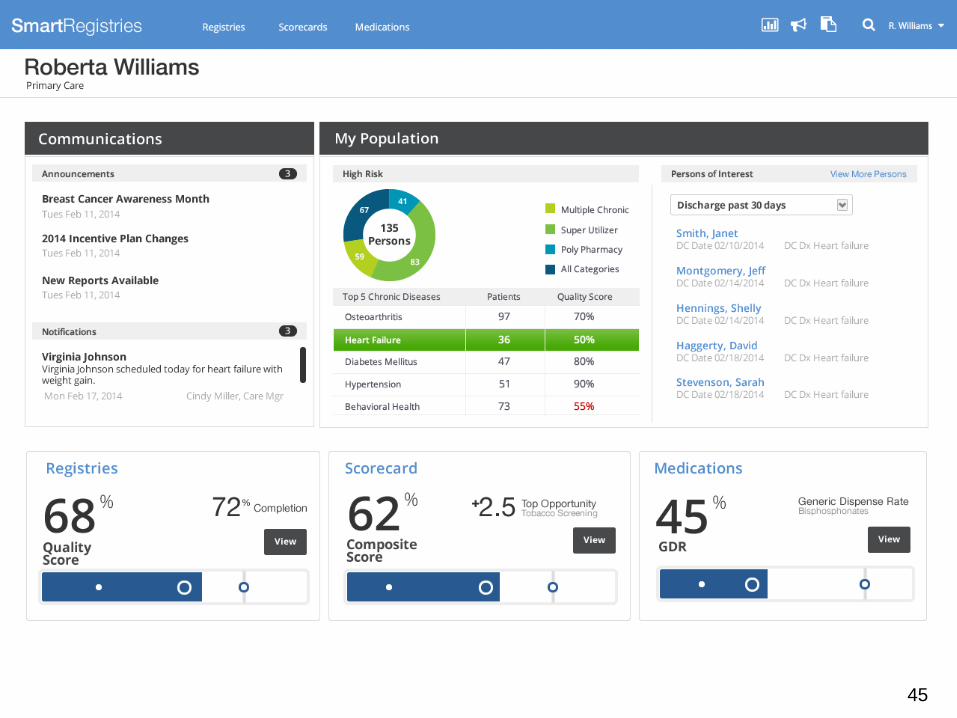

Smart Registries Home Page

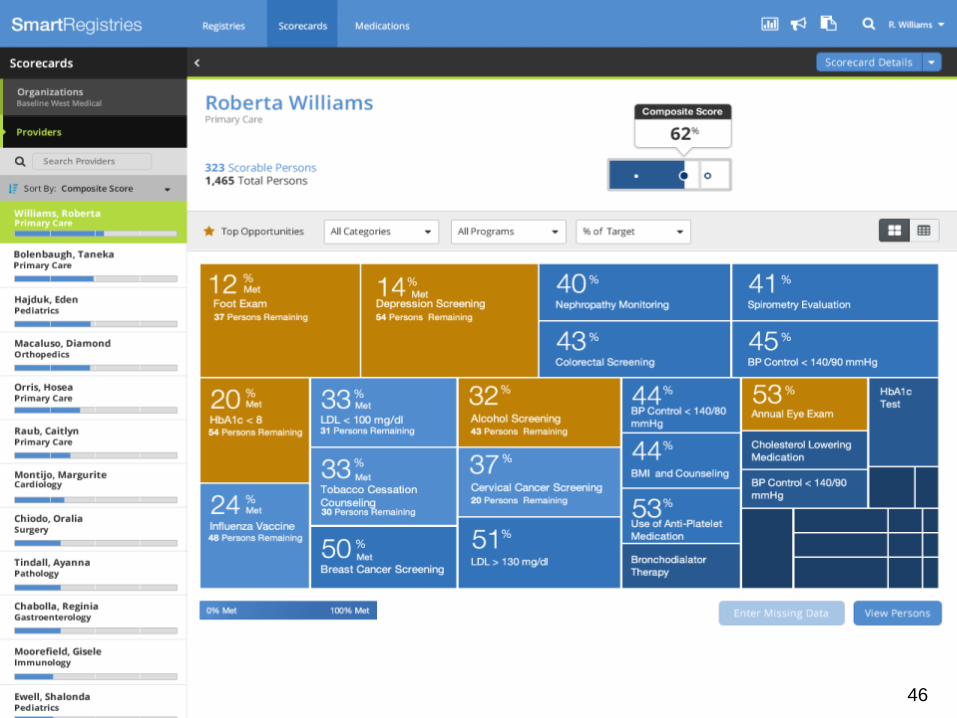

Scorecard Treemap Scorecard Registry Person View

Medication Utilization

Builder/Editors

Registry Treemap Analytics Dashboard

Healthe Intent Platform

Smart Registries

Rishi Sikka, MD

SVP, Clinical Transformation

Advocate Health Care

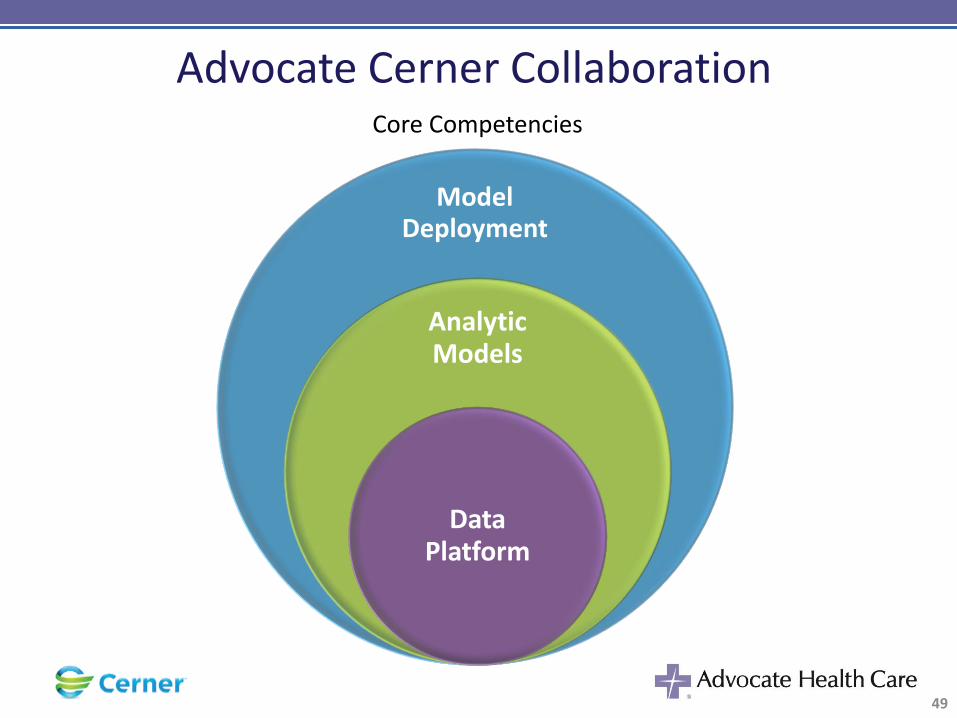

Advocate Cerner Collaboration

Model Deployment

Analytic Models

Data Platform

49

Core Competencies

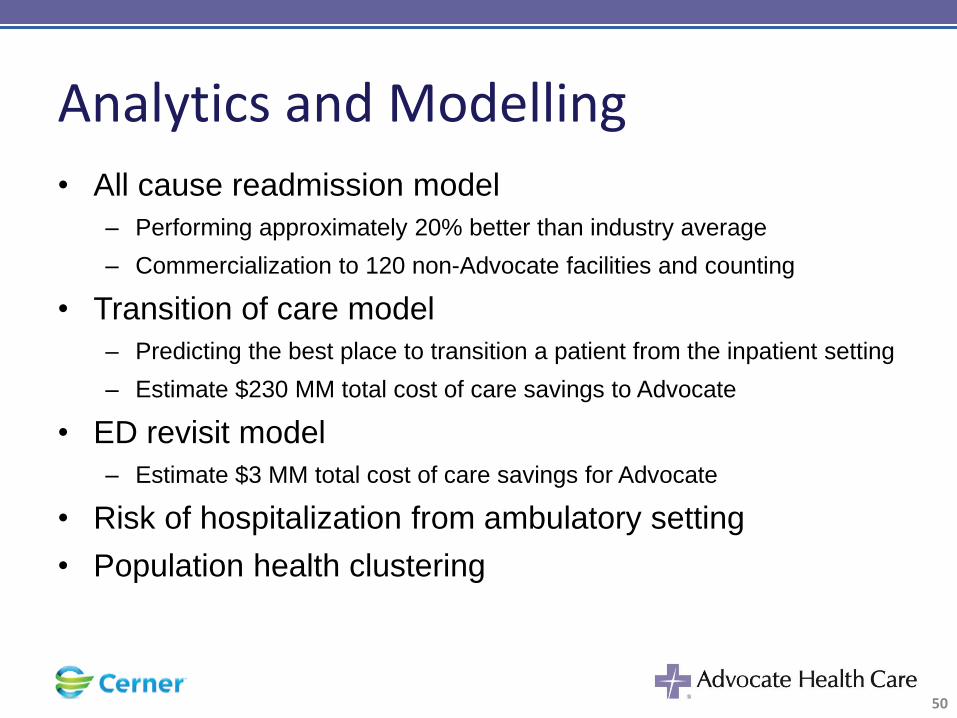

Analytics and Modelling

• All cause readmission model

– Performing approximately 20% better than industry average

– Commercialization to 120 non-Advocate facilities and counting

• Transition of care model

– Predicting the best place to transition a patient from the inpatient setting

– Estimate $230 MM total cost of care savings to Advocate

• ED revisit model

– Estimate $3 MM total cost of care savings for Advocate

• Risk of hospitalization from ambulatory setting

• Population health clustering

50

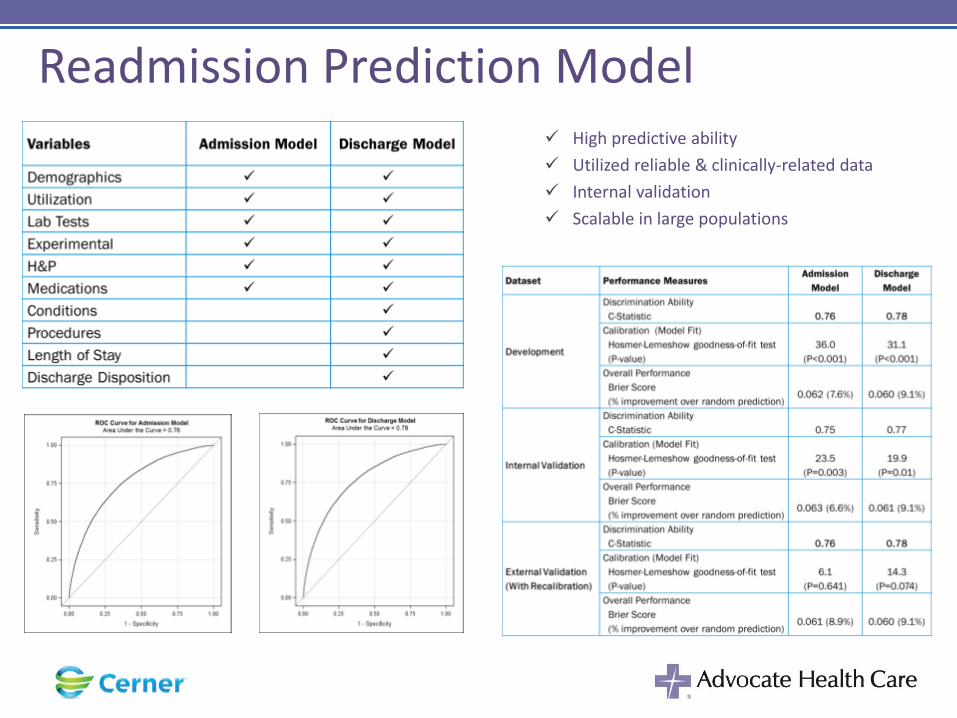

Readmission Prediction Model High predictive ability

Utilized reliable & clinically-related data

Internal validation

Scalable in large populations

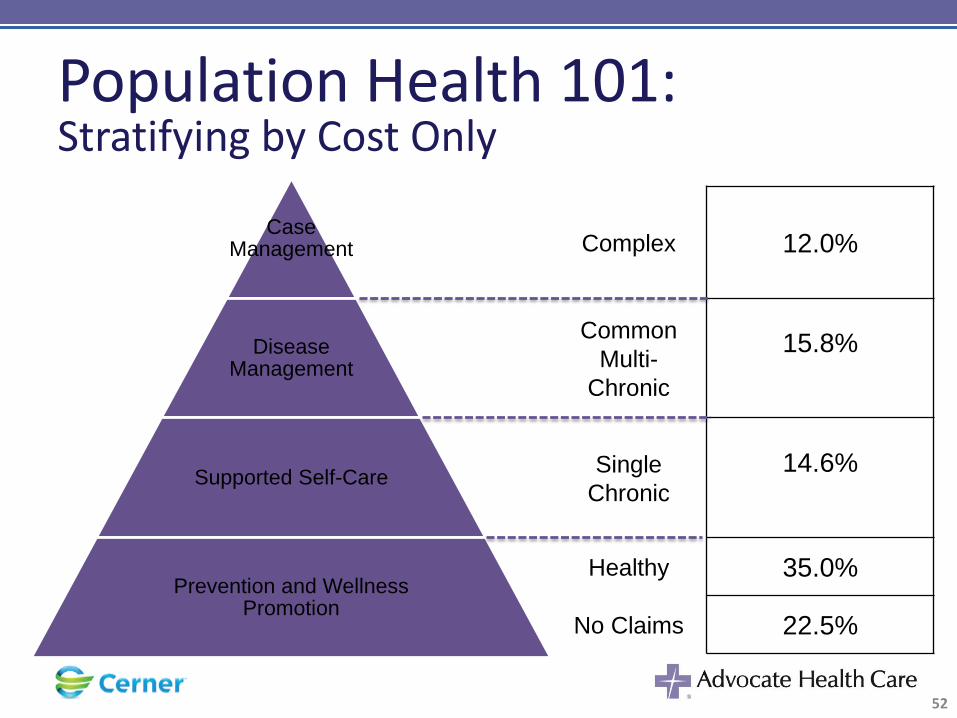

Population Health 101: Stratifying by Cost Only

Case Management

Disease Management

Supported Self-Care

Prevention and Wellness Promotion

Complex 12.0%

Common

Multi-

Chronic

15.8%

Single

Chronic

14.6%

Healthy 35.0%

No Claims 22.5%

52

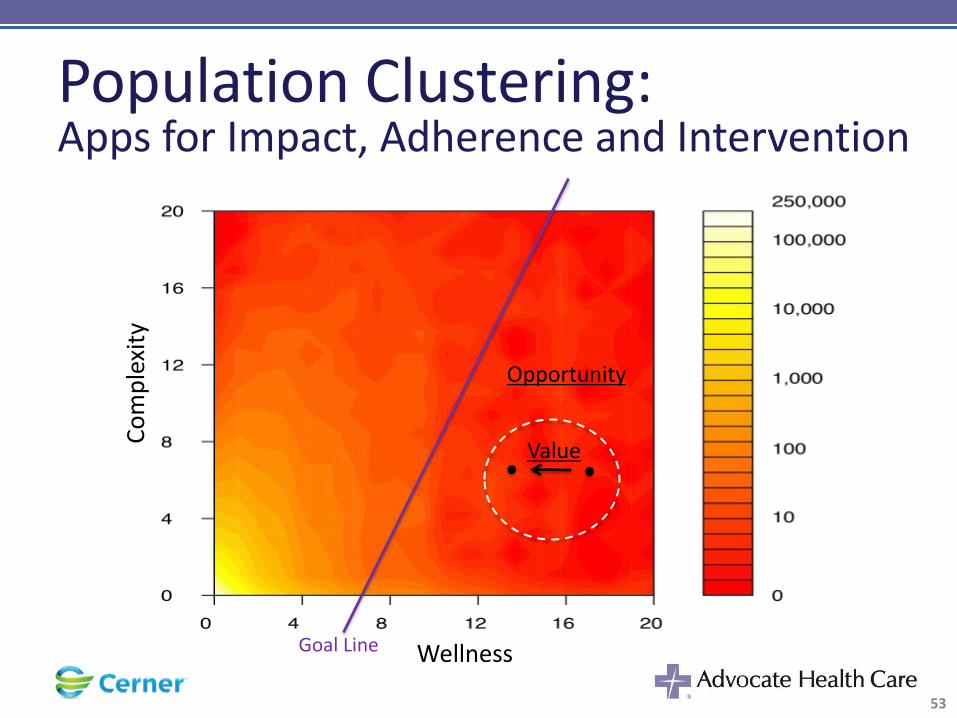

Population Clustering: Apps for Impact, Adherence and Intervention

Wellness

Co

mp

lexi

ty

Goal Line

Opportunity

Value

53

Intermountain Healthcare Strategic Partnership

Jeff Townsend Executive Vice President and Chief of Staff

Bert Zimmerli Chief Financial Officer, Executive Vice President

Intermountain Healthcare

Intermountain Healthcare and Cerner The Future in Health IT

Bert Zimmerli, CFO, Executive Vice President

Since 1975 • 22 hospitals • 2,784 licensed beds

Since 1983 • Health plans • 635,000 members

Since 1994 • 1,200 employed physicians • 530 advanced practice clinicians

Since 1997 • 9 key service lines

Highly Integrated Health System

Hospitals

SelectHealth

Medical Group

Clinical Programs

Our Charge: To become a “Model Healthcare System”

Core Business

Our efforts are ultimately centered around what matters most to our patients, employees, members and communities:

Perfecting the Clinical Work Process

Best clinical care in the world doesn’t matter

if no one can afford it.

The Intermountain Way

Improved quality & service

Evidence-based practice

Systematic approach- measure & improve

SUCCESS Always led by clinical but including operational, financial and even governance!

ALWAYS DO THE RIGHT THING!

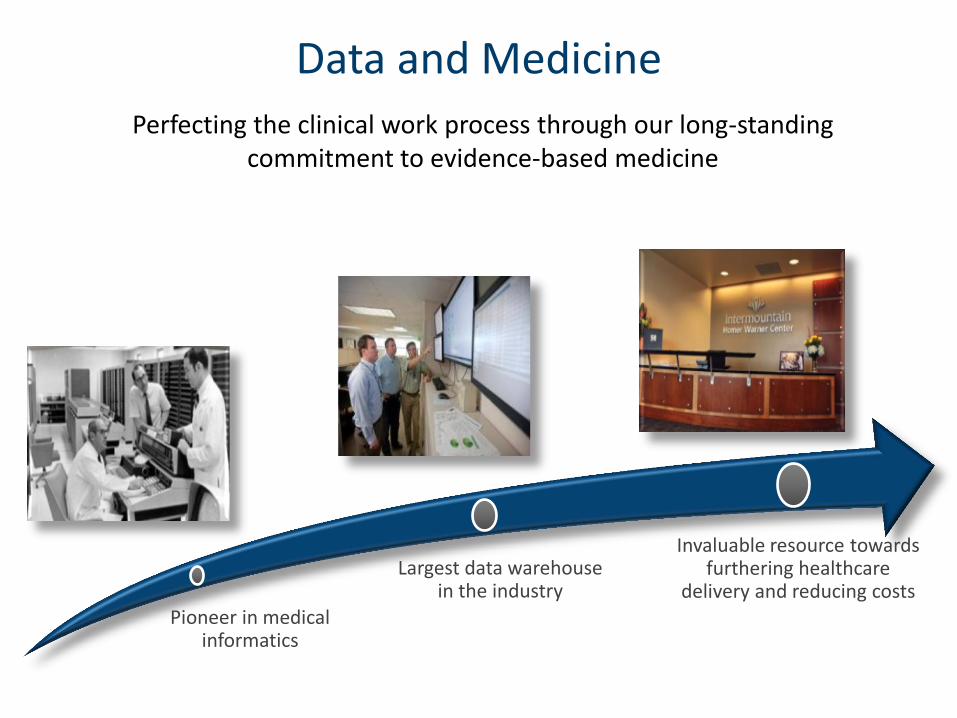

Perfecting the clinical work process through our long-standing commitment to evidence-based medicine

Pioneer in medical informatics

Largest data warehouse in the industry

Invaluable resource towards furthering healthcare

delivery and reducing costs

Data and Medicine

60

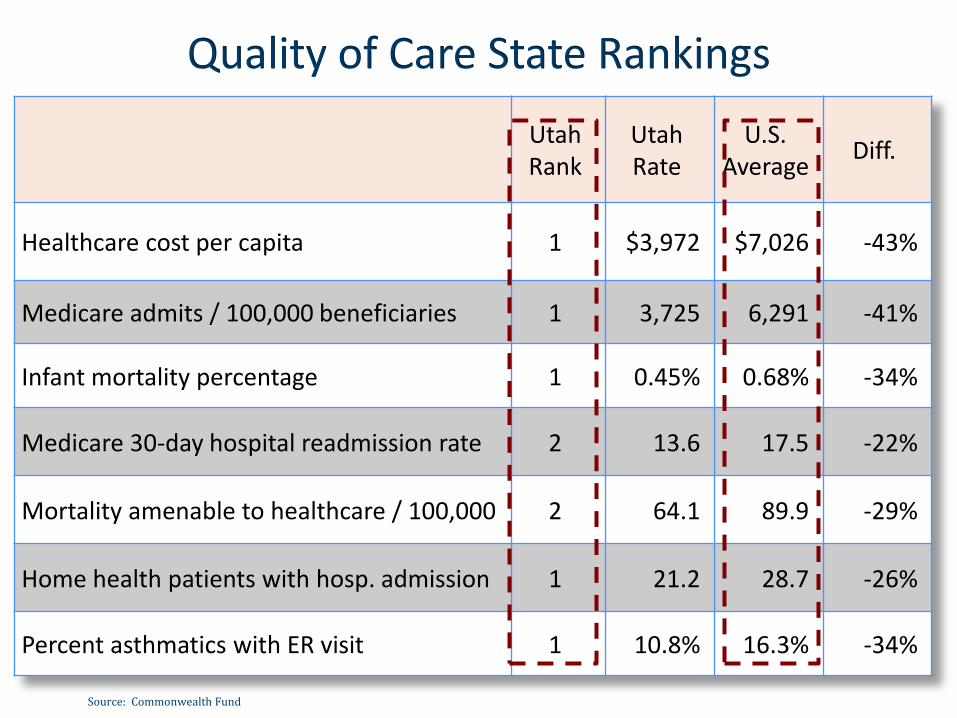

Quality of Care State Rankings

Utah Rank

Utah Rate

U.S. Average

Diff.

Healthcare cost per capita 1 $3,972 $7,026 -43%

Medicare admits / 100,000 beneficiaries 1 3,725 6,291 -41%

Infant mortality percentage 1 0.45% 0.68% -34%

Medicare 30-day hospital readmission rate 2 13.6 17.5 -22%

Mortality amenable to healthcare / 100,000 2 64.1 89.9 -29%

Home health patients with hosp. admission 1 21.2 28.7 -26%

Percent asthmatics with ER visit 1 10.8% 16.3% -34%

Source: Commonwealth Fund

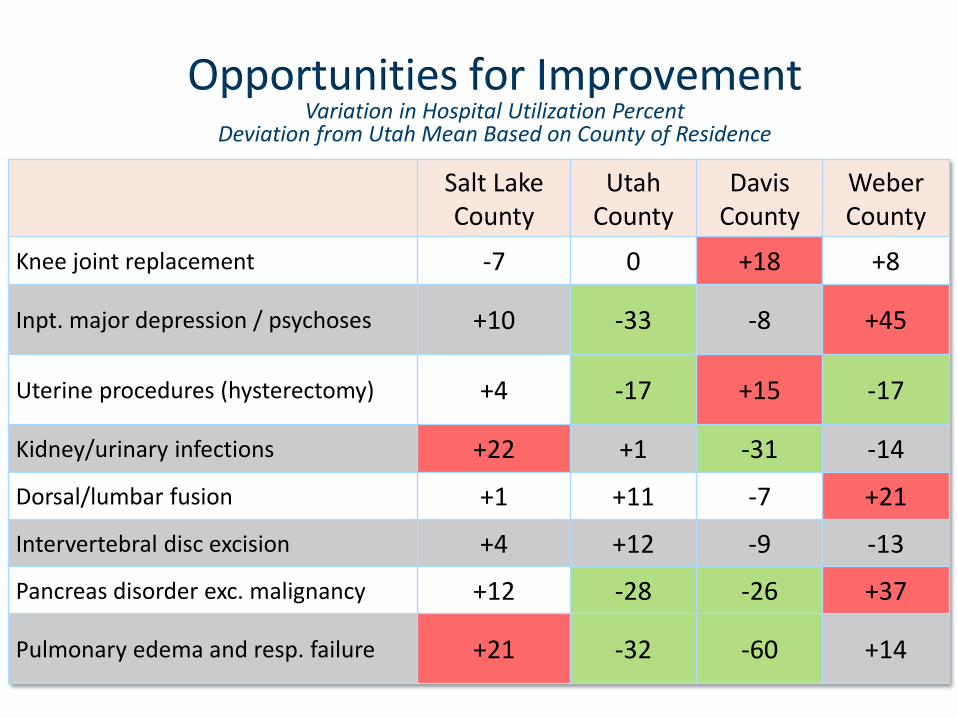

Opportunities for Improvement Variation in Hospital Utilization Percent

Deviation from Utah Mean Based on County of Residence

Salt Lake County

Utah County

Davis County

Weber County

Knee joint replacement -7 0 +18 +8

Inpt. major depression / psychoses +10 -33 -8 +45

Uterine procedures (hysterectomy) +4 -17 +15 -17

Kidney/urinary infections +22 +1 -31 -14

Dorsal/lumbar fusion +1 +11 -7 +21

Intervertebral disc excision +4 +12 -9 -13

Pancreas disorder exc. malignancy +12 -28 -26 +37

Pulmonary edema and resp. failure +21 -32 -60 +14

Aa1/Stable AA+/Stable

“Intermountain has a long track record of producing consistently exceptional results by employing financial and operational best practices under the direction of a seasoned management and Board of Trustees.” — Moody’s, 2013

“A strong board of trustees committed to consistent improvement in governance and active in the setting and monitoring of key medical and safety indicators.” — Standard & Poor’s, 2005

Principles that never change

1. Not for profit must never mean not as efficient

Principles that never change

2. Operate as a system with no unnecessary variation or waste… “Healthcare is a team sport.”

3. Understand and implement best practices including those from other industries and other countries

4. Invest in R&D and process development – always supported by data and metrics… “Process without metrics is religion.”

Principles that never change

5. Always do the right thing which is usually the best long-term financial decision

Where we are going

Clinical excellence Aligned incentives

Efficient operations

Engaged, informed patients

Engaged communities

Transforming Healthcare To Achieve Better Health and Cost Outcomes

Being the Best

“A good hockey player skates to where the puck is…

A GREAT hockey player skates to where the puck is going to be.”

- Wayne Gretzky

70

• Mobile Outreach Focus

• Service Oriented Architecture

• Activity Based Costing

An Investment with a Strategic Partner

• Strong leadership and vision

• Similar company culture

• Modern infrastructure and commitment to standards

• Innovative and forward looking

• Experience with implementation and co-development

We’re all in!

WE ARE THE BRAND

THIS IS PERSONAL

Intermountain Healthcare Strategic Partnership

Jeff Townsend Executive Vice President and Chief of Staff

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 74

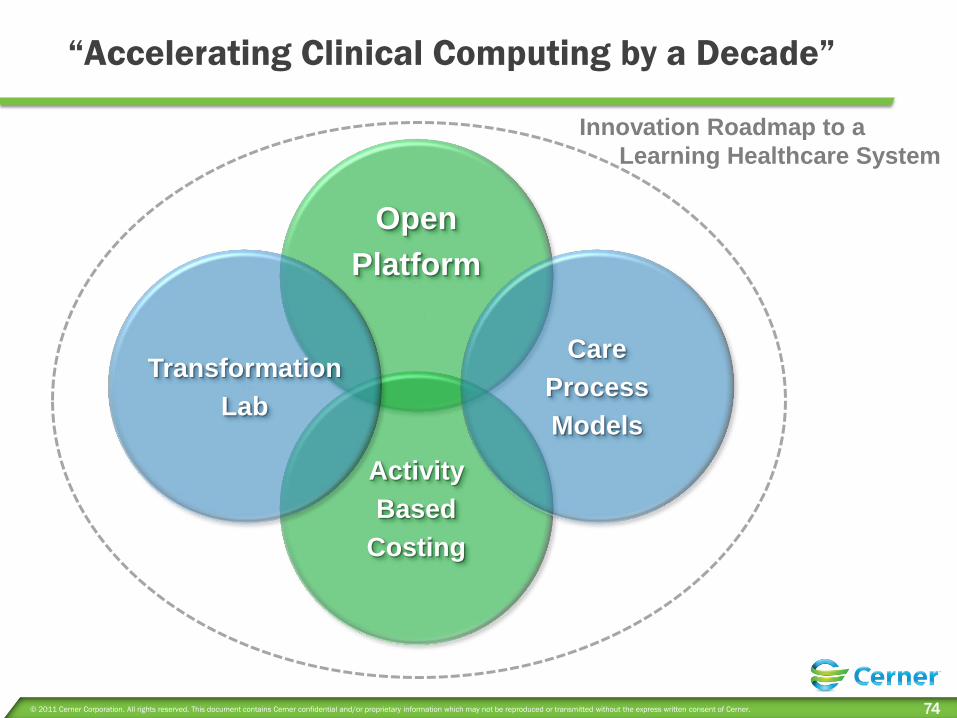

“Accelerating Clinical Computing by a Decade”

Open

Platform

Activity

Based

Costing

Transformation

Lab

Care

Process

Models

Innovation Roadmap to a

Learning Healthcare System

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 75

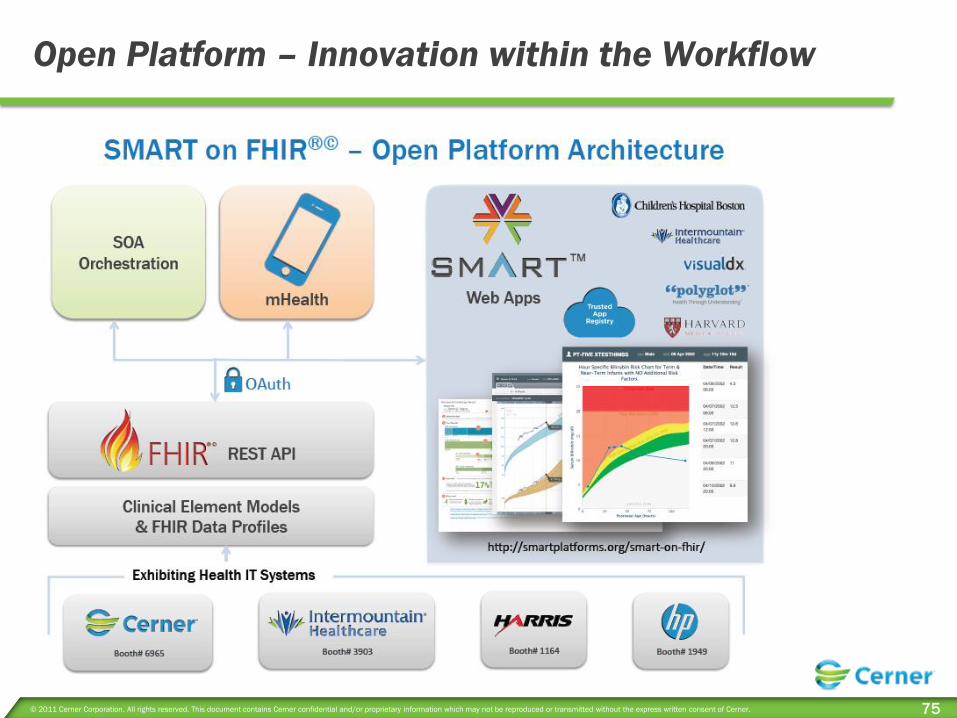

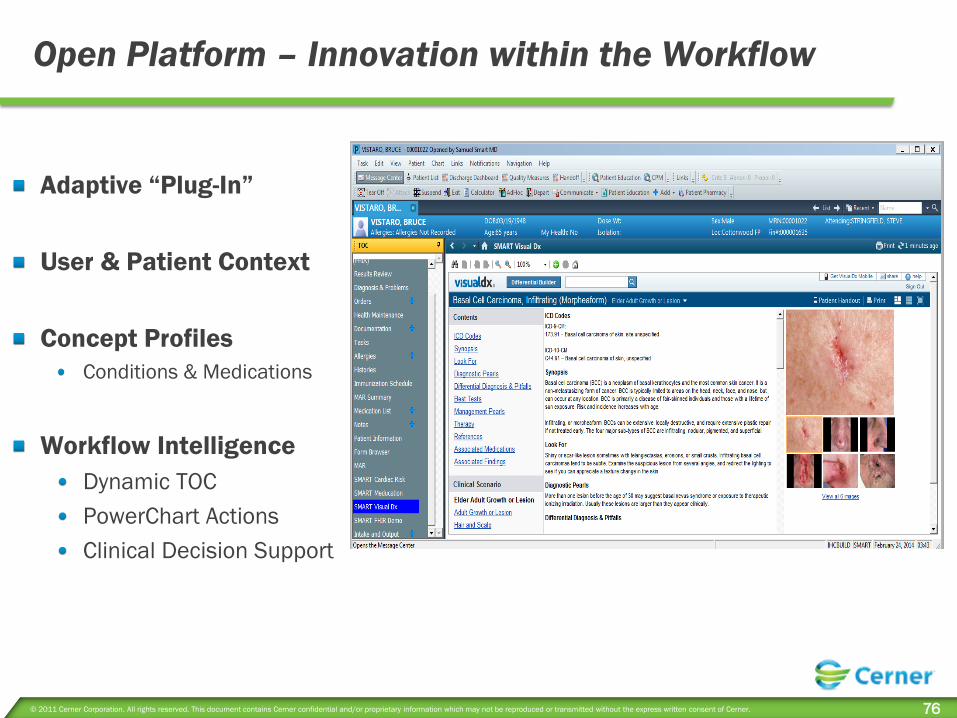

Open Platform – Innovation within the Workflow

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 76

Open Platform – Innovation within the Workflow

Adaptive “Plug-In”

User & Patient Context

Concept Profiles

Conditions & Medications

Workflow Intelligence

Dynamic TOC

PowerChart Actions

Clinical Decision Support

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 77

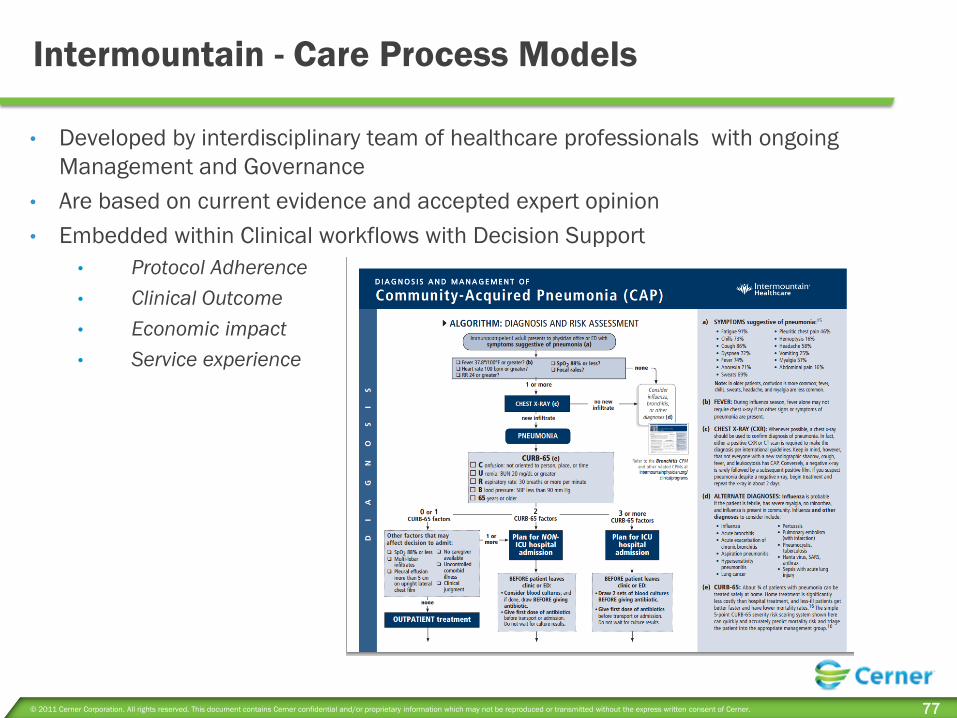

Intermountain - Care Process Models

• Developed by interdisciplinary team of healthcare professionals with ongoing

Management and Governance

• Are based on current evidence and accepted expert opinion

• Embedded within Clinical workflows with Decision Support

• Protocol Adherence

• Clinical Outcome

• Economic impact

• Service experience

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 78

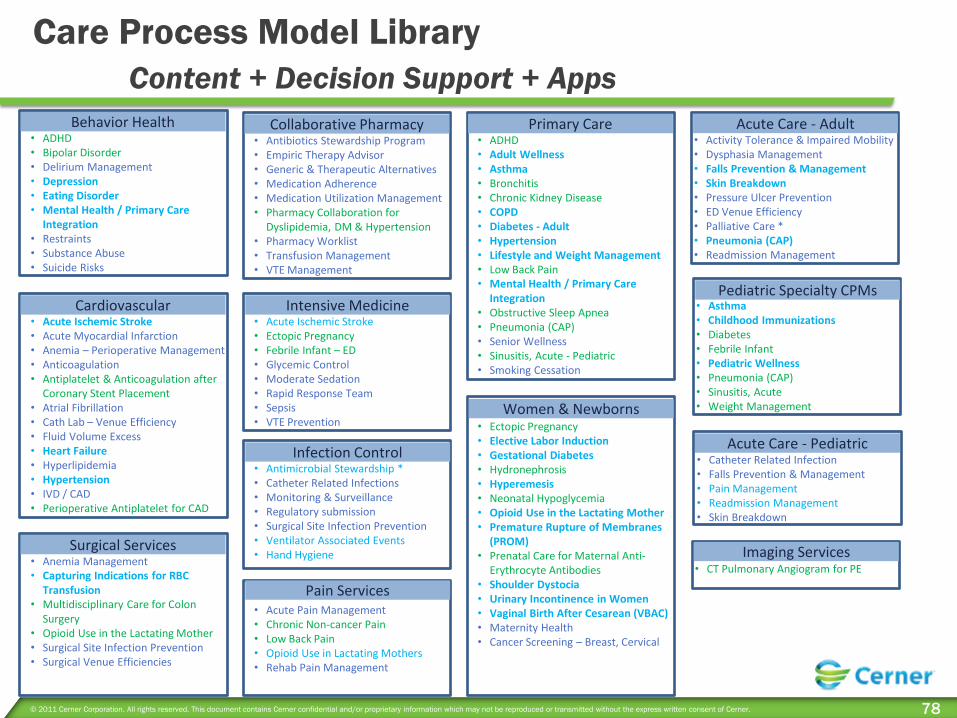

Care Process Model Library

Content + Decision Support + Apps

Behavior Health • ADHD • Bipolar Disorder • Delirium Management • Depression • Eating Disorder • Mental Health / Primary Care

Integration • Restraints • Substance Abuse • Suicide Risks

Cardiovascular • Acute Ischemic Stroke • Acute Myocardial Infarction • Anemia – Perioperative Management • Anticoagulation • Antiplatelet & Anticoagulation after

Coronary Stent Placement • Atrial Fibrillation • Cath Lab – Venue Efficiency • Fluid Volume Excess • Heart Failure • Hyperlipidemia • Hypertension • IVD / CAD • Perioperative Antiplatelet for CAD

Imaging Services • CT Pulmonary Angiogram for PE

Intensive Medicine • Acute Ischemic Stroke • Ectopic Pregnancy • Febrile Infant – ED • Glycemic Control • Moderate Sedation • Rapid Response Team • Sepsis • VTE Prevention

Collaborative Pharmacy • Antibiotics Stewardship Program • Empiric Therapy Advisor • Generic & Therapeutic Alternatives • Medication Adherence • Medication Utilization Management • Pharmacy Collaboration for

Dyslipidemia, DM & Hypertension • Pharmacy Worklist • Transfusion Management • VTE Management

Pediatric Specialty CPMs • Asthma • Childhood Immunizations • Diabetes • Febrile Infant • Pediatric Wellness • Pneumonia (CAP) • Sinusitis, Acute • Weight Management

Pain Services • Acute Pain Management • Chronic Non-cancer Pain • Low Back Pain • Opioid Use in Lactating Mothers • Rehab Pain Management

Primary Care • ADHD

• Adult Wellness • Asthma • Bronchitis • Chronic Kidney Disease

• COPD

• Diabetes - Adult • Hypertension • Lifestyle and Weight Management • Low Back Pain • Mental Health / Primary Care

Integration

• Obstructive Sleep Apnea

• Pneumonia (CAP) • Senior Wellness

• Sinusitis, Acute - Pediatric

• Smoking Cessation

Surgical Services • Anemia Management • Capturing Indications for RBC

Transfusion

• Multidisciplinary Care for Colon Surgery

• Opioid Use in the Lactating Mother • Surgical Site Infection Prevention

• Surgical Venue Efficiencies

Infection Control • Antimicrobial Stewardship * • Catheter Related Infections • Monitoring & Surveillance • Regulatory submission • Surgical Site Infection Prevention • Ventilator Associated Events • Hand Hygiene

Acute Care - Adult • Activity Tolerance & Impaired Mobility • Dysphasia Management • Falls Prevention & Management • Skin Breakdown • Pressure Ulcer Prevention • ED Venue Efficiency • Palliative Care * • Pneumonia (CAP) • Readmission Management

Acute Care - Pediatric • Catheter Related Infection

• Falls Prevention & Management • Pain Management • Readmission Management • Skin Breakdown

Women & Newborns • Ectopic Pregnancy • Elective Labor Induction • Gestational Diabetes • Hydronephrosis • Hyperemesis • Neonatal Hypoglycemia • Opioid Use in the Lactating Mother • Premature Rupture of Membranes

(PROM) • Prenatal Care for Maternal Anti-

Erythrocyte Antibodies • Shoulder Dystocia • Urinary Incontinence in Women • Vaginal Birth After Cesarean (VBAC) • Maternity Health • Cancer Screening – Breast, Cervical

79 79

Intermountain Transformation Lab

Booth #3903

Collaborative Workflows with Awareness

Orchestrated Activity Management & Measurement

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 80

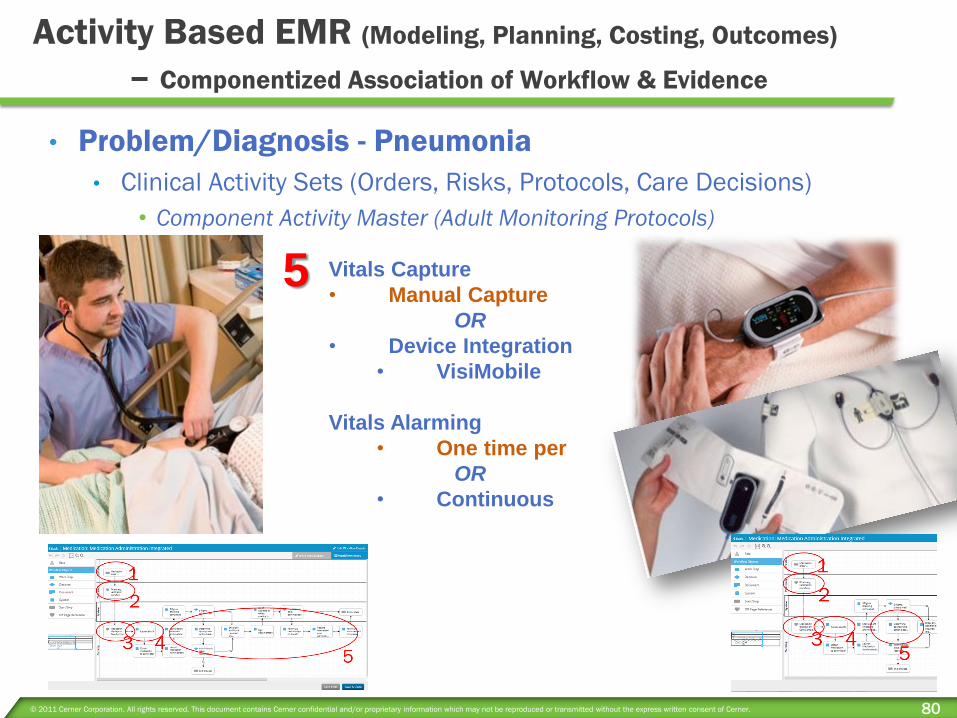

Activity Based EMR (Modeling, Planning, Costing, Outcomes)

– Componentized Association of Workflow & Evidence

• Problem/Diagnosis - Pneumonia

• Clinical Activity Sets (Orders, Risks, Protocols, Care Decisions)

• Component Activity Master (Adult Monitoring Protocols)

Vitals Capture

• Manual Capture

OR

• Device Integration

• VisiMobile

Vitals Alarming

• One time per

OR

• Continuous

5

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 81

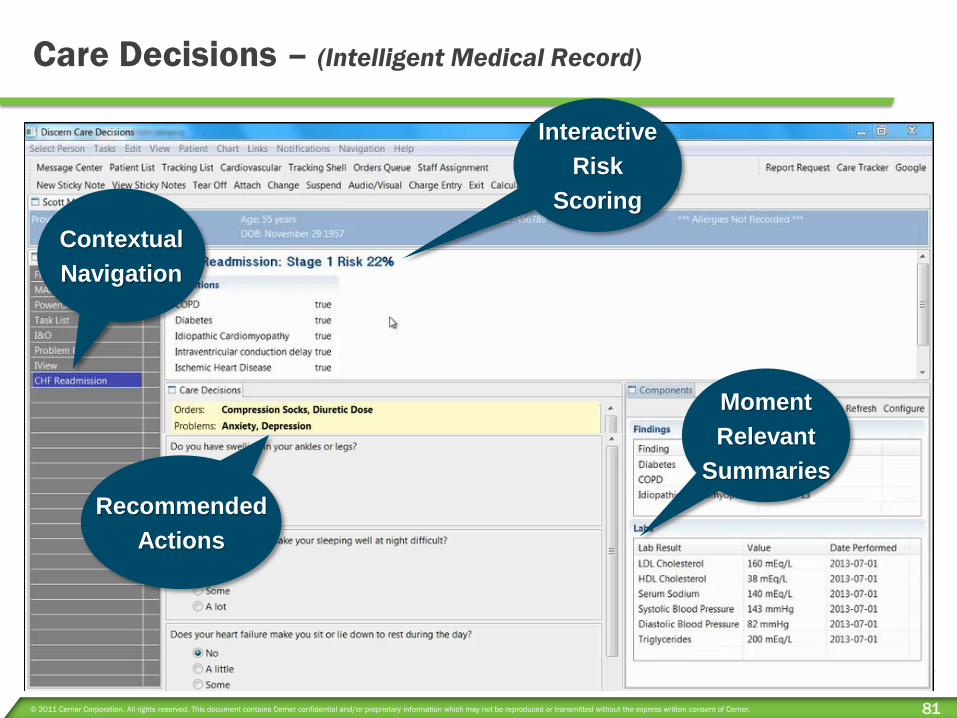

Care Decisions – (Intelligent Medical Record)

Contextual

Navigation

Moment

Relevant

Summaries

Interactive

Risk

Scoring

Recommended

Actions

Chairman’s Comments and Q&A

Neal Patterson Chairman, Chief Executive Officer and Co-Founder

Health care is too important to stay the same.TM

© 2011 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 84

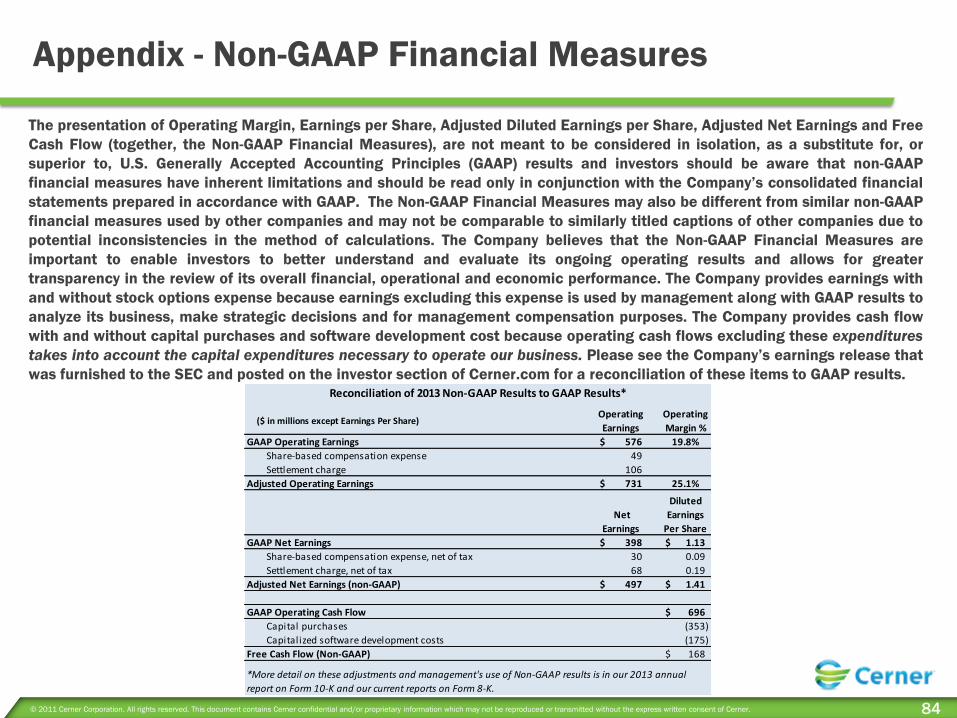

Appendix - Non-GAAP Financial Measures

The presentation of Operating Margin, Earnings per Share, Adjusted Diluted Earnings per Share, Adjusted Net Earnings and Free

Cash Flow (together, the Non-GAAP Financial Measures), are not meant to be considered in isolation, as a substitute for, or

superior to, U.S. Generally Accepted Accounting Principles (GAAP) results and investors should be aware that non-GAAP

financial measures have inherent limitations and should be read only in conjunction with the Company’s consolidated financial

statements prepared in accordance with GAAP. The Non-GAAP Financial Measures may also be different from similar non-GAAP

financial measures used by other companies and may not be comparable to similarly titled captions of other companies due to

potential inconsistencies in the method of calculations. The Company believes that the Non-GAAP Financial Measures are

important to enable investors to better understand and evaluate its ongoing operating results and allows for greater

transparency in the review of its overall financial, operational and economic performance. The Company provides earnings with

and without stock options expense because earnings excluding this expense is used by management along with GAAP results to

analyze its business, make strategic decisions and for management compensation purposes. The Company provides cash flow

with and without capital purchases and software development cost because operating cash flows excluding these expenditures

takes into account the capital expenditures necessary to operate our business. Please see the Company’s earnings release that

was furnished to the SEC and posted on the investor section of Cerner.com for a reconciliation of these items to GAAP results.

($ in millions except Earnings Per Share)

Operating

Earnings

Operating

Margin %

GAAP Operating Earnings 576$ 19.8%

Share-based compensation expense 49

Settlement charge 106

Adjusted Operating Earnings 731$ 25.1%

Net

Earnings

Diluted

Earnings

Per Share

GAAP Net Earnings 398$ 1.13$

Share-based compensation expense, net of tax 30 0.09

Settlement charge, net of tax 68 0.19

Adjusted Net Earnings (non-GAAP) 497$ 1.41$

GAAP Operating Cash Flow 696$

Capital purchases (353)

Capitalized software development costs (175)

Free Cash Flow (Non-GAAP) 168$

Reconciliation of 2013 Non-GAAP Results to GAAP Results*

*More detail on these adjustments and management's use of Non-GAAP results is in our 2013 annual

report on Form 10-K and our current reports on Form 8-K.