Embed Size (px)

Citation preview

2010AnnuAl REpoRt

3

Table of conTenTS4

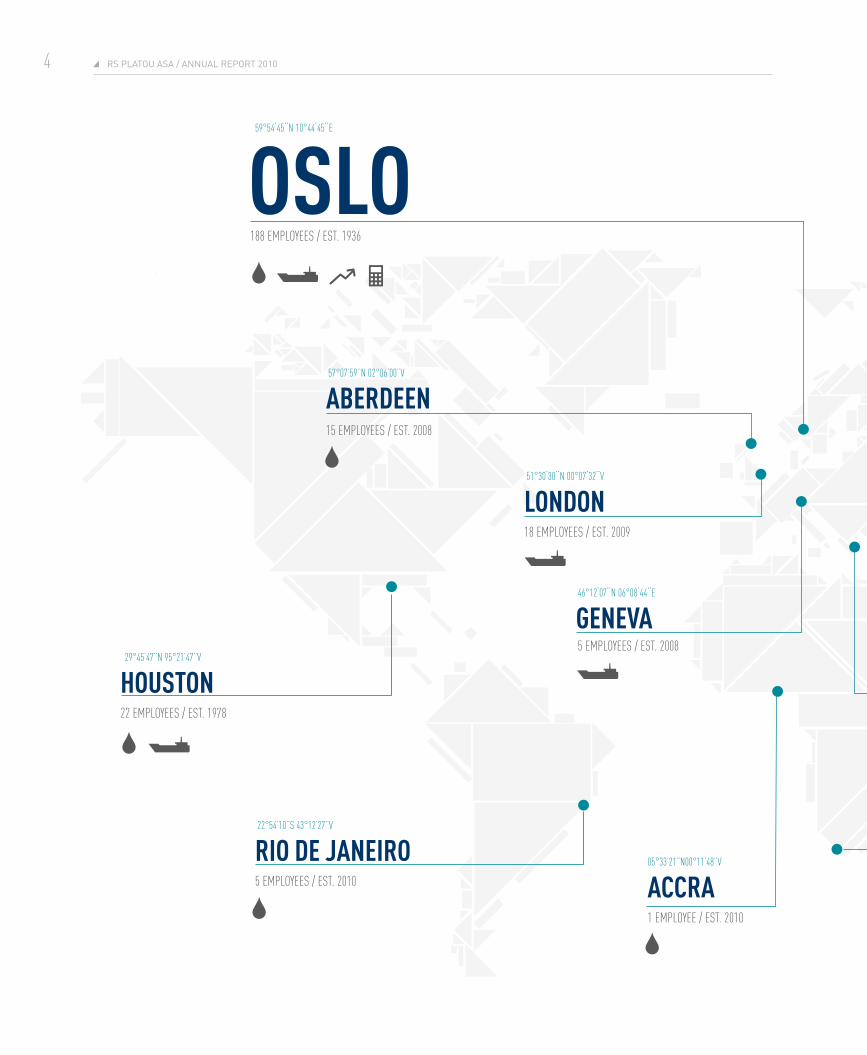

Global Presence

6Letter from the Chairman

8Key Financial Figures – RS Platou Group

10History – RS Platou Group

14Overview of our Business Areas

24Corporate Governance

32Board of Director’s Report for 2010

38Consolidated Financial Statements

p. 48 - Notes to the Consolidated Financial Statements

94Accounts for RS Platou ASA

p. 99 - Notes to the Accounts for RS Platou ASA

111Auditor’s Report for 2010

RS Platou aSa / annual RePoRt 20104

59°54’45’’n 10°44’45’’e

OslO188 employeeS / eST. 1936

51°30’30’’n 00°07’32’’V

lONDON18 employeeS / eST. 2009

57°07’59’’n 02°06’00’’V

AberDeeN15 employeeS / eST. 2008

29°45’47’’n 95°21’47’’V

HOUsTON22 employeeS / eST. 1978

22°54’10’’S 43°12’27’’V

rIO De JANeIrO5 employeeS / eST. 2010

05°33’21’’n00°11’48’’V

ACCrA1 employee / eST. 2010

46°12’07’’n 06°08’44’’e

GeNeVA5 employeeS / eST. 2008

5GloBal PReSenCe

projecT finance inVeSTmenT banKinG ShipbroKinG offShore

Global preSenceThe world accordinG To rS plaTou

31°13’19’’n 121°27’29’’e

sHANGHAI4 employeeS / eST. 2007

33°55’0’’S 18°25’0’’e

CApe TOwN3 employeeS / eST. 2011

01°17’22’’n 103°51’00’’e

sINGApOre 62 employeeS / eST. 1989

55°45’07’’n 37°36’56’’e

MOsCOw5 employeeS / eST. 2004

37°56’50’’n 23°38’13’’e

pIrAeUs10 employeeS / eST. 2009

RS Platou aSa / annual RePoRt 20106

…SinCe 2003, BuSineSS Booked haS GRown 5-fold and headCount haS Gone fRom aBout 100 to aBout 350 emPloyeeS. almoSt half of

2010 RevenueS and BuSineSS Booked Stemmed fRom oPeRationS that have Been added to the “Platou PoRtfolio” SinCe 2003.

7letteR fRom the ChaiRman

and headcount has gone from about 100 to about 350 employees. Almost half of 2010 revenues and business booked stemmed from operations that have been added to the “Platou portfolio” since 2003.

After 75 years of operations, RS Platou has a rich history and is recognized as a global industry leader, and the Board of Directors and senior management are energized and excited about the group prospects. We are in the early stages of globally reaping the full benefit of synergies from our shipping and offshore broking, finance and investment banking operations. This also goes for continued expansion of the global footprint, where enhanced utilization of our industry expertise and investment placing power should create great values for our customers.

On behalf of the company’s Board of Directors, I would like to extend my gratitude to our clients, employees and shareholders for their continued support, hard work and loyalty. We look forward to working with you and improving our services in 2011.

Yours sincerely,

Ragnar HornChairman

While we were positively surprised by the strength of the economic recovery in 2010, the year offered extraordinary events like the Deepwater Horizon oil spill in the Gulf of Mexico and the “flying ash” from Iceland putting pressure on the world financial markets. In 2011, this “trend” has continued with various natural disasters, the Fukushima nuclear accident and increasing turmoil in the Middle East. However, none of these events have been able to suppress a buoyant world economy and the general optimism of the financial markets. In this context, RS Platou has once again been able to “seize the moment” and is, in the opinion of the Board of Directors, better positioned than ever to capitalize on the prevailing market conditions.

A loss in 2009, due to write-downs and restructuring expenses in RS Platou Markets, was turned around into net income of MNOK 125 in 2010. Along with revenue growth of 19 % and commission reserves approaching record levels, we must be quite satisfied with our overall performance.

The RS Platou Group aspires to be the most reliable and attractive partner for international shipping and offshore companies seeking high value-added brokerage and investment banking services. This requires absolute commitment on our part to invest in the develop-ment and growth of our organization as well as a continuous focus on expansion of our global footprint. Even though this is an ongoing journey, we are quite thrilled about the contributions to date made by various past “counter-cyclical” investments like RS Platou London, RS Platou Markets, The Stewart Group as well as expan-sion of various regional offices.

Today, RS Platou is a very different company compared to what it was a few years ago. Since 2003, business booked has grown 5-fold

GraSpinG opporTuniTieS

leTTer from The chairman

-

RS Platou aSa / annual RePoRt 20108

Key financial fiGureSFigures in NOK 1,000

Income statement

Revenues - Shipbroking - Offshore - Markets - Finance - UnallocatedeBIt before bonus paymentsBonuseseBIt after bonus paymentsnet financial itemsProfit before taxesnet profit - net profit for equity holders of Parent - net profit for non-controlling intereststotal comPRehensIve Income

Balance sheet

non-current assetscurrent assetstotal equitylong-term liabilitiescurrent liabilitiestotal equIty and lIaBIlItIes

Key fIguRes

equity ratio (%) Book value per share (noK) dividend per share (noK)

PRofItaBIlIty

eBIt margin after bonus payments (%)Return on equity (%) ordinary & diluted earnings per share (noK) no. of shares outstanding at 31.12 (in 1,000)Weighted average no. of shares outstanding (in 1,000)

oRganIsatIon

no. of employees at 31.12

563 403 323 825 172 008

- 67 570

- 374 733192 398

182 335 83 419

265 754 213 262 187 071

26 191 175 589

41 904 398 578 231 982

18 321 190 179 440 182

52,7 %5,92,0

151

32,4 %116,7 %

5,5 34 484 33 872

749 634 439 801 208 484

- 101 349

- 526 242 262 008

264 234 31 879

296 113 224 287 191 749

32 538 222 874

58 208 441 503 255 922

21 706 222 083 499 711

51,2 %6,45,1

192

35,2 %91,1 %

5,6 34 021 34 021

919 813 403 683 433 545

6 749 81 584 (5 748)

580 717 251 377

329 340(106 120) 223 220 162 117 146 250

15 867 175 354

275 470 1 314 023

286 593 56 364

1 246 536 1 589 492

18,0 %5,83,0

298

35,8 %70,5 %

4,3 34 021 33 809

837 300 313 980 360 843 108 703

63 635 (9 860)

363 840 271 736 92 103

(138 974) (46 871) (40 907) (12 244) (28 663)

(65 194)

282 630 602 180 206 648

96 950 581 212 884 810

23,4 %4,51,0

312

11,0 %-6,4 %

(0,3) 40 688 35 389

994 117 346 151 356 998 232 998

65 889 (7 918)

500 596276 074

224 522 (43 954)

180 568 120 198 102 075

18 123 121 403

249 663 633 852 285 834 124 859 472 822 883 515

32,4 %6,21,5

346

22,6 %46,6 %

2,5 40 971 40 495

2010 2009 2008 2007 2006

-

key finanCial fiGuReS 9

reVeNUe DeVelOpMeNT

reTUrN ON eqUITy

ebIT

eps ordinary & diluTed

ShiPBRokinG offShoRe inveStment BankinG finanCe unalloCated RevenueS (nok 1,00) eBit maRGin afteR BonuS PaymentS (%)

Roe (%)ePS, oRdinaRy & diluted in nok (%)

20062006

2006 2006

400 000

300 000

200 000

100 000

40 %

30 %

20 %

10 %

8

6

4

2

1 000 000

800 000

600 000

400 000

200 000

125

100

75

50

25

20072007

2007 2007

20082008

2008 2008

20092009

2009 2009

20102010

2010 2010

bUsINess bOOkeD

2006

2 000 000

1 500 000

1 000 000

500 000

2007 2008 2009 2010

fOrwArD bOOk

2006

1 250 000

1 000 000

750 000

500 000

250 000

2007 2008 2009 2010

RS Platou aSa / annual RePoRt 201010

hiSTory–rS plaTou Group expandinG wiTh The marKeTS

11hiStoRy – RS Platou GRouP

1936 1973The Shipbroking Company was established on 1 February 1936 with Ragnar S. Platou as founding partner and Hans T. Gram as junior partner. With three employees in one room, they quickly built a company that took a fair share of the shipbroking business in Norway, thanks to Platou’s reputation and contacts, and Gram’s international experience. At that time, Norway was already one of the big players in international shipping, primarily based on a strong position in tank.

Specialization was key to Platou’s strategy from the start. Instead of just trading tonnage on behalf of the ship owner, the Company used their gained industrial knowledge to take part in sale and purchase of second hand ships and new buildings. They quickly achieved close relations with major ship owners. In the years between start-up and the outbreak of World War II they had a market share between 15 – 20 % in second hand ship trading.

After the war, which naturally became years of martial law for the industry, the company was able to continue the growth of the ship-broking business as the world trade prospered with increasing trade of consumer goods, energy and industrial supplies. There is an unbroken line from the founding fathers “garage firm” to today’s world leading ship broker business with more than 100 brokers worldwide and MNOK 339 in turnover in 2010.

In the spring of 1973, Platou decided to set up its own Offshore Department. The decision came after years with growing involve-ment in the emerging Norwegian oil service industry. In fact, Platou’s participation goes back to 1965, when the Platou Group took part in the establishment of the Norwegian Oil Consortium (NOCO). Together with other key players in Norwegian shipping and industry they decided not to leave the possible adventure at the Norwegian Continental Shelf to American companies. After all, American companies had no experience with harsh sea environment. So they soon saw the advantages with cooperation with local expertise.

From the successful shipbroking business Platou brought the busi-ness model and the network. Recruiting people with engineering knowledge they were soon able to be partners in new building, sale and purchase and trading of supply vessels and oil rigs. It is no exaggeration to say that Platou had a fair share in design, build-ing and financing of important types of both. From the semi-submersible Aker H3, through Trosvik’s BINGO-rigs up to floating deep water rigs and production units, the company has played a key role. Ulstein’s successful UT 704, 705 and 706 is also on the list of key Platou engagements.

With no doubt, Platou’s ability to see the opportunities in the offshore industry very early is key to the company’s position in the industry today. With 85 employees and a turnover of MNOK 357 in 2010 as the company has established itself as a front runner with a global perspective to the offshore industry.

RS Platou aSa / annual RePoRt 201012

1987

1989This year the Singapore office was opened. With 62 employees and a fully diversified business covering all the business areas of Platou, the office is a strong symbol of the true globalization that has taken place in the company.

It was not the first international office in the company’s history. As early as in 1946 a sub-sidiary was set up in New York but was later sold to the local employees. To serve the oil industry better, Platou also established an office in Houston in 1978.

But the Singapore step was different. First, it recognized that sustainable business must

In 1987, the current CEO, Peter M. Anker, with some key partners, chaired a manage-ment buyout operation. Times had changed and the partnership structure had devel-oped as the most viable way for further suc-cess. As a result, 73 % of the shares in the company are now held by employees in the company, while the remaining shares are still with the founding families. This owner-ship model has been vital in attracting and keeping first class talents in the company, optimizing the age distribution among the partners by combining experience of sen-iority and aggressiveness of youth. In the modern competitive world, incentives that give a fair share of the values created over time are demanded by people that dedicate a substantial part of their lives to a business. Platou’s wish to invest in their people cre-ates also the necessary continuity needed for future sustainability. This ownership model is a fundamental part of the success story of Platou in modern times.

be local. Although modern communication makes the world a small place, people still prefer to do business with their neighbors. Hence, to be global you need to be local. Second, the office opening in Singapore was also a recognition of Asia as a major player in the future world.

Following Singapore, a handful of key local offices have been established. Rio de Ja-neiro, Accra, Geneva, Aberdeen, Moscow, Shanghai, Pireus and London is all up and running while Cape Town will be in busi-ness soon. This will surely not be the last piece in Platou’s global puzzle.

13

2004 2008RS Platou Finans was established in 2004. Through the company’s history, the ship & offshore broking business had been closely involved with the financial engineering needed to get the necessary funding for their customers. With the establishment of RS Platou Finans, the company took a formal step into this part of the balance sheet. The company is a specialist in develop ment of projects with limited partnership (KS/DIS). It cooperates with brokers, shipping banks and shipping owners worldwide and can offer clients a broad variety of projects.

In 2009, the division expanded with the establishment of RS Platou Real Estate focusing on structuring real estate projects and corporate finance related to the real estate sector. The two sister companies enjoys several synergies regarding project management and client preferences. Together RS Platou Finance and RS Platou Real Estate provide full scale services with-in project financing, corporate finance and corporate advisory as well as second-ary trading of shares and parts in limited liability project companies.

Following the history of service and geo-graphic expansion, RS Platou decided to acquire 50,01 % of Glitnir Securities AS in October 2008. It was a move desired for years and rendered possible by the overall global financial situation. For RS Platou, this move represented a major investment in the investment banking industry; a huge global industry with one of the greatest financial track records over the past decades. To make the acquisition a success it was important to implement a new strategy for RS Platou Markets and adjust the organization, both to gain control over costs and to lay the foundation for future value creation and profits.

RS Platou Markets changed its strategy in 2009 from being an investment bank with main focus on the retail market to become a corporate- and research driven investment bank with main focus on institutional and professional clients within the core areas of the RS Platou Group – off-shore, E&P and shipping in addition to sea-food where RS Platou Markets traditionally has had strong competence.

RS Platou Markets offers a wide range of services within equity sales and trading, fixed income, research and corporate finance to both domestic and foreign in-stitutional clients and investors. RS Platou Markets has currently approximately 95 employees worldwide and has a profes-sional environment with Norwegian and international competence and a clear strategy for further growth. RS Platou Markets also opened an office in Singapore in early 2009, in order to offer corporate financial advisory services to clients in the Asian shipping, oil service, offshore and E&P sectors. The subsidiary received their license to offer corporate finance advisory services during the year-end of 2010.

Through 75 years of steady business RS Platou has developed from a local ship broker in Norway to a global player; offering shipping and offshore customers a more or less complete range of commercial and financial services. But the goal remains the same: Create success for the customers in good and bad times.

hiStoRy – RS Platou GRouP

RS Platou aSa / annual RePoRt 201014

36%offShore

35%ShipbroKinG

23%inVeSTmenT banKinG

7%projecT finance

sHAre Of reVeNUes

kolumnetittel 15

oVerView of our buSineSS areaS

RS Platou aSa / annual RePoRt 201016

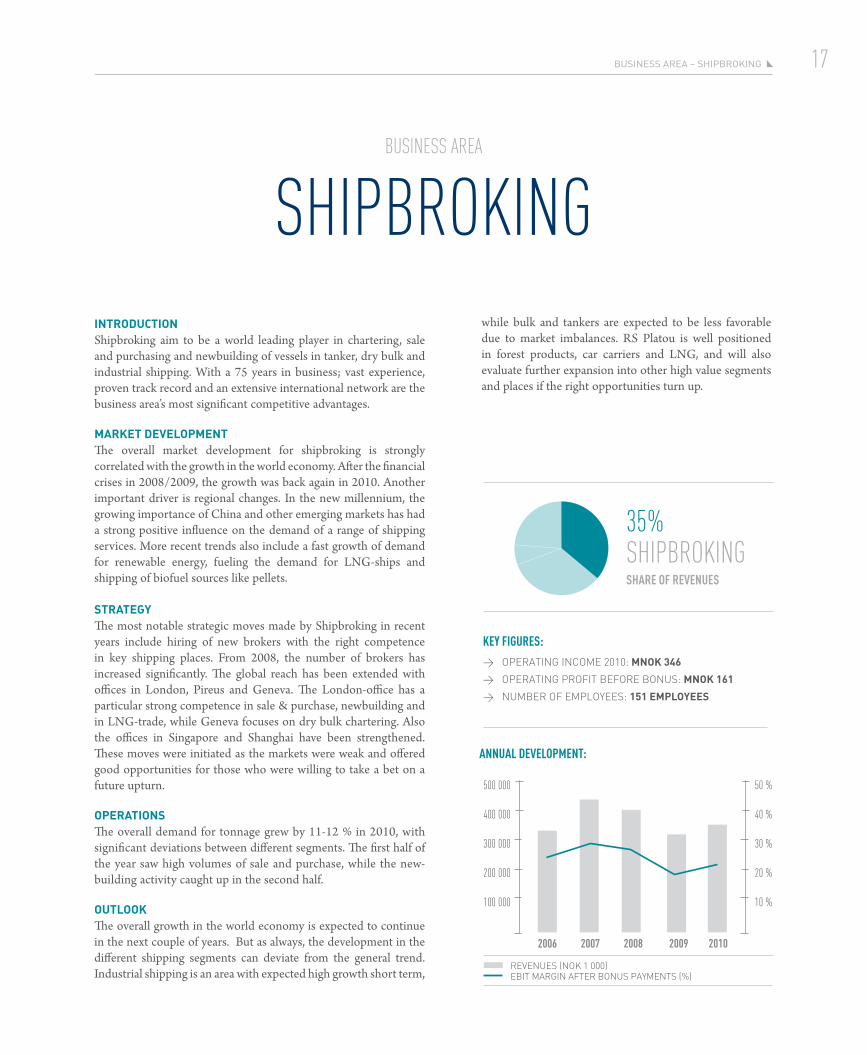

17BuSineSS aRea – ShiPBRokinG

IntRoductIonShipbroking aim to be a world leading player in chartering, sale and purchasing and newbuilding of vessels in tanker, dry bulk and industrial shipping. With a 75 years in business; vast experience, proven track record and an extensive international network are the business area’s most significant competitive advantages.

maRKet develoPmentThe overall market development for shipbroking is strongly correlated with the growth in the world economy. After the financial crises in 2008/2009, the growth was back again in 2010. Another important driver is regional changes. In the new millennium, the growing importance of China and other emerging markets has had a strong positive influence on the demand of a range of shipping services. More recent trends also include a fast growth of demand for renewable energy, fueling the demand for LNG-ships and shipping of biofuel sources like pellets.

stRategyThe most notable strategic moves made by Shipbroking in recent years include hiring of new brokers with the right competence in key shipping places. From 2008, the number of brokers has increased significantly. The global reach has been extended with offices in London, Pireus and Geneva. The London-office has a particular strong competence in sale & purchase, newbuilding and in LNG-trade, while Geneva focuses on dry bulk chartering. Also the offices in Singapore and Shanghai have been strengthened. These moves were initiated as the markets were weak and offered good opportunities for those who were willing to take a bet on a future upturn.

oPeRatIonsThe overall demand for tonnage grew by 11-12 % in 2010, with significant deviations between different segments. The first half of the year saw high volumes of sale and purchase, while the new-building activity caught up in the second half.

outlooKThe overall growth in the world economy is expected to continue in the next couple of years. But as always, the development in the different shipping segments can deviate from the general trend. Industrial shipping is an area with expected high growth short term,

ShipbroKinGbuSineSS area

key fIGUres:

> Operating incOme 2010: mnoK 346

> Operating prOfit befOre bOnus: mnoK 161

> number Of emplOyees: 151 emPloyees

while bulk and tankers are expected to be less favorable due to market imbalances. RS Platou is well positioned in forest products, car carriers and LNG, and will also evaluate further expansion into other high value segments and places if the right opportunities turn up.

35%ShipbroKinG

2006

500 000

400 000

300 000

200 000

100 000

50 %

40 %

30 %

20 %

10 %

2007 2008 2009 2010

ANNUAl DeVelOpMeNT:

sHAre Of reVeNUes

reVenues (nOK 1 000) ebit margin after bOnus payments (%)

RS Platou aSa / annual RePoRt 201018

19BuSineSS aRea – offShoRe

IntRoductIonBeing on of the largest offshore broker in the world, Offshore targets to maintain and strengthen this position in the years to come. RS Platou Offshore’s business covers sale & purchase of drilling, field development and offshore support vessels and new-buildings, as well as chartering. Important competitive factors for RS Platou Offshore include global reads, local presence in the vicinity of all major offshore oil fields, reputation as a highly skilled broker since the opening of the North Sea oil adventure and a solid track record of deals.

develoPment In 2010Two major themes dominated the offshore market in 2010; recov-ery from the financial crises and a temporary setback of this processcaused by the Macondo incident in the Gulf of Mexico. The latter both increased the attention to safety procedures in the industry in general and delayed new drilling permissions in the area. But steady growth in the oil prices and announcements of higher E&P activity into 2011 signals increasing acitivity in the offshore market in 2011/2012.

stRategyExtended global presence and more integration with other Platou services are cornerstones in Offshore’s strategy. The new office in Accra is expected to fuel the West-African business better and through full operation at the Rio de Janeiro office RS PLatou Offshore will be close to an expected hot market in Brasil as Petrobras increases exploration of new fields.

ouR oPeRatIonsThe number of new rig commitments increased from 350 to 500 from 2009 to 2010, which proves a significant recovery of the over-all offshore market. This is also the key driver for offshore supply vessels, but the upturn here was halted by the supply surplus of vessels ordered before the financial crises. But financially, the bottom line for Offshore was healthy.

outlooKThe overall offshore market is expected to grow further in the nextyears, driven by high oil price and increased demand for energy. The drilling market is expected to be strong, and the offshore vesselmarket will gradually improve. Platou’s Offshore business is well positioned to take its share of the new growth, and will take full advantage of a fully operational investment bank in-house.

key fIGUres: > Operating incOme 2010: mnoK 357

> Operating prOfit befOre bOnus: mnoK 233

> number Of emplOyees: 87 emPloyees

36%offShore

2006

500 000

400 000

300 000

200 000

100 000

50 %

40 %

30 %

20 %

10 %

2007 2008 2009 2010

ANNUAl DeVelOpMeNT:

reVenues (nOK 1 000) ebit margin after bOnus payments (%)

offShorebuSineSS area

sHAre Of reVeNUes

RS Platou aSa / annual RePoRt 201020

inVeSTmenT banKinGbuSineSS area

IntRoductIonRS Platou Markets is a Norwegian-based full service investment banking firm, licensed and supervised by the Norwegian Financial Supervisory Authority. RS Platou Markets offers a wide range of services within equity sales and trading, fixed income, research and corporate finance to both domestic and foreign institutional clients and investors within the core sectors E&P, shipping, offshore and seafood. Established in late 2008, RS Platou Markets offer important complementary services to other business areas within the Platou Group.

develoPment In 2010During 2010, the stock markets globally and in Norway rebounded from the financial crisis which severely influenced 2008 and 2009. Despite the rocky start of 2010, the year marked the return of meas-ured confidence for the investment banking industry. While the US was showing good signs of recovery, Asia and the emerging markets continued to play an increasingly important role in global deal making. With companies and corporations holding record amounts of cash, attractive financing opportunities and a growing IPO pipe-line, many factors are in place for the continued momentum into 2011.

RS Platou Markets has in 2010 been retained as advisor in several high profiled equity and debt transactions in Norway, Europe, the US and Asia. In addition, RS Platou Markets has completed several valuation assignments throughout the year, in addition to two stock exchange listings. RS Platou Markets participated in 40 transactions worldwide including fixed income deals, equity offerings, block trades, valuations, acquisitions and listings with a total value of approx. NOK 21 billion.

2010 was a year of restructuring for RS Platou Markets, and the organization was strengthened, including critical support functions. In addition, the business area started up FX trading and estab-lished a presence in Asia through an office in Singapore. Despite restructuring, the business area managed to produce market- leading research, established strong institutional client relationships worldwide and built a leading bond franchise.

key fIGUres: > Operating incOme 2010: mnoK 233

> Operating prOfit befOre bOnus: mnoK 75

> number Of emplOyees: 83 emPloyees

2006

250 000

200 000

150 000

100 000

50 000

100 %

50 %

0

-50 %

-100 %

-150 %2007 2008 2009 2010

23%inVeSTmenT banKinG

ANNUAl DeVelOpMeNT

reVenues (nOK 1 000) ebit margin after bOnus payments (%)

sHAre Of reVeNUes

21BuSineSS aReaS – inveStment BankinG

oPeRatIonsRS Platou Markets offers services within equity sales and trading, fixed income, research and corporate finance. The equity sales team offer a broad range of products and services, including domestic- and international sales, sales trading, market-making and execution. While most of the trading is done on the Oslo Stock Exchange, RS Platou Markets can offer its clients trading in international stock-, derivative- and commodity markets through cooperation with in-dustry partners.

RS Platou Markets professional fixed income team is research driven and focuses on the core industries with a “niche” approach to high yield and convertible issuers in the market. RS Platou Markets are actively structuring, originating, syndicating and trading fixed income instruments and we focus on high yield bonds (secured and unsecured), convertible bonds, mezzanine instruments, pri-vately structured fixed income deals and bridge financing. RS Platou Markets act as advisers to issuers globally, and the team works with major international institutional clients in Europe, Asia and the US.

RS Platou Markets also offer financial advice in all types of ECM transactions, including initial public offerings (IPOs), secondary offer-ings and private placements. In addition, the Corporate finance team advice clients on mergers, acquisitions, divestitures, corporate

restructurings, joint ventures, exchange offers and leveraged buy-outs in order to find optimal solutions enabling them to secure long-term value creation and achieve short and long-term strategic objectives. The research department strives to provide consistent, high quality and timely research to clients and maintain an ongoing coverage of companies covering more than 90% of the market capitalization of the Oslo Stock Exchange with an emphasis of company’s within the core sectors offshore, E&P, shipping and seafood. In addition, research analysts also offer global coverage within the core sectors internationally.

outlooKThe Group shall throughout 2011 continue to utilize the synergy effects with RS Platou within core areas. The approach to the combination of ship- and rig broking and financial services (”steel and paper”) has been appreciated by customers and it is the company’s view that this continued synergy utilization will result in several transactions and other assignments. Including FX ser-vices, the company currently has a service range that covers all our customers’ needs. There are several indications that the Company will have a stronger 2011 than 2010 as a result of improved market conditions and available capital in the market in addition to internal operational improvements and additional strengthening of the organization.

RS Platou aSa / annual RePoRt 201022

IntRoductIonDirect investments in shipping and offshore has long traditions in Norway. The Platou Group decided to focus on this business area in 2004 with the establishment of RS Platou Finance. In 2009 the division expanded with the establishment of RS Platou Real Estate focusing on structuring real estate projects and corporate finance related to the real estate sector.

The two sister companies enjoys several synergies within project development, running management and client preferences. RS Platou Finance and RS Platou Real Estate have become leading players within the Norwegian market for project financing. Both companies have a built up a broad network within banks, investors, ship owners, charterers and real estate players. The division is capable of both establishing projects, syndication of equity and debt capital, restructuring debt, corporate and strategic advisory, company set-ut (both financial and legally)allocation strategies and

managing projects throughout the their life time. At every stage of the process, the ambition is to create maximum value for the clients and investors.

stRategyRS Platou Finance and RS Platou Real Estate are above all a full scale service provider, services including market and projects analysis, project structuring including establishment of KS/DIS structures and limited liability companies, equity capital market and providing all forms of project financing (bank loans, bonds, mezzanine) etc, as well as providing a market place for active secondary trading. RS Platou Finance and RS Platou Real Estate also provide a range of financial services related to asset management and corporate management, besides assisting private individuals with investor services. RS Platou Finance has significant synergies with the shipping and offshore brokerage business – through mutual utilization of client base and networks.

23BuSineSS aRea – PRojeCt finanCe

projecTfinance

buSineSS area

maRKets and oPeRatIonsThe KS/DIS market declined significantly in 2009 and 2010, compared to previous years. While Norwegian investors have previously dominated this market for shipping investments, the demand now comes from international investors. The real estate investors are still dominated by Norwegian players.

Despite a present slow market for new business, the division is managing existing assets with a market value above USD 2,5 billion. This includes more than 110 vessels and offshore units and two real estate properties.

outlooKThe market is expected to improve during the course of 2011, but to remain lower than previous peak years from 2006 to 2008.

key fIGUres: > Operating incOme 2010: mnoK 66

> Operating prOfit befOre bOnus: mnoK 36

> number Of emplOyees: 24 emPloyees

7%projecT finance

2006

125 000

100 000

75 000

50 000

25 000

125 %

100 %

75 %

50 %

25 %

2007 2008 2009 2010

ANNUAl DeVelOpMeNT

reVenues (nOK 1 000) ebit margin after bOnus payments (%)

sHAre Of reVeNUes

RS Platou aSa / annual RePoRt 201024

kolumnetittel 25

corporaTeGoVernance

RS Platou aSa / annual RePoRt 201026

ImPlementatIon of and RePoRtIng on coRPoRate goveRnanceRS Platou aims to follow the Norwegian Code of Practice for Corporate Governance, cf. latest version dated 21 October 2010, and the Board of Directors (the “Board”) have ensured that the Group has implemented sound corporate governance. There are no significant deviations between the Code and Corporate Governance in the Group. Deviations, if any, have been accounted for under each section.

Corporate governance deals with issues and principles associated with the distribution of roles between the governing bodies in the Company, and the responsibility and authority assigned to each body. Good corporate governance is distinguished by responsible interaction between owners, the Board and management in a long-term, productive and sustainable perspective.

Platou has adopted ethical guidelines and guidelines for corpo-rate social responsibility in accordance with the Company’s basic corporate values. In line with the Norwegian code of practice for corporate governance, a review of the major aspects of Platou’s governance structure follows below.

coRPoRate goveRnance PRIncIPlesPlatou aims to create value for its shareholders through deliver-ing first class brokerage services to its clients, mainly within the shipping and offshore industries.

Platou believes there is a link between high quality governance and the creation of shareholder value. Our governance structures and controls help to ensure that we run our business in a profitable manner for the benefit of our shareholders, employees and other stakeholders.

Our basic corporate values for how to conduct our business can be summarized as follows:

ConfidentialityAll employees has a duty to, during the term of employment and after termination, to keep confidentiality towards third parties of all matters the employee has retained knowledge of during the employment, including matters of commercial-, market-, financial and/or internal nature. This also applies to information relating to Platou’s clients and their businesses or business associates. The confidentiality does not apply to matters that has or is made public without the assistance of the employee, nor do the conditions apply to any potential injunctions made by a court or in accordance with law or regulation.

All employees are required to sign a confidentiality agreement that cover the confidentiality between the employee, Platou and towards third parties.

indePendenCeNo one should ever be able to suggest or infer that we do not hold the highest standards of ethics in our daily activities. Everyone in the firm shall act independently, and irrelevant considerations shall never influence the advice or services provided to clients.

All employees shall comply with laws and regulations in force and common practice on a continuous basis. All payments and transfers shall appear in the accounts and systems used and shall be traceable and searchable. No employee shall receive or handle capital that has no named source.

Each employee shall waive any actions that may cause conflict between own personal economical situations and those interests they are to safeguard or ensure being an employee in Platou, or that may be interpreted as such.

loyaltyThe potential for conflict is inherent in our business. To avoid that the loyalty to our clients are questioned, no one shall accept an assignment which may result in a conflict of interest. Each employee shall contribute to the safeguarding of Platou’s trust and reputation by behaving in an ethical and proper way.

CoRPoRate GoveRnanCe 27

inteGRityPlatou is committed to provide first class brokerage services. No one shall accept an amount of work which may comprise the quality of the services provided. No one shall provide services with-in an area which he or she does not master. Each employee shall act factual, correct, honest and in accordance with good business practice. Good business practice is to perform and conduct the relevant work in accordance with ethical and professional principles generally known and practiced by experienced and conscientious persons in the business.

BusIness actIvItIesThe Group’s business activities have been defined in the Articles of Association. The Group’s website also details the Group’s activities, objectives and strategies and in total these should provide both shareholders and the capital market with an understanding of the current business activities of the Group and likely future development.

equIty and dIvIdendsThe Board and the management of the Group aim at all times at keeping the Company’s equity and other financing adapted to the Company’s objective, strategy and risk profile. The Group’s business is of such a nature that modest equity is required to conduct the business, however, the Board continuously evaluates the equity position of the Company.

Platou’s objective is to yield a competitive return on invested capital to the shareholders through a combination of distribution of divi-dends and increase in share price. When evaluating the amount of dividend payable, the Board of Directors places emphasis on certainty, foreseeability and stable development, the Company’s dividend capacity, the requirements for sound and optimal equity capital as well as adequate financial resources to enable future growth and investments, applicable legal or contractual restrictions and the desire to minimize the cost of capital. The Company will pay dividends directly to the VPS Registrar, which has undertaken, in turn, to distribute the dividends to the beneficial shareholders as registered in VPS.

To ensure flexibility in the Group’s capital structure and capital management, the Board of Directors has been granted authorisa-tion to repurchase own shares by the Annual General Meeting. The General Meeting has authorised the Board of Directors to acquire own shares for a total face value of NOK 1 024 279, corresponding to 10 % of the Company’s share capital. In addition, the Board of Directors has been authorized to increase the share capital of the Company by NOK 1 024 279 by issuance of new shares. Both of the above mentioned authorizations are valid until the next annual general meeting in 2012.

equal tReatment of shaReholdeRs and tRansactIons WIth close assocIatesThere is only one class of shares, and all shares are equal in all respects.

The Board will take into account the interest of all the shareholders of the Group and treat all shareholders fairly. All transactions that are not immaterial between the Company and a shareholder, a director or senior manager of the Company (or related parties to such persons) will be subject to a valuation from an independent third party. The directors and senior management shall notify the Board if they have any material direct or indirect interest in any transaction entered into by Platou. The Group has not entered into any transactions or other agreements with shareholders, members of the Board or management outside the normal scope of business, and during 2010 no material transactions with shareholders, members of the Board or management occurred.

As a deviation from the Code, the Company’s corporate governance principles states that any transactions the Company carries out in its own shares, pursuant to the shareholder agree-ment entered into with the working partners, may be carried out at other prices than prevailing stock exchange prices. Furthermore, such transactions, pursuant to the shareholder agreement en-tered into with the working partners, can be carried out without obtaining a valuation by a third party.

In cases where a share capital increase is to be carried out which involves waiver of the pre-emption rights of existing shareholders,

RS Platou aSa / annual RePoRt 201028

and the board resolves to carry out such an increase on the basis of an authorisation granted by the general meeting, the Company should explain the justification for waiving the pre-emption rights in the public announcement to be issued in connection with the increase in share capital.

fReely negotIaBle shaResThere are no restrictions on trading of the Company’s shares in the Articles of Association.

In order to maintain stability, loyalty and long term value creation, in the interest of all shareholders, a shareholder agreement exists between the Company and working partners which include restric-tions on negotiability.

geneRal meetIngsThe shareholders exercise the supreme authority in Platou through the general meetings. The Annual General Meeting (the “AGM”) of Platou will be held each year prior to the end of June. The AGM shall approve the annual accounts and report as well as the distribu-tion of dividend, and otherwise make such resolutions as required under applicable law.

The Board of Directors may convene extraordinary general meetings whenever it deems necessary or when otherwise legally required. Platou’s auditor and any shareholder or group of shareholders representing more than 5% of the current issued and outstand-ing share capital of Platou may require that the Board of Directors convene an extraordinary general meeting.

The Board adheres to the requirements of the Norwegian code of practice for corporate governance with respect to the summons to the General Assembly. The Board summons the meeting and make the supporting information on the resolutions to be considered at the general meeting available on the company’s website no later than 21 days prior to the date of the general meeting. In addition, the Board send notices of general meetings to shareholders no later than three weeks prior to the meeting and will observe that the notice and any supporting material are sufficiently detailed and comprehensive.

Any deadline for shareholders to give notice of their intention to attend the meeting shall be set as close to the date of the meeting as possible.

The Board shall make arrangements to ensure an independent chairman for the general meeting. The Board and the person chair-ing the meeting shall arrange for the general meeting to vote sepa-rately on each candidate nominated for election to the Company’s corporate bodies, and further ensure that members of the Board and the nomination committee and the auditor are present at the general meeting.

Shareholders who are unable to attend may vote by proxy. The Company shall in this respect: ■ provide information on the procedure for representation at the

meeting through a proxy; ■ nominate a person who will be available to vote on behalf of

shareholders as their proxy; and ■ prepare a form for the appointment of a proxy, which to the

extent possible allows separate voting instructions to be given for each matter to be considered by the meeting and for each of the candidates nominated for election.

nomInatIon commItteeThe nomination committee’s duty is to nominate candidates to the AGM for the election of the Board and to propose the fees to be paid to members of the Board. The nomination committee shall justify its recommendations.

Platou has a nomination committee and the general meeting shall elect the chairperson and members of the nomination committee and shall determine the committee’s remuneration.

The nomination committee is stipulated in the Company’s Articles of Association. The general meeting shall stipulate guidelines for the duties of the nomination committee.

The nomination committee shall be composed in a way that takes into account the interests of all the Company’s shareholders in general. At least one member of the nomination committee shall

CoRPoRate GoveRnanCe 29

not be a member of the Board. No more than one member of the nomination committee shall be a member of the Board. The nomi-nation committee shall not include the Company’s CEO. Due to the composition of shareholders in the Company, the Board has resolved certain deviations from the Code with respect to how the nomination committee shall be composed, namely:

(i) A majority of the committee does not have to be independent of the Board and the executive management;(ii) Up to one member of the committee may be a member of the Board, and such member may offer himself for re-election; and(iii) The committee may include executive personnel, except the Company’s CEO.

The current nomination committee consists of Jørgen Lund (Chair-man), Ragnar Horn (member) and Wilhelm L. Holst (member). The current nomination committee has one independent member, one member who is also a member of the Board, and one member who is also part of the Company’s executive management.

Platou shall provide information on the members of the committee and any deadlines for submitting proposals to the committee.

coRPoRate assemBly and WoRK of BoaRd of dIRectoRs: comPosItIon and IndePendencePlatou does not have a corporate assembly. The composition of the Board ensures that the Board can attend to the common interests of all shareholders and meet the Company’s need for expertise, capacity and diversity. Attention is paid to ensuring that the Board can function effectively as a collegiate body. The composition of the Board ensures that it can operate independently of any special interests.

The Board consist of five directors, of which two are female direc-tors. The majority of the shareholder-elected members of the Board are independent of the Company’s executive management and material business contacts. The two members of the Board elected by shareholders are independent of the Company’s main shareholders and the Board does not include executive management.

The chairman of the Board has been elected by the general meeting. The term of office for members of the Board is not longer than two years at a time.

The annual report shall provide information to illustrate the exper-tise of the members of the Board, and information on their record of participation in board meetings. A comprehensive biography of the Board of Directors and the Executive Management is also available on Platou’s web pages.

the WoRK of the BoaRd of dIRectoRsThe Board of Directors works in accordance with the rules laid down by Norwegian law.

Annually, in connection with the first board meeting in each calendar year, the Board evaluates its performance in the previous year. The evaluation includes its own performance, the performance of the sub-committees and the performance of the individual directors. In order for the evaluation to be effective, the Board sets objectives, on both a collective and individual level, against which their perfor-mance can be measured. The results of this evaluation are not made available to the public, but only to the Nomination Committee.

In order to ensure a more independent consideration of matters of a material character in which the chairman of the Board is, or has been, personally involved, the Board’s consideration of such matters will be chaired by some other member of the Board. The division of responsibilities between the Board and the CEO has been set out in writing and agreed by the Board.

The Company has established an audit committee, the duties of which are to carry out preparatory work for the Board with respect to monitoring the financial reporting, monitor the Company’s systems for internal control and risk management, maintain regular contact with the Company’s elected auditor, and review the independence of the statutory auditor.

RS Platou aSa / annual RePoRt 201030

RIsK management and InteRnal contRolThe Board works to be continuously updated on the financial situ-ation of the Company and ensures that the Company’s operations, accounting and asset management have satisfactory control, and the directors of the Board have full and free access to officers, employees and the books and records of the Company. The Board ensures that the CEO reports monthly to the Board on the financial situation of the Company. The Board also carries out an annual review of the Company’s most important areas of exposure to risk and its internal control arrangements, which encompass the Company’s corporate values, ethical guidelines and guidelines for social responsibility.

RemuneRatIon of the BoaRd of dIRectoRsThe remuneration of the members of the Board of Directors is determined by the shareholders in a general meeting and disclosed in the annual accounts of Platou, cf. note 4. Based on the consent of the AGM, it is assumed that the remuneration of Board members reflects the respective members’ responsibility, expertise, time commitment and the complexity of the Group’s activities. This remuneration is not linked to Company’s results.

The directors of the Board (the “Directors”), or companies to which they are associated, have not accepted other appointments or engagements for the Company. The Directors have not received shares, nor have they been granted share options, as part of their remuneration as directors.

RemuneRatIon of executIve PeRsonnelThe Board has adopted guidelines for remuneration to management employees. The general meeting is informed of the guidelines annually. Salary and other remunerations to the CEO is determined by the Board. All elements of remuneration to the CEO and the total remuneration for management appear in the annual report, cf. note 4. Performance-related remuneration of the executive management in the form of share options, bonus programmes etc. is linked to value creation for shareholders. As a deviation from the Code, the Board has resolved not to include an absolute limit on performance related remuneration in the Company’s corporate governance policy.

InfoRmatIon and communIcatIonAll Group financial reporting complies with Norwegian legislation. The financial statements and annual reports are prepared to ensure accountability, transparency and fairness to all shareholders in the Group.

A financial calendar will be prepared and published on the Group website and is also distributed in accordance with the rules of the Public Companies Act and the rules applicable to companies listed on the Oslo Stock Exchange. All the information distributed to the shareholders is also published on the Group website. The Group will have regular investor meetings and public interim results presenta-tions.

The Board considers that these measures enable and ensure continuous informative interaction between the Company and the shareholders.

The Directors make themselves available for discussions with the major shareholders from time to time to develop a balanced under-standing of the issues and concerns of such shareholders, subject always to applicable law and listing rules. Information given to the Company’s shareholders shall simultaneously be made available on the Company’s web site.

taKe-oveRsThere are no limitations with respect to the purchase of shares in the Company. In the event of a take-over bid the Board of Directors will act in the best interest of the shareholders and in compliance with all rules and regulations applicable in such an event. In the case of a take-over bid the Board will refrain from taking any obstructive action unless agreed upon by the Company’s shareholders.

In a bid situation, the Board and management have an independent responsibility to help ensure that shareholders are treated equally, and that the Company’s business activities are not disrupted unnecessarily. The Board has a particular responsibility to ensure that shareholders are given sufficient information and time to form a view of the offer.

CoRPoRate GoveRnanCe 31

The Board will not seek to hinder or obstruct take-over bids for the Company’s activities or shares unless there are particular reasons for this.

In the event of a take-over bid for the Company’s shares, the Board will not exercise mandates or pass any resolutions with the intention of obstructing the take-over bid unless this is approved by the general meeting following announcement of the bid.

If an offer is made for a Company’s shares, the Board shall issue a statement making a recommendation as to whether shareholders should or should not accept the offer. The Board’s statement on the offer shall make it clear whether the views expressed are unanimous, and if this is not the case it shall explain the basis on which specific members of the Board have excluded themselves from the Board’s statement. The Board shall arrange a valuation from an independent expert. The valuation shall include an explanation, and shall be made public no later than at the time of the public disclosure of the Board’s statement.

Any transaction that is in effect a disposal of all, or a substantial part of the Company’s assets, shall be decided by a general meeting.

audItoRThe Company’s auditor shall be elected by the shareholders at the general meeting.

The auditor shall submit the main features of the plan for the audit of the Company to the Board annually.

The auditor shall participate in board meetings that deal with the annual accounts. At these meetings the auditor shall review any significant changes in the Company’s accounting principles, assess any important accounting estimates and matters of importance on which there has been disagreement between the auditor and the management.

The auditor shall at least once a year present to the Board a review of the Company’s internal control procedures, including identifying weaknesses and proposed improvements.

The Board shall hold a meeting with the auditor at least once a year at which neither the CEO nor any other representative of the management is present.

The Board shall specify guidelines for the right of the management to use the auditor for purposes other than auditing. The Board shall provide recommendations to the general meeting for the election, removal and payment of auditors.

The Board must inform the shareholders at the AGM of the remuneration paid to the auditor, including details of the fee paid for auditing work and any fees paid for other specific assignments.

RS Platou aSa / annual RePoRt 201032

kolumnetittel 33

board of direcTor´SreporT for 2010

RS Platou aSa / annual RePoRt 201034

postponements and cancellations. Only around two-thirds of the planned newbuilds scheduled for delivery were launched during 2010. This enabled utilisation rates to once more increase to more comfortable levels and charter rates to remain acceptable at least for the first half of the year. The level of newbuild orders placed during 2010 took many by surprise as the yards saw order intakes close to treble 2009 levels. It has also been a relief to see that the ro-ro and container sectors have picked up from depressed levels.

For Markets, the trading environment kept improving during the year. However concerns related to sovereign debt in Europe and the overheating of the Chinese economy caused disturbances during the year. Towards the end of 2010, monetary policies throughout Europe eased markets and helped to ensure that economic growth stayed on track. In sum for Markets, 2010 was a fair trading year, and this is reflected in the financial results for the division.

For Finance, the year 2010 was more or less as expected. The main focus was on existing projects and the need to pilot investors through difficult market conditions. Despite a few challenges, the majority of the project portfolio performed well and a few projects were added to the portfolio within dry bulk, tankers and offshore.

For all divisions, an ongoing focus on existing client relationships is essential to preserving our strong market position and continual efforts are made to increase our client base.

In 2010, business booked for the Group was MNOK 1 152,7, representing a 90 % increase from 2009. Shipbroking was the largest contributor with MNOK 512,3, followed by MNOK 345,5 in Offshore, MNOK 233,8 in Markets and MNOK 61,1 in Finance.

Income statementTotal revenues for the Group were MNOK 994,1 in 2010 an increase of 19 % from 2009 revenues of MNOK 837,3.

Shipbroking revenues improved from 2009 mainly due to the es-tablishment of the London and Piraeus offices during 2009. During the first half of 2010, sale and purchase volumes were high, while the second half of the year saw more newbuilding activity. For 2010, revenues generated by the forward book were relatively less important than in 2009.

IntRoductIonThe RS Platou Group is a leading international ship and offshore broking and investment banking group. The Group has four divisions: ■ Shipbroking ■ Offshore ■ Markets ■ Finance

Through Shipbroking and Offshore, the Group serves the shipping and offshore industry worldwide by providing services within chartering, sale and purchase and contracting of ships and offshore units. Through Finance, equity and debt capital is syndicated for shipping, offshore and real estate projects. The investment bank, Markets, offers financial advisory services within brokerage, corporate finance and bond issues for both Norwegian and international clients. RS Platou Markets AS is authorised by the Norwegian Financial Supervisory Authority (Finanstilsynet). It is licensed to offer services within equity sales and trading, fixed income, research and corporate finance to domestic and foreign clients and investors. The Group’s head office is in Oslo, with regional offices in Singapore, Houston, Aberdeen, London, Rio de Janeiro, Moscow, Geneva, Accra, Shanghai and Piraeus.

In accordance with the Accounting Act § 3-3a, we confirm that the financial statements have been prepared under the assumption of going concern. This assumption is based on profit forecasts for the year 2011 and the Group’s long-term strategic forecasts. The Group’s economic and financial position is sound.

oPeRatIons In 20102010 was predicted by many to be a difficult year for the shipping and offshore industries. However, higher than expected global economic activity resulted in a better year than initially anticipated for the Group. Offshore has been through a dramatic year of con-trasts with renewed optimism for jack-ups and semis, turbulent market conditions for offshore support vessels and the tragic Deepwater Horizon accident. Exciting areas and projects such as the offshore activities in Brazil keep driving demand for the exist-ing offshore fleet. At the same time, the industry is continuing to invest in new technology to meet the increased demands generated by both complex challenges and regulatory requirements. As for offshore, yards producing shipping tonnage also had to report order

35BoaRd of diReCtoRS

AS and RS Platou LLP and constituted MNOK 18,1, up from MNOK -28,7 in 2009. The non-controlling interests in 2009 was influenced by the loss attributable to non-controlling interest in RS Platou Markets AS.

Profit attributable to owners of the parent in 2010 was MNOK 102,1 compared with MNOK -12,2 in 2009. This represents an earnings per share of NOK 2,52 in 2010 and NOK -0,35 in 2009.

fInancIal PosItIonIn the opinion of the Board of Directors, the Group’s financial position is sound. Total assets amounted to MNOK 883,5, of which MNOK 249,7 are non-current and primarily relate to a deferred tax asset generated by historical losses in RS Platou Markets AS, PPE and goodwill generated through acquisitions. Total current assets of MNOK 633,9 exceed total current liabilities of MNOK 472,8. Total current assets primarily consist of accounts receivable and cash. The total cash position has increased from MNOK 158,0 at 31 December 2009 to MNOK 280,7 at 31 December 2010. The Group had long term liabilities of MNOK 124,9 at 31 December 2010, compared to MNOK 97,0 at 31 December 2009.

Total equity has increased by 38,3 % to MNOK 285,8 from 2009. The Group’s equity ratio was 32,3 % at 31 December 2010, up from 23,4 % at 31 December 2009.

RS Platou Markets AS had a tier 2 capital ratio of 20,26 % at 31 December 2010 compared to the requirement set by the Financial Supervisory Authority of Norway of a tier 2 capital ratio in excess of 8 %.

The Group’s cash flow from operations was MNOK 171,8 in 2010, up from MNOK -6,9 in 2009. The Group has sufficient cash to finance the existing operations of the Group. Due to fluctuating working capital requirements during the year, the Group has estab-lished overdraft facilities. These facilities were utilised from time to time during the year, but were not utilised on a net basis at year-end.

The main differences between the operating profit and net cash flow from operating activities are primarily related to net financial income, taxes paid, non-cash items recognised in profit or loss, change in working capital and certain other capitalized items not included in cash flow from investing activities.

Offshore saw a relatively modest increase in revenues. It was a difficult year, still influenced by delays and cancellations especially at yards in the Far East, but both sale and purchase and charter-ing activities generated higher revenues than expected. During the spring of 2011, the offshore office in Lagos will be closed, while a new subsidiary has been established in Accra, Ghana, to serve the West African offshore chartering market.

Markets more than doubled its revenues from 2009. Active equity and debt capital markets, combined with opportunities for initial public offerings and stock exchange listings, contributed to the growth in revenues. Several high profile transactions were completed during 2010 for international clients, underpinning Market’s ambitions to build on the Group’s global reach.

Finance saw 2010 revenues slightly higher than in 2009 which is satisfactory as 2010 was still influenced by difficult market condi-tions. A few new projects were added to the portfolio in 2010, and revenues from the real estate team contributed positively to the division.

Operating expenses for 2010 were MNOK 493,5. This included non-recurring costs of about MNOK 34 primarily related to the restructuring of Markets and the write off of capitalised sign-on fees. For 2009, the non-recurring costs were MNOK 81. Excluding non-recurring costs underlying operating expenses increased by 4 % from MNOK 441,0 in 2009 to MNOK 459,5 in 2010. The mod-est increase in costs is primarily related to increased head count during the year.

In line with the long established practice within the Group, MNOK 276,1 has been allocated for bonuses. The allocation is based on operating profit before bonus.

Net financial income improved from MNOK -139,0 in 2009 to MNOK -44,0 in 2010. Net financial income is volatile from period to period because it mainly comprises exchange rate fluctuations.

Profit before tax was MNOK 180,6 in 2010, which is a signifi-cant improvement from MNOK -46,9 in 2009. Profit after tax was MNOK 120,2 in 2010, and MNOK -40,9 in 2009. The non- controlling interests for 2010 primarily relate to RS Platou Finans

RS Platou aSa / annual RePoRt 201036

The Board of Directors has developed appropriate procedures to manage the Group’s short, medium and long-term funding and liquidity management requirements. Risk is managed by maintaining adequate borrowing facilities and by the regular monitoring of fore-cast and actual cash flows. Liquidity risk arises from the Group’s ongoing financial commitments and obligations, particularly the settlement of financial liabilities.

management, emPloyees and envIRonmental InfoRmatIonAt 31 December 2010, the Group employed 89 women and 257 men, totalling 346 employees. The Group is committed to giving men and women equal opportunities for professional and personal development, compensation and benefits, and general career develop ment. Women occupy important positions throughout the Group. The parent company’s Board of Directors consists of three men and two women, while senior management consists of six men. Throughout the Group, continual efforts are made to secure equality between genders, and under no circumstances will gender, ethnicity, religion, nationality or other criteria not relevant to a position be used when evaluating existing employees or consider-ing potential new employees. In general, the Board of Directors considers the Group’s working environment to be good. Absence due to sickness in RS Platou ASA of 1,5 % in 2010 and 1,2 % in 2009 is considered to be low. However continual efforts are still made to reduce the absence due to sickness.

The Group has a direct impact on the environment through its consumption of energy, procurement of goods, transport and waste management. However, the impact is considered to be normal and not material as operations of the Group are primarily related to office operations.

PRosPects foR the futuReIn recent years, RS Platou has spent significant resources on developing its service offering platform and the Group will continue to focus on cross border and cross service synergy realisation. The Board notes with satisfaction that the realised synergies in the Group have so far exceeded expectations. Further expansion, both in our present locations and possibly into some new locations will have strategic priority in 2011. The revenue levels in the Group are dependent upon the general development of the world economy in general, and the shipping and offshore markets

The consolidated statement of comprehensive income, and the consolidated statement of financial position dot not include oper-ating costs or capitalised costs related to research and development (R&D) as the Group has no material R&D activities.

RIsKsThe Board of Directors has overall responsibility for setting up and monitoring the Group’s risk management framework. Risk manage-ment policies are established to identify and analyse the risks faced by the Group, to implement appropriate controls over those risks and to monitor these risks and the effectiveness of the controls. Risk management policies and systems are reviewed regularly to take into account changes in market conditions and the Group’s policies. There may be deviations in the policies across the various subsidiaries within the Group.

Fluctuations in exchange rates may affect both the consolidated statement of comprehensive income and the consolidated statement of financial position. In terms of revenues, the main exposure is in USD, however, the Group also has income in NOK, EUR and GBP amongst other currencies. Most expenses are in NOK, although the Group also has significant expenses in GBP, USD and SGD. The Group may decide to use foreign currency swaps or forward exchange contracts to hedge its future exchange rate exposure.

Market risk is the risk that changes in market prices will affect the Group’s results or the value of its financial instruments, or that the development in the demand for the Group’s services changes. The objective of market risk management is to manage and control market risk exposures within acceptable limits, but also to optimise the returns available.

Credit risk is the risk of financial loss to the business if a customer or counterparty to a financial instrument fails to meet its contractual obligations. This arises principally from the Group’s receivables from its clients. Exposure to credit risk on trade receivables is monitored on a routine basis and credit evaluations are performed on clients before entering into significant transactions. Risk is managed by maintaining close contact with each client and carry-ing out regular billing and cash collection for services provided. The Group makes impairment provisions for estimated losses on of trade and other receivables on a case by case basis.

37BoaRd of diReCtoRS

in particular. The Group will strive to increase the market share across its divisions, however, price levels and absolute transaction volumes are difficult to predict. Operating cost visibility is fair, and given the expansion plans for the Group, it is likely that operating cost levels will increase.

In February 2011, The Court of Appeal gave a judgment in favour of RS Platou Markets AS in relation to a lawsuit filed by BNbank ASA, further details are included in Note 22 – Contingent liabilities. Since year-end, no other matters have arisen which have a mate-rial effect on the Group’s consolidated statement of comprehensive income, nor the consolidated statement of financial position. The same is true for the parent company.

shaReholdeRs and allocatIon of PRofItRS Platou ASA had 72 shareholders at 31 December 2010. The Board of Directors proposes that the following allocation of RS Platou ASA’s profit after tax to be adopted at the annual general meeting:

fiGuReS in nok 1.000

PRofit afteR tax 54 386

dividend -61 457

to otheR equity -7 071

The allocation is based on dividends of NOK 1,50 per share, which is in line with the policy of a maximum payout to shareholders provided that equity and working capital are adequate. RS Platou ASA will have distributable equity of MNOK 126,3 if the above allocation is adopted by the annual general meeting.

Oslo, 22 March 2011

Ragnar Horn (Chairman) Birger Nergaard

Marianne Lie Gustave Brun-Lie

Marianne Aamodt Peter M. Anker (CEO)

RS Platou aSa / annual RePoRt 201038

kolumnetittel 39

conSolidaTed financialSTaTemenTS for 2010

40 RS Platou aSa / annual RePoRt 2010

note 2010 2009

oPeRatinG RevenueS 3 992 250 836 601

otheR RevenueS 3 1 867 699

ToTal revenues 994 117 837 300

SalaRieS and PayRoll CoStS 4,18 289 751 282 917

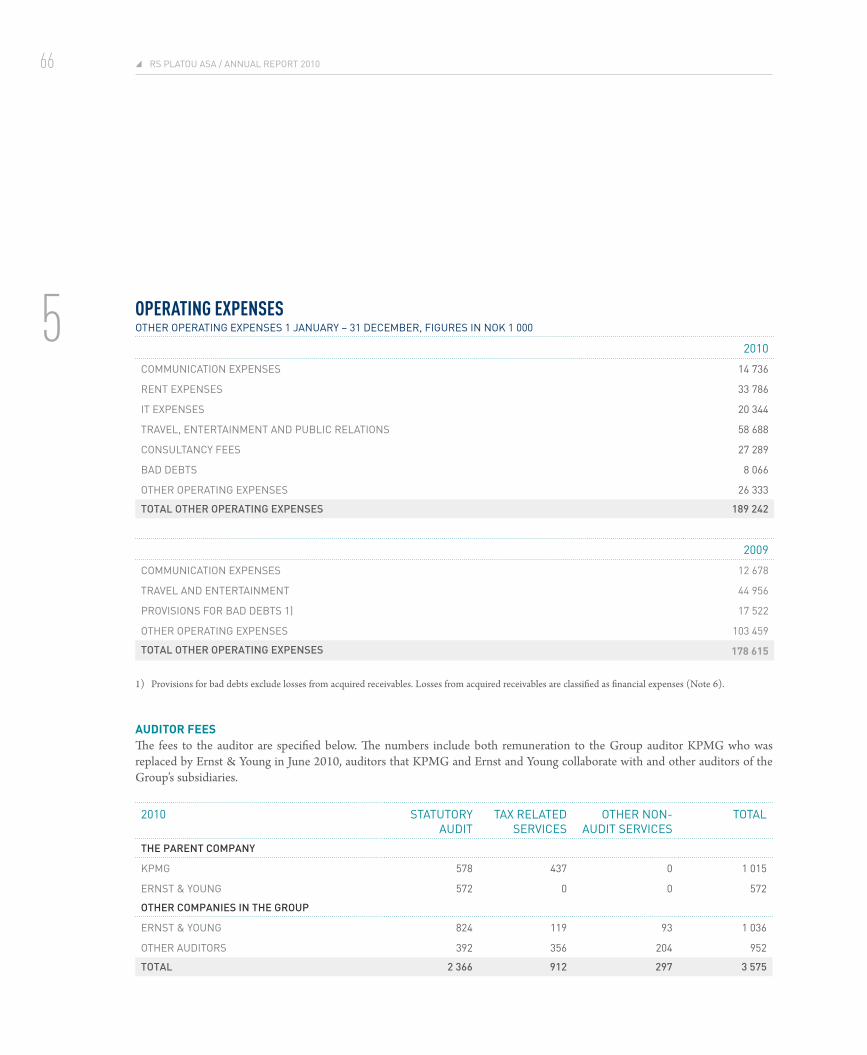

otheR oPeRatinG exPenSeS 5 189 242 178 615

dePReCiation and imPaiRment of tanGiBle aSSetS 9 13 774 10 097

amoRtiSation and imPaiRment of intanGiBle aSSetS 10 754 1 832

operaTing expenses before bonuses 493 521 473 460

operaTing profiT before bonuses 3 500 596 363 840

BonuSeS 4 276 074 271 736

operaTing profiT 3 224 522 92 103

inteReSt inCome 6 10 983 25 029

otheR finanCial inCome 6 3 521 86 828

inteReSt exPenSeS 6 -13 031 -25 657

otheR finanCial exPenSeS 6 -44 431 -226 421

ShaRe of PRofit fRom aSSoCiated ComPanieS 6,11 -996 1 246

neT financial income/expenses -43 954 -138 974

PRofIt BefoRe tax 180 568 -46 871

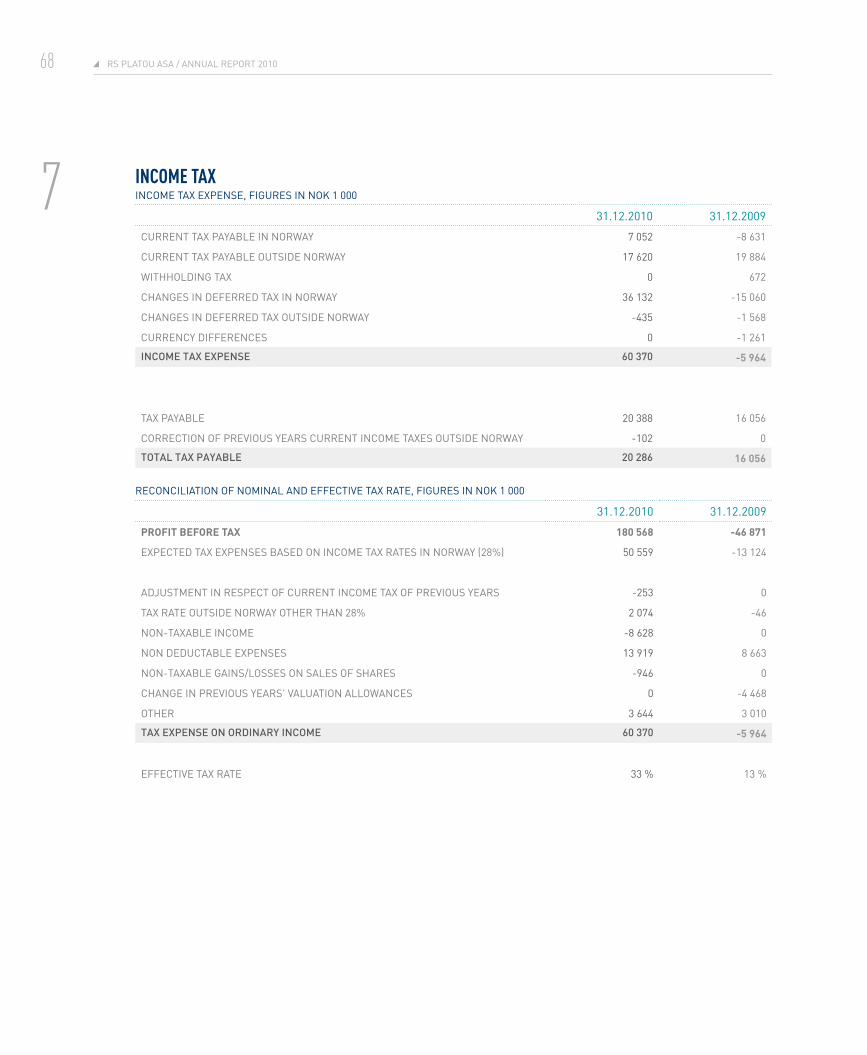

inCome tax exPenSe 7 60 370 -5 964

profiT afTer Tax 120 198 -40 907

oTher comprehensive income 2010 2009

exChanGe Rate diffeRenCeS 1 205 -24 287

ToTal comprehensive income for The Year 121 403 -65 194

CONsOlIDATeD sTATeMeNT Of COMpreHeNsIVe INCOMe1 januaRy – 31 deCemBeR, fiGuReS in nok 1 000

41ConSolidated finanCial StatementS

profiT afTer Tax for The Year aTTribuTable To: 2010 2009

equity holdeRS of the PaRent 102 075 -12 244

non-ContRollinG inteReStS 18 123 -28 663

ToTal profiT afTer Tax for The Year 120 198 -40 907

ToTal comprehensive income aTTribuTable To: 2010 2009

equity holdeRS of the PaRent 102 938 -35 893

non-ContRollinG inteReStS 18 465 -29 301

ToTal comprehensive income for The Year 121 403 -65 194

earnings per share 2010 2009

oRdinaRy 8 2,52 -0,35

diluted 8 2,52 -0,35

42 RS Platou aSa / annual RePoRt 2010

note 2010 2009

asseTs

non-currenT asseTs

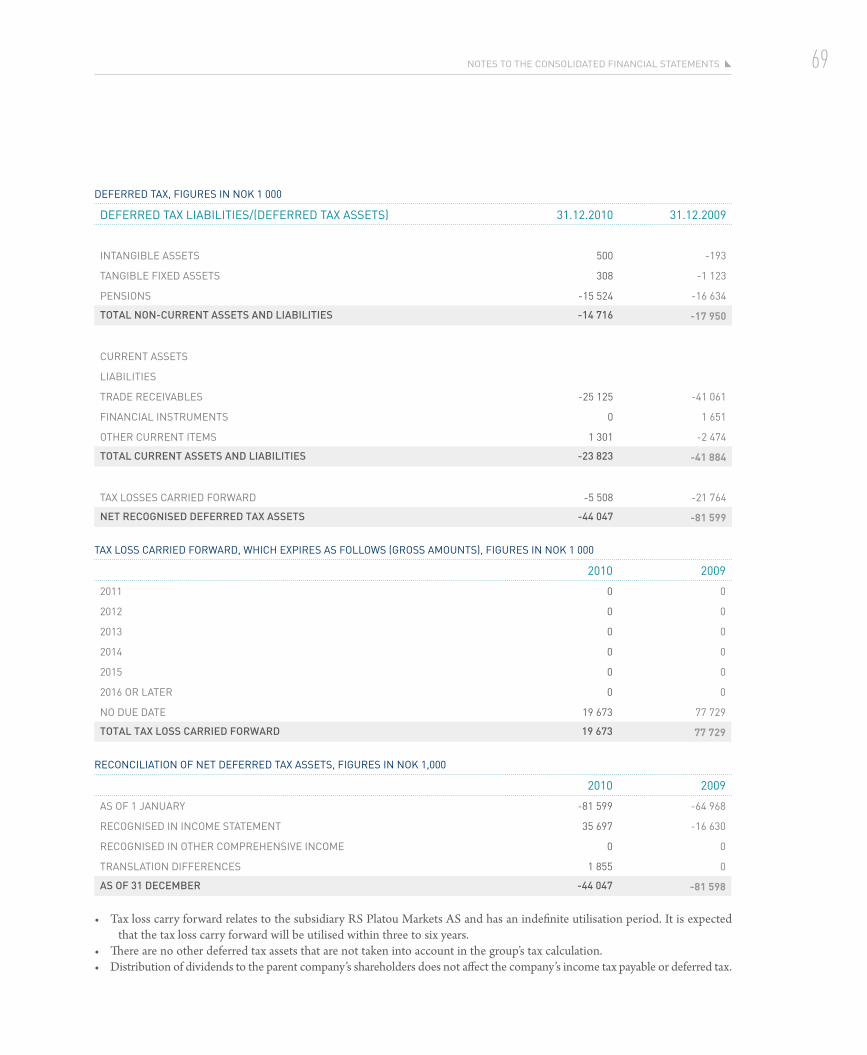

defeRRed tax aSSetS 7 44 047 81 599

PRoPeRty, Plant and equiPment 9 55 473 49 786

intanGiBle aSSetS 10 140 976 141 274

lonG-teRm ReCeivaBleS 6 991 6 919

finanCial inveStmentS 2 177 2 060

inveStmentS in aSSoCiateS 11 0 992

ToTal non-currenT asseTs 249 663 282 630

currenT asseTs

aCCountS ReCeivaBle 12,19 264 351 374 316

otheR ShoRt-teRm ReCeivaBleS 13,19 66 208 46 830

finanCial inveStmentS 14,19 22 577 22 989

CaSh and CaSh equivalentS 15,19 280 715 158 046

ToTal currenT asseTs 633 852 602 180

ToTal asseTs 883 515 884 810

CONsOlIDATeD sTATeMeNT Of fINANCIAl pOsITIONaSSetS aS at 31 deCemBeR, fiGuReS in nok 1 000

43ConSolidated finanCial StatementS

note 2010 2009

equiTY

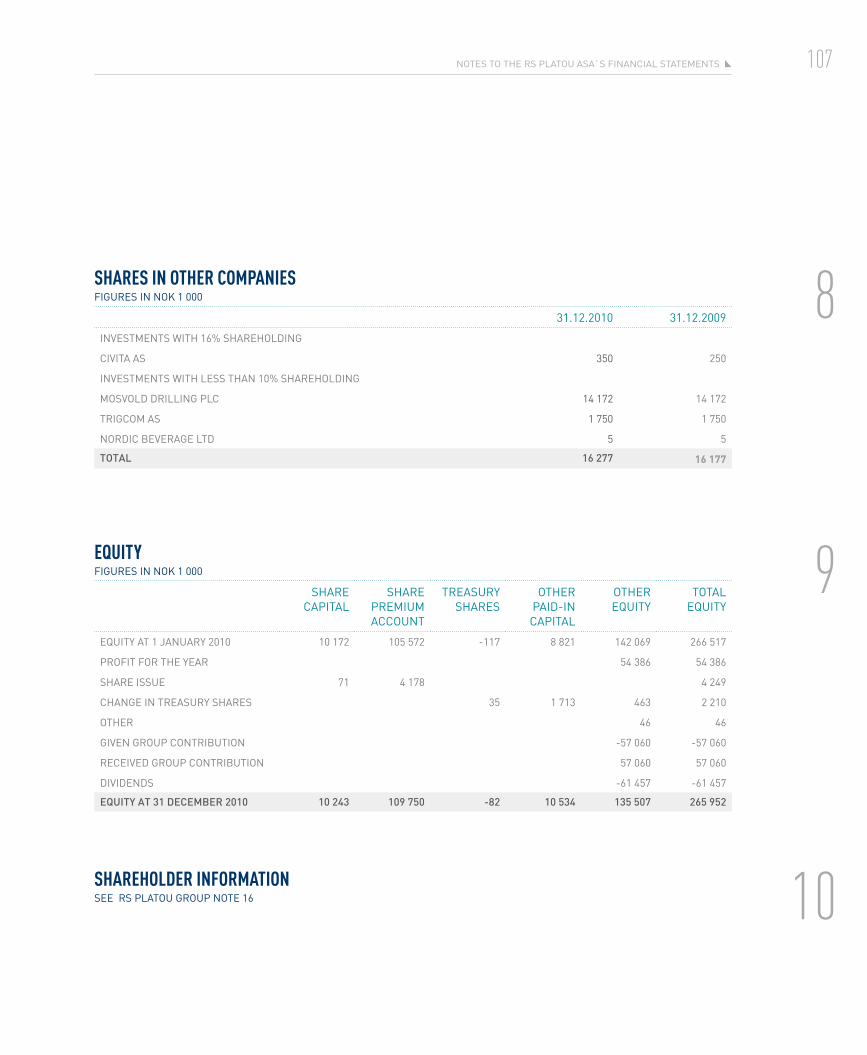

ShaRe CaPital 16 10 243 10 172

ShaRe PRemium aCCount 109 750 105 572

tReaSuRy ShaReS 16 -82 -117

otheR Paid-in CaPital 16 10 534 8 821

ToTal paid-in capiTal 130 444 124 448

reTained earnings

otheR equity 124 362 59 045

ToTal reTained earnings 124 362 59 045

non-contRollIng InteRests 31 028 23 155

ToTal equiTY 285 834 206 648

long-Term liabiliTies

lonG-teRm inteReSt-BeaRinG liaBilitieS 17 78 244 54 097

PenSion liaBilitieS 18 46 616 42 853

ToTal long-Term liabiliTies 124 859 96 950

currenT liabiliTies

inteReSt-BeaRinG liaBilitieS due to CRedit inStitutionS 17 13 495 50 000

otheR inteReSt-BeaRinG liaBilitieS 17 63 746 0

aCCountS PayaBle 19 57 225 197 229

taxeS PayaBle 7 20 286 16 056

finanCial inStRumentS 19 0 5 895

otheR CuRRent liaBilitieS 19 318 069 312 031

ToTal currenT liabiliTies 472 822 581 212

total lIaBIlItIes 597 681 678 162

ToTal equiTY and liabiliTies 883 515 884 810

CONsOlIDATeD sTATeMeNT Of fINANCIAl pOsITION – CONTINUeDequity and liaBilitieS aS at 31 deCemBeR, fiGuReS in nok 1 000

Oslo, 22 March 2011

Ragnar Horn (Chairman) Birger Nergaard Marianne Lie

Gustave Brun-Lie Marianne Aamodt Peter M. Anker (CEO)

44 RS Platou aSa / annual RePoRt 2010

note 2010 2009

cash flow from operaTing acTiviTies

PRofit BefoRe tax 180 568 -46 871

adjusTmenTs

taxeS Paid -9 523 -103 547

dePReCiation and imPaiRmentS 9 13 774 10 097

amoRtiSation and imPaiRmentS 10 754 1 832

diffeRenCe Between PenSion CoSt and PenSion PaymentS 3 300 7 460

aSSoCiateS 11 992 253

PRofit(-)/loSS (+) on Sale of PRoPeRty, Plant and equiPment 9 0 0

ChanGeS in tRade ReCeivaBleS, tRade PayaBleS and CuStomeR PRePaymentS 5 361 208 649

net finanCial inCome 6 917 -13 250

otheR ChanGeS -30 359 -71 566

net CaSh flow fRom oPeRatinG aCtivitieS 171 783 -6 944

cash flow from invesTing acTiviTies

dividendS ReCeived 0 2 500

foRwaRd ContRaCtS 0 -80 387

PuRChaSe of PRoPeRty, Plant and equiPment -19 688 -29 327

PRoCeedS fRom Sale of PRoPeRty, Plant and equiPment 210 2 504

PRoCeedS fRom RePayment of otheR inveStmentS -1 327 -839

net amount Paid out on PuRChaSe of SuBSidiaRieS -1 804 0

PuRChaSe of otheR inveStmentS 0 2 148

net CaSh flow fRom inveStinG aCtivitieS -22 609 -103 401

CONsOlIDATeD sTATeMeNT Of CAsH flOw1 januaRy – 31 deCemBeR, fiGuReS in nok 1 000

45ConSolidated finanCial StatementS

cash flow from financing acTiviTies

iSSuanCe of ShaRe CaPital 4 249 99 000

tReaSuRy ShaReS 2 211 -7 895

RePayment of BoRRowinGS -133 979 -98 322

new lonG-teRm BoRRowinGS 149 966 27 838

net inteReSt inCome/inteReSt exPenSe -6 917 628

dividendS Paid 16 -40 643 -101 747

dividendS Paid to non-ContRollinG inteReStS -6 230 -19 499

net CaSh flow fRom finanCinG aCtivitieS -31 342 -99 997

net tRanSlation diffeRenCe 4 837 0

net IncRease In cash and cash equIvalents 122 669 -210 341

cash and cash equIvalents as of 1 JanuaRy 15,19 158 046 368 388

cash and cash equivalenTs as of 31 december 15,19 280 715 158 046

CONsOlIDATeD sTATeMeNT Of CAsH flOw – CONTINUeD1 januaRy – 31 deCemBeR, fiGuReS in nok 1 000

RS Platou aSa / annual RePoRt 201046

Share capital

Share premium

treasury shares

other paid-in capital

trans-lation

reserve

fair value

reserveother equity total

non-controlling

intereststotal

equity

BalanCe at 1 januaRy 2010 10 172 105 572 -117 8 821 -11 861 84 70 822 183 492 23 155 206 648

comprehensive income for The period

PRofit foR the yeaR 0 0 0 0 0 0 102 075 102 075 18 123 120 198

foReiGn CuRRenCy tRanSlation diffeRenCeS 0 0 0 0 863 0 0 863 342 1 205

total otheR inCome 0 0 0 0 863 0 0 863 342 1 205

comprehensive income for The period 0 0 0 0 863 0 102 075 102 938 18 465 121 403

TransacTions wiTh owners, recognised in equiTY

ContRiButionS fRom/diSBuRSement to owneRS

ShaRe iSSue 71 4 178 0 0 0 0 0 4 249 0 4 249

ChanGe in tReaSuRy ShaReS 0 0 35 1 713 0 0 463 2 211 0 2 211

dividendS 0 0 0 0 0 0 -40 643 -40 643 -6 230 -46 873

ToTal conTribuTions from and disbursemenT To owners 71 4 178 35 1 713 0 0 -40 180 -34 182 -6 230 -40 413

changes in ownership inTeresTs in subsidiaries wiThouT loss of conTrol

acquisiTion of non-conTrolling ownership inTeresTs 0 0 0 0 0 0 0 0 0 0

ChanGe in non-ContRollinG owneRShiP inteReStS 0 0 0 0 0 0 2 557 2 557 -4 361 -1 805

ToTal change in ownership in subsidiaries (noTe 2) 0 0 0 0 0 0 2 557 2 557 -4 361 -1 805

equiTY aT 31 december 2010 10 243 109 750 -82 10 534 -10 998 84 135 273 254 805 31 028 285 834

CONsOlIDATeD sTATeMeNT Of CHANGes IN eqUITyConSolidated Statement of ChanGeS in equity, fiGuReS in nok 1 000

47ConSolidated finanCial StatementS

Share capital

Share premium

accounttreasury

shares

other paid-in capital

trans-lation

reserve

fair value

reserveother equity total

non-controlling

intereststotal

equity

BalanCe at 1 januaRy 2009 8 505 8 239 -218 3 691 11 788 84 165 022 197 112 89 480 286 593

comprehensive income for The period

PRofit foR the yeaR 0 0 0 0 0 0 -12 244 -12 244 -28 663 -40 907

foReiGn CuRRenCy tRanSlation diffeRenCeS 0 0 0 0 -23 650 0 0 -23 650 -638 -24 288

total otheR inCome 0 0 0 0 -23 650 0 0 -23 650 -638 -24 288

comprehensive income for The period 0 0 0 0 -23 650 0 -12 244 -35 894 -29 301 -65 194

TransacTions wiTh owners, recognised in equiTY

ContRiButionS fRom/ diSBuRSement to owneRS

ShaRe iSSue 1 667 97 333 0 0 0 0 0 99 000 0 99 000

ChanGe in tReaSuRy ShaReS 0 0 -43 -984 0 0 2 741 1 713 0 1 713

ShaReS owned By SuBSidiaRieS 0 0 144 6 114 0 0 4 054 10 312 0 10 312

dividendS 0 0 0 0 0 0 -102 063 -102 063 -19 499 -121 562

ToTal conTribuTions from and disbursemenT To owners 1 667 97 333 101 5 130 0 0 -95 268 8 962 -19 499 -10 537

changes in ownership inTeresTs in subsidiaries wiThouT loss of conTrol

addiTions of non-conTrolling ownership inTeresTs 0 0 0 0 0 0 0 0 547 547

aCquiSition of non-ContRol-linG owneRShiP inteReStS 0 0 0 0 0 0 0 0 547 547

ChanGe in non-ContRollinG owneRShiP inteReStS (note 2) 0 0 0 0 0 0 13 312 13 312 -18 073 -4 761

ToTal change in ownership in subsidiaries 0 0 0 0 0 0 13 312 13 312 -18 073 -4 761

equiTY aT 31 december 2009 10 172 105 572 -117 8 821 -11 861 84 70 822 183 492 23 155 206 648

48 RS Platou aSa / annual RePoRt 2010

noTeS To The conSolidaTed financial

STaTemenTSACCOUNTING prINCIplesInfoRmatIon aBout the comPanyRS Platou ASA is a public limited company registered in Norway. The company’s head office is located at Haakon VII’s gate 10, 0119 Oslo, Norway. The company’s consolidated financial statements for the accounting year 2010 comprise the company and its subsidiaries (collectively referred to as the Group, and individually as a Group company), together with the Group’s interests in associated companies (see note 2 for a list of subsidiary companies). The company’s business activities are described in note 2.

BasIs foR the PRePaRatIon of the fInancIal statementsThe consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs) and appropriate interpretations as adopted by the EU for application as at 31 December 2010, and additional notification or disclosure requirements under the Norwegian Accounting Act, also as at 31 December 2010.

The proposed consolidated financial statements were approved by the company’s Board of Directors and CEO on the date the balance sheet was signed. The consolidated financial statements will be considered for final approval by the Annual General Meeting in May 2011.